Table of Contents

As filed with the Securities and Exchange Commission on June 30, 2021

Registration No. 333-256165

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ROIVANT SCIENCES LTD.

(Exact Name of Registrant as Specified in Its Charter)

| Bermuda | 2834 | 98-1173944 | ||

| (State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

Suite 1, 3rd Floor

11-12 St. James’s Square

London SW1Y 4LB

United Kingdom

Telephone: +44 207 400 3347

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Copies to:

Derek J. Dostal Lee Hochbaum Brian Wolfe Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 | Sophia Hudson, P.C. Tamar Donikyan Alla Digilova Kirkland & Ellis LLP 601 Lexington Avenue New York, New York 10022 (212) 446-4800 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective and all other conditions to the business combination described in the enclosed proxy statement/prospectus have been satisfied or waived.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, as amended (the “Securities Act”), check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Securities Exchange Act of 1934 as amended (the “Exchange Act”).

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☒ | |||

| Emerging Growth Company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☒

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-l(d) (Cross-Border Third-Party Tender Offer) ☐

CALCULATION OF REGISTRATION FEE

| ||||||||

| Title of Each Class of Securities to be Registered | Amount to be Registered(1)(2) | Proposed Maximum Offering Price Per Unit(2)(3) | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee(4) | ||||

Roivant Common Shares(5) | 51,339,779 | $9.89 | $507,750,414.31 | $55,395.57 | ||||

Warrants to purchase Roivant Common Shares(6) | 30,750,276 | $12.825 | $394,372,289.70 | $43,026.02 | ||||

Total | $902,122,704.01 | $98,421.59(7) | ||||||

| ||||||||

| ||||||||

| (1) | The number of common shares, par value $0.000000007 per share (“Roivant Common Shares”), of Roivant Sciences Ltd. (“Roivant”) and Roivant Common Shares issuable upon the exercise of warrants to purchase Roivant Common Shares (“Roivant Warrants”) being registered is based upon an estimate of the sum of (a) the maximum number of shares of Class A common stock, par value $0.0001 per share (“MAAC Class A Shares”), of Montes Archimedes Acquisition Corp. (“MAAC”) that will be outstanding immediately prior to the Business Combination (as defined herein) and exchanged for an equal number of Roivant Common Shares (including the maximum number of shares of Class B common stock, par value $0.0001 per share (“MAAC Class B Shares” and, together with the MAAC Class A Shares, the “MAAC Shares”), of MAAC that will be converted to MAAC Class A Shares immediately prior to the Business Combination); and (b) the maximum number of MAAC Class A Shares underlying each warrant of MAAC entitling the holder to purchase one MAAC Class A Share per warrant at a price of $11.50 per share (“MAAC Warrants”), which will be assumed by Roivant and will become Roivant Warrants. |

| (2) | Pursuant to Rule 416(a), there are also being registered an indeterminable number of additional securities as may be issued to prevent dilution resulting from stock splits, stock dividends or similar transactions. |

| (3) | In accordance with Rule 457(f)(1) and Rule 457(c), as applicable, based on (i) in respect of Roivant Common Shares issued to MAAC securityholders, the average of the high ($9.90) and low ($9.88) prices of the MAAC Class A Shares on the Nasdaq Stock Market LLC (“Nasdaq”) on May 12, 2021 and (ii) in respect of Roivant Common Shares underlying Roivant Warrants issued to MAAC security holders, the sum of (a) the average of the high ($1.40) and low ($1.25) prices of the MAAC Warrants on Nasdaq on May 12, 2021 and (b) $11.50, the exercise price of the MAAC Warrants, resulting in a combined maximum offering price per warrant of $12.825. The maximum number of Roivant Common Shares issuable upon exercise of the Roivant Warrants are being simultaneously registered hereunder. Consistent with the response to Question 240.06 of the Securities Act Rules Compliance and Disclosure Interpretations, the registration fee with respect to the Roivant Warrants has been allocated to the underlying Roivant Common Shares and those Roivant Common Shares are included in the registration fee. |

| (4) | Determined in accordance with Section 6(b) of the Securities Act at a rate equal to $109.10 per $1,000,000 of the proposed maximum aggregate offering price. |

| (5) | Represents Roivant Common Shares issuable in exchange for outstanding MAAC Shares upon the merger of Rhine Merger Sub, Inc., a wholly owned subsidiary of Roivant, with and into MAAC pursuant to the Business Combination. |

| (6) | Represents Roivant Common Shares underlying Roivant Warrants. |

| (7) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary proxy statement/prospectus is not complete and may be changed. The registrant may not sell the securities described in this preliminary proxy statement/prospectus until the registration statement filed with the Securities and Exchange Commission is declared effective. This preliminary proxy statement/prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY—SUBJECT TO COMPLETION, DATED JUNE 30, 2021

Montes Archimedes Acquisition Corp.

724 Oak Grove Ave, Suite 130

Menlo Park, CA 94025

Dear Montes Archimedes Acquisition Corp. stockholders:

You are cordially invited to attend the special meeting (the “MAAC Special Meeting”) of Montes Archimedes Acquisition Corporation, a Delaware corporation (“MAAC”), at a.m., Eastern Time, on , 2021, unless postponed or adjourned to a later date or time. In light of the novel coronavirus disease (referred to as “COVID-19”) pandemic and to support the well-being of MAAC’s stockholders and employees, the MAAC Special Meeting will be completely virtual. All MAAC stockholders as of the record date, or their duly appointed proxies, may attend the MAAC Special Meeting virtually. Registration will begin at Eastern Time.

At the MAAC Special Meeting, MAAC stockholders are being asked to consider and vote upon a proposal, which is referred to herein as the “Business Combination Proposal,” to approve and adopt the Business Combination Agreement, dated as of May 1, 2021 (as amended on June 9, 2021 to reflect the execution of the lock-up agreements entered into by MAAC’s independent directors and Roivant Sciences Ltd., a Bermuda exempted limited company (“Roivant”), and as may be further amended, supplemented or otherwise modified from time to time, the “Business Combination Agreement”; the Business Combination Agreement and the transactions contemplated thereby, collectively, the “Business Combination”) among MAAC, Roivant and Rhine Merger Sub, Inc., a Delaware corporation (“Merger Sub”), a copy of which is attached to the accompanying proxy statement/prospectus as Annex A. The Business Combination will not occur unless MAAC stockholders approve the Business Combination Proposal. In connection with the Business Combination, outstanding shares and warrants of MAAC will be automatically canceled and extinguished and converted into shares and warrants of Roivant that are expected to be listed on Nasdaq under the new ticker symbols “ROIV” and “ROIVW,” in each case in accordance with the terms of the Business Combination Agreement.

In addition, MAAC and Roivant entered into subscription agreements (collectively, the “Subscription Agreements”) with certain institutional and accredited investors (collectively, the “PIPE Investors”), pursuant to which PIPE Investors agreed to subscribe for and purchase, and MAAC agreed to issue and sell to PIPE Investors, prior to and substantially concurrently with the closing of the Business Combination (the “Closing”), an aggregate of 22,000,000 MAAC Class A Shares at a purchase price of $10.00 per share, for aggregate gross proceeds of $220,000,000 (the “PIPE Financing”). The MAAC Class A Shares to be offered and sold pursuant to the Subscription Agreements and the Roivant Common Shares into which such MAAC Class A Shares are converted in connection with the Merger have not been registered under the Securities Act of 1933, as amended (the “Securities Act”), in reliance upon the exemption provided in Section 4(a)(2) thereof. Each MAAC Class A Share issued in the PIPE Financing will be automatically canceled and extinguished and converted into one Roivant Common Share in the Merger.

The closing of the PIPE Financing is subject to customary conditions for a financing of this nature, including the substantially concurrent consummation of the Business Combination. The Subscription Agreements provide that Roivant will grant the PIPE Investors certain customary registration rights with respect to their Roivant Common Shares following the closing of the Business Combination.

Table of Contents

In connection with the Business Combination, certain related agreements were entered into in connection with the signing of the Business Combination Agreement, including the Subscription Agreements, the Transaction Support Agreements, the Sponsor Support Agreement and the Lock-Up Agreements (as defined and each described in more detail in the accompanying proxy statement/prospectus). See the section entitled “The Business Combination Proposal—Related Agreements” in the accompanying proxy statement/prospectus for more information.

