UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-23016

(Investment Company Act file number)

Alternative Credit Income Fund

(Exact name of Registrant as specified in charter)

650 Madison Avenue, 23rd Floor

New York, NY 10022

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

Corporation Trust Center, 1209 Orange Street

Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 891-2880

Date of fiscal year end: September 30

Date of reporting period: October 1, 2022– September 30, 2023

Item 1. Reports to Stockholders.

| TABLE OF CONTENTS | |

| Shareholder Letter | 1 |

| Portfolio Update | 7 |

| Consolidated Schedule of Investments | 9 |

| Consolidated Statement of Assets and Liabilities | 16 |

| Consolidated Statement of Operations | 17 |

| Consolidated Statements of Changes in Net Assets | 18 |

| Consolidated Statement of Cash Flows | 20 |

| Financial Highlights | |

| Class A | 21 |

| Class C | 22 |

| Class W | 23 |

| Class I | 24 |

| Class L | 25 |

| Notes to Consolidated Financial Statements | 26 |

| Report of Independent Registered Public Accounting Firm | 38 |

| Additional Information | 39 |

| Trustees & Officers | 41 |

| Privacy Notice | 44 |

| Alternative Credit Income Fund | Shareholder Letter |

| | September 30, 2023 (Unaudited) |

Dear Shareholders:

We are pleased to share with our partners the performance for the Alternative Credit Income Fund (ticker: RCIIX)1 for fiscal year ended September 30, 2023, as well as to provide our perspective on the current market backdrop.

The Fund returned 4.35%1 in fiscal 2023, with notable strength in the back-half of the period.

We will concede our vulnerability to be biased toward fixed income, in general, and corporate credit, in particular. Nevertheless, it would be difficult to temper our enthusiasm about the backdrop. In short, opportunities abound.

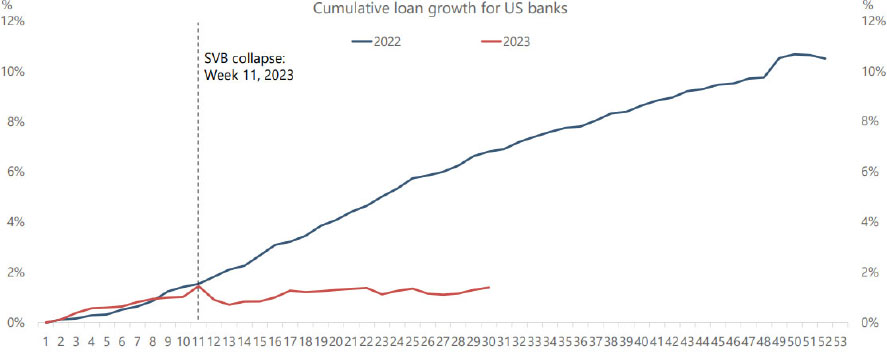

Enough time has passed since the collapse of Silicon Valley Bank to quell concerns about a widespread banking panic. However, as reflect in the following chart, credit conditions in the U.S. have tightened notably this year:

Cumulative Loan Growth in the U.S. Banks by Week

Source: FRB

Some restraining of lending has been intentional: the Fed has hiked +550bps in 18 months to temper economic activity to combat inflation. However, a derivative of these rate hikes has amplified the pullback by banks.

| Annual Report | September 30, 2023 | 1 |

| Alternative Credit Income Fund | Shareholder Letter |

| | September 30, 2023 (Unaudited) |

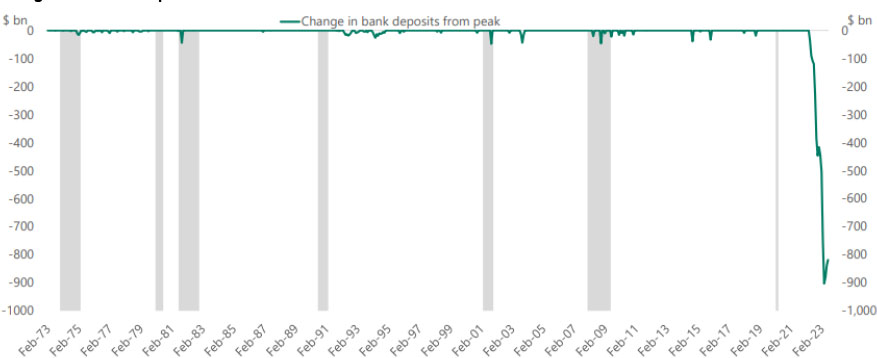

There is currently a yawning gap between what investors earn holding dollars inside banks versus outside banks. Federal Deposit Insurance Corp. data suggests the average cost of deposits at U.S. banks is currently 1.78% compared to the Fed Fund rate above 5.0%—the widest gap since the 1980s.6 As this chart starkly reveals, dollars have been racing out of banks as depositors seek higher yielding alternatives like money market funds or Treasuries:

Change in U.S. bank deposits

Source: FRB, Havner Analytics

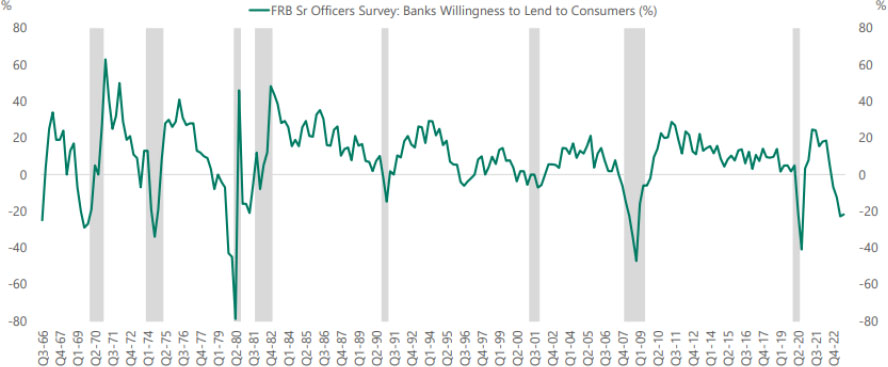

This “cash sorting” or “depositor flight” has crippled U.S. banks’ ability and willingness to lend. In fact, Senior Loan Officer Survey Data suggests that credit conditions are approaching levels normally associated with recessions:

Federal Reserve Bank: Sr. Officers Survey: Banks Willingness to Lend to Consumers (%)

Source: FRB, Bloomberg

| Alternative Credit Income Fund | Shareholder Letter |

| | September 30, 2023 (Unaudited) |

Forecasting the direction of the U.S. economy is difficult given the many discordant signals. The most notably positive data pertains to jobs. An economy at full employment (and with more openings than workers) does not suggest imminent collapse. Layoffs have remained muted as companies appear reticent to lose a workforce they have spent years trying to re-build. Additionally, household and corporate balance sheets remain ironclad, bolstered by extraordinary COVID-era fiscal and monetary accommodation.

Despite some clear positives, we remain concerned that lower credit creation risks tipping us into a downturn. As evident in the chart below, changes in credit conditions have historically closely tracked changes in U.S. GDP:

Sr. Loan Officer Opinion Survey C&I Lending Standards vs. Changes in U.S. GDP

Source: FRB, Bloomberg

The gap between current lending standards and changes in GDP augers concern, in our view. To reconcile the current disconnect, amid the Fed’s “higher for longer” drumbeat, we view GDP declines as more likely than a loosening of credit conditions.

Hence, we view a so-called “soft landing” as fanciful. This is not to suggest a searing 2008-like downturn awaits. Again, jobs remain plentiful, and the economy lacks meaningful distortions or misallocations of capital that would lead to a protracted downturn. Nevertheless, I believe the economy will not be able to escape +500bps of higher rates without a modicum of economic pain.

As we have noted before, we never cheer for economic uncertainty. However, we have designed our structure and strategy to capitalize on these inevitable periods of tumult. Today, small- and medium-sized businesses still want and, importantly, many need capital. Traditional banks pulling back has created more opportunities for our firm and fund to provide solutions.

As an aside, when this letter publishes, the Fund will have celebrated its eight-year anniversary—a milestone we are endlessly proud of and thank our partners for helping us achieve. We have successfully navigated our shareholders through three extreme market dislocations: the Oil & Gas panic, rate collapse in 4Q 2018 and COVID. Outside of those turbulent periods, the current backdrop provides the deepest pipeline of deals we have ever seen. At the moment particularly in private markets, again, opportunity abounds.

Additionally, should the backdrop deteriorate, we expect even more opportunities to source dislocated liquid credit. We would ask our partners: what else in your portfolio directly benefits from downturns? Over eight years, the Credit Income Fund has demonstrated its ability to translate market disruptions into meaningful gains for our shareholders. Thus, we believe we are ideally positioned for the current environment.

| Annual Report | September 30, 2023 | 3 |

| Alternative Credit Income Fund | Shareholder Letter |

| | September 30, 2023 (Unaudited) |

Fund Performance

The Fund generated a gain of 4.31% in the six-month period ended 9/30/2023. Cumulative returns remains our focus, however, because they reflect the Fund’s longer-term investing perspective:

| Alternative Credit Income Fund (RCIIX) | 66.7% |

| Barclay’s U.S. Aggregate Total Return Value Index2 | 3.9% |

| Morningstar LSTA US Leveraged Loan TR USD Index3 | 45.4% |

| Bank of America High Yield Index4 | 41.6% |

Source: Bloomberg. Total return from 10/27/2015 through September 30, 2023

I would argue a Fund cannot beat its benchmark by more than 1.5x by focusing on quarterly performance.

We would highlight a recent realization as illustrative of the Fund’s long-view of markets. Investors may recall that the Credit Income Fund purchased convertible bonds for Whiting Petroleum at a significant discount in early 2020. We had expected a par payoff at maturity but anticipated a strong recovery in the unlikely event of a restructuring. Despite sufficient liquidity, Whiting elected to seek the shelter of bankruptcy at the height of the pandemic.

In early October, given our concern about the broader market, the Fund sold its reorg equity in Chord Energy (the successor entity of Whiting), for a 16.1% IRR and 1.67x MOIC. We actively seek to avoid restructurings given the resulting NAV “noise.” However, our long-term perspective enabled us to correct our misstep and maximize return for our shareholders.

As for a recent private market deal, the Credit Income Fund recently extended credit to a company known as Phillips Pet & Supply—a leading distributor of pet supplies to specialty retailers. We note that BC Partners' private equity segment owns PetSmart and its online platform Chewy, providing us deep insight into this category.

