Exhibit (c)(14) Discussion Materials May 6, 2024 HIGHLY CONFIDENTIAL

Historical Trading Performance Share Price Performance Indexed Share Price Performance Over Last Twelve Months • Prior to the announcement % of Indiana’s take private bid, Arizona had 115 underperformed its regulated utility peers over the last twelve months March 7, 2024: Arizona announces receipt of take-private proposal from Indiana 100 (3.0%) (4.3%) (9.7%) 85 70 55 May-23 Jun-23 Jul-23 Aug-23 Sep-23 Oct-23 Nov-23 Dec-23 Jan-24 Feb-24 Mar-24 Apr-24 May-24 (1) (2) Arizona Arizona Peers UTY Source: Capital IQ as of May 1, 2024 Notes: 1. Represents the simple median of peers including ED, ES, EXC, FE and PPL 2. Represent the UTY index’s constituents HIGHLY CONFIDENTIAL 2

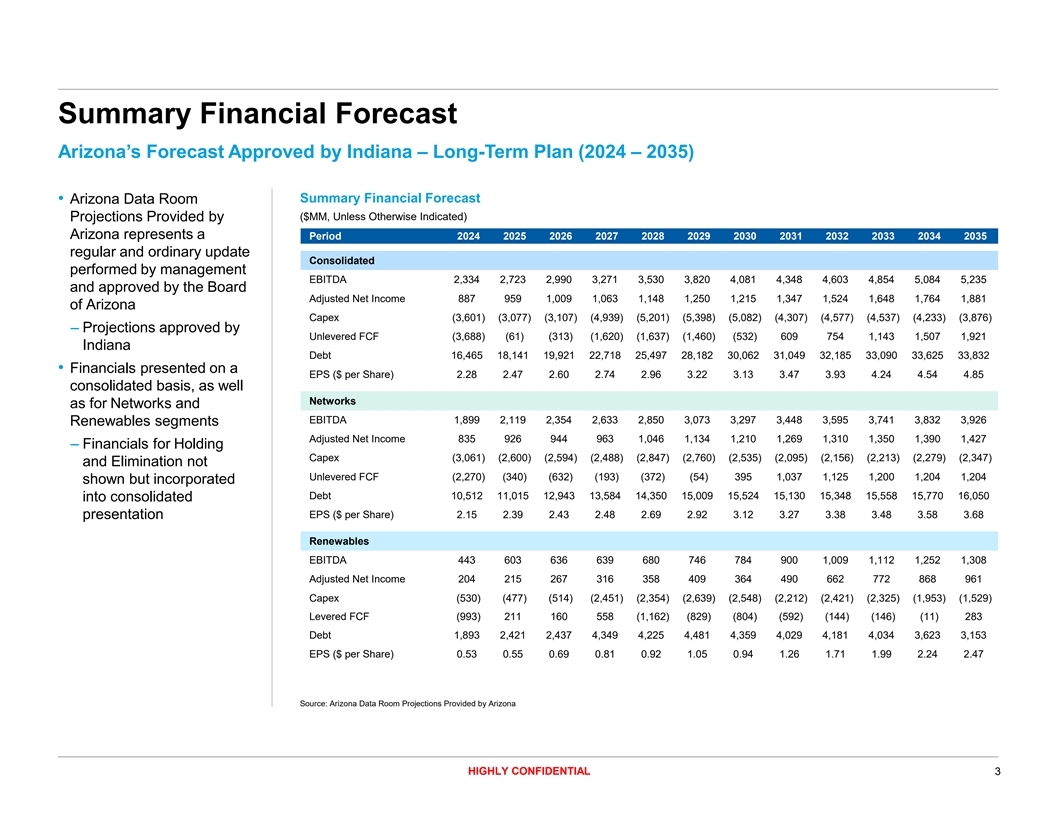

Summary Financial Forecast Arizona’s Forecast Approved by Indiana – Long-Term Plan (2024 – 2035) Summary Financial Forecast • Arizona Data Room ($MM, Unless Otherwise Indicated) Projections Provided by Arizona represents a Period 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 regular and ordinary update Consolidated performed by management EBITDA 2,334 2,723 2,990 3,271 3,530 3,820 4,081 4,348 4,603 4,854 5,084 5,235 and approved by the Board Adjusted Net Income 887 959 1,009 1,063 1,148 1,250 1,215 1,347 1,524 1,648 1,764 1,881 of Arizona Capex (3,601) (3,077) (3,107) (4,939) (5,201) (5,398) (5,082) (4,307) (4,577) (4,537) (4,233) (3,876) – Projections approved by Unlevered FCF (3,688) (61) (313) (1,620) (1,637) (1,460) (532) 609 754 1,143 1,507 1,921 Indiana Debt 16,465 18,141 19,921 22,718 25,497 28,182 30,062 31,049 32,185 33,090 33,625 33,832 • Financials presented on a EPS ($ per Share) 2.28 2.47 2.60 2.74 2.96 3.22 3.13 3.47 3.93 4.24 4.54 4.85 consolidated basis, as well Networks as for Networks and EBITDA 1,899 2,119 2,354 2,633 2,850 3,073 3,297 3,448 3,595 3,741 3,832 3,926 Renewables segments Adjusted Net Income 835 926 944 963 1,046 1,134 1,210 1,269 1,310 1,350 1,390 1,427 – Financials for Holding Capex (3,061) (2,600) (2,594) (2,488) (2,847) (2,760) (2,535) (2,095) (2,156) (2,213) (2,279) (2,347) and Elimination not Unlevered FCF (2,270) (340) (632) (193) (372) (54) 395 1,037 1,125 1,200 1,204 1,204 shown but incorporated Debt 10,512 11,015 12,943 13,584 14,350 15,009 15,524 15,130 15,348 15,558 15,770 16,050 into consolidated presentation EPS ($ per Share) 2.15 2.39 2.43 2.48 2.69 2.92 3.12 3.27 3.38 3.48 3.58 3.68 Renewables EBITDA 443 603 636 639 680 746 784 900 1,009 1,112 1,252 1,308 Adjusted Net Income 204 215 267 316 358 409 364 490 662 772 868 961 Capex (530) (477) (514) (2,451) (2,354) (2,639) (2,548) (2,212) (2,421) (2,325) (1,953) (1,529) Levered FCF (993) 211 160 558 (1,162) (829) (804) (592) (144) (146) (11) 283 Debt 1,893 2,421 2,437 4,349 4,225 4,481 4,359 4,029 4,181 4,034 3,623 3,153 EPS ($ per Share) 0.53 0.55 0.69 0.81 0.92 1.05 0.94 1.26 1.71 1.99 2.24 2.47 Source: Arizona Data Room Projections Provided by Arizona HIGHLY CONFIDENTIAL 3

