INVESTMENT MANAGERS SERIES TRUST II

235 W. Galena Street

Milwaukee, Wisconsin 53212

VIA EDGAR

December 2, 2021

U.S. Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549

Attention: Division of Investment Management

| Re: | Investment Managers Series Trust II (the “Trust” or “Registrant”) (File Nos. 333-191476 and 811-22894) on behalf of the Ambassador Fund (the “Fund”) |

Ladies and Gentlemen:

This letter summarizes the comments provided to me by Ms. Deborah O’Neal of the staff of the Securities and Exchange Commission (the “Commission”) by telephone on October 8, 2021, regarding Post-Effective Amendment No. 253 to the Registrant’s Form N-1A registration statement filed on August 23, 2021, with respect to The Ambassador Fund (formerly, Ambassador Fund), a series of the Registrant. Responses to all of the comments are included below and, as appropriate, will be reflected in a Post-Effective Amendment to the Fund’s Form N-1A registration statement (the “Amendment”), which will be filed separately.

GENERAL

| 1. | Please file a delaying amendment to with respect to PEA No. 253 to allow the staff sufficient time to review the Registrant’s proposed responses to the comments received on October 8, 2021. | |

| Response: Post-Effective Amendment No. 253 was expected to be effective on November 8, 2021. As requested by the staff, numerous delaying amendments have been filed with the effectiveness of the Fund’s Registration Statement currently scheduled for December 6, 2021. |

PROSPECTUS

SUMMARY SECTION

Fees and Expenses

| 2. | Please provide the Fund’s completed Fee Table and Example to the Commission for review at least five business days prior to filing the Amendment. |

Response: The Fund’s completed Fee Table and Example are as follows:

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees to financial intermediaries which are not reflected in the table and example below.

| Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) | |||

| Management fees | 1.20% | ||

| Other expenses1 | 0.20% | ||

| Total annual fund operating expenses | 1.40% | ||

| 1 | “Other expenses” have been estimated for the current fiscal year. Actual expenses may differ from estimates. |

Example

This example is intended to help you compare the costs of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. The example reflects the Fund’s contractual fee waiver and/or expense reimbursement only for the term of the contractual fee waiver and/or expense reimbursement.

Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| One Year | Three Years |

| $143 | $443 |

| 3. | In footnote 2 to the Fees and Expenses Table, please confirm that the contractual fee waiver and/or expense reimbursement for the Fund is effective for at least one year from the effective date of the Fund’s Registration Statement. |

Response: The Registrant confirms that the contractual fee waiver and/or expense reimbursement for the Fund will be effective for at least one year from the effective date of the Fund’s Registration Statement. It is anticipated that the Fund’s total annual fund operating expenses for the current fiscal year will be below the expense cap; therefore, the fee table will not reflect this information. However, the disclosure below is included in the back section of the prospectus pursuant to Item 10 of Form N-1A.

The Advisor has contractually agreed to waive its fees and/or pay for operating expenses of the Fund to ensure that total annual fund operating expenses (excluding any taxes, interest on borrowings, expenses incurred with respect to the acquisition and disposition of portfolio securities and the execution of portfolio transactions, including brokerage commissions, dividend and interest expenses on short sales, acquired fund fees and expenses (as determined in accordance with SEC Form N-1A), other expenditures which are capitalized in accordance with generally accepted accounting principles, expenses incurred in connection with any merger or reorganization, or extraordinary expenses such as litigation expenses) do not exceed 1.40% of the average daily net assets of the Fund. This agreement is in effect until February 28, 2023, and it may be terminated before that date only by the Trust’s Board of Trustees.

2

Any reduction in advisory fees or payment of the Fund’s expenses made by the Advisor in a fiscal year may be reimbursed by the Fund for a period ending three full fiscal years after the date of reduction or payment if the Advisor so requests. This reimbursement may be requested from the Fund if the reimbursement will not cause the Fund’s annual expense ratio to exceed the lesser of (a) the expense limitation in effect at the time such fees were waived or payments made, or (b) the expense limitation in effect at the time of the reimbursement. However, the reimbursement amount may not exceed the total amount of fees waived and/or Fund expenses paid by the Advisor and will not include any amounts previously reimbursed to the Advisor by the Fund. Any such reimbursement is contingent upon the Board’s subsequent review of the reimbursed amounts. The Fund must pay current ordinary operating expenses before the Advisor is entitled to any reimbursement of fees and/or Fund expenses.

