| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | January 31, 2017 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .20.6 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-22955 |

|

Tekla Healthcare Opportunities Fund |

(Exact name of registrant as specified in charter) |

|

100 Federal Street, 19th Floor, Boston, MA | | 02110 |

(Address of principal executive offices) | | (Zip code) |

|

100 Federal Street, 19th Floor, Boston, MA 02110 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 617-772-8500 | |

|

Date of fiscal year end: | September 30 | |

|

Date of reporting period: | October 1, 2015 to September 30, 2016 | |

| | | | | | | | | |

ITEM 1. REPORTS TO STOCKHOLDERS.

TEKLA HEALTHCARE

OPPORTUNITIES FUND

TEKLA HEALTHCARE

OPPORTUNITIES FUND

Distribution policy: The Fund has implemented a managed distribution policy (the Policy) that provides for monthly distributions at a rate set by the Board of Trustees. Under the current Policy, the Fund intends to make monthly distributions at a rate of $0.1125 per share to shareholders of record. The Policy would result in a return of capital to shareholders, if the amount of the distribution exceeds the Fund's net investment income and realized capital gains. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund's investment performance and should not be confused with "yield" or "income."

The amounts and sources of distributions reported in the Fund's notices pursuant to Section 19(a) of the Investment Company Act of 1940 are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund's investment experience during its fiscal year and may be subject to changes based on tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that tells you how to report distributions for federal income tax purposes.

You should not draw any conclusions about the Fund's investment performance from the amount of distributions pursuant to the Policy or from the terms of the Policy. The Policy has been established by the Trustees and may be changed or terminated by them without shareholder approval. The Trustees regularly review the Policy and the frequency and rate of distributions considering the purpose and effect of the Policy, the financial market environment, and the Fund's income, capital gains and capital available to pay distributions. The suspension or termination of the Policy could have the effect of creating a trading discount or widening an existing trading discount. At this time there are no reasonably foreseeable circumstances that might cause the Trustees to terminate the Policy.

Consider these risks before investing: As with any investment company that invests in equity securities, the Fund is subject to market risk—the possibility that the prices of equity securities will decline over short or extended periods of time. As a result, the value of an investment in the Fund's shares will fluctuate with the market generally and market sectors in particular. You could lose money over short or long periods of time. Political and economic news can influence market-wide trends and can cause disruptions in the U.S. or world financial markets. Other factors may be ignored by the market as a whole but may cause movements in the price of one company's stock or the stock of companies in one or more industries. All of these factors may have a greater impact on initial public offerings and emerging company shares. Different types of equity securities tend to shift into and out of favor with investors, depending on market and economic conditions. The performance of funds that invest in equity securities of Healthcare Companies may at times be better or worse than the performance of funds that focus on other types of securities or that have a broader investment style.

TEKLA HEALTHCARE

OPPORTUNITIES FUND

Dear Shareholders,

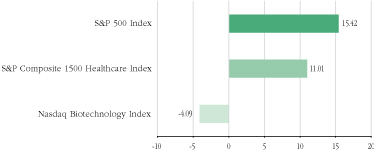

As you know, Tekla Healthcare Opportunities Fund ("THQ" or "the Fund") invests in healthcare/biotechnology. As you may also know, after an extended period of growth, volatility in this sector has been elevated and performance weak as of late. Part of the increased volatility is inherent in our sector while another part probably results from the election season discussion we have been having in the U.S. about the value healthcare brings to our citizens and to what extent the prices of drugs should reflect that value rather than merely production cost. Healthcare fundamentals have been solid in recent years (as reflected generally by the S&P Composite 1500 Healthcare Index®*) and particularly in the biotech sector (as reflected by the NASDAQ Biotechnology Index®*). Strength in healthcare relative to the S&P 500 Index®* over the last five years is illustrated in the following chart.

5 Year Performance

Ending September 30, 2106

It seems pretty clear that questions about pricing have attenuated the upward climb in the healthcare sector since a mid-2015 high. In the last 12 months, this has resulted in a more moderate return for the healthcare sector in general and for biotechnology in particular. We see much of this result as a disconnect between sector potential and performance. It is our view that, as we head into 2017, we may well experience heightened volatility as Mr. Trump's intentions and priorities become clear, but over the longer term, we are confident that we will return to a period where fundamentals drive performance. We see this as a positive for the healthcare/biotechnology sector.

1

Respectfully yours,

Daniel R. Omstead, Ph.D.

President and Portfolio Manager

2

Thoughts on the State of the Healthcare/

Biotechnology Industry

The healthcare/biotechnology sector has been much in the news of late. Moreover, this sector has been drawn into the political discussion surrounding the 2016 national election season. At times, this has caused some volatility and probably some downward movement within the healthcare/biotechnology sector. It is not the first time the sector has been drawn into national debate (recall the discussions surrounding the creation and implementation of the Affordable Care Act ("Obamacare")) nor will it likely be the last.

The current discussion undoubtedly results from a number of both macro and micro factors. On the macro level, healthcare represents nearly 20% of the US economy. Moreover, the sector is growing relatively rapidly and projections suggest that this growth could overwhelm other parts of the economy. Such concern results in much debate, but in the end we believe sector growth reflects its contribution to societal welfare and is good for the Fund and its shareholders.

On the micro level, healthcare is also a significant portion of the "economy". Obamacare has increased the number of people who are covered by health insurance and imposed a number of mandated criteria. Healthcare products and services are difficult and expensive to develop and therefore expensive to purchase. For many years, most Americans paid health insurance premiums (or had them largely paid for by their employers) and received services at relatively modest out-of-pocket costs (i.e., at a low "co-pay") to the individual. Recent trends have, in our view, produced a change in this profile. For a variety of reasons, probably related to the increasing cost/price of healthcare products, we have seen what we expect will be a migration to higher deductible healthcare insurance plans. The consequence has been that, in some cases, the cost to the consumer for certain basic medical products or services has increased, sometimes dramatically. Focusing for the moment on healthcare products rather than services, in some cases, such increases can be the result of over-reaching drug company pricing strategies while in other cases the increases might be the result of fairly priced drugs where the individual or employers have elected to use high deductible plans. Such plans decrease insurance premiums but increase out of pocket costs to the individual at or near the point of care.

This topic has become a controversial issue generating a great deal of public and political attention. Politicians at the national level have spoken aggressively about the need to limit price increases for some drugs. Our

3

view is that a significant portion of this discussion is political rather than substantive as we believe that most drug companies do and will price their drugs based on the value they provide to patients. It is also our view that many or most drugs produce a significant benefit to patients. We would expect that as time goes on, drugs will be more and more targeted to specific patients with specific conditions and that, in the extreme, companies will get paid more when a drug successfully treats a patient's malady and less (or nothing) when the drug is ineffective. We don't see the likelihood of drug price controls or the introduction of a single payer solution as some have suggested or pushed for. In our view, these solutions won't work well. Having said this, the fact of the matter is that we are currently in an environment where a tweet from a national political candidate or other politician can have an impact on the price of a given company's stock and in some cases on the price of a group of stocks. It is our expectation that after Mr. Trump's priorities have been articulated, sector volatility will decrease and the market will be able to focus on the fundamentals of the healthcare/biotechnology sector. We believe these fundamentals are sound.

We continue to be impressed by the potential of the healthcare sector to improve the quality and durability of patients' lives. As we have previously noted, there have been approximately 250 new public companies formed in the healthcare/biotechnology sector over the last several years. These companies are seeking to develop treatments for a myriad of diseases in nearly every area of clinical research. It is difficult to generalize, but we see promising opportunities in treatments aimed at a wide variety of cancers, as well as in the areas of rare diseases, ophthalmology, various blood disorders, the central nervous system, dermatology and antibiotics, among a wide variety of indications.

In addition, we see many developments in the next year or so which are poised to have an effect on healthcare. For example, we note that there are several drugs in late stage development intended for use in Alzheimer's disease. Many people experience a loss of cognitive function, but there are few effective treatments. Results from several late stage clinical trials sponsored by prominent pharmaceutical and biotech companies involving the use of antibody based therapies are expected to be reported in the coming years. If successful, these drugs would be widely used and would help a large number of patients in need.

We are also impressed by progress in the general area of immuno-oncology. This is a field in which drugs or other treatments are used to boost a patient's own immune system, typically to treat hematologic or solid tumors. Initial generations of so-called checkpoint inhibitors which

4

take the "brakes" off a patient's own self limited response to cancer have been remarkably effective in treating lung and other cancers. An additional generation of drugs and treatments stimulate or enhance other aspects of a patient's intrinsic immune response to cancer. Clinical trial results for these so-called immuno-oncology agents have been particularly impressive and have the potential to dramatically improve the lives of certain cancer patients. We would expect FDA approval of one or more new groups in this class soon.

