As filed with the Securities and Exchange Commission on January 30, 2015

Registration No. 333-199113

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3 TO

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Costamare Partners LP

(Exact name of Registrant as specified in its charter)

|

|

|

|

|

Republic of the Marshall Islands | 4412 | 98-1200487 |

60 Zephyrou Street & Syngrou Avenue, 17564 Athens Greece, +30-210-949-0050

(Address, including zip code, and telephone number, including area code, of Registrant’s principal

executive offices)

CT Corporation System

111 Eighth Avenue

New York, New York 10011

(212) 590-9338

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

|

|

|

|

|

William P. Rogers, Jr. | Stephen P. Farrell | Sean T. Wheeler |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.£

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.£

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.£

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.£

CALCULATION OF REGISTRATION FEE

|

|

|

|

| ||||||||||

| ||||||||||||||

Title of Each Class of | Proposed | Amount of | ||||||||||||

| ||||||||||||||

Common units representing limited partner interests |

|

| $ |

| 100,000,000 |

|

| $ |

| 12,880(3 | ) |

| ||

| ||||||||||||||

(1) | Includes common units issuable upon exercise of the underwriters’ option to purchase additional common units. | ||

(2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o). | ||

(3) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JANUARY 30, 2015

PRELIMINARY PROSPECTUS

Costamare Partners LP

Common Units

Representing Limited Partner Interests

$ per common unit

This is the initial public offering of our common units. We currently expect the initial public offering price to be between $ and $ per common unit.

We have granted the underwriters an option to purchase up to an additional common units.

Members of the Konstantakopoulos family and certain funds managed by York Capital Management Global Advisors LLC, which is the joint venture partner of Costamare Inc., or “Costamare”, for the ownership of certain vessels, have indicated that they currently intend to purchase up to an aggregate of approximately $ million and $ million, respectively, of common units in the offering at the public offering price. This represents an aggregate of approximately common units based on the midpoint of the price range set forth above. The number of common units available for sale to the general public will be reduced to the extent of these sales.

We intend to apply to list the common units on the New York Stock Exchange under the symbol “CMRP”.

We are an “emerging growth company”, and we are eligible for reduced reporting requirements. See “Summary—Implications of Being an Emerging Growth Company”.

Investing in our common units involves risks. See “Risk Factors” beginning on page 31.

These risks include the following:

• | We may not have sufficient cash from operations, following the establishment of cash reserves and payment of fees and expenses, to enable us to pay the minimum quarterly distribution on our common units and subordinated units. | ||

• | We will be required to make substantial capital expenditures to maintain the operating capacity of our fleet and acquire vessels, which may reduce or eliminate the amount of cash available for distribution. | ||

• | Our ability to acquire additional containerships from Costamare or third parties will depend upon our ability to raise additional equity and debt financing, to fund all or a portion of the acquisition costs of these vessels, and may be dependent on the consent of existing lenders to Costamare. | ||

• | Our debt levels may limit our ability to obtain additional financing, pursue other business opportunities and pay distributions to unitholders. | ||

• | We depend on Costamare and its affiliates, including Costamare Shipping Company S.A., to operate and expand our businesses and compete in our markets. | ||

• | Our future performance depends on the level of world and regional demand for chartering containerships, and a recurrence of the recent global economic slowdown may impede our ability to continue to grow our business. | ||

• | We have only four vessels in our initial fleet. Any limitation in the availability or operation of those vessels could have a material adverse effect on our business, financial condition, results of operations and cash flows, which effect would be amplified by the small size of our initial fleet. | ||

• | Unitholders have limited voting rights, and our partnership agreement restricts the voting rights of unitholders (other than our general partner and its affiliates, including Costamare) owning more than 4.9% of our common units. | ||

• | Our unitholders will not be entitled to elect our general partner or its directors, subject to our general partner’s option to cause us at some point in the future to be managed by our own board of directors and, in that connection, to cause the common unitholders to permanently have the right to elect a majority of our directors. | ||

• | Upon completion of this offering, Costamare and our general partner will own a % interest in us and will have conflicts of interest and limited fiduciary and contractual duties to us and our common unitholders, which may permit them to favor their own interests to your detriment. | ||

• | Even if public unitholders are dissatisfied, they cannot initially remove our general partner without Costamare’s consent. | ||

• | You will experience immediate and substantial dilution of $ per common unit. | ||

• | Our general partner has a limited call right that may require you to sell your common units at an undesirable time or price. | ||

• | U.S. tax authorities could treat us as a “passive foreign investment company” under certain circumstances, which would have adverse U.S. federal income tax consequences to U.S. unitholders. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

|

|

|

| ||||||||||

| Per | Total | ||||||||||||

Public Offering Price |

|

| $ |

|

|

|

| $ |

|

| ||||

Underwriting Discount(1) |

|

| $ |

|

| $ | ||||||||

Proceeds, before expenses, to Costamare Partners LP(1)(2) |

|

| $ |

|

| $ | ||||||||

(1) | Excludes an aggregate structuring fee of % of the offering proceeds before discounts and expenses, payable to Morgan Stanley & Co. LLC, Barclays Capital Inc. and Citigroup Global Markets Inc. We will also pay up to $25,000 of reasonable fees and expenses of counsel related to the review by the Financial Industry Regulatory Authority, Inc. of the terms of sale of the common units offered hereby. See “Underwriting”. | ||

(2) | Excludes offering expenses payable by us as described in “Expenses Related to This Offering”. |

The underwriters expect to deliver the common units to purchasers on or about , 2015 through the book-entry facilities of The Depository Trust Company.

|

|

|

|

|

|

|

Morgan Stanley | Barclays | Citigroup | Wells Fargo Securities | |||

Credit Suisse | J.P. Morgan | |||||

, 2015

|

|

|

|

|

|

|

| |

|

|

|

|

|

We are responsible for the information contained in this prospectus and in any free writing prospectus we prepare or authorize. We have not authorized anyone to provide you with different information, and we take no responsibility for any other information others may give you. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date of this prospectus.

TABLE OF CONTENTS

i

|

|

| |||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 110 | ||||||

110 | |||||||

115 | |||||||

117 | |||||||

118 | |||||||

121 | |||||||

123 | |||||||

123 | |||||||

123 | |||||||

127 | |||||||

127 | |||||||

130 | |||||||

131 | |||||||

131 | |||||||

131 | |||||||

135 | |||||||

135 | |||||||

137 | |||||||

155 | |||||||

155 | |||||||

155 | |||||||

156 | |||||||

157 | |||||||

159 | |||||||

161 | |||||||

164 | |||||||

166 | |||||||

170 | |||||||

171 | |||||||

172 | |||||||

178 | |||||||

178 | |||||||

179 | |||||||

179 | |||||||

184 | |||||||

184 | |||||||

186 | |||||||

188 | |||||||

188 | |||||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 189 | ||||||

190 | |||||||

Distributions and Payments to our General Partner and its Affiliates | 190 | ||||||

190 | |||||||

190 | |||||||

191 | |||||||

192 | |||||||

202 | |||||||

202 | |||||||

202 | |||||||

203 | |||||||

205 | |||||||

205 | |||||||

213 | |||||||

ii

|

|

| |||||

213 | |||||||

213 | |||||||

214 | |||||||

214 | |||||||

214 | |||||||

214 | |||||||

214 | |||||||

215 | |||||||

216 | |||||||

217 | |||||||

218 | |||||||

218 | |||||||

218 | |||||||

220 | |||||||

221 | |||||||

221 | |||||||

221 | |||||||

223 | |||||||

223 | |||||||

223 | |||||||

223 | |||||||

224 | |||||||

Our General Partner’s Option to Create a Partnership Board of Directors | 224 | ||||||

