Exhibit 99.2

ASCENDIS PHARMA A/S

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

You should read the following discussion and analysis of our financial condition and results of operations in conjunction with our unaudited condensed consolidated interim financial statements, including the notes thereto, included with this report and the section contained in our Annual Report on Form 20-F for the year ended December 31, 2019 – “Item 5. Operating and Financial Review and Prospects”. The following discussion is based on our financial information prepared in accordance with International Accounting Standard 34, “Interim Financial Reporting.” Certain information and disclosures normally included in the consolidated financial statements prepared in accordance with International Financial Reporting Standards (“IFRS”) have been condensed or omitted. IFRS as issued by the International Accounting Standards Board, and as adopted by the European Union, might differ in material respects from generally accepted accounting principles in other jurisdictions.

Special Note Regarding Forward-Looking Statements

This report contains forward-looking statements concerning our business, operations and financial performance and conditions, as well as our plans, objectives and expectations for our business operations and financial performance and conditions. Any statements contained herein that are not statements of historical facts may be deemed to be forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “aim,” “anticipate,” “assume,” “believe,” “contemplate,” “continue,” “could,” “due,” “estimate,” “expect,” “goal,” “intend,” “may,” “objective,” “plan,” “predict,” “potential,” “positioned,” “seek,” “should,” “target,” “will,” “would,” and other similar expressions that are predictions or indicate future events and future trends, or the negative of these terms or other comparable terminology. These forward-looking statements include, but are not limited to, statements about:

| • | our expectations regarding a Biologics License Application and Marketing Authorization Application for TransCon Growth Hormone, or TransCon hGH (lonapegsomatropin); |

| • | the scope, progress, results and costs of developing our product candidates or any other future product candidates, and conducting preclinical studies and clinical trials, including our ongoing phase 3 study of TransCon hGH for the treatment of adult growth hormone deficiency, our ongoing phase 3 study of TransCon hGH for the treatment of pediatric growth hormone deficiency, our ongoing phase 2 study of TransCon Parathyroid Hormone, or TransCon PTH, and our ongoing phase 2 study of TransCon C-Type Natriuretic Peptide, or TransCon CNP; |

| • | our pursuit of oncology as our second of three independent therapeutic areas of focus, and our development of a pipeline of product candidates in this therapeutic area; |

| • | our receipt of future milestone or royalty payments from our collaboration partners, and the expected timing of such payments; |

| • | our expectations regarding the potential market size and the size of the patient populations for our product candidates, if approved for commercial use; |

| • | our expectations regarding the potential advantages of our product candidates over existing therapies; |

| • | our ability to enter into new collaborations; |

| • | our expectations with regard to the ability to develop additional product candidates using our TransCon technologies and file Investigational New Drug Applications, or INDs, or similar for such product candidates; |

| • | our expectations with regard to the ability to seek expedited regulatory approval pathways for our product candidates, including the potential ability to rely on the parent drug’s clinical and safety data with regard to our product candidates; |

| • | our expectations with regard to our current and future collaboration partners to pursue the development of our product candidates and file INDs or similar for such product candidates; |

| • | our development plans with respect to our product candidates; |

| • | our ability to develop, acquire and advance product candidates into, and successfully complete, clinical trials; |

| • | the timing or likelihood of regulatory filings and approvals for our product candidates; |

| • | the commercialization of our product candidates, if approved; |

| • | our commercialization, marketing and manufacturing capabilities of our product candidates and associated devices; |

| • | the implementation of our business model and strategic plans for our business, product candidates and technology; |

| • | the scope of protection we are able to establish and maintain for intellectual property rights covering our product candidates; |

| • | estimates of our expenses, future revenue, capital requirements, our needs for additional financing and our ability to obtain additional capital; |

| • | our financial performance; |

| • | developments and projections relating to our competitors and our industry; and |

| • | the effects on our business of the worldwide COVID-19 pandemic. |

These forward-looking statements are based on senior management’s current expectations, estimates, forecasts and projections about our business and the industry in which we operate and involve known and unknown risks, uncertainties and other factors that are in some cases beyond our control. As a result, any or all of our forward-looking statements in this report may turn out to be inaccurate. Factors that may cause actual results to differ materially from current expectations include, among other things, those listed under the section in our Annual Report on Form 20-F for the year ended December 31, 2019 — “Item 3.D. Risk Factors”. You are urged to consider these factors carefully in evaluating the forward-looking statements. These forward-looking statements speak only as of the date of this report. Except as required by law, we assume no obligation to update or revise these forward-looking statements for any reason, even if new information becomes available in the future. Given these risks and uncertainties, you are cautioned not to rely on such forward-looking statements as predictions of future events.

You should read this report and the documents that we reference in this report and have filed as exhibits to this report completely and with the understanding that our actual future results may be materially different from what we expect. You should also review the factors and risks we describe in the reports we will file or submit from time to time with the Securities and Exchange Commission after the date of this report. We qualify all of our forward-looking statements by these cautionary statements.

Overview

We are applying our innovative TransCon technologies to build a leading, fully integrated biopharmaceutical company and develop a pipeline of product candidates with potential best-in-class profiles to address unmet medical needs. We currently have three product candidates in clinical development in rare endocrine diseases and we are advancing multiple preclinical candidates in oncology, our second therapeutic area of focus. We are also working to apply our TransCon technology platform in additional therapeutic areas to address unmet patient needs. We submitted regulatory applications for marketing approval for TransCon hGH (lonapegsomatropin) this year in the United States and Europe, and we are building our commercial organization, starting with a focus in the United States.