The development of drugs to treat rare diseases is a further example of recent progress. These are diseases which affect a small number of patients. There are upwards of a thousand such diseases which result from a single gene defect. In recent years, we have seen the development of more and more drugs to treat such diseases. We were particularly impressed in the last year to note the FDA's benevolence in approving a drug which appears to have activity in a very rare disease called Duchenne's Muscular Dystrophy. This disease causes debilitating effects and ultimately death, predominantly in young males.

The emergence of generic biological drugs is also notable. Both traditional generic and branded pharmaceutical companies are moving ahead diligently to create and gain approval of drugs that are biosimilar to the now extensive group of biological drugs that have reached the marketplace. This trend should allow the price of some drugs to decrease through competition to the benefit of payers and patients but should also allow the original sponsors to continue to benefit (if at a lower economic reward) after the expiration of governing patents.

Beyond the developments described above, we would also note trends we have observed in the product reimbursement area as being significant. Over the last several years we have seen more competition even for branded products. As an example, multiple antibody products (so-called PCSK9 inhibitors) capable of treating recalcitrant hypercholesterolemia have reached the marketplace. While each of these products is patent protected, due to their similar therapeutic effects, payers have been able to negotiate attractive pricing for these products. We see this trend, along with the development of generic biosimilars, as evidence of enhanced competition in the drug industry.

5

TEKLA HEALTHCARE

OPPORTUNITIES FUND

Fund Essentials

Objective of the Fund

The Fund's investment objective is to seek current income and long-term capital appreciation by investing primarily in securities of healthcare companies. In addition, the Fund seeks to provide regular distribution of income and realized capital gains.

Description of the Fund

Tekla Healthcare Opportunities Fund ("THQ") is a non-diversified closed-end fund traded on the New York Stock Exchange under the ticker THQ. THQ employs a versatile investment strategy with broad access to opportunities within 11 sub-sectors of healthcare and has the ability to invest across a company's full capital structure.

Investment Philosophy

Tekla Capital Management LLC, the Investment Adviser to the Fund, believes that:

• Aging demographics and adoption of new medical products and services can provide long-term tailwinds for healthcare companies

• Late stage biotechnology product pipeline could lead to significant increases in biotechnology sales

• Investment opportunity spans 11 sub-sectors including biotechnology, healthcare technology, managed care and healthcare REITs

• Robust M&A activity in healthcare may create additional investment opportunities

Fund Overview and Characteristics as of 9/30/16

Market Price1 | | $17.48 | |

NAV2 | | $19.14 | |

Premium/(Discount) | | -8.67% | |

Average 30 Day Volume | | 130,973 | |

Net Assets | | $837,073,481 | |

Managed Assets | | $1,062,073,481 | |

Leverage Outstanding | | $225,000,000 | |

Total Leverage Ratio3 | | 21.18% | |

Ticker | | THQ | |

NAV Ticker | | XTHQX | |

Commencement of

Operations Date | |

7/31/14 | |

Fiscal Year

Distributions

Per Share | | $1.65 | |

1 The closing price at which the Fund's shares were traded on the exchange.

2 Per-share dollar value of the Fund, calculated by dividing the total value of all the securities in its portfolio, plus any other assets and less liabilities, by the number of Fund shares outstanding.

3 As a percentage of managed assets.

Holdings of the Fund (Data is based on net assets)

Asset Allocation as of 9/30/16

Sub-Sector Allocation as of 9/30/16

This data is subject to change on a daily basis.

6

TEKLA HEALTHCARE

OPPORTUNITIES FUND

Largest Holdings by Issuer

(Excludes Short-Term Investments)

As of September 30, 2016

| Issuer – Sector | | % of Net

Assets | |

| Gilead Sciences, Inc. – Biotechnology | | | 8.0 | % | |

| Merck & Co., Inc. – Pharmaceuticals | | | 6.5 | % | |

| UnitedHealth Group, Inc. – Health Care Providers & Services | | | 5.8 | % | |

| Abbott Laboratories – Health Care Equipment & Supplies | | | 5.7 | % | |

| Celgene Corporation – Biotechnology | | | 5.1 | % | |

| Biogen Inc. – Biotechnology | | | 5.0 | % | |

| Johnson & Johnson – Pharmaceuticals | | | 4.8 | % | |

| Medtronic plc – Health Care Equipment & Supplies | | | 4.7 | % | |

| Eli Lilly & Company – Pharmaceuticals | | | 4.6 | % | |

| Allergan plc – Pharmaceuticals | | | 4.5 | % | |

| Amgen Inc. – Biotechnology | | | 4.2 | % | |

| Alexion Pharmaceuticals, Inc. – Biotechnology | | | 3.3 | % | |

| CVS Caremark Corporation – Health Care Providers & Services | | | 3.0 | % | |

| Vertex Pharmaceuticals Incorporated – Biotechnology | | | 2.8 | % | |

| ARIAD Pharmaceuticals, Inc. – Biotechnology | | | 2.7 | % | |

| Cigna Corporation – Health Care Providers & Services | | | 2.6 | % | |

| Pfizer, Inc. – Pharmaceuticals | | | 2.6 | % | |

| Humana, Inc. – Healthcare Providers & Services | | | 2.4 | % | |

| Zimmer Biomet Holdings, Inc. – Healthcare Equipment & Supplies | | | 2.3 | % | |

| HCA Holdings, Inc. – Health Care Equipment & Supplies | | | 1.9 | % | |

Fund Performance

THQ is a closed-end fund which invests predominantly in healthcare companies. Subject to regular consideration, the Trustees of THQ have instituted a policy of making monthly distributions to shareholders.

The Fund invests in equity and debt of healthcare companies. The Fund seeks to benefit from the earnings growth of the healthcare industry while capturing income. Income is derived from multiple sources including equity dividends, fixed income coupons, real estate investment trust distributions, convertible securities coupons and selective equity covered call writing premiums. In order to accomplish its objectives, THQ often holds a majority of its assets in equities. Allocation of assets to various healthcare sectors can vary significantly as can the percentage of the portfolio which is overwritten.

7

The Fund may invest up to 15 percent of managed assets, measured at the time of investment, in the debt of healthcare companies. It may also invest up to 25 percent of managed assets in healthcare REITs. The Fund may also hold up to 30 percent of managed assets in convertible securities and may invest a portion of its assets in restricted securities. In order to generate additional "current" income THQ often sells (or writes) calls against a material portion of its equity assets. The portion of equity assets overwritten can vary, but usually represents less than 20 percent of managed assets. At times, the overwritten portion of assets is materially less than 20 percent of managed assets. The use of covered calls is intended to produce "current" income, but may limit upside in bullish markets. The Fund may also use leverage to enhance yield. The Fund may incur leverage up to 20 percent of managed assets at the time of borrowing. "Managed assets" means the total assets of the Fund (including any assets attributable to borrowings for investment purposes) minus the sum of the Fund's accrued liabilities (other than liabilities representing borrowings for investment purposes).

The Fund considers investments in companies of all sizes and in all healthcare subsectors, including but not limited to, biotechnology, pharmaceuticals, healthcare equipment, healthcare supplies, life science tools and services, healthcare distributors, managed healthcare, healthcare technology, and healthcare facilities. The Fund emphasizes innovation, investing both in public and pre-public venture companies. The Fund considers its pre-public and other restricted investments to be a differentiating characteristic. Among the various healthcare subsectors, THQ has considered the biotechnology subsector, including both pre-public and public companies, to be a key contributor to the healthcare sector. The Fund holds biotech assets, including both public and pre-public, often representing 25-35% of net assets.

There is no commonly published index which matches the investment strategy of THQ. With respect to the Fund's equity investments, THQ often holds 20-40% of its managed assets, measured at the time of investment, in biotechnology. By contrast, the S&P Composite 1500 Healthcare Index® ("S15HLTH") consists of more than 160 companies representing most or all of the healthcare subsectors in which THQ typically invests; biotechnology often represents 15-20% of this index. By contrast, the NASDAQ Biotechnology Index® ("NBI"), which contains approximately 180 constituents, is much more narrowly constructed. The vast majority of this index is comprised of biotechnology, pharmaceutical and life science tools companies. In recent years, biotechnology has often represented 72-82% of the NBI. Neither the S15HLTH nor NBI indices contain any material amount of pre-public company assets.

8

The S&P 500 Health Care Corporate Bond Index®* ("SP5HCBIT") measures the performance of U.S. corporate debt issued by constituents in the healthcare sector of the S&P 500 Index® ("SPX"). This index is generally reflective of the debt assets in which THQ invests though the Fund invests in the SPX debt components as well as those of smaller capitalization companies.

