UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22980

Angel Oak Funds Trust

(Exact name of registrant as specified in charter)

3344 Peachtree Rd. NE, Suite 1725

Atlanta, Georgia 30326

(Address of principal executive offices) (Zip code)

Dory S. Black, Esq., President

3344 Peachtree Rd. NE, Suite 1725

Atlanta, Georgia 30326

(Name and address of agent for service)

Copy to:

Douglas P. Dick

Stephen T. Cohen

Dechert LLP

1900 K Street NW

Washington, DC 20006

(404) 953-4900

Registrant’s telephone number, including area code

Date of fiscal year end: January 31

Date of reporting period: January 31, 2022

Item 1. Reports to Stockholders.

Annual Report

January 31, 2022

Angel Oak Multi-Strategy Income Fund

Angel Oak Financials Income Fund

Angel Oak High Yield Opportunities Fund

Angel Oak UltraShort Income Fund

Angel Oak Core Impact Fund

Angel Oak Capital Advisors, LLC

3344 Peachtree Road NE

Suite 1725

Atlanta, GA 30326

(404) 953-4900

Table of Contents

Dear Shareholder,

Chairman Jerome Powell has pivoted from a transitory to persistent view of inflation (the “Powell Pivot”), and the time to prepare for interest rate liftoff is here. Fears of a Federal Reserve (Fed) behind the curve on inflation had markets on edge heading into the final days of 2021. Unlike in 2018, when Powell pivoted from “a long way from neutral” to suddenly dovish rhetoric and subsequent easing, Powell pivoted to a more hawkish tone on November 30 in his Senate Banking Committee testimony, when he offered a mea culpa, stating it was time to retire the word “transitory.” On December 1, he went on to tell the House Financial Services Committee, “We’ve seen inflation be more persistent. We’ve seen the factors that are causing higher inflation to be more persistent. Policy has adapted to that and will continue to adapt.” This is a significant shift away from his previous transitory stance and emphasis on maximum employment. In fact, Powell suddenly shifted, noting persistent inflation might hamper maximum employment: “To get back to the kind of great labor market we had before the pandemic, we are going to need price stability, and in a sense, the risk of persistent inflation is also a major risk to getting back to such a labor market.” We were not expecting this policy U-turn, especially considering the recent rise of the omicron variant, but like in 2021, we expect our positioning toward high-quality income in shorter-duration areas of U.S. structured credit, high yield, and financials will continue to outperform in 2022.

As we expected in our 2021 outlook, inflation and growth were brisk in 2021, and more importantly, our persistent view steered us away from long-duration, more interest rate sensitive areas of traditional fixed income, where yields pale in comparison to the recent inflation levels, which were last seen in the 1980s. We favored high-quality, short-duration areas of U.S. structured credit, notably mortgage and consumer collateral, select high-yield issuers, and select tranches of collateralized loan obligation (CLO) tranches. This view and positioning resulted in positive performance amid a yield-starved world at the zero-bound challenged by rising rates. Like 2021, we believe 2022 will continue to be driven by strong growth, persistent inflation pressures, and a robust consumer, and despite the unexpected pivot toward liftoff, financial conditions will remain extraordinarily accommodative. Amid a backdrop of solid growth, we expect a benign credit environment driven by lower but still solid earnings and extraordinarily low default expectations. Therefore, we continue to target similar positioning in 2022 and especially favor amortizing areas of mortgage- and consumer-centric areas of structured credit backed by rising collateral values.

The year 2021 was defined by historic growth and inflation amid a V-shaped recovery that will rival anything in recent economic history. Real gross domestic product (GDP) averaged 5.6%, and the headline Consumer Price Index (CPI) averaged 4.6%, which sent risk assets, particularly those benefiting from higher inflation, soaring. Long-duration fixed income, despite the rally in rates in the second half of 2021, had its worst year since 2013, the year of the taper tantrum. Our structured credit, high-yield, and financials strategies had solid performance despite the rising rate environment and waffling credit markets in the second half of 2021 due to high current income, spread compression on favorable fundamentals, and short-duration profiles. We expect that the higher yield profile relative to the duration will continue to stand out as a performance differentiator in 2022, as we expect U.S. real GDP to average 4%, headline CPI to average 5%, and the headline unemployment rate to descend to its pre-COVID-19 level of 3.5% by the end of 2022. We remain in the persistent inflation camp, as we wrote extensively about in our 2021 Mid-Year Outlook. After the Powell Pivot and the January 26th Federal Open Market Comittee (FOMC) meeting, we now expect two to three target rate hikes in 2022 and the 10-year note yield to end the year at approximately 2.25%. Expectations for an even tighter labor market amid the “Great Resignation” will further enhance an incredibly robust U.S. consumer, as it should result in more wage growth. Wage growth is expected to continue, as the U.S. consumer has already accumulated a $2.2 trillion war chest of excess savings since March 2020!1 As the U.S. consumer is saving and earning more, household debt ratios are at historic lows. A strong U.S. consumer credit profile coupled with pent-up demand because of the pandemic should further support our view for solid growth and high inflation in 2022. This environment should continue to pressure risk-free rates and long-duration fixed income as market participants price in more Fed tightening in the future but recognize how easy financial conditions remain, reinvigorating the bear curve-steepening trend witnessed in the first half of 2021.

It’s important to emphasize that even with the Powell Pivot, financial conditions are still near their most favorable point in the history of the Goldman Sachs Financial Conditions Index. Moreover, the 10-year real yield is extremely negative, and we expect it will remain near these levels in 2022. Recall that this sustained level of negative real yields has only occurred twice before in the post-WWII era, in the mid-1970s and the early 1980s, lasting several years in both instances. This backdrop will support not only our consensus view of solid growth and inflation but also a favorable earnings environment, low default expectations, and stable credit spreads. In fact, corporate profit margins are at levels last seen in the 1950s! Even if these subside in 2022, we believe that they will likely remain at historically attractive levels. The last time the Fed began tightening on the front end, in 2015, high-yield spreads tightened into 2017. It wasn’t until Powell’s first pivot in 2018 that credit spreads began to widen as the market began to price in the fact that the Fed had gone too far, and a slowdown was imminent. Moreover, in the past 13 hiking cycles since 1955, U.S. corporate BBB spreads on average were 47 basis points tighter in the 12 months following the first hike.2

1 Source: Morgan Stanley

2 Source: Deutsche Bank

1

While broader credit markets took a pause in the second half of 2021 due to new COVID-19 variants and the Powell Pivot, we remain constructive toward credit, particularly U.S. structured credit. We are positioning for a longer-term expansion in areas of mortgage- and consumer-centric structured credit with attractive income and the potential for spread tightening and price appreciation in 2022. In addition to a brisk recovery of growth and inflation, 2021 brought a historic supply of new issuance in the credit markets, particularly in U.S. structured credit. After issuance came to a grinding halt in 2020 due to the pandemic, the V-shaped recovery, improving consumer confidence, and a growing appetite for attractive financing on the heels of post-COVID-19 accommodation sent issuance to post-global financial crisis (GFC) highs across all subsectors in 2021. Technical headwinds of heavy supply began to weigh on credit spreads in some of our more favored areas of structured credit toward the end of 2021 and into 2022 despite improving fundamentals. We will seek to take advantage of any technical weakness into 2022. We will continue to target de-leveraging, short-duration areas of U.S. structured credit, and select areas of high yield and financials within corporate credit as markets navigate potential interest rate liftoff in 2022.

Thank you for your continued support.

Respectfully yours,

Sam Dunlap

Chief Investment Officer, Public Strategies

The opinions expressed are subject to change at any time, are not guaranteed, and should not be considered investment advice. Please refer to the Schedule of Investments in this report for a complete list of Funds’ holdings.

Must be accompanied or preceded by a prospectus.

Mutual fund investing involves risk. Principal loss is possible.

The Angel Oak Funds are distributed by Quasar Distributors, LLC.

Definitions:

Basis Point (bps): One hundredth of one percent. Used to denote the percentage change in a financial instrument.

Spread: The difference in yield between two bonds of similar maturity but different credit quality.

2

Angel Oak Multi-Strategy Income Fund

How did the Fund perform during the period?