Principal Investment Strategies

| 4. | The Fund’s principal investment strategies indicate the Fund will invest significantly in catastrophe (“Cat”) bonds. Given the liquidity profile of these investments, please explain in your written response how the Fund determined that its investment strategy is appropriate for the open-end fund structure. Your response should address the following: |

| (a) | Information concerning the relevant factors referenced in the release adopting rule 22e-4 under the Investment Company Act of 1940, as amended (the “1940 Act”). Rule 22e-4 requires each fund to assess, manage, and periodically review (no less frequently than annually) its liquidity risk concerning the following factors as applicable: (a) investment strategy and liquidity of portfolio investments during both normal and reasonably foreseeable stressed conditions (including whether the investment strategy is appropriate for an open-end fund, the extent to which the strategy involves a relatively concentrated portfolio or large positions in particular issuers, and the use of borrowings for investment purposes and derivatives); (b) short-term and long-term cash flow projections during both normal and reasonably foreseeable stressed conditions; and (c) holdings of cash and cash equivalents, as well as borrowing arrangements and other funding sources; |

| (b) | Include general market data on liquidity for each specific type of investments that the Fund will invest in as part of its principal strategy to provide exposure to catastrophes, including Cat bonds, quota shares, excess of loss notes, and industry loss warranties (“ILWs”), including if and how the liquidity of these instruments changes around triggering events, with recent examples; |

| (c) | Include a discussion of the Advisor’s and Sub-Advisor’s past experience of investing in these instruments and how that experience informs them of the liquidity of each of these instruments; |

| (d) | How the fact that generally only qualified institutional buyers (“QIBs”) can purchase the Cat bonds and other investments that the Fund targets impacts the advisor’s assessment of liquidity; and |

| (e) | How the Fund’s intended exposures across events and geographies impact liquidity. |

Response: The Fund invests primarily in liquid securities. More specifically, a very high percentage of the Fund’s investments are expected to be classified as highly liquid investments under Rule 22e-4 (the “Liquidity Rule”) under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund has engaged ICE Data Services (“ICE”) to provide the liquidity classifications for its holdings. Based on a sample portfolio, ICE determined that more than 90% of the holdings would be classified as highly liquid. As a result, the Fund does not anticipate any difficulty in complying with the liquidity requirements applicable to an open-end fund. In accordance with the Trust’s liquidity risk management program, the Fund has adopted a liquidity risk management program (the “Fund Program”). The Fund Program sets forth the obligations of the Fund and the administrator of the Fund Program (the “Program Administrator”) with respect to managing and overseeing the Fund’s liquidity risk management requirements as well as the specific reporting obligations set forth in the Liquidity Rule.

3

More detailed information with respect to each of the above listed items is provided below.

(a) In determining the investment strategy, the Fund’s advisor, Embassy Asset Management LP (“Embassy”) considered that many open-end funds invest a portion of their portfolio in Cat bonds. Further, a few open-end funds invest primarily in insurance-linked securities including Cat bonds. The Fund intends to hold approximately 100 positions that will be diversified among countries, perils, issuers and triggers. The Fund will provide investors with the opportunity to earn an attractive return that is uncorrelated with the returns of other financial market instruments in exchange for assuming catastrophe insurance risks. The Advisor and Sub-Advisor assess the liquidity of the portfolio during both normal and reasonably stressed conditions. In determining the Fund’s holdings, the sub-advisor employs catastrophe risk models to calculate a variety of probable loss scenarios and evaluate the merits of each potential investment and its liquidity.

As the Fund is new, it does not have historical purchase and redemption activity to examine short-term and long-term cash flow projections during both normal and reasonably foreseeable stressed conditions. The Advisor and Sub-Advisor have reviewed the purchase and redemption activity of other funds with similar investment strategies to analyze how shareholder activity may be impacted by triggering events. The Fund does not anticipate holding a large percentage of cash and cash equivalents. However, Embassy expects to establish a credit facility on behalf of the Fund to process timely redemptions if needed.

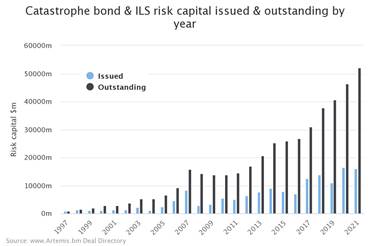

(b) With respect to the fund’s specific investments, the Fund primarily invest in Cat bonds. The market for Cat bonds has matured significantly in the past 15 years. In 2021, $15.9 billion Cat bonds have been issued year-to-date. The notional amount of outstanding CAT bonds is approximately $52 billion.

4

Cat bonds are typically purchased on an initial offering basis and held to maturity. However, there is a robust secondary market maintained by leading institutional brokers. A number of brokers, including but not limited to Swiss Re, Aon Benfield, GC Securities, RBC, Beech Hill Securities, Tiger Risk Capital Markets, Willis Capital Markets, and Tullett Prebon, facilitate secondary market trading of CAT bonds. These firms provide both indicative and firm bid/ask prices and match buyers and sellers of CAT bonds. The typical purchasers of CAT bonds on the secondary market are other investors like dedicated insurance-linked security (“ILS”) funds, institutional investors, and open and closed end registered investment companies.

