UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22906

Virtus Alternative Solutions Trust

(Exact name of registrant as specified in charter)

101 Munson Street

Greenfield, MA 01301

(Address of principal executive offices) (Zip code)

Jennifer Fromm, Esq.

Vice President, Chief Legal Officer, Counsel and Secretary for Registrant

One Financial Plaza

Hartford, CT 06103-4506

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800)-243-1574

Date of fiscal year end: October 31

Date of reporting period: October 31, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

| Virtus Aviva Multi-Strategy Target Return Fund* |

| Virtus Duff & Phelps Select MLP and Energy Fund* |

| Virtus KAR Long/Short Equity Fund* |

| 1 | ||

| 2 | ||

| 4 | ||

| Fund | Fund Summary | Schedule of Investments |

| 6 | 15 | |

| 9 | 25 | |

| 12 | 27 | |

| 29 | ||

| 31 | ||

| 33 | ||

| 35 | ||

| 37 | ||

| 54 | ||

| 55 | ||

| 56 | ||

| 57 | ||

President, Virtus Funds

| Beginning Account Value May 1, 2020 | Ending Account Value October 31, 2020 | Annualized Expense Ratio* | Expenses Paid During Period** | |||||

Aviva Multi-Strategy Target Return Fund | ||||||||

| Class A | $ 1,000.00 | $ 995.80 | 1.69 % | $ 8.48 | ||||

| Class C | 1,000.00 | 991.50 | 2.44 | 12.21 | ||||

| Class I | 1,000.00 | 995.90 | 1.44 | 7.22 | ||||

| Class R6 | 1,000.00 | 996.90 | 1.38 | 6.93 | ||||

Duff & Phelps Select MLP and Energy Fund | ||||||||

| Class A | 1,000.00 | 948.50 | 1.40 | 6.86 | ||||

| Class C | 1,000.00 | 944.20 | 2.15 | 10.51 | ||||

| Class I | 1,000.00 | 949.40 | 1.15 | 5.64 | ||||

KAR Long/Short Equity Fund | ||||||||

| Class A | 1,000.00 | 1,239.80 | 2.29 | 12.87 | ||||

| Class C | 1,000.00 | 1,235.50 | 3.02 | 16.96 | ||||

| Class I | 1,000.00 | 1,241.90 | 2.04 | 11.49 | ||||

| Class R6 | 1,000.00 | 1,241.70 | 2.05 | 11.53 |

| * | Annualized expense ratios include dividend and interest expense on securities sold short. |

| ** | Expenses are equal to the relevant Fund’s annualized expense ratio, which is net of waived fees and reimbursed expenses, if applicable, multiplied by the average account value over the period, multiplied by the number of days (184) expenses were accrued in the most recent fiscal half-year, then divided by 366 to reflect the one-half year period. |

| Beginning Account Value May 1, 2020 | Ending Account Value October 31, 2020 | Annualized Expense Ratio* | Expenses Paid During Period** | |||||

Aviva Multi-Strategy Target Return Fund | ||||||||

| Class A | $ 1,000.00 | $ 1,016.64 | 1.69 % | $ 8.57 | ||||

| Class C | 1,000.00 | 1,012.87 | 2.44 | 12.34 | ||||

| Class I | 1,000.00 | 1,017.90 | 1.44 | 7.30 | ||||

| Class R6 | 1,000.00 | 1,018.20 | 1.38 | 7.00 | ||||

Duff & Phelps Select MLP and Energy Fund | ||||||||

| Class A | 1,000.00 | 1,018.10 | 1.40 | 7.10 | ||||

| Class C | 1,000.00 | 1,014.33 | 2.15 | 10.89 | ||||

| Class I | 1,000.00 | 1,019.35 | 1.15 | 5.84 | ||||

KAR Long/Short Equity Fund | ||||||||

| Class A | 1,000.00 | 1,013.64 | 2.29 | 11.57 | ||||

| Class C | 1,000.00 | 1,009.96 | 3.02 | 15.25 | ||||

| Class I | 1,000.00 | 1,014.89 | 2.04 | 10.32 | ||||

| Class R6 | 1,000.00 | 1,014.85 | 2.05 | 10.37 |

| * | Annualized expense ratios include dividend and interest expense on securities sold short. |

| ** | Expenses are equal to the relevant Fund’s annualized expense ratio, which is net of waived fees and reimbursed expenses, if applicable, multiplied by the average account value over the period, multiplied by the number of days (184) expenses were accrued in the most recent fiscal half-year, then divided by 366 to reflect the one-half year period. |

October 31, 2020

| Ticker Symbols: | |

| Class A: VMSAX | |

| Class C: VCMSX | |

| Class I: VMSIX | |

| Class R6: VMSRX |

Aviva Investors Americas LLC

| ■ | The Fund is diversified and has an investment objective of long-term total return. There is no guarantee that the Fund will meet its objective. |

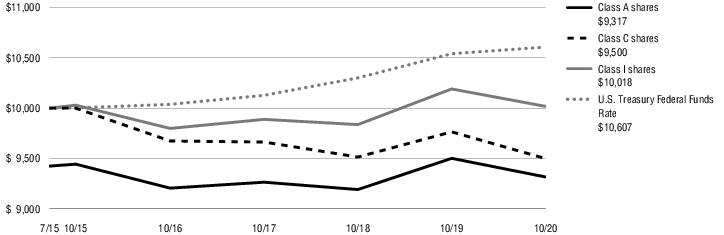

| ■ | For the fiscal year ended October 31, 2020, the Fund’s Class A shares at NAV returned -1.95%, Class C shares at NAV returned -2.71%, Class I shares at NAV returned -1.70% and Class R6 shares at NAV returned -1.65%. For the same period, the U.S. Treasury Federal Funds Rate, which serves as both the Fund’s broad-based and style-specific benchmark appropriate for comparison, returned 0.63%. |

| ■ | Financial markets ended 2019 on a positive note, as improving investor sentiment regarding global economic growth contributed to increased demand for riskier assets. Bonds underperformed, however, as the yields on safe-haven assets, such as U.S. government bonds, rose to levels that were not seen again over the course of the first 10 months of 2020. |

| ■ | The beginning of 2020 saw a continuation of market leadership by risk assets before the first signs of the COVID-19 outbreak triggered volatility in the equity markets. While Chinese stocks were the first to react to the news in January, most other global equity markets, including that of the U.S., were more resilient. This changed abruptly at the end of February, however, as the markets went into panic mode in anticipation of a severe global economic recession due to expected coronavirus lockdowns in a large number of countries. This led to investors selling both riskier and more defensive assets, which in turn created a liquidity |

| ■ | This trend continued throughout the second quarter of 2020 as markets welcomed the flurry of stimulus measures, which helped combat the dramatic slowdown of economic activity in the U.S. and other countries. Some clear winners emerged from the global lockdowns, as some of the largest household names in the technology and consumer discretionary sectors saw an opportunity to grow profits in the “work-from-home” environment. Investors were quick to reward financially stable companies, particularly those on track to grow their market share in the highly uncertain environment. While some sectors saw a relatively smooth recovery over the following months, cyclically sensitive parts of the equity market remained in deeply negative territory for the year. |

| ■ | In July and August, market sentiment continued to improve, with some countries, such as Australia, New Zealand, Canada, and Germany showing relative success in containing the spread of COVID-19 and supporting their economies. However, September and October saw volatility pick up due to investor concerns regarding delays to additional fiscal stimulus, rising political uncertainty around the U.S. presidential election, and increasing COVID-19 cases. |

| ■ | While equities in most developed and emerging markets declined during the fiscal year, bonds rose significantly on the back of the enormous monetary packages deployed by the major central banks. The U.S. dollar ended the year weaker against most peers, having seen a period of sharp appreciation during the market stress in March. Gold saw significant gains due to investor expectations around the real value of money being diluted by the trillions thrown into the system by global governments and central banks. |

| ■ | Credit assets benefitted from lower risk-free rates |

| across the board, however credit spreads rose in both the investment grade and high yield sectors across both developed and emerging markets. This reflected a deterioration in corporate fundamentals due to the challenging environment. Finally, volatility rose throughout the fiscal year as market stress reached extreme highs in March and subsided somewhat over the following months. |

| ■ | The Fund delivered negative performance for the fiscal year ended October 31, 2020. Performance was driven by gains in the Opportunistic Return strategies (a portion of the portfolio that consists of positions broadly uncorrelated to traditional asset classes) and Risk-Reducing Return strategies (a defensive part of the portfolio). The Fund’s Market Return strategies generated losses, as they consisted of riskier positions that were impacted by the deterioration in investor appetite for risk over the fiscal year. |

| ■ | The Fund’s performance benefitted from its bond exposure the most while being hurt by currencies and credit. |

| ■ | Within top contributors, the Fund’s exposure to U.S. government bonds proved to be particularly profitable due to two positions – an outright long position, and a relative value strategy in which U.S. government bonds were paired against German government bonds. U.S. interest rates collapsed following the decisive rate cut by the Fed, while German bond yields had been already very low for a number of years. This allowed the spread between the two types of bonds to shrink significantly during the year’s volatile market conditions. |

| ■ | The Fund’s position in U.S. equities added to returns. The Fund’s strategy favored companies with strong balance sheets in the Russell 2000® Index over the broader market. This approach contributed positively to performance, as investors showed a preference for companies with stable finances during the peak of the crisis. An outright long exposure to U.S. equities also contributed to performance. |

| ■ | Finally, a strategy that was designed to benefit from lower real yields in the U.S. (that is, the difference between nominal interest rates and |

| inflation) also delivered strong gains on the back of a sharp decline in nominal yields. | |

| ■ | The five biggest detractors from performance included a mixed bag of strategies, two of which are no longer held in the Fund. A position in the Japanese yen detracted the most. The strategy was implemented for risk reduction purposes, but proved to be less effective after March as investor appetite for risk recovered. Most of the riskier global currencies saw sharp gains in the second and third quarters of 2020. |

| ■ | The Fund’s position in U.S. inflation-linked assets also detracted as inflation expectations collapsed in March. Most investors anticipated a sharp fall in economic activity across the globe, which in turn led to speculation that inflationary pressures would decline. |

| ■ | Three equity strategies delivered negative returns, as well. The Fund’s exposure to Japanese and European stocks resulted in negative performance as both markets suffered extreme volatility at the beginning of the year, and prices were slow to recover. Finally, the Fund’s emphasis on value stocks over global consumer staples names also generated negative performance. Investors saw more stability and potential in consumer staples stocks, which typically do well in recessionary economic conditions. |

