UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-23016

(Investment Company Act file number)

Resource Credit Income Fund

(Exact name of Registrant as specified in charter)

650 Madison Avenue, 23rd Floor

New York, NY 10022

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

Corporation Trust Center, 1209 Orange Street

Wilmington, DE 19801

(Name and address of agent for service)

Registrant's telephone number, including area code: (212) 891-2880

Date of fiscal year end: September 30

Date of reporting period: October 1, 2019– September 30, 2020

Item 1. Reports to Stockholders.

TABLE OF CONTENTS

| Shareholder Letter | 1 |

| Portfolio Update | 4 |

| Consolidated Schedule of Investments | 6 |

| Consolidated Statement of Assets and Liabilities | 11 |

| Consolidated Statement of Operations | 12 |

| Consolidated Statements of Changes in Net Assets | 13 |

| Financial Highlights | |

| Class A | 15 |

| Class C | 17 |

| Class W | 19 |

| Class I | 21 |

| Class L | 23 |

| Notes to Consolidated Financial Statements | 24 |

| Report of Independent Registered Public Accounting Firm | 35 |

| Additional Information | 36 |

| Trustees & Officers | 38 |

| Privacy Notice | 41 |

Beginning in 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically by calling the Fund at 833-404-4103, or submitting a signed letter of instruction requesting paperless reports to PO Box 219169, Kansas City, MO 64121. If you own shares through a financial intermediary, you may contact your financial intermediary to request your shareholder reports electronically.

You may elect to receive all future reports in paper free of charge. You can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by calling the Fund at 833-404-4103, or by submitting a signed letter of instruction requesting paper reports to PO Box 219169, Kansas City, MO 64121. If you own shares through a financial intermediary, contact the financial intermediary to request paper copies. Your election to receive reports in paper will apply to all funds held with the fund complex or your financial intermediary.

| Resource Credit Income Fund | Shareholder Letter |

September 30, 2020 (Unaudited)

Dear Shareholders:

First and foremost, we hope you and your family remain safe. While health and welfare remain everyone’s primary concern, we want to provide insights into the performance and positioning of the Resource Credit Income Fund (the “Fund”) for the year ended September 30, 2020 (the “annual period”).

For the annual period, the Fund1 posted a return of -2.0%. Fund performance was helped by a return of 14.5% during the six months ended September 30, 2020 — handily outpacing the Barclay’s U.S. Aggregate Total Return Value Index2 (+3.5%) and beating the S&P/LSTA Leveraged Loan Total Return Index3 (+14.2%). A number of notable “wins” during the last six months helped drive these returns.

The Fund purchased loans of sewing and crafts retailer Jo-Ann Stores LLC’s in 2019 at roughly 35 cents on the dollar (yielding greater than 30%). These loans traded down to the single-digits during the COVID-19 panic as investors indiscriminately punished all retailers.

In September 2020, Jo-Ann Stores reported historically strong quarterly results for the quarter ended August 1, 2020 as “Do It Yourself” mask-making drove a dramatic increase in store traffic. “Same Store Sales” increased 54% and EBITDA increased to $100.9 million, compared to a loss of $2.4 million in the same period last year. Importantly, management used the windfall to buyback the company’s debt in the open market. The Fund’s loans now trade in the 70s, helping the Fund’s investment in Jo-Ann Stores to produce a return of 221.0% during the last twelve months.

Another Fund holding, Advantage Sales and Marketing, a marketing services business targeting the grocery channel, also boosted its bottom-line during COVID-19. Management nimbly repositioned many of its in-store marketing employees to providing temporary cleaning services to their grocery customers, enabling Advantage Sales and Marketing to post significant growth during 2020.

Bolstered by recent performance, Advantage Sales and Marketing announced in September that it would be acquired by a Special Purpose Acquisition Company (SPAC). As part of the transaction, which is slated to close in 4Q2020, the Fund’s loans will be refinanced at par. Advantage Sales and Marketing loans that traded in the 60s during the March/April selloff have re-priced in the high 90s and are expected to be taken-out at 100 (par) after deal close, providing another gain for the Fund’s shareholders.

In our semi-annual report letter, we remarked that the Fund’s investments in business development companies (BDCs) were, in our opinion, dramatically oversold during the early stages of COVID-19. Despite declining 40% in the month of March alone, the Fund’s allocation to BDCs finished the annual period down 15.2%; for comparison, the S&P BDC Index4 returned -19.7% during the same period.

The Fund’s BDC segment decidedly outpaced the broader BDC market during the six months ended September 30, 2020—gaining 45.6% compared to a return of 36.9% for the S&P BDC Index during that period. The Fund’s largest gainers included shares of TriplePoint Venture Growth BDC Corp. (+105.2%), PennantPark Floating Rate Capital Ltd. (+86.6%), Whitehorse Finance, Inc. (+47.7%) and FS KKR Capital Corp. (+42.1%).

Despite the recent recovery, the S&P BDC Index remained negative for the year through September 30, 2020 at -22.6%. Highlighting this dynamic, the S&P BDC Index yielded 9.3% at the beginning of the year before peaking at 18.9% during the COVID-19 selloff; as of September 30, 2020, the S&P BDC Index yields around 11.6%. Hence, the Fund’s BDC investments have not fully retraced its year-to-date losses as of September 30, 2020, but we continue to find opportunities in this beaten-up market segment.

As for performance detractors, we previously touched on the bonds of CEC Entertainment, Inc. (also known as Chuck E. Cheese), which provided one of the Fund’s few negative performers during the last six months. Nevertheless, CEC proved a meaningful performance drag as the Fund’s investment value plummeted near zero amidst the COVID-induced selloff.

In late June, Chuck E. Cheese sought bankruptcy protection after the pandemic brought its business to a dramatic halt. Resource has been working diligently with other creditors to support the company’s restructuring and to help recover value for the Fund’s investors.

The Fund’s Private Investment Funds gained 0.7% for the annual period. The Fund redeemed its investment in GoldenTree Credit Opportunities Fund LP, given that fund’s uneven performance and to help bolster the Fund’s liquidity. The Fund used the GoldenTree inflow to pay off Fund-level debt and return to a zero leverage position as of September 30, 2020.

The Fund has employed leverage opportunistically throughout its more than five-year history. During periods of volatility — most notably, the Oil & Gas panic of 2015 and 2016, the sudden market selloff in 4Q2018 and during the COVID-19-crisis in March 2020 —the Fund deployed debt to purchase securities at what I believe are “fire sale” prices. The Fund’s quarterly liquidity and borrowing capacity positions the Fund to capitalize on market dislocation.

| Annual Report | September 30, 2020 | 1 |

| Resource Credit Income Fund | Shareholder Letter |

September 30, 2020 (Unaudited)

The Fund’s core market segment—lower middle market corporate credit—remains one of the last “cheap” parts of the current market. We continue to find credits trading at meaningful discounts and attractive yields. Nevertheless, the market is far from the “ultra-cheap” levels witnessed in March/April. Hence, we believe managing the Fund without significant leverage represents a prudent orientation in the current environment.

Fund Performance

During the year ended September 30, 2020, the Fund posted a loss of -2.0%1.

Even during periods of strong gains, as experienced over the last six months, we encourage our investors to view the Fund from a long-term perspective. The Fund has outpaced its most relevant fixed income indices since inception5, including Barclay’s U.S. Aggregate Total Return Value Index, ICE BofA U.S. High Yield Index6 and S&P/LSTA Leveraged Loan Total Return Index.

Positioning

The Fund ended calendar year 2019 with a 10% allocation to BDCs, the lowest positioning in its history. This weighting proved prescient as the market pummeled public BDCs during the COVID-19 downdraft.

Buying into this selloff, the Fund has increased its BDC positioning to around 15% at the end of the annual period. Again, with the S&P BDC Index currently yielding around 11.6% compared to around 9.3% pre-COVID-19, we continue to view BDCs as “cheap” and expect to maintain a relatively elevated allocation.

The Fund ended the annual period with roughly 60% of assets under management (“AUM”) invested in Direct Credit, which represents the Fund’s investments in bonds, loans and CLOs. This is roughly in-line with historic positioning.

The Fund ended the annual period with 23.3% of AUM invested in Private Credit. The Fund anticipates modest capital calls from our existing Private Investment Funds in the coming quarters. The Fund ended the annual period with a modest cash position of 1.3% of AUM.

Conclusion

The Fund continued to execute on its core investment mandate—generating high income-oriented returns from investments across the corporate credit universe, including both public and private markets. The Fund remains, in our opinion, a small and nimble credit fund that attempts to uncover opportunities below the radar of the big credit shops. This capability has become crucial to our investors in the current market.

In short, investors find themselves trapped in a brutal backdrop for traditional fixed income. Yields for so-called “high quality” corporate credit have collapsed as global central banks have pushed rates near zero. Direct purchases of corporate bonds by central banks have further drained yield from traditional investments.

We would highlight that the U.S. Federal Reserve (“Fed”) has been purchasing bonds of Apple Inc., a company that enjoys a $2 trillion market cap. This remarkable policy decision underscores the Fed’s commitment to maintaining liquidity and, in turn, keeping rates low. Whether this represents a prudent policy can be argued. However, it is not our job to debate what the Fed should do, but rather to anticipate and respond to what we expect the Fed will do.

