UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-23161

NuShares ETF Trust

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Christopher M. Rohrbacher

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: July 31

Date of reporting period: July 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

| | | | | | | | | | |

| | | | | | | Listing Exchange | | Ticker Symbol |

| | | Fund Name | | | | | | | | |

|

| | NuShares Enhanced Yield U.S. Aggregate Bond ETF | | | | NYSE Arca | | NUAG | | |

| | NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF | | | | NYSE Arca | | NUSA | | |

| | | | | | | | | | | | |

| | | | | | |

| | | | |

| | | | | | | | |

| |

| | Life is Complex |

| |

| | Nuveen makes things e-simple. It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready—no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish. |

| | |

| | Free e-Reports right to your e-mail! |

| |

| | www.investordelivery.com If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account. |

| |

| or | | www.nuveen.com/accountaccess If you receive your Nuveen Fund distributions and statements directly from Nuveen. Must be preceded by or accompanied by a prospectus. NOT FDIC INSURED MAY LOSE VALUE

NO BANK GUARANTEE |

Table

of Contents

Chairman’s Letter

to Shareholders

Dear Shareholders,

Some of the key assumptions driving the markets higher at the beginning of 2017 have recently come into question. Following the collapse of the health care reform bill in the Senate, investors are concerned about President Trump’s ability to accomplish the remainder of his pro-growth fiscal agenda, including tax reform and large infrastructure projects. Economic growth projections, in turn, have been lowered and with inflation recently waning, the markets are expecting fewer rate hikes from the Federal Reserve (Fed) than the Fed itself had predicted. Yet, asset prices continued to rise.

Investors have largely looked beyond policy disappointments and focused instead on the healthy profits reported by U.S. companies during the first two quarters of 2017. U.S. growth has remained slow and steady, European growth has surprised to the upside and concern that China would decelerate too rapidly has eased, further contributing to an optimistic tone in the markets. Additionally, political risk in Europe has moderated, with the election of mainstream candidates in the Dutch and French elections earlier this year.

The remainder of the year could bring challenges to this benign macro environment. The U.S. government voted to temporarily increase the nation’s debt limit, but the debate will resume again in December when the current extension of the debt limit expires. In addition, the need for disaster relief and recovery following Hurricanes Harvey and Irma has further muddied the outlook on the White House’s promised agenda. Markets will be watching the “Brexit” negotiations and the North American Free Trade Agreement (NAFTA) talks while assessing the implications for key trade and political partnerships. A tightening of financial conditions in China or a more aggressive-than-expected policy action from the Fed, European Central Bank or Bank of Japan could also turn into headwinds. On the geopolitical front, tensions with North Korea may continue to flare.

Market volatility readings have been remarkably low lately, but conditions can change quickly. As market conditions evolve, Nuveen remains committed to rigorously assessing opportunities and risks. If you’re concerned about how resilient your investment portfolio might be, we encourage you to talk to your financial advisor. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

William J. Schneider

Chairman of the Board

September 20, 2017

Portfolio Managers’

Comments

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

These Funds feature portfolio management by Teachers Advisors, LLC, an affiliate of Nuveen Fund Advisors, LLC. Portfolio managers Lijun (Kevin) Chen, CFA, and Jayesh D. Bhansali, CFA.

Here they discuss U.S. economic and market conditions, key investment strategies and the performance of NUAG during the abbreviated reporting period from NUAG’s commencement of operations on September 14, 2016 through July 31, 2017, and the performance of NUSA during the abbreviated reporting period from the NUSA’s commencement of operations on March 31, 2017 through July 31, 2017.

What factors affected the U.S. economy and the U.S. bond market during the abbreviated annual reporting period ended July 31, 2017?

During the abbreviated reporting period, the U.S. economy continued to grow moderately, now ranking the current expansion as the third-longest since World War II, according to the National Bureau of Economic Research. The second half of 2016 saw a short-term boost in economic activity, driven by a one-time jump in exports during the third quarter, but the economy resumed a below-trend pace in the fourth quarter of 2016 and first quarter of 2017. The Bureau of Economic Analysis reported an annual growth rate of 3.0% for the U.S. economy in the second quarter of 2017, as measured by the “second” estimate of real gross domestic product (GDP), which is the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. Growth in the second quarter was boosted by stronger consumer spending and business investment, which helped offset weaker government spending. By comparison, the annual GDP growth rate in the first quarter of 2017 was 1.2%.

Despite the slowdown in early 2017, other data pointed to positive momentum. The labor market continued to tighten, inflation ticked higher, and consumer and business confidence surveys reflected optimism about the economy’s prospects. As reported by the Bureau of Labor Statistics, the unemployment rate fell to 4.3% in July 2017 from 4.9% in July 2016 and job gains averaged around 181,000 per month for the past twelve months. Higher oil prices helped drive a steady increase in inflation over this reporting period. The Consumer Price Index (CPI) increased 1.7% over the twelve-month reporting period ended July 31, 2017 on a seasonally adjusted basis, as reported by the Bureau of Labor Statistics. The core CPI (which excludes food and energy) increased 1.7% during the same period, slightly below the Federal Reserve’s (Fed) unofficial longer term inflation objective of 2.0%. The housing market also continued to improve, with historically low mortgage rates and low inventory driving home prices higher. The S&P CoreLogic Case-Shiller U.S. National Home Price Index, which covers all nine U.S. census divisions, recorded a 5.8% annual gain in June 2017 (most recent data available at the time this report was prepared). The 10-City and 20-City Composites reported year-over-year increases of 4.9% and 5.7%, respectively.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Fund disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

The ratings disclosed reflects net exposure to credit ratings by one or more of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). If there are multiple ratings for a security, the average rating is used, with evenly split ratings being rounded down to the lower rating, which is the method used by the Index. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this report for further definition of the terms used within this section.

Portfolio Managers’ Comments (continued)

The U.S. economic outlook struck a more optimistic tone, prompting the Fed’s policy making committee to raise its main benchmark interest rate in December 2016, March 2017 and June 2017. These moves were widely expected by the markets and, while the Fed acknowledged in its June 2017 statement that inflation has remained unexpectedly low, an additional increase is anticipated later in 2017 as the Fed seeks to gradually “normalize” interest rates. Also after the June 2017 meeting, the Fed revealed its plan to begin shrinking its balance sheets by allowing a small amount of maturing Treasury and mortgage securities to roll off without reinvestment. The timing of this is less certain, however, as it depends on whether the economy performs in line with the Fed’s expectations. As expected, the Fed left rates unchanged at its July 2017 meeting.

Politics also dominated the headlines in this reporting period with two major electoral surprises: the U.K.’s vote to leave the European Union and Donald Trump’s win in the U.S. presidential race. Market volatility increased as markets digested the initial shocks, but generally recovered and, in the case of the “Trump rally,” U.S. equities saw significant gains. Investors also closely watched elections across Europe. To the markets’ relief, more mainstream candidates were elected in the Dutch and French elections in the spring of 2017. However, Britain’s June 2017 snap election unexpectedly overturned the Conservative Party’s majority in Parliament, which increased uncertainties about the Brexit negotiation process. Additionally, in the U.S., legislative delays with health care reform dimmed the prospects for President Trump’s tax cuts and other fiscal stimulus, while investors braced for a showdown in Congress over increasing the nation’s debt limit. Toward the end of the reporting period, escalating tensions between the U.S. and North Korea led to some near-term volatility in global equity shares to the benefit of perceived safe-haven assets such as gold, U.S. Treasury bonds and Japanese yen.

The broad U.S. bond market had a small gain during the abbreviated reporting period. A period of heightened volatility after the U.S. presidential election drove bond prices sharply lower in the fourth quarter of 2016. However, bonds largely recovered their losses by the end of the reporting period. The Fed’s rate hikes lifted interest rates on the short end of the spectrum, but intermediate- and longer-term rates remained relatively stable as investors have been satisfied with the Fed’s gradual pace of tightening. Muted inflation, moderate economic growth and strong corporate and real estate fundamentals helped non-government bond sectors outperform Treasuries during the abbreviated reporting period.

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

What key strategies were used to manage the Fund during the abbreviated reporting period and how did these strategies influence performance?

The Fund employs a passive management (or “indexing”) approach, seeking to track the investment results, before fees and expenses, of the BofA/Merrill Lynch Enhanced Yield U.S. Broad Bond Index (the “Enhanced Index”). The Enhanced Index is designed to broadly capture the U.S. investment grade fixed income market and uses a rules-based weighting methodology that seeks to enhance yield while maintaining comparable risk. The Enhanced Index is primarily comprised of U.S. government securities, debt securities issued by U.S. corporations, residential and commercial mortgage-backed securities, asset-backed securities and U.S. dollar-denominated debt securities issued by non-U.S. governments and corporations that are publicly offered for sale in the United States. The Fund generally invests in a sample of the securities in the Enhanced Index whose risk, return and other characteristics resemble the risk, return and other characteristics of the Enhanced Index. Under normal market conditions, the Fund invests at least 80% of its assets, exclusive of collateral held from securities lending, in component securities of the Enhanced Index. The Fund rebalances its holdings monthly in response to the monthly Enhanced Index rebalances.