For the 12-month period that ended January 31, 2022, the Fund’s Institutional Shares (ANGIX) returned 2.87%, while the Fund’s A Shares (ANGLX) and C Shares (ANGCX) returned 2.71%1 and 1.78%1, respectively. During the same period, the Fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index, returned -2.97%.

What were the main contributors to and detractors from the Fund’s performance during the period?

The primary positive contributor to performance was higher current income and duration short of the benchmark due to an overweight to predominately amortizing areas of U.S. structured credit. The Fund’s current income of 4.76% was a positive contributor relative to the benchmark, offsetting a decline in prices of approximately -1.92%. Prices were lower during the period, notably during the second half due to the rise of new COVID-19 variants, concerns surrounding the Powell Pivot, surging inflation, and robust new issue supply in structured credit. The effective duration of the Fund continues to be much lower than the benchmark. The duration of the strategy was approximately 2.8-3.1 throughout 2022 compared to the benchmark, which was in the range of 6.0-6.5 during the period. The portfolio’s duration remains well short of the benchmark, and we believe this profile could lead to continued outperformance in the year ahead.

For the period, the majority of the allocation and contribution to the Fund came from non-agency residential mortgage-backed securities (NA RMBS). NA RMBS currently stands at approximately 63.21% of the Fund and had a total return of approximately 4.32%, contributing approximately 2.84% to the Fund’s performance. The asset-backed securities (ABS) allocation, approximately 9.55% of the allocation, was up approximately 3.07% total return, contributing approximately 0.29% to performance. The corporate bond allocation, approximately 4.88% of the allocation, was up 3.71% total return, contributing approximately 0.24%. The collateralized loan obligation (CLO) allocation, approximately 4.09% of the Fund was up 8.45% total return, contributing approximately 0.52%. Finally, the non-agency commercial mortgage-backed securities (NA CMBS) allocation, currently 3.37% of the Fund, was up approximately 6.36%, contributing approximately 0.19%. The only detractor to performance was the agency CMBS and U.S. Treasury portion of the portfolio, detracting approximately 0.25% during the period due to higher rates.

As we expected in our 2021 outlook, inflation and growth were brisk in 2021. More importantly, our persistent view steered us away from long-duration, more interest rate sensitive areas of traditional fixed income, where yields pale in comparison to the recent inflation levels, which were last seen in the early 1980s. We favored high-quality, short-duration areas of U.S. structured credit, notably mortgage and consumer collateral, select high-yield issuers, and select tranches of CLOs. This view and positioning resulted in positive performance amid a yield-starved world at the zero-bound challenged by rising interest rates. Our structured credit, high-yield, and financials strategies had solid performance despite the rising rate environment and waffling credit markets in the second half of 2021 due to high current income, favorable credit fundamentals, and short-duration profiles.

What is your outlook heading into 2022, and how is the Fund positioned?

Like 2021, we believe that 2022 will continue to be driven by strong growth, persistent inflation pressures, and a robust consumer and, despite the unexpected Powell Pivot toward liftoff, financial conditions should remain extraordinarily accommodative. Amid a backdrop of solid growth, we expect a benign credit environment driven by lower but still solid earnings and extraordinarily low default expectations. Therefore, we continue to target similar positioning in 2022 and especially favor amortizing areas of mortgage- and consumer-centric areas of structured credit backed by rising collateral values.

The higher yield profile relative to the duration will continue to stand out as a performance differentiator in 2022, as we expect U.S. real GDP to average 4%, headline CPI to average 5%, and the headline unemployment rate to descend to its pre-COVID-19 level of 3.5% by the end of 2022. We remain in the persistent inflation camp. After the Powell Pivot and the January 26th FOMC meeting, we now expect two to three target rate hikes in 2022 and the 10-year note yield to end the year at approximately 2.25%. Expectations for an even tighter labor market amid the “Great Resignation” will further enhance an incredibly robust U.S. consumer, as it should result in more wage growth. Wage growth is expected to continue, as the U.S. consumer has already accumulated a $2.2 trillion war chest of excess savings since March 2020!2 As the U.S. consumer is saving and earning more, household debt ratios are at historic lows. A strong U.S. consumer credit profile coupled with pent-up demand because of the COVID-19 pandemic should further support our view for solid growth and high inflation in 2022. This environment should continue to pressure risk-free rates and long-duration fixed income as market participants price in more Fed tightening in the future but recognize how easy financial conditions remain, reinvigorating the bear curve-steepening trend witnessed in the first half of 2021.

1Returns presented are without load. Please reference the investments results section of the report for with load returns.

2 Source: Morgan Stanley

3

While broader credit markets took a pause in the second half of 2021 due to the rising COVID-19 variants and the Powell Pivot, we remain constructive toward credit, particularly U.S. structured credit. We are positioning for a longer-term expansion in areas of mortgage- and consumer-centric structured credit with attractive income and the potential for spread tightening and price appreciation in 2022. In addition to a brisk recovery of growth and inflation, 2021 brought a historic supply of new issuance in the credit markets, particularly in U.S. structured credit. After issuance came to a grinding halt in 2020 due to the pandemic, the V-shaped recovery, improving consumer confidence, and growing appetite for attractive financing on the heels of post-COVID-19 accommodation sent issuance to post-GFC highs across all subsectors. Technical headwinds of heavy supply began to weigh on credit spreads in some of our more favored areas of structured credit toward the end of 2021 and into 2022 despite improving fundamentals. We will seek to take advantage of any technical weakness into 2022.

As of 1/31/22, the subsidized and unsubsidized 30-Day SEC yield for ANGIX were 3.79% and 3.79%, respectively.

Past performance is not a guarantee of future results.

Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower rated and non-rated securities present a greater risk of loss to principal and interest than higher rated securities. Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware of including credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Derivatives involve risks different from, and in certain cases, greater than the risks presented by more traditional investments. Derivatives may involve certain costs and risks such as illiquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. The Fund may use leverage, which may exaggerate the effect of any increase or decrease in the value of securities in the Fund’s portfolio or higher and duplicative expenses when it invests in mutual funds, ETFs, and other investment companies. For more information on these risks and other risks of the Fund, please see the Prospectus.

Definitions:

Bloomberg U.S. Aggregate Bond Index: An unmanaged index that measures the performance of the investment-grade universe of bonds issued in the United States. The index includes institutionally traded U.S. Treasury, government-sponsored, mortgage, and corporate securities. It is not possible to invest directly in an index.

Current Income: Represents return from interest and amortized/accrued cost basis.

Duration: Measures a portfolio’s sensitivity to changes in interest rates. Generally, the longer the duration, the greater the price change relative to interest rate movements.

Tranche: A portion of debt or structured financing. Each portion, or tranche, is one of several related securities offered at the same time but with different risks, rewards, and maturities.

4

Angel Oak Financials Income Fund

How did the Fund perform during the period?

For the 12-month period that ended January 31, 2022, the Fund’s Institutional Shares (ANFIX) returned 5.64%, while the Fund’s A Shares (ANFLX) and C Shares (AFLCX) returned 5.48%1 and 4.63%1, respectively. During the same period, the Fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index, returned -2.97%, and the Bloomberg U.S. Aggregate 3-5 Year Index, which most closely matches the Fund’s duration profile, returned -2.82%.

What were the main contributors to and detractors from the Fund’s performance during the period?

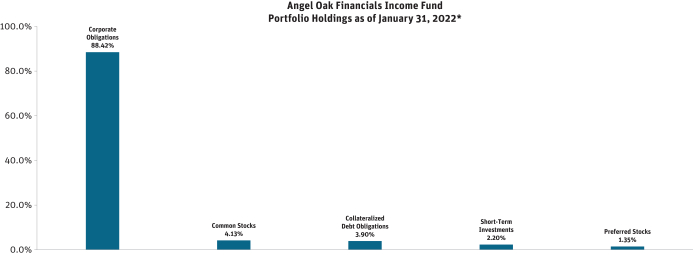

The financial sector accounts for substantially all of the Fund’s assets. There are three areas of primary focus within the financial sector: community bank debt, non-bank financials debt, and community bank equity. The Fund’s financial sector asset allocation (98% of Fund assets) comprises 75% of assets in community bank debt, 21% of assets in non-bank financials, and 4% of assets in community bank equities. In addition, 2% of Fund assets are in cash and other assets.