Cat bonds became significant in the early 1990s in the wake of various natural disasters, including the Northridge, California earthquake and southern Florida’s Hurricane Andrew. Such disasters stressed insurance and reinsurance companies and they sought alternative sources of risk capacity. The capital markets provided a sufficiently large base to assume and spread the risk of these catastrophes and increased the number of Cat bonds available in response to the need for alternative sources of risk management.

A Cat bond is a form of ILS that is sold in the capital markets. To issue a Cat bond, the sponsor, typically a reinsurance company, creates a special purpose vehicle (“SPV”) that issues individual notes to capital markets investors. Unlike a corporate bond, the money contributed by investors is held by the SPV in low-risk securities, such as U.S. treasuries, and not on the sponsor's balance sheet. The coupon that is paid to investors is made up of the return on these low-risk investments and the premiums paid to the SPV by the sponsor.

Cat bonds typically mature in three years, although terms generally range from one to five years, depending on the bond, and issue quarterly interest payments (coupons). Cat bonds derive their value from the frequency of natural phenomena; thus, their performance is relatively uncorrelated with fluctuations in the financial markets, making them attractive fixed income investments for investors looking to diversify their portfolios and hedge against other market volatility.

Cat bonds are structured based on the likelihood of "super" catastrophes. Damage from hurricanes and earthquakes are the most common types of losses against which sponsors protect themselves, but bonds protecting against damage from other events such as tornadoes and large hailstorms are also created. In the event that the specific natural catastrophe mentioned in the bond causes a specified amount of damage, the bond is "triggered" and all or a portion of the original principal can be used to pay those obligations. The average expected loss for Cat bonds issued in 2020 was 2.5%. Below is the current list of potential Cat bond losses for 2021.

5

| Cat bond | Sponsor | Orig. size | Cause of loss | Loss amount | ~Time to payment | Date of loss |

| Pelican IV Re Ltd. (Series 2021-1) - Class A | Louisiana Citizens Property Insurance Corporation | $75m | Hurricane Ida | Mark to market implied ~80% loss of principal | Ongoing | 2021 |

| Catahoula Re Pte. Ltd. (Series 2020-1) | Louisiana Citizens Property Insurance Corporation | $60m | Hurricane Ida | Mark to market implied ~90% loss of principal | Ongoing | 2021 |

| Sanders Re II Ltd. (Series 2019-1) | Allstate | $300m | Aggregate losses, largely from winter storm Uri and related Texas freeze | $253m of principal eroded in H1 2021 | Ongoing | 2021 |

| Caelus Re VI Ltd. (Series 2020-2) Class A-2 | Nationwide Mutual Insurance Co. | $75m | Hurricanes, severe weather and winter storms 2020/21 risk period | Mark to market implied ~$22m (priced for ~30% loss) | Ongoing | 2020/21 |

| Caelus Re VI Ltd. (Series 2020-2) Class B-2 | Nationwide Mutual Insurance Co. | $75m | Hurricanes, severe weather and winter storms 2020/21 risk period | Mark to market implied ~$56m (priced for ~75% loss) | Ongoing | 2020/21 |

| Caelus Re VI Ltd. (Series 2020-2) Class C-2 | Nationwide Mutual Insurance Co. | $40m | Hurricanes, severe weather and winter storms 2020/21 risk period | Mark to market implied ~$36m (priced for ~90% loss) | Ongoing | 2020/21 |

| Caelus Re V Ltd. (Series 2018-1) Class B | Nationwide Mutual Insurance Co. | $75m | Hurricanes, severe weather and winter storms 2020/21 risk period | Mark to market implied ~$30m (priced for ~40% loss) | Ongoing | 2020/21 |

| Caelus Re V Ltd. (Series 2018-1) Class C | Nationwide Mutual Insurance Co. | $175m | Hurricanes, severe weather and winter storms 2020/21 risk period | Mark to market implied ~$123m (priced for ~70% loss) | Ongoing | 2020/21 |

| Caelus Re V Ltd. (Series 2018-1) Class D | Nationwide Mutual Insurance Co. | $75m | Hurricanes, severe weather and winter storms 2020/21 risk period | Mark to market implied ~$75m (priced for ~100% loss) | Ongoing | 2020/21 |

Source: www.artemis.bm

To further illustrate the liquidity of the Cat bond market, Exhibit A provides detailed information on the growth, size and sponsors of cat bonds over the years.

The Fund may also invest in Quota Shares, Excess of Loss Notes and ILWs. Quota Shares, Excess of Loss Notes, and ILWs are generally considered illiquid securities by the Fund, and the Fund will not invest more than 15% of its net assets in illiquid securities.