MAAC’s units, consisting of one MAAC Class A Share and one-half of one MAAC Warrant (the “MAAC Units”), MAAC Class A Shares and MAAC Warrants are currently listed on the Nasdaq Capital Market LLC (“Nasdaq”) under the symbols “MAACU,” “MAAC” and “MAACW,” respectively. MAAC will apply for listing, to be effective at the time of the Closing, of Roivant Common Shares and Roivant Warrants on Nasdaq under the symbols “ROIV” and “ROIVW,” respectively. It is a condition of the consummation of the Business Combination that Roivant’s initial listing application with Nasdaq shall have been approved. If such listing condition is not met or if such confirmation is not obtained, the Business Combination may not be consummated.

You will be also asked to vote upon (a) a proposal herein referred to as the “Nasdaq Proposal” to approve, for the purposes of complying with Nasdaq Listing Rule 5635(a), (b) and (d), the issuance of more than 20% of the issued and outstanding MAAC Shares upon the completion of the Business Combination and (b) a proposal herein referred to as the “Adjournment Proposal” to consider and vote upon a proposal to adjourn the MAAC Special Meeting to a later date or time, if necessary, to permit further solicitation of proxies if, based upon the tabulated vote at the time of the MAAC Special Meeting, there are not sufficient votes to approve the Business Combination Proposal, or holders of MAAC Class A Shares have elected to redeem an amount of MAAC Class A Shares such that (i) MAAC would have less than $5,000,001 of net tangible assets or (ii) the aggregate cash proceeds from the Trust Account are not equal to or greater than $210,000,000 and the related closing condition has not been waived by Roivant.

The MAAC board of directors has unanimously approved the Business Combination Agreement and the transactions contemplated thereby and recommends that MAAC stockholders vote “FOR” each of the proposals to be considered at the MAAC Special Meeting. The Business Combination Agreement and the transactions contemplated thereby (collectively, the “Business Combination”) were approved by the boards of directors of each of MAAC, Roivant and Merger Sub, the requisite shareholders of Roivant and Roivant in its capacity as the sole shareholder of Merger Sub.

YOUR VOTE IS VERY IMPORTANT, REGARDLESS OF THE NUMBER OF MAAC CLASS A SHARES YOU OWN. To ensure your representation at the MAAC Special Meeting, please complete and return the enclosed proxy card or submit your proxy by following the instructions contained in the accompanying proxy statement/prospectus and on your proxy card. Please submit your proxy promptly whether or not you expect to attend the MAAC Special Meeting. Submitting a proxy now will NOT prevent you from being able to vote online at the meeting.

You may attend the meeting and vote your shares electronically during the meeting via live audio webcast by visiting . You will need the control number that is printed on your proxy card to enter the MAAC Special Meeting. MAAC recommends that you log in at least 15 minutes before the meeting to ensure you are logged in when the MAAC Special Meeting starts. Please note that you will not be able to attend the MAAC Special Meeting in person. If your shares are held in “street name” in a stock brokerage account or by a broker, bank or other nominee, you will need to contact Continental Stock Transfer & Trust Company (“CST”) to receive a control number.

The accompanying proxy statement/prospectus provides you with detailed information about the proposed Business Combination. It also contains or references information about MAAC, Roivant and certain related matters. You are encouraged to read the accompanying proxy statement/prospectus carefully. In particular, you should read the “Risk Factors” section beginning on page 34 for a discussion of the risks you should consider in evaluating the proposed Business Combination and how it will affect you.

Table of Contents

If you have any questions regarding the accompanying proxy statement/prospectus, you may contact , MAAC’s proxy solicitor, toll-free at (banks and brokers call ) or email at .

Sincerely,

|

James C. Momtazee Chairman of the Board |

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the Business Combination, the issuance of Roivant Common Shares in connection with the Business Combination or the other transactions described in the accompanying proxy statement/prospectus, or passed upon the adequacy or accuracy of the disclosure in the accompanying proxy statement/prospectus. Any representation to the contrary is a criminal offense.

The accompanying proxy statement/prospectus is dated , 2021, and is first being mailed to MAAC’s stockholders on or about , 2021.

Table of Contents

Montes Archimedes Acquisition Corp.

724 Oak Grove Ave, Suite 130

Menlo Park, CA 94025

NOTICE OF THE SPECIAL MEETING OF STOCKHOLDERS TO BE HELD ON , 2021

NOTICE IS HEREBY GIVEN that a special meeting of the stockholders of Montes Archimedes Acquisition Corp., a Delaware corporation, will be held virtually, conducted via live audio webcast on , 2021, unless postponed or adjourned to a later date or time. In light of the COVID-19 pandemic and to support the well-being of MAAC’s stockholders and employees, the MAAC Special Meeting will be completely virtual. All MAAC stockholders as of the record date, or their duly appointed proxies, may attend the MAAC Special Meeting. Registration will begin at Eastern Time. You may attend the meeting and vote your shares electronically during the meeting via live audio webcast by visiting . You will need the control number that is printed on your proxy card to enter the MAAC Special Meeting. MAAC recommends that you log in at least 15 minutes before the meeting to ensure you are logged in when the MAAC Special Meeting starts. Please note that you will not be able to attend the MAAC Special Meeting in person.

On May 1, 2021, Montes Archimedes Acquisition Corp., a Delaware corporation (“MAAC”), entered into a Business Combination Agreement (as amended on June 9, 2021 to reflect the execution of the lock-up agreements entered into by MAAC’s independent directors (the “MAAC Independent Directors” and each, a “MAAC Independent Director”) and Roivant Sciences Ltd., a Bermuda exempted limited company (“Roivant”), and as may be further amended, supplemented or otherwise modified from time to time, the “Business Combination Agreement”) with Roivant, and Rhine Merger Sub, Inc., a Delaware corporation (“Merger Sub”), a copy of which is attached to the accompanying proxy statement/prospectus as Annex A.

The Business Combination Agreement and the transactions contemplated thereby (collectively, the “Business Combination”) were approved by the boards of directors of each of MAAC, Roivant and Merger Sub. The Business Combination Agreement provides for, among other things, the following transactions: (i) the bye-laws of Roivant will be amended and restated; (ii) Merger Sub will merge with and into MAAC, with MAAC surviving the merger as a wholly-owned subsidiary of Roivant (the “Merger”); and (iii) in connection with the aforementioned transactions and the other transactions contemplated by the Business Combination Agreement, the PIPE Financing and the Transaction Support Agreements (each as defined and described in more detail in the accompanying proxy statement/prospectus) will be completed. As described in the accompanying proxy statement/prospectus, MAAC’s stockholders are being asked to consider a vote on the Business Combination, among other proposals.

At the effective time of the Merger (the “Effective Time”), (a) each share of MAAC Class A common stock (the “MAAC Class A Shares”) and each share of MAAC Class B common stock (the “MAAC Class B Shares,” together with the MAAC Class A Shares, the “MAAC Shares”) that is outstanding immediately before the Effective Time (other than treasury shares and any shares held by the MAAC Sponsor, any affiliate of the MAAC Sponsor or any MAAC Independent Director or its transferee) will be automatically canceled and extinguished and converted into one Roivant Common Share, (b) each MAAC Class B Share that is outstanding immediately before the Effective Time and held by the MAAC Sponsor, any affiliate of the MAAC Sponsor or any MAAC Independent Director or its transferee will be automatically canceled and extinguished and converted into a number of Roivant Common Shares based on an exchange ratio (the “MAAC Sponsor Exchange Ratio”), with a portion of such Roivant Common Shares issued to the MAAC Sponsor, any affiliate of the MAAC Sponsor, any MAAC Independent Director or its transferee by virtue of the Merger being subject to the vesting and other terms and conditions set forth in the Sponsor Support Agreement (as defined and more fully described in the accompanying proxy statement/prospectus), and (c) each warrant to purchase MAAC Class A Shares (the “MAAC Warrants”) that is outstanding immediately before the Effective Time will be converted automatically into the right to acquire Roivant Common Shares on the terms and subject to the conditions set forth in the MAAC Warrant Agreement, dated as of October 6, 2020, by and between MAAC and the Continental Stock Transfer & Trust Company. Pursuant to the Sponsor Support Agreement, the MAAC Sponsor Exchange Ratio is 1.0, subject to reduction in an amount equal to one-half of the percentage of MAAC Class A Shares redeemed in

Table of Contents

connection with the Business Combination (i.e., if 10% of the MAAC Class A Shares are so redeemed, then the MAAC Sponsor Exchange Ratio will be equal to 0.95), provided that in no event will the MAAC Sponsor Exchange Ratio be less than 0.75.

