Table of Contents

As filed with the Securities and Exchange Commission on March 30, 2015

Registration No. 333-202665

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2 TO

FORM F-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

TRILLIUM THERAPEUTICS INC.

(Exact name of Registrant as specified in its charter)

| Ontario, Canada | 2834 | Not applicable | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

96 Skyway Avenue, Toronto, Ontario, Canada M9W 4Y9

Telephone: (416) 595-0627

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Puglisi & Associates, 850 Library Avenue, Suite 204, Newark, Delaware 19711

Telephone: (302) 738-6680

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

| Daniel M. Miller Dorsey & Whitney LLP Suite 1605, Pacific Centre 777 Dunsmuir Street Vancouver, British Columbia Canada V7Y 1K4 (604) 687-5151 | Thomas S. Levato Goodwin Procter LLP The New York Times Building 620 Eighth Avenue New York, NY 10018 (212) 813-8800 | |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [ ]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

CALCULATION OF REGISTRATION FEE

Title of each class of securities to be registered | Proposed maximum aggregate offering price(1)(3)(4) | Amount of registration fee(2) | ||

| Common shares, no par value | ||||

| Series II First Preferred shares, no par value | ||||

| Total | US$57,500,000 | US$6,682 |

(1) Estimated solely for the purpose of determining the amount of registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended.

(2) Previously paid.

(3) Includes shares that the underwriters may purchase pursuant to their option to purchase additional common shares, if any.

(4) Includes the common shares issuable upon conversion of the Series II First Preferred shares being registered.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the United States Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MARCH 30, 2015

PROSPECTUS

US$50,000,000

Common Shares

Series II First Preferred Shares

Trillium Therapeutics Inc. is offering US$50,000,000 of common shares and Series II Non-Voting Convertible First Preferred Shares, or the Series II First Preferred Shares, including the common shares issuable from time to time upon conversion of the Series II First Preferred Shares, pursuant to this prospectus. The Series II First Preferred Shares are being offered to certain of our existing shareholders whose purchase of common shares in this offering may result in such shareholder, together with its affiliates and certain related parties, beneficially owning more than 4.99% of our outstanding common shares following the consummation of this offering.

Our common shares are listed for trading on the Toronto Stock Exchange under the symbol “TR” and on the NASDAQ Capital Market under the symbol “TRIL”. On March 27, 2015, the closing price of the common shares on the Toronto Stock Exchange was $23.00 and on the NASDAQ Capital Market was US$18.37. There is no established public trading market for our Series II First Preferred Shares, and we do not expect a market to develop. In addition, we do not intend to apply for listing of our Series II First Preferred Shares on any national securities exchange or other nationally recognized trading system.

Each Series II First Preferred Share is convertible into one common share, subject to adjustment, at any time at the option of the holder, provided that the holder will be prohibited from converting Series II First Preferred Shares into common shares if, as a result of such conversion, the holder, together with its affiliates, would own more than 4.99% of the total number of our common shares then issued and outstanding, unless the holder gives us at least 61 days prior notice of an intent to convert into common shares that would cause the holder to own more than 4.99% of the total number of our common shares then issued and outstanding. See the discussion in the section of this prospectus entitled “Description of Share Capital – First Preferred Shares — Series II First Preferred Shares”.

We are an “emerging growth company” under the U.S. Jumpstart Our Business Startups Act of 2012 and as such have elected to comply with certain reduced public company disclosure requirements. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Implications of Being an Emerging Growth Company”.

Investing in our securities involves risks. See “Risk Factors” beginning on page 9 of this prospectus.

| Per Share | Total | |||||||

Price to the public, common shares | US$ | US$ | ||||||

Underwriting discount, common shares(1) | US$ | US$ | ||||||

Proceeds to us (before expenses), common shares | US$ | US$ | ||||||

Price to the public, Series II First Preferred Shares | US$ | US$ | ||||||

Underwriting discount, Series II First Preferred Shares (1) | US$ | US$ | ||||||

Proceeds to us (before expenses), Series II First Preferred Shares | US$ | US$ | ||||||

Aggregate proceeds, before expenses, to us | US$ | US$ | ||||||

(1) Please see the section of this prospectus entitled “Underwriting” for a complete description of the compensation payable to the underwriters.

We have granted the underwriters an option to purchase up to an additional 15% of the total number of common shares sold in this offering. The underwriters can exercise this option at any time within 30 days after the date of this prospectus.

Neither the United States Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the offered shares on or about , 2015.

Joint Book-Running Managers

| Leerink Partners | Cowen and Company |

Co-Manager

Oppenheimer & Co.

The date of this prospectus is , 2015.

Table of Contents

i

Table of Contents

All references in this prospectus to “the Company”, “Trillium”, “we”, “us”, or “our” refer to Trillium Therapeutics Inc. and the subsidiaries through which it conducts its business, unless otherwise indicated.

Neither we nor the underwriters have authorized anyone to provide information different from that contained in this prospectus, any amendment or supplement to this prospectus or in any free writing prospectus prepared by us or on our behalf. Neither we nor the underwriters take any responsibility for, and can provide no assurance as to the reliability of, any information other than the information in this prospectus, any amendment or supplement to this prospectus, and any free writing prospectus prepared by us or on our behalf. Neither the delivery of this prospectus nor the sale of our securities means that information contained in this prospectus is correct after the date of this prospectus. This prospectus is not an offer to sell or the solicitation of an offer to buy our securities in any circumstances under which such offer or solicitation is unlawful.

For investors outside the United States, neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus. The offered shares have not been and will not be qualified for distribution pursuant to a prospectus filed with the securities regulatory authorities in any of the provinces or territories of Canada and may not be offered or sold in Canada except pursuant to an exemption from the prospectus requirements of applicable Canadian securities laws.

This prospectus includes statistical data, market data and other industry data and forecasts, which we obtained from market research, publicly available information and independent industry publications and reports that we believe to be reliable sources.

All references in this prospectus to the number of common shares, stock options and deferred share units, or DSUs, the conversion ratio of our Series II First Preferred Shares, our Series I Non-Convertible First Preferred Shares, or the Series I First Preferred Shares, and warrants, and the market price of our common shares prior to November 14, 2014 are presented on a pre-consolidated basis, and on or after November 14, 2014 on a post-consolidation basis, unless otherwise noted.

Unless otherwise indicated, all references to “dollars” or the use of the symbol “$” are to Canadian dollars, and all references to “US dollars” or “US$” are to United States dollars.

ii

Table of Contents

The following table sets forth, for each period indicated, the high, low and average exchange rates for Canadian dollars expressed in United States dollars, provided by the Bank of Canada. The exchange rates set forth below demonstrate trends in exchange rates, but the actual exchange rates used throughout this prospectus may vary. The average exchange rate is calculated by using the average of the closing prices on the last day of each month during the relevant period. On March 27, 2015, the noon exchange rate for one Canadian dollar expressed in United States dollars as reported by the Bank of Canada, was $1.00 = US$0.7949. The high and low exchange rates are intra-day values rather than noon or closing rates.

|

| |||||||||||

$1 Canadian dollar equivalent in United States dollars | High | Low | Average | |||||||||

Year ended December 31, 2010 | US$ | 1.0069 | US$ | 0.9218 | US$ | 0.9657 | ||||||