In 2018, we formed VISEN Pharmaceuticals, or VISEN, a company established to develop and commercialize our endocrinology rare disease therapies in the People’s Republic of China, Hong Kong, Macau and Taiwan, or Greater China. We received 50% ownership in the outstanding shares of VISEN and concurrently with the rights we granted to VISEN for lonapegsomatropin, TransCon PTH and TransCon CNP, entities affiliated with Vivo Capital and Sofinnova Ventures purchased shares in VISEN for an aggregate purchase price of $40 million in cash.

We had a net loss of €280.0 million for the nine months ended September 30, 2020 and a net loss of €218.0 million for the year ended December 31, 2019. Our total equity was €951.6 million as of September 30, 2020 compared to €597.1 million as of December 31, 2019.

TransCon Technology Platform

Our TransCon technologies enable us to create long-acting prodrug therapies with potentially significant advantages over existing marketed drug products. Our TransCon technologies are designed to transiently link an unmodified parent drug to a TransCon carrier via our proprietary TransCon linkers. Our TransCon linkers are designed to predictably release an unmodified active parent drug at predetermined rates governed by physiological conditions (e.g., pH and temperature), supporting administration frequencies from daily to more than every six months. Depending upon the type of TransCon carrier we employ, we can design our TransCon prodrugs to act systemically or locally in areas that are difficult to treat with conventional therapies.

We believe that the potential of our TransCon technologies is supported by data from our preclinical research and the ongoing clinical programs, including the lonapegsomatropin, TransCon PTH and TransCon CNP programs, as well as findings from our ongoing development of other product candidates. We have applied the TransCon technologies to clinically validated parent drugs to create product candidates using our algorithm for product innovation that we believe have the potential to be best-in-class in endocrinology rare diseases, and we will continue to apply this algorithm for product selection in oncology and additional therapeutic areas to address unmet patient needs. We believe this approach may reduce the risks associated with traditional drug development.

Lonapegsomatropin

Our most advanced investigational product candidate, lonapegsomatropin, is a once-weekly long-acting prodrug of somatropin, also referred to as recombinant human growth hormone, or hGH, as a potential treatment for growth hormone deficiency, or GHD. We believe that lonapegsomatropin, if approved, may offer a once-weekly therapy for both pediatric and adult GHD with the potential to improve outcomes compared to currently approved daily somatropin. If approved, we believe lonapegsomatropin will reduce the burden of daily treatment by requiring significantly fewer injections, which we believe may improve compliance and treatment outcomes.

Our phase 3 pediatric program for lonapegsomatropin includes the heiGHt, fliGHt and enliGHten Trials. Our results from the pivotal, phase 3 heiGHt Trial demonstrated a statistically significant improvement in annualized height velocity, or AHV, compared to daily somatropin at 52 weeks and showed a safety profile comparable to that of daily somatropin in pediatric subjects who were treatment-naïve. The fliGHt Trial was designed to evaluate lonapegsomatropin in subjects who were primarily treatment experienced with daily somatropin, although a subgroup of younger subjects were treatment-naïve. Nearly all subjects who completed the heiGHt or fliGHt Trials have enrolled in the open-label extension study, or the enliGHten Trial, which is designed to provide long-term safety data to support the regulatory submissions for lonapegsomatropin. We initiated the enliGHten Trial in 2017 as the first subjects began to roll over from the heiGHt Trial, and we have enrolled approximately 300 subjects, which formed the safety database required by the U.S. Food and Drug Administration, or FDA, and the European Medicines Agency’s, or EMA’s, Committee for Medicinal Products for Human Use, and was included in our Biologics License Application, or BLA, submission in June 2020.

In September 2020, we filed a Clinical Trial Notification, or CTN, with the Pharmaceuticals and Medical Devices Agency, or PMDA in Japan, to initiate our phase 3 riGHt Trial of lonapegsomatropin for the treatment for pediatric GHD. The primary objective of the riGHt Trial is to evaluate and compare the AHV of 40 Japanese prepubertal treatment naïve children with GHD treated with weekly lonapegsomatropin to that of a commercially available daily somatropin formulation at 52 weeks.

In September 2020, we submitted a Marketing Authorization Application, or MAA, to the EMA seeking approval for lonapegsomatropin for the treatment of pediatric patients who are diagnosed with GHD. Subsequently, the EMA validated the MAA application.

In September 2020, the FDA accepted our BLA for lonapegsomatropin for the treatment for pediatric GHD and set a PDUFA date for June 25, 2021. The FDA also indicated that it is currently not planning to hold an Advisory Committee Meeting to discuss the application at this time.

In July 2020, the EMA adopted a decision agreeing with the positive opinion from the Paediatric Committee, or PDCO, on agreeing with the proposed Paediatric Investigation Plan, or PIP, for lonapegsomatropin. The PIP endorsed the lonapegsomatropin program as acceptable for assessment of safety and efficacy for the use of lonapegsomatropin as a treatment for GHD in children from six months to less than 18 years of age, mirroring the population covered by the studies conducted in the program.

In April 2020, we received orphan drug designation from the FDA for lonapegsomatropin in the United States for the treatment of GHD. The FDA grants orphan designation to drugs that are intended for the treatment, diagnosis, or prevention of rare diseases or disorders that affect fewer than 200,000 people in the United States, and potentially may be safer or more effective than already approved products.