The Business Combination Proposal — To consider and vote upon a proposal to approve the Business Combination Agreement, certain related agreements and the transactions contemplated thereby (including the Business Combination, as defined in the accompanying proxy statement/prospectus). The Business Combination Agreement provides for, among other things, that the Business Combination shall be effectuated through Merger Sub merging with and into MAAC, with MAAC surviving the merger as a wholly-owned subsidiary of Roivant. As described in the accompanying proxy statement/prospectus, MAAC’s stockholders are being asked to consider a vote on the Business Combination, among other proposals. A copy of the Business Combination Agreement is attached to the accompanying proxy statement/prospectus as Annex A (Proposal No. 1).

The Nasdaq Proposal — To consider and vote upon a proposal to approve, for the purposes of complying with Nasdaq Listing Rule 5635(a), (b) and (d), the issuance of more than 20% of the issued and outstanding MAAC Shares upon the completion of the Business Combination (Proposal No. 2).

The Adjournment Proposal — To consider and vote upon a proposal to adjourn the MAAC Special Meeting to a later date or time, if necessary, to permit further solicitation of proxies if, based upon the tabulated vote at the time of the MAAC Special Meeting, there are not sufficient votes to approve the Business Combination Proposal, or holders of MAAC Class A Shares have elected to redeem an amount of MAAC Class A Shares such that (i) MAAC would have less than $5,000,001 of net tangible assets or (ii) the aggregate cash proceeds from the Trust Account not being equal to or greater than $210,000,000 would not be satisfied or waived by Roivant. The Business Combination is not conditioned upon the approval of the Adjournment Proposal (Proposal No. 3).

Only holders of record of MAAC Shares at the close of business on , 2021 are entitled to notice of the MAAC Special Meeting and to vote at the MAAC Special Meeting and any adjournments or postponements thereof. A complete list of MAAC stockholders of record entitled to vote at the MAAC Special Meeting will be available for ten days before the MAAC Special Meeting at the principal executive offices of MAAC for inspection by stockholders during ordinary business hours for any purpose germane to the MAAC Special Meeting. The eligible MAAC stockholder list will also be available on the MAAC Special Meeting website for examination by any stockholder attending the MAAC Special Meeting live audio webcast.

Holders of MAAC Class A Shares have the right to redeem such shares for a pro rata portion of the cash held in a trust account (the “Trust Account”), which holds the net proceeds of MAAC’s initial public offering, as of two business days prior to the consummation of the transactions contemplated by the Business Combination Agreement (including interest earned on the funds held in the Trust Account and not previously released to MAAC to pay taxes, if any) upon the closing of the transactions contemplated by the Business Combination Agreement. Notwithstanding the foregoing, a holder of MAAC Class A Shares, together with any affiliate of such holder or any other person with whom such holder is acting in concert or as a “group” (as defined in Section 13(d)(3) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), will be restricted from seeking redemption with respect to more than 15% of the MAAC Class A Shares. Holders of the outstanding MAAC Warrants do not have redemption rights with respect to such warrants in connection with the transactions contemplated by the Business Combination Agreement.

Approval of the Business Combination Proposal requires that the initial Business Combination be approved by the affirmative vote of the holders of a majority of MAAC Shares outstanding as of the date of the stockholder meeting held to consider such initial Business Combination. Approval of the Adjournment Proposal requires the affirmative vote of a majority of MAAC Shares present in person or represented by proxy at the MAAC Special Meeting and entitled to vote at the meeting, regardless of whether a quorum is present. Broker non-votes, while considered present for the purposes of establishing a quorum, will not count as shares entitled to vote or votes cast at the MAAC Special Meeting, and otherwise will have no effect on the Nasdaq Proposal and Adjournment Proposal. Broker non-votes will have the same effect as a vote “AGAINST” the Business Combination Proposal. The MAAC board of directors has approved each of the proposals.

As of March 31, 2021, there was approximately $410.8 million in the Trust Account, which MAAC intends to use for the purposes of consummating the Business Combination within the time period described in the accompanying proxy statement/prospectus and to pay $14,375,138 in deferred underwriting commissions to the

Table of Contents

underwriters of MAAC’s initial public offering. Each redemption of MAAC Class A Shares by its public stockholders will decrease the amount in the Trust Account. MAAC will not consummate the Business Combination if the redemption of MAAC Class A Shares would result in MAAC’s failure to have at least $5,000,001 of net tangible assets (as determined in accordance with Rule 3a51-1(g)(1) of the Exchange Act) (or any successor rule).

If MAAC stockholders fail to approve the Business Combination Proposal, the Business Combination will not occur. The proxy statement/prospectus accompanying this notice explains the Business Combination Agreement and the transactions contemplated thereby, as well as the proposals to be considered at the MAAC Special Meeting. Please review the proxy statement/prospectus carefully.

YOUR VOTE IS VERY IMPORTANT, REGARDLESS OF THE NUMBER OF MAAC CLASS A SHARES YOU OWN. To ensure your representation at the MAAC Special Meeting, please complete and return the enclosed proxy card or submit your proxy by following the instructions contained in the accompanying proxy statement/prospectus and on your proxy card. Please submit your proxy promptly whether or not you expect to attend the meeting. Submitting a proxy now will NOT prevent you from being able to vote online at the MAAC Special Meeting. If your shares are held in “street name” in a stock brokerage account or by a broker, bank or other nominee, you will need to contact CST to receive a control number.

The MAAC board of directors has unanimously approved the Business Combination Agreement and the transactions contemplated thereby and recommends that you vote “FOR” the Business Combination Proposal, “FOR” the Nasdaq Proposal and, if required, “FOR” the Adjournment Proposal.

If you plan to vote at the MAAC Special Meeting you will need to have a legal proxy from your bank, broker, or other nominee or if you would like to join and not vote CST will issue you a guest control number with proof of ownership. In either case, you must contact CST for specific instructions on how to receive the control number. Please allow up to 72 hours prior to the meeting for processing your control number.

If you do not have internet capabilities, you can listen only to the meeting by dialing +1 (toll-free) inside the U.S. and Canada or +1 (standard rates apply), and when prompted enter the pin number #. This is listen-only, you will not be able to vote or enter questions during the meeting.

| BY ORDER OF THE BOARD OF DIRECTORS |

James C. Momtazee |

| Chairman of the Board |

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE TRANSACTIONS DESCRIBED IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS OR ANY OF THE SECURITIES TO BE ISSUED IN CONNECTION WITH THE BUSINESS COMBINATION, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION OR RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

Table of Contents

ANNEXES

| A-1 | ||||

Annex AA – Amendment No. 1 to the Business Combination Agreement | AA-1 | |||

| B-1 | ||||

| C-1 | ||||

| D-1 | ||||

| E-1 | ||||

| EE-1 | ||||

| F-1 |

i

Table of Contents

MAAC and Roivant are responsible for the information contained in this proxy statement/prospectus. Neither MAAC nor Roivant have authorized anyone to provide you with different information, and neither MAAC nor Roivant take responsibility for any other information others may give you. MAAC and Roivant are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than its date.

