As filed with the Securities and Exchange Commission on 9/08/2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-23011

Investment Company Act file number

The RBB FUND TRUST

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Steven Plump, President

c/o U.S. Bank Global Fund Services

615 East Michigan Street

Milwaukee, WI 53202

(Name and address of agent for service)

(609) 731-6256

Registrant's telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: June 30, 2023

Item 1. Reports to Stockholders.

(a)

Evermore Global Value Fund

of The RBB Fund Trust

Semi-Annual Report ● June 30, 2023

This report is submitted for the general information of the shareholders of the Evermore Global Value Fund and may not be used as sales literature unless preceded or accompanied by a current prospectus for the Fund.

Table of Contents

Shareholder Letter & Management Discussion of Fund Performance (Unaudited) | 1 |

Performance Information (Unaudited) | 8 |

Sector Allocation (Unaudited) | 9 |

Expense Example (Unaudited) | 10 |

Schedule of Investments (Unaudited) | 11 |

Statement of Assets and Liabilities (Unaudited) | 14 |

Statement of Operations (Unaudited) | 15 |

Statements of Changes in Net Assets (Unaudited) | 16 |

Financial Highlights (Unaudited) | 17 |

Notes to Financial Statements (Unaudited) | 21 |

Approval of Investment Advisory and Sub-Advisory Agreements (Unaudited) | 36 |

Additional Information (Unaudited) | 38 |

Privacy Notice (Unaudited) | 39 |

Evermore Global Value Fund

Elements of Our Investment Approach

As the sub-adviser to the Evermore Global Value Fund, MFP Investors LLC seeks to leverage our deep operating and investing experience and extensive global relationships to identify and invest in special situations — companies around the world that have compelling valuations and are undergoing strategic changes which we believe will unlock value.

Seeking to Generate Value . . .

● | Catalyst-Driven Investing. We do more than simply picking undervalued stocks and hoping for their prices to rise. We invest in companies where we have determined a series of catalysts exist to unlock value. The catalysts we look for are not broadly recognized, but they are likely to have a significant impact on a stock’s performance over time. Catalysts may include management changes, shareholder activism, and operational and financial restructurings (e.g., cost-cutting, asset sales, breakups, spinoffs, mergers, acquisitions, liquidations, share buybacks, recapitalizations, etc.). |

Supporting Our Active Value Orientation . . .

● | Original Fact-Based Research. We conduct our own, original fact-based research to validate a company’s stated objectives and identify catalysts to unlock value. We also perform detailed business segment analysis on each company we research. |

● | Business Operating Experience. Our senior investment team has hands-on business operating experience including starting and managing businesses, sitting on company boards, and assisting multi-national corporations with restructuring their businesses. We rely on our team’s experience to better evaluate investment opportunities. |

● | A Global Network of Strategic Relationships. Over the past 25+ years, members of our investment team have developed extensive global networks of strategic relationships, including individuals and families that control businesses, corporate board members, corporate management, regional brokerage firms, press contacts, etc. We leverage these relationships to help generate ideas and better evaluate investment opportunities. |

● | We Invest Like Owners. When we are interested in an investment opportunity, we get to know the management team of the company, study the company’s business model, evaluate the competitive and regulatory environment, and test and crosscheck everything the company’s management team tells us against our own experience. We ask ourselves if we would want to own the entire company. If the answer is no, we will not invest in the company. |

● | Not Activists, Often Collaborators. We almost always take the approach of collaborative engagement with management of a company, rather than taking an aggressive activist stance. On limited occasions, when we are not satisfied with the efforts of the incumbent company leadership, we may work with other shareholders to help facilitate change. |

Executing Our Approach . . .

● | Concentration Maintains Focus. Focused and disciplined investing means knowing our businesses intimately and staying patient as the process of value creation unfolds. We maintain focus by typically investing in 25 to 40 securities with a high percentage of investments in our top 10 holdings. |

● | Investing Across the Capital Structure. We evaluate all components of a company’s capital structure to determine where the best risk-adjusted return potential exists. At times, we may invest in multiple parts of a company’s capital structure (e.g., investing in both a company’s debt and equity). |

● | Targeting Complex Investment Opportunities. We often research family-controlled holding companies or conglomerates that are often under-researched and/or misunderstood, which can create gaps between price and value. |

● | Merger Arbitrage and Distressed Companies. We may take advantage of announced merger and acquisition deals where an attractive spread (difference) exists between the market price and the announced deal price for the target company. We also look for opportunities in distressed companies that have filed or may file for bankruptcy, distressed companies involved in reorganizations or financial restructurings, and distressed companies that emerged from a bankruptcy or reorganization. |

● | Tactically Managing Cash Levels. We are not afraid to hold significant cash positions when it makes sense for the portfolio. |

1

Evermore Global Value Fund

A Letter from the Portfolio Managers

Dear Shareholder,

As the second quarter of 2023 kicked off, headlines were filled with all kinds of negative rhetoric and discussions. These topics included: the banking sector on the brink of disaster, interest rates continuing to ratchet up, corporate earnings that had peaked and could only go lower, Russia warming up the nukes, and a global recession that was all but assured. As usual, the forecasts overall, at least so far, have proven to be way off the mark. Instead, the markets plowed ahead and grinded higher. In fact, the first half of 2023 was one of the best first half starts to a year in history from a markets perspective. Investors and the markets overall have had an incredible resiliency to take so many macro punches, absorb them and then just keep moving forward. Yes, it’s true that much of the positive performance in the markets was driven by a smaller subset of names, but that does not matter to many market participants. With the fear of missing out at top of mind, investors have been swarming into securities that had some semblance of involvement with artificial intelligence (AI) in hopes of having some exposure (real or perceived) to the technology. It has been a risk-on strategy by investors that has delivered so far. However, when the music stops or at least slows a bit, the carnage could be quite material.

Our focus is on finding compelling investment cases across a variety of sectors and industries, keeping trading to a minimum and “tagging along” with compelling yet cheap situations that have the ability to compound well over time. Institutional Class shares of the Evermore Global Value Fund (the “Fund”) were down 0.56% for the second quarter of 2023, versus the MSCI All-Country World Index ex USA (the “Index”), which was up 2.44% for the same period. For the year-to-date period through June 30, 2023, Institutional Class shares of the Fund were up 7.67% and the Index was up 9.47%.

We were on track for a good second quarter of 2023 until one of our investments had a surprising drawdown, which detracted about 3% from our total return during the six-month period ended June 30, 2023 (the “Period”). Viaplay AB which is a free-to-air and pay tv business based in Sweden missed its numbers. The stock had been a very strong performer for the Fund since it was spun off from another of our holdings, Modern Times Group AB (MTG) several years ago. We have a more extensive discussion of this situation later in the letter under the heading “Portfolio Review - Top Contributors & Detractors”.

The largest contributors to performance so far this year are in a category we categorize as Family-Controlled Companies (FCC). We expect this area to continue to grow within the portfolio as the number of family-controlled businesses that are undergoing value-creating changes has been growing over the last few years. Companies in the portfolio like Bolloré, Exor and BW LPG all had compelling news in the second quarter of 2023 that pushed their stock prices higher, but at the same time we believe these gains were not commensurate to the unrealized value creation from asset sales, stock buybacks and acquisitions. In other words, this means we believe they remain undervalued. Excluding the impact of cash, hedges, options and warrants, our investments in FCC represent 74.5% of the portfolio at the end of the second quarter.

Portfolio Review – Investment Performance

Institutional Class shares of the Fund were down 0.56% for the quarter ended June 30, 2023. As shown in the chart below, the Fund’s performance in the second quarter of 2023 underperformed the Index and the Fund’s peer fund category average but outperformed the HFRX Event Driven Index.

The performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data current to the most recent month end may be obtained by calling 866-EVERMORE (866-383-7667). Prior to December 28, 2022, the Fund imposed a 2% redemption fee on shares redeemed within 90 days. Performance data quoted does not reflect the redemption fee. If reflected, total returns would be reduced. The performance data quoted reflects fee waivers in effect and would have been less in their absence. Please click here for standardized performance of the Fund.

2

Quarter Ended June 30, 2023

Morningstar Global Small/Mid Stock Category Average represents an average of all funds in the Morningstar Global Small/Mid Stock Category.