In October 2019, we received orphan designation from the European Commission, or EC, for lonapegsomatropin for GHD. Orphan designation is granted to therapies aimed at the treatment, prevention or diagnosis of a disease that is life-threatening or chronically debilitating, affects no more than five in 10,000 persons in the European Union and for which no satisfactory method of diagnosis, prevention, or treatment has been authorized (or the product would provide significant additional benefit over existing therapies).

Additionally, we have initiated a global, phase 3 trial in subjects with adult GHD, the foresiGHt Trial, with enrollment planned to begin later this year and a phase 3 trial is ongoing in Greater China through our strategic investment in VISEN. We intend to pursue other indications for lonapegsomatropin consistent with our strategy to create sustainable growth.

TransCon Parathyroid Hormone

We are using our TransCon technology platform to develop TransCon Parathyroid Hormone, or TransCon PTH, an investigational once-daily long-acting prodrug of parathyroid hormone, or PTH, as a potential treatment for adult hypoparathyroidism, or HP, a rare endocrine disorder of calcium and phosphate metabolism. TransCon PTH is designed to replace PTH at physiologic levels for 24 hours each day to address both the short-term symptoms and long-term complications of HP. The current standard of care for HP is calcium and active vitamin D (calcitriol or alfacalcidol).

In October 2020, the EC granted orphan designation to TransCon PTH for the treatment of HP.

In September 2020, we submitted an amendment to our investigational new drug application (IND) with the FDA for the PaTHway phase 3 clinical trial evaluating the safety, tolerability and efficacy of TransCon PTH in adults with hypoparathyroidism (HP). We have also submitted regulatory filings to enable initiation of European and Canadian sites for the PaTHway Trial. PaTHway is a double-blind, placebo-controlled trial that is expected to enroll approximately 76 subjects at sites in North America and Europe in order to obtain 68 evaluable subjects. The primary composite endpoint of the PaTHway Trial at 26 weeks is the proportion of subjects with (1) serum calcium in the normal range, (2) independence from active vitamin D, and (3) taking £600 mg/day of calcium supplements.

In September 2020, we announced preliminary six-month results from the open-label extension, or OLE, portion of PaTH Forward, a global phase 2 trial evaluating the safety, tolerability and efficacy of TransCon PTH in adult subjects with HP. The preliminary results support potential use of TransCon PTH as a hormone replacement therapy for HP and demonstrated normalization of quality of life for subjects based on the SF-36® Health Survey, a standard, validated tool for assessing health-related quality of life in general.

In August 2020, we reported data from the four-week fixed dose, blinded portion of PaTH Forward Trial on SF-36® Health Survey which demonstrated that TransCon PTH significantly improved quality of life and restored physical and mental functioning toward a normal level compared to placebo.

In April 2020, we reported positive top-line results from the four-week fixed dose, blinded portion of our phase 2 PaTH Forward Trial, which evaluated the safety, tolerability and efficacy of three fixed doses of TransCon PTH using a ready-to-use prefilled pen injector planned for commercial presentation. The goal of PaTH Forward is to identify a starting dose for a pivotal phase 3 trial, establish a titration regimen for complete withdrawal of standard of care (i.e., active vitamin D and calcium supplements), and evaluate TransCon PTH control of serum and urinary calcium. A total of 59 subjects were randomized in a blinded manner to receive fixed doses of TransCon PTH at 15, 18 or 21 µg/day or placebo for four weeks. All doses of TransCon PTH were well-tolerated, and no serious or severe adverse events were shown during this period. No treatment-emergent adverse events, or TEAEs, led to discontinuation of study drug, and the overall incidence of TEAEs was comparable between TransCon PTH and placebo. Additionally, there were no drop-outs during the four-week fixed dose period.

In June 2018, we were granted orphan drug designation by the FDA for TransCon PTH for the treatment of hypoparathyroidism.

TransCon C-Type Natriuretic Peptide

We are also developing TransCon C-Type Natriuretic Peptide, or TransCon CNP, an investigational long-acting prodrug of C-type natriuretic peptide, or CNP, as a potential therapeutic option for achondroplasia, the most common form of dwarfism, and potentially other related growth disorders. TransCon CNP is designed to provide continuous CNP exposure with the goal of optimizing efficacy with a safe and convenient once-weekly dose. Currently, there are no medical therapies for achondroplasia approved by the FDA.

In October 2020, in collaboration with VISEN, we filed an IND to initiate the phase 2 ACcomplisH China Trial of TransCon CNP. The ACcomplisH China Trial is a phase 2, randomized, double-blind, placebo-controlled trial evaluating the safety, efficacy, and pharmacokinetics of multiple subcutaneous doses of TransCon CNP administered once weekly. The primary objectives of the study are to determine the safety of TransCon CNP in infants and prepubertal children (age <11 years) with achondroplasia and to evaluate the effect of TransCon CNP on 12-month AHV in infants and prepubertal children (age <11 years) with achondroplasia. All subjects who complete the trial will have the opportunity to receive TransCon CNP in a long-term extension trial.

In July 2020, we received orphan designation from the EC for TransCon CNP for treatment of achondroplasia.

In July 2019, we initiated the phase 2 ACcomplisH Trial to evaluate safety and efficacy of TransCon CNP in children (ages 2-10 years) with achondroplasia.

In February 2019, we were granted orphan drug designation by the FDA for TransCon CNP for the treatment of achondroplasia.

In November 2018, we reported preliminary results from a phase 1 trial in healthy adult subjects, which we believe supported our target product profile for TransCon CNP.