Year ended December 31, 2011 | 1.0630 | 0.9383 | 1.0136 | |||||||||

Year ended December 31, 2012 | 1.0371 | 0.9576 | 1.0010 | |||||||||

Year ended December 31, 2013 | 1.0188 | 0.9314 | 0.9662 | |||||||||

Year ended December 31, 2014 | 0.9444 | 0.8568 | 0.9021 | |||||||||

September 2014 | 0.9241 | 0.8913 | ||||||||||

October 2014 | 0.9017 | 0.8783 | ||||||||||

November 2014 | 0.8936 | 0.8732 | ||||||||||

December 2014 | 0.8839 | 0.8568 | ||||||||||

January 2015 | 0.8562 | 0.7813 | ||||||||||

February 2015 | 0.8095 | 0.7876 | ||||||||||

iii

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements within the meaning of applicable securities laws. All statements contained herein that are not clearly historical in nature are forward-looking, and the words ���anticipate”, “believe”, “expect”, “estimate”, “may”, “will”, “could”, “leading”, “intend”, “contemplate”, “shall” and similar expressions are generally intended to identify forward-looking statements. Forward-looking statements in this prospectus include, but are not limited to, statements with respect to:

| • | our expected future loss and accumulated deficit levels; |

| • | our projected financial position and estimated cash burn rate; |

| • | our expectations about the timing of achieving milestones and the cost of our development programs; |

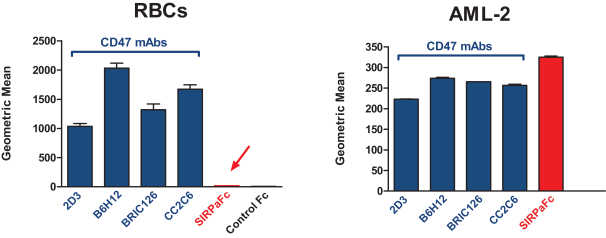

| • | our observations and expectations regarding the binding profile of SIRPaFc with red blood cells compared to anti-CD47 monoclonal antibodies and proprietary CD47-blocking agents and the potential benefits to patients; |

| • | our requirements for, and the ability to obtain, future funding on favorable terms or at all; |

| • | our projections for the SIRPaFc development plan and progress of each of our products and technologies, particularly with respect to the timely and successful completion of studies and trials and availability of results from such studies and trials; |

| • | our expectations about our products’ safety and efficacy; |

| • | our expectations regarding our ability to arrange for the manufacturing of our products and technologies; |

| • | our expectations regarding the progress, and the successful and timely completion, of the various stages of the regulatory approval process; |

| • | our ability to secure strategic partnerships with larger pharmaceutical and biotechnology companies; |

| • | our strategy to acquire and develop new products and technologies and to enhance the capabilities of existing products and technologies; |

| • | our plans to market, sell and distribute our products and technologies; |

| • | our expectations regarding the acceptance of our products and technologies by the market; |

| • | our ability to retain and access appropriate staff, management, and expert advisers; |

| • | our expectations with respect to existing and future corporate alliances and licensing transactions with third parties, and the receipt and timing of any payments to be made by us or to us in respect of such arrangements; and |

| • | our strategy with respect to the protection of our intellectual property. |

All forward-looking statements reflect our beliefs and assumptions based on information available at the time the assumption was made. These forward-looking statements are not based on historical facts but rather on management’s expectations regarding future activities, results of operations, performance, future capital and other expenditures (including the amount, nature and sources of funding thereof), competitive advantages, business prospects and opportunities. By its nature, forward-looking information involves numerous assumptions, inherent risks and uncertainties, both general and specific, known and unknown, that contribute to the possibility that the predictions, forecasts, projections or other forward-looking statements will not occur. Factors which could cause future outcomes to differ materially from those set forth in the forward-looking statements include, but are not limited to:

| • | the effect of continuing operating losses on our ability to obtain, on satisfactory terms, or at all, the capital required to maintain us as a going concern; |

| • | the ability to obtain sufficient and suitable financing to support operations, preclinical development, clinical trials, and commercialization of products; |

| • | the risks associated with the development of novel compounds at early stages of development in our intellectual property portfolio; |

| • | the risks of reliance on third-parties for the planning, conduct and monitoring of clinical trials and for the manufacture of drug product; |

| • | the risks associated with the development of our product candidates including the demonstration of efficacy and safety; |

| • | the risks related to clinical trials including potential delays, cost overruns and the failure to demonstrate efficacy and safety; |

iv

Table of Contents

| • | the risks of delays and inability to complete clinical trials due to difficulties enrolling patients; |

| • | risks associated with our inability to successfully develop companion diagnostics for our development candidates; |

| • | delays or negative outcomes from the regulatory approval process; |

| • | our ability to successfully compete in our targeted markets; |

| • | our ability to attract and retain key personnel, collaborators and advisors; |

| • | risks relating to the increase in operating costs from expanding existing programs, acquisition of additional development programs and increased staff; |

| • | risk of negative results of clinical trials or adverse safety events by us or others related to our product candidates; |

| • | the potential for product liability claims; |

| • | our ability to achieve our forecasted milestones and timelines on schedule; |

| • | financial risks related to the fluctuation of foreign currency rates and expenses denominated in foreign currencies; |

| • | our ability to adequately protect proprietary information and technology from competitors; |

| • | risks related to changes in patent laws and their interpretations; |

| • | our ability to source and maintain licenses from third-party owners; and |

| • | the risk of patent-related litigation and the ability to protect trade secrets, |

all as further and more fully described under the section of this prospectus entitled “Risk Factors”.

Although the forward-looking statements contained in this prospectus are based upon what our management believes to be reasonable assumptions, we cannot assure readers that actual results will be consistent with these forward-looking statements.

Any forward-looking statements represent our estimates only as of the date of this prospectus and should not be relied upon as representing our estimates as of any subsequent date. We undertake no obligation to update any forward-looking statement or statements to reflect events or circumstances after the date on which such statement is made or to reflect the occurrence of unanticipated events, except as may be required by securities legislation.

v

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that you should consider before deciding to invest in our common shares or Series II First Preferred Shares. You should carefully read this entire prospectus, including the sections of this prospectus entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, and the financial statements and related notes included in this prospectus, before investing.