During the abbreviated reporting period, the Fund has remained fully invested within its allocation targets to track the Enhanced Index. As of July 31, 2017, the Fund’s net assets were invested in 40.0% securitized debt, 35.5% corporate debt, 20.2% U.S. Treasuries and 3.4% government-related debt. Despite heightened volatility surrounding the U.S. elections in early November 2016, the Fund delivered index-like performance results and minimized tracking error (i.e. the divergence in performance from that of the Enhanced Index), in this abbreviated reporting period.

How did the Fund perform during this abbreviated reporting period ended July 31, 2017?

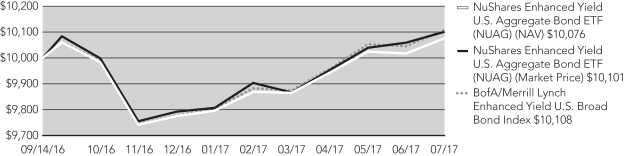

The table in the Fund’s Performance Overview and Expense Ratios section of this report provides the Fund’s total return performance for the abbreviated reporting period from the Fund’s commencement of operation on September 14, 2016 through

July 31, 2017. The Fund’s total returns at net asset value (NAV) are compared with the performance of the Enhanced Index, which the Fund is designed to track.

The Fund’s total return underperformed the Enhanced Index over this abbreviated reporting period. As expected, the relative underperformance is mainly attributable to the transaction costs related to the Fund’s acquisition of structured securities, as well as fees and expenses incurred by the Fund that are not incurred by the Enhanced Index. The Enhanced Index is unmanaged and therefore its returns do not reflect any fees or expenses, which would detract from its performance. You cannot invest directly in an index.

NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

What key strategies were used to manage the Fund during the abbreviated reporting period and how did these strategies influence performance?

The Fund employs a passive management (or “indexing”) approach, seeking to track the investment results, before fees and expenses, of the BofA/Merrill Lynch Enhanced Yield 1-5 Year U.S. Broad Bond Index (the “Enhanced Index”). The Enhanced Index is designed to broadly capture the 1-5 year U.S. investment grade fixed income market and uses a rules-based weighting methodology that seeks to enhance yield while maintaining comparable risk. The Enhanced Index is primarily comprised of U.S. government securities, debt securities issued by U.S. corporations, residential and commercial mortgage-backed securities, asset-backed securities and U.S. dollar-denominated debt securities issued by non-U.S. governments and corporations that are publicly offered for sale in the United States. The Fund generally invests in a sample of the securities in the Enhanced Index whose risk, return and other characteristics resemble the risk, return and other characteristics of the Enhanced Index. Under normal market conditions, the Fund invests at least 80% of its assets and the amount of any borrowings for investment purposes in component securities of the Enhanced Index. The Fund rebalances its holdings monthly in response to the monthly Enhanced Index rebalances.

During the abbreviated reporting period, the Fund has remained fully invested within its allocation targets to track the Enhanced Index. As of July 31, 2017, the Fund’s net assets were invested in 51.1% corporate debt, 25.1% securitized debt, 22.3% U.S. Treasuries and 0.8% government-related debt. The Fund delivered index-like performance results and minimized tracking error (i.e. the divergence in performance from that of the Enhanced Index), in this abbreviated reporting period.

How did the Fund perform during this abbreviated reporting period ended July 31, 2017?

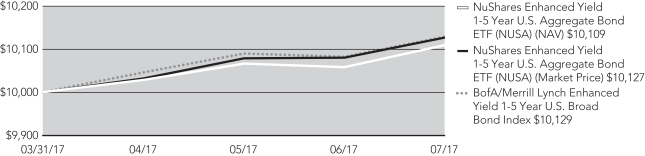

The table in the Fund’s Performance Overview and Expense Ratios section of this report provides the Fund’s total return performance for the abbreviated reporting period from the Fund’s commencement of operation on March 31, 2017 through July 31, 2017. The Fund’s total returns at net asset value (NAV) are compared with the performance of the Enhanced Index, which the Fund is designed to track.

The Fund’s total return underperformed the Enhanced Index over this abbreviated reporting period. As expected, the relative underperformance is mainly attributable to the transaction costs related to the Fund’s acquisition of structured securities, as well as fees and expenses incurred by the Fund that are not incurred by the Enhanced Index. The Enhanced Index is unmanaged and therefore its returns do not reflect any fees or expenses, which would detract from its performance. You cannot invest directly in an index.

Risk Considerations

and Dividend Information

NuShares Enhanced Yield U.S. Aggregate Bond ETF

Investing involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. An exchange-traded fund seeks to generally track the investment results of an index; however the Fund may underperform, outperform or be more volatile than the referenced index. Interest rate risk occurs when interest rates rise causing bond prices to fall. Credit risk arises from an issuer’s ability to make interest and principal payments when due, as well as the prices of bonds declining when an issuer’s credit quality is expected to deteriorate. These and other risk considerations are described in detail in the Fund’s prospectus.

NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF

Investing involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. This ETF seeks to generally track the investment results of an index; however the Fund may underperform, outperform or be more volatile than the referenced index. Interest rate risk is the risk that the value of the Fund’s portfolio will decline because of rising interest rates. Credit risk is the risk that an issuer of a debt security may be unable or unwilling to make interest and principal payments when due and the related risk that the value of a debt security may decline because of concerns about the issuer’s ability or willingness to make such payments. This ETF is concentrated in the financial sector. Performance of companies in the financial sector may be adversely impacted by many factors, including, among others, government regulations, economic conditions, changes in interest rates and decreased liquidity in credit markets. These and other risk considerations are described in detail in the Fund’s prospectus.

Dividend Information

Each Fund seeks to pay monthly dividends out of its net investment income. Monthly distributions are not expected to be a level amount from period-to-period. Each Fund will, over time, pay all its net investment income as dividends to shareholders.

As of July 31, 2017, the Funds had positive UNII balances for tax purposes and positive UNII balances for financial reporting purposes.

All monthly dividends paid by each Fund during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions was sourced from or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders would have received a notice to that effect. For financial reporting purposes, the composition and per share amounts of each Fund’s dividends for the reporting period are presented in this report’s Statement of Changes in Net Assets and Financial Highlights, respectively. For income tax purposes, distribution information for each Fund as of its July 31, 2017 tax year end will be presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

Fund Performance

and Expense Ratios

The Fund Performance and Expense Ratio for each Fund are shown within this section of the report.

Returns quoted represent past performance, which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are sold, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Total returns for a period of less than one year are not annualized. Returns assume reinvestment of dividends and capital gains. Market price returns are based on the closing market price as of the end of the reporting period. For performance current to the most recent month-end visit nuveen.com or call (800) 257-8787.

Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

The expense ratios represents each Fund’s total operating expenses as reflected in the most recent prospectus. The expense ratios shown include the management fees and other applicable fees and expenses paid by the Fund.

Fund Performance and Expense Ratios (continued)

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance

Total Returns as of July 31, 2017

| | | | |

| | | Cumulative | |

| | | Since

Inception | |

NUAG at NAV | | | 0.74% | |

NUAG at Market Price | | | 1.00% | |

BofA Merrill Lynch Enhanced Yield U.S. Broad Bond Index | | | 1.08% | |

Bloomberg Barclays U.S. Aggregate Bond Index | | | 0.21% | |

Total Returns as of June 30, 2017 (Most Recent Calendar Quarter)

| | | | |

| | | Cumulative | |

| | | Since

Inception | |

NUAG at NAV | | | 0.17% | |

NUAG at Market Price | | | 0.57% | |

Since inception returns are from 9/14/16. Indexes are not available for direct investment.

Expense Ratio as of Most Recent Prospectus

Growth of an Assumed $10,000 Investment as of July 31, 2017

The graph does not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance

Total Returns as of July 31, 2017

| | | | |

| | | Cumulative | |

| | | Since

Inception | |

NUSA at NAV | | | 1.10% | |

NUSA at Market Price | | | 1.26% | |

BofA Merrill Lynch Enhanced Yield 1-5 Year U.S. Broad Bond Index | | | 1.29% | |

Bloomberg Barclays 1-5 Year Government/Credit Index | | | 0.92% | |

Total Returns as of June 30, 2017 (Most Recent Calendar Quarter)

| | | | |

| | | Cumulative | |

| | | Since

Inception | |

NUSA at NAV | | | 0.69% | |

NUSA at Market Price | | | 0.80% | |

Since inception returns are from 3/31/17. Indexes are not available for direct investment.

Expense Ratio as of Most Recent Prospectus

Growth of an Assumed $10,000 Investment as of July 31, 2017

The graph does not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Yields as of July 31, 2017

Dividend Yield is the most recent dividend per share (annualized) divided by the market price per share.

The SEC 30-Day Yield is a standardized measure of a fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum market price per share. Dividend Yield may differ from the SEC 30-Day Yield because the fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium.