TransCon Product Candidates within Oncology

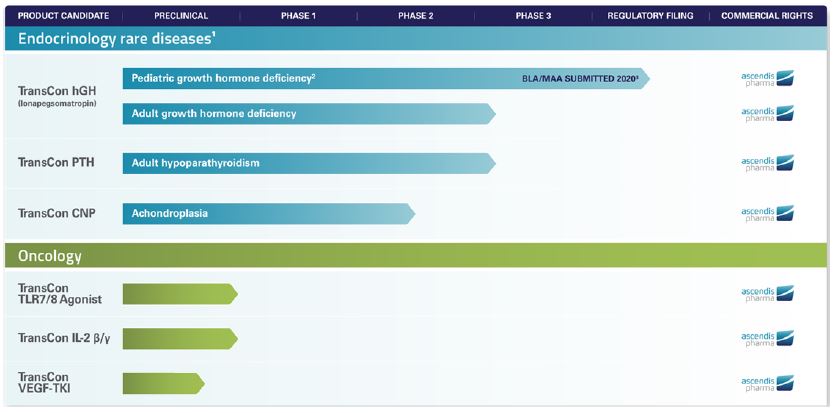

In January 2019, we established oncology as our second independent therapeutic area of focus for our TransCon technologies. Our goal is to improve treatment efficacy while limiting or reducing toxicity by applying TransCon technologies to clinically validated drugs, using our unique algorithm for product innovation.

We are conducting preclinical studies within the field of oncology to explore multiple potential product candidates and evaluate systemic as well as localized delivery systems using our TransCon technology platform. We have presented preclinical data on three of the programs currently in our oncology pipeline: TransCon Toll-like Receptor, or TLR, 7/8 Agonist, TransCon Interleukin-2, or IL-2, ß/g, and TransCon Vascular Endothelial Growth Factor-Tyrosine Kinase Inhibitor, or VEGF-TKI.

TransCon TLR7/8 Agonist is a long-acting prodrug of resiquimod that is transiently conjugated to a hydrogel carrier via a TransCon linker. Administered as an intratumoral injection, TransCon TLR7/8 Agonist is designed to provide sustained release of unmodified resiquimod directly to the tumor. In preclinical studies, the effective half-life of resiquimod released from TransCon TLR7/8 Agonist has been found to be approximately 25-fold longer than the parent drug, resiquimod. We plan to submit an IND or similar filing for TransCon TLR7/8 Agonist by year-end.

We are also developing TransCon IL-2 ß/g, a novel long-acting prodrug of IL-2 ß/g designed to address limitations of alternative IL-2 treatments, including aldesleukin, which has been available since the 1990’s as a treatment for advanced kidney cancer and advanced melanoma. TransCon IL-2 ß/g is designed with a parent drug that selectively binds and activates the IL-2Rß/g. By applying the innovative TransCon technology platform, preclinical data also showed that TransCon IL-2 ß/g demonstrated a long in vivo half-life of approximately 32 hours, expected to support potential dosing of every three weeks in patients. Preclinical results show a single dose of TransCon IL-2 ß/g selectively expanded lymphocyte counts (i.e., CD8+ T cells and NK cells) in non-human primates, with minimal signs of systemic inflammation (IL-5 and IL-6 markers) or endothelial cell damage (E-Selectin and VCAM-1 markers) and no dose-limiting toxicities. We plan to submit an IND filing in the United States for TransCon IL-2 ß/g in 2021.

TransCon Product Candidate Pipeline

| 1. | Excludes rights granted to VISEN Pharmaceuticals in Greater China |

| 2. | In phase 3 development for pediatric growth hormone deficiency in Greater China through VISEN Pharmaceuticals. |

| 3. | U.S. PDUFA June 25, 2021. |

Results of Operations

Impact from COVID-19 Pandemic

As reported in the audited consolidated financial statements as of and for the year ended December 31, 2019, a novel strain of coronavirus, (“COVID-19”), was reported to have surfaced in Wuhan, China, in December 2019. Since then, COVID-19 has spread around the world into a pandemic, including into countries where we are operating from, where we have planned or have ongoing clinical trials, and where we rely on third parties to manufacture preclinical and clinical supplies, as well as commercial supply.

The COVID-19 pandemic may negatively impact our business in many ways. There is a potential evolving impact on the conduct of clinical trials of our product candidates, and any challenges which may arise, may lead to difficulties in meeting protocol-specified procedures. In addition, while we rely on third parties to manufacture preclinical and clinical supplies and materials, we can potentially experience delays in providing sufficient supplies according to our planned and ongoing clinical trials. Further, if our product candidates are approved, we will need to secure sufficient manufacturing capacity with our third-party manufacturers to produce the quantities necessary to meet anticipated market demand, which may be delayed by the pandemic.

In order to deliver on business objectives and to ensure the safety of the patients when conducting clinical trials, we have implemented several measures. Those measures include implementing remote-visits and ensure safe delivery and dosage of clinical drugs and are continuously monitored and reassessed to ensure efficient and safe conduction of the trials. In addition, we monitor and have a close dialogue with third-party manufacturing suppliers, in order to mitigate the risk from COVID-19 supplier disruptions.

As of the reporting date, we have not identified significant COVID-19 related disruptions to our business, including clinical trial operations, or identified any of our third-party manufacturers not being able to meet their obligations. In addition, no significant transactions, as a result of COVID-19, have been recognized during the first nine months of 2020.

To minimize the risk of spread of COVID-19, we have taken precautionary measures within our organization, including encouraging our employees to work remotely, reducing travel activity, and minimizing face-to-face meetings. To accommodate efficient procedures for financial reporting, including internal controls, we have, also before the pandemic, structured our work environment to enable our employees to perform their tasks remotely. Accordingly, it has not been necessary to make material changes to our internal control over financial reporting due to the pandemic.