Overview

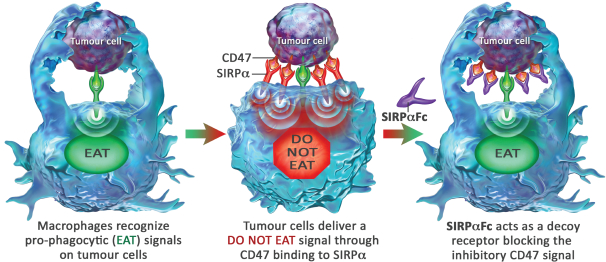

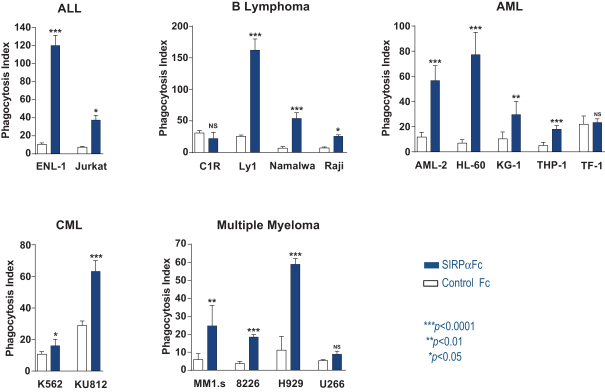

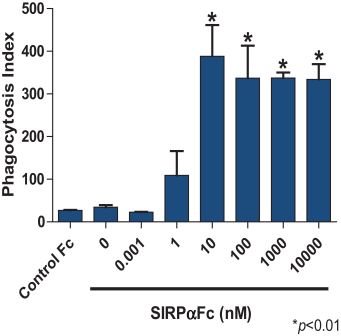

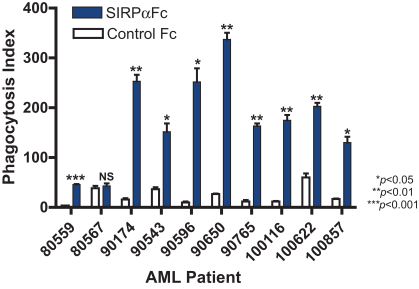

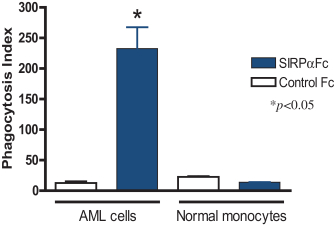

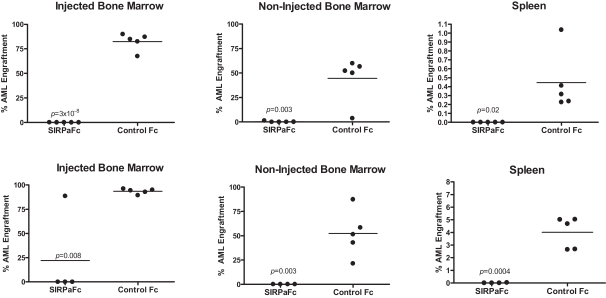

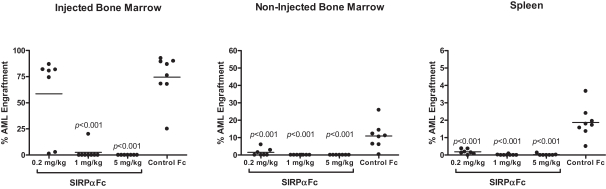

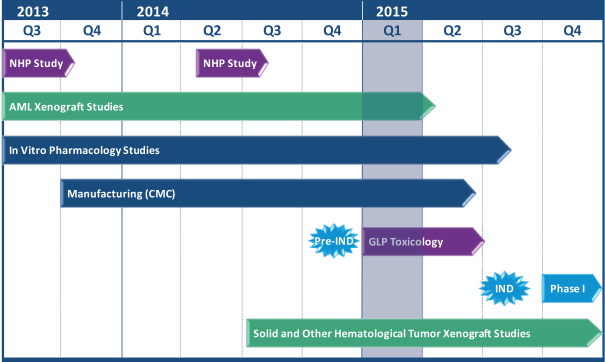

We are an immuno-oncology company developing innovative therapies for the treatment of cancer. Our lead program, SIRPaFc, is a novel, antibody-like protein that harnesses the innate immune system by blocking the activity of CD47, a molecule whose expression is increased on cancer cells to evade the host immune system. Expressed at high levels on the cell surface of a variety of liquid and solid tumors, CD47 functions as a signal that inhibits the destruction of tumor cells by macrophages via phagocytosis. By blocking the activity of CD47, we believe SIRPaFc has the ability to promote the macrophage-mediated killing of tumor cells in a broad variety of cancers both as a monotherapy and in combination with other immune therapies. We expect to file an investigational new drug, or IND, application in the third quarter of 2015, and shortly thereafter commence phase I studies in acute myeloid leukemia, or AML, and myelodysplastic syndrome, or MDS. In the first phase I study we are also considering dosing patients with solid tumors or lymphomas who have normal bone marrow function in order to more clearly assess the potential hematological toxicity of SIRPaFc. We also plan to continue to conduct preclinical studies in other liquid and solid tumors to identify future clinical indications.

The immune system is the body’s mechanism to identify and eliminate pathogens, and can be divided into the innate immune system and the adaptive immune system. The innate immune system is the body’s first line of defense and consists of proteins and cells, such as macrophages, that identify and provide an immediate response to pathogens. The adaptive immune system is activated by, and adapts to, pathogens, creating a targeted and durable response. Cancer cells often have the ability to reduce the immune system’s ability to recognize and destroy them. We believe SIRPaFc plays a critical role in enhancing the innate immune system and importantly, because of its ability to target macrophages, also has an important downstream effect on the adaptive immune system.

SIRPaFc Key Attributes

| • | Potential efficacy in a broad range of cancers. SIRPaFc blocks the tumor’s ability to transmit a “do not eat” signal allowing macrophages to destroy tumor cells; a mechanism that we believe has broad applicability. | |||

| • | Potential for use as monotherapy and in combination with other therapies. We intend to develop SIRPaFc as a monotherapy as well as potentially for use in combination with other cancer immuno-therapies. | |||

| • | Differentiated pharmacokinetic and safety profile. We believe SIRPaFc’s low level of binding to red blood cells lowers the risk of anemia and lowers the loss of drug from circulation. This pharmacokinetic profile potentially allows for lower dosing and a positive safety profile. | |||

| • | May enhance both innate and adaptive immune response. SIRPaFc may enhance stimulation of tumor attacking T-cells since macrophages, in addition to their role in phagocytosis, can also prime T-cells through antigen-presentation. |

1

Table of Contents

Our Strategy

Our goal is to become a leading innovator in the field of immuno-oncology by targeting immune-regulatory pathways that tumor cells exploit to evade the host immune system. We believe that SIRPaFc has the potential to improve survival and quality of life for cancer patients.

| • | Rapidly advance the clinical development of SIRPaFc. Following the completion of ongoing toxicology studies and current Good Manufacturing Practice, or cGMP, production of our clinical lot, we plan to file an IND in the third quarter of 2015 for a first-in-human trial of SIRPaFc in AML and MDS patients, and possibly solid tumor or lymphoma patients with normal bone marrow function. | |||

| • | Expand our SIRPaFc clinical program to include additional cancer indications. Because CD47 is highly expressed by multiple liquid and solid tumors, and high expression is correlated with worse clinical outcomes, we believe SIRPaFc has potential to be effective in a wide variety of tumors. We plan to carry out the preclinical work necessary to select additional, high potential cancer indications for clinical development. | |||

| • | Maximize value of SIRPaFc through scientific collaborations. SIRPaFc has broad potential applicability in various cancer indications, and we believe it is well suited for use as both a monotherapy and in combination with other agents. We plan to selectively and opportunistically pursue scientific collaborations with academic researchers as well as other companies, in order to realize the full value proposition of SIRPaFc. | |||

| • | To become a leading integrated immuno-oncology company. Developing cancer immunotherapies requires significant experience and development expertise. Our experienced management team, board of directors, scientific advisory board and in-house capabilities enable us to execute against our product development plan. We intend to continue to invest in the infrastructure and personnel to support our continued growth that will enable us to become a leading immuno-oncology company. |

Risk Factors

Our business is subject to a number of risks of which you should be aware before making an investment decision. These risks are discussed more fully in the section of this prospectus entitled “Risk Factors.” These risks include, but are not limited to, the following:

| • | We expect to incur future losses and we may never become profitable. |

| • | We currently have no product revenue and will not be able to maintain our operations and research and development without additional funding. |

| • | We will require additional capital to finance our operations, which may not be available to us on acceptable terms, or at all. As a result, we may not complete the development and commercialization of our product candidates or develop new product candidates. |

| • | Our prospects depend on the success of our product candidates, which are at early stages of development, and we may not generate revenue for several years, if at all, from these products. |

| • | We rely on third parties to plan, conduct and monitor our preclinical studies and clinical trials, and their failure to perform as required would interfere with our product development. |

| • | We expect to be classified as a passive foreign investment company, or PFIC, for 2015 and certain of our U.S. shareholders may suffer adverse tax consequences as a result. |

Implications of Being an Emerging Growth Company

We are an “emerging growth company” under the U.S. Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and will continue to qualify as an “emerging growth company” until the earliest to occur of: (a) the last day of the fiscal year during which we have total annual gross revenues of $1,000,000,000 (as

2

Table of Contents

such amount is indexed for inflation every 5 years by the United States Securities and Exchange Commission, or SEC) or more; (b) the last day of our fiscal year following the fifth anniversary of the date of the first sale of our common shares pursuant to an effective registration statement under the U.S. Securities Act of 1933, as amended, or the Securities Act; (c) the date on which we have, during the previous 3-year period, issued more than $1,000,000,000 in non-convertible debt; or (d) the date on which we are deemed to be a “large accelerated filer”, as defined in Rule 12b–2 of the U.S. Securities Exchange Act of 1934, as amended, or the Exchange Act.