Our $5mn facility to Phillips Pet slots ahead of the company’s existing Term Loan, putting our shareholders in a “super priority” position. Our rate of SOFR+700bps and 5 points of discount translates into a yield of ~13%—an objectively strong return profile in any market.

Again, we do not extend loans with the intention of taking over businesses. However, being at the top of the capital structure positions us to steer positive outcomes should a situation deteriorate. BC Partners’ unparalleled expertise in the pet channel would enable us to maximize returns should the Phillips loan not unfold as expected. This risk-adjusted perspective only amplifies the attractive return profile of our Phillips Pet & Supply loan.

Positioning

Before digging into our allocations, we hope to modestly change our disclosure in future quarters. We feel our historical categories do not sufficiently describe the underlying investments. Hence, we intend to provide more portfolio detail in the coming periods. To be clear, this does not reflect a change in strategy, merely a semantic shift.

Private Credit (27.1% of the portfolio at 9/30/2023)

The Fund has historically characterized its allocations to LP stakes of credit funds as “Private Credit.” These assets comprised 27.1% of our assets at period end.

As we have previously shared, this segment has been de-emphasized as part of the BC Partners transition. The Fund’s expanded private market capabilities provide our investors a more efficient point of access. These Private Credit stakes nonetheless remain important to our shareholders in providing institutional access as well as providing asset level and manager diversification. We have nearly fully deployed our Private Credit commitments and have begun receiving returns of capital from certain vehicles in winddown.

We continue to actively manage this segment, seeking both primary and secondary investments, but have made no new allocations in the period.

Public Credit (4.5%)

We have classified our investments in public Business Development Companies (or BDCs) as “Public Credit.” These assets made up 4.5% of the portfolio at fiscal yearend.

Fundamentals for BDCs have remained notably strong. Higher interest rates have boosted dividend income and portfolio stress has remained limited, with both non-accrual and defaults well below historic levels.

| Alternative Credit Income Fund | Shareholder Letter |

| | September 30, 2023 (Unaudited) |

The Fund has generated unique total returns within this oft-ignored market niche. Plus, as “point-and-click” assets, Public Credit enables the Fund to unlock an illiquidity premium elsewhere in the portfolio.

Nevertheless, BDCs demand active management, in our view. Because they are largely owned by retail investors, BDCs have often exhibited volatility during downturns. Late in the credit cycle, we have reduced our Public Credit exposure to mute future NAV drag. Additionally, shrinking this segment now will enable us to reload should BDCs become cheap again.

Direct Credit (68.4%)

The balance of the portfolio entails investments in directly originated private deals as well as syndicated bonds, loans and (to a lesser extent) CLOs purchased at discounts in the secondary market.

Spreads have widened in recent weeks but remain relatively benign at around 450bps over Treasuries. However, we are uncovering significant dispersion within the Index, providing an ideal backdrop for credit selection. Through active management, there have been ample opportunities to earn low-double digit yields for first lien risk.

Further, the bonds and loans we have acquired in recent quarters continue to trade at notable discounts, which we believe represents future capital gains; we calibrate our assets as trading roughly 13% below par, currently.

Another recent crystallization provides a window into these potential future capital gains. The Credit Income Fund held loans for a company known as Virgin Pulse, a mobile-first digital wellness platform. In early October, HealthComp, a benefits and analytics business, announced plans to acquire Virgin Pulse for $3bn, which will entail refinancing our debt. In the days after the announcement, we sold our Virgin Pulse debt, previously marked in the mid-80s, for 99.5—leaving 50bps behind in exchange for eliminating deal risk and the ability to recycle our capital more quickly.

As Virgin Pulse underscores, we cannot time the potential pull to par. However, buying assets at discounts represents the core of our strategy— providing shareholders another avenue for return beyond our robust income.

Conclusion

The current market requires investors consider their portfolio allocations more broadly, in our view.

A convergence of geopolitical forces has enabled the S&P 5005 to deliver an annual return of nearly 9.0% since the Great Financial Crisis8, including the following:

| · | Low interest rates / Low inflation |

| · | Inexpensive cost of energy |

| · | Lower cost of labor (due to China integrating its workforce) |

The factors prevailing in the current backdrop, however, which we outline below, suggest a reversal of these equity-friendly trends:

| · | Higher rates / “Non-zero” inflation |

| · | De-globalizing and re-shoring |

Despite this clear paradigm shift, most investors remain under-invested in fixed income. Recency-bias likely underpins these allocations; being overweight stocks and underweighted credit has heretofore unambiguously “worked.” However, we believe credit-based investments will outperform equities in the years ahead—both on an absolute basis and (almost certainly) from a risk-adjusted perspective.

Finally, the Credit Income Fund built the bulk of its track-record during what we would characterize as a brutal backdrop for fixed income investing. From October 2015 through March 2022 (the Fed’s first hike of the post-COVID era), the 10 Year U.S. Treasury averaged just 1.91%.7 The Fund nonetheless has beaten its most relevant benchmarks by more than 1.5x. With higher rates, a deluge of deals from retrenching banks and the expanded firepower of BC Partners, we believe the next eight years can be even better.

Amid this context, we would argue that any portfolio and/or platform would benefit from an enhanced allocation to the Alternative Credit Income Fund.

| Annual Report | September 30, 2023 | 5 |

| Alternative Credit Income Fund | Shareholder Letter |

| | September 30, 2023 (Unaudited) |

Regards,

Michael Terwilliger, CFA

Portfolio Manager*

Alternative Credit Income Fund

| * | Effective October, 31, 2020, Sierra Crest Investment Management LLC (“Sierra Crest”) replaced Resource Alternative Advisor, LLC (“Resource”) as the Fund’s investment adviser. Michael Terwilliger has joined Sierra Crest as a portfolio manager to the Fund. |

| 1 | Fund performance refers to that of Class I. Unless otherwise stated, all performance figures provided are for the six-month period ended September 30, 2023. The returns were calculated using the net asset values used for shareholder transactions and thus do not include certain adjustments in accordance with accounting principles generally accepted in the United States of America. The net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. Past performance is not indicative of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. Performance figures for periods less than one year are not annualized. For performance information current to the most recent month-end, please call toll-free 1-833-404-4103. |

The Adviser and the Fund have entered into an Expense Limitation Agreement under which the Adviser has agreed, until at least January 31, 2024 to waive its management fees (excluding any incentive fee) and to pay or absorb the ordinary annual operating expenses of the Fund (excluding interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses), to the extent that its management fees plus the Fund’s ordinary annual operating expenses exceed 2.34% per annum of the Fund’s average daily net assets attributable to Class I shares. Such Expense Limitation Agreement may not be terminated by the Adviser, but it may be terminated by the Board of Trustees, upon 60 days written notice to the Adviser. Any waiver or reimbursement by the Adviser is subject to repayment by the Fund within the three (3) years from the date the Adviser (or the previous investment adviser) waived any payment or reimbursed any expense, if the Fund is able to make the repayment without exceeding the lesser of the expense limitation in place at the time of the waiver or the current expense limitation and the repayment is approved by the Board of Trustees.

| 2 | Barclays U.S. Aggregate Total Return Value Index - The Barclays U.S. Aggregate Total Return Value Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and nonagency). Investors cannot invest directly in an index. |

| 3 | Morningstar LSTA US Leveraged Loan TR USD Index - Morningstar LSTA US Leveraged Loan TR USD Index is a market value-weighted index designed to measure the performance of the U.S. leveraged loan market based upon market weightings, spreads and interest payments. Investors cannot invest directly in an index. |

| 4 | ICE BofA U.S. High Yield Index – The ICE BofA U.S. High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market. Investors cannot invest directly in an index. |

| 5 | S&P 500 – The S&P 500 is a market-capitalization-weighted index of the 500 largest publicly-traded companies in the U.S. Investors cannot invest directly in an index. |

| 6 | Wall Street Journal (10/13/2023) |

| 7 | Bloomberg, Average 10 Year U.S. Treasury Yield 10/28/2015 through 03/30/2022 |

| 8 | Bloomberg, SPY Index from 12/31/2007 through 10/23/2023, annual equivalent return of 8.99%. |

| Alternative Credit Income Fund | Portfolio Update |

| | September 30, 2023 (Unaudited) |

The Fund’s performance figures for the periods ended September 30, 2023, compared to its benchmark:

| Alternative Credit Income Fund | 1 Month | Quarter | 6 Month | YTD | 1 Year | 3 Year | 5 Year | Since Inception* | Inception |

| Class A Shares - Without Load | 1.28% | 2.63% | 4.61% | 4.24% | 4.19% | 7.09% | 4.60% | 5.98% | 4/17/15 |

| Class A Shares - With Load | -4.54% | -3.25% | -1.39% | -1.71% | -1.84% | 5.02% | 3.36% | 5.13% | 4/17/15 |

| Class C Shares - Without Load | 1.19% | 2.32% | 4.20% | 3.56% | 3.33% | 6.28% | 3.79% | 5.40% | 4/17/15 |

| Class C Shares - With Load(a) | 0.19% | 1.32% | 3.20% | 2.57% | 2.36% | 6.28% | 3.79% | 5.40% | 4/17/15 |

| Class W Shares - Without Load | 1.28% | 2.63% | 4.61% | 4.13% | 4.19% | 7.09% | 4.58% | 5.92% | 4/17/15 |

| Class I Shares - Without Load | 1.24% | 2.70% | 4.74% | 4.33% | 4.36% | 7.33% | 4.83% | 6.22% | 4/17/15 |

| Class L Shares - Without Load | 1.21% | 2.57% | 4.59% | 4.04% | 3.93% | 6.82% | 4.33% | 4.61% | 7/28/17 |

| Class L Shares - With Load | -3.12% | -1.78% | 0.14% | -0.38% | -0.51% | 5.29% | 3.44% | 3.87% | 7/28/17 |

Morningstar LSTA US Leveraged Loan TR

USD Index | 0.96% | 3.46% | 6.72% | 9.97% | 12.98% | 6.08% | 4.46% | 4.36% | 4/17/15 |

| (a) | Effective as of December 23, 2016, Class C shares no longer have a sales charge. |

The Morningstar LSTA US Leveraged Loan TR USD Index is a market value-weighted index designed to measure the performance of the U.S. leveraged loan market based upon market weightings, spreads and interest payments. Investors cannot invest directly in an index.