However, while the global outbreak of COVID-19 continues to impact global societies, the extent to which COVID-19 impacts our business will depend on the future development, which is highly uncertain and cannot be reliably predicted. While COVID-19 continues to impact the world in several aspects, the development is monitored closely by our management, including any impact this may have on our financial performance and financial position.

Comparison of the Three Months Ended September 30, 2020 and 2019 (unaudited):

| Three Months Ended September 30, | ||||||||

| 2020 | 2019 | |||||||

| (EUR’000) | ||||||||

Revenue | 2,757 | 2,243 | ||||||

Research and development costs | (64,059 | ) | (46,258 | ) | ||||

Selling, general and administrative expenses | (17,523 | ) | (10,000 | ) | ||||

|

|

|

| |||||

Operating profit / (loss) | (78,825 | ) | (54,015 | ) | ||||

Share of profit / (loss) of associate | (3,101 | ) | (1,338 | ) | ||||

Finance income | 136 | 30,547 | ||||||

Finance expenses | (39,970 | ) | (368 | ) | ||||

|

|

|

| |||||

Profit / (loss) before tax | (121,760 | ) | (25,174 | ) | ||||

|

|

|

| |||||

Tax on profit / (loss) for the period | 19 | 61 | ||||||

|

|

|

| |||||

Net profit / (loss) for the period | (121,741 | ) | (25,113 | ) | ||||

|

|

|

| |||||

Revenue

Total revenue for the three months ended September 30, 2020 was €2.8 million compared to €2.2 million for the three months ended September 30, 2019, and comprised sale of clinical supply, rendering of services, and recognition of internal profit deferred from November 2018 when we entered into the collaboration with VISEN. The increase was due to a higher amount of sale of clinical supply and services to VISEN, partly offset by a lower amount of license revenue being recognized.

Research and Development Costs

Research and development costs were €64.1 million for the three months ended September 30, 2020, an increase of €17.8 million, or 38%, compared to €46.3 million for the three months ended September 30, 2019.

External development costs related to lonapegsomatropin, primarily comprising manufacturing of product supply and costs of clinical trials, increased by €1.2 million compared to the same period last year, reflecting higher costs for manufacturing of product supply, partly reduced by lower costs for manufacturing of validation batches and device development. Costs of clinical trials and clinical supplies were slightly higher compared to the same period last year.

External development costs related to TransCon PTH increased by €3.7 million, primarily reflecting increased costs related to manufacturing and device development, whereas clinical trial costs and clinical supplies were in line with the same period last year.

External development costs related to TransCon CNP increased by €1.4 million, primarily reflecting an increase in manufacturing costs.

External development costs related to our oncology product candidates increased by €4.1 million, primarily reflecting higher manufacturing and preclinical costs.

Other research and development costs increased by €7.4 million, primarily driven by an increase in personnel costs of €4.3 million and non-cash share-based payment of €2.0 million due to a higher number of employees in research and development functions. Other costs allocated to research and development functions increased by a total of €2.1 million, including IT and telecommunication, laboratory operations, depreciation and professional fees. Travel costs decreased by €1.0 million, primarily reflecting the reduction in travel activity due to the COVID-19 pandemic.

Research and development costs included non-cash share-based payment of €7.0 million for the three months ended September 30, 2020, compared to €5.1 million for the three months ended September 30, 2019.

Selling, General and Administrative Expenses

Selling, general and administrative expenses were €17.5 million for the three months ended September 30, 2020, an increase of €7.5 million, or 75%, compared to €10.0 million for the three months ended September 30, 2019. The higher expenses were primarily due to an increase in personnel costs of €3.0 million and non-cash share-based payment of €0.4 million for additional commercial and administrative personnel. Other costs allocated to selling, general and administrative functions increased by a total of €4.4 million, primarily reflecting the implementation of a new ERP-system and professional fees for building our commercial business. Travel costs decreased by €0.3 million, reflecting the reduction in travel activity due to the COVID-19 pandemic.

Selling, general and administrative expenses included non-cash share-based payment of €3.4 million for the three months ended September 30, 2020, compared to €3.0 million for the three months ended September 30, 2019.

Net Profit / (Loss) in Associate

Net loss in associate was €3.1 million, compared to €1.3 million for the three months ended September 30, 2019. The net loss represents our share of net result from VISEN.

Finance Income and Finance Expenses

Finance income was €0.1 million for the three months ended September 30, 2020 compared to €30.5 million for the three months ended September 30, 2019. Finance expenses were €40.0 million for the three months ended September 30, 2020 compared to €0.4 million for the same period in 2019. As we hold positions of marketable securities and cash and cash equivalents in U.S. Dollar, we are affected by exchange rate fluctuations when reporting our financial results in Euro. For the three months ended September 30, 2020, we recognized an exchange rate loss when reporting our U.S. Dollar positions in Euro, reflecting negative exchange rate fluctuations, whereas we recognized a gain for the same period in 2019, reflecting positive exchange rate fluctuations, primarily between the U.S. Dollar and Euro. Further, the change in net finance income reflects a decrease in interest income of €3.0 million due to declining interest rates.

We did not have any interest-bearing debt for any of the periods presented. However, IFRS 16, “Leases”, requires interest expenses to be recognized on lease liabilities.