The FTSE NAREIT Health Care Property Sector Index®* ("FNHEA") is comprised of U.S. publicly traded REITs in the healthcare sector. This index is generally reflective of the REITs in which THQ invests.

We present both NAV and stock returns for the Fund in comparison to several commonly published indices. We note that THQ is a dynamically configured multi-asset class healthcare growth and income fund. There is no readily available index comprised of similar characteristics to THQ and to which THQ can directly be compared. Therefore, we provide returns for a number of indices representing the major components of THQ's assets. Having said this, we note that there are no readily available indices representing the covered call strategy employed by THQ or the restricted security components of THQ. The following data for available funds over the six-month, one-year and since inception periods are provided for comparison.

Fund Performance for the Period Ended September 30, 2016

| Period | | THQ

NAV | | THQ

MKT | | NBI | | S15HLTH | | SPX | | SP5HCBIT | | FNHEA | |

| 6 month | | | 12.33 | | | | 14.32 | | | | 11.23 | | | | 7.56 | | | | 6.40 | | | | 3.77 | | | | 14.93 | | |

| 1 year | | | 12.44 | | | | 18.25 | | | | -4.09 | | | | 11.01 | | | | 15.42 | | | | 8.77 | | | | 22.40 | | |

inception | | | 8.48 | | | | 1.64 | | | | 6.39 | | | | 9.51 | | | | 6.76 | | | | 5.08 | | | | 10.33 | | |

Inception date July 29,2014

All performance over one-year has been annualized.

Performance data quoted represents past performance, which is no guarantee of future results, and current performance may be lower or higher than the figures shown. The NAV total return takes into account the Fund's total annual expenses and does not reflect transaction charges. If transaction charges were reflected, NAV total return would be reduced. All distributions are assumed to be reinvested either in accordance with the dividend reinvestment plan (DRIP) for market price returns or NAV for NAV returns. Until the DRIP price is available from the Plan Agent, the market price returns reflect the reinvestment at the closing market price on the last business day of the month. Once the DRIP is available around mid-month, the market price returns are updated to reflect reinvestment at the DRIP price.

9

Portfolio Highlights as of September 30, 2016

Among other investments, Tekla Healthcare Opportunities' performance benefitted in the past year from the following:

Immunomedics, Inc. (IMMU) showed significant stock strength over the past year based on generally positive efficacy data for their agent IMMU-132 for a severe subtype of breast cancer known as triple-negative, increasing the value of our convertible debt position.

In Ariad Pharmaceuticals, Inc. (ARIA) we saw improved commercial execution under new management, as well as underappreciated activity of pipeline agent Brigatinib in ALK+ non-small cell lung cancer which helped our convertible debt holding.

Positioning in Bristol-Myers Squibb Company (BMY) had a positive relative impact in 2016. BMY was a significant outperformer for the majority of 2016, however a negative clinical catalyst in August resulted in a below average full year performance.

Among other examples, Tekla Healthcare Opportunities' performance was negatively impacted by the following investments:

AbbVie Inc. (ABBV) experienced a year of relative outperformance in 2016 following a year of significant underperformance in 2015. Our positioning in this name had a negative relative impact on a 1 year basis.

Allergan PLC (AGN) is a large and well diversified pharmaceutical company with products in various therapeutic areas including central nervous system, eye care, aesthetics, dermatology, and gastroenterology. In November 2015, Pfizer announced a merger deal with AGN which we believe would have benefited AGN. However, the merger was ultimately abandoned by Pfizer. AGN's stock price subsequent to Pfizer's abandonment has been poor.

*The trademarks NASDAQ Biotechnology Index®, S&P Composite 1500 Healthcare Index®, S&P 500 Index®, S&P 500 Health Care Corporate Bond Index® and FTSE NAREIT Health Care Property Sector Index® referenced in this report are the property of their respective owners. These trademarks are not owned by or associated with the Fund or its service providers, including Tekla Capital Management LLC.

10

TEKLA HEALTHCARE

OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2016

SHARES | | CONVERTIBLE PREFERRED

STOCKS (Restricted) (a) (b) - 0.6% of Net Assets | | VALUE | |

| | | Biotechnology - 0.5% | |

| | 1,464,497 | | | BioClin Therapeutics, Inc. Series A | | $ | 951,923 | | |

| | 2,133,333 | | | GenomeDx Biosciences, Inc. Series C | | | 3,199,999 | | |

| | | | 4,151,922 | | |

| | | Health Care Equipment & Supplies - 0.1% | |

| | 407,078 | | | IlluminOss Medical, Inc. Series AA | | | 407,078 | | |

| | 383,470 | | | IlluminOss Medical, Inc. Series Junior Preferred | | | 383,470 | | |

| | | | 790,548 | | |

| | | | | TOTAL CONVERTIBLE

PREFERRED STOCKS

(Cost $4,567,718) | | | 4,942,470 | | |

| | | PREFERRED STOCK - 1.6% of Net Assets | |

| | | Real Estate Investment Trust - 1.6% | |

| | 200,000 | | | Welltower, Inc. | | | 13,310,000 | | |

| | | | | TOTAL PREFERRED STOCK

(Cost $11,919,596) | | | 13,310,000 | | |

| | | | | MANDATORY CONVERTIBLE

PREFERRED STOCKS - 1.7% of Net Assets | | | |

| | | Pharmaceuticals - 1.7% | |

| | 5,000 | | | Allergan plc, 5.50% due 03/01/18 | | | 4,108,150 | | |

| | 13,000 | | | Teva Pharmaceutical Industries Ltd.,

7.00% due 12/15/18 | | | 10,573,020 | | |

| | | | | TOTAL MANDATORY CONVERTIBLE

PREFERRED STOCKS

(Cost $18,000,000) | | | 14,681,170 | | |

The accompanying notes are an integral part of these financial statements.

11

TEKLA HEALTHCARE

OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2016

(continued)

PRINCIPAL

AMOUNT | | CONVERTIBLE AND NON-CONVERTIBLE

NOTES - 18.2% of Net Assets

Convertible Notes - 4.9% | | VALUE | |

| | | Biotechnology - 3.2% | |

$ | 14,330,000 | | | ARIAD Pharmaceuticals, Inc.,

3.63% due 6/15/19 (c) | | $ | 22,981,738 | | |

| | 4,000,000 | | | Immunomedics, Inc., 4.75% due 2/15/20 | | | 3,377,500 | | |

| | | | 26,359,238 | | |

| | | Pharmaceuticals - 1.7% | |

| | 13,000,000 | | | Aegerion Pharmaceuticals, Inc.,

2.00% due 8/15/19 (c) | | | 8,571,875 | | |

| | 7,000,000 | | | Egalet Corporation, 5.50% due 4/1/20 (c) | | | 5,963,125 | | |

| | | | 14,535,000 | | |

| | | | | TOTAL CONVERTIBLE NOTES | | | 40,894,238 | | |

| | | Non-Convertible Notes - 13.3% | |

| | | Biotechnology - 1.3% | |

| | 10,000,000 | | | Amgen Inc. 3.63% due 5/15/22 | | | 10,736,860 | | |

| | | | 10,736,860 | | |

| | | Health Care Equipment & Supplies - 1.4% | |

| | 5,000,000 | | | Medtronic, Inc., 3.50% due 3/15/25 | | | 5,384,330 | | |

| | 6,000,000 | | | Zimmer Biomet Holdings, Inc.,

4.25% due 8/15/35 | | | 6,088,812 | | |

| | | | 11,473,142 | | |

| | | Health Care Providers & Services - 8.9% | |

| | 12,693,000 | | | Acadia Healthcare Company. Inc.,

5.13% due 7/01/22 | | | 12,566,070 | | |

| | 10,500,000 | | | Anthem Inc., 3.50% due 8/15/24 | | | 11,054,873 | | |

| | 8,665,000 | | | Cigna Corporation, 5.88% due 3/15/41 | | | 10,891,784 | | |

| | 8,250,000 | | | Express Scripts Holding Company,

6.13% due 11/15/41 | | | 10,217,988 | | |

| | 9,700,000 | | | HCA Holdings, Inc., 6.25% due 2/15/21 | | | 10,524,500 | | |

| | 7,500,000 | | | HealthSouth Corporation,

5.75% due 11/01/24 | | | 7,767,150 | | |

| | 10,500,000 | | | UnitedHealth Group Inc.,

4.38% due 3/15/42 | | | 11,706,251 | | |

| | | | 74,728,616 | | |

The accompanying notes are an integral part of these financial statements.