Past performance is not indicative of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. Performance figures for periods less than one year are not annualized. As of the Fund’s most recent prospectus dated January 27, 2023, the Fund’s total annual operating expenses, including acquired fund fees and expenses, before fee waivers is 4.75% for Class A, 5.53% for Class C, 4.75% for Class W, 4.51% for Class I and 5.04% for Class L shares. After fee waivers, the Fund’s total annual operating expense is 4.75% for Class A, 5.50% for Class C, 4.75% for Class W, 4.50% for Class I and 5.00% for Class L shares. Class A shares are subject to maximum sales loads of 5.75% imposed on purchases. Class L shares are subject to a maximum sales load of 4.25% imposed on purchases. Share repurchases within 365 days may be subject to an early withdrawal charge of 0.50% for Class A and 1.00% for Class C shares. For performance information current to the most recent month-end, please call toll-free 1-833-404-4103.

| Annual Report | September 30, 2023 | 7 |

| Alternative Credit Income Fund | Portfolio Update |

| | September 30, 2023 (Unaudited) |

Comparison of the Change in Value of a $10,000 Investment

| * | Commencement of operations for Class A Shares. |

Consolidated Portfolio Composition as of September 30, 2023

| Asset Type | | Percent of Net Assets | |

| Bank Loans | | | 46.96% | |

| Private Investment Funds | | | 22.25% | |

| Common Equity | | | 9.27% | |

| Short Term Investments | | | 6.12% | |

| Asset Backed Securities | | | 5.22% | |

| Interval Fund | | | 3.12% | |

| Corporate Bonds | | | 2.89% | |

| Preferred Stock | | | 2.12% | |

| Warrants | | | 0.33% | |

| Joint Venture | | | 0.19% | |

| Securities Sold Short | | | -3.41% | |

| Total Investments | | | 95.06% | |

| Other Assets in Excess of Liabilities | | | 4.94% | |

| Net Assets | | | 100.00% | |

Please see the Consolidated Schedule of Investments for a detailed listing of the Fund’s holdings.

| Alternative Credit Income Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| | | Coupon | | | Reference Rate & Spread | | Maturity | | | Principal | | | Value | |

| BANK LOANS (46.96%)(a) | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Communication Services (1.73%) | | | | | | | | | | | | | | |

| Neptune Bidco US Inc., First Lien Term Loan(b) | | | 10.40 | % | | 3M SOFR + 5.00%, 0.50% Floor | | | 04/11/2029 | | | $ | 4,837,875 | | | $ | 4,371,238 | |

| | | | | | | | | | | | | | | | | | | |

| Consumer Discretionary (2.14%) | | | | | | | | | | | | | | | | | | |

| Arrow Purchaser, Inc., First Lien Initial Term Loan(b) | | | 12.18 | % | | 1M SOFR + 6.75%, 1.00% Floor | | | 04/15/2026 | | | | 2,145,833 | | | | 2,120,083 | |

| Jo-Ann Stores LLC, First Lien Initial Term Loan(b) | | | 10.36 | % | | 3M SOFR + 4.75%, 0.75% Floor | | | 06/30/2028 | | | | 3,949,622 | | | | 1,323,123 | |

| Lucky Bucks Holdings LLC, Subordinated Note(b)(c)(d)(o) | | | – | % | | N/A | | | 05/29/2028 | | | | 9,617,393 | | | | 1,947,522 | |

| | | | | | | | | | | | | | | | | | 5,390,728 | |

| Consumer Staples (5.38%) | | | | | | | | | | | | | | | | | | |

| 8th Avenue Food & Provisions, Inc., Second Lien Term Loan(b) | | | 13.18 | % | | 1M SOFR + 7.75% | | | 10/01/2026 | | | | 2,500,000 | | | | 1,721,875 | |

| BrightPet, First Lien Term Loan(b)(e) | | | 12.54 | % | | 3M SOFR + 6.25%, 0.75% PIK, 1.00% Floor | | | 10/06/2026 | | | | 1,948,697 | | | | 1,889,067 | |

| BrightPet, Revolver(b)(f) | | | 13.27 | % | | 3M SOFR + 7.00%, 1.00% Floor | | | 10/06/2026 | | | | 187,648 | | | | 172,344 | |

| Florida Food Products LLC, Second Lien Term Loan(b) | | | 13.43 | % | | 1M SOFR + 8.00%, 0.75% Floor | | | 10/18/2029 | | | | 5,000,000 | | | | 4,777,000 | |

| Phillips Feed Service, Inc., First Lien Term Loan(b) | | | 12.55 | % | | 3M SOFR + 7.00% | | | 05/30/2025 | | | | 5,250,000 | | | | 5,000,100 | |

| | | | | | | | | | | | | | | | | | 13,560,386 | |

| Financials (6.63%) | | | | | | | | | | | | | | | | | | |

| BetaNXT, Inc., First Lien Term Loan(b) | | | 11.14 | % | | 3M SOFR + 5.75% | | | 07/01/2029 | | | | 2,970,000 | | | | 2,773,980 | |

| Cor Leonis Limited, Revolver(b)(f) | | | 12.89 | % | | 3M SOFR + 7.50%, 1.50% Floor | | | 05/15/2028 | | | | 1,244,892 | | | | 1,244,892 | |

| H-CA II, LLC, First Lien Term Loan(b)(c) | | | 16.00 | % | | N/A | | | 04/01/2024 | | | | 1,897,831 | | | | 1,897,831 | |

| Hunter Point Capital Structured Notes Issuer, LLC, Subordinated Delayed Draw Notes(b)(f) | | | N/A | | | N/A | | | 07/15/2052 | | | | 506,711 | | | | 524,598 | |

| Irradiant Intermediate Holdings, L.P., Delayed Draw Term Loan(b) | | | – | % | | 3M SOFR + 6.50%, 1.50% Floor | | | 06/08/2028 | | | | – | | | | (28,130 | ) |

| Irradiant Intermediate Holdings, L.P., First Lien Term Loan(b) | | | 11.99 | % | | 3M SOFR + 6.50%, 1.50% Floor | | | 06/08/2028 | | | | 1,450,000 | | | | 1,421,870 | |

| Money Transfer Acquisition Inc., First Lien Term Loan(b) | | | 13.67 | % | | 1M SOFR + 8.25%, 1.00% Floor | | | 12/14/2027 | | | | 6,868,750 | | | | 6,761,598 | |

| SouthStreet Securities Holdings, Inc., First Lien Term Loan(b)(c) | | | 9.00 | % | | N/A | | | 09/20/2027 | | | | 2,700,000 | | | | 2,126,250 | |

| | | | | | | | | | | | | | | | | | 16,722,889 | |

| Health Care (8.18%) | | | | | | | | | | | | | | | | | | |

| American Academy Holdings, LLC, First Lien Term Loan(b)(e) | | | 16.43 | % | | 3M SOFR + 5.75%, 5.25% PIK, 1.00% Floor | | | 01/01/2025 | | | | 2,298,783 | | | | 2,310,277 | |

| American Academy Holdings, LLC, Second Lien Term Loan(b)(c)(e) | | | 14.50 | % | | PIK | | | 03/01/2028 | | | | 3,545,394 | | | | 3,115,693 | |

| PhyNet Dermatology LLC, Delayed Draw Term Loan(b)(f) | | | – | % | | 6M SOFR + 6.50%, 0.75% Floor | | | 08/16/2024 | | | | – | | | | 15,517 | |

| PhyNet Dermatology LLC, First Lien Term Loan(b) | | | 11.87 | % | | 6M SOFR + 6.50%, 0.75% Floor | | | 08/16/2024 | | | | 1,960,603 | | | | 1,960,603 | |

| Upstream Rehabilitation, Inc., Second Lien Term Loan(b) | | | 13.92 | % | | 1M SOFR + 8.50%, 2.00% Floor | | | 11/22/2027 | | | | 7,500,000 | | | | 6,425,025 | |

| VBC Spine Opco LLC (DxTX Pain and Spine LLC), Delayed Draw Term Loan(b)(f) | | | – | % | | 3M SOFR + 8.00%, 2.00% Floor | | | 06/14/2028 | | | | – | | | | 1,545 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | September 30, 2023 | 9 |

| Alternative Credit Income Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| VBC Spine Opco LLC (DxTX Pain and Spine LLC), First Lien Term Loan(b) | | | 13.56 | % | | 3M SOFR + 8.00%, 2.00% Floor | | | 06/14/2028 | | | $ | 2,193,145 | | | $ | 2,152,133 | |

| VBC Spine Opco LLC (DxTX Pain and Spine LLC), Revolver(b)(f) | | | – | % | | 3M SOFR + 8.00%, 2.00% Floor | | | 06/14/2028 | | | | – | | | | (4,525 | ) |

| Viant Medical Holdings, Inc., Second Lien Initial Term Loan(b) | | | 13.18 | % | | 1M SOFR + 7.75% | | | 07/02/2026 | | | | 5,000,000 | | | | 4,637,500 | |

| | | | | | | | | | | | | | | | | | 20,613,768 | |

| Industrials (7.32%) | | | | | | | | | | | | | | | | | | |

| Accordion Partners, LLC, Delayed Draw Term Loan A(b) | | | 11.89 | % | | 3M SOFR + 6.50%, 0.75% Floor | | | 08/29/2029 | | | | 284,053 | | | | 282,349 | |

| Accordion Partners, LLC, Delayed Draw Term Loan B(b) | | | 11.62 | % | | 3M SOFR + 6.25%, 0.75% Floor | | | 08/29/2029 | | | | 355,956 | | | | 353,821 | |

| Accordion Partners, LLC, First Lien Term Loan A(b) | | | 11.64 | % | | 3M SOFR + 6.25%, 0.75% Floor | | | 08/29/2029 | | | | 3,236,106 | | | | 3,216,689 | |

| Epic Staffing Group, Delayed Draw Term Loan(b)(f) | | | – | % | | N/A | | | 06/28/2029 | | | | – | | | | (12,266 | ) |

| Epic Staffing Group, First Lien Term Loan(b) | | | 11.14 | % | | 3M SOFR + 5.75%, 0.50% Floor | | | 06/28/2029 | | | | 1,700,408 | | | | 1,625,591 | |

| Material Handling Systems, Inc., First Lien Term Loan(b) | | | 10.76 | % | | 3M SOFR + 5.50%, 0.50% Floor | | | 06/01/2029 | | | | 4,950,000 | | | | 4,399,560 | |

| Qualtek LLC, First Lien Term Loan (b)(e) | | | 15.31 | % | | 3M SOFR + 1.00%, 9.00% PIK, 1.00% Floor | | | 07/14/2025 | | | | 3,260,829 | | | | 3,260,828 | |