225 | |||||||

225 | |||||||

225 | |||||||

226 | |||||||

226 | |||||||

226 | |||||||

227 | |||||||

228 | |||||||

229 | |||||||

229 | |||||||

229 | |||||||

234 | |||||||

234 | |||||||

235 | |||||||

235 | |||||||

236 | |||||||

244 | |||||||

244 | |||||||

244 | |||||||

245 | |||||||

245 | |||||||

246 | |||||||

| 247 | ||||||

|

| A-i | |||||

iii

This summary highlights information contained elsewhere in this prospectus. Unless we otherwise specify, all references to information and data in this prospectus about our business and fleet refer to our business and fleet to be contributed to the Partnership upon the closing of this offering. Prior to the closing of this offering, the Partnership will not own any vessels. You should read the entire prospectus carefully, including the historical financial statements of Costamare Partners LP Predecessor, which includes the subsidiaries of Costamare Inc. that own the vessels in our initial fleet, and the notes to those financial statements. The information presented in this prospectus assumes, unless otherwise noted, (1) an initial public offering price of $ per common unit (the midpoint of the price range set forth on the cover of this prospectus) and (2) that the underwriters do not exercise their option to purchase additional common units. You should read “Risk Factors” for more information about important risks that you should consider carefully before buying our common units. Unless otherwise indicated, all references to “dollars” and “$” in this prospectus are to, and amounts are presented in, U.S. dollars.

References in this prospectus to “Costamare Partners”, “we”, “our”, “us” and “the Partnership” or similar terms when used in a historical context refer to Capetanissa Maritime Corporation, Jodie Shipping Co., Kayley Shipping Co. and Raymond Shipping Co., the subsidiaries of Costamare Inc. that hold interests in the vessels in our initial fleet. When used in the present tense or prospectively, those terms refer to Costamare Partners LP or any one or more of its subsidiaries, or to all such entities unless the context otherwise indicates. Please read “—Summary Financial, Operating and Pro Forma Data” beginning on page 26 for an overview of our predecessor’s operating results and financial position.

References in this prospectus to “our general partner” refer to Costamare Partners GP LLC, the general partner of Costamare Partners. References in this prospectus to “Costamare” refer, depending on the context, to Costamare Inc. and to any one or more of its direct and indirect subsidiaries, including Croy Holdings Inc., other than us. References in this prospectus to “Costamare Shipping” refer to Costamare Shipping Company S.A., an affiliate of Costamare controlled by Costamare’s chairman and chief executive officer. References in this prospectus to “Shanghai Costamare” refer to Shanghai Costamare Ship Management Co., Ltd., a Chinese corporation affiliated with Costamare Inc. References in this prospectus to “York” refer to York Capital Management Global Advisors LLC, Sparrow Holdings L.P., Bluebird Holdings L.P. and certain affiliated funds on whose behalf York Capital Management Global Advisors LLC has entered into the Framework Agreement (as defined herein) and the omnibus agreement (as discussed elsewhere in this prospectus), as the context may require. References in this prospectus to the “Framework Agreement” refer to the Framework Deed between Costamare Inc. and its wholly- owned subsidiary, Costamare Ventures Inc., on the one hand, and York and its affiliated fund, Sparrow Holdings, L.P., on the other, as amended from time to time, pursuant to which Costamare and York agreed to jointly invest in newbuild and secondhand container vessels through jointly held companies in which Costamare holds a 25% to 75% interest (any such entity, referred to as a “JV Entity”, and any such jointly owned or acquired vessel, referred to as a “JV vessel”). References in this prospectus to “V.Ships Greece” refer to V.Ships Greece Ltd. We use the term “twenty foot equivalent unit”, or “TEU”, the international standard measure of containers, in describing the capacity of our containerships.

We are a growth-oriented limited partnership formed to own, operate and acquire containerships under long-term, fixed-rate charters, which we define as charters of five full years or more. As of December 31, 2014, our initial fleet of four containerships had an average capacity of approximately 9,000 TEU and an average remaining charter term (weighted by TEU capacity) of approximately 6.2 years, with charter terms expiring between April 2018 and February 2023. These four vessels will be contributed to us by Costamare, one of the largest publicly listed containership owners by TEU capacity, which will control us through its ownership of our general partner. We believe that Costamare intends to utilize us as its primary growth vehicle to pursue the acquisition

1

of containerships that are expected to generate long-term, predictable cash flows, although there is no guarantee that we will be able to take advantage of opportunities to grow or generate the desired cash flows, nor is there any guarantee that Costamare will utilize us in this manner.

We are an owner of containerships and we generate our revenues by chartering them to leading liner companies pursuant to long-term, fixed-rate charters. Under the terms of these charters, we provide crewing and technical management, while the charterer is generally responsible for securing cargos, fuel costs and voyage expenses. Our charters provide for a fixed hire rate over the life of the charter, regardless of the utilization of the vessel. We intend to focus primarily on large modern vessels because we believe that the economies of scale and fuel savings of newly designed vessels are most appealing to our customers, the major liner companies. We believe our focus on owning modern, high quality containerships, chartered under long-term contracts with staggered maturities, will provide stability and predictability to our revenues and cash flows and minimize re-chartering risk. In addition, we are focused on providing charters to a diversified group of leading liner companies, which we believe will minimize our counterparty risk. Though there is no guarantee that we will be able to take advantage of opportunities to grow or generate the desired cash flows, we believe that our strategy will ensure the long-term stability of our distributions.

Upon the closing of this offering, we will own four containerships, of which three were built in 2013 and one in 2006. These containerships operate under long-term charters with Mediterranean Shipping Company, S.A., or “MSC”, affiliates of the Evergreen Marine Corporation Taiwan Ltd., or “Evergreen”, and Cosco Container Lines Co., Ltd., or “COSCO”. We will also have options to acquire an additional ten identified vessels and certain other rights under which we may acquire additional containerships with long-term charters from Costamare and, with respect to the JV vessels, York as described below. We believe that such options and rights will provide us with significant built-in growth opportunities. We may also grow through further acquisitions of containerships, not only from Costamare and York, but also from liner companies, shipyards and other shipowners. We believe that executing our growth strategy, while providing reliable service to our customers, will enable us to grow our distributions per unit. However, we cannot assure you that we will make any particular acquisition or that as a consequence we will successfully grow the amount of our per unit distributions. Among other things, our ability to acquire additional containerships will be dependent upon our ability to raise additional equity and debt financing.