Portfolio Review – Characteristics

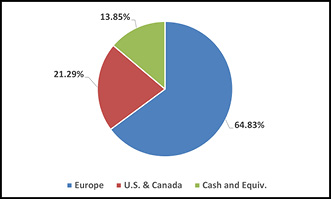

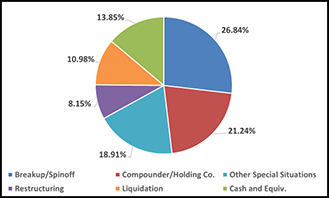

The Fund ended the Period with $106.9 million in net assets and 23 issuer positions. As of the Period’s end, 35.9% of the Fund’s net assets were in micro- and small-capitalization (up to $2 billion) companies; 17.2% were in mid-capitalization (between $2 billion and $10 billion) companies; and 22.0% were in large-capitalization (> $10 billion) companies. Set forth below please find the following geographic and strategy classification breakdowns (shown as a % of Fund net assets) as of the Period’s end.

Region Exposure | Strategy Classification |

|

|

3

Country Exposure

^ | Excludes cash and equivalent holdings (13.9% of net assets) consisting of Short-Term Investment-Money Market Fund (13.4%), Securities Held as Collateral on Loaned Securities (4.1%) and net of Liabilities in Excess of Other Assets (-3.6%). |

Portfolio Review – New Investments

The Fund ended the second quarter of 2023 with one new position – Genco Shipping & Trading (GNK US; Marshall Islands). Below please find a summary of our investment in Genco.

The Fund re-initiated a position Genco Shipping & Trading (GNK US), one of the largest U.S.-listed dry bulk operators with a market cap of $596 million. This security should ring a bell with our long-time investors in the Fund, as we previously owned it a few years ago before exiting the position at the end of 2020 / early Q1 2021. Headquartered in New York with global offices in Singapore and Copenhagen, Genco currently has a fleet of 44 modern, fuel efficient vessels with direct exposure to transporting all types of dry bulk trades including major (iron ore, coal) and minor (grains, cement, fertilizers, etc.) bulk all around the world.

We are excited to get another opportunity with this investment based on its compelling valuation. The setup appears exceptionally good with:

● | A historically low order book for the industry that is less than 5% of the total fleet in 2023 onward |

● | Favorable environmental regulations (International Maritime Organization or IMO compliance leading to lower new orders, increased scrapping, and slower voyage speeds) |

● | China’s reopening that should continue to spur global trade |

● | Geopolitical turmoil (i.e., Ukraine/Russia) that has resulted in disrupted cargo routes, which means longer ton miles needed for coal and grain transport |

Since 2021, Genco has refocused on shareholder value creation through paying out significant dividends, deleveraging the balance sheet and optimizing its fleet composition by opportunistically selling older ships. The company has paid down approx. $287 million of debt since embarking on this strategy and, as a result, sits on a strong balance sheet with leverage at a mere 11% net loan-to-value (LTV) and no significant debt maturities coming due until second half of 2026. Genco is trading at about 0.6x our estimate of price/NAV, a compelling valuation for a company that is in a superior position compared to when we previously owned the security, further underpinned by a favorable regulatory environment, strengthening industry fundamentals and longer distances.

4

Portfolio Review – Exited Investments

The Fund exited one investment during the second quarter of 2023:

● | BW LPG (BWLPG NO): The Fund exited its position in BW LPG in the second quarter of 2023, realizing a healthy gain for a position that we held for just under a year. It was the largest contributor to Fund performance with the share price appreciating 37% in the second quarter. |

BW LPG is one of the leading liquified petroleum gas (“LPG”) vessel operators in the world. Headquartered in Singapore and listed on the Oslo exchange, BW LPG has a market cap of $1.4 billion and a fleet of 45 Very Large Gas Carriers (VLGCs), of which 16 vessels are outfitted with the latest cost-effective, low emissions LPG dual-fuel propulsion technology. The main family-controlled shareholder is the BW Group (41% stake), a well-regarded maritime and green-related family-controlled holding company managed by the long-term oriented value creator and savvy investor, Andreas Sohmen-Pao. It should be noted that the BW Group is also an anchor shareholder in another Fund investment, Cadeler, an offshore wind installation vessel operator. |

Since we initiated our position in late August 2022, the VLGC rates continued to strengthen, and the order book of new vessels delivered this year has been well absorbed. Given the strong cash flow generation, BW LPG has paid a significant amount of dividends so far this year, representing a 100% payout ratio and dividend yield in excess of 30%. Last May, the company announced a share buyback program to purchase up to 6 million shares for a maximum of $50 million. In mid-June, BW LPG announced a reverse book building process to purchase shares through a Dutch Auction. We decided to tender all our shares at NOK 108 per share and lock in a substantial return as the share price appreciated faster than we expected (approximately NOK 60 per share to over NOK 100 per share during the first half of 2023). We will continue to monitor BW LPG for an opportunity to possibly become shareholders again in the future. |

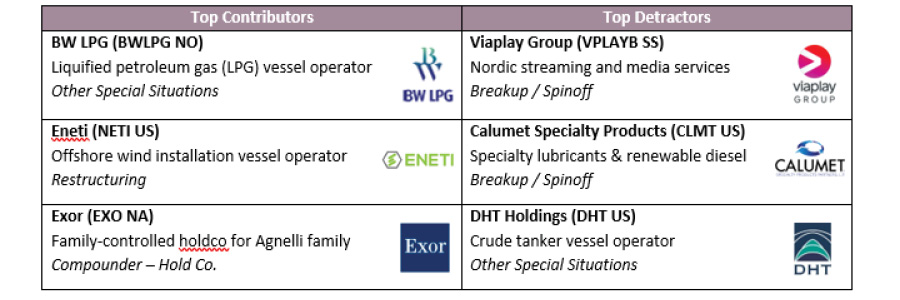

Portfolio Review - Top Contributors & Detractors

The top three contributors to and detractors from Fund performance in the second quarter of 2023 and summaries for two of the most impactful contributors and detractors can be found below.

Eneti (NETI US) is a $470 million market cap offshore wind turbine installation vessel operator. Eneti was the second largest contributor (approx. +30%) to Fund performance in the second quarter of 2023. The most significant news came out just this past June, when Eneti announced a transformative merger with its biggest competitor, Cadeler A/S (which we own in the Fund), in an all-stock deal which is expected to close in the fourth quarter of 2023.

As a reminder, we have owned Eneti in our Fund since it was formerly known as Scorpio Bulkers, a dry bulk operator that transitioned its strategy from the dry bulk sector into offshore wind in August 2020. In fact, Eneti’s decision to pursue this dramatic shift into the nascent offshore wind sector was the impetus for us to start our deep dive analyses on the sector which resulted in our investment in Cadeler.

With a market cap of $900 million, Cadeler is one of the few pureplay offshore wind installation vessel operators in the world. Since 2010, the company has installed over 280 wind turbines and 400 foundations, making it the largest and preeminent offshore wind installation company with over 50% global market share. Founded in 2008, Cadeler was 100% acquired in 2010 by the Swire Pacific Group, a Hong Kong-listed holding company that was formerly called Swire Blue Ocean. Due to liquidity needs to address financial issues in its underlying companies, Swire Pacific was a forced seller and listed Cadeler on the Oslo Bors in November 2020. Swire Pacific now owns a residual 15% and a new strategic partner, BW Group, came in as a cornerstone investor (30% stake) which we mentioned under the BW LPG section. We believe this is a game-changing merger that solidifies Cadeler/Eneti as the largest offshore wind vessel operator in the world with significant operational synergies. With wind turbines getting larger and the European Union’s strong stance on the renewables and green initiatives, we

5

believe that the need for bigger wind turbine capacity will grow substantially over the next 5 to 10 years. Given the limited supply of modern vessels to handle such increased capacity, Cadeler/Eneti is extremely well positioned to be the beneficiary of this global structural shift to green initiatives.

Exor (EXO NA) was another contributor to Fund performance. Exor is a $21 billion market cap, holding company for the Agnelli family of Italy. Through its stake in the listed auto group Stellantis, the fourth largest auto original equipment manufacturer (OEM) that Exor helped to form via Fiat Chrysler’s merger with Peugeot, Exor controls Ferrari, Fiat, Chrysler, Maserati, Peugeot, Alfa Romeo and a number of other brands. They also control 64% of the soccer club Juventus, 43% of the Economist magazine, 24% of Louboutin (the famous red sole shoes and accessories global luxury brand) and a myriad of other businesses. The head of the family is John Elkann, great-great grandson of Giovanni Agnelli, the founder of Fiat. He has done an admirable job of building great business franchises through acquisitions, portfolio harvesting, and targeted investments within portfolio companies.