| Qualtek LLC, Second Lien Term Loan (b)(e) | | | 15.31 | % | | 3M SOFR + 1.00%, 9.00% PIK, 1.00% Floor | | | 01/14/2027 | | | | 513,599 | | | | 513,599 | |

| Secure Acquisition, Inc., Second Lien Term Loan(b) | | | 13.29 | % | | 3M SOFR + 7.75%, 0.75% Floor | | | 12/14/2029 | | | | 5,000,000 | | | | 4,819,000 | |

| | | | | | | | | | | | | | | | | | 18,459,171 | |

| Information Technology (15.58%) | | | | | | | | | | | | | | | | | | |

| Accurate Background, LLC, First Lien Term Loan(b) | | | 11.65 | % | | 3M SOFR + 6.00%, 1.00% Floor | | | 03/26/2027 | | | | 4,424,086 | | | | 4,274,552 | |

| Ancile Solutions, Inc., First Lien Term Loan(b)(e) | | | 15.67 | % | | 3M SOFR + 10.00%, 1.00% Floor | | | 06/11/2026 | | | | 3,610,054 | | | | 3,601,029 | |

| DCert Buyer, Inc. First Amendment Term Loan Refinancing, Second Lien Term Loan(b) | | | 12.32 | % | | 1M SOFR + 7.00% | | | 02/16/2029 | | | | 3,600,000 | | | | 3,378,006 | |

| Diamanti, Inc., Subordinated Note(b)(c)(e) | | | 12.50 | % | | PIK | | | 05/01/2024 | | | | 3,498,686 | | | | 3,555,714 | |

| EagleView Technology Corp., Second Lien Term Loan(b) | | | 13.04 | % | | 3M SOFR + 7.50% | | | 08/14/2026 | | | | 1,495,652 | | | | 1,331,130 | |

| Ivanti Software, Inc., Second Lien Initial Term Loan(b) | | | 12.78 | % | | 3M US L + 7.25%, 0.50% Floor | | | 12/01/2028 | | | | 4,000,000 | | | | 2,896,680 | |

| Kofax, Inc., First Lien Term Loan(b) | | | 10.72 | % | | 3M SOFR + 5.25%, 0.50% Floor | | | 07/20/2029 | | | | 3,970,000 | | | | 3,702,025 | |

| Kofax, Inc., Second Lien Term Loan(b) | | | 13.12 | % | | 3M SOFR + 7.75%, 0.50% Floor | | | 07/20/2030 | | | | 4,000,000 | | | | 3,810,000 | |

| Naviga, Inc., First Lien Term Loan(b) | | | 12.49 | % | | 3M SOFR + 7.00%, 1.00% Floor | | | 12/29/2023 | | | | 3,031,616 | | | | 3,011,305 | |

| Precisely Software Incorporated, Second Lien Term Loan(b) | | | 12.86 | % | | 3M SOFR + 7.25%, 0.75% Floor | | | 04/23/2029 | | | | 3,000,000 | | | | 2,717,415 | |

| Redstone HoldCo 2 LP, Second Lien Term Loan(b) | | | 13.18 | % | | 1M SOFR + 7.75%, 0.75% Floor | | | 04/16/2029 | | | | 5,000,000 | | | | 3,293,750 | |

| Spectrio, First Lien Term Loan(b) | | | 11.50 | % | | 6M SOFR + 6.00%, 1.00% Floor | | | 12/09/2026 | | | | 3,891,645 | | | | 3,726,249 | |

| | | | | | | | | | | | | | | | | | 39,297,855 | |

| TOTAL BANK LOANS | | | | | | | | | | | | | | | | | | |

| (Cost $133,528,017) | | | | | | | | | | | | | | | | | 118,416,035 | |

| See Notes to Consolidated Financial Statements. | |

| 10 | www.altcif.com |

| Alternative Credit Income Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| ASSET BACKED SECURITIES AND CORPOATE BONDS (8.11%) | | | | | | | | | | | | | | |

| ASSET BACKED SECURITIES (5.22%)(a) | | | | | | | | | | | | | | |

| Canyon Capital CLO 2014-1, Ltd., Class ER(g) | | | 13.33 | % | | 3M US L + 7.70% | | | 01/30/2031 | | | $ | 1,000,000 | $ | | | 735,570 | |

| Jamestown CLO V, Ltd., Class F(g)(o)(p) | | | 10.64 | % | | 3M US L + 5.85% | | | 01/17/2027 | | | | 536,203 | | | | 43,915 | |

| JMP Credit Advisors CLO IV, Ltd.(b) | | | 24.43 | % | | N/A | | | 07/17/2029 | | | | 4,836,540 | | | | 316,310 | |

| JMP Credit Advisors CLO V, Ltd.(b) | | | 2.16 | % | | N/A | | | 07/17/2030 | | | | 4,486,426 | | | | 1,020,213 | |

| Mount Logan Funding 2018-1 LP(b)(g)(k) | | | 25.47 | % | | N/A | | | 01/22/2033 | | | | 7,798,575 | | | | 7,139,595 | |

| Octagon Investment Partners 36, Ltd., Class F(g) | | | 13.47 | % | | 3M US L + 7.75% | | | 04/15/2031 | | | | 1,000,000 | | | | 656,875 | |

| Octagon Investment Partners XIV, Ltd., Class ER(g)(p) | | | 13.92 | % | | 3M US L + 8.35% | | | 07/15/2029 | | | | 2,132,000 | | | | 1,203,506 | |

| Saranac CLO VII, Ltd., Class ER(g) | | | 12.23 | % | | 3M US L + 6.72% | | | 11/20/2029 | | | | 500,000 | | | | 265,679 | |

| Tralee CLO II, Ltd., Class ER(g)(p) | | | 13.44 | % | | 3M US L + 7.85% | | | 07/20/2029 | | | | 1,000,000 | | | | 933,557 | |

| Tralee CLO II, Ltd., Class FR(g)(o)(p) | | | – | % | | 3M US L + 8.85% | | | 07/20/2029 | | | | 1,000,000 | | | | 421,797 | |

| Voya CLO 2014-2, Ltd., Class ER(g) | | | 13.56 | % | | 3M US L + 7.70% | | | 04/17/2030 | | | | 1,000,000 | | | | 421,848 | |

| | | | | | | | | | | | | | | | | | 13,158,865 | |

| CORPORATE BONDS (2.89%) | | | | | | | | | | | | | | | | | | |

| Communications (0.80%) | | | | | | | | | | | | | | | | | | |

| Spanish Broadcasting System, Inc.(c)(g)(p) | | | 9.75 | % | | N/A | | | 03/01/2026 | | | | 3,000,000 | | | | 2,018,465 | |

| | | | | | | | | | | | | | | | | | | |

| Consumer Discretionary (0.15%) | | | | | | | | | | | | | | | | | | |

| Monitronics - Escrow(p) | | | 0.00 | % | | N/A | | | 12/31/2049 | | | | 2,650,000 | | | | – | |

| Real Hero Merger Sub 2, Inc.(c)(g)(p) | | | 6.25 | % | | N/A | | | 02/01/2029 | | | | 500,000 | | | | 386,753 | |

| | | | | | | | | | | | | | | | | | 386,753 | |

| Consumer Staples (0.80%) | | | | | | | | | | | | | | | | | | |

| H-Food Holdings LLC / Hearthside Finance Co., Inc.(c)(g)(p) | | | 8.50 | % | | N/A | | | 06/01/2026 | | | | 7,978,000 | | | | 2,004,034 | |

| | | | | | | | | | | | | | | | | | | |

| Industrials (1.14%) | | | | | | | | | | | | | | | | | | |

| PECF USS Intermediate Holding III Corp.(c)(g)(p) | | | 8.00 | % | | N/A | | | 11/15/2029 | | | | 5,000,000 | | | | 2,719,500 | |

| Wesco Aircraft Holdings, Inc.(c)(g)(o)(p) | | | – | % | | N/A | | | 11/15/2027 | | | | 4,636,000 | | | | 162,260 | |

| | | | | | | | | | | | | | | | | | 2,881,760 | |

| TOTAL ASSET BACKED | | | | | | | | | | | | | | | | | | |

| SECURITIES AND CORPOATE BONDS | | | | | | | | | | | | | | | | | | |

| (Cost $34,580,158) | | | | | | | | | | | | | | | | | 20,449,877 | |

| | | Dividend Rate | | | Shares | | | Value | |

| PREFERRED STOCK (2.12%) | | | | | | | | | |

| Consumer Discretionary (1.99%) | | | | | | | | | |

| Pennfoster(a)(b)(e)(i) | | | 16.30 | % | | | 5,133,089 | | | | 5,018,108 | |

| | | | | | | | | | | | | |

| Health Care (0.05%) | | | | | | | | | | | | |

| American Academy Holdings. Inc., Preferred Units(b)(i)(j) | | | 18.00 | % | | | 90,970 | | | | 116,897 | |

| | | | | | | | | | | | | |

| Industrials (0.08%) | | | | | | | | | | | | |

| GreenPark Infrastructure, LLC Series A(b)(i)(j)(k) | | | | | | | 400 | | | | 200,000 | |

| | | | | | | | | | | | | |

| TOTAL PREFERRED STOCK | | | | | | | | | | | | |

| (Cost $5,236,819) | | | | | | | | | | | 5,335,005 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | September 30, 2023 | 11 |

| Alternative Credit Income Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| | | Shares | | | Value | |

| COMMON EQUITY (9.27%) | | | | | | |

| Consumer Discretionary (0.56%) | | | | | | |

| CEC Entertainment, Inc.(i) | | | 79,564 | | | $ | 1,405,657 | |

| | | | | | | | | |

| Diversified (4.18%) | | | | | | | | |

| Ares Capital Corp.(p) | | | 117,223 | | | | 2,282,332 | |

| CION Investment Corp.(p) | | | 120,800 | | | | 1,276,856 | |

| FS KKR Capital Corp.(p) | | | 105,137 | | | | 2,070,148 | |

| Portman Ridge Finance Corp.(k)(p) | | | 25,504 | | | | 490,952 | |

| SLR Investment Corp.(p) | | | 115,211 | | | | 1,773,097 | |

| WhiteHorse Finance, Inc.(p) | | | 207,328 | | | | 2,647,579 | |

| | | | | | | | 10,540,964 | |

| | | | | | | | | |

| Energy (1.44%) | | | | | | | | |

| Chord Energy Corp.(p) | | | 22,373 | $ | | | 3,625,992 | |

| | | | | | | | | |

| Financials (0.84%) | | | | | | | | |

| Aperture Dodge 18 LLC(b)(i) | | | 2,038,970 | | | | 2,124,000 | |

| | | | | | | | | |

| Health Care (0.17%) | | | | | | | | |

| American Academy Holdings. Inc., Common Units(b)(i)(j) | | | 0.05 | | | | 274,283 | |