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

| | | | |

Dividend Yield | | | 3.12% | |

SEC 30-Day Yield | | | 2.64% | |

NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

| | | | |

Dividend Yield | | | 2.85% | |

SEC 30-Day Yield | | | 1.99% | |

Holding

Summaries as of July 31, 2017

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

The ratings disclosed reflects net exposure to credit ratings by one or more of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). If there are multiple ratings for a security, the average rating is used, with evenly split ratings being rounded down to the lower rating, which is the method used by the Index. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

Fund Allocation

(% of net assets)

| | | | |

Corporate Debt | | | 35.5% | |

Government Related | | | 3.4% | |

U.S. Treasury | | | 20.2% | |

Securitized | | | 40.0% | |

Short-Term Investments | | | 1.0% | |

Other Assets Less Liabilities | | | (0.1)% | |

Net Assets | | | 100% | |

Corporate Debt: Industries

(% of total corporate debt holdings)

| | | | |

Industrial | | | 49.9% | |

Financials | | | 28.0% | |

Utility | | | 22.1% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total investments)

| | | | |

AAA | | | 58.7% | |

AA | | | 3.0% | |

A | | | 4.8% | |

BBB | | | 32.4% | |

BB or Lower | | | 0.1% | |

N/R (Not Rated) | | | 1.0% | |

Total | | | 100% | |

Holding Summaries as of July 31, 2017 (continued)

NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

Fund Allocation

(% of net assets)

| | | | |

Corporate Debt | | | 51.1% | |

U.S. Treasury | | | 22.3% | |

Securitized | | | 25.1% | |

Short-Term Investments | | | 0.8% | |

Other Assets Less Liabilities | | | 0.7% | |

Net Assets | | | 100% | |

Corporate Debt: Industries

(% of total corporate debt holdings)

| | | | |

Financials | | | 62.4% | |

Industrial | | | 23.5% | |

Utility | | | 14.1% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total investments)

| | | | |

AAA | | | 47.8% | |

AA | | | 2.0% | |

A | | | 18.8% | |

BBB | | | 30.6% | |

N/R (Not Rated) | | | 0.8% | |

Total | | | 100% | |

Expense

Examples

As a shareholder of one or more of the funds, you incur two types of costs: (1) transaction costs, including brokerage commissions on purchases and sales of Fund shares, and (2) ongoing costs, including management fees and other applicable Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other funds. Since NUSA’s expense example below reflects only the first 123 days of the Fund’s operations, it may not provide a meaningful understanding of the Fund’s ongoing expenses.

The Examples below are based on an investment of $1,000 invested at the beginning of the period and held through July 31, 2017.

The beginning of the period of NUAG is February 1, 2017 and the beginning of the period for NUSA is March 31, 2017 (commencement of operations).

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your Fund in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance” provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

| | | | |

Actual Performance | | | | |

Beginning Account Value | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,028.50 | |

Expenses Incurred During Period | | $ | 1.01 | |

Hypothetical Performance (5% annualized return before expenses) | | | | |

Beginning Account Value | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,023.80 | |

Expenses Incurred During Period | | $ | 1.00 | |

Expenses are equal to the Fund’s annualized net expense ratio of 0.20% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Expense Examples (continued)

NuShares Enhanced Yield 1-5 year U.S. Aggregate Bond ETF (NUSA)

| | | | |

Actual Performance | | | | |

Beginning Account Value | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,011.00 | |

Expenses Incurred During Period | | $ | 0.68 | |

Hypothetical Performance (5% annualized return before expenses) | | | | |

Beginning Account Value | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,016.18 | |

Expenses Incurred During Period | | $ | 0.68 | |

Expenses are equal to the Fund’s annualized net expense ratio of 0.20% multiplied by the average account value over the period, multiplied by 123/365 (to reflect the 123 days in the period since commencement of operations).

Report of

Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

NuShares ETF Trust:

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of NuShares Enhanced Yield U.S. Aggregate Bond ETF and NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (two of the funds comprising NuShares ETF Trust) (the “Funds”) as of July 31, 2017, and the related statements of operations and changes in net assets, and the financial highlights for the periods September 14, 2016 (commencement of operations) through July 31, 2017 for NuShares Enhanced Yield U.S. Aggregate Bond ETF and March 31, 2017 (commencement of operations) through July 31, 2017 for NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF. These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of July 31, 2017, by correspondence with the custodian and brokers or other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Funds as of July 31, 2017, the results of their operations, the changes in their net assets, and the financial highlights for the periods specified in the first paragraph, in conformity with U.S. generally accepted accounting principles.

/s/ KPMG LLP

Chicago, Illinois

September 29, 2017

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG)

| | |

| Portfolio of Investments | | July 31, 2017 |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | LONG-TERM INVESTMENTS – 99.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | CORPORATE DEBT – 35.5% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | Financials – 9.9% | | | | | | | | | | | | |

| | | | | |

| $ | 80 | | | AerCap Ireland Capital Limited / AerCap Global Aviation Trust | | | 4.250% | | | | 7/01/20 | | | | BBB– | | | $ | 84,097 | |

| | | | | |

| | 70 | | | American International Group, Inc. | | | 4.125% | | | | 2/15/24 | | | | BBB+ | | | | 74,414 | |

| | | | | |

| | 46 | | | Anthem, Inc. | | | 3.500% | | | | 8/15/24 | | | | BBB+ | | | | 47,601 | |

| | | | | |

| | 88 | | | Bank of America Corporation | | | 4.200% | | | | 8/26/24 | | | | BBB | | | | 92,044 | |

| | | | | |

| | 146 | | | Bank of America Corporation | | | 3.950% | | | | 4/21/25 | | | | BBB | | | | 149,539 | |

| | | | | |

| | 115 | | | Bank of America Corporation | | | 4.183% | | | | 11/25/27 | | | | BBB | | | | 118,760 | |

| | | | | |

| | 200 | | | Bank of New York Mellon | | | 2.600% | | | | 2/07/22 | | | | A+ | | | | 201,841 | |

| | | | | |

| | 40 | | | Barclays Bank PLC | | | 3.750% | | | | 5/15/24 | | | | A | | | | 41,594 | |

| | | | | |

| | 86 | | | BGC Partners Inc. | | | 5.375% | | | | 12/09/19 | | | | BBB– | | | | 90,930 | |

| | | | | |

| | 350 | | | Capital One Bank | | | 3.375% | | | | 2/15/23 | | | | BBB+ | | | | 355,212 | |

| | | | | |

| | 120 | | | Citigroup Inc. | | | 3.500% | | | | 5/15/23 | | | | BBB | | | | 122,502 | |

| | | | | |

| | 120 | | | Citigroup Inc. | | | 3.700% | | | | 1/12/26 | | | | A– | | | | 122,130 | |

| | | | | |

| | 227 | | | Citigroup Inc. | | | 4.750% | | | | 5/18/46 | | | | BBB | | | | 240,938 | |

| | | | | |

| | 40 | | | Credit Suisse Group Funding Guernsey Limited | | | 3.800% | | | | 9/15/22 | | | | BBB+ | | | | 41,851 | |

| | | | | |

| | 162 | | | Credit Suisse New York | | | 5.400% | | | | 1/14/20 | | | | BBB | | | | 174,077 | |

| | | | | |

| | 72 | | | Delphi Financial Group | | | 7.875% | | | | 1/31/20 | | | | BBB | | | | 80,783 | |

| | | | | |

| | 100 | | | Deutsche Bank AG | | | 2.850% | | | | 5/10/19 | | | | BBB | | | | 101,150 | |

| | | | | |

| | 145 | | | Deutsche Bank AG | | | 2.950% | | | | 8/20/20 | | | | BBB | | | | 146,559 | |

| | | | | |

| | 70 | | | Deutsche Bank AG | | | 3.375% | | | | 5/12/21 | | | | BBB | | | | 71,194 | |

| | | | | |

| | 86 | | | E Trade Financial Corporation | | | 4.625% | | | | 9/15/23 | | | | BBB– | | | | 90,057 | |

| | | | | |

| | 94 | | | Fifth Third Bancorp. | | | 4.300% | | | | 1/16/24 | | | | BBB+ | | | | 99,920 | |

| | | | | |

| | 40 | | | First Niagara Financial Group, Inc. | | | 6.750% | | | | 3/19/20 | | | | BBB+ | | | | 44,640 | |

| | | | | |

| | 127 | | | FS Investment Corporation | | | 4.000% | | | | 7/15/19 | | | | BBB– | | | | 128,651 | |

| | | | | |

| | 94 | | | Goldman Sachs Group Inc., Series EMC | | | 3.750% | | | | 2/25/26 | | | | A– | | | | 96,121 | |

| | | | | |

| | 253 | | | Goldman Sachs Group, Inc. | | | 3.000% | | | | 4/26/22 | | | | A– | | | | 256,345 | |

| | | | | |

| | 115 | | | Goldman Sachs Group, Inc. | | | 3.500% | | | | 11/16/26 | | | | A– | | | | 114,727 | |

| | | | | |

| | 40 | | | Government Properties Income Trust | | | 3.750% | | | | 8/15/19 | | | | BBB– | | | | 40,487 | |

| | | | | |

| | 44 | | | Host Hotel & Resorts Inc. | | | 6.000% | | | | 10/01/21 | | | | BBB | | | | 49,133 | |