Exor makes long-term investments in companies primarily in Europe and Asia, but with global reach, and often in partnership with founding families. In recent years, Exor has shifted its emphasis to less capital-intensive business such as luxury fashion houses (Shang Xia, Christian Louboutin), healthcare (Institut Mérieux, initial 10% stake) and other enduring franchises (The Economist, etc.). Lastly, the $9 billion sale of PartnerRe to Covéa provides significant equity firepower for compelling future acquisitions. Since the creation of Exor in 2009 through 2022, the company’s NAV per share has compounded at an impressive 17.6% CAGR. We continue to maintain high conviction in Exor and further believe the 40% discount to our estimated NAV should narrow over time as the holding company goes through periods of harvesting and investing in the portfolio.

Viaplay Group (VPLAYB SS), a $453 million market cap, Nordic streaming media company, was the largest detractor to performance in the second quarter of 2023 after having been the second largest contributor in the prior quarter. In June, Viaplay had an unexpected turn of events, announcing a profit warning and the CEO’s resignation on a Sunday afternoon (NY time).

We were certainly surprised and extremely disappointed by these recent developments, especially for our long-term holding that had successfully navigated the pandemic and grew the subscriber base significantly over the last two years. Earlier this year, Viaplay initiated its planned price increases across various markets but clearly those efforts were unsuccessful with a higher-than-expected churn recently. Management revised downward the full-year 2023 guidance and withdrew the operating and financial targets for 2025 citing a rapid deterioration of advertising revenues and lower demand in the Nordic and international streaming markets. They attributed the higher churn levels to the rising cost of living following the price increases.

Anders Jensen, who was the CEO since Viaplay spun out from its former parent, Modern Times Group (MTG) in April 2019, has resigned effective immediately. Anders was replaced by Jorgen Madsen Lindemann, who was the former CEO of the predecessor parent company, MTG, and prior to that held senior leadership positions at MTG spanning over 26 years including head of Nordic operations and international operations, and head of sports rights acquisition and production. Subsequent to the end of the second quarter of 2023, Viaplay withdrew its full year 2023 guidance (but kept the Q2 2023 guidance intact) on the back of the new CEO’s review of current operations and the Chairman, Pernille Erenbjerg, stepped down from the board due to personal health-related reasons in July. With increased uncertainty, diminishing investor confidence, and a greater likelihood of impairments in the expanded international markets, we have ultimately decided to exit our position in Viaplay at a loss. While we believe there should be minimal solvency risk, a potential liquidity constraint could result in a dilutive equity raise if Viaplay’s core Nordic markets slow down at a sharper pace. We will monitor how the situation unfolds at Viaplay as the company provides an update on its strategy and medium-term outlook which will include cost savings program, content cost savings initiatives, review of the international operations and non-core assets and renegotiations with its distribution partners.

Calumet Specialty Products (CLMT US) was the second largest detractor to Fund performance during the second quarter of 2023. Calumet is a $1.27 billion market cap producer of branded and unbranded specialty petrochemicals, as well as a refiner of petroleum-derived fuels and renewables. There were a number of notable positive developments during the quarter.

The Montana Renewables (“MRL”) facility located in Great Falls, Montana is now fully operational with renewable hydrogen, pretreatment unit and sustainable aviation fuel (SAF) all online. As you may recall, the conversion of the MRL facility was completed last September, transforming it from a traditional refiner to one capable of producing renewable diesel (RD) and SAF. MRL has already started to produce the initial 2,000 barrels per day (bpd) or 30 million gallons per year of SAF which is all being sold to Shell Aviation under an offtake agreement. Calumet has reached its milestone of becoming the largest SAF producer in North America. MRL intends to significantly increase SAF production over the next two to three years reaching a maximum level of 15,000 bpd or approx. 230 million gallons annually.

In addition, Calumet continues to adhere to its strategic objectives and further de-levered the balance sheet. As of Q1 2023, the company had a net debt to trailing-12-months adjusted EBITDA of 3.0x which is significantly lower than where it stood a year ago (8.2x). In June, Calumet completed a private placement offering of $325 million of 9.75% Senior Notes due 2028, with proceeds earmarked to tender for all of its $200 million of 9.25% Senior Secured First Lien Notes due 2024 and up to $100 million of the 11% Senior Notes due 2025. While total debt will remain about the same, the company has extended maturities and secured a modest interest expense reduction. We continue to have high conviction in management’s ability to ramp up MRL’s production, continued execution at Calumet’s core segments, and on-going deleveraging (from MRL’s operating cash flows or liquidity event from monetizing a portion or all of MRL).

6

Closing Thoughts

As we ended the second quarter of 2023, it was also the second chapter in the life of the Evermore Global Value Fund. We have settled in well within MFP Investors LLC and the Price Family Office. The knowledge, experience and drive that are swirling around this office are intense and incredible. We have full access to the larger MFP Investors group and ideas are shared and discussed across the room. To that end, we believe this is a huge, undervalued asset that should benefit the investors in the Fund over time.

Please feel free to contact us at dmarcus@mfpllc.com or to@mfpllc.com with any questions or thoughts.

Sincerely,

|

|

David E. Marcus

Lead Portfolio Manager | Thomas O

Co-Portfolio Manager |

Opinions expressed are those of MFP Investors LLC and are subject to change, are not guaranteed and should not be considered investment advice.

Fund holdings and sector allocations are subject to change at any time and should not be considered recommendations to buy or sell any security. Current and future portfolio holdings are subject to risk.

MSCI All-Country World Index Ex USA captures large and mid-cap representation across 22 Developed Markets countries.

The HFRX Event Driven Index utilizes a UCITSIII compliant methodology to construct the HFRX Hedge Fund Indices. The methodology is based on defined and predetermined rules and objective criteria to select and rebalance components to maximize representation of the Hedge fund Universe.

EV/EBITDA - Enterprise Value/Earning Before Interest, Taxes, Depreciation and Amortization is the most widely used valuation multiple based on enterprise value and is often used in conjunction with, or as an alternative to the price to earnings ratio to determine the fair market value of a company.

Free cash flow represents the cash a company generates after cash outflows to support operations and maintain its capital assets.

EBIT means earnings before interest and taxes and is an indicator of a company’s profitability.

Please click here for the most recent holdings of the Fund. Please view the schedule of investments for holdings information as of June 30, 2023.

Mutual fund investing involves risk. Principal loss is possible. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. This risk is greater for investments in Emerging Markets. Investing in smaller companies involves additional risks such as limited liquidity and greater volatility than larger companies. The Fund may make short sales of securities, which involve the risk that losses may exceed the original amount invested in the securities. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment in lower-rated, non-rated and distressed securities presents a greater risk of loss to principal and interest than higher-rated securities. Due to the focused portfolio, the Fund may have more volatility and more risk than a fund that invests in a greater number of securities. Additional special risks relevant to the Fund involve liquidity, currency, derivatives and hedging. Please refer to the Fund’s prospectus for further details.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. This and other important information is contained in the Fund’s statutory and summary prospectus, which may be obtained by contacting your financial advisor, by calling MFP Investors at 866-EVERMORE (866-383-7667) or on www.evermoreglobal.com. Please read the prospectus carefully before investing.

You cannot invest directly in an index.

MFP Investors LLC is the sub-advisor to the Evermore Global Value Fund, which is distributed by Quasar Distributors, LLC.

7

Evermore Global Value Fund

Performance Information (Unaudited) |

Comparison of Change in Value of $10,000 Investment in Evermore Global Value Fund - Investor Class vs. MSCI All-Country World Index ex USA & HFRX Event Driven Index

Total Annualized Returns For the Periods Ended June 30, 2023: | ||||||||||||||||||||||||

1 Year | 3 Year | 5 Year | 10 Year | Since Inception | Value of | |||||||||||||||||||

Investor Class(1) | 9.85 | % | 0.59 | % | -5.06 | % | 3.07 | % | 2.19 | % | $13,393 | |||||||||||||

Institutional Class(1) | 10.07 | % | 0.85 | % | -4.81 | % | 3.33 | % | 2.44 | % | $13,842 | |||||||||||||

MSCI All-Country World Index ex USA | 12.72 | % | 7.22 | % | 3.52 | % | 4.75 | % | 4.37 | %(2) | $17,812 | |||||||||||||

HFRX Event Driven Index | -4.05 | % | -1.05 | % | 0.02 | % | 0.69 | % | 1.24 | %(2) | $11,814 | |||||||||||||

(1) | The Fund commenced operations on January 1, 2010 as a separate series (the “Predecessor Fund”) of Evermore Funds Trust. Effective as of the close of business on December 27, 2022, the Predecessor Fund was reorganized as a new series of The RBB Fund Trust (the “Reorganization”). The performance shown for periods prior to December 28, 2022 represents the performance of the Predecessor Fund. |

(2) | Index performance shown is from inception date of the Fund and is not the inception date of the index itself. |

This chart illustrates the performance of a hypothetical $10,000 investment made in the Investor Class shares on January 1, 2010 and reflects all Fund expenses. The chart is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The chart assumes reinvestment of capital gains and dividends for a fund and dividends for an index. Index returns do not reflect the effects of fees and expenses. It is not possible to invest directly in an index.