6

(c) Advisor – Embassy

Embassy, the Fund’s investment advisor, is a new asset manager. The principals of the firm have decades of experience at other fund management companies and are familiar with closed-end and open-end registered funds, exchange-traded funds (“ETFs”), collective investment trusts, limited partnership structures, separate accounts, hedge funds and offshore investment vehicles. Below is information on the principals and their related experience.

| Name, Title | Summary of business experience over past 5 years |

Adam Gurwitz, CFA Managing Member | Venture capital and angel investor, former chief operating officer of True Arrow Capital Management, an SEC-registered investment advisor. Hedge fund sales, focused on institutional investors.

|

John Kidd, CFA Managing Member | Senior vice president of client strategies at Stone Ridge Asset Management. Mutual fund sales, focused on the RIA marketplace.

|

Steve Connors, CPA Chief Financial Officer | Head of traditional fund accounting at SEI. Treasurer, controller, and CFO of The Advisors’ Inner Circle Funds. Overall responsibility for all accounting and financial reporting related to all funds and trusts utilizing SEI’s master series trust platform.

|

Sub-advisor – Tangency Capital Investment Advisory Ltd. (TCIA)

Tangency Capital Limited (“TCL”), the parent company of TCIA, has been established since 2017 and launched its first fund, the Select Market Access Fund, in June 2018. TCL has $403 million of assets under management as of September 30, 2021. TCL’s existing investor base is institutional, comprised of pension funds, endowments, and family offices. The partners and employees of TCL, including the senior portfolio manager, have several decades of experience in pricing and structuring insurance/reinsurance-linked securities, fund operations, and portfolio and risk management, and have deep experience with respect to the liquidity of ILS. TCIA is a new investment advisor and is wholly owned by TCL.

TCL has deep experience with reinsurance and insurance-linked securities and its partners and employees have experience with underwriting Cat bonds and other ILS for decades. Specifically, below is information for the Partners and Senior Portfolio Manager:

Partners

| - | Dominik Hagedorn served as Vice President at Deutsche Bank Securities Inc. with global coverage responsibilities in the insurance and reinsurance sector; |

| - | Michael Jedraszak served as Chief Investment Officer and was responsible for Hiscox Ltd.’s overall ILS strategy including product innovation, portfolio construction and investor relations; and |

| - | Kai Morgenstern was Managing Director of Renaissance Re Ltd., where he managed a cat bond fund and other third-party capital structures managed by the Ventures group of Renaissance Re. |

7

Senior Portfolio Manager

Niall MacGillivray is the main day-to-day portfolio manager. For the past five years, Mr. MacGillivray was the head of the Cat bond portfolio at Nephila Capital, which TCL believes is the world’s largest ILS manager. He had additional responsibilities in risk pricing, structuring and investor relations. Mr. MacGillivray is a Fellow of the Society of Actuaries specializing in Quantitative Finance and has been in the world of reinsurance and ILS for his entire career. Before Nephila Capital, Mr. MacGillivray began his career as a trader at Deutsche Bank Securities in structured finance.

| (d) | Although Cat bonds can only be sold to QIBs, the impact of this restriction on liquidity is minimal. The CAT bond market has a growing core of experienced investors including money managers, hedge funds, dedicated CAT funds, banks, reinsurers, life insurers, non-life insurers, and some money funds. On average, according to data from the Trade Reporting and Compliance Engine (TRACE) and Tullett Prebon, approximately $4 billion of Cat bonds are traded each year, translating to an average of $15 million per day, with lot sizes of $250,000 to $10 million. Larger sales can also occur through organized Bid Wanted in Competition auctions (BWICs). Liquidity has tended to improve as the total market and the average deal size has increased. |

| (e) | Embassy and TCIA will seek to manage the Fund to achieve the best risk adjusted return while evaluating the Fund’s exposure to any single catastrophic event. TCIA will construct a portfolio that will include exposures to a highly varied group of available perils, geographic regions and structures and issuers. Further, within each region and peril, Embassy and TCIA seek to hold a balance of exposures to underlying insurance carriers, trigger types, and lines of business. Once fully invested, Embassy and TCIA expect that the Fund will have exposure to a significant percentage of the recently issued outstanding Cat bonds. Embassy and TCIA believe the Fund’s portfolio’s investment across multiple perils and geographic regions will help minimize the risk of loss and that the Fund’s portfolio holdings will be highly liquid. |

| 5. | Please explain how each investment (i.e., Cat bonds, quota shares, excess of loss notes and ILWs) will be classified under the Fund’s liquidity risk management program. |

Response: As noted in the response to comment four above, the Fund has engaged ICE to provide liquidity classification for its holdings. Based on preliminary testing, Cat bonds are primarily classified as highly liquid investments. Other insurance linked securities, such as quota shares, excess of loss notes and industry loss warranties are expected to be less liquid investments and/or illiquid investments. The Fund will not exceed the 15% limitation with respect to illiquid investments.