Tax for the Period

Tax for the three months ended September 30, 2020 was a net tax credit of €19 thousand compared to a net tax credit of €61 thousand for the three months ended September 30, 2019. Taxes for the three months ended September 30, 2020 comprised an estimated tax credit of €186 thousand in the group of Danish companies, partly offset by tax provisions of €167 thousand in our U.S. and German subsidiaries.

Comparison of the Nine Months Ended September 30, 2020 and 2019 (unaudited):

| Nine Months Ended September 30, | ||||||||

| 2020 | 2019 | |||||||

| (EUR’000) | ||||||||

Revenue | 6,418 | 10,868 | ||||||

Research and development costs | (185,152 | ) | (141,343 | ) | ||||

Selling, general and administrative expenses | (56,243 | ) | (31,396 | ) | ||||

|

|

|

| |||||

Operating profit / (loss) | (234,977 | ) | (161,871 | ) | ||||

Share of profit / (loss) in associates | (6,501 | ) | (5,452 | ) | ||||

Finance income | 1,677 | 30,285 | ||||||

Finance expenses | (40,391 | ) | (812 | ) | ||||

|

|

|

| |||||

Profit / (loss) before tax | (280,192 | ) | (137,850 | ) | ||||

|

|

|

| |||||

Tax on profit / (loss) for the period | 202 | 196 | ||||||

|

|

|

| |||||

Net profit / (loss) for the period | (279,990 | ) | (137,654 | ) | ||||

|

|

|

| |||||

Revenue

Total revenue for the nine months ended September 30, 2020 was €6.4 million compared to €10.9 million for the nine months ended September 30, 2019, and comprised sale of clinical supply, rendering of services, and recognition of internal profit deferred from November 2018 when we entered into the collaboration with VISEN. The decrease was due to a lower amount of license and service revenue, partly offset by sale of clinical supply, to VISEN.

Research and Development Costs

Research and development costs were €185.2 million for the nine months ended September 30, 2020, an increase of €43.9 million, or 31%, compared to €141.3 million for the nine months ended September 30, 2019.

External development costs related to lonapegsomatropin decreased by €3.2 million, primarily driven by lower costs for manufacturing of validation batches, or process performance qualification batches, and device development costs, partly offset by increases in clinical trial costs and costs of commercial product supply, as well as costs related to regulatory, statistical and medical activities preparing for the BLA-filing.

External development costs related to TransCon PTH increased by €6.7 million, reflecting increased clinical trial costs related to the progress of our phase 2 PaTH Forward clinical trial, increased costs of device development, and increased cost of biometric activities, whereas preclinical costs decreased compared to the same period last year.

External development costs related to TransCon CNP increased by €3.4 million, primarily reflecting an increase in manufacturing costs and clinical trial costs for our phase 2 ACcomplisH Trial, partly offset by a decrease in preclinical costs.

External costs related to our oncology product candidates increased by €10.0 million, primarily reflecting an increase in manufacturing costs and preclinical costs as these product candidates progress through the early development stages and into manufacturing.

Other research and development costs increased by €27.0 million, primarily driven by an increase in personnel costs of €14.2 million and non-cash share-based payment of €8.9 million due to a higher number of employees in research and development functions, but also reflecting increases of €2.3 million in IT and telecommunication costs and €1.7 million in facility costs and depreciation allocated to research and development functions. Other costs, including laboratory operations, supplies and professional fees, increased by net €1.9 million compared to the same period last year. Travel costs decreased by €2.0 million, primarily due to the COVID-19 pandemic.

Research and development costs included non-cash share-based payment of €24.1 million for the nine months ended September 30, 2020, compared to €15.2 million for the nine months ended September 30, 2019.

Selling, General and Administrative Expenses

Selling, general and administrative expenses were €56.2 million for the nine months ended September 30, 2020, an increase of €24.8 million, or 79%, compared to €31.4 million for the nine months ended September 30, 2019. The higher expenses were primarily due to an increase in personnel costs of €7.6 million and non-cash share-based payment of €3.7 million for additional commercial and administrative personnel. IT costs increased by €4.0 million and insurance costs increased by €2.4 million. Professional fees, primarily related to building up our commercial capabilities, increased by €6.8 million. Travel costs decreased by €0.6 million, primarily due to the COVID-19 pandemic, and other costs, including facility costs and depreciation, increased by net €0.9 million compared to the same period last year.

Selling, general and administrative expenses included non-cash share-based payment of €14.7 million for the nine months ended September 30, 2020, compared to €11.0 million for the nine months ended September 30, 2019.

Net Profit / (Loss) in Associate

Net loss in associate was €6.5 million, compared to €5.5 million for the nine months ended September 30, 2019. The net loss represents our share of net result from VISEN.

Finance Income and Finance Expenses

Finance income was €1.7 million for the nine months ended September 30, 2020 compared to €30.3 million for the nine months ended September 30, 2019. Finance expenses were €40.4 million for the nine months ended September 30, 2020 compared to €0.8 million in the same period in 2019. As we hold positions of marketable securities and cash and cash equivalents in U.S. Dollar, we are affected by exchange rate fluctuations when reporting our financial results in Euro. For the nine months ended September 30, 2020, we recognized an exchange rate loss when reporting our U.S. Dollar positions in Euro, reflecting negative exchange rate fluctuations, whereas we recognized a gain for the same period in 2019, reflecting positive exchange rate fluctuations, primarily between the U.S. Dollar and Euro. Further, the change reflects a €6.4 million decrease in interest income due to declining interest rates compared to the same period of last year.

We did not have any interest-bearing debt for any of the periods presented. However, IFRS 16, “Leases”, requires interest expenses to be recognized on lease liabilities.