12

TEKLA HEALTHCARE

OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2016

(continued)

| PRINCIPAL AMOUNT | |

Pharmaceuticals - 1.7% | | VALUE | |

$ | 4,750,000 | | | AstraZeneca PLC, 6.45% due 9/15/37 (f) | | $ | 6,623,699 | | |

| | 780,000 | | | Mallinckrodt International Finance SA,

4.75% due 4/15/23 | | | 702,000 | | |

| | 5,020,000 | | | Wyeth LLC, 5.95% due 4/01/37 | | | 6,713,100 | | |

| | | | 14,038,799 | | |

| | | TOTAL NON-CONVERTIBLE NOTES | | | 110,977,417 | | |

| | | TOTAL CONVERTIBLE AND

NON-CONVERTIBLE NOTES

(Cost $144,301,815) | | | 151,871,655 | | |

SHARES | | COMMON STOCKS AND

WARRANTS - 103.6% of Net Assets | | | |

| | | Biotechnology - 35.8% | |

| | 156 | | | AbbVie Inc. | | | 9,839 | | |

| | 224,090 | | | Alexion Pharmaceuticals, Inc. (b) (d) | | | 27,459,989 | | |

| | 72,601 | | | Alkermes plc (b) | | | 3,414,425 | | |

| | 146,000 | | | Amgen Inc. | | | 24,354,260 | | |

| | 33,451 | | | Ardelyx, Inc. (b) | | | 432,856 | | |

| | 133,931 | | | Biogen Inc. (b) | | | 41,924,421 | | |

| | 137,500 | | | BioMarin Pharmaceutical Inc. (b) | | | 12,721,500 | | |

| | 404,864 | | | Celgene Corporation (b) | | | 42,320,434 | | |

| | 159,000 | | | Cepheid, Inc. (b) | | | 8,377,710 | | |

| | 305,100 | | | Eleven Biotherapeutics, Inc. warrants

(Restricted, expiration 11/24/17) (a) (b) | | | 15,255 | | |

| | 845,719 | | | Gilead Sciences, Inc. (d) | | | 66,913,287 | | |

| | 112,223 | | | Incyte Corporation (b) | | | 10,581,507 | | |

| | 125,100 | | | Juno Therapeutics, Inc. (b) | | | 3,754,251 | | |

| | 300,000 | | | Karyopharm Therapeutics, Inc. (b) | | | 2,919,000 | | |

| | 320,405 | | | Natera, Inc. (b) | | | 3,559,699 | | |

| | 1,409,626 | | | Pieris Pharmaceuticals, Inc. (b) | | | 2,579,615 | | |

| | 40,496 | | | Pieris Pharmaceuticals, Inc., Series A

warrants (Restricted, expiration 6/8/21) (a) (b) | | | 12,959 | | |

| | 20,248 | | | Pieris Pharmaceuticals, Inc., Series B

warrants (Restricted, expiration 6/8/21) (a) (b) | | | 9,314 | | |

| | 165,000 | | | Puma Biotechnology, Inc. (b) | | | 11,063,250 | | |

| | 93,700 | | | Sarepta Therapeutics, Inc. (b) (d) | | | 5,754,117 | | |

The accompanying notes are an integral part of these financial statements.

13

TEKLA HEALTHCARE

OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2016

(continued)

SHARES | | Biotechnology - continued | | VALUE | |

| | 68,700 | | | United Therapeutics Corporation (b) (d) | | $ | 8,112,096 | | |

| | 265,543 | | | Vertex Pharmaceuticals Incorporated (b) (d) | | | 23,158,005 | | |

| | | | 299,447,789 | | |

| | | Health Care Equipment & Supplies - 13.3% | |

| | 1,138,300 | | | Abbott Laboratories (d) | | | 48,138,707 | | |

| | 32,278 | | | Becton Dickinson and Co. | | | 5,801,325 | | |

| | 773,500 | | | Endologix, Inc. (b) | | | 9,900,800 | | |

| | 397,030 | | | Medtronic plc | | | 34,303,392 | | |

| | 102,300 | | | Zimmer Biomet Holdings, Inc. | | | 13,301,046 | | |

| | | | 111,445,270 | | |

| | | Health Care Providers & Services - 19.1% | |

| | 134,007 | | | AmerisourceBergen Corporation | | | 10,825,085 | | |

| | 112,200 | | | Centene Corporation (b) | | | 7,512,912 | | |

| | 60,950 | | | Charles River Laboratories International, Inc. (b) | | | 5,079,573 | | |

| | 86,400 | | | Cigna Corporation | | | 11,259,648 | | |

| | 209,572 | | | Community Health Systems, Inc. (b) | | | 2,418,461 | | |

| | 278,479 | | | CVS Caremark Corporation (d) | | | 24,781,846 | | |

| | 161,100 | | | DaVita, Inc. (b) (d) | | | 10,643,877 | | |

| | 65,784 | | | HCA Holdings, Inc. (b) | | | 4,975,244 | | |

| | 112,000 | | | Humana, Inc. | | | 19,811,680 | | |

| | 190,000 | | | Molina Healthcare, Inc. (b) | | | 11,080,800 | | |

| | 52,393 | | | Quorum Health Corporation (b) | | | 328,504 | | |

| | 164,500 | | | Tenet Healthcare Corporation (b) | | | 3,727,570 | | |

| | 264,121 | | | UnitedHealth Group, Inc. | | | 36,976,940 | | |

| | 86,604 | | | Universal Health Services, Inc. | | | 10,671,345 | | |

| | | | 160,093,485 | | |

| | | Health Care Technology - 0.3% | |

| | 173,600 | | | Allscripts Healthcare Solutions, Inc. (b) | | | 2,286,312 | | |

| | | Life Sciences Tools & Services - 1.9% | |

| | 249,600 | | | Agilent Technologies, Inc. | | | 11,753,664 | | |

| | 25,750 | | | Thermo Fisher Scientific Inc. | | | 4,095,795 | | |

| | | | 15,849,459 | | |

| | | Pharmaceuticals - 23.5% | |

| | 145,970 | | | Allergan plc (b) (d) | | | 33,618,351 | | |

| | 87,163 | | | Diplomat Pharmacy, Inc. (b) | | | 2,441,436 | | |

| | 478,005 | | | Eli Lilly & Company (d) | | | 38,364,681 | | |

| | 337,312 | | | Johnson & Johnson | | | 39,846,666 | | |

| | 870,500 | | | Merck & Co., Inc. | | | 54,327,905 | | |

The accompanying notes are an integral part of these financial statements.

14

TEKLA HEALTHCARE

OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2016

(continued)

SHARES | | Pharmaceuticals - continued | | VALUE | |

| | 70,900 | | | Mylan NV (b) (d) | | $ | 2,702,708 | | |

| | 646,037 | | | Pfizer, Inc. | | | 21,881,273 | | |

| | 72,300 | | | Teva Pharmaceutical Industries Ltd. (d) (e) | | | 3,326,523 | | |

| | | | 196,509,543 | | |

| | | Real Estate Investment Trusts - 9.7% | |

| | 203,105 | | | Care Capital Properties, Inc. | | | 5,788,493 | | |

| | 106,212 | | | LTC Properties, Inc. | | | 5,521,962 | | |

| | 709,455 | | | Medical Properties Trust, Inc. | | | 10,478,650 | | |

| | 413,116 | | | Omega Healthcare Investors, Inc. | | | 14,644,962 | | |

| | 530,672 | | | Physicians Realty Trust | | | 11,430,675 | | |

| | 456,190 | | | Sabra Health Care REIT, Inc. | | | 11,486,864 | | |

| | 479,604 | | | Senior Housing Properties Trust | | | 10,891,807 | | |

| | 15,000 | | | Ventas Realty, LP / Ventas Capital

Corporation | | | 399,900 | | |

| | 152,491 | | | Ventas, Inc. | | | 10,770,439 | | |

| | | | 81,413,752 | | |

| | | | | Real Estate Management &

Development - 0.0% | | | |

| | 5,323 | | | The RMR Group Inc, Class A | | | 201,955 | | |

| | | | 201,955 | | |

| | | | | TOTAL COMMON STOCKS

AND WARRANTS

(Cost $890,259,629) | | | 867,247,565 | | |

PRINCIPAL

AMOUNT | | SHORT-TERM INVESTMENT - 2.1% of

Net Assets | | | |

$ | 18,034,000 | | | Repurchase Agreement, Fixed Income Clearing

Corp., repurchase value $18,034,000,

0.03%, dated 09/30/16, due 10/03/16

(collateralized by U.S. Treasury

Note 3.50%, due 5/15/20, market value

$18,395,213) | | | 18,034,000 | | |

| | | | | TOTAL SHORT-TERM INVESTMENTS

(Cost $18,034,000) | | | 18,034,000 | | |

| | | | | TOTAL INVESTMENTS - 127.8%

(Cost $1,087,082,758) | | | 1,070,086,860 | | |

The accompanying notes are an integral part of these financial statements.