| ■ | The Fund’s usage of derivatives did not materially impact returns, since derivatives are used for risk management and efficient portfolio management purposes, as opposed to return enhancement. |

| Common Stocks | 49% |

| Short-Term Investment | 47 |

| Exchange-Traded Fund | 5 |

| Purchased Options | 2 |

| Written Options | (3) |

| Total | 100% |

| 1 Year | 5 Years | Since inception | Inception date | |||||||

| Class A shares at NAV2 | -1.95 % | -0.27 % | -0.22 % | 7/20/15 | ||||||

| Class A shares at POP3,4 | -7.59 | -1.44 | -1.33 | 7/20/15 | ||||||

| Class C shares at NAV and with CDSC2,4 | -2.71 | -1.02 | -0.97 | 7/20/15 | ||||||

| Class I shares at NAV | -1.70 | -0.02 | 0.03 | 7/20/15 | ||||||

| Class R6 shares at NAV | -1.65 | — | 0.84 | 11/3/16 | ||||||

| U.S. Treasury Federal Funds Rate | 0.63 | 1.18 | — 5 | — | ||||||

| Fund Expense Ratios6: A Shares: Gross 2.24%, Net 1.78%; C Shares: Gross 2.97%, Net 2.53%; I Shares: Gross 1.97%, Net 1.53%, R6 Shares: Gross 1.93%, Net 1.47%. | ||||||||||

| All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end. |

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gain distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 5.75% sales charge. |

| 4 | “CDSC” (contingent deferred sales charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC for certain redemptions of Class A shares made within 18 months of a finder’s fee being paid and all Class C shares are 1% within the first year and 0% thereafter. |

| 5 | The since inception index returned 1.42% for Class R6 and 1.13% for Class A, C and I shares of the respective share classes. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective February 28, 2020, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by the contractual fee waiver and expense limitation in effect through February 28, 2021. Gross Expense: Does not reflect the effect of the fee waiver or expense limitation. Expense ratios reflect fees and expenses associated with any underlying funds. |

| Ticker Symbols: | |

| Class A: VLPAX | |

| Class C: VLPCX | |

| Class I: VLPIX |

Duff & Phelps Investment Management Co.

| ■ | The Fund is non-diversified and has an investment objective of total return with a secondary objective of income. There is no guarantee that the Fund will meet its objective. |

| ■ | For the fiscal year ended October 31, 2020, the Fund’s Class A shares at NAV returned -32.15%, Class C shares at NAV returned -32.76%, and Class I shares at NAV returned -32.03%. For the same period, the Alerian MLP Index, which serves as both the Fund’s broad-based and style-specific benchmark appropriate for comparison, returned -42.52%. |

| ■ | Stable energy markets depend on the forces of supply and demand finding relative balance, but two seismic developments made the fiscal year ended October 31, 2020, one of the most difficult periods on record for the energy sector. During the period, midstream energy stocks fell 42.5%, as measured by the Alerian MLP Index, and massively underperformed the broader S&P 500® Index. The first quarter of the fiscal year was characterized by the volatility that has become commonplace for the midstream sector. With the sector badly lagging the S&P 500® Index and a number of stocks in the red on a calendar year basis in 2019, November brought a round of tax-loss selling, followed by a sharp rebound starting in December and carrying through much of January 2020. The rally began to fade around mid-month as the market began to worry about the impact of COVID-19 on Chinese energy |

| ■ | In February, the global reach of COVID-19 was becoming clearer, and by March, governments across the world were orchestrating coordinated shutdowns of their economies in order to control the spread of the virus. As estimated by some observers, this ultimately drove a sharp decline of over 26 million barrels per day in oil demand at the trough, amounting to roughly 25% of global petroleum consumption. This represented the greatest demand shock in modern times. |

| ■ | Around the same time, OPEC and allied countries (OPEC+) met in early March to address severe oversupply in crude oil markets, but members were unable to find consensus on a strategy. With key participants Saudi Arabia and Russia advocating for diametrically opposite actions, these two countries effectively launched a price war for market share that pushed the U.S. West Texas Intermediate (WTI) crude oil benchmark down 45% over the following two weeks. |

| ■ | This period was disastrous for midstream energy stock performance, and there was nowhere to hide. The Alerian MLP Index fell nearly 60% from the start of March to its bottom around mid-month. Selling pressure was relentless and indiscriminate, exacerbated by the unwinding of many master limited partnership (MLP) closed-end funds, most of which had taken on leverage to amplify their buying power. |

| ■ | With demand in apparent free fall and Saudi Arabia flooding the markets with additional crude that could not be absorbed, every nook and cranny of global storage started to rapidly fill. Production needed to decline, deeply and immediately, and the world was waiting on U.S. shale producers to blink. With storage approaching tank tops, the WTI crude index briefly went into negative territory, closing below -$37 per barrel in late April, before returning to positive territory. It closed the month at just under $19 per barrel. |

| ■ | Surprisingly, midstream stocks rose sharply beginning in late March, as closed-end fund liquidations ended and savvy investors stepped up, understanding that the stocks had been oversold. The Alerian MLP Index rallied more than |

| 90% from the bottom in March through the end of April, but this still left the index down 33% for the fiscal year to date. | |

| ■ | With crude oil prices far below the cash cost to operate wells, shale producers took the first step toward rebalancing the market. They not only halted all new drilling, but even curtailed wells that were already online and flowing, which pushed U.S. production into decline. Then Saudi Arabia and Russia came back together to broker the largest production cut in OPEC history, removing roughly 9% of global supply. With the necessary supply response in place and demand losses bottoming out, crude oil prices rebounded to positive $40 per barrel by the end of July. And with oil prices back above the cash cost, producers brought shut-in volumes back online, improving the near-term outlook for midstream companies. However, as the market came to realize that the pandemic would go on far longer than most had envisioned, the stocks failed to sustain any positive momentum, falling another 12% over the last six months of the fiscal year. WTI ended the fiscal year just under $36 per barrel, down 34%. |

| ■ | Despite the broad-based carnage in the sector, there were still relative winners and losers, with trading activity becoming more discriminate as the pandemic wore on. First, the market showed a clear preference for the strongest balance sheets. All companies slashed their capital expenditure (capex) budgets and reduced operating and overhead expenses, accelerating a pivot to free cash flow generation that had been forming prior to the pandemic. But companies with too much debt were forced to go a step further, slashing their dividends and distributions. Those companies earliest to take action saw their stock prices rebound more quickly. |

| ■ | Asset mix also led to select opportunities for well-positioned companies. Natural gas and natural gas liquids (NGL) prices actually rose during the year, benefitting companies with assets in the Marcellus/Utica regions and those with NGL export facilities. A significant quantity of these commodities are produced alongside crude oil in key shale basins, so the sharp decline in crude oil production also resulted in lower volumes and higher prices for natural gas and NGLs. Owners of crude oil storage also benefitted, as the short-term oversupply condition created a window for |

| operators to fully contract those facilities with substantial tariff increases. Generally, the stocks that were more challenged during the fiscal year represented gathering and processing companies, those with volumetric exposure to crude oil and refined product pipelines, and companies whose balance sheets remained stretched even after dividend/distribution cuts. | |

| ■ | While pandemic-related impacts largely drove sector performance, there were other contributing factors. Investor adoption of environmental, social & governance (ESG) principles and focus on the transition to cleaner energy accelerated during the fiscal year. Traditional energy companies are thought to be long-term losers to solar, wind, and other green technologies. The good news is the sector started to take these issues more seriously, with several companies publishing their first sustainability reports and committing to specific operating practices that reduce emissions. Midstream energy scores particularly poorly on governance given the particulars of the MLP structure and a recent history of egregious outcomes for limited partner investors. A number of MLPs have converted to traditional C-corporations where governance protections are greater, but several large midstream companies continue to back the MLP structure. Uncertainty around the U.S. presidential election was also a factor, as investors worried about an acceleration of the transition to cleaner sources of energy should the Democrats win control of the White House and Congress. To that end, Canadian midstream companies generally outperformed their U.S. counterparts in the fiscal year. |

| ■ | The Fund outperformed the Alerian MLP Index for the 12 months ended October 31, 2020. The Fund benefitted on a relative basis from finding value outside of the large MLPs that dominate the benchmark. This was particularly true with investments in midstream C-corporations oriented toward natural gas and liquefied natural gas (LNG). The Fund was significantly underweight the large MLPs, which we believe need to attract a broader investor base with governance reforms and major index inclusion through eventual conversions to C-corporations. The Fund outperformed the benchmark over the second, |

| third, and fourth quarters of the fiscal year, and was roughly in-line for the first quarter. Outperformance was most pronounced in the second and third quarters of the fiscal year, when the effects of the pandemic ravaged the market most severely. | |

| ■ | The five largest individual contributors to Fund performance on an absolute basis were Antero Midstream, Williams, Hess Midstream LP, MPLX LP, and NextEra Energy Partners LP. Antero Midstream traded higher on the improvement in natural gas prices, along with significant progress by its parent, Antero Resources, in reducing near-term debt maturities and the market’s perception of elevated counterparty risk. Williams performed well on the relative stability of its natural gas-heavy business mix. Hess Midstream demonstrated base business resilience from its unique contract structure with its parent, Hess Corporation. MPLX responded to a strategic re-commitment from its parent, Marathon Petroleum, as well as an improved production outlook in the gassy Marcellus/Utica shales of the Appalachia Basin. NextEra Energy Partners, a leading operator of renewable power generation assets in the U.S., benefited from a strong rally in clean energy stocks. |

| ■ | The five largest individual detractors from Fund performance on an absolute basis were Plains GP Holdings LP, ONEOK, Energy Transfer LP, Targa Resources, and Enterprise Products Partners. Plains, Energy Transfer, and Targa were three companies with elevated leverage and heavily dependent on production from the Permian Basin, where drilling activity fell to levels insufficient to offset natural declines on existing wells. ONEOK also suffered from high leverage and concerns about the sustainability of its dividend, especially given sharp production curtailments on its core Williston Basin footprint. Enterprise, while certainly not unscathed by the pandemic, held up relatively well on a fundamental basis, but the market failed to reward the resiliency of its vertically integrated asset base, likely reflecting the MLP structure being out of favor. |

| Diversified | 28% | |

| Gathering/Processing | 19 | |

| Downstream/Other | 17 | |

| Petroleum Transportation & Storage | 15 | |

| Natural Gas Pipelines | 11 | |

| Electric, LDC & Power | 9 | |

| Upstream | 1 | |

| Total | 100% |

| 1 Year | 5 Years | Since inception | Inception date | |||||||

| Class A shares at NAV2 | -32.15 % | -8.72 % | -8.86 % | 9/9/15 | ||||||

| Class A shares at POP3,4 | -36.05 | -9.79 | -9.90 | 9/9/15 | ||||||

| Class C shares at NAV and with CDSC2,4 | -32.76 | -9.44 | -9.58 | 9/9/15 | ||||||