| 6. | In your written response, please explain whether the Fund invests in special purchase vehicles (“SPVs”) that rely on section 3(c)(1) or 3(c)(7) of the 1940 Act. If the Fund invests in SPVs that do not rely on these exclusions, please explain why these SPVs are not required to register. |

Response: The Fund will invest in Cat bonds and other ILS that are issued in Rule 144A, and to a lesser extent 4(a)2 and Reg D, offerings. Rule 144A offerings are available only to institutional investors and are not subject to the SEC's registration and disclosure requirements. As a result, many of the normal investor protections that are common to most traditional registered investments are missing. For example, issuers of Cat bonds are not required to file a registration statement or periodic reports with the SEC, unlike issuers of registered bonds. While general prohibitions against securities fraud apply to Rule 144A offerings, the lack of public disclosure may make it difficult for both individuals and fund managers to obtain and evaluate the information used to price and structure Cat bonds.

8

| 7. | In your written response, please explain whether there are any custody issues with these derivatives. |

Response: The Fund’s investments are cleared through DTC or Euroclear and the Registrant does not anticipate any custody issues.

| 8. | The third sentence of the second paragraph under “Principal Investment Strategies” states “[s]ince insurance-linked securities are typically unrated, a substantial portion of the Fund’s assets may be invested in unrated securities that are high risk or speculative.” Please use bold or italicized font to highlight this sentence for investors. |

Response: The Registrant has bolded the sentence as requested.

| 9. | Please explain the process for valuing Cat bonds and other insurance related investments and how that valuation will be consistent with rule 2a-5 under the 1940 Act. In addition, please provide the Fund’s percentages that will be classified as level 1, 2 or 3. |

Response: There is an active secondary market in Cat bonds, with trading over-the-counter through half a dozen significant broker-dealers. On average, according to data from the Trade Reporting and Compliance Engine (TRACE) and Tullett Prebon, approximately $4 billion of securities are traded each year, translating to an average of $15 million per day, with lot sizes of $250,000 to $10 million. Larger sales can also occur through organized Bid Wanted in Competition auctions (BWICs). Liquidity has tended to improve as the total market and the average deal size has increased.

There are several pricing services that value Cat bonds. ICE provides daily Cat bond pricing, and the Fund intends to use ICE as its pricing agent (and liquidity classification vendor). Cat bond brokers usually present their bid/ask prices on at least a weekly basis. IDC takes quotes and through matrix pricing and other available sources, issues daily prices. Spreads on Cat bonds generally range approximately 1.2%, and in Embassy’s and TCIA’s experience, most Cat bond trades take place within the spread, and near the valuations set by IDC.

Other than supply and demand, Cat bond prices only change when there is new information that is relevant to the underlying natural catastrophe risk of the Cat bond. For example, in the weeks leading up to and following superstorm Sandy, non-hurricane Cat bonds (i.e., bonds with no exposure to hurricanes) did not experience any material price movement, because Sandy did not impact their underlying risks. In addition, about 40% of the hurricane Cat bonds had no exposure to the Northeast, and thus, these Cat bonds also did not experience price movement. The prices of the Cat bonds that did have Northeast U.S. hurricane exposure moved roughly according to the level of vulnerability to Sandy. For example, the Cat bonds that were most exposed to losses due to a hurricane in the Northeast experienced the most significant price drops, while CAT bonds that were only marginally exposed to Northeast hurricane losses experienced very small price movements.

Additionally, Cat bond prices are not correlated with those of the broader fixed income or equity markets. The performance of Cat bonds is determined by the incidence and severity of natural catastrophes, whereas fixed income and equity security performance is more tightly linked to global macro, political or financial market events.

The Fund expects most of its investments will be Level 2 securities, with some Level 1 or Level 3 holdings. Looking at other registered funds that invest in similar securities shows that Cat bonds’ values are generally derived from observable inputs and classified as Level 2 in accordance with ASC 820. Furthermore, the Fund’s administrator has submitted a sample of Cat bonds to an independent third-party pricing provider which provided evaluated bids for these securities and supports classification as Level 2.