Upon the closing of this offering, our initial fleet will consist of the following four vessels. As of December 31, 2014, these four vessels had an average age (weighted by TEU capacity) of approximately 3.5 years and an average remaining charter term (weighted by TEU capacity) of approximately 6.2 years:

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Vessel Name | Charterer | Year Built | Capacity | Daily Charter Rate | Expiration of | ||||||||||||||||||||

MSC ATHOS | MSC |

|

| 2013 |

|

| 8,827 |

|

| 42,000 | February 2023 | ||||||||||||||

MSC ATHENS | MSC |

|

| 2013 |

|

| 8,827 |

|

| 42,000 | January 2023 | ||||||||||||||

VALUE | Evergreen |

|

| 2013 |

|

| 8,827 |

|

| 41,700 | April 2020(2) | ||||||||||||||

COSCO BEIJING | COSCO |

|

| 2006 |

|

| 9,469 |

|

| 36,400 | April 2018 | ||||||||||||||

(1) | Charter terms and expiration dates are based on the earliest scheduled date charters could expire. Amounts set out for daily charter rate are the amounts contained in the charter contracts. | ||

(2) | Assumes exercise of owner’s unilateral options to extend the charter of this vessel for two one-year periods at the same charter rate. The charterer also has corresponding options to unilaterally extend the charter for the same periods at the same charter rate. |

2

We will have the option to purchase from Costamare theValence(and shares in the vessel-owning entity) within 12 months following the closing of this offering at fair market value as determined in accordance with the omnibus agreement, provided that Costamare may, at its option, replace the Valence with any of the three vessels that are sister ships to theValence with the same specifications, including TEU capacity, which vessels were delivered in 2013 and are chartered to the same charterer, Evergreen, subject to the same daily charter rate and charter length as those applicable to the Valence(each such sister ship is hereinafter referred to as the “substitute vessel”). In addition, Costamare and York have a 36-month period after each such vessel’s acceptance by its charterer, in which they may offer us the right to purchase nine additional JV vessels (and shares in the vessel-owning entities) that Costamare and York jointly own, in each case at fair market value as determined in accordance with the omnibus agreement. Within 30 days of receiving such notice, our general partner must make an election on whether to purchase the relevant vessel. If Costamare and York do not reach an agreement to offer us such right during the 36-month period, we will have the right to purchase such vessels at the end of such 36-month period, provided that, at the end of the 36-month period, the relevant vessel is subject to a charter with a remaining term of five full years or more.

As of the date of this prospectus, we have not secured any financing in connection with the ten option vessels. Our ability to purchase these ten option vessels, should we exercise our right to purchase such vessels, is dependent on our ability to obtain financing to fund all or a portion of the acquisition costs and may be dependent on the consent of existing lenders to Costamare and, as applicable, York with respect to these option vessels, as we may seek to transfer existing financing arrangements, including any financing leases, in connection with an acquisition. There are no assurances that we will purchase any of the option vessels. See “Risk Factors—Risk Inherent in Our Business—We may have difficulty obtaining consents that are necessary to acquire vessels with an existing charter or financing agreement”.

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Vessel Name | Charterer | Date of Delivery(1) | Capacity (TEU) | Daily Charter Rate | Expiration of | |||||||||||||||

S2125* | Evergreen | Q3 2016 |

|

| 14,354 |

|

| 46,700 | 2026(2) | |||||||||||

S2124* | Evergreen | Q3 2016 |

|

| 14,354 |

|

| 46,700 | 2026(2) | |||||||||||

S2123* | Evergreen | Q3 2016 |

|

| 14,354 |

|

| 46,700 | 2026(2) | |||||||||||

S2122* | Evergreen | Q2 2016 |

|

| 14,354 |

|

| 46,700 | 2026(2) | |||||||||||

S2121* | Evergreen | Q2 2016 |

|

| 14,354 |

|

| 46,700 | 2026(2) | |||||||||||

VALENCE** | Evergreen | 2013 |

|

| 8,827 |

|

| 41,700 | July 2020(3) | |||||||||||

Not currently chartered |

|

|

|

|

|

|

|

|

|

| ||||||||||

NCP0116* | — | Q2 2016 |

|

| 11,000 |

|

| — | — | |||||||||||

NCP0115* | — | Q2 2016 |

|

| 11,000 |

|

| — | — | |||||||||||

NCP0114* | — | Q1 2016 |

|

| 11,000 |

|

| — | — | |||||||||||

NCP0113* | — | Q4 2015 |

|

| 11,000 |

|

| — | — | |||||||||||

(1) | For newbuilds, expected delivery quarters are presented. | ||

(2) | Assumes exercise of owner’s unilateral options to extend the charter of this vessel for one three-year period and an additional one two-year period at the same charter rate. The charterer also has unilateral options to extend the charter for one three-year period and one two-year period, which correspond to owner’s extension option periods, and an additional two-year period, in each case at the same charter rate. | ||

(3) | Assumes exercise of owner’s unilateral options to extend the charter of this vessel for two one-year periods at the same charter rate. The charterer also has corresponding options to unilaterally extend the charter for the same periods at the same charter rate. | ||

* | Denotes vessels acquired by the JV Entities pursuant to the Framework Agreement with York. |

3

** | Costamare may, at its option, replace theValence with any of its three substitute vessels. The charters for the three substitute vessels expire in April 2020, June 2020 and September 2020, assuming the exercise of owner’s unilateral options to extend the charter of each such vessels for two one-year periods at the same charter rate. The charterer also has corresponding options to unilaterally extend the charter for the same periods at the same charter rate. |

In addition to the initial fleet and the option vessels described above, we intend to leverage our relationship with Costamare to make additional accretive acquisitions of containerships with long-term charters. Upon the earliest date on which the purchase options are no longer exercisable, either as a result of the expiration of the last of the option periods described above (which may be as late as 2019 based on the expected delivery schedule) or our having made elections with respect to such options (the “Non-Compete Commencement Date”), the following non-competition provisions of the omnibus agreement will become applicable to Costamare, the JV Entities, York and us. Following the Non-Compete Commencement Date, Costamare and, as applicable, York have agreed to offer us the right to purchase any other containerships (and shares in the vessel-owning entities), including the JV vessels, with the following characteristics:

• | vessel is less than seven years old with a carrying capacity of greater than 8,000 TEU; and | ||

• | charters are secured with committed terms of five full years or more, which for existing charters shall mean charters with a remaining term of five full years or more. |

We refer to any such vessel (and shares in the vessel-owning entities) as a “non-compete vessel”. Costamare and, with respect to any JV vessel, the JV Entities and York have agreed to offer us the right to purchase such non-compete vessel at fair market value as determined in accordance with the omnibus agreement.

In the case of any vessel that constitutes a non-compete vessel as of the Non-Compete Commencement Date, Costamare and, with respect to any JV vessels, the applicable JV Entity and York, have agreed to notify our general partner and offer us, within 36 months following the Non-Compete Commencement Date or, if later, the date of delivery to and acceptance by the charterer, the right to purchase such vessel.

For all vessels that become non-compete vessels after the Non-Compete Commencement Date, Costamare and, with respect to any JV vessels, the applicable JV Entity and York, have agreed to notify our general partner and offer us the right to purchase such non-compete vessels within (1) 36 months after the delivery to and acceptance by the charterer in the case of any newbuild non-compete vessels or (2) 24 months after the consummation of the acquisition or the commencement of operations or charter in the case of any secondhand non-compete vessels.

Costamare and, with respect to any JV vessel, the applicable JV Entity and York will be subject to the requirements described above to provide notice and offer for purchase any non-compete vessel (whether the relevant vessel constitutes a non-compete vessel as of the Non-Compete Commencement Date or becomes a non-compete vessel after the Non-Compete Commencement Date) only if, at the time of such notice and offer, the relevant vessel constitutes a non-compete vessel. If at the end of any such 36-month period or 24-month period, as applicable, the relevant vessel constitutes a non- compete vessel, and Costamare and York have not previously notified and offered us the right to purchase such vessel, we will have the right to do so at the end of such 36-month period or 24-month period, as applicable. Under these provisions, if a vessel ceases to be a non-compete vessel before they are offered to us, that vessel will cease to be subject to these non-competition provisions.