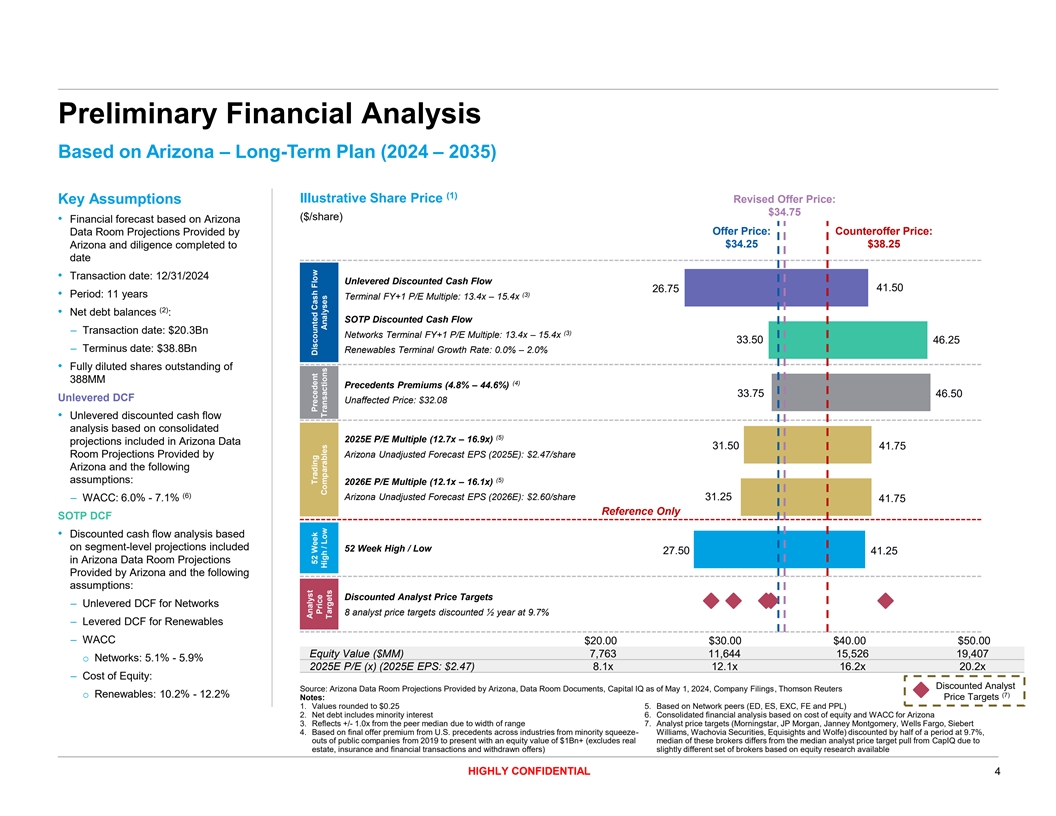

Preliminary Financial Analysis Based on Arizona – Long-Term Plan (2024 – 2035) (1) Illustrative Share Price Revised Offer Price: Key Assumptions $34.75 ($/share) • Financial forecast based on Arizona Offer Price: Counteroffer Price: Data Room Projections Provided by $34.25 $38.25 Arizona and diligence completed to date • Transaction date: 12/31/2024 Unlevered Discounted Cash Flow 26.75 41.50 • Period: 11 years (3) Terminal FY+1 P/E Multiple: 13.4x – 15.4x (2) • Net debt balances : SOTP Discounted Cash Flow – Transaction date: $20.3Bn (3) Networks Terminal FY+1 P/E Multiple: 13.4x – 15.4x 33.50 46.25 – Terminus date: $38.8Bn Renewables Terminal Growth Rate: 0.0% – 2.0% • Fully diluted shares outstanding of 388MM (4) Precedents Premiums (4.8% – 44.6%) 33.75 46.50 Unlevered DCF Unaffected Price: $32.08 • Unlevered discounted cash flow analysis based on consolidated (5) 2025E P/E Multiple (12.7x – 16.9x) projections included in Arizona Data 31.50 41.75 Room Projections Provided by Arizona Unadjusted Forecast EPS (2025E): $2.47/share Arizona and the following (5) assumptions: 2026E P/E Multiple (12.1x – 16.1x) (6) Arizona Unadjusted Forecast EPS (2026E): $2.60/share 31.25 – WACC: 6.0% - 7.1% 41.75 Reference Only SOTP DCF • Discounted cash flow analysis based on segment-level projections included 52 Week High / Low 27.50 41.25 in Arizona Data Room Projections Provided by Arizona and the following assumptions: Discounted Analyst Price Targets – Unlevered DCF for Networks 8 analyst price targets discounted ½ year at 9.7% – Levered DCF for Renewables – WACC $20.00 $30.00 $40.00 $50.00 Equity Value ($MM) 7,763 11,644 15,526 19,407 o Networks: 5.1% - 5.9% 2025E P/E (x) (2025E EPS: $2.47) 8.1x 12.1x 16.2x 20.2x – Cost of Equity: Discounted Analyst Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings, Thomson Reuters o Renewables: 10.2% - 12.2% (7) Notes: Price Targets 1. Values rounded to $0.25 5. Based on Network peers (ED, ES, EXC, FE and PPL) 2. Net debt includes minority interest 6. Consolidated financial analysis based on cost of equity and WACC for Arizona 3. Reflects +/- 1.0x from the peer median due to width of range 7. Analyst price targets (Morningstar, JP Morgan, Janney Montgomery, Wells Fargo, Siebert 4. Based on final offer premium from U.S. precedents across industries from minority squeeze- Williams, Wachovia Securities, Equisights and Wolfe) discounted by half of a period at 9.7%, outs of public companies from 2019 to present with an equity value of $1Bn+ (excludes real median of these brokers differs from the median analyst price target pull from CapIQ due to estate, insurance and financial transactions and withdrawn offers) slightly different set of brokers based on equity research available HIGHLY CONFIDENTIAL 4 Analyst 52 Week Trading Precedent Discounted Cash Flow Price High / Low Comparables Transactions Analyses Targets