Performance data quoted represents past performance; past performance does not guarantee future results. The performance data quoted reflects fee waivers in effect and would have been less in their absence. The investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 866-EVERMORE or (866-383-7667). The Total Annual Fund Operating Expenses as stated in the Fund’s Prospectus dated March 30, 2023, as revised May 2, 2023, are 1.73% and 1.48% for Investor Class and Institutional Class, respectively. The Total Annual Fund Operating Expenses After Fee Waiver/Expense Reimbursements, as stated in the Fund’s Prospectus dated March 30, 2023, as revised May 2, 2023, are 1.61% and 1.36% for Investor Class and Institutional Class, respectively.

8

Evermore Global Value Fund

Sector Allocation* as a Percentage of Total Portfolio at June 30, 2023 (Unaudited) |

* | Data is expressed as a percentage of total portfolio. Data expressed excludes collateral on loaned securities and forward foreign currency contracts. Please refer to the Schedule of Investments and Schedule of Forward Foreign Currency Contracts for more details on the Fund’s individual holdings. |

9

Evermore Global Value Fund

Expense Example for the Six Months Ended June 30, 2023 (Unaudited) |

As a shareholder of the Evermore Global Value Fund (the “Fund”), you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including investment advisory fees, distribution fees, and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (01/01/23 – 06/30/23).

Actual Expenses

The first line of the table on the next page provides information about actual account values based on actual returns and actual expenses. You will be assessed fees for outgoing wire transfers, returned checks and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Fund’s transfer agent. If you request a redemption be made by wire transfer, currently a $15.00 fee is charged by the Fund’s transfer agent. An Individual Retirement Account (“IRA”) will be charged a $15.00 annual maintenance fee. To the extent the Fund invests in shares of other investment companies as part of its investment strategy, you will indirectly bear your proportionate share of any fees and expenses charged by the underlying funds in which the Fund invests in addition to the expenses of the Fund. Actual expenses of the underlying funds may vary. These expenses are not included in the example below. The example below includes, but is not limited to, investment advisory fees, shareholder servicing fees, fund accounting fees, custody fees and transfer agent fees. However, the example below does not include portfolio trading commissions and related expenses, and other extraordinary expenses as determined under generally accepted accounting principles. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period’’ to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account value and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning | Ending | Expenses Paid | ||||||||||

Investor Class Actual* | $ | 1,000 | $ | 1,074.20 | $ | 12.36 | ||||||

Investor Class Hypothetical (5% annual return before expenses) | $ | 1,000 | $ | 1,025.33 | $ | 12.07 | ||||||

Institutional Class Actual* | $ | 1,000 | $ | 1,076.70 | $ | 10.44 | ||||||

Institutional Class Hypothetical (5% annual return before expenses) | $ | 1,000 | $ | 1,027.19 | $ | 10.19 | ||||||

* | Expenses are equal to the Fund’s annualized net expense ratios for the most recent six-month period of 1.60% for Investor Class shares and 1.35% for Institutional Class shares multiplied by the average account value over the period multiplied by 181/365 (to reflect the one-half year period). |

10

Evermore Global Value Fund

Schedule of Investments at June 30, 2023 (Unaudited) |

Country Allocation for Investments in Securities at June 30, 2023 (Unaudited) |

Country | Long Exposure | |||

United States^ | 21.3 | % | ||

Ireland | 11.0 | % | ||

Sweden | 10.4 | % | ||

France | 9.5 | % | ||

Netherlands | 9.0 | % | ||

Monaco | 6.8 | % | ||

Norway | 6.0 | % | ||

Denmark | 5.0 | % | ||

Italy | 3.2 | % | ||

Austria | 2.3 | % | ||

Switzerland | 1.6 | % | ||

Subtotal | 86.1 | % | ||

Percentages are stated as a percent of net assets.

^ | Excludes cash and equivalent holdings (13.9% of net assets) consisting of Short-Term Investment-Money Market und (13.4%), Securities Held as Collateral on Loaned Securities (4.1%) and net of Liabilities in Excess of Other Assets (-3.6%). |

| Shares | Value | |||||||

| COMMON STOCKS — 75.1% | ||||||||

| Aerospace & Defense — 1.6% | ||||||||

| 108,272 | Montana Aerospace AG (Switzerland) (1) | $ | 1,746,771 | |||||

| Capital Markets — 4.5% | ||||||||

| 86,155 | KKR & Co, Inc. - Class A (United States) | 4,824,680 | ||||||

| Entertainment — 2.3% | ||||||||

| 389,297 | Modern Times Group MTG AB (Sweden) (1) | 2,481,530 | ||||||

| Health Care Equipment & Supplies — 1.8% | ||||||||

| 29,600 | Enovis Corp. (United States) (1) | 1,897,952 | ||||||

| Industrial Conglomerates — 16.7% | ||||||||

| 896,827 | Bollore SE (France) | 5,587,921 | ||||||

| 67,968 | EXOR NV (Netherlands) (1) | 6,057,950 | ||||||

| 287,085 | LIFCO AB (Sweden) | 6,236,608 | ||||||

| 11,824,529 | ||||||||

| IT Services — 0.9% | ||||||||

| 57,00 | Hemnet Group AB (Sweden) | 997,798 | ||||||

| Machinery — 3.0% | ||||||||

| 48,800 | Esab Corp. (United States) | 3,247,152 | ||||||

| Marine — 16.4% | ||||||||

| 1,287,384 | Cadeler A/S (Denmark) (1)(2) | 5,385,289 | ||||||

| 375,973 | Eneti, Inc. - (Monaco) ADR | 4,553,033 | ||||||

| 91,300 | Genco Shipping & Trading, Ltd. - (United States) | 1,280,939 | ||||||

| 739,873 | Hoegh Autoliners ASA (Norway) | 4,194,424 | ||||||

| 456,500 | Stainless Tankers ASA (Norway)(1) | 2,167,754 | ||||||

| 17,581,439 | ||||||||

| Media — 11.2% | ||||||||

| 39,051 | IAC, Inc. (United States)(1) | $ | 2,452,403 | |||||

| 161,892 | Universal Music Group NV (Netherlands) | 3,594,970 | ||||||

| 236,397 | Viaplay Group AB (Sweden) (1) | 1,354,554 | ||||||

| 501,648 | Vivendi SA (France) | 4,601,441 | ||||||

| 12,003,368 | ||||||||

| Oil, Gas & Consumable Fuels — 11.0% | ||||||||

| 571,155 | Calumet Specialty Products Partners LP (United States) (1) | 9,058,518 | ||||||

| 318,300 | DHT Holdings, Inc. - (Monaco) ADR | 2,715,099 | ||||||

| 11,773,617 | ||||||||

| Real Estate Management — 3.2% | ||||||||

| 263,500 | Infrastrutture Wireless Italiane SpA (Italy) | 3,473,386 | ||||||

| Technology Hardware, Storage & Peripherals — 2.3% | ||||||||

| 122,313 | Kontron AG (Austria) | 2,417,111 | ||||||

TOTAL COMMON STOCKS | ||||||||

(Cost $57,626,251) | 80,327,283 | |||||||

The accompanying notes are an integral part of these financial statements.

11

Evermore Global Value Fund

Schedule of Investments at June 30, 2023 (Unaudited), Continued |

| Shares | Principal Amount | |||||

| CORPORATE OBLIGATION — 11.0% | ||||||

| Consumer Finance — 11.0% | ||||||

| 15,140,944 Lamington Road DAC 9.750%, Cash or 14.000% PIK, 4/7/2121 (Ireland)(3)(4)(6)(7) | $ | 11,740,288 | ||||

TOTAL CORPORATE OBLIGATION (Cost $14,570,940) | 11,740,288 | |||||

| SHORT-TERM INVESTMENT — 13.4% | ||||||

| Money Market — 13.4% | ||||||

| 14,273,166 First American Treasury Obligations Fund - Class X, 5.04% (5) | 14,273,166 | |||||

TOTAL SHORT-TERM INVESTMENT (Cost | 14,273,166 | |||||

SECURITIES HELD AS COLLATERAL ON LOANED SECURITIES — 4.1% | ||||||

| Money Market — 4.1% | ||||||

| 4,400,000 First American Government Obligations Fund, Class X, 4.93% (5) | 4,400,000 | |||||

TOTAL SECURITIES HELD AS COLLATERAL | 4,400,000 | |||||

TOTAL INVESTMENTS IN SECURITIES — | 110,740,737 | |||||

| Liabilities in Excess of Other Assets — (3.6)% | (3,838,982 | ) | ||||

TOTAL NET ASSETS — 100.0% | $ | 106,901,755 | ||||

Percentages are stated as a percent of net assets.

