Diversified Real Asset Income Fund (DRA) Inactive

Filed: 8 Aug 16, 12:00am

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-22936 |

Diversified Real Asset Income Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: May 31

Date of reporting period: May 31, 2016

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

| ||

| Closed-End Funds |

| Nuveen | ||

| Closed-End Funds |

| Annual Report May 31, 2016

| |||||

| DRA | ||||||

| Diversified Real Asset Income Fund | ||||||

| ||||||||||||

| ||||||||||||

Life is Complex | ||||||||||||

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish. | ||||||||||||

| Free e-Reports right to your e-mail! | ||

www.investordelivery.com If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account. | ||

www.nuveen.com/accountaccess If you receive your Nuveen Fund distributions and statements directly from Nuveen. | ||

| ||||||

of Contents

| 4 | ||||

| 9 | ||||

| 10 | ||||

| 12 | ||||

| 14 | ||||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| 27 | ||||

| 28 | ||||

| 29 | ||||

| 30 | ||||

| 32 | ||||

| 34 | ||||

| 46 | ||||

| 47 | ||||

| 49 | ||||

| 50 | ||||

| NUVEEN | 3 |

Comments

Diversified Real Asset Income Fund (DRA) (the Fund) is a closed-end fund managed by Nuveen Fund Advisors, LLC (NFAL) and sub-advised by Nuveen Asset Management, LLC (NAM). The Fund is sub-advised by NAM using its real asset income strategy, and its portfolio managers are John G. Wenker, Jay L. Rosenberg, Jeffrey T. Schmitz, CFA, Brenda A. Langenfeld, CFA, and Tryg T. Sarsland. David A. Yale was also a part of DRA’s management team until February 29, 2016, when he retired from NAM.

Here the portfolio management team reviews economic and market conditions, key investment strategies and the Fund’s performance for the twelve-month reporting period ended May 31, 2016.

What factors affected the U.S. economy and financial markets during the twelve-month reporting period ended May 31, 2016?

Over the twelve-month period, U.S. economic data continued to point to subdued growth, rising employment and tame inflation. Economic activity has continued to hover around a 2% annualized growth rate since the end of the Great Recession in 2009, as measured by real gross domestic product (GDP), which is the value of the goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. For the first quarter of 2016, real GDP increased at an annual rate of 0.8%, as reported by the “second” estimate of the Bureau of Economic Analysis, down from 1.4% in the fourth quarter of 2015.

The labor and housing markets were among the bright spots in the economy during the reporting period, as both showed steady improvement. As reported by the Bureau of Labor Statistics, the unemployment rate fell to 4.7% in May 2016 from 5.5% in May 2015, and job gains averaged slightly above 200,000 per month for the past twelve months. The S&P/Case-Shiller U.S. National Home Price Index, which covers all nine U.S. census divisions, recorded a 5.0% annual gain in April 2016 (most recent data available at the time this report was prepared). The 10-City and 20-City Composites reported year-over-year increases of 4.7% and 5.4%, respectively.

Consumers, whose purchases comprise the largest component of the U.S. economy, benefited from lower gasoline prices and an improving jobs market but didn’t necessarily spend more. Pessimism about the economy’s future and lackluster wage growth likely contributed to consumers’ somewhat muted spending. Lower energy prices and tepid wage growth also weighed on inflation during this reporting period. The Consumer Price Index CPI rose 1.0% over the twelve-month period ended May 2016 on a seasonally adjusted basis, as reported by the U.S. Bureau of Labor Statistics. The core CPI (which excludes food and energy) increased 2.2% during the same period, slightly above the Fed’s unofficial longer term inflation objective of 2.0%.

Business investment was also rather restrained. Corporate earnings growth slowed during 2015, reflecting an array of factors ranging from weakening demand amid sluggish U.S. and global growth to the impact of falling commodity prices and a strong U.S. dollar. Energy, materials and industrials companies were hit particularly hard by the downturn in

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Fund disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service (Moody’s), Inc. or Fitch, Inc. (Fitch). Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

| 4 | NUVEEN |

natural resource prices, as well as the expectation of rising interest rates, which would make their debts more costly to service. With demand waning, companies, especially in the health care and technology sectors, looked to consolidations with rivals as a way to boost revenues. Merger and acquisition deals, both in the U.S. and globally, reached record levels in the calendar year 2015.

With the current expansion on solid footing, the U.S. Federal Reserve (Fed) prepared to raise one of its main interest rates, which had been held near zero since December 2008 to help stimulate the economy. After delaying the rate change for most of 2015 because of a weak global economic growth outlook, the Fed announced in December 2015 that it would raise the fed funds target rate by 0.25%. The news was widely expected and therefore had a relatively muted impact on the financial markets.

Although the Fed continued to emphasize future rate increases would be gradual, investors worried about the pace. This, along with uncertainties about the global macroeconomic backdrop, another downdraft in oil prices and a spike in stock market volatility triggered significant losses across assets that carry more risk and fueled demand for “safe haven” assets such as Treasury bonds and gold from January through mid-February. However, fear began to subside in March, propelling assets that carry more risk higher. The Fed held the rate steady at both the January and March policy meetings, as well as lowered its expectations to two rate increases in 2016 from four. Also boosting investor confidence were reassuring statements from the European Central Bank (ECB), some positive economic data in the U.S. and abroad, a retreat in the U.S. dollar and an oil price rally. At its April meeting, the Fed indicated its readiness to raise its benchmark rate at the next policy meeting in June. However, a very disappointing jobs growth report in May and the significant uncertainty surrounding the U.K.’s referendum on whether Britain should leave the European Union (EU), colloquially known as “Brexit,” dampened the Fed’s outlook. These concerns led the Fed to again hold rates steady at its June meeting (after the close of this reporting period). Subsequent to the close of this reporting period, on June 23, 2016, the U.K. voted in favor of leaving the EU. The event triggered considerable market volatility, with a steep drop in the U.K. sterling, turbulence in global equity markets and a rotation into safe-haven assets such as gold, the U.S. dollar and U.S. Treasuries.

During the reporting period, three of the five “real asset” categories represented in DRA’s Custom Blended Index produced positive absolute returns. Both real estate segments were strong performers with the real estate investment trust (REIT) preferred benchmark for the Fund gaining 8.23%, as measured by the Wells Fargo Hybrid & Preferred Securities REIT Index, while the public commercial REIT sector advanced 4.29%, according to the FTSE EPRA/NAREIT Developed Index. Both real estate sectors substantially outperformed the broad global market MSCI World Index, which returned -3.96% over the same time frame. These segments were supported by positive commercial real estate fundamentals as well as interest rates that remained well contained as the U.S. Fed remained on hold after its December hike and the ECB embarked on additional monetary easing. The other preferred benchmark for the Fund, the Barclays Global Capital Securities Index, gained 1.81%. Meanwhile, global infrastructure equities fell -3.93%, as measured by the S&P Global Infrastructure Index. Much of the downfall occurred during the first half of the reporting period in the utility and energy sectors, which are both large components of the S&P Global Infrastructure Index. The dramatic decline in oil prices put pressure on pipeline and master limited partnership (MLP) companies in the energy sector, while increasing interest rates hampered the utility names. High yield bonds also took a step backward as spreads widened during the “risk-off” environment experienced in the first half of the reporting period, caused by the sustained downward movement in oil prices. The overall high yield market, as measured by the Barclays U.S. Corporate High Yield Bond Index, produced a -0.81 % return during the reporting period.

What key strategies were used to manage the Fund during this twelve-month reporting period ended May 31, 2016?

The Fund’s investment objective is a high level of current income and long-term capital appreciation. Since the Fund’s commencement of operations in 2014, the portfolio management team has been repositioning its assets to align DRA’s

| NUVEEN | 5 |

Portfolio Managers’ Comments (continued)

portfolio with NAM’s real asset income strategy. With this strategy, at least 80% of the Fund’s managed assets will be invested in a global portfolio of securities that provide investment exposure to real assets, focusing on infrastructure and REIT securities. The portfolio management team actively manages the Fund’s allocations among the infrastructure and real estate categories, with the flexibility to invest across the capital structure in any type of equity and debt security offered by a particular company, including common shares, preferred shares, corporate debt instruments and mortgage-backed securities. All of the Fund’s debt investments may be rated lower than investment grade (Ba1/BB+ or lower by S&P, Moody’s or Fitch), but no more than 10% of the Fund’s managed assets may be invested in securities rated CCC+/Caa1 or lower at any time. The Fund may also invest up to 75% of its managed assets in non-U.S. issuers. Our goal is to have the Fund’s portfolio fairly equally balanced between U.S. and non-U.S. exposure, although this allocation may change based on market conditions. We may also opportunistically write (sell) call options primarily on securities issued by real asset related companies, seeking to enhance the Fund’s risk-adjusted total returns over time.

In addition, we typically use leverage as part of the Fund’s management strategy, which we are currently doing through the use of bank borrowings. The Fund utilizes credit facilities that charge either one-month LIBOR plus a spread, or three-month LIBOR plus a spread. The borrowed proceeds are used to invest in more securities that the Fund would typically hold. Leverage is discussed in more detail in the Fund Leverage section of this report.