APPENDIX Supplementary Financial Analysis HIGHLY CONFIDENTIAL 5

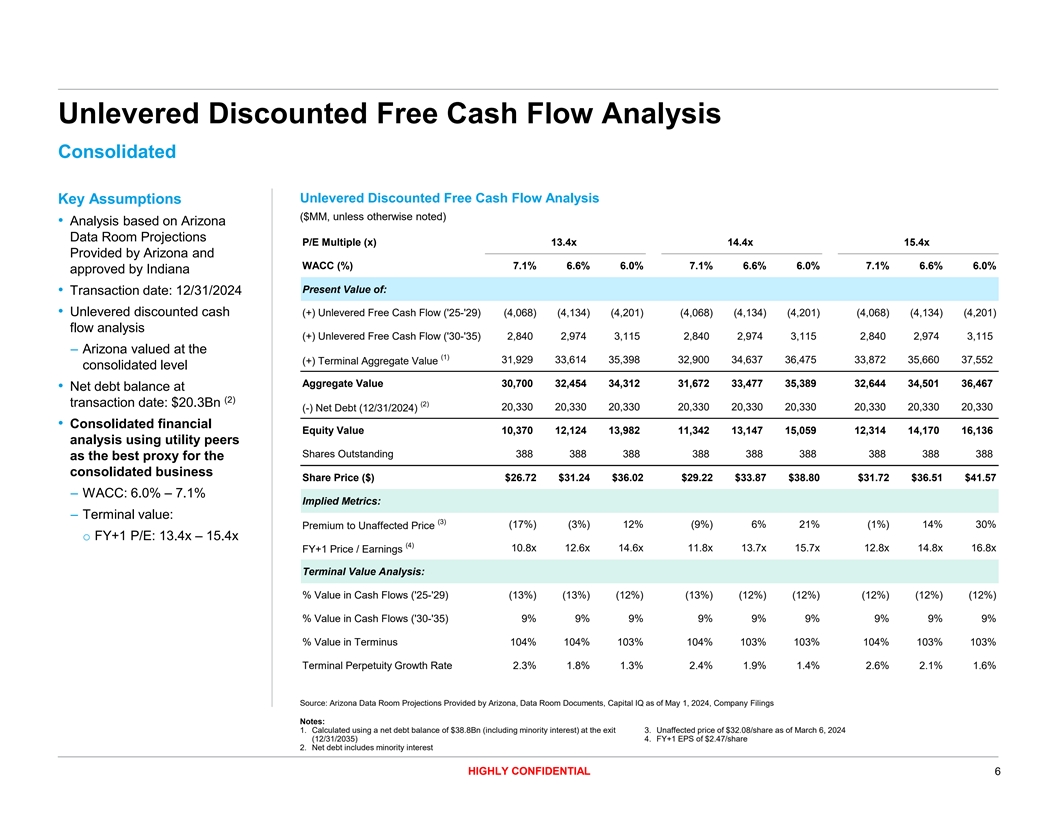

Unlevered Discounted Free Cash Flow Analysis Consolidated Unlevered Discounted Free Cash Flow Analysis Key Assumptions ($MM, unless otherwise noted) • Analysis based on Arizona Data Room Projections P/E Multiple (x) 13.4x 14.4x 15.4x Provided by Arizona and WACC (%) 7.1% 6.6% 6.0% 7.1% 6.6% 6.0% 7.1% 6.6% 6.0% approved by Indiana Present Value of: • Transaction date: 12/31/2024 • Unlevered discounted cash (+) Unlevered Free Cash Flow ('25-'29) (4,068) (4,134) (4,201) (4,068) (4,134) (4,201) (4,068) (4,134) (4,201) flow analysis (+) Unlevered Free Cash Flow ('30-'35) 2,840 2,974 3,115 2,840 2,974 3,115 2,840 2,974 3,115 – Arizona valued at the (1) 31,929 33,614 35,398 32,900 34,637 36,475 33,872 35,660 37,552 (+) Terminal Aggregate Value consolidated level Aggregate Value 30,700 32,454 34,312 31,672 33,477 35,389 32,644 34,501 36,467 • Net debt balance at (2) transaction date: $20.3Bn (2) 20,330 20,330 20,330 20,330 20,330 20,330 20,330 20,330 20,330 (-) Net Debt (12/31/2024) • Consolidated financial Equity Value 10,370 12,124 13,982 11,342 13,147 15,059 12,314 14,170 16,136 analysis using utility peers Shares Outstanding 388 388 388 388 388 388 388 388 388 as the best proxy for the consolidated business Share Price ($) $26.72 $31.24 $36.02 $29.22 $33.87 $38.80 $31.72 $36.51 $41.57 – WACC: 6.0% – 7.1% Implied Metrics: – Terminal value: (3) (17%) (3%) 12% (9%) 6% 21% (1%) 14% 30% Premium to Unaffected Price o FY+1 P/E: 13.4x – 15.4x (4) 10.8x 12.6x 14.6x 11.8x 13.7x 15.7x 12.8x 14.8x 16.8x FY+1 Price / Earnings Terminal Value Analysis: % Value in Cash Flows ('25-'29) (13%) (13%) (12%) (13%) (12%) (12%) (12%) (12%) (12%) % Value in Cash Flows ('30-'35) 9% 9% 9% 9% 9% 9% 9% 9% 9% % Value in Terminus 104% 104% 103% 104% 103% 103% 104% 103% 103% Terminal Perpetuity Growth Rate 2.3% 1.8% 1.3% 2.4% 1.9% 1.4% 2.6% 2.1% 1.6% Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Notes: 1. Calculated using a net debt balance of $38.8Bn (including minority interest) at the exit 3. Unaffected price of $32.08/share as of March 6, 2024 (12/31/2035) 4. FY+1 EPS of $2.47/share 2. Net debt includes minority interest HIGHLY CONFIDENTIAL 6