For investors outside of the United States, neither MAAC nor Roivant have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about, and to observe any restrictions relating to, this offering and the distribution of this prospectus outside of the United States.

ii

Table of Contents

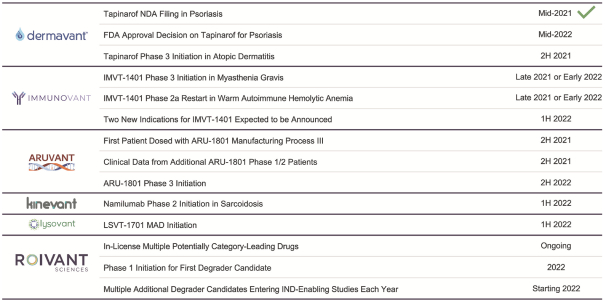

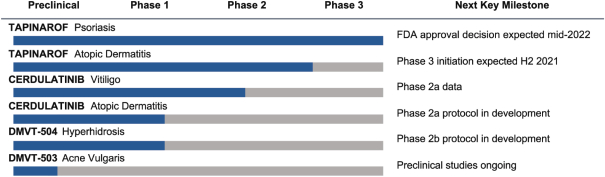

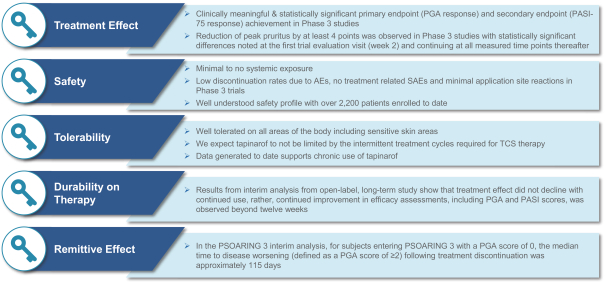

This proxy statement/prospectus includes references to the clinical trials that Roivant has conducted with respect to its product candidates. Where reference is made to a clinical trial being “successful,” that indicates that the product candidate under evaluation in that clinical trial met its pre-specified primary endpoint(s). The eight successful Phase 3 clinical trials referenced in this proxy statement/prospectus evaluated four distinct drug candidates or combination therapies: tapinarof, vibegron, relugolix monotherapy, and a combination of relugolix, estradiol, and norethindrone acetate. The one unsuccessful Phase 3 clinical trial evaluated intepirdine for the treatment of Alzheimer’s disease. With respect to the drug candidates that have completed successful Phase 3 clinical trials: (i) our subsidiary, Dermavant Sciences, has submitted an NDA to the FDA for tapinarof, for which a decision on its approval is expected in mid-2022; (ii) our former subsidiary, Myovant Sciences, has received FDA approval for relugolix (marketed as Orgovyx) for the treatment of prostate cancer and the combination of relugolix, estradiol and norethindrone acetate (marketed as Myfembree) for the treatment of uterine fibroids; (iii) our former subsidiary, Urovant Sciences, has received FDA approval for vibegron (marketed as Gemtesa) for the treatment of overactive bladder.

Certain summary statistics and other information presented in proxy statement/prospectus, including our pipeline of drug candidates, our clinical trial count, the number of Vant launches and the return on our investment in publicly-listed Vants, include three entities in which we retain both a substantial economic interest and have representation on the entities’ boards of directors: Arbutus Biopharma, Sio Gene Therapies and Datavant. Other than the potential appreciation in the value of our equity interests in these entities, we do not have any further economic interests in the product candidates they are developing or their marketed technology products, as applicable.

MARKET, INDUSTRY AND OTHER DATA

This proxy statement/prospectus contains estimates, projections and other information concerning Roivant’s industry, Roivant’s business and the markets for Roivant’s products. Some market data and statistical information contained in this proxy statement/prospectus are also based on Roivant’s management’s estimates and calculations, which are derived from their review and interpretation of the independent sources listed below, internal research and knowledge of Roivant’s market. While we are not aware of any misstatements regarding the market, industry or other data presented herein, such projections, assumptions and estimates of the future performance of the industry in which Roivant operates and Roivant’s future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described in the sections titled “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors.”

Unless otherwise expressly stated, we obtained industry, business, market and other data from the reports, publications and other materials and sources listed below. In some cases, we do not expressly refer to the sources from which this data is derived. In that regard, when we refer to one or more sources of this type of data in any paragraph, you should assume that other data of this type appearing in the same paragraph is derived from the same sources, unless otherwise expressly stated or the context otherwise requires.

This document contains references to trademarks, trade names and service marks belonging to other entities. Solely for convenience, trademarks, trade names and service marks referred to in this proxy statement/consent solicitation statement/prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. MAAC and Roivant do not intend that use or display of other companies’ trade names, trademarks, or service marks to imply a relationship with, or endorsement or sponsorship of us, by any other companies.

1

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This proxy statement/prospectus may contain “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future, and statements that are not historical facts, including statements about the Business Combination. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements contained in this proxy statement/prospectus are based on our current expectations and beliefs concerning future developments and their potential effects on us taking into account information currently available to us. There can be no assurance that future developments affecting us will be those that we have anticipated. Should one or more of these risks or uncertainties materialize, they could cause our actual results to differ materially from the forward-looking statements. Some factors that could cause actual results to differ include, but are not limited to:

| • | the timing to complete the Business Combination; |

| • | the occurrence of any event, change or other circumstances that could give rise to the termination of the Business Combination Agreement; |

| • | the outcome of any legal proceedings that may be instituted against MAAC or Roivant in connection with the Business Combination and related transactions; |

| • | the inability to complete the Business Combination and the other transactions contemplated by the Business Combination Agreement due to the failure to obtain the requisite approval of our shareholders, or other conditions to closing in the Business Combination Agreement; |

| • | MAAC’S ability to obtain the listing of Roivant Common Shares and Roivant Warrants on Nasdaq following the Business Combination; |

| • | the risk that the Business Combination disrupts Roivant’s current operations as a result of the announcement and consummation of the transactions described herein; |

| • | the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, and the ability of the combined business to grow and manage growth profitably; |

| • | costs related to the Business Combination; |

| • | changes in applicable laws or regulations; |

| • | the possibility that MAAC or Roivant may be adversely affected by other economic, business and/or competitive factors; and |

| • | other risks and uncertainties, including those described under the heading “Risk Factors.” |

We are not undertaking any obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise. You should not take any statement regarding past trends or activities as a representation that the trends or activities will continue in the future. Accordingly, you should not put undue reliance on these statements in deciding how to grant your proxy or instruct how your vote should be cast on the proposals set forth in this proxy statement/prospectus.

��

2

Table of Contents

Unless the context otherwise requires, references in this proxy statement/prospectus to:

“Basic” means, when referring to Roivant’s ownership interest in an entity, and unless otherwise indicated, Roivant’s percentage ownership of the issued and outstanding shares of the entity.

“Business Combination” means the merger pursuant to the Business Combination Agreement, whereby, among other things, (a) the bye-laws of Roivant will be amended and restated, (ii) Merger Sub will merge with and into MAAC, with MAAC surviving the merger as a wholly-owned subsidiary of Roivant, and (iii) and the other transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of May 1, 2021, by and among MAAC, Roivant and Merger Sub, as amended on June 9, 2021 to reflect the execution of the lock-up agreements entered into by the MAAC Independent Directors and Roivant and as may be further amended, supplemented or otherwise modified from time to time.

“Closing” means the closing of the Business Combination.

“Effective Time” means the effective time of the Merger.

“FDA” means the U.S. Food and Drug Administration.

“Founder Shares” means 10,267,956 MAAC Class B Shares outstanding as of the date of this proxy statement/prospectus that were issued to the MAAC Sponsor in a private placement prior to MAAC’s initial public offering, which immediately prior to the Effective Time will automatically convert, on a one-for-one basis, into 10,267,956 MAAC Class A Shares subject to the terms of the Sponsor Support Agreement.

“Fully Diluted” means, when referring to Roivant’s ownership interest in an entity, and unless otherwise indicated, Roivant’s percentage ownership of all outstanding equity interests, whether vested or unvested, of the entity.

“HSR Act” means the Hart-Scott-Rodino Antitrust Improvements Act of 1976 and the rules and regulations promulgated thereunder.

“MAAC” means Montes Archimedes Acquisition Corp., a Delaware corporation.

“MAAC Class A Shares” means each share of Class A common stock of MAAC, par value $0.0001 per share.

“MAAC Class B Shares” means each share of Class B common stock of MAAC, par value $0.0001 per share.

“MAAC Shares” means, collectively, the MAAC Class A Shares and the MAAC Class B Shares.