9

| 10. | The fourth sentence of the fourth paragraph under “Principal Investment Strategies” states “[i]n addition, the Fund invests in Cat Bonds and other insurance-linked securities across a varied group of available perils and geographic regions.” Please provide some examples of the varied group of perils and geographic regions. |

Response: The disclosure has been revised as follows:

The Fund invests in Cat Bonds and other insurance-linked securities across a varied group of available perils and geographic regions (for example Florida hurricanes, California earthquakes, Japan typhoons, Europe windstorms, and Europe earthquakes).

| 11. | The last sentence of the fourth paragraph under “Principal Investment Strategies” states “[m]ost of the securities in which the Fund invests have high quality collateral that includes U.S. government securities (e.g., U.S. Treasury bills, U.S. Treasury money market fund shares, or equivalents).” Consider whether investors may be misled or confused by this sentence given that if an event is triggered, the sponsor will receive the collateral, and not the Fund. |

Response: The disclosure has been revised as follows:

Insurance-linked securities are typically structured using an SPV the proceeds of which are held in a dedicated, escrowed collateral account and are invested in The SPVMost of the securities in which the Fund invests have high quality collateral that includes U.S. government securities (e.g., U.S. Treasury bills, U.S. Treasury money market fund shares, or equivalents). If a trigger event occurs, the SPV will liquidate collateral to make the agreed-upon payment and reimburse the counterparty. If no trigger event occurs then the collateral is liquidated at the end of the term and investors are repaid.

Principal Risk of Investing

| 12. | In “Insurance-Linked Securities Risk” it discusses certain triggering events including natural and non-natural events. Please provide some examples of non-natural events. |

Response: The Registrant has revised the disclosure as follows:

The principal risk of an investment in an insurance-linked security is that a triggering event(s) (e.g., (i) natural events, such as hurricanes, earthquakes, tornados, pandemics, fires and flood; or (ii) certain non-natural events resulting from human activity such as commercial and industrial accidents or business interruptions), will occur and the Fund will lose all or a significant portion of the principal it has invested in the security and the right to additional interest payments with respect to the security. For example, major natural disasters (such as in the cases of super typhoon Goni in the Philippines in 2020, monsoon flooding in China in 2020, hurricane Irma in Florida and the Caribbean in 2017, and super storm Sandy in 2012) or commercial and industrial accidents (such as aviation disasters and oil spills) can result in significant losses and investors in insurance-linked securities tied to such exposures may also experience substantial losses. If the likelihood and severity of natural and other large disasters increase, the risk of significant losses to reinsurers may increase. Typically, one significant triggering event (even in a major metropolitan area) will not result in financial failure to a reinsurer. However, a series of major triggering events could cause the failure of a reinsurer. Similarly, to the extent the Fund invests in insurance-linked securities for which a triggering event occurs, losses associated with such event will result in losses to the Fund and a series of major triggering events affecting a large portion of the insurance-linked securities held by the Fund will result in substantial losses to the Fund. If multiple triggering events occur that impact a significant portion of the Fund’s portfolio, the Fund could suffer substantial losses and an investor may lose money. A majority of the Fund’s assets will typically be invested in insurance-linked securities tied to natural events and/or non-natural disasters and there is inherent uncertainty as to whether, when or where such events will occur. There is no way to accurately predict whether a triggering event will occur and, because of this uncertainty, insurance-linked securities carry a high degree of risk.

10

| 13. | With respect to “Insurance-Linked Securities Risk” consider whether there should be some additional disclosure based on recent climate related events. See IM Guidance Update 2016-02 which reminds funds that they should review their risk disclosures on an ongoing basis and consider whether their disclosures remain adequate in light of current conditions. |

Response: The Registrant has reviewed its risk disclosure in light of IM Guidance Update 2016-02 and has revised its disclosure as noted in the response to comment #12 above.

| 14. | Under “QIB Qualification Risk” the last sentence states “[f]or any period during which the Fund does not qualify as a QIB, it will not be able to purchase Cat Bonds or other insurance-linked securities, which may prevent the Fund from achieving its investment objective. Consider whether this sentence should be part of the Principal Investment Strategies for the Fund. |

Response: The Registrant has added the sentence as part of its Principal Investment Strategies.

| 15. | Please add a concentration risk factor. |

Response: The Fund concentrates its investments in the financial services group of industries. The Registrant has added the following disclosure:

Concentration Risk: The Fund concentrates its investments in the financial services group of industries. Concentrating assets in a particular industry, sector of the economy, or markets can increase volatility because the investment will be more susceptible to the impact of market, economic, regulatory, and other factors affecting that industry or sector compared with a more broadly diversified asset allocation.

Purchase and Sale of Fund Shares

| 16. | The Fund indicates it is available for investment only by: (i) clients of registered investment advisors; (ii) institutional investors, including professional firms in the investment business, registered investment advisors (RIAs), family offices, pensions, endowments and foundations; (iii) clients of institutional investors; (iv) tax-exempt retirement plans of the Advisor and its affiliates; (iv) current directors and employees of the Advisor and its affiliates, and Trustees of the Trust; (v) investment professionals or other financial intermediaries investing for their own accounts, and their immediate family members; and (vi) certain other eligible investors as approved from time to time by the Advisor. Please provide what the minimum investment will be for an initial investment in the Fund. |

Response: The disclosure has been replaced with the following:

11

The Fund is generally sold to (i) institutional investors, including registered investment advisers (RIAs), that meet certain qualifications and have completed an educational program provided by the Advisor; and (ii) clients of such institutional investors. The minimum initial investment (which may be waived or reduced in certain circumstances) is $250,000. These minimums may be modified and/or applied in the aggregate for certain intermediaries that submit trades on behalf of underlying investors (e.g., registered investment advisers or benefit plans). Differences in the policies of different intermediaries may include different minimum investment amounts. There is no minimum for subsequent investments. All share purchases are subject to approval of the Advisor.