Except as discussed elsewhere in this prospectus, this right to purchase non-compete vessels pursuant to the omnibus agreement will run from the Non-Compete Commencement Date through the entire term of the omnibus agreement. In addition, starting from the closing of this offering, we will have a right of first offer with regard to any proposed sale, transfer or other disposition of any

4

non-compete vessels that Costamare wholly or jointly with York owns, as discussed elsewhere in this prospectus.

Our ability to acquire additional containerships, including option vessels and non-compete vessels, from Costamare and, as applicable, a JV Entity and York is subject to obtaining any applicable consents of governmental authorities and other non-affiliated third parties, including the relevant lenders and charterers. Under the omnibus agreement, Costamare and, as applicable, a JV Entity and York will be obligated to use commercially reasonable efforts to obtain any such consents and to indemnify us if such consents are not obtained. The fair market value to be paid for such vessels and other terms of the purchase will be subject to approval by the conflicts committee of the board of directors of the general partner. Our ability to exercise any right to acquire additional containerships will also be subject to our ability to obtain additional equity and debt financing. We cannot assure you that in any particular case the necessary consent will be obtained. See “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Omnibus Agreement”.

As of December 31, 2014, Costamare had a fleet of 68 containerships with a total capacity of approximately 447,000 TEU, including nine newbuilds on order, making it one of the largest public containership companies in the world, based on total TEU capacity. Costamare is controlled by members of the Konstantakopoulos family, which has a long history of operating and investing in the international shipping industry, including a long history of vessel ownership.

Costamare Inc. was incorporated in the Republic of The Marshall Islands on April 21, 2008, under the Marshall Islands Business Corporations Act, for the purpose of completing a reorganization of 53 ship-owning companies then owned by our general partner���s chief executive officer and other members of the Konstantakopoulos family under a single corporate holding company. Costamare initially owned and operated drybulk carrier vessels, but in 1984 became the first Greek-owned company to enter the containership market, and, since 1992, it has focused exclusively on containerships. In November 2010, Costamare completed an initial public offering of its common stock in the United States, and its common stock began trading on the New York Stock Exchange under the ticker symbol “CMRE”.

In May 2013, Costamare entered into the Framework Agreement with York, a New York-based investment management firm, to jointly invest in equity for the acquisition of newbuild and secondhand container vessels. The Framework Agreement, which was amended and restated on October 1, 2014, is expected to be each party’s exclusive joint venture for the acquisition of vessels in the containership industry during the commitment period ending May 15, 2020 (unless terminated earlier in certain circumstances). As of December 31, 2014, the joint venture had executed transactions with capital expenditure commitments of approximately $979.8 million. As of the same date, Costamare and York had made equity payments of $231.3 million, which was subsequently decreased to $154.9 million, based on debt financing arrangements. As part of the Framework Agreement, Costamare holds a minority stake in the existing JV vessels and expects to hold a stake of 25% to 75% in future JV vessels. Nine of our option vessels are JV vessels.

Our Relationship with Costamare Inc.

We believe that one of our principal strengths is our relationship with Costamare and its affiliates. We believe our relationship with Costamare will give us access to its relationships with leading liner companies, shipbuilders, financing sources and suppliers and to its technical, commercial and managerial expertise, which we believe will allow us to compete more effectively when seeking additional customers and expanding our fleet. As of December 31, 2014, Costamare’s fleet consisted of (i) 59 vessels in the water, aggregating approximately 332,000 TEU and (ii) nine newbuild vessels aggregating in excess of 115,000 TEU that are scheduled to be delivered through third quarter 2016, based on the current shipyard schedule. As of December 31, 2014, 13 of Costamare’s containerships,

5

including nine newbuilds, had been acquired pursuant to the Framework Agreement with York by vessel-owning joint venture entities in which Costamare holds a minority equity interest.

The vessels in our initial fleet will be managed by Costamare’s affiliated manager, Costamare Shipping, which is controlled by Costamare’s chairman and chief executive officer, unless Costamare Shipping decides to delegate certain of its management services to an affiliated manager (such as Shanghai Costamare), V.Ships Greece or, subject to our consent, other third party managers. Costamare Shipping will also provide certain administrative and commercial management services to the Partnership. Costamare Shipping is a global operator that has successfully managed Costamare’s growing and diverse fleet for the past 41 years. Costamare Shipping utilizes both affiliated and unaffiliated managers for the technical management of vessels, which provides scale and flexibility to its operations. We believe that Costamare Shipping provides superior management services based on its market-specific experience and relationships, and we expect to rely on substantially the same management platform to manage our growing fleet. On January 7, 2013, Costamare Shipping entered into a Co-operation Agreement, or the “Co-operation Agreement”, with V.Ships Greece, a member of V.Group, to establish a ship management cell that, subject to limited exceptions, serves as the exclusive third-party manager of Costamare Shipping.

Upon completion of this offering, Costamare will own our 2.0% general partner interest, all of our incentive distribution rights and a % limited partner interest in us, which consists of common units and all of our subordinated units. As a result, Costamare will hold a majority of our total equity interests. Our general partner will manage our operations and day-to-day activities and Costamare will appoint all of the directors of the board of our general partner.

We believe there are a number of market factors that create a favorable backdrop for a growth oriented containership company:

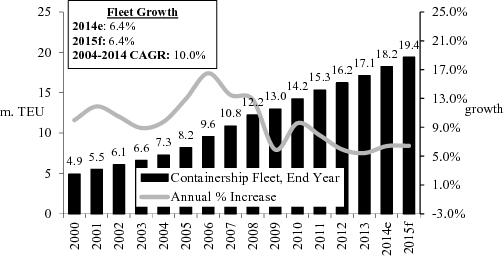

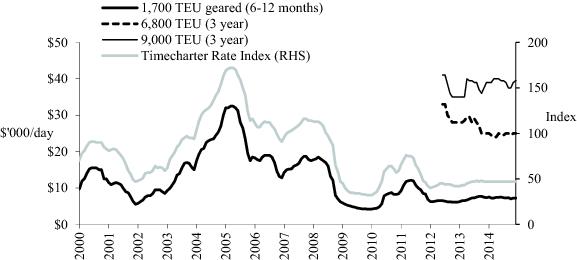

• | Growing demand for large, modern containerships provided by well-capitalized owners.As reported by Clarkson Research Services Limited, or “Clarkson Research”, due to a combination of high bunker prices and low freight rates in the container shipping market since 2009, liner companies are increasingly relying on large, modern containerships with high TEU capacity and fuel efficiency features, which minimize average operating expenses per TEU of capacity. According to Clarkson Research, this focus on maximizing economies of scale has been accompanied by a compound annual growth rate, or “CAGR”, of 23.7% in total capacity of containerships 8,000 TEU or larger over the last five years, compared to a CAGR of just 1.5% for containerships smaller than 8,000 TEU in size during the same period. On a year-on-year basis, the total capacity of containerships 8,000 TEU or larger grew by 20.8% in 2014, 19.2% in 2013, 23.2% in 2012, 26.4% in 2011, 29.1% in 2010 and 17.3% in 2009. This is compared to year-on-year contraction in the total capacity of containerships smaller than 8,000 TEU by 0.6% in 2014 and by 0.2% in 2013, and growth of just 0.2% in 2012, 2.9% in 2011, 5.3% in 2010 and 3.7% in 2009. Furthermore, Clarkson Research reported that recently built vessels with fuel efficiency features or environmental compliance features can achieve significant premium in the charter market. These large, modern containerships are capital intensive assets, and liner companies have traditionally relied on well-capitalized containership owners such as us to help manage their balance sheets. As the global economy continues to strengthen and liner companies continue to balance their capital expenditures and debt capacity with their requirement for larger vessels, we believe they will continue to rely on shipowners like us who can provide them with large vessels with minimal upfront capital outlay. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