Generally, a company that registers any class of its securities under Section 12 of the Exchange Act is required to include in the second and all subsequent annual reports filed by it under the Exchange Act, a management report on internal control over financial reporting and, subject to an exemption available to companies that meet the definition of a “smaller reporting company” in Rule 12b-2 under the Exchange Act, an auditor attestation report on management’s assessment of the company’s internal control over financial reporting. However, for so long as we continue to qualify as an emerging growth company, we will be exempt from the requirement to include an auditor attestation report in our annual reports filed under the Exchange Act, even if we do not qualify as a “smaller reporting company”. In addition, Section 103(a)(3) of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, has been amended by the JOBS Act to provide that, among other things, auditors of an emerging growth company are exempt from any rules of the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the company.

Any U.S. domestic issuer that is an emerging growth company is able to avail itself of the reduced disclosure obligations regarding executive compensation in periodic reports and proxy statements, and to not present to its shareholders a non-binding advisory vote on executive compensation, obtain approval of any golden parachute payments not previously approved, or present the relationship between executive compensation actually paid and our financial performance. So long as we are a foreign private issuer, we are not subject to such requirements, and will not become subject to such requirements even if we were to cease to be an emerging growth company.

As a reporting issuer under the securities legislation of the Canadian provinces of Ontario, British Columbia, Manitoba, Nova Scotia and Alberta, we are required to comply with all new or revised accounting standards that apply to Canadian public companies. Pursuant to Section 107(b) of the JOBS Act, an emerging growth company may elect to utilize an extended transition period for complying with new or revised accounting standards for public companies until such standards apply to private companies. We have elected not to utilize this extended transition period.

Implications of Being a Foreign Private Issuer

We are also considered a “foreign private issuer” pursuant to Rule 405 promulgated under the Securities Act. In our capacity as a foreign private issuer, we are exempt from certain rules under the Exchange Act that impose certain disclosure obligations and procedural requirements for proxy solicitations under Section 14 of the Exchange Act. In addition, our officers, directors and principal shareholders are exempt from the reporting and “short-swing” profit recovery provisions of Section 16 of the Exchange Act and the rules under the Exchange Act with respect to their purchases and sales of our common shares. Moreover, we are not required to file periodic reports and financial statements with the SEC as frequently or as promptly as United States companies whose securities are registered under the Exchange Act. In addition, we are not required to comply with Regulation FD, which restricts the selective disclosure of material information.

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities

3

Table of Contents

are held by United States residents and any of the following three circumstances applies: (1) the majority of our executive officers or directors are United States citizens or residents; (2) more than 50% of our assets are located in the United States; or (3) our business is administered principally in the United States.

We have taken advantage of certain reduced reporting and other requirements in this prospectus. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold equity securities.

Trading Markets

Our common shares began trading on the Toronto Stock Exchange, or TSX, under the symbol “TR” in April 2014. As of December 2014, our common shares also trade on the NASDAQ Capital Market under the symbol “TRIL”. There is no established public trading market for our Series II First Preferred Shares, and we do not expect a market to develop. In addition, we do not intend to apply for listing of our Series II First Preferred Shares on any national securities exchange or other nationally recognized trading system.

Corporate Information

We were incorporated under the Business Corporations Act (Alberta) on March 31, 2004 as Neurogenesis Biotech Corp. On October 19, 2004, we amended our articles of incorporation to change our name from Neurogenesis Biotech Corp. to Stem Cell Therapeutics Corp., or SCT. On November 7, 2013 SCT was continued under the Business Corporations Act (Ontario), or OBCA. On June 1, 2014 we filed articles of amalgamation to amalgamate SCT with our wholly-owned subsidiary, Trillium Therapeutics Inc., or Trillium Privateco, and renamed the combined company Trillium Therapeutics Inc. We are a company domiciled in Ontario, Canada.

On March 26, 2015, we incorporated a subsidiary, Trillium Therapeutics USA Inc., under the laws of Delaware.

We had one wholly-owned subsidiary, Stem Cell Therapeutics Inc., which was incorporated under the Business Corporations Act (Alberta) on December 22, 1999 and was continued under the OBCA on November 12, 2003 and then extra-provincially registered in Alberta on January 11, 2005. This inactive subsidiary was dissolved on September 17, 2014.

Our head and registered offices are located at 96 Skyway Avenue, Toronto, Ontario, Canada M9W 4Y9. Our telephone number is (416) 595-0627. Our agent for service of process in the United States is Puglisi & Associates, 850 Library Avenue, Suite 204, Newark, Delaware 19711, Telephone: (302) 738-6680. Our website address is www.trilliumtherapeutics.com. Our website and the information contained on, or that can be accessed through, our website will not be deemed to be incorporated by reference in, and are not considered part of, this prospectus. You should not rely on our website or any such information in making your decision whether to purchase our securities.

4

Table of Contents

Issuer | Trillium Therapeutics Inc. | |

Offering Amount | US$50,000,000 of common shares and Series II First Preferred Shares (including the common shares issuable from time to time upon conversion of the Series II First Preferred Shares) | |

Common Shares | ||

Common shares being offered | common shares | |

Common shares to be outstanding immediately after this offering | common shares | |

Option to purchase additional shares | We have granted the underwriters an option for a period of up to 30 days from the date of this prospectus to purchase up to an additional 15% of the total number of common shares sold in this offering at the public offering price less the underwriting discounts and commissions. | |

TSX symbol | TR | |

NASDAQ Capital Market symbol | TRIL | |

Series II First Preferred Shares | ||

Series II First Preferred Shares being offered |

Series II First Preferred Shares (including the common shares issuable from time to time upon conversion of the Series II First Preferred Shares). The Series II First Preferred Shares are being offered to certain of our existing shareholders whose purchase of common shares in this offering may result in such shareholder, together with its affiliates and certain related parties, beneficially owning more than 4.99% of our outstanding common shares following the consummation of this offering. | |

Conversion | Each Series II First Preferred Share is convertible into one common share at any time at the option of the holder, provided that the holder will be prohibited from converting Series II First Preferred Shares into common shares if, as a result of such conversion, the holder, together with its affiliates, would own more than 4.99% of the total number of our common shares then issued and outstanding, unless the holder gives us at least 61 days prior notice of an intent to convert into common shares that would cause the holder to own more than 4.99% of the total number of our common shares then issued and outstanding.See “Description of Share Capital – First Preferred Shares — Series II First Preferred Shares”. | |

Liquidation preference | In the event of our liquidation, dissolution or winding-up, whether voluntary or involuntary, or in the event of any other distribution of our assets among our shareholders for the purpose of winding-up our affairs, or in the event of a reduction or redemption of our capital stock, the holders of Series II First Preferred Shares are entitled to receive an amount per share equal to that amount of money that we received as consideration for such Series II First Preferred Shares divided by the | |