Financials debt outperformed the broader corporate credit market due to the fundamental strength of the sector as well as its short-duration profile. Additionally, the investor base of the underlying bonds tends toward buy-and-hold investors, which contributes to the low relative volatility.

| | • | | Capital: Tier 1 and total regulatory capital remain near multi-decade highs for U.S. commercial banks. We are seeing increasing capital optimization since the Fed has loosened COVID-19-related restrictions on capital management and allowed banks to resume managing their excess capital. |

| | • | | Asset Quality: A large majority of banks have emerged largely unscathed from any potential COVID-19-related credit cycle. Loan deferrals have returned to performing status, and non-performing assets are at the lowest levels in 15 years. We do expect we could see some modest normalization over 2022 as the benefits from stimulus programs roll off, but banks remain well reserved for any modest increase in credit costs. |

| | • | | Excess Liquidity: Banks are flush with liquidity given the various stimulus plans, including the paycheck protection program (PPP). Loan to deposit ratios are hovering near 50%, and cash is running at approximately double normalized levels. |

What is your outlook for 2022, and how is the Fund positioned?

We maintain a high degree of conviction toward the financial sector broadly heading into 2022, with positive tailwinds to growth driven by the continued economic recovery and the expected Fed Funds rate hikes. We see compelling opportunities across community bank debt, small-cap non-bank financials debt, and select pockets of financial services preferred and common equity.

The outlook is particularly bright for the banking sector in 2022, with the Fed poised to raise rates, loan growth inflecting positively, and significant excess liquidity available for deployment. Mergers and acquisitions (M&A) continue to accelerate from COVID-19 lows and have hit 20-plus-year highs in terms of “mega deals” (deal value more than $500 million). In the banking sector, we see the best relative value in the community bank sub-sector, in both subordinated debt and small-cap equities.

Fundamentally, banks should benefit from stronger net interest income and earnings as (1) net interest margin (NIM) expands from a combination of higher rates, low deposit betas, and an asset mix shift from cash and investments to loans, and (2) higher-earning asset balances as PPP forgiveness runs its course and organic loan growth accelerates.

We believe community bank debt offers one of the best risk/reward opportunities across investment-grade credit, with its excess yield, short-duration, and low volatility profile. Bank debt issuance remains robust, with expected community bank debt issuance in the range of $8-$10 billion annually. While spreads compressed in 2021 as the market continued to mature, and the investor base expanded to see broader participation from banks, we expect spreads will begin to normalize toward 2019 levels as banks’ excess liquidity gets redeployed into lending opportunities.

On the equity side, despite relative outperformance in 2021, banking sector valuations remain attractive relative to historical levels and the broader market. We expect NIM expansion and higher loan growth will benefit valuation multiples, and we see value in the smaller banks, which tend to be more asset sensitive. Additionally, smaller banks could see outsized returns as likely consolidation targets in an accelerating M&A environment.

1Returns presented are without load. Please reference the investments results section of the report for with load returns.

5

Across the financial services landscape more broadly, we are most positive on investment-grade, small-cap insurance senior debt and residential mortgage REIT common and preferred equities.

Senior debt opportunities in small-cap insurance have been expanding over the past several years, but the sector remains a niche investment opportunity that provides corresponding excess yield for investment-grade debt in a highly regulated industry. We are most favorable on the property and casualty and the fronting sub-segments. Industry fundamentals remain positive, with premium pricing increases expected to persist in 2022.

Additionally, we have a positive bias to hybrid and non-agency mortgage REITs (mREITs) within the residential mREIT universe, given expectations for robust home price appreciation, a strong consumer, still-low interest rates, and the prospects for a reduced Government Sponsored Entity (GSE) footprint. Upside to book value and dividends, along with attractive valuation and dividend yields, drives our constructive view on common equity, and we see selective opportunities within preferred equity as well.

We do not anticipate any meaningful credit deterioration in 2022. Nonperforming asset levels remain strong, sitting at the lowest level in 15 years. Industry profitability remains solid, and capital levels continue to increase, providing a sizable cushion for any adverse credit events as well as currency for inorganic growth opportunities. We remain disciplined in our underwriting, with particular emphasis on credit and interest rate risks.

We do not anticipate our sub-sector allocations within financial services will change materially in 2022.

Past performance is not a guarantee of future results.

Mutual fund investing involves risk; principal loss is possible. Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and nonrated securities present a greater risk of loss to principal and interest than higher-rated securities do. Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware of, including credit risk, prepayment risk, possible illiquidity, and default, as well as increased susceptibility to adverse economic developments. Derivatives involve risks different from—and in certain cases, greater than—the risks presented by more traditional investments. Derivatives may involve certain costs and risks such as illiquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Investing in derivatives could lead to losses that are greater than the amount invested. The Fund may make short sales of securities, which involves the risk that losses may exceed the original amount invested. The Fund may use leverage, which may exaggerate the effect of any increase or decrease in the value of securities in the Fund’s portfolio or the Fund’s net asset value, and therefore may increase the volatility of the Fund. Investments in foreign securities involve greater volatility and political, economic, and currency risks and differences in accounting methods. These risks are increased for emerging markets. Investments in fixed-income instruments typically decrease in value when interest rates rise. The Fund will incur higher and duplicative costs when it invests in mutual funds, ETFs, and other investment companies. There is also the risk that the Fund may suffer losses due to the investment practices of the underlying funds. For more information on these risks and other risks of the Fund, please see the Prospectus.

Definitions:

Bloomberg U.S. Aggregate Bond Index: An unmanaged index that measures the performance of the investment-grade universe of bonds issued in the United States. The index includes institutionally traded U.S. Treasury, government-sponsored, mortgage and corporate securities. It is not possible to invest directly in an index.

Bloomberg U.S. Aggregate 3-5 Year Index: An index that tracks bonds with 3-5 year maturities within the Bloomberg U.S. Aggregate Bond Index.

Duration: Measures a portfolio’s sensitivity to changes in interest rates. Generally, the longer the duration, the greater the price change relative to interest rate movements.

Spread: The difference in yield between two bonds of similar maturity but different credit quality.

Tier 1 Capital: Tier 1 capital comprises common equity, retained earnings, and perpetual preferred stock. Tier 1 capital represents the core source of funding that the bank uses to ensure long term viability and acts as a cushion to protect depositors against loss.

6

Angel Oak High Yield Opportunities Fund

How did the Fund perform during the period?

For the 12-month period that ended January 31, 2022, the Fund’s Institutional Shares (ANHIX) returned 3.62%, while the Fund’s A Shares (ANHAX) returned 3.34%1. During the same period, the Fund’s benchmark, the Bloomberg U.S. Corporate High Yield Index, returned 2.06%.

What were the main contributors to and detractors from the Fund’s performance during the period?

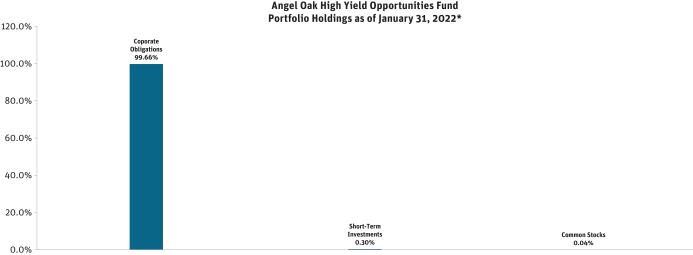

The corporate bond allocation, which accounted for more than 99% of the asset allocation, returned 4.44%, outperforming the benchmark return of 2.06%, and contributed 4.26% to the total return of the Fund. Within the corporate bond allocation, the largest positive contributor to performance was the basic industry sector, and the positive attribution was primarily driven by selection. The contribution was broad-based across holdings, with the biggest contribution from a supplier of metallurgical coal necessary in the production of virgin steel that was in strong demand and saw record prices in 2021.

With contribution on par with basic industry, the communications sector was the second-largest positive contributor to performance. The positive attribution was evenly split between allocation and selection. Being underweight, one of only two sectors with a negative return for the period accounted for the positive attribution from allocation. The positive attribution from selection was from being overweight on advertising dependent issuers in the television and radio subsectors that have benefited from the economic recovery more so than the utility-like cable and telecom issuers.