Tax for the Period

Tax for the nine months ended September 30, 2020 was a net credit of €0.2 million in line with a net credit of €0.2 million for the nine months ended September 30, 2019. Taxes for the nine months ended September 30, 2020 comprised an estimated tax credit of €0.6 million in the group of Danish companies partly offset by tax expenses of €0.4 million in our U.S. and German subsidiaries.

Liquidity and Capital Resources

As of September 30, 2020, we had cash and cash equivalents, where cash equivalents comprise highly liquid marketable securities with a maturity of three months or less at the date of acquisition, totaling €763.5 million compared to €598.1 million as of December 31, 2019. In addition, in order to mitigate concentration of credit risks on cash deposits, we held marketable securities of €194.1 million, all denominated in U.S. Dollar and with a weighted average duration of 5.5 months from the reporting date.

We have funded our operations primarily through issuance of preference shares, ordinary shares and convertible debt securities and payments to us under our collaboration agreements. Our expenditures are primarily related to research and development activities, and general and administrative activities to support research and development, as well as initial selling activities, building up our sales and marketing capabilities.

In February 2015, we announced the closing of our initial public offering, with net proceeds of $111.5 million (or €101.4 million). In addition, we have completed follow-on public offerings of American Depositary Shares (“ADSs”) as specified below:

| • | In 2016, with net proceeds of $127.1 million (or €116.6 million); |

| • | In 2017, with net proceeds of $145.2 million (or €123.1 million); |

| • | In 2018, with net proceeds of $242.5 million (or €198.6 million); |

| • | In 2019, with net proceeds of $539.4 million (or €480.3 million); and |

| • | In July 2020, with net proceeds of $654.6 million (or €580.5 million). |

Based on our current operating plan, we believe that our existing cash, cash equivalents and marketable securities as of September 30, 2020, will be sufficient to meet our projected cash requirements for at least 12 months from the date of this report. However, our operating plan may change as a result of many factors currently unknown to us, and we may need to seek additional funds sooner than planned. Our future funding requirements will depend on many factors, including, but not limited to:

| • | the progress, timing, scope, results and costs of our clinical trials and preclinical studies for our product candidates and manufacturing activities, including the ability to enroll patients in a timely manner for clinical trials; |

| • | the time and cost necessary to obtain regulatory approvals for our product candidates and the costs of post-marketing studies that could be required by regulatory authorities; |

| • | the manufacturing, selling and marketing costs associated with product candidates, including the cost and timing of building our sales and marketing capabilities; |

| • | our ability to establish and maintain strategic partnerships, licensing or other arrangements and the financial terms of such agreements; |

| • | the achievement of development, regulatory and commercial milestones resulting in the payment to us from our collaboration partners of contractual milestone payments and the timing of receipt of such payments, if any; |

| • | the timing, receipt, and amount of sales of, or royalties on, our future products, if any; |

| • | the sales price and the availability of adequate third-party coverage and reimbursement for our product candidates; |

| • | the cash requirements of any future acquisitions or discovery of product candidates; |

| • | the number and scope of preclinical and discovery programs that we decide to pursue or initiate; |

| • | the potential acquisition and in-licensing of other technologies, products or assets; |

| • | the time and cost necessary to respond to technological and market developments, including further development of our TransCon technologies; |

| • | our progress (and the progress of our collaboration partners, if any) in the successful commercialization and co-promotion of our most advanced product candidates and our efforts to develop and commercialize our other existing product candidates; and |

| • | the costs of filing, prosecuting, maintaining, defending and enforcing any patent claims and other intellectual property rights, including litigation costs and the outcome of such litigation, including costs of defending any claims of infringement brought by others in connection with the development, manufacture or commercialization of our product candidates. |

Additional funds may not be available when we need them on terms that are acceptable to us, or at all. If adequate funds are not available to us on a timely basis, we may be required to delay, limit, scale back or cease our research and development activities, preclinical studies and clinical trials for our product candidates for which we retain such responsibility and our establishment and maintenance of sales and marketing capabilities or other activities that may be necessary to commercialize our product candidates.

The following table summarizes our cash flows for each of the unaudited nine months periods ended September 30, 2020 and 2019:

| Nine Months Ended September 30, | ||||||||

| 2020 | 2019 | |||||||

| (EUR’000) | ||||||||

Cash flows from / (used in) operating activities | (181,216 | ) | (126,700 | ) | ||||

Cash flows from / (used in) investing activities | (220,067 | ) | (4,030 | ) | ||||

Cash flows from / (used in) financing activities | 592,336 | 489,330 | ||||||

|

|

|

| |||||

Net increase / (decrease) in cash and cash equivalents | 191,053 | 358,600 | ||||||

|

|

|

| |||||

Cash Flows From / (Used in) Operating Activities

Net cash used in operating activities for the nine months ended September 30, 2020 was €181.2 million compared to €126.7 million for the nine months ended September 30, 2019. The net loss for the nine months ended September 30, 2020 of €280.0 million included non-cash charges of €45.2 million, comprising share-based payment and depreciation, and non-cash net financial expenses and taxes, of €43.2 million. The net change in working capital contributed positively to cash flows by €10.4 million, primarily due to a net increase in trade payables and other payables of €20.7 million, partly offset by an increase in receivables and prepayments of €9.7 million and a decrease in deferred income of €0.6 million.