In our view, the Fed will likely continue propping up asset prices, which could spell the demise of many traditional fixed income vehicles. In recent months, asset managers have scrambled to slash, if not eliminate, fees to maintain a positive yield on their funds. In this environment, investors should consider alternative fixed income solutions like the Fund.

Fund investors have enjoyed a level dividend of 17.5 cents per share for greater than five years. The yield on the Class A Shares of the Fund of approximately 7.2% stands-out in a world where the U.S. 10 Year Treasury yields approximately 0.68% and U.S. Investment Grade yields 2.01% (before fees)7 as of September 30, 2020. We have always viewed the Fund’s yield as objectively attractive, but the impact of COVID-19 has boosted the Fund’s relative value.

More important than our income returns, the Fund has unequivocally demonstrated its resilience in the twelve months ended September 30, 2020, which included (1) the Fund’s announcement in early December 2019 of a proposed reorganization with another fund and (2) decreased sales (as measured against historical levels) amid the loss of salesforce and suspension of many selling agreements given this announcement. As such, the Fund entered the COVID-downturn in an unsettled state.

| Resource Credit Income Fund | Shareholder Letter |

September 30, 2020 (Unaudited)

The Fund nevertheless navigated these rough waters and we believe is positioned for continued long-term success, as a now more battle-tested Fund. In our view, nothing is more important in the world of investing than resilience.

Thank you for your continued support in the Resource Credit Income Fund.

Regards,

Michael Terwilliger, CFA

Portfolio Manager*

Resource Credit Income Fund

| * | Effective October 31, 2020, Sierra Crest Investment Management LLC (“Sierra Crest”) replaced Resource Alternative Advisor, LLC (“Resource”) as the investment advisor of the Fund. Michael Terwilliger has joined Sierra Crest as a portfolio manager to the Fund. For additional information, please see the Subsequent Event footnote to the Consolidated Financial Statements. |

| 1 | Fund performance refers to that of Class I. Total returns presented are calculated based on the traded NAV on September 30, 2020. |

| 2 | Barclays U.S. Aggregate Total Return Value Index - The Barclays U.S. Aggregate Total Return Value Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency). Investors cannot invest directly in an index. |

| 3 | S&P/LSTA Leveraged Loan Total Return Index - The S&P/LSTA Leveraged Loan Index is a market value-weighted index designed to measure the performance of the U.S. leveraged loan market based upon market weightings, spreads and interest payments. Investors cannot invest directly in an index. |

| 4 | S&P BDC Index - The S&P BDC Index is designed to track leading business development companies that trade on major U.S. exchanges. Investors cannot invest directly in an index. |

| 5 | Fund and index performance measured from April 17, 2015 to September 30, 2020. During this period, the Fund (Class I) posted annualized performance of 5.53%, relative to 3.64%, 4.85% and 3.42% for the Barclay’s U.S. Aggregate Total Return Value Index, ICE BofA U.S. High Yield Index, and S&P/LSTA Leveraged Loan Total Return Index, respectively. |

| 6 | ICE BofA U.S. High Yield Index – The ICE BofA U.S. High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market. Investors cannot invest directly in an index. |

| 7 | ICE BofA U.S. Corporate Index (C0A0) – The ICE BofA U.S. Corporate Index tracks the performance of U.S. dollar denominated investment grade corporate debt publicly issued in the U.S. domestic market. Investors cannot invest directly in an index. |

| Annual Report | September 30, 2020 | 3 |

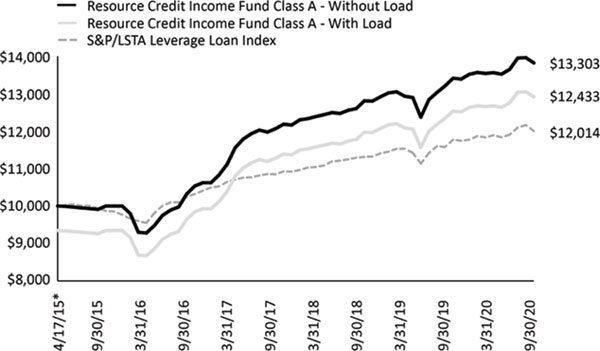

| Resource Credit Income Fund | Portfolio Update |

September 30, 2020 (Unaudited)

The Fund’s performance figures for the periods ended September 30, 2020, compared to its benchmark:

| Resource Credit Income Fund | 1 Month | Quarter | 6 Month | YTD | 1 Year | 3 Year | 5 Year | Since Inception* | Inception |

| Class A Shares – Without Load | 1.38% | 6.84% | 17.15% | -4.63% | -1.88% | 2.65% | 5.87% | 5.37% | 4/17/2015 |

| Class A Shares – With Load | -4.47% | 0.66% | 10.37% | -10.12% | -7.53% | 0.64% | 4.45% | 4.07% | 4/17/2015 |

| Class C Shares – Without Load | 1.30% | 6.58% | 16.67% | -5.16% | -2.61% | 1.89% | 5.39% | 4.93% | 4/17/2015 |

| Class C Shares – With Load(a) | -1.20% | 4.03% | 13.98% | -7.50% | -5.00% | 1.38% | 5.07% | 4.64% | 4/17/2015 |

| Class W Shares – Without Load | 1.38% | 6.73% | 17.03% | -4.64% | -1.89% | 2.65% | 5.77% | 5.28% | 4/17/2015 |

| Class I Shares – Without Load | 1.45% | 6.90% | 17.27% | -4.42% | -1.61% | 2.92% | 6.13% | 5.61% | 4/17/2015 |

| Class L Shares – Without Load | 1.42% | 6.77% | 17.01% | -4.72% | -2.04% | 2.42% | 0.00% | 2.57% | 7/28/2017 |

| Class L Shares – With Load | -2.85% | 2.26% | 12.07% | -8.78% | -6.21% | 0.96% | 0.00% | 1.17% | 7/28/2017 |

| S&P/LSTA Leverage Loan Index | 0.63% | 4.14% | 14.24% | -0.66% | 1.06% | 3.10% | 4.01% | 3.42% | 4/17/2015 |

| (a) | Effective as of December 23, 2016, Class C shares no longer have a sales charge. |

The S&P/LSTA Leveraged Loan Index is a market value-weighted index designed to measure the performance of the U.S. leveraged loan market based upon market weightings, spreads and interest payments. Investors cannot invest directly in an index.

Past performance is not indicative of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. Performance figures for periods less than one year are not annualized. As of the Fund’s most recent prospectus dated January 15, 2020, the Fund’s total annual operating expenses, including acquired fund fees and expenses, before fee waivers is 5.08% for Class A, 5.84% for Class C, 5.08% for Class W, 4.83% for Class I and 5.35% for Class L shares. After fee waivers, the Fund’s total annual operating expense is 4.96% for Class A, 5.71% for Class C, 4.96% for Class W, 4.71% for Class I and 5.21% for Class L shares. Class A shares are subject to maximum sales loads of 5.75% imposed on purchases. Class L shares are subject to a maximum sales load of 4.25% imposed on purchases. Share repurchases within 365 days may be subject to an early withdrawal charge of 0.50% for Class A and 1.00% for Class C shares. For performance information current to the most recent month-end, please call toll-free 1-833-404-4103.

| Resource Credit Income Fund | Portfolio Update |

September 30, 2020 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment

| * | Commencement of operations for Class A Shares. |

Consolidated Portfolio Composition as of September 30, 2020

| Asset Type | Percent of Net Assets |

| Bank Loans | 31.73% |

| Bonds & Notes | 24.50% |

| Private Investment Funds | 23.33% |

| Common Equity | 14.95% |

| Preferred Stocks | 3.02% |

| Short Term Investment | 0.95% |

| Total Investments | 98.48% |

| Other Assets in Excess of Liabilities | 1.52% |

| Net Assets | 100.00% |

Please see the Consolidated Schedule of Investments for a detailed listing of the Fund’s holdings.

| Annual Report | September 30, 2020 | 5 |

| Resource Credit Income Fund | Consolidated Schedule of Investments |

September 30, 2020

| | | Coupon | | | Reference Rate & Spread | | Maturity | | | Principal | | | Value | |

| BANK LOANS (31.73%)(a) | | | | | | | | | | | | | | | | | | |

| Communication Services (0.93%) | | | | | | | | | | | | | | | | | | |

| Advantage Sales & Marketing, Inc., Second Lien Term Loan | | | 7.50% | | | 1M US L + 6.50%, 1.00% Floor | | | 07/25/2022 | | | $ | 2,425,000 | | | $ | 2,352,420 | |

| Consumer Discretionary (4.47%) | | | | | | | | | | | | | | | | | | |

| Bass Pro Group LLC, First Lien Initial Term Loan | | | 5.75% | | | 3M US L + 5.00%, 0.75% Floor | | | 09/25/2024 | | | | 2,961,832 | | | | 2,941,484 | |

| BBB Industries US Holdings, Inc., Second Lien Term Loan | | | 9.58% | | | 3M US L + 8.50% | | | 06/29/2026 | | | | 5,000,000 | | | | 3,625,000 | |

| Jo-Ann Stores LLC, Second Lien Initial Term Loan | | | 10.25% | | | 3M US L + 9.25%, 1.00% Floor | | | 05/21/2024 | | | | 4,277,967 | | | | 3,550,713 | |

| WASH Multifamily Laundry Systems LLC, Second Lien Initial US Term Loan | | | 8.00% | | | 1M US L + 7.00%, 1.00% Floor | | | 05/15/2023 | | | | 1,320,145 | | | | 1,207,933 | |