(1) | Non-income producing security. |

(2) | All or a portion of this security is on loan. At June 30, 2023 the total value of securities on loan was $4,190,954, which represents 3.9% of total net assets. The remaining contractual maturity of all of the securities lending transactions is overnight and continuous. |

(3) | This security was fair valued in good faith by F/m Investments, LLC d/b/a North Slope Capital, LLC (the “Adviser”), as Valuation Designee, under the oversight of The RBB Fund Trust’s Board of Trustees. The aggregate value of this security at June 30, 2023 was $11,740,288, which represents 11.0% of net assets. |

(4) | Affiliated company as defined by the Investment Company Act of 1940, as amended. Please refer to Note 7 for further disclosures related to this affiliated security. |

(5) | Seven-day yield as of June 30, 2023. |

(6) | The Adviser has deemed all or a portion of this security as illiquid. This security has a value of $11,740,288, which represents 11.0% of total net assets at June 30, 2023. |

(7) | Value determined using significant unobservable inputs. |

Glossary of Terms

ADTR - | American Depositary Receipt |

PIK - | Payment In Kind |

The accompanying notes are an integral part of these financial statements.

12

Evermore Global Value Fund

Schedule of Investments at June 30, 2023 (Unaudited), Continued |

SCHEDULE OF FORWARD FOREIGN CURRENCY CONTRACTS at June 30, 2023 (Unaudited) |

As of June 30, 2023, the Fund had the following forward currency contracts outstanding

Currency to be Received | Currency to be Delivered | |||||||||||||||||||||||||||

Settlement Date | Amount | Currency | USD Value | Amount | Currency | USD Value | Net | |||||||||||||||||||||

7/31/2023 | 1,705,257 | USD | $ | 1,705,257 | 1,524,500 | CHF | $ | 1,709,161 | $ | (3,904 | )(a) | |||||||||||||||||

7/31/2023 | 25,132,635 | USD | 25,132,635 | 23,004,700 | EUR | 25,144,602 | (11,967 | )(a) | ||||||||||||||||||||

7/31/2023 | 11,105,030 | USD | 11,105,030 | 119,857,700 | NOK | 11,180,358 | (75,328 | )(a) | ||||||||||||||||||||

7/31/2023 | 10,676,942 | USD | 10,676,942 | 115,101,700 | SEK | 10,688,418 | (11,477 | )(a) | ||||||||||||||||||||

| $ | 48,619,864 | $ | 48,722,539 | $ | (102,676 | ) | ||||||||||||||||||||||

CHF | Swiss Franc |

EUR | Euro |

NOK | Norwegian Krone |

SEK | Swedish Krona |

USD | U.S. Dollar |

(a) | Counterparty: forward foreign currency contracts outstanding with Bank of New York Mellon. |

The accompanying notes are an integral part of these financial statements.

13

Evermore Global Value Fund

Statement of Assets and Liabilities of June 30, 2023 (Unaudited) |

ASSETS | ||||

Investments in securities, at value (cost $90,870,357) (1) (Note 2) | $ | 110,740,737 | ||

Foreign currency, at value (Cost $7) | 7 | |||

Receivables: | ||||

Capital shares sold | 132,857 | |||

Income from securities loaned(1) | 354 | |||

Dividends and interest, net of foreign withholding taxes | 336,800 | |||

Dividend reclaims | 435,832 | |||

Prepaid expenses | 20,613 | |||

Total assets | 111,667,200 | |||

LIABILITIES | ||||

Unrealized depreciation on forward foreign currency contracts | 102,676 | |||

Payables: | ||||

Capital shares redeemed | 54,170 | |||

Securities lending collateral(1) | 4,400,000 | |||

Investment advisory fees | 86,403 | |||

Administration fees | 47,027 | |||

Custody fees | 6,504 | |||

Distribution fees - Investor Class | 2,961 | |||

Transfer agent fees | 12,609 | |||

Other accrued fees | 48,897 | |||

Total liabilities | 4,765,445 | |||

NET ASSETS | $ | 106,901,755 | ||

COMPONENTS OF NET ASSETS | ||||

Par Value | $ | 10,033 | ||

Paid-in capital | 153,377,709 | |||

Total distributable earnings | (46,485,987 | ) | ||

Net assets | $ | 106,901,755 | ||

Investor Class: | ||||

Net assets | $ | 14,367,347 | ||

Shares issued and outstanding (unlimited number of shares authorized without par value) | 1,359,081 | |||

Net asset value | $ | 10.57 | ||

Institutional Class: | ||||

Net assets | $ | 92,534,408 | ||

Shares issued and outstanding (unlimited number of shares authorized without par value) | 8,673,987 | |||

Net asset value | $ | 10.67 |

(1) | The market value of securities out on loan was $4,190,954 as of June 30, 2023. |

The accompanying notes are an integral part of these financial statements.

14

Evermore Global Value Fund

Statement of Operations for the Six Months Ended June 30, 2023 (Unaudited) |

INVESTMENT INCOME | ||||

Dividends (net of $185,079 foreign withholding taxes) | $ | 1,571,299 | ||

Interest | 1,007,125 | |||

Income from securities loaned | 121,536 | |||

Total investment income | 2,699,960 | |||

EXPENSES (Note 3) | ||||

Advisory fees | 536,063 | |||

Legal fees | 82,393 | |||

Administration and accounting fees | 61,153 | |||

Transfer agent fees | 48,021 | |||

Audit and tax fees | 26,972 | |||

Registration fees | 22,388 | |||

Distribution fees - Investor Class | 18,644 | |||

Custody fees | 16,491 | |||

Shareholder reporting fees | 13,686 | |||

Trustee fees | 573 | |||

Interest expense | 543 | |||

Chief Compliance Officer fees | 402 | |||

Insurance fees | 315 | |||

Miscellaneous fees | 16,090 | |||

Total expenses before reimbursements | 843,734 | |||

Net expense reimbursement by Adviser | (93,552 | ) | ||

Net expenses | 750,182 | |||

Net Investment Income | 1,949,778 | |||

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS, FOREIGN CURRENCIES, FORWARD FOREIGN CURRENCY CONTRACTS & WRITTEN OPTIONS | ||||

Net realized gain (loss) on: | ||||

Investments in unaffiliated securities | (3,962,380 | ) | ||

Foreign currencies | (49,489 | ) | ||

Forward foreign currency contracts | 1,448,115 | |||

Change in net unrealized appreciation (depreciation) on: | ||||

Investments in unaffiliated securities | 7,548,706 | |||

Investments in affiliated securities | 537,504 | |||

Foreign currencies | 15,617 | |||

Forward foreign currency contracts | 525,409 | |||

Net realized and unrealized gain (loss) on investments, foreign currencies, forward foreign currency contracts & written options | 6,063,482 | |||

Net increase in net assets resulting from operations | $ | 8,013,260 |

The accompanying notes are an integral part of these financial statements.

15

Evermore Global Value Fund

Statements of Changes in Net Assets |

| Six Months | Year Ended | ||||||

INCREASE (DECREASE) IN NET ASSETS FROM: | ||||||||

OPERATIONS | ||||||||

Net investment income (loss) | $ | 1,949,778 | $ | 4,369,491 | ||||

Net realized gain (loss) on investments, foreign currency transactions, forward foreign currency contracts & written options | (2,563,754 | ) | (12,069,254 | ) | ||||

Change in unrealized depreciation on investments, foreign currency transactions, forward foreign currency contracts & written options | 8,627,236 | (45,380,079 | ) | |||||

Net increase (decrease) in net assets resulting from operations | 8,013,260 | (53,079,842 | ) | |||||

DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS (NOTE 6) | ||||||||

Investor Class | — | (324,216 | ) | |||||

Institutional Class | — | (2,263,202 | ) | |||||

Total distributions to shareholders | — | (2,587,418 | ) | |||||

CAPITAL SHARE TRANSACTIONS | ||||||||

Net decrease in net assets derived from net change in outstanding shares – Investor Class | (1,593,042 | ) | (1,895,450 | ) | ||||

Net decrease in net assets derived from net change in outstanding shares – Institutional Class | (3,967,789 | ) | (64,577,199 | ) | ||||

Total decrease in net assets from capital share transactions | (5,560,831 | ) | (66,472,649 | ) | ||||

