UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-23011

PENN CAPITAL FUNDS TRUST

(Exact name of registrant as specified in charter)

Navy Yard Corporate Center

1200 Intrepid Ave., Suite 400

Philadelphia, Pennsylvania 19112

(Address of principal executive offices) (Zip code)

Richard A. Hocker

Navy Yard Corporate Center

1200 Intrepid Ave., Suite 400

Philadelphia, Pennsylvania 19112

(Name and address of agent for service)

With copies to:

Lisa L.B. Matson, Esq.

Navy Yard Corporate Center

1200 Intrepid Ave., Suite 400

Philadelphia, Pennsylvania 19112

Michael P. O’Hare, Esq.

Stradley Ronon Stevens & Young, LLP

2005 Market Street, Suite 2600

Philadelphia, Pennsylvania 19103

(215) 302-1500

Registrant's telephone number, including area code

Date of fiscal year end: June 30, 2018

Date of reporting period: June 30, 2018

Item 1. Reports to Stockholders.

![]()

ANNUAL REPORT

JUNE 30, 2018

PENN CAPITAL MANAGED ALPHA SMID CAP EQUITY FUND

PENN CAPITAL SPECIAL SITUATIONS SMALL CAP EQUITY FUND

PENN CAPITAL MULTI-CREDIT HIGH INCOME FUND

PENN CAPITAL DEFENSIVE FLOATING RATE INCOME FUND

PENN CAPITAL DEFENSIVE SHORT DURATION HIGH INCOME FUND

PENN CAPITAL FUNDS TRUST

PRESIDENT’S LETTER TO SHAREHOLDERS (UNAUDITED)

Dear Penn Capital Funds Shareholder:

As we approach the three-year anniversary of launching the PENN Capital Funds Trust, I would like to thank our shareholders for entrusting their investments with our firm. Our team remains committed to focusing our efforts on our shareholders, and we value your confidence in our vision.

Our investment strategies incorporate Penn Capital’s Complete Capital Structure Analysis®, an in-depth high yield and equity research philosophy used to identify a company’s optimal capital structure. Our investment professionals are capital structure generalists, meaning they are responsible for understanding the entire capital structure of the companies they follow. By following this philosophy, we believe that integrating credit and equity research allows us to construct a more comprehensive investment mosaic. Participating in both credit and equity markets, along with this integrated research process, provides Penn Capital’s investment team with what we believe is an informational advantage. Finding inefficiencies in the market has never been more challenging, but we remain committed to the pursuit of strong investment returns on behalf of our shareholders.

The current Penn Capital fund line-up embodies our investment philosophy and our research-driven process. We are excited to note that this year’s annual report includes the most recent addition to our fund family: the Penn Capital Defensive Short Duration High Income Fund (the “Short Duration Fund”), which launched in July 2017 and which seeks to provide a high level of current income through primarily investing in fixed income securities and senior floating rate loans that are rated below investment grade.

Finally, I am excited to share with you recent ventures by Penn Capital to expand our philanthropic endeavors and support diversity in the financial services industry. Through a partnership with Invest in Girls, Penn Capital’s PRIME Program is sponsoring a three-year financial literacy and investing curriculum for female high school students attending a school in the Philadelphia School District. The PRIME Program is also pleased to announce the first year of the PRIME Internship, which will further expand our commitment to community outreach and promoting gender and racial diversity by offering a summer Internship to a collegiate female majoring in business or finance.

The following pages review the current market environment and provides additional insight into our funds over the past year. Once again, I would like to thank you for your confidence in investing with us.

Overview

Looking ahead, we anticipate nominal Gross Domestic Product (GDP) growth should benefit the cyclical sectors where our equity strategies tend to favor. Smaller, domestically-focused companies should, in our view, benefit disproportionately from the recently enacted US tax policy and are poised to outperform the global large-cap companies, which could be negatively impacted by evolving trade policies. We expect a moderation of spreads to continue in the latter half of 2018 as the US economy absorbs measured Federal Reserve (Fed) interest rate increases. We believe commodities will continue to rebound over the next year as we anticipate that the supply and demand for both oil and natural gas will come into balance. Most of our equity strategies continue to underweight the defensive-oriented areas of their respective benchmarks that generally offer low earnings growth with high dividend payouts such as the Utilities, Consumer Staples, and Real Estate sectors. These sectors are more influenced by rising interest rates because of their increased cost of capital without the offset of growth in their earnings power. We expect that rising rates will also make dividend yields less attractive since yields tend to rise on more traditional fixed income products.

With solid recovery in both the employment and housing fronts, we believe the US economy will accelerate from last year’s moderate growth. As a result, we continue to be overweight our respective benchmarks in the Consumer Discretionary sector and believe the US consumer stands to benefit from these trends.

During the last fiscal year, economic numbers continued to impress with the Fed raising interest rates three times during the period, in-line with expectations. After a period of GDP growth during the first half of the fiscal year, the stock market began to experience a bout of volatility in 2018 as the reality of potential US tariff conflicts emerged. The current White House Administration continues to raise expectations for fiscal policies with a focus on higher domestic growth rates despite recent news at fiscal year-end regarding potential US tariff wars. With this in mind, we continue to stress the importance of asset allocation in a potentially higher growth and interest rate environment. Typically, high yield and smaller cap equity asset classes are more influenced by economic growth than by rising interest rates. As a manager of both below investment grade debt and smaller (micro, small, and small to mid) cap equities, we believe our funds could benefit in an environment of expanding GDP growth and government spending.

Spreads have compressed modestly during the fiscal year and we are still forecasting coupon-like bond market returns in 2018. In a low-rate world, we believe mid-single digit returns with relatively less duration risk still represent attractive value relative

1

PENN CAPITAL FUNDS TRUST

PRESIDENT’S LETTER TO SHAREHOLDERS (UNAUDITED)

to most other fixed income asset classes due to a defensive nature. To the extent that long-term interest rates rise in a growing economy, we believe larger-cap dividend paying equities and longer duration fixed income asset classes, including investment-grade corporates, may underperform. We continue to favor the senior floating rate bank loan asset class, especially for more conservative investors. Although bank loan returns have generally lagged bonds, we believe they provide an effective complement to bonds, particularly given their seniority and floating rate nature.

The following paragraphs provide more detailed information on the performance of our funds, as well as selected holdings.

Penn Capital Defensive Floating Rate Income Fund

For the fiscal year ended June 30, 2018, the Penn Capital Defensive Floating Rate Income Fund (formerly the Penn Capital Senior Floating Rate Income Fund) (the “Floating Rate Income Fund”) generated a 3.71% return versus 4.19% for its benchmark, S&P/LSTA Leveraged BB/B Loan Index. The three-month LIBOR rate rose 100 basis points during the fiscal year, providing a tailwind for bank loans compared with other fixed income asset classes. The Floating Rate Income Fund is managed with a conservative bias, prioritizing safety of principal over maximizing yield. To carry out this objective, the Floating Rate Income Fund excludes CCC-rated bank loans or second lien loans; both areas of the market are exposed to a higher degree of volatility and potential investment losses. With bank loans outperforming bonds during the fiscal year, the Floating Rate Income Fund’s high yield allocation, nearly 12% of Fund assets, was a modest detractor from performance. The Floating Rate Income Fund holds conservative short duration high yield bonds in an effort to enhance the Fund’s liquidity, as opposed to seeking higher yields and adding additional risk.

The Floating Rate Income Fund’s investments in Healthcare, Materials, and Transportation sectors made positive contributions to performance. However, the Fund’s exposure to Financial and Media sectors detracted from performance. Top single name contributors were Windstream and GIII Apparel. As of fiscal year-end, the Floating Rate Income Fund maintained its allocation in the Windstream term loan and had exited GIII Apparel on valuation concerns. Top single name detractors included PetSmart and Save-A-Lot. Both names triggered our sell discipline threshold and were sold from the Fund as of fiscal year-end.

We continue to be very selective in credit selection reflecting our belief that we are in the mid-to-late stages of the current credit cycle, and as we focus on risk-adjusted, rather than absolute, returns.

Penn Capital Defensive Short Duration High Income Fund

For the period beginning July 17, 2017 (inception) through June 30, 2018, the Penn Capital Defensive Short Duration High Income Fund (the “Short Duration Fund”) generated a 1.03% return versus 1.64% for its benchmark, the ICE BofAML1-3 Year BB-Rated US Cash Pay High Yield Index.

The Short Duration Fund benefitted from security selection within the Metals & Mining and Technology sectors. Technology benefitted as several high coupon bonds were tendered for refinancing, including Allegheny Technologies, Cleveland-Cliffs, and Western Digital. The Fund maintained an underweight position in the sector compared to its benchmark, which further strengthened performance. Within Energy, the Short Duration Fund benefitted from its security selection within the Distribution segment of that sector from improved fundamentals at PBF Holding Company and NGPL PipeCo. An overweight position compared to its benchmark in the Exploration & Production segment saw rising oil prices that also helped to contribute to the Fund’s performance. Security selection within Utilities added value as Dynegy refinanced debt and was then acquired by Vistra, a higher quality company. Weakness within the Media & Telecommunications sector was the primary detractor for the fiscal year, mainly in the first quarter of 2018, including DISH Network, Frontier, Windstream, CenturyLink, and Sprint. However, this underperformance was partially offset by a benchmark overweight to the Aerospace & Defense sector.

During the fiscal year, LIBOR rose over 100 basis points and loan coupons began to rise. During the period, the Short Duration Fund held an average weighting of 10% in bank loans (through its investment in the Penn Capital Defensive Floating Rate Income Fund). The position contributed positively to the Short Duration Fund’s performance and was gradually increased throughout the period to end the fiscal year representing approximately 15% of the Fund’s assets.

We continue to believe that a complementary allocation to bank loans is prudent given today’s rising interest rate environment.

Penn Capital Multi-Credit High Income Fund

For the fiscal year ended June 30, 2018, the Penn Capital Multi-Credit High Income Fund (formerly the Penn Capital Opportunistic High Yield Fund) (the “High Income Fund”) generated a 3.81% return, outperforming the 2.52% return of its

2

PENN CAPITAL FUNDS TRUST

PRESIDENT’S LETTER TO SHAREHOLDERS (UNAUDITED)

benchmark, the ICE BofAML US High Yield Constrained Index. The High Income Fund increased its bank loan exposure to approximately 26% of its assets at period end, a shift that proved beneficial as loans outperformed bonds during the fiscal year. With LIBOR rising 100 basis points over the past year, we believe the bias towards floating rate bank loans will likely increase the Fund’s allocation within this segment of the market.