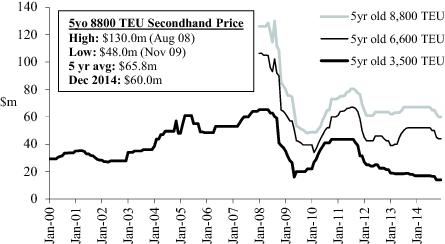

• | Availability of attractive acquisition opportunities in the container shipping industry. Shipbuilding prices for new containerships and prices for secondhand vessels have been, and remain, near historically low levels since the recent economic downturn. As reported by Clarkson Research, benchmark prices for 6,600 TEU new containerships and 8,800 TEU secondhand five-year-old vessels in December 2014 were approximately 37% and 54%, | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

6

| respectively, below their peaks in 2008. The competition for these acquisition opportunities has changed as several historical lenders to shipping companies have tightened lending criteria and either stopped or severely reduced lending to shipping companies. In addition, certain German shipping funds that have historically contracted for nearly half of the containerships ordered between 1999 and 2008 have faced significant financial challenges and, as a result, their share of containership orders in 2014 fell to 19%. Furthermore, we believe liner companies typically prefer to charter from shipowners such as Costamare, who have demonstrated the financial wherewithal to acquire and offer them several vessels in a single transaction. We believe that our moderate leverage profile will position us well to obtain financing to allow us to exploit attractive growth opportunities and enhance our ability to earn an attractive yield on our vessels. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

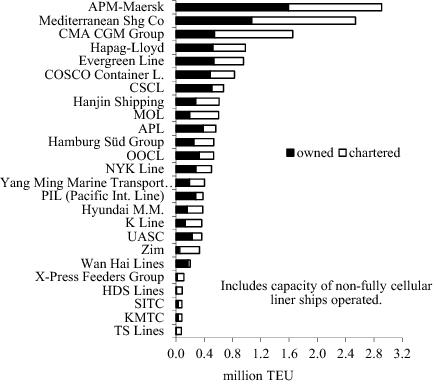

• | Containership owners play a significant role in containership trade. Historically, a significant share of the global containership fleet by TEU capacity was owned by the liner companies. Since the 1990s, however, liner companies have increasingly chartered in a larger proportion of the capacity that they operate. Based on Clarkson Research information, the portion of liner companies’ fully cellular containership capacity, meaning that the vessel is a dedicated container vessel, that is supplied by independent charter owners has grown from 29% at the start of 1996 to 47.3% in January 2015. As one of the largest publicly traded containership owners, Costamare has informed us that it expects to participate directly in the continued growth and recovery of the global containership trade. In turn, we believe this will provide us with increased opportunities to grow our fleet and distributable cash flow. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

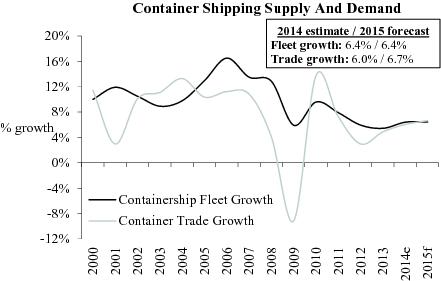

• | Global containership trade continues to grow.As reported by Clarkson Research, global container trade grew by 4.0% in 2008, contracted by 9.2% in 2009, rebounded by 13.8% in 2010 and, between 2010 and 2013, grew by a CAGR of 5.0% per annum, and is estimated to have grown by 6.0% in 2014. According to Clarkson Research, current projections suggest that growth will reach 6.7% in 2015, outpacing expected growth in global containership fleet capacity. Clarkson Research also reported relative stability in the benchmark three-year charter rates for 9,000 TEU containerships in the past two and a half years and a reduction in the proportion of the vessels in layup from the levels reached in 2009. Clarkson Research projects that this dynamic will help improve the supply and demand balance of the containership market through 2015. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | High barriers to entry to the long term charter market.According to Clarkson Research, availability of capital and selectivity by major liner companies can create barrier to entry in the long-term time charter market for larger vessels. We also believe that, given the large capital requirements, limited availability of financing, and need for a high level of operational and technical management expertise, the long-term charter market for larger vessels is difficult to penetrate. Our liner customers are extremely selective, and we believe that our relationship with Costamare provides us with a significant advantage in being able to attract long-term charters from high quality customers. We believe our relationship with Costamare and Costamare Shipping, and their long track record of operating containerships for some of the largest liner companies in the world, including A.P. Moller- Maersk, MSC, Evergreen, Hapag Lloyd Aktiengesellschaft, or “Hapag Lloyd”, and COSCO, allows us to benefit from the preference for experienced, high-quality operators. We believe this enhances our ability to compete for new customers and charters relative to less qualified and less experienced ship operators. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

We believe that our future business prospects are well supported by the following factors:

• | Significant built-in growth opportunities.In addition to our initial fleet of four containerships, we will have the option to purchase one wholly-owned vessel of Costamare for which a long-term charter has been arranged. Additionally, Costamare and York have a 36-month period after each such vessel’s acceptance by its charterer, in which they may offer us the right to purchase nine JV vessels expected to be delivered to Costamare and York |

7

| between the fourth quarter of 2015 and the end of 2016, for five of which long-term charters have been arranged. If they do not reach an agreement to offer us such right during the 36-month period, we will have the right to purchase such vessels at the end of such 36-month period, provided that, at the end of the 36-month period, the relevant vessel constitutes a non-compete vessel. Once such purchase options are no longer exercisable, Costamare and, with respect to the JV vessels, the JV Entity and York have agreed to offer us the right to purchase at fair market value as determined in accordance with the omnibus agreement other non-compete vessels that Costamare, either by itself or jointly with York owns or acquires, to the extent such vessels constitute non-compete vessels at the time of such offer to us, in each case in accordance with the terms of the omnibus agreement. We believe these acquisition opportunities, as well as other future acquisition opportunities from Costamare, JV Entities and York or other third parties, will facilitate the growth of our distributions per unit. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Predictable cash flow profile through long-term charters to leading liner companies with staggered expiration dates. Our initial fleet will operate under charters with initial terms that expire between 2018 and 2023, and six of the ten containerships for which we have options to purchase from Costamare and, with respect to the JV vessels, York have or will have charter durations ranging from approximately 5.5 to 10 years with Evergreen. The staggered maturities of the charters for vessels in our initial fleet will mean that we will likely conduct our re-chartering activity in varying rate environments and we will seek to tailor our charter terms accordingly. Our current charters do not provide the charterers with the option to purchase the vessels at the end of the charter term, which we believe will allow us to take advantage of any improvement in the container shipping market at the end of the charter terms. Furthermore, by contracting with the liner companies that we perceive to be the most financially and operationally sound, such as MSC, Evergreen and COSCO, we believe that we have reduced our potential counterparty risk. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Enhanced growth opportunities through our relationship with Costamare, an established owner of containerships with significant experience and relationships in the containership sector.We believe our relationship with Costamare will provide us with many benefits that should drive growth in our distributions per unit. We believe charterers award new business to established participants in the containership sector because of their demonstrated technical, commercial and managerial expertise. Because our initial fleet is managed by the same ship manager as Costamare, we believe that we will benefit from the record that Costamare’s containerships have of low unscheduled off-hire days, with fleet utilization levels, excluding scheduled dry-dockings, of 99.9%, 99.9% and 99.8% in 2012, 2013 and 2014, respectively. Furthermore, over the last three years Costamare’s largest customers by revenue included many of the world’s largest liner companies, including A.P. Moller-Maersk, MSC, Evergreen, Hapag-Lloyd and COSCO. We believe that our relationship with Costamare and its affiliated ship managers, with their track record and reputation, will help us to similarly maintain a customer base of large liner companies, as well as to attract additional long-term charters for containerships. Further, we believe that we will be able to enhance our operational and financial efficiency through Costamare’s strong relationships with customers, shipyards and established financing providers, and its large pool of experienced and qualified global seafarers. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Scale and flexibility in vessel operation.Our vessels will be managed by Costamare Shipping, as head manager, and the same technical managers used for Costamare’s own fleet, which consist of Costamare Shipping, its affiliated manager, Shanghai Costamare (which acts as a sub-manager), V.Ships Greece and, in certain cases, subject to our consent, other third party managers. We believe that utilizing both affiliated and unaffiliated managers will provide us with operational scale, geographical flexibility and market-specific experience and relationships, which will allow us to grow appropriately to meet demand and manage our vessels in an efficient and cost-effective manner. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Newly constructed and high specification containerships.Our initial fleet will be among the youngest of any containership operator, with three of the four vessels built in 2013 and an | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