| Class I shares at NAV | -32.03 | -8.52 | -8.66 | 9/9/15 | ||||||

| Alerian MLP Index | -42.52 | -12.46 | -12.75 5 | — | ||||||

| Fund Expense Ratios6: A Shares: Gross 2.62%, Net 1.43%; C Shares: Gross 3.38%, Net 2.18%; I Shares: Gross 2.33%, Net 1.18%. | ||||||||||

| All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end. |

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gain distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 5.75% sales charge. |

| 4 | “CDSC” (contingent deferred sales charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC for certain redemptions of Class A shares made within 18 months of a finder’s fee being paid and all Class C shares are 1% within the first year and 0% thereafter. |

| 5 | The since inception index return is from the Fund’s inception date. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective February 28, 2020, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by the contractual expense limitation in effect through February 28, 2021. Gross Expense: Does not reflect the effect of the expense limitation. Expense ratios reflect fees and expenses associated with any underlying funds. |

| Ticker Symbols: | |

| Class A : VLSAX | |

| Class C: VLSCX | |

| Class I: VLSIX | |

| Class R6: VLSRX |

Kayne Anderson Rudnick Investment Management, LLC

| ■ | The Fund is non-diversified and has an investment objective of seeking long-term capital appreciation. There is no guarantee that the Fund will meet its objective. |

| ■ | Stock market returns were mostly positive during the fiscal year. For the 12 months ended October 31, 2020, the S&P 500® Index advanced 9.71%, while small-capitalization stocks, as represented by the Russell 2000® Index, declined 0.14%. The Russell 3000® Index increased 10.15% during the period. International developed markets, as measured by the MSCI EAFE® Index (net), declined 6.86% while the MSCI Emerging Markets Index (net) gained 8.25%. |

| ■ | Equity investors enjoyed solid returns in the fourth quarter of 2019 and then went for a roller coaster ride in the first quarter of 2020, as markets around the world declined due to the COVID-19 pandemic, which necessitated an almost complete shutdown of economic activity. After a nosedive first quarter of 2020, the S&P 500® Index recovered in the following three months to have its best quarter in over 20 years, erasing most of the first-quarter loss. With aggressive stimulus from governments around the world flowing into the markets as a |

| ■ | The Fund meaningfully outperformed its benchmark, the Russell 3000® Index, on an absolute basis for the 12 months ended October 31, 2020. The long portfolio outpaced the return of the Russell 3000® Index, while the short portfolio, which profits when its holdings decline in value, also made a positive contribution to performance. |

| ■ | In the long portfolio, strong stock selection in industrials and information technology contributed meaningfully to performance. Poor stock selection and an underweight in consumer discretionary, as well as poor stock selection in real estate, detracted from performance. |

| ■ | In the short portfolio, strong stock selection in real estate and consumer discretionary contributed positively to performance. Poor stock selection in information technology and consumer staples detracted from performance. |

| ■ | The Trade Desk outperformed as growth returned to programmatic advertising in the most recent quarter, after the ad spending slowdown that followed the first COVID-19 wave. At about 25% of revenue, Connected Television (CTV) is The Trade Desk’s most important strategic focus at the moment, and one that could thrive under stay-at-home restrictions. The global TV ad market is at least $250 billion and CTV is estimated to be just 3% penetrated, with The Trade Desk named as the preferred provider by Disney and getting premium inventory from Amazon, Comcast, and Roku. |

| ■ | DocuSign had strong momentum in signing new |

| users for its contract management solutions. With COVID-19, the need to move to digital document management accelerated further. DocuSign also experienced accelerating growth for its e-signature solutions. | |

| ■ | Other top contributors included CoreLogic (long), Avalara (long), and POOLCORP (long). |

| ■ | Thor Industries manufactures and sells recreational vehicles (RVs). While Thor successfully weathered past recessions due to its variable cost structure, it entered the current recession with debt on its balance sheet. We decided to exit the position in the first quarter of 2020, and missed the subsequent rally in the stock as demand for RVs skyrocketed in the spring and summer travel seasons. The need for social distancing during the COVID-19 pandemic increased the appeal of traveling in an RV, driving Thor’s shares higher. |

| ■ | Endurance International specializes in web hosting and email marketing. The company’s stock price declined in the first quarter of 2020 as investors assessed the negative impact COVID-19 and shelter-in-place orders would have on the company. However, the stock rallied in the second quarter and remained on an upswing through the end of the fiscal year. COVID-19 has forced many businesses to invest more in digital advertising and communication to stay top-of-mind with consumers. As a result, Endurance reported positive customer count growth in 2020, after several years of declines. |

| ■ | Other top detractors included Lamar Advertising (long), Focus Financial Partners (short), and Century Communities (short). |

| Common Stocks | 110% | |

| Information Technology | 27% | |

| Industrials | 17 | |

| Communication Services | 15 | |

| Financials | 14 | |

| Consumer Staples | 11 | |

| Consumer Discretionary | 10 | |

| Health Care | 8 | |

| All other Common Stocks | 8 | |

| Short-Term Investment | 9 | |

| Securities Sold Short | (19) | |

| Industrials | (6) | |

| Real Estate | (2) | |

| Consumer Discretionary | (4) | |

| Information Technology | (2) | |

| Consumer Staples | (1) | |

| Financials | (4) | |

| Total | 100% |

| 1 Year | Since inception | Inception date | ||||||

| Class A shares at NAV2 | 30.01 % | 30.13 % | 12/6/18 | |||||

| Class A shares at POP3,4 | 22.54 | 26.13 | 12/6/18 | |||||

| Class C shares at NAV2 | 29.01 | 29.17 | 12/6/18 | |||||

| Class C shares at NAV and with CDSC4 | 29.01 | 29.17 | 12/6/18 | |||||

| Class I shares at NAV | 30.41 | 30.50 | 12/6/18 | |||||

| Class R6 shares at NAV | 30.39 | 30.54 | 12/6/18 | |||||

| Russell 3000® Index | 10.15 | 12.69 5 | — | |||||

| Fund Expense Ratios6: A Shares: Gross 4.20%, Net 2.34%; C Shares: Gross 4.95%, Net 3.09%; I Shares: Gross 4.04%, Net 2.09%, R6 Shares: Gross 3.94%, Net 2.02%. | ||||||||

| All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end. |

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gain distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 5.75% sales charge. |

| 4 | “CDSC” (contingent deferred sales charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC for certain redemptions of Class A shares made within 18 months of a finder’s fee being paid and all Class C shares are 1% within the first year and 0% thereafter. |

| 5 | The since inception index return is from the Fund’s inception date. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective February 28, 2020, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by the contractual expense limitation in effect through February 28, 2021. Gross Expense: Does not reflect the effect of the expense limitation. Expense ratios reflect fees and expenses associated with any underlying funds. |