“MAAC Sponsor” means Patient Square Capital LLC, a limited liability company organized under the State of Delaware.

“MAAC Unit” means each issued and outstanding unit of MAAC, consisting of one MAAC Class A Share and one-half of one MAAC Warrant.

“MAAC Warrant” means each whole warrant of MAAC entitling the holder to purchase one MAAC Class A Share per warrant at a price of $11.50 per share.

3

Table of Contents

“MAAC Warrant Agreement” means the Warrant Agreement, dated as of October 6, 2020, by and between MAAC and the Continental Stock Transfer & Trust Company.

“Merger” means the merger between MAAC and Merger Sub.

“Merger Sub” means Rhine Merger Sub, Inc., a Delaware corporation and a wholly owned subsidiary of the Roivant.

“NDA” means a New Drug Application.

“PIPE Financing” means the commitment by the PIPE Investors to purchase an aggregate of 22,000,000 MAAC Class A Shares at a purchase price of $10.00 per share, for aggregate gross proceeds to MAAC of $220,000,000.

“PIPE Investors” means those certain institutional and accredited investors that entered into the Subscription Agreements in connection with the PIPE Financing.

“Roivant” means Roivant Sciences Ltd., an exempted company incorporated under the laws of Bermuda.

“Roivant Common Shares” means each common share of Roivant either, as context requires, prior to or following the consummation of the Business Combination.

“Roivant Warrants” means each warrant to be issued by Roivant to MAAC Warrant holders and the Roivant Common Shares underlying such warrants.

“Sponsor Support Agreement” means the agreement, dated as of May 1, 2021, as amended by Amendment No. 1, dated as of June 9, 2021, pursuant to which the MAAC Sponsor agreed to undertake certain actions in support of the Business Combination, including, but not limited to, delivering a voting proxy pursuant to which the MAAC Sponsor will vote in favor of the proposals presented for approval herein.

“Subscription Agreements” means the subscription agreements entered into among MAAC, Roivant and the PIPE Investors, pursuant to which such investors have agreed to subscribe for and purchase, and MAAC has agreed to issue and sell to such investors, an aggregate of 22,000,000 MAAC Class A Shares at a price of $10.00 per share, for aggregate gross proceeds of $220,000,000.

“Transaction Support Agreements” means, collectively, the agreements pursuant to which certain shareholders of Roivant entered into with MAAC and Roivant, pursuant to which such shareholders of Roivant have agreed to, among other things, certain covenants and agreements, to support, or that are otherwise related to, the Business Combination, including an agreement to terminate certain existing agreements between Roivant and such shareholders, an agreement to not transfer his, her or its Roivant Common Shares prior to Closing and, in the case of certain Roivant shareholders also participating in the PIPE Financing, certain covenants related to the expiration or termination of the waiting period under the HSR Act, to the extent applicable, with respect to the issuance of Roivant Common Shares to such shareholder in connection with the Business Combination.

4

Table of Contents

The following are answers to certain questions that you, as a stockholder of MAAC, may have regarding the Business Combination and the stockholder meeting. We urge you to carefully read the remainder of this proxy statement/prospectus because the information in this section may not provide all the information that might be important to you in determining how to vote. Additional important information is also contained in the annexes to this proxy statement/prospectus.

QUESTIONS AND ANSWERS ABOUT THE BUSINESS COMBINATION

| Q: | WHAT IS THE BUSINESS COMBINATION? |

| A: | MAAC, Roivant and Merger Sub have entered into a Business Combination Agreement, dated as of May 1, 2021 (as amended on June 9, 2021 to reflect the execution of the lock-up agreements entered into by the MAAC Independent Directors and Roivant and as may be further amended, supplemented or otherwise modified from time to time), pursuant to which, among other things: (i) the bye-laws of Roivant will be amended and restated; (ii) Merger Sub will merge with and into MAAC, with MAAC surviving the merger as a wholly-owned subsidiary of Roivant; and (iii) in connection with the aforementioned transactions and the other transactions contemplated by the Business Combination Agreement, the PIPE Financing and the Transaction Support Agreements will be completed. |

MAAC will hold the MAAC Special Meeting of stockholders to consider matters relating to the proposed Business Combination. See “The Business Combination Proposal—Business Combination.” In addition, a copy of the Business Combination Agreement is attached to this proxy statement/prospectus as Annex A. We urge you to carefully read this proxy statement/prospectus and the Business Combination Agreement in their entirety. MAAC and Roivant cannot complete the Business Combination unless MAAC’s stockholders approve the Business Combination Agreement and the transactions contemplated thereby. MAAC is sending you this proxy statement/prospectus to ask you to vote in favor of these and the other matters described in this proxy statement/prospectus.

| Q: | WHY AM I RECEIVING THIS DOCUMENT? |

| A: | MAAC is sending this proxy statement/prospectus to its stockholders to help them decide how to vote their MAAC Shares with respect to the matters to be considered at the MAAC Special Meeting. |

The Business Combination cannot be completed unless MAAC’s stockholders approve the Business Combination Proposal, as set forth in this proxy statement/prospectus. Information about the MAAC Special Meeting, the Business Combination and the other business to be considered by stockholders at the MAAC Special Meeting is contained in this proxy statement/prospectus.

This document constitutes a proxy statement of MAAC and a prospectus of Roivant. It is a proxy statement because the board of directors of MAAC is soliciting proxies using this proxy statement/prospectus from its stockholders. It is a prospectus because Roivant, in connection with the Merger, is offering Roivant Common Shares in exchange for the outstanding MAAC Class A Shares and MAAC Class B Shares.

| Q: | WHAT WILL HAPPEN TO MAAC’S SECURITIES UPON CONSUMMATION OF THE BUSINESS COMBINATION? |

| A: | MAAC Units, the MAAC Class A Shares and the MAAC Warrants are publicly traded on Nasdaq under the symbols “MAACU,” “MAAC” and “MAACW,” respectively. At the effective time of the Merger, outstanding MAAC Class A Shares and MAAC Warrants will be exchanged for newly issued Roivant Common Shares and Roivant Warrants, respectively, which are expected to be listed on Nasdaq under the new ticker symbols “ROIV” and “ROIVW.” MAAC warrant holders and those stockholders who do not elect to have their shares redeemed need not deliver their MAAC Class A Shares or warrant certificates to MAAC or MAAC’s transfer agent and they will remain outstanding. |

5

Table of Contents

| Q: | WHAT WILL MAAC STOCKHOLDERS RECEIVE IN THE BUSINESS COMBINATION? |

| A: | At the effective time of the Merger, (a) each MAAC Class A Share and each MAAC Class B Share that is outstanding immediately before the effective time (other than treasury shares and any shares held by the MAAC Sponsor, any affiliate of the MAAC Sponsor or any MAAC Independent Director or its transferee) will be automatically canceled and extinguished and converted into one Roivant Common Share, (b) each MAAC Class B Share that is outstanding immediately before the effective time held by the MAAC Sponsor, any affiliate of the MAAC Sponsor or any MAAC Independent Director or its transferee will be automatically canceled and extinguished and converted into a number of Roivant Common Shares based on an exchange ratio, with a portion of such Roivant Common Shares issued to the MAAC Sponsor , any affiliate of the MAAC Sponsor or any MAAC Independent Director or its transferee by virtue of the Merger being subject to the vesting and other terms and conditions set forth in the Sponsor Support Agreement (as more fully described in the section entitled “Summary of the Proxy Statement/Prospectus—Sponsor Support Agreement” below), and (c) each MAAC Warrant that is outstanding immediately before the effective time will be converted automatically into the right to acquire Roivant Common Shares on the terms and subject to the conditions set forth in the MAAC Warrant Agreement, dated as of October 6, 2020, by and between MAAC and the Continental Stock Transfer & Trust Company. Pursuant to the Sponsor Support Agreement, the MAAC Sponsor Exchange Ratio is 1.0, subject to reduction in an amount equal to one-half of the percentage of MAAC Class A Shares redeemed in connection with the Business Combination (i.e., if 10% of the MAAC Class A Shares are so redeemed, then the MAAC Sponsor Exchange Ratio will be equal to 0.95), provided that in no event will the MAAC Sponsor Exchange Ratio be less than 0.75. |