NAM’s real asset income strategy invests primarily in five security types: global infrastructure common stock, REIT common stock, global infrastructure preferred stock and hybrids, REIT preferred stock, and debt securities. The Fund’s primary benchmark is the Morgan Stanley Capital International (MSCI) World Index. The Fund’s comparative benchmark is a Custom Blended Index, which is an index NAM created to represent a model asset allocation for an income-oriented product providing investment exposure to real assets. Effective December 31, 2015, we changed the Custom Blended Index constituents to the following: 28% S&P Global Infrastructure Index, 21% FTSE EPRA/NAREIT Developed Index, 18% Wells Fargo Hybrid & Preferred Securities REIT Index, 15% Barclays Global Capital Securities Index and 18% Barclays U.S. Corporate High Yield Bond Index. The changes were made with the aim to more accurately reflect the investment team’s experience and expectations for the long-run strategy positioning and offer a more appropriate performance benchmark. Our real asset income strategy attempts to add value versus the benchmark in two ways: by re-allocating among the five main security types when we see pockets of value at differing times and, more importantly, through individual security selection.

Our security selection process starts with a screening process for securities across the real assets markets that provide higher yields. From the group of securities providing significant yields, we focus on owning those securities with the highest total return potential. Our process places a premium on finding securities with revenues that come from tangible assets with long-term concessions, contracts or leases, which are therefore capable of producing steady, predictable and recurring cash flows. We employ a bottom-up, fundamental approach to security selection and portfolio construction. We look for stable companies that demonstrate consistent and growing cash flow, strong balance sheets and histories of being good stewards of shareholder capital.

During the reporting period, we made further progress in repositioning the Fund with approximately 90% of the portfolio’s total assets realigned with the real asset income strategy as of May 31, 2016. As part of this repositioning, we have been selling holdings that we believe have lower yield and lower capital appreciation potential and buying assets that have more potential to achieve the Fund’s objectives, while also more equally balancing the Fund’s U.S. and non-U.S. exposure. This includes looking for ways to opportunistically monetize the Fund’s whole loan positions, but only when we are confident that we are achieving fair value for these assets.

In an effort to protect against potential increases in interest rates, we also sold (shorted) five-year U.S. Treasury futures contracts for part of the reporting period to hedge some of the duration, or interest rate sensitivity, of the bonds in the portfolio. However, rates for Treasury securities with maturities of five years and longer moved generally lower during the reporting period. Therefore, the hedge decreased in value on a mark-to-market basis, which was offset by higher prices of the underlying bonds resulting in a negligible impact on performance over the reporting period.

| 6 | NUVEEN |

How did the Fund perform during this twelve-month reporting period ended May 31, 2016?

The table in the Performance Overview and Holding Summaries section of this report provides total return performance for the Fund for the one-year and since inception periods ended May 31, 2016. For the twelve-month period reporting period ended May 31, 2016, the Fund’s total return at net asset value (NAV) outperformed both the MSCI World Index and its Custom Blended Index.

Our management team is still in the process of transitioning the Fund’s portfolio to our global real asset income strategy, making comparisons to its global, equity-oriented benchmarks somewhat less meaningful. That being said, the Fund exhibited strong performance during a generally difficult market environment for most asset classes, particularly international equities.

Much of the Fund’s outperformance during the reporting period was due to security selection within the equity universes of both global infrastructure and global real estate, with infrastructure equities responsible for the majority of the better-than-benchmark return. The story for the period revolved around declining oil prices and the effect they had on both equity and debt prices. Global oil markets continued to grapple with oversupply amidst the glut created as a result of the U.S. shale energy boom, which has led to very high domestic production. The inventory of crude oil in the U.S. is approximately 100 million barrels higher than it has averaged over the past five years, and while the total number of rigs is down more than 60% from the peak, production remains elevated due to efficiency gains. Our underweight position and security selection in pipeline equities was the most significant positive factor for the Fund as energy infrastructure sold off dramatically amid the softening global economic data and continued pressure on oil prices. We have positioned the Fund with an underweight in energy equities for nearly a year and a half, while also staying focused on higher-quality companies. Pipeline companies in the infrastructure index were down nearly 30% on a weighted basis during the reporting period, while our portfolio’s holdings fell less than 9%.

Relative to the Fund’s benchmark, the REIT common equity portion of the portfolio was also beneficial to returns as security selection within the group contributed positively. Generally speaking, real estate equities rallied for much of the reporting period. Within the portfolio, given our primary objective to provide a high level of income, domestic health care companies represented a sizeable allocation because of their superior yields relative to some of the higher growth sectors within real estate. Our holdings within the portfolio performed well during the reporting period; therefore, given our overweight in the area relative to benchmark, this positioning was the leading factor in the Fund’s REIT equity outperformance. The Fund also benefited from an overweight position in the net lease sector. This area of the REIT market turned in strong results as concerns around global growth led to a more sanguine outlook for interest rates, which benefited the sector’s longer duration leases in relative terms.

High yield debt was the Fund’s leading detractor during the reporting period relative to the benchmark. Throughout the reporting period, the performance of the high yield portfolio was hampered by heightened concerns for the energy sector and independent power producers. The significant drop in oil prices through mid-February 2016 was taken as a signal by the market that a global economic recession was imminent. Given the Fund’s mandate to invest in real asset companies, it will hold more infrastructure names than the broader high yield benchmark. As a result, approximately 4% of the portfolio was allocated to pipelines, which were adversely affected by the declining prices of oil and natural gas. While the debt of these companies held up much better than their equity prices, these holdings were still the leading area of underperformance within our high yield debt portfolio relative to the benchmark.

The credit performance of the Fund’s whole loan portfolio was relatively stable during the reporting period due to the continued strong performance of the commercial real estate sector. As of May 31, 2016, approximately 11% of the Fund’s net asset value remained in whole loans, which we are continuing to monetize. During the reporting period, twenty-eight loans were sold or paid off and two participating loans were settled. We used the proceeds from the whole loan sales and payoffs to provide liquidity for the tender offer noted below, and to partially pay down leverage and reallocate to the generally higher yielding real asset income strategy.

| NUVEEN | 7 |

Portfolio Managers’ Comments (continued)

In the real asset income portion of the portfolio, we reduced the Fund’s U.S. exposure slightly, keeping it roughly in line with what we expect over the long term. The change in geography was mostly due to our continued reduction to U.S. REIT equities. While real estate fundamentals remain supportive and many REITs are trading at discounts, we believe that growth within the sector is beginning to slow modestly, especially in some of the larger coastal markets such as New York City and San Francisco. In most major property sectors, building prices are also well past 2007 peak prices, which may indicate that REITs are a little later in their cycle. We reallocated the capital to the global infrastructure equity and preferred sectors, where we believe we can find commensurate income characteristics with similar-to-better total return potential. Our outlook for global growth is somewhat sanguine which, combined with very easy global monetary policy, should keep interest rates well contained. In turn, we believe this should benefit the higher-yielding and longer asset duration companies the Fund holds within infrastructure.

In the Fund’s high yield debt portfolio, our largest absolute exposure remained in pipeline companies, although we slightly reduced exposure to that group during the period. Real estate debt was the recipient of the bulk of the proceeds. As noted, the slowdown in cash flow growth and property price appreciation likely reduces potential total returns for REIT equities. However, given high occupancies, continued economic growth and supportive jobs numbers, we believe real estate companies will continue to have the ability to service their debt, making their bonds attractive on a relative basis. That being said, we continued to invest our high yield portfolio across the spectrum of real estate and infrastructure segments. We also looked for opportunities to rotate out of the more economically-sensitive areas of energy midstream and independent power producers and into more stable sectors such as health care real estate, data centers and waste.

Also, the Fund conducted a third and final tender offer to purchase up to 10% of its outstanding shares for cash at a price per share equal to 99% of NAV on the expiration date of December 1, 2015. The tender offer was oversubscribed, which meant that the Fund purchased 10% of its respective outstanding common shares on a pro-rata basis based on the number of shares tendered. Refer to the Share Information section of this report for more details.

| 8 | NUVEEN |

Leverage

IMPACT OF THE FUND’S LEVERAGE STRATEGY ON PERFORMANCE

One important factor impacting the return of the Fund relative to its benchmarks was the Fund’s utilization of leverage through the use of bank borrowings. The Fund uses leverage because our research has shown that, over time, leveraging provides opportunities for additional income and total return for shareholders. However, the use of leverage also can expose shareholders to additional volatility. For example, as the prices of securities held by the Fund decline, the negative impact of these valuation changes on NAV and shareholder total return is magnified by the use of leverage. Conversely, leverage may enhance returns during periods when the prices of securities held by the Fund generally are rising. During the reporting period, the income generated from the spread between the cost of borrowing and the yield from invested assets was positive. The Fund’s use of leverage had a positive impact on the performance of the Fund over the reporting period.

As of May 31, 2016, the Fund’s percentages of leverage are as shown in the accompanying table.

| DRA | ||||

Effective Leverage* | 28.87 | % | ||

Regulatory Leverage* | 28.87 | % | ||

| * | Effective leverage is the Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. During this reporting period, the Fund was not invested in any derivatives or other investments that resulted in economic leverage. Regulatory leverage consists of borrowings of the Fund. Both of these are part of the Fund’s capital structure. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

THE FUND’S REGULATORY LEVERAGE

Bank Borrowings

As noted above the Fund employs leverage through the use of bank borrowings. The Fund’s bank borrowing activities are as shown in the accompanying table.

| Current Reporting Period | Subsequent to the Close of the Reporting Period | |||||||||||||||||||||||||||||||

| Regulatory Leverage | June 1, 2015 | Draws | Paydowns | May 31, 2016 | Draws | Paydowns | July 27, 2016 | |||||||||||||||||||||||||

Bank Borrowings | $ | 170,300,000 | $ | — | $ | (34,000,000 | ) | $ | 136,300,000 | $ | — | $ | — | $ | 136,300,000 | |||||||||||||||||

Refer to Notes to Financial Statements, Note 8 – Borrowing Arrangements for further details.