October 31, 2020

| Shares | Value | ||

| Common Stocks—36.8% | |||

| Communication Services—3.4% | |||

| Altice USA, Inc. Class A(1) | 3,177 | $ 86 | |

| Anterix, Inc.(1) | 284 | 9 | |

| Bandwidth, Inc. Class A(1) | 61 | 10 | |

| Cable One, Inc. | 6 | 10 | |

| Cargurus, Inc.(1) | 437 | 9 | |

| Charter Communications, Inc. Class A(1) | 566 | 342 | |

| Comcast Corp. Class A | 7,775 | 328 | |

| Elisa OYJ | 987 | 48 | |

| Infrastrutture Wireless Italiane SpA 144A(2) | 5,527 | 60 | |

| Liberty Broadband Corp. Class A(1) | 72 | 10 | |

| Liberty Broadband Corp. Class C(1) | 71 | 10 | |

| NetEase, Inc. ADR | 520 | 45 | |

| New York Times Co. (The) Class A | 242 | 9 | |

| Nintendo Co. Ltd. | 100 | 54 | |

| Scout24 AG 144A(2) | 677 | 55 | |

| Spotify Technology SA(1) | 42 | 10 | |

| Take-Two Interactive Software, Inc.(1) | 62 | 10 | |

| TechTarget, Inc.(1) | 250 | 11 | |

| Vodafone Group PLC | 89,096 | 119 | |

| Zynga, Inc. Class A(1) | 1,187 | 11 | |

| 1,246 | |||

| Consumer Discretionary—4.5% | |||

| Accor SA(1) | 106 | 3 | |

| Aptiv PLC | 900 | 87 | |

| Aramark | 122 | 3 | |

| Aristocrat Leisure Ltd. | 317 | 6 | |

| Burlington Stores, Inc.(1) | 328 | 63 | |

| Carnival Corp. | 277 | 4 | |

| Carnival PLC | 9,817 | 108 | |

| Chegg, Inc.(1) | 151 | 11 | |

| Chipotle Mexican Grill, Inc.(1) | 22 | 26 | |

| Cie Generale des Etablissements Michelin SCA | 704 | 76 | |

| Columbia Sportswear Co. | 116 | 9 | |

| Compass Group PLC | 1,072 | 15 | |

| Crown Resorts Ltd. | 242 | 1 | |

| Darden Restaurants, Inc. | 68 | 6 | |

| Deckers Outdoor Corp.(1) | 48 | 12 | |

| Delivery Hero SE 144A(1)(2) | 537 | 62 | |

| Domino’s Pizza, Inc. | 24 | 9 | |

| Dorman Products, Inc.(1) | 124 | 11 | |

| EssilorLuxottica SA(1) | 474 | 59 | |

| Evolution Gaming Group AB 144A(2) | 59 | 4 | |

| Ferrari NV | 323 | 58 | |

| Flutter Entertainment PLC | 481 | 84 | |

| Galaxy Entertainment Group Ltd. Class L | 1,340 | 9 | |

| Garmin Ltd. | 109 | 11 | |

| Gentex Corp. | 408 | 11 | |

| Shares | Value | ||

| Consumer Discretionary—continued | |||

| Genting Singapore Ltd. | 3,600 | $ 2 | |

| Grand Canyon Education, Inc.(1) | 123 | 10 | |

| GVC Holdings PLC(1) | 290 | 4 | |

| Hilton Worldwide Holdings, Inc. | 156 | 14 | |

| InterContinental Hotels Group PLC(1) | 92 | 5 | |

| Just Eat Takeaway.com NV 144A(1)(2) | 531 | 59 | |

| Kering SA | 89 | 54 | |

| La Francaise des Jeux SAEM 144A(2) | 47 | 2 | |

| Las Vegas Sands Corp. | 203 | 10 | |

| Lululemon Athletica, Inc.(1) | 33 | 10 | |

| LVMH Moet Hennessy Louis Vuitton SE | 129 | 60 | |

| Marriott International, Inc. Class A | 158 | 15 | |

| McDonald’s Corp. | 413 | 88 | |

| McDonald’s Holdings Co. Japan Ltd. | 100 | 5 | |

| Melco Resorts & Entertainment Ltd. | 136 | 2 | |

| MGM Resorts International | 271 | 6 | |

| Oriental Land Co. Ltd | 100 | 14 | |

| Peugeot SA(1) | 10,074 | 181 | |

| Pool Corp. | 34 | 12 | |

| Prosus NV | 650 | 65 | |

| Restaurant Brands International, Inc. | 163 | 8 | |

| Royal Caribbean Cruises Ltd. | 104 | 6 | |

| Sands China Ltd. | 1,609 | 6 | |

| SJM Holdings Ltd. | 1,417 | 1 | |

| Sodexo SA | 52 | 3 | |

| Starbucks Corp. | 648 | 56 | |

| Tabcorp Holdings Ltd. | 1,251 | 3 | |

| Tiffany & Co. | 89 | 12 | |

| Toyota Motor Corp. | 1,200 | 79 | |

| Tractor Supply Co. | 73 | 10 | |

| Vail Resorts, Inc. | 22 | 5 | |

| Volkswagen AG | 509 | 74 | |

| Wingstop, Inc. | 72 | 8 | |

| Winmark Corp. | 66 | 11 | |

| Wynn Macau Ltd.(1) | 1,051 | 1 | |

| Wynn Resorts Ltd. | 57 | 4 | |

| Yum China Holdings, Inc. | 202 | 11 | |

| Yum! Brands, Inc. | 161 | 15 | |

| 1,679 | |||

| Consumer Staples—2.4% | |||

| Beiersdorf AG | 535 | 56 | |

| BellRing Brands, Inc. Class A(1) | 539 | 10 | |

| Boston Beer Co., Inc. (The) Class A(1) | 11 | 11 | |

| Brown-Forman Corp. Class A | 151 | 10 | |

| Brown-Forman Corp. Class B | 136 | 10 | |

| Shares | Value | ||

| Consumer Staples—continued | |||

| Calavo Growers, Inc. | 154 | $ 10 | |

| Cal-Maine Foods, Inc.(1) | 267 | 10 | |

| Carrefour SA | 7,531 | 117 | |

| Church & Dwight Co., Inc. | 113 | 10 | |

| Clorox Co. (The) | 49 | 10 | |

| Constellation Brands, Inc. Class A | 354 | 59 | |

| Danone SA | 916 | 51 | |

| Flowers Foods, Inc. | 439 | 10 | |

| Freshpet, Inc.(1) | 96 | 11 | |

| Heineken NV | 665 | 59 | |

| Henkel AG & Co. KGaA | 574 | 56 | |

| Hershey Co. (The) | 75 | 10 | |

| Hormel Foods Corp. | 212 | 10 | |

| J&J Snack Foods Corp. | 82 | 11 | |

| John B Sanfilippo & Son, Inc. | 139 | 10 | |

| Kerry Group PLC Class A | 450 | 54 | |

| Lancaster Colony Corp. | 58 | 10 | |

| L’Oreal SA | 184 | 60 | |

| McCormick & Co., Inc. | 54 | 10 | |

| National Beverage Corp.(1) | 142 | 11 | |

| Pernod Ricard SA | 372 | 60 | |

| Remy Cointreau SA | 334 | 56 | |

| Sanderson Farms, Inc. | 88 | 11 | |

| Tootsie Roll Industries, Inc. | 348 | 10 | |

| Unilever NV | 996 | 56 | |

| WD-40 Co. | 53 | 13 | |

| 892 | |||

| Energy—0.9% | |||

| BP PLC | 38,975 | 99 | |

| Koninklijke Vopak NV | 1,012 | 53 | |

| Reliance Industries Ltd. | 2,193 | 61 | |

| TOTAL SE | 3,372 | 101 | |

| 314 | |||

| Financials—2.7% | |||

| Aon PLC Class A | 430 | 79 | |

| Arch Capital Group Ltd.(1) | 2,130 | 64 | |

| AXA SA | 1,722 | 28 | |

| Banco Santander SA(1) | 84,064 | 168 | |

| Brown & Brown, Inc. | 645 | 28 | |

| Credicorp Ltd. | 364 | 42 | |

| Gallagher (Arthur J.) & Co. | 852 | 88 | |

| Marsh & McLennan Cos., Inc. | 765 | 79 | |

| Societe Generale SA(1) | 11,461 | 155 | |

| Standard Chartered PLC(1) | 6,603 | 30 | |

| UniCredit SpA(1) | 18,834 | 141 | |

| Willis Towers Watson PLC | 422 | 77 | |

| 979 | |||

| Health Care—4.8% | |||

| 10X Genomics, Inc. Class A(1) | 84 | 11 | |

| ABIOMED, Inc.(1) | 38 | 10 | |

| ACADIA Pharmaceuticals, Inc.(1) | 252 | 12 | |

| Acceleron Pharma, Inc. (1) | 94 | 10 | |

| Shares | Value | ||

| Health Care—continued | |||

| Agilent Technologies, Inc. | 105 | $ 11 | |

| Agios Pharmaceuticals, Inc.(1) | 282 | 11 | |

| Alexion Pharmaceuticals, Inc.(1) | 90 | 10 | |

| Allakos, Inc.(1) | 130 | 12 | |

| Allogene Therapeutics, Inc.(1) | 287 | 10 | |

| Alnylam Pharmaceuticals, Inc.(1) | 77 | 9 | |

| Amedisys, Inc.(1) | 44 | 11 | |

| Arena Pharmaceuticals, Inc.(1) | 140 | 12 | |

| Argenx SE(1) | 244 | 61 | |

| AtriCure, Inc.(1) | 265 | 9 | |

| Atrion Corp. | 16 | 10 | |

| Axonics Modulation Technologies, Inc.(1) | 235 | 11 | |

| BioMerieux | 392 | 58 | |

| Bio-Rad Laboratories, Inc. Class A(1) | 20 | 12 | |

| Bio-Techne Corp. | 42 | 11 | |

| Cardiovascular Systems, Inc.(1) | 293 | 10 | |

| Carl Zeiss Meditec AG | 502 | 65 | |

| Cerner Corp. | 150 | 10 | |

| Chemed Corp. | 21 | 10 | |

| ChemoCentryx, Inc.(1) | 195 | 9 | |

| Codexis, Inc.(1) | 862 | 11 | |

| Cooper Cos., Inc. (The) | 30 | 10 | |

| Corcept Therapeutics, Inc.(1) | 579 | 10 | |

| CryoPort, Inc.(1) | 226 | 9 | |

| Deciphera Pharmaceuticals, Inc.(1) | 198 | 11 | |

| DiaSorin SpA | 298 | 65 | |

| Eagle Pharmaceuticals Inc.(1) | 259 | 12 | |

| Eidos Therapeutics, Inc.(1) | 228 | 16 | |

| Enanta Pharmaceuticals, Inc.(1) | 232 | 10 | |

| Exelixis, Inc.(1) | 403 | 8 | |

| Global Blood Therapeutics, Inc.(1) | 193 | 10 | |

| Globus Medical, Inc. Class A(1) | 205 | 11 | |

| Guardant Health, Inc.(1) | 96 | 10 | |

| Haemonetics Corp.(1) | 122 | 12 | |

| Halozyme Therapeutics, Inc.(1) | 388 | 11 | |

| HMS Holdings Corp.(1) | 428 | 11 | |

| ICU Medical, Inc.(1) | 55 | 10 | |

| IDEXX Laboratories, Inc.(1) | 28 | 12 | |

| Immunovant, Inc.(1) | 289 | 13 | |

| Incyte Corp.(1) | 119 | 10 | |