Over the last twelve (12) months, Transportation and Metals & Mining sectors were the largest positive contributors to performance as a combination of credit specific developments, strong industry fundamentals, and recovering commodity prices aided these sectors. The Fund also benefitted from strong security selection within Energy, specifically in the Exploration & Production segment of the market. The Fund’s investment in VistaJet, a private aviation company, benefitted from a large capital injection provided by a European private equity sponsor. News of this capitalization event relieved market uncertainty concerning their ability to address a 2020 bond maturity (as of fiscal year-end, the Fund maintained its holding in VistaJet bonds). The Fund also benefitted from an overweight investment position compared to its benchmark in Valeant Pharmaceuticals as those bonds outperformed due to a successful tender offer and refinancing transaction that allowed for additional operating capital. As of fiscal year-end, the Fund maintained this overweight position to the Valeant Pharmaceuticals complex. Financial Services and Telecommunication sectors contributed the greatest share of negative performance during the fiscal period. PetroQuest, a distressed natural gas producer, underwent an out-of-court restructuring detracted from performance as the Fund exited this position by the conclusion of the fiscal period. Performance was also negatively impacted by DISH Network, a satellite TV company. However, we believe this company controls a highly valuable strategic asset in its ownership of Spectrum, a cable service provider, and we retain our conviction in this investment.

Penn Capital Managed Alpha SMID Cap Equity Fund

For the fiscal year ended June 30, 2018, the Penn Capital Managed Alpha SMID Cap Equity Fund (formerly the Penn Capital Small/Mid Cap Equity Fund) (the “Managed Alpha SMID Fund”) generated a 17.41% return outperforming the 16.24% returns of its benchmark, the Russell 2500™ Index. At the sector level, Consumer Discretionary, Information Technology, and Industrials contributed positively to performance driven by favorable bottom-up stock selection. In the Consumer Discretionary sector, Roku, Inc., a streaming video player manufacturer, performed well as an increased number of users viewed more hours on Roku’s over-the-top platform. Building product companies also benefitted as a solid housing market lead to new home starts and increased investments in renovations. Within Technology, consumer focused software companies performed well as their user base expanded while increasing average revenue per user. In the Industrials sector, transportation stocks strengthened as freight pricing increased as new regulations pressured industry capacity.

The Healthcare, Materials, and Energy sectors hindered relative performance in the Managed Alpha SMID Fund. In Healthcare, Acadia Healthcare struggled to integrate their United Kingdom-based acquisition due to local market challenges. Pharmaceutical companies, such as Pacira Pharmaceuticals, struggled to realize pricing and procedure volume growth, while managed care companies focused on cost containment. Materials companies, such as Commercial Metals Company and Berry Global Group, suffered margin pressures as higher energy prices increased input costs, reduced margins, and required higher levels of working capital. Energy services companies experienced increased activity, but demand fell short in an effort to raise prices in line with expectations.

Penn Capital Special Situations Small Cap Equity Fund

For the fiscal year ended June 30, 2018 the Penn Capital Special Situations Small Cap Equity Fund (formerly the Penn Capital Small Cap Equity Fund) (the “Special Situations Fund”) generated a 20.31% return outperforming the 17.57% return of its benchmark, the Russell 2000® Index. At the sector level, Utilities, Real Estate and Financials contributed positively to performance driven by favorable bottom-up stock selection. In the Utilities space, Dynegy was acquired by Vistra Energy for a sizeable premium, which bested the Index by a considerable margin. Real Estate was the weakest sector in an otherwise strong environment, as the Fund’s overall underweight to the group compared to its benchmark was rewarded. Pebblebrook Hotel Trust is a lone position in the space and benefited from an uptick in corporate group and leisure travel. In Financials, higher rate expectations propelled the sector broadly with both banks and financial services firms benefitting. As a result, Hamilton Lane and PJT Partners experienced strong performance.

The Healthcare, Materials, and Energy sectors hindered relative performance during the period. In Healthcare, Acadia Healthcare struggled to integrate their United Kingdom- based acquisition due to local market challenges. Within the Healthcare sector, companies such as NuVasive, Inc. struggled to realize pricing and procedure volume growth as managed care companies focused on cost containment. In Materials, the Fund suffered margin pressures from Venator Materials and Cleveland-Cliffs, Inc.

3

PENN CAPITAL FUNDS TRUST

PRESIDENT’S LETTER TO SHAREHOLDERS (UNAUDITED)

as higher energy prices reduced margins and required higher levels of working capital. Energy services companies experienced increased activity, but demand fell short in an effort to raise prices in line with expectations. Despite the positive commodity backdrop, Sanchez Energy, an exploration and production company, struggled operationally with an acquired asset which offset the positive effects of higher oil prices.

Looking Forward

This report contains Fund performance data and financial information. Please keep in mind that all securities markets, as well as mutual fund prices, fluctuate in value. If you would like more frequent updates, http://www.penncapitalfunds.com provides daily NAV, monthly performance figures, portfolio holdings, and other valuable information. We encourage you to visit penncapitalfunds.com, through which you may access your account, buy and sell shares, and find other helpful tools.

At Penn Capital Funds, we believe that active management continues to serve as a critical element of investing in high yield debt securities and equity securities of smaller companies. Although challenges remain, and markets may continue to be uneven, we are confident that investors with a well-diversified portfolio and a patient, long-term outlook should be well positioned for the years ahead.

We thank you for investing with us and look forward to continuing to serve your investment needs.

Sincerely,

Richard A. Hocker

Chairman & President

PENN Capital Funds Trust

This letter reflects Penn Capital’s analysis and opinions as of the most recent fiscal year-end. The information is not a complete analysis of any market, country, industry, security, or fund and should not be considered as a recommendation to buy, sell or hold any specific security or securities.

All investments involve risk, including possible loss of principal, and there is no guarantee the Funds will achieve their investment objectives. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. Investments in ETFs are subject to the same risks as the underlying securities in which the ETF invests as well as entails higher expenses than if invested into the underlying ETF directly. Investments in foreign securities and ADRs involve certain risks such as currency volatility, political and social instability and reduced market liquidity. As interest rates rise the value of bond prices will decline. Credit risk refers to the loss in the value of a security based on a default in the payment of principle and/or interest of the security, or the perception of the market of such default. High-yield bonds have a higher risk of default or other adverse credit events, but have the potential to pay higher earnings over investment grade bonds. The value of convertible securities tends to decline as interest rates rise and, because of the conversion feature, tends to vary with fluctuations in the market value of the underlying securities. Bank loans in which the Fund may invest have similar risks to below investment grade fixed income securities. In the event of the insolvency of an agent bank, a loan could be subject to settlement risk as well as the risk of interruptions in the administrative duties performed in the day to day administration of the loan.

Index Definitions

The ICE BofAML US High Yield Constrained Index contains all securities in the ICE BofAML US High Yield Index but caps issuer exposure at 2%.

The ICE BofAML 1-3 Year BB US Cash Pay High Yield Index is a subset of the ICE BofAML US Cash Pay High Yield Index, which tracks the performance of non-investment-grade corporate bonds with a remaining term to final maturity less than three years and rated BB.

4

PENN CAPITAL FUNDS TRUST

PRESIDENT’S LETTER TO SHAREHOLDERS (UNAUDITED)

The S&P/LSTA Leveraged BB/B Loan Index is a market value-weighted index designed to measure the performance of the US leveraged loan market and is comprised of loans whose rating is BB+, BB, BB-, B+, B or B-. Standard & Poor’s Rating Services is used to determine membership within this sub-index.

The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 Index is constructed to provide a comprehensive and unbiased small-cap opportunity barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set.

The Russell 2500™ Index is composed of the bottom 500 stocks in the Russell 1000® Index and all the stocks in the Russell 2000® Index. The Russell 2500™ Index return reflect adjustments for income dividends and capital gains distributions reinvested as of the ex-dividend dates.

5

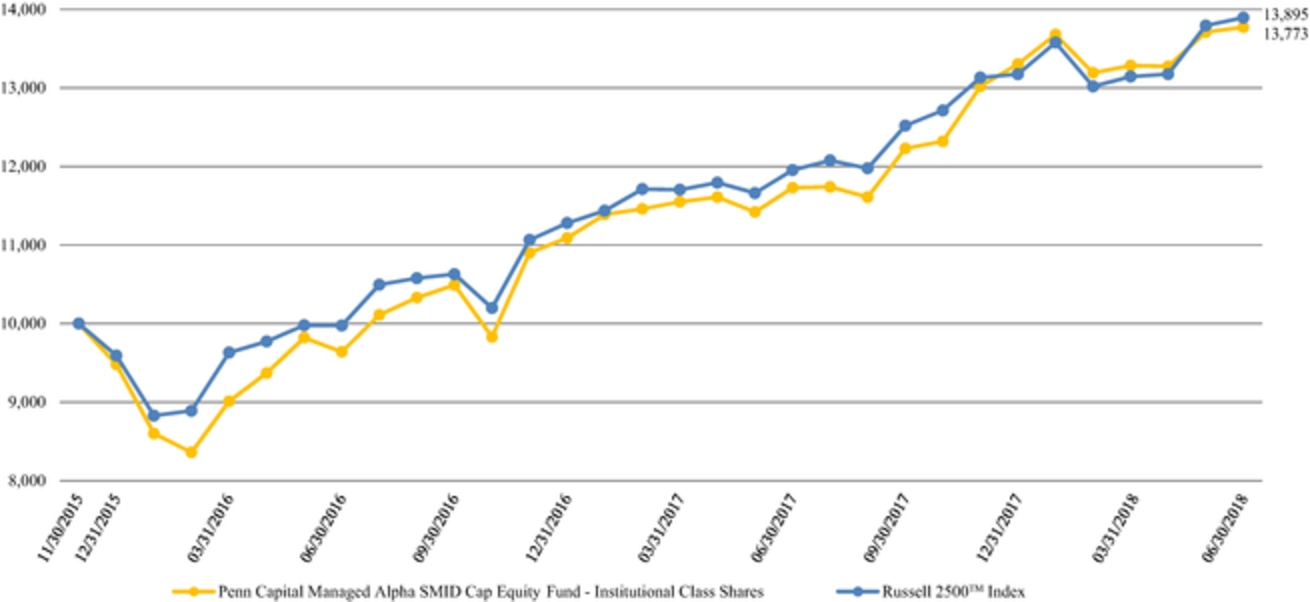

PENN CAPITAL MANAGED ALPHA SMID CAP EQUITY FUND

FUND SUMMARY (UNAUDITED)

This chart assumes an initial gross investment of $10,000 made on December 1, 2015, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index. No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018.