THE FUND’S EFFECTIVE LEVERAGE

Total Return Swaps

Subsequent to the close of the reporting period, the Fund invested in total return swaps which modestly increased the overall effective leverage of the Fund. Under the terms of the swaps, the Fund receives the total return on an underlying basket of exchange-traded-funds (ETFs) in exchange for periodic interest payments.

| NUVEEN | 9 |

Information

DISTRIBUTION INFORMATION

The following information regarding the Fund’s distributions is current as of May 31, 2016, and may differ from previously issued distribution notifications.

The Fund has a cash flow-based distribution program. Under this program, the Fund seeks to maintain an attractive and stable regular distribution based on the Fund’s net cash flow received from its portfolio investments. Fund distributions are not intended to include expected portfolio appreciation; however, the Fund invests in securities that make payments which ultimately may be fully or partially treated as gains or return of capital for tax purposes. This tax treatment will generally “flow through” to the Fund’s distributions, but the specific tax treatment is often not known with certainty until after the end of the Fund’s tax year. As a result, regular distributions throughout the year are likely to be re-characterized for tax purposes as either long-term gains (both realized and unrealized), or as a non-taxable return of capital.

The figures in the table below provide the sources (for tax purposes) of the Fund’s distributions as of May 31, 2016. These sources include amounts attributable to realized gains and/or returns of capital. The information shown below is for the distributions paid on common shares for all prior months in the current fiscal year. These amounts should not be used for tax reporting purposes, and the distribution sources may differ for financial reporting than for tax reporting. The final determination of the tax characteristics of all distributions paid in 2016 will be made in early 2017 and reported to you on Form 1099-DIV. More details about the tax characteristics of the Fund’s distributions are available on www.nuveen.com/CEFdistributions.

Data as of May 31, 2016

Current Month | Fiscal YTD | |||||||||||||||||||||||||||

Estimated Percentage of Distributions | Estimated Per Share Amounts | |||||||||||||||||||||||||||

| Net Investment Income | Realized Gains | Return of Capital | Total Distributions | Net Investment Income | Realized Gains | Return of Capital | ||||||||||||||||||||||

100% | 0.0% | 0.0% | $ | 1.6450 | $ | 1.6450 | $ | 0.0000 | $ | 0.0000 | ||||||||||||||||||

The following table provides information regarding fund distributions and total return performance over various time periods. This information is intended to help you better understand whether fund returns for the specified time periods were sufficient to meet fund distributions.

Data as of May 31, 2016

| Annualized | Cumulative | |||||||||||||||||||||||

| Inception Date | Latest Monthly Per Share Distribution | Current Distribution on NAV | 1-Year Return on NAV | Since Inception Return on NAV | Calendar YTD Distributions on NAV | Calendar YTD Return on NAV | ||||||||||||||||||

9/8/2014 | $ | 0.1180 | 7.54 | % | 2.26 | % | 4.54 | % | 8.08 | % | 8.44 | % | ||||||||||||

| 10 | NUVEEN |

SHARE REPURCHASES

The Fund’s Board of Trustees has authorized the Fund to participate in Nuveen’s closed-end fund complex-wide share repurchase program. Under the share repurchase program, the Fund may repurchase annually up to 10% of its outstanding shares in open-market transactions at the Adviser’s discretion. The Fund is prohibited, however, from repurchasing its shares during periods when the Fund also has an outstanding tender offer (as described below).

As of May 31, 2016, and since the inception of the Fund’s repurchase program, the Fund has cumulatively repurchased and retired its outstanding shares as shown in the accompanying table.

| DRA | ||||

Shares cumulatively repurchased and retired | 622,500 | |||

Approximate number of shares authorized for repurchase | 2,025,000 | |||

During the current reporting period, the Fund repurchased and retired its shares at a weighted average price per share and a weighted average discount per share as shown in the accompanying table.

| DRA | ||||

Shares repurchased and retired | 496,500 | |||

Weighted average price per share repurchased and retired | $15.41 | |||

Weighted average discount per share repurchased and retired | 14.63 | % | ||

TENDER OFFER

The Fund’s Board of Trustees has authorized the Fund to conduct a series of up to three tender offers pursuant to which the Fund would offer to purchase up to 10% of the Fund’s outstanding shares for cash on a pro rata basis at a price per share equal to 99% of the NAV per common share, as determined as of the close of regular trading on the NYSE on the expiration date of the tender offer.

During the period September 8, 2014 (commencement of operations) through May 31, 2015, the Fund conducted two tender offers. On October 22, 2015, Nuveen announced the Fund’s third tender offer, which commenced on November 2, 2015 and expired on December 1, 2015. The tender offer was oversubscribed (55% of the outstanding shares were tendered), and therefore the Fund purchased 10% of its outstanding shares from participating shareholders on a pro-rata basis based on the number of shares properly tendered.

Refer to Notes to Financial Statements, Note 4 – Fund Shares, Tender Offers for further details.

OTHER SHARE INFORMATION

As of May 31, 2016, and during the current reporting period, the Fund’s share price was trading at a premium/(discount) to its NAV as shown in the accompanying table.

| DRA | ||||

NAV | $ | 18.77 | ||

Share price | $ | 16.19 | ||

Premium/(Discount) to NAV | (13.75 | )% | ||

12-month average premium/(discount) to NAV | (12.72 | )% | ||

| NUVEEN | 11 |

Considerations

Diversified Real Asset Income Fund (DRA)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value. Concentration in specific sectors may involve greater risk and volatility than more diversified investments: real estate investments may suffer due to economic downturns and changes in real estate values, rents, property taxes, interest rates and tax laws; infrastructure-related securities may face adverse economic, regulatory, political, and legal changes. Prices of equity securities may decline significantly over short or extended periods of time. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, derivatives risk, liquidity risk, and income risk. As interest rates rise, bond prices fall. Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. For these and other risks such as whole loan risk and foreign investment risk, see the Fund’s web page at www.nuveen.com/DRA.

| 12 | NUVEEN |

THIS PAGE INTENTIONALLY LEFT BLANK

| NUVEEN | 13 |

DRA

Diversified Real Asset Income Fund

Performance Overview and Holding Summaries as of May 31, 2016

Refer to the Glossary of Terms Used in this Report for further definitions of terms used in this section.

Average Annual Total Returns as of May 31, 2016

| Average Annual | ||||||||

| 1-Year | Since Inception | |||||||

| DRA at NAV | 2.26% | 4.54% | ||||||

| DRA at Share Price | 0.09% | 2.34% | ||||||

| MSCI World Index | (3.96)% | (0.37)% | ||||||

| Custom Blended Index (New Comparative Benchmark) | 1.57% | 1.62% | ||||||

| Custom Blended Index (Old Comparative Benchmark) | 3.21% | 3.25% | ||||||

As previously noted in the Portfolio Managers’ Comments section of this report, the Fund is in the process of transitioning its portfolio to a global real asset income strategy. Therefore, comparisons to the Fund’s global, equity-oriented benchmarks are less meaningful until the Fund’s transitioning is complete. The Fund’s goal over time will be to opportunistically reduce its whole loan exposure while also more equally balancing its U.S. and non-U.S. exposure. Effective December 31, 2015, the Custom Blended Index constituents were changed. The changes were made with the aim to more accurately reflect the investment team’s experience and expectations for the long-run strategy positioning and offer a more appropriate performance benchmark. The Fund maintains the MSCI World Index as its primary benchmark.

Since inception returns are from September 8, 2014. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

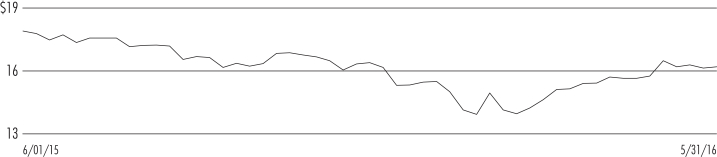

Share Price Performance — Weekly Closing Price

| 14 | NUVEEN |

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| Whole Loans | 10.7% | |||

| Corporate Notes | 2.4% | |||

| Other Fixed-Income Type Securities1 | 65.2% | |||

| Equity Type Securities2 | 57.1% | |||

Repurchase Agreements | 4.6% | |||

| Other Assets Less Liabilities | 0.6% | |||

| Net Assets Plus Borrowings | 140.6% | |||

| Borrowings | (40.6)% | |||

| Net Assets | 100% |

Portfolio Asset Allocation

(% of total investments, at value)

| Whole Loans | 7.6% | |||

| Corporate Notes | 1.7% | |||

| Other Fixed-Income Type Securities1 | 46.5% | |||

| Equity Type Securities2 | 40.9% | |||

Repurchase Agreements | 3.3% | |||

| Total | 100% |

Whole Loans and Industries

(% of total investments, at value)

| Real Estate Investment Trust | 35.2% | |||

Electric Utilities | 15.6% | |||

| Multi-Utilities | 8.1% | |||

| Whole Loans | 7.6% | |||

Oil, Gas & Consumable Fuels | 6.5% | |||

| Transportation Infrastructure | 4.1% | |||

Repurchase Agreements | 3.3% | |||

| Other | 19.6% | |||

| Total | 100% |

Whole Loan

State Concentration

(% of total whole loans, at value)