5

Table of Contents

| number of Series II First Preferred Shares issued. After such payment, the holders of Series II First Preferred Shares are not entitled to share in any further distribution of our property or assets. See “Description of Share Capital – First Preferred Shares – Series II First Preferred Shares”. | ||

Voting rights | The holders of our Series II First Preferred Shares will generally have no voting rights, except with respect to such matters and in the manner as to which voting rights are accorded to the holders of specified classes of shares pursuant to the Business Corporations Act (Ontario). | |

Dividends | Holders of Series II First Preferred Shares are entitled to receive dividends as determined and declared at the discretion of our board of directors equally on a one-for-one basis with the holders of the other series of First Preferred Shares and, at the discretion of our board of directors, either in priority to, or equally on a one-for-one basis with, the holders of our common shares and Class B shares. See “Description of Share Capital – First Preferred Shares – Series II First Preferred Shares”. | |

Market for Series II First Preferred Shares | There is no established public trading market for our Series II First Preferred Shares, and we do not expect a market to develop. In addition, we do not intend to apply for listing of our Series II First Preferred Shares on any national securities exchange or other nationally recognized trading system. | |

Offering restrictions | The common shares and Series II First Preferred Shares described in this prospectus are not being offered in Canada, and each purchaser of common shares and Series II First Preferred Shares from the underwriters is deemed to agree, upon acceptance of delivery of the purchased common shares and Series II First Preferred Shares, that the purchaser will not resell the purchased common shares or Series II First Preferred Shares to any resident of Canada or (in the case of the common shares) over the Toronto Stock Exchange or otherwise in Canada for a period of 90 days following the completion of this offering, and to represent that it is not a resident of Canada or purchasing the offered shares on behalf of or as agent for any person that is in or a resident of Canada. See “Underwriting – International Selling Restrictions – Canada”. | |

Use of proceeds | We estimate that we will receive net proceeds from this offering of approximately US$ million, or US$ million if the underwriters exercise in full their option to purchase additional common shares, after deducting underwriting discounts and commissions and estimated offering expenses.

We currently intend to use the net proceeds we receive from this offering for the development of SIRPaFc in AML, MDS, and other potential indications; working capital; and other general corporate purposes.

See the section of this prospectus entitled “Use of Proceeds” for additional information. | |

6

Table of Contents

Dividend policy | We have not declared any dividends since our inception and do not anticipate that we will do so in the foreseeable future. We currently intend to retain future earnings, if any, to finance the development of our business. Any future payment of dividends or distributions will be determined by our board of directors on the basis of our earnings, financial requirements and other relevant factors. | |

Risk factors | Investing in our securities involves a high degree of risk and purchasers of our securities may lose part or all of their investment. See the section of this prospectus entitled “Risk Factors” for a discussion of factors you should carefully consider before deciding to invest in our securities. | |

The number of our common shares to be outstanding after this offering is based on 5,018,139 of our common shares outstanding as of March 20, 2015. The number of common shares to be outstanding after this offering excludes the following:

| • | 64,904,689 Series I First Preferred Shares convertible into 2,163,490 common shares; |

| • | 125,797,904 common share purchase warrants convertible into 4,193,263 common shares at aweighted-average exercise price of $8.66 per common share; |

| • | 580,475 stock options with a weighted-average exercise price of $9.68 per common share; |

| • | 28,777 DSUs; and |

| • | Series II First Preferred Shares being offered pursuant to this prospectus convertible into common shares. |

Except as otherwise indicated herein, all information in this prospectus assumes no exercise of the underwriters’ option to purchase additional common shares.

7

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL INFORMATION

The following tables summarize financial data as at and for the fiscal years ended December 31, 2014, 2013, 2012, 2011, and 2010 prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. The financial information in the tables below as at December 31, 2014, 2013 and 2012 and for the years then ended has been derived from our audited consolidated financial statements and related notes included in this prospectus. The financial information in the tables below as at December 31, 2011 and 2010 and for the years then ended has been derived from our audited consolidated financial statements and related notes for those years.

The summary financial data below should be read in conjunction with the financial statements included in this prospectus beginning on page F-1 of this prospectus and with the information appearing in the section of this prospectus entitled “Selected Consolidated Financial Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”. Our historical results do not necessarily indicate results expected for any future period.

Consolidated statement of loss and comprehensive loss data | Year ended December 31, | |||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| Net sales | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||

| Net loss and comprehensive loss | 12,881,820 | 4,289,308 | 1,061,502 | 3,173,947 | 4,305,867 | |||||||||||||||

| Loss from continuing operations per share(1) | 3.06 | 3.16 | 1.71 | 5.22 | 8.24 | |||||||||||||||

| Net loss per common share(1) | 3.06 | 3.16 | 1.71 | 5.22 | 8.24 | |||||||||||||||

| Fully dilute net loss per common share(1) | 3.06 | 3.16 | 1.71 | 5.22 | 8.24 | |||||||||||||||

| As at December 31, 2014 | ||||||||

Consolidated statement of financial position data | (actual) | (as adjusted)(4) | ||||||

Total assets | $ | 28,186,032 | $ | |||||

Net assets | $ | 24,304,294 | $ | |||||

Capital stock - common | $ | 49,505,792 | $ | |||||

Number of common shares outstanding(2) | 4,427,244 | |||||||

Capital stock - preferred | $ | 10,076,151 | $ | |||||

Number of preferred shares outstanding(3) | 69,504,689 | |||||||

Dividends declared per share | - | - | ||||||

Notes:

| (1) | The per share figures have been restated to reflect a share consolidation ratio of one post-consolidated common share for each 30 pre-consolidation common shares on November 14, 2014. |

| (2) | The number of common shares has been restated to reflect a share consolidation ratio of 1 post-consolidated common share for each 30 pre-consolidation common shares on November 14, 2014. |

| (3) | 30 preferred shares are convertible into one common share. |

| (4) | The as adjusted column reflects the sale by us of common shares at a price of US$ per share and Series II First Preferred Shares at a price of US$ per Series II First Preferred Share in this offering. |

8

Table of Contents

An investment in our securities involves a high degree of risk and should be considered speculative. An investment in our securities should only be undertaken by those persons who can afford the total loss of their investment. You should carefully consider the risks and uncertainties described below, as well as other information contained in this prospectus. The risks and uncertainties below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we believe to be immaterial may also adversely affect our business. If any of the following risks occur, our business, financial condition and results of operations could be seriously harmed and you could lose all or part of your investment. Further, if we fail to meet the expectations of the public market in any given period, the market price of our common shares could decline, which could cause the value of our Series II First Preferred Shares to decline. We operate in a highly competitive environment that involves significant risks and uncertainties, some of which are outside of our control.

Risks Related to our Business and our Industry

We expect to incur future losses and we may never become profitable.

We have incurred losses of $12.9 million, $4.3 million and $1.1 million during 2014, 2013 and 2012, respectively, and expect to incur an operating loss in 2015. We have an accumulated deficit since inception through December 31, 2014 of $50.6 million. We believe that operating losses will continue in and beyond 2015 because we are planning to incur significant costs associated with the preclinical and clinical development of SIRPaFc. Our net losses have had and will continue to have an adverse effect on, among other things, our shareholders’ equity, total assets and working capital. We expect that losses will fluctuate from quarter to quarter and year to year, and that such fluctuations may be substantial. We cannot predict when we will become profitable, if at all.

We currently have no product revenue and will not be able to maintain our operations and research and development without additional funding.