Average Annual Total Returns for the Year Ended June 30, 2018 | One Year | Since Inception(1) | ||||

Penn Capital Managed Alpha SMID Cap Equity Fund | ||||||

Institutional Class Shares | 17.41 | % | 13.19 | % | ||

Russell 2500™ Index | 16.24 | % | 13.58 | %(2) | ||

| (1) | Inception date is 12/1/15. |

| (2) | The return shown for the Russell 2500™ Index is from the inception date of the Institutional Class shares. |

6

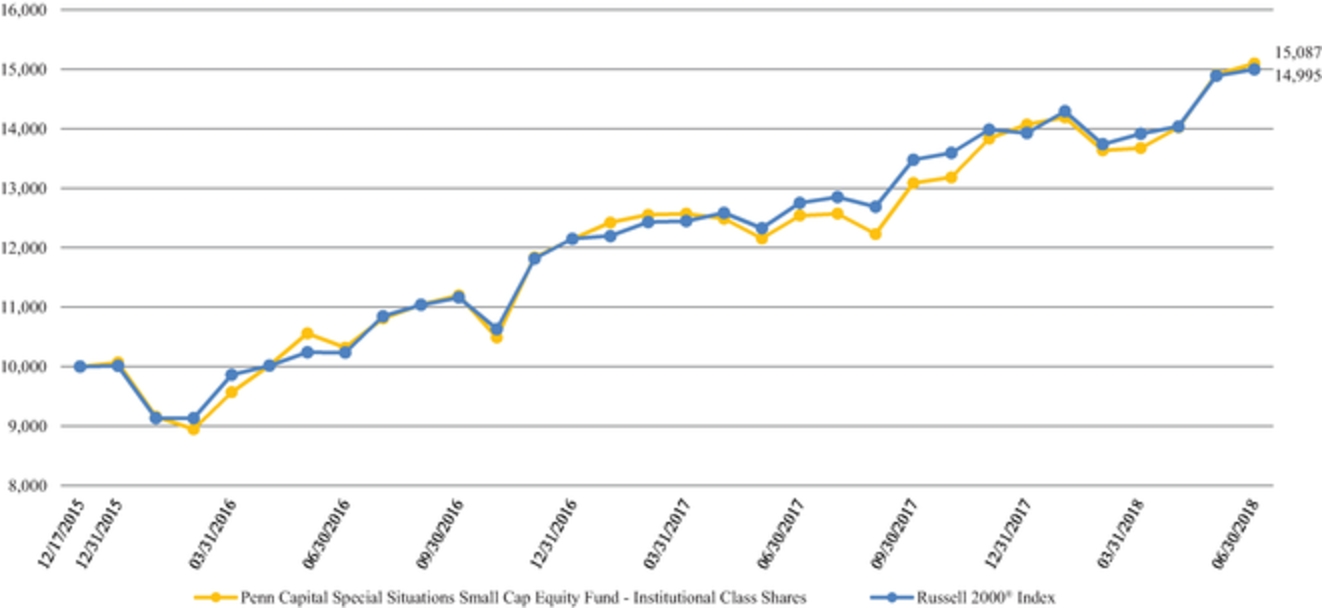

PENN CAPITAL SPECIAL SITUATIONS SMALL CAP EQUITY FUND

FUND SUMMARY (UNAUDITED)

This chart assumes an initial gross investment of $10,000 made on December 18, 2015, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index. No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018.

Average Annual Total Returns for the Year Ended June 30, 2018 | One Year | Since Inception(1) | ||||

Penn Capital Special Situations Small Cap Equity Fund | ||||||

Institutional Class Shares | 20.31 | % | 17.60 | % | ||

Russell 2000® Index | 17.57 | % | 17.31 | %(2) | ||

| (1) | Inception date is 12/18/15. |

| (2) | The return shown for the Russell 2000® Index is from the inception date of the Institutional Class shares. |

7

PENN CAPITAL MULTI-CREDIT HIGH INCOME FUND

FUND SUMMARY (UNAUDITED)

This chart assumes an initial gross investment of $10,000 made on December 1, 2015, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index. No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018.

Average Annual Total Returns for the Year Ended June 30, 2018 | One Year | Since Inception(1) | ||||

Penn Capital Multi-Credit High Income Fund | ||||||

Institutional Class Shares | 3.81 | % | 7.59 | % | ||

ICE BofAML US High Yield Constrained Index | 2.52 | % | 8.38 | %(2) | ||

| (1) | Inception date is 12/1/15. |

| (2) | The return shown for the ICE BofAML US High Yield Constrained Index is from the inception date of the Institutional Class shares. |

8

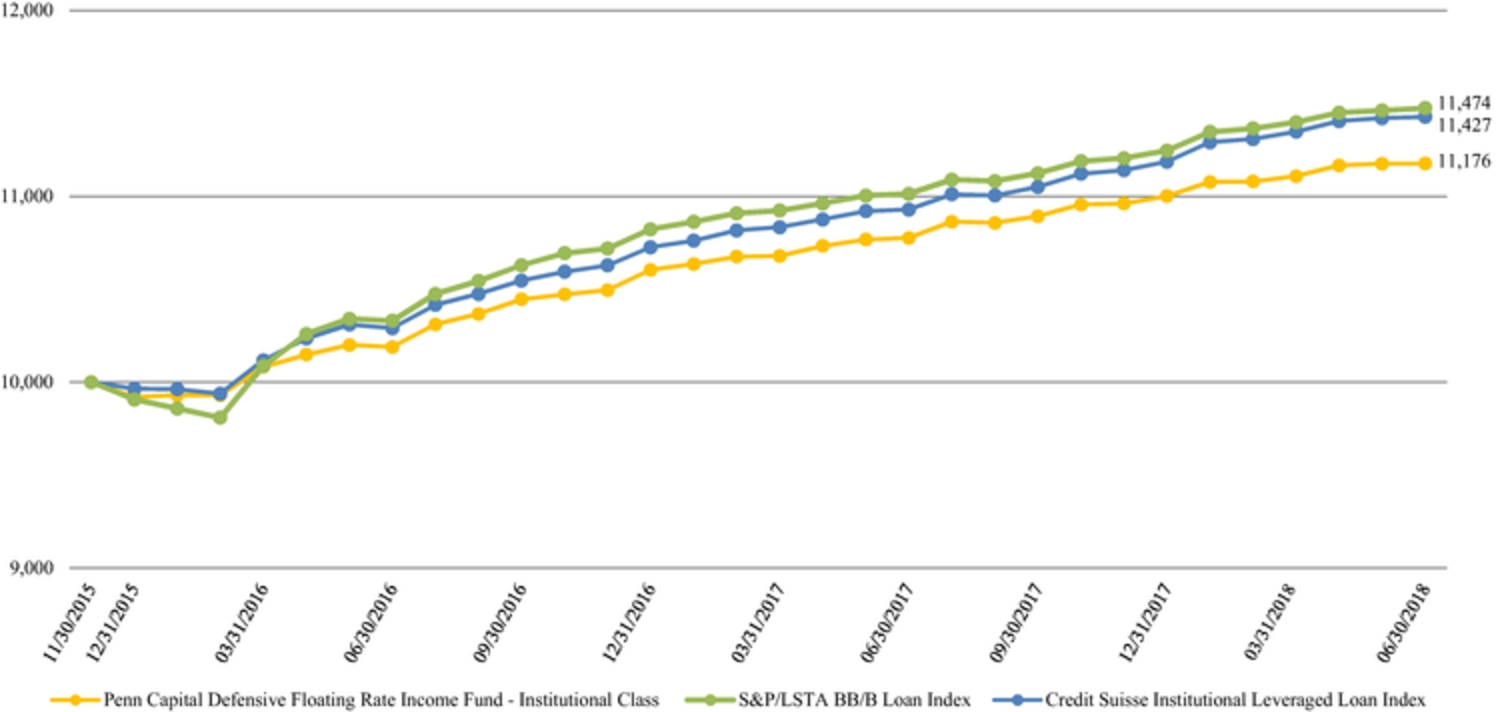

PENN CAPITAL DEFENSIVE FLOATING RATE INCOME FUND

FUND SUMMARY (UNAUDITED)

This chart assumes an initial gross investment of $10,000 made on December 1, 2015, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index. No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018.

Average Annual Total Returns for the Year Ended June 30, 2018 | One Year | Since Inception(1) | ||||

Penn Capital Defensive Floating Rate Income Fund | ||||||

Institutional Class Shares | 3.71 | % | 4.40 | % | ||

S&P/LSTA BB/B Loan Index(2) | 4.19 | % | 5.47 | %(3) | ||

Credit Suisse Institutional Leveraged Loan Index | 4.56 | % | 5.31 | %(4) | ||

| (1) | Inception date is 12/1/15. |

| (2) | The S&P/LSTA BB/B Loan Index has replaced the Credit Suisse Institutional Leveraged Loan Index as the Fund’s primary benchmark. Penn Capital Management Company, Inc. believes that the new index is more appropriate given the Fund’s holdings. |

| (3) | The return shown for the S&P/LSTA BB/B Loan Index is from the inception date of the Institutional Class shares. |

| (4) | The return shown for the Credit Suisse Institutional Leveraged Loan Index is from the inception date of the Institutional Class shares. |