Washington | 21.2% | |||

Texas | 17.9% | |||

National | 16.2% | |||

Florida | 12.6% | |||

Oklahoma | 11.2% | |||

Arizona | 6.2% | |||

Other | 14.7% | |||

| Total | 100% |

Credit Quality

(% of total other fixed-income type securities, at value)1

| A | 1.8% | |||

| BBB | 29.0% | |||

| BB | 24.3% | |||

| B | 10.9% | |||

| CCC | 2.2% | |||

| N/R (not rated) | 31.8% | |||

| Total | 100% |

Country Allocation

(% of total investments, at value)

| United States | 65.1% | |||

Canada | 6.1% | |||

| United Kingdom | 5.4% | |||

Australia | 5.4% | |||

Singapore | 3.1% | |||

Hong Kong | 2.7% | |||

Italy | 2.4% | |||

| Other | 9.8% | |||

| Total | 100% |

| 1 | Includes convertible preferred, $25 par (or similar) retail preferred, convertible bonds, corporate bonds and $1,000 par (or similar) institutional preferred. |

| 2 | Includes common stocks, common stock rights and investment companies. |

| NUVEEN | 15 |

Meeting Report

The annual meeting of shareholders was held in the offices of Nuveen Investments on December 16, 2015 for DRA; at this meeting the shareholders were asked to elect Board Members.

| DRA | ||||

| Common Shares | ||||

Approval of the Board Members was reached as follows: | ||||

Roger A. Gibson | ||||

For | 16,064,312 | |||

Withhold | 683,311 | |||

Total | 16,747,623 | |||

Leonard W. Kedrowski | ||||

For | 16,033,784 | |||

Withhold | 713,839 | |||

Total | 16,747,623 | |||

Richard K. Riederer | ||||

For | 16,063,976 | |||

Withhold | 683,647 | |||

Total | 16,747,623 | |||

James M. Wade | ||||

For | 16,032,685 | |||

Withhold | 714,938 | |||

Total | 16,747,623 | |||

| 16 | NUVEEN |

Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

Diversified Real Asset Income Fund:

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations, of changes in net assets, and of cash flows and the financial highlights present fairly, in all material respects, the financial position of Diversified Real Asset Income Fund (hereinafter referred to as the “Fund”) at May 31, 2016, the results of its operations and its cash flows for the year then ended, and the changes in its net assets and the financial highlights for the year then ended and for the period September 8, 2014 (commencement of operations) through May 31, 2015, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at May 31, 2016 by correspondence with the custodian, provides a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Chicago, IL

July 27, 2016

| NUVEEN | 17 |

DRA

Diversified Real Asset Income Fund | ||

| May 31, 2016 |

| Principal Amount (000) | Description (1) | Interest Rate (7) | Maturity (7) | Value | ||||||||||||||||||

LONG-TERM INVESTMENTS – 135.4% (96.7% of Total Investments) |

| |||||||||||||||||||||

WHOLE LOANS – 10.7% (7.6% of Total Investments) (2), (3), (4) |

| |||||||||||||||||||||

| Commercial Loans – 7.2% (5.1% of Total Investments) | ||||||||||||||||||||||

| $ | 2,222 | 150 North Pantano I, AZ | 4.900% | 8/01/19 | $ | 2,222,233 | ||||||||||||||||

| 1,350 | Carl’s Jr., Idaho Springs, CO | 4.125% | 5/01/23 | 1,276,242 | ||||||||||||||||||

| 6,896 | Clear Lake Central I, Webster, TX, (5) | 4.925% | 9/01/16 | 2,640,025 | ||||||||||||||||||

| 3,750 | Magnolia Retail Land, Magnolia, TX, (5) | 6.900% | 10/01/16 | 3,750,000 | ||||||||||||||||||

| 14,000 | NCH Commercial Pool II, Rocky Point, Mexico, (5), (6) | 11.925% | 8/01/14 | 5,749,800 | ||||||||||||||||||

| 1,859 | Palace Court, Santa Fe, NM, (5) | 4.875% | 8/01/16 | 1,055,863 | ||||||||||||||||||

| 1,222 | Perkins Restaurant, Maple Grove, MN | 6.375% | 1/01/18 | 1,221,511 | ||||||||||||||||||

| 4,523 | RealtiCorp Fund III, Crystal River, FL, (5) | 5.925% | 7/01/16 | 4,522,755 | ||||||||||||||||||

| 2,106 | RL Stowe Portfolio, Belmont, NC and Chattanooga, TN | 3.925% | 1/01/20 | 1,716,112 | ||||||||||||||||||

| 37,928 | Total Commercial Loans | 24,154,541 | ||||||||||||||||||||

| Multifamily Loans – 3.5% (2.5% of Total Investments) | ||||||||||||||||||||||

| 4,915 | NCH Multifamily Pool, Oklahoma City, OK, (5), (6) | 11.925% | 8/01/14 | 38,134 | ||||||||||||||||||

| 4,400 | NCH Multifamily Pool II, Rocky Point Mexico, (5), (6) | 11.925% | 8/01/14 | 4,001,360 | ||||||||||||||||||

| 12,774 | Sapphire Skies I, Cle Elum, WA, (5), (8) | 0.925% | 3/01/20 | 7,600,006 | ||||||||||||||||||

| 22,089 | Total Multifamily Loans | 11,639,500 | ||||||||||||||||||||

| $ | 60,017 | Total Whole Loans (cost 58,380,362) | 35,794,041 | |||||||||||||||||||

| Principal Amount (000) | Description (1) | Coupon | Maturity | Value | ||||||||||||||||||

CORPORATE NOTES – 2.4% (1.7% of Total Investments) (2), (3), (4) |

| |||||||||||||||||||||

| Diversified Financial Services – 2.4% (1.7% of Total Investments) | ||||||||||||||||||||||

| $ | 8,000 | Stratus III, Stratus Properties Inc., (5) | 7.250% | 12/31/16 | $ | 8,000,000 | ||||||||||||||||

| $ | 8,000 | Total Corporate Notes (cost $8,000,000) | 8,000,000 | |||||||||||||||||||

| Shares | Description (1) | Value | ||||||||||||||||||||

COMMON STOCKS – 56.0% (40.0% of Total Investments) |

| |||||||||||||||||||||

| Air Freight & Logistics – 1.8% (1.3% of Total Investments) | ||||||||||||||||||||||

| 193,890 | BPost SA | $ | 5,110,685 | |||||||||||||||||||

| 27,043 | Oesterreichische Post AG | 968,728 | ||||||||||||||||||||

Total Air Freight & Logistics | 6,079,413 | |||||||||||||||||||||

| Commercial Services & Supplies – 0.1% (0.1% of Total Investments) | ||||||||||||||||||||||

| 15,920 | Covanta Holding Corporation | 265,386 | ||||||||||||||||||||

| Diversified Telecommunication Services – 1.2% (0.9% of Total Investments) | ||||||||||||||||||||||

| 2,181,653 | HKBN Limited | 2,667,143 | ||||||||||||||||||||

| 533,514 | Singapore Telecommunications Limited | 1,499,309 | ||||||||||||||||||||

Total Diversified Telecommunication Services | 4,166,452 | |||||||||||||||||||||

| Electric Utilities – 8.7% (6.2% of Total Investments) | ||||||||||||||||||||||

| 109,388 | Alupar Investimento SA | 374,152 | ||||||||||||||||||||

| 1,773,725 | AusNet Services | 2,019,087 | ||||||||||||||||||||

| 873 | Avangrid Inc. | 36,683 | ||||||||||||||||||||

| 24,770 | Brookfield Infrastructure Partners LP | 1,059,165 | ||||||||||||||||||||

| 677,100 | Contact Energy Limited | 2,469,299 | ||||||||||||||||||||

| 18,279 | Duke Energy Corporation | 1,429,966 | ||||||||||||||||||||

| 567,863 | EDP - Energias de Portugal, S.A. | 1,892,340 | ||||||||||||||||||||

| 44,325 | Endesa S.A, (9) | 911,401 | ||||||||||||||||||||

| 3,081 | Hafslund ASA, Class B Shares | 23,939 | ||||||||||||||||||||

| 1,996,873 | HK Electric Investments Limited, 144A | 1,752,556 | ||||||||||||||||||||

| 18 | NUVEEN |

| Shares | Description (1) | Value | ||||||||||||||||||||

| Electric Utilities (continued) | ||||||||||||||||||||||

| 1,491,550 | Infratil Limited | $ | 3,405,992 | |||||||||||||||||||

| 60,820 | Scottish and Southern Energy PLC | 1,349,518 | ||||||||||||||||||||

| 123,884 | Southern Company | 6,124,825 | ||||||||||||||||||||

| 3,031,580 | Spark Infrastructure Group | 5,039,472 | ||||||||||||||||||||

| 220,385 | Transmissora Alianca de Energia Eletrica SA | 1,166,694 | ||||||||||||||||||||