To date, we have generated no product revenue and cannot predict when and if we will generate product revenue. Our ability to generate product revenue and ultimately become profitable depends upon our ability, alone or with partners, to successfully develop our product candidates, obtain regulatory approval and commercialize products, including any of our current product candidates, or other product candidates that we may develop, in-license or acquire in the future. We do not anticipate generating revenue from the sale of products for the foreseeable future. We expect our research and development expenses to increase substantially in connection with our ongoing activities, particularly as we advance our product candidates into clinical trials.

Our prospects depend on the success of our product candidates, which are at early stages of development, and we may not generate revenue for several years, if at all, from these products.

Given the early stage of our product development, we can make no assurance that our research and development programs will result in regulatory approval or commercially viable products. To achieve profitable operations, we, alone or with others, must successfully develop, gain regulatory approval and market our future products. We currently have no products that have been approved by the U.S. Food and Drug Administration, or FDA, Health Canada, or HC, or any similar regulatory authority. To obtain regulatory approvals for our product candidates being developed and to achieve commercial success, clinical trials must demonstrate that the product candidates are safe for human use and that they demonstrate efficacy. While SIRPaFc has begun preclinical studies to support an IND application, we have not yet completed cGMP manufacturing, formal toxicology studies, a phase I clinical trial or subsequent required clinical trials. Our CD200 program is ready to enter formal IND-enabling preclinical studies, but we do not plan to initiate these studies until we have a development partner to share in the cost and responsibility of the program.

Many product candidates never reach the stage of clinical testing and even those that do have only a small chance of successfully completing clinical development and gaining regulatory approval. Product candidates may fail for

9

Table of Contents

a number of reasons, including, but not limited to, being unsafe for human use or due to the failure to provide therapeutic benefits equal to or better than the standard of treatment at the time of testing. Unsatisfactory results obtained from a particular study relating to a research and development program may cause us or our collaborators to abandon commitments to that program. Positive results of early preclinical research may not be indicative of the results that will be obtained in later stages of preclinical or clinical research. Similarly, positive results from early- stage clinical trials may not be indicative of favorable outcomes in later-stage clinical trials. We can make no assurance that any future studies, if undertaken, will yield favorable results. We can make no assurances that toxicology studies in non-human primates will yield results that will allow us to proceed with clinical trials in humans.

The early stage of our product development makes it particularly uncertain whether any of our product development efforts will prove to be successful and meet applicable regulatory requirements, and whether any of our product candidates will receive the requisite regulatory approvals, be capable of being manufactured at a reasonable cost or be successfully marketed. If successful in developing our current and future product candidates into approved products, we will still experience many potential obstacles such as the need to develop or obtain manufacturing, marketing and distribution capabilities. If we are unable to successfully commercialize any of our products, our financial condition and results of operations may be materially and adversely affected.

We rely and will continue to rely on third parties to plan, conduct and monitor our preclinical studies and clinical trials, and their failure to perform as required could cause substantial harm to our business.

We rely and will continue to rely on third parties to conduct a significant portion of our preclinical and clinical development activities. Preclinical activities include in vivo studies providing access to specific disease models, pharmacology and toxicology studies, and assay development. Clinical development activities include trial design, regulatory submissions, clinical patient recruitment, clinical trial monitoring, clinical data management and analysis, safety monitoring and project management. If there is any dispute or disruption in our relationship with third parties, or if they are unable to provide quality services in a timely manner and at a feasible cost, our active development programs will face delays. Further, if any of these third parties fails to perform as we expect or if their work fails to meet regulatory requirements, our testing could be delayed, cancelled or rendered ineffective.

We rely on contract manufacturers over whom we have limited control. If we are subject to quality, cost or delivery issues with the preclinical and clinical grade materials supplied by contract manufacturers, our business operations could suffer significant harm.

We have limited manufacturing experience and rely on contract manufacturing organizations, or CMOs, to manufacture our product candidates for larger preclinical studies and clinical trials. We produce small quantities of our product candidates at bench scale in our laboratory facilities for use in smaller preclinical studies. We rely on CMOs for manufacturing, filling, packaging, storing and shipping of drug product in compliance with cGMP regulations applicable to our products. The FDA ensures the quality of drug products by carefully monitoring drug manufacturers’ compliance with cGMP regulations. The cGMP regulations for drugs contain minimum requirements for the methods, facilities and controls used in manufacturing, processing and packing of a drug product.

We have contracted with Catalent Pharma Solutions, LLC, or Catalent, for the manufacture of the SIRPaFc protein needed for our pre-IND toxicology and pharmacology studies and to supply drug product for our phase I clinical trial. The manufacture of recombinant proteins uses well established processes including a protein expression system. Catalent is producing SIRPaFc using their proprietary GPEx® expression system. We believe that Catalent has the capacity, the systems and the experience to supply SIRPaFc for our planned phase I clinical trial and we may consider using Catalent for manufacturing for later clinical trials. However, since the Catalent manufacturing facility where SIRPaFc is being produced was only recently established, it has not been inspected by the FDA. Any manufacturing failures or delays or compliance issues could cause delays in the completion of our preclinical studies of SIRPaFc, and delays in the submission or approval of our IND and the initiation of our phase I clinical trial.

10

Table of Contents

There can be no assurances that CMOs will be able to meet our timetable and requirements. We have not contracted with alternate suppliers in the event Catalent is unable to scale up production, or if Catalent otherwise experiences any other significant problems. If we are unable to arrange for alternative third-party manufacturing sources on commercially reasonable terms or in a timely manner, we may be delayed in the development of our product candidates. Further, contract manufacturers must operate in compliance with cGMP and failure to do so could result in, among other things, the disruption of product supplies. Our dependence upon third parties for the manufacture of our products may adversely affect our profit margins and our ability to develop and deliver products on a timely and competitive basis.

If clinical trials of our product candidates fail to demonstrate safety and efficacy to the satisfaction of regulatory authorities or do not otherwise produce positive results, we would incur additional costs or experience delays in completing, or ultimately be unable to complete, the development and commercialization of our product candidates.

Before obtaining marketing approval from regulatory authorities for the sale of our product candidates, we must conduct preclinical studies in animals and extensive clinical trials in humans to demonstrate the safety and efficacy of the product candidates. Clinical testing is expensive and difficult to design and implement, can take many years to complete and has uncertain outcomes. The outcome of preclinical studies and early clinical trials may not predict the success of later clinical trials, and interim results of a clinical trial do not necessarily predict final results. A number of companies in the pharmaceutical and biotechnology industries have suffered significant setbacks in advanced clinical trials due to lack of efficacy or unacceptable safety profiles, notwithstanding promising results in earlier trials. We do not know whether the clinical trials we may conduct will demonstrate adequate efficacy and safety to result in regulatory approval to market any of our product candidates in any jurisdiction. A product candidate may fail for safety or efficacy reasons at any stage of the testing process. A major risk we face is the possibility that none of our product candidates under development will successfully gain market approval from the FDA or other regulatory authorities, resulting in us being unable to derive any commercial revenue from them after investing significant amounts of capital in multiple stages of preclinical and clinical testing.

If we experience delays in clinical testing, we will be delayed in commercializing our product candidates, and our business may be substantially harmed.