MORE ABOUT THE FUND’S INVESTMENT OBJECTIVE, PRINCIPAL INVESTMENT STRATEGIES AND RISKS

Principal Investment Strategies and Principal Risks of Investing

| 17. | Apply all applicable comments from the summary section for the Fund to Item 9 of Form N-1A. |

Response: The Registrant confirms that all applicable comments from the summary section have been made to the Item 9 disclosure.

STATEMENT OF ADDITIONAL INFORMATION (“SAI”)

Investment Restrictions

| 18. | Please confirm whether the Fund should have a concentration policy. |

Response: The Registrants confirm that the Fund will concentrate its investments in the financial services group of industries. The following disclosure has been added to the fundamental restrictions in the SAI.

The Fund may not: (6) Invest 25% or more of its total assets, calculated at the time of purchase, in any one industry or related group of industries, except the Fund will invest 25% or more of its total assets in the financial services group of industries or as permitted by exemptive or other relief or permission from the SEC, SEC staff or other authority of competent jurisdiction. This limit does not apply to securities issued or guaranteed by the U.S. government, its agencies or instrumentalities.

With respect to the fundamental policy relating to concentration set forth in (6) above, the 1940 Act does not define what constitutes “concentration” in an industry. The SEC staff has taken the position that investment of 25% or more of a fund’s total assets in one or more issuers conducting their principal activities in the same industry or group of industries constitutes concentration. It is possible that interpretations of concentration could change in the future. A fund that invests a significant percentage of its total assets in a single industry may be particularly susceptible to adverse events affecting that industry and may be more risky than a fund that does not concentrate in an industry. The policy in (6) above will be interpreted to refer to concentration as that term may be interpreted from time to time. The policy also will be interpreted to permit investment without limit in securities of the U.S. Government and its agencies or instrumentalities and repurchase agreements collateralized by any such obligations. Accordingly, issuers of the foregoing securities will not be considered to be members of any industry. The policy also will be interpreted to give broad authority to the Fund as to how to classify issuers within or among industries. When identifying industries for purposes of its concentration policy, the Fund may rely upon available industry classifications (e.g., Bloomberg L.P. classifications, MSCI Global Industry Classification Standard). The Fund may change any source used for determining industry classifications without shareholder approval.

12

PART C

| 19. | Please include the investment advisory agreement and investment sub-advisory agreement with the Registrant’s response for review. |

Response: The Registrant has included the form of investment advisory agreement and investment sub-advisory agreement with this correspondence and these agreements will be included as exhibits to the Amendment. The Registrant has revised the disclosure in the SAI regarding the Sub-Advisor and Sub-Advisory Agreement:

Sub-Advisor

The Advisor has entered into a sub-advisory agreement with the Sub-Advisor with respect to the Fund (the “Sub-Advisory Agreement”). Tangency is owned by Tangency Capital Limited, which is 100% employee-owned.

The Advisor compensates the Sub-Advisor out of the investment advisory fees the Advisor receives from the Fund. The Sub-Advisor makes investment decisions for the assets it has been allocated to manage, subject to the overall supervision of the Advisor.

The Sub-Advisory Agreement will remain in effect for an initial two-year period. After the initial two-year period, the Sub-Advisory Agreement will continue in effect from year to year only as long as such continuance is specifically approved at least annually by (i) the Board of Trustees of the Trust or by the vote of a majority of the outstanding voting shares of the Fund, and (ii) by the vote of a majority of the Trustees of the Trust who are not parties to the Sub-Advisory Agreement or interested persons of the Advisor or the Sub-Advisor or the Trust. Pursuant to the Sub-Advisory Agreement, the Sub-Advisory Agreement may be terminated at any time without the payment of any penalty by the Board of Trustees of the Trust or by the vote of a majority of the outstanding voting shares of the Fund, or by the Advisor upon 60 days’ written notice to the Sub-Advisor. The Sub-Advisory Agreement also may be terminated by the Sub-Advisor on six months’ written notice to the Trust.

The Advisor has entered into a separate agreement with the Sub-Advisor, which provides that in the event the Advisor terminates the Sub-Advisory Agreement, the Advisor will pay the Sub-Advisor certain fees from the Advisor’s retained earnings for a period of six months after the Adviser provides notice of such termination. This agreement creates a potential conflict of interest in that the Advisor may have a disincentive to terminate the Sub-Advisory Agreement. In any case, the Sub-Advisory Agreement may be terminated by the Trust’s Board of Trustees, which oversees the Advisor and the Sub-Advisor, or by the vote of a majority of the outstanding voting securities of the Fund, at any time upon 60 days’ notice to the Sub-Advisor without the payment of any penalty by the Fund.

