SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

Pursuant to Rule 13a-16 or 15d-16 under

the Securities Exchange Act of 1934

For the Month of March, 2017

Commission File Number: 001-37668

FERROGLOBE PLC

(Name of Registrant)

2nd Floor West Wing, Lansdowne House

57 Berkeley Square

London, W1J 6ER

(Address of Principal Executive Office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ☐

Indicate by check mark whether by furnishing the information contained in this Form, the registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ☐ No ☒

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): N/A

This Form 6-K consists of the following materials, which appear immediately following this page:

▪ Press release dated March 16, 2017 announcing results for the quarter and year ended December 31, 2016

▪ Fourth quarter and year-end earnings call presentation

2

Ferroglobe Reports Results for Fourth Quarter and Full Year 2016

| · | Q4 2016 revenue of $394.4 million, up from $364.7 million in Q3 2016; FY 2016 revenue of $1,580.5 million, down from $2,039.6 million in FY 2015 |

| · | Q4 2016 net loss of $(44.4) million, or $(0.23) on a fully diluted per share basis; FY 2016 net loss of $(156.7) million, or $(0.79) on a fully diluted per share basis |

| · | Q4 2016 adjusted net loss of $(16.9) million, or $(0.09) on a fully diluted per share basis; FY 2016 adjusted net loss of $(40.6) million, or $(0.24) on a fully diluted per share basis |

| · | Q4 2016 reported EBITDA loss of $(23.3) million, which includes executive severance expense of $24.4 million and impairment losses of $7.9 million; FY 2016 reported EBITDA loss of $(51.9) million, which includes impairment losses of $79.9 million and executive severance expense of $24.4 million |

| · | Q4 2016 adjusted EBITDA of $9.1 million, down from $12.8 million in the previous quarter; FY 2016 adjusted EBITDA of $72.9 million, down from $294.8 million year-over-year |

| · | Q4 2016 operating cash flow generation of $38.1 million and free cash flow generation of $20.3 million; FY 2016 operating cash flow generation of $114.4 million and free cash flow generation of $75.9 million |

| · | Exceeded working capital synergies target of $100 million by reducing working capital by $192.0 million in FY 2016 |

| · | Captured $57 million in synergies for FY 2016, and reached a level of $72 million in run-rate synergies in Q4 2016; on track to achieve $85 million of total annual synergies in 2017 |

LONDON, March 16, 2017 – Ferroglobe PLC (NASDAQ: GSM), the world’s leading producer of silicon metal, and a leading silicon- and manganese-based specialty alloys producer, announced today results for the fourth quarter and fiscal year of 2016.

In the fourth quarter of 2016, Ferroglobe posted a net loss of $(44.4) million, or $(0.23) per share on a fully diluted basis. In the fiscal year of 2016, Ferroglobe posted a net loss of $(156.7) million, or $(0.79) per share on a fully diluted basis. Excluding impairment losses, executive severance expense and other non-recurring items on an after tax basis, the company posted an adjusted net loss of $(16.9) million, or $(0.09) per share on a fully diluted basis for the quarter, and an adjusted net loss of $(40.6) million, of $(0.24) per share on a fully diluted basis for the year.

Ferroglobe reported an EBITDA loss of $(23.3) million for the fourth quarter of 2016 after charging executive severance expense of $24.4 million and impairment losses of $7.9 million. Excluding these charges, adjusted EBITDA for the fourth quarter of 2016 was $9.1 million. For full year of 2016, Ferroglobe reported an EBITDA loss of $(51.9) million due to impairment losses of $79.9 million and executive severance expense of $24.4 million. Excluding these charges, adjusted EBITDA for the full year of 2016 was $72.9 million.