| DxTx Pain and Spine LLC, Common Units(b)(i)(j) | | | 98,854 | | | | 161,132 | |

| | | | | | | | 435,415 | |

| | | | | | | | | |

| Industrials (0.74%) | | | | | | | | |

| GreenPark Infrastructure, LLC Series M-1 (b)(f)(i)(j)(k) | | | 200 | | | | 70,626 | |

| Qualtek LLC(b)(i) | | | 287,540 | | | | 1,785,623 | |

| | | | | | | | 1,856,249 | |

| | | | | | | | | |

| Real Estate (1.34%) | | | | | | | | |

| Copper Property CTL Pass Through Trust(i)(p) | | | 319,520 | | | | 3,386,912 | |

| | | | | | | | | |

| TOTAL COMMON EQUITY | | | | | | | | |

| (Cost $20,893,537) | | | | | | | 23,375,189 | |

| | | | | | | | | |

| JOINT VENTURE (0.19%) | | | | | | | | |

| Joint Venture (0.19%) | | | | | | | | |

| Great Lakes Funding II LLC, Series A(f)(k)(l) | | | 480,978 | | | | 470,515 | |

| | | | | | | | 470,515 | |

| | | | | | | | | |

| TOTAL JOINT VENTURE | | | | | | | | |

| (Cost $480,978) | | | | | | | 470,515 | |

| | | | | | | | | |

| INTERVAL FUND (3.12%) | | | | | | | | |

| Interval Fund (3.12%) | | | | | | | | |

| Opportunistic Credit Interval Fund(k) | | | 664,452 | | | | 7,860,465 | |

| | | | | | | | | |

| TOTAL INTERVAL FUND | | | | | | | | |

| (Cost $8,000,000) | | | | | | | 7,860,465 | |

| See Notes to Consolidated Financial Statements. | |

| 12 | www.altcif.com |

| Alternative Credit Income Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

| | | Shares | | | Value | |

| PRIVATE INVESTMENT FUNDS (22.25%) | | | | | | |

| BlackRock Global Credit Opportunities Fund, LP(f)(l)(m) | | | | | | $ | 13,867,068 | |

| CVC European Mid-Market Solutions Fund(f)(l)(m) | | | | | | | 9,223,615 | |

| GSO Credit Alpha Fund II LP(f)(l)(m) | | | | | | | 5,150,526 | |

| Monroe Capital Private Credit Fund III LP(f)(l)(m) | | | | | | | 8,838,545 | |

| Pelham S2K SBIC II, L.P.(f)(l)(m) | | | | | | | 200,000 | |

| Tree Line Credit Strategies LP(l)(m) | | | | | | | 18,818,454 | |

| | | | | | | | 56,098,208 | |

| | | | | | | | | |

| TOTAL PRIVATE INVESTMENT | | | | | | | | |

| FUNDS | | | | | | | | |

| (Cost $54,570,613) | | | | | | | 56,098,208 | |

| | | | | | | | | |

| WARRANTS (0.33%) | | | | | | | | |

| CEC Entertainment, Inc.(P) | | | 237,941 | | | | 475,882 | |

| Diamanti, Inc., Class A(b) | | | 146,413 | | | | – | |

| SouthStreet Securities Holdings, Inc., Warrants(b) | | | 3,400 | | | $ | 349,690 | |

| | | | | | | | | |

| TOTAL WARRANTS | | | | | | | | |

| (Cost $390,456) | | | | | | | 825,572 | |

| | | | | | | | | |

| SHORT TERM INVESTMENTS (6.12%) | | | | | | | | |

| Money Market Funds (6.12%) | | | | | | | | |

| US BANK MMDA - USBGFS 9, 5.20%(n) | | | | | | | | |

| | | 15,443,162 | | | | 15,443,162 | |

| | | | | | | | | |

| TOTAL SHORT TERM | | | | | | | | |

| INVESTMENTS | | | | | | | | |

| (Cost $15,443,162) | | | | | | | 15,443,162 | |

SCHEDULE OF SECURITIES SOLD SHORT (-3.41%)

| | | Interest Rate | | | Maturity | | | Principal | | | Value | |

| CORPORATE BONDS (-3.41%) | | | | | | | | | | | | |

| Enviva Partners LP(c) | | | 6.50 | % | | | 01/15/2026 | | | | (4,500,000 | ) | | $ | (3,674,565 | ) |

| Life Time, Inc.(c) | | | 8.00 | % | | | 04/15/2026 | | | | (5,000,000 | ) | | | (4,917,825 | ) |

| | | | | | | | | | | | | | | | | |

| TOTAL CORPORATE BONDS | | | | | | | | | | | | | | | (8,592,390 | ) |

| | | | | | | | | | | | | | | | | |

| TOTAL SCHEDULE OF SECURITIES SOLD SHORT | | | | | | | | | | | | | | | | |

| (Proceeds $9,295,618) | | | | | | | | | | | | | | $ | (8,592,390 | ) |

| | | | | | | | | | | | | | | | | |

| INVESTMENTS, AT VALUE (95.06%) | | | | | | | | | | | | | | | | |

| (Cost $263,828,122) | | | | | | | | | | | | | | $ | 239,681,638 | |

| | | | | | | | | | | | | | | | | |

| Other Assets In Excess Of Liabilities (4.94%) | | | | | | | | | | | | | | | 12,479,554 | |

| | | | | | | | | | | | | | | | | |

| NET ASSETS (100.00%) | | | | | | | | | | | | | | $ | 252,161,192 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | September 30, 2023 | 13 |

| Alternative Credit Income Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

Investment Abbreviations:

LIBOR - London Interbank Offered Rate

SOFR - Secured Overnight Financing Rate

PIK - Payment in-Kind

Reference Rates:

1M US L - 1 Month LIBOR as of September 30, 2023 was 5.43%

3M US L - 3 Month LIBOR as of September 30, 2023 was 5.66%

1M US SOFR - 1 Month SOFR as of September 30, 2023 was 5.32%.

3M US SOFR - 3 Month SOFR as of September 30, 2023 was 5.40%.

6M US SOFR - 6 Month SOFR as of September 30, 2023 was 5.44%.

| (a) | Variable rate investment, unless otherwise noted. Interest rates reset periodically. Interest rate shown reflects the rate in effect at September 30, 2023. For securities based on a published reference rate and spread, the reference rate and spread are indicated in the description above. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. |

| (b) | As a result of the use of significant unobservable inputs to determine fair value, these investments have been classified as Level 3 assets. |

| (c) | Fixed rate investment. |

| (d) | Non-accrual investment. |

| (e) | Payment in kind security which may pay interest in additional par. |

| (f) | All or a portion of this commitment was unfunded as of September 30, 2023. |

| (g) | Securities exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be sold in the ordinary course of business in transactions exempt from registration, normally to qualified institutional buyers. As of September 30, 2023, the aggregate market value of those securities was $19,113,354, representing 7.58% of net assets. |

| (i) | Non-income producing security. |

| (j) | Investment is held through ACIF Master Blocker, LLC, wholly owned subsidiary. |

| (l) | Restricted security. See chart below. |

| (m) | Investment is held through CIF Investments LLC, a wholly-owned subsidiary. |

| (n) | Money market fund; interest rate reflects seven-day effective yield on September 30, 2023. |

| (o) | Non-accrual investment. |

| (p) | All or a portion of each of these securities have been segregated as collateral for line of credit. The aggregate market value of those securities was $27,923,537 (see Note 7) |

Securities determined to be restricted under the procedures approved by the Fund's Board of Trustees are as follows.

| Date(s) of Purchase | | | Security | | Cost | | | Value | | | % of Net Assets | |

| | 3/31/2018 - 6/30/2022 | | | BlackRock Global Credit Opportunities Fund, LP | | $ | 13,076,282 | | | $ | 13,867,068 | | | | 5.50 | % |

| | 09/30/2017 - 09/30/2021 | | | CVC European Mid-Market Solutions Fund | | | 10,003,216 | | | | 9,223,615 | | | | 3.66 | % |

| | 6/30/2018 - 3/31/2021 | | | GSO Credit Alpha Fund II LP | | | 3,789,855 | | | | 5,150,526 | | | | 2.04 | % |

| | 9/30/2018 - 12/31/2020 | | | Monroe Capital Private Credit Fund III LP | | | 8,501,260 | | | | 8,838,545 | | | | 3.51 | % |

| | 11/14/2022 - 03/31/2023 | | | Pelham S2K SBIC II, L.P. | | | 200,000 | | | | 200,000 | | | | 0.08 | % |

| | 12/31/2017 - 06/30/2019 | | | Tree Line Credit Strategies LP | | | 19,000,000 | | | | 18,818,454 | | | | 7.46 | % |

| | 08/05/2022 - 09/30/2023 | | | Great Lakes Funding II LLC, Series A | | | 480,978 | | | | 470,515 | | | | 0.19 | % |

| | | | | Total | | $ | 55,051,591 | | | $ | 56,568,723 | | | | 22.44 | % |

| See Notes to Consolidated Financial Statements. | |

| 14 | www.altcif.com |

| Alternative Credit Income Fund | Consolidated Schedule of Investments |

| | September 30, 2023 |

Additional information on investments in private investment funds, including our joint venture Great Lakes Funding II LLC, and unfunded commitments:

| Security | | Value | | | Redemption Frequency | | | Redemption Notice(Days) | | | Unfunded Commitments as of September 30, 2023 | |

| BlackRock Global Credit Opportunities Fund, LP(a) | | $ | 13,867,068 | | | | N/A | | | | N/A | | | $ | 4,883,202 | |

| CVC European Mid-Market Solutions Fund(b) | | | 9,223,615 | | | | N/A | | | | N/A | | | | 206,342 | |

| Great Lakes Funding II LLC, Series A(a) | | | 470,515 | | | | N/A | | | | N/A | | | | 13,760 | |

| GSO Credit Alpha Fund II LP(a) | | | 5,150,526 | | | | N/A | | | | N/A | | | | 7,382,124 | |

