UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: 811-22895 |

Capitol Series Trust

(Exact name of registrant as specified in charter)

Ultimus Fund Solutions, LLC

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Address of principal executive offices) (Zip code)

Zachary P. Richmond

Ultimus Fund Solutions, LLC

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Name and address of agent for service)

| Registrant’s telephone number, including area code: | 513-587-3400 |

| Date of fiscal year end: | September 30 |

| Date of reporting period: | September 30, 2023 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| |

| |

| |

| |

| |

|

| |

| |

| |

| |

| |

| Guardian Capital Dividend Growth Fund |

| |

| Institutional Shares – DIVGX |

| |

| |

| |

| |

| |

| Guardian Capital Fundamental Global Equity Fund |

| |

| Institutional Shares – GFGEX |

| |

| |

| |

| |

| |

| Alta Quality Growth Fund |

| |

| Institutional Shares – AQLGX |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Annual Report |

| |

| |

| |

| |

| |

| September 30, 2023 |

Guardian Capital Dividend Growth Fund

Letter to Shareholders (Unaudited)

Dear Fellow Shareholders,

Guardian Capital has provided investment management services to our clients for more than 60 years and we remain steadfast in our belief that the Guardian Capital Dividend Growth Fund (the “Guardian Dividend Fund”) represents a unique approach to investing in global equities. We are grateful for the continued growth and support of our shareholders as we have navigated the pandemic and the “new normal”.

Global equity markets came under pressure during the period as persistently high inflation rates prompted central banks to sustain the tightening cycle, which pushed interest rates higher.

Risk appetites reversed earlier in the year 2023, when investors welcomed a strong start to corporate earnings season when companies posted better-than-expected first-quarter results. However, the impact of the global central banks’ ongoing tightening campaign became increasingly apparent as the more interest rate-sensitive areas of the economy felt greater pressure. In particular, the failure of two U.S. regional banks and concerns about Europe’s Credit Suisse triggered a sharp reversal in investor sentiment from the optimism that had built up at the beginning of the year. Adding to the weaker market sentiment was the surge in oil prices, which surged in the quarter ending September 2023, as OPEC members deepened their supply cuts over concerns about global demand.

Developed equity markets rallied against this backdrop as volatility gauges were muted and valuations moved higher. Despite facing the negative energy-price shock and higher interest rates, growth stocks had strong year-to-date outperformance versus developed market equities generally. Contributing to the higher valuations mid-year was the sharp and decisive rally in a handful of large- and mega-cap technology stocks, fueled by AI (artificial intelligence) euphoria and significantly adding to the overall gains in the year’s first half. The United States led the charge, and gains were spearheaded by the Technology sector. The NASDAQ Composite Index reached record highs during the period, and stock indices MSCI AC World Total Return Index, MSCI World Index and MSCI EAFE Total Return Index were also up by double digits recovering from negative returns in 2022.

Recent economic indicators have also demonstrated consumer-driven resilience, suggesting continued growth, notwithstanding the burden of higher interest rates. Wage pressures gradually eased, signalling a more balanced supply and demand, and instilling confidence that labour markets may continue to cool off. Amid the challenging supply-chain landscape, the U.S. ISM Manufacturing Purchasing Managers’ Index (PMI) showed signs of improvement, reflecting a move toward recovery driven by an increase in factory

Guardian Capital Dividend Growth Fund

Letter to Shareholders (Unaudited) (continued)

employment and a rise in new orders. Overall, economic and earnings growth forecasts, which faced downgrades earlier in the year, have adjusted upward, and concerns about a significant near-term economic downturn were muted.

The Guardian Dividend Fund returned 18.91% in the twelve months ended September 30, 2023, underperforming the MSCI World Index, which returned 21.95%. Stock selection in the Health Care, Energy and Financials sectors contributed to performance. Top individual contributors to performance included, Novo-Nordisk, Broadcom, Microsoft, Allianz and Total Energies. Stock selection in the Communications, Industrials and Real Estate sectors detracted from performance. Individual securities which detracted from performance included Telus, Verizon and Medical Properties REIT. The 2022 headwinds that punished equities (inflation, rising rates, geopolitical turmoil and recession fears) remain a force in 2023, although they continue to shift and vary in magnitude.

The Guardian Dividend Fund’s Adviser continues to favour companies with solid free cash flow and earnings, and strong balance sheets, with the ability to continue to grow dividends and with a low probability of dividend cuts. Over the past 12 months, 100% of the companies in the portfolio had dividend increases, and there have been no dividend cuts. The portfolio is overweight Energy as we continue to see strong dividends coming from the Energy sector. Other sector overweights are Health Care and Consumer Staples. The portfolio is underweight Consumer Discretionary, Materials and Financials.

There has been some dividend yield and growth moderation, but going forward the Adviser is expecting some strength towards year-end and into 2024. The Adviser aims to construct a portfolio with attractive dividend yields and earnings growth with a low probability of dividend cuts, rather than chasing the highest-yielding companies that may create exposure to unwanted credit risk and potential dividend cuts. A yield-for-yield sake approach is not beneficial, and this is especially apparent in a higher interest rate environment where credit is much more important.

The Adviser’s key focus is to invest in companies with quality earnings growth, rising cash flows and low borrowing costs, which makes them less sensitive to interest-rate movement. The Adviser believes anticipated dividend stability and potential growth can provide an effective inflation hedge.

We thank you for your support of the Guardian Dividend Fund.

Sincerely,

Guardian Capital LP

Guardian Capital Fundamental Global Equity Fund

Letter to Shareholders (Unaudited)

Dear Fellow Shareholders,

We are grateful for the trust and support of our shareholders amidst the economic uncertainty of the past year. Guardian Capital has provided investment management services to our clients for more than 60 years and we remain steadfast, alongside our Sub-Adviser GuardCap Asset Management Limited, in our belief that the Guardian Capital Fundamental Global Equity Fund (the “Guardian Equity Fund”) represents a unique approach to investing in global equities. The focus on investing in high quality companies is a key factor in what the Sub-Adviser believes will drive performance in the year ahead.

Investment performance for this fiscal year encompasses the twelve month period ending September 30, 2023. For this period, the Guardian Equity Fund returned 22.73%. In comparison, the benchmark, the MSCI World Index returned 21.95%. The Guardian Equity Fund’s Sub-Adviser’s underlying investment philosophy emphasizes long-term thinking, long-term forecasting, and long-term holding periods. This is in contrast to the trend of shortening holding periods and time horizons in the general market. Periods of greater uncertainty and volatility, such as we have experienced over the last six months, tend to exacerbate the market’s short-termism even further. As the Sub-Adviser, we are not investing in companies based on expectations for financial results during the next quarter, but instead over the next 20 quarters or more.

When analyzing companies, the Sub-Adviser measures them against 10 “Confidence Criteria” – 5 Growth Criteria and 5 Quality Criteria. Companies must satisfy all criteria in order to be considered for inclusion in the Guardian Equity Fund. One of these criteria is the existence, and persistence, of a secular industry growth trend. To us, this means that regardless of economic conditions, market volatility, geopolitical risks, or other external factors, the subject company operates in an industry that is growing sustainably at above-average rates for at least the next 5 years. While none of us could have predicted a global pandemic and the resulting social or economic effects, many of these existing trends have rapidly accelerated as a result. For instance, the rapid digitization of our world has only accelerated since COVID-19 lockdowns were first put in place, with Work-from-Home arrangements permanently solidifying these gains.

For this fiscal period, the Guardian Equity Fund outperformed the MSCI World Index primarily due to stock selection. Specifically, the positions in Novo Nordisk (+84%), Booking Holdings (+88%), Mastercard (+40%), EssilorLuxottica (+29%), and Alphabet (+37%), rounded out the top 5 contributors. The bottom contributors for the period included: Illumina (total return -28%), Novozymes (-19%), FANUC (-5%), Coloplast (+6%), and UnitedHealth (+1%).

Guardian Capital Fundamental Global Equity Fund

Letter to Shareholders (Unaudited) (continued)

The Guardian Equity Fund does not hold securities in the Utilities, Energy, or Real Estate sectors. It also avoids stocks in industries where company revenues have above-average sensitivity to the economic cycle, such as commodity producers and banks. Companies in these sectors and industries have historically failed to meet both Growth and Quality requirements of the Sub-Adviser’s 10 Confidence Criteria. Shares of these types of companies outperformed during the period and, as a result, detracted from relative performance.

During the fiscal period the Guardian Equity Fund did not initiate any new positions or exit any existing holdings. The Guardian Equity Fund adjusted existing holdings on the basis of valuation, trimming holdings the Sub-Adviser deemed to be relatively overvalued and consequently adding to positions the Sub-Adviser deemed to be relatively undervalued.

The current 25 portfolio holdings are those that the Sub-Adviser’s portfolio management team feels best represent its investment philosophy: growth drives returns, quality protects to the downside, and valuation matters. The team has built confidence over an exhaustive research process that these holdings will continue to remain high quality companies capable of sustaining above-average growth well beyond the normal market time horizon. We thank you for your support of the Guardian Equity Fund.

Sincerely,

Guardian Capital LP

Alta Quality Growth Fund

Letter to Shareholders (Unaudited)

Dear Fellow Shareholders,

The whipsaw pattern of equity markets continued this past year, following positive double-digit returns two years ago driven by pandemic-driven stimulus and negative double-digit returns last year due to soaring inflation and the reduction of stimulus. Even though inflation has steadily come down throughout the year, the Federal Reserve continues to communicate a hawkish stance, that rates will stay higher for longer. The market has grappled with a rising 10-year treasury bond rate, with that rate now near 4.7%, reflecting uncertainty surrounding monetary policy. Stock (and by inference, market) valuation is based on interest rates, and all things equal, the higher the interest rates, the lower the value of a future stream of cash flow. Despite the fastest rate hike cycle in recent memory, the stock market over the past 12 months has again produced positive double-digit returns. Interest rate changes typically filter through the economy with a lag, meaning we have yet to see the full effects of recent rate hikes.