The largest detractor from corporate bond performance was the electrics sector. The negative attribution was due to selection and attributable to an independent power producer whose primary market is the PJM region of the U.S. where where capacity prices have been weak; they had an unexpected loss due to winter storm Uri, and liquidity is under pressure due to the need to post additional collateral related to existing hedges that are now underwater as forward prices have risen.

The finance companies sector was also a detractor. The negative attribution was due to selection and our exposure to several mortgage originators that underperformed, with rising interest rates negatively impacting mortgage origination volumes and margins.

What is your outlook for 2022, and how is the Fund positioned?

Although pandemic-related fiscal stimulus is tailing off, and the Fed is beginning to tighten monetary policy with the wind down of asset purchases, and are expected to raise interest rates and shrink the size of their holdings of mortgages and treasuries, the fundamental outlook for high yield corporate credit is generally favorable, reflecting expectations for above-trend economic growth supported by an improving employment market, excess household savings, record net worth, and household debt payments as a percentage of disposable income near historic lows. In a rising rate environment, we believe that high-yield corporate bonds with less than half the duration, more than three times as much credit spread, and almost double the total yield, look well positioned relative to the investment-grade Bloomberg U.S. Corporate Bond Index.

While the ultimate goal of the Fed is to orchestrate a soft landing by slowing growth and reducing inflationary pressures just enough to avoid tipping the economy into recession, corporations are in a strong position with record margins, strong free cash flow generation, and declining leverage. That said, we are sensitive to the fact that we are entering a period of tightening monetary policy that includes accelerated tapering of asset purchases, interest rate increases, and the potential reduction of the size of the Fed’s balance sheet. The compressed nature of events has the potential for increased risk asset volatility. As such, we are focused on risk/reward and the risk of idiosyncratic events, underscoring our emphasis on credit selection.

Past performance is not a guarantee of future results.

Mutual fund investing involves risk; principal loss is possible. Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and nonrated securities present a greater risk of loss to principal and interest than higher-rated securities do. Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware of, including credit risk, prepayment risk, possible illiquidity, and default, as well as increased susceptibility to adverse economic developments. Derivatives involve risks different from—and in certain cases, greater than— the risks presented by more traditional investments. Derivatives may involve certain costs and risks such as illiquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Investing in derivatives could lead to losses that are greater than the amount invested. For more information on these risks and other risks of the Fund, please see the Prospectus.

1Returns presented are without load. Please reference the investments results section of the report for with load returns.

7

Definitions:

Bloomberg U.S. Corporate High Yield Bond Index: An unmanaged market value-weighted index that covers the universe of fixed rate, non-investment-grade debt. It is not possible to invest directly in an index.

Spread: The difference in yield between two bonds of similar maturity but different credit quality.

Duration: Measures a portfolio’s sensitivity to changes in interest rates. Generally, the longer the duration, the greater the price change relative to interest rate movements.

Free Cash Flow: A financial performance calculation that measures how much operating cash flows exceed capital expenditures.

8

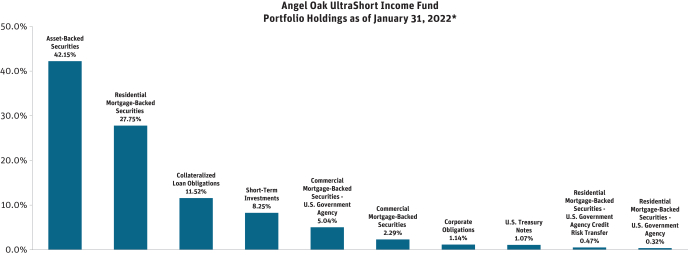

Angel Oak UltraShort Income Fund

How did the Fund perform during the period?

For the 12-month period that ended January 31, 2022, the Fund’s Institutional Shares (AOUIX) returned 0.51%, while the Fund’s A Shares (AOUAX) returned 0.27%. During the same period, the Fund’s benchmark, the Bloomberg U.S. Treasury Bill 9-12 Month Total Return Index, was down -0.26%.

What were the main contributors to and detractors from the Fund’s performance during the period?

Credit strategies and higher current income were the primary benefits to Fund performance relative to the benchmark. Duration positioning short of the index was a contributor relative to the benchmark, as short-term Treasury yields increased, particularly throughout the second half of the year. Spread duration longer than the benchmark was a net contributor due to higher income and modestly tighter credit spreads of approximately 20 basis points year over year. Short-term rates repriced higher in the final quarter as markets repriced Fed expectations. To start 2021, markets expected the Fed to be on hold through 2023 as most economists predicted inflation pressures would be more transitory than persistent. The resurgence of inflationary pressures following the decrease in COVID-19 cases from the COVID-19 delta variant in early Q3 shifted market participants’ view that short-term inflation pressures would be sustained for many months. Subsequently, short-term rates repriced the FOMC’s hiking path in 2022, from zero hikes to over six hikes in just a few months. The one-year swap rate increased 70 basis points, from 0.18% to 0.88%, while the two-year swap rate increased 1.14%, from 0.19% to 1.33%. Overall, the interest rate duration remained short of the Fund’s benchmark, in the range of 0.5 to 0.75, benefiting performance as short-term rates rose in the final few months of the fiscal year.

The Fund’s overweight to credit, particularly structured credit, over government bonds provided for higher current income than the benchmark. The current yield of the benchmark was very low throughout the majority of the year, while the average distribution yield of the Fund was 1.31%. For the fiscal year, income return was 1.30% for the Fund while price return was -0.79%, netting a total return of 0.51%.

Residential mortgage-backed securities (RMBS), asset-backed securities (ABS), and collateralized loan obligations (CLOs), the largest credit asset classes within the Fund, were all positive contributors to Fund performance. RMBS produced a total return of 0.69% and contributed 22 basis points to Fund performance. The RMBS allocation is a targeted mix of primarily new-issue subsectors. Portfolio managers found particular value in new-issue sectors of RMBS credit but shortened spread duration during the middle of the year, as spreads tightened in the first half. The strategy focused on areas of non-Qualified Mortgage (non-QM) seniors, Reperforming Loan/Non-Performing Loans (RPL/NPL), and prime jumbo seniors, which subsequently saw measurable spread tightening as markets normalized throughout the first half of 2021. Additionally, portfolio managers viewed underlying call risk in the first half of 2021 as mispriced. Calling seasoned non-QM deals is less efficient due to the underlying owners of the call rights and their ability to warehouse loans of called collateral and/or resecuritize into new deals. This focus on seasoned, increasingly callable tranches provided a shorter-duration profile for the allocation while taking advantage of the inefficiency of non-QM callability. This was an attractive allocation for the Fund while spreads and short-term interest rates were low during the middle of 2021. The allocation to non-agency RMBS was reduced during the year, as total return opportunities were limited in the sector. The allocation fell approximately 7%, from 35% to 28%.

The ABS allocation was a positive contributor to Fund performance. ABS had a total return of approximately 88 basis points, contributing 42 basis points to Fund performance. The allocation to ABS increased throughout the period, from 36% to 42%, mainly as a rotation from non-agency RMBS. The focus of the ABS allocation was within short-duration, high-credit quality assets. As spreads continued to tighten for high-quality assets in the first half of the year, the focus of the allocation was within amortizing loans of senior and mezzanine tranches of ABS. Auto ABS started the year as an outperformer within short-duration ABS markets. Given the shifting relative value landscape, the Fund rotated from auto to consumer ABS throughout the period. Senior tranches of consumer loan ABS tend to be rated AA through BBB and begin to amortize on the first remittance date, while AA-BBB-rated auto ABS do not receive principal paydowns for many months. Given the current macro backdrop, the portfolio focused on senior and mezzanine consumer loan ABS, while rotating out of auto ABS. The consumer loan allocation started the period at approximately 10% of the Fund and ended the period at approximately 22% of the Fund. Conversely, auto ABS started the period at 20% of the Fund and ended the period at 16% of the Fund.