| Monroe Capital Private Credit Fund III LP(b) | | | 8,838,545 | | | | N/A | | | | N/A | | | | 1,498,740 | |

| Pelham S2K SBIC II, L.P. | | | 200,000 | | | | N/A | | | | N/A | | | | 1,800,000 | |

| Tree Line Credit Strategies LP | | | 18,818,454 | | | | Quarterly | | | | 90 | | | | N/A | |

| Total | | $ | 56,568,723 | | | | | | | | | | | $ | 15,784,168 | |

Unfunded commitments:

| Security | | Value | | | Maturity | | | Unfunded Commitment | |

| BrightPet, Revolver | | $ | 172,344 | | | | 10/06/2026 | | | $ | 312,500 | |

| Cor Leonis Limited, Revolver | | | 1,244,892 | | | | 05/15/2028 | | | | 904,014 | |

| Epic Staffing Group, Delayed Draw Term Loan | | | (12,266 | ) | | | 06/28/2029 | | | | 278,777 | |

| GreenPark Infrastructure, LLC Series M-1 | | | 70,626 | | | | 12/31/2049 | | | | 731,500 | |

| Hunter Point Capital Structured Notes Issuer, LLC, Subordinated Delayed Draw Notes | | | 524,598 | | | | 07/15/2052 | | | | 5,368,289 | |

| Irradiant Intermediate Holdings, L.P., Delayed Draw Term Loan | | | (28,130 | ) | | | 06/08/2028 | | | | 1,450,000 | |

| PhyNet Dermatology LLC, Delayed Draw Term Loan | | | 15,517 | | | | 08/16/2024 | | | | 1,034,483 | |

| VBC Spine Opco LLC (DxTX Pain and Spine LLC), Delayed Draw Term Loan | | | 1,545 | | | | 06/14/2028 | | | | 1,188,455 | |

| VBC Spine Opco LLC (DxTX Pain and Spine LLC), Revolver | | | (4,525 | ) | | | 06/14/2028 | | | | 241,936 | |

| Total | | $ | 1,984,601 | | | | | | | $ | 11,509,954 | |

| | | | | | | | | | | | | |

| Total Unfunded Commitments | | | | | | | | | | $ | 27,294,122 | |

| (a) | A voluntary withdrawal may be permitted at the General Partner's discretion with the General Partner's consent. |

| (b) | A voluntary withdrawal may be permitted with the General Partner's prior written consent. |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | September 30, 2023 | 15 |

| Alternative Credit Income Fund | Consolidated Statement of Assets and Liabilities |

| | September 30, 2023 |

| ASSETS | | | |

| Investments, at value (Cost $257,285,640) | | $ | 232,041,875 | |

| Affiliated investments, at value (Cost $15,838,100) | | | 16,232,153 | |

| Deposit with broker for securities sold short | | | 9,356,283 | |

| Interest and distributions receivable | | | 3,764,884 | |

| Receivable for investments sold | | | 5,558,729 | |

| Receivable for fund shares sold | | | 76,372 | |

| Prepaid expenses and other assets | | | 171,714 | |

| Total assets | | | 267,202,010 | |

| | | | | |

| LIABILITIES | | | | |

| Securities sold short (Proceeds $9,295,618) | | | 8,592,390 | |

| Line of credit payable | | | 3,878,632 | |

| Interest payable | | | 20,906 | |

| Payable for investments purchased | | | 235,318 | |

| Due to Adviser | | | 419,932 | |

| Payable for interest expense on securities sold short | | | 246,780 | |

| Administration fees payable | | | 194,500 | |

| Custody fees payable | | | 41,863 | |

| Incentive fees payable | | | 220,881 | |

| Distribution fees payable | | | 27,490 | |

| Shareholder servicing fees payable | | | 56,951 | |

| Transfer agency fees payable | | | 111,061 | |

| Accrued expenses and other liabilities | | | 994,114 | |

| Total liabilities | | | 15,040,818 | |

| Commitments and contingencies (Note 2) | | | | |

| NET ASSETS | | $ | 252,161,192 | |

| | | | | |

| NET ASSETS CONSISTS OF | | | | |

| Paid-in capital | | $ | 275,170,387 | |

| Total accumulated deficit | | | (23,009,195 | ) |

| NET ASSETS | | $ | 252,161,192 | |

| | | | | |

| Common Shares: | | | | |

| Class A | | | | |

| Net assets | | $ | 36,233,208 | |

| Shares of beneficial interest outstanding (no par value; unlimited number of shares) | | | 3,702,370 | |

| Net asset value(a) | | $ | 9.79 | |

| Maximum offering price per share (maximum sales charge of 5.75%) | | $ | 10.39 | |

| Class C | | | | |

| Net assets | | $ | 40,947,271 | |

| Shares of beneficial interest outstanding (no par value; unlimited shares) | | | 4,134,367 | |

| Net asset value(a) | | $ | 9.90 | |

| Class W | | | | |

| Net assets | | $ | 53,123,329 | |

| Shares of beneficial interest outstanding (no par value; unlimited shares) | | | 5,430,569 | |

| Net asset value | | $ | 9.78 | |

| Class I | | | | |

| Net assets | | $ | 110,738,577 | |

| Shares of beneficial interest outstanding (no par value; unlimited shares) | | | 11,298,324 | |

| Net asset value | | $ | 9.80 | |

| Class L | | | | |

| Net assets | | $ | 11,118,807 | |

| Shares of beneficial interest outstanding (no par value; unlimited shares) | | | 1,136,034 | |

| Net asset value | | $ | 9.79 | |

| Maximum offering price per share (maximum sales charge of 4.25%) | | $ | 10.22 | |

| (a) | Redemption price varies based on length of time held (Note 6). |

| See Notes to Consolidated Financial Statements. | |

| 16 | www.altcif.com |

| Alternative Credit Income Fund | Consolidated Statement of Operations |

| | For the Year Ended September 30, 2023 |

| INVESTMENT INCOME | | | |

| Interest | | $ | 21,519,994 | |

| Interest - Affiliates | | | 741,968 | |

| Dividends | | | 7,827,574 | |

| Dividends - Affiliates | | | 395,688 | |

| Other Income | | | 409,805 | |

| Total investment income | | | 30,895,029 | |

| EXPENSES | | | | |

| Investment advisory fees (Note 4) | | | 4,650,865 | |

| Administrative fees (Note 4) | | | 349,298 | |

| Distribution fees (Note 4): | | | | |

| Class C | | | 313,172 | |

| Class L | | | 28,456 | |

| Shareholder servicing fees (Note 4): | | | | |

| Class A | | | 92,591 | |

| Class C | | | 104,391 | |

| Class W | | | 133,277 | |

| Class L | | | 28,456 | |

| Interest and amortization/accretion on securities sold short | | | 442,835 | |

| Interest expense (Note 7) | | | 52,867 | |

| Incentive fees (Note 4) | | | 220,881 | |

| Transfer agent fees (Note 4) | | | 240,470 | |

| Professional fees | | | 275,601 | |

| Printing expense | | | 173,662 | |

| Registration fees | | | 130,719 | |

| Custody fees | | | 62,501 | |

| Insurance expense | | | 239,284 | |

| Trustee fees and expenses (Note 4) | | | 31,500 | |

| Networking Fees: | | | | |

| Class A | | | 7,993 | |

| Class C | | | 8,540 | |

| Class W | | | 2,224 | |

| Class I | | | 23,887 | |

| Class L | | | 3,264 | |

| Other expenses | | | 7,873 | |

| Total expenses | | | 7,624,607 | |

| Fees waived by Adviser (Note 4) | | | (360,993 | ) |

| Recoupment of previously waived fees (Note 4) | | | 59,466 | |

| Total net expenses | | | 7,323,080 | |

| NET INVESTMENT INCOME | | | 23,571,949 | |

| Net realized loss on investments | | | (1,309,135 | ) |

| Net change in unrealized depreciation on investments | | | (13,211,870 | ) |

| Net change in unrealized appreciation on securities sold short | | | 703,228 | |

| Net change in unrealized depreciation on affiliated investments | | | 253,865 | |

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | | | (13,563,912 | ) |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 10,008,037 | |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | September 30, 2023 | 17 |

| Alternative Credit Income Fund | Consolidated Statements of Changes in Net Assets |

| | | For the Year Ended September 30, 2023 | | | For the Year Ended September 30, 2022 | |

| OPERATIONS | | | | | | |

| Net investment income | | $ | 23,571,949 | | | $ | 14,286,823 | |

| Net realized loss on investments | | | (1,309,135 | ) | | | (1,815,526 | ) |

| Net change in unrealized depreciation on investments | | | (12,958,005 | ) | | | (20,272,028 | ) |

| Net change in unrealized appreciation on securities sold short | | | 703,228 | | | | – | |

| Net increase/(decrease) in net assets resulting from operations | | | 10,008,037 | | | | (7,800,731 | ) |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Total Distributable Earnings | | | | | | | | |

| Class A | | | (2,622,103 | ) | | | (2,402,335 | ) |

| Class C | | | (2,637,980 | ) | | | (2,443,171 | ) |

| Class W | | | (3,744,180 | ) | | | (3,687,216 | ) |

| Class I | | | (8,114,488 | ) | | | (6,420,554 | ) |

| Class L | | | (774,234 | ) | | | (737,636 | ) |

| From return of capital: | | | | | | | | |

| Class A | | | – | | | | (181,145 | ) |

| Class C | | | – | | | | (184,186 | ) |

| Class W | | | – | | | | (277,971 | ) |

| Class I | | | – | | | | (484,007 | ) |

| Class L | | | – | | | | (55,610 | ) |

| Total distributions to shareholders | | | (17,892,985 | ) | | | (16,873,831 | ) |

| | | | | | | | | |

| COMMON SHARE TRANSACTIONS | | | | | | | | |

| Class A | | | | | | | | |

| Proceeds from sales of shares | | | 2,849,033 | | | | 7,096,469 | |

| Distributions reinvested | | | 1,321,049 | | | | 1,180,078 | |

| Cost of shares redeemed | | | (4,557,578 | ) | | | (7,434,940 | ) |

| Net transferred in(out) | | | (684,076 | ) | | | (233,721 | ) |

| Net increase/(decrease) from share transactions | | | (1,071,572 | ) | | | 607,886 | |