| | | | | |

| | 200 | | | HSBC Holdings PLC | | | 4.250% | | | | 3/14/24 | | | | A | | | | 208,975 | |

| | | | | |

| | 46 | | | Humana, Inc. | | | 3.850% | | | | 10/01/24 | | | | BBB | | | | 48,363 | |

| | | | | |

| | 60 | | | Huntington BancShares Inc. | | | 7.000% | | | | 12/15/20 | | | | BBB | | | | 68,551 | |

| | | | | |

| | 88 | | | Jefferies Group Inc. | | | 8.500% | | | | 7/15/19 | | | | BBB– | | | | 98,246 | |

| | | | | |

| | 100 | | | JPMorgan Chase & Company | | | 2.972% | | | | 1/15/23 | | | | A | | | | 101,377 | |

| | | | | |

| | 80 | | | JPMorgan Chase & Company | | | 3.375% | | | | 5/01/23 | | | | A– | | | | 81,690 | |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Financials (continued) | | | | | | | | | | | | |

| | | | | |

| $ | 100 | | | JPMorgan Chase & Company | | | 3.200% | | | | 6/15/26 | | | | A | | | $ | 99,368 | |

| | | | | |

| | 40 | | | Key Bank NA | | | 3.400% | | | | 5/20/26 | | | | BBB+ | | | | 39,659 | |

| | | | | |

| | 94 | | | Lincoln National Corporation | | | 4.200% | | | | 3/15/22 | | | | BBB+ | | | | 100,235 | |

| | | | | |

| | 40 | | | Mitsubishi UFJ Financial Group, Inc. | | | 3.850% | | | | 3/01/26 | | | | A | | | | 41,929 | |

| | | | | |

| | 88 | | | Morgan Stanley Dean Witter & Company | | | 4.875% | | | | 11/01/22 | | | | BBB | | | | 95,773 | |

| | | | | |

| | 94 | | | Morgan Stanley | | | 3.875% | | | | 1/27/26 | | | | A– | | | | 97,190 | |

| | | | | |

| | 62 | | | Pennantpark Investment Corporation | | | 4.500% | | | | 10/01/19 | | | | BBB– | | | | 63,210 | |

| | | | | |

| | 38 | | | Primerica Inc. | | | 4.750% | | | | 7/15/22 | | | | BBB+ | | | | 41,194 | |

| | | | | |

| | 84 | | | Principal Financial Inc. | | | 3.125% | | | | 5/15/23 | | | | BBB+ | | | | 85,804 | |

| | | | | |

| | 70 | | | Prospect Capital Corporation | | | 5.000% | | | | 7/15/19 | | | | BBB– | | | | 71,893 | |

| | | | | |

| | 48 | | | Prudential Financial Inc. | | | 3.500% | | | | 5/15/24 | | | | A– | | | | 50,219 | |

| | | | | |

| | 46 | | | Prudential Financial Inc. | | | 5.875% | | | | 9/15/42 | | | | BBB | | | | 51,232 | |

| | | | | |

| | 40 | | | Rabobank Nederland | | | 3.950% | | | | 11/09/22 | | | | A– | | | | 42,103 | |

| | | | | |

| | 41 | | | Reinsurance Group of America Inc. | | | 4.700% | | | | 9/15/23 | | | | BBB+ | | | | 44,544 | |

| | | | | |

| | 44 | | | Select Income REIT | | | 3.600% | | | | 2/01/20 | | | | BBB– | | | | 44,668 | |

| | | | | |

| | 40 | | | Senior Housing Properties Trust | | | 3.250% | | | | 5/01/19 | | | | BBB– | | | | 40,525 | |

| | | | | |

| | 77 | | | Stifel Financial Corporation | | | 3.500% | | | | 12/01/20 | | | | BBB– | | | | 79,184 | |

| | | | | |

| | 42 | | | Sumitomo Mitsui Financial Group, Inc. | | | 3.784% | | | | 3/09/26 | | | | A | | | | 43,885 | |

| | | | | |

| | 40 | | | Suntrust Bank, Subordinate Note | | | 3.300% | | | | 5/15/26 | | | | BBB+ | | | | 39,539 | |

| | | | | |

| | 40 | | | SVB Financial Group | | | 5.375% | | | | 9/15/20 | | | | BBB+ | | | | 43,585 | |

| | | | | |

| | 60 | | | Synovus Financial Corp. | | | 7.875% | | | | 2/15/19 | | | | BBB– | | | | 64,968 | |

| | | | | |

| | 41 | | | Torchmark Corporation | | | 3.800% | | | | 9/15/22 | | | | A– | | | | 42,466 | |

| | | | | |

| | 48 | | | UnumProvident Corporation | | | 5.625% | | | | 9/15/20 | | | | BBB | | | | 52,707 | |

| | | | | |

| | 38 | | | Voya Financial Inc. | | | 5.500% | | | | 7/15/22 | | | | BBB | | | | 42,546 | |

| | | | | |

| | 86 | | | Wells Fargo & Company | | | 3.000% | | | | 4/22/26 | | | | A+ | | | | 84,641 | |

| | 5,185 | | | Total Financials | | | | | | | | | | | | | | | 5,387,566 | |

| | | | | |

| | | | Industrial – 17.7% | | | | | | | | | | | | |

| | | | | |

| | 46 | | | AbbVie Inc. | | | 3.600% | | | | 5/14/25 | | | | BBB+ | | | | 47,408 | |

| | | | | |

| | 32 | | | AGCO Corporation | | | 5.875% | | | | 12/01/21 | | | | BBB– | | | | 35,055 | |

| | | | | |

| | 138 | | | Allergan | | | 3.850% | | | | 6/15/24 | | | | BBB– | | | | 144,995 | |

| | | | | |

| | 35 | | | AT&T, Inc. | | | 4.500% | | | | 5/15/35 | | | | BBB+ | | | | 34,085 | |

| | | | | |

| | 228 | | | AT&T, Inc. | | | 4.300% | | | | 12/15/42 | | | | BBB+ | | | | 209,341 | |

| | | | | |

| | 187 | | | AT&T, Inc. | | | 4.350% | | | | 6/15/45 | | | | BBB+ | | | | 169,419 | |

| | | | | |

| | 44 | | | AutoNation Inc. | | | 4.500% | | | | 10/01/25 | | | | BBB– | | | | 46,603 | |

| | | | | |

| | 66 | | | Baxalta, Inc. | | | 2.875% | | | | 6/23/20 | | | | BBB– | | | | 67,409 | |

| | | | | |

| | 46 | | | Baxalta, Inc. | | | 3.600% | | | | 6/23/22 | | | | BBB– | | | | 47,383 | |

| | | | | |

| | 80 | | | Baxter International Inc. | | | 3.500% | | | | 8/15/46 | | | | BBB+ | | | | 72,102 | |

| | | | | |

| | 128 | | | Becton Dickinson & Company | | | 4.685% | | | | 12/15/44 | | | | BBB | | | | 135,096 | |

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG) (continued)

| | |

| Portfolio of Investments | | July 31, 2017 |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Industrial (continued) | | | | | | | | | | | | |

| | | | | |

| $ | 143 | | | Boardwalk Pipelines LP | | | 3.375% | | | | 2/01/23 | | | | BBB– | | | $ | 142,947 | |

| | | | | |

| | 40 | | | BorgWarner Inc. | | | 3.375% | | | | 3/15/25 | | | | BBB+ | | | | 40,513 | |

| | | | | |

| | 46 | | | BorgWarner Inc. | | | 4.375% | | | | 3/15/45 | | | | BBB+ | | | | 45,994 | |

| | | | | |

| | 64 | | | Buckeye Partners LP | | | 4.150% | | | | 7/01/23 | | | | BBB– | | | | 66,611 | |

| | | | | |

| | 137 | | | Canadian Natural Resources Limited | | | 3.900% | | | | 2/01/25 | | | | BBB | | | | 139,843 | |

| | | | | |

| | 46 | | | Canadian Pacific Railway Company | | | 4.800% | | | | 9/15/35 | | | | BBB+ | | | | 51,472 | |

| | | | | |

| | 120 | | | Cardinal Health Inc. | | | 4.500% | | | | 11/15/44 | | | | BBB+ | | | | 124,947 | |

| | | | | |

| | 54 | | | Celanese US Holdings LLC | | | 5.875% | | | | 6/15/21 | | | | BBB– | | | | 60,518 | |

| | | | | |

| | 46 | | | Celgene Corporation | | | 3.625% | | | | 5/15/24 | | | | BBB | | | | 48,074 | |

| | | | | |

| | 46 | | | Charter Communications Operating Capital Corporation | | | 4.908% | | | | 7/23/25 | | | | BBB– | | | | 49,432 | |

| | | | | |

| | 100 | | | Cimarex Energy Company | | | 4.375% | | | | 6/01/24 | | | | BBB– | | | | 105,867 | |

| | | | | |

| | 42 | | | Coach, Inc. | | | 4.250% | | | | 4/01/25 | | | | BBB– | | | | 43,427 | |