| | | | | | | | | | | | | | | | | | 11,325,130 | |

| Consumer Staples (3.68%) | | | | | | | | | | | | | | | | | | |

| 8th Avenue Food & Provisions, Inc., Second Lien Term Loan | | | 7.90% | | | 1M US L + 7.75% | | | 10/01/2026 | | | | 2,500,000 | | | | 2,471,875 | |

| Alphabet Holding Co., Inc., Second Lien Initial Term Loan | | | 7.90% | | | 1M US L + 7.75% | | | 08/15/2025 | | | | 5,000,000 | | | | 4,850,000 | |

| Winebow Group LLC, First Lien Term Loan | | | 4.75% | | | 1M US L + 3.75%, 1.00% Floor | | | 07/01/2021 | | | | 2,382,933 | | | | 1,984,912 | |

| | | | | | | | | | | | | | | | | | 9,306,787 | |

| Financials (2.62%) | | | | | | | | | | | | | | | | | | |

| Asurion LLC, Second Lien Replacement B-2 Term Loan | | | 6.65% | | | 1M US L + 6.50% | | | 08/04/2025 | | | | 4,696,970 | | | | 4,714,090 | |

| Asurion LLC, First Lien New B-7 Term Loan | | | 3.15% | | | 1M US L + 3.00% | | | 11/03/2024 | | | | 1,959,900 | | | | 1,930,100 | |

| | | | | | | | | | | | | | | | | | 6,644,190 | |

| Health Care (5.65%) | | | | | | | | | | | | | | | | | | |

| Outcomes Group Holdings, Inc., Second Lien Term Loan | | | 7.72% | | | 3M US L + 7.50% | | | 10/26/2026 | | | | 2,000,000 | | | | 1,800,000 | |

| Sound Inpatient Physicians, Inc., Second Lien Initial Term Loan | | | 6.90% | | | 1M US L + 6.75% | | | 06/28/2026 | | | | 1,000,000 | | | | 979,380 | |

| Upstream Newco, Inc., Second Lien Term Loan | | | 8.65% | | | 1M US L + 8.50% | | | 11/20/2027 | | | | 7,500,000 | | | | 7,312,500 | |

| Viant Medical Holdings, Inc., Second Lien Initial Term Loan | | | 7.90% | | | 1M US L + 7.75% | | | 07/02/2026 | | | | 5,000,000 | | | | 4,202,500 | |

| | | | | | | | | | | | | | | | | | 14,294,380 | |

| Industrials (6.82%) | | | | | | | | | | | | | | | | | | |

| Jazz Acquisition, Inc., Second Lien Term Loan | | | 8.15% | | | 1M US L + 8.00% | | | 06/18/2027 | | | | 4,000,000 | | | | 3,135,000 | |

| Restaurant Technologies, Inc., Second Lien Initial Term Loan | | | 6.65% | | | 1M US L + 6.50% | | | 10/01/2026 | | | | 4,500,000 | | | | 4,185,000 | |

| Tempo Acquisition LLC, First Lien Extended Term Loan | | | 3.75% | | | 1M US L + 3.25%, 0.50% Floor | | | 10/31/2026 | | | | 2,592,018 | | | | 2,521,554 | |

| USS Ultimate Holdings, Inc., Second Lien Initial Term Loan | | | 8.75% | | | 3M US L + 7.75%, 1.00% Floor | | | 08/25/2025 | | | | 7,750,000 | | | | 7,415,820 | |

| | | | | | | | | | | | | | | | | | 17,257,374 | |

| Information Technology (5.83%) | | | | | | | | | | | | | | | | | | |

| EagleView Technology Corp., First Lien Term Loan | | | 3.76% | | | 3M US L + 3.50% | | | 08/14/2025 | | | | 4,934,773 | | | | 4,786,113 | |

| EagleView Technology Corp., Second Lien Term Loan | | | 8.50% | | | 3M US L + 7.50%, 1.00% Floor | | | 08/14/2026 | | | | 2,000,000 | | | | 1,740,000 | |

| Hyland Software, Inc., Second Lien Initial Term Loan | | | 7.75% | | | 1M US L + 7.00%, 0.75% Floor | | | 07/07/2025 | | | | 2,000,000 | | | | 1,995,840 | |

| Renaissance Holdings Corp., Second Lien Initial Term Loan | | | 7.15% | | | 1M US L + 7.00% | | | 05/29/2026 | | | | 6,486,683 | | | | 6,240,189 | |

| | | | | | | | | | | | | | | | | | 14,762,142 | |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund | Consolidated Schedule of Investments |

September 30, 2020

| | | Coupon | | | Reference Rate & Spread | | Maturity | | | Principal | | | Value | |

| Materials (1.73%) | | | | | | | | | | | | | | |

| Ball Metalpack Finco LLC, Second Lien Initial Term Loan | | | 9.75% | | | 3M US L + 8.75%, 1.00% Floor | | | 07/31/2026 | | | $ | 5,000,000 | | | $ | 4,375,000 | |

| | | | | | | | | | | | | | | | | | | |

| TOTAL BANK LOANS | | | | | | | | | | | | | | | | | | |

| (Cost $83,968,988) | | | | | | | | | | | | | | | | | 80,317,423 | |

| | | | | | | | | | | | | | | | | | | |

| BONDS & NOTES (24.50%) | | | | | | | | | | | | | | | | | | |

| ASSET BACKED SECURITIES (2.73%)(a)(b) | | | | | | | | | | | | | | | | | | |

| Financials (2.73%) | | | | | | | | | | | | | | | | | | |

| Bowman Park CLO, Ltd., Class F(c) | | | 7.26% | | | 3M US L + 7.00% | | | 11/23/2025 | | | | 1,000,000 | | | | 761,014 | |

| Canyon Capital CLO 2014-1, Ltd., Class ER | | | 7.97% | | | 3M US L + 7.70% | | | 01/30/2031 | | | | 1,000,000 | | | | 638,895 | |

| Jamestown CLO V, Ltd., Class F(c) | | | 6.12% | | | 3M US L + 5.85% | | | 01/17/2027 | | | | 1,452,399 | | | | 447,847 | |

| OCP CLO 2013-4, Ltd., Class DR(c) | | | 7.03% | | | 3M US L + 6.77% | | | 04/24/2029 | | | | 1,000,000 | | | | 874,196 | |

| Octagon Investment Partners 36, Ltd., Class F | | | 8.03% | | | 3M US L + 7.75% | | | 04/15/2031 | | | | 1,000,000 | | | | 740,110 | |

| Octagon Investment Partners XIV, Ltd., Class ER(c) | | | 8.63% | | | 3M US L + 8.35% | | | 07/15/2029 | | | | 2,132,000 | | | | 1,441,104 | |

| Saranac CLO VII, Ltd., Class ER | | | 6.97% | | | 3M US L + 6.72% | | | 11/20/2029 | | | | 519,777 | | | | 303,075 | |

| Tralee CLO II, Ltd., Class ER(c) | | | 8.12% | | | 3M US L + 7.85% | | | 07/20/2029 | | | | 1,024,173 | | | | 707,424 | |

| Tralee CLO II, Ltd., Class FR(c) | | | 9.12% | | | 3M US L + 8.85% | | | 07/20/2029 | | | | 1,000,000 | | | | 166,914 | |

| Trinitas CLO III, Ltd., Class F(c) | | | 6.78% | | | 3M US L + 6.50% | | | 07/15/2027 | | | | 572,540 | | | | 223,124 | |

| Voya CLO 2014-2, Ltd., Class ER | | | 7.97% | | | 3M US L + 7.70% | | | 04/17/2030 | | | | 1,000,000 | | | | 610,721 | |

| | | | | | | | | | | | | | | | | | 6,914,424 | |

| CONVERTIBLE CORPORATE BONDS (1.35%) | | | | | | | | | | | | | | | | | | |

| Financials (1.35%) | | | | | | | | | | | | | | | | | | |

| GSV Capital Corp. | | | 4.750% | | | N/A | | | 03/28/2023 | | | | 515,000 | | | | 599,357 | |

| Scorpio Tankers, Inc.(c) | | | 3.000% | | | N/A | | | 05/15/2022 | | | | 3,025,000 | | | | 2,813,849 | |

| | | | | | | | | | | | | | | | | | 3,413,206 | |

| CORPORATE BONDS (20.42%) | | | | | | | | | | | | | | | | | | |

| Consumer Discretionary (20.42%) | | | | | | | | | | | | | | | | | | |

| Carvana Co.(c) | | | 8.875% | | | N/A | | | 10/01/2023 | | | | 3,300,000 | | | | 3,446,454 | |

| CEC Entertainment, Inc.(c)(d) | | | 8.000% | | | N/A | | | 02/15/2022 | | | | 11,549,000 | | | | 1,039,410 | |

| Cooke Omega Investments, Inc. / Alpha VesselCo Holdings, Inc.(b)(c) | | | 8.500% | | | N/A | | | 12/15/2022 | | | | 6,011,000 | | | | 6,227,486 | |

| Dole Food Co., Inc.(b)(c) | | | 7.250% | | | N/A | | | 06/15/2025 | | | | 7,000,000 | | | | 6,990,515 | |