We cannot predict whether any clinical trials will begin as planned, will need to be restructured or will be completed on schedule, or at all. Our product development costs will increase if we experience delays in clinical testing. Significant clinical trial delays could shorten any periods during which we may have the exclusive right to commercialize our product candidates or allow our competitors to bring products to market before us, which would impair our ability to successfully commercialize our product candidates and may harm our financial condition, results of operations and prospects. The commencement and completion of clinical trials for our products, including our planned SIRPaFc phase I clinical trial, may be delayed for a number of reasons, including delays related, but not limited, to:

| • | failure by regulatory authorities to grant permission to proceed or placing the clinical trial on hold; |

| • | patients failing to enroll or remain in our trials at the rate we expect; |

| • | suspension or termination of clinical trials by regulators for many reasons, including concerns about patient safety or failure of our contract manufacturers to comply with cGMP requirements; |

| • | any changes to our manufacturing process that may be necessary or desired; |

| • | delays or failure to obtain clinical supply from contract manufacturers of our products necessary to conduct clinical trials; |

| • | product candidates demonstrating a lack of safety or efficacy during clinical trials; |

| • | patients choosing an alternative treatment for the indications for which we are developing any of our product candidates or participating in competing clinical trials; |

| • | patients failing to complete clinical trials due to dissatisfaction with the treatment, side effects or other reasons; |

11

Table of Contents

| • | reports of clinical testing on similar technologies and products raising safety and/or efficacy concerns; |

| • | competing clinical trials and scheduling conflicts with participating clinicians; |

| • | clinical investigators not performing our clinical trials on their anticipated schedule, dropping out of a trial, or employing methods not consistent with the clinical trial protocol, regulatory requirements or other third parties not performing data collection and analysis in a timely or accurate manner; |

| • | failure of our contract research organizations, or CROs, to satisfy their contractual duties or meet expected deadlines; |

| • | inspections of clinical trial sites by regulatory authorities or Institutional Review Boards, or IRBs, or ethics committees finding regulatory violations that require us to undertake corrective action, resulting in suspension or termination of one or more sites or the imposition of a clinical hold on the entire study; |

| • | one or more IRBs or ethics committees rejecting, suspending or terminating the study at an investigational site, precluding enrollment of additional subjects, or withdrawing its approval of the trial; or |

| • | failure to reach agreement on acceptable terms with prospective clinical trial sites. |

Our product development costs will increase if we experience delays in testing or approval or if we need to perform more or larger clinical trials than planned. Additionally, changes in regulatory requirements and policies may occur, and we may need to amend study protocols to reflect these changes. Amendments may require us to resubmit our study protocols to regulatory authorities or IRBs or ethics committees for re-examination, which may impact the cost, timing or successful completion of that trial. Delays or increased product development costs may have a material adverse effect on our business, financial condition and prospects.

If we have difficulty enrolling patients in clinical trials, the completion of the trials may be delayed or cancelled.

As our product candidates advance from preclinical testing to clinical testing, and then through progressively larger and more complex clinical trials, we will need to enroll an increasing number of patients that meet our eligibility criteria. There is significant competition for recruiting cancer patients in clinical trials, and we may be unable to enroll the patients we need to complete clinical trials on a timely basis or at all. The factors that affect our ability to enroll patients are largely uncontrollable and include, but are not limited to, the following:

| • | size and nature of the patient population; |

| • | eligibility and exclusion criteria for the trial; |

| • | design of the study protocol; |

| • | competition with other companies for clinical sites or patients; |

| • | the perceived risks and benefits of the product candidate under study; |

| • | the patient referral practices of physicians; and |

| • | the number, availability, location and accessibility of clinical trial sites. |

If we are unable to successfully develop companion diagnostics for our therapeutic product candidates, or experience significant delays in doing so, we may not achieve marketing approval or realize the full commercial potential of our therapeutic product candidates.

We plan to develop companion diagnostics for our therapeutic product candidates. We expect that, at least in some cases, regulatory authorities may require the development and regulatory approval of a companion diagnostic as a condition to approving our therapeutic product candidates. We have limited experience and capabilities in developing or commercializing diagnostics and plan to rely in large part on third parties to perform these functions. We do not currently have any agreement in place with any third party to develop or commercialize companion diagnostics for any of our therapeutic product candidates.

Companion diagnostics are subject to regulation by the FDA, HC and comparable foreign regulatory authorities as medical devices and may require separate regulatory approval or clearance prior to commercialization. If we,

12

Table of Contents

or any third parties that we engage to assist us, are unable to successfully develop companion diagnostics for our therapeutic product candidates, or experience delays in doing so, our business may be substantially harmed.

Regulatory approval processes are lengthy, expensive and inherently unpredictable. Our inability to obtain regulatory approval for our product candidates would substantially harm our business.

Our development and commercialization activities and product candidates are significantly regulated by a number of governmental entities, including the FDA, HC and by comparable authorities in other countries. Regulatory approvals are required prior to each clinical trial and we may fail to obtain the necessary approvals to commence or continue clinical testing. We must comply with regulations concerning the manufacture, testing, safety, effectiveness, labeling, documentation, advertising and sale of products and product candidates and ultimately must obtain regulatory approval before we can commercialize the product candidate. The time required to obtain approval by such regulatory authorities is unpredictable but typically takes many years following the commencement of preclinical studies and clinical trials. Any analysis of data from clinical activities we perform is subject to confirmation and interpretation by regulatory authorities, which could delay, limit or prevent regulatory approval. Even if we believe results from our clinical trials are favorable to support the marketing of our product candidates, the FDA or other regulatory authorities may disagree. In addition, approval policies, regulations, or the type and amount of clinical data necessary to gain approval may change during the course of a product candidate’s clinical development and may vary among jurisdictions. We have not obtained regulatory approval for any product candidate and it is possible that none of our existing product candidates or any future product candidates will ever obtain regulatory approval.

We could fail to receive regulatory approval for our product candidates for many reasons, including, but not limited to:

| • | disagreement with the design or implementation of our clinical trials; |

| • | failure to demonstrate that a product candidate is safe and effective for its proposed indication; |

| • | failure of clinical trials to meet the level of statistical significance required for approval; |

| • | failure to demonstrate that a product candidate’s clinical and other benefits outweigh its safety risks; |

| • | disagreement with our interpretation of data from preclinical studies or clinical trials; |

| • | the insufficiency of data collected from clinical trials of our product candidates to support the submission and filing of a biologics license application, or BLA, or other submission or to obtain regulatory approval; |

| • | deficiencies in the manufacturing processes or the failure of facilities of CMOs with whom we contract for clinical and commercial supplies to pass a pre-approval inspection; or |

| • | changes in the approval policies or regulations that render our preclinical and clinical data insufficient for approval. |

A regulatory authority may require more information, including additional preclinical or clinical data to support approval, which may delay or prevent approval and our commercialization plans, or we may decide to abandon the development program. If we were to obtain approval, regulatory authorities may approve any of our product candidates for fewer or more limited indications than we request, may grant approval contingent on the performance of costly post-marketing clinical trials, or may approve a product candidate with a label that does not include the labeling claims necessary or desirable for the successful commercialization of that product candidate. Moreover, depending on any safety issues associated with our product candidates that garner approval, the FDA may impose a risk evaluation and mitigation strategy, thereby imposing certain restrictions on the sale and marketability of such products.

We will require additional capital to finance our operations, which may not be available to us on acceptable terms, or at all. As a result, we may not complete the development and commercialization of our product candidates or develop new product candidates.