8

| average age (weighted by TEU capacity) of approximately 3.5 years as of December 31, 2014. We believe the large size of the vessels in our initial fleet will be attractive to liner companies as such vessels provide economies of scale, reducing costs per TEU of capacity, and can be deployed in numerous trade routes, providing liner companies with operational flexibility. The majority of the vessels in our initial fleet and all of our option vessels are equipped with the latest electronically controlled engines and have been designed with optimized hulls and propulsion systems, which allows the vessels to achieve relatively high fuel efficiency at lower speeds. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Experienced management team.Our ship managers’ senior management teams have a combined average of approximately 38 years of experience in the shipping industry. In addition, we believe that we will be able to secure attractive long-term charters with leading liner companies because of, among other things, our relationship with Costamare, which has an established operating track record and a high level of service and support. The Chief Executive Officer of our general partner, Konstantinos Konstantakopoulos, and Chief Financial Officer of our general partner, Gregory Zikos, will allocate their time between managing our business and affairs and the business and affairs of Costamare. Mr. Konstantakopoulos is the Chief Executive Officer and Chairman of the Board of Costamare. Mr. Zikos is the Chief Financial Officer and a member of the board of directors of Costamare. The amount of time Mr. Konstantakopoulos and Mr. Zikos will allocate between our business and the businesses of Costamare will vary from time to time depending on various circumstances and needs of the businesses, such as the relative levels of strategic activities of the businesses. Mr. Konstantakopoulos and Mr. Zikos will devote sufficient time to our business and affairs as they believe is necessary for their proper conduct. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Financial flexibility and access to capital to support our growth.After giving effect to this offering, we expect to have a moderate level of debt. We believe that such capital structure will allow us to pursue accretive vessel acquisitions and explore various ways to maximize unitholder value and grow distributable cash flow per share. Since Costamare’s initial public offering in November 2010, its management team has successfully raised over $2.2 billion in the equity and bank debt markets. We will be managed by the same management team as that of Costamare and we believe that, as a public company, we will have access to the public equity and bank debt markets in order to pursue expansion opportunities. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

We can provide no assurance, however, that we will be able to utilize our strengths described above. For further discussion of the risks that we face, see “Risk Factors”.

Our primary business objective is to grow our business profitably and increase quarterly distributions per unit over time by executing the following strategies:

• | Pursue strategic and accretive acquisitions of containerships on long-term, fixed-rate charters.We will seek to leverage our relationship with Costamare to make strategic acquisitions that are accretive to our distributions per unit. As of December 31, 2014, Costamare had 68 containership vessels in its fleet, including 13 vessels in its joint venture with York. This fleet includes a substantial built-in pipeline of potential acquisition targets for us. Furthermore, under the omnibus agreement, we will have the option to purchase one wholly-owned vessel of Costamare for which a long-term charter has been arranged. Additionally, Costamare and York have a 36-month period after each such vessel’s acceptance by its charterer, in which they may offer us the right to purchase nine JV vessels expected to be delivered to Costamare and York between the fourth quarter of 2015 and the end of 2016, for five of which long-term charters have been arranged. If they do not reach an agreement to offer us such right during the 36-month period, we will have the right to purchase such vessels at the end of such 36-month period, provided that, at the end of the 36-month period, the relevant vessel constitutes a non-compete vessel. Once such purchase options are no longer exercisable, Costamare and, with respect to the JV vessels, the JV Entity and York have agreed to offer | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

9

| us the right to purchase other non-compete vessels in the Costamare fleet, to the extent such vessels constitute non-compete vessels at the time of such offer to us, in each case in accordance with the terms of the omnibus agreement. Finally, we will continuously evaluate potential vessel acquisitions from third-parties and seek to acquire those vessels that meet our rigorous quality standards, have long-term charters and that we believe will be accretive to distributions per unit. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Acquire attractively priced vessels.We believe we are well-positioned to take advantage of the significant opportunities created by the recent economic downturn to acquire vessels at attractively low prices. In addition to our initial fleet of four containerships, we will also have options to acquire one wholly-owned vessel of Costamare and, subject to being offered such vessels by Costamare and York, nine JV vessels, which are delivered or expected to be delivered to Costamare and York between the fourth quarter of 2015 and the end of 2016, and other rights under which we may acquire additional containerships from Costamare and, with respect to the JV vessels, York, as described above. We intend to expand our fleet by acquiring additional containerships at relatively low prices using proceeds from this offering to the extent available and proceeds from future equity and debt financings. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Manage our fleet and charter portfolio to provide a stable base of cash flows.We intend to maintain and grow our cash flow by expanding our relationships with creditworthy counterparties, growing our fleet of vessels on long-term time charters, and minimizing operating costs, while maintaining a high level of service to our customers. Costamare’s largest customers over the last three years have been A.P. Moller-Maersk, MSC, Evergreen, Hapag-Lloyd and COSCO, which we perceive to be among the more creditworthy liner companies. We believe that Costamare will continue to maintain and develop relationships with these and other liner companies, with a particular focus on counterparty diversification and credit quality, in order to support its growth programs. We expect to benefit from these growth and diversification initiatives as we seek to acquire additional vessels with long- term charters from Costamare. We believe that the long-term fixed-rate nature of our charters will continue to provide us with a stable base of contracted future revenue. As of December 31, 2014, the time charters for our initial fleet represented an aggregate of $343.1 million of contracted revenue through 2023. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Maintain a strong balance sheet through moderate use of leverage.We intend to use approximately $ million of the net proceeds from this offering and the borrowings under our new credit facility to repay the outstanding indebtedness under our existing credit facilities. We intend to manage our balance sheet conservatively, targeting a modest amount of leverage, managing our maturity profile and maintaining an adequate level of liquidity. We believe that managing our balance sheet in a conservative manner will minimize our financial risk while providing a solid foundation for our future expansion and enhancing our ability to apply a substantial portion of our cash flow to the payment of distributions to our unitholders. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Provide high-quality, low-cost customer service through efficient vessel management.We seek to provide high-quality, low-cost customer service that allows our customers to implement integrated logistics solutions in the marketplace in a cost-effective manner. Our managers’ ship management approach is to provide tailored services based on the customers’ needs, which we believe has helped extend Costamare’s charters and the useful lives of its containerships, and can differentiate us from our competitors. We believe that our partnership with Costamare Shipping, who may delegate certain management services to its affiliated managers, V.Ships Greece and, subject to our consent, other unaffiliated managers, will allow us to have a deep pool of operational management in multiple locations around the globe with the market-specific experience and relationships necessary to manage a large fleet with a high level of service at a low-cost, while offering the scalability and flexibility for future growth. We also believe that our focus on customer service and reliability will enhance our relationships with our charterers. In the past decade, Costamare and our other managers have had successful chartering relationships with the majority of the top 20 liner companies by TEU capacity. We also intend to apply high standards of vessel operation and maintenance to | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