CLOs were the best-performing asset class of the top three allocations. CLOs exhibited a total return of approximately 1.23%, contributing 19 basis points to Fund performance. The CLO allocation primarily consists of AAA-rated tranches, and the floating rate nature of the asset class was an attractive organic fit for the targeted duration below the benchmark. The CLO allocation consists of a combination of X classes and very seasoned AAA/AA/A-rated tranches. Given the specific cashflow window of the X-tranche structure, the Fund was focused on acquiring these tranches in the primary market when they were available. The

9

allocation remained in the 10% to 15% range throughout most of the fiscal year while finishing the year down only 1% year over year, or at approximately 12%. Within the sector, the X-tranche allocation increased from 28% to 41% during the fiscal year. The CLO allocation ended the period at a current yield-to-worst of 2.33% and a weighted average life of 1.5, with over 85% AAA-rated tranches.

The government allocation is a strategic allocation in the Fund that provides many benefits, including improved diversification, low correlation to credit, and enhanced liquidity. The government allocation is a combination of cash, US Treasuries, agencies, and agency-backed securities. The government allocation was near unchanged at approximately 14% of Fund assets. Within the allocation, US Treasuries were reduced while cash and equivalents and agency CMBS were increased. The government allocation was a net detractor to performance of 3 basis points to the Fund.

What is your outlook heading into 2022, and how is the Fund positioned?

The sharp repricing of Fed expectations and the prospect for higher interest rates in 2022 will be the key drivers of performance for ultrashort strategies over the intermediate term. The current market expectation for interest rate increases in 2022 is six, which would increase the Fed Funds’ target rate above 1.5% by the end of the year. This rate path is very bullish for rising income within the Fund, but expected volatility is higher than a year prior. Simultaneously, higher total return opportunities are becoming available, with a steeper yield curve and a steeper credit term structure. Looking forward, the potential for price appreciation has increased compared to a year prior.

The Fund continues to focus across a diversified mix of primarily structured credit. Recently, the Fund has increased the allocation to ABS and short-duration corporate bonds to focus on high-current-income, limited-duration, and attractive-spread profiles. The effective duration of the Fund was reduced initially in the prior year but may increase in the future if markets price in an overly hawkish FOMC. Heading into 2022, the Fund has maintained a higher allocation to AAA-rated assets, at approximately 45%. The coming year should provide significant opportunity in the ultrashort markets.

As of 1/31/22, the subsidized and unsubsidized 30-Day SEC yield for AOUIX were 1.30% and 1.09%, respectively.

Past performance is not a guarantee of future results.

Investing involves risk. Principal loss is possible. The Fund’s derivative investments have risks, including the imperfect correlation between the value of such instruments and the underlying asset, rate or index, which creates the possibility that the loss on such instruments may be greater than the gain in the value of the underlying asset, rate or index; the loss of principal; the possible default of the other party to the transaction; and illiquidity of the derivative investments. The Fund may invest in illiquid securities and restricted securities. Investments in restricted securities could have the effect of increasing the amount of the Fund’s assets invested in illiquid securities if qualified institutional buyers are unwilling to purchase these securities. Changes in interest rates generally will cause the value of fixed-income instruments held by the Fund to vary inversely to such changes. Below investment grade instruments are commonly referred to as “junk” or high-yield instruments and are regarded as predominantly speculative with respect to the issuer’s capacity to pay interest and repay principal. Lower grade instruments may be particularly susceptible to economic downturns. The price paid by the Fund for asset-backed securities, including CLOs, the yield the Fund expects to receive from such securities and the average life of such securities are based on a number of factors, including the anticipated rate of prepayment of the underlying assets. Mortgage-backed securities are subject to the general risks associated with investing in real estate securities; that is, they may lose value if the value of the underlying real estate to which a pool of mortgages relates declines. For more information on these risks and other risks of the Fund, please see the Prospectus.

Definitions:

Average Distribution Yield: The sum of the twelve monthly distributions during the period divided by the end of period NAV of AOUIX.

Basis point (bps): One hundredth of one percent. Used to denote the percentage change in a financial instrument.

Bloomberg 9-12 Month U.S. Treasury Bill Index: Measures the performance of U.S. Treasury bills, notes and bonds with a remaining maturity between 9-12 months. The index does not include trading and management costs. It is not possible to invest directly in an index.

Current Yield: A bond’s current yield is an investment’s annual income, including both interest payments and dividends payments, which are then divided by the current price of the security.

Distribution Yield: The distribution yield is calculated by annualizing actual dividends distributed for the monthly period ended on the date shown and dividing by the net asset value on the last business day for the same period. The yield does not include long-or short-term capital gains distributions or the return of capital.

Duration: Measures a portfolio’s sensitivity to changes in interest rates. Generally, the longer the duration, the greater the price change relative to interest rate movements.

Income Return: The positive/negative return from interest and accrued/amortized income.

Spread: The difference in yield between two bonds of similar maturity but different credit quality.

Tranche: A portion of debt or structured financing. Each portion, or tranche, is one of several related securities offered at the same time but with different risks, rewards and maturities.

Weighted Average Life (WAL): Average length of time that each dollar of unpaid principal on a loan, a mortgage or an amortizing bond remains outstanding.

Yield-to-Worst (YTW): The lowest potential yield that can be received on a bond without the issuer actually defaulting. Loss-adjusted (LA) takes into account Angel Oak Capital’s assumptions for prepayment speeds and defaults.

Diversification does not guarantee a profit or protect against a loss in declining markets.

10

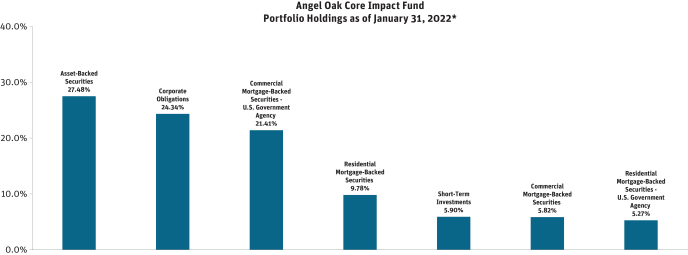

Angel Oak Core Impact Fund

How did the Fund perform during the period?

For the period ended January 31, 2022, the Fund’s Institutional Shares (AOIIX) returned -1.28%. During the same period, the Fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index returned -1.53%.

What were the main contributors to and detractors from the Fund’s performance during the period?

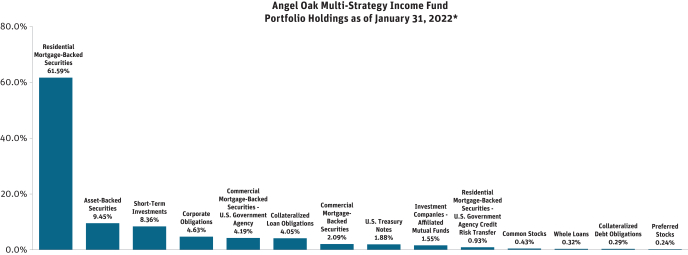

The primary positive contributor to performance was duration short of the benchmark. The Fund’s current income was approximately 0.46% and prices were down approximately -1.74%. Prices were lower during the period due to rising rates, concerns surrounding the Powell Pivot, surging inflation, and robust new issue supply in structured credit. The duration of the strategy was approximately 4.2-4.4 throughout the period compared to the benchmark, which was in the range of 6.5-6.7 during the period. The portfolio’s duration is short of the benchmark, and we believe this profile could potentially lead to continued outperformance in the year ahead.

For the period, the largest allocation in the Fund was the asset-backed securities (ABS) allocation, approximately 27.48% of the allocation, which was up approximately 0.12% total return but detracted approximately -0.04% as the portfolio was ramping. The corporate bond allocation, approximately 24.34% of the allocation, was up 0.79% total return, but detracted approximately -0.07% as the portfolio was ramping. The agency commercial mortgage-backed securities (CMBS) allocation, approximately 20.64% of the allocation, was down approximately -3.95%, detracting -0.48%. The non-agency residential mortgage-backed securities (NA RMBS) was approximately 9.78% of the Fund and had a total return of approximately -0.15% but contributed approximately 0.02% to the Fund’s performance as the Fund was ramping. The non-agency CMBS (NA CMBS) allocation, currently 6.59% of the Fund, was up approximately 0.54%, contributing approximately 0.03%. Finally, the agency RMBS allocation, approximately 5.27% of the Fund, was down approximately -1.83% total return, detracting approximately -0.09%.