Total Electric Utilities | 29,055,089 | |||||||||||||||||||||

| Gas Utilities – 2.7% (1.9% of Total Investments) | ||||||||||||||||||||||

| 10,550 | AmeriGas Partners, LP | 484,034 | ||||||||||||||||||||

| 26,697 | Enagas | 800,237 | ||||||||||||||||||||

| 1,359,845 | Snam Rete Gas S.p.A | 7,784,549 | ||||||||||||||||||||

Total Gas Utilities | 9,068,820 | |||||||||||||||||||||

| Health Care Providers & Services – 0.4% (0.3% of Total Investments) | ||||||||||||||||||||||

| 109,737 | Sienna Senior Living Inc., Subscription | 1,452,728 | ||||||||||||||||||||

| Independent Power & Renewable Electricity Producers – 1.3% (0.9% of Total Investments) | ||||||||||||||||||||||

| 14,978 | Brookfield Renewable Energy Partners LP | 432,415 | ||||||||||||||||||||

| 31,621 | NextEra Energy Partners LP | 902,147 | ||||||||||||||||||||

| 839,598 | Renewables Infrastructure Group Limited | 1,190,495 | ||||||||||||||||||||

| 168,453 | Saeta Yield S.A, (9) | 1,676,367 | ||||||||||||||||||||

| 26,829 | TransAlta Renewables Inc. | 263,104 | ||||||||||||||||||||

Total Independent Power & Renewable Electricity Producers | 4,464,528 | |||||||||||||||||||||

| Media – 0.2% (0.1% of Total Investments) | ||||||||||||||||||||||

| 31,326 | SES SA | 701,629 | ||||||||||||||||||||

| Multi-Utilities – 8.2% (5.8% of Total Investments) | ||||||||||||||||||||||

| 71,209 | CenterPoint Energy, Inc. | 1,604,339 | ||||||||||||||||||||

| 770,152 | Centrica PLC | 2,273,286 | ||||||||||||||||||||

| 1,915,134 | Duet Group | 3,252,784 | ||||||||||||||||||||

| 227,724 | Engie | 3,508,007 | ||||||||||||||||||||

| 13,091,020 | Keppel Infrastructure Trust | 4,848,174 | ||||||||||||||||||||

| 98,321 | National Grid PLC | 7,257,073 | ||||||||||||||||||||

| 790,271 | Redes Energeticas Nacionais SA | 2,331,891 | ||||||||||||||||||||

| 1,023,267 | Vector Limited | 2,340,118 | ||||||||||||||||||||

Total Multi-Utilities | 27,415,672 | |||||||||||||||||||||

| Oil, Gas & Consumable Fuels – 3.7% (2.7% of Total Investments) | ||||||||||||||||||||||

| 13,954 | AltaGas Limited, (WI/DD) | 322,527 | ||||||||||||||||||||

| 79,551 | Enbridge Energy Partners LP | 1,729,439 | ||||||||||||||||||||

| 60,489 | Enbridge Income Fund Holdings Inc. | 1,430,868 | ||||||||||||||||||||

| 232,123 | Enterprise Products Partnership LP | 6,443,734 | ||||||||||||||||||||

| 47,770 | Spectra Energy Corporation | 1,521,952 | ||||||||||||||||||||

| 143,636 | Veresen Inc. | 1,123,808 | ||||||||||||||||||||

Total Oil, Gas & Consumable Fuels | 12,572,328 | |||||||||||||||||||||

| Real Estate Investment Trust – 21.4% (15.3% of Total Investments) | ||||||||||||||||||||||

| 443,564 | AEW UK REIT PLC | 630,390 | ||||||||||||||||||||

| 15,332 | Agree Realty Corporation | 652,683 | ||||||||||||||||||||

| 218,261 | Armada Hoffler Properties Inc. | 2,640,958 | ||||||||||||||||||||

| 572,895 | Ascendas Real Estate Investment Trust | 952,676 | ||||||||||||||||||||

| 77,103 | Blackstone Mortgage Trust Inc., Class A | 2,173,534 | ||||||||||||||||||||

| 3,086 | Camden Property Trust | 262,958 | ||||||||||||||||||||

| 68,491 | CapitaMall Trust | 100,963 | ||||||||||||||||||||

| 3,334 | Care Capital Properties, Inc. | 86,651 | ||||||||||||||||||||

| 59,374 | CareTrust REIT Inc. | 795,018 | ||||||||||||||||||||

| 76,066 | Choice Properties Real Estate Investment Trust | 795,841 | ||||||||||||||||||||

| 165,118 | City Office REIT, Inc. | 1,943,439 | ||||||||||||||||||||

| 2,643 | Cofinimmo, SANV | 322,010 | ||||||||||||||||||||

| 58,594 | Colony Financial Inc. | 1,073,442 | ||||||||||||||||||||

| 95,639 | Community Healthcare Trust Inc. | 1,784,624 | ||||||||||||||||||||

| 156,580 | Crombie Real Estate Investment Trust | 1,750,458 | ||||||||||||||||||||

| 4,811 | DiamondRock Hospitality Company | 43,010 | ||||||||||||||||||||

| NUVEEN | 19 |

| DRA | Diversified Real Asset Income Fund | |||

| Portfolio of Investments (continued) | May 31, 2016 |

| Shares | Description (1) | Value | ||||||||||||||||||||

| Real Estate Investment Trust (continued) | ||||||||||||||||||||||

| 6,151 | Digital Realty Trust Inc. | $ | 587,113 | |||||||||||||||||||

| 71,156 | Easterly Government Properties, Inc. | 1,332,040 | ||||||||||||||||||||

| 5,395 | Entertainment Properties Trust | 384,556 | ||||||||||||||||||||

| 32,964 | Eurocommercial Properties NV | 1,550,721 | ||||||||||||||||||||

| 474,398 | Fortune REIT | 526,855 | ||||||||||||||||||||

| 1,787 | Four Corners Property Trust, Inc. | 34,739 | ||||||||||||||||||||

| 2,055,667 | Frasers Centrepoint Trust | 3,015,356 | ||||||||||||||||||||

| 77,367 | Gaming and Leisure Properties Inc. | 2,546,148 | ||||||||||||||||||||

| 28,424 | Health Care Property Investors Inc. | 934,297 | ||||||||||||||||||||

| 9,323 | ICADE | 673,327 | ||||||||||||||||||||

| 167,263 | Immobiliare Grande Distribuzione SIIQ SpA | 150,745 | ||||||||||||||||||||

| 70,451 | Independence Realty Trust | 549,518 | ||||||||||||||||||||

| 142,978 | InnVest Real Estate Investment Trust | 723,967 | ||||||||||||||||||||

| 38,309 | Investors Real Estate Trust | 238,282 | ||||||||||||||||||||

| 1,071,711 | Keppel DC REIT | 840,497 | ||||||||||||||||||||

| 279,212 | Killam Apartment Real Estate I, (WI/DD) | 2,533,742 | ||||||||||||||||||||

| 18,936 | Lexington Corporate Properties Trust | 178,945 | ||||||||||||||||||||

| 97,966 | Liberty Property Trust | 3,656,091 | ||||||||||||||||||||

| 70,309 | LondonMetric Property PLC | 167,514 | ||||||||||||||||||||

| 36,946 | LTC Properties Inc. | 1,722,423 | ||||||||||||||||||||

| 2,643,850 | Mapletree Greater China Commercial Trust | 1,881,470 | ||||||||||||||||||||

| 417,690 | Mapletree Logistics Trust | 295,728 | ||||||||||||||||||||

| 67,382 | MGM Growth Properties LLC, (9) | 1,549,786 | ||||||||||||||||||||

| 4,821 | Monmouth Real Estate Investment Corporation | 57,322 | ||||||||||||||||||||

| 15,228 | New Senior Investment Group Inc. | 157,914 | ||||||||||||||||||||

| 151,700 | Crombie Real Estate Investment Receipt, (9) | 1,694,746 | ||||||||||||||||||||

| 237,733 | NorthWest Healthcare Properties REIT | 1,734,933 | ||||||||||||||||||||

| 35,003 | Omega Healthcare Investors Inc. | 1,117,296 | ||||||||||||||||||||

| 105,508 | OneREIT | 276,774 | ||||||||||||||||||||

| 643,582 | Parkway Life Real Estate Investment Trust | 1,149,671 | ||||||||||||||||||||

| 19,045 | Pebblebrook Hotel Trust | 488,504 | ||||||||||||||||||||

| 225,345 | Physicians Realty Trust | 4,279,302 | ||||||||||||||||||||

| 615,754 | Plaza Retail REIT | 2,291,440 | ||||||||||||||||||||

| 644,300 | Prologis Property Mexico SA de CV | 973,253 | ||||||||||||||||||||

| 191,477 | Pure Industrial Real Estate Trust | 746,138 | ||||||||||||||||||||

| 19,956 | Sabra Health Care Real Estate Investment Trust Inc. | 417,879 | ||||||||||||||||||||

| 60,803 | Smart Real Estate Investment Trust | 1,599,652 | ||||||||||||||||||||

| 159,200 | Spirit Realty Capital Inc. | 1,822,840 | ||||||||||||||||||||

| 39,849 | STAG Industrial Inc. | 850,776 | ||||||||||||||||||||

| 82,903 | Starwood Property Trust Inc. | 1,709,460 | ||||||||||||||||||||

| 945,954 | TF Administradora Industrial S de RL de CV | 1,578,063 | ||||||||||||||||||||

| 245,382 | Tritax Big Box REIT PLC | 488,673 | ||||||||||||||||||||

| 18,419 | Universal Health Realty Income Trust | 985,416 | ||||||||||||||||||||

| 25,700 | Urstadt Biddle Properties Inc. | 543,812 | ||||||||||||||||||||

| 149,407 | VEREIT, Inc. | 1,432,813 | ||||||||||||||||||||

| 1,487 | Welltower Inc. | 102,469 | ||||||||||||||||||||

| 49,675 | Wereldhave NV | 2,529,473 | ||||||||||||||||||||

| 69,190 | WPT Industrial Real Estate Investment Trust | 729,954 | ||||||||||||||||||||