Total increase/(decrease) in net assets | 2,452,429 | (122,139,909 | ) | |||||

NET ASSETS | ||||||||

Beginning of period | 104,449,326 | 226,589,235 | ||||||

End of period | $ | 106,901,755 | $ | 104,449,326 | ||||

Summary of capital share transactions is as follows:

| Six Months Ended June 30, 2023 (Unaudited) | Year Ended December 31, 2022 | |||||||||||||||

| Investor Class | Share | Value | Share | Value | ||||||||||||

| Shares sold | 85,915 | $ | 907,033 | 169,348 | $ | 1,892,776 | ||||||||||

| Shares issued in reinvestment of distributions | — | — | 30,832 | 313,248 | ||||||||||||

Shares redeemed* | (236,261 | ) | (2,500,075 | ) | (375,107 | ) | (4,101,474 | ) | ||||||||

| Net decrease | (150,346 | ) | $ | (1,593,042 | ) | (174,927 | ) | $ | (1,895,450 | ) | ||||||

| Six Months Ended June 30, 2023 (Unaudited) | Year Ended December 31, 2022 | |||||||||||||||

| Institutional Class | Share | Value | Share | Value | ||||||||||||

| Shares sold | 583,859 | $ | 6,248,560 | 1,664,628 | $ | 17,782,419 | ||||||||||

| Shares issued in reinvestment of distributions | — | — | 214,739 | 2,196,781 | ||||||||||||

Shares redeemed* | (948,452 | ) | (10,216,349 | ) | (7,622,197 | ) | (84,556,399 | ) | ||||||||

| Net decrease | (364,593 | ) | $ | (3,967,789 | ) | (5,742,830 | ) | $ | (64,577,199 | ) | ||||||

* | Prior to December 28, 2022, there was a 2.00% redemption fee to the value of shares redeemed or exchanged within 90 days of purchase. The redemption fees were retained by the Fund for the benefit of the remaining shareholders and recorded as paid-in capital. Effective December 28, 2022, the Fund eliminated its redemption fee. |

The accompanying notes are an integral part of these financial statements.

16

Evermore Global Value Fund

Financial Highlights for a capital share outstanding throughout the period/year |

Investor Class

Six Months | Year Ended December 31, | |||||||||||||||||||||||

| 2023 | 2022^ | 2021 | 2020 | 2019 | 2018 | ||||||||||||||||||

Net asset value, beginning of year | $ | 9.84 | $ | 13.66 | $ | 13.24 | $ | 14.26 | $ | 11.70 | $ | 15.08 | ||||||||||||

INCOME FROM INVESTMENT OPERATIONS | ||||||||||||||||||||||||

Net investment income (loss)* | 0.17 | 0.28 | 0.19 | (0.00 | )1 | 0.09 | 0.06 | |||||||||||||||||

Net realized and unrealized gain (loss) on investments | 0.56 | (3.89 | ) | 0.59 | (1.00 | ) | 2.83 | (3.16 | ) | |||||||||||||||

Total from investment operations | 0.73 | (3.61 | ) | 0.78 | (1.00 | ) | 2.92 | (3.10 | ) | |||||||||||||||

LESS DISTRIBUTIONS | ||||||||||||||||||||||||

From net investment income | — | (0.21 | ) | (0.36 | ) | (0.02 | ) | (0.10 | ) | (0.06 | ) | |||||||||||||

Net realized gains | — | — | — | — | (0.26 | ) | (0.22 | ) | ||||||||||||||||

Total distributions | — | (0.21 | ) | (0.36 | ) | (0.02 | ) | (0.36 | ) | (0.28 | ) | |||||||||||||

Paid-in capital from redemption fees2 | — | — | 0.00 | 1 | 0.00 | 1 | 0.00 | 1 | 0.00 | 1 | ||||||||||||||

Net asset value, end of year | $ | 10.57 | $ | 9.84 | $ | 13.66 | $ | 13.24 | $ | 14.26 | $ | 11.70 | ||||||||||||

Total return4 | 7.42 | %(5) | (26.48 | )% | 5.93 | % | (7.01 | )% | 25.05 | % | (21.07 | )% | ||||||||||||

SUPPLEMENTAL DATA | ||||||||||||||||||||||||

Net assets, end of year (thousands) | $ | 14,367 | $ | 14,847 | $ | 23,009 | $ | 27,956 | $ | 61,296 | $ | 63,584 | ||||||||||||

Portfolio turnover rate | 12 | %(5) | 17 | % | 33 | % | 21 | % | 28 | % | 29 | % | ||||||||||||

RATIO OF EXPENSES TO AVERAGE NET ASSETS3 | ||||||||||||||||||||||||

Before expense waivers/reimbursement and recoupments, including interest and dividend expense | 1.77 | %(6) | 1.72 | % | 1.57 | % | 1.55 | % | 1.47 | % | 1.44 | % | ||||||||||||

Before expense waivers/reimbursement and recoupments, excluding interest and dividend expense | 1.77 | %(6) | 1.72 | % | 1.57 | % | 1.55 | % | 1.47 | % | 1.44 | % | ||||||||||||

After expense waivers/reimbursement and recoupments, including interest and dividend expense | 1.60 | %(6) | 1.60 | % | 1.57 | % | 1.55 | % | 1.47 | % | 1.44 | % | ||||||||||||

After expense waivers/reimbursement and recoupments, excluding interest and dividend expense | 1.60 | %(6) | 1.60 | % | 1.57 | % | 1.55 | % | 1.47 | % | 1.44 | % | ||||||||||||

The accompanying notes are an integral part of these financial statements.

17

Evermore Global Value Fund

Financial Highlights for a capital share outstanding throughout the period/year, Continued |

Six Months | Year Ended December 31, | |||||||||||||||||||||||

| 2023 | 2022^ | 2021 | 2020 | 2019 | 2018 | ||||||||||||||||||

RATIO OF NET INVESTMENT INCOME (LOSS) TO AVERAGE NET ASSETS2 | ||||||||||||||||||||||||

Before expense waivers/reimbursement and recoupments, including interest and dividend expense | 3.19 | %(6) | 2.39 | % | 1.35 | % | (0.04 | )% | 0.69 | % | 0.35 | % | ||||||||||||

After expense waivers/reimbursement and recoupments, including interest and dividend expense | 3.37 | %(6) | 2.52 | % | 1.35 | % | (0.04 | )% | 0.69 | % | 0.35 | % | ||||||||||||

Portfolio turnover is calculated for the Fund as a whole.

^ | Prior to the close of business on December 27, 2022, the Fund was a series (the “Predecessor Fund”) of Evermore Funds Trust, an open-end management investment company organized as a Massachusetts business trust. The Predecessor Fund was reorganized into the Fund following the close of business on December 27, 2022 (the “Reorganization”). As a result of the Reorganization, the performance and accounting history of the Predecessor Fund was assumed by the Fund. Performance and accounting information prior to December 28, 2022 included herein is that of the Predecessor Fund. |

# | Effective March 31, 2023, the Fund’s former investment adviser (the “Predecessor Adviser”), sold substantially all of its business and advisory assets to MFP Investors LLC (“the Sub-Adviser”). In connection with the change of control, F/m Investments, LLC d/b/a North Slope Capital, LLC was appointed as the investment adviser to the Fund and the Sub-Adviser was appointed as sub-adviser to the Fund. The performance shown for periods prior to March 31, 2023 represents the performance of the Fund or Predecessor Fund, as applicable, under the management of the Predecessor Adviser. |

* | Calculated using the average shares outstanding method. |

1 | Amount less than $0.01. |

2 | Prior to December 28, 2022, there was a 2.00% redemption fee to the value of shares redeemed or exchanged within 90 days of purchase. The redemption fees were retained by the Fund for the benefit of the remaining shareholders and recorded as paid-in capital. Effective December 28, 2022, the Fund eliminated its redemption fee. |

3 | Does not include expenses of the investment companies in which the Fund invests. |

4 | Total investment return/(loss) is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestments of dividends and distributions, if any. Total investment return does not reflect any applicable sales charge. |

5 | Not Annualized |

6 | Annualized |

The accompanying notes are an integral part of these financial statements.