Net cash used in operating activities for the nine months ended September 30, 2019 was €126.7 million. The net loss for the nine months ended September 30, 2019 of €137.7 million included non-cash charges of €30.9 million, comprising share-based payment and depreciation, and non-cash net income, including net financial income and taxes, of €22.2 million. The net change in working capital contributed positively to cash flows by €2.3 million, primarily due to a net increase in trade payables and other payables of €3.7 million, a decrease in receivables and prepayments of €4.4 million, partly offset by a decrease in deferred income of €5.5 million and an increase in deposits of €0.3 million.

Cash Flows From / (Used in) Investing Activities

Cash flows used in investing activities for the nine months ended September 30, 2020 of €220.1 million were related to acquisition of marketable securities of €340.4 million and settlement of marketable securities of €132.7 million, to acquisition of property, plant and equipment of €11.7 million, primarily related to our oncology laboratories in the United States and for use in the laboratories of our German facility, and to acquisition of software of €0.7 million.

Cash flows used in investing activities for the nine months ended September 30, 2019 of €4.0 million were related to acquisition of property, plant and equipment, primarily equipment for use in the laboratories of our German facility and in our oncology laboratories in the United States.

Cash Flows From / (Used in) Financing Activities

Cash flows from financing activities for the nine months ended September 30, 2020 of €592.3 million were comprised of €580.5 million in net proceeds from our follow-on public offering of ADSs completed in July 2020 and €15.3 million in net proceeds from warrant exercises in April, May, June, August and September 2020, partly offset by payments on lease liabilities of €3.5 million.

Cash flows from financing activities for the nine months ended September 30, 2019 of €489.3 million were comprised of €480.3 million in net proceeds from our follow-on public offering of ADSs completed in March 2019 and €12.0 million in net proceeds from warrant exercises in April, June, and September 2019, partly offset by payments on lease liabilities of €3.0 million.

Off-balance Sheet Arrangements

We have not entered into any off-balance sheet arrangements or any holdings in variable interest entities.

Qualitative Disclosures about Market Risk

Our activities expose us to the financial risks of changes in foreign currency exchange rates and interest rates. We do not enter into derivative financial instruments to manage our exposure to such risks. Further, we are exposed to credit risk and liquidity risk.

Foreign Currency Risk

We are exposed to foreign exchange risk arising from various currency exposures, primarily with respect to the U.S. Dollar, the British Pound and the Danish Krone. We have received payments in U.S. Dollars under our collaborations, and the proceeds from our series D financing in November 2014, our initial public offering in February 2015, and our follow-on offerings, the latest being in July 2020, were in U.S. Dollars. We seek to minimize our exchange rate risk by maintaining cash positions in the currencies in which we expect to incur the majority of our future expenses and we make payments from those positions.

Interest Rate Risk

We have no interest-bearing debt to third parties. In addition, while we have no derivatives or financial assets and liabilities measured at fair value, our exposure to interest rate risk primarily relates to the interest rates for our positions of cash and cash equivalents and marketable securities. Our future interest income from interest-bearing bank deposits and marketable securities may fall short of expectations due to changes in interest rates. We do not consider the effects of interest rate fluctuations to be a material risk to our financial position.

Credit Risk

We have adopted an investment policy with the primary purpose of preserving capital, fulfilling our liquidity needs and diversifying the risks associated with cash and marketable securities. This investment policy establishes minimum ratings for institutions with which we hold cash, cash equivalents and marketable securities, as well as rating and concentration limits for marketable securities that we may hold.

We consider all of our material counterparties to be creditworthy. While the concentration of credit risk may be significant, we consider the credit risk for each of our individual counterparts to be low. Our exposure to credit risk primarily relates to our cash and cash equivalents, and marketable securities. The credit risk on bank deposits is limited because the counterparties, holding significant deposits, are banks with high credit-ratings (minimum A3/A-) assigned by international credit-rating agencies. The banks are reviewed on a regular basis and our deposits may be transferred during the year to mitigate credit risk.

We have considered the risk of expected credit loss on our cash deposits, including the hypothetical impact arising from the probability of default considering in conjunction with the expected loss given default from banks with similar credit ratings and attributes. In line with previous periods, our assessment did not reveal a material impairment loss, and accordingly no provision for expected credit loss has been recognized.

Since March 2020, in order to mitigate concentration of credit risks, we have placed a portion of our bank deposits into primarily U.S. government bonds, treasury bills, corporate bonds, and commercial papers. Our investment policy only allows investment in marketable securities having investment grade credit-ratings, assigned by international credit-rating agencies and accordingly, the risk from probability of default is low.

The risk of expected credit loss over marketable securities has been considered, including the hypothetical impact arising from the probability of default considering in conjunction with the expected loss given default from securities with similar credit rating and attributes. This assessment did not reveal a material expected credit loss, and accordingly no provision for expected credit loss has been recognized.

For other assets, including deposits and receivables, we consider the credit risk to be low and no provision for expected credit loss has been recognized.

Liquidity Risk

Historically we have addressed the risk of insufficient funds through proceeds from sale of our securities in private and public offerings.

We manage our liquidity risk by maintaining adequate cash reserves and banking facilities, and by matching the maturity profiles of financial assets including marketable securities, with cash-forecasts including payment profiles on liabilities. We monitor the risk of a shortage of funds using a liquidity planning tool, to ensure sufficient funds available to settle liabilities as they fall due.

Marketable securities are all denominated in U.S. Dollars and have a weighted average duration of 3.0 and 20.2 months, for current (i.e., those maturing within 12 months at the reporting date) and non-current positions, respectively. The entire portfolio of marketable securities (current and non-current) has a weighted average duration of 5.5 months.