INVESTMENT MANAGERS SERIES TRUST II

235 W. Galena Street

Milwaukee, Wisconsin 53212

VIA EDGAR

January 21, 2022

Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549

Attention: Division of Investment Management

| Re: | Investment Managers Series Trust II File No. 333-191476 and 811-22894 (the “Registrant”) on behalf of the AXS Change Finance ESG ETF |

Ladies and Gentlemen:

This letter summarizes the comments provided to me by Ms. Samantha Brutlag of the staff of the Securities and Exchange Commission (the “Commission”) by telephone on December 29, 2021, on the Registrant’s registration statement filed on Form N-1A (the “Registration Statement”) relating to the AXS Change Finance ESG ETF (the “Fund”), a series of the Registrant. Responses to all of the comments are included below and, as appropriate, will be reflected in a Post-Effective Amendment to the Fund’s Form N-1A registration statement (the “Amendment”) which will be filed separately. Capitalized terms not otherwise defined in this letter have the meanings assigned to them in the Registration Statement.

GENERAL

| 1. | Please confirm that the Fund’s Prospectus and Statement of Additional Information (“SAI”) will not be used to offer shares to investors until after the reorganization is completed. |

Response: The Registrant so confirms.

| 2. | Please confirm in your written response that the comments given on the Registration Statement on Form N-1A will be made to the Registration Statement on Form N-14, as applicable. |

Response: The Registrant so confirms.

PROSPECTUS

SUMMARY SECTION

Fees and Expenses

| 3. | Please provide the completed Fees and Expenses Table and Example one week in advance prior to filing the Amendment. |

Response: Below are the Fees and Expenses Table and Example for the Fund:

1

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy, hold and sell shares of the Fund (“Shares”). Investors may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the table and example set forth below.

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

| Management Fees | 0.49% |

| Distribution and Service (12b-1) Fees | 0.00% |

| Other Expenses(1) | 0.00% |

| Total Annual Fund Operating Expenses | 0.49% |

| (1) | “Other Expenses” are estimates based on the expenses the Fund expects to incur for the current fiscal year. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other funds.

This example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your Shares at the end of those periods. The example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain at current levels. This example does not include the brokerage commissions that investors may pay to buy and sell Shares.

Although your actual costs may be higher or lower, your costs, based on these assumptions, would be:

| 1 Year | 3 Years |

| $50 | $157 |

Principal Risks

| 4. | With respect to “Risk of Investing in ESG Companies,” consider adding disclosure that third-party data used to select ESG companies may be unreliable. |

Response: The Registrant has revised the risk disclosure as follows:

Risk of Investing in ESG Companies. The universe of acceptable investments for the Fund may be limited as compared to other funds due to the Fund’s ESG investment screening. This may affect the Fund’s exposure to certain companies or industries and the Fund will forgo certain investment opportunities. The Fund’s performance may be lower than other funds that do not seek to invest in companies based on ESG factors and/or remove certain companies or industries from its selection process. The Sub-Advisor seeks to identify companies that it believes may have higher ESG scores under its proprietary methodology, but investors may differ in their views of ESG characteristics.Additionally, theThe Fund may not remove investments from its selection process based on certain ESG standards. As a result, the Fund may invest in companies that do not reflect the beliefs and values of any particular investor. Additionally, ESG information from third-party data providers may be incomplete, inaccurate or unavailable, which could cause the Sub-Advisor to incorrectly assess a company’s ESG characteristics.