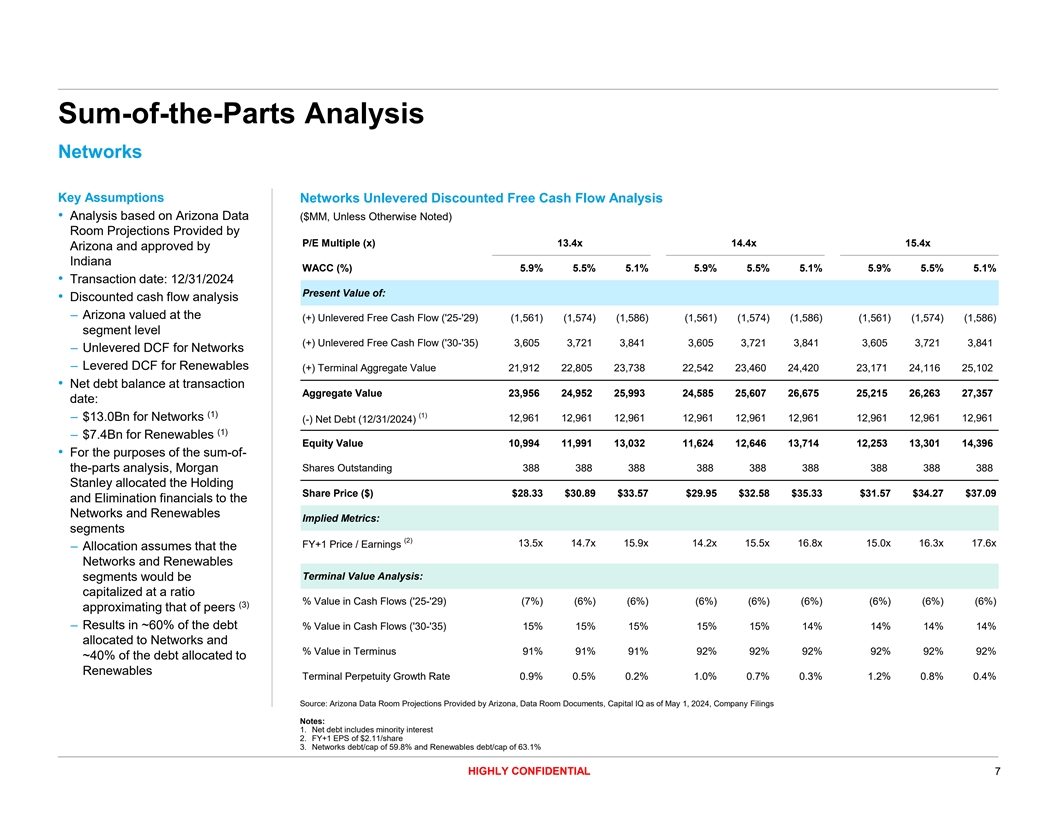

Sum-of-the-Parts Analysis Networks Key Assumptions Networks Unlevered Discounted Free Cash Flow Analysis • Analysis based on Arizona Data ($MM, Unless Otherwise Noted) Room Projections Provided by P/E Multiple (x) 13.4x 14.4x 15.4x Arizona and approved by Indiana WACC (%) 5.9% 5.5% 5.1% 5.9% 5.5% 5.1% 5.9% 5.5% 5.1% • Transaction date: 12/31/2024 Present Value of: • Discounted cash flow analysis – Arizona valued at the (+) Unlevered Free Cash Flow ('25-'29) (1,561) (1,574) (1,586) (1,561) (1,574) (1,586) (1,561) (1,574) (1,586) segment level (+) Unlevered Free Cash Flow ('30-'35) 3,605 3,721 3,841 3,605 3,721 3,841 3,605 3,721 3,841 – Unlevered DCF for Networks – Levered DCF for Renewables (+) Terminal Aggregate Value 21,912 22,805 23,738 22,542 23,460 24,420 23,171 24,116 25,102 • Net debt balance at transaction Aggregate Value 23,956 24,952 25,993 24,585 25,607 26,675 25,215 26,263 27,357 date: (1) (1) – $13.0Bn for Networks 12,961 12,961 12,961 12,961 12,961 12,961 12,961 12,961 12,961 (-) Net Debt (12/31/2024) (1) – $7.4Bn for Renewables Equity Value 10,994 11,991 13,032 11,624 12,646 13,714 12,253 13,301 14,396 • For the purposes of the sum-of- the-parts analysis, Morgan Shares Outstanding 388 388 388 388 388 388 388 388 388 Stanley allocated the Holding Share Price ($) $28.33 $30.89 $33.57 $29.95 $32.58 $35.33 $31.57 $34.27 $37.09 and Elimination financials to the Networks and Renewables Implied Metrics: segments (2) 13.5x 14.7x 15.9x 14.2x 15.5x 16.8x 15.0x 16.3x 17.6x FY+1 Price / Earnings – Allocation assumes that the Networks and Renewables Terminal Value Analysis: segments would be capitalized at a ratio % Value in Cash Flows ('25-'29) (7%) (6%) (6%) (6%) (6%) (6%) (6%) (6%) (6%) (3) approximating that of peers – Results in ~60% of the debt % Value in Cash Flows ('30-'35) 15% 15% 15% 15% 15% 14% 14% 14% 14% allocated to Networks and % Value in Terminus 91% 91% 91% 92% 92% 92% 92% 92% 92% ~40% of the debt allocated to Renewables Terminal Perpetuity Growth Rate 0.9% 0.5% 0.2% 1.0% 0.7% 0.3% 1.2% 0.8% 0.4% Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Notes: 1. Net debt includes minority interest 2. FY+1 EPS of $2.11/share 3. Networks debt/cap of 59.8% and Renewables debt/cap of 63.1% HIGHLY CONFIDENTIAL 7

Sum-of-the-Parts Analysis (Cont’d) Renewables Key Assumptions Renewables Levered Discounted Free Cash Flow Analysis • Analysis based on Arizona Data ($MM, Unless Otherwise Noted) Room Projections Provided by Terminal Perpetuity Growth Rate (%) 0.0% 1.0% 2.0% Arizona and approved by Indiana Cost of Equity (%) 12.2% 11.2% 10.2% 12.2% 11.2% 10.2% 12.2% 11.2% 10.2% • Transaction date: 12/31/2024 Present Value of: • Discounted cash flow analysis – Arizona valued at the (+) Levered Free Cash Flow ('25-'29) 327 322 317 327 322 317 327 322 317 segment level (+) Levered Free Cash Flow ('30-'35) ( 220) (229) (237) (220) (229) (237) (220) (229) (237) – Unlevered DCF for Networks (+) Terminal Equity Value 1,882 2,252 2,720 2,071 2,499 3,047 2,297 2,799 3,454 – Levered DCF for Renewables • Net debt balance at transaction Equity Value 1,988 2,346 2,799 2,178 2,592 3,126 2,404 2,892 3,534 date: (1) (1) 7,365 7,365 7,365 7,365 7,365 7,365 7,365 7,365 7,365 (+) Net Debt (12/31/2024) – $13.0Bn for Networks (1) – $7.4Bn for Renewables Aggregate Value 9,353 9,710 10,164 9,542 9,957 10,491 9,768 10,257 10,898 • For the purposes of the sum-of- Shares Outstanding 388 388 388 388 388 388 388 388 388 the-parts analysis, Morgan Stanley allocated the Holding Share Price ($) $5.12 $6.04 $7.21 $5.61 $6.68 $8.05 $6.19 $7.45 $9.10 and Elimination financials to the Networks and Renewables Terminal Value Analysis: segments % Value in Cash Flows ('25-'29) 16% 14% 11% 15% 12% 10% 14% 11% 9% – Allocation assumes that the Networks and Renewables % Value in Cash Flows ('30-'35) (11%) (10%) (8%) (10%) (9%) (8%) (9%) (8%) (7%) segments would be capitalized at a ratio % Value in Terminus 95% 96% 97% 95% 96% 97% 96% 97% 98% (2) approximating that of peers Terminal AV / EBITDA 9.7x 10.3x 11.1x 10.0x 10.7x 11.6x 10.4x 11.2x 12.2x – Results in ~60% of the debt allocated to Networks and ~40% of the debt allocated to Renewables Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Notes: 1. Net debt includes minority interest 2. Networks debt/cap of 59.8% and Renewables debt/cap of 63.1% HIGHLY CONFIDENTIAL 8