| | | | | |

| | 40 | | | Columbia Pipeline Group, Inc. | | | 5.800% | | | | 6/01/45 | | | | BBB | | | | 47,643 | |

| | | | | |

| | 40 | | | CVS Health Corporation | | | 4.875% | | | | 7/20/35 | | | | BBB+ | | | | 44,453 | |

| | | | | |

| | 46 | | | CVS Health Corporation | | | 5.125% | | | | 7/20/45 | | | | BBB+ | | | | 52,788 | |

| | | | | |

| | 84 | | | Delphi Corporation | | | 4.150% | | | | 3/15/24 | | | | BBB | | | | 88,807 | |

| | | | | |

| | 80 | | | Discovery Communications Inc. | | | 3.250% | | | | 4/01/23 | | | | BBB– | | | | 80,067 | |

| | | | | |

| | 42 | | | Discovery Communications Inc. | | | 4.900% | | | | 3/11/26 | | | | BBB– | | | | 44,862 | |

| | | | | |

| | 40 | | | Eaton Corporation | | | 4.000% | | | | 11/02/32 | | | | BBB+ | | | | 42,116 | |

| | | | | |

| | 46 | | | Eaton Corporation | | | 4.150% | | | | 11/01/42 | | | | BBB+ | | | | 47,413 | |

| | | | | |

| | 160 | | | EcoPetrol SA | | | 4.250% | | | | 9/18/18 | | | | BBB | | | | 163,229 | |

| | | | | |

| | 46 | | | Electronic Arts, Inc. | | | 4.800% | | | | 3/01/26 | | | | BBB | | | | 50,697 | |

| | | | | |

| | 80 | | | Enable Midstream Partners LP | | | 2.400% | | | | 5/15/19 | | | | BBB– | | | | 79,797 | |

| | | | | |

| | 70 | | | Enable Midstream Partners LP | | | 3.900% | | | | 5/15/24 | | | | BBB– | | | | 69,842 | |

| | | | | |

| | 94 | | | Enterprise Products Operating LP | | | 5.750% | | | | 3/01/35 | | | | BBB+ | | | | 106,282 | |

| | | | | |

| | 60 | | | EQT Corporation | | | 6.500% | | | | 4/01/18 | | | | BBB– | | | | 61,765 | |

| | | | | |

| | 60 | | | EQT Corporation | | | 4.875% | | | | 11/15/21 | | | | BBB– | | | | 64,878 | |

| | | | | |

| | 94 | | | FedEx Corporation | | | 3.900% | | | | 2/01/35 | | | | BBB | | | | 94,802 | |

| | | | | |

| | 110 | | | Flowers Foods, Inc. | | | 3.500% | | | | 10/01/26 | | | | BBB | | | | 109,277 | |

| | | | | |

| | 40 | | | Flowserve Corporation | | | 4.000% | | | | 11/15/23 | | | | BBB | | | | 41,527 | |

| | | | | |

| | 60 | | | FMC Corporation | | | 5.200% | | | | 12/15/19 | | | | BBB | | | | 63,812 | |

| | | | | |

| | 44 | | | Ford Motor Company | | | 6.375% | | | | 2/01/29 | | | | BBB | | | | 50,931 | |

| | | | | |

| | 46 | | | Ford Motor Company | | | 4.750% | | | | 1/15/43 | | | | BBB | | | | 44,563 | |

| | | | | |

| | 160 | | | Ford Motor Credit Company | | | 3.664% | | | | 9/08/24 | | | | BBB | | | | 160,518 | |

| | | | | |

| | 42 | | | Fortive Corporation | | | 4.300% | | | | 6/15/46 | | | | BBB | | | | 43,743 | |

| | | | | |

| | 93 | | | General Motors Corporation | | | 6.600% | | | | 4/01/36 | | | | BBB | | | | 109,309 | |

| | | | | |

| | 160 | | | General Motors Financial Company Inc. | | | 5.250% | | | | 3/01/26 | | | | BBB | | | | 173,448 | |

| | | | | |

| | 80 | | | Grupo Televisa SAB | | | 5.000% | | | | 5/13/45 | | | | BBB+ | | | | 79,487 | |

| | | | | |

| | 196 | | | Halliburton Company | | | 3.800% | | | | 11/15/25 | | | | BBB+ | | | | 202,260 | |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Industrial (continued) | | | | | | | | | | | | |

| | | | | |

| $ | 70 | | | Harman International Industries, Inc. | | | 4.150% | | | | 5/15/25 | | | | BBB | | | $ | 72,741 | |

| | | | | |

| | 99 | | | Helmerich and Payne International Drilling Company | | | 4.650% | | | | 3/15/25 | | | | BBB+ | | | | 105,145 | |

| | | | | |

| | 80 | | | Interpublic Group of Companies Inc. | | | 3.750% | | | | 2/15/23 | | | | BBB | | | | 83,232 | |

| | | | | |

| | 40 | | | Johnson Controls International PLC | | | 4.625% | | | | 7/02/44 | | | | BBB+ | | | | 42,683 | |

| | | | | |

| | 40 | | | Johnson Controls International PLC | | | 5.125% | | | | 9/14/45 | | | | BBB+ | | | | 46,290 | |

| | | | | |

| | 60 | | | Kennametal Inc. | | | 2.650% | | | | 11/01/19 | | | | BBB– | | | | 60,613 | |

| | | | | |

| | 39 | | | Kennametal Inc. | | | 3.875% | | | | 2/15/22 | | | | BBB– | | | | 40,058 | |

| | | | | |

| | 40 | | | Kohl’s Corporation | | | 4.250% | | | | 7/17/25 | | | | BBB | | | | 39,989 | |

| | | | | |

| | 46 | | | Kraft Heinz Foods Company | | | 5.000% | | | | 7/15/35 | | | | BBB– | | | | 49,790 | |

| | | | | |

| | 94 | | | Lockheed Martin Corporation | | | 3.600% | | | | 3/01/35 | | | | BBB+ | | | | 92,557 | |

| | | | | |

| | 42 | | | Macy’s Retail Holdings Inc. | | | 6.650% | | | | 7/15/24 | | | | BBB– | | | | 46,167 | |

| | | | | |

| | 39 | | | Magellan Midstream Partners LP | | | 4.200% | | | | 3/15/45 | | | | BBB+ | | | | 36,849 | |

| | | | | |

| | 167 | | | Marathon Oil Corporation | | | 2.700% | | | | 6/01/20 | | | | BBB– | | | | 166,392 | |

| | | | | |

| | 94 | | | Marathon Petroleum Corporation | | | 3.625% | | | | 9/15/24 | | | | BBB | | | | 95,642 | |

| | | | | |

| | 46 | | | Marriott International, Inc. | | | 4.500% | | | | 10/01/34 | | | | BBB | | | | 48,359 | |

| | | | | |

| | 20 | | | Martin Marietta Materials | | | 6.600% | | | | 4/15/18 | | | | BBB | | | | 20,655 | |

| | | | | |

| | 48 | | | McDonald’s Corporation | | | 4.700% | | | | 12/09/35 | | | | BBB+ | | | | 53,230 | |

| | | | | |

| | 88 | | | McDonald’s Corporation | | | 4.875% | | | | 7/15/40 | | | | BBB+ | | | | 96,972 | |

| | | | | |

| | 44 | | | McKesson Corporation | | | 4.883% | | | | 3/15/44 | | | | BBB+ | | | | 49,505 | |

| | | | | |

| | 200 | | | MPLX LP | | | 4.500% | | | | 7/15/23 | | | | BBB– | | | | 213,313 | |

| | | | | |

| | 74 | | | Mylan Inc. | | | 3.150% | | | | 6/15/21 | | | | BBB– | | | | 75,566 | |

| | | | | |

| | 80 | | | National Fuel Gas Company | | | 8.750% | | | | 5/01/19 | | | | BBB | | | | 88,356 | |

| | | | | |

| | 88 | | | National Oilwell Varco inc. | | | 2.600% | | | | 12/01/22 | | | | BBB+ | | | | 85,864 | |

| | | | | |

| | 40 | | | Newell Brands Inc. | | | 5.000% | | | | 11/15/23 | | | | BBB– | | | | 42,893 | |

| | | | | |

| | 46 | | | Newell Brands Inc. | | | 5.375% | | | | 4/01/36 | | | | BBB– | | | | 53,683 | |

| | | | | |

| | 64 | | | Newmont Mining Corporation | | | 3.500% | | | | 3/15/22 | | | | BBB | | | | 66,514 | |

| | | | | |

| | 64 | | | Noble Energy Inc. | | | 3.900% | | | | 11/15/24 | | | | BBB– | | | | 65,802 | |

| | | | | |

| | 35 | | | Nordstrom, Inc. | | | 6.950% | | | | 3/15/28 | | | | BBB+ | | | | 39,020 | |

| | | | | |

| | 57 | | | Northern Border Pipeline Company | | | 7.500% | | | | 9/15/21 | | | | BBB+ | | | | 65,801 | |

| | | | | |

| | 100 | | | Nucor Corporation | | | 4.125% | | | | 9/15/22 | | | | BBB+ | | | | 107,244 | |