Total Real Estate Investment Trust | 71,841,088 | |||||||||||||||||||||

| Road & Rail – 0.5% (0.4% of Total Investments) | ||||||||||||||||||||||

| 381,015 | MTR Corporation | 1,804,376 | ||||||||||||||||||||

| Transportation Infrastructure – 5.5% (3.9% of Total Investments) | ||||||||||||||||||||||

| 257,196 | Cosco Pacific Limited | 261,143 | ||||||||||||||||||||

| 6,502,771 | Hopewell Highway Infrastructure Limited | 3,230,151 | ||||||||||||||||||||

| 5,158,024 | Hutchison Port Holdings Trust | 2,217,950 | ||||||||||||||||||||

| 193,099 | Jiangsu Expressway Company Limited | 265,392 | ||||||||||||||||||||

| 27,921 | Macquarie Infrastructure Corporation | 1,999,423 | ||||||||||||||||||||

| 676,587 | Sydney Airport | 3,462,144 | ||||||||||||||||||||

| 755,074 | Transurban Group | 6,576,045 | ||||||||||||||||||||

| 388,357 | Zhejiang Expressway Company Limited | 363,831 | ||||||||||||||||||||

Total Transportation Infrastructure | 18,376,079 | |||||||||||||||||||||

| Water Utilities – 0.3% (0.2% of Total Investments) | ||||||||||||||||||||||

| 671,766 | Inversiones Aguas Metropolitanas SA | 992,020 | ||||||||||||||||||||

Total Common Stocks (cost $178,947,947) | 188,255,608 | |||||||||||||||||||||

| 20 | NUVEEN |

| Shares | Description (1) | Coupon | Ratings (11) | Value | ||||||||||||||||||

CONVERTIBLE PREFERRED SECURITIES – 6.4% (4.6% of Total Investments) |

| |||||||||||||||||||||

| Electric Utilities – 2.4% (1.8% of Total Investments) | ||||||||||||||||||||||

| 58,787 | Exelon Corporation | 6.500% | BB+ | $ | 2,775,922 | |||||||||||||||||

| 83,598 | NextEra Energy Inc. | 6.371% | BBB | 5,052,663 | ||||||||||||||||||

| 7,366 | NextEra Energy Inc. | 5.799% | BBB | 452,714 | ||||||||||||||||||

Total Electric Utilities | 8,281,299 | |||||||||||||||||||||

| Gas Utilities – 0.5% (0.3% of Total Investments) | ||||||||||||||||||||||

| 27,189 | Spire, Inc., (10) | 6.750% | N/R | 1,566,630 | ||||||||||||||||||

| Multi-Utilities – 0.2% (0.1% of Total Investments) | ||||||||||||||||||||||

| 8,317 | Black Hills Corp, Convertible Preferred | 7.750% | N/R | 565,722 | ||||||||||||||||||

| Oil, Gas & Consumable Fuels – 0.2% (0.1% of Total Investments) | ||||||||||||||||||||||

| 17,217 | Anadarko Petroleum Corporation | 7.500% | N/R | 671,463 | ||||||||||||||||||

| Real Estate Investment Trust – 3.1% (2.3% of Total Investments) | ||||||||||||||||||||||

| 65,693 | Alexandria Real Estate Equities Inc., (10) | 7.000% | Baa3 | 2,152,471 | ||||||||||||||||||

| 45,883 | American Homes 4 Rent | 5.000% | N/R | 1,220,947 | ||||||||||||||||||

| 44,237 | American Tower Corporation | 5.500% | N/R | 4,671,870 | ||||||||||||||||||

| 15,639 | Equity Commonwealth | 6.500% | Ba1 | 407,709 | ||||||||||||||||||

| 1,147 | FelCor Lodging Trust Inc., Series A. | 1.950% | CCC | 28,893 | ||||||||||||||||||

| 6,205 | Lexington Corporate Properties Trust, Series B | 6.500% | N/R | 310,250 | ||||||||||||||||||

| 27,446 | Ramco-Gershenson Properties Trust | 7.250% | N/R | 1,794,419 | ||||||||||||||||||

Total Real Estate Investment Trust | 10,586,559 | |||||||||||||||||||||

Total Convertible Preferred Securities (cost $20,046,269) | 21,671,673 | |||||||||||||||||||||

| Shares | Description (1) | Coupon | Ratings (11) | Value | ||||||||||||||||||

$25 PAR (OR SIMILAR) RETAIL PREFERRED – 31.5% (22.5% of Total Investments) |

| |||||||||||||||||||||

| Electric Utilities – 6.6% (4.7% of Total Investments) | ||||||||||||||||||||||

| 11,814 | APT Pipelines Limited, (10) | 6.840% | N/R | $ | 876,143 | |||||||||||||||||

| 111,794 | Entergy Arkansas Inc., (10) | 6.450% | Baa3 | 2,829,786 | ||||||||||||||||||

| 64,379 | Entergy New Orleans, Inc. | 5.500% | A– | 1,687,374 | ||||||||||||||||||

| 37,111 | Entergy Texas Inc. | 5.625% | A– | 999,028 | ||||||||||||||||||

| 78,424 | Integrys Energy Group Inc., (10) | 6.000% | Baa1 | 2,058,630 | ||||||||||||||||||

| 66,732 | NextEra Energy Inc. | 5.000% | BBB | 1,698,329 | ||||||||||||||||||

| 63,074 | NextEra Energy Inc., (WI/DD) | 5.250% | Baa2 | 1,576,850 | ||||||||||||||||||

| 68,738 | Pacific Gas & Electric Corporation | 6.000% | BBB+ | 2,163,872 | ||||||||||||||||||

| 163,255 | PPL Capital Funding, Inc. | 5.900% | BBB | 4,357,276 | ||||||||||||||||||

| 75,040 | SCE Trust I | 5.625% | Baa1 | 1,963,046 | ||||||||||||||||||

| 64,585 | SCE Trust V | 5.450% | Baa1 | 1,845,839 | ||||||||||||||||||

Total Electric Utilities | 22,056,173 | |||||||||||||||||||||

| Independent Power & Renewable Electricity Producers – 0.2% (0.1% of Total Investments) | ||||||||||||||||||||||

| 35,503 | Brookfield Renewable Partners, Preferred Equity | 5.750% | BB+ | 680,090 | ||||||||||||||||||

| Multi-Utilities – 1.4% (1.0% of Total Investments) | ||||||||||||||||||||||

| 45,190 | Dominion Resources Inc. | 6.375% | Baa3 | 2,266,279 | ||||||||||||||||||

| 6,736 | DTE Energy Company | 5.250% | Baa1 | 171,499 | ||||||||||||||||||

| 87,209 | DTE Energy Company, (10) | 5.375% | Baa1 | 2,188,405 | ||||||||||||||||||

Total Multi-Utilities | 4,626,183 | |||||||||||||||||||||

| Oil, Gas & Consumable Fuels – 0.7% (0.5% of Total Investments) | ||||||||||||||||||||||

| 7,841 | Kinder Morgan Inc., Delaware | 9.750% | N/R | 358,491 | ||||||||||||||||||

| 27,207 | Nustar Logistics Limited Partnership | 7.625% | Ba2 | 699,220 | ||||||||||||||||||

| 70,252 | Pembina Pipeline Corporation | 5.750% | BB+ | 1,348,414 | ||||||||||||||||||

Total Oil, Gas, & Consumable Fuels | 2,406,125 | |||||||||||||||||||||

| Real Estate Investment Trust – 22.3% (16.0% of Total Investments) | ||||||||||||||||||||||

| 5,585 | American Homes 4 Rent | 5.500% | N/R | 147,835 | ||||||||||||||||||

| 37,395 | American Homes 4 Rent | 5.000% | N/R | 1,005,926 | ||||||||||||||||||

| NUVEEN | 21 |

| DRA | Diversified Real Asset Income Fund | |||

| Portfolio of Investments (continued) | May 31, 2016 |

| Shares | Description (1) | Coupon | Ratings (11) | Value | ||||||||||||||||||

| Real Estate Investment Trust (continued) | ||||||||||||||||||||||

| 118,661 | American Homes 4 Rent | 6.500% | N/R | $ | 3,032,975 | |||||||||||||||||

| 20,397 | Apartment Investment & Management Company | 6.875% | BB | 566,017 | ||||||||||||||||||

| 27,746 | Apollo Commercial Real Estate Finance | 8.625% | N/R | 712,517 | ||||||||||||||||||

| 50,287 | Arbor Realty Trust Incorporated | 7.375% | N/R | 1,260,192 | ||||||||||||||||||

| 38,141 | CBL & Associates Properties Inc. | 7.375% | BB | 941,701 | ||||||||||||||||||

| 141,933 | CBL & Associates Properties Inc. | 6.625% | BB | 3,439,037 | ||||||||||||||||||

| 183,565 | Cedar Shopping Centers Inc., Series A | 7.250% | N/R | 4,829,595 | ||||||||||||||||||

| 51,391 | Chesapeake Lodging Trust | 7.750% | N/R | 1,344,902 | ||||||||||||||||||

| 89,981 | Colony Financial Inc. | 7.125% | N/R | 2,124,451 | ||||||||||||||||||

| 31,117 | Colony Financial Inc. | 8.500% | N/R | 809,042 | ||||||||||||||||||

| 27,720 | Colony Financial Inc. | 7.500% | N/R | 686,902 | ||||||||||||||||||

| 35,581 | Coresite Realty Corporation | 7.250% | N/R | 946,455 | ||||||||||||||||||

| 51,216 | Corporate Office Properties Trust | 7.375% | BB | 1,327,007 | ||||||||||||||||||

| 133,569 | Digital Realty Trust Inc. | 6.350% | Baa3 | 3,538,243 | ||||||||||||||||||

| 62,222 | Dupont Fabros Technology | 6.625% | Ba2 | 1,601,594 | ||||||||||||||||||

| 56,817 | EPR Properties Inc. | 9.000% | BB | 1,969,845 | ||||||||||||||||||

| 20,575 | EPR Properties Inc. | 6.625% | Baa3 | 544,620 | ||||||||||||||||||

| 22,267 | EPR Properties Inc. | 5.750% | BB | 618,800 | ||||||||||||||||||

| 740 | Equity Lifestyle Properties Inc. | 6.750% | N/R | 19,277 | ||||||||||||||||||

| 83,444 | General Growth Properties | 6.375% | N/R | 2,252,988 | ||||||||||||||||||

| 89,228 | Gramercy Property Trust | 7.125% | N/R | 2,377,926 | ||||||||||||||||||