15

TEKLA HEALTHCARE

OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

SEPTEMBER 30, 2016

(continued)

NUMBER OF

CONTRACTS

(100 SHARES

EACH) | | CALL OPTION CONTRACTS

WRITTEN - (0.1)%

of Net Assets | | VALUE | |

| | 2,539 | | | Abbott Laboratories Oct16 43 Call | | $ | (139,645 | ) | |

| | 822 | | | Alexion Pharmaceuticals, Inc. Oct16 133 Call | | | (50,964 | ) | |

| | 263 | | | Allergan plc Oct16 260 Call | | | (3,945 | ) | |

| | 1,182 | | | CVS Caremark Corporation Oct16 91 Call | | | (68,556 | ) | |

| | 1,611 | | | DaVita, Inc. Oct16 67.5 Call | | | (88,605 | ) | |

| | 1,327 | | | Eli Lilly & Company Oct16 82 Call | | | (92,890 | ) | |

| | 1,300 | | | Gilead Sciences, Inc. Oct16 86 Call | | | (19,500 | ) | |

| | 709 | | | Mylan NV Oct16 43.5 Call | | | (4,609 | ) | |

| | 937 | | | Sarepta Therapeutics, Inc. Oct16 60 Call | | | (356,060 | ) | |

| | 686 | | | Teva Pharmaceutical Industries Ltd.

Oct16 53.5 Call | | | (4,802 | ) | |

| | 189 | | | United Therapeutics Corporation

Oct16 130 Call | | | (6,615 | ) | |

| | 227 | | | Vertex Pharmaceuticals Incorporated

Oct16 96.5 Call | | | (17,025 | ) | |

| | | | | TOTAL CALL OPTION CONTRACTS

WRITTEN

(Premiums received $1,441,696) | | | (853,216 | ) | |

| | | | | TOTAL INVESTMENTS LESS CALL

OPTION CONTRACTS

WRITTEN - 127.7%

(Cost $1,085,641,062) | | | 1,069,233,644 | | |

| | | | | OTHER LIABILITIES IN EXCESS

OF OTHER ASSETS - (27.7)% | | | (232,160,163 | ) | |

| | | | | NET ASSETS - 100% | | $ | 837,073,481 | | |

(a) Security fair valued. See Investment Valuation and Fair Value Measurements.

(b) Non-income producing security.

(c) Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

(d) A portion of security is pledged as collateral for call options written.

(e) American Depository Receipt

(f) Foreign security.

The accompanying notes are an integral part of these financial statements.

16

TEKLA HEALTHCARE

OPPORTUNITIES FUND

STATEMENT OF ASSETS AND LIABILITIES

SEPTEMBER 30, 2016

ASSETS: | |

Investments, at value (cost $1,087,082,758) | | $ | 1,070,086,860 | | |

Cash | | | 533 | | |

Dividends and interest receivable | | | 2,337,203 | | |

Receivable for investments sold | | | 158,480 | | |

Prepaid expenses | | | 137,159 | | |

Total assets | | | 1,072,720,235 | | |

LIABILITIES: | |

Payable for investments purchased | | | 7,721,280 | | |

Accrued advisory fee | | | 905,123 | | |

Accrued investor support service fees | | | 45,256 | | |

Accrued shareholder reporting fees | | | 47,257 | | |

Accrued trustee fees | | | 565 | | |

Loan Payable | | | 225,000,000 | | |

Options written, at value (premium received $1,441,696) | | | 853,216 | | |

Income distribution payable | | | 219,228 | | |

Interest payable | | | 731,398 | | |

Accrued other | | | 123,431 | | |

Total liabilities | | | 235,646,754 | | |

Commitments and Contingencies (see Note 1) | | | | | |

NET ASSETS | | $ | 837,073,481 | | |

SOURCES OF NET ASSETS: | |

Shares of beneficial interest, par value $.01 per share,

unlimited number of shares authorized, amount paid

in on 43,725,090 shares issued and outstanding | | $ | 833,597,610 | | |

Accumulated net investment loss | | | (219,228 | ) | |

Accumulated net realized gain on investments and

options | | | 20,102,517 | | |

Net unrealized loss on investments and options | | | (16,407,418 | ) | |

Total net assets (equivalent to $19.14 per

share based on 43,725,090 shares outstanding) | | $ | 837,073,481 | | |

The accompanying notes are an integral part of these financial statements.

17

TEKLA HEALTHCARE

OPPORTUNITIES FUND

STATEMENT OF OPERATIONS

YEAR ENDED SEPTEMBER 30, 2016

INVESTMENT INCOME: | |

Dividend income (net of foreign tax of $140,970) | | $ | 15,600,688 | | |

Interest and other income | | | 7,577,333 | | |

Total investment income | | | 23,178,021 | | |

EXPENSES: | |

Advisory fees | | | 10,368,888 | | |

Interest expense | | | 3,092,735 | | |

Investor support service fees | | | 645,315 | | |

Administration fees | | | 166,693 | | |

Auditing fees | | | 38,730 | | |

Shareholder reporting | | | 160,393 | | |

Trustees' fees and expenses | | | 139,110 | | |

Custodian fees | | | 139,039 | | |

Legal fees | | | 125,313 | | |

Transfer agent fees | | | 26,349 | | |

Other (see Note 2) | | | 407,949 | | |

Total expenses | | | 15,310,514 | | |

Net investment gain | | | 7,867,507 | | |

REALIZED AND UNREALIZED GAIN (LOSS): | |

Net realized gain (loss) on: | |

Investments | | | 24,642,204 | | |

Closed or expired option contracts written | | | 6,767,438 | | |

Net realized gain | | | 31,409,642 | | |

Change in unrealized appreciation (depreciation) | |

Investments | | | 50,432,066 | | |

Option contracts written | | | (1,127,168 | ) | |

Change in unrealized appreciation (depreciation) | | | 49,304,898 | | |

Net realized and unrealized gain (loss) | | | 80,714,540 | | |

Net increase in net assets resulting

from operations | | $ | 88,582,047 | | |

The accompanying notes are an integral part of these financial statements.

18

TEKLA HEALTHCARE

OPPORTUNITIES FUND

STATEMENTS OF CHANGES IN NET ASSETS

| | | Year ended

September 30,

2016 | | Year ended

September 30,

2015 | |

NET INCREASE (DECREASE) IN

NET ASSETS RESULTING FROM

OPERATIONS: | |

Net investment gain | | $ | 7,867,507 | | | $ | 4,665,864 | | |

Net realized gain | | | 31,409,642 | | | | 101,554,427 | | |

Change in net unrealized

appreciation (depreciation) | | | 49,304,898 | | | | (71,464,348 | ) | |

Net increase in net assets

resulting from operations | | | 88,582,047 | | | | 34,755,943 | | |

DISTRIBUTIONS TO SHAREHOLDERS

FROM: | |

Net investment income | | | (72,504,372 | ) | | | (59,235,598 | ) | |

Total distributions | | | (72,504,372 | ) | | | (59,235,598 | ) | |

CAPITAL SHARE TRANSACTIONS: | |

Fund shares repurchased (153,131 and

0 shares, respectively) (see Note 1) | | | (2,709,105 | ) | | | — | | |

Total capital share transactions | | | (2,709,105 | ) | | | — | | |

Net increase (decrease) in

net assets | | | 13,368,570 | | | | (24,479,655 | ) | |

NET ASSETS: | |

Beginning of year | | | 823,704,911 | | | | 848,184,566 | | |

End of year | | $ | 837,073,481 | | | $ | 823,704,911 | | |

Accumulated net investment loss

included in net assets at end of year | | ($ | 219,228 | ) (a) | | ($ | 319,519 | ) (a) | |

(a) Reflects reclassifications to the Fund's capital accounts to reflect income and gains available for distribution under income tax regulations.

The accompanying notes are an integral part of these financial statements.