| | | | | |

| | 60 | | | Oceaneering International, Inc. | | | 4.650% | | | | 11/15/24 | | | | BBB– | | | | 59,329 | |

| | | | | |

| | 46 | | | Orange SA | | | 5.375% | | | | 1/13/42 | | | | BBB+ | | | | 53,815 | |

| | | | | |

| | 42 | | | Owens and Minor, Inc. | | | 4.375% | | | | 12/15/24 | | | | BBB– | | | | 42,765 | |

| | | | | |

| | 80 | | | Perrigo Finance Unlimited Company | | | 3.500% | | | | 3/15/21 | | | | BBB– | | | | 82,520 | |

| | | | | |

| | 315 | | | Petroleos Mexicanos | | | 6.000% | | | | 3/05/20 | | | | BBB | | | | 339,772 | |

| | | | | |

| | 70 | | | Phillips 66 | | | 4.650% | | | | 11/15/34 | | | | BBB+ | | | | 74,176 | |

| | | | | |

| | 60 | | | Pioneer Natural Resources Company | | | 3.950% | | | | 7/15/22 | | | | BBB | | | | 63,203 | |

| | | | | |

| | 70 | | | Pioneer Natural Resources Company | | | 4.450% | | | | 1/15/26 | | | | BBB | | | | 75,156 | |

| | | | | |

| | 80 | | | Qwest Corp. | | | 6.875% | | | | 9/15/33 | | | | BBB– | | | | 79,168 | |

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG) (continued)

| | |

| Portfolio of Investments | | July 31, 2017 |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Industrial (continued) | | | | | | | | | | | | |

| | | | | |

| $ | 59 | | | Qwest Corporation | | | 7.125% | | | | 11/15/43 | | | | BBB– | | | $ | 58,484 | |

| | | | | |

| | 52 | | | Rayonier, Inc. | | | 3.750% | | | | 4/01/22 | | | | BBB– | | | | 52,570 | |

| | | | | |

| | 70 | | | Reliance Steel and Aluminum Co | | | 4.500% | | | | 4/15/23 | | | | BBB | | | | 74,435 | |

| | | | | |

| | 46 | | | Reynolds American Inc. | | | 5.700% | | | | 8/15/35 | | | | BBB | | | | 54,802 | |

| | | | | |

| | 126 | | | Rogers Communications Inc. | | | 5.000% | | | | 3/15/44 | | | | BBB+ | | | | 143,134 | |

| | | | | |

| | 88 | | | RPM International, Inc. | | | 6.125% | | | | 10/15/19 | | | | BBB | | | | 95,329 | |

| | | | | |

| | 79 | | | Scripps Networks Interactive Inc. | | | 3.900% | | | | 11/15/24 | | | | BBB | | | | 81,089 | |

| | | | | |

| | 40 | | | Signet UK Finance PLC | | | 4.700% | | | | 6/15/24 | | | | BB+ | | | | 39,351 | |

| | | | | |

| | 80 | | | Spectra Energy Partners LP | | | 4.500% | | | | 3/15/45 | | | | BBB | | | | 78,787 | |

| | | | | |

| | 100 | | | Stanley Black & Decker Inc. | | | 5.750% | | | | 12/15/53 | | | | BBB | | | | 105,066 | |

| | | | | |

| | 44 | | | Sysco Corporation | | | 5.375% | | | | 9/21/35 | | | | BBB+ | | | | 51,358 | |

| | | | | |

| | 110 | | | Talisman Energy Inc. | | | 7.750% | | | | 6/01/19 | | | | BBB | | | | 120,031 | |

| | | | | |

| | 96 | | | TC Pipelines LP | | | 4.650% | | | | 6/15/21 | | | | BBB– | | | | 101,855 | |

| | | | | |

| | 119 | | | TechnipFMC PLC, 144A | | | 3.450% | | | | 10/01/22 | | | | BBB | | | | 118,765 | |

| | | | | |

| | 44 | | | The JM Smucker Company | | | 4.250% | | | | 3/15/35 | | | | BBB | | | | 46,129 | |

| | | | | |

| | 46 | | | Thermo Fischer Scientific Inc. | | | 5.300% | | | | 2/01/44 | | | | BBB | | | | 54,085 | |

| | | | | |

| | 44 | | | Tyson Foods | | | 4.875% | | | | 8/15/34 | | | | BBB | | | | 48,161 | |

| | | | | |

| | 161 | | | Valero Energy Corporation | | | 3.650% | | | | 3/15/25 | | | | BBB | | | | 165,389 | |

| | | | | |

| | 88 | | | Valmont Industries, Inc. | | | 6.625% | | | | 4/20/20 | | | | BBB | | | | 97,209 | |

| | | | | |

| | 160 | | | Verizon Communications | | | 4.400% | | | | 11/01/34 | | | | BBB+ | | | | 157,140 | |

| | | | | |

| | 94 | | | Verizon Communications | | | 4.750% | | | | 11/01/41 | | | | BBB+ | | | | 92,171 | |

| | | | | |

| | 139 | | | Verizon Communications | | | 4.125% | | | | 8/15/46 | | | | BBB+ | | | | 122,906 | |

| | | | | |

| | 127 | | | Viacom Inc. | | | 4.250% | | | | 9/01/23 | | | | BBB- | | | | 132,009 | |

| | | | | |

| | 41 | | | Walgreen Company | | | 4.400% | | | | 9/15/42 | | | | BBB | | | | 41,385 | |

| | | | | |

| | 40 | | | Walgreens Boots Alliance, Inc. | | | 4.500% | | | | 11/18/34 | | | | BBB | | | | 41,633 | |

| | | | | |

| | 41 | | | Waste Management Inc. | | | 3.900% | | | | 3/01/35 | | | | BBB+ | | | | 42,223 | |

| | | | | |

| | 79 | | | Western Gas Partners LP | | | 4.000% | | | | 7/01/22 | | | | BBB– | | | | 81,499 | |

| | | | | |

| | 40 | | | Worthington Industries, Inc. | | | 4.550% | | | | 4/15/26 | | | | BBB– | | | | 41,384 | |

| | | | | |

| | 40 | | | Zimmer Biomet Holdings, Inc. | | | 4.250% | | | | 8/15/35 | | | | BBB– | | | | 39,422 | |

| | | | | |

| | 40 | | | Zimmer Biomet Holdings, Inc. | | | 5.750% | | | | 11/30/39 | | | | BBB– | | | | 46,978 | |

| | 9,227 | | | Total Industrial | | | | | | | | | | | | | | | 9,592,465 | |

| | | | | |

| | | | Utility - 7.9% | | | | | | | | | | | | |

| | | | | |

| | 84 | | | Appalachian Power Company | | | 5.800% | | | | 10/01/35 | | | | BBB+ | | | | 100,922 | |

| | | | | |

| | 46 | | | Appalachian Power Company | | | 4.400% | | | | 5/15/44 | | | | BBB+ | | | | 48,953 | |

| | | | | |

| | 80 | | | Black Hills Corporation | | | 3.150% | | | | 1/15/27 | | | | BBB | | | | 77,870 | |

| | | | | |

| | 40 | | | Black Hills Corporation | | | 4.200% | | | | 9/15/46 | | | | BBB | | | | 39,125 | |

| | | | | |

| | 64 | | | Cleco Corporate Holdings LLC | | | 3.743% | | | | 5/01/26 | | | | BBB– | | | | 64,932 | |

| | | | | |

| | 80 | | | CMS Energy Corporation | | | 4.700% | | | | 3/31/43 | | | | BBB | | | | 86,791 | |

| | | | | |

| | 72 | | | Dominion Resources Inc. | | | 5.250% | | | | 8/01/33 | | | | BBB | | | | 82,095 | |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Utility (continued) | | | | | | | | | | | | |

| | | | | |

| $ | 147 | | | Dominion Resources Inc. | | | 4.700% | | | | 12/01/44 | | | | BBB | | | $ | 159,481 | |

| | | | | |

| | 400 | | | DTE Electric, (WI/DD) | | | 3.750% | | | | 8/15/47 | | | | A+ | | | | 399,784 | |

| | | | | |

| | 197 | | | Duke Energy Corporation | | | 2.650% | | | | 9/01/26 | | | | BBB+ | | | | 190,610 | |

| | | | | |

| | 115 | | | Duke Energy Corporation | | | 3.750% | | | | 9/01/46 | | | | BBB+ | | | | 111,605 | |

| | | | | |

| | 88 | | | Edison International | | | 2.950% | | | | 3/15/23 | | | | BBB+ | | | | 88,798 | |

| | | | | |

| | 80 | | | El Paso Electric Company | | | 5.000% | | | | 12/01/44 | | | | BBB | | | | 86,878 | |

| | | | | |

| | 44 | | | Emera US Finance LP | | | 3.550% | | | | 6/15/26 | | | | BBB– | | | | 44,623 | |

| | | | | |

| | 46 | | | Emera US Finance LP | | | 4.750% | | | | 6/15/46 | | | | BBB– | | | | 49,272 | |

| | | | | |

| | 88 | | | Entergy Corporation | | | 2.950% | | | | 9/01/26 | | | | BBB | | | | 85,478 | |