Net sales in the fourth quarter of 2016 totaled $394.4 million, up from $364.7 million in the third quarter of 2016. Net sales in the full year of 2016 totaled $1,580.5 million, down from $2,039.6 million year-over-year. Over the course of the fourth quarter of 2016, spot prices for Ferroglobe’s key products in the United States and Europe increased substantially as compared to the third quarter of 2016. However, this increase has not been reflected in Ferroglobe´s selling prices due to time lags in certain contracts and the existence of fixed priced contracts:

| · | In the fourth quarter of 2016, the average selling price for silicon metal was relatively flat from the previous quarter. |

| · | During the fourth quarter, the average selling price for silicon-based alloys decreased 3.2% from the third quarter of 2016 and the average selling price for manganese alloys increased 3.1% from the third quarter of 2016. |

| · | During the full year of 2016, the average selling price for silicon metal declined 18.9%, the average selling price for silicon-based alloys decreased 15.8% and the average selling price for manganese alloys decreased 15.6%, each as compared to the average selling price for the full year of 2015. |

3

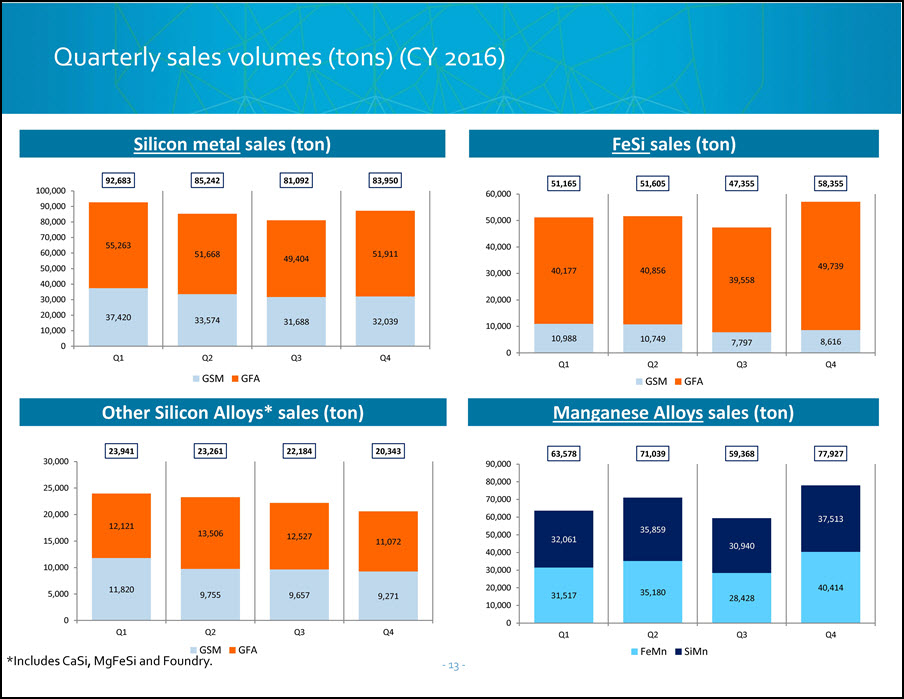

In terms of sales volumes, in the fourth quarter of 2016, silicon metal experienced a 3.53% increase quarter-over-quarter, silicon alloys experienced a 13.17% increase quarter-over-quarter, and manganese alloys experienced a 31.26% increase quarter-over-quarter, reflecting recovery in the market.

| Year Ended December 31, 2016 | Quarter Ended December 31, 2016 | Quarter Ended September 30, 2016 | Pro forma for the Year Ended December 31, 2015 ** | |||||||||||||

| Shipments in metric tons: | ||||||||||||||||

| Silicon Metal | 342,966 | 83,950 | 81,091 | 373,355 | ||||||||||||

| Silicon Alloys | 296,969 | 78,698 | 69,539 | 323,761 | ||||||||||||

| Manganese Alloys | 271,912 | 77,927 | 59,368 | 264,022 | ||||||||||||

| Total shipments* | 911,847 | 240,575 | 209,998 | 961,138 | ||||||||||||

| Year Ended December 31, 2016 | Quarter Ended December 31, 2016 | Quarter Ended September 30, 2016 | Pro forma for the Year Ended December 31, 2015 ** | |||||||||||||