| Q: | WHEN WILL THE BUSINESS COMBINATION BE COMPLETED? |

| A: | MAAC and Roivant currently expect that the Business Combination will be completed during the third calendar quarter of 2021. However, MAAC cannot assure you of when or if the Business Combination will be completed, and it is possible that factors outside of the control of MAAC could result in the Business Combination being completed at a different time or not at all. MAAC must first obtain the approval of MAAC stockholders for each of the proposals set forth in this proxy statement/prospectus (other than the Adjournment Proposal) and certain other closing conditions must be fulfilled. See “The Business Combination Proposal—Business Combination—Conditions to the Closing of the Business Combination.” |

| Q: | WHAT ARE THE U.S. FEDERAL INCOME TAX CONSEQUENCES OF THE MERGER TO U.S. HOLDERS OF MAAC CLASS A SHARES AND/OR MAAC WARRANTS? |

| A: | Subject to the limitations and qualifications described in “Material United States Tax Considerations—Tax Consequences of the Merger” below, the Merger is generally intended to be tax-deferred to U.S. Holders (as defined in “Material United States Tax Considerations”) of MAAC Class A Shares and MAAC Warrants for U.S. federal income tax purposes, except to the extent that such U.S. Holders of MAAC Class A Shares receive cash pursuant to the exercise of redemption rights. However, there are significant factual and legal uncertainties as to whether the Merger qualifies for tax-deferred treatment as a “reorganization” under Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”). If any requirement for Section 368(a) of the Code is not met, then a U.S. Holder of MAAC Class A Shares or MAAC Warrants may recognize gain or loss in an amount equal to the difference, if any, between the fair market value (as of the date of the Closing) of Roivant Common Shares received in the Merger or MAAC Warrants assumed by Roivant in the Merger, over such U.S. Holder’s aggregate tax basis in the corresponding MAAC Class A Shares surrendered by such U.S. Holder in the Merger or MAAC Warrants assumed by Roivant in the Merger, respectively. |

Section 367(a) of the Code and the Treasury regulations promulgated thereunder, in certain circumstances, may impose additional requirements for certain U.S. Holders to qualify for tax-deferred treatment with respect to the exchange of MAAC Class A Shares and/or the assumption of MAAC Warrants by Roivant in the Merger.

6

Table of Contents

The tax consequences of the Merger are complex and will depend on your particular circumstances. For a more complete discussion of the U.S. federal income tax considerations of the Merger, including the application of Section 367(a) of the Code, see the sections entitled “Material United States Tax Considerations—Tax Consequences of the Merger”, and “Material United States Tax Considerations—Additional Requirements for Tax Deferral.”

If you are a U.S. Holder whose MAAC Class A Shares are exchanged, or whose MAAC Warrants are assumed by Roivant, in the Merger, you are urged to consult your tax advisor to determine the tax consequences thereof. The summary above is qualified in its entirety by the more detailed discussion provided in the section entitled “Material United States Tax Considerations.”

| Q: | WHAT ARE THE U.S. FEDERAL INCOME TAX CONSEQUENCES OF EXERCISING MY REDEMPTION RIGHTS? |

| A: | Whether the redemption is subject to U.S. federal income tax depends on the particular facts and circumstances. Please see the section entitled “Material United States Tax Considerations—Tax Consequences of Exercising Redemption Rights.” We urge you to consult your tax advisors regarding the tax consequences of exercising your redemption rights. |

QUESTIONS AND ANSWERS ABOUT THE MAAC SPECIAL MEETING

| Q: | WHAT AM I BEING ASKED TO VOTE ON AND WHY IS THIS APPROVAL NECESSARY? |

| A: | MAAC stockholders are being asked to vote on the following proposals: |

| • | the Business Combination Proposal; |

| • | the Nasdaq Proposal; and |

| • | the Adjournment Proposal. |

The Business Combination will not occur unless MAAC stockholders approve each of the proposals specified in this proxy statement/prospectus, other than the Adjournment Proposal.

| Q: | WHY IS MAAC PROPOSING THE BUSINESS COMBINATION? |

| A: | MAAC is a blank check company incorporated to effect a merger, capital stock exchange, asset acquisition, share purchase, reorganization or other similar business combination with one or more businesses. |

On October 9, 2020, MAAC completed its initial public offering, generating gross proceeds of $410,718,230 (which includes the gross proceeds from the partial exercise of the underwriters’ over-allotment option on November 10, 2020), which were placed in the Trust Account. All of MAAC’s activity since its initial public offering has related to identifying a target company for a business combination.

Based on its due diligence investigations of Roivant and the industry in which Roivant operates, including the financial and other information provided by Roivant in the course of the negotiations of the Business Combination Agreement, MAAC believes that Roivant aligns well with the objectives laid out in MAAC’s investment thesis. As a result, MAAC believes that a business combination with Roivant will provide MAAC stockholders with an opportunity to participate in the ownership of a publicly-listed company with significant growth potential at an attractive valuation. See “The Business Combination Proposal—Business Combination—The MAAC Board of Directors’ Reasons for the Business Combination.”

| Q: | DID THE MAAC BOARD OBTAIN A THIRD-PARTY VALUATION OR FAIRNESS OPINION IN DETERMINING WHETHER OR NOT TO PROCEED WITH THE BUSINESS COMBINATION? |

| A: | MAAC’s board of directors did not obtain a third-party valuation or fairness opinion in connection with its determination to approve the Business Combination. MAAC’s officers have more than 50 years of |

7

Table of Contents

| combined investing experience during which they have conducted diligence on a broad set of private and publicly held health care companies. MAAC’s directors also have significant operating experience, acquisition experience and relationships in the health care industry. MAAC’s officers and directors, together with their advisors, employed a disciplined and highly selective investment process that focused on accessing differentiated opportunities through deep relationships with executives, advisors, and intermediaries to enhance the growth potential and value of a target business and provide opportunities for an attractive return to our stockholders. They concluded that their experience and backgrounds, together with the experience and sector expertise of MAAC’s advisors, enabled them to make the necessary analyses and determinations regarding the Business Combination. Accordingly, investors will be relying solely on the judgment of MAAC’s board of directors in valuing Roivant’s business. |

| Q: | DO I HAVE REDEMPTION RIGHTS? |

| A: | If you are a holder of MAAC Class A Shares, you have the right to redeem such shares for a pro rata portion of the cash held in the Trust Account, which holds the net proceeds of MAAC’s initial public offering, as of two business days prior to the consummation of the transactions contemplated by the Business Combination Agreement (including interest earned on the funds held in the Trust Account and not previously released to MAAC to pay taxes, if any) upon the closing of the transactions contemplated by the Business Combination Agreement. |

Notwithstanding the foregoing, a holder of MAAC Class A Shares, together with any affiliate of such holder or any other person with whom such holder is acting in concert or as a “group” (as defined in Section 13(d)(3) of the Exchange Act), will be restricted from seeking redemption with respect to more than 15% of the MAAC Class A Shares.

Holders of the outstanding MAAC Warrants do not have redemption rights with respect to such warrants in connection with the transactions contemplated by the Business Combination Agreement.