| H-Food Holdings LLC / Hearthside Finance Co., Inc.(b)(c) | | | 8.500% | | | N/A | | | 06/01/2026 | | | | 11,438,000 | | | | 11,220,392 | |

| Mileage Plus Holdings LLC / Mileage Plus Intellectual Property Assets, Ltd.(b)(c) | | | 6.500% | | | N/A | | | 06/20/2027 | | | | 1,000,000 | | | | 1,043,750 | |

| Monitronics - Escrow(c)(d) | | | –% | | | N/A | | | 12/31/2049 | | | | 2,650,000 | | | | – | |

| New Enterprise Stone & Lime Co., Inc.(b)(c) | | | 6.250% | | | N/A | | | 03/15/2026 | | | | 1,475,000 | | | | 1,522,016 | |

| New Enterprise Stone & Lime Co., Inc.(b) | | | 9.750% | | | N/A | | | 07/15/2028 | | | | 1,000,000 | | | | 1,085,000 | |

| Trident TPI Holdings, Inc.(b)(c) | | | 6.625% | | | N/A | | | 11/01/2025 | | | | 2,399,000 | | | | 2,371,759 | |

| Trident TPI Holdings, Inc.(b)(c) | | | 9.250% | | | N/A | | | 08/01/2024 | | | | 7,000,000 | | | | 7,448,350 | |

| Whiting Petroleum Corp.(c)(d) | | | –% | | | N/A | | | 12/31/2020 | | | | 2,600,000 | | | | – | |

| Wolverine Escrow LLC(b)(c) | | | 13.125% | | | N/A | | | 11/15/2027 | | | | 5,000,000 | | | | 3,512,500 | |

| Wolverine Escrow LLC(b)(c) | | | 9.000% | | | N/A | | | 11/15/2026 | | | | 2,000,000 | | | | 1,653,750 | |

| Wolverine Escrow LLC(b)(c) | | | 8.500% | | | N/A | | | 11/15/2024 | | | | 5,000,000 | | | | 4,112,500 | |

| | | | | | | | | | | | | | | | | | 51,673,882 | |

| TOTAL BONDS & NOTES | | | | | | | | | | | | | | | | | | |

| (Cost $74,808,344) | | | | | | | | | | | | | | | | | 62,001,512 | |

| | | Shares | | | Value | |

| COMMON EQUITY (14.95%) | | | | | | | | |

| Financials (14.95%) | | | | | | | | |

| Apollo Investment Corp.(c) | | | 106,332 | | | | 879,366 | |

| Ares Capital Corp.(c) | | | 361,124 | | | | 5,037,680 | |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 7 |

| Resource Credit Income Fund | Consolidated Schedule of Investments |

September 30, 2020

| | | Shares | | | Value | |

| COMMON EQUITY (14.95%) (continued) | | | | | | | | |

| Financials (14.95%) (continued) | | | | | | | | |

| BlackRock Capital Investment Corp.(c) | | | 478,501 | | | $ | 1,167,542 | |

| FS KKR Capital Corp.(c) | | | 150,016 | | | | 2,379,254 | |

| FS KKR Capital Corp. II | | | 195,000 | | | | 2,868,450 | |

| Owl Rock Capital Corp.(c) | | | 5,949 | | | | 71,745 | |

| PennantPark Floating Rate Capital Ltd.(c) | | | 303,163 | | | | 2,558,696 | |

| PennantPark Investment Corp.(c) | | | 250,000 | | | | 797,500 | |

| Solar Capital Ltd.(c) | | | 514,872 | | | | 8,160,721 | |

| Solar Senior Capital Ltd.(c) | | | 178,599 | | | | 2,250,347 | |

| Trinity Capital Inc.(b)(c) | | | 100,000 | | | | 1,274,000 | |

| TriplePoint Venture Growth BDC Corp.(c) | | | 415,109 | | | | 4,582,803 | |

| WhiteHorse Finance, Inc.(c) | | | 524,959 | | | | 5,139,349 | |

| Whiting Petroleum Corp.(c)(e) | | | 39,046 | | | | 675,105 | |

| | | | | | | | 37,842,558 | |

| | | | | | | | | |

| TOTAL COMMON EQUITY | | | | | | | | |

| (Cost $46,188,512) | | | | | | | 37,842,558 | |

| | | Dividend Rate | | | | | | Shares | | | Value | |

| PREFERRED STOCKS (3.02%) | | | | | | | | | | | | | | | |

| Financials (3.02%) | | | | | | | | | | | | | | | |

| Maiden Holdings North America, Ltd.(c) | | | 7.750% | | | | | | | 88,000 | | | | 1,939,520 | |

| Trinity Capital, Inc.(b)(c) | | | 7.000% | | | | | | | 240,000 | | | | 5,700,000 | |

| | | | | | | | | | | | | | | 7,639,520 | |

| | | | | | | | | | | | | | | | |

| TOTAL PREFERRED STOCKS | | | | | | | | | | | | | | | |

| (Cost $8,000,240) | | | | | | | | | | | | | | 7,639,520 | |

| | | | | | | | | | | | | | | | |

| PRIVATE INVESTMENT FUNDS (23.33%) | | | | | | | | | | | | | | | |

| BlackRock Global Credit Opportunities Fund, LP(f)(g) | | | | | | | | | | | | | | 14,576,268 | |

| CVC European Mid-Market Solutions Fund(f)(g) | | | | | | | | | | | | | | 12,807,016 | |

| GSO Credit Alpha Fund II LP(f)(g) | | | | | | | | | | | | | | 6,133,066 | |

| Monroe Capital Private Credit Fund III LP(f)(g) | | | | | | | | | | | | | | 7,132,272 | |

| Tree Line Credit Strategies LP(f)(g) | | | | | | | | | | | | | | 18,391,189 | |

| | | | | | | | | | | | | | | 59,039,811 | |

| | | | | | | | | | | | | | | | |

| TOTAL PRIVATE INVESTMENT FUNDS | | | | | | | | | | | | | | | |

| (Cost $60,763,482) | | | | | | | | | | | | | | 59,039,811 | |

| | | | | | | | | | | | | | | | |

| SHORT TERM INVESTMENT (0.95%) | | | | | | | | | | | | | | | |

| Dreyfus Treasury Cash Management, Institutional Class, 0.01%(h) | | | | | | | | | | 2,403,459 | | | | 2,403,459 | |

| | | | | | | | | | | | | | | | |

| TOTAL SHORT TERM INVESTMENT | | | | | | | | | | | | | | | |

| (Cost $2,403,459) | | | | | | | | | | | | | | 2,403,459 | |

| | | | | | | | | | | | | | | | |

| INVESTMENTS, AT VALUE (98.48%) | | | | | | | | | | | | | | | |

| (Cost $276,133,025) | | | | | | | | | | | | | $ | 249,244,283 | |

| | | | | | | | | | | | | | | | |

| Other Assets In Excess Of Liabilities (1.52%) | | | | | | | | | | | | | | 3,852,817 | |

| | | | | | | | | | | | | | | | |

| NET ASSETS (100.00%) | | | | | | | | | | | | | $ | 253,097,100 | |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund | Consolidated Schedule of Investments |

September 30, 2020

Investment Abbreviations:

LIBOR - London Interbank Offered Rate

Reference Rates:

1M US L - 1 Month LIBOR as of September 30, 2020 was 0.15%

3M US L - 3 Month LIBOR as of September 30, 2020 was 0.23%

| (a) | Variable rate investment. Interest rates reset periodically. Interest rate shown reflects the rate in effect at September 30, 2020. For securities based on a published reference rate and spread, the reference rate and spread are indicated in the description above. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| (b) | Securities exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be sold in the ordinary course of business in transactions exempt from registration, normally to qualified institutional buyers. As of September 30, 2020, the aggregate market value of those securities was $61,076,442, representing 24.13% of net assets. |

| (c) | All or a portion of each of these securities have been segregated as collateral for line of credit. The aggregate market value of those securities was $99,446,161 (see Note 6). |

| (d) | Security in default on interest payments. |

| (e) | Non-income producing security. |

| (f) | Investment is held through CIF Investments LLC, a wholly-owned subsidiary (see Note 1). |

| (g) | Illiquid/restricted security. See chart next page. |

| (h) | Money market fund; interest rate reflects seven-day effective yield on September 30, 2020. |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 9 |

| Resource Credit Income Fund | Consolidated Schedule of Investments |

September 30, 2020

Securities determined to be illiquid/restricted under the procedures approved by the Fund's Board of Trustees are as follows.

| Date(s) of Purchase | | Security | | Cost | | | Value | | | % of Net Assets | |

| 03/31/2018 - 09/30/2020 | | BlackRock Global Credit Opportunities Fund, LP | | $ | 14,923,216 | | | $ | 14,576,268 | | | | 5.76 | % |

| 09/30/2017 - 03/31/2020 | | CVC European Mid-Market Solutions Fund | | | 13,556,610 | | | | 12,807,016 | | | | 5.06 | % |

| 6/30/2018 - 6/30/2020 | | GSO Credit Alpha Fund II LP | | | 6,222,799 | | | | 6,133,066 | | | | 2.42 | % |

| 09/30/2018 - 12/31/2019 | | Monroe Capital Private Credit Fund III LP | | | 7,060,857 | | | | 7,132,272 | | | | 2.82 | % |

| 12/31/2017 - 06/30/2019 | | Tree Line Credit Strategies LP | | | 19,000,000 | | | | 18,391,189 | | | | 7.27 | % |

| | | Total | | $ | 60,763,482 | | | $ | 59,039,811 | | | | 23.33 | % |

Additional information on investments in private investment funds:

| Security | | Value | | | Redemption Frequency | | Redemption Notice (Days) | | | Unfunded