| Average selling price ($/MT): | ||||||||||||||||

| Silicon Metal | $ | 2,200 | $ | 2,075 | $ | 2,090 | $ | 2,713 | ||||||||

| Silicon Alloys | $ | 1,403 | $ | 1,340 | $ | 1,391 | $ | 1,668 | ||||||||

| Manganese Alloys | $ | 827 | $ | 892 | $ | 865 | $ | 986 | ||||||||

| Total* | $ | 1,531 | $ | 1,451 | $ | 1,512 | $ | 1,887 | ||||||||

| Year Ended December 31, 2016 | Quarter Ended December 31, 2016 | Quarter Ended September 30, 2016 | Pro forma for the Year Ended December 31, 2015 ** | |||||||||||||

| Average selling price ($/lb.): | ||||||||||||||||

| Silicon Metal | $ | 1.00 | $ | 0.94 | $ | 0.95 | $ | 1.23 | ||||||||

| Silicon Alloys | $ | 0.64 | $ | 0.61 | $ | 0.63 | $ | 0.76 | ||||||||

| Manganese Alloys | $ | 0.38 | $ | 0.40 | $ | 0.39 | $ | 0.45 | ||||||||

| Total* | $ | 0.69 | $ | 0.66 | $ | 0.69 | $ | 0.86 | ||||||||

* Excludes by-products and other.

** Represents combined Globe and FerroAtlantica results on a pro forma basis.

“Our fourth quarter earnings are in line with the guidance provided at our recent trading update. Stabilized pricing along with strong demand resulted in a more than 8% revenue increase from the prior quarter,” said CEO Pedro Larrea. “Overall, market trends continue to move in our favor with gradual price improvements in silicon metal and silicon alloys and a dramatic increase in manganese alloys margins. We continue to see strong demand in our end markets and have entered into sales contracts for 2017 that are 15-20% above fourth quarter spot prices, partially offset in the short term by the roll-off of high-priced legacy contracts. After one year as a combined company, we have successfully integrated the organization, captured enhanced synergies, strengthened our commercial strategy and restructured our balance sheet, setting us up for a healthy improvement of our financials in the wake of the market recovery.”

Mr. Larrea concluded, “We recently filed a petition with the U.S. Department of Commerce and the U.S. International Trade Commission, as well as a separate complaint with the Canada Border Services Agency, seeking relief from unfairly traded, low-priced imports in North America. Favorable decisions in these proceedings will positively impact our profitability.”

Recent developments

On February 1, 2017, Ferroglobe announced the pricing of $350,000,000 aggregate principal amount of Senior Notes due 2022. The Notes, co-issued with Globe and guaranteed by certain of Ferroglobe’s other subsidiaries, bear interest at an annual rate of 9.375% and were issued at 100% of their nominal value. The proceeds from the offering of the Notes were used primarily to repay certain existing indebtedness.

4

On February 1, 2017, Ferroglobe announced that it has entered into a definitive agreement to sell the hydro-electric operations of its non-core Energy segment in Spain for estimated gross cash proceeds of €255 million (approximately $270 million). The company continues to work with the relevant governmental authorities in order to obtain the necessary regulatory approvals.

On February 20, 2017, the Canada Border Services Agency announced that is launching an investigation into whether or not certain silicon metal originating in or exported from Brazil, Kazakhstan, Malaysia, Norway and Thailand is being sold at unfair prices in Canada. It will also investigate whether or not subsidies are being applied to certain silicon metal originating in or exported from these five countries.

On March 8, 2017, Globe Specialty Metals, Inc. (“Globe”) a subsidiary of Ferroglobe, filed a petition with the U.S. Department of Commerce and the U.S. International Trade Commission to stop and provide relief from unfairly traded silicon metal imports from Brazil, Kazakhstan, Norway and Australia. Globe’s petitions outlined deliberate practices by producers from these four countries to sell silicon metal at artificially low prices in the U.S.

In another development, Ferroglobe’s Executive Chairman Javier López Madrid has advised the company that a ruling was issued by the Spanish High Court (Audiencia Nacional) on February 23, 2017, pursuant to which he has been convicted, together with 64 other former directors or executives of Bankia, S.A. and/or Caja Madrid, of certain charges as an accessory (not as an author) in connection with the alleged misuse of corporate credit cards for €34,807.81 in expenditures between 2010 and 2012 while he was a non-executive director of Bankia, S.A. and Caja Madrid (this proceeding has previously been disclosed by Ferroglobe in its regulatory filings). The directors and executives of the bank over a period of 25 years were granted corporate credit cards as part of their remuneration, an arrangement that has been deemed unlawful pursuant to the ruling. All these events took place prior to Mr. López Madrid joining Ferroglobe. Mr. López Madrid has advised the company that he has filed an appeal with the Spanish Supreme Court (Tribunal Supremo) in response to the ruling and will continue to defend himself vigorously in this matter. The Ferroglobe Board of Directors has reviewed the developments in this legal proceeding, agreed that Mr. López Madrid remain as a director and continues to support him in his role as Executive Chairman.