The Fund seeks total return while giving special consideration to positive aggregate environmental, social, and/or governance (ESG) impact outcomes. The Fund allocates to fixed income securities that have a positive impact on the global environment across all levels of society and utilizes active engagement with issuers to positively impact their ESG factors by promoting sustainable practices. In addition to our ESG considerations, the Fund was positioned consistent with our 2021 outlook. Inflation and growth were brisk in 2021, and more importantly, our persistent view steered us away from long-duration, more interest rate-sensitive areas of traditional fixed income. We favored shorter-duration areas of U.S. structured credit, notably mortgage and consumer collateral, and select corporate issuers with higher current income profiles relative to the benchmark. This view and positioning resulted in outperformance of the index amid a yield-starved world at the zero-bound challenged by rising rates.

What is your outlook heading into 2022, and how is the Fund positioned?

Like 2021, we believe that 2022 will continue to be driven by strong growth, persistent inflation pressures, and a robust consumer and, despite the unexpected Powell Pivot toward liftoff, financial conditions will likely remain extraordinarily accommodative. Amid a backdrop of solid growth, we expect a benign credit environment driven by lower but still solid earnings and extraordinarily low default expectations. Therefore, we continue to target similar positioning in 2022 and especially favor amortizing areas of mortgage- and consumer-centric areas of structured credit backed by rising collateral values.

The higher yield profile relative to the duration will continue to stand out as a performance differentiator in 2022, as we expect U.S. real GDP to average 4%, headline CPI to average 5%, and the headline unemployment rate to descend to its pre-COVID-19 level of 3.5% by the end of 2022. We remain in the persistent inflation camp. After the Powell Pivot and the January 26th FOMC meeting, we now expect four target rate hikes in 2022 and the 10-year note yield to end the year at approximately 2.25%. Expectations for an even tighter labor market amid the “Great Resignation” will further enhance an incredibly robust U.S. consumer, as it should result in more wage growth. Wage growth is expected to continue, as the U.S. consumer has already accumulated a $2.2 trillion war chest of excess savings since March 2020!1 As the U.S. consumer is saving and earning more, household debt ratios are at historic lows. A strong U.S. consumer credit profile coupled with pent-up demand because of the pandemic should further support our view for solid growth and high inflation in 2022. This environment should continue to pressure risk-free rates and long-duration fixed income as market participants price in more Fed tightening in the future but recognize how easy financial conditions remain, reinvigorating the bear curve-steepening trend witnessed in the first half of 2021.

While broader credit markets took a pause in the second half of 2021 due to the rising COVID-19 variants and the Powell Pivot, we remain constructive toward credit, particularly U.S. structured credit. We are positioning for a longer-term expansion in areas of mortgage- and consumer-centric structured credit with attractive income and the potential for spread tightening and price appreciation in 2022. In addition to a brisk recovery of growth and inflation, 2021 brought a historic supply of new issuance in

1 Source: Morgan Stanley

11

the credit markets, particularly in U.S. structured credit. After issuance came to a grinding halt in 2020 due to the pandemic, the V-shaped recovery, improving consumer confidence, and growing appetite for attractive financing on the heels of post-COVID-19 accommodation sent issuance to post-GFC highs across all subsectors. Technical headwinds of heavy supply began to weigh on credit spreads in some of our more favored areas of structured credit toward the end of 2021 and into 2022 despite improving fundamentals, and we will seek to take advantage of any technical weakness into 2022.

We are also excited about growing ESG issuance in structured credit. Although COVID-19 roiled the financial markets over the course of 2020 and into the first quarter of 2021, the flow of capital into sustainable investment strategies actually accelerated over that period. This was in part driven by the focus that COVID-19 brought to social issues such as employment stability, access to healthcare, income inequality, and racial justice. While climate-related issues remain top of mind for many investors, we believe that the opportunity to support socially responsible initiatives through targeted investment strategies will be a significant driver of growth in the issuance of sustainable investment securities for the foreseeable future.

While we expect the issuance of specifically labeled ESG investment securities will continue to grow, we believe much of the opportunity to deploy the Fund’s capital into environmentally sustainable and socially responsible investments in 2022 will come from traditional structured instruments with desirable environmental and social attributes. Angel Oak’s strategies have utilized a data-driven approach to opportunistically identify RMBS, CMBS, ABS, and collateralized loan obligations (CLOs) that align with specific ESG and sustainable impact themes. The sustainable impact themes on which we focus today are broadening access to housing, expanding access to consumer credit, embedding environmental sustainability, and strengthening corporate governance.

In order to target the Fund’s corporate credit allocation, Angel Oak Capital Advisors, LLC (the “Adviser” or “Angel Oak”) utilizes proprietary scorecard-based methodologies to identify investment securities issued by companies with positive social or environmental impacts and strong governance factors. Scores are developed from publicly available data sources as well as active engagement with issuers. These engagement activities are designed to enable Angel Oak to work collaboratively with senior management to establish concrete objectives to improve the social and environmental impact of the applicable issuer’s business model.

The Fund currently focuses on two segments of the corporate credit markets when deploying capital into sustainable impact themes that Angel Oak believes have positive aggregate ESG outcomes.

| | • | | Financial institutions such as community banks and insurance companies that have been identified using Angel Oak’s proprietary scorecard methodology as Responsible Financial Institutions (RFIs) that rate highly on environmental, social, and governance factors. |

| | • | | Issuers of high-yield debt securities across a broad range of industries that have positive ESG factors or that have implemented best-in-class strategies to transition away from carbon-intensive processes toward more sustainable business models. |

Past performance is not a guarantee of future results.

Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower rated and non-rated securities present a greater risk of loss to principal and interest than higher rated securities. Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware of including credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Derivatives involve risks different from, and in certain cases, greater than the risks presented by more traditional investments. Derivatives may involve certain costs and risks such as illiquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. The Fund may use leverage, which may exaggerate the effect of any increase or decrease in the value of securities in the Fund’s portfolio or higher and duplicative expenses when it invests in mutual funds, ETFs, and other investment companies. For more information on these risks and other risks of the Fund, please see the Prospectus.

ESG investment strategies limit the universe of investment opportunities available to any Fund and will affect a Fund’s exposure to certain issuers, sectors, regions, and types of investments, which may result in a Fund forgoing opportunities to buy or sell certain securities when it might otherwise be advantageous to do so. Adhering to a Fund’s ESG investment strategy may also affect the Fund’s performance relative to similar funds that do not seek to invest in companies based on their ESG impact. Securities of issuers that the Adviser has identified as having favorable ESG characteristics may shift into and out of favor depending on market and economic conditions, and certain investments may be dependent on U.S. and foreign government policies, including tax incentives and subsidies, which may change without notice. ESG determinations are inherently subjective and investors’ views may differ as to what constitutes a positive or negative aggregate ESG impact outcome. There is no guarantee that the Adviser’s views, security selection criteria, or investment judgment will reflect the beliefs or values of any particular investor. In addition, there can be no assurance that issuers in which any Fund invests will be successful in their efforts to offer solutions that generate a positive ESG impact. When assessing whether an issuer meets any related Fund’s investment strategy and criteria, the Adviser may rely on third-party data that it believes to be reliable, but it does not guarantee the accuracy of such third-party data.

Definitions:

Spread: The difference in yield between two bonds of similar maturity but different credit quality.

Current Income: Represents return from interest and amortized/accrued cost basis.

Bloomberg U.S. Aggregate Bond Index: An unmanaged index that measures the performance of the investment-grade universe of bonds issued in the United States. The index includes institutionally traded U.S. Treasury, government-sponsored, mortgage, and corporate securities. It is not possible to invest directly in an index.

Duration: Measures a portfolio’s sensitivity to changes in interest rates. Generally, the longer the duration, the greater the price change relative to interest rate movements.

Powell Pivot: A change in policy announced by U.S. Federal Reserve Bank chairman Jerome Powell in November 2021 signaling that inflation has become a permanent, rather than transitory, aspect of the economy.