Commitments

as of

September 30, 2020

(See Note 2) | |

| BlackRock Global Credit Opportunities Fund, LP(a) | | $ | 14,576,268 | | | N/A | | | N/A | | | $ | 10,079,776 | |

| CVC European Mid-Market Solutions Fund(b) | | | 12,807,016 | | | N/A | | | N/A | | | | 1,525,516 | |

| GSO Credit Alpha Fund II LP(a) | | | 6,133,066 | | | N/A | | | N/A | | | | 8,777,201 | |

| Monroe Capital Private Credit Fund III LP(b) | | | 7,132,272 | | | N/A | | | N/A | | | | 2,939,143 | |

| Tree Line Credit Strategies LP | | | 18,391,189 | | | Quarterly | | | 90 | | | | N/A | |

| | | | | | | | | | | | | $ | 23,321,636 | |

| (a) | A voluntary withdrawal may be permitted at the General Partner's discretion with the General Partner's consent. |

| (b) | A voluntary withdrawal may be permitted with the General Partner's prior written consent. |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund | Consolidated Statement of Assets and Liabilities |

September 30, 2020

| ASSETS | | |

| Investments, at value (Cost $276,133,025) | | $ | 249,244,283 | |

| Cash | | | 355,263 | |

| Interest and dividends receivable | | | 3,649,434 | |

| Receivable for investments sold | | | 393,889 | |

| Receivable for fund shares sold | | | 39,161 | |

| Prepaid expenses and other assets | | | 27,196 | |

| Total assets | | | 253,709,226 | |

| | | | | |

| LIABILITIES | | | | |

| Interest on line of credit payable | | | 2,111 | |

| Due to adviser | | | 281,524 | |

| Administration fees payable | | | 56,291 | |

| Custody fees payable | | | 11,913 | |

| Compliance services fees payable | | | 16,667 | |

| Distribution fees payable | | | 29,549 | |

| Shareholder servicing fees payable | | | 34,156 | |

| Transfer agency fees payable | | | 26,206 | |

| Accrued expenses and other liabilities | | | 153,709 | |

| Total liabilities | | | 612,126 | |

| NET ASSETS | | $ | 253,097,100 | |

| Commitments and contingencies (Note 2) | | | – | |

| | | | | |

| NET ASSETS CONSISTS OF | | | | |

| Paid-in capital | | $ | 279,493,660 | |

| Total accumulated deficit | | | (26,396,560 | ) |

| NET ASSETS | | $ | 253,097,100 | |

| | | | | |

| Capital Shares: | | | | |

| Class A | | | | |

| Net assets | | $ | 38,829,130 | |

| Shares of beneficial interest outstanding (no par value; unlimited number of shares) | | | 3,983,125 | |

| Net asset value and redemption price per share(a) | | $ | 9.75 | |

| Maximum offering price per share (maximum sales charge of 5.75%) | | $ | 10.34 | |

| Class C | | | | |

| Net assets | | $ | 43,984,206 | |

| Shares of beneficial interest outstanding (no par value; unlimited shares) | | | 4,461,067 | |

| Net asset value, offering and redemption price per share(a) | | $ | 9.86 | |

| Class W | | | | |

| Net assets | | $ | 69,993,270 | |

| Shares of beneficial interest outstanding (no par value; unlimited shares) | | | 7,183,343 | |

| Net asset value, offering and redemption price per share | | $ | 9.74 | |

| Class I | | | | |

| Net assets | | $ | 87,634,115 | |

| Shares of beneficial interest outstanding (no par value; unlimited shares) | | | 8,971,423 | |

| Net asset value, offering and redemption price per share | | $ | 9.77 | |

| Class L | | | | |

| Net assets | | $ | 12,656,379 | |

| Shares of beneficial interest outstanding (no par value; unlimited shares) | | | 1,298,691 | |

| Net asset value and redemption price per share | | $ | 9.75 | |

| Maximum offering price per share (maximum sales charge of 4.25%) | | $ | 10.18 | |

| (a) | Redemption price varies based on length of time held (Note 5). |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 11 |

| Resource Credit Income Fund | Consolidated Statement of Operations |

For the Year Ended September 30, 2020

| INVESTMENT INCOME | | |

| Interest | | $ | 15,492,269 | |

| Dividends | | | 9,622,384 | |

| Total investment income | | | 25,114,653 | |

| EXPENSES | | | | |

| Investment advisory fees (Note 3) | | | 4,828,992 | |

| Administrative fees (Note 3) | | | 305,038 | |

| Distribution fees (Note 3): | | | | |

| Class C | | | 318,855 | |

| Class L | | | 31,966 | |

| Shareholder servicing fees (Note 3): | | | | |

| Class A | | | 96,219 | |

| Class C | | | 106,886 | |

| Class W | | | 197,386 | |

| Class L | | | 31,966 | |

| Interest expense (Note 6) | | | 165,652 | |

| Interest and amortization/accretion on securities sold short | | | 87,154 | |

| Transfer agent fees (Note 3) | | | 319,123 | |

| Professional fees | | | 147,944 | |

| Printing expense | | | 171,811 | |

| Registration fees | | | 88,112 | |

| Custody fees | | | 41,038 | |

| Trustee fees and expenses (Note 3) | | | 63,900 | |

| Compliance services fees (Note 3) | | | 200,000 | |

| Networking Fees: | | | | |

| Class A | | | 12,806 | |

| Class C | | | 12,459 | |

| Class W | | | 8,061 | |

| Class I | | | 19,909 | |

| Class L | | | 5,588 | |

| Other expenses | | | 97,366 | |

| Total expenses | | | 7,358,231 | |

| Fees waived by Adviser (Note 3) | | | (223,829 | ) |

| Recoupment of previously waived fees (Note 3) | | | 11,918 | |

| Total net expenses | | | 7,146,320 | |

| NET INVESTMENT INCOME | | | 17,968,333 | |

| Net realized loss on investments | | | (3,391,875 | ) |

| Gains increase from payments by affiliates (Note 3) | | | 335,295 | |

| Net realized loss on securities sold short | | | (434,122 | ) |

| Long-term capital gains distributions from other investment companies | | | 640,367 | |

| Net change in unrealized depreciation on investments | | | (22,488,468 | ) |

| Net change in unrealized appreciation on securities sold short | | | 451,779 | |

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | | | (24,887,024 | ) |

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (6,918,691 | ) |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund | Consolidated Statements of Changes in Net Assets |

| | | For the

Year Ended

September 30,

2020 | | For the

Year Ended

September 30,

2019 |

| OPERATIONS | | | | | | | | |

| Net investment income | | $ | 17,968,333 | | | $ | 14,433,882 | |

| Net realized loss on investments | | | (3,391,875 | ) | | | (879,604 | ) |

| Gains increase from payments by affiliates (Note 3) | | | 335,295 | | | | – | |

| Net realized loss on securities sold short | | | (434,122 | ) | | | (14,551 | ) |

| Long-term capital gains distributions from other investment companies | | | 640,367 | | | | – | |

| Net realized loss on foreign currency transactions | | | – | | | | (21,214 | ) |

| Net change in unrealized depreciation on investments | | | (22,488,468 | ) | | | (4,149,368 | ) |

| Net change in unrealized appreciation on securities sold short | | | 451,779 | | | | (451,779 | ) |

| Net increase/(decrease) in net assets resulting from operations | | | (6,918,691 | ) | | | 8,917,366 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Total Distributable Earnings | | | | | | | | |

| Class A | | | (2,742,822 | ) | | | (1,746,235 | ) |

| Class C | | | (2,783,170 | ) | | | (1,583,627 | ) |

| Class W | | | (5,637,361 | ) | | | (4,232,879 | ) |

| Class I | | | (6,545,582 | ) | | | (3,098,932 | ) |

| Class L | | | (877,305 | ) | | | (583,569 | ) |

| From return of capital: | | | | | | | | |

| Class A | | | (449,557 | ) | | | (504,734 | ) |

| Class C | | | (456,521 | ) | | | (464,754 | ) |

| Class W | | | (890,742 | ) | | | (1,164,640 | ) |

| Class I | | | (1,063,106 | ) | | | (1,001,812 | ) |

| Class L | | | (142,599 | ) | | | (173,643 | ) |

| Total distributions to shareholders | | | (21,588,765 | ) | | | (14,554,825 | ) |

| | | | | | | | | |

| CAPTIAL SHARE TRANSACTIONS | | | | | | | | |

| Class A | | | | | | | | |

| Proceeds from sales of shares | | | 5,840,049 | | | | 11,882,666 | |

| Distributions reinvested | | | 1,781,074 | | | | 1,274,924 | |

| Cost of shares redeemed | | | (3,245,836 | ) | | | (2,823,417 | ) |

| Net transferred in(out) | | | (414,003 | ) | | | (256,215 | ) |

| Net increase from share transactions | | | 3,961,284 | | | | 10,077,958 | |

| Class C | | | | | | | | |

| Proceeds from sales of shares | | | 8,319,399 | | | | 16,475,462 | |

| Distributions reinvested | | | 1,859,781 | | | | 1,214,219 | |

| Cost of shares redeemed | | | (2,869,823 | ) | | | (1,876,193 | ) |

| Net transferred in(out) | | | (347,881 | ) | | | (104,502 | ) |

| Net increase from share transactions | | | 6,961,476 | | | | 15,708,986 | |

| Class W | | | | | | | | |

| Proceeds from sales of shares | | | 13,839,560 | | | | 51,120,662 | |

| Distributions reinvested | | | 2,285,342 | | | | 2,392,701 | |

| Cost of shares redeemed | | | (18,542,424 | ) | | | (19,680,340 | ) |

| Net transferred in(out) | | | (4,584,446 | ) | | | (21,160,923 | ) |

| Net increase/(decrease) from share transactions | | | (7,001,968 | ) | | | 12,672,100 | |