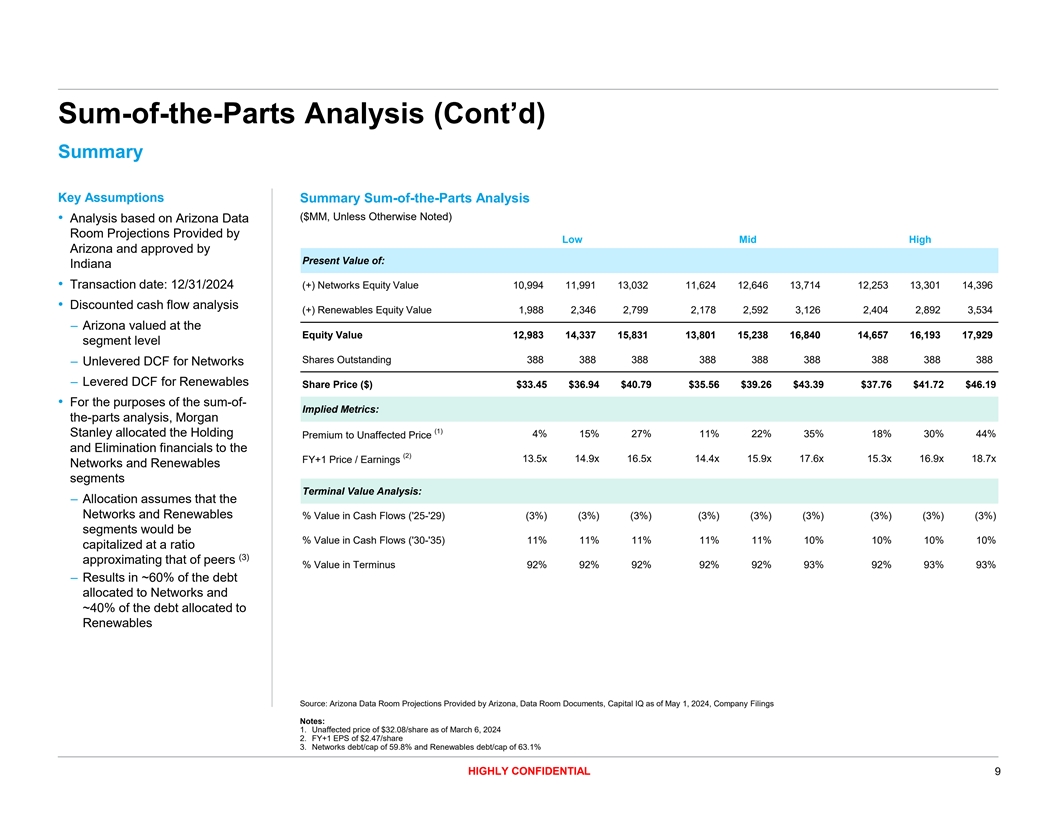

Sum-of-the-Parts Analysis (Cont’d) Summary Key Assumptions Summary Sum-of-the-Parts Analysis ($MM, Unless Otherwise Noted) • Analysis based on Arizona Data Room Projections Provided by Low Mid High Arizona and approved by Present Value of: Indiana • Transaction date: 12/31/2024 (+) Networks Equity Value 10,994 11,991 13,032 11,624 12,646 13,714 12,253 13,301 14,396 • Discounted cash flow analysis (+) Renewables Equity Value 1,988 2,346 2,799 2,178 2,592 3,126 2,404 2,892 3,534 – Arizona valued at the Equity Value 12,983 14,337 15,831 13,801 15,238 16,840 14,657 16,193 17,929 segment level Shares Outstanding 388 388 388 388 388 388 388 388 388 – Unlevered DCF for Networks – Levered DCF for Renewables Share Price ($) $33.45 $36.94 $40.79 $35.56 $39.26 $43.39 $37.76 $41.72 $46.19 • For the purposes of the sum-of- Implied Metrics: the-parts analysis, Morgan (1) Stanley allocated the Holding 4% 15% 27% 11% 22% 35% 18% 30% 44% Premium to Unaffected Price and Elimination financials to the (2) FY+1 Price / Earnings 13.5x 14.9x 16.5x 14.4x 15.9x 17.6x 15.3x 16.9x 18.7x Networks and Renewables segments Terminal Value Analysis: – Allocation assumes that the Networks and Renewables % Value in Cash Flows ('25-'29) (3%) (3%) (3%) (3%) (3%) (3%) (3%) (3%) (3%) segments would be % Value in Cash Flows ('30-'35) 11% 11% 11% 11% 11% 10% 10% 10% 10% capitalized at a ratio (3) approximating that of peers % Value in Terminus 92% 92% 92% 92% 92% 93% 92% 93% 93% – Results in ~60% of the debt allocated to Networks and ~40% of the debt allocated to Renewables Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Notes: 1. Unaffected price of $32.08/share as of March 6, 2024 2. FY+1 EPS of $2.47/share 3. Networks debt/cap of 59.8% and Renewables debt/cap of 63.1% HIGHLY CONFIDENTIAL 9