The Sub-Advisory Agreement automatically terminates in the event of its assignment. The Sub-Advisory Agreement provides that the Sub-Advisor shall not be liable for any mistake of judgment or in any event, except for lack of good faith or liability to which the Sub-advisor would otherwise be subject by reason of willful misfeasance, bad faith or negligence in the performance of the Sub-advisor's duties, or by reason of the Sub-advisor's reckless disregard of its obligations and duties. In addition, the Sub-Advisor shall not be liable for any failure or delay in performance of its obligations arising out of or caused, directly or indirectly, by circumstances beyond its reasonable control.

.

13

**************

If you have any questions or additional comments, please contact me at (626) 385-5777 or diane.drake@mfac-ca.com or you can contact Joy Ausili at (909) 816-7378 or joy.ausili@mfac-ca.com. Thank you.

Sincerely,

| /s/ Diane J. Drake |

Diane J. Drake

Secretary

Enclosures

14

Exhibit A

| Before January 1, 2002 | January 1, 2002 to November 31, 2012 | December 1, 2012 to September 30, 2021 | |||

| Total Bonds Issued | 67 | 439 | ~750+ | ||

| Total Notional Issued | ~$4.4 billion | ~$43.1 billion | ~150.5 billion | ||

| Average Size of Issuance | ~$65 million | ~$98 million | ~$205 million | ||

| Current Notional Outstanding | ~$16 billion | ~52 billion | |||

| Total Number of CAT Bond Sponsors | 17 | 66 | 81 | ||

| Published index that tracks the asset class for reference | No | Yes: | Yes

| ||

| ● | Swiss Re Global CAT Bond Price, Coupon, and Total Return Indices | · | Swiss Re Global CAT Bond Price, Coupon, and Total Return Indices | ||

| ● | Swiss Re Global Unhedged CAT Bond Price, Coupon, and Total Return Indices | · | Swiss Re Global Unhedged CAT Bond Price, Coupon, and Total Return Indices | ||

| ● | Swiss Re USD CAT Bond Price, Coupon Total Return Indices | · | Swiss Re USD CAT Bond Price, Coupon Total Return Indices | ||

| ● | Swiss Re BB CAT Bond Price, Coupon, Total Return Indices | · | Swiss Re BB CAT Bond Price, Coupon, Total Return Indices | ||

| ● | Swiss Re US Wind CAT Bond Price, Coupon, Total Return Indices | · | Swiss Re US Wind CAT Bond Price, Coupon, Total Return Indices | ||

| ● | Aon Benfield All CAT Bond Index | · | Aon US Hurricane Bond Index (AONCUSHU) | ||

| ● | Aon Benfield BB-rated CAT Bond Index | · | Aon All Bond Bloomberg Ticker (AONCILS) | ||

| ● | Aon Benfield US Hurricane CAT Bond Index | · | Lane Financial LLC Synthetic Rate on Line Index (tracks movements in the cat bond and ILS markets | ||

| ● | Aon Benfield US Earthquake CAT Bond Index | ||||

| ● | Lane Financial Insurance Return Index (tracks only CAT bond returns) | ||||

| ● | Lane Financial Insurance Total Return Index (tracks only CAT bond returns) | ||||

| Number of Peril Types | 7 (California earthquake, Central US earthquake, European windstorm, Japan earthquake, Japan typhoon, multiperil, US hurricane) | 21 (Atlantic windstorm, auto, California earthquake, Central US earthquake, credit, European windstorm, event cancellation, extreme morbidity, extreme mortality, industrial accident, Japan earthquake, Japan typhoon, longevity divergence, Mexico earthquake, multiperil, other, Pacific wind, Pacific Northwest earthquake, US convective storm, US earthquake, US hurricane) | 35 + (including the 21 mentioned in the period prior, in addition to: Philippines Typhoon, Philippines Earthquake, South American EQ, pandemic, Australia Cyclone, Australia Earthquake, New Zealand Earthquake, California Wildfire, Canadian Earthquake, Canadian Named Storm, Canada Severe Convective Storm, UK Terrorism, UK flood, Turkish Earthquake, China Earthquake) | ||

| Collateral Management Strategies | Total Return Swaps | US Treasury Money Market funds, Puttable Floating Rate Notes (issued by AAA-rated entities) | US Treasury Money Market funds, T-bills with maturities typically no more than 3 months, Puttable Floating Rate Notes (issued by AAA-rated entities – e.g., International Bank for Reconstruction and Development) | ||

15