Tranche: A portion of debt or structured financing. Each portion, or tranche, is one of several related securities offered at the same time but with different risks, rewards, and maturities.

12

Investment Results – (Unaudited)

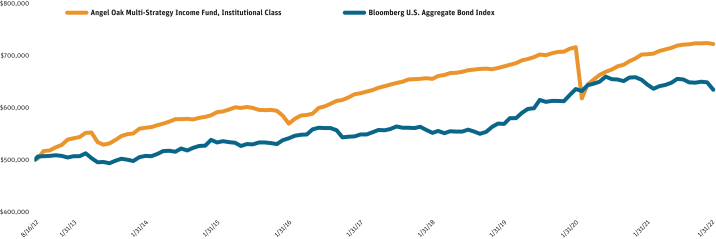

Angel Oak Multi-Strategy Income Fund

Total Return Based on a $500,000 Investment

The Fund is the successor to the investment performance of the Angel Oak Multi-Strategy Income Fund (the “Predecessor Multi-Strategy Income Fund”) as a result of the reorganization of the Predecessor Multi-Strategy Income Fund into the Fund on April 10, 2015. Accordingly, the performance information shown in the chart above and table below for periods prior to April 10, 2015 is that of the Predecessor Multi-Strategy Income Fund. The Predecessor Multi-Strategy Income Fund was also advised by the Fund’s investment adviser, Angel Oak Capital Advisors, LLC (the “Adviser”), and had the same investment objective, policies, and strategies as the Fund.

The chart above assumes an initial investment of $500,000 made on August 16, 2012 (commencement of operations). Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees or expenses. It is not possible to invest directly in an index.

Total Returns(1)

(For the year ended January 31, 2022)

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Returns | |

| | | One Year | | | Three Year | | | Five Year | | | Ten Year | | | Since Inception(2) | |

Angel Oak Multi-Strategy Income Fund, Institutional Class | | | 2.87 | % | | | 2.20 | % | | | 2.90 | % | | | N/A | | | | 3.96 | % |

Angel Oak Multi-Strategy Income Fund, Class A without load | | | 2.71 | % | | | 1.97 | % | | | 2.66 | % | | | 4.85 | % | | | 5.42 | % |

Angel Oak Multi-Strategy Income Fund, Class A with load | | | 0.40 | % | | | 1.21 | % | | | 2.19 | % | | | 4.61 | % | | | 5.19 | % |

Angel Oak Multi-Strategy Income Fund, Class C without load | | | 1.78 | % | | | 1.18 | % | | | 1.89 | % | | | N/A | | | | 1.83 | % |

Angel Oak Multi-Strategy Income Fund, Class C with load | | | 0.80 | % | | | 1.18 | % | | | 1.89 | % | | | N/A | | | | 1.83 | % |

Bloomberg U.S. Aggregate Bond Index(3) | | | (2.97 | %) | | | 3.67 | % | | | 3.08 | % | | | 2.59 | % | | | 2.55 | %(4) |

(1) Return figures reflect any change in price per share and assume the reinvestment of all distributions. Total returns for Class A Shares, with load, include the maximum 2.25% sales charge. Total returns for Class C Shares, with load, include the maximum 1.00% deferred sales charge.

(2) Inception date is August 16, 2012 for Institutional Class Shares, June 28, 2011 for Class A Shares, and August 4, 2015 for Class C Shares.

(3) The Bloomberg U.S. Aggregate Bond Index (formerly Bloomberg Barclays U.S. Aggregate Bond Index) measures the performance of the investment-grade, fixed-rate bond market, including government and credit securities, agency pass-through securities, asset-backed securities and commercial mortgage-backed securities. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. You cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

13

Investment Results – (Unaudited) (continued)

(4) The return shown for the Bloomberg U.S. Aggregate Bond Index is from the inception date of the Institutional Class Shares. The Bloomberg U.S. Aggregate Bond Index return from the inception date of Class A Shares is 2.97% and for Class C Shares is 2.81%.

14

Investment Results – (Unaudited) (continued)

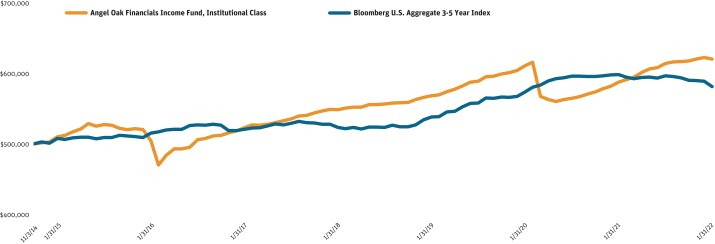

Angel Oak Financials Income Fund

Total Return Based on a $500,000 Investment

The chart above assumes an initial investment of $500,000 made on November 3, 2014 (commencement of operations). Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees or expenses. It is not possible to invest directly in an index.

Total Returns(1)

(For the year ended January 31, 2022)

| | | | | | | | | | | | | | | | |

| | | Average Annual Returns | |

| | | One Year | | | Three Year | | | Five Year | | | Since Inception(2) | |

Angel Oak Financials Income Fund, Institutional Class | | | 5.64 | % | | | 3.00 | % | | | 3.52 | % | | | 3.05 | % |

Angel Oak Financials Income Fund, Class A without load | | | 5.48 | % | | | 2.78 | % | | | 3.28 | % | | | 2.82 | % |

Angel Oak Financials Income Fund, Class A with load | | | 3.14 | % | | | 2.02 | % | | | 2.80 | % | | | 2.49 | % |

Angel Oak Financials Income Fund, Class C without load | | | 4.63 | % | | | 2.02 | % | | | 2.51 | % | | | 1.55 | % |

Angel Oak Financials Income Fund, Class C with load | | | 3.63 | % | | | 2.02 | % | | | 2.51 | % | | | 1.55 | % |

Bloomberg U.S. Aggregate 3-5 Year Index(3) | | | (2.82 | %) | | | 2.64 | % | | | 2.26 | % | | | 2.12 | %(4) |

(1) Return figures reflect any change in price per share and assume the reinvestment of all distributions. Total returns for Class A Shares, with load, include the maximum 2.25% sales charge. Total returns for Class C Shares, with load, include the maximum 1.00% deferred sales charge.

(2) Inception date is November 3, 2014 for Institutional Class and Class A Shares and August 4, 2015 for Class C Shares.

(3) The Bloomberg U.S. Aggregate 3-5 Year Index (formerly Bloomberg Barclays U.S. Aggregate 3-5 Year Index) tracks bonds with 3-5 year maturities within the Bloomberg U.S. Aggregate Bond Index. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. You cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

(4) The return shown for the Bloomberg U.S. Aggregate 3-5 Year Index is from the inception date of the Institutional Class and Class A Shares. The Bloomberg U.S. Aggregate 3-5 Year Index return from the inception date of the Class C Shares is 2.11%.

15

Investment Results – (Unaudited) (continued)

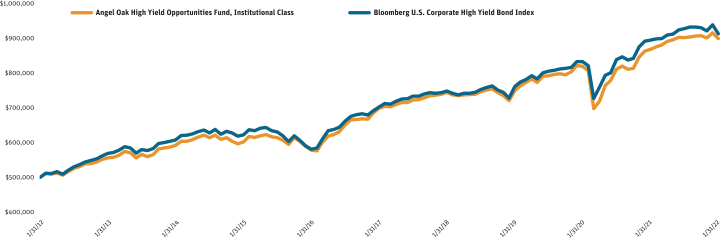

Angel Oak High Yield Opportunities Fund

Total Return Based on a $500,000 Investment

The Fund is the successor to the investment performance of the Rainier High Yield Fund (the “Predecessor High Yield Fund”) as a result of the reorganization of the Predecessor High Yield Fund into the Fund on April 15, 2016. Accordingly, the performance information shown in the chart above and table below for periods prior to April 15, 2016 is that of the Predecessor High Yield Fund’s Institutional Shares and Original Shares for the Fund’s Institutional Class and Class A shares, respectively. The Predecessor High Yield Fund was managed by the same portfolio managers as the Fund and when the Predecessor High Yield Fund was reorganized into the Fund had substantially the same investment objectives, policies, and strategies as the Fund.