| 80,071 | Hersha Hospitality Trust | 6.875% | N/R | 2,094,657 | ||||||||||||||||||

| 88,840 | Hersha Hospitality Trust | 6.500% | N/R | 2,204,120 | ||||||||||||||||||

| 78,372 | Investors Real Estate Trust | 7.950% | N/R | 2,072,156 | ||||||||||||||||||

| 5,052 | LaSalle Hotel Properties | 6.375% | N/R | 128,220 | ||||||||||||||||||

| 82,560 | LaSalle Hotel Properties | 6.300% | N/R | 2,079,686 | ||||||||||||||||||

| 3,055 | Monmouth Real Estate Investment Corp | 7.875% | N/R | 79,827 | ||||||||||||||||||

| 685 | Northstar Realty Finance Corporation | 8.875% | N/R | 16,926 | ||||||||||||||||||

| 26,061 | Northstar Realty Finance Corporation | 8.750% | N/R | 639,276 | ||||||||||||||||||

| 144,100 | Pebblebrook Hotel Trust | 6.500% | N/R | 3,717,780 | ||||||||||||||||||

| 22,084 | Post Properties, Inc., Series A | 8.500% | Baa3 | 1,460,415 | ||||||||||||||||||

| 23,041 | Rait Financial Trust | 7.125% | N/R | 555,519 | ||||||||||||||||||

| 39,071 | Saul Centers, Inc. | 6.875% | N/R | 1,028,349 | ||||||||||||||||||

| 4,233 | STAG Industrial Inc. | 9.000% | BB+ | 110,481 | ||||||||||||||||||

| 62,200 | STAG Industrial Inc. | 6.875% | BB+ | 1,648,300 | ||||||||||||||||||

| 14,210 | Summit Hotel Properties Inc. | 9.250% | N/R | 365,055 | ||||||||||||||||||

| 82,307 | Summit Hotel Properties Inc. | 7.875% | N/R | 2,130,105 | ||||||||||||||||||

| 123,744 | Summit Hotel Properties Inc. | 7.125% | N/R | 3,144,335 | ||||||||||||||||||

| 919 | Sun Communities Inc. | 7.125% | N/R | 24,041 | ||||||||||||||||||

| 105,364 | Sunstone Hotel Investors Inc. | 6.450% | N/R | 2,736,303 | ||||||||||||||||||

| 86,598 | Taubman Centers Incorporated., Series J | 6.500% | N/R | 2,254,146 | ||||||||||||||||||

| 52,608 | Taubman Centers Incorporated, Series K | 6.250% | N/R | 1,359,917 | ||||||||||||||||||

| 13,319 | Terreno Realty Corporation | 7.750% | �� | BB | 349,624 | |||||||||||||||||

| 54,781 | UMH Properties Inc. | 8.000% | N/R | 1,440,740 | ||||||||||||||||||

| 58,201 | Urstadt Biddle Properties | 7.125% | N/R | 1,521,956 | ||||||||||||||||||

| 113,565 | Urstadt Biddle Properties | 6.750% | N/R | 3,038,999 | ||||||||||||||||||

| 6,339 | VEREIT, Inc. | 6.700% | N/R | 166,018 | ||||||||||||||||||

| 40,338 | WP GLIMCHER, Inc. | 7.500% | Ba1 | 1,037,090 | ||||||||||||||||||

| 61,190 | WP GLIMCHER, Inc. | 6.875% | Ba1 | 1,556,674 | ||||||||||||||||||

Total Real Estate Investment Trust | 75,058,562 | |||||||||||||||||||||

| Trading Companies & Distributors – 0.3% (0.2% of Total Investments) | ||||||||||||||||||||||

| 36,000 | GATX Corporation | 5.625% | BBB | 888,840 | ||||||||||||||||||

Total $25 Par (or similar) Retail Preferred (cost $102,801,469) |

| 105,715,973 | ||||||||||||||||||||

| Principal Amount (000) | Description (1) | Coupon | Maturity | Ratings (11) | Value | |||||||||||||||||

CONVERTIBLE BONDS – 0.8% (0.6% of Total Investments) |

| |||||||||||||||||||||

| Multi-Utilities – 0.5% (0.4% of Total Investments) | ||||||||||||||||||||||

| $ | 1,670 | Dominion Resources Inc. | 5.750% | 10/01/54 | BBB– | $ | 1,636,600 | |||||||||||||||

| 22 | NUVEEN |

| Principal Amount (000) | Description (1) | Coupon | Maturity | Ratings (11) | Value | |||||||||||||||||

| Oil, Gas & Consumable Fuels – 0.3% (0.2% of Total Investments) | ||||||||||||||||||||||

| $ | 1,705 | DCP Midstream LLC, 144A | 5.850% | 5/21/43 | BB– | $ | 1,159,400 | |||||||||||||||

| $ | 3,375 | Total Convertible Bonds (cost $3,312,587) | 2,796,000 | |||||||||||||||||||

| Principal Amount (000) (12) | Description (1) | Coupon | Maturity | Ratings (11) | Value | |||||||||||||||||

CORPORATE BONDS – 19.4% (13.8% of Total Investments) |

| |||||||||||||||||||||

| Commercial Services & Supplies – 2.0% (1.4% of Total Investments) | ||||||||||||||||||||||

| $ | 1,610 | ADS Waste Holdings Inc. | 8.250% | 10/01/20 | CCC+ | $ | 1,658,300 | |||||||||||||||

| 1,370 | Casella Waste Systems Inc. | 7.750% | 2/15/19 | B | 1,399,113 | |||||||||||||||||

| 2,140 | Covanta Holding Corporation | 5.875% | 3/01/24 | Ba3 | 2,129,300 | |||||||||||||||||

| 1,485 | GFL Environmental Corporation, 144A | 9.875% | 2/01/21 | B | 1,581,525 | |||||||||||||||||

Total Commercial Services & Supplies | 6,768,238 | |||||||||||||||||||||

| Construction & Engineering – 0.2% (0.2% of Total Investments) | ||||||||||||||||||||||

| 6,500 | NOK | VV Holding AS, 144A | 6.370% | 7/10/19 | N/R | 753,682 | ||||||||||||||||

| Consumer Finance – 0.2% (0.1% of Total Investments) | ||||||||||||||||||||||

| 705 | Covenant Surgical Partners Inc., 144A | 8.750% | 8/01/19 | B– | 671,512 | |||||||||||||||||

| Diversified Telecommunication Services – 1.6% (1.1% of Total Investments) | ||||||||||||||||||||||

| 1,452 | CyrusOne LP Finance | 6.375% | 11/15/22 | B+ | 1,539,120 | |||||||||||||||||

| 1,930 | Qualitytech LP/QTS Finance Corp. | 5.875% | 8/01/22 | BB– | 1,968,600 | |||||||||||||||||

| 1,890 | SBA Communications Corporation | 4.875% | 7/15/22 | B | 1,894,725 | |||||||||||||||||

Total Diversified Telecommunication Services | 5,402,445 | |||||||||||||||||||||

| Electric Utilities – 0.2% (0.1% of Total Investments) | ||||||||||||||||||||||

| 775 | Intergen NV, 144A | 7.000% | 6/30/23 | B+ | 548,312 | |||||||||||||||||

| Energy Equipment & Services – 0.7% (0.5% of Total Investments) | ||||||||||||||||||||||

| 1,020 | Compressco Partners LP / Compressco Finance Corporation | 7.250% | 8/15/22 | B– | 826,200 | |||||||||||||||||

| 1,390 | EUR | Origin Energy Finance Limited, Reg S | 7.875% | 6/16/71 | BB | 1,542,359 | ||||||||||||||||

Total Energy Equipment & Services | 2,368,559 | |||||||||||||||||||||

| Gas Utilities – 1.2% (0.9% of Total Investments) | ||||||||||||||||||||||

| 895 | AmeriGas Finance LLC | 7.000% | 5/20/22 | Ba2 | 943,106 | |||||||||||||||||

| 1,465 | Ferrellgas LP | 6.750% | 1/15/22 | B+ | 1,377,100 | |||||||||||||||||

| 765 | LBC Tank Terminals Holdings Netherlands BV, 144A | 6.875% | 5/15/23 | B | 738,225 | |||||||||||||||||

| 975 | Suburban Propane Partners LP | 5.750% | 3/01/25 | BB– | 957,938 | |||||||||||||||||

Total Gas Utilities | 4,016,369 | |||||||||||||||||||||

| Health Care Equipment & Supplies – 0.3% (0.2% of Total Investments) | ||||||||||||||||||||||

| 895 | Tenet Healthcare Corporation | 8.125% | 4/01/22 | B– | 900,594 | |||||||||||||||||

| Health Care Providers & Services – 2.3% (1.7% of Total Investments) | ||||||||||||||||||||||

| 1,195 | Acadia Healthcare | 5.625% | 2/15/23 | B | 1,214,419 | |||||||||||||||||

| 1,035 | Community Health Systems, Inc. | 6.875% | 2/01/22 | B+ | 889,469 | |||||||||||||||||

| 1,235 | HCA Inc. | 5.375% | 2/01/25 | BB | 1,253,525 | |||||||||||||||||

| 1,010 | IASIS Healthcare Capital Corporation | 8.375% | 5/15/19 | CCC+ | 969,600 | |||||||||||||||||

| 1,295 | Kindred Healthcare Inc. | 6.375% | 4/15/22 | B2 | 1,165,500 | |||||||||||||||||

| 1,200 | Lifepoint Health Inc. | 5.875% | 12/01/23 | Ba2 | 1,239,000 | |||||||||||||||||

| 1,225 | Select Medical Corporation | 6.375% | 6/01/21 | B– | 1,179,062 | |||||||||||||||||