| | | | | |

| | 139 | | | Exelon Corporation | | | 4.950% | | | | 6/15/35 | | | | BBB | | | | 151,870 | |

| | | | | |

| | 94 | | | Exelon Corporation | | | 4.450% | | | | 4/15/46 | | | | BBB | | | | 97,468 | |

| | | | | |

| | 80 | | | Indiana Michigan Power Company | | | 3.200% | | | | 3/15/23 | | | | BBB+ | | | | 81,830 | |

| | | | | |

| | 100 | | | Indiana Michigan Power Company | | | 3.750% | | | | 7/01/47 | | | | BBB+ | | | | 98,756 | |

| | | | | |

| | 46 | | | Interstate Power And Light Company | | | 4.700% | | | | 10/15/43 | | | | BBB+ | | | | 50,507 | |

| | | | | |

| | 120 | | | ITC Holdings Corp. | | | 3.250% | | | | 6/30/26 | | | | BBB | | | | 119,370 | |

| | | | | |

| | 40 | | | ITC Holdings Corp. | | | 5.300% | | | | 7/01/43 | | | | BBB | | | | 46,195 | |

| | | | | |

| | 55 | | | John Sevier Combined Cycle Generation LLC | | | 4.626% | | | | 1/15/42 | | | | AA | | | | 60,417 | |

| | | | | |

| | 46 | | | Kansas City Power and Light Co | | | 5.300% | | | | 10/01/41 | | | | BBB+ | | | | 53,519 | |

| | | | | |

| | 107 | | | Kansas City Power and Light Co | | | 4.200% | | | | 6/15/47 | | | | BBB+ | | | | 109,629 | |

| | | | | |

| | 64 | | | KeySpan Corporation | | | 5.803% | | | | 4/01/35 | | | | BBB+ | | | | 77,594 | |

| | | | | |

| | 140 | | | National Rural Utilities Cooperative Finance Corporation | | | 2.850% | | | | 1/27/25 | | | | A+ | | | | 139,598 | |

| | | | | |

| | 72 | | | NiSource Finance Corporation | | | 5.250% | | | | 2/15/43 | | | | BBB | | | | 82,996 | |

| | | | | |

| | 72 | | | NiSource Finance Corporation | | | 4.800% | | | | 2/15/44 | | | | BBB | | | | 79,091 | |

| | | | | |

| | 94 | | | PPL Capital Funding Inc. | | | 4.700% | | | | 6/01/43 | | | | BBB | | | | 100,469 | |

| | | | | |

| | 62 | | | PSE&G Power LLC | | | 4.300% | | | | 11/15/23 | | | | BBB+ | | | | 65,593 | |

| | | | | |

| | 250 | | | Public Service of Colorado | | | 3.800% | | | | 6/15/47 | | | | A+ | | | | 252,090 | |

| | | | | |

| | 60 | | | Public Service Company of New Mexico | | | 3.850% | | | | 8/01/25 | | | | BBB | | | | 61,909 | |

| | | | | |

| | 66 | | | Puget Energy, Inc. | | | 3.650% | | | | 5/15/25 | | | | BBB– | | | | 66,073 | |

| | | | | |

| | 66 | | | SCANA Corporation | | | 4.125% | | | | 2/01/22 | | | | BBB– | | | | 68,634 | |

| | | | | |

| | 77 | | | Southaven Combined Cycle Generation LLC | | | 3.846% | | | | 8/15/33 | | | | AA | | | | 78,002 | |

| | | | | |

| | 188 | | | Southern Company Gas Capital Corporation | | | 4.400% | | | | 6/01/43 | | | | BBB+ | | | | 193,443 | |

| | | | | |

| | 60 | | | Spire, Inc. | | | 4.700% | | | | 8/15/44 | | | | BBB | | | | 61,098 | |

| | | | | |

| | 130 | | | The Southern Company | | | 4.250% | | | | 7/01/36 | | | | BBB+ | | | | 134,577 | |

| | | | | |

| | 46 | | | The Southern Company | | | 4.400% | | | | 7/01/46 | | | | BBB+ | | | | 47,963 | |

| | | | | |

| | 70 | | | TransAlta Corporation | | | 4.500% | | | | 11/15/22 | | | | BBB– | | | | 70,525 | |

| | | | | |

| | 44 | | | Tucson Electric Power Company | | | 3.050% | | | | 3/15/25 | | | | A– | | | | 43,163 | |

| | | | | |

| | 46 | | | Xcel Energy Inc. | | | 4.800% | | | | 9/15/41 | | | | BBB+ | | | | 50,831 | |

| | 4,105 | | | Total Utility | | | | | | | | | | | | | | | 4,260,427 | |

| $ | 18,517 | | | Total Corporate Debt (cost $19,330,971) | | | | | | | | | | | | | | | 19,240,458 | |

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG) (continued)

| | |

| Portfolio of Investments | | July 31, 2017 |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | GOVERNMENT RELATED – 3.4% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | Sovereign Debt – 1.7% | | | | | | | | | | | | |

| | | | | |

| $ | 60 | | | Republic of Chile | | | 3.625% | | | | 10/30/42 | | | | A+ | | | $ | 59,634 | |

| | | | | |

| | 120 | | | Republic of Colombia | | | 6.125% | | | | 1/18/41 | | | | BBB | | | | 138,960 | |

| | | | | |

| | 40 | | | Republic of Italy | | | 5.375% | | | | 6/15/33 | | | | BBB | | | | 45,588 | |

| | | | | |

| | 60 | | | Republic of Panama | | | 4.300% | | | | 4/29/53 | | | | BBB | | | | 59,850 | |

| | | | | |

| | 139 | | | Republic of Peru | | | 4.125% | | | | 8/25/27 | | | | BBB+ | | | | 151,927 | |

| | | | | |

| | 100 | | | Republic of Uruguay | | | 5.100% | | | | 6/18/50 | | | | BBB | | | | 103,250 | |

| | | | | |

| | 192 | | | United Mexican States | | | 4.750% | | | | 3/08/44 | | | | BBB+ | | | | 194,304 | |

| | | | | |

| | 160 | | | United Mexican States | | | 4.350% | | | | 1/15/47 | | | | BBB+ | | | | 152,960 | |

| | 871 | | | Total Sovereign Debt | | | | | | | | | | | | | | | 906,473 | |

| | | | | |

| | | | Municipal Bonds – 1.2% (3) | | | | | | | | | | | | |

| | | | | |

| | 60 | | | Board of Regents of the University of Texas System, Revenue Financing System Bonds, Green Series 2016A (No Optional Call) | | | 3.852% | | | | 8/15/46 | | | | AAA | | | | 63,944 | |

| | | | | |

| | 88 | | | California State, General Obligation Bonds, Various Purpose Build America Taxable Bond Series 2010 (Optional Call: 3/20 at 100.00) | | | 7.950% | | | | 3/01/36 | | | | AA– | | | | 100,747 | |

| | | | | |

| | 60 | | | Missouri Health and Educational Facilities Authority, Revenue Bonds, Washington University, Series 2016B (No Optional Call) | | | 3.086% | | | | 9/15/51 | | | | AA+ | | | | 52,998 | |

| | | | | |

| | 80 | | | New Jersey Transportation Trust Fund Authority, Transportation System Bonds, Build America Bonds Issuer Subsidy Program, Series 2009B (Optional Call: 6/19 at 100.00) | | | 6.875% | | | | 12/15/39 | | | | BBB+ | | | | 83,994 | |

| | | | | |

| | 96 | | | New Jersey Transportation Trust Fund Authority, Transportation System Bonds, Build America Bonds Issuer Subsidy Program, Series 2010C (Optional Call: 12/20 at 100.00) | | | 6.104% | | | | 12/15/28 | | | | BBB+ | | | | 101,346 | |

| | | | | |

| | 40 | | | Ohio State University, General Receipts Bonds, Multiyear Debt Issuance Program, Refunding Series 2016A (No Optional Call) | | | 3.798% | | | | 12/01/46 | | | | AA | | | | 41,059 | |

| | | | | |

| | 110 | | | Phoenix, Arizona, Various Purpose General Obligation Bonds, Build America Taxable Bonds, Series 2009A (No Optional Call) | | | 5.269% | | | | 7/01/34 | | | | AA+ | | | | 131,517 | |

| | | | | |

| | 71 | | | Texas State, General Obligation Bonds, Transportation Commission, Build America Taxable Bonds, Series 2010A (No Optional Call) | | | 4.631% | | | | 4/01/33 | | | | AAA | | | | 80,808 | |

| | 605 | | | Total Municipal Bonds | | | | | | | | | | | | | | | 656,413 | |

| | | | | |

| | | | Government Agency – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 127 | | | Inter-American Development Bank | | | 3.200% | | | | 8/07/42 | | | | AAA | | | | 125,135 | |

| | | | | |

| | 120 | | | Tennessee Valley Authority | | | 3.500% | | | | 12/15/42 | | | | AAA | | | | 124,101 | |