| Class I | | | | | | | | |

| Proceeds from sales of shares | | | 21,748,932 | | | | 41,858,117 | |

| Distributions reinvested | | | 4,502,319 | | | | 2,246,428 | |

| Cost of shares redeemed | | | (21,289,740 | ) | | | (6,383,090 | ) |

| Net transferred in(out) | | | 5,346,330 | | | | 21,555,338 | |

| Net increase from share transactions | | | 10,307,841 | | | | 59,276,793 | |

| Class L | | | | | | | | |

| Proceeds from sales of shares | | | 348,597 | | | | 4,075,265 | |

| Distributions reinvested | | | 577,980 | | | | 421,315 | |

| Cost of shares redeemed | | | (905,353 | ) | | | (284,303 | ) |

| Net transferred in(out) | | | – | | | | (33,698 | ) |

| Net increase from share transactions | | | 21,224 | | | | 4,178,579 | |

| Net increase/(decrease) from share transactions | | | (14,257,599 | ) | | | 96,276,957 | |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 13 |

| Resource Credit Income Fund | Consolidated Statements of Changes in Net Assets (continued) |

| | | For the

Year Ended

September 30,

2020 | | For the

Year Ended

September 30,

2019 |

| NET ASSETS | | | | | | | | |

| Beginning of year | | | 267,354,699 | | | | 171,077,742 | |

| End of year | | $ | 253,097,100 | | | $ | 267,354,699 | |

| | | | | | | | | |

| OTHER INFORMATION | | | | | | | | |

| Capital Shares Transactions | | | | | | | | |

| Class A | | | | | | | | |

| Issued | | | 568,509 | | | | 1,087,050 | |

| Distributions reinvested | | | 181,466 | | | | 118,824 | |

| Redeemed | | | (328,793 | ) | | | (258,196 | ) |

| Net Transferred in(out) | | | (40,820 | ) | | | (23,363 | ) |

| Net increase in shares | | | 380,362 | | | | 924,315 | |

| | | | | | | | | |

| Class C | | | | | | | | |

| Issued | | | 783,402 | | | | 1,492,724 | |

| Distributions reinvested | | | 187,748 | | | | 111,935 | |

| Redeemed | | | (281,781 | ) | | | (170,167 | ) |

| Net Transferred in(out) | | | (35,195 | ) | | | (9,507 | ) |

| Net increase in shares | | | 654,174 | | | | 1,424,985 | |

| | | | | | | | | |

| Class W | | | | | | | | |

| Issued | | | 1,366,034 | | | | 4,696,724 | |

| Distributions reinvested | | | 232,125 | | | | 223,882 | |

| Redeemed | | | (1,873,525 | ) | | | (1,821,984 | ) |

| Net Transferred in(out) | | | (475,259 | ) | | | (1,952,992 | ) |

| Net increase(decrease) in shares | | | (750,625 | ) | | | 1,145,630 | |

| | | | | | | | | |

| Class I | | | | | | | | |

| Issued | | | 2,049,788 | | | | 3,821,467 | |

| Distributions reinvested | | | 458,248 | | | | 207,906 | |

| Redeemed | | | (2,151,489 | ) | | | (581,417 | ) |

| Net Transferred in(out) | | | 550,137 | | | | 1,983,560 | |

| Net increase in shares | | | 906,684 | | | | 5,431,516 | |

| | | | | | | | | |

| Class L | | | | | | | | |

| Issued | | | 32,215 | | | | 373,660 | |

| Distributions reinvested | | | 58,939 | | | | 39,218 | |

| Redeemed | | | (86,798 | ) | | | (26,185 | ) |

| Net Transferred in(out) | | | – | | | | (3,069 | ) |

| Net increase in shares | | | 4,356 | | | | 383,624 | |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund – Class A | Financial Highlights |

For a Share Outstanding Throughout the Years Presented

| | | Year Ended

September 30,

2020 | | Year Ended

September 30,

2019 | | Year Ended

September 30,

2018 | | Year Ended

September 30,

2017 | | Year Ended

September 30,

2016 |

| NET ASSET VALUE, BEGINNING OF YEAR | | $ | 10.80 | | | $ | 11.09 | | | $ | 11.13 | | | $ | 10.26 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.69 | | | | 0.73 | | | | 0.79 | | | | 0.57 | | | | 0.43 | |

| Net realized and unrealized gain/(loss) on investments | | | (0.92 | ) | | | (0.32 | ) | | | (0.13 | ) | | | 1.02 | | | | 0.18 | |

| Total income/(loss) from investment operations | | | (0.23 | ) | | | 0.41 | | | | 0.66 | | | | 1.59 | | | | 0.61 | |

| | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.70 | ) | | | (0.55 | ) | | | (0.57 | ) | | | (0.47 | ) | | | (0.27 | ) |

| From net realized gain on investments | | | – | | | | – | | | | (0.04 | ) | | | (0.16 | ) | | | – | |

| From return of capital | | | (0.12 | ) | | | (0.15 | ) | | | (0.09 | ) | | | (0.09 | ) | | | (0.08 | ) |

| Total distributions | | | (0.82 | ) | | | (0.70 | ) | | | (0.70 | ) | | | (0.72 | ) | | | (0.35 | ) |

| INCREASE/(DECREASE) IN NET ASSET VALUE | | | (1.05 | ) | | | (0.29 | ) | | | (0.04 | ) | | | 0.87 | | | | 0.26 | |

| NET ASSET VALUE, END OF YEAR | | $ | 9.75 | | | $ | 10.80 | | | $ | 11.09 | | | $ | 11.13 | | | $ | 10.26 | |

| | | | | | | | | | | | | | | | | | | | | |

| TOTAL RETURN(b) | | | (1.88 | )%(c)(d) | | | 3.91 | % | | | 6.09 | % | | | 15.79 | %(c) | | | 6.22 | %(c) |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000s) | | $ | 38,829 | | | $ | 38,901 | | | $ | 29,712 | | | $ | 16,049 | | | $ | 4,043 | |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS(e) | | | | | | | | | | | | | | | | | | | | |

| Including interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.78 | % | | | 2.79 | % | | | 2.93 | % | | | 4.90 | % | | | 31.46 | % |

| Expenses, net of fees waived/expenses reimbursed by investment adviser | | | 2.68 | % | | | 2.67 | % | | | 2.61 | % | | | 2.59 | % | | | 2.59 | % |

| Excluding interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.69 | % | | | 2.71 | % | | | 2.91 | % | | | 4.90 | % | | | 34.54 | % |

| Expenses, net of fees waived/expenses reimbursed by investment adviser | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % |

| Net investment income | | | 6.93 | % | | | 6.68 | % | | | 7.06 | % | | | 5.20 | % | | | 4.43 | % |

| | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE | | | 39 | % | | | 29 | % | | | 43 | % | | | 39 | % | | | 22 | % |

| | | | | | | | | | | | | | | | | | | | | |

| BORROWINGS AT END OF YEAR | | | | | | | | | | | | | | | | | | | | |

| Aggregate amount outstanding (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | | | $ | 5 | |

| Asset coverage per $1,000 (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | | | $ | 1,032,060 | |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 15 |

| Resource Credit Income Fund – Class A | Financial Highlights |

For a Share Outstanding Throughout the Years Presented

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Total returns shown are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distribution, if any. Had the Adviser not absorbed a portion of Fund expenses, total returns would have been lower. Returns shown exclude applicable sales charges. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. |

| (d) | 0.10% of the Fund’s total return consists of a reimbursement by the Adviser caused by an error in inadvertently effecting a corporate action. Excluding this item, total return would have been (1.98)%. |

| (e) | Ratios do not include expenses of underlying investment companies and private investment funds in which the Fund invests. |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund – Class C | Financial Highlights |