| Inspire Medical Systems, Inc.(1) | 81 | 10 | |

| Insulet Corp.(1) | 45 | 10 | |

| Ionis Pharmaceuticals, Inc.(1) | 203 | 10 | |

| iRhythm Technologies, Inc.(1) | 46 | 10 | |

| Karuna Therapeutics, Inc.(1) | 130 | 11 | |

| Shares | Value | ||

| Health Care—continued | |||

| Kodiak Sciences, Inc.(1) | 197 | $ 18 | |

| Koninklijke Philips NV(1) | 1,310 | 61 | |

| Krystal Biotech, Inc.(1) | 238 | 10 | |

| Kura Oncology, Inc.(1) | 354 | 11 | |

| LeMaitre Vascular, Inc. | 318 | 10 | |

| LHC Group, Inc.(1) | 51 | 11 | |

| Livongo Health, Inc.(1) | 75 | 10 | |

| Luminex Corp. | 418 | 9 | |

| Madrigal Pharmaceuticals, Inc.(1) | 83 | 11 | |

| Masimo Corp.(1) | 47 | 11 | |

| Merck & Co., Inc. | 796 | 60 | |

| Mesa Laboratories, Inc. | 44 | 11 | |

| Mettler-Toledo International, Inc.(1) | 10 | 10 | |

| Mirati Therapeutics, Inc.(1) | 63 | 14 | |

| MyoKardia, Inc.(1) | 78 | 17 | |

| Neogen Corp.(1) | 131 | 9 | |

| Neurocrine Biosciences, Inc.(1) | 103 | 10 | |

| Nevro Corp.(1) | 71 | 11 | |

| Novocure Ltd.(1) | 99 | 12 | |

| Orion Oyj Class B | 1,289 | 55 | |

| OrthoPediatrics Corp.(1) | 242 | 11 | |

| Penumbra, Inc.(1) | 51 | 13 | |

| PerkinElmer, Inc. | 86 | 11 | |

| QIAGEN NV(1) | 1,178 | 56 | |

| QIAGEN NV(1) | 205 | 10 | |

| Relmada Therapeutics, Inc.(1) | 275 | 8 | |

| Repligen Corp.(1) | 72 | 12 | |

| ResMed, Inc. | 60 | 12 | |

| Rhythm Pharmaceuticals, Inc.(1) | 395 | 8 | |

| Sanofi | 594 | 54 | |

| Sarepta Therapeutics, Inc.(1) | 70 | 10 | |

| Sartorius AG | 148 | 63 | |

| Sartorius Stedim Biotech | 176 | 67 | |

| Seagen, Inc.(1) | 57 | 9 | |

| Shockwave Medical, Inc.(1) | 147 | 10 | |

| Silk Road Medical, Inc.(1) | 149 | 9 | |

| Simulations Plus, Inc. | 160 | 10 | |

| STAAR Surgical Co.(1) | 187 | 14 | |

| STERIS PLC | 61 | 11 | |

| Stoke Therapeutics, Inc.(1) | 301 | 12 | |

| Tactile Systems Technology, Inc.(1) | 316 | 12 | |

| Tandem Diabetes Care, Inc.(1) | 95 | 10 | |

| Teladoc Health, Inc.(1) | 48 | 9 | |

| Teleflex, Inc. | 31 | 10 | |

| Thermo Fisher Scientific, Inc. | 166 | 79 | |

| Turning Point Therapeutics, Inc.(1) | 122 | 11 | |

| UCB SA | 526 | 52 | |

| United Therapeutics Corp.(1) | 101 | 14 | |

| Varian Medical Systems, Inc.(1) | 60 | 10 | |

| Veeva Systems, Inc. Class A(1) | 38 | 10 | |

| Shares | Value | ||

| Health Care—continued | |||

| Veracyte, Inc.(1) | 327 | $ 11 | |

| Viking Therapeutics, Inc.(1) | 1,548 | 9 | |

| Waters Corp.(1) | 53 | 12 | |

| West Pharmaceutical Services, Inc. | 37 | 10 | |

| Wright Medical Group NV(1) | 362 | 11 | |

| Y-mAbs Therapeutics, Inc.(1) | 270 | 12 | |

| 1,791 | |||

| Industrials—7.9% | |||

| A.O. Smith Corp. | 196 | 10 | |

| AAON, Inc. | 181 | 11 | |

| Acuity Brands Inc. | 152 | 14 | |

| AeroVironment, Inc.(1) | 164 | 13 | |

| Air China Ltd. Class H | 11,612 | 8 | |

| Allegion PLC | 1,412 | 139 | |

| AMETEK, Inc. | 106 | 10 | |

| ANA Holdings, Inc.(1) | 1,700 | 37 | |

| Assa Abloy AB Class B | 5,936 | 127 | |

| Bouygues SA | 3,183 | 104 | |

| Brady Corp. Class A | 263 | 10 | |

| C.H. Robinson Worldwide, Inc. | 101 | 9 | |

| Carrier Global Corp. | 1,229 | 41 | |

| China Southern Airlines Co. Ltd. Class H(1) | 14,000 | 7 | |

| Cie de Saint-Gobain(1) | 1,129 | 44 | |

| Cintas Corp. | 32 | 10 | |

| Copart, Inc.(1) | 754 | 83 | |

| CoStar Group, Inc.(1) | 12 | 10 | |

| CSW Industrials, Inc. | 138 | 12 | |

| Daikin Industries Ltd. | 500 | 94 | |

| Delta Air Lines, Inc. | 3,506 | 107 | |

| Deutsche Lufthansa AG(1) | 2,385 | 20 | |

| Donaldson Co., Inc. | 221 | 11 | |

| easyJet PLC | 1,716 | 11 | |

| Encore Wire Corp. | 225 | 10 | |

| Equifax, Inc. | 747 | 102 | |

| Experian PLC | 3,319 | 121 | |

| Exponent, Inc. | 140 | 10 | |

| Fastenal Co. | 230 | 10 | |

| Graco, Inc. | 171 | 11 | |

| Heartland Express, Inc. | 559 | 10 | |

| HEICO Corp. | 96 | 10 | |

| HEICO Corp. Class A | 115 | 11 | |

| Hubbell, Inc. | 335 | 49 | |

| IDEX Corp. | 57 | 10 | |

| IHS Markit Ltd. | 131 | 11 | |

| Japan Airlines Co. Ltd.(1) | 2,700 | 47 | |

| JetBlue Airways Corp.(1) | 1,257 | 15 | |

| Johnson Controls International PLC | 892 | 38 | |

| Kingspan Group PLC(1) | 190 | 17 | |

| Kingspan Group PLC(1) | 693 | 60 | |

| Knorr-Bremse AG | 509 | 59 | |

| Kone OYJ Class B | 1,753 | 140 | |

| Landstar System, Inc. | 81 | 10 | |

| Legrand SA | 765 | 57 | |

| Lennox International, Inc. | 171 | 46 | |

| Lincoln Electric Holdings, Inc. | 116 | 12 | |

| Shares | Value | ||

| Industrials—continued | |||

| Mercury Systems, Inc.(1) | 134 | $ 9 | |

| MSC Industrial Direct Co., Inc. Class A | 166 | 12 | |

| National Presto Industries, Inc. | 124 | 10 | |

| Nordson Corp. | 55 | 11 | |

| Old Dominion Freight Line, Inc. | 57 | 11 | |

| Otis Worldwide Corp. | 2,015 | 123 | |

| Proto Labs, Inc.(1) | 77 | 9 | |

| Raven Industries, Inc. | 472 | 10 | |

| Republic Services, Inc. | 109 | 10 | |

| Robert Half International, Inc. | 196 | 10 | |

| Rollins, Inc. | 195 | 11 | |

| Ryanair Holdings PLC(1) | 2,635 | 36 | |

| Safran SA(1)(3)(4) | 246 | 26 | |

| Schindler Holding AG | 343 | 88 | |

| Schneider Electric SE | 898 | 109 | |

| Schneider National, Inc. Class B | 412 | 9 | |

| Signify NV 144A(1)(2) | 884 | 31 | |

| Simpson Manufacturing Co., Inc. | 109 | 10 | |

| Singapore Airlines Ltd. | 3,000 | 7 | |

| Southwest Airlines Co. | 1,829 | 72 | |

| Teledyne Technologies, Inc.(1) | 33 | 10 | |

| Teleperformance | 200 | 60 | |

| Toro Co. (The) | 124 | 10 | |

| Trane Technologies PLC | 921 | 122 | |

| TransUnion | 1,345 | 107 | |

| Trex Co., Inc.(1) | 151 | 11 | |

| UniFirst Corp. | 56 | 9 | |

| Union Pacific Corp. | 355 | 63 | |

| Verisk Analytics, Inc. | 57 | 10 | |

| Vicor Corp.(1) | 133 | 10 | |

| Watsco, Inc. | 200 | 45 | |

| Wolters Kluwer NV | 702 | 57 | |

| 2,936 | |||

| Information Technology—6.7% | |||

| Acacia Communications, Inc.(1) | 153 | 10 | |

| Adyen NV 144A(1)(2) | 32 | 54 | |

| Akamai Technologies, Inc.(1) | 92 | 9 | |

| Alarm.com Holdings, Inc.(1) | 186 | 11 | |

| Ambarella, Inc.(1) | 204 | 11 | |

| Amdocs Ltd. | 178 | 10 | |

| Amphenol Corp. Class A | 99 | 11 | |

| ANSYS, Inc.(1) | 32 | 10 | |

| Appfolio, Inc. Class A(1) | 72 | 10 | |

| Arista Networks, Inc.(1) | 52 | 11 | |

| ASML Holding NV | 164 | 60 | |

| Aspen Technology, Inc.(1) | 79 | 9 | |

| Avalara, Inc.(1) | 83 | 12 | |

| Badger Meter, Inc. | 161 | 12 | |

| Black Knight, Inc.(1) | 120 | 11 | |

| Blackline, Inc.(1) | 119 | 12 | |

| Shares | Value | ||

| Information Technology—continued | |||

| Booz Allen Hamilton Holding Corp. | 118 | $ 9 | |

| Broadcom, Inc. | 320 | 112 | |

| Broadridge Financial Solutions, Inc. | 78 | 11 | |

| Cadence Design Systems, Inc.(1) | 100 | 11 | |

| Capgemini SE | 270 | 31 | |

| Citrix Systems, Inc. | 75 | 9 | |

| Cloudflare, Inc. Class A(1) | 259 | 13 | |

| Cognex Corp. | 166 | 11 | |

| Crowdstrike Holdings, Inc. Class A(1) | 72 | 9 | |

| Dassault Systemes SE | 319 | 54 | |

| Datadog, Inc. Class A(1) | 111 | 10 | |

| DocuSign, Inc.(1) | 49 | 10 | |

| Dolby Laboratories, Inc. Class A | 156 | 12 | |

| DSP Group, Inc.(1) | 797 | 11 | |

| EPAM Systems, Inc.(1) | 32 | 10 | |

| F5 Networks, Inc.(1) | 86 | 11 | |

| Fair Isaac Corp.(1) | 24 | 9 | |

| Fastly, Inc. Class A(1) | 109 | 7 | |

| Fitbit, Inc. Class A(1) | 1,608 | 11 | |

| Five9, Inc.(1) | 82 | 12 | |

| Guidewire Software, Inc.(1) | 97 | 9 | |

| Infineon Technologies AG | 4,504 | 125 | |

| Jack Henry & Associates, Inc. | 63 | 9 | |

| LiveRamp Holdings, Inc.(1) | 198 | 13 | |