Focus on cost management, cash-flow generation and synergy attainment

Ferroglobe reported an EBITDA loss of $(23.3) million for the fourth quarter of 2016. Excluding charges related to asset and inventory impairments, and executive severance expense, adjusted EBITDA for the fourth quarter of 2016 was $9.1 million.

Ferroglobe maintains its expectations for synergy attainment to $85 million on an annual basis, up from $65 million previously. The company has achieved a total of $57 million of savings from synergies for the full year of 2016, implying a run-rate of $72 million in the fourth quarter of 2016. Production costs were reduced by 13% for the full year of 2016.

Ferroglobe generated operating cash flows of $38.1 million in the fourth quarter of 2016, and $114.4 million for the full year of 2016. Part of the operating cash flows comes from working capital improvements of $54.7 million during the fourth quarter of 2016, bringing improvements for the full year of 2016 to $191.2 million. The company generated $75.9 million of free cash flow in the fiscal year of 2016, of which $20.3 million was generated during the fourth quarter of 2016.1 Ferroglobe’s net debt was $404.6 million at the end of the fourth quarter of 2016, compared to $430 million at the end of third quarter of 2016.

1 Free cash-flow defined as “Net cash provided by operating activities” minus “Payments for property, plant and equipment.”

5

Year Ended December 31, 2016 | Quarter Ended December 31, 2016 | Quarter Ended September 30, 2016 | ||||||||||

| Loss attributable to the parent | $ | (136,552 | ) | (40,092 | ) | (28,523 | ) | |||||

| Loss attributable to non-controlling interest | (20,186 | ) | (4,350 | ) | (2,545 | ) | ||||||

| Income tax benefit | (57,556 | ) | (19,137 | ) | (10,158 | ) | ||||||

| Net finance expense | 28,715 | 7,499 | 6,693 | |||||||||

| Exchange differences | 3,507 | 627 | 876 | |||||||||

| Depreciation and amortization charges, operating allowances and write-downs | 130,172 | 32,200 | 30,440 | |||||||||

| EBITDA | (51,900 | ) | (23,253 | ) | (3,217 | ) | ||||||

| Transaction and due diligence expenses | 7,979 | - | 111 | |||||||||

| Impairment loss | 74,465 | 6,834 | 9,043 | |||||||||

| Globe purchase price allocation adjustments | 10,022 | - | - | |||||||||

| Business interruption | 2,532 | - | 2,532 | |||||||||

| Inventory impairment | 5,410 | 1,080 | 4,330 | |||||||||

| Executive severance | 24,430 | 24,430 | - | |||||||||

| Adjusted EBITDA, excluding above items | $ | 72,938 | 9,091 | 12,799 | ||||||||

Year Ended December 31, 2016 | Quarter Ended December 31, 2016 | Quarter Ended September 30, 2016 | ||||||||||

| Diluted loss per ordinary share | (0.79 | ) | (0.23 | ) | (0.17 | ) | ||||||

| Tax rate adjustment | 0.06 | 0.01 | 0.01 | |||||||||

| Transaction and due diligence expenses | 0.03 | - | - | |||||||||

| Impairment loss | 0.29 | 0.03 | 0.04 | |||||||||

| Globe purchase price allocation adjustments | 0.04 | - | - | |||||||||

| Business interruption | 0.01 | - | 0.01 | |||||||||

| Inventory impairment | 0.02 | - | 0.02 | |||||||||

| Executive severance | 0.10 | 0.10 | - | |||||||||

| Adjusted diluted loss per ordinary share | (0.24 | ) | (0.09 | ) | (0.09 | ) | ||||||