19

TEKLA HEALTHCARE

OPPORTUNITIES FUND

STATEMENT OF CASH FLOWS

YEAR ENDED SEPTEMBER 30, 2016

CASH FLOWS FROM OPERATING ACTIVITIES: | |

Purchases of portfolio securities | | ($ | 475,413,339 | ) | |

Purchases to close option contracts written | | | (69,206 | ) | |

Net maturities of short-term investments | | | (6,851,000 | ) | |

Sales of portfolio securities | | | 541,672,830 | | |

Proceeds from option contracts written | | | 8,252,345 | | |

Interest income received | | | 7,678,346 | | |

Dividend income received | | | 15,765,047 | | |

Other operating receipts (expenses paid) | | | (16,040,348 | ) | |

Net cash provided from operating activities | | | 74,994,675 | | |

CASH FLOWS FROM FINANCING ACTIVITIES: | |

Cash distributions paid | | | (72,285,144 | ) | |

Fund shares repurchased | | | (2,709,105 | ) | |

Net cash used for financing activities | | | (74,994,249 | ) | |

NET INCREASE IN CASH | | | 426 | | |

CASH AT BEGINNING OF YEAR | | | 107 | | |

CASH AT END OF YEAR | | $ | 533 | | |

RECONCILIATION OF NET INCREASE IN NET ASSETS

RESULTING FROM OPERATIONS TO NET CASH

PROVIDED FROM OPERATING ACTIVITIES: | |

Net increase in net assets resulting from operations | | $ | 88,582,047 | | |

Purchases of portfolio securities | | | (475,413,339 | ) | |

Purchases to close option contracts written | | | (69,206 | ) | |

Net maturities of short-term investments | | | (6,851,000 | ) | |

Sales of portfolio securities | | | 541,672,830 | | |

Proceeds from option contracts written | | | 8,252,345 | | |

Accretion of discount | | | (280,794 | ) | |

Net realized gain on investments and options | | | (31,409,642 | ) | |

Increase in net unrealized appreciation

(depreciation) on investments and options | | | (49,304,898 | ) | |

Decrease in dividends and interest receivable | | | 546,166 | | |

Decrease in accrued expenses | | | (588,206 | ) | |

Decrease in prepaid expenses and interest payable | | | (141,628 | ) | |

Net cash provided from operating activities | | $ | 74,994,675 | | |

The accompanying notes are an integral part of these financial statements.

20

TEKLA HEALTHCARE

OPPORTUNITIES FUND

FINANCIAL HIGHLIGHTS

| | | Year ended

September 30,

2016 | | Year ended

September 30,

2015 | | Period

July 31,

2014 to

September 30,

2014 (1) | |

OPERATING PERFORMANCE FOR A SHARE

OUTSTANDING THROUGHOUT EACH PERIOD | |

Net asset value per share, beginning of period | | $ | 18.77 | | | $ | 19.33 | | | $ | 19.10 | (2) | |

Net investment income (loss) (3) | | | 0.18 | | | | 0.11 | | | | (0.01 | ) | |

Net realized and unrealized gain | | | 1.78 | | | | 0.68 | | | | 0.39 | | |

Total increase (decrease) from investment operations | | | 1.96 | | | | 0.79 | | | | 0.38 | | |

Distributions to shareholders from: | |

Income distributions to shareholders | | | (1.65 | ) | | | (1.35 | ) | | | (0.11 | ) | |

Total distributions | | | (1.65 | ) | | | (1.35 | ) | | | (0.11 | ) | |

Capital charges with respect to issuance of shares | | | — | | | | — | | | | (0.04 | ) | |

Increase resulting from shares repurchased (3) | | | 0.06 | | | | — | | | | — | | |

Net asset value per share, end of period | | $ | 19.14 | | | $ | 18.77 | | | $ | 19.33 | | |

Per share market value, end of period | | $ | 17.48 | | | $ | 16.30 | | | $ | 18.85 | | |

Total investment return at market value | | | 18.25 | % | | | (7.37 | %) | | | (5.42 | %)* | |

Total investment return at net asset value | | | 12.44 | % | | | 4.02 | % | | | 2.02 | %* | |

RATIOS | |

Expenses to average net assets | | | 1.88 | % | | | 1.60 | % | | | 1.28 | %** | |

Expenses, excluding interest expense, to average net assets | | | 1.50 | % | | | 1.44 | % | | | 1.28 | %** | |

Net investment income (loss) to average net assets | | | 0.96 | % | | | 0.50 | % | | | (0.41 | %)** | |

SUPPLEMENTAL DATA | |

Net assets at end of period (in millions) | | $ | 837 | | | $ | 824 | | | $ | 848 | | |

Portfolio turnover rate | | | 48.24 | % | | | 92.61 | % | | | 19.61 | %* | |

* Not Annualized.

** Annualized.

(1) Commenced operations on July 31, 2014.

(2) Net asset value beginning of period reflects a deduction of $0.90 per share sales charge from the initial offering price of $20.00 per share.

(3) Computed using average shares outstanding.

The accompanying notes are an integral part of these financial statements.

21

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(1) Organization and Significant Accounting Policies

Tekla Healthcare Opportunities Fund (the Fund) is a Massachusetts business trust formed on April 2, 2014 and registered under the Investment Company Act of 1940 as a non-diversified closed-end management investment company. The Fund commenced operations on July 31, 2014. The Fund's investment objective is to seek current income and long-term capital appreciation through investments in U.S. and non-U.S. companies in the healthcare industry (including equity securities, debt securities and pooled investment vehicles). The Fund invests primarily in securities of public and private companies believed by the Fund's Investment Adviser, Tekla Capital Management LLC (the Adviser), to have significant potential for above-average growth. The Fund may invest in private companies and other restricted securities, including private investments in public equity and venture capital investments, if these securities would currently comprise 10% or less of Managed Assets.

The preparation of these financial statements requires the use of certain estimates by management in determining the Fund's assets, liabilities, revenues and expenses. Actual results could differ from these estimates and such differences could be material. The following is a summary of significant accounting policies followed by the Fund, which are in conformity with accounting principles generally accepted in the United States of America ("GAAP"). The Fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board Accounting Standards Codification 946. Events or transactions occurring after September 30, 2016, through the date that the financial statements were issued, have been evaluated in the preparation of these financial statements.

Derivatives Strategy Changes

Earlier this year, the Board approved an expanded use of derivatives by the Fund. Prior to this approval, the Fund's investment strategy provided that the Fund would not invest more than 30% of its Managed Assets as measured at the time of investment, in derivatives, including options, futures, options on futures, forwards, swaps, options on swaps and other derivatives, for hedging purposes. The Board approved the Fund's use of these derivatives for non-hedging purposes as well. Accordingly, the Fund may now also invest in derivatives for hedging and non-hedging purposes, subject to a limit of 10% of its Managed Assets in derivatives other than its option writing strategy.

A revised description of the Fund's investment strategy with respect to derivatives is as follows: The Fund will not invest more than 30% of its Managed Assets (the total assets of the Fund (including any assets attributable to borrowings for investment purposes) minus the sum of the Fund's accrued liabilities (other than liabilities representing borrowings for investment purposes)) as measured at the time of investment in derivatives, including options, futures, options on futures, forwards, swaps, options on swaps and other derivatives. The Fund employs a strategy of writing (selling) covered call options on a portion of the common stocks in its portfolio, writing (selling) put options on a portion of the common stocks in its portfolio and, to a lesser extent, writing (selling) covered call and writing (selling) put options on indices of securities and sectors of securities generally within the healthcare industry. This option strategy is intended to generate current income from option premiums as a means to enhance distributions payable to the Fund's Shareholders. Over time, as the Fund's portfolio becomes more seasoned, its ability to benefit from capital appreciation may become more limited, and the Fund will lose money to the extent that it writes covered call options and the

22

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(continued)

securities on which it writes the option appreciates above the exercise price of the option by an amount that exceeds the exercise price of the option. Therefore, over time, the Adviser may choose to decrease its use of the option writing strategy to the extent that it may negatively impact the Fund's ability to benefit from capital appreciation. Other than the Fund's option strategy, the Fund may invest up to 10% of its Managed Assets in derivatives. Derivative instruments can be illiquid, may disproportionately increase losses, and may have a potentially large adverse impact on Fund performance.

Although both OTC and exchange-traded derivatives markets may experience the lack of liquidity, OTC non-standardized derivative transactions are generally less liquid than exchange-traded instruments. The illiquidity of the derivatives markets may be due to various factors, including congestion, disorderly markets, limitations on deliverable supplies, the participation of speculators, government regulation and intervention, and technical and operational or system failures. In addition, daily limits on price fluctuations and speculative position limits on exchanges on which the Fund may conduct its transactions in derivative instruments may prevent prompt liquidation of positions, subjecting the Fund to the potential of greater losses. Losses from investments in derivative instruments can result from a lack of correlation between changes in the value of derivative instruments and the portfolio assets (if any) being hedged, the potential illiquidity of the markets for derivative instruments, the failure of the counterparty to perform its contractual obligations, or the risks arising from margin requirements and related leverage factors associated with such transactions. Losses may also arise if the Fund receives cash collateral under the transactions and some or all of that collateral is invested in the market. To the extent that cash collateral is so invested, such collateral will be subject to market depreciation or appreciation, and the Fund may be responsible for any loss that might result from its investment of the counterparty's cash collateral. The use of these management techniques also involves the risk of loss if the Adviser is incorrect in its expectation of the timing or level of fluctuations in securities prices, interest rates or currency prices. Investments in derivative instruments may be harder to value, subject to greater volatility and more likely subject to changes in tax treatment than other investments. For these reasons, the Adviser's use of derivative instruments may not be successful. Trading in derivative instruments can result in large amounts of leverage. Thus, the leverage offered by trading in derivative instruments will magnify the gains and losses experienced by the Fund and could cause the Fund's net asset value to be subject to wider fluctuations than would be the case if the Fund did not use the leverage feature in derivative instruments.