| Class C | | | | | | | | |

| Proceeds from sales of shares | | | 2,457,255 | | | | 4,341,937 | |

| Distributions reinvested | | | 1,210,338 | | | | 1,354,973 | |

| Cost of shares redeemed | | | (4,398,432 | ) | | | (4,576,994 | ) |

| Net transferred in(out) | | | (415,344 | ) | | | (1,134,257 | ) |

| Net decrease from share transactions | | | (1,146,183 | ) | | | (14,341 | ) |

| Class W | | | | | | | | |

| Proceeds from sales of shares | | | 8,000,677 | | | | 11,291,567 | |

| Distributions reinvested | | | 974,679 | | | | 1,199,030 | |

| Cost of shares redeemed | | | (8,988,259 | ) | | | (10,281,935 | ) |

| Net transferred in(out) | | | (3,645,027 | ) | | | (83,840 | ) |

| Net increase/(decrease) from share transactions | | | (3,657,930 | ) | | | 2,124,822 | |

| Class I | | | | | | | | |

| Proceeds from sales of shares | | | 15,729,005 | | | | 38,980,395 | |

| Distributions reinvested | | | 4,180,602 | | | | 4,007,867 | |

| Cost of shares redeemed | | | (20,944,050 | ) | | | (17,954,999 | ) |

| Net transferred in(out) | | | 4,751,895 | | | | 1,451,819 | |

| Net increase from share transactions | | | 3,717,452 | | | | 26,485,082 | |

| Class L | | | | | | | | |

| Proceeds from sales of shares | | | 26,026 | | | | 8,714 | |

| Distributions reinvested | | | 462,806 | | | | 468,500 | |

| Cost of shares redeemed | | | (927,995 | ) | | | (1,409,496 | ) |

| Net transferred in(out) | | | (23,479 | ) | | | – | |

| Net decrease from share transactions | | | (462,642 | ) | | | (932,282 | ) |

| Total net increase/(decrease) in net assets | | | (10,505,823 | ) | | | 3,596,605 | |

| See Notes to Consolidated Financial Statements. | |

| 18 | www.altcif.com |

| Alternative Credit Income Fund | Consolidated Statements of Changes in Net Assets (continued) |

| | | For the Year Ended September 30, 2023 | | | For the Year Ended September 30, 2022 | |

| NET ASSETS | | | | | | |

| Beginning of year | | | 262,667,015 | | | | 259,070,410 | |

| End of year | | $ | 252,161,192 | | | $ | 262,667,015 | |

| | | | | | | | | |

| OTHER INFORMATION | | | | | | | | |

| Common Shares Transactions | | | | | | | | |

| Class A | | | | | | | | |

| Issued | | | 286,914 | | | | 658,525 | |

| Distributions reinvested | | | 135,876 | | | | 111,687 | |

| Redeemed | | | (462,919 | ) | | | (682,622 | ) |

| Net Transferred in(out) | | | (68,557 | ) | | | (21,441 | ) |

| Net increase/(decrease) in shares | | | (108,686 | ) | | | 66,149 | |

| | | | | | | | | |

| Class C | | | | | | | | |

| Issued | | | 243,786 | | | | 395,978 | |

| Distributions reinvested | | | 122,973 | | | | 126,440 | |

| Redeemed | | | (441,790 | ) | | | (417,696 | ) |

| Net Transferred in(out) | | | (41,807 | ) | | | (101,599 | ) |

| Net increase/(decrease) in shares | | | (116,838 | ) | | | 3,123 | |

| | | | | | | | | |

| Class W | | | | | | | | |

| Issued | | | 811,476 | | | | 1,047,560 | |

| Distributions reinvested | | | 100,325 | | | | 113,394 | |

| Redeemed | | | (911,159 | ) | | | (951,268 | ) |

| Net Transferred in(out) | | | (361,196 | ) | | | (7,603 | ) |

| Net increase/(decrease) in shares | | | (360,554 | ) | | | 202,083 | |

| | | | | | | | | |

| Class I | | | | | | | | |

| Issued | | | 1,588,810 | | | | 3,612,283 | |

| Distributions reinvested | | | 429,277 | | | | 378,923 | |

| Redeemed | | | (2,125,471 | ) | | | (1,649,652 | ) |

| Net Transferred in(out) | | | 473,281 | | | | 131,447 | |

| Net increase in shares | | | 365,897 | | | | 2,473,001 | |

| | | | | | | | | |

| Class L | | | | | | | | |

| Issued | | | 2,662 | | | | 812 | |

| Distributions reinvested | | | 47,604 | | | | 44,282 | |

| Redeemed | | | (94,229 | ) | | | (127,872 | ) |

| Net Transferred in(out) | | | (2,600 | ) | | | – | |

| Net decrease in shares | | | (46,563 | ) | | | (82,778 | ) |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | September 30, 2023 | 19 |

| Alternative Credit Income Fund | Consolidated Statement of Cash Flows |

| | For the Year Ended September 30, 2023 |

| CASH FLOWS FROM OPERATING ACTIVITIES: | | | |

| Net increase in net assets from operations | | $ | 10,008,037 | |

| Adjustments to reconcile net increase in net assets resulting from operations to net cash provided by operating activities: | | | | |

| Purchase of investment securities | | | (55,738,224 | ) |

| Proceeds from sale of investment securities | | | 53,998,146 | |

| Proceeds from securities sold short transactions | | | 9,243,750 | |

| Payment-in-kind income | | | (1,995,987 | ) |

| Purchase of short-term investment securities - net | | | 864,984 | |

| Amortization of discount and accretion of discount on investments | | | (2,318,091 | ) |

| Net realized (gain)/loss on: | | | | |

| Investments | | | 1,309,135 | |

| Net change in unrealized (appreciation)/depreciation on: | | | | |

| Investments | | | 12,254,777 | |

| (Increase)/Decrease in assets: | | | | |

| Deposit with broker for securities sold short | | | (9,356,283 | ) |

| Receivable from paydowns | | | 1,236,858 | |

| Interest and distributions receivable | | | (869,888 | ) |

| Receivable for investments sold | | | (5,558,729 | ) |

| Prepaid expenses and other assets | | | (23,226 | ) |

| Increase/(Decrease) in liabilities: | | | | |

| Due to Adviser | | | (167,298 | ) |

| Payable for investments purchased | | | (659,371 | ) |

| Administration fees payable | | | 92,203 | |

| Custody fees payable | | | 28,297 | |

| Shareholder servicing fees payable | | | 18,284 | |

| Trustee fees and expenses payable | | | (6,000 | ) |

| Distribution fees payable | | | (2,233 | ) |

| Transfer agency fees payable | | | (54,662 | ) |

| Interest expense on securities sold short payable | | | 246,780 | |

| Incentive fees payable | | | 220,881 | |

| Interest payable | | | 20,906 | |

| Accrued expenses and other liabilities | | | 541,083 | |

| Net cash provided by operating activities | | | 13,334,129 | |

| | | | | |

| CASH FLOWS FROM FINANCING ACTIVITIES: | | | | |

| Proceeds from sales of shares | | | 29,440,695 | |

| Cost of shares redeemed | | | (39,832,345 | ) |

| Borrowings on the BNP line of credit | | | 3,878,632 | |

| Cash distributions paid | | | (9,743,511 | ) |

| Net cash used in financing activities | | | (16,256,529 | ) |

| | | | | |

| Net change in cash & cash equivalents | | | (2,922,400 | ) |

| | | | | |

| Restricted and unrestricted cash, beginning of year | | $ | 2,922,400 | |

| Restricted and unrestricted cash, end of year | | $ | – | |

| | | | | |

| Non-cash financing activities not included herein consist of reinvestment of distributions of: | | $ | 8,149,474 | |

| See Notes to Consolidated Financial Statements. | |

| 20 | www.altcif.com |

| Alternative Credit Income Fund – Class A | Financial Highlights |

| | For a Share Outstanding Throughout the Years Presented |

| | | Year Ended September 30, 2023 | | | Year Ended September 30, 2022 | | | Year Ended September 30, 2021 | | | Year Ended September 30, 2020 | | | Year Ended September 30, 2019 | | |

| NET ASSET VALUE, BEGINNING OF YEAR | | $ | 10.09 | | | $ | 11.09 | | | $ | 9.75 | | | $ | 10.80 | | | $ | 11.09 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.93 | | | | 0.61 | | | | 0.74 | | | | 0.69 | | | | 0.73 | | |

| Net realized and unrealized gain/(loss) on investments | | | (0.53 | ) | | | (0.91 | ) | | | 1.30 | | | | (0.92 | ) | | | (0.32 | ) | |

| Total income/(loss) from investment operations | | | 0.40 | | | | (0.30 | ) | | | 2.04 | | | | (0.23 | ) | | | 0.41 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.70 | ) | | | (0.66 | ) | | | (0.63 | ) | | | (0.70 | ) | | | (0.55 | ) | |

| From return of capital | | | – | | | | (0.04 | ) | | | (0.07 | ) | | | (0.12 | ) | | | (0.15 | ) | |

| Total distributions | | | (0.70 | ) | | | (0.70 | ) | | | (0.70 | ) | | | (0.82 | ) | | | (0.70 | ) | |

| INCREASE/(DECREASE) IN NET ASSET VALUE | | | (0.30 | ) | | | (1.00 | ) | | | 1.34 | | | | (1.05 | ) | | | (0.29 | ) | |

| NET ASSET VALUE, END OF YEAR | | $ | 9.79 | | | $ | 10.09 | | | $ | 11.09 | | | $ | 9.75 | | | $ | 10.80 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| TOTAL RETURN(b) | | | 4.19 | %(c) | | | (2.85 | )% | | | 21.33 | %(c) | | | (1.88 | )%(c)(d) | | | 3.91 | % | |

| | | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000s) | | $ | 36,233 | | | $ | 38,452 | | | $ | 41,519 | | | $ | 38,829 | | | $ | 38,901 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS(e) | | | | | | | | | | | | | | | | | | | | | |

| Including incentive fees, interest expense on borrowings and interest expense on securities sold short: | | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 3.00 | % | | | 2.60 | % | | | 2.84 | % | | | 2.78 | % | | | 2.79 | % | |

| Expenses, net of fees waived/expenses reimbursed by Adviser | | | 2.87 | % | | | 2.60 | % | | | 2.65 | % | | | 2.68 | % | | | 2.67 | % | |

| Excluding incentive fees, interest expense on borrowings and interest expense on securities sold short: | | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.72 | % | | | 2.59 | % | | | 2.78 | % | | | 2.69 | % | | | 2.71 | % | |

| Expenses, net of fees waived/expenses reimbursed by Adviser | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | |

| Net investment income | | | 9.36 | % | | | 5.60 | % | | | 6.87 | % | | | 6.93 | % | | | 6.68 | % | |

| | | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE | | | 23 | % | | | 26 | % | | | 49 | % | | | 39 | % | | | 29 | % | |

| BORROWINGS AT END OF YEAR | | | | | | | | | | | | | | | | | | | | | |

| Aggregate amount outstanding (000s) | | $ | 3,879 | | | | – | | | | – | | | | – | | | | – | | |

| Asset coverage per $1,000 (000s) | | $ | 66,093 | | | | – | | | | – | | | | – | | | | – | | |