18

Evermore Global Value Fund

Financial Highlights for a capital share outstanding throughout the period/year, Continued |

Institutional Class

Six Months | Year Ended December 31, | |||||||||||||||||||||||

| 2023 | 2022^ | 2021 | 2020 | 2019 | 2018 | ||||||||||||||||||

Net asset value, beginning of year | $ | 9.91 | $ | 13.77 | $ | 13.35 | $ | 14.35 | $ | 11.77 | $ | 15.20 | ||||||||||||

INCOME FROM INVESTMENT OPERATIONS | ||||||||||||||||||||||||

Net investment income (loss)* | 0.20 | 0.33 | 0.23 | 0.03 | 0.12 | 0.09 | ||||||||||||||||||

Net realized and unrealized gain (loss) on investments | 0.56 | (3.95 | ) | 0.59 | (1.00 | ) | 2.86 | (3.30 | ) | |||||||||||||||

Total from investment operations | 0.76 | (3.62 | ) | 0.82 | (0.97 | ) | 2.98 | (3.21 | ) | |||||||||||||||

LESS DISTRIBUTIONS | ||||||||||||||||||||||||

From net investment income | — | (0.24 | ) | (0.40 | ) | (0.03 | ) | (0.14 | ) | 0.00 | ||||||||||||||

Net realized gains | — | — | — | — | (0.26 | ) | (0.22 | ) | ||||||||||||||||

Total distributions | — | (0.24 | ) | (0.40 | ) | (0.03 | ) | (0.40 | ) | (0.22 | ) | |||||||||||||

Paid-in capital from redemption fees2 | — | — | 0.00 | 1 | 0.00 | 1 | 0.00 | 1 | 0.00 | 1 | ||||||||||||||

Net asset value, end of year | $ | 10.67 | $ | 9.91 | $ | 13.77 | $ | 13.35 | $ | 14.35 | $ | 11.77 | ||||||||||||

Total return4 | 7.67 | %(5) | (26.35 | )% | 6.16 | % | (6.78 | )% | 25.41 | % | (20.92 | )% | ||||||||||||

SUPPLEMENTAL DATA | ||||||||||||||||||||||||

Net assets, end of year (thousands) | $ | 92,534 | $ | 89,603 | $ | 203,580 | $ | 253,364 | $ | 533,731 | $ | 443,904 | ||||||||||||

Portfolio turnover rate | 12 | %(5) | 17 | % | 33 | % | 21 | % | 28 | % | 29 | % | ||||||||||||

RATIO OF EXPENSES TO AVERAGE NET ASSETS3 | ||||||||||||||||||||||||

Before expense waivers/reimbursement and recoupments, including interest and dividend expense | 1.52 | %(6) | 1.47 | % | 1.32 | % | 1.29 | % | 1.22 | % | 1.19 | % | ||||||||||||

Before expense waivers/reimbursement and recoupments, excluding interest and dividend expense | 1.52 | %(6) | 1.47 | % | 1.32 | % | 1.29 | % | 1.22 | % | 1.19 | % | ||||||||||||

After expense waivers/reimbursement and recoupments, including interest and dividend expense | 1.35 | %(6) | 1.35 | % | 1.32 | % | 1.29 | % | 1.22 | % | 1.19 | % | ||||||||||||

After expense waivers/reimbursement and recoupments, excluding interest and dividend expense | 1.35 | %(6) | 1.35 | % | 1.32 | % | 1.29 | % | 1.22 | % | 1.19 | % | ||||||||||||

The accompanying notes are an integral part of these financial statements.

19

Evermore Global Value Fund

Financial Highlights for a capital share outstanding throughout the period/year, Continued |

Six Months | Year Ended December 31, | |||||||||||||||||||||||

| 2023 | 2022^ | 2021 | 2020 | 2019 | 2018 | ||||||||||||||||||

RATIO OF NET INVESTMENT INCOME (LOSS) TO AVERAGE NET ASSETS2 | ||||||||||||||||||||||||

Before expense waivers/reimbursement and recoupments, including interest and dividend expense | 3.47 | %(6) | 2.71 | % | 1.60 | % | 0.21 | % | 0.91 | % | 0.60 | % | ||||||||||||

After expense waivers/reimbursement and recoupments, including interest and dividend expense | 3.65 | %(6) | 2.83 | % | 1.60 | % | 0.21 | % | 0.91 | % | 0.60 | % | ||||||||||||

Portfolio turnover is calculated for the Fund as a whole.

^ | Prior to the close of business on December 27, 2022, the Fund was a series (the “Predecessor Fund”) of Evermore Funds Trust, an open-end management investment company organized as a Massachusetts business trust. The Predecessor Fund was reorganized into the Fund following the close of business on December 27, 2022 (the “Reorganization”). As a result of the Reorganization, the performance and accounting history of the Predecessor Fund was assumed by the Fund. Performance and accounting information prior to December 28, 2022 included herein is that of the Predecessor Fund. |

# | Effective March 31, 2023, the Fund’s former investment adviser (the “Predecessor Adviser”), sold substantially all of its business and advisory assets to MFP Investors LLC (“the Sub-Adviser”). In connection with the change of control, F/m Investments, LLC d/b/a North Slope Capital, LLC was appointed as the investment adviser to the Fund and the Sub-Adviser was appointed as sub-adviser to the Fund. The performance shown for periods prior to March 31, 2023 represents the performance of the Fund or Predecessor Fund, as applicable, under the management of the Predecessor Adviser. |

* | Calculated using the average shares outstanding method. |

1 | Amount less than $0.01. |

2 | Prior to December 28, 2022, there was a 2.00% redemption fee to the value of shares redeemed or exchanged within 90 days of purchase. The redemption fees were retained by the Fund for the benefit of the remaining shareholders and recorded as paid-in capital. Effective December 28, 2022, the Fund eliminated its redemption fee. |

3 | Does not include expenses of the investment companies in which the Fund invests. |

4 | Total investment return/(loss) is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestments of dividends and distributions, if any. Total investment return does not reflect any applicable sales charge. |

5 | Not Annualized |

6 | Annualized |

20

Evermore Global Value Fund

Notes to Financial Statements June 30, 2023 (Unaudited) |

NOTE 1 – ORGANIZATION

The Evermore Global Value Fund (the “Fund”) is a series of The RBB Fund Trust (the “Trust”). The Trust was organized as a Delaware statutory trust on August 29, 2014 and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Fund commenced operations on January 1, 2010 as a separate series (the “Predecessor Fund”) of Evermore Funds Trust, a Massachusetts business trust. Effective as of the close of business on December 27, 2022, the Predecessor Fund was reorganized into a new series of the Trust in a tax-free reorganization (the “Reorganization”). The Agreement and Plan of Reorganization pursuant to which the Reorganization was accomplished was approved by shareholders of the Predecessor Fund on December 21, 2022. Unless otherwise indicated, references to the “Fund” in these Notes to Financial Statements refer to the Predecessor Fund and Fund. Evermore Global Advisors, LLC (the “Predecessor Adviser”) served as the investment adviser to the Predecessor Fund until December 27, 2022 and served as the investment adviser to the Fund until March 31, 2023. Effective March 31, 2023, the Predecessor Adviser, sold substantially all of its business and advisory assets to MFP Investors LLC (the “Sub-Adviser” or “MFP”). In connection with the change of control of the Predecessor Adviser, F/m Investments, LLC d/b/a North Slope Capital, LLC (the “Adviser”) was appointed as the investment adviser to the Fund, MFP was appointed as sub-adviser to the Fund, and David Marcus and Thomas O were hired by MFP to be the sole portfolio managers of the Fund. Other than the Adviser replacing the Predecessor Adviser as the Fund’s investment adviser and MFP becoming the sub-adviser to the Fund, the change of control did not result in any significant changes to the day-to-day management or operation of the Fund.

The investment objective of the Fund is to seek capital appreciation by investing in securities from markets around the world, including U.S. markets.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 “Financial Services-Investment Companies.”

The Fund offers Investor Class and Institutional Class shares. Each class of shares has equal rights as to earnings and assets except that each class bears different distribution expenses. Each class of shares has exclusive voting rights with respect to matters that affect just that class. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets. Investor Class shares have no sales charge. Institutional Class shares have no sales charge and are offered primarily for direct investment by investors such as pension and profit sharing plans, employee benefit trusts, certain financial intermediaries, endowments, foundations and corporations. For Investor Class and Institutional Class shares, the offering and redemption price per share for the Fund is equal to the Fund’s net asset value (“NAV”) per share.

The end of the reporting period for the Fund is June 30, 2023, and the period covered by these Notes to Financial Statements is the six months ended June 30, 2023 (the “current fiscal period”).

As a tax-free reorganization, any unrealized appreciation or depreciation on the securities held by the Fund on the date of Reorganization was treated as a non-taxable event, thus the cost basis of the securities held reflects their historical cost basis as of the date of Reorganization. Immediately prior to the Reorganization, the net assets, fair value of investments, net unrealized appreciation and fund shares outstanding of the Predecessor Fund were as follows:

| Net Assets | Fair Value of Investments | Net Unrealized Appreciation | Fund Shares Outstanding |

| $104,322,957 | $107,265,185 | $13,373,967 | 10,773,951 |

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund. These policies are in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”).