2

Performance

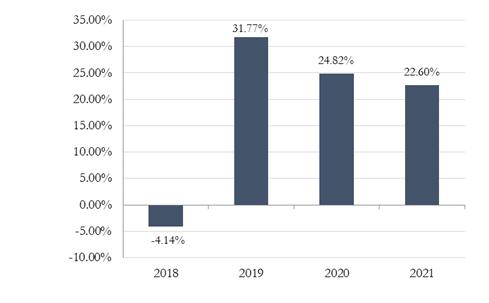

| 5. | Please update the Fund’s performance information with the Predecessor Fund’s performance for 2020 and 2021 and provide the updated performance information one week in advance prior to filing the Amendment. |

Response: The Registrant has updated the performance information as follows:

Calendar-Year Total Return (before taxes) for Predecessor Fund

For each calendar year at NAV

The Predecessor Fund’s highest quarterly return was 24.15% (quarter ended 6/30/2020) and the Fund’s lowest quarterly return was -19.94% (quarter ended 3/31/2020).

| Average Annual Total Return as of December 31, 2021 | ||

| 1 Year | Since Inception (10/9/2017) | |

| Return Before Taxes | 22.60% | 18.02% |

| Return After Taxes on Distributions | 22.43% | 17.79% |

| Return After Taxes on Distributions and Sale of Fund Shares | 13.49% | 14.44% |

| Change Finance Diversified Impact U.S. Large Cap Fossil Fuel Free Index (reflects no deduction for fees, expenses or taxes) | 23.31% | 18.77% |

| S&P 500® Index (reflects no deduction for fees, expenses or taxes) | 28.71% | 18.12% |

The Predecessor Fund’s past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future.

Returns before taxes do not reflect the effects of any income or capital gains taxes. All after-tax returns are calculated using the historical highest individual federal marginal income taxes and do not reflect the impact of any state or local tax. Returns after taxes on distributions reflect the taxed return on the payment of dividends and capital gains.

MORE ABOUT THE FUND’S INVESTMENT OBJECTIVES, PRINCIPAL INVESTMENT STRATEGIES AND RISKS

Principal Investment Strategies and Principal Risks of Investing

| 6. | Apply all applicable comments from the summary section for the Fund to Item 9 of Form N-1A. |

Response: The Registrant confirms that all applicable comments from the summary section have been made to the Item 9 disclosure.

STATEMENT OF ADDITIONAL INFORMATION (“SAI”)

| 7. | The disclosure contained in the Fund’s principal investment strategies and concentration risk indicate the that the Fund will be concentrated (i.e., invest more than 25% of Fund assets) in the industries or group of industries within a single sector to the extent that the Index is so concentrated. Please add this disclosure to the Fund’s investment limitation regarding concentration contained in the SAI. |

Response: The Registrant has revised the disclosure as follows:

The Fund may not invest 25% or more of its total assets, calculated at the time of purchase in any one industry (other than securities issued by the U.S. government, its agencies or instrumentalities), except that the Fund will concentrate to approximately the same extent that the Index concentrates in the securities of such particular industry or group of related industries.

| 8. | Under “Proxy Voting” please disclose how the Fund will approach ESG issues when voting proxies or explain why it is not required. |

Response: The Registrant has added the following disclosure under “Proxy Voting Policy”:

The Sub-Advisor’s environmental, social and governance (“ESG”) process extends to its proxy voting practices in that it will utilize recommendations from Glass Lewis and data available from ISS ESG and other sources to assess the likely impact of proposals on the ESG indicators that underpin the Index, and will vote against proposals that are likely to lower scores on any of those indicators, while supporting proposals that are likely to increase scores. In addition to considering the effects of a proposal on the indicators that make up the Fund’s Index, the Sub-Advisor may also consider effects that are in keeping with the principles of the Index, even if they are not specifically measured. For example, the Sub-Advisor will likely vote in favor of proposals that increase diversity on the Board of Directors or in senior leadership and against proposals that would allow the gap between executive pay and pay for low-level employees to grow too large.

3

* * * * *

The Registrant believes that it has fully responded to each comment. If, however, you have any further questions or require clarification of any response, please contact me at (626) 385-5777. I may also be reached at diane.drake@mfac-ca.com.

Sincerely,

/s/ DIANE J. DRAKE

Diane J. Drake

Secretary

4