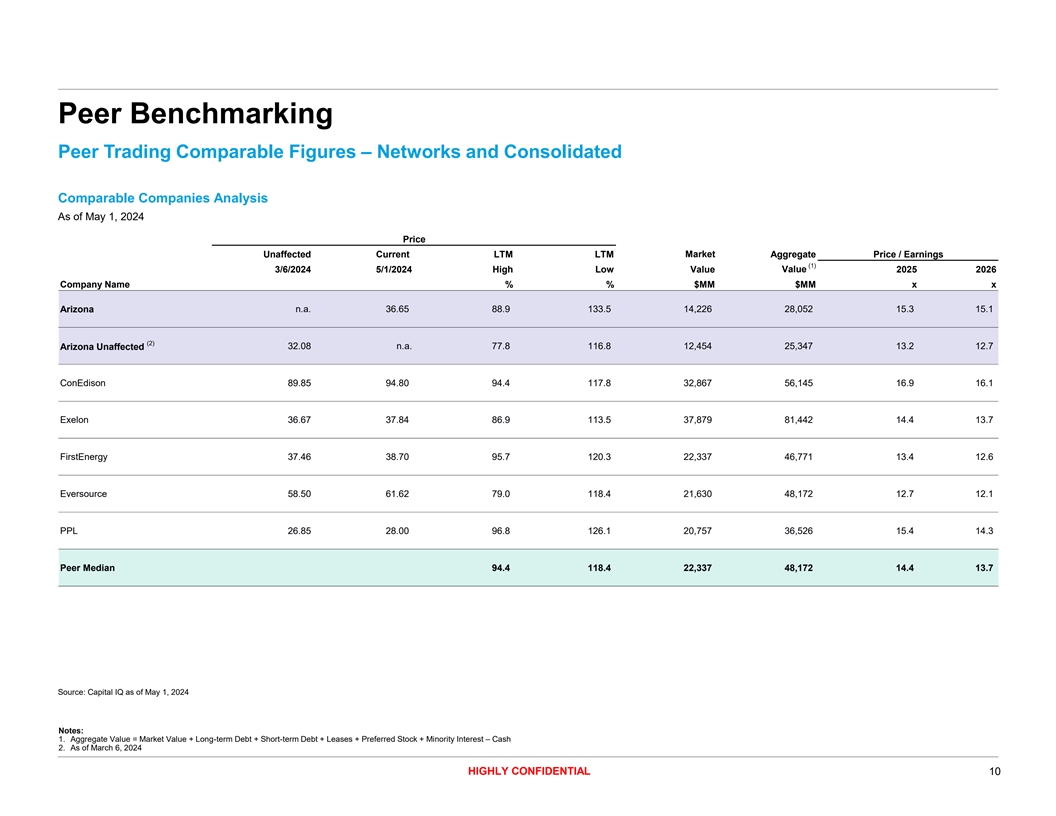

Peer Benchmarking Peer Trading Comparable Figures – Networks and Consolidated Comparable Companies Analysis As of May 1, 2024 Price Unaffected Current LTM LTM Market Aggregate Price / Earnings (1) Value 3/6/2024 5/1/2024 High Low Value 2025 2026 Company Name % % $MM $MM x x Arizona n.a. 36.65 88.9 133.5 14,226 28,052 15.3 15.1 (2) 32.08 n.a. 77.8 116.8 12,454 25,347 13.2 12.7 Arizona Unaffected ConEdison 89.85 94.80 94.4 117.8 32,867 56,145 16.9 16.1 Exelon 36.67 37.84 86.9 113.5 37,879 81,442 14.4 13.7 FirstEnergy 37.46 38.70 95.7 120.3 22,337 46,771 13.4 12.6 Eversource 58.50 61.62 79.0 118.4 21,630 48,172 12.7 12.1 PPL 26.85 28.00 96.8 126.1 20,757 36,526 15.4 14.3 Peer Median 94.4 118.4 22,337 48,172 14.4 13.7 Source: Capital IQ as of May 1, 2024 Notes: 1. Aggregate Value = Market Value + Long-term Debt + Short-term Debt + Leases + Preferred Stock + Minority Interest – Cash 2. As of March 6, 2024 HIGHLY CONFIDENTIAL 10

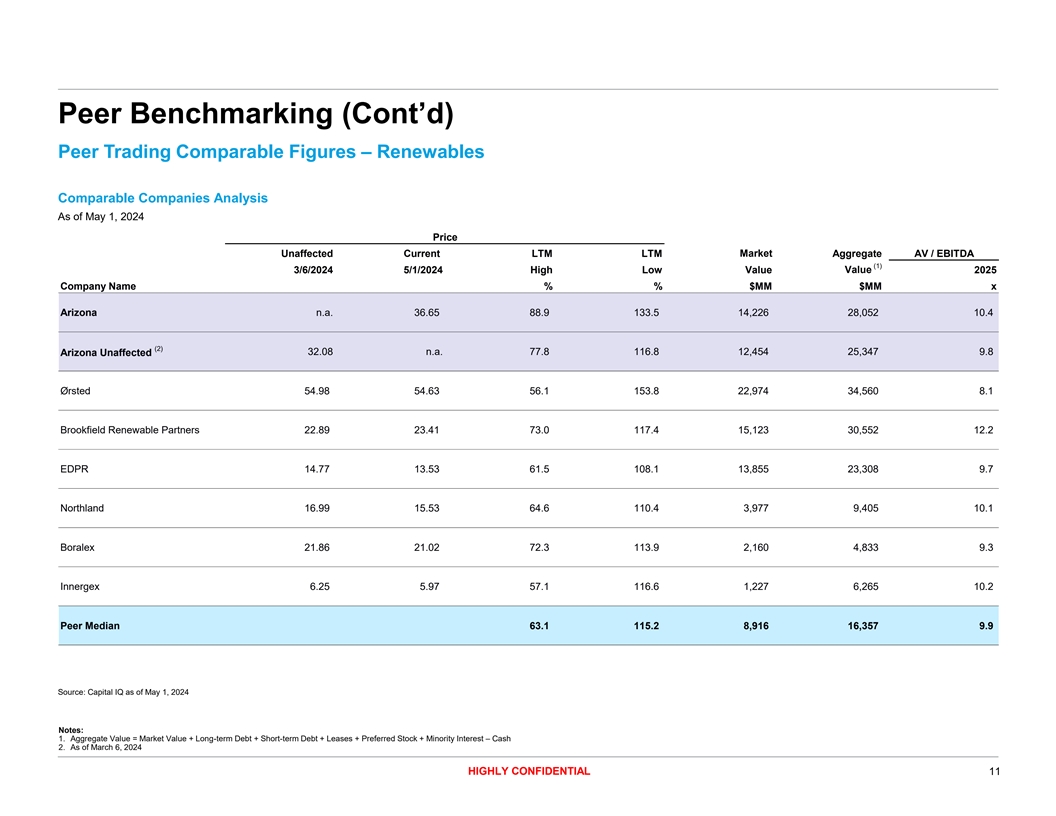

Peer Benchmarking (Cont’d) Peer Trading Comparable Figures – Renewables Comparable Companies Analysis As of May 1, 2024 Price Unaffected Current LTM LTM Market Aggregate AV / EBITDA (1) 3/6/2024 5/1/2024 High Low Value Value 2025 Company Name % % $MM $MM x Arizona n.a. 36.65 88.9 133.5 14,226 28,052 10.4 (2) Arizona Unaffected 32.08 n.a. 77.8 116.8 12,454 25,347 9.8 Ørsted 54.98 54.63 56.1 153.8 22,974 34,560 8.1 Brookfield Renewable Partners 22.89 23.41 73.0 117.4 15,123 30,552 12.2 EDPR 14.77 13.53 61.5 108.1 13,855 23,308 9.7 Northland 16.99 15.53 64.6 110.4 3,977 9,405 10.1 Boralex 21.86 21.02 72.3 113.9 2,160 4,833 9.3 Innergex 6.25 5.97 57.1 116.6 1,227 6,265 10.2 Peer Median 63.1 115.2 8,916 16,357 9.9 Source: Capital IQ as of May 1, 2024 Notes: 1. Aggregate Value = Market Value + Long-term Debt + Short-term Debt + Leases + Preferred Stock + Minority Interest – Cash 2. As of March 6, 2024 HIGHLY CONFIDENTIAL 11