10

| enhance the predictability of our operating expenses and the operational efficiencies of our fleet. |

We can provide no assurance, however, that we will be able to implement our business strategies described above. For further discussion of the risks that we face, see “Risk Factors”.

An investment in our common units involves risks associated with our business, our partnership structure and the tax characteristics of our common units. Please read carefully the risks described under “Risk Factors” beginning on page 31 of this prospectus.

These risks include, among other things, the following:

• | We may not have sufficient cash from operations, following the establishment of cash reserves and payment of fees and expenses, to enable us to pay the minimum quarterly distribution on our common units and subordinated units. | ||

• | We will be required to make substantial capital expenditures to maintain the operating capacity of our fleet and acquire vessels, which may reduce or eliminate the amount of cash available for distribution. | ||

• | Our ability to acquire additional containerships from Costamare or third parties will depend upon our ability to raise additional equity and debt financing, to fund all or a portion of the acquisition costs of these vessels, and may be dependent on the consent of existing lenders to Costamare. | ||

• | Our debt levels may limit our ability to obtain additional financing, pursue other business opportunities and pay distributions to unitholders. | ||

• | We depend on Costamare and its affiliates, including Costamare Shipping, to operate and expand our businesses and compete in our markets. | ||

• | Our future performance depends on the level of world and regional demand for chartering containerships, and a recurrence of the recent global economic slowdown may impede our ability to continue to grow our business. | ||

• | We have only four vessels in our initial fleet. Any limitation in the availability or operation of those vessels could have a material adverse effect on our business, financial condition, results of operations and cash flows, which effect would be amplified by the small size of our initial fleet. | ||

• | Unitholders have limited voting rights and our partnership agreement restricts the voting rights of unitholders (other than our general partner and its affiliates, including Costamare) owning more than 4.9% of our common units. | ||

• | Our unitholders will not be entitled to elect our general partner or its directors, subject to our general partner’s option to cause us at some point in the future to be managed by our own board of directors and, in that connection, to cause the common unitholders to permanently have the right to elect a majority of our directors. | ||

• | Upon completion of this offering, Costamare and our general partner will own a % interest in us and will have conflicts of interest and limited fiduciary and contractual duties to us and our common unitholders, which may permit them to favor their own interests to your detriment. | ||

• | Even if public unitholders are dissatisfied, they cannot initially remove our general partner without Costamare’s consent. | ||

• | You will experience immediate and substantial dilution of $ per common unit. | ||

• | Our general partner has a limited call right that may require you to sell your common units at an undesirable time or price. | ||

• | U.S. tax authorities could treat us as a “passive foreign investment company” under certain circumstances, which would have adverse U.S. federal income tax consequences to U.S. unitholders. |

11

This is not a comprehensive list of risks to which we are subject, and you should carefully consider all the information in this prospectus prior to investing in our common units.

Implications of Being an Emerging Growth Company

Our Predecessor had less than $1.0 billion in revenue during our last fiscal year, which means that we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act, or the “JOBS Act”. An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include, among others:

• | the ability to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in the registration statement of its initial public offering; | ||

• | exemption from the auditor attestation requirement in the assessment of the emerging growth company’s internal control over financial reporting; | ||

• | exemption from new or revised financial accounting standards applicable to public companies until such standards are also applicable to private companies; and | ||

• | exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board, or “PCAOB”, requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and financial statements. |

We may take advantage of these provisions until the end of the fiscal year following the fifth anniversary of our initial public offering or such earlier time that we are no longer an emerging growth company. We will cease to be an emerging growth company as of the earliest to occur of: (i) the last day of the fiscal year during which we had $1 billion or more in annual gross revenues; (ii) the date of our issuance, in a three-year period, of more than $1 billion in non-convertible debt; or (iii) the date on which we are deemed to be a “large accelerated filer” as defined for purposes of the Securities Exchange Act of 1934, or the “Exchange Act”, which will occur if the market value of our common units held by non-affiliates exceeds $700 million on the last business day of our second fiscal quarter. We may choose to take advantage of some, but not all, of these reduced burdens. For as long as we take advantage of the reduced reporting obligations, the information that we provide unitholders may be different than information provided by other public companies. We have elected to opt out of the extended transition period for complying with new or revised accounting standards applicable to public companies until such standards are also applicable to private companies, which election is irrevocable.

General

We were formed on July 30, 2014 as a Marshall Islands limited partnership. We intend to own, operate and acquire containerships under long-term charters with terms of five full years or more, although the vessels in our initial fleet will have charters with remaining terms ranging from 3.3 years to 8.2 years, as of December 31, 2014. Prior to the closing of this offering, our partnership will not own any vessels. At the closing of this offering, Costamare will contribute to us a 100% interest in entities which own a 100% interest in theCosco Beijing, theMSC Athens, theMSC Athosand theValue. Prior to this offering, we have been a wholly-owned subsidiary of Costamare, and our vessels have operated as part of Costamare’s larger fleet.

At or prior to the closing of this offering, the following transactions will occur:

• | we will issue to Costamare common units and all of our subordinated units, representing a % limited partner interest in us, and all of our incentive distribution rights, which will entitle Costamare to increasing percentages of the cash we distribute in excess of $ per unit per quarter; |

12

• | we will issue to Costamare Partners GP LLC, a wholly-owned subsidiary of Costamare, general partner units, representing a 2.0% general partner interest in us; and | ||

• | we will sell common units to the public in this offering, representing a % limited partner interest in us, which includes up to an aggregate of approximately $ million and $ million of common units that members of the Konstantakopoulos family and certain funds managed by York have indicated that they currently intend to purchase, respectively. |

At or promptly following the closing of this offering;

• | we will use the net proceeds from this offering, together with the borrowings under our new credit facility, to repay $ million of outstanding borrowings as part of a refinancing of our vessel financing agreements and retain $ million for general partnership purposes; and | ||

• | we will make a payment of the remaining proceeds of approximately $ million to Costamare as partial consideration for the interest described above. |

In addition, at or prior to the closing of this offering:

• | we, as guarantor, and our vessel owning subsidiaries, as borrowers, have entered into a new credit facility to refinance the existing vessel financing agreements, which will consist of a $126.6 million term loan facility and a $53.4 million revolving credit facility (provided that the amount drawn under the revolving credit facility, when aggregated with the term loan actually drawn, may not exceed 50% of the fair market value of the relevant security vessels). We expect to borrow under the term loan facility concurrently with the closing of this offering. Such new credit facility will be secured solely by vessels in our initial fleet. No guarantee or collateral will be provided by Costamare and its subsidiaries, other than us, in connection with such credit facility; | ||