| Lumentum Holdings, Inc.(1) | 1,129 | 93 | |

| Manhattan Associates, Inc.(1) | 107 | 9 | |

| Maxim Integrated Products, Inc. | 157 | 11 | |

| MAXIMUS, Inc. | 150 | 10 | |

| Micron Technology, Inc.(1) | 3,612 | 182 | |

| Mitek Systems, Inc.(1) | 824 | 10 | |

| Monolithic Power Systems, Inc. | 40 | 13 | |

| Murata Manufacturing Co. Ltd. | 2,400 | 168 | |

| National Instruments Corp. | 296 | 9 | |

| Nemetschek SE | 799 | 58 | |

| NIC, Inc. | 509 | 11 | |

| Okta, Inc.(1) | 49 | 10 | |

| Pegasystems, Inc. | 85 | 10 | |

| Power Integrations, Inc. | 196 | 12 | |

| PTC, Inc.(1) | 120 | 10 | |

| Qorvo, Inc.(1) | 797 | 102 | |

| QUALCOMM, Inc. | 923 | 114 | |

| Qualys, Inc.(1) | 106 | 9 | |

| RingCentral, Inc. Class A(1) | 38 | 10 | |

| Samsung Electronics Co. Ltd. | 3,618 | 182 | |

| SAP SE | 380 | 41 | |

| SK Hynix, Inc. | 2,586 | 183 | |

| Skyworks Solutions, Inc. | 792 | 112 | |

| Smartsheet, Inc. Class A(1) | 214 | 11 | |

| SPS Commerce, Inc.(1) | 139 | 12 | |

| Synopsys, Inc.(1) | 50 | 11 | |

| Shares | Value | ||

| Information Technology—continued | |||

| Teradyne, Inc. | 135 | $ 12 | |

| Twilio Inc. Class A(1) | 43 | 12 | |

| Tyler Technologies, Inc.(1) | 30 | 12 | |

| Universal Display Corp. | 60 | 12 | |

| Varonis Systems, Inc.(1) | 89 | 10 | |

| VeriSign, Inc.(1) | 50 | 10 | |

| VirnetX Holding Corp. | 2,016 | 11 | |

| Visa, Inc. Class A | 346 | 63 | |

| Win Semiconductors Corp. | 10,000 | 109 | |

| Xilinx, Inc. | 103 | 12 | |

| Zscaler, Inc.(1) | 75 | 10 | |

| 2,468 | |||

| Materials—3.2% | |||

| Air Liquide SA | 370 | 54 | |

| Akzo Nobel NV | 599 | 58 | |

| Albemarle Corp. | 921 | 86 | |

| Anglo American PLC | 5,958 | 140 | |

| AptarGroup, Inc. | 90 | 10 | |

| ArcelorMittal SA(1) | 10,045 | 136 | |

| Balchem Corp. | 108 | 11 | |

| BHP Group PLC | 5,297 | 102 | |

| Fuchs Petrolub SE | 1,246 | 64 | |

| Glencore PLC(1) | 34,837 | 70 | |

| Johnson Matthey PLC | 4,086 | 114 | |

| Koninklijke DSM NV | 372 | 60 | |

| LG Chem Ltd. | 129 | 70 | |

| NewMarket Corp. | 29 | 10 | |

| Novagold Resources, Inc.(1) | 910 | 9 | |

| Royal Gold, Inc. | 84 | 10 | |

| Symrise AG | 429 | 53 | |

| Umicore SA | 1,710 | 66 | |

| UPM-Kymmene OYJ | 1,929 | 55 | |

| 1,178 | |||

| Real Estate—0.3% | |||

| Alexandria Real Estate Equities, Inc. | 402 | 61 | |

| Rexford Industrial Realty, Inc. | 1,435 | 66 | |

| 127 | |||

| Total Common Stocks (Identified Cost $12,740) | 13,610 | ||

| Exchange-Traded Fund—4.1% | |||

| Invesco DB Gold Fund | 27,646 | 1,518 | |

| Total Exchange-Traded Fund (Identified Cost $1,532) | 1,518 | ||

| Shares | Value | ||

| Purchased Options—1.5% | |||

| (See open purchased options schedule) | |||

| Total Purchased Options (Premiums paid $952) | $ 560 | ||

| Total Long-Term Investments—42.4% (Identified Cost $15,224) | 15,688 | ||

| Short-Term Investment—35.4% | |||

| Money Market Mutual Fund—35.4% | |||

| Dreyfus Government Cash Management Fund - Institutional Shares (seven-day effective yield 0.021%)(5) | 13,102,582 | 13,103 | |

| Total Short-Term Investment (Identified Cost $13,103) | 13,103 | ||

| TOTAL INVESTMENTS, BEFORE WRITTEN OPTIONS—77.8% (Identified Cost $28,327) | 28,791 | ||

| Written Options—(2.0)% | |||

| (See open written options schedule) | |||

| Total Written Options (Premiums received $809) | (750) | ||

| TOTAL INVESTMENTS, NET OF WRITTEN OPTIONS—75.8% (Identified Cost $27,518) | $28,041 | ||

| Other assets and liabilities, net—24.2% | 8,931 | ||

| NET ASSETS—100.0% | $36,972 | ||

| Abbreviations: | |

| ADR | American Depositary Receipt |

| LIBOR | London Interbank Offered Rate |

| PLC | Public Limited Company |

| QTR | Quarterly |

| TERM | Payment Frequency at Termination |

| Footnote Legend: | |

| (1) | Non-income producing. |

| (2) | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At October 31, 2020, these securities amounted to a value of $327 or 0.9% of net assets. |

| (3) | Security valued at fair value as determined in good faith by or under the direction of the Trustees. |

| (4) | Restricted security. |

| (5) | Shares of this fund are publicly offered, and its prospectus and annual report are publicly available. |

| Counterparties: | |

| BNP | BNP Paribas |

| CITI | Citibank |

| GS | Goldman Sachs & Co. |

| JPM | JPMorgan Chase Bank N.A. |

| ML | Merrill Lynch |

| Soc Gen | Societe Generale |

| Foreign Currencies: | |

| AUD | Australian Dollar |

| CHF | Swiss Franc |

| CNY | Chinese Yuan |

| EUR | Euro |

| GBP | United Kingdom Pound Sterling |

| INR | Indian Rupee |

| JPY | Japanese Yen |

| KRW | South Korean Won |

| MXN | Mexican Peso |

| SEK | Swedish Krona |

| SGD | Singapore Dollar |

| TWD | Taiwan Dollar |

| USD | United States Dollar |

| Country Weightings (Unaudited)† | |

| United States | 72% |

| France | 6 |

| Germany | 3 |

| Netherlands | 3 |

| United Kingdom | 3 |

| Ireland | 3 |

| Japan | 2 |

| Other | 8 |

| Total | 100% |

| † % of total investments, net of written options, as of October 31, 2020. | |

| Open purchased option contracts as of October 31, 2020 were as follows: | ||||||

| Description of Options | Counterparty | Number of Contracts | Contract Notional Amount | Strike Price(1) | Expiration Date | Value |

| Call Options | ||||||

| Euro Stoxx 50® Index | JPM | 12 | $ 390 | $ 3,250.00 | 12/18/20 | $ 3 |

| FTSE 100 Index | JPM | 60 | 3,720 | 6,200.00 | 12/18/20 | 14 |

| Euro Stoxx Banks | JPM | 926 | 2,778 | 60.00 | 12/18/20 | 70 |

| Swiss Market Index | JPM | 10 | 1,040 | 10,400.00 | 12/18/20 | 4 |

| Swiss Market Index | JPM | 3 | 315 | 10,500.00 | 12/18/20 | 1 |

| Russell 2000® Index | JPM | 16 | 2,720 | 1,700.00 | 01/15/21 | 43 |

| Russell 2000® Index | JPM | 4 | 620 | 1,550.00 | 11/20/20 | 19 |

| FTSE 100 Index | JPM | 12 | 750 | 6,250.00 | 11/20/20 | 1 |

| Euro Stoxx Banks | JPM | 686 | 2,315 | 67.50 | 12/18/20 | 14 |

| Euro Stoxx 50® Index | JPM | 28 | 959 | 3,425.00 | 11/20/20 | — (2) |

| Euro Stoxx 50® Index | JPM | 12 | 390 | 3,250.00 | 01/15/21 | 4 |

| Euro Stoxx Banks | JPM | 926 | 2,778 | 60.00 | 11/20/20 | 32 |

| Euro Stoxx Banks | JPM | 116 | 435 | 75.00 | 11/20/20 | — (2) |

| Swiss Market Index | JPM | 4 | 412 | 10,300.00 | 11/20/20 | 1 |

| Euro Stoxx Banks | JPM | 116 | 450 | 77.50 | 12/18/20 | — (2) |

| Euro Stoxx Banks | JPM | 33 | 89 | 54.00 | 12/18/20 | 7 |

| Swiss Market Index | JPM | 3 | 312 | 10,400.00 | 01/15/21 | 2 |

| Put Options | ||||||

| Euro Stoxx 50® Index | JPM | 50 | 1,500 | 3,000.00 | 12/18/20 | 86 |

| S&P 500® Index | JPM | 3 | 1,005 | 3,350.00 | 12/18/20 | 57 |

| S&P 500® Index | JPM | 3 | 1,020 | 3,400.00 | 11/20/20 | 51 |

| MSCI Emerging Markets Index | JPM | 3 | 324 | 1,080.00 | 12/18/20 | 10 |

| Euro Stoxx 50® Index | JPM | 38 | 988 | 2,600.00 | 11/20/20 | 7 |

| Euro Stoxx 50® Index | JPM | 39 | 985 | 2,525.00 | 12/18/20 | 14 |

| S&P 500® Index | JPM | 3 | 1,038 | 3,460.00 | 01/15/21 | 81 |

| MSCI Emerging Markets Index | JPM | 3 | 324 | 1,080.00 | 11/20/20 | 7 |

| S&P 500® Index | JPM | 4 | 1,070 | 2,675.00 | 11/13/20 | 3 |

| S&P 500® Index | JPM | 4 | 1,110 | 2,775.00 | 11/27/20 | 9 |

| MSCI Emerging Markets Index | JPM | 3 | 339 | 1,130.00 | 01/15/21 | 20 |

| Total | $ 560 | |||||

| Footnote Legend: | |

| (1) | Strike price not reported in thousands. |

| (2) | Amount is less than $500. |

| Open written option contracts as of October 31, 2020 were as follows: | ||||||

| Description of Options | Counterparty | Number of Contracts | Contract Notional Amount | Strike Price(1) | Expiration Date | Value |