Under the Pre-Closing MAAC Certificate of Incorporation, the Business Combination may be consummated only if MAAC has at least $5,000,001 of net tangible assets after giving effect to redemptions by all holders of MAAC Class A Shares that properly demand redemption of their MAAC Class A Shares for cash.

| Q: | WILL MY VOTE AFFECT MY ABILITY TO EXERCISE MY REDEMPTION RIGHTS? |

| A: | No. You may exercise your redemption rights whether you vote your MAAC Class A Shares for or against, or whether you abstain from voting on, the Business Combination Proposal or any other proposal described in this proxy statement/prospectus. As a result, the Business Combination Proposal can be approved by stockholders who will redeem their MAAC Class A Shares and will no longer be stockholders and the Business Combination may be consummated even though the funds available from the Trust Account and the number of public stockholders are substantially reduced as a result of redemptions by public stockholders. With fewer MAAC Class A Shares and public stockholders, the trading market for MAAC Class A Shares may be less liquid than the market for MAAC Class A Shares prior to the Business Combination and MAAC may not be able to meet the listing standards of a national securities exchange, including Nasdaq. In addition, with fewer funds available from the Trust Account, the capital infusion from the Trust Account into Roivant’s business will be reduced and the amount of working capital available to Roivant following the Business Combination may be reduced. Your decision to exercise your redemption rights with respect to MAAC Class A Shares will have no effect on the MAAC Warrants you may also hold. |

| Q: | HOW DO I EXERCISE MY REDEMPTION RIGHTS? |

| A: | If you are a holder of MAAC Class A Shares and wish to exercise your redemption rights, you are required to tender your share certificates or deliver your shares to the transfer agent electronically using The Depository Trust Company’s DWAC (Deposit/Withdrawal at Custodian) system, at your option, in each |

8

Table of Contents

| case by the date that is two business days prior to the initially scheduled vote to approve the Business Combination. Accordingly, you have until two days prior to the initial vote on the Business Combination to tender your shares if you wish to exercise your redemption rights. Given the relatively short period in which to exercise redemption rights, it is advisable for you to use electronic delivery of your shares. If you exercise your redemption right, your shares will be redeemed for a pro rata portion of the amount then in the Trust Account (which, for illustrative purposes, was $410,790,995, or $10.00 per MAAC Class A Share, as of March 31, 2021). Such amount, including interest earned on the funds held in the Trust Account and not previously released to MAAC to pay its taxes, if any, will be paid promptly upon consummation of the Business Combination. However, under Delaware law, the proceeds held in the Trust Account could be subject to claims that could take priority over those of MAAC’s public stockholders exercising redemption rights, regardless of whether such holders vote for or against the Business Combination Proposal. The per share distribution from the Trust Account in such a situation may be less than originally anticipated due to such claims. Your vote on any proposal other than the Business Combination Proposal will have no impact on the amount you will receive if you exercise your redemption rights. |

Any request for redemption, once made by a holder of MAAC Class A Shares, may be withdrawn at any time up to two days prior to the vote on the Business Combination Proposal at the MAAC Special Meeting. If you deliver your shares for redemption to MAAC’s transfer agent and later decide, prior to the MAAC Special Meeting, not to redeem your shares, you may request that MAAC’s transfer agent return the shares electronically.

No demand will be effectuated unless the holder’s MAAC Class A Shares have been delivered electronically to the transfer agent prior to the vote on the Business Combination Proposal at the MAAC Special Meeting.

If a holder of MAAC Class A Shares properly makes a request for redemption and the MAAC Class A Shares are delivered to MAAC’s transfer agent no later than two business days prior to the initially scheduled vote to approve the Business Combination, then, if the Business Combination is consummated, MAAC will redeem these shares for a pro rata portion of funds deposited in the Trust Account. If you exercise your redemption rights, then you will be exchanging your MAAC Class A Shares for cash.

For a discussion of the material U.S. federal income tax considerations for holders of MAAC Class A Shares with respect to the exercise of these redemption rights, see “Material United States Tax Considerations—Tax Consequences of Exercising Redemption Rights.”

| Q: | WHAT HAPPENS TO THE FUNDS DEPOSITED IN THE TRUST ACCOUNT AFTER CONSUMMATION OF THE BUSINESS COMBINATION? |

| A: | The net proceeds of MAAC’s initial public offering, together with funds raised from the sale of the private placement warrants simultaneously with the consummation of MAAC’s initial public offering, were placed in the Trust Account immediately following MAAC’s initial public offering. After consummation of the Business Combination, the funds in the Trust Account will be used to pay holders of the MAAC Class A Shares who exercise redemption rights, to pay fees and expenses incurred in connection with the Business Combination (including aggregate fees of $14,375,138 as deferred underwriting commissions related to MAAC’s initial public offering) and for Roivant’s working capital and general corporate purposes, which may include future strategic transactions. |

| Q: | WHAT HAPPENS IF THE BUSINESS COMBINATION IS NOT CONSUMMATED? |

| A: | If MAAC does not complete the Business Combination with Roivant for any reason, MAAC intends to search for another target business with which to complete a business combination. If MAAC does not complete the Business Combination with Roivant or another target business by October 9, 2022, MAAC will (i) cease all operations except for the purpose of winding up; (ii) as promptly as reasonably possible but not more than ten business days thereafter, redeem the MAAC Class A Shares at a per-share price, payable |

9

Table of Contents

| in cash, equal to the aggregate amount then on deposit in the Trust Account including interest earned on the funds held in the Trust Account and not previously released to us to pay its taxes, if any (less up to $100,000 of interest to pay dissolution expenses), divided by the number of the then outstanding MAAC Class A Shares, which redemption will completely extinguish public stockholders’ rights as stockholders (including the right to receive further liquidation distributions, if any), subject to applicable law; and (iii) as promptly as reasonably possible following such redemption, subject to the approval of the remaining stockholders and the board of directors, liquidate and dissolve, subject in each case, to our obligations under Delaware law to provide for claims of creditors and the requirements of other applicable law. |

| Q: | HOW DOES THE MAAC SPONSOR INTEND TO VOTE ON THE PROPOSALS? |

| A: | The MAAC Sponsor owns of record, and is entitled to vote, an aggregate of approximately 20% of the outstanding MAAC Shares. The MAAC Sponsor has agreed to vote any MAAC Class B Shares, and any MAAC Class A Shares held by it as of the record date, in favor of the Business Combination Proposal. Further, the MAAC Sponsor intends to vote in favor of all of the proposals. |

| Q: | WHAT CONSTITUTES A QUORUM AT THE MAAC SPECIAL MEETING? |

| A: | A majority of the voting power of the issued and outstanding MAAC Shares entitled to vote at the MAAC Special Meeting as of the MAAC record date must be present virtually or by proxy, at the MAAC Special Meeting to constitute a quorum and in order to conduct business at the MAAC Special Meeting. Abstentions and broker non-votes will be counted as present for the purpose of determining a quorum. The holders of the MAAC Class B Shares, who currently own approximately 20% of the issued and outstanding MAAC Class A Shares, will count towards this quorum. In the absence of a quorum, the holders of a majority of the MAAC Shares present in person or represented by proxy at the meeting, and entitled to vote at the meeting, may adjourn the MAAC Special Meeting. |

As of the MAAC record date, 25,669,890 MAAC Shares would be required to achieve a quorum.

| Q: | WHAT VOTE IS REQUIRED TO APPROVE EACH PROPOSAL AT THE MAAC SPECIAL MEETING? |

| A: | The Business Combination Proposal: MAAC shall consummate the proposed initial Business Combination only if it is approved by the affirmative vote of the holders of a majority of MAAC Shares outstanding as of the date of the stockholder meeting held to consider such initial Business Combination. |

The Nasdaq Proposal: The affirmative vote of a majority of MAAC Shares present in person or represented by proxy at the MAAC Special Meeting and entitled to vote at the meeting is required to approve the Nasdaq Proposal.

The Adjournment Proposal: The affirmative vote of a majority of MAAC Shares present in person or represented by proxy at the MAAC Special Meeting and entitled to vote at the meeting, regardless of whether a quorum is present, is required to approve the Adjournment Proposal. The Business Combination is not conditioned upon the approval of the Adjournment Proposal.

| Q: | DO ANY OF MAAC’S DIRECTORS OR OFFICERS HAVE INTERESTS IN THE BUSINESS COMBINATION THAT DIFFER FROM OR ARE IN ADDITION TO THE INTERESTS OF MAAC’S PUBLIC STOCKHOLDERS? |

| A: | Each of MAAC’s directors and officers owns MAAC Class B Shares and/or MAAC Warrants and therefore may have a conflict of interest in determining whether a particular target business is an appropriate business with which to effectuate our initial business combination. MAAC’s board of directors was aware of and considered this, among other matters, in approving the Business Combination Agreement and in |

10

Table of Contents

| recommending that the Business Combination be approved by MAAC’s stockholders of MAAC. See “The Business Combination Proposal—Business Combination—Interests of Certain MAAC Persons in the Business Combination.” |

| Q: | WHAT DO I NEED TO DO NOW? |

| A: | After carefully reading and considering the information contained in this proxy statement/prospectus, please submit your proxies as soon as possible so that your shares will be represented at the MAAC Special Meeting. Please follow the instructions set forth on the proxy card or on the voting instruction card provided by your broker, bank or other nominee if your shares are held in the name of your broker, bank or other nominee. |

| Q: | HOW DO I VOTE? |

| A: | If you are a stockholder of record of MAAC as of , 2021, the record date, you may submit your proxy before the MAAC Special Meeting in any of the following ways, if available: |

| • | use the toll-free number shown on your proxy card; |

| • | visit the website shown on your proxy card to vote via the Internet; or |

| • | complete, sign, date and return your proxy card in the enclosed postage-paid envelope. |

Stockholders who choose to participate in the MAAC Special Meeting can vote their shares electronically during the meeting via live audio webcast by visiting www. .com. You will need the control number that is printed on your proxy card to enter the MAAC Special Meeting. MAAC recommends that you log in at least 15 minutes before the meeting to ensure you are logged in when the MAAC Special Meeting starts.