Investment Valuation

Shares of publicly traded companies listed on national securities exchanges or trading in the over-the-counter market are typically valued at the last sale price, as of the close of trading, generally 4 p.m., Eastern time. The Board of Trustees of the Fund (the "Trustees") has established and approved fair valuation policies and procedures with respect to securities for which quoted prices may not be available or which do not reflect fair value. Convertible bonds, corporate and government bonds are valued using a third-party pricing service. Convertible bonds are valued using this pricing service only on days when there is no sale reported. Puts and calls generally are valued at the close of regular trading on the securities or commodities exchange on which they are primarily traded. Options on securities generally are valued at their last sale price in the case of exchange traded options or, in the case of OTC-traded options, the average of the last sale price as obtained from two or more dealers unless there is only

23

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(continued)

one dealer, in which case that dealer's price is used. Gain or loss is recognized when the option contract expires, is exercised, or is closed. Forward foreign currency contracts are valued on the basis of the value of the underlying currencies at the prevailing currency exchange rate. Restricted securities of companies that are publicly traded are typically valued based on the closing market quote on the valuation date adjusted for the impact of the restriction as determined in good faith by the Adviser also using fair valuation policies and procedures approved by the Trustees described below. Non-exchange traded warrants of publicly traded companies are generally valued using the Black-Scholes model, which incorporates both observable and unobservable inputs. Short-term investments with a maturity of 60 days or less are generally valued at amortized cost, which approximates fair value.

Convertible preferred shares, warrants or convertible note interests in private companies, milestone interests, and other restricted securities, as well as shares of publicly traded companies for which market quotations are not readily available, such as stocks for which trading has been halted or for which there are no current day sales, or which do not reflect fair value, are typically valued in good faith, based upon the recommendations made by the Adviser pursuant to fair valuation policies and procedures approved by the Trustees.

The Adviser has a Valuation Sub-Committee comprised of senior management which reports to the Valuation Committee of the Board at least quarterly. Each fair value determination is based on a consideration of relevant factors, including both observable and unobservable inputs. Observable and unobservable inputs the Adviser considers may include (i) the existence of any contractual restrictions on the disposition of securities; (ii) information obtained from the company, which may include an analysis of the company's financial statements, the company's products or intended markets or the company's technologies; (iii) the price of the same or similar security negotiated at arm's length in an issuer's completed subsequent round of financing; (iv) the price and extent of public trading in similar securities of the issuer or of comparable companies; or (v) a probability and time value adjusted analysis of contractual terms. Where available and appropriate, multiple valuation methodologies are applied to confirm fair value. Significant unobservable inputs identified by the Adviser are often used in the fair value determination. A significant change in any of these inputs may result in a significant change in the fair value measurement. Due to the uncertainty inherent in the valuation process, such estimates of fair value may differ significantly from the values that would have been used had a ready market for the investments existed, and differences could be material. Additionally, changes in the market environment and other events that may occur over the life of the investments may cause the gains or losses ultimately realized on these investments to be different from the valuations used at the date of these financial statements.

Options on Securities

An option contract is a contract in which the writer (seller) of the option grants the buyer of the option, upon payment of a premium, the right to purchase from (call option) or sell to (put option) the writer a designated instrument at a specified price within a specified period of time. Certain options, including options on indices, will require cash settlement by the Fund if the option is exercised. The Fund enters into option contracts in order to hedge against potential adverse price movements in the value of portfolio assets, as a temporary substitute for selling selected investments, to lock in the purchase price of a security or currency which it expects to purchase in the near future, as a temporary substitute for

24

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(continued)

purchasing selected investments, or to enhance potential gain or to gain or hedge exposure to financial market risk.

The Fund's obligation under an exchange traded written option or investment in an exchange-traded purchased option is valued at the last sale price or in the absence of a sale, the mean between the closing bid and asked prices.

If the Fund writes a covered call option, the Fund foregoes, in exchange for the premium, the opportunity to profit during the option period from an increase in the market value of the underlying security above the exercise price. If the Fund writes a put option it accepts the risk of a decline in the market value of the underlying security below the exercise price. Over-the-counter options have the risk of the potential inability of counterparties to meet the terms of their contracts. The Fund's maximum exposure to purchased options is limited to the premium initially paid. In addition, certain risks may arise upon entering into option contracts including the risk that an illiquid secondary market will limit the Fund's ability to close out an option contract prior to the expiration date and that a change in the value of the option contract may not correlate exactly with changes in the value of the securities or currencies hedged.

All options on securities and securities indices written by the Fund are required to be covered. When the Fund writes a call option, this means that during the life of the option the Fund may own or have the contractual right to acquire the securities subject to the option or may maintain with the Fund's custodian in a segregated account appropriate liquid securities in an amount at least equal to the market value of the securities underlying the option. When the Fund writes a put option, this means that the Fund will maintain with the Fund's custodian in a segregated account appropriate liquid securities in an amount at least equal to the exercise price of the option.

Transactions in call options written for the year ended September 30, 2016 were as follows:

| | | Contracts | | Premiums | |

Options outstanding, September 30, 2015 | | | 9,815 | | | $ | 2,210,005 | | |

Options written | | | 56,500 | | | | 8,252,345 | | |

Options terminated in closing purchase transactions | | | (2,751 | ) | | | (226,665 | ) | |

Options exercised | | | (13,750 | ) | | | (2,184,010 | ) | |

Options expired | | | (38,022 | ) | | | (6,609,979 | ) | |

Options outstanding, September 30, 2016 | | | 11,792 | | | $ | 1,441,696 | | |

Average Number of Contracts | | | 5,056 | | | | | | |

Derivatives not accounted

for as hedging instruments

under ASC 815 | | Statement of Assets and

Liabilities Location | | Statement of Operations Location | |

Equity Contracts

| |

| | Liabilities, options

written, at value

| | |

$853,216

| | | Net realized gain on

closed or expired option

contracts written | | |

$6,767,438 | | |

| | | | | | | | | | | | | Change in unrealized

appreciation (depreciation)

on option contracts

written | | | ($1,127,168) | | |

25

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(continued)

Investment Transactions and Income

Investment transactions are recorded on a trade date basis. Gains and losses from sales of investments are recorded using the "identified cost" method. Interest income is recorded on the accrual basis, adjusted for amortization of premiums and accretion of discounts. Dividend income is recorded on the ex-dividend date, less any foreign taxes withheld. Upon notification from issuers, some of the dividend income received may be redesignated as a reduction of cost of the related investment if it represents a return of capital.

The aggregate cost of purchases and proceeds from sales of investment securities (other than short-term investments) for the year ended September 30, 2016 totaled $476,032,438 and $534,750,308, respectively.

Repurchase Agreements

In managing short-term investments the Fund may from time to time enter into transactions in repurchase agreements. In a repurchase agreement, the Fund's custodian takes possession of the underlying collateral securities from the counterparty, the market value of which is at least equal to the principal, including accrued interest, of the repurchase transaction at all times. In the event of default or bankruptcy by the other party to the agreement, realization and/or retention of the collateral by the Fund may be delayed. The Fund may enter into repurchase transactions with any broker, dealer, registered clearing agency or bank. Repurchase agreement transactions are not counted for purposes of the limitations imposed on the Fund's investment in debt securities.

Distribution Policy

Pursuant to a Securities and Exchange Commission exemptive order the Fund may make periodic distributions that include capital gains as frequently as 12 times in any one taxable year in respect of its common shares, and the Fund has implemented a managed distribution policy (the Policy) providing for monthly distributions at a rate set by the Board of Trustees. Under the current Policy, the Fund intends to make monthly distributions at a rate of $0.1125 per share to shareholders of record. If taxable income and net long-term realized gains exceed the amount required to be distributed under the Policy, the Fund will at a minimum make distributions necessary to comply with the requirements of the Internal Revenue Code. The Policy has been established by the Trustees and may be changed by them without shareholder approval. The Trustees regularly review the Policy and the frequency and distribution rate considering the purpose and effect of the Policy, the financial market environment, and the Fund's income, capital gains and capital available to pay distributions.

Share Repurchase Program

In March 2016, the Trustees approved the renewal of the share repurchase program to allow the Fund to purchase up to 12% of its outstanding common shares in the open market for a one-year period beginning July 11, 2016. Prior to this renewal, in March 2015, the Trustees approved the renewal of the share repurchase program to allow the Fund to repurchase up to 12% of its outstanding shares for a one year period beginning July 11, 2015. The share repurchase program is intended to enhance shareholder value and potentially reduce the discount between the market price of the Fund's shares and the Fund's net asset value.