A. | Investment Valuation and Fair Value Measurement. The Board of Trustees (“Board”) of the Trust has adopted a pricing and valuation policy for use by the Fund and its Valuation Designee (as defined below) in calculating the Fund’s NAV. Pursuant to Rule 2a-5 under the 1940 Act, the Fund has designated the Adviser as its “Valuation Designee” to perform all of the fair value determinations as well as to perform all of the responsibilities that may be performed by the Valuation Designee in accordance with Rule 2a-5. The Valuation Designee is authorized to make all necessary determinations of the fair values of portfolio securities and other assets for which market quotations are not readily available or if it is deemed that the prices obtained from brokers and dealers or independent pricing services are unreliable. All domestic equity securities that are traded on a national securities exchange, except those listed on the National Association of Securities Dealers Automated Quotation System (“NASDAQ”) Global Market® are valued at the last reported sale price on the exchange on which the security is principally traded. Securities traded on NASDAQ will be valued at the NASDAQ Official Closing Price on each business |

21

Evermore Global Value Fund

Notes to Financial Statements June 30, 2023, (Unaudited), Continued |

day. If, on a particular day, an exchange-traded or NASDAQ security does not trade, then the mean between the most recent quoted bid and ask prices will be used, except on days when the ask price is more than 10% greater than the bid price. In such instances, the Valuation Designee will price the security based on fair value. All equity securities that are not traded on a listed exchange are valued at the last sale price in the over-the-counter (“OTC”) market. If a non-exchange traded security does not trade on a particular day, then the mean between the last quoted closing bid and ask price will be used, except on days when the ask price is more than 10% greater than the bid price. In such instances, the Valuation Designee will price the security based on fair value.

The Fund invests substantially in securities traded on foreign exchanges (see “Foreign Currency Translation” below). Investments that are primarily traded on foreign exchanges are generally valued in their local currencies as of the close of their primary exchange or market, or if there were no transactions on such day, at the mean between the bid and ask prices, except on days when the ask price is more than 10% greater than the bid price. In such instances, the Valuation Designee will price the security based on fair value. The local prices are converted to U.S. dollars using the applicable currency exchange rates as of the close of the New York Stock Exchange (“NYSE”). Exchange rates are provided daily by recognized independent pricing agents. Foreign currency forward contracts are valued at the current day’s interpolated foreign exchange rate, as calculated using the current day’s exchange rate, and the relevant forward rates provided by an independent pricing service.

There may be less publicly available information about a foreign company than about a U.S. company. Foreign issuers may not be subject to accounting, auditing and financial reporting standards and requirements comparable to, or as uniform as, those of U.S. issuers. The number of securities traded, and the frequency of such trading, in non-U.S. securities markets, while growing in volume, is for the most part, substantially less in U.S. markets. As a result, securities of many foreign issuers may be less liquid and their prices more volatile than securities of comparable U.S. issues. Transaction costs, the costs associated with buying and selling securities on non-U.S. securities markets may be higher than in the U.S. There is generally less government supervision and regulation of exchanges, brokers and issuers than there is in the U.S. The Fund’s foreign investments may include both voting and non-voting securities, sovereign debt and participations in foreign government deals. The Fund may have greater difficulty taking appropriate legal action with respect to foreign issuers in U.S. courts.

For foreign securities traded on foreign exchanges, the Trust has selected Intercontinental Exchange’s Fair Value Information Services (“FVIS”) to provide pricing data with respect to foreign security holdings held by the Fund. The use of this third-party pricing service is designed to capture events occurring after a foreign exchange closes that may affect the value of certain holdings of the Fund’s securities traded on those foreign exchanges. The Fund utilizes a “trigger level”, which is a pre-determined percentage move in a specified index that must occur before foreign securities will be fair value priced using FVIS prices. The Fund utilizes a “confidence interval” when determining the use of the FVIS prices. The confidence interval is a measure of the historical relationship that each foreign exchange traded security has to movements in various indices and the price of the security’s corresponding American Depositary Receipt, if one exists. FVIS provides the confidence interval for each security for which it provides a price. If the FVIS provided price falls within the confidence interval, the Fund will value the particular security at that price. If the FVIS provided price does not fall within the confidence interval, the particular security will be valued at the preceding closing price on its respective foreign exchange, or if there were no transactions on such day, at the mean between the bid and asked prices. There were no foreign equities fair valued using FVIS as of June 30, 2023.

Securities for which quotations are not readily available are fair valued in accordance with the Fund’s pricing and valuation policy. When a security is “fair valued,” consideration is given to the facts and circumstances relevant to the particular situation. Fundamental valuation methods may be used to fair value a security held by the Fund, which methods may include, but are not limited to, an analysis of the effect of any restrictions on the resale of the security, industry analysis and trends, significant changes in the issuer’s financial position, and any other event that could have a significant impact on the value of the security. The use of fair value pricing by a fund may cause the NAV of its shares to differ significantly from the NAV that would be calculated without regard to such considerations.

As described above, the Fund utilizes various methods to measure the fair value of its investments on a recurring basis. U.S. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

Level 1 — | Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. The types of assets generally included in this category are domestic equities listed in active markets and foreign equities listed in active markets that have not been fair valued using FVIS. |

Level 2 — | Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, credit risk, yield curves and similar data. The types of assets generally included in this category are bonds, financial instruments classified as derivatives and foreign equities fair valued using FVIS. |

22

Evermore Global Value Fund

Notes to Financial Statements June 30, 2023, (Unaudited), Continued |

Level 3 — | Significant unobservable inputs that are supported by limited or no market activity. Level 3 may include financial instruments whose values are determined using indicative market quotes or required significant management judgment or estimation. These unobservable valuation inputs may include estimates for current yields, maturity/duration, prepayment speed, default rates and indicative market quotes for comparable investments along with other assumptions relating to credit quality, collateral value, complexity of the investment structure, general market conditions and liquidity. This category may also include investments where trading has been halted or there are certain restrictions on trading. While these investments are priced using unobservable inputs, the valuation of these investments reflects the best available data and management believes the prices are a reasonable representation of exit price. |

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following is a summary of the level inputs used to value the Fund’s net assets as of June 30, 2023 (see Schedule of Investments for industry breakout):

Level 1 | Level 2 | Level 3 | Total | |||||||||||||

Assets | ||||||||||||||||

Common Stocks | $ | 80,327,283 | $ | — | $ | — | $ | 80,327,283 | ||||||||

Corporate Obligations | — | — | 11,740,288 | 11,740,288 | ||||||||||||

Short-Term Investments | 14,273,166 | — | — | 14,273,166 | ||||||||||||

Securities Held as Collateral on Loaned Securities | 4,400,000 | — | — | 4,400,000 | ||||||||||||

Total Investments in Securities | 99,000,449 | — | 11,740,288 | 110,740,737 | ||||||||||||

Unrealized appreciation on Forward Foreign Currency * | — | — | — | — | ||||||||||||

Total Assets | $ | 99,000,449 | $ | — | $ | 11,740,288 | $ | 110,740,737 | ||||||||

Liabilities | ||||||||||||||||

Unrealized depreciation on Forward Foreign Currency* | — | 102,676 | — | 102,676 | ||||||||||||

Total Liabilities | $ | — | $ | 102,676 | $ | — | $ | 102,676 | ||||||||

* | Forward foreign currency contracts are reflected at the unrealized appreciation (depreciation). |

Below is a reconciliation of Level 3 assets for which significant unobservable inputs were used to determine fair value:

| Description | Common Stocks | Corporate Obligations | Warrants | |||||||||

| Balance as of January 1, 2023 | — | $ | 11,202,784 | — | ||||||||

| Purchases | — | — | — | |||||||||

| Sales proceeds and paydowns | — | — | — | |||||||||

| Accreted discounts, net | — | — | — | |||||||||

| Corporate Actions | — | — | — | |||||||||

| Realized gain (loss) | — | — | — | |||||||||

| Change in unrealized appreciation (depreciation) | — | 537,504 | — | |||||||||

| Transfers into/(out of ) Level 3 | — | — | — | |||||||||

| Balance as of June 30, 2023 | $ | — | $ | 11,740,288 | $ | — | ||||||

| Change in unrealized appreciation (depreciation) during the current fiscal period for Level 3 investments held at June 30, 2023 | $ | — | $ | 537,504 | $ | — | ||||||

23

Evermore Global Value Fund

Notes to Financial Statements June 30, 2023, (Unaudited), Continued |