Year Ended December 31, 2016 | Quarter Ended December 31, 2016 | Quarter Ended September 30, 2016 | ||||||||||

| Loss attributable to the parent | $ | (136,552 | ) | (40,092 | ) | (28,523 | ) | |||||

| Tax rate adjustment | 11,018 | 1,208 | 3,035 | |||||||||

| Transaction and due diligence expenses | 5,426 | - | 75 | |||||||||

| Impairment loss | 50,636 | 4,648 | 6,149 | |||||||||

| Globe purchase price allocation adjustments | 6,815 | - | - | |||||||||

| Business interruption | 1,722 | - | 1,722 | |||||||||

| Inventory impairment | 3,679 | 735 | 2,944 | |||||||||

| Executive severance | 16,612 | 16,612 | - | |||||||||

| Adjusted loss attributable to the parent | $ | (40,644 | ) | (16,889 | ) | (14,598 | ) | |||||

6

Conference Call

Ferroglobe will review the results for the fourth quarter of 2016 results during a conference call at 9:00 a.m. Eastern Time on March 17, 2017. The dial-in number for the call for participants in the United States is 877-293-5491 (conference ID 88145142). International callers should dial +1 914-495-8526 (conference ID 88145142). Please dial in at least five minutes prior to the call to register. The call may also be accessed via an audio webcast available at http://edge.media-server.com/m/p/qfukfe99.

About Ferroglobe

Ferroglobe PLC is one of the world’s leading suppliers of silicon metal, silicon-based specialty alloys, and ferroalloys serving a customer base across the globe in dynamic and fast-growing end markets, such as solar, automotive, consumer products, construction and energy. The company is based in London. For more information, visit http://investor.ferroglobe.com.

Forward-Looking Statements

This release contains “forward-looking statements” within the meaning of Section 27A of the United States Securities Act of 1933, as amended, and Section 21E of the United States Securities Exchange Act of 1934, as amended. Forward-looking statements are not historical facts but are based on certain assumptions of management and describe the company’s future plans, strategies and expectations. Forward-looking statements generally can be identified by the use of forward-looking terminology, including, but not limited to, “may,” “could,” “seek,” “guidance,” “predicts,” “potential,” “likely,” “believe,” “will,” “expect,” “anticipate,” “estimate,” “plan,” “intends” or “forecast,” variations of these terms and similar expressions, or the negative of these terms or similar expressions.

Forward-looking statements contained in this press release are based on information presently available to us and assumptions that we believe to be reasonable, but are inherently uncertain. As a result, our actual results, performance or achievements may differ materially from those expressed or implied by these forward-looking statements, which are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors that are, in some cases, beyond our control.

You are cautioned that all such statements involve risks and uncertainties, including, without limitation, risks that the legacy businesses of Globe and FerroAtlántica will not be integrated successfully or that we will not realize estimated cost savings, value of certain tax assets, synergies and growth, or that such benefits may take longer to realize than expected. Important factors that may cause actual results to differ include, but are not limited to: (i) risks relating to unanticipated costs of integration, including operating costs, customer loss and business disruption being greater than expected; (ii) our organizational and governance structure; (iii) the ability to hire and retain key personnel; (iv) regional, national or global political, economic, business, competitive, market and regulatory conditions including, among others, changes in metals prices; (v) increases in the cost of raw materials or energy; (vi) competition in the metals and foundry industries; (vii) environmental and regulatory risks; (viii) ability to identify liabilities associated with acquired properties prior to their acquisition; (ix) ability to manage price and operational risks including industrial accidents and natural disasters; (x) ability to manage foreign operations; (xi) changes in technology; (xii) ability to acquire or renew permits and approvals; (xiii) changes in legislation or governmental regulations affecting Ferroglobe; (xiv) conditions in the credit markets; (xv) risks associated with assumptions made in connection with critical accounting estimates and legal proceedings; (xvi) Ferroglobe’s international operations, which are subject to the risks of currency fluctuations and foreign exchange controls; and (xvii) the potential for international unrest, economic downturn or effects of currencies, tax assessments, tax adjustments, anticipated tax rates, raw material costs or availability or other regulatory compliance costs. The foregoing list is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties that affect our business, including those described in the “Risk Factors” section of our Annual Reports on Form 20-F, Current Reports on Form 6-K and other documents we file from time to time with the United States Securities and Exchange Commission. We do not give any assurance (1) that we will achieve our expectations or (2) concerning any result or the timing thereof, in each case, with respect to any regulatory action, administrative proceedings, government investigations, litigation, warning letters, consent decree, cost reductions, business strategies, earnings or revenue trends or future financial results. Forward-looking financial information and other metrics presented herein represent our key goals and are not intended as guidance or projections for the periods presented herein or any future periods.