For a Share Outstanding Throughout the Years Presented

| | | | | | | | | | | | | | | | |

| | | Year Ended

September 30, 2020 | | | Year Ended

September 30, 2019 | | | Year Ended

September 30, 2018 | | | Year Ended

September 30, 2017 | | | Year Ended

September 30, 2016 | |

| NET ASSET VALUE, BEGINNING OF YEAR | | $ | 10.92 | | | $ | 11.22 | | | $ | 11.25 | | | $ | 10.36 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.62 | | | | 0.66 | | | | 0.72 | | | | 0.50 | | | | 0.59 | |

| Net realized and unrealized gain/(loss) on investments | | | (0.92 | ) | | | (0.34 | ) | | | (0.13 | ) | | | 1.03 | | | | 0.08 | |

| Total income/(loss) from investment operations | | | (0.30 | ) | | | 0.32 | | | | 0.59 | | | | 1.53 | | | | 0.67 | |

| | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.66 | ) | | | (0.48 | ) | | | (0.50 | ) | | | (0.40 | ) | | | (0.24 | ) |

| From net realized gain on investments | | | – | | | | – | | | | (0.04 | ) | | | (0.16 | ) | | | – | |

| From return of capital | | | (0.10 | ) | | | (0.14 | ) | | | (0.08 | ) | | | (0.08 | ) | | | (0.07 | ) |

| Total distributions | | | (0.76 | ) | | | (0.62 | ) | | | (0.62 | ) | | | (0.64 | ) | | | (0.31 | ) |

| INCREASE/(DECREASE) IN NET ASSET VALUE | | | (1.06 | ) | | | (0.30 | ) | | | (0.03 | ) | | | 0.89 | | | | 0.36 | |

| NET ASSET VALUE, END OF YEAR | | $ | 9.86 | | | $ | 10.92 | | | $ | 11.22 | | | $ | 11.25 | | | $ | 10.36 | |

| | | | | | | | | | | | | | | | | | | | | |

| TOTAL RETURN(b) | | | (2.61 | )%(c)(d) | | | 3.05 | % | | | 5.39 | % | | | 15.03 | %(c) | | | 6.85 | %(c) |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000s) | | $ | 43,984 | | | $ | 41,575 | | | $ | 26,720 | | | $ | 8,965 | | | $ | 434 | |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS(e) | | | | | | | | | | | | | | | | | | |

| Including interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 3.53 | % | | | 3.55 | % | | | 3.75 | % | | | 5.28 | % | | | 18.42 | % |

| Expenses, net of fees waived/expenses reimbursed by investment adviser | | | 3.43 | % | | | 3.42 | % | | | 3.37 | % | | | 3.34 | % | | | 3.34 | % |

| Excluding interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 3.44 | % | | | 3.47 | % | | | 3.72 | % | | | 5.28 | % | | | 18.42 | % |

| Expenses, net of fees waived/expenses reimbursed by investment adviser | | | 3.34 | % | | | 3.34 | % | | | 3.34 | % | | | 3.34 | % | | | 3.34 | % |

| Net investment income | | | 6.19 | % | | | 5.95 | % | | | 6.38 | % | | | 4.46 | % | | | 5.85 | % |

| | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE | | | 39 | % | | | 29 | % | | | 43 | % | | | 39 | % | | | 22 | % |

| | | | | | | | | | | | | | | | | | | | | |

| BORROWINGS AT END OF YEAR | | | | | | | | | | | | | | | | | | | | |

| Aggregate amount outstanding (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | | | $ | 5 | |

| Asset coverage per $1,000 (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | | | $ | 1,032,060 | |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 17 |

| Resource Credit Income Fund – Class C | Financial Highlights |

For a Share Outstanding Throughout the Years Presented

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Total returns shown are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distribution, if any. Had the Adviser not absorbed a portion of Fund expenses, total returns would have been lower. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. |

| (d) | 0.10% of the Fund’s total return consists of a reimbursement by the Adviser caused by an error in inadvertently effecting a corporate action. Excluding this item, total return would have been (2.71)%. |

| (e) | Ratios do not include expenses of underlying investment companies and private investment funds in which the Fund invests. |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund – Class W | Financial Highlights |

For a Share Outstanding Throughout the Years Presented

| | | | | | | | | | | | | | | | |

| | | Year Ended

September 30, 2020 | | | Year Ended

September 30, 2019 | | | Year Ended

September 30, 2018 | | | Year Ended September 30,

2017 | | | Year Ended

September 30,

2016 | |

| NET ASSET VALUE, BEGINNING OF YEAR | | $ | 10.79 | | | $ | 11.09 | | | $ | 11.12 | | | $ | 10.24 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.69 | | | | 0.73 | | | | 0.79 | | | | 0.58 | | | | 0.63 | |

| Net realized and unrealized gain/(loss) on investments | | | (0.92 | ) | | | (0.33 | ) | | | (0.12 | ) | | | 1.01 | | | | (0.07 | )(b) |

| Total income/(loss) from investment operations | | | (0.23 | ) | | | 0.40 | | | | 0.67 | | | | 1.59 | | | | 0.56 | |

| | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.70 | ) | | | (0.55 | ) | | | (0.57 | ) | | | (0.46 | ) | | | (0.25 | ) |

| From net realized gain on investments | | | – | | | | – | | | | (0.04 | ) | | | (0.16 | ) | | | – | |

| From return of capital | | | (0.12 | ) | | | (0.15 | ) | | | (0.09 | ) | | | (0.09 | ) | | | (0.07 | ) |

| Total distributions | | | (0.82 | ) | | | (0.70 | ) | | | (0.70 | ) | | | (0.71 | ) | | | (0.32 | ) |

| INCREASE/(DECREASE) IN NET ASSET VALUE | | | (1.05 | ) | | | (0.30 | ) | | | (0.03 | ) | | | 0.88 | | | | 0.24 | |

| NET ASSET VALUE, END OF YEAR | | $ | 9.74 | | | $ | 10.79 | | | $ | 11.09 | | | $ | 11.12 | | | $ | 10.24 | |

| | | | | | | | | | | | | | | | | | | | | |

| TOTAL RETURN(c) | | | (1.89 | )%(d)(e) | | | 3.81 | % | | | 6.19 | % | | | 15.77 | %(d) | | | 5.74 | %(d) |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000s) | | $ | 69,993 | | | $ | 85,642 | | | $ | 75,275 | | | $ | 26,757 | | | $ | 494 | |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS(f) | | | | | | | | | | | | | | | | | | |

| Including interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.75 | % | | | 2.79 | % | | | 2.98 | % | | | 4.35 | % | | | 17.52 | % |

| Expenses, net of fees waived/expenses reimbursed by investment adviser | | | 2.68 | % | | | 2.67 | % | | | 2.62 | % | | | 2.61 | %(g) | | | 3.09 | % |

| Excluding interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.66 | % | | | 2.71 | % | | | 2.95 | % | | | 4.35 | % | | | 17.52 | % |

| Expenses, net of fees waived/expenses reimbursed by investment adviser | | | 2.59 | % | | | 2.59 | % | | | 2.59 | % | | | 2.61 | %(g) | | | 3.09 | % |

| Net investment income | | | 6.92 | % | | | 6.68 | % | | | 7.10 | % | | | 5.22 | %(g) | | | 6.24 | % |

| | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE | | | 39 | % | | | 29 | % | | | 43 | % | | | 39 | % | | | 22 | % |

| | | | | | | | | | | | | | | | | | | | | |

| BORROWINGS AT END OF YEAR | | | | | | | | | | | | | | | | | | | | |

| Aggregate amount outstanding (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | | | $ | 5 | |

| Asset coverage per $1,000 (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | | | $ | 1,032,060 | |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 19 |

| Resource Credit Income Fund – Class W | Financial Highlights |

| | For a Share Outstanding Throughout the Years Presented |

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Realized and unrealized losses per share do not correlate to the aggregate of the net realized and unrealized gains on the Statement of Operations for the year ended September 30, 2016, primarily due to the timing of sales and repurchases of the Fund's shares in relation to fluctuating market values for the Fund's portfolio. |

| (c) | Total returns shown are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distribution, if any. Had the Adviser not absorbed a portion of Fund expenses, total returns would have been lower. |

| (d) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. |

| (e) | 0.10% of the Fund’s total return consists of a reimbursement by the Adviser caused by an error in inadvertently effecting a corporate action. Excluding this item, total return would have been (1.99)%. |

| (f) | Ratios do not include expenses of underlying investment companies and private investment funds in which the Fund invests. |

| (g) | Effective January 5, 2017, the annual expense limitation changed from 3.09% to 2.59%. |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund – Class I | Financial Highlights |

For a Share Outstanding Throughout the Years Presented

| | | | | | | | | | | | | | | | |

| | | Year Ended

September 30,

2020 | | | Year Ended

September 30,

2019 | | | Year Ended

September 30,

2018 | | | Year Ended

September 30,

2017 | | | Year Ended

September 30,

2016 | |

| NET ASSET VALUE, BEGINNING OF YEAR | | $ | 10.82 | | | $ | 11.12 | | | $ | 11.15 | | | $ | 10.28 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.72 | | | | 0.77 | | | | 0.84 | | | | 0.63 | | | | 0.35 | |

| Net realized and unrealized gain/(loss) on investments | | | (0.92 | ) | | | (0.34 | ) | | | (0.14 | ) | | | 0.99 | | | | 0.28 | |

| Total income/(loss) from investment operations | | | (0.20 | ) | | | 0.43 | | | | 0.70 | | | | 1.62 | | | | 0.63 | |

| | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.73 | ) | | | (0.57 | ) | | | (0.60 | ) | | | (0.50 | ) | | | (0.27 | ) |

| From net realized gain on investments | | | – | | | | – | | | | (0.04 | ) | | | (0.16 | ) | | | – | |

| From return of capital | | | (0.12 | ) | | | (0.16 | ) | | | (0.09 | ) | | | (0.09 | ) | | | (0.08 | ) |

| Total distributions | | | (0.85 | ) | | | (0.73 | ) | | | (0.73 | ) | | | (0.75 | ) | | | (0.35 | ) |