9

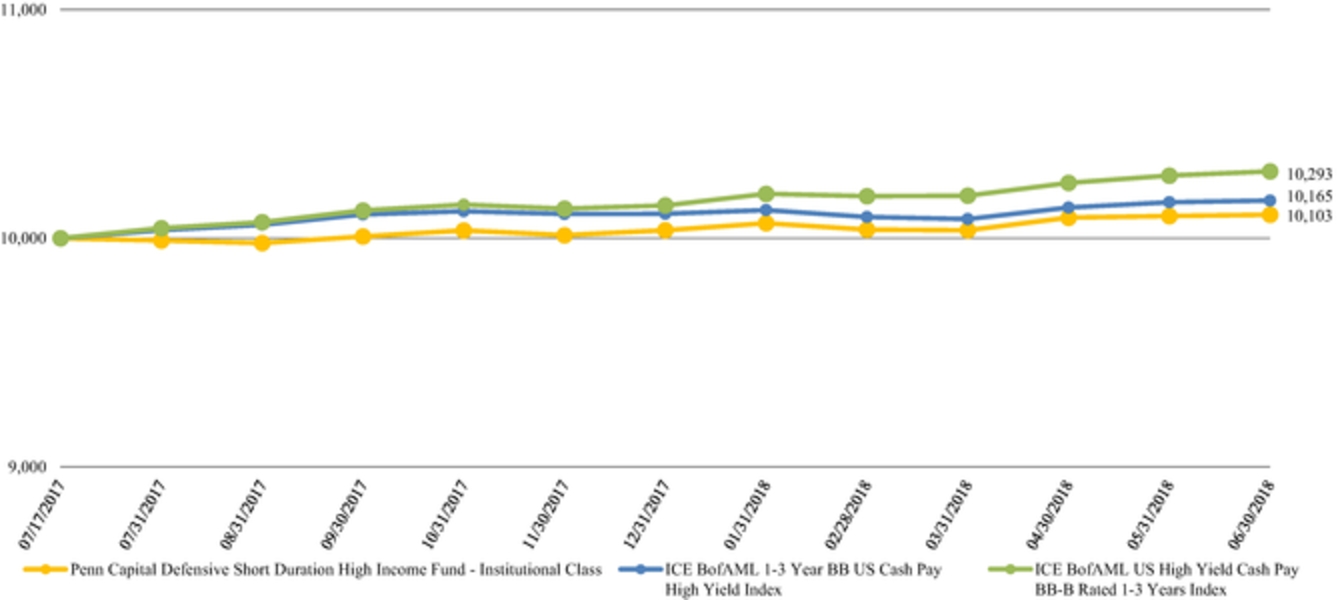

PENN CAPITAL DEFENSIVE SHORT DURATION HIGH INCOME FUND

FUND SUMMARY (UNAUDITED)

This chart assumes an initial gross investment of $10,000 made on July 17, 2017, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index.

Total Returns for the Fiscal Period Ended June 30, 2018 | Since Inception(1) | ||

Penn Capital Defensive Short Duration High Income Fund | |||

Institutional Class Shares | 1.03 | % | |

ICE BofAML 1-3 Year BB US Cash Pay High Yield Index | 1.64 | %(2) | |

ICE BofAML US High Yield Cash Pay BB-B Rated 1-3 Years Index | 2.91 | %(3) | |

| (1) | Inception date is 7/17/17. |

| (2) | The return shown for the ICE BofAML 1-3 Year BB US Cash Pay High Yield Index is from the inception date of the Institutional Class shares. |

| (3) | The return shown for the ICE BofAML US High Yield Cash Pay BB-B Rated 1-3 Years Index is from the inception date of the Institutional Class shares. |

10

PENN CAPITAL FUNDS TRUST

DISCLOSURE OF FUND EXPENSES (UNAUDITED)

FOR THE SIX MONTH PERIOD FROM JANUARY 1, 2018 TO JUNE 30, 2018

Cost in Dollars of a $1,000 Investment in Penn Capital Managed Alpha SMID Cap Equity Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from January 1, 2018 to June 30, 2018, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including redemption fees on sales (as applicable) and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from January 1, 2018 to June 30, 2018.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended June 30, 2018. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled Expenses Paid During Period to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Actual | Hypothetical | ||||||||||||||

Share Class1 | Beginning Account Value 1/1/18 | Ending Account Value (Based on Actual Returns and Expenses) 6/30/18 | Expenses Paid During Period2 | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 6/30/18 | Expenses Paid During Period2 | ||||||||||

Institutional Class Shares | $ | 1,000.00 | $ | 1,035.10 | $ | 5.35 | $ | 1,019.54 | $ | 5.31 | |||||

| 1. | No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018. |

| 2. | Expenses are equal to the Fund’s annualized expense ratio, net of waivers and excluding acquired fund fees and expenses if any (1.06% for the Institutional Class), multiplied by the average account value over the period, divided by 365 and multiplied by 181 for the Institutional Class (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

11

PENN CAPITAL FUNDS TRUST

DISCLOSURE OF FUND EXPENSES (UNAUDITED)

FOR THE SIX MONTH PERIOD FROM JANUARY 1, 2018 TO JUNE 30, 2018

Cost in Dollars of a $1,000 Investment in Penn Capital Special Situations Small Cap Equity Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from January 1, 2018 to June 30, 2018, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including redemption fees on sales (as applicable) and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from January 1, 2018 to June 30, 2018.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended June 30, 2018. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled Expenses Paid During Period to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Actual | Hypothetical | ||||||||||||||

Share Class1 | Beginning Account Value 1/1/18 | Ending Account Value (Based on Actual Returns and Expenses) 6/30/18 | Expenses Paid During Period2 | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 6/30/18 | Expenses Paid During Period2 | ||||||||||

Institutional Class Shares | $ | 1,000.00 | $ | 1,072.40 | $ | 5.60 | $ | 1,019.39 | $ | 5.46 | |||||

| 1. | No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018. |

| 2. | Expenses are equal to the Fund’s annualized expense ratio, net of waivers and excluding acquired fund fees and expenses if any (1.09% for the Institutional Class), multiplied by the average account value over the period, divided by 365 and multiplied by 181 for the Institutional Class (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

12

PENN CAPITAL FUNDS TRUST

DISCLOSURE OF FUND EXPENSES (UNAUDITED)

FOR THE SIX MONTH PERIOD FROM JANUARY 1, 2018 TO JUNE 30, 2018

Cost in Dollars of a $1,000 Investment in Penn Capital Multi-Credit High Income Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from January 1, 2018 to June 30, 2018, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including redemption fees on sales (as applicable) and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from January 1, 2018 to June 30, 2018.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended June 30, 2018. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled Expenses Paid During Period to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Actual | Hypothetical | ||||||||||||||

Share Class1 | Beginning Account Value 1/1/18 | Ending Account Value (Based on Actual Returns and Expenses) 6/30/18 | Expenses Paid During Period2 | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 6/30/18 | Expenses Paid During Period2 | ||||||||||

Institutional Class Shares | $ | 1,000.00 | $ | 1,010.50 | $ | 3.59 | $ | 1,021.22 | $ | 3.61 | |||||

| 1. | No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018. |

| 2. | Expenses are equal to the Fund’s annualized expense ratio, net of waivers and excluding acquired fund fees and expenses if any (0.72% for the Institutional Class), multiplied by the average account value over the period, divided by 365 and multiplied by 181 for the Institutional Class (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

13

PENN CAPITAL FUNDS TRUST

DISCLOSURE OF FUND EXPENSES (UNAUDITED)

FOR THE SIX MONTH PERIOD FROM JANUARY 1, 2018 TO JUNE 30, 2018

Cost in Dollars of a $1,000 Investment in Penn Capital Defensive Floating Rate Income Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from January 1, 2018 to June 30, 2018, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including redemption fees on sales (as applicable) and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from January 1, 2018 to June 30, 2018.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended June 30, 2018. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled Expenses Paid During Period to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Actual | Hypothetical | ||||||||||||||

Share Class1 | Beginning Account Value 1/1/18 | Ending Account Value (Based on Actual Returns and Expenses) 6/30/18 | Expenses Paid During Period2 | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 6/30/18 | Expenses Paid During Period2 | ||||||||||

Institutional Class Shares | $ | 1,000.00 | $ | 1,015.80 | $ | 3.20 | $ | 1,021.62 | $ | 3.21 | |||||

| 1. | No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018. |

| 2. | Expenses are equal to the Fund’s annualized expense ratio, net of waivers and excluding acquired fund fees and expenses if any (0.64% for the Institutional Class), multiplied by the average account value over the period, divided by 365 and multiplied by 181 for the Institutional Class (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

14

PENN CAPITAL FUNDS TRUST

DISCLOSURE OF FUND EXPENSES (UNAUDITED)

FOR THE PERIOD FROM JANUARY 1, 2018 TO JUNE 30, 2018

Cost in Dollars of a $1,000 Investment in Penn Capital Defensive Short Duration High Income Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from January 1, 2018 to June 30, 2018, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including redemption fees on sales (as applicable) and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from January 1, 2018 to June 30, 2018.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the period ended June 30, 2018. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled Expenses Paid During Period to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Actual | Hypothetical | ||||||||||||||

Share Class | Beginning Account Value 1/1/18 | Ending Account Value (Based on Actual Returns and Expenses) 6/30/18 | Expenses Paid During Period1 | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 6/30/18 | Expenses Paid During Period1 | ||||||||||

Institutional Class Shares2 | $ | 1,000.00 | $ | 1,006.80 | $ | 2.69 | $ | 1,022.12 | $ | 2.71 | |||||

| 1. | No information is provided for Investor Class shares because shares of that class had not yet been issued as of June 30, 2018. |

| 2. | Expenses are equal to the Fund’s annualized expense ratio, net of waivers and excluding acquired fund fees and expenses if any (0.54% for the Institutional Class), multiplied by the average account value over the period, divided by 365 and multiplied by 181 for the Institutional Class (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