Relevant Precedent Transactions Minority Squeeze-Outs of Public Companies Precedents (U.S. Transactions Across Industries) U.S. Squeeze-Out Precedents Across Industries Basis of Presentation Unaffected • Time Period: 2019 to Ownership Final Prior to Ann. Stake Sought Offer Equity Value present Date Ann. Target Acquirer Industry Target Nation (%) (%) (%) ($MM) • Precedents across 2022 Shell Midstream Partners LP Shell Midstream LP Hldg LLC Energy United States 68.5 31.5 9.6 1,963 industries from minority squeeze-outs of public companies in the U.S. • Equity Value Size: 2022 Continental Resources Inc Omega Acquisition Inc Energy United States 82.6 17.4 15.2 4,701 $1,000MM+ • Excludes real estate, insurance and financial 2021 Phillips 66 Partners LP Phillips 66 Co Energy United States 74.3 25.7 4.8 2,961 transactions • Excludes withdrawn offers 2020 Eidos Therapeutics Inc BridgeBio Pharma Inc Biotech/Pharma United States 60.8 39.2 41.1 1,113 2020 TerraForm Power Inc Brookfield Renewable Partners Utilities United States 61.6 38.4 17.4 1,440 2019 AVX Corp KYOCERA Corp Technology United States 72.0 28.0 44.6 1,031 Source: Thomson Reuters, Company Filings, Deal Point Data HIGHLY CONFIDENTIAL 12

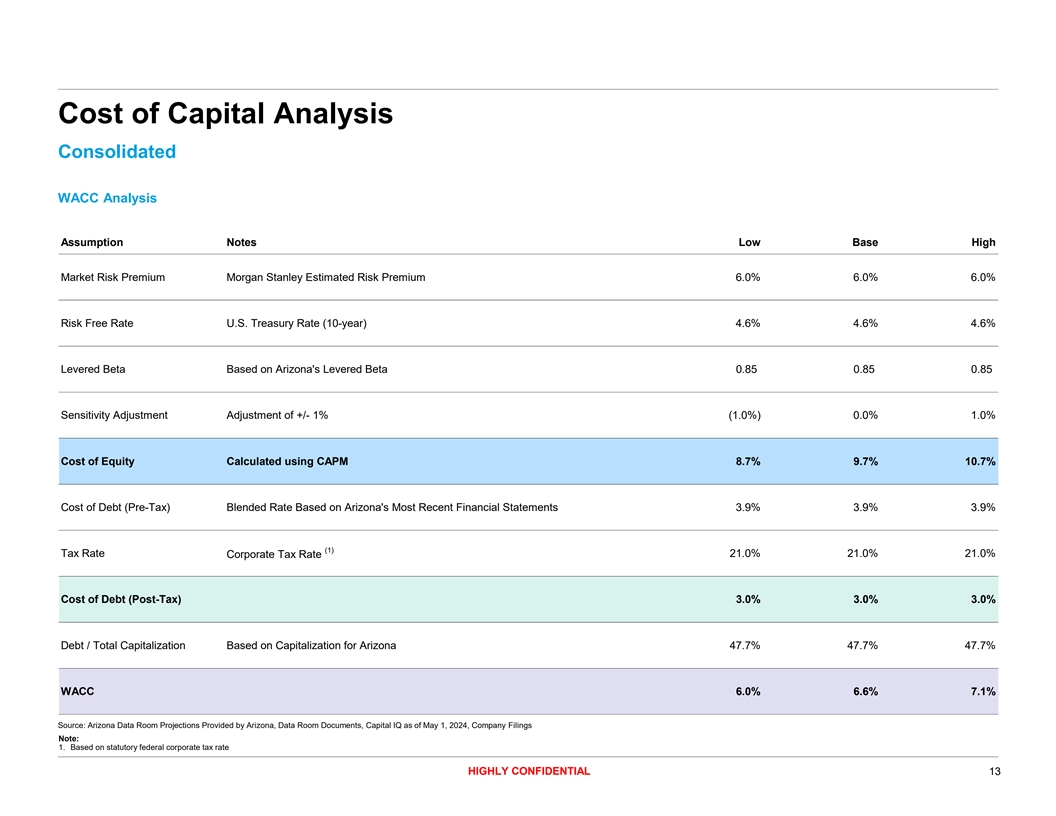

Cost of Capital Analysis Consolidated WACC Analysis Assumption Notes Low Base High Market Risk Premium Morgan Stanley Estimated Risk Premium 6.0% 6.0% 6.0% Risk Free Rate U.S. Treasury Rate (10-year) 4.6% 4.6% 4.6% Levered Beta Based on Arizona's Levered Beta 0.85 0.85 0.85 Sensitivity Adjustment Adjustment of +/- 1% (1.0%) 0.0% 1.0% Cost of Equity Calculated using CAPM 8.7% 9.7% 10.7% Cost of Debt (Pre-Tax) Blended Rate Based on Arizona's Most Recent Financial Statements 3.9% 3.9% 3.9% (1) Tax Rate 21.0% 21.0% 21.0% Corporate Tax Rate Cost of Debt (Post-Tax) 3.0% 3.0% 3.0% Debt / Total Capitalization Based on Capitalization for Arizona 47.7% 47.7% 47.7% WACC 6.0% 6.6% 7.1% Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Note: 1. Based on statutory federal corporate tax rate HIGHLY CONFIDENTIAL 13

Cost of Capital Analysis (Cont’d) Networks WACC Analysis • Capitalization reflects allocation of Holding and Assumption Notes Low Base High Elimination Market Risk Premium Morgan Stanley Estimated Risk Premium 6.0% 6.0% 6.0% Risk Free Rate U.S. Treasury Rate (10-year) 4.6% 4.6% 4.6% Unlevered Beta Based on Median Peer Unlevered Beta 0.35 0.35 0.35 Levered Beta Re-levered at Arizona Networks Segment's Capitalization 0.76 0.76 0.76 Sensitivity Adjustment Adjustment of +/- 1% (1.0%) 0.0% 1.0% Cost of Equity Calculated using CAPM 8.2% 9.2% 10.2% Cost of Debt (Pre-Tax) Blended Rate Based on Arizona's Most Recent Financial Statements 3.9% 3.9% 3.9% (1) Tax Rate Corporate Tax Rate 21.0% 21.0% 21.0% Cost of Debt (Post-Tax) 3.0% 3.0% 3.0% (2) Debt / Total Capitalization Based on Arizona Networks Segment's Capitalization 59.8% 59.8% 59.8% WACC 5.1% 5.5% 5.9% Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Peer Capitalization Company Levered Beta Unlevered Beta Debt to Cap. Levered Beta Calculation Peers ConEdison 0.51 0.32 42.7% Levered Beta Calculation Exelon 0.67 0.35 53.7% Median Peer Unlevered Beta 0.35 FirstEnergy 0.61 0.33 51.9% (2) (2) 59.8% Networks Segment's Capitalization Eversource 0.89 0.45 54.9% Arizona Assumed Tax Rate 21.0% PPL 0.60 0.37 43.6% Arizona Networks Levered Beta 0.76 Median 0.61 0.35 51.9% Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Notes: 1. Based on statutory federal corporate tax rate 2. Reflects assumed allocation of ~60% of Holdings debt to Networks and ~40% to Renewables HIGHLY CONFIDENTIAL 14