| INCREASE/(DECREASE) IN NET ASSET VALUE | | | (1.05 | ) | | | (0.30 | ) | | | (0.03 | ) | | | 0.87 | | | | 0.28 | |

| NET ASSET VALUE, END OF YEAR | | $ | 9.77 | | | $ | 10.82 | | | $ | 11.12 | | | $ | 11.15 | | | $ | 10.28 | |

| | | | | | | | | | | | | | | | | | | | | |

| TOTAL RETURN(b) | | | (1.61 | )%(c)(d) | | | 4.08 | % | | | 6.46 | % | | | 16.07 | %(c) | | | 6.42 | %(c) |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000s) | | $ | 87,634 | | | $ | 87,265 | | | $ | 29,273 | | | $ | 2,982 | | | $ | 213 | |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS(e) | | | | | | | | | | | | | | | | | | |

| Including interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.52 | % | | | 2.54 | % | | | 2.78 | % | | | 4.45 | % | | | 72.33 | % |

| Expenses, net of fees waived/expenses reimbursed by investment adviser | | | 2.43 | % | | | 2.42 | % | | | 2.37 | % | | | 2.34 | % | | | 2.34 | % |

| Excluding interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.43 | % | | | 2.46 | % | | | 2.75 | % | | | 4.45 | % | | | 72.33 | % |

| Expenses, net of fees waived/expenses reimbursed by investment adviser | | | 2.34 | % | | | 2.34 | % | | | 2.34 | % | | | 2.34 | % | | | 2.34 | % |

| Net investment income | | | 7.20 | % | | | 7.00 | % | | | 7.51 | % | | | 5.71 | % | | | 3.53 | % |

| | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE | | | 39 | % | | | 29 | % | | | 43 | % | | | 39 | % | | | 22 | % |

| | | | | | | | | | | | | | | | | | | | | |

| BORROWINGS AT END OF YEAR | | | | | | | | | | | | | | | | | | | | |

| Aggregate amount outstanding (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | | | $ | 5 | |

| Asset coverage per $1,000 (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | | | $ | 1,032,060 | |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 21 |

| Resource Credit Income Fund – Class I | Financial Highlights |

For a Share Outstanding Throughout the Years Presented

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Total returns shown are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distribution, if any. Had the Adviser not absorbed a portion of Fund expenses, total returns would have been lower. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. |

| (d) | 0.10% of the Fund’s total return consists of a reimbursement by the Adviser caused by an error in inadvertently effecting a corporate action. Excluding this item, total return would have been (1.71)%. |

| (e) | Ratios do not include expenses of underlying investment companies and private investment funds in which the Fund invests. |

See Notes to Consolidated Financial Statements.

| Resource Credit Income Fund – Class L | Financial Highlights |

For a Share Outstanding Throughout the Years or Period Presented

| | | | | | | | | | | | | |

| | | Year Ended September 30,

2020 | | | Year Ended September 30,

2019 | | | Year Ended September 30,

2018 | | | For the

Period Ended

September 30,

2017(a) | |

| NET ASSET VALUE, BEGINNING OF YEAR OR PERIOD | | $ | 10.79 | | | $ | 11.09 | | | $ | 11.12 | | | $ | 11.19 | |

| | | | | | | | | | | | | | | | | |

| INCOME/(LOSS) FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | | | | |

| Net investment income(b) | | | 0.67 | | | | 0.70 | | | | 0.77 | | | | 0.13 | |

| Net realized and unrealized loss on investments | | | (0.91 | ) | | | (0.33 | ) | | | (0.13 | ) | | | (0.03 | )(c) |

| Total income/(loss) from investment operations | | | (0.24 | ) | | | 0.37 | | | | 0.64 | | | | 0.10 | |

| | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.69 | ) | | | (0.52 | ) | | | (0.55 | ) | | | (0.10 | ) |

| From net realized gain on investments | | | – | | | | – | | | | (0.04 | ) | | | (0.04 | ) |

| From return of capital | | | (0.11 | ) | | | (0.15 | ) | | | (0.08 | ) | | | (0.03 | ) |

| Total distributions | | | (0.80 | ) | | | (0.67 | ) | | | (0.67 | ) | | | (0.17 | ) |

| INCREASE/(DECREASE) IN NET ASSET VALUE | | | (1.04 | ) | | | (0.30 | ) | | | (0.03 | ) | | | (0.07 | ) |

| NET ASSET VALUE, END OF YEAR OR PERIOD | | $ | 9.75 | | | $ | 10.79 | | | $ | 11.09 | | | $ | 11.12 | |

| | | | | | | | | | | | | | | | | |

| TOTAL RETURN(d) | | | (2.04 | )%(e)(f) | | | 3.55 | %(e) | | | 5.92 | % | | | 0.88 | %(i) |

| | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA | | | | | | | | | | | | | | | | |

| Net assets, end of year or period (in 000s) | | $ | 12,656 | | | $ | 13,972 | | | $ | 10,098 | | | $ | 2,445 | |

| | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS(g) | | | | | | | | | | | | | | | | |

| Including interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 3.04 | % | | | 3.06 | % | | | 3.24 | % | | | 4.39 | %(h) |

| Expenses, net of fees waived/expenses reimbursed by investment advisor | | | 2.93 | % | | | 2.92 | % | | | 2.87 | % | | | 2.84 | %(h) |

| Excluding interest expense and interest amortization/accretion on securities sold short: | | | | | | | | | | | | | | | | |

| Expenses, gross | | | 2.95 | % | | | 2.98 | % | | | 3.21 | % | | | 4.39 | %(h) |

| Expenses, net of fees waived/expenses reimbursed by investment advisor | | | 2.84 | % | | | 2.84 | % | | | 2.84 | % | | | 2.84 | %(h) |

| Net investment income | | | 6.66 | % | | | 6.42 | % | | | 6.92 | % | | | 6.67 | %(h) |

| | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE | | | 39 | % | | | 29 | % | | | 43 | % | | | 39 | %(i)(j) |

| | | | | | | | | | | | | | | | | |

| BORROWINGS AT END OF YEAR OR PERIOD | | | | | | | | | | | | | | | | |

| Aggregate amount outstanding (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | |

| Asset coverage per $1,000 (000s) | | $ | – | | | $ | – | | | $ | – | | | $ | – | |

| (a) | The Fund's Class L commenced operations on July 28, 2017. |

| (b) | Per share numbers have been calculated using the average shares method. |

| (c) | Realized and unrealized losses per share do not correlate to the aggregate of the net realized and unrealized gains on the Statement of Operations for the year ended September 30, 2017, primarily due to the timing of sales and repurchases of the Fund's shares in relation to fluctuating market values for the Fund's portfolio. |

| (d) | Total returns shown are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distribution, if any. Had the Adviser not absorbed a portion of Fund expenses, total returns would have been lower. |

| (e) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and, as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from net asset values and returns for shareholder transactions. |

| (f) | 0.10% of the Fund’s total return consists of a reimbursement by the Adviser caused by an error in inadvertently effecting a corporate action. Excluding this item, total return would have been (2.14)%. |

| (g) | Ratios do not include expenses of underlying investment companies and private investment funds in which the Fund invests. |

| (j) | Portfolio turnover rate is calculated at the Fund level and represents the year ended September 30, 2017. |

See Notes to Consolidated Financial Statements.

| Annual Report | September 30, 2020 | 23 |

| Resource Credit Income Fund | Notes to Consolidated Financial Statements |

September 30, 2020

1. ORGANIZATION

Resource Credit Income Fund (the “Fund”) was organized as a Delaware statutory trust on December 11, 2014 and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a closed-end management investment company that operates as an interval fund with a continuous offering of its shares. During the fiscal year ended September 30, 2020, Resource Alternative Advisor, LLC (the “Adviser”) served as the Fund’s investment adviser. The Fund’s investment objectives are to produce current income and to achieve capital preservation with moderate volatility and low to moderate correlation to the broader equity markets. Effective December 5, 2019, the Fund is diversified and pursues its investment objectives by investing, under normal circumstances, at least 80% of its assets (defined as net assets plus the amount of any borrowing for investment purposes) in fixed-income and fixed-income related securities.

On February 3, 2020, the Fund formed a wholly-owned subsidiary, CIF Investments LLC, a Delaware corporation.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies followed by the Fund in preparation of its consolidated financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”). These consolidated financial statements reflect adjustments that in the opinion of the Fund are necessary for the fair presentation of the financial position and results of operations as of and for the periods presented herein. The Fund is considered an investment company for financial reporting purposes under U.S. GAAP and therefore applies the accounting and reporting guidance applicable to investment companies. The preparation of the consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the year. Actual results could differ from those estimates, and such difference could be material. In accordance with U.S. GAAP guidance on consolidation, the Fund will generally not consolidate its investment in a portfolio company other than an investment company subsidiary or a controlled operating company whose business consists of providing services to the Fund. Accordingly, the Fund consolidated the accounts of the Fund’s wholly-owned subsidiary, CIF Investments LLC, in its consolidated financial statements. All significant intercompany balances and transactions have been eliminated in consolidation. All references made to the “Fund” herein include Resource Credit Income Fund and its consolidated subsidiary, except as stated otherwise.

Securities Transactions and Investment Income – Investment transactions are recorded on the trade date. Realized gains or losses on investments are calculated using the specific identification method for both financial statement and federal income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Premiums on securities are accreted to the earliest call date and purchase discounts are amortized over the life of the respective securities using the effective interest method.