| | 247 | | | Total Government Agency | | | | | | | | | | | | | | | 249,236 | |

| $ | 1,723 | | | Total Government Related (cost $1,869,499) | | | | | | | | | | | | | | | 1,812,122 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | U.S. TREASURY – 20.2% | | | | | | | | | | | | |

| | | | | |

| $ | 2,724 | | | U.S. Treasury Notes | | | 0.750% | | | | 8/15/19 | | | | AAA | | | $ | 2,690,269 | |

| | | | | |

| | 707 | | | U.S. Treasury Notes | | | 0.875% | | | | 9/15/19 | | | | AAA | | | | 699,709 | |

| | | | | |

| | 300 | | | U.S. Treasury Notes | | | 2.000% | | | | 12/31/21 | | | | AAA | | | | 302,836 | |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | U.S. TREASURY (continued) | | | | | | | | | | | | |

| | | | | |

| $ | 1,060 | | | U.S. Treasury Notes | | | 2.750% | | | | 11/15/23 | | | | AAA | | | $ | 1,105,919 | |

| | | | | |

| | 945 | | | U.S. Treasury Notes | | | 2.250% | | | | 11/15/24 | | | | AAA | | | | 952,309 | |

| | | | | |

| | 1,688 | | | U.S. Treasury Notes | | | 2.000% | | | | 8/15/25 | | | | AAA | | | | 1,662,943 | |

| | | | | |

| | 1,948 | | | U.S. Treasury Notes | | | 2.250% | | | | 2/15/27 | | | | AAA | | | | 1,941,685 | |

| | | | | |

| | 1,550 | | | U.S. Treasury Notes | | | 2.375% | | | | 5/15/27 | | | | AAA | | | | 1,561,079 | |

| $ | 10,922 | | | Total U.S. Treasury (cost $11,081,208) | | | | | | | | | | | | | | | 10,916,749 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | SECURITIZED – 40.0% | | | | | | | | | | | | |

| | | | | |

| $ | 600 | | | Commercial Mortgage Pass-Through Certificates, Series 2015-LC19 | | | 3.527% | | | | 2/10/48 | | | | AA+ | | | $ | 614,190 | |

| | | | | |

| | 500 | | | CSAIL Commercial Mortgage Trust, Commercial Mortgage Pass-Through Certificates, Series 2015-C2 | | | 3.849% | | | | 6/15/57 | | | | Aa2 | | | | 520,565 | |

| | | | | |

| | 1,151 | | | Fannie Mae Mortgage Pool AL9125 | | | 4.000% | | | | 10/01/43 | | | | AAA | | | | 1,215,807 | |

| | | | | |

| | 2,117 | | | Fannie Mae Mortgage Pool AS6302 | | | 3.500% | | | | 12/01/45 | | | | AAA | | | | 2,180,943 | |

| | | | | |

| | 1,160 | | | Fannie Mae Mortgage Pool AX4887 | | | 4.000% | | | | 12/01/44 | | | | AAA | | | | 1,222,046 | |

| | | | | |

| | 2,100 | | | Fannie Mae Mortgage Pool MA1489 | | | 3.000% | | | | 7/01/43 | | | | AAA | | | | 2,114,003 | |

| | | | | |

| | 1,309 | | | Fannie Mae Mortgage Pool MA2671 | | | 3.500% | | | | 7/01/46 | | | | AAA | | | | 1,348,172 | |

| | | | | |

| | 3,602 | | | Fannie Mae Mortgage Pool MA2929 | | | 3.500% | | | | 3/01/47 | | | | AAA | | | | 3,711,230 | |

| | | | | |

| | 2,439 | | | Ginnie Mae Mortgage Pool MA2149 | | | 4.000% | | | | 8/20/44 | | | | AAA | | | | 2,580,227 | |

| | | | | |

| | 1,549 | | | Ginnie Mae Mortgage Pool MA3311 | | | 4.000% | | | | 12/20/45 | | | | AAA | | | | 1,631,063 | |

| | | | | |

| | 1,003 | | | Ginnie Mae Mortgage Pool MA3310 | | | 3.500% | | | | 12/20/45 | | | | AAA | | | | 1,043,983 | |

| | | | | |

| | 360 | | | Ginnie Mae Mortgage Pool MA3874 | | | 3.500% | | | | 8/20/46 | | | | AAA | | | | 373,940 | |

| | | | | |

| | 1,977 | | | Ginnie Mae Mortgage Pool MA3937 | | | 3.500% | | | | 9/20/46 | | | | AAA | | | | 2,056,916 | |

| | | | | |

| | 500 | | | Wells Fargo Commercial Mortgage Trust, Commercial Mortgage-Pass-Through Certificates, Series 2014-LC16 | | | 4.020% | | | | 8/15/50 | | | | Aaa | | | | 527,310 | |

| | | | | |

| | 500 | | | World Financial Network Credit Card Master Trust, Series 2012-A | | | 3.140% | | | | 1/15/23 | | | | AAA | | | | 510,684 | |

| $ | 20,867 | | | Total Securitized (cost $21,952,966) | | | | | | | | | | | | | | | 21,651,079 | |

| | | | Total Long-Term Investments (cost $54,234,644) | | | | | | | | | | | | | | | 53,620,408 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | SHORT-TERM INVESTMENTS – 1.0% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | GOVERNMENT RELATED – 1.0% | | | | | | | | | | | | |

| | | | | |

| $ | 550 | | | Federal Farm Credit Bank, Discount Notes | | | 0.000% | | | | 8/01/17 | | | | N/R | | | $ | 550,000 | |

| $ | 550 | | | Total Short-Term Investments (cost $550,000) | | | | | | | | | | | | | | | 550,000 | |

| | | | Total Investments (cost $54,784,644) – 100.1% | | | | | | | | | | | | | | | 54,170,408 | |

| | | | Other Assets Less Liabilities – (0.1)% | | | | | | | | | | | | | | | (35,695) | |

| | | | Net Assets – 100% | | | | | | | | | | | | | | $ | 54,134,713 | |

NuShares Enhanced Yield U.S. Aggregate Bond ETF (NUAG) (continued)

| | |

| Portfolio of Investments | | July 31, 2017 |

For Fund portfolio compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications into sectors for reporting ease.

| (1) | All percentages shown in the Portfolio of Investments are based on net assets. |

| (2) | The ratings disclosed reflects net exposure to credit ratings by one or more of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). If there are multiple ratings for a security, the average rating is used, with evenly split ratings being rounded down to the lower rating, which is the method used by the Index. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies. Ratings are not covered by the report of independent registered public accounting firm. |

| (3) | Optional Call Provisions: Dates (month and year) and prices of the earliest optional call or redemption. There may be other call provisions at varying prices at later dates. Certain mortgage-backed securities may be subject to periodic principal paydowns. Optional Call Provisions are not covered by the report of independent registered public accounting firm. |

| 144A | Investment is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These investments may only be resold in transactions exempt from registration, which are normally those transactions with qualified institutional buyers. |

| REIT | Real Estate Investment Trust |

| (WI/DD) | Investment, or portion of investment, purchased on a when-issued or delayed delivery basis. |

See accompanying notes to financial statements.

NuShares Enhanced Yield 1-5 Year U.S. Aggregate Bond ETF (NUSA)

| | |

| Portfolio of Investments | | July 31, 2017 |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | LONG-TERM INVESTMENTS – 98.5% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | CORPORATE DEBT – 51.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | Financials – 31.9% | | | | | | | | | | | | |

| | | | | |

| $ | 168 | | | Air Lease Corporation | | | 4.750% | | | | 3/01/20 | | | | BBB | | | $ | 178,597 | |

| | | | | |

| | 72 | | | Allied World Assurance Holdings Limited | | | 5.500% | | | | 11/15/20 | | | | BBB | | | | 78,266 | |

| | | | | |

| | 240 | | | American Express Credit Corporation | | | 2.250% | | | | 5/05/21 | | | | A | | | | 240,396 | |

| | | | | |

| | 348 | | | American International Group, Inc. | | | 3.375% | | | | 8/15/20 | | | | BBB+ | | | | 360,370 | |

| | | | | |

| | 84 | | | Ameriprise Financial, Inc. | | | 5.300% | | | | 3/15/20 | | | | A– | | | | 90,953 | |

| | | | | |

| | 120 | | | Ares Capital Corporation | | | 4.875% | | | | 11/30/18 | | | | BBB | | | | 124,297 | |

| | | | | |

| | 204 | | | Associates Corporation of North America | | | 6.950% | | | | 11/01/18 | | | | A– | | | | 216,598 | |

| | | | | |

| | 324 | | | Bank of America Corporation | | | 2.250% | | | | 4/21/20 | | | | A– | | | | 325,412 | |

| | | | | |

| | 204 | | | Bank of America Corporation | | | 5.000% | | | | 5/13/21 | | | | A– | | | | 223,104 | |

| | | | | |

| | 84 | | | Bank of New York Mellon | | | 2.600% | | | | 2/07/22 | | | | A+ | | | | 84,773 | |

| | | | | |

| | 180 | | | BB&T Corporation | | | 2.050% | | | | 5/10/21 | | | | A | | | | 179,310 | |

| | | | | |