15

PENN CAPITAL FUNDS TRUST |

PENN CAPITAL MANAGED ALPHA SMID CAP EQUITY FUND |

SCHEDULE OF INVESTMENTS |

JUNE 30, 2018 |

Shares | Value | |||||

Common Stocks: 91.6% | ||||||

Air Freight & Logistics: 1.3% | ||||||

XPO Logistics, Inc. (a) | 2,011 | $ | 201,462 | |||

Banks: 9.6% | ||||||

BOK Financial Corp. | 2,635 | 247,716 | ||||

Chemical Financial Corp. | 4,167 | 231,977 | ||||

Pinnacle Financial Partners, Inc. | 3,186 | 195,461 | ||||

Sterling Bancorp | 10,243 | 240,711 | ||||

Webster Financial Corp. | 4,413 | 281,108 | ||||

Western Alliance Bancorp (a) | 4,105 | 232,384 | ||||

1,429,357 | ||||||

Biotechnology: 2.8% | ||||||

Exelixis, Inc. (a) | 8,382 | 180,381 | ||||

Ironwood Pharmaceuticals, Inc. (a) | 12,361 | 236,342 | ||||

416,723 | ||||||

Building Products: 1.3% | ||||||

Allegion PLC | 2,480 | 191,853 | ||||

Capital Markets: 1.4% | ||||||

Affiliated Managers Group, Inc. | 1,415 | 210,368 | ||||

Chemicals: 2.5% | ||||||

HB Fuller Co. | 4,146 | 222,557 | ||||

Valvoline, Inc. | 6,995 | 150,882 | ||||

373,439 | ||||||

Commercial Services & Supplies: 1.8% | ||||||

KAR Auction Services, Inc. | 4,800 | 263,040 | ||||

Construction Materials: 1.4% | ||||||

Summit Materials, Inc. - Class A (a) | 7,806 | 204,907 | ||||

Consumer Finance: 1.3% | ||||||

SLM Corp. (a) | 17,400 | 199,230 | ||||

Containers & Packaging: 1.2% | ||||||

Berry Global Group, Inc. (a) | 3,745 | 172,045 | ||||

Diversified Financial Services: 3.2% | ||||||

FNF Group | 5,482 | 206,233 | ||||

Voya Financial, Inc. | 5,713 | 268,511 | ||||

474,744 | ||||||

Electronic Equipment, Instruments & Components: 1.1% | ||||||

Mercury Systems, Inc. (a) | 4,398 | 167,388 | ||||

Energy Equipment & Services: 0.7% | ||||||

FTS International, Inc. (a) | 7,722 | 109,961 | ||||

Health Care Equipment & Supplies: 4.6% | ||||||

ICU Medical, Inc. (a) | 913 | 268,102 | ||||

Teleflex, Inc. | 784 | 210,277 | ||||

Wright Medical Group NV (a) | 7,965 | 206,771 | ||||

685,150 | ||||||

Health Care Providers & Services: 2.9% | ||||||

LHC Group, Inc. (a) | 1,437 | 122,993 | ||||

WellCare Health Plans, Inc. (a) | 1,234 | 303,860 | ||||

426,853 | ||||||

Shares | Value | |||||

Hotels, Restaurants & Leisure: 5.1% | ||||||

Boyd Gaming Corp. | 7,160 | 248,166 | ||||

Red Rock Resorts, Inc. - Class A | 7,392 | 247,632 | ||||

Vail Resorts, Inc. | 983 | 269,529 | ||||

765,327 | ||||||

Household Durables: 2.0% | ||||||

Roku, Inc. (a) | 3,573 | 152,281 | ||||

TopBuild Corp. (a) | 1,811 | 141,874 | ||||

294,155 | ||||||

Independent Power and Renewable Electricity Producers: 1.5% | ||||||

Ormat Technologies, Inc. | 4,150 | 220,739 | ||||

Insurance: 1.8% | ||||||

Arch Capital Group Ltd. (a) | 9,936 | 262,907 | ||||

Internet Software & Services: 6.4% | ||||||

Five9, Inc. (a) | 3,419 | 118,195 | ||||

GoDaddy, Inc. - Class A (a) | 4,519 | 319,041 | ||||

IAC/InterActiveCorp (a) | 1,284 | 195,797 | ||||

Match Group, Inc. (a) | 3,030 | 117,382 | ||||

MongoDB, Inc. (a) | 4,005 | 198,768 | ||||

949,183 | ||||||

IT Services: 1.6% | ||||||

Black Knight, Inc. (a) | 4,591 | 245,848 | ||||

Machinery: 2.9% | ||||||

Allison Transmission Holdings, Inc. | 4,407 | 178,439 | ||||

Oshkosh Corp. | 3,666 | 257,793 | ||||

436,232 | ||||||

Media: 5.4% | ||||||

Gray Television, Inc. (a) | 13,060 | 206,348 | ||||

Live Nation Entertainment, Inc. (a) | 6,252 | 303,660 | ||||

Nexstar Media Group, Inc. - Class A | 3,927 | 288,242 | ||||

798,250 | ||||||

Metals & Mining: 0.9% | ||||||

Commercial Metals Co. | 6,066 | 128,053 | ||||

Multiline Retail: 1.8% | ||||||

Burlington Stores, Inc. (a) | 1,784 | 268,546 | ||||

Oil, Gas & Consumable Fuels: 4.5% | ||||||

Arch Coal, Inc. - Class A | 1,262 | 98,979 | ||||

Cabot Oil & Gas Corp. | 7,796 | 185,545 | ||||

Callon Petroleum Co. (a) | 17,605 | 189,078 | ||||

Cimarex Energy Co. | 2,012 | 204,701 | ||||

678,303 | ||||||

Pharmaceuticals: 1.1% | ||||||

Pacira Pharmaceuticals, Inc. (a) | 5,088 | 163,070 | ||||

Professional Services: 2.4% | ||||||

TransUnion | 5,105 | 365,722 | ||||

Road & Rail: 1.7% | ||||||

Schneider National, Inc. - Class B | 9,165 | 252,129 | ||||

The Accompanying Notes are an Integral Part of these Financial Statements.

16

PENN CAPITAL FUNDS TRUST |

PENN CAPITAL MANAGED ALPHA SMID CAP EQUITY FUND |

SCHEDULE OF INVESTMENTS |

JUNE 30, 2018 |

Shares | Value | |||||

Semiconductors & Semiconductor Equipment: 5.4% | ||||||

Cavium, Inc. (a) | 1,873 | 162,015 | ||||

Semtech Corp. (a) | 2,726 | 128,258 | ||||

Silicon Laboratories, Inc. (a) | 2,559 | 254,876 | ||||

Teradyne, Inc. | 6,942 | 264,282 | ||||

809,431 | ||||||

Software: 3.0% | ||||||

Nice Ltd. - ADR (a) | 2,093 | 217,191 | ||||

Tyler Technologies, Inc. (a) | 1,031 | 228,985 | ||||

446,176 | ||||||

Specialty Retail: 2.8% | ||||||

Camping World Holdings, Inc. - Class A | 6,683 | 166,941 | ||||

Floor & Decor Holdings, Inc. - Class A (a) | 5,104 | 251,780 | ||||

TravelCenters of America LLC (a) | - | 2 | ||||

418,723 | ||||||

Trading Companies & Distributors: 2.9% | ||||||

United Rentals, Inc. (a) | 1,788 | 263,945 | ||||

WESCO International, Inc. (a) | 2,894 | 165,247 | ||||

429,192 | ||||||

Water Utilities: 1.3% | ||||||

Aqua America, Inc. | 5,461 | 192,118 | ||||

Total Common Stocks (cost $11,369,380) | 13,650,624 | |||||

Real Estate Investment Trusts (REITs): 6.3% | ||||||

CyrusOne, Inc. | 4,457 | 260,110 | ||||

Invitation Homes, Inc. | 10,262 | 236,642 | ||||

MGM Growth Properties LLC - Class A | 8,146 | 248,127 | ||||

The GEO Group, Inc. | 7,063 | 194,515 | ||||

Total REITS (cost $862,609) | 939,394 | |||||

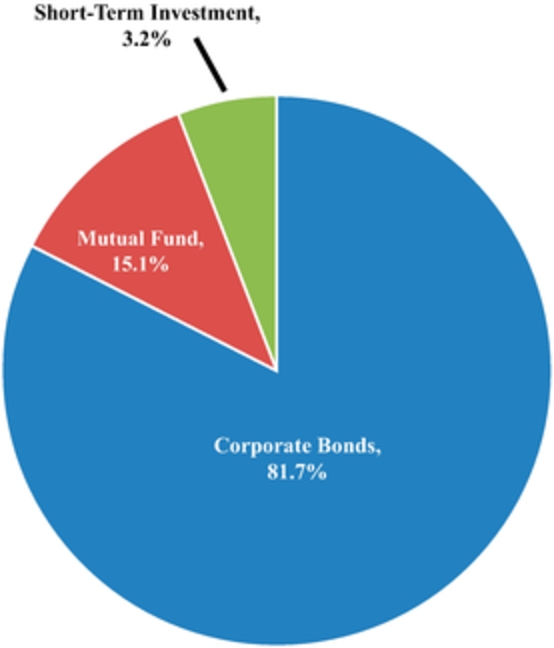

Short-Term Investment: 2.4% | ||||||

Short-Term Investment Trust Treasury Portfolio Institutional Class, 1.750% (b) | 362,429 | 362,429 | ||||

Total Short-Term Investment (cost $362,429) | 362,429 | |||||

Total Investments - 100.3% (cost $12,594,418) | 14,952,447 | |||||

Liabilities in Excess of Other Assets (0.3)% | (42,264 | ) | ||||

Net Assets: 100.0% | $ | 14,910,183 | ||||

Percentages are stated as a percent of net assets.

| (a) | No distribution or dividend was made during the year ending June 30, 2018. As such, it is classified as a non-income producing security as of June 30, 2018. |

| (b) | Rate reported is the 7-day effective yield as of June 30, 2018. |

Country Exposure (as a percentage of total investments) (Unaudited) | |||

United States | 94.13 | % | |

Bermuda | 1.76 | % | |

Israel | 1.45 | % | |

Netherlands | 1.38 | % | |

Ireland | 1.28 | % | |

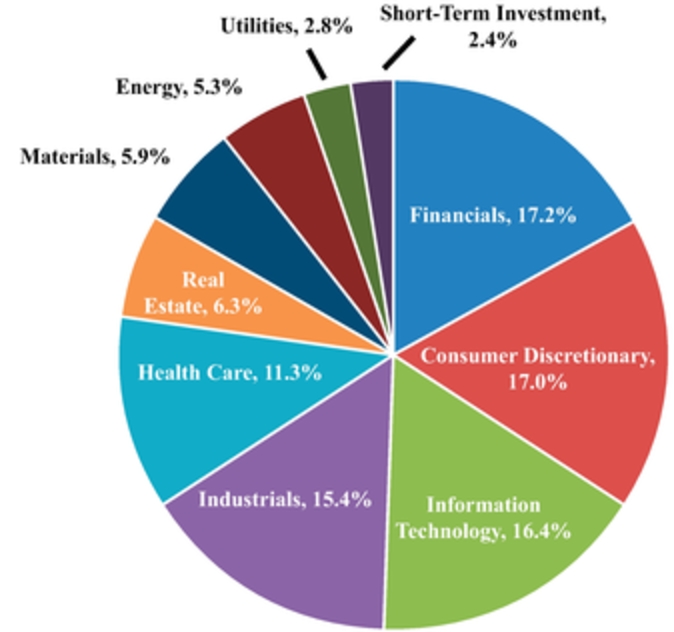

Sector Allocation (as a percentage of total investments) (Unaudited) |

The industry classifications presented in this report, present the Global Industry Classification Standard (GICS®). GICS® was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS® is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The Accompanying Notes are an Integral Part of these Financial Statements.