7

All information in this press release is as of the date of its release. We do not undertake or assume any obligation to update publicly any of the forward-looking statements in this press release to reflect actual results, new information or future events, changes in assumptions or changes in other factors affecting forward-looking statements. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements. We caution you not to place undue reliance on any forward-looking statements, which are made only as of the date of this press release.

Non-GAAP Measures

EBITDA, adjusted EBITDA, adjusted loss attributable to the parent and adjusted diluted loss per ordinary share are pertinent non-GAAP financial metrics that Ferroglobe utilizes to measure its success.

Ferroglobe has included these financial metrics to provide supplemental measures of its performance. The company believes these metrics are important because they eliminate items that have less bearing on the company’s current and future operating performance and highlight trends in its core business that may not otherwise be apparent when relying solely on U.S. GAAP financial measures. Reconciliations of these measures to the comparable U.S. GAAP financial measures are provided above and in the attached financial statements.

* * *

INVESTOR CONTACT:

Ferroglobe PLC

Joe Ragan, US: 001-786-509-6925, UK: +44 (0) 7827 227 688

Chief Financial Officer

Email: jragan@ferroglobe.com

8

Ferroglobe PLC and Subsidiaries

Unaudited Condensed Consolidated Income Statement

(in thousands of U.S. dollars, except per share amounts)

Year Ended December 31, 2016 | Quarter Ended December 31, 2016 | Quarter Ended September 30, 2016 | Year Ended December 31, 2015* | |||||||||||||

| Sales | $ | 1,580,524 | $ | 394,365 | $ | 364,727 | $ | 2,039,608 | ||||||||

| Cost of sales | (1,049,994 | ) | (278,756 | ) | (236,631 | ) | (1,225,313 | ) | ||||||||

| Other operating income | 29,339 | 18,326 | 4,963 | 20,455 | ||||||||||||

| Staff costs | (294,629 | ) | (87,810 | ) | (67,586 | ) | (330,382 | ) | ||||||||

| Other operating expense | (243,594 | ) | (63,789 | ) | (60,490 | ) | (351,929 | ) | ||||||||

| Depreciation and amortization charges, operating allowances and write-downs | (130,172 | ) | (32,200 | ) | (30,440 | ) | (141,097 | ) | ||||||||

| Impairment losses | (75,089 | ) | (7,458 | ) | (9,044 | ) | (52,042 | ) | ||||||||

| Other gain (loss) | 1,543 | 1,869 | 844 | (3,473 | ) | |||||||||||

| Operating loss | (182,072 | ) | (55,453 | ) | (33,657 | ) | (44,173 | ) | ||||||||

| Finance income | 1,554 | 321 | 548 | 1,343 | ||||||||||||

| Finance expense | (30,269 | ) | (7,820 | ) | (7,241 | ) | (34,521 | ) | ||||||||

| Exchange differences | (3,507 | ) | (627 | ) | (876 | ) | 29,993 | |||||||||

| Loss before tax | (214,294 | ) | (63,579 | ) | (41,226 | ) | (47,358 | ) | ||||||||

| Income tax benefit (expense) | 57,556 | 19,137 | 10,158 | (62,546 | ) | |||||||||||

| Loss for the period | (156,738 | ) | (44,442 | ) | (31,068 | ) | (109,904 | ) | ||||||||

| Loss attributable to non-controlling interest | 20,186 | 4,350 | 2,545 | 13,308 | ||||||||||||

| Loss attributable to the parent | $ | (136,552 | ) | $ | (40,092 | ) | $ | (28