The chart above assumes an initial investment of $500,000 made on January 31, 2012. Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees or expenses. It is not possible to invest directly in an index.

Total Returns(1)

(For the year ended January 31, 2022)

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Returns | |

| | | One Year | | | Three Year | | | Five Year | | | Ten Year | | | Since Inception(2) | |

Angel Oak High Yield Opportunities Fund, Institutional Class | | | 3.62 | % | | | 6.26 | % | | | 5.19 | % | | | 6.05 | % | | | 8.29 | % |

Angel Oak High Yield Opportunities Fund, Class A without load | | | 3.34 | % | | | 6.01 | % | | | 4.93 | % | | | N/A | | | | 5.55 | % |

Angel Oak High Yield Opportunities Fund, Class A with load | | | 1.03 | % | | | 5.21 | % | | | 4.46 | % | | | N/A | | | | 5.30 | % |

Bloomberg U.S. Corporate High Yield Bond Index(3) | | | 2.06 | % | | | 6.26 | % | | | 5.40 | % | | | 6.21 | % | | | 9.99 | %(4) |

(1) Return figures reflect any change in price per share and assume the reinvestment of all distributions. Total returns for Class A Shares, with load, include the maximum 2.25% sales charge.

(2) Inception date is March 31, 2009 for Institutional Class Shares and July 31, 2012 for Class A Shares.

(3) The Bloomberg U.S. Corporate High Yield Bond Index (formerly Bloomberg Barclays U.S. Corporate High Yield Bond Index) is an unmanaged market value-weighted index that covers the universe of fixed-rate, non-investment grade debt. The index return does not reflect expenses, which have been deducted from the Fund’s return. You cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

(4) The return shown for the Bloomberg U.S. Corporate High Yield Bond Index is from the inception date of the Institutional Class Shares. The Bloomberg U.S. Corporate High Yield Bond Index return from the inception date of Class A Shares is 5.89%.

16

Investment Results – (Unaudited) (continued)

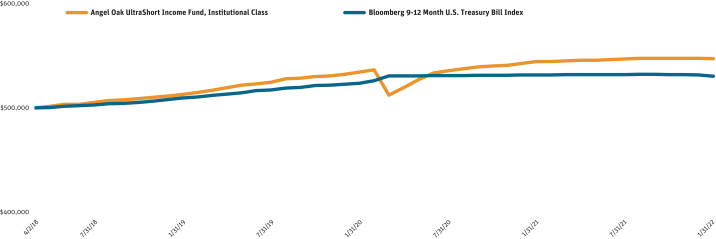

Angel Oak UltraShort Income Fund

Total Return Based on a $500,000 Investment

The chart above assumes an initial investment of $500,000 made on April 2, 2018 (commencement of operations). Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees or expenses. It is not possible to invest directly in an index.

Total Returns(1)

(For the year ended January 31, 2022)

| | | | | | | | | | | | |

| | | Average Annual Returns | |

| | | One Year | | | Three Year | | | Since Inception(2) | |

Angel Oak UltraShort Income Fund, Institutional Class | | | 0.51 | % | | | 2.17 | % | | | 2.38 | % |

Angel Oak UltraShort Income Fund, Class A | | | 0.27 | % | | | 1.89 | % | | | 2.08 | % |

Bloomberg 9-12 Month U.S. Treasury Bill Index(3) | | | (0.26 | %) | | | 1.35 | % | | | 1.54 | %(4) |

(1) Return figures reflect any change in price per share and assume the reinvestment of all distributions.

(2) Inception date is April 2, 2018 for Institutional Class and April 30, 2018 for Class A Shares.

(3) The Bloomberg 9-12 Month U.S. Treasury Bill Index (formerly Bloomberg Barclays 9-12 Month U.S. Treasury Bill Index) measures the performance of U.S. Treasury bills, notes, and bonds with a remaining maturity between 9-12 months. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. You cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

(4) The return shown for the Bloomberg 9-12 Month U.S. Treasury Bill Index is from the inception date of the Institutional Class Shares. The Bloomberg 9-12 Month U.S. Treasury Bill Index return from the inception date of the Class A Shares is 1.56%.

17

Investment Results – (Unaudited) (continued)

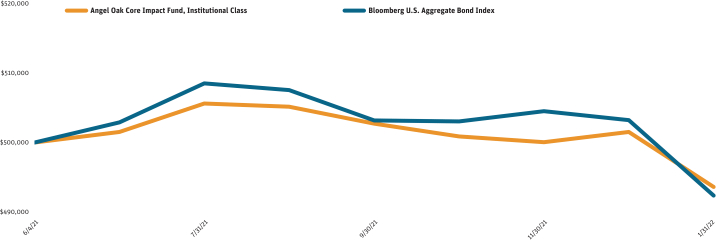

Angel Oak Core Impact Fund

Total Return Based on a $500,000 Investment

The chart above assumes an initial investment of $500,000 made on June 4, 2021 (commencement of operations). Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees or expenses. It is not possible to invest directly in an index.

Cumulative Returns(1)

(For the period ended January 31, 2022)

| | | | |

| | | Since Inception(2) | |

Angel Oak Core Impact Fund, Institutional Class | | | (1.28 | %) |

Bloomberg U.S. Aggregate Bond Index(3) | | | (1.53 | %) |

(1) Return figures reflect any change in price per share and assume the reinvestment of all distributions.

(2) Inception date is June 4, 2021.

(3) The Bloomberg U.S. Aggregate Bond Index (formerly Bloomberg Barclays U.S. Aggregate Bond Index) measures the performance of the investment-grade, fixed-rate bond market, including government and credit securities, agency pass-through securities, asset-backed securities and commercial mortgage-backed securities. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. You cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

18

Summary of Funds’ Expenses – (Unaudited)

As a shareholder of the Funds, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees and other expenses of the Funds. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period.

Actual Expenses

The first lines of the tables below provide information about actual account values and actual expenses. You may use the information in these lines, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = $8.60), then multiply the result by the numbers in the first lines under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second lines of the tables below provide information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the second lines of the tables below are useful in comparing ongoing costs only and will not help you determine the relative costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | |

| Angel Oak Multi-Strategy Income Fund | | Beginning

Account Value,

August 1, 2021 | | Ending

Account Value,

January 31, 2022 | | Expenses Paid

During Period(1) | | Annualized

Expense Ratio |

Class A | | Actual | | $1,000.00 | | $1,003.10 | | $6.61 | | 1.31% |

| | | Hypothetical(2) | | $1,000.00 | | $1,018.60 | | $6.67 | | 1.31% |

Class C | | Actual | | $1,000.00 | | $998.40 | | $10.38 | | 2.06% |

| | | Hypothetical(2) | | $1,000.00 | | $1,014.82 | | $10.46 | | 2.06% |

Institutional Class | | Actual | | $1,000.00 | | $1,003.50 | | $5.35 | | 1.06% |

| | | Hypothetical(2) | | $1,000.00 | | $1,019.86 | | $5.40 | | 1.06% |

| | | | | | | | | | |

| Angel Oak Financials Income Fund | | Beginning

Account Value,

August 1, 2021 | | Ending

Account Value,

January 31, 2022 | | Expenses Paid

During Period(1) | | Annualized

Expense Ratio |

Class A | | Actual | | $1,000.00 | | $1,010.50 | | $4.76 | | 0.94% |

| | | Hypothetical(2) | | $1,000.00 | | $1,020.47 | | $4.79 | | 0.94% |

Class C | | Actual | | $1,000.00 | | $1,005.80 | | $8.54 | | 1.69% |

| | | Hypothetical(2) | | $1,000.00 | | $1,016.69 | | $8.59 | | 1.69% |

Institutional Class | | Actual | | $1,000.00 | | $1,010.70 | | $3.50 | | 0.69% |

| | | Hypothetical(2) | | $1,000.00 | | $1,021.73 | | $3.52 | | 0.69% |

| | | | | | | | | | |

| Angel Oak High Yield Opportunities Fund | | Beginning

Account Value,

August 1, 2021 | | Ending

Account Value,

January 31, 2022 | | Expenses Paid

During Period(1) | | Annualized

Expense Ratio |

Class A | | Actual | | $1,000.00 | | $996.60 | | $4.53 | | 0.90% |