17

PENN CAPITAL FUNDS TRUST |

PENN CAPITAL SPECIAL SITUATIONS SMALL CAP EQUITY FUND |

SCHEDULE OF INVESTMENTS |

JUNE 30, 2018 |

Shares | Value | |||||

Common Stocks: 97.9% | ||||||

Auto Components: 1.4% | ||||||

Modine Manufacturing Co. (a) | 15,907 | $ | 290,303 | |||

Banks: 10.6% | ||||||

Banc of California, Inc. | 14,583 | 285,098 | ||||

Chemical Financial Corp. | 5,041 | 280,632 | ||||

FB Financial Corp. | 9,392 | 382,442 | ||||

Sterling Bancorp | 15,392 | 361,712 | ||||

Texas Capital Bancshares, Inc. (a) | 4,169 | 381,463 | ||||

Webster Financial Corp. | 3,865 | 246,201 | ||||

Western Alliance Bancorp (a) | 5,790 | 327,772 | ||||

2,265,320 | ||||||

Biotechnology: 1.6% | ||||||

Ironwood Pharmaceuticals, Inc. (a) | 18,227 | 348,500 | ||||

Capital Markets: 2.6% | ||||||

Hamilton Lane, Inc. - Class A | 5,943 | 285,086 | ||||

PJT Partners, Inc. - Class A | 5,002 | 267,057 | ||||

552,143 | ||||||

Chemicals: 1.2% | ||||||

Venator Materials PLC (a) | 16,126 | 263,821 | ||||

Construction & Engineering: 1.5% | ||||||

MasTec, Inc. (a) | 6,193 | 314,295 | ||||

Diversified Consumer Services: 1.3% | ||||||

Chegg, Inc. (a) | 9,532 | 264,894 | ||||

Electronic Equipment, Instruments & Components: 1.2% | ||||||

Mercury Systems, Inc. (a) | 6,818 | 259,493 | ||||

Energy Equipment & Services: 5.6% | ||||||

C&J Energy Services, Inc. (a) | 6,299 | 148,657 | ||||

Keane Group, Inc. (a) | 21,303 | 291,212 | ||||

Mammoth Energy Services, Inc. (a) | 12,365 | 419,915 | ||||

Noble Corp. PLC (a) | 52,303 | 331,078 | ||||

1,190,862 | ||||||

Food & Staples Retailing: 0.6% | ||||||

BJ’s Wholesale Club Holdings, Inc. (a) | 5,190 | 122,744 | ||||

Health Care Equipment & Supplies: 6.0% | ||||||

ICU Medical, Inc. (a) | 1,316 | 386,443 | ||||

K2M Group Holdings, Inc. (a) | 13,628 | 306,630 | ||||

LivaNova PLC (a) | 2,989 | 298,362 | ||||

Wright Medical Group NV (a) | 11,335 | 294,257 | ||||

1,285,692 | ||||||

Health Care Providers & Services: 3.7% | ||||||

LHC Group, Inc. (a) | 3,243 | 277,568 | ||||

R1 RCM, Inc. (a) | 25,633 | 222,495 | ||||

WellCare Health Plans, Inc. (a) | 1,193 | 293,764 | ||||

793,827 | ||||||

Health Care Technology: 1.3% | ||||||

Omnicell, Inc. (a) | 5,212 | 273,369 | ||||

Shares | Value | |||||

Hotels, Restaurants & Leisure: 9.8% | ||||||

Extended Stay America, Inc. | 6,874 | 148,547 | ||||

Full House Resorts, Inc. (a) | 64,588 | 215,078 | ||||

Golden Entertainment, Inc. (a) | 6,077 | 164,018 | ||||

Penn National Gaming, Inc. (a) | 11,441 | 384,303 | ||||

Planet Fitness, Inc. - Class A (a) | 5,362 | 235,606 | ||||

Red Rock Resorts, Inc. - Class A | 10,345 | 346,558 | ||||

Scientific Games Corp. (a) | 6,271 | 308,220 | ||||

SeaWorld Entertainment, Inc. (a) | 12,715 | 277,441 | ||||

2,079,771 | ||||||

Household Durables: 1.4% | ||||||

TopBuild Corp. (a) | 3,767 | 295,107 | ||||

Internet Software & Services: 8.3% | ||||||

Carbonite, Inc. (a) | 7,370 | 257,213 | ||||

Five9, Inc. (a) | 6,034 | 208,595 | ||||

Gogo, Inc. (a) | 29,194 | 141,883 | ||||

Hortonworks, Inc. (a) | 16,983 | 309,430 | ||||

Instructure, Inc. (a) | 5,948 | 253,088 | ||||

Mimecast Ltd. (a) | 5,129 | 211,366 | ||||

MINDBODY, Inc. (a) - Class A | 3,748 | 144,673 | ||||

Q2 Holdings, Inc. (a) | 4,305 | 245,600 | ||||

1,771,848 | ||||||

IT Services: 2.6% | ||||||

Everi Holdings, Inc. (a) | 35,534 | 255,845 | ||||

InterXion Holding NV (a) | 4,839 | 302,050 | ||||

557,895 | ||||||

Machinery: 3.9% | ||||||

Astec Industries, Inc. | 5,732 | 342,774 | ||||

Milacron Holdings Corp. (a) | 13,140 | 248,740 | ||||

Woodward, Inc. | 2,953 | 226,967 | ||||

818,481 | ||||||

Media: 8.7% | ||||||

AMC Entertainment Holdings, Inc. - Class A | 17,384 | 276,405 | ||||

The E. W. Scripps Co. - Class A | 15,877 | 212,593 | ||||

Gray Television, Inc. (a) | 37,977 | 600,037 | ||||

Nexstar Media Group, Inc. - Class A | 5,344 | 392,250 | ||||

Sinclair Broadcast Group, Inc. - Class A | 11,273 | 362,427 | ||||

1,843,712 | ||||||

Metals & Mining: 0.9% | ||||||

Cleveland-Cliffs, Inc. (a) | 23,490 | 198,021 | ||||

Oil, Gas & Consumable Fuels: 5.9% | ||||||

Enerplus Corp. | 24,851 | 313,123 | ||||

Resolute Energy Corp. (a) | 9,670 | 301,704 | ||||

Sanchez Energy Corp. (a) | 29,537 | 133,507 | ||||

Whiting Petroleum Corp. (a) | 5,238 | 276,147 | ||||

WPX Energy, Inc. (a) | 12,946 | 233,417 | ||||

1,257,898 | ||||||

The Accompanying Notes are an Integral Part of these Financial Statements.

18

PENN CAPITAL FUNDS TRUST |

PENN CAPITAL SPECIAL SITUATIONS SMALL CAP EQUITY FUND |

SCHEDULE OF INVESTMENTS |

JUNE 30, 2018 |

Shares | Value | |||||

Pharmaceuticals: 1.0% | ||||||

Pacira Pharmaceuticals, Inc. (a) | 6,854 | 219,671 | ||||

Road & Rail: 2.2% | ||||||

Marten Transport Ltd. | 6,810 | 159,695 | ||||

Schneider National, Inc. - Class B | 10,999 | 302,582 | ||||

462,277 | ||||||

Semiconductors & Semiconductor Equipment: 2.6% | ||||||

Semtech Corp. (a) | 7,019 | 330,244 | ||||

Versum Materials, Inc. | 6,088 | 226,169 | ||||

556,413 | ||||||

Software: 3.2% | ||||||

Nice Ltd. - ADR (a) | 2,693 | 279,453 | ||||

Tyler Technologies, Inc. (a) | 816 | 181,233 | ||||

Zynga, Inc. - Class A (a) | 51,589 | 209,967 | ||||

670,653 | ||||||

Specialty Retail: 2.0% | ||||||

Camping World Holdings, Inc. - Class A | 8,488 | 212,030 | ||||

Five Below, Inc. (a) | 2,250 | 219,848 | ||||

431,878 | ||||||

Textiles, Apparel & Luxury Goods: 1.5% | ||||||

G-III Apparel Group Ltd. (a) | 7,297 | 323,987 | ||||

Thrifts & Mortgage Finance: 1.5% | ||||||

WSFS Financial Corp. | 6,117 | 326,036 | ||||

Trading Companies & Distributors: 3.8% | ||||||

Beacon Roofing Supply, Inc. (a) | 8,230 | 350,763 | ||||

DXP Enterprises, Inc. (a) | 5,330 | 203,606 | ||||

Triton International Ltd. | 8,003 | 245,372 | ||||

799,741 | ||||||

Total Common Stocks (cost $18,047,942) | 20,838,652 | |||||

Contingent Value Right - 0.0% | ||||||

Media - 0.0% | ||||||

Media General, Inc. | 1,867 | 93 | ||||

Total Contingent Value Right (cost $0) | 93 | |||||

Real Estate Investment Trust (REIT): 1.2% | ||||||

Pebblebrook Hotel Trust | 6,308 | 244,750 | ||||

Total REIT (cost $227,382) | 244,750 | |||||

Short-Term Investment: 0.4% | ||||||

Money Market Fund - 0.4% | ||||||

Short-Term Investments Trust Treasury Portfolio Institutional Class, 1.750% (b) | 90,106 | 90,106 | ||||

Total Short-Term Investment (cost $90,106) | 90,106 | |||||

Shares | Value | |||||

Total Investments - 99.5% (cost $18,365,430) | 21,173,601 | |||||

Other Assets and Liabilities 0.5% | 115,307 | |||||

Net Assets: 100.0% | $ | 21,288,908 | ||||

Percentages are stated as a percent of net assets.