Cost of Capital Analysis (Cont’d) Renewables Cost of Equity Analysis • Capitalization reflects allocation of Holding and Assumption Notes Low Base High Elimination Market Risk Premium Morgan Stanley Estimated Risk Premium 6.0% 6.0% 6.0% Risk Free Rate U.S. Treasury Rate (10-year) 4.6% 4.6% 4.6% Unlevered Beta Based on Median Peer Unlevered Beta 0.46 0.46 0.46 Levered Beta Re-levered at Arizona Renewables Segment's Capitalization 1.09 1.09 1.09 Sensitivity Adjustment Adjustment of +/- 1% (1.0%) 0.0% 1.0% Cost of Equity Calculated using CAPM 10.2% 11.2% 12.2% Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Peer Capitalization Company Levered Beta Unlevered Beta Debt to Cap. Levered Beta Calculation Peers Orsted 0.98 0.61 43.6% Levered Beta Calculation Brookfield Renewable Partners 0.91 0.49 51.9% Median Peers Unlevered Beta 0.46 EDPR 1.17 0.76 39.9% Renewables Segment's 63.1% (1) Northland 0.81 0.38 58.9% Capitalization Boralex 0.87 0.43 55.9% Arizona Assumed Tax Rate 21.0% Innergex 0.89 0.21 80.5% Arizona Renewables Levered Beta 1.09 Median 0.90 0.46 53.9% Source: Arizona Data Room Projections Provided by Arizona, Data Room Documents, Capital IQ as of May 1, 2024, Company Filings Note: 1. Reflects assumed allocation of ~60% of Holdings debt to Networks and ~40% to Renewables HIGHLY CONFIDENTIAL 15

Legal Disclaimer We have prepared this document solely for informational purposes. You should not definitively rely upon it or use it to form the definitive basis for any decision, contract, commitment or action whatsoever, with respect to any proposed transaction or otherwise. You and your directors, officers, employees, agents and affiliates must hold this document and any oral information provided in connection with this document in strict confidence and may not communicate, reproduce, distribute or disclose it to any other person, or refer to it publicly, in whole or in part at any time except with our prior written consent. If you are not the intended recipient of this document, please delete and destroy all copies immediately. We have prepared this document and the analyses contained in it based, in part, on certain assumptions and information obtained by us from the recipient, its directors, officers, employees, agents, affiliates and/or from other sources. Our use of such assumptions and information does not imply that we have independently verified or necessarily agree with any of such assumptions or information, and we have assumed and relied upon the accuracy and completeness of such assumptions and information for purposes of this document. Neither we nor any of our affiliates, or our or their respective officers, employees or agents, make any representation or warranty, express or implied, in relation to the accuracy or completeness of the information contained in this document or any oral information provided in connection herewith, or any data it generates and accept no responsibility, obligation or liability (whether direct or indirect, in contract, tort or otherwise) in relation to any of such information. We and our affiliates and our and their respective officers, employees and agents expressly disclaim any and all liability which may be based on this document and any errors therein or omissions therefrom. Neither we nor any of our affiliates, or our or their respective officers, employees or agents, make any representation or warranty, express or implied, that any transaction has been or may be effected on the terms or in the manner stated in this document, or as to the achievement or reasonableness of future projections, management targets, estimates, prospects or returns, if any. Any views or terms contained herein are preliminary only, and are based on financial, economic, market and other conditions prevailing as of the date of this document and are therefore subject to change. We undertake no obligation or responsibility to update any of the information contained in this document. Past performance does not guarantee or predict future performance. This document and the information contained herein do not constitute an offer to sell or the solicitation of an offer to buy any security, commodity or instrument or related derivative, nor do they constitute an offer or commitment to lend, syndicate or arrange a financing, underwrite or purchase or act as an agent or advisor or in any other capacity with respect to any transaction, or commit capital, or to participate in any trading strategies, and do not constitute legal, regulatory, accounting or tax advice to the recipient. We recommend that the recipient seek independent third party legal, regulatory, accounting and tax advice regarding the contents of this document. This document does not constitute and should not be considered as any form of financial opinion or recommendation by us or any of our affiliates. This document is not a research report and was not prepared by the research department of Morgan Stanley or any of its affiliates. Notwithstanding anything herein to the contrary, each recipient hereof (and their employees, representatives, and other agents) may disclose to any and all persons, without limitation of any kind from the commencement of discussions, the U.S. federal and state income tax treatment and tax structure of the proposed transaction and all materials of any kind (including opinions or other tax analyses) that are provided relating to the tax treatment and tax structure. For this purpose, tax structure is limited to facts relevant to the U.S. federal and state income tax treatment of the proposed transaction and does not include information relating to the identity of the parties, their affiliates, agents or advisors. This document is provided by Morgan Stanley & Co. LLC and/or certain of its affiliates or other applicable entities, which may include Morgan Stanley Realty Incorporated, Morgan Stanley Senior Funding, Inc., Morgan Stanley Bank, N.A., Morgan Stanley & Co. International plc, Morgan Stanley Securities Limited, Morgan Stanley Europe SE, Morgan Stanley MUFG Securities Co., Ltd., Mitsubishi UFJ Morgan Stanley Securities Co., Ltd., Morgan Stanley Asia Limited, Morgan Stanley Australia Securities Limited, Morgan Stanley Australia Limited, Morgan Stanley Asia (Singapore) Pte., Morgan Stanley Services Limited, Morgan Stanley & Co. International plc Seoul Branch and/or Morgan Stanley Canada Limited Unless governing law permits otherwise, you must contact an authorized Morgan Stanley entity in your jurisdiction regarding this document or any of the information contained herein. © Morgan Stanley and/or certain of its affiliates. All rights reserved. HIGHLY CONFIDENTIAL 16