| Call Options | ||||||

| Euro Stoxx 50® Index | JPM | 12 | $ 420 | $ 3,500.00 | 01/15/21 | $ (1) |

| Euro Stoxx 50® Index | JPM | 12 | 420 | 3,500.00 | 12/18/20 | (—) (2) |

| FTSE 100 Index | JPM | 60 | 3,780 | 6,300.00 | 12/18/20 | (8) |

| Swiss Market Index | JPM | 3 | 330 | 11,000.00 | 12/18/20 | (—) (2) |

| DJ Euro Stoxx Banks | JPM | 686 | 2,401 | 70.00 | 12/18/20 | (10) |

| MSCI Emerging Markets Index | JPM | 3 | 354 | 1,180.00 | 12/18/20 | (4) |

| Russell 2000® Index | JPM | 16 | 2,800 | 1,750.00 | 01/15/21 | (23) |

| Russell 2000® Index | JPM | 4 | 660 | 1,650.00 | 11/20/20 | (6) |

| DJ Euro Stoxx Banks | JPM | 845 | 2,640 | 62.50 | 12/18/20 | (44) |

| S&P 500® Index | JPM | 4 | 1,428 | 3,570.00 | 11/20/20 | (2) |

| MSCI Emerging Markets Index | JPM | 3 | 351 | 1,170.00 | 11/20/20 | (2) |

| DJ Euro Stoxx Banks | JPM | 926 | 2,894 | 62.50 | 11/20/20 | (19) |

| Swiss Market Index | JPM | 4 | 428 | 10,700.00 | 11/20/20 | (—) (2) |

| S&P 500® Index | JPM | 4 | 1,480 | 3,700.00 | 11/13/20 | (—) (2) |

| MSCI Emerging Markets Index | JPM | 3 | 366 | 1,220.00 | 01/15/21 | (3) |

| Swiss Market Index | JPM | 3 | 324 | 10,800.00 | 01/15/21 | (1) |

| Put Options | ||||||

| Euro Stoxx 50® Index | JPM | 62 | 1,736 | 2,800.00 | 12/18/20 | (56) |

| FTSE 100 Index | JPM | 5 | 298 | 5,950.00 | 12/18/20 | (29) |

| Swiss Market Index | JPM | 10 | 1,040 | 10,400.00 | 12/18/20 | (98) |

| S&P 500® Index | JPM | 3 | 945 | 3,150.00 | 12/18/20 | (32) |

| Swiss Market Index | JPM | 2 | 194 | 9,700.00 | 12/18/20 | (9) |

| S&P 500® Index | JPM | 3 | 960 | 3,200.00 | 11/20/20 | (25) |

| Russell 2000® Index | JPM | 4 | 608 | 1,520.00 | 01/15/21 | (38) |

| Russell 2000® Index | JPM | 2 | 310 | 1,550.00 | 11/20/20 | (13) |

| DJ Euro Stoxx Banks | JPM | 116 | 319 | 55.00 | 12/18/20 | (30) |

| FTSE 100 Index | JPM | 6 | 339 | 5,650.00 | 11/20/20 | (15) |

| Euro Stoxx 50® Index | JPM | 14 | 441 | 3,150.00 | 11/20/20 | (34) |

| MSCI Emerging Markets Index | JPM | 3 | 294 | 980.00 | 12/18/20 | (4) |

| DJ Euro Stoxx Banks | JPM | 179 | 559 | 62.50 | 12/18/20 | (104) |

| S&P 500® Index | JPM | 3 | 978 | 3,260.00 | 01/15/21 | (55) |

| Euro Stoxx 50® Index | JPM | 12 | 360 | 3,000.00 | 01/15/21 | (24) |

| MSCI Emerging Markets Index | JPM | 3 | 297 | 990.00 | 11/20/20 | (2) |

| DJ Euro Stoxx Banks | JPM | 116 | 319 | 55.00 | 11/20/20 | (23) |

| Swiss Market Index | JPM | 2 | 192 | 9,600.00 | 11/20/20 | (6) |

| DJ Euro Stoxx Banks | JPM | 33 | 89 | 54.00 | 12/18/20 | (7) |

| MSCI Emerging Markets Index | JPM | 3 | 324 | 1,080.00 | 01/15/21 | (13) |

| Swiss Market Index | JPM | 2 | 194 | 9,700.00 | 01/15/21 | (10) |

| Total | $(750) | |||||

| Footnote Legend: | |

| (1) | Strike price not reported in thousands. |

| (2) | Amount is less than $500. |

| Futures contracts as of October 31, 2020 were as follows: | ||||

| Issue | Expiration | Contracts Purchased/(Sold) | Notional Value | Value/Unrealized Appreciation (Depreciation) |

| TOPIX Index Future | December 2020 | (7) | $ (1,052) | $ 15 |

| Euro Stoxx 50® Future | December 2020 | (28) | (965) | 96 |

| MSCI All Country World Index Future | December 2020 | (39) | (1,091) | 33 |

| MSCI Emerging Markets Index Future | December 2020 | 19 | 1,047 | 14 |

| MSCI World Index Future | December 2020 | (31) | (2,116) | 91 |

| MSCI World Industrials Future | December 2020 | 5 | 381 | (25) |

| MSCI World Industrials Future | December 2020 | (10) | (367) | 13 |

| Russell 2000® Future | December 2020 | (34) | (2,612) | (83) |

| S&P 500® Index E-Mini Future | December 2020 | 13 | 2,122 | (42) |

| Stoxx ® Europe Mid 600 Index Future | December 2020 | (87) | (1,731) | 139 |

| 10 Year U.S. Treasury Note Future | December 2020 | 131 | 18,107 | (121) |

| S&P 500® Annual Dividend Index Future | December 2021 | 15 | 195 | 10 |

| S&P 500® Annual Dividend Index Future | December 2022 | 15 | 190 | 1 |

| Total | $ 141 | |||

| Forward foreign currency exchange contracts as of October 31, 2020 were as follows: | ||||||||

| Currency Purchased | Value (1) | Currency Sold | Value (1) | Counterparty | Settlement Date | Unrealized Appreciation | Unrealized (Depreciation) | |

| AUD (2) | 722 | USD | 529 | CITI | 11/12/20 | $ — | $(21) | |

| AUD (2) | 479 | USD | 345 | JPM | 11/12/20 | — | (8) | |

| AUD (2) | 83 | USD | 60 | ML | 11/12/20 | — | (2) | |

| EUR (2) | 371 | USD | 439 | BNP | 11/12/20 | — | (7) | |

| EUR (2) | 505 | USD | 600 | CITI | 11/12/20 | — | (11) | |

| EUR (2) | 1,956 | USD | 2,309 | JPM | 11/12/20 | — | (30) | |

| EUR (2) | 422 | USD | 501 | Soc Gen | 11/12/20 | — | (8) | |

| GBP (2) | 92 | USD | 122 | Soc Gen | 11/12/20 | — | (3) | |

| JPY (2) | 407,567 | USD | 3,859 | JPM | 11/12/20 | 35 | — | |

| KRW (2) | 543,094 | USD | 461 | CITI | 11/12/20 | 17 | — | |

| MXN (2) | 33,490 | USD | 1,544 | ML | 01/14/21 | 22 | — | |

| SGD (2) | 627 | USD | 461 | CITI | 11/12/20 | — | (2) | |

| SGD (2) | 312 | USD | 228 | JPM | 11/12/20 | — (3) | — | |

| SGD (2) | 158 | USD | 115 | ML | 11/12/20 | 1 | — | |

| SGD (2) | 154 | USD | 113 | Soc Gen | 11/12/20 | — | (—) (3) | |

| TWD (2) | 13,470 | USD | 468 | GS | 12/11/20 | 3 | — | |

| USD (2) | 922 | AUD | 1,285 | ML | 11/12/20 | 19 | — | |

| USD (2) | 90 | CHF | 82 | JPM | 11/12/20 | — (3) | — | |

| USD (2) | 327 | EUR | 276 | BNP | 11/12/20 | 5 | — | |

| USD (2) | 125 | EUR | 106 | GS | 11/12/20 | 2 | — | |

| USD (2) | 1,692 | EUR | 1,434 | JPM | 11/12/20 | 21 | — | |

| USD (2) | 169 | EUR | 143 | ML | 11/12/20 | 3 | — | |

| USD (2) | 41 | GBP | 31 | BNP | 11/12/20 | — (3) | — | |

| USD (2) | 1,112 | GBP | 850 | JPM | 11/12/20 | 11 | — | |

| USD (2) | 48 | INR | 3,639 | BNP | 11/12/20 | — | (1) | |

| USD (2) | 100 | JPY | 10,461 | CITI | 11/12/20 | — | (—) (3) | |

| USD (2) | 375 | JPY | 39,603 | JPM | 11/12/20 | — | (4) | |

| USD (2) | 211 | KRW | 242,697 | CITI | 11/12/20 | — | (3) | |

| USD (2) | 636 | KRW | 756,094 | ML | 11/12/20 | — | (31) | |

| USD (2) | 64 | KRW | 76,075 | Soc Gen | 11/12/20 | — | (3) | |

| USD (2) | 90 | SEK | 784 | JPM | 11/12/20 | 2 | — | |

| USD (2) | 910 | SGD | 1,250 | JPM | 11/12/20 | — | (5) | |

| USD (2) | 105 | TWD | 3,064 | BNP | 11/12/20 | — | (2) | |

| USD (2) | 463 | TWD | 13,470 | BNP | 12/11/20 | — | (8) | |

| USD (2) | 3,148 | EUR | 2,664 | CITI | 01/20/21 | 39 | — | |

| Total | $180 | $(149) | ||||||

| Footnote Legend: | |

| (1) | Reported in thousands. |

| (2) | Non deliverable forward. See Note 3b. |

| (3) | Amount is less than $500. |

| Centrally Cleared credit default swaps - sell protection(1) outstanding as of October 31, 2020 was as follows: | |||||||||||||

| Reference Entity | Payment Frequency | Counterparty | Fixed Rate | Expiration Date | Notional Amount(2) | Value | Premiums Paid (Received) | Unrealized Appreciation | Unrealized (Depreciation) | ||||

| iTraxx Europe | QTR | JPM | 5.000% | 12/20/25 | 4,304 | EUR | $332 | $405 | $— | $(73) | |||

| CDX North American High Yield Index | QTR | JPM | 5.000% | 12/20/25 | 5,469 | USD | 222 | 241 | — | (19) | |||

| Total | $554 | $646 | $— | $(92) | |||||||||

| Footnote Legend: | |

| (1) | If the Fund is a seller of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) pay to the buyer of protection an amount equal to the notional amount of the swap and take delivery of the referenced obligation or underlying investments comprising the referenced index or (ii) pay a net settlement amount in the form of cash or investments equal to the notional amount of the swap less the recovery value of the referenced obligation or underlying investments comprising the referenced index. |

| (2) | The maximum potential amount the Fund could be required to pay as a seller of credit protection or receive as a buyer of credit protection if a credit event occurs as defined under the terms of that particular swap agreement. |

| Centrally cleared inflation swaps outstanding as of October 31, 2020 were as follows: | |||||||||||||

| Fixed Rate | Floating Rate | Payment Frequency | Counterparty | Expiration Date | Notional Amount | Value | Premiums Paid (Received) | Unrealized Appreciation | Unrealized Depreciation | ||||

| 1.807% (1) | 1-Month-USCPI | TERM | JPM | 07/28/50 | 145 | USD | $17 | $— | $17 | $— | |||

| 1.828% (1) | 1-Month-USCPI | TERM | JPM | 07/28/50 | 144 | USD | 16 | — | 16 | — | |||

| 1.810% (1) | 1-Month-USCPI | TERM | JPM | 07/29/50 | 144 | USD | 16 | — | 16 | — | |||

| 2.087% (1) | 1-Month-USCPI | TERM | JPM | 10/26/50 | 525 | USD | (2) | — | — | (2) | |||

