S-11/Afalse0001585389Notional amounts shown are denominated in CAD. On January 16, 2024 we rolled this hedge without any cash settlement, effectively extending the maturity date to February 15, 2024 at a strike rate of 1.3781. Additionally, on February 16, 2024 we further rolled this hedge without any cash settlement at a strike rate of 1.3781. This hedge ultimately matured on March 7, 2024 whereby we owed and paid approximately $0.5 million at settlement. We paid our Dealer Manager an ongoing stockholder servicing fee that is payable monthly and accrues daily in an amount equal to 1/365th of 1% of the purchase price per share of the Class T Shares sold in the Primary Offering. The amount incurred during the year ended December 31, 2022 represents an adjustment to the estimated stockholder servicing fee recorded at the time of the sale of the Class T Shares, based on the cessation date of such stockholder servicing fee of March 31, 2022.On March 17, 2021, we acquired SST IV and no longer earn such fees. Additionally, the Tenant Protection Program revenue for SST IV is now included in ancillary operating revenue in our consolidated statements of operations.On June 1, 2022, we acquired SSGT II and no longer earn such fees. Additionally, the Tenant Protection Program revenue for SSGT II is now included in ancillary operating revenue in our consolidated statements of operations.Such revenue primarily includes other property management related fees, construction management fees, development fees, and other miscellaneous revenues.Pursuant to the Sponsor Funding Agreement, SmartStop funds certain costs of SST VI's share sales, and in return receives Series C Units in SST VI's OP. The excess of the funding over the value of the Series C Units received is accounted for as a reduction of Managed REIT Platform revenues from SST VI over the remaining estimated term of the management contracts with SST VI.As of December 31, 2023, $1.5 million was available to be drawn on the SSGT III Mezzanine Loan.The approximately $76.3 million in cash was primarily used to pay off approximately $75.1 million of SSGT II’s debt that we did not assume in the SSGT II Merger, as well as approximately $1.2 million in transaction costs.Upon our acquisition of SSGT II, we recorded a gain of approximately $16.1 million to record the then fair market value of our special limited partnership interest in SSGT II operating partnership.Liabilities assumed represents accounts payable and other liabilities.Approximately $8.0 million of the intangible assets acquired related to the intrinsic value of a purchase and sale agreement for the acquisition of a property in San Gabriel, CA that we assumed in the SSGT II Merger and acquired on July 13, 2023. The remainder of the intangible asset relates to value ascribed to the in-place leases on the properties acquired.The approximately $54.3 million in cash was primarily used to pay off approximately $54.0 million of SST IV debt that we did not assume in the SST IV Merger, as well as approximately $0.3 million in transaction costs.The allocation noted above is based on a determination of the relative fair value of the total consideration provided and represents the amount paid including capitalized acquisition costs.The operating results of the self storage property acquired have been included in our consolidated statements of operations since its acquisition date.Net operating loss excludes corporate general and administrative expenses, interest expenses, depreciation, amortization and acquisition related expenses.Net operating income excludes corporate general and administrative expenses, interest expense, depreciation, amortization and acquisition related expenses.The operating results of the self storage properties acquired have been included in our consolidated statements of operations since their acquisition dates.Included in the assets of the Self Storage segment as of December 31, 2023 and 2022 were approximately $52.2 million of goodwill. Additionally, as of December 31, 2023 and 2022 there were no accumulated impairment charges to goodwill within the Self Storage segment.Included in the assets of the Managed REIT Platform segment as of December 31, 2023 and 2022, was approximately $1.4 million of goodwill. Such goodwill is net of accumulated impairment charges in the Managed REIT Platform segment of approximately $24.7 million, which relates to the impairment charge recorded during the year ended December 31, 2020.Other than our investments in and advances to Managed REITs and investments in JV properties, substantially all of our investments in real estate facilities and intangible assets as of December 31, 2023 and 2022, respectively, were associated with our self storage platform.We deferred payment on this SOFR cap until its maturity. We deferred payment on this SOFR cap until January 2, 2025, at which point, monthly payments will become due on the first of each month until the date of its maturity. Notional amount shown is denominated in CAD. Included herein is the value of certain SOFR interest rate caps, net of approximately $8.2 million in deferred payments, as well as the fair value of our CORRA swap. These joint venture properties were acquired through the SSGT II Merger, which closed on June 1, 2022.These joint venture properties were acquired through the SST IV Merger, which closed on March 17, 2021.This property is currently leased as a single tenant industrial lease. The joint venture plans to develop this property into a self storage facility in the future.This property was acquired on January 12, 2023 in connection with a purchase agreement assumed in the SSGT II Merger.On April 15, 2021, we purchased the Oakville III Property. We partially financed the Oakville III Property acquisition with a loan from Bank of Montreal (the “Oakville III BMO Loan”), which was secured by a first lien on the Oakville III Property. The loan is denominated in Canadian dollars and the proceeds from the loan were approximately CAD $16.3 million. The interest only loan was prepayable at any time without penalty. On March 24, 2023, we fully paid off this loan, including all outstanding accrued interest.The amounts shown above are in USD based on the foreign exchange rate in effect as of the date presented. This fixed rate loan encumbers 29 properties (Whittier, La Verne, Santa Ana, Upland, La Habra, Monterey Park, Huntington Beach, Chico, Lancaster I, Riverside, Fairfield, Lompoc, Santa Rosa, Federal Heights,Aurora, Littleton, Bloomingdale, Crestwood, Forestville, Warren I, Sterling Heights, Troy, Warren II, Beverly, Everett, Foley, Tampa, Boynton Beach, and Lancaster II) with monthly interest only payments until September 2021, at which time both interest and principal payments became due monthly. The separate assets of these encumbered properties are not available to pay our other debts. As of March 31, 2023, a Total Leverage Ratio Event (as defined below) had occurred, and the interest rate on such Note increased to 5.28% prospectively. For additional information regarding this loan, see below. This fixed rate, interest only loan encumbers 10 properties (Myrtle Beach I, Myrtle Beach II, Port St. Lucie, Plantation, Sonoma, Las Vegas I, Las Vegas II, Las Vegas III, Ft Pierce, and Nantucket Island). The separate assets of these encumbered properties are not available to pay our other debts. This fixed rate loan encumbers five properties (Pompano Beach, Lake Worth, Jupiter, Royal Palm Beach, and Delray) with monthly interest only payments until June 2022, at which time both interest and principal payments became due monthly. The separate assets of these encumbered properties are not available to pay our other debts.On March 17, 2021, in connection with the SST IV Merger, we assumed a $40.5 million fixed rate CMBS financing with KeyBank as the initial lender pursuant to a mortgage loan (the “SST IV CMBS Loan”). This fixed rate loan encumbers seven properties owned by us (Jensen Beach, Texas City, Riverside, Las Vegas IV, Puyallup, Las Vegas V, and Plant City). The separate assets of these encumbered properties are not available to pay our other debt. The loan has a maturity date of February 1, 2030. Monthly payments due under the loan agreement (the “SST IV CMBS Loan Agreement”) are interest only, with the full principal amount becoming due and payable on the maturity date.Included in the assets of the Managed REIT Platform segment as of September 30, 2024 and December 31, 2023 was approximately $1.4 million of goodwill. Such goodwill is net of accumulated impairment charges in the Managed REIT Platform segment of approximately $24.7 million, which relates to the impairment charge recorded during the quarter ended March 31, 2020.Included in the assets of the Self Storage segment as of September 30, 2024 and December 31, 2023 was approximately $52.2 million of goodwill. Additionally, as of September 30, 2024 and December 31, 2023, there were no accumulated impairment charges to goodwill within the Self Storage segment.Other than our investments in and advances to Managed REITs and investments in joint ventures, substantially all of our investments in real estate facilities and intangible assets as of September 30, 2024 and December 31, 2023, respectively, were associated with our self storage platform.The SSGT III Mezzanine Loan expired on the maturity date of August 9, 2024, as such there is no further ability for SSGT III to borrow on this loan.As of September 30, 2024, these properties were encumbered by first mortgages pursuant to the RBC JV Term Loan (defined below).As of September 30, 2024, these properties were encumbered by first mortgages pursuant to the RBC JV Term Loan II (defined below).This property is encumbered by a first mortgage pursuant to the SmartCentres Financings (defined below).This property was leased as a single tenant industrial lease as of September 30, 2024. The joint venture plans to develop this property into a self storage facility in the future.This fixed rate loan encumbers 29 properties (Whittier, La Verne, Santa Ana, Upland, La Habra, Monterey Park, Huntington Beach, Chico, Lancaster I, Riverside, Fairfield, Lompoc, Santa Rosa, Federal Heights, Aurora, Littleton, Bloomingdale, Crestwood, Forestville, Warren I, Sterling Heights, Troy, Warren II, Beverly, Everett, Foley, Tampa, Boynton Beach, and Lancaster II) with monthly interest only payments until September 2021, at which time both interest and principal payments became due monthly. The separate assets of these encumbered properties are not available to pay our other debts. This loan incurs interest at an all in rate of CORRA (as defined further below under the section entitled “2027 NBC Loan”), plus a CORRA adjustment of approximately 0.30%, plus a spread of 2.20%. Theeffective interest rate on this loan is 6.42% when factoring the effects of a CORRA Swap which we entered into with the National Bank of Canada for the initial term of the loan. The Dufferin, Oakville II, Burlington II, Iroquois Shore Rd, and Stoney Creek I properties are encumbered by this loan. See Note 7 – Derivative Instruments for additional information. On November 16, 2023, we, through eight of our wholly-owned Canadian subsidiaries entered into a term loan (the “2028 Canadian Term Loan”) with affiliates of QuadReal Finance LP, receiving net proceeds of $110.0 million CAD on such date. The 2028 Canadian Term Loan is secured by eight Canadian properties, has a maturity date of December 1, 2028, and carries a fixed interest rate for the term of the loan of 6.41%. The first two years of the Canadian Term Loan are interest only, after which it requires monthly amortizing payments based on a 25-year amortization schedule. As of March 31, 2023, a Total Leverage Ratio Event (as defined below) had occurred, and the interest rate on such Note increased to 5.28% prospectively. For additional information regarding this loan, see 2032 Private Placement Notes below. The equity interest in these wholly-owned subsidiaries that directly own these unencumbered real estate assets comprise the borrowing base of the Credit Facility and the 2032 Private Placement Notes, and such equity interests were pledged as of December 31, 2023 for the benefit of the lenders thereunder.This property is located in Ontario, Canada.The change in cost at these self storage facilities are the net of the impact of foreign exchange rate changes and any actual additions.The aggregate cost of real estate for United States federal income tax purposes is approximately $1,921,347,528On March 2, 2023 the Compensation Committee of the board of directors approved the vesting of the 2020 performance grant at 200% of the targeted award. Accordingly, individuals who elected to receive performance based restricted stock were issued and immediately vested additional shares to equal 200% of their targeted award.Hurricane Helene caused record flooding in late September 2024 in Asheville, North Carolina. One of our 14 wholly-owned properties in this market was severely flooded. As a result of the storm event, flooding and related damage, we recorded a net casualty loss related to this property of approximately $4.6 million during the three and nine months ended September 30, 2024, to write-off the carrying value. We expect to rebuild and therefore we believe it is probable that we will receive insurance proceeds to offset the casualty loss and have recorded a receivable related to our pending insurance claims. Consequently the casualty loss was completely offset in our consolidated statements of operations by such recovery. Any amount of insurance recovery related to the property damage in excess of the casualty loss incurred is considered a gain contingency, and will be recognized upon final settlement of the claims.

As filed with the Securities and Exchange Commission on December 9, 2024

Registration No. 333-264449

SECURITIES AND EXCHANGE COMMISS

I

O

N

FOR REGISTRATION UNDER THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

SMARTSTOP SELF STORAGE REIT, INC.

(Exact Name of Registrant as Specified in its Governing Instruments)

Ladera Ranch, California 92694

(Address, including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

General Counsel and Secretary

Ladera Ranch, California 92694

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

| | |

Nelson Mullins Riley & Scarborough LLP 201 17 th Street NW, Suite 1700 | | 355 South Grand Avenue, Suite 100 Los Angeles, California 90071-1560 |

Approximate date of commencement of the proposed sale of the securities to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the Securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule

12b-2

of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer | | ☐ | | Accelerated filer | | ☐ |

| | | |

| Non-accelerated filer | | ☒ | | Smaller reporting company | | ☐ |

| | | |

| | | | Emerging growth company | | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the United States Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION

PRELIMINARY PROSPECTUS DATED DECEMBER 9, 2024

Shares

SMARTSTOP SELF STORAGE REIT, INC.

Common Stock

SmartStop Self Storage REIT, Inc. is an internally-managed real estate investment trust, or REIT, and a premier owner and operator of self storage facilities in the United States and Canada. We are offering shares of our common stock as described in this prospectus. All of the shares of our common stock offered by this prospectus are being sold by us. We currently expect the public offering price to be between $ and $ per share. We intend to apply to have our common stock listed on the New York Stock Exchange, or NYSE, under the symbol “SMA.” Currently, our common stock is not traded on a national securities exchange, and this will be our first listed public offering.

We were formed as a Maryland corporation in January 2013 and have elected to be taxed as a REIT for U.S. federal income tax purposes beginning with our taxable year ended December 31, 2014. Shares of our common stock are subject to ownership limitations that are primarily intended to assist us in maintaining our qualification as a REIT. Our charter contains certain restrictions relating to the ownership and transfer of our common stock, including, subject to certain exceptions, a 9.8% ownership limit of common stock by value or number of shares, whichever is more restrictive. See “Description of Capital Stock—Restrictions on Ownership and Transfer” beginning on page 187 of this prospectus.

Investing in our common stock involves risk. See “Risk Factors” beginning on page 22 of this prospectus.

| | | | | | | | |

| | | Per Share | | | Total | |

Public offering price | | $ | | | | $ | | |

Underwriting discount(1) | | $ | | | | $ | | |

Proceeds, before expenses, to us | | $ | | | | $ | | |

| (1) | | See the section entitled “Underwriting” for a complete description of the compensation payable to the underwriters. |

At our request, the underwriters have reserved percent of the shares of common stock to be issued by us and offered by this prospectus for sale, at the initial public offering price, to (i) certain of our directors, officers and employees, and (ii) friends and family members of certain of our directors, officers and employees. The number of shares of common stock available for sale to the general public will be reduced to the extent these individuals purchase such reserved shares. Any reserved shares that are not so purchased will be offered by the underwriters to the general public on the same basis as the other shares offered by this prospectus. See “Underwriters—Directed Share Program” for additional information.

We have granted the underwriters the option to purchase an additional shares of our common stock on the same terms and conditions set forth above within 30 days after the date of this prospectus.

Neither the United States Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of our common stock on or about , 2025.

| | | | | | | | |

| J.P. Morgan | | Wells Fargo Securities | | KeyBanc Capital Markets | | BMO Capital Markets | | Truist Securities |

The date of this prospectus is , 2025

GENERAL DISCLAIMERS

You should rely only on the information contained in this prospectus or in any free writing prospectus prepared by us. We have not, and the underwriters have not, authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it.

You should assume that the information appearing in this prospectus and in any free writing prospectus prepared by us is accurate only as of their respective dates or on the date or dates specified in these documents. Our assets, business, cash flows, financial condition, liquidity, results of operations, and prospects may have changed since those dates.

This prospectus describes the specific details regarding this offering and the terms and conditions of our common stock being offered hereby and the risks of investing in our common stock. For additional information, please see the section entitled “Where You Can Find More Information.”

You should not interpret the contents of this prospectus or any free writing prospectus to be legal, business, investment or tax advice. You should consult with your own advisors for that type of advice and consult with them about the legal, tax, business, financial and other issues that you should consider before investing in our common stock.

“SmartStop Self Storage” and its logos and other trademarks referred to and included in this prospectus belong to us. Solely for convenience, we refer to our trademarks in this prospectus without the ® or the ™ or symbols, but such references are not intended to indicate that we will not assert, to the fullest extent under applicable law, our rights to our trademarks. Other service marks, trademarks and trade names referred to in this prospectus, if any, are the property of their respective owners, although for presentational convenience we may not use the ® or the ™ symbols to identify such trademarks.

MARKET, INDUSTRY, AND OTHER DATA

We use market data throughout this prospectus which has generally obtained from publicly available information and industry publications. These sources generally state that the information they provide has been obtained from sources believed to be reliable, but the accuracy and completeness of the information are not guaranteed. The market data includes forecasts and projections that are based on industry surveys and the preparers’ experiences in the industry, and there is no assurance that any of the projections or forecasts will be achieved. We believe that the surveys and market research others have performed are reliable, but we have not independently verified this information.

Unless otherwise indicated, references in this prospectus to information reported by U.S. Listed Self Storage REITs refer to metrics and data publicly reported by the U.S. Listed Self Storage REITs. See “Certain Defined Terms Used in This Prospectus.” The U.S. Listed Self Storage REITs may define or calculate such metrics or data differently than we do. Accordingly, our metrics or data may differ from, or may not be comparable to, the metrics and data of the U.S. Listed Self Storage REITs.

CONVERSION OF CLASS A COMMON STOCK AND CLASS T COMMON STOCK

Our charter provides that, upon the six-month anniversary of the listing of shares of our common stock for trading on a national securities exchange or such earlier date as approved by our Board, each share of Class A common stock and Class T common stock will automatically, and without any stockholder action, convert into a number of shares of our common stock equal to a fraction, the numerator of which is the net asset value of the Company allocable to the shares of Class A common stock and shares of Class T common stock, as applicable, and the denominator of which is the net asset value of the Company allocable to the shares of our common stock, or the Conversion.

ii

Shares of our common stock issued as a result of the conversion of shares of our Class A common stock and shares of Class T common stock, as described in the preceding paragraph, will be listed on the NYSE upon such conversion, which shall occur upon the six-month anniversary of the listing of shares of our common stock sold in this offering or such earlier date as approved by our Board. We have agreed that, without the prior written consent of the representatives on behalf of the underwriters, we will not approve the conversion of any of the outstanding shares of Class A common stock or shares of Class T common stock into shares of our common stock before the six-month anniversary of the listing of our common stock for trading on a national securities exchange.

CERTAIN DEFINED TERMS USED IN THIS PROSPECTUS

adjusted gross margin percentage | Net operating income divided by gross revenue less revenue from the tenant protection program. |

Board | The board of directors of SmartStop. |

CAGR | Compound annual growth rate. |

Code | The Internal Revenue Code of 1986, as amended. |

economically stabilized | Having achieved market rents on a per-unit and overall store basis, without having material in-place discounts or concessions. |

Exchange Act | The Securities Exchange Act of 1934, as amended. |

GAAP | United States generally accepted accounting principles. |

GTA | The Greater Toronto Area of Ontario, Canada. |

LTIP unit | A unit of limited partnership interest in our operating partnership issued or to be issued as a form of equity compensation to our executive officers and directors, subject to vesting criteria, with the rights, preferences and other privileges set forth in our operating partnership agreement. |

Managed REIT platform | Our platform to sponsor non-traded REITs that will invest in, among other things, non-stabilized, growth-oriented assets, and development projects. |

Managed REITs | The various REITs sponsored by SmartStop REIT Advisors, LLC, our indirect subsidiary, which may include in certain contexts one or more of Strategic Storage Trust IV, Inc., Strategic Storage Growth Trust II, Inc., Strategic Storage Trust VI, Inc., Strategic Storage Growth Trust III, Inc., and any future sponsored REITs. |

MGCL | Maryland General Corporation Law or any successor statute. |

iii

NAREIT | The National Association of Real Estate Investment Trusts. |

NYSE | The New York Stock Exchange. |

operating partnership | Our operating partnership, SmartStop OP, L.P., a Delaware limited partnership. |

operating partnership agreement | The Third Amended and Restated Limited Partnership Agreement of our operating partnership, as amended from time to time. |

OP unit | A common unit of limited partnership interest of our operating partnership. |

physically stabilized | Assets have achieved greater than 80% occupancy as measured by net rentable square feet. |

REIT | A real estate investment trust within the meaning of Section 856 through 860 of the Code. |

RentPOF | Annualized rental revenue net of discounts and concessions, excluding late fees, administrative fees and parking income for the period indicated, divided by the associated occupied square feet of storage for the period indicated. |

SAM | Strategic Asset Management I, LLC (f/k/a SmartStop Asset Management, LLC), the former sponsor of SmartStop, SST IV, and SSGT II. |

same-store | Assets are included in the same-store pool when we have owned them since January 1 of the prior calendar year and they have been physically stabilized for at least one full year prior to the beginning of the prior calendar year. |

Securities Act | The Securities Act of 1933, as amended. |

self administration transaction | The self administration transaction that closed in June 2019 in which we acquired the self storage advisory, asset management and property management businesses and certain joint venture interests of SAM, along with certain other assets of SAM. |

tenant protection program | Tenant protection plan, tenant insurance plan, and similar arrangements with respect to the protection of customer goods at our properties. |

U.S. Listed Self Storage REITs | CubeSmart, Extra Space Storage Inc., National Storage Affiliates Trust and Public Storage. |

As used in this prospectus, unless the context otherwise requires, references to “SmartStop,” “we,” “us,” “our,” the “Company” and similar references refer to SmartStop Self Storage REIT, Inc., a Maryland corporation, together with its consolidated subsidiaries, including its operating partnership.

iv

PROSPECTUS SUMMARY

This summary highlights some of the information in this prospectus. It does not contain all of the information that you should consider before investing in shares of our common stock. You should read carefully the more detailed information set forth under the heading “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our consolidated financial statements and related notes and the other information included in this prospectus. Unless otherwise indicated, information contained in this prospectus assumes that the underwriters do not exercise their option to purchase additional shares.

Our Company

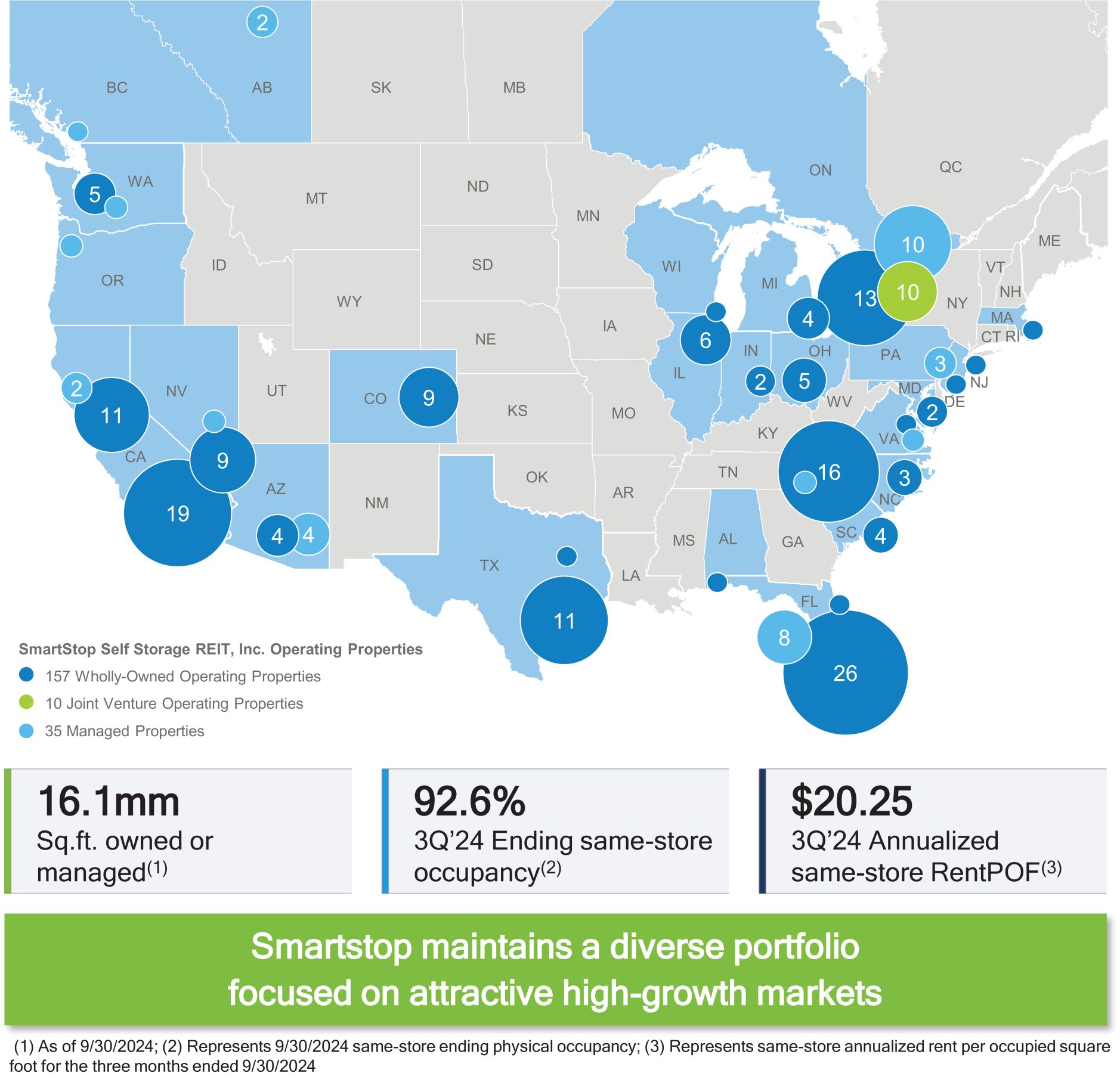

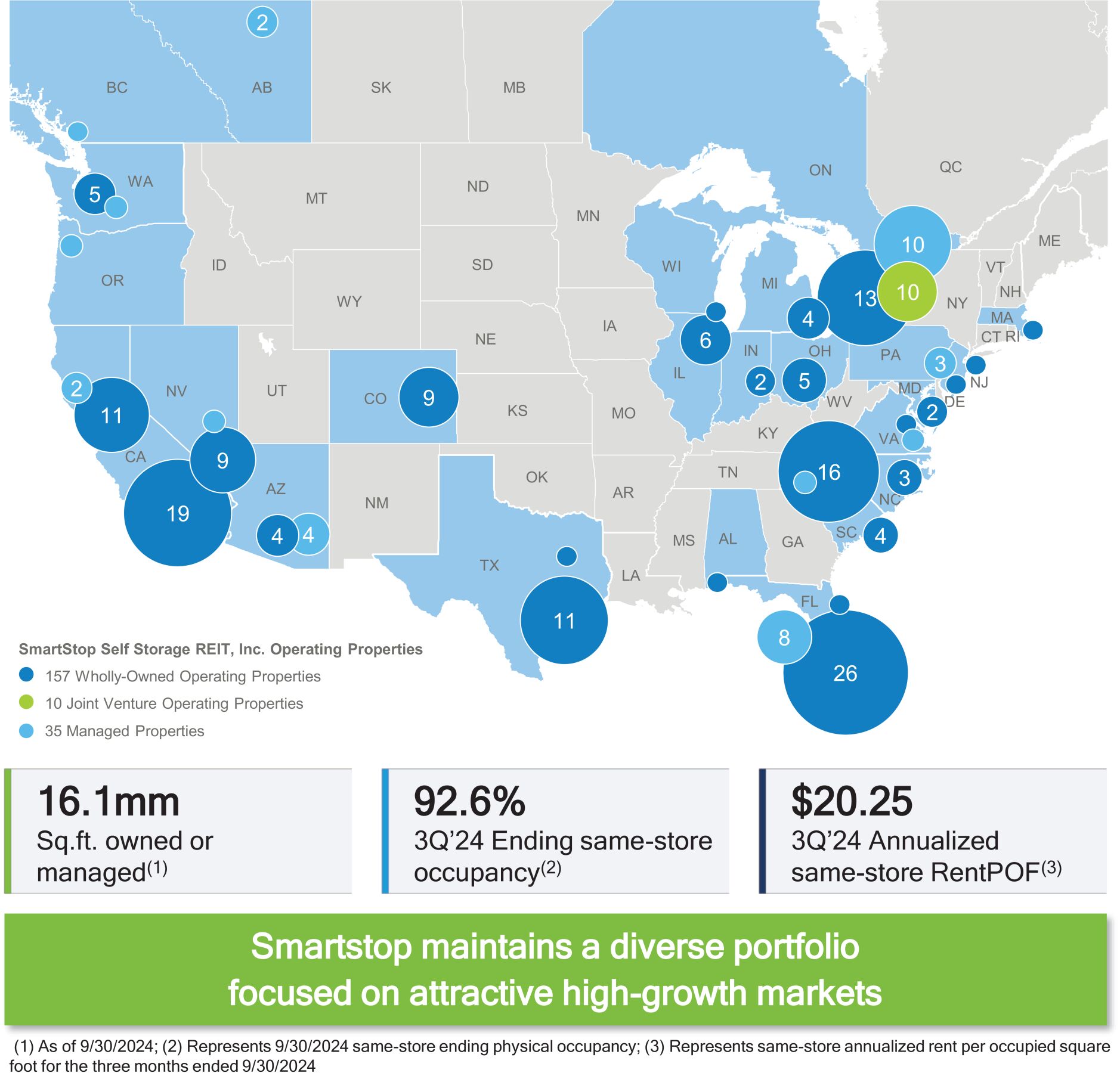

We are a premier owner and operator of self storage facilities in the United States and Canada. We are internally managed and have built a fully integrated, technology-enabled, data-driven, and scalable platform that is positioned for growth. We operate an institutional-quality portfolio of self storage properties that are located primarily within top metropolitan statistical areas, or MSAs, throughout the United States and within top census metropolitan areas, or CMAs, in Canada, including the Greater Toronto Area, or GTA. According to the Inside Self Storage Top-Operators List for 2024, we are the tenth largest owner and operator of self storage properties in the United States and according to Colliers, the largest in the GTA based on rentable square footage. As of September 30, 2024, we owned or managed 202 operating stores across 22 states and three provinces in Canada, comprising approximately 143,190 units and 16.1 million net rentable square feet.

The following table summarizes our owned and managed operating properties in our portfolio as of September 30, 2024:

| | | | | | | | | | | | | | | | |

Operating Portfolio Snapshot | | # of Stores | | | Net Rentable

Sq. Ft. | | | Units | | | 3Q24

Ending

Occupancy | |

Wholly-owned Stores | | | 157 | | | | 12,208,000 | | | | 106,300 | | | | 92.2 | % |

Joint Venture Stores | | | 10 | | | | 897,400 | | | | 9,440 | | | | 80.0 | % |

| | | | | | | | | | | | | | | | |

Total Owned Stores | | | 167 | | | | 13,105,400 | | | | 115,740 | | | | — | |

Managed Stores | | | 35 | | | | 3,040,200 | | | | 27,450 | | | | | |

| | | | | | | | | | | | | | | | |

Total Stores | | | 202 | | | | 16,145,600 | | | | 143,190 | | | | | |

We believe the self storage sector has distinguished itself as a core asset class with attractive long-term organic growth characteristics and strong free cash flow generation. We expect long-term self storage drivers, which include population growth, the percentage of renter occupied housing units and self storage supply constraints, to continue to underpin competitive risk adjusted returns relative to the broader real estate sector.

Since our founding, we have built a leading self storage brand in the United States and Canada, growing our total operating portfolio to 202 operating properties as of September 30, 2024. We have seen meaningful growth in our owned and managed portfolio, growing from 83 stores as of January 1, 2019 to 202 as of September 30, 2024 (representing a 16% CAGR). We maintain an investment strategy focused on acquiring or developing properties located in high quality sub-markets that offer our customers convenient, affordable and secure access to self storage units. Furthermore, we have created a scalable, leading technology-enabled platform that drives customer acquisition, customer service efficiencies and revenue management capabilities that optimize profitability across the portfolio.

A unique element to our growth story has been the successful expansion of our Canadian portfolio. Upon completion of this offering, we believe we will be the only U.S. listed self storage REIT with an owned portfolio

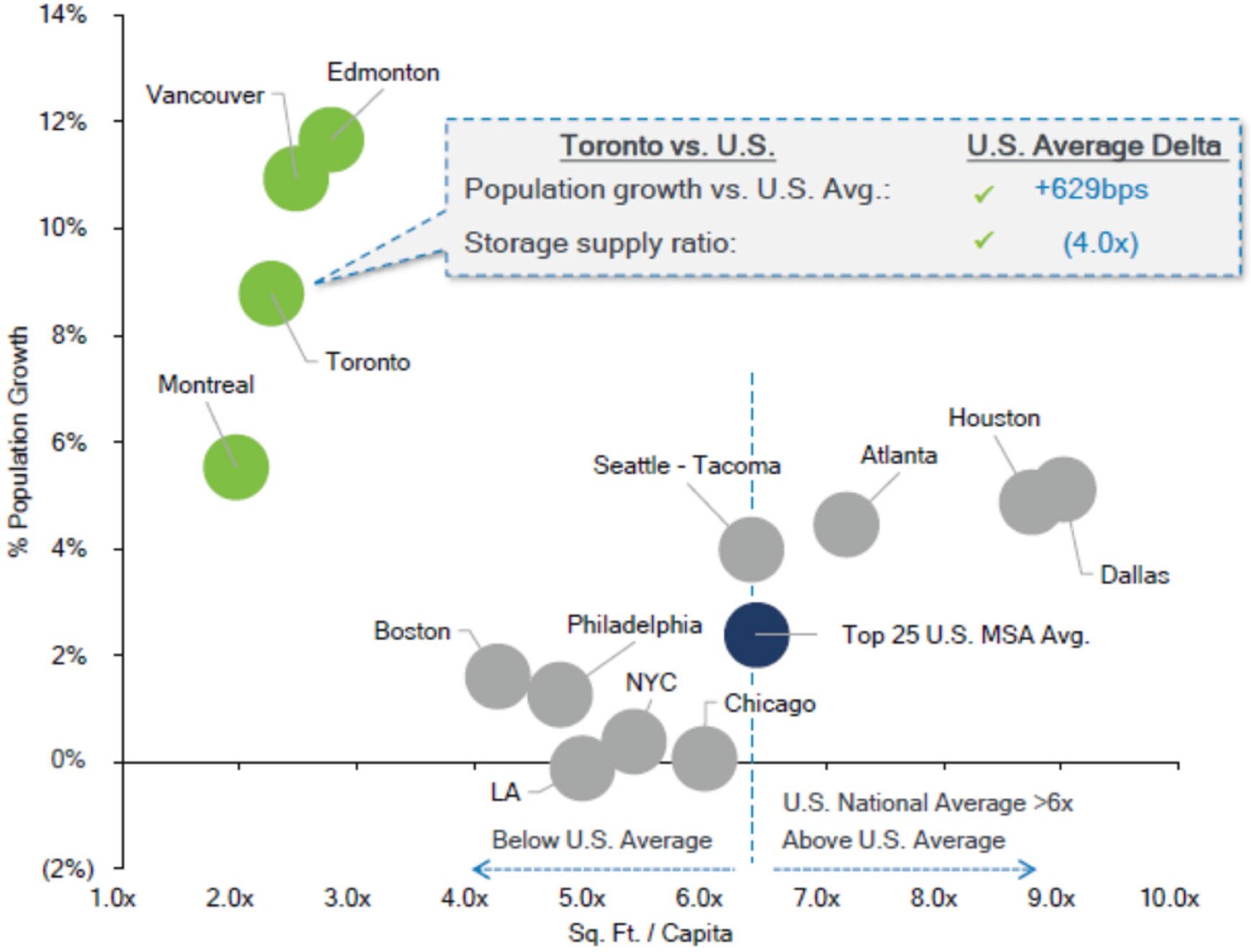

1

and operating platform in Canada (including in the GTA, one of the fastest growing and undersupplied markets in North America). Supported by strong demographic trends (according to Claritas, S&P Global, and Statistics Canada), GTA population growth from 2024 through 2029 is expected to be approximately 630 bps greater than the U.S. average. We believe Canada presents a compelling investment opportunity as home to several of the most attractive North American storage markets, highlighted by low supply per capita (2.3 square feet of existing self-storage space per capita in the GTA vs. 6.3 in the United States, according to Colliers and the 2024 Self-Storage Almanac), increasing product utilization, top-tier demographic trends, and limited institutional competition. Our joint venture in Canada with SmartCentres, one of the largest Toronto Stock Exchange-listed REITs, provides a pipeline of development opportunities at well trafficked locations within demographically advantaged CMAs. As of September 30, 2024, we owned or managed a portfolio of 33 operating properties comprising 3.1 million square feet in the GTA. This number included 13 wholly-owned facilities and 10 facilities in unconsolidated joint ventures in which we maintain a 50% equity interest. This number also included 10 facilities under management that were wholly-owned by the Managed REITs.

We employ a multi-pronged growth strategy focused on organic and external growth. We aim to grow the cash flow of our existing portfolio by utilizing our revenue management systems to grow revenue and leverage the scalability of our platform to increase expense efficiencies over time. Additionally, we expect to grow externally via acquisitions of newly built properties, ground up developments and strategic stabilized acquisitions, all of which we can execute either on-balance sheet or off-balance sheet through our Managed REITs. Our same-store portfolio, which represents 93.4% of our owned operating portfolio as measured by net rentable square feet, has averaged 8.3% NOI growth over the three-year period ended September 30, 2024. We have deep acquisition capabilities that allow us to focus on properties across the asset life cycle, from ground-up development to stabilized property acquisitions in many of the top MSAs in the United States and CMAs in Canada. Additionally, through a subsidiary, we serve as the sponsor of the Managed REITs. Our Managed REITs not only generate fees that offset our operating and general and administrative expenses but also enable us to strategically expand our platform off-balance sheet while providing potential future acquisition opportunities. Upon completion of this offering, we expect to have a fortified balance sheet with low leverage and ample liquidity that will position us to take advantage of growth opportunities.

Our Founder, Chairman and Chief Executive Officer, H. Michael Schwartz, founded our company in 2013, recognizing a market opportunity for a differentiated public self storage REIT focused on high quality self storage assets in high growth markets across the United States and Canada. Mr. Schwartz entered the self storage business in 2005 and has established a successful 20-year track record in the sector. In 2007, Mr. Schwartz founded Strategic Storage Trust, Inc., which became a fully integrated and self-managed self storage company that grew to own and/or operate 169 self storage properties and was ultimately sold to Extra Space Storage, Inc. for $1.4 billion in October 2015. In addition to Mr. Schwartz, we maintain a seasoned and multidisciplined executive management team with over 20 years of storage experience, on average.

We are organized as a Maryland corporation that has elected to be taxed as a REIT with operational headquarters in Ladera Ranch, CA. We generally will not be subject to U.S. federal income tax on our REIT taxable income to the extent that we distribute annually 100% of our REIT taxable income (including capital gains and computed without regard to the dividends paid deduction) to our stockholders and maintain our intended qualification as a REIT. We serve as the sole general partner of, and operate our business through, our operating partnership subsidiary, SmartStop OP, L.P., a Delaware limited partnership. Our operating partnership enables us to facilitate additional tax deferred acquisitions using OP units as consideration for these transactions.

Our Competitive Strengths

High-quality and Diversified Self Storage Portfolio. We own a large, geographically diversified portfolio comprised exclusively of self storage properties. Our portfolio consists of 167 wholly-owned and joint venture

2

operating self storage properties located in 19 states and Ontario, Canada. Our largest markets based on square footage owned include: Toronto, ON; Miami–Ft. Lauderdale, FL; Las Vegas, NV; Asheville, NC; Los Angeles, CA; and Houston, TX. Our properties are primarily located in high quality markets with attractive supply and demand characteristics. Many of these markets exhibit multiple barriers to entry against increased supply, including zoning restrictions that limit new self storage construction. Furthermore, we believe that our scale and the overall geographic diversification of our portfolio reduces risks associated with specific local or regional economic downturns or natural disasters.

The following map highlights the geographic diversification of our owned and managed operating properties in our portfolio, as of September 30, 2024:

3

The following table summarizes information about our wholly-owned and owned joint venture operating properties in our portfolio by MSA and the census metropolitan area, or CMA, as of September 30, 2024:

| | | | | | | | | | | | | | | | | | | | | | | | |

MSA/CMA(1) | | % of

Portfolio by

NRSF | | | Net

Rentable

Sq. Ft. | | | Units | | | # of

Stores | | | 3Q24

Ending

Occupancy | | | 3Q24

RentPOF | |

Toronto | | | 15.3 | % | | | 2,008,100 | | | | 20,050 | | | | 23 | | | | 86.8 | % | | $ | 20.47 | |

Miami - Fort Lauderdale | | | 9.3 | % | | | 1,221,100 | | | | 10,470 | | | | 12 | | | | 84.6 | % | | $ | 25.66 | |

Asheville | | | 6.6 | % | | | 869,900 | | | | 6,200 | | | | 14 | | | | 92.8 | % | | $ | 16.80 | |

Las Vegas | | | 6.6 | % | | | 865,000 | | | | 7,160 | | | | 9 | | | | 93.9 | % | | $ | 18.81 | |

Los Angeles | | | 5.6 | % | | | 738,500 | | | | 6,990 | | | | 11 | | | | 91.4 | % | | $ | 25.05 | |

Houston | | | 5.2 | % | | | 676,800 | | | | 5,130 | | | | 9 | | | | 93.2 | % | | $ | 19.02 | |

Tampa | | | 3.6 | % | | | 478,100 | | | | 3,890 | | | | 5 | | | | 93.8 | % | | $ | 18.46 | |

Denver | | | 3.3 | % | | | 437,300 | | | | 3,860 | | | | 7 | | | | 91.8 | % | | $ | 18.47 | |

Chicago | | | 3.3 | % | | | 432,450 | | | | 3,785 | | | | 6 | | | | 91.5 | % | | $ | 15.68 | |

Seattle - Tacoma | | | 3.0 | % | | | 390,550 | | | | 3,430 | | | | 5 | | | | 92.8 | % | | $ | 20.38 | |

Dayton | | | 2.9 | % | | | 375,800 | | | | 3,390 | | | | 7 | | | | 93.2 | % | | $ | 12.78 | |

Phoenix | | | 2.5 | % | | | 329,100 | | | | 3,130 | | | | 4 | | | | 93.0 | % | | $ | 17.50 | |

San Francisco - Oakland | | | 2.5 | % | | | 322,600 | | | | 2,920 | | | | 4 | | | | 90.0 | % | | $ | 23.90 | |

Port St. Lucie | | | 2.4 | % | | | 318,900 | | | | 2,610 | | | | 4 | | | | 93.6 | % | | $ | 19.53 | |

Sacramento | | | 2.4 | % | | | 308,100 | | | | 2,895 | | | | 4 | | | | 89.5 | % | | $ | 16.38 | |

Riverside - SB | | | 2.3 | % | | | 306,700 | | | | 2,690 | | | | 5 | | | | 94.0 | % | | $ | 21.67 | |

Detroit | | | 2.0 | % | | | 266,100 | | | | 2,220 | | | | 4 | | | | 93.3 | % | | $ | 15.83 | |

Myrtle Beach | | | 1.5 | % | | | 197,800 | | | | 1,450 | | | | 2 | | | | 90.8 | % | | $ | 14.55 | |

All Other(2) | | | 19.7 | % | | | 2,562,500 | | | | 23,470 | | | | 32 | | | | 87.4 | % | | $ | 20.79 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total Stores(3) | | | 100.0 | % | | | 13,105,400 | | | | 115,740 | | | | 167 | | | | 90.7 | % | | $ | 19.93 | |

| (1) | | MSAs (Metropolitan Statistical Areas) as defined by the U.S. Census Bureau. Toronto CMA (Census Metropolitan Area) as defined by Statistics Canada. |

| (2) | | Other markets include: Baltimore, Charleston, Charlotte, Charlottesville, College Station, Colorado Springs, Dallas, Jacksonville, Milwaukee, Mobile, Nantucket, Naples, New York – Newark, Orlando, Punta Gorda, Raleigh – Cary, San Antonio, San Diego, Santa Maria – Santa Barbara, Santa Rosa – Petaluma, Sarasota, Stockton, Trenton – Princeton and Washington – Arlington. None of these markets represent more than 1.5% of the total portfolio by NRSF. |

| (3) | | Joint venture properties owned in our portfolio are included herein as if 100% owned. |

Our portfolio consists of a combination of recently constructed vertical facilities and early-generation facilities. The weighted average age of our portfolio by rentable square feet since initial construction or significant property redevelopment, whichever is more recent, is approximately 21 years. Our properties are designed to cater to the needs of both residential and commercial customers with features such as electronic gate entry, easy access, climate control, high quality security systems, keypad access, large truck accessibility and pest control. Some of our properties also offer outside storage for vehicles, boats and equipment.

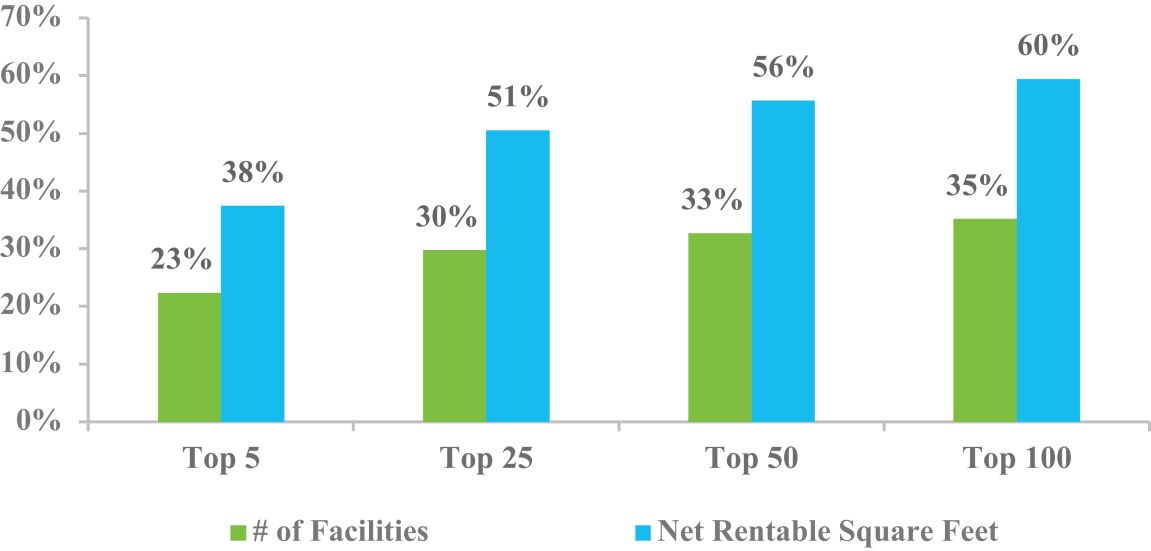

Key Growth Markets and Sub-Markets with Strong Demographics. We seek to own properties that are conveniently located with highly accessible street access in high growth MSAs/CMAs and sub-markets. This includes markets with strong population and household income growth, high levels of population density and supply per capita that is below the U.S. national average. Approximately 65% of our portfolio is located in the top 25 MSAs and over 80% is located in the top 100 MSAs, based on net rentable square feet. While we have meaningful concentration in larger markets, we have also targeted specific smaller markets that exhibit underlying fundamentals that we believe are conducive to attractive risk-adjusted returns. We have invested in

4

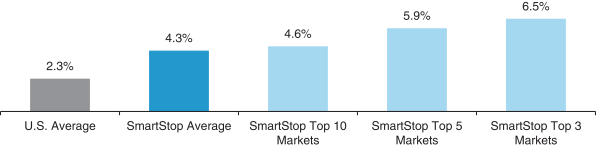

smaller markets, including Asheville, NC and Dayton, OH, due to a combination of low supply per capita and limited competition from institutional operators, among other factors. According to statistics from Claritas and S&P Global, population growth for our top 10 markets is expected to grow approximately 120 bps faster (on a weighted average basis by rentable square feet) than the U.S. average from 2024 to 2029.

Differentiated Exposure to the Greater Toronto Area. Upon the completion of this offering, we believe we will be the only U.S. listed self storage REIT with an owned portfolio and operating platform in Canada and, more specifically, the GTA. As one of the world’s premier financial centers and sixth largest metro area in North America, the GTA has rapidly expanded its population of younger workers. Professionals are drawn to the GTA by its high quality, ubiquitous academic resources, which has resulted in the GTA becoming an emerging market for the digital economy. Supported by strong demographic trends (according to Claritas, S&P Global, and Statistics Canada, GTA population growth from 2024 through 2029 is expected to be approximately 630 bps greater than the U.S. average), we believe the GTA continues to represent a compelling market opportunity, highlighted by low supply per capita (according to Colliers and the 2024 Self-Storage Almanac, the GTA has 2.3x square feet per capita vs. 6.3x in the United States), increasing product utilization, and limited institutional competition. Below we highlight our management team’s history in the market, our existing portfolio and growth initiatives.

| | • | | Our Canadian Platform. Our management team has over 14 years of experience sourcing, developing, acquiring and operating in the GTA. During that time, we have built the local infrastructure to drive our future growth, with approximately 85 employees based in Canada, an executive vice president, or EVP, of Canada, and multi-lingual agents in our Canadian call center. We combine the institutional front and back office of the SmartStop platform with a unique Canadian-specific offering that includes a country specific website and domain, Canadian versions of the SmartStop branding package at all of our stores, and a dedicated and highly trained Canadian team of onsite professionals, all of whom are based in Canada. |

| | • | | Our Canadian Portfolio. We own or manage a portfolio of 33 operating properties in the GTA, comprising approximately 3.1 million square feet, which provides meaningful economies of scale within the GTA self storage market. This number includes 13 wholly-owned facilities and 10 facilities in unconsolidated joint ventures in which we maintain a 50% equity interest. This number also includes 10 facilities under management that were wholly-owned by the Managed REITs. We also manage two properties in Edmonton and one property in Vancouver. At September 30, 2024, we had 13 wholly-owned operating properties in the GTA accounting for approximately 1.1 million net rentable square feet, which accounted for 9.1% of our total wholly-owned portfolio as of September 30, 2024 and 11.4% of our net operating income, or NOI, for the quarter ended September 30, 2024. We have a joint venture with SmartCentres, which owns a diversified portfolio of real estate in Canada and is one of the largest Toronto Stock Exchange-listed REITs. The 50/50 joint venture affords each party a right of first offer to develop self storage facilities in certain CMAs in Canada. We owned 11 joint venture properties with SmartCentres as of September 30, 2024, of which 10 were operating self storage properties and an additional property which we intend to develop into a self storage facility in the future. We have a development pipeline of approximately 1.1 million net rentable square feet, which we believe we are capable of executing on over the next five years throughout multiple CMAs in Canada. |

Institutional-Quality, Technology-enabled, Data-driven Operations Focused on Customer Service. Over the past decade, we have made significant investments in technology, infrastructure, and human capital to support our operational and digital platforms and enable real-time decision making at scale. Digital tools, resources and enhancements are leveraged across our organization to jointly coordinate marketing and pricing activities, improve the customer experience, grow rental revenue and enhance expense efficiencies. Further, we have multiple data science-driven pricing automation systems that are proprietary to our operations platform. In 2022, we completed our transition to a new property management system, furthering our management

5

capabilities and facilitating continued property growth. Built on the latest cloud-based technology, the platform allows us greater flexibility in positioning competitive offerings in our customer pipeline. Aligned with this platform upgrade, SmartStop site managers are now using tablets as the primary tool when engaging with customers on new leasing opportunities. Store managers are no longer confined to the retail office in order to rent units, take payments, conduct lock checks, and conduct other business. We believe this system will help us compete as a top operator and foster continued property performance growth in the future. Today, our technology-driven operating platform includes:

| | • | | consistent and recognizable brand across store locations; |

| | • | | digital brand presence and protection; |

| | • | | highly sophisticated and responsive user-friendly website with mobile optimization; |

| | • | | proprietary data warehouse supported by a multitude of internal and external data sources, algorithmically driving pricing changes with over 18 billion data points; |

| | • | | dedicated, in-house call center; |

| | • | | ability to transact across a spectrum of mediums, including contactless, online rentals, call center rentals, reservations systems and in person rentals; |

| | • | | highly trained staff, focused on enhancing the customer experience; and |

| | • | | automated proprietary digital marketing algorithms driving near real time targeting and spend decisions. |

We are focused on creating a convenient and hassle-free customer experience with an emphasis on the leasing process, regardless of individual customer preferences. Accordingly, we offer website and call center reservations, in person leasing, call center leasing and website leasing, all from a variety of devices, including mobile phones and tablets. In the first nine months of 2024, approximately 35% of all rentals were executed in a contactless manner through our website, with another approximately 10–15% originating from our call center. Meeting the customer at their level has allowed us to bolster our digital marketing efforts, primarily driven by a combination of pay-per-click and search engine optimization campaigns, to continue to maintain attractive returns on invested marketing dollars. The technological backbone of our operating platform is further supported by a dedicated staff of operations professionals, including approximately 400 store-level employees. Our dedicated staff, institutional technology platform and branding presence led to Newsweek ranking us #1 in the self storage business for Best Customer Service in 2021, 2023 and 2024.

Scalable Platform and Asset Base to Drive Significant Growth. Our technology and human capital investments have resulted in a platform that we believe is capable of supporting a portfolio significantly larger than our existing operating portfolio. Our current back-office infrastructure—including accounting, acquisitions, operations and corporate finance—is well positioned to scale. We believe we can grow our portfolio at a rate significantly faster than our general and administrative expenses, which in turn should generate positive operating leverage and enhanced income growth. Additionally, we believe we have an opportunity to drive net operating income margin improvement on our same-store portfolio, as we continue to build out clusters in MSAs where we have less than 10 properties. Furthermore, with our smaller asset base relative to our publicly traded self storage peers, we believe we have an opportunity to achieve out-sized growth through manageable acquisition volumes.

Proven Acquisition Execution in the Self Storage Space. Our management team has significant experience acquiring self storage facilities across a broad spectrum of opportunities, including stabilized facilities, recently developed facilities in lease-up, facilities that have just received a certificate of occupancy, facilities in need of renovation and/or re-development and ground up development. Since the end of 2016, we have acquired over $1.7 billion in self-storage assets either on our balance sheet or on behalf of the Managed REITs. Our dedicated acquisitions team, located in both the United States and Canada, possesses an average of over 20 years of real

6

estate transaction experience and is responsible for executing all of our acquisitions through the use of our proprietary underwriting methodology. More importantly, our acquisitions team has cultivated relationships in the industry that are highly beneficial to our overall deal sourcing. We believe that we maintain a competitive advantage in acquiring facilities given the scale of our business, our experience and the networks of our team.

Further, we believe the acquisition environment has become more constructive. We maintain a disciplined approach to capital deployment and our underwriting standards. Since 2022, we have not observed many attractive opportunities to acquire assets accretively on our balance sheet. However, more recently, we have seen an improvement in seller expectations, coupled with an improved financing backdrop, resulting in an increase in self storage properties listed for sale across the United States and Canada. We have capitalized on the improving deal environment, as demonstrated by recently completed transactions, acquiring 17,350 net rentable square feet of self storage in attractive high-growth markets subsequent to September 30, 2024 (see External Growth Strategies for more detail), and have compiled a robust acquisition pipeline that we expect to close before March 31, 2025. We believe our platform is well positioned to pursue attractive and accretive acquisition opportunities.

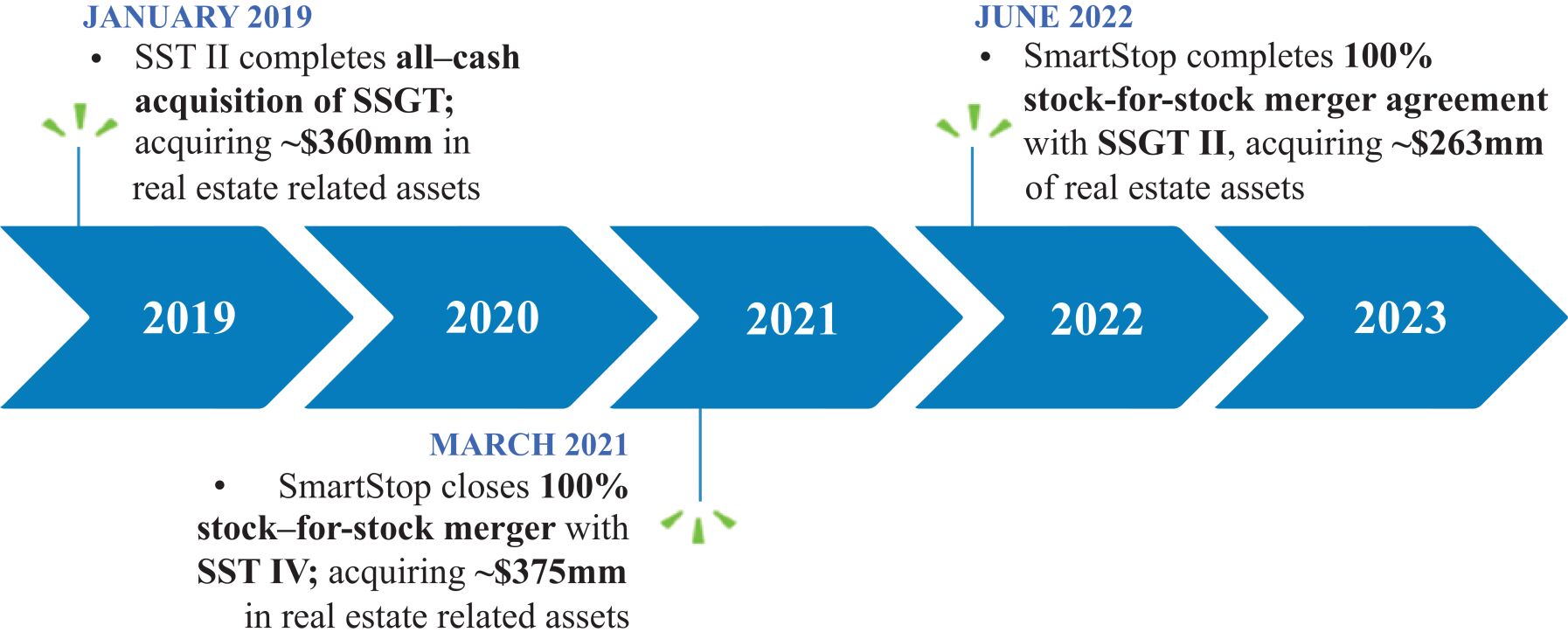

Differentiated Capital Allocation Capability Through Managed REIT Platform Provides Additional Revenues and Potential Acquisition Pipeline. Our management team has an extensive track record of sponsoring and managing non-traded REITs. Since inception, our management team has raised approximately $2.4 billion across nine self storage programs. We currently sponsor and manage two non-traded REITs, Strategic Storage Trust VI, Inc., or SST VI, and Strategic Storage Growth Trust III, Inc., or SSGT III, from which we generate asset management fees, property management fees, acquisition fees, other fees and substantially all of the tenant protection program revenue. In the short-to-medium term, we plan to utilize our Managed REIT platform to sponsor non-traded REITs that will invest in, among other things, non-stabilized, growth-oriented assets, and development projects. We maintain an acquisition allocation policy that provides us the right of first allocation between us and the Managed REITs. As the assets under management in our Managed REITs grow, we will benefit from the additional management fees as well as the economies of scale that will reduce our operating expenses and improve our margins. Additionally, upon stabilization, our Managed REITs serve as potential accretive acquisition targets to drive our external growth. Since 2019, we have acquired or merged with three affiliated REITs. These include (i) the all-cash acquisition of Strategic Storage Growth Trust, Inc., or SSGT, in January 2019 whereby we acquired approximately $360 million in real estate related assets, (ii) the 100% stock-for-stock merger with Strategic Storage Trust IV, Inc., or SST IV, in March 2021 whereby we acquired approximately $375 million of real estate related assets, and (iii) the 100% stock-for-stock merger with Strategic Storage Growth Trust II, Inc., or SSGT II, in June 2022 whereby we acquired approximately $263 million of real estate related assets. With extensive start-up costs and the lack of established track records creating significant barriers to entry for others with respect to the non-traded REIT, we believe our Managed REIT platform provides us a competitive advantage relative to other U.S. Listed Self Storage REITs, which do not have such a platform.

Investment Grade Balance Sheet Well Positioned for Expansion. Upon completion of this offering, we will be well positioned to grow our portfolio by opportunistically pursuing acquisitions in a disciplined manner, while maintaining an attractive leverage profile and flexible balance sheet. Our leverage profile and significant liquidity is expected to position us to pursue attractive external growth opportunities in an accretive and prudently capitalized manner. Becoming a publicly traded REIT will enable us to access multiple forms of equity and debt capital currently not available to us, further enhancing our financial flexibility, cost of capital and external growth. In March 2022, we received an investment grade rating of BBB- with a Stable outlook from Kroll Bond Rating Agency, Inc. (KBRA), which we believe will be further enhanced upon completion of this offering and represents an important step towards our goal of becoming a fully unsecured issuer. KBRA reaffirmed this rating and outlook in April 2023. KBRA reaffirmed this rating again in April 2024 but downgraded the outlook to Negative.

7

Experienced and Aligned Management Team with Extensive Operating Expertise. Our management team has strong insight and operating acumen developed from decades of successfully operating self storage facilities and creating value while navigating through multiple real estate and economic cycles. Our Founder, Chairman and Chief Executive Officer, H. Michael Schwartz, has transacted more than $7.9 billion in commercial real estate, with more than $6.2 billion in the self storage industry. The other five members of our management team have extensive self storage experience with an average of 17 years in self storage roles. We benefit from the significant experience of our management team and its ability to effectively navigate changing market conditions and achieve sustained growth. In addition, we believe the interests of our management team are strongly aligned with our stockholders. As of the completion of this offering, we expect our management team to collectively own approximately % of our outstanding common stock and OP units, which represents $ million at the midpoint of the price range set forth on the front cover of this prospectus (assuming neither our Chief Executive Officer nor his affiliates purchase any shares of our common stock pursuant to the directed share program or in this offering).

Our Business Objectives and Growth Strategies

Our primary business objective is to deliver attractive risk-adjusted returns by investing in and operating a portfolio of newer generation self storage facilities and earlier generation self storage facilities, both primarily located in urban sub-markets. We intend to maximize cash flow to stockholders through both organic and external growth utilizing multiple levers and channels.

Organic Growth Strategies:

Leverage our Technology-Driven Operating Platform to Drive Optimal Asset Level Performance. We are highly focused on maximizing cash flows at our properties by leveraging the economies of scale provided by our technology-enabled platform and proprietary systems. As we continue to scale, we intend to utilize our revenue management capabilities which include digital marketing algorithms, data warehouse with algorithmic pricing, digital tools and a dedicated call center, among others, to position us to achieve optimal market rents and occupancy, reduce operating expenses and increase the sale of ancillary products and services. Our ability to drive enhanced revenue is highlighted by our three-year average same-store revenue growth, which was 7.3%, or approximately 10 bps higher than the U.S. Publicly Listed REITs over the same period.

Margin Expansion and Other Ancillary Revenue Opportunities. There is a substantial opportunity to grow our profitability and earnings through margin improvement. The adjusted gross margin percentage of our same-store portfolio was 67.6% for the quarter ended September 30, 2024, 530 basis points below that of the average of the U.S. Listed Self Storage REITs, and the adjusted gross margin percentage for our non-stabilized wholly-owned portfolio was 47.7%. Our ability to drive rental rate growth and the maturation of our wholly-owned portfolio (both same-store and non-same-store) will lead to expanded adjusted gross margin percentage at the property level. We have also focused on reducing operating expenses and are utilizing renewable energy to reduce our utility costs. As of September 30, 2024, we have installed solar panels on 49 properties in our owned portfolio and have additional projects underway at 13 of our facilities. Those projects are expected to yield a weighted average return in the low-teens on our investment. Furthermore, the sale of ancillary products and services that are complementary to our customers’ use of our self storage facilities, including, but not limited to, tenant protection programs, locks, boxes and other packing supplies present an additional area of potential organic net operating income growth. Lastly, expanding our presence in markets where we don’t currently have significant clustering of our properties, primarily through external growth, should enable cost efficiencies through expense line items such as payroll and advertising amongst others. As an example, among our same-store portfolio, for markets where we own 10 or more properties, our average adjusted gross margin is over 70%, or approximately 300 basis points higher than the same-store portfolio average. The combination of rental rate

8

growth, general maturation, increased clustering, expense control and ancillary sales should enable both our same-store and non-same-store portfolios to achieve higher adjusted gross margin percentages than they achieve today.

Maximize Property Level Cash Flow at Non-Stabilized Stores. As of September 30, 2024, approximately 6.6% of our wholly-owned stores, as measured by net rentable square feet, were characterized as non-stabilized, or not economically stabilized. This exposure includes certificate of occupancy and lease-up stores, which are generally dilutive to cash flow in the near-term but generally have higher longer-term yield potential than investments in physically stabilized self storage facilities. During the quarter ended September 30, 2024, the average RentPOF for what we consider our non-stabilized wholly-owned portfolio was $15.56 as compared to $20.25 for our same-store portfolio. Likewise, the physical occupancy of our non-stabilized wholly-owned portfolio was 86.4%, or 620 basis points below that of our same-store portfolio. Further, our adjusted gross margin percentage was 47.7% for our non-stabilized wholly-owned portfolio, 19.9% below that of our same-store portfolio and 25.2% below the average of the U.S. Listed Self Storage REITs’ same-store portfolios for the quarter ended September 30, 2024. We believe that by leveraging our operating platform and experience, this non-stabilized portfolio has the potential to produce higher revenue and net operating income growth than our same-store portfolio until economic stabilization.

The following table breaks out our owned operating stores as of September 30, 2024, by stabilized and non-stabilized classifications:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | RentPOF

for the

Three Months

Ended

September 30,(1) | | | Ending Occupancy

as of

September 30, | |

Owned Operating Stores | | # of

Stores | | | Net Rentable

Sq. Ft. | | | Units | | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Same-Store Wholly-Owned | | | 148 | | | | 11,403,300 | | | | 98,675 | | | $ | 20.25 | | | $ | 20.14 | | | | 92.6 | % | | | 92.8 | % |

Non Stabilized Wholly-Owned | | | 9 | | | | 804,700 | | | | 7,625 | | | $ | 15.56 | | | | NM | | | | 86.4 | % | | | NM | |

Total Wholly-Owned Operating Stores | | | 157 | | | | 12,208,000 | | | | 106,300 | | | $ | 20.01 | | | | NM | | | | 92.2 | % | | | NM | |

Total Joint Venture Operating Stores | | | 10 | | | | 897,400 | | | | 9,440 | | | $ | 18.85 | | | | NM | | | | 80.0 | % | | | NM | |

Total All Owned Operating Stores | | | 167 | | | | 13,105,400 | | | | 115,740 | | | | | | | | | | | | | | | | | |

NM: Not meaningful comparison

| (1) | | RentPOF defined as annualized rental revenue net of discounts and concessions, excluding late fees, administrative fees and parking income, divided by occupied square feet of storage. Not in thousands. |

External Growth Strategies:

Our portfolio growth will primarily be driven through the acquisition of stabilized facilities, but we also intend to opportunistically acquire facilities in lease-up, facilities that have just received a certificate of occupancy, facilities in need of renovation, re-development or expansion and ground up development. As a publicly listed REIT, we believe we will have access to a more favorable cost of capital and broader capital markets solutions to help us execute on our external growth strategy. To date, we have not regularly utilized OP units as consideration for acquisitions; however, we may do so as a listed REIT using an umbrella partnership, or UPREIT, structure.

Our relative size is a key differentiator between us and the U.S. Listed Self Storage REITs. Our portfolio consists of 167 owned self storage facilities, encompassing 13.1 million net rentable square feet. By comparison, the average owned portfolio of the U.S. Listed Self Storage REITs is approximately 1,800 facilities, encompassing over 130 million net rentable square feet as of September 30, 2024, or approximately 10 times our

9

size by both metrics. We believe this dynamic will allow us to be more nimble and selective in our external growth strategy, while capitalizing on economies of scale as we grow. We intend to execute our external growth strategy in our existing markets and target markets that have comparably strong demographic and competitive trends.

| | • | | On-Balance Sheet Acquisitions. We expect to acquire stabilized and non-stabilized properties on-balance sheet in the United States and Canada in an accretive manner to FFO, as adjusted. In Canada specifically, we believe our scale and experience competitively positions us to capitalize on acquisition opportunities in a highly fragmented market that has relatively less sophisticated and smaller operators than are in the United States. |

| | • | | Embedded Acquisition Pipeline. Subsequent to the quarter ending September 30, 2024, we acquired one property for $9.5 million, totaling approximately 17,350 NRSF and 200 self storage units. Additionally, we have built a pipeline of acquisitions that we are scheduled to close before March 31, 2025 for approximately $225 million, totaling approximately 659,500 NRSF and 6,830 self storage units. This pipeline comprises deals that are either under contract or for which we have a letter of intent to acquire. Although we are scheduled to close these acquisitions prior to the end of the first quarter of 2025, the acquisitions are subject to customary closing conditions, and there is no assurance that these properties will be acquired or will be acquired at the time or pursuant to the terms currently contemplated. These assets are located in attractive high-growth submarkets within the top 25 U.S. MSA’s or the top 25 Canadian CMA’s. These acquisitions include the following: |

| | • | | Boston MSA: We closed on the acquisition of a property in the Boston, MA MSA on November 20, 2024 for approximately $9.5 million, totaling approximately 17,350 NRSF and 200 self storage units; |

| | • | | Denver MSA: We are under contract on the acquisition of a property in the Denver, CO MSA for approximately $14.7 million, totaling approximately 87,450 NRSF and 740 self storage units; |

| | • | | San Jose MSA: We are under contract on the acquisition of a property in the San Jose, CA MSA for approximately $19.4 million, totaling approximately 59,650 NRSF and 650 self storage units; |

| | • | | Los Angeles MSA: We are under contract on the acquisition of a property in the Los Angeles, CA MSA for $70.0 million, totaling approximately 136,300 NRSF and 1,300 self storage units; |

| | • | | Washington MSA: We are under contract on the acquisition of a property in the Washington-Arlington-Alexandria MSA for $18.0 million, totaling approximately 74,300 NRSF and 830 self storage units; |

| | • | | New York MSA: We are under contract on the acquisition of two properties in the New York, NY MSA for $74.5 million. These properties represent approximately 227,700 NRSF and 2,500 self storage units; |

| | • | | Kelowna CMA: We are under contract on the acquisition of a property in the Kelowna, BC CMA for approximately $28.1 million ($39.3 million CAD), totaling approximately 74,100 NRSF and 810 self storage units; |

| | • | | Canadian Platform Provides Growth Opportunities with Less Institutional Competition. According to Colliers, we are currently the fifth largest self storage operator in Canada based on rentable square footage and believe we will be the only U.S. Listed Self Storage REIT with an owned portfolio and operating platform in Canada. The percentage of self storage assets operated by sophisticated institutions is significantly lower in Canada than in the United States. This dynamic allows for a relatively lower level of operating competition while offering a range of acquisition opportunities. Our portfolio in Canada |

10

| | accounts for 15.6% of our total owned portfolio as measured by rentable square feet and is exclusively in the GTA. We intend to target investments in other CMAs in Canada, including, but not limited to, Vancouver, Montreal, Edmonton, Calgary, and Ottawa. As of September 30, 2024, we have a 50% interest in a joint venture, along with SmartCentres, which owns a property in the Vancouver CMA. The joint venture intends to develop this property into a self storage facility in the future. Also, as of September 30, 2024, the Managed REITs own an operating property in Vancouver, three properties in development in Vancouver, two operating properties in Edmonton, and three properties in development in Montreal. |

| | • | | Joint Ventures. We have a joint venture with SmartCentres, which owns a diversified portfolio of real estate in Canada and is one of the largest TSX-listed REITs. The 50/50 joint venture affords each party a right of first offer to develop self storage facilities in certain CMAs in Canada. As of September 30, 2024, the joint venture owned 10 operating properties in the GTA. Through this joint venture, we have a development pipeline of approximately 600,000 net rentable square feet, representing approximately 6,600 units across multiple CMAs in Canada. We expect to continue to utilize the joint venture to develop and redevelop in Canada. |

| | • | | Strategic Combinations of Affiliated Funds. With our management of the Managed REITs and our demonstrated track record of acquiring or merging with previous Managed REITs, we believe our Managed REIT platform provides a potential future pipeline of relatively large portfolio acquisitions for us, serving to enhance our external growth and cash flow to stockholders. As of September 30, 2024, the Managed REITs owned 34 assets, representing approximately 2.9 million of net rentable square feet across 26,500 units. |

| | • | | Redevelopment. Our team of seasoned professionals identifies opportunities to unlock additional value at our properties through selectively redeveloping certain properties. We plan to actively reinvest in our portfolio going forward. |

| | • | | Third-Party Management Platform. According to Colliers, the top 10 operators in Canada, as determined by square footage, account for only 20% of all self storage facilities across the country. The percentage of self storage assets operated by owners with only one or two stores in Canada is estimated at approximately 70% according to Colliers. We intend to capitalize on the nascent institutional competitive landscape by establishing a market leading third-party management platform in Canada, in which we manage and operate self storage properties owned by third parties in exchange for fees. We believe there is an opportunity to establish our third-party management platform in both Canada and the United States with nominal incremental investment, either through the development of our own third-party management platform or an investment in an existing third-party management platform. |

Post Quarter-End Operations Update:

Subsequent to the quarter ending September 30, 2024, we provided an update to the following metrics for our 2024 same-store pool:

| | • | | Physical occupancy as of October 31, 2024 and October 31, 2023 was 92.4% and 92.4%, respectively. Physical occupancy as of November 30, 2024 and November 30, 2023 was 92.3% and 92.2%, respectively. |

| | • | | Monthly web rates as of October 31, 2024 and October 31, 2023 were $1.08 and $1.18, respectively. Monthly web rates as of November 30, 2024 and November 30, 2023 were $0.97 and $1.17, respectively. |

| | • | | Monthly move-in rates as of October 31, 2024 and October 31, 2023 were $1.05 and $1.01, respectively. Monthly move-in rates as of November 30, 2024 and November 30, 2023 were $1.00 and $1.05, respectively. |

11

| | • | | Monthly in-place rates as of October 31, 2024 and October 31, 2023 were $1.64 and $1.62, respectively. Monthly in-place rates as of November 30, 2024 and November 30, 2023 were $1.64 and $1.60, respectively. |

Self Storage Industry Overview and Market Opportunity

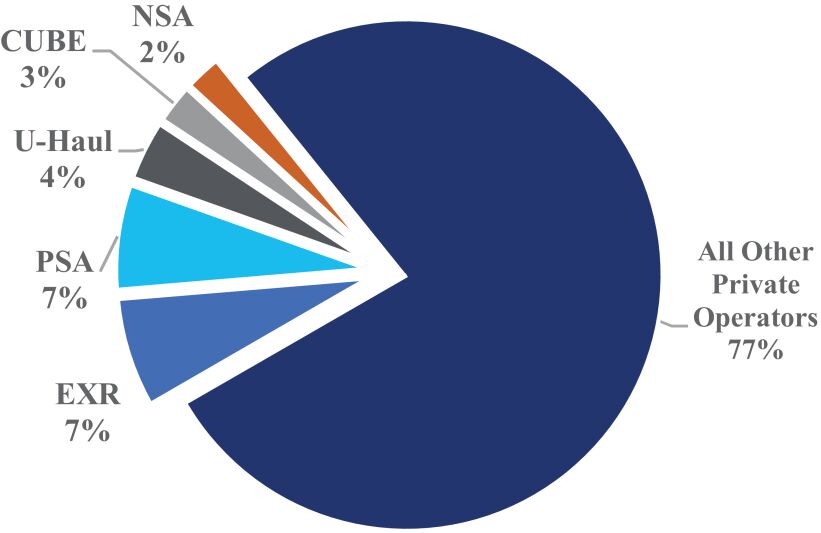

The self storage industry is highly fragmented, with owners and operators ranging from individual property owners to blue chip institutional investors and large, publicly traded REITs. According to the 2024 Self-Storage Almanac published by Mini-Storage Messenger and MiniCo Publishing, or the 2024 Self-Storage Almanac, there are approximately 52,300 primary self storage facilities in the United States representing a total of 2.1 billion rentable square feet. The largest 100 operators manage approximately 60% of net rentable square footage, but only 35% of all U.S.-based self storage properties. The U.S. Listed Self Storage REITs and AMERCO (NASDAQ: UHAL) operate approximately 23% of all U.S.-based self storage properties. Similar to the U.S. self storage market, the self storage market in Canada exhibits highly fragmented ownership, albeit to a much greater extent. Colliers estimates that approximately 70% of all self storage facilities in Canada are owned by individuals with only one or two stores. The top 10 operators in Canada, as determined by square footage, account for only 20% of all self storage facilities across the country. With the majority of the existing supply operated locally by non-institutional groups in the United States and Canada, there is a significant market opportunity to acquire existing facilities and increase revenue and profitability through professional management, technological platforms and physical expansion projects.

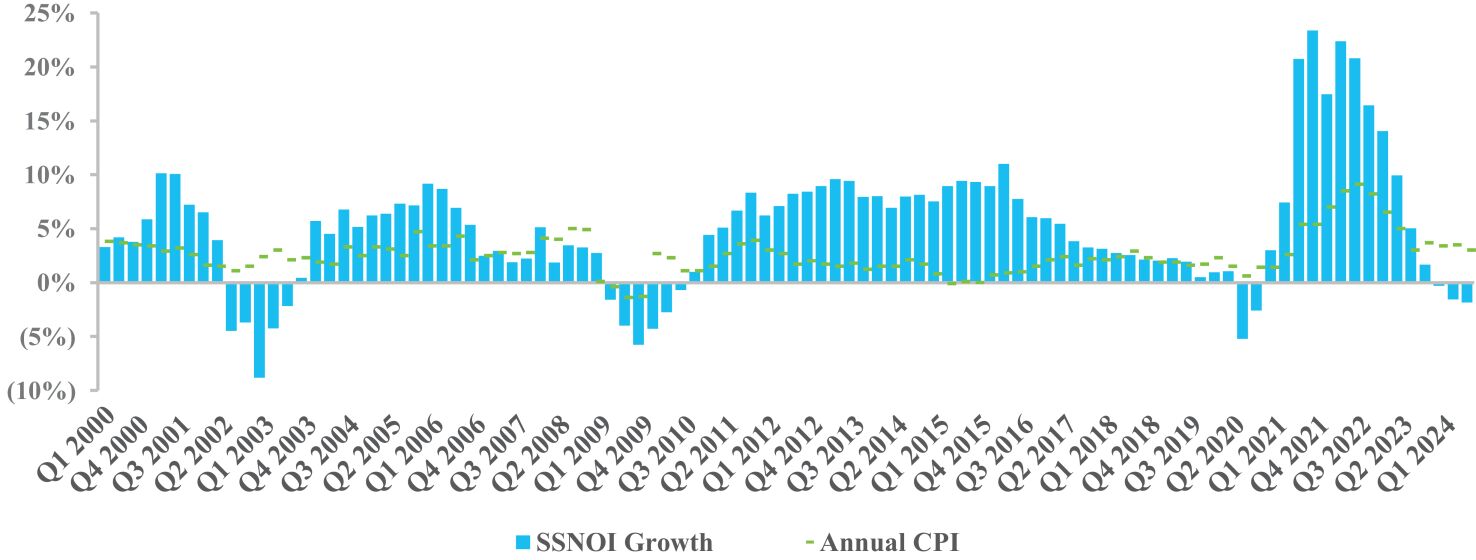

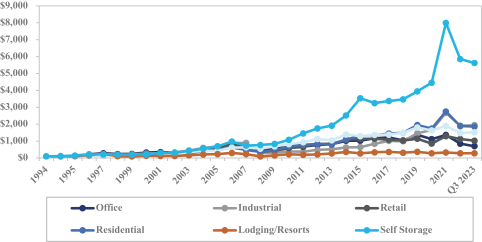

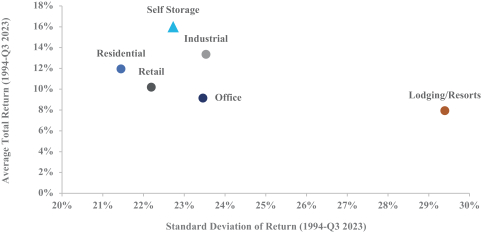

The combination of attractive fundamentals and superior operating performance has driven self storage to outperform other real estate sectors in both the private and public markets. According to NAREIT, the self storage sector has been one of the best performing REIT sectors since 1994. While past performance is not indicative of future results, a $100 investment in the self storage sector in 1994 would have yielded $6,941 through 2023, an approximately 6,900% total return. The second best performing NAREIT real estate sub-sector, residential, would have yielded a value of $2,036 over the same period, while a $100 investment in lodging / resorts would have only yielded $345. Furthermore, the self storage sector was the best performing real estate sector in 2021 and was the fifth best performing real estate sector in 2023.

More recently, strength in housing markets and the ability for employees to work remotely has fueled demand for storage, leading to a record year of operating performance across the industry in 2021 and 2022. High occupancy levels, supply constraints and inelasticity in pricing, coupled with underlining demand drivers, position the sector for continued rent growth and accelerating profitability. These drivers allowed the self storage sector to achieve outsized rent growth relative to other REIT sectors in 2021 and 2022. While the work from home environment remains elevated over pre-COVID-19 pandemic levels, this trend began to wane in 2023, which we believe led to elevated move-outs. As a result, occupancy, same-store growth and overall results began normalizing. Further, the broader economy has been experiencing elevated levels of inflation, higher interest rates, tightening monetary policies and a slowdown in home price appreciation and home sales. This could result in less discretionary spending, weakening consumer balance sheets and reduced demand for self storage. Additionally, a prolonged period of elevated inflation and/or higher interest rates could result in a further contraction of self storage demand. However, demand for the self storage sector is dynamic, with drivers that function in a multitude of economic environments, both cyclically and counter-cyclically. Demand for self storage tends to be needs-based, with numerous factors that lead customers to renting and maintaining storage units. We believe the nimble rate and leasing strategies that sophisticated operators have executed on, coupled with the improving supply environment, should position self storage favorably to achieve incremental growth in a variety of economic environments, including an inflationary environment.

12

Our Structure

Share Classes and Conversion

Our charter authorizes us to issue up to 900,000,000 shares of stock, of which 700,000,000 shares are designated as common stock at $0.001 par value per share and 200,000,000 shares are designated as preferred stock at $0.001 par value per share. Of the 700,000,000 shares of common stock authorized, shares are classified as Class A common stock, shares are classified as Class T common stock, and shares are unclassified common stock.