If your shares are held in “street name” through a broker, bank or other nominee, your broker, bank or other nominee will send you separate instructions describing the procedure for voting your shares. “Street name” stockholders who wish to vote at the MAAC Special Meeting will need to obtain a legal proxy from their broker, bank or other nominee.

| Q: | WHEN AND WHERE IS THE MAAC SPECIAL MEETING? |

| A: | The MAAC Special Meeting of stockholders will be held on , 2021, unless postponed or adjourned to a later date. In light of the COVID-19 pandemic and to support the well-being of MAAC’s stockholders and employees, the MAAC Special Meeting will be completely virtual. All MAAC stockholders as of the record date, or their duly appointed proxies, may attend the MAAC Special Meeting. Registration will begin at Eastern Time. |

| Q: | HOW CAN MAAC’S STOCKHOLDERS ATTEND THE SPECIAL MEETING? |

| A: | If you are a registered stockholder, you will receive a proxy card from MAAC’s transfer agent, CST. Your proxy card contains instructions on how to attend the virtual MAAC Special Meeting including the URL address, along with your control number. You will need your control number to vote at the MAAC Special Meeting. If you do not have your control number, contact CST at the phone number or e-mail address below. CST’s contact information is as follows: , or email . |

You can pre-register to attend the virtual MAAC Special Meeting three days prior to the meeting date starting , 2021 at Eastern Time. Enter the URL address into your browser , enter your control number, name and email address. Once you pre-register you can vote or enter questions in the chat box. At the start of the meeting you will need to re-log in using your control number and will also be prompted to enter your control number if you vote during the meeting. MAAC recommends that you log in at least 15 minutes before the meeting to ensure you are logged in when the MAAC Special Meeting starts.

11

Table of Contents

If your shares are held in “street name” in a stock brokerage account or by a broker, bank or other nominee, you will need to contact CST to receive a control number. If you plan to vote at the MAAC Special Meeting you will need to have a legal proxy from your bank, broker, or other nominee or if you would like to join and not vote CST will issue you a guest control number with proof of ownership. In either case, you must contact CST for specific instructions on how to receive the control number. Please allow 72 hours prior to the meeting for processing your control number.

If you do not have internet capabilities, you can listen only to the meeting by dialing +1 (toll-free) inside the U.S. and Canada or +1 (standard rates apply), and when prompted enter the pin number #. This is listen-only, you will not be able to vote or enter questions during the meeting.

| Q: | WHY IS THE SPECIAL MEETING A VIRTUAL MEETING? |

| A: | MAAC has decided to hold the MAAC Special Meeting virtually due to the COVID-19 pandemic. MAAC is sensitive to the public health and travel concerns of MAAC’s stockholders and employees and the protocols that federal, state and local governments may impose. MAAC believes that hosting a virtual meeting will enable greater stockholder attendance and participation from any location around the world. |

| Q: | WHAT IF DURING THE CHECK-IN TIME OR DURING THE SPECIAL MEETING I HAVE TECHNICAL DIFFICULTIES OR TROUBLE ACCESSING THE VIRTUAL MEETING WEBSITE? |

| A: | If you encounter any difficulties accessing the virtual meeting during the check-in or meeting time, please call the technical support number that will be posted on the virtual stockholder meeting log in page. |

| Q: | IF MY SHARES ARE HELD IN “STREET NAME” BY A BROKER, BANK OR OTHER NOMINEE, WILL MY BROKER, BANK OR OTHER NOMINEE VOTE MY SHARES FOR ME? |

| A: | If your shares are held in “street name” in a stock brokerage account or by a broker, bank or other nominee, you must provide the record holder of your shares with instructions on how to vote your shares. Please follow the voting instructions provided by your broker, bank or other nominee. Please note that you may not vote shares held in “street name” by returning a proxy card directly to MAAC or by voting online at the MAAC Special Meeting unless you provide a “legal proxy,” which you must obtain from your broker, bank or other nominee. |

Pursuant to applicable rules, brokers who hold shares in “street name” for a beneficial owner of those shares typically have the authority to vote in their discretion on “routine” proposals when they have not received instructions from beneficial owners. However, brokers are not permitted to exercise their voting discretion with respect to the approval of matters that the Nasdaq determines to be “non-routine” without specific instructions from the beneficial owner. It is expected that all proposals to be voted on at the MAAC Special Meeting will be “non-routine” matters.

If you are a holder of MAAC Shares holding your shares in “street name” and you do not instruct your broker, bank or other nominee on how to vote your shares, your broker, bank or other nominee will not vote your shares on any of the proposals presented in this proxy statement/prospectus. The failure of your broker to vote will have no effect on the vote count for such proposals.

| Q: | WHAT HAPPENS IF I SELL MY MAAC CLASS A SHARES BEFORE THE MAAC SPECIAL MEETING? |

| A: | The record date for the MAAC Special Meeting will be earlier than the date of the consummation of the Business Combination. If you transfer your MAAC Class A Shares after the record date, but before the MAAC Special Meeting, unless the transferee obtains from you a proxy to vote those shares, you will retain |

12

Table of Contents

| your right to vote at the MAAC Special Meeting. However, you will not be able to seek redemption of your MAAC Class A Shares because you will no longer be able to deliver them for cancellation upon the consummation of the Business Combination in accordance with the provisions described herein. If you transfer your MAAC Class A Shares prior to the record date, you will have no right to vote those shares at the MAAC Special Meeting or redeem those shares for a pro rata portion of the proceeds held in the Trust Account. |

| Q: | WHAT IF I ATTEND THE MAAC SPECIAL MEETING AND ABSTAIN OR DO NOT VOTE? |

| A: | For purposes of the MAAC Special Meeting, an abstention occurs when a stockholder attends the meeting online and does not vote or returns a proxy with an “abstain” vote. |

If you are a holder of MAAC Shares that attends the MAAC Special Meeting virtually and fails to vote, or if you vote abstain, your failure to vote or abstention will have the same effect as a vote “AGAINST” the Business Combination Proposal, the Nasdaq Proposal and the Adjournment Proposal. Broker non-votes, while considered present for the purposes of establishing a quorum, will not count as shares entitled to vote or votes cast at the MAAC Special Meeting, and otherwise will have no effect on the Nasdaq Proposal and Adjournment Proposal. Broker non-votes will have the same effect as a vote “AGAINST” the Business Combination Proposal.

| Q: | WHAT WILL HAPPEN IF I RETURN MY PROXY CARD WITHOUT INDICATING HOW TO VOTE? |

| A: | If you sign and return your proxy card without indicating how to vote on any particular proposal, the MAAC Shares represented by your proxy will be voted as recommended by MAAC’s board of directors with respect to that proposal. |

| Q: | MAY I CHANGE MY VOTE AFTER I HAVE DELIVERED MY PROXY OR VOTING INSTRUCTION CARD? |

| A: | Yes. You may change your vote at any time before your proxy is voted at the MAAC Special Meeting (provided that you do not hold your shares through a broker, bank or other nominee). |

You may do this in one of two ways:

| • | mailing a new, subsequently dated proxy card; or |

| • | by attending the MAAC Special Meeting virtually and electing to vote your shares online at the meeting. |