| (a) | No distribution or dividend was made during the year ending June 30, 2018. As such, it is classified as a non-income producing security as of June 30, 2018. |

| (b) | Rate reported is the 7-day effective yield as of June 30, 2018. |

Country Exposure (as a percentage of total investments) (Unaudited) | |||

United States | 88.01 | % | |

United Kingdom | 4.22 | % | |

Netherlands | 2.81 | % | |

Canada | 1.48 | % | |

Israel | 1.32 | % | |

Bermuda | 1.16 | % | |

Jersey | 1.00 | % | |

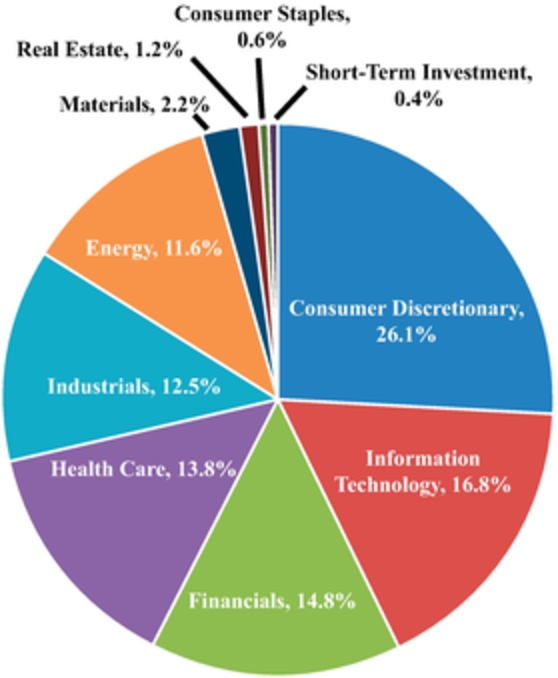

Sector Allocation (as a percentage of total investments) (Unaudited) |

The Accompanying Notes are an Integral Part of these Financial Statements.

19

PENN CAPITAL FUNDS TRUST |

PENN CAPITAL MULTI-CREDIT HIGH INCOME FUND |

SCHEDULE OF INVESTMENTS |

JUNE 30, 2018 |

Principal | Value | |||||

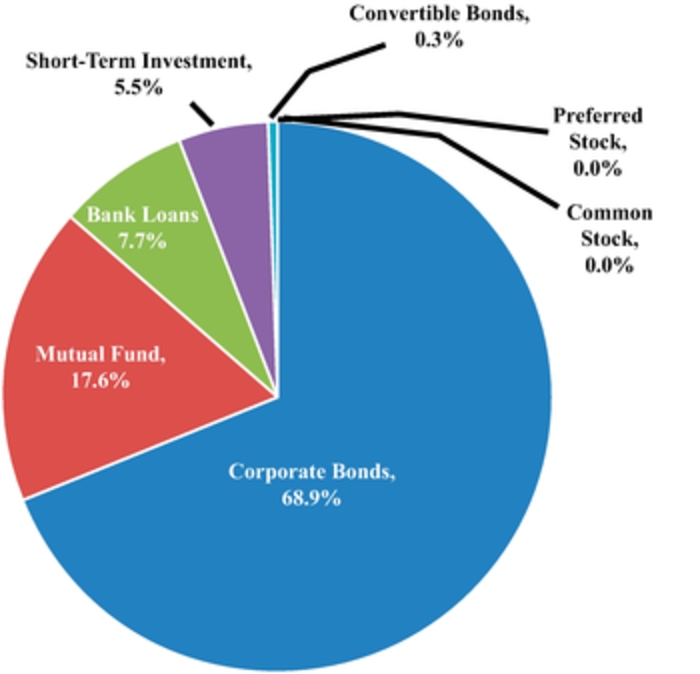

Corporate Bonds: 70.9% | ||||||

Aerospace: 0.8% | ||||||

Bombardier, Inc., 8.750%, 12/1/21 (a) | 105,000 | $ | 115,500 | |||

Agriculture: 0.2% | ||||||

Simmons Foods, Inc., 5.750%, 11/1/24 (a) | 40,000 | 34,700 | ||||

Airline Companies: 1.8% | ||||||

Air Canada, 7.750%, 4/15/21 (a) | 50,000 | 53,375 | ||||

VistaJet Malta Finance PLC, 7.750%, 6/1/20 (a) | 200,000 | 198,000 | ||||

251,375 | ||||||

Auto Parts & Equipment: 0.3% | ||||||

Meritor, Inc., 6.250%, 2/15/24 | 35,000 | 35,263 | ||||

Automotive: 0.7% | ||||||

Navistar International Corp., 6.625%, 11/1/25 (a) | 100,000 | 102,750 | ||||

Banking: 1.2% | ||||||

Ally Financial, Inc., 8.000%, 11/1/31 | 25,000 | 29,750 | ||||

Ally Financial, Inc., 5.750%, 11/20/25 | 90,000 | 91,687 | ||||

Ally Financial, Inc., 5.125%, 9/30/24 | 50,000 | 50,875 | ||||

�� | 172,312 | |||||

Brokerage: 0.4% | ||||||

Oppenheimer Holdings, Inc., 6.750%, 7/1/22 | 60,000 | 61,275 | ||||

Building & Construction: 0.5% | ||||||

Ashton Woods USA LLC, 6.750%, 8/1/25 (a) | 50,000 | 47,500 | ||||

Ashton Woods USA LLC, 6.875%, 2/15/21 (a) | 24,000 | 24,120 | ||||

71,620 | ||||||

Building Materials: 1.2% | ||||||

Griffon Corp., 5.250%, 3/1/22 | 105,000 | 102,155 | ||||

U.S. Concrete, Inc., 6.375%, 6/1/24 | 60,000 | 60,000 | ||||

162,155 | ||||||

Chemical Companies: 1.4% | ||||||

Platform Specialty Products Corp., 5.875%, 12/1/25 (a) | 80,000 | 78,200 | ||||

Trinseo Materials Operating SCA, 5.375%, 9/1/25 (a) | 45,000 | 44,606 | ||||

Versum Materials, Inc., 5.500%, 9/30/24 (a) | 65,000 | 65,904 | ||||

188,710 | ||||||

Computer Hardware: 1.1% | ||||||

Dell International LLC, 8.100%, 7/15/36 (a) | 85,000 | 99,255 | ||||

Western Digital Corp., 4.750%, 2/15/26 | 55,000 | 53,487 | ||||

152,742 | ||||||

Consumer/Commercial/Lease Financing: 1.9% | ||||||

International Lease Finance Corp., 8.625%, 1/15/22 | 35,000 | 40,145 | ||||

Navient Corp., 7.250%, 9/25/23 | 35,000 | 36,662 | ||||

Navient Corp., 6.125%, 3/25/24 | 15,000 | 14,813 | ||||

Navient Corp., 5.875%, 10/25/24 | 65,000 | 62,806 | ||||

Navient Corp., 6.625%, 7/26/21 | 10,000 | 10,272 | ||||

Principal | Value | |||||

Park Aerospace Holdings Ltd., 5.250%, 8/15/22 (a) | 100,000 | 99,001 | ||||

263,699 | ||||||

Electric-Generation: 2.1% | ||||||

Calpine Corp., 5.375%, 1/15/23 (a) | 35,000 | 33,294 | ||||

Calpine Corp., 5.875%, 1/15/24 (a) | 25,000 | 24,750 | ||||

NRG Energy, Inc., 5.750%, 1/15/28 (a) | 25,000 | 24,563 | ||||

NRG Energy, Inc., 6.625%, 1/15/27 | 25,000 | 25,688 | ||||

NRG Energy, Inc., 7.250%, 5/15/26 | 20,000 | 21,300 | ||||

Vistra Energy Corp, 8.125%, 1/30/26 (a) | 50,000 | 54,312 | ||||

Vistra Energy Corp., 7.625%, 11/1/24 | 70,000 | 74,637 | ||||

Vistra Energy Corp., 7.375%, 11/1/22 | 25,000 | 26,125 | ||||

284,669 | ||||||

Electric-Integrated: 0.2% | ||||||

Talen Energy Supply LLC, 9.500%, 7/15/22 (a) | 35,000 | 34,366 | ||||

Energy-Exploration & Production: 4.7% | ||||||

Antero Resources Corp., 5.125%, 12/1/22 | 50,000 | 50,125 | ||||

Approach Resources, Inc., 7.000%, 6/15/21 | 40,000 | 39,000 | ||||

Callon Petroleum Co., 6.125%, 10/1/24 | 35,000 | 35,437 | ||||

Carrizo Oil & Gas, Inc., 8.250%, 7/15/25 | 25,000 | 26,500 | ||||

Centennial Resource Production LLC, 5.375%, 1/15/26 (a) | 30,000 | 29,175 | ||||

Gulfport Energy Corp., 6.000%, 10/15/24 | 60,000 | 57,750 | ||||

Gulfport Energy Corp., 6.625%, 5/1/23 | 15,000 | 15,113 | ||||

HighPoint Operating Corp., 7.000%, 10/15/22 | 35,000 | 35,000 | ||||

Jagged Peak Energy LLC, 5.875%, 5/1/26 (a) | 40,000 | 39,200 | ||||

Range Resources Corp., 5.000%, 8/15/22 | 80,000 | 79,200 | ||||

Resolute Energy Corp., 8.500%, 5/1/20 | 125,000 | 124,922 | ||||

Sanchez Energy Corp., 7.250%, 2/15/23 (a) | 55,000 | 54,450 | ||||

Unit Corp., 6.625%, 5/15/21 | 70,000 | 69,825 | ||||

655,697 | ||||||

Entertainment: 0.8% | ||||||

AMC Entertainment Holdings, Inc., 5.875%, 11/15/26 | 25,000 | 24,062 | ||||

AMC Entertainment Holdings, Inc., 5.750%, 6/15/25 | 55,000 | 53,900 | ||||

National CineMedia LLC, 5.750%, 8/15/26 | 40,000 | 36,500 | ||||

114,462 | ||||||

Food-Wholesale: 1.3% | ||||||

JBS USA LUX SA, 5.875%, 7/15/24 (a) | 100,000 | 95,500 | ||||

JBS USA LUX SA, 7.250%, 6/1/21 (a) | 15,000 | 15,150 | ||||

JBS USA LUX SA, 7.250%, 6/1/21 (a) | 15,000 | 15,150 | ||||

Pilgrim’s Pride Corp., 5.750%, 3/15/25 (a) | 60,000 | 57,600 | ||||

183,400 | ||||||

Food & Drug Retailers: 1.1% | ||||||

Albertsons Cos LLC, 6.625%, 6/15/24 | 60,000 | 56,550 | ||||

Albertsons Cos, Inc., 6.085% (3 Month LIBOR USD + 3.750%), 1/15/24 (a)(b) | 35,000 | 35,087 | ||||

Ingles Markets, Inc., 5.750%, 6/15/23 | 65,000 | 64,025 | ||||

The Accompanying Notes are an Integral Part of these Financial Statements.