• | we have entered into an omnibus agreement with Costamare, York, our general partner and other affiliates of Costamare and York governing, among other things: |

• | the extent to which we, Costamare and York may compete with each other; | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | following the Non-Compete Commencement Date, our agreement with Costamare and, with respect to any JV vessels, the JV Entities and York regarding their offer to us of certain rights to purchase non-compete vessels with charters having committed terms of five full years or more, which for existing charters shall mean charters with a remaining term of five full years or more; | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | our options to purchase theValence(or, at Costamare’s option, one of the substitute vessels) from Costamare within 12 months following the closing of this offering, and our agreement with Costamare, the JV Entities and York regarding their offer to us, within 36 months following each vessel’s acceptances by its respective charterer, of certain rights to purchase Hulls NCP0113, NCP0114, NCP0115, NCP0116, S2121, S2122, S2123, S2124 and S2125, in each case, at their respective fair market values, as described under “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Omnibus Agreement”; | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | certain rights of first offer on non-compete vessels under charters of five full years or more that Costamare or, with respect to the JV vessels, York proposes to sell, as described under “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Omnibus Agreement”; and | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | Costamare’s and, with respect to the JV vessels, York’s provision of certain indemnities to us; | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

• | we and our general partner will enter into a partnership management agreement with Costamare Shipping, pursuant to which Costamare Shipping will agree to provide us and our general partner certain administrative, commercial and technical management services; and |

13

• | we expect to enter into an addendum for each of the existing ship management agreements, which govern the crew and technical management of the vessels in our initial fleet, such that our operating subsidiaries will continue to be party to such existing ship management agreements with Costamare Shipping pursuant to the partnership management agreement. |

For further details on our agreements with Costamare and its affiliates, including amounts involved, see “Certain Relationships and Related Party Transactions”.

The consideration for the 100% interests in the entities which own a 100% interest in theCosco Beijing, theMSC Athens, theMSC Athosand theValuethat will be contributed to us will be determined based on fair values; however, since Costamare and the Partnership are entities under common control, the consideration will be accounted for at historical carrying values. The amount of cash consideration will be calculated after deducting from the net proceeds of this offering and the borrowings under our new credit facility the amount that will be used for the debt prepayment and the amount that will remain as cash for general corporate purposes for the Partnership. The non-cash consideration to Costamare will be equal to the fair value of the net assets as adjusted for the fair value of the vessels that will be contributed to the Partnership less the cash consideration. The difference between the fair value of consideration issued to Costamare and the net assets to be received will be accounted for as an equity transaction in the financial statements of the Partnership.

Holding Company Structure

We are a holding entity and will conduct our operations and business through subsidiaries, as is common with publicly traded limited partnerships, to maximize operational flexibility. We believe that conducting our operations through a publicly traded limited partnership will offer us the following advantages:

• | access to the public equity and debt capital markets; | ||

• | a lower cost of capital for expansion and acquisitions; and | ||

• | an enhanced ability to use equity securities as consideration in future acquisitions. |

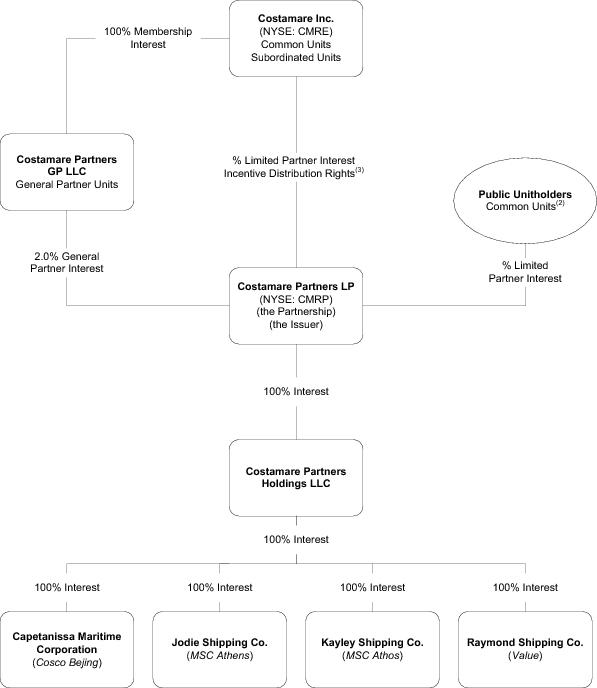

Simplified Organizational and Ownership Structure After this Offering

The following table and diagram depict our simplified organizational and ownership structure, after giving effect to the offering and related transactions described above, assuming no exercise of the underwriters’ option to purchase additional common units:

|

|

|

|

| ||||||||||

| Number of | Percentage | ||||||||||||

Public Common Units(1)(2) |

|

|

|

| ||||||||||

Costamare Inc. Common Units(1) |

|

|

|

| ||||||||||

York Common Units |

|

|

|

| ||||||||||

Konstantakopoulos Family Common Units |

|

|

|

| ||||||||||

Costamare Inc. Subordinated Units |

|

|

|

| ||||||||||

General Partner Units |

|

|

|

|

| 2.0% | ||||||||

|

|

|

|

| ||||||||||

|

|

|

| 100.0% | ||||||||||

|

|

|

|

| ||||||||||

14

(1) | Assumes the underwriters do not exercise their option to purchase additional common units. If the underwriters do not exercise their option to purchase additional common units in full, we will issue up to an additional common units to Costamare at the expiration of the option. Any such units issued to Costamare will be issued for no additional consideration. If the underwriters exercise their option to purchase up to additional common units, the number of common units purchased by the underwriters pursuant to such exercise will be sold to the public instead of being issued to Costamare. Accordingly, the exercise of the underwriters’ option will not affect the total number of common units outstanding. If the underwriters’ option is exercised in full, then Costamare would own common units, representing a % ownership interest in us and the public would own common units, representing a % ownership interest in us. | ||

(2) | Includes up to $ of common units that members of the Konstantakopoulos family have indicated that they currently intend to purchase and up to $ of common units that |

15

| certain funds managed by York have indicated that they currently intend to purchase, in each case in the offering at the public offering price. | ||

(3) | Pursuant to a separate agreement between Costamare and York, York will be entitled to receive from Costamare certain incentive payments based primarily on York’s interest in the JV vessels acquired by the Partnership and the amount of any incentive distributions received by Costamare. For more information, see “How We Make Cash Distributions—Incentive Distribution Rights”. |

16

Our partnership agreement provides that our general partner, Costamare Partners GP LLC, a Marshall Islands limited liability company, will manage our operations and day-to-day activities. The executive officers and two of the directors of Costamare Partners GP LLC also serve as executive officers or directors of Costamare, and another director of Costamare Partners GP LLC also serves as a key employee of an affiliate of Costamare. For more information about these individuals, see “Management—Directors and Executive Officers”.

Our unitholders will not be entitled to elect our general partner or its directors. Our general partner will not receive a management fee in connection with its management of our business, but it will be entitled to be reimbursed for all direct and indirect expenses incurred on our behalf. Our general partner will also be entitled to distributions on its general partner interest. Please read “Certain Relationships and Related Party Transactions” and “Management”.