26

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(continued)

During the year ended September 30, 2016 the Fund repurchased 153,131 shares at a total cost of $2,709,105. The weighted average discount per share between the cost of repurchase and the net asset value applicable to such shares at the date of repurchase was 8.76%.

During the period July 11, 2015 to September 30, 2015, the Fund did not repurchase any shares through the repurchase program.

Federal Taxes

It is the Fund's policy to comply with the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute to its shareholders substantially all of its taxable income and its net realized capital gains, if any. Therefore, no Federal income or excise tax provision is required.

As of September 30, 2016, the Fund had no uncertain tax positions that would require financial statement recognition or disclosure. The Fund's federal tax returns are subject to examination by the Internal Revenue Service for a period of three years.

Distributions

The Fund records all distributions to shareholders on the ex-dividend date. Such distributions are determined in conformity with income tax regulations, which may differ from GAAP. These differences include temporary and permanent differences from losses on wash sale transactions, installment sale adjustments and ordinary loss netting to reduce short term capital gains. Reclassifications are made to the Fund's capital accounts to reflect income and gains available for distribution under income tax regulations. At September 30, 2016, the Fund reclassified $64,737,156 from accumulated net realized gain on investment and $64,737,156 to accumulated net investment loss, to adjust for current period book/tax differences.

The tax basis components of distributable earnings and the tax cost as of September 30, 2016 were as follows:

Cost of Investments for tax purposes | | $ | 1,085,480,445 | | |

Gross tax unrealized appreciation | | $ | 73,355,421 | | |

Gross tax unrealized depreciation | | ($ | 89,602,222 | ) | |

Net tax unrealized depreciation on investments | | ($ | 16,246,801 | ) | |

Undistributed long-term capital gains | | $ | 19,941,900 | | |

The Fund has designated the distributions for its taxable years ended September 30, 2016 and 2015 as follows:

| | | 2016 | | 2015 | |

Ordinary income (includes short-term capital gain) | | $ | 60,171,751 | | | $ | 59,235,598 | | |

Long-term capital gain | | $ | 12,332,621 | | | $ | — | | |

Statement of Cash Flows

The cash amount shown in the Statement of Cash Flows is the amount included in the Fund's Statement of Assets and Liabilities and represents cash on hand at September 30, 2016.

27

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(continued)

Commitments and Contingencies

Under the Fund's organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into agreements with service providers that may contain indemnification clauses. The Fund's maximum exposure under these agreements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

Loan Payable

The Fund maintains a $225,000,000 line of credit with the Bank of Nova Scotia (the "Line of Credit") which expires on January 6, 2017. As of September 30, 2016, the Fund had drawn down $225,000,000 from the Line of Credit, which was the maximum borrowing outstanding during the period. The Fund is charged interest at the rate of 0.70% above the relevant LIBOR rate adjusted by the Statutory Reserve Rate for borrowing (per annum). The Fund is also charged a commitment fee on the daily unused balance of the line of credit at the rate of 0.25% (per annum). Per the Line of Credit agreement, the Fund paid an upfront fee of 0.10% on the total line of credit balance, which is being amortized through January 4, 2017. The Fund pledges its investment securities as the collateral for the line of credit per the terms of the agreement. The weighted average interest rate and the weighted average outstanding loan payable for the period from October 1, 2015 to September 30, 2016 were 1.3579% and $225,000,000, respectively. The stated carrying amount of the line of credit approximates its fair value based upon the short term nature of the borrowings and the interest rates being based upon the market terms. The borrowings under the line of credit would be considered as Level 2 in the fair value hierarchy (See Note 3) at September 30, 2016.

Investor Support Services

The Fund has retained Destra Capital Investment LLC to provide investor support services in connection with the ongoing operation of the Fund. The Fund will pay Destra a fee in an annual amount equal to, (i) 0.10% of the average aggregate daily value of the Fund's Managed Assets from July 31, 2015 to December 31, 2015 and (ii) 0.05% of the average aggregate daily value of the Fund's Managed Assets from January 1, 2016 through the remaining term of the investor support services agreement.

(2) Investment Advisory and Other Affiliated Fees

The Fund has entered into an Investment Advisory Agreement (the Advisory Agreement) with the Adviser. Pursuant to the terms of the Advisory Agreement, the Fund pays the Adviser a monthly fee at the rate when annualized of 1.00% of the average daily value of the Fund's Managed Assets. Managed Assets means the total assets of the Fund minus the Fund's liabilities other than the loan payable.

The Fund has entered into a Services Agreement (the Agreement) with the Adviser. Pursuant to the terms of the Agreement, the Fund reimburses the Adviser for certain services related to a portion of the payment of salary and provision of benefits to the Fund's Chief Compliance

28

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(continued)

Officer. During the year ended September 30, 2016, these payments amounted to $73,132 and are included in the Other category of expenses in the Statement of Operations, together with insurance and other expenses incurred to unaffiliated entities. Expenses incurred pursuant to the Agreement as well as certain expenses paid for by the Adviser are allocated to the Fund in an equitable fashion as approved by the Trustees of the Fund.

The Fund pays compensation to Independent Trustees in the form of a retainer, attendance fees, and additional compensation to Board and Committee chairpersons. The Fund does not pay compensation directly to Trustees or officers of the Fund who are also officers of the Adviser.

(3) Fair Value Measurements

The Fund uses a three-tier hierarchy to prioritize the assumptions, referred to as inputs, used in valuation techniques to measure fair value. The three-tier hierarchy of inputs is summarized in the three broad levels. Level 1 includes quoted prices in active markets for identical investments. Level 2 includes prices determined using other significant observable inputs (including quoted prices for similar investments, interest rates, credit risk, etc.). The independent pricing vendor may value bank loans and debt securities at an evaluated bid price by employing methodologies designed to identify the market value for such securities and such securities are considered Level 2 in the fair value hierarchy. Level 3 includes prices determined using significant unobservable inputs (including the Fund's own assumptions in determining the fair value of investments). These inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used as of September 30, 2016 to value the Fund's net assets. For the year ended September 30, 2016, there were no transfers between Levels 1 and 2. The Fund accounts for transfers between levels at the beginning of the period.

Assets at Value | | Level 1 | | Level 2 | | Level 3 | | Total | |

Convertible Preferred Stocks | |

Biotechnology | | | | | | | | | | $ | 4,151,922 | | | $ | 4,151,922 | | |

Health Care Equipment & Supplies | | | | | | | | | | | 790,548 | | | | 790,548 | | |

Preferred Stock | |

Real Estate Investment Trust | | $ | 13,310,000 | | | | | | | | — | | | | 13,310,000 | | |

Mandatory Convertible Preferred Stocks | |

Pharmaceuticals | | | 14,681,170 | | | | | | | | — | | | | 14,681,170 | | |

Convertible Notes | |

Biotechnology | | | — | | | $ | 26,359,238 | | | | — | | | | 26,359,238 | | |

Pharmaceuticals | | | — | | | | 14,535,000 | | | | — | | | | 14,535,000 | | |

Non-Convertible Notes | |

Biotechnology | | | — | | | | 10,736,860 | | | | — | | | | 10,736,860 | | |

Health Care Equipment & Supplies | | | — | | | | 11,473,142 | | | | — | | | | 11,473,142 | | |

Health Care Providers & Services | | | — | | | | 74,728,616 | | | | — | | | | 74,728,616 | | |

Pharmaceuticals | | | — | | | | 14,038,799 | | | | — | | | | 14,038,799 | | |

29

TEKLA HEALTHCARE

OPPORTUNITIES FUND

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2016

(continued)

Assets at Value | | Level 1 | | Level 2 | | Level 3 | | Total | |

Common Stocks and Warrants | |

Biotechnology | | $ | 299,410,261 | | | | — | | | $ | 37,528 | | | $ | 299,447,789 | | |

Health Care Equipment & Supplies | | | 111,445,270 | | | | — | | | | — | | | | 111,445,270 | | |

Health Care Providers & Services | | | 160,093,485 | | | | — | | | | — | | | | 160,093,485 | | |

Health Care Technology | | | 2,286,312 | | | | — | | | | — | | | | 2,286,312 | | |

Life Sciences Tools & Services | | | 15,849,459 | | | | — | | | | — | | | | 15,849,459 | | |

Pharmaceuticals | | | 196,509,543 | | | | — | | | | — | | | | 196,509,543 | | |

Real Estate Investment Trusts | | | 81,413,752 | | | | — | | | | — | | | | 81,413,752 | | |