As a research and development company, our operations have consumed substantial amounts of cash since inception. We expect to spend substantial funds to continue the research, development and testing of our product

13

Table of Contents

candidates that are in the preclinical testing stages of development, and to prepare to commercialize products subject to FDA approval in the U.S. and similar approvals in other jurisdictions. We will also require significant additional funds if we expand the scope of our current clinical plans for the SIRPaFc program or if we were to acquire any new assets and advance those towards clinical testing. Therefore, for the foreseeable future, we will have to fund all of our operations and development expenditures from cash on hand, equity or debt financings, through collaborations with other biotechnology or pharmaceutical companies or through financings from other sources. We expect that our existing cash at December 31, 2014 of $26,165,056 will enable us to fund our current operating plan requirements into the fourth quarter of 2016. Additional financing will be required to meet our long term liquidity needs. If we do not succeed in raising additional funds on acceptable terms, we might not be able to complete planned preclinical studies and clinical trials or pursue and obtain approval of any product candidates from the FDA and other regulatory authorities. It is possible that future financing will not be available or, if available, may not be on favorable terms. The availability of financing will be affected by the achievement of our corporate goals, the results of scientific and clinical research, the ability to obtain regulatory approvals, the state of the capital markets generally and with particular reference to drug development companies, the status of strategic alliance agreements and other relevant commercial considerations. If adequate funding is not available, we may be required to delay, reduce or eliminate one or more of our product development programs, or obtain funds through corporate partners or others who may require us to relinquish significant rights to product candidates or obtain funds on less favorable terms than we would otherwise accept. To the extent that external sources of capital become limited or unavailable or available on onerous terms, our intangible assets and our ability to continue our clinical development plans may become impaired, and our assets, liabilities, business, financial condition and results of operations may be materially or adversely affected.

We face competition from other biotechnology and pharmaceutical companies and our financial condition and operations will suffer if we fail to effectively compete.

The biotechnology and pharmaceutical industries are intensely competitive and subject to rapid and significant technological change. Our competitors include large, well-established pharmaceutical companies, biotechnology companies, and academic and research institutions developing cancer therapeutics for the same indications we are targeting and competitors with existing marketed therapies. Many other companies are developing or commercializing therapies to treat the same diseases or indications for which our product candidates may be useful. Although there are no approved therapies that specifically target the CD47 pathway, some competitors use therapeutic approaches that may compete directly with our product candidates. For example, SIRPaFc is in direct competition with CD47 blocking antibodies from Stanford University, Celgene Corporation and Novimmune SA.

Many of our competitors have substantially greater financial, technical and human resources than we do and have significantly greater experience than us in conducting preclinical testing and human clinical trials of product candidates, scaling up manufacturing operations and obtaining regulatory approvals of products. Accordingly, our competitors may succeed in obtaining regulatory approval for products more rapidly than we do. Our ability to compete successfully will largely depend on:

| • | the efficacy and safety profile of our product candidates relative to marketed products and other product candidates in development; |

| • | our ability to develop and maintain a competitive position in the product categories and technologies on which we focus; |

| • | the time it takes for our product candidates to complete clinical development and receive marketing approval; |

| • | our ability to obtain required regulatory approvals; |

| • | our ability to commercialize any of our product candidates that receive regulatory approval; |

| • | our ability to establish, maintain and protect intellectual property rights related to our product candidates; and |

| • | acceptance of any of our product candidates that receive regulatory approval by physicians and other healthcare providers and payers. |

14

Table of Contents

If we are not able to compete effectively against our current and future competitors, our business will not grow and our financial condition and operations will substantially suffer.

We heavily rely on the capabilities and experience of our key executives and scientists and the loss of any of them could affect our ability to develop our products.

The loss of Dr. Niclas Stiernholm, our President and Chief Executive Officer, or other key members of our staff, including Dr. Robert Uger, our Chief Scientific Officer, James Parsons, our Chief Financial Officer, or Dr. Penka Petrova, our Vice President, Drug Development, could harm us. We have employment agreements with Drs. Stiernholm, Uger and Petrova and Mr. Parsons, although such employment agreements do not guarantee their retention. We also depend on our scientific and clinical collaborators and advisors, all of whom have outside commitments that may limit their availability to us. In addition, we believe that our future success will depend in large part upon our ability to attract and retain highly skilled scientific, managerial, medical, clinical and regulatory personnel, particularly as we expand our activities and seek regulatory approvals for clinical trials. We routinely enter into consulting agreements with our scientific and clinical collaborators and advisors, key opinion leaders and academic partners in the ordinary course of our business. We also enter into contractual agreements with physicians and institutions who will recruit patients into our clinical trials on our behalf in the ordinary course of our business. Notwithstanding these arrangements, we face significant competition for these types of personnel from other companies, research and academic institutions, government entities and other organizations. We cannot predict our success in hiring or retaining the personnel we require for continued growth. The loss of the services of any of our executive officers or other key personnel could potentially harm our business, operating results or financial condition.

Our employees may engage in misconduct or other improper activities, including noncompliance with regulatory standards and requirements, which could have a material adverse effect on our business.

We are exposed to the risk of employee fraud or other misconduct. Misconduct by employees could include failures to comply with FDA regulations, provide accurate information to the FDA, comply with manufacturing standards we have established, comply with federal and state health-care fraud and abuse laws and regulations, report financial information or data accurately or disclose unauthorized activities to us. In particular, sales, marketing and business arrangements in the healthcare industry are subject to extensive laws and regulations intended to prevent fraud, kickbacks, self-dealing and other abusive practices. These laws and regulations may restrict or prohibit a wide range of pricing, discounting, marketing and promotion, sales commission, customer incentive programs and other business arrangements. Employee misconduct could also involve the improper use of information obtained in the course of clinical trials, which could result in regulatory sanctions and serious harm to our reputation. If any such actions are instituted against us, and we are not successful in defending ourselves or asserting our rights, those actions could have a substantial impact on our business and results of operations, including the imposition of substantial fines or other sanctions.

We may expand our business through the acquisition of companies or businesses or by entering into collaborations or by in-licensing product candidates, each of which could disrupt our business and harm our financial condition.

We have in the past and may in the future seek to expand our pipeline and capabilities by acquiring one or more companies or businesses, entering into collaborations or in-licensing one or more product candidates. For example, in April 2013, we acquired Trillium Privateco to acquire novel cancer therapeutics, an experienced scientific management team and internal development capabilities. We licensed intellectual property relating to methods and compounds for the modulation of the SIRPa-CD47 interaction for therapeutic cancer applications from University Health Network, or UHN, and Hospital for Sick Children, or HSC. In April 2013, we also in-licensed tigecycline which was subsequently returned to the UHN in 2014. Acquisitions, collaborations and in-licenses involve numerous risks, including, but not limited to:

| • | substantial cash expenditures; |

15

Table of Contents

| • | technology development risks; |

| • | potentially dilutive issuances of equity securities; |

| • | incurrence of debt and contingent liabilities, some of which may be difficult or impossible to identify at the time of acquisition; |

| • | difficulties in assimilating the operations of the acquired companies; |

| • | potential disputes regarding contingent consideration; |

| • | diverting our management’s attention away from other business concerns; |

| • | entering markets in which we have limited or no direct experience; and |

| • | potential loss of our key employees or key employees of the acquired companies or businesses. |

We have experience in making acquisitions, entering collaborations and in-licensing product candidates, however, we cannot provide assurance that any acquisition, collaboration or in-license will result in short-term or long-term benefits to us. We may incorrectly judge the value or worth of an acquired company or business or in-licensed product candidate. In addition, our future success would depend in part on our ability to manage the rapid growth associated with some of these acquisitions, collaborations and in-licenses. We cannot assure you that we would be able to successfully combine our business with that of acquired businesses, manage a collaboration or integrate in-licensed product candidates. Furthermore, the development or expansion of our business may require a substantial capital investment by us.

Negative results from clinical trials or studies of others and adverse safety events involving the targets of our products may have an adverse impact on our future commercialization efforts.