| Total | $47 | $— | $49 | $ (2) | |||||||||

| Footnote Legend: | |

| (1) | Fund pays the fixed rate and receives the floating rate. |

| Centrally cleared interest rate swaps outstanding as of October 31, 2020 were as follows: | |||||||||||||

| Fixed Rate | Floating Rate | Payment Frequency | Counterparty | Expiration Date | Notional Amount | Value | Premiums Paid (Received) | Unrealized Appreciation | Unrealized Depreciation | ||||

| 2.880% (1) | China Fixing Repo Rates 7 Days | TERM | JPM | 12/16/25 | 13,044 | CNY | $25 | $— | $25 | $— | |||

| 2.883% (1) | China Fixing Repo Rates 7 Days | TERM | JPM | 12/16/25 | 15,361 | CNY | 29 | — | 29 | — | |||

| 2.875% (1) | China Fixing Repo Rates 7 Days | TERM | JPM | 12/16/25 | 9,492 | CNY | 18 | — | 18 | — | |||

| 2.825% (1) | China Fixing Repo Rates 7 Days | TERM | JPM | 12/16/25 | 15,576 | CNY | 24 | — | 24 | — | |||

| Total | $96 | $— | $96 | $— | |||||||||

| Footnote Legend: | |

| (1) | Fund pays the floating rate and receives the fixed rate. |

| Over-the-counter variance swaps outstanding as of October 31, 2020 were as follows: | |||||||||||||

| Referenced Entity | Strike Price | Payment Frequency | Counterparty | Expiration Date | Notional Amount | Value | Premiums Paid (Received) | Unrealized Appreciation | Unrealized Depreciation | ||||

| S&P 500® Composite Stock Price Index(1) | $29.70 | TERM | GS | 06/18/21 | 41 | USD | $(150) | $— | $— | $(150) | |||

| S&P 500® Composite Stock Price Index(2) | 29.70 | TERM | GS | 01/15/21 | 16 | USD | 78 | — | 78 | — | |||

| Total | $ (72) | $— | $78 | $(150) | |||||||||

| Footnote Legend: | |

| (1) | Fund pays the fixed strike price and receives the variance payment. |

| (2) | Fund pays the variance payment and receives the fixed strike price. |

| Over-the-counter total return swaps outstanding as of October 31, 2020 were as follows: | |||||||||||||

| Referenced Entity | Floating Rate(1) | Payment Frequency | Counterparty | Expiration Date | Notional Amount | Value | Premiums Paid (Received) | Unrealized Appreciation | Unrealized Depreciation | ||||

| CenturyLink, Inc. | 1-Month LIBOR | Monthly | Soc Gen | 01/13/21 | 33 | USD | $ 13 | $— | $ 13 | $ — | |||

| Walt Disney Co. | 1-Month LIBOR | Monthly | Soc Gen | 01/13/21 | 38 | USD | 6 | — | 6 | — | |||

| Fox Corp. | 1-Month LIBOR | Monthly | Soc Gen | 01/13/21 | 36 | USD | 11 | — | 11 | — | |||

| Netflix, Inc. | 1-Month LIBOR | Monthly | Soc Gen | 01/13/21 | 39 | USD | (16) | — | — | (16) | |||

| AT&T, Inc. | 1-Month LIBOR | Monthly | Soc Gen | 01/13/21 | 73 | USD | 21 | — | 21 | — | |||

| Verizon Communications, Inc. | 1-Month LIBOR | Monthly | Soc Gen | 01/13/21 | 76 | USD | 2 | — | 2 | — | |||

| ViacomCBS, Inc. | 1-Month LIBOR | Monthly | Soc Gen | 01/13/21 | 37 | USD | 11 | — | 11 | — | |||

| Discovery, Inc. | 1-Month LIBOR | Monthly | Soc Gen | 01/13/21 | 36 | USD | 14 | — | 14 | — | |||

| MSCI EMU Net Total Return EUR Index | 1-Month LIBOR | Monthly | ML | 07/13/21 | 1,234 | EUR | 116 | — | 116 | — | |||

| MSCI EMU Net Total Return EUR Index | 1-Month LIBOR | Monthly | ML | 07/13/21 | 226 | EUR | 21 | — | 21 | — | |||

| MSCI World Industrials Net Total Return USD Index | 1-Month LIBOR | Monthly | Soc Gen | 09/10/21 | 749 | USD | 44 | — | 44 | — | |||

| MSCI EMU Net Total Return EUR Index | 1-Month LIBOR | Monthly | ML | 07/13/21 | 413 | EUR | 39 | — | 39 | — | |||

| CenturyLink, Inc. | 1-Month LIBOR | Monthly | ML | 01/13/21 | 39 | USD | 5 | — | 5 | — | |||

| AT&T, Inc. | 1-Month LIBOR | Monthly | ML | 01/13/21 | 97 | USD | 3 | — | 3 | — | |||

| Discovery, Inc. | 1-Month LIBOR | Monthly | ML | 01/13/21 | 50 | USD | 2 | — | 2 | — | |||

| Fox Corp. | 1-Month LIBOR | Monthly | ML | 01/13/21 | 48 | USD | 1 | — | 1 | — | |||

| ViacomCBS, Inc. | 1-Month LIBOR | Monthly | ML | 01/13/21 | 49 | USD | 1 | — | 1 | — | |||

| Verizon Communications, Inc. | 1-Month LIBOR | Monthly | ML | 01/13/21 | 75 | USD | 1 | — | 1 | — | |||

| Discovery, Inc. | 1-Month LIBOR | Monthly | ML | 01/13/21 | 42 | USD | 2 | — | 2 | — | |||

| Netflix, Inc. | 1-Month LIBOR | Monthly | ML | 01/13/21 | 14 | USD | — (2) | — | — (2) | — | |||

| Total | $ 297 | $— | $ 313 | $(16) | |||||||||

| Footnote Legend: | |

| (1) | The Fund pays the floating rate (+/- a spread) and receives the total return of the reference entity. |

| (2) | Amount is less than $500. |

| Total Value at October 31, 2020 | Level 1 Quoted Prices | Level 2 Significant Observable Inputs | |||

| Assets: | |||||

| Equity Securities: | |||||

| Common Stocks | $13,610 | $12,420 | $1,190 | ||

| Exchange-Traded Fund | 1,518 | 1,518 | — | ||

| Money Market Mutual Fund | 13,103 | 13,103 | — | ||

| Other Financial Instruments: | |||||

| Purchased Options | 560 | 399 | 161 | ||

| Futures Contracts | 412 | 412 | — | ||

| Forward Foreign Currency Exchange Contracts | 180 | — | 180 | ||

| Centrally Cleared Inflation Swaps | 49 | — | 49 | ||

| Centrally Cleared Interest Rate Swaps | 96 | — | 96 | ||

| Over-the-Counter Total Return Swaps | 313 | — | 313 | ||

| Over-the-Counter Variance swaps | 78 | — | 78 | ||

| Centrally Cleared Credit Default Swap | 554 | — | 554 | ||

| Total Assets | 30,473 | 27,852 | 2,621 | ||

| Liabilities: | |||||

| Other Financial Instruments: | |||||

| Written Options | (750) | (723) | (27) | ||

| Futures Contracts | (271) | (271) | — | ||

| Forward Foreign Currency Exchange Contracts | (149) | — | (149) | ||

| Centrally Cleared Inflation Swaps | (2) | — | (2) | ||

| Over-the-Counter Variance swaps | (150) | — | (150) | ||

| Over-the-Counter Total Return Swaps | (16) | — | (16) | ||

| Total Liabilities | (1,338) | (994) | (344) | ||

| Total Investments | $29,135 | $26,858 | $2,277 |

October 31, 2020

| Shares | Value | ||

| Common Stocks & MLP Interests—99.2% | |||

| Diversified—27.9% | |||

| Energy Transfer LP | 34,219 | $ 176 | |

| Enterprise Products Partners LP | 17,285 | 286 | |

| Keyera Corp. | 9,120 | 129 | |

| Kinder Morgan, Inc. | 20,640 | 246 | |

| MPLX LP | 10,321 | 178 | |

| ONEOK, Inc. | 6,085 | 177 | |

| Pembina Pipeline Corp. | 6,440 | 135 | |

| 1,327 | |||

| Downstream/Other—16.5% | |||

| Cheniere Energy, Inc.(1) | 8,217 | 393 | |

| Enviva Partners LP | 1,500 | 64 | |

| GasLog Ltd. | 15,840 | 38 | |

| Golar LNG Ltd.(1) | 10,340 | 78 | |

| Marathon Petroleum Corp. | 3,750 | 111 | |

| Phillips 66 | 2,150 | 100 | |

| 784 | |||

| Electric, LDC & Power—9.1% | |||

| CenterPoint Energy, Inc. | 6,000 | 127 | |

| NextEra Energy Partners LP | 2,510 | 158 | |

| Sempra Energy | 1,200 | 150 | |

| 435 | |||

| Gathering/Processing—18.8% | |||

| DCP Midstream LP | 5,600 | 72 | |

| Enable Midstream Partners LP | 11,500 | 51 | |

| Equitrans Midstream Corp. | 19,000 | 138 | |

| Hess Midstream LP Class A | 11,590 | 198 | |

| Rattler Midstream LP | 19,870 | 117 | |

| Shares | Value | ||

| Gathering/Processing—continued | |||

| Targa Resources Corp. | 19,900 | $ 319 | |

| 895 | |||

| Natural Gas Pipelines—11.2% | |||

| TC Energy Corp. | 4,850 | 191 | |

| Williams Cos., Inc. (The) | 17,970 | 345 | |

| 536 | |||

| Petroleum Transportation & Storage—14.4% | |||

| Enbridge, Inc. | 5,500 | 152 | |

| Genesis Energy LP | 13,565 | 57 | |

| Magellan Midstream Partners LP | 5,770 | 205 | |

| Phillips 66 Partners LP | 2,000 | 47 | |

| Plains GP Holdings LP Class A | 35,434 | 226 | |

| 687 | |||

| Upstream—1.3% | |||

| EQT Corp. | 4,000 | 60 | |

| Total Common Stocks & MLP Interests (Identified Cost $6,487) | 4,724 | ||

| Total Long-Term Investments—99.2% (Identified Cost $6,487) | 4,724 | ||

| TOTAL INVESTMENTS—99.2% (Identified Cost $6,487) | $4,724 | ||

| Other assets and liabilities, net—0.8% | 36 | ||

| NET ASSETS—100.0% | $4,760 | ||

| Abbreviations: | |

| LP | Limited Partnership |