20

PENN CAPITAL FUNDS TRUST |

PENN CAPITAL MULTI-CREDIT HIGH INCOME FUND |

SCHEDULE OF INVESTMENTS |

JUNE 30, 2018 |

Principal | Value | |||||

155,662 | ||||||

Forestry/Paper: 0.5% | ||||||

Rayonier AM Products, Inc., 5.500%, 6/1/24 (a) | 70,000 | 65,800 | ||||

Gaming: 1.3% | ||||||

Gateway Casinos & Entertainment Ltd., 8.250%, 3/1/24 (a) | 40,000 | 42,200 | ||||

MGM Resorts International, 7.750%, 3/15/22 | 30,000 | 32,700 | ||||

The Stars Group Holdings, 7.000%, 7/15/26 (a) | 50,000 | 50,500 | ||||

Wynn Las Vegas LLC, 5.500%, 3/1/25 (a) | 55,000 | 54,038 | ||||

179,438 | ||||||

Gas Distribution: 3.6% | ||||||

Blue Racer Midstream LLC, 6.125%, 11/15/22 (a) | 45,000 | 45,450 | ||||

Cheniere Energy Partners LP, 5.250%, 10/1/25 (a) | 65,000 | 63,404 | ||||

DCP Midstream Operating LP, 3.875%, 3/15/23 (a) | 55,000 | 53,144 | ||||

DCP Midstream Operating LP, 4.950%, 4/1/22 | 33,000 | 33,371 | ||||

DCP Midstream Operating LP, 5.850% (3 Month LIBOR USD + 3.850%), 5/21/43 (b) | 90,000 | 82,350 | ||||

NGL Energy Partners LP, 5.125%, 7/15/19 | 65,000 | 65,081 | ||||

NGL Energy Partners LP, 6.875%, 10/15/21 | 20,000 | 20,250 | ||||

NGPL PipeCo LLC, 7.768%, 12/15/37 (a) | 45,000 | 52,875 | ||||

Rockies Express Pipeline LLC, 6.875%, 4/15/40 (a) | 45,000 | 51,300 | ||||

Targa Resources Partners LP, 5.250%, 5/1/23 | 30,000 | 30,000 | ||||

497,225 | ||||||

Health Services: 2.0% | ||||||

Acadia Healthcare Co., Inc., 5.625%, 2/15/23 | 50,000 | 50,375 | ||||

Acadia Healthcare Co., Inc., 6.125%, 3/15/21 | 35,000 | 35,350 | ||||

Centene Escrow I Corp., 5.375%, 6/1/26 | 30,000 | 31,612 | ||||

Centene Corp., 6.125%, 2/15/24 (a) | 30,000 | 30,394 | ||||

DaVita, Inc., 5.125%, 6/15/24 | 40,000 | 38,800 | ||||

Encompass Health Corp., 5.750%, 9/15/25 | 50,000 | 50,500 | ||||

Universal Hospital Services, Inc., 7.625%, 8/15/20 | 35,000 | 34,913 | ||||

271,944 | ||||||

Hospitals: 1.6% | ||||||

HCA, Inc., 7.500%, 2/15/22 | 25,000 | 27,188 | ||||

HCA, Inc., 5.250%, 6/15/26 | 40,000 | 39,728 | ||||

HCA, Inc., 5.375%, 2/1/25 | 65,000 | 64,005 | ||||

Tenet Healthcare Corp., 8.125%, 4/1/22 | 80,000 | 83,500 | ||||

214,421 | ||||||

Household & Leisure Products/Durables: 0.3% | ||||||

Tempur Sealy International, Inc., 5.500%, 6/15/26 | 45,000 | 43,538 | ||||

Principal | Value | |||||

Investments & Misc Financial Services: 2.4% | ||||||

First Data Corp., 5.750%, 1/15/24 (a) | 50,000 | 49,968 | ||||

First Data Corp., 7.000%, 12/1/23 (a) | 75,000 | 78,118 | ||||

Icahn Enterprises LP, 6.375%, 12/15/25 | 60,000 | 60,075 | ||||

Icahn Enterprises LP, 6.750%, 2/1/24 | 110,000 | 110,825 | ||||

VFH Parent LLC, 6.750%, 6/15/22 (a) | 35,000 | 36,269 | ||||

335,255 | ||||||

Machinery Companies: 0.7% | ||||||

Apergy Corp., 6.375%, 5/1/26 (a) | 35,000 | 35,569 | ||||

Zekelman Industries, Inc., 9.875%, 6/15/23 (a) | 50,000 | 54,750 | ||||

90,319 | ||||||

Media-Broadcast: 3.2% | ||||||

Gray Television, Inc., 5.125%, 10/15/24 (a) | 25,000 | 23,875 | ||||

Gray Television, Inc., 5.875%, 7/15/26 (a) | 25,000 | 23,781 | ||||

Salem Media Group, Inc., 6.750%, 6/1/24 (a) | 45,000 | 40,838 | ||||

Sinclair Television Group, Inc., 5.625%, 8/1/24 (a) | 65,000 | 64,513 | ||||

Townsquare Media, Inc., 6.500%, 4/1/23 (a) | 40,000 | 36,000 | ||||

Univision Communications, Inc., 5.125%, 5/15/23 (a) | 60,000 | 57,600 | ||||

Univision Communications, Inc., 5.125%, 2/15/25 (a) | 15,000 | 13,856 | ||||

Urban One, Inc., 7.375%, 4/15/22 (a) | 45,000 | 43,537 | ||||

Urban One, Inc., 9.250%, 2/15/20 (a) | 140,000 | 135,800 | ||||

439,800 | ||||||

Media-Cable: 4.4% | ||||||

Altice France SA, 6.000%, 5/15/22 (a) | 200,000 | 201,250 | ||||

Altice Luxembourg SA, 7.750%, 5/15/22 (a) | 200,000 | 193,500 | ||||

DISH DBS Corp., 5.875%, 7/15/22 | 185,000 | 173,900 | ||||

DISH DBS Corp., 7.750%, 7/1/26 | 40,000 | 35,050 | ||||

603,700 | ||||||

Media-Services: 0.7% | ||||||

Clear Channel Worldwide Holdings, Inc., 7.625%, 3/15/20 | 40,000 | 39,700 | ||||

MDC Partners, Inc., 6.500%, 5/1/24 (a) | 70,000 | 60,725 | ||||

100,425 | ||||||

Metals/Mining Excluding Steel: 3.8% | ||||||

Alliance Resource Operating Partners LP, 7.500%, 5/1/25 (a) | 65,000 | 69,225 | ||||

Century Aluminum Co., 7.500%, 6/1/21 (a) | 60,000 | 60,450 | ||||

Cleveland-Cliffs, Inc., 5.750%, 3/1/25 | 35,000 | 33,162 | ||||

CONSOL Energy, Inc., 11.000%, 11/15/25 (a) | 90,000 | 99,000 | ||||

Freeport-McMoRan, Inc., 4.550%, 11/14/24 | 15,000 | 14,250 | ||||

Freeport-McMoRan, Inc., 5.450%, 3/15/43 | 50,000 | 43,860 | ||||

Freeport-McMoRan, Inc., 3.875%, 3/15/23 | 5,000 | 4,725 | ||||

Peabody Energy Corp., 10.000%, 3/15/22 (c) | 95,000 | 0 | ||||

Peabody Energy Corp., 6.375%, 3/31/25 (a) | 45,000 | 46,237 | ||||

SunCoke Energy Partners LP, 7.500%, 6/15/25 (a) | 65,000 | 66,138 | ||||

The Accompanying Notes are an Integral Part of these Financial Statements.

21

PENN CAPITAL FUNDS TRUST |

PENN CAPITAL MULTI-CREDIT HIGH INCOME FUND |

SCHEDULE OF INVESTMENTS |

JUNE 30, 2018 |

Principal | Value | |||||

Teck Resources Ltd., 5.200%, 3/1/42 | 35,000 | 30,669 | ||||

Teck Resources Ltd., 3.750%, 2/1/23 | 35,000 | 33,206 | ||||

Teck Resources Ltd., 6.250%, 7/15/41 | 25,000 | 24,875 | ||||

525,797 | ||||||

Non-Food & Drug Retailers: 0.9% | ||||||

Hot Topic, Inc., 9.250%, 6/15/21 (a) | 65,000 | 61,994 | ||||

The Men’s Wearhouse, Inc., 7.000%, 7/1/22 | 55,000 | 56,787 | ||||

118,781 | ||||||

Oil Field Equipment & Services: 3.0% | ||||||

CSI Compressco LP, 7.250%, 8/15/22 | 45,000 | 41,175 | ||||

CSI Compressco LP, 7.500%, 4/1/25 (a) | 25,000 | 25,094 | ||||

Nabors Industries, Inc., 5.500%, 1/15/23 | 60,000 | 57,360 | ||||

Noble Holding International Ltd., 7.875%, 2/1/26 (a) | 25,000 | 25,750 | ||||

Noble Holding International Ltd., 7.750%, 1/15/24 | 130,000 | 123,175 | ||||

Pioneer Energy Services Corp., 6.125%, 3/15/22 | 60,000 | 57,000 | ||||

Transocean, Inc., 8.375%, 12/15/21 | 35,000 | 37,450 | ||||

Transocean, Inc., 6.800%, 3/15/38 | 50,000 | 40,625 | ||||

407,629 | ||||||

Oil Refining & Marketing: 0.6% | ||||||

PBF Holding Co. LLC, 7.250%, 6/15/25 | 35,000 | 36,794 | ||||

PBF Holding Co. LLC, 7.000%, 11/15/23 | 40,000 | 41,400 | ||||

78,194 | ||||||

Pharmaceuticals & Devices: 4.6% | ||||||

Endo Finance LLC, 5.375%, 1/15/23 (a) | 55,000 | 44,000 | ||||

Jaguar Holding Co. II, 6.375%, 8/1/23 (a) | 55,000 | 54,736 | ||||

Kinetic Concepts, Inc., 12.500%, 11/1/21 (a) | 75,000 | 82,875 | ||||