Total Health Care Providers & Services | 7,910,575 | |||||||||||||||||||||

| Independent Power & Renewable Electricity Producers – 0.3% (0.2% of Total Investments) | ||||||||||||||||||||||

| 1,355 | GenOn Energy Inc. | 9.500% | 10/15/18 | CCC+ | 1,067,062 | |||||||||||||||||

| NUVEEN | 23 |

| DRA | Diversified Real Asset Income Fund | |||

| Portfolio of Investments (continued) | May 31, 2016 |

| Principal Amount (000) (12) | Description (1) | Coupon | Maturity | Ratings (11) | Value | |||||||||||||||||

| Internet Software & Services – 0.4% (0.3% of Total Investments) | ||||||||||||||||||||||

| $ | 1,445 | Equinix Inc. | 5.750% | 1/01/25 | BB | $ | 1,502,800 | |||||||||||||||

| IT Services – 0.5% (0.3% of Total Investments) | ||||||||||||||||||||||

| 1,510 | Zayo Group LLC / Zayo Capital Inc. | 6.000% | 4/01/23 | B– | 1,551,525 | |||||||||||||||||

| Marine – 0.2% (0.1% of Total Investments) | ||||||||||||||||||||||

| 955 | Navios South American Logistics Inc., Finance US Inc., 144A | 7.250% | 5/01/22 | B– | 604,037 | |||||||||||||||||

| Media – 0.4% (0.3% of Total Investments) | ||||||||||||||||||||||

| 1,170 | Lamar Media Corporation, 144A | 5.750% | 2/01/26 | Ba1 | 1,231,425 | |||||||||||||||||

| Multi-Utilities – 1.1% (0.8% of Total Investments) | ||||||||||||||||||||||

| 1,505 | GBP | Centrica PLC, Reg S | 5.250% | 4/10/75 | BBB | 2,057,294 | ||||||||||||||||

| 1,200 | GBP | RWE AG, Reg S | 7.000% | 3/29/49 | BB+ | 1,664,960 | ||||||||||||||||

Total Multi-Utilities | 3,722,254 | |||||||||||||||||||||

| Oil, Gas & Consumable Fuels – 3.2% (2.3% of Total Investments) | ||||||||||||||||||||||

| 100 | Calumet Specialty Products | 6.500% | 4/15/21 | CCC+ | 67,000 | |||||||||||||||||

| 1,415 | Calumet Specialty Products | 7.625% | 1/15/22 | CCC+ | 937,437 | |||||||||||||||||

| 510 | Crestwood Midstream Partners LP | 6.125% | 3/01/22 | BB– | 481,797 | |||||||||||||||||

| 1,090 | Energy Transfer Equity LP | 5.500% | 6/01/27 | BB+ | 945,575 | |||||||||||||||||

| 835 | Gibson Energy, 144A | 6.750% | 7/15/21 | BB | 828,738 | |||||||||||||||||

| 670 | Global Partners LP/GLP Finance | 6.250% | 7/15/22 | B+ | 547,725 | |||||||||||||||||

| 95 | Global Partners LP/GLP Finance | 7.000% | 6/15/23 | B+ | 77,662 | |||||||||||||||||

| 1,015 | Martin Mid-Stream Partners LP Finance | 7.250% | 2/15/21 | B– | 941,412 | |||||||||||||||||

| 1,205 | NGL Energy Partners LP/Fin Co | 5.125% | 7/15/19 | BB– | 1,084,500 | |||||||||||||||||

| 705 | NGL Energy Partners LP/Fin Co | 6.875% | 10/15/21 | BB– | 606,300 | |||||||||||||||||

| 920 | Northern Tier Energy LLC | 7.125% | 11/15/20 | BB– | 908,500 | |||||||||||||||||

| 470 | PBF Holding Company LLC | 8.250% | 2/15/20 | BBB– | 488,800 | |||||||||||||||||

| 1,505 | Rose Rock Midstream LP / Rose Rock Finance Corporation | 5.625% | 7/15/22 | B | 1,298,062 | |||||||||||||||||

| 925 | Sabine Pass Liquefaction LLC | 6.250% | 3/15/22 | BB+ | 945,813 | |||||||||||||||||

| 765 | Summit Midstream Holdings LLC Finance | 5.500% | 8/15/22 | B | 627,300 | |||||||||||||||||

Total Oil, Gas, & Consumable Fuels | 10,786,621 | |||||||||||||||||||||

| Real Estate Investment Trust – 2.3% (1.7% of Total Investments) | ||||||||||||||||||||||

| 1,285 | Corporate Office Properties LP | 5.000% | 7/01/25 | BBB– | 1,320,679 | |||||||||||||||||

| 1,725 | DuPont Fabros Technology LP | 5.625% | 6/15/23 | Ba1 | 1,772,438 | |||||||||||||||||

| 270 | EPR Properties Inc. | 4.500% | 4/01/25 | Baa2 | 264,331 | |||||||||||||||||

| 1,010 | Geo Group Inc. | 6.000% | 4/15/26 | Ba3 | 1,020,100 | |||||||||||||||||

| 1,615 | Omega Healthcare Investors Inc. | 4.500% | 4/01/27 | BBB– | 1,543,559 | |||||||||||||||||

| 1,400 | PLA Administradora Industrial, S. de R.L. de C.V., 144A | 5.250% | 11/10/22 | Baa3 | 1,400,140 | |||||||||||||||||

| 445 | Vereit Operating Partner, (WI/DD) | 4.875% | 6/01/26 | BB+ | 454,456 | |||||||||||||||||

Total Real Estate Investment Trust | 7,775,703 | |||||||||||||||||||||

| Real Estate Management & Development – 0.9% (0.6% of Total Investments) | ||||||||||||||||||||||

| 1,165 | Hunt Companies Inc., 144A | 9.625% | 3/01/21 | N/R | 1,141,700 | |||||||||||||||||

| 1,800 | Kennedy-Wilson Holdings Incorporated | 5.875% | 4/01/24 | BB– | 1,759,500 | |||||||||||||||||

Total Real Estate Management & Development | 2,901,200 | |||||||||||||||||||||

| Road & Rail – 0.3% (0.2% of Total Investments) | ||||||||||||||||||||||

| 1,075 | Watco Companies LLC Finance, 144A | 6.375% | 4/01/23 | B | 1,076,344 | |||||||||||||||||

| Software – 0.4% (0.3% of Total Investments) | ||||||||||||||||||||||

| 1,265 | SixSigma Networks Mexico SA de CV, 144A | 8.250% | 11/07/21 | B+ | 1,227,050 | |||||||||||||||||

| Transportation Infrastructure – 0.3% (0.2% of Total Investments) | ||||||||||||||||||||||

| 1,020 | Aeropuerto Internacional de Tocumen SA | 5.750% | 10/09/23 | BBB | 1,049,886 | |||||||||||||||||

| 24 | NUVEEN |

| Principal Amount (000) (12) | Description (1) | Coupon | Maturity | Ratings (11) | Value | |||||||||||||||||

| Wireless Telecommunication Services – 0.4% (0.3% of Total Investments) | ||||||||||||||||||||||

| $ | 1,546 | Inmarsat Finance PLC, 144A | 4.875% | 5/15/22 | BB+ | $ | 1,364,345 | |||||||||||||||

Total Corporate Bonds (cost $67,671,359) | 65,200,538 | |||||||||||||||||||||

| Shares | Description (1) | Value | ||||||||||||||||||||

COMMON STOCK RIGHTS – 0.0% (0.0% of Total Investments) |

| |||||||||||||||||||||

| Utilities – 0.0% (0.0% of Total Investments) | ||||||||||||||||||||||

| 14,031 | Alupar Investimento SA | $ | 1,009 | |||||||||||||||||||

Total Common Stock Rights (cost $—) | 1,009 | |||||||||||||||||||||

| Principal Amount (000) (12) | Description (1) | Coupon | Maturity | Ratings (11) | Value | |||||||||||||||||

1,000 PAR (OR SIMILAR) INSTITUTIONAL PREFERRED – 7.1% (5.0% of Total Investments) |

| |||||||||||||||||||||

| Diversified Financial Services – 0.4% (0.3% of Total Investments) | ||||||||||||||||||||||

| $ | 1,200 | National Rural Utilities Cooperative Finance Corporation | 5.250% | 4/20/46 | A3 | $ | 1,214,250 | |||||||||||||||

| Electric Utilities – 4.0% (2.8% of Total Investments) | ||||||||||||||||||||||

| 2,360 | AES Gener SA, 144A | 8.375% | 12/18/73 | BB | 2,478,000 | |||||||||||||||||

| 1,080 | ComEd Financing III | 6.350% | 3/15/33 | Baa2 | 1,143,242 | |||||||||||||||||

| 1,995 | Enel SpA, 144A | 8.750% | 9/24/73 | BBB– | 2,299,238 | |||||||||||||||||

| 1,800 | EUR | Energias de Portugal, SA, Reg S | 5.375% | 9/16/75 | Ba2 | 1,978,237 | ||||||||||||||||

| 995 | FPL Group Capital Inc. | 6.350% | 10/01/66 | BBB | 756,200 | |||||||||||||||||

| 3,065 | GBP | NGG Finance PLC, Reg S | 5.625% | 6/18/73 | BBB | 4,651,279 | ||||||||||||||||

Total Electric Utilities | 13,306,196 | |||||||||||||||||||||

| Energy Equipment & Services – 1.4% (1.0% of Total Investments) | ||||||||||||||||||||||

| 5,290 | Transcanada Trust | 5.625% | 5/20/75 | BBB | 4,744,495 | |||||||||||||||||