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Total returns shown are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distribution, if any. Had the Adviser not absorbed a portion of Fund expenses, total returns would have been lower. Returns shown exclude applicable sales charges. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. |

| (d) | 0.10% of the Fund’s total return consists of a reimbursement by the Adviser for a loss on a transaction. Excluding this item, total return would have been (1.98)%. |

| (e) | Ratios do not include expenses of underlying investment companies and private investment funds in which the Fund invests. |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | September 30, 2023 | 21 |

| Alternative Credit Income Fund – Class C | Financial Highlights |

| | For a Share Outstanding Throughout the Years Presented |

| | | Year Ended September 30, 2023 | | | Year Ended September 30, 2022 | | | Year Ended September 30, 2021 | | | Year Ended September 30, 2020 | | | Year Ended September 30, 2019 | | |

| NET ASSET VALUE, BEGINNING OF YEAR | | $ | 10.21 | | | $ | 11.21 | | | $ | 9.86 | | | $ | 10.92 | | | $ | 11.22 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.86 | | | | 0.53 | | | | 0.66 | | | | 0.62 | | | | 0.66 | | |

| Net realized and unrealized gain/(loss) on investments | | | (0.54 | ) | | | (0.90 | ) | | | 1.31 | | | | (0.92 | ) | | | (0.34 | ) | |

| Total income/(loss) from investment operations | | | 0.32 | | | | (0.37 | ) | | | 1.97 | | | | (0.30 | ) | | | 0.32 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.63 | ) | | | (0.59 | ) | | | (0.56 | ) | | | (0.66 | ) | | | (0.48 | ) | |

| From return of capital | | | – | | | | (0.04 | ) | | | (0.06 | ) | | | (0.10 | ) | | | (0.14 | ) | |

| Total distributions | | | (0.63 | ) | | | (0.63 | ) | | | (0.62 | ) | | | (0.76 | ) | | | (0.62 | ) | |

INCREASE/(DECREASE) IN NET ASSET VALUE | | | (0.31 | ) | | | (1.00 | ) | | | 1.35 | | | | (1.06 | ) | | | (0.30 | ) | |

| NET ASSET VALUE, END OF YEAR | | $ | 9.90 | | | $ | 10.21 | | | $ | 11.21 | | | $ | 9.86 | | | $ | 10.92 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| TOTAL RETURN(b) | | | 3.33 | %(c) | | | (3.48 | )% | | | 20.36 | %(c) | | | (2.61 | )%(c)(d) | | | 3.05 | % | |

| | | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000s) | | $ | 40,947 | | | $ | 43,391 | | | $ | 47,640 | | | $ | 43,984 | | | $ | 41,575 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS(e) | | | | | | | | | | | | | | | | | | | | | |

| Including incentive fees, interest expense on borrowings and interest expense on securities sold short: | | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 3.74 | % | | | 3.38 | % | | | 3.59 | % | | | 3.53 | % | | | 3.55 | % | |

| Expenses, net of fees waived/expenses reimbursed by Adviser | | | 3.62 | % | | | 3.35 | % | | | 3.40 | % | | | 3.43 | % | | | 3.42 | % | |

| Excluding incentive fees, interest expense on borrowings and interest expense on securities sold short: | | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 3.46 | % | | | 3.37 | % | | | 3.53 | % | | | 3.44 | % | | | 3.47 | % | |

| Expenses, net of fees waived/expenses reimbursed by Adviser | | | 3.34 | % | | | 3.34 | % | | | 3.34 | % | | | 3.34 | % | | | 3.34 | % | |

| Net investment income | | | 8.61 | % | | | 4.87 | % | | | 6.12 | % | | | 6.19 | % | | | 5.95 | % | |

| | | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE | | | 23 | % | | | 26 | % | | | 49 | % | | | 39 | % | | | 29 | % | |

| BORROWINGS AT END OF YEAR | | | | | | | | | | | | | | | | | | | | | |

| Aggregate amount outstanding (000s) | | $ | 3,879 | | | | – | | | | – | | | | – | | | | – | | |

| Asset coverage per $1,000 (000s) | | $ | 66,093 | | | | – | | | | – | | | | – | | | | – | | |

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Total returns shown are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distribution, if any. Had the Adviser not absorbed a portion of Fund expenses, total returns would have been lower. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. |

| (d) | 0.10% of the Fund’s total return consists of a reimbursement by the Adviser for a loss on a transaction. Excluding this item, total return would have been (2.71)%. |

| (e) | Ratios do not include expenses of underlying investment companies and private investment funds in which the Fund invests. |

| See Notes to Consolidated Financial Statements. | |

| 22 | www.altcif.com |

| Alternative Credit Income Fund – Class W | Financial Highlights |

| | For a Share Outstanding Throughout the Years Presented |

| | | Year Ended September 30, 2023 | | | Year Ended September 30, 2022 | | | Year Ended September 30, 2021 | | | Year Ended September 30, 2020 | | | Year Ended September 30, 2019 | | |

| NET ASSET VALUE, BEGINNING OF YEAR | | $ | 10.08 | | | $ | 11.08 | | | $ | 9.74 | | | $ | 10.79 | | | $ | 11.09 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.93 | | | | 0.61 | | | | 0.74 | | | | 0.69 | | | | 0.73 | | |

| Net realized and unrealized gain/(loss) on investments | | | (0.53 | ) | | | (0.91 | ) | | | 1.30 | | | | (0.92 | ) | | | (0.33 | ) | |

| Total income/(loss) from investment operations | | | 0.40 | | | | (0.30 | ) | | | 2.04 | | | | (0.23 | ) | | | 0.40 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.70 | ) | | | (0.66 | ) | | | (0.63 | ) | | | (0.70 | ) | | | (0.55 | ) | |

| From return of capital | | | – | | | | (0.04 | ) | | | (0.07 | ) | | | (0.12 | ) | | | (0.15 | ) | |

| Total distributions | | | (0.70 | ) | | | (0.70 | ) | | | (0.70 | ) | | | (0.82 | ) | | | (0.70 | ) | |

| INCREASE/(DECREASE) IN NET ASSET VALUE | | | (0.30 | ) | | | (1.00 | ) | | | 1.34 | | | | (1.05 | ) | | | (0.30 | ) | |

| NET ASSET VALUE, END OF YEAR | | $ | 9.78 | | | $ | 10.08 | | | $ | 11.08 | | | $ | 9.74 | | | $ | 10.79 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| TOTAL RETURN(b) | | | 4.19 | %(c) | | | (2.86 | )% | | | 21.35 | %(c) | | | (1.89 | )%(c)(d) | | | 3.81 | % | |

| | | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000s) | | $ | 53,123 | | | $ | 58,382 | | | $ | 61,915 | | | $ | 69,993 | | | $ | 85,642 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS(e) | | | | | | | | | | | | | | | | | | | | | |

| Including incentive fees, interest expense on borrowings and interest expense on securities sold short: | | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.98 | % | | | 2.60 | % | | | 2.81 | % | | | 2.75 | % | | | 2.79 | % | |

| Expenses, net of fees waived/expenses reimbursed by Adviser | | | 2.87 | % | | | 2.60 | % | | | 2.65 | % | | | 2.68 | % | | | 2.67 | % | |

| Excluding incentive fees, interest expense on borrowings and interest expense on securities sold short: | | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.70 | % | | | 2.59 | % | | | 2.75 | % | | | 2.66 | % | | | 2.71 | % | |

| Expenses, net of fees waived/expenses reimbursed by Adviser | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | |

| Net investment income | | | 9.36 | % | | | 5.63 | % | | | 6.89 | % | | | 6.92 | % | | | 6.68 | % | |

| | | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE | | | 23 | % | | | 26 | % | | | 49 | % | | | 39 | % | | | 29 | % | |

| BORROWINGS AT END OF YEAR | | | | | | | | | | | | | | | | | | | | | |

| Aggregate amount outstanding (000s) | | $ | 3,879 | | | | – | | | | – | | | | – | | | | – | | |

| Asset coverage per $1,000 (000s) | | $ | 66,093 | | | | – | | | | – | | | | – | | | | – | | |

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Total returns shown are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distribution, if any. Had the Adviser not absorbed a portion of Fund expenses, total returns would have been lower. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. |

| (d) | 0.10% of the Fund’s total return consists of a reimbursement by the Adviser for a loss on a transaction. Excluding this item, total return would have been (1.99)%. |

| (e) | Ratios do not include expenses of underlying investment companies and private investment funds in which the Fund invests. |

| See Notes to Consolidated Financial Statements. | |

| Annual Report | September 30, 2023 | 23 |

| Alternative Credit Income Fund – Class I | Financial Highlights |

| | For a Share Outstanding Throughout the Years Presented |

| | | Year Ended September 30, 2023 | | | Year Ended September 30, 2022 | | | Year Ended September 30, 2021 | | | Year Ended September 30, 2020 | | | Year Ended September 30, 2019 | | |

| NET ASSET VALUE, BEGINNING OF YEAR | | $ | 10.11 | | | $ | 11.11 | | | $ | 9.77 | | | $ | 10.82 | | | $ | 11.12 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.95 | | | | 0.63 | | | | 0.76 | | | | 0.72 | | | | 0.77 | | |

| Net realized and unrealized gain/(loss) on investments | | | (0.53 | ) | | | (0.90 | ) | | | 1.30 | | | | (0.92 | ) | | | (0.34 | ) | |

| Total income/(loss) from investment operations | | | 0.42 | | | | (0.27 | ) | | | 2.06 | | | | (0.20 | ) | | | 0.43 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.73 | ) | | | (0.69 | ) | | | (0.65 | ) | | | (0.73 | ) | | | (0.57 | ) | |

| From return of capital | | | – | | | | (0.04 | ) | | | (0.07 | ) | | | (0.12 | ) | | | (0.16 | ) | |