For the twelve months ended September 30, 2023, the Alta Quality Growth Fund (the “Alta Growth Fund”) returned 21.04% versus the Russell 1000 Growth Index’s return of 27.72%, with security selection producing the majority of the underperformance. Specifically, selection in the Technology and Communications sectors hurt relative returns. Conversely, stock selection in the Consumer Discretionary sector produced positive allocation effects for the portfolio.

Booking Holdings, Adobe, TJX, Mastercard and Microsoft were our top 5 performing positions for the year. Each of these companies are leaders in their respective industries and benefited from continued high demand for their products during this economically uncertain time. Our laggards for the period, Dollar General, PayPal, Meta Platforms, Walt Disney, and RTX were all impacted by some combination of higher interest rates, the effects of higher inflation and disappointing operating results.

We added the following five new positions to the Alta Growth Fund: Amazon, Dollar General, UnitedHealth Group, Icon, and Intuit. During the period we sold the following five positions in their entirety: Fortune Brands Innovations, Master Brands, Steris, Match Group, and Meta Platforms. Amazon, UnitedHealth, Icon, and Intuit are leaders in the technology and health care industries, respectively, leveraging technology to create and maintain competitive advantages relative to peers. Likewise, Dollar General is a leader in the U.S. discount retailer industry, but also provides the portfolio with a counter-cyclical exposure to the economic uncertainty. The companies that we sold either reached our internal intrinsic valuation target (Fortune Brands Innovations and Master Brands) or a

Alta Quality Growth Fund

Letter to Shareholders (Unaudited) (continued)

degradation of our investment thesis (Steris, Match Group and Meta Platforms). The Alta Growth Fund ended the fiscal year with thirty holdings.

Financial conditions have tightened significantly, both as a result of rising rates but also due to continued quantitative tightening action by the Fed. Oil prices are closing in on $100 per barrel, keeping inflation worries at the forefront of consumers’ and investors’ minds. In the meantime, many continue to expect a recession that, to date, has not materialized. The economy has softened to be sure, but has proven to be much more resilient than many expected. Recent economic gains seem precarious with talk of strikes, shutdowns, and student loans repayments looming.

At the same time, with everyone positioned for a recession, that in and of itself could be good news for the market. It is the opposite of a stock bubble.

What else could propel this market higher into year end and into 2024? Inflation, particularly core inflation, ex food and energy prices, continues to be on a steady glide path lower, giving the Fed room to pause, if not stop, raising rates. On the earnings front, there is no indication that things are on the cusp of blowing up. Since everyone has been expecting a recession for over a year now, consumers and businesses have adjusted their behavior accordingly. Growth levels have slowly normalized from generational highs to pre-crisis levels. The economy is slowing but not falling off a cliff, credit quality is good, wage growth is moderating. Consensus earnings estimates for the S&P 500® are forecast at +2% for the third quarter and +12% for 2024. Yes, rates have been higher than expected and will probably be higher for longer than expected. Even if inflation falls, a stronger than expected economy allows the Fed to keep rates higher for longer. Having said that, higher yields don’t necessarily preclude stock performance: in the mid-80s to 2008, real rates were higher than now and over that period, stocks returned 15% per annum.

The Alta Growth Fund seeks to invest in businesses with attractive fundamental characteristics and a supporting secular theme, priced at reasonable valuations. We believe that the best companies offer consistent and growing revenue and cash flow, good returns on investment, and durable competitive advantages. These companies generally all benefit from pricing power due to their strong position in the marketplace. While it may seem appealing to chase high-flying, innovative, and yet-to-be-proven growth companies, we believe that the best risk-adjusted returns are delivered by owning quality growth companies with a proven ability to generate profit. We thank you for your confidence and support of the Alta Growth Fund.

Sincerely,

Alta Capital Management, LLC

Investment Results (Unaudited)

Average Annual Total Returns(a) as of September 30, 2023

| | | | Since |

| | | | Inception |

| | One Year | Three Year | 5/1/2019 |

| Guardian Capital Dividend Growth Fund | | | |

| Institutional Shares | 18.91% | 7.40% | 8.14% |

| MSCI World Index(b) | 21.95% | 8.08% | 8.15% |

| | | | |

| | | Expense | |

| | | Ratios(c) | |

| | | Institutional | |

| | | Shares | |

| Gross | | 1.67% | |

| With Applicable Waivers | | 0.95% | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Guardian Capital Dividend Growth Fund (the “Guardian Dividend Fund”) distributions or the redemption of Guardian Dividend Fund shares. Current performance of the Guardian Dividend Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (800) 957-0681.

| (a) | Return figures reflect any change in price per share and assume the reinvestment of all distributions. The Guardian Dividend Fund’s returns reflect any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. |

| (b) | The MSCI World Index is an unmanaged free float-adjusted market capitalization index that is designed to measure global developed market equity performance. Currently the MSCI World Index consists of the following 23 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The performance of the index is expressed in terms of U.S. dollars, and does not reflect the deduction of fees or taxes with a mutual fund, such as investment management and fund accounting fees. Individuals cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

| (c) | The expense ratio is from the Guardian Dividend Fund’s prospectus dated January 27, 2023. Guardian Capital LP, the Guardian Dividend Fund’s adviser (the “Adviser”), has contractually agreed to waive its management fee and/or reimburse expenses so that total annual operating expenses for the Guardian Dividend Fund (excluding (i) interest; (ii) taxes; (iii) brokerage fees and commissions; (iv) other extraordinary expenses not incurred in the ordinary course of the Guardian Dividend Fund’s business; (v) dividend expense on short sales; and (vi) indirect expenses such as acquired fund fees and expenses) do not exceed 0.95% of the Guardian Dividend Fund’s average daily net assets through January 31, 2024 (the “Expense Limitation”). During any fiscal year that the Investment Advisory Agreement between the Adviser and the Capitol Series Trust (the “Trust”) is in effect, the Adviser may recoup the sum of all fees previously waived or expenses reimbursed, less any |

Investment Results (Unaudited) (continued)

reimbursement previously paid, provided that the Adviser is only permitted to recoup fees or expenses within 36 months from the date the fee waiver or expense reimbursement first occurred and provided further that such recoupment can be achieved within the Expense Limitation Agreement currently in effect and the Expense Limitation Agreement in place when the waiver/reimbursement occurred. This Expense Limitation Agreement may be terminated by the Board of Trustees (the “Board”) at any time. The Expense Limitation Agreement terminates automatically upon the termination of the Investment Advisory Agreement with the Adviser. Additional information pertaining to the Guardian Dividend Fund’s expense ratios as of September 30, 2023, can be found in the financial highlights.

The Guardian Dividend Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Guardian Dividend Fund and may be obtained by calling (800) 957-0681. Please read it carefully before investing.

The Guardian Dividend Fund is distributed by Ultimus Fund Distributors, LLC, Member FINRA/SIPC.

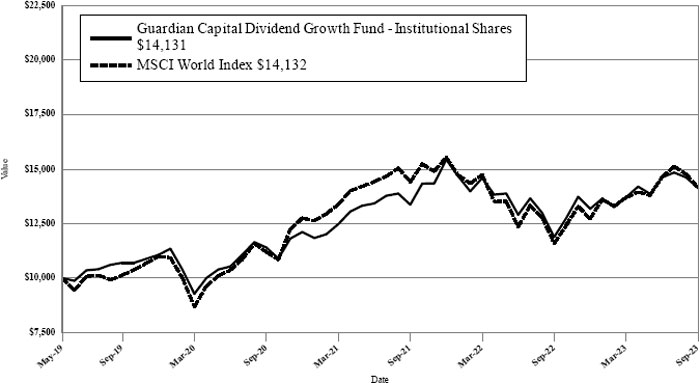

Investment Results (Unaudited) (continued)

Comparison of the Growth of a $10,000 Investment in the Guardian Capital Dividend Growth Fund – Institutional Shares and the MSCI World Index

The chart above assumes an initial investment of $10,000 made on May 1, 2019 (commencement of operations) and held through September 30, 2023. THE GUARDIAN DIVIDEND FUND’S RETURNS REPRESENT PAST PERFORMANCE AND DO NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on the Guardian Dividend Fund’s distributions or the redemption of the Guardian Dividend Fund’s shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Guardian Dividend Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call (800) 957-0681. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Guardian Dividend Fund before investing. The Guardian Dividend Fund’s prospectus contains this and other information about the Guardian Equity Fund and should be read carefully before investing.

The Guardian Dividend Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

Investment Results (Unaudited) (continued)

Average Annual Total Returns(a) as of September 30, 2023

| | | | Since |

| | | | Inception |

| | One Year | Three Year | (12/19/19) |

| Guardian Capital Fundamental Global Equity Fund | | | |

| Institutional Shares | 22.73% | 5.46% | 6.02% |

| MSCI World Index(b) | 21.95% | 8.08% | 7.06% |

| | | | |

| | | | Expense |

| | | | Ratios(c) |

| | | | Institutional |

| | | | Shares |

| Gross | | | 1.51% |

| With Applicable Waivers | | | 0.99% |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Guardian Capital Fundamental Global Equity Fund (“Guardian Equity Fund”) distributions or the redemption of Guardian Equity Fund shares. Current performance of the Guardian Equity Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (800) 957-0681.

| (a) | Return figures reflect any change in price per share and assume the reinvestment of all distributions. The Guardian Equity Fund’s returns reflect any fee reductions during the applicable period. If such fee reductions had not occurred, the quoted performance would have been lower. |

| (b) | The MSCI World Index is an unmanaged free float-adjusted market capitalization index that is designed to measure global developed market equity performance. Currently the MSCI World Index consists of the following 23 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The performance of the index is expressed in terms of U.S. dollars, and does not reflect the deduction of fees or taxes with a mutual fund, such as investment management and fund accounting fees. Individuals cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

| (c) | The expense ratios are from the Guardian Equity Fund’s prospectus dated January 27, 2023. The Adviser has contractually agreed to waive its management fee and/or reimburse expenses so that total annual operating expenses for the Guardian Equity Fund (excluding (i) interest; (ii) taxes; (iii) brokerage fees and commissions; (iv) other extraordinary expenses not incurred in the ordinary course of the Guardian Equity Fund’s business; (v) dividend expense on short sales; and (vi) indirect expenses such as acquired fund fees and expenses) do not exceed 0.99% of the average daily net assets of the Guardian Equity Fund through January 31, 2024 (the “Expense Limitation”). During any fiscal year that the Investment Advisory Agreement between the Adviser and Trust is in effect, the Adviser may recoup the sum of all fees previously waived or expenses reimbursed, less any reimbursement previously paid, provided that the Adviser is only permitted to recoup fees or |

Investment Results (Unaudited) (continued)

expenses within 36 months from the date the fee waiver or expense reimbursement first occurred and provided further that such recoupment can be achieved within the Expense Limitation Agreement currently in effect and the Expense Limitation Agreement in place when the waiver/reimbursement occurred. This Expense Limitation Agreement may be terminated by the Board at any time. The Expense Limitation Agreement terminates automatically upon the termination of the Investment Advisory Agreement with the Adviser. Additional information pertaining to the Guardian Equity Fund’s expense ratios as of September 30, 2023, can be found in the financial highlights.

The Guardian Equity Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Guardian Equity Fund and may be obtained by calling (800) 957-0681. Please read it carefully before investing

The Guardian Equity Fund is distributed by Ultimus Fund Distributors, LLC, Member FINRA/SIPC.

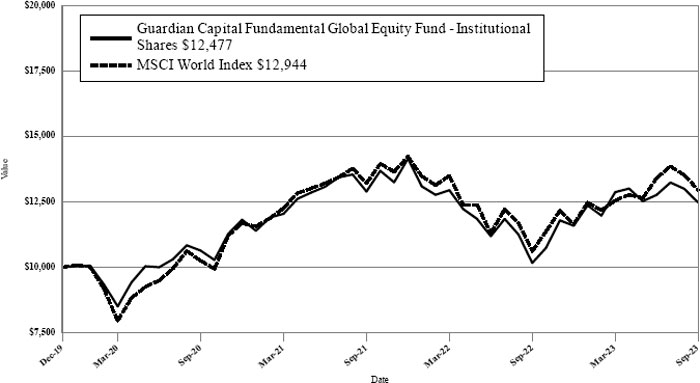

Investment Results (Unaudited) (continued)

Comparison of the Growth of a $10,000 Investment in the Guardian Capital Fundamental Global Equity Fund – Institutional Shares and the MSCI World Index

The chart above assumes an initial investment of $10,000 made on December 19, 2019 (commencement of operations) and held through September 30, 2023. THE GUARDIAN EQUITY FUND’S RETURNS REPRESENT PAST PERFORMANCE AND DO NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on the Guardian Equity Fund’s distributions or the redemption of the Guardian Equity Fund’s shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Guardian Equity Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call (800) 957-0681. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Guardian Equity Fund before investing. The Guardian Equity Fund’s prospectus contains this and other information about the Guardian Equity Fund and should be read carefully before investing.

The Guardian Equity Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

Investment Results (Unaudited) (continued)

Average Annual Total Returns(a) as of September 30, 2023

| | | | Since |

| | | | Inception |

| | One Year | Three Year | (12/19/18) |

| Alta Quality Growth Fund-Institutional Shares | 21.04% | 3.96% | 10.26% |

| S&P 500® Index (b) | 21.62% | 10.15% | 13.81% |

| Russell 1000® Growth Index (c) | 27.72% | 7.97% | 17.26% |

| | | | |

| | | Expense | |

| | | Ratios(d) | |

| | | Institutional | |

| | | Shares | |

| Gross | | 1.18% | |

| With Applicable Waivers | | 0.79% | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Alta Quality Growth Fund (“Alta Growth Fund”) distributions or the redemption of Alta Growth Fund shares. Current performance of the Alta Growth Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (800) 957-0681.

| (a) | Return figures reflect any change in price per share and assume the reinvestment of all distributions. The Alta Growth Fund’s returns reflect any fee reductions during the applicable period. If such fee reductions had not occurred, the quoted performance would have been lower. |

| (b) | The S&P 500® Index is a widely recognized unmanaged index of equity securities and is representative of a broader domestic equity market and range of securities than is found in the Alta Growth Fund’s portfolio. Individuals cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

| (c) | The Russell 1000® Growth Index is a widely recognized unmanaged index of equity securities and is representative of a broader domestic equity market and range of securities than is found in the Alta Growth Fund’s portfolio. Individuals cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

| (d) | The expense ratios are from the Alta Growth Fund’s prospectus dated January 27, 2023. Alta Capital Management, LLC, the Alta Growth Fund’s adviser has contractually agreed to waive its management fee and/or reimburse expenses so that total annual operating expenses for the Alta Growth Fund (excluding (i) interest; (ii) taxes; (iii) brokerage fees and commissions; (iv) other extraordinary expenses not incurred in the ordinary course of the Alta Growth Fund’s business; (v) dividend expense on short sales; and (vi) indirect expenses such as acquired fund fees and expenses) do not exceed 0.79% of the average daily net assets of the Alta Growth Fund through January 31, 2024 (the “Expense Limitation”). During any fiscal year that the Investment Advisory Agreement between Alta Capital Management, LLC and the Trust is in effect, Alta Capital Management, LLC |

Investment Results (Unaudited) (continued)

may recoup the sum of all fees previously waived or expenses reimbursed, less any reimbursement previously paid, provided that the Alta Capital Management, LLC is only permitted to recoup fees or expenses within 36 months from the date the fee waiver or expense reimbursement first occurred and provided further that such recoupment can be achieved within the Expense Limitation Agreement currently in effect and the Expense Limitation Agreement in place when the waiver/reimbursement occurred. This Expense Limitation Agreement may be terminated by the Board at any time. The Expense Limitation Agreement terminates automatically upon the termination of the Advisory Agreement with Alta Capital Management, LLC. Additional information pertaining to the Alta Growth Fund’s expense ratios as of September 30, 2023, can be found in the financial highlights.

The Alta Growth Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Alta Growth Fund and may be obtained by calling (800) 957-0681. Please read it carefully before investing.

The Alta Growth Fund is distributed by Ultimus Fund Distributors, LLC, Member FINRA/SIPC.

Investment Results (Unaudited) (continued)

Comparison of the Growth of a $10,000 Investment in the Alta Quality Growth Fund – Institutional Shares, the S&P 500® Index and the Russell 1000® Growth Index

The chart above assumes an initial investment of $10,000 made on December 19, 2018 (commencement of operations) and held through September 30, 2023. THE ALTA GROWTH FUND’S RETURNS REPRESENT PAST PERFORMANCE AND DO NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on the Alta Growth Fund’s distributions or the redemption of Alta Growth Fund’s shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Alta Growth Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call (800) 957-0681. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Alta Growth Fund before investing. The Alta Growth Fund’s prospectus contains this and other information about the Alta Growth Fund and should be read carefully before investing.

The Alta Growth Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

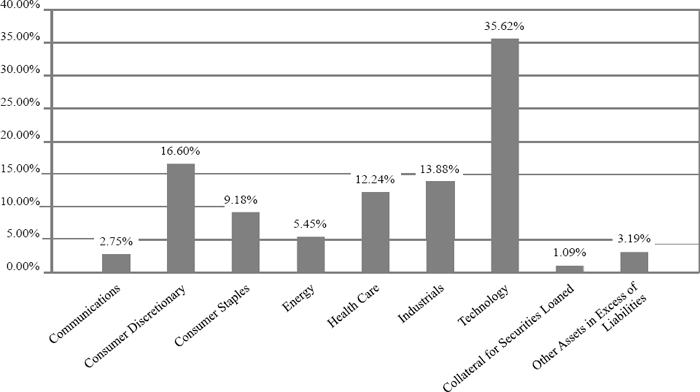

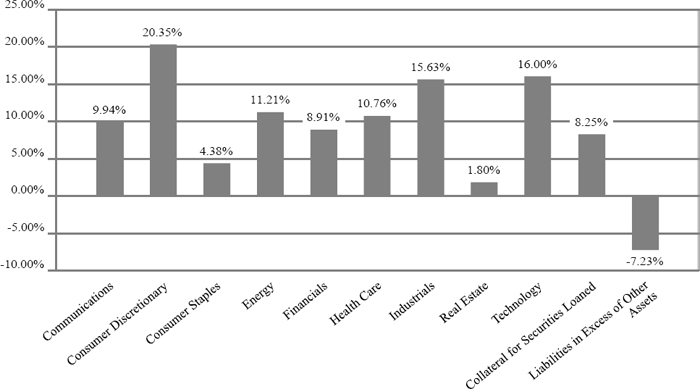

Fund Holdings (Unaudited)

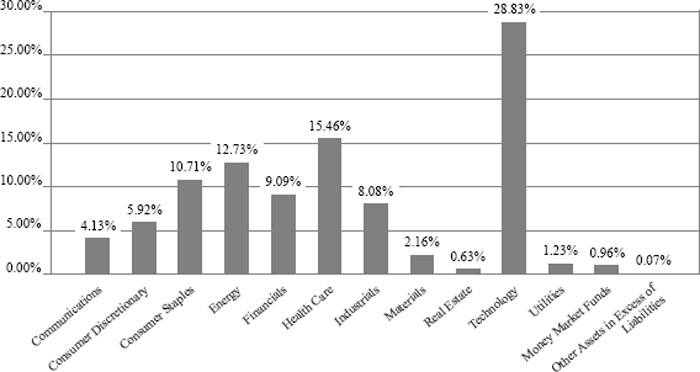

Guardian Capital Dividend Growth Fund Holdings as of September 30, 2023.*

| * | As a percentage of net assets. |

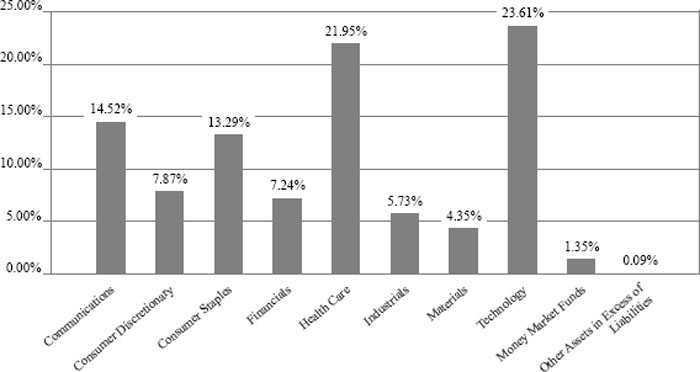

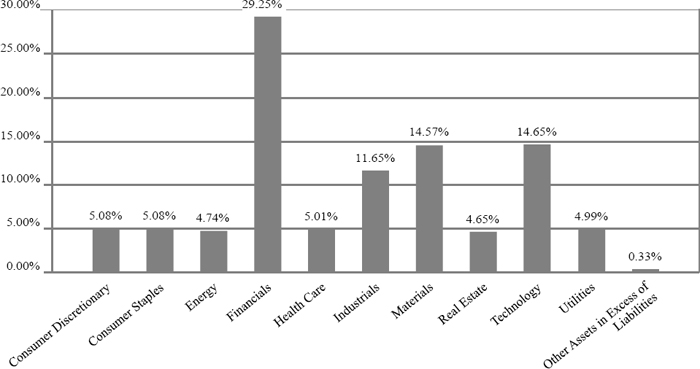

Guardian Capital Fundamental Global Equity Fund Holdings as of September 30, 2023.*

| * | As a percentage of net assets. |

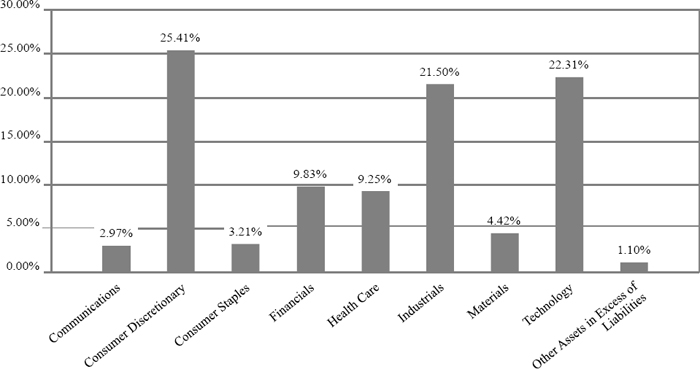

Fund Holdings (Unaudited)

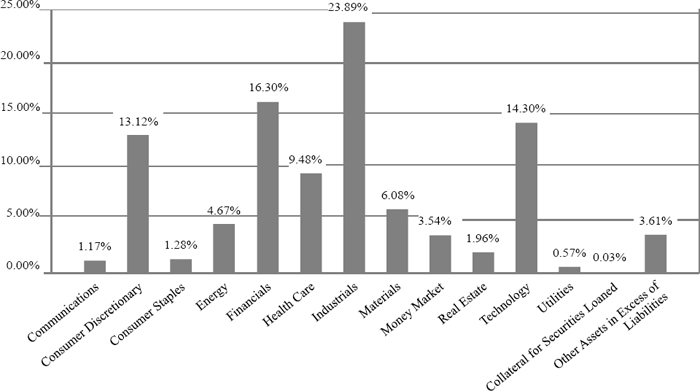

Alta Quality Growth Fund Holdings as of September 30, 2023.*

| * | As a percentage of net assets. |

Availability of Portfolio Schedules (Unaudited)

The Funds file a complete schedule of portfolio holdings with the Securities and Exchange Commission (the “SEC”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Funds’ Form N-PORT reports are available on the SEC’s website at http:// www.sec.gov or on the Funds’ website at www.guardiancapitalfunds.com.

| Guardian Capital Dividend Growth Fund |

| Schedule of Investments |

| September 30, 2023 |

| | | Shares | | | Fair Value | |

| Common Stocks — 98.97% | | | | | | |

| Australia — 0.72% | | | | | | | | |

| Energy — 0.72% | | | | | | | | |

| Woodside Energy Group Ltd. - ADR | | | 6,450 | | | $ | 150,221 | |

| Total Australia | | | | | | | 150,221 | |

| | | | | | | | | |

| Canada — 5.86% | | | | | | | | |

| Communications — 2.50% | | | | | | | | |

| BCE, Inc. | | | 5,162 | | | | 197,056 | |

| TELUS Corp. | | | 19,751 | | | | 322,533 | |

| | | | | | | | 519,589 | |

| Financials — 3.36% | | | | | | | | |

| Royal Bank of Canada | | | 7,987 | | | | 698,004 | |

| Total Canada | | | | | | | 1,217,593 | |

| | | | | | | | | |

| Denmark — 3.07% | | | | | | | | |

| Health Care — 3.07% | | | | | | | | |

| Novo Nordisk A/S - ADR | | | 7,020 | | | | 638,400 | |

| Total Denmark | | | | | | | 638,400 | |

| | | | | | | | | |

| France — 10.58% | | | | | | | | |

| Consumer Discretionary — 1.55% | | | | | | | | |

| LVMH Moet Hennessy Louis Vuitton S.A. - ADR | | | 2,131 | | | | 322,015 | |

| | | | | | | | | |

| Energy — 3.93% | | | | | | | | |

| TotalEnergies S.E. - ADR | | | 12,452 | | | | 818,843 | |

| | | | | | | | | |

| Financials — 1.96% | | | | | | | | |

| AXA S.A. | | | 13,700 | | | | 408,147 | |

| | | | | | | | | |

| Health Care — 0.99% | | | | | | | | |

| Sanofi - ADR | | | 3,830 | | | | 205,441 | |

| | | | | | | | | |

| Industrials — 2.15% | | | | | | | | |

| Schneider Electric S.E. - ADR | | | 13,574 | | | | 447,806 | |

| Total France | | | | | | | 2,202,252 | |

| | | | | | | | | |

| Germany — 2.07% | | | | | | | | |

| Financials — 2.07% | | | | | | | | |

| Allianz S.E. | | | 1,800 | | | | 429,495 | |

| Total Germany | | | | | | | 429,495 | |

| | | | | | | | | |

| Ireland — 3.49% | | | | | | | | |

| Technology — 3.49% | | | | | | | | |

| Accenture PLC, Class A | | | 2,372 | | | | 728,464 | |

| Total Ireland | | | | | | | 728,464 | |

| | | | | | | | | |

| Netherlands — 4.96% | | | | | | | | |

| Technology — 4.96% | | | | | | | | |

| ASML Holding N.V. | | | 653 | | | | 384,395 | |

| | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Dividend Growth Fund |

| Schedule of Investments (continued) |

| September 30, 2023 |

| | | Shares | | | Fair Value | |

| Common Stocks — 98.97% - (continued) | | | | | | | | |

| Netherlands — 4.96% - (continued) | | | | | | | | |

| Technology — 4.96% - (continued) | | | | | | | | |

| Wolters Kluwer N.V. - ADR | | | 5,350 | | | $ | 647,297 | |

| | | | | | | | 1,031,692 | |

| Total Netherlands | | | | | | | 1,031,692 | |

| | | | | | | | | |

| Switzerland — 3.67% | | | | | | | | |

| Consumer Staples — 3.67% | | | | | | | | |

| Nestle S.A. - ADR | | | 6,742 | | | | 762,992 | |

| Total Switzerland | | | | | | | 762,992 | |

| | | | | | | | | |

| United Kingdom — 4.03% | | | | | | | | |

| Consumer Staples — 1.14% | | | | | | | | |

| Unilever PLC - ADR | | | 4,784 | | | | 236,330 | |

| | | | | | | | | |

| Health Care — 2.89% | | | | | | | | |

| AstraZeneca PLC - ADR | | | 8,878 | | | | 601,218 | |

| Total United Kingdom | | | | | | | 837,548 | |

| | | | | | | | | |

| United States — 60.52% | | | | | | | | |

| Communications — 1.63% | | | | | | | | |

| Verizon Communications, Inc. | | | 10,429 | | | | 338,004 | |

| | | | | | | | | |

| Consumer Discretionary — 4.37% | | | | | | | | |

| Home Depot, Inc. (The) | | | 1,502 | | | | 453,844 | |

| McDonald’s Corp. | | | 1,727 | | | | 454,962 | |

| | | | | | | | 908,806 | |

| Consumer Staples — 5.90% | | | | | | | | |

| Costco Wholesale Corp. | | | 1,581 | | | | 893,202 | |

| Procter & Gamble Co. (The) | | | 2,292 | | | | 334,311 | |

| | | | | | | | 1,227,513 | |

| Energy — 8.08% | | | | | | | | |

| EOG Resources, Inc. | | | 1,734 | | | | 219,802 | |

| Shell PLC - ADR | | | 10,651 | | | | 685,711 | |

| Williams Cos., Inc. (The) | | | 22,943 | | | | 772,950 | |

| | | | | | | | 1,678,463 | |

| Financials — 1.70% | | | | | | | | |

| Hartford Financial Services Group, Inc. (The) | | | 4,993 | | | | 354,054 | |

| | | | | | | | | |

| Health Care — 8.51% | | | | | | | | |

| AbbVie, Inc. | | | 2,491 | | | | 371,308 | |

| Amgen, Inc. | | | 773 | | | | 207,751 | |

| Johnson & Johnson | | | 4,031 | | | | 627,828 | |

| UnitedHealth Group, Inc. | | | 1,114 | | | | 561,668 | |

| | | | | | | | 1,768,555 | |

| Industrials — 5.93% | | | | | | | | |

| Illinois Tool Works, Inc. | | | 778 | | | | 179,181 | |

| Republic Services, Inc. | | | 4,113 | | | | 586,144 | |

| Waste Management, Inc. | | | 3,061 | | | | 466,619 | |

| | | | | | | | 1,231,944 | |

| | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Dividend Growth Fund |

| Schedule of Investments (continued) |

| September 30, 2023 |

| | | Shares | | | Fair Value | |

| Common Stocks — 98.97% - (continued) | | | | | | | | |

| United States — 60.52% - (continued) | | | | | | | | |

| Materials — 2.16% | | | | | | | | |

| Air Products & Chemicals, Inc. | | | 1,586 | | | $ | 449,472 | |

| | | | | | | | | |

| Real Estate — 0.63% | | | | | | | | |

| Crown Castle, Inc. | | | 1,425 | | | | 131,143 | |

| | | | | | | | | |

| Technology — 20.38% | | | | | | | | |

| Apple, Inc. | | | 7,575 | | | | 1,296,916 | |

| Broadcom, Inc. | | | 1,469 | | | | 1,220,122 | |

| MasterCard, Inc., Class A | | | 1,326 | | | | 524,977 | |

| Microsoft Corp. | | | 3,779 | | | | 1,193,219 | |

| | | | | | | | 4,235,234 | |

| Utilities — 1.23% | | | | | | | | |

| WEC Energy Group, Inc. | | | 3,166 | | | | 255,021 | |

| Total United States | | | | | | | 12,578,209 | |

| | | | | | | | | |

| Total Common Stocks | | | | | | | | |

| (Cost $15,535,158) | | | | | | | 20,576,866 | |

| | | | | | | | | |

| Money Market Funds - 0.96% | | | | | | | | |

| Morgan Stanley Institutional Liquidity Funds Treasury Securities Portfolio, Institutional Class, 5.21%(a) | | | 198,872 | | | | 198,872 | |

| Total Money Market Funds | | | | | | | | |

| (Cost $198,872) | | | | | | | 198,872 | |

| | | | | | | | | |

| Total Investments — 99.93% | | | | | | | | |

| (Cost $15,734,030) | | | | | | | 20,775,738 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 0.07% | | | | | | | 13,665 | |

| Net Assets — 100.00% | | | | | | $ | 20,789,403 | |

| (a) | Rate disclosed is the seven day effective yield as of September 30, 2023. |

ADR - American Depositary Receipt

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Fundamental Global Equity Fund |

| Schedule of Investments |

| September 30, 2023 |

| | | Shares | | | Fair Value | |

| Common Stocks — 98.56% | | | | | | | | |

| China — 4.60% | | | | | | | | |

| Consumer Discretionary — 4.60% | | | | | | | | |

| Yum China Holdings, Inc. | | | 65,097 | | | $ | 3,627,205 | |

| Total China | | | | | | | 3,627,205 | |

| | | | | | | | | |

| Denmark — 12.27% | | | | | | | | |

| Health Care — 7.92% | | | | | | | | |

| Coloplast A/S, Class B | | | 6,658 | | | | 705,562 | |

| Novo Nordisk A/S, Class B | | | 60,668 | | | | 5,537,327 | |

| | | | | | | | 6,242,889 | |

| Materials — 4.35% | | | | | | | | |

| Chr. Hansen Holdings A/S | | | 29,266 | | | | 1,793,788 | |

| Novozymes A/S, Class B | | | 40,607 | | | | 1,638,741 | |

| | | | | | | | 3,432,529 | |

| Total Denmark | | | | | | | 9,675,418 | |

| | | | | | | | | |

| France — 10.15% | | | | | | | | |

| Consumer Staples — 3.27% | | | | | | | | |

| L’Oréal S.A. | | | 6,199 | | | | 2,576,855 | |

| | | | | | | | | |

| Health Care — 6.88% | | | | | | | | |

| EssilorLuxottica S.A. | | | 31,059 | | | | 5,423,094 | |

| Total France | | | | | | | 7,999,949 | |

| | | | | | | | | |

| Ireland — 5.05% | | | | | | | | |

| Technology — 5.05% | | | | | | | | |

| Accenture PLC, Class A | | | 12,953 | | | | 3,977,995 | |

| Total Ireland | | | | | | | 3,977,995 | |

| | | | | | | | | |

| Japan — 3.55% | | | | | | | | |

| Industrials — 3.55% | | | | | | | | |

| FANUC Corp. | | | 54,700 | | | | 1,424,958 | |

| Keyence Corp. | | | 3,700 | | | | 1,374,121 | |

| | | | | | | | 2,799,079 | |

| Total Japan | | | | | | | 2,799,079 | |

| | | | | | | | | |

| Switzerland — 3.60% | | | | | | | | |

| Consumer Staples — 3.60% | | | | | | | | |

| Nestle S.A. | | | 25,065 | | | | 2,840,585 | |

| Total Switzerland | | | | | | | 2,840,585 | |

| | | | | | | | | |

| United Kingdom — 4.72% | | | | | | | | |

| Consumer Staples — 2.54% | | | | | | | | |

| Reckitt Benckiser Group PLC | | | 28,350 | | | | 2,004,000 | |

| | | | | | | | | |

| Industrials — 2.18% | | | | | | | | |

| Intertek Group PLC(a) | | | 34,313 | | | | 1,721,385 | |

| Total United Kingdom | | | | | | | 3,725,385 | |

| | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Fundamental Global Equity Fund |

| Schedule of Investments (continued) |

| September 30, 2023 |

| | | Shares | | | Fair Value | |

| Common Stocks — 98.56% - (continued) | | | | | | | | |

| United States — 54.62% | | | | | | | | |

| Communications — 14.52% | | | | | | | | |

| Alphabet, Inc., Class A(a) | | | 37,543 | | | $ | 4,912,877 | |

| Booking Holdings, Inc.(a) | | | 2,118 | | | | 6,531,805 | |

| | | | | | | | 11,444,682 | |

| Consumer Discretionary — 3.27% | | | | | | | | |

| Nike, Inc., Class B | | | 26,985 | | | | 2,580,306 | |

| | | | | | | | | |

| Consumer Staples — 3.88% | | | | | | | | |

| Colgate-Palmolive Co. | | | 42,959 | | | | 3,054,815 | |

| | | | | | | | | |

| Financials — 7.24% | | | | | | | | |

| CME Group, Inc. | | | 28,503 | | | | 5,706,871 | |

| | | | | | | | | |

| Health Care — 7.15% | | | | | | | | |

| Illumina, Inc.(a) | | | 14,626 | | | | 2,007,857 | |

| UnitedHealth Group, Inc. | | | 7,199 | | | | 3,629,664 | |

| | | | | | | | 5,637,521 | |

| Technology — 18.56% | | | | | | | | |

| Automatic Data Processing, Inc. | | | 12,331 | | | | 2,966,592 | |

| MarketAxess Holdings, Inc. | | | 13,145 | | | | 2,808,298 | |

| MasterCard, Inc., Class A | | | 11,427 | | | | 4,524,063 | |

| Microsoft Corp. | | | 8,534 | | | | 2,694,611 | |

| Verisk Analytics, Inc. | | | 6,919 | | | | 1,634,545 | |

| | | | | | | | 14,628,109 | |

| Total United States | | | | | | | 43,052,304 | |

| | | | | | | | | |

| Total Common Stocks | | | | | | | | |

| (Cost $72,338,164) | | | | | | | 77,697,920 | |

| | | | | | | | | |

| Money Market Funds - 1.35% | | | | | | | | |

| Morgan Stanley Institutional Liquidity Funds Treasury Portfolio, Institutional Class, 5.20%(b) | | | 1,060,555 | | | | 1,060,555 | |

| Total Money Market Funds | | | | | | | | |

| (Cost $1,060,555) | | | | | | | 1,060,555 | |

| | | | | | | | | |

| Total Investments — 99.91% | | | | | | | | |

| (Cost $73,398,719) | | | | | | | 78,758,475 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 0.09% | | | | | | | 70,158 | |

| Net Assets — 100.00% | | | | | | $ | 78,828,633 | |

| (a) | Non-income producing security. |

| (b) | Rate disclosed is the seven day effective yield as of September 30, 2023. |

See accompanying notes which are an integral part of these financial statements.

| Alta Quality Growth Fund |

| Schedule of Investments |

| September 30, 2023 |

| | | Shares | | | Fair Value | |

| Common Stocks — 98.31% | | | | | | | | |

| Ireland — 7.35% | | | | | | | | |

| Health Care — 3.33% | | | | | | | | |

| ICON PLC(a) | | | 7,800 | | | $ | 1,920,749 | |

| | | | | | | | | |

| Technology — 4.02% | | | | | | | | |

| Accenture PLC, Class A | | | 7,550 | | | | 2,318,680 | |

| Total Ireland | | | | | | | 4,239,429 | |

| | | | | | | | | |

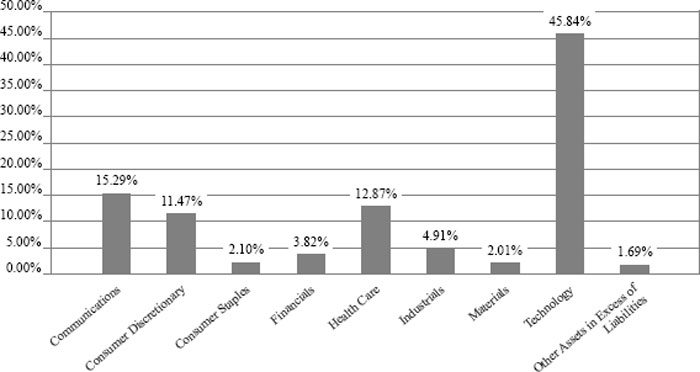

| United States — 90.96% | | | | | | | | |

| Communications — 15.29% | | | | | | | | |

| Alphabet, Inc., Class A(a) | | | 31,950 | | | | 4,180,977 | |

| Booking Holdings, Inc.(a) | | | 650 | | | | 2,004,568 | |

| Take-Two Interactive Software, Inc.(a) | | | 8,500 | | | | 1,193,315 | |

| Walt Disney Co. (The)(a) | | | 18,000 | | | | 1,458,900 | |

| | | | | | | | 8,837,760 | |

| Consumer Discretionary — 11.47% | | | | | | | | |

| Amazon.com, Inc.(a) | | | 4,775 | | | | 606,998 | |

| Home Depot, Inc. (The) | | | 8,200 | | | | 2,477,712 | |

| Restaurant Brands International, Inc. | | | 25,000 | | | | 1,665,500 | |

| TJX Companies, Inc. (The) | | | 21,200 | | | | 1,884,256 | |

| | | | | | | | 6,634,466 | |

| Consumer Staples — 2.10% | | | | | | | | |

| Dollar General Corp. | | | 11,500 | | | | 1,216,700 | |

| | | | | | | | | |

| Financials — 3.82% | | | | | | | | |

| Markel Corp.(a) | | | 1,500 | | | | 2,208,735 | |

| | | | | | | | | |

| Health Care — 9.54% | | | | | | | | |

| Thermo Fisher Scientific, Inc. | | | 3,850 | | | | 1,948,755 | |

| UnitedHealth Group, Inc. | | | 3,650 | | | | 1,840,294 | |

| Zoetis, Inc., Class A | | | 9,950 | | | | 1,731,101 | |

| | | | | | | | 5,520,150 | |

| Industrials — 4.91% | | | | | | | | |

| Amphenol Corp., Class A | | | 21,300 | | | | 1,788,987 | |

| Raytheon Technologies Corp. | | | 14,600 | | | | 1,050,762 | |

| | | | | | | | 2,839,749 | |

| Materials — 2.01% | | | | | | | | |

| Sherwin-Williams Co. (The) | | | 4,550 | | | | 1,160,478 | |

| | | | | | | | | |

| Technology — 41.82% | | | | | | | | |

| Adobe Systems, Inc.(a) | | | 4,700 | | | | 2,396,530 | |

| Apple, Inc. | | | 18,800 | | | | 3,218,748 | |

| Autodesk, Inc.(a) | | | 8,800 | | | | 1,820,808 | |

| Broadridge Financial Solutions, Inc. | | | 9,300 | | | | 1,665,165 | |

| Fiserv, Inc.(a) | | | 17,150 | | | | 1,937,264 | |

| Intuit, Inc. | | | 3,100 | | | | 1,583,914 | |

| MasterCard, Inc., Class A | | | 5,350 | | | | 2,118,118 | |

| Microsoft Corp. | | | 10,450 | | | | 3,299,588 | |

| PayPal Holdings, Inc.(a) | | | 20,500 | | | | 1,198,430 | |

| | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Alta Quality Growth Fund |

| Schedule of Investments (continued) |

| September 30, 2023 |

| | | Shares | | | Fair Value | |

| Common Stocks — 98.31% - (continued) | | | | | | | | |

| United States — 90.96% - (continued) | | | | | | | | |

| Technology — 41.82% - (continued) | | | | | | | | |

| S&P Global, Inc. | | | 3,900 | | | $ | 1,425,099 | |

| Visa, Inc., Class A | | | 7,700 | | | | 1,771,077 | |

| Zebra Technologies Corp., Class A(a) | | | 7,400 | | | | 1,750,322 | |

| | | | | | | | 24,185,063 | |

| Total United States | | | | | | | 52,603,101 | |

| | | | | | | | | |

| Total Common Stocks/Investments — 98.31% | | | | | | | | |

| (Cost $46,116,866) | | | | | | $ | 56,842,530 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 1.69% | | | | | | | 975,814 | |

| Net Assets — 100.00% | | | | | | $ | 57,818,344 | |

| (a) | Non-income producing security. |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Funds |

| Statements of Assets and Liabilities |

| September 30, 2023 |

| | | | | | Guardian | | | | |

| | | Guardian | | | Capital | | | | |

| | | Capital | | | Fundamental | | | | |

| | | Dividend | | | Global Equity | | | Alta Quality | |

| | | Growth Fund | | | Fund | | | Growth Fund | |

| Assets | | | | | | | | | | | | |

| Investments in securities at fair value (cost $15,734,030, $73,398,719 and $46,116,866) | | $ | 20,775,738 | | | $ | 78,758,475 | | | $ | 56,842,530 | |

| Cash and cash equivalents | | | — | | | | — | | | | 860,895 | |

| Receivable for fund shares sold | | | — | | | | — | | | | 761 | |

| Receivable for investments sold | | | — | | | | — | | | | 717,501 | |

| Dividends and interest receivable | | | 23,162 | | | | 59,444 | | | | 28,265 | |

| Tax reclaims receivable | | | 21,584 | | | | 76,671 | | | | — | |

| Receivable from Adviser | | | 206 | | | | — | | | | — | |

| Prepaid expenses | | | 6,646 | | | | 7,286 | | | | 9,383 | |

| Total Assets | | | 20,827,336 | | | | 78,901,876 | | | | 58,459,335 | |

| | | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | |

| Payable for fund shares redeemed | | | — | | | | 99 | | | | — | |

| Payable for investments purchased | | | — | | | | — | | | | 601,185 | |

| Payable for distributions to shareholders | | | 20,207 | | | | 1,842 | | | | — | |

| Payable to Adviser | | | — | | | | 43,649 | | | | 19,551 | |

| Payable to | | | 6,398 | | | | 7,951 | | | | 7,609 | |

| Payable to auditors | | | 4,240 | | | | 4,240 | | | | 4,240 | |

| Payable to trustees | | | 200 | | | | 200 | | | | 200 | |

| Other accrued expenses | | | 6,888 | | | | 15,262 | | | | 8,206 | |

| Total Liabilities | | | 37,933 | | | | 73,243 | | | | 640,991 | |

| Net Assets | | $ | 20,789,403 | | | $ | 78,828,633 | | | $ | 57,818,344 | |

| | | | | | | | | | | | | |

| Net Assets consist of: | | | | | | | | | | | | |

| Paid-in capital | | $ | 16,203,485 | | | $ | 71,650,236 | | | $ | 47,208,654 | |

| Accumulated earnings | | | 4,585,918 | | | | 7,178,397 | | | | 10,609,690 | |

| Net Assets | | $ | 20,789,403 | | | $ | 78,828,633 | | | $ | 57,818,344 | |

| | | | | | | | | | | | | |

| Institutional Shares: | | | | | | | | | | | | |

| Net Assets | | $ | 20,789,403 | | | $ | 78,828,633 | | | $ | 57,818,344 | |

| Shares outstanding (unlimited number of shares authorized, no par value) | | | 1,600,213 | | | | 6,594,595 | | | | 4,051,891 | |

| Net asset value, offering and redemption price per share | | $ | 12.99 | | | $ | 11.95 | | | $ | 14.27 | |

| | | | | | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Funds |

| Statements of Operations |

| For the year ended September 30, 2023 |

| | | | | | Guardian | | | | |

| | | Guardian | | | Capital | | | | |

| | | Capital | | | Fundamental | | | | |

| | | Dividend | | | Global Equity | | | Alta Quality | |

| | | Growth Fund | | | Fund | | | Growth Fund | |

| Investment Income | | | | | | | | | | | | |

| Dividend income (net of foreign taxes withheld of $48,318, $80,607 and $7,531) | | $ | 539,079 | | | $ | 1,116,223 | | | $ | 366,346 | |

| Interest income | | | — | | | | — | | | | 49,220 | |

| Total investment income | | | 539,079 | | | | 1,116,223 | | | | 415,566 | |

| | | | | | | | | | | | | |

| Expenses | | | | | | | | | | | | |

| Adviser | | | 151,989 | | | | 569,694 | | | | 372,912 | |

| Administration | | | 63,268 | | | | 73,472 | | | | 69,161 | |

| Legal | | | 19,106 | | | | 22,106 | | | | 19,106 | |

| Audit and tax preparation | | | 16,881 | | | | 16,881 | | | | 16,881 | |

| Trustee | | | 16,420 | | | | 16,420 | | | | 16,420 | |

| Transfer agent | | | 12,854 | | | | 19,282 | | | | 19,282 | |

| Compliance services | | | 12,167 | | | | 12,167 | | | | 12,167 | |

| Registration | | | 10,055 | | | | 8,904 | | | | 13,368 | |

| Custodian | | | 7,211 | | | | 37,490 | | | | 6,548 | |

| Report printing | | | 4,321 | | | | 4,323 | | | | 3,300 | |

| Pricing | | | 1,165 | | | | 1,712 | | | | 541 | |

| Miscellaneous | | | 21,221 | | | | 25,399 | | | | 27,310 | |

| Total expenses | | | 336,658 | | | | 807,850 | | | | 576,996 | |

| Fees contractually waived by Adviser | | | (144,066 | ) | | | (102,610 | ) | | | (183,313 | ) |

| Net operating expenses | | | 192,592 | | | | 705,240 | | | | 393,683 | |

| Net investment income | | | 346,487 | | | | 410,983 | | | | 21,883 | |

| | | | | | | | | | | | | |

| Net Realized and Change in Unrealized Gain (Loss) on Investments | | | | | | | | | | | | |

| Net realized gain (loss) on investment securities transactions | | | (459,574 | ) | | | 1,867,686 | | | | 73,179 | |

| Net realized gain (loss) on foreign currency transactions | | | 274 | | | | (111,198 | ) | | | — | |

| Net change in unrealized appreciation of investment securities | | | 3,432,613 | | | | 7,531,937 | | | | 8,478,170 | |

| Net change in unrealized appreciation on foreign currency translations | | | 1,118 | | | | 2,381 | | | | — | |

| Net realized and change in unrealized gain on investments | | | 2,974,431 | | | | 9,290,806 | | | | 8,551,349 | |

| Net increase in net assets resulting from operations | | $ | 3,320,918 | | | $ | 9,701,789 | | | $ | 8,573,232 | |

| | | | | | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Funds |

| Statements of Changes in Net Assets |

| | | Guardian Capital Dividend Growth | |

| | | Fund | |

| | | For the | | | For the | |

| | | Year Ended | | | Year Ended | |

| | | September 30, | | | September 30, | |

| | | 2023 | | | 2022 | |

| Increase (Decrease) in Net Assets due to: | | | | | | | | |

| Operations | | | | | | | | |

| Net investment income | | $ | 346,487 | | | $ | 353,810 | |

| Net realized gain (loss) on investment securities transactions | | | (459,300 | ) | | | 476,664 | |

| Net change in unrealized appreciation (depreciation) of investment securities | | | 3,433,731 | | | | (3,030,488 | ) |

| Net increase (decrease) in net assets resulting from operations | | | 3,320,918 | | | | (2,200,014 | ) |

| | | | | | | | | |

| Distributions to Shareholders from: | | | | | | | | |

| Earnings | | | (572,974 | ) | | | (346,059 | ) |

| Total distributions | | | (572,974 | ) | | | (346,059 | ) |

| | | | | | | | | |

| Capital Transactions - Institutional Shares | | | | | | | | |

| Reinvestment of distributions | | | 468,216 | | | | 255,402 | |

| Amount paid for shares redeemed | | | — | | | | (14 | ) |

| Net increase in net assets resulting from capital transactions | | | 468,216 | | | | 255,388 | |

| Total Increase (Decrease) in Net Assets | | | 3,216,160 | | | | (2,290,685 | ) |

| | | | | | | | | |

| Net Assets | | | | | | | | |

| Beginning of year | | | 17,573,243 | | | | 19,863,928 | |

| End of year | | $ | 20,789,403 | | | $ | 17,573,243 | |

| | | | | | | | | |

| Share Transactions - Institutional Shares | | | | | | | | |

| Shares issued in reinvestment of distributions | | | 37,055 | | | | 20,173 | |

| Shares redeemed | | | — | | | | (1 | ) |

| Net increase in shares | | | 37,055 | | | | 20,172 | |

| | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Funds |

| Statements of Changes in Net Assets (continued) |

| | | Guardian Capital Fundamental | |

| | | Global Equity Fund | |

| | | For the | | | For the | |

| | | Year Ended | | | Year Ended | |

| | | September 30, | | | September 30, | |

| | | 2023 | | | 2022 | |

| Increase (Decrease) in Net Assets due to: | | | | | | | | |

| Operations | | | | | | | | |

| Net investment income | | $ | 410,983 | | | $ | 84,610 | |

| Net realized gain on investment securities transactions | | | 1,756,488 | | | | 353,136 | |

| Net change in unrealized appreciation (depreciation) of investment securities | | | 7,534,318 | | | | (7,578,605 | ) |

| Net increase (decrease) in net assets resulting from operations | | | 9,701,789 | | | | (7,140,859 | ) |

| | | | | | | | | |

| Distributions to Shareholders from: | | | | | | | | |

| Earnings | | | (701,199 | ) | | | (929,320 | ) |

| Total distributions | | | (701,199 | ) | | | (929,320 | ) |

| | | | | | | | | |

| Capital Transactions - Institutional Shares | | | | | | | | |

| Proceeds from shares sold | | | 41,348,047 | | | | 6,600,837 | |

| Reinvestment of distributions | | | 671,327 | | | | 889,230 | |

| Amount paid for shares redeemed | | | (438,677 | ) | | | (928,553 | ) |

| Net increase in net assets resulting from capital transactions | | | 41,580,697 | | | | 6,561,514 | |

| Total Increase (Decrease) in Net Assets | | | 50,581,287 | | | | (1,508,665 | ) |

| | | | | | | | | |

| Net Assets | | | | | | | | |

| Beginning of year | | | 28,247,346 | | | | 29,756,011 | |

| End of year | | $ | 78,828,633 | | | $ | 28,247,346 | |

| | | | | | | | | |

| Share Transactions - Institutional Shares | | | | | | | | |

| Shares sold | | | 3,697,496 | | | | 574,288 | |

| Shares issued in reinvestment of distributions | | | 59,281 | | | | 67,321 | |

| Shares redeemed | | | (36,874 | ) | | | (84,142 | ) |

| Net increase in shares | | | 3,719,903 | | | | 557,467 | |

| | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Funds |

| Statements of Changes in Net Assets (continued) |

| | | Alta Quality Growth Fund | |

| | | For the | | | For the | |

| | | Year Ended | | | Year Ended | |

| | | September 30, | | | September 30, | |

| | | 2023 | | | 2022 | |

| Increase (Decrease) in Net Assets due to: | | | | | | | | |

| Operations | | | | | | | | |

| Net investment income (loss) | | $ | 21,883 | | | $ | (117,696 | ) |

| Net realized gain on investment securities transactions | | | 73,179 | | | | 2,545,812 | |

| Net change in unrealized appreciation (depreciation) of investment securities | | | 8,478,170 | | | | (17,301,496 | ) |

| Net increase (decrease) in net assets resulting from operations | | | 8,573,232 | | | | (14,873,380 | ) |

| | | | | | | | | |

| Distributions to Shareholders from: | | | | | | | | |

| Earnings | | | (2,565,420 | ) | | | (1,061,299 | ) |

| Total distributions | | | (2,565,420 | ) | | | (1,061,299 | ) |

| | | | | | | | | |

| Capital Transactions - Institutional Shares | | | | | | | | |

| Proceeds from shares sold | | | 17,106,042 | | | | 7,123,253 | |

| Reinvestment of distributions | | | 2,349,234 | | | | 1,040,688 | |

| Amount paid for shares redeemed | | | (6,772,532 | ) | | | (4,906,688 | ) |

| Net increase in net assets resulting from capital transactions | | | 12,682,744 | | | | 3,257,253 | |

| Total Increase (Decrease) in Net Assets | | | 18,690,556 | | | | (12,677,426 | ) |

| | | | | | | | | |

| Net Assets | | | | | | | | |

| Beginning of year | | | 39,127,788 | | | | 51,805,214 | |

| End of year | | $ | 57,818,344 | | | $ | 39,127,788 | |

| | | | | | | | | |

| Share Transactions - Institutional Shares | | | | | | | | |

| Shares sold | | | 1,237,131 | | | | 465,116 | |

| Shares issued in reinvestment of distributions | | | 189,454 | | | | 57,087 | |

| Shares redeemed | | | (489,025 | ) | | | (343,679 | ) |

| Net increase in shares | | | 937,560 | | | | 178,524 | |

| | | | | | | | | |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Dividend Growth Fund – Institutional Class |

| Financial Highlights |

(For a share outstanding during each period)

| | | | | | For the Five | | | | | | | |

| | | | | | Months | | | | | | For the | |

| | | For the Years Ended | | | Ended | | | For the Year | | | Period | |

| | | September 30, | | | September | | | Ended April | | | Ended April | |

| | | 2023 | | | 2022 | | | 30, 2021 (a) | | | 30, 2021 | | | 30, 2020(b) | |

| Net asset value, beginning of period | | $ | 11.24 | | | $ | 12.87 | | | $ | 12.68 | | | $ | 9.85 | | | $ | 10.00 | |

| Investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.22 | | | | 0.22 | | | | 0.11 | | | | 0.16 | | | | 0.17 | |

| Net realized and unrealized gain (loss) on investments | | | 1.89 | | | | (1.63 | ) | | | 0.20 | | | | 2.82 | | | | (0.16 | ) |

| Total from investment operations | | | 2.11 | | | | (1.41 | ) | | | 0.31 | | | | 2.98 | | | | 0.01 | |

| Distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (0.22 | ) | | | (0.22 | ) | | | (0.12 | ) | | | (0.15 | ) | | | (0.16 | ) |

| Net realized gains | | | (0.14 | ) | | | — | | | | — | | | | — | | | | — | |

| Total from distributions | | | (0.36 | ) | | | (0.22 | ) | | | (0.12 | ) | | | (0.15 | ) | | | (0.16 | ) |

| Net asset value, end of period | | $ | 12.99 | | | $ | 11.24 | | | $ | 12.87 | | | $ | 12.68 | | | $ | 9.85 | |

| Total Return(c) | | | 18.91 | % | | | (11.11 | )% | | | 2.42 | % (d) | | | 30.41 | % | | | 0.10 | % (d) |

| Ratios/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000 omitted) | | $ | 20,789 | | | $ | 17,573 | | | $ | 19,864 | | | $ | 19,449 | | | $ | 14,953 | |

| Before waiver or recoupment: | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets | | | 1.66 | % | | | 1.67 | % | | | 1.78 | % (e) | | | 1.73 | % | | | 1.94 | % (e) |

| After waiver or recoupment: | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets | | | 0.95 | % | | | 0.95 | % | | | 0.95 | % (e) | | | 0.95 | % | | | 0.95 | % (e) |

| Ratio of net investment income to average net assets | | | 1.71 | % | | | 1.71 | % | | | 1.94 | % (e) | | | 1.40 | % | | | 1.64 | % (e) |

| Portfolio turnover rate | | | 7 | % | | | 25 | % | | | 6 | % (d) | | | 47 | % | | | 29 | % (d) |

| (a) | The Fund changed its fiscal year end to September 30. |

| (b) | For the period May 1, 2019 (commencement of operations) to April 30, 2020. |

| (c) | Total return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Fundamental Global Equity Fund - Institutional Shares |

| Financial Highlights |

(For a share outstanding during each period)

| | | | | | For the | |

| | | | | | | | | | | | Period | |

| | | | | | | | | | | | Ended | |

| | | For the Years Ended September 30, | | | September | |

| | | 2023 | | | 2022 | | | 2021 | | | 30, 2020(a) | |

| Net asset value, beginning of period | | $ | 9.83 | | | $ | 12.84 | | | $ | 10.62 | | | $ | 10.00 | |

| Investment operations: | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.07 | | | | 0.03 | | | | 0.03 | | | | 0.02 | |

| Net realized and unrealized gain (loss) on investments | | | 2.16 | | | | (2.65 | ) | | | 2.22 | | | | 0.62 | |

| Total from investment operations | | | 2.23 | | | | (2.62 | ) | | | 2.25 | | | | 0.64 | |

| Distributions from: | | | | | | | | | | | | | | | | |

| Net investment income | | | (0.05 | ) | | | (0.02 | ) | | | (0.03 | ) | | | (0.02 | ) |

| Net realized gains | | | (0.06 | ) | | | (0.37 | ) | | | — | | | | — | |

| Total from distributions | | | (0.11 | ) | | | (0.39 | ) | | | (0.03 | ) | | | (0.02 | ) |

| Net asset value, end of period | | $ | 11.95 | | | $ | 9.83 | | | $ | 12.84 | | | $ | 10.62 | |

| Total Return(b) | | | 22.73 | % | | | (21.15 | )% | | | 21.19 | % | | | 6.39 | % (c) |

| Ratios/Supplemental Data: | | | | | | | | | | | | | | | | |

| Net assets, end of period (000 omitted) | | $ | 78,829 | | | $ | 28,247 | | | $ | 29,756 | | | $ | 22,862 | |

| Before waiver or recoupment: | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets | | | 1.13 | % | | | 1.51 | % | | | 1.53 | % | | | 1.82 | % (d) |

| After waiver or recoupment: | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets | | | 0.99 | % | | | 0.99 | % | | | 0.99 | % | | | 0.99 | % (d) |

| Ratio of net investment income to average net assets | | | 0.58 | % | | | 0.28 | % | | | 0.22 | % | | | 0.26 | % (d) |

| Portfolio turnover rate | | | 4 | % | | | 4 | % | | | 14 | % | | | 10 | % (c) |

| (a) | For the period December 19, 2019 (commencement of operations) to September 30, 2020. |

| (b) | Total return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

See accompanying notes which are an integral part of these financial statements.

| Alta Quality Growth Fund - Institutional Shares |

| Financial Highlights |

(For a share outstanding during each period)

| | | | | | | | | For the | |

| | | | | | | | | | | | | | | Period | |

| | | | | | | | | | | | | | | Ended | |

| | | For the Years Ended September 30, | | | September | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 30, 2019(a) | |

| Net asset value, beginning of period | | $ | 12.56 | | | $ | 17.65 | | | $ | 13.80 | | | $ | 12.57 | | | $ | 10.00 | |

| Investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | | 0.01 | | | | (0.04 | ) | | | (0.05 | ) | | | 0.02 | | | | 0.04 | |

| Net realized and unrealized gain (loss) on investments | | | 2.51 | | | | (4.70 | ) | | | 3.91 | | | | 1.59 | | | | 2.53 | |

| Total from investment operations | | | 2.52 | | | | (4.74 | ) | | | 3.86 | | | | 1.61 | | | | 2.57 | |

| Distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | — | | | | — | | | | (0.01 | ) | | | (0.05 | ) | | | — | |

| Net realized gains | | | (0.81 | ) | | | (0.35 | ) | | | — | | | | (0.33 | ) | | | — | |

| Total from distributions | | | (0.81 | ) | | | (0.35 | ) | | | (0.01 | ) | | | (0.38 | ) | | | — | |

| Net asset value, end of period | | $ | 14.27 | | | $ | 12.56 | | | $ | 17.65 | | | $ | 13.80 | | | $ | 12.57 | |

| Total Return(b) | | | 21.04 | % | | | (27.45 | )% | | | 27.96 | % | | | 12.92 | % | | | 25.70 | % (c) |

| Ratios/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000 omitted) | | $ | 57,818 | | | $ | 39,128 | | | $ | 51,805 | | | $ | 38,490 | | | $ | 27,446 | |

| Before waiver or recoupment: | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets | | | 1.16 | % | | | 1.18 | % | | | 1.18 | % | | | 1.30 | % | | | 1.54 | % (d) |

| After waiver or recoupment: | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets | | | 0.79 | % | | | 0.79 | % | | | 0.79 | % | | | 0.79 | % | | | 0.79 | % (d) |

| Ratio of net investment income (loss) to average net assets | | | 0.04 | % | | | (0.24 | )% | | | (0.32 | )% | | | 0.14 | % | | | 0.45 | % (d) |

| Portfolio turnover rate | | | 22 | % | | | 19 | % | | | 16 | % | | | 26 | % | | | 16 | % (c) |

| (a) | For the period December 19, 2018 (commencement of operations) to September 30, 2019. |

| (b) | Total return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

See accompanying notes which are an integral part of these financial statements.

| Guardian Capital Funds |

| Notes to the Financial Statements |

| September 30, 2023 |

NOTE 1. ORGANIZATION

The Guardian Capital Dividend Growth Fund (“Guardian Dividend Fund”), Guardian Capital Fundamental Global Equity Fund (“Guardian Equity Fund”) and Alta Quality Growth Fund (“Alta Growth Fund”) (each a “Fund” and, collectively the “Funds”) were organized as diversified (Guardian Dividend Fund and Alta Growth Fund) and non-diversified (Guardian Equity Fund) series of the Capitol Series Trust (the “Trust”). The Funds are registered under the Investment Company Act of 1940, as amended (“1940 Act”). The Trust is an open-end investment company established under the laws of Ohio by an Agreement and Declaration of Trust dated September 18, 2013 as amended and restated November 18, 2021 (the “Trust Agreement”). The Trust Agreement permits the Board of Trustees of the Trust (the “Board”) to issue an unlimited number of shares of beneficial interest of separate series without par value. The Guardian Dividend Fund’s and Guardian Equity Fund’s investment adviser is Guardian Capital LP and the Alta Growth Fund’s investment adviser is Alta Capital Management, LLC (each an “Adviser”). Alta Capital Management, LLC is a majority-owned U.S. domiciled subsidiary of Guardian Capital LP. The Guardian Equity Fund’s sub-adviser is GuardCap Asset Management Limited, a non-U.S. wholly-owned subsidiary of Guardian Capital LP domiciled in the United Kingdom. The investment objective of the Guardian Dividend Fund is to provide long-term capital appreciation and current income. The investment objective of the Guardian Equity Fund is to provide long-term capital appreciation. The investment objective of the Alta Growth Fund is to seek long-term growth of capital with lower than market volatility.

Each Fund currently offers one class of shares, Institutional Shares. Each share represents an equal proportionate interest in the assets and liabilities belonging to the Funds and is entitled to such dividends and distributions out of income belonging to the Funds as are declared by the Board.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

The Funds are investment companies and follow accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”, including Accounting Standards Update 2013-08. The following is a summary of significant accounting policies followed by the Funds in the preparation of their financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Regulatory update – Tailored Shareholder Reports for Mutual Funds and Exchange-Traded Funds (“ETFs”) – Effective January 24, 2023, the SEC adopted rule and form amendments to require mutual funds and ETFs to transmit concise and visually engaging streamlined annual and semiannual reports to shareholders that highlight key information.

| Guardian Capital Funds |

| Notes to the Financial Statements (continued) |

| September 30, 2023 |

Other information, including financial statements, will no longer appear in a streamlined shareholder report but must be available online, delivered free of charge upon request, and filed on a semiannual basis on Form N-CSR. The rule and form amendments have a compliance date of July 24, 2024. At this time, management is evaluating the impact of these amendments on the shareholder reports for the Funds.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Foreign Currency Translation – The accounting records of the Funds are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars at the current rate of exchange each business day to determine the value of investments, and other assets and liabilities. Purchases and sales of foreign securities, and income and expenses, are translated at the prevailing rate of exchange on the respective date of these transactions. The Funds do not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from fluctuation arising from changes in market prices of securities held. These fluctuations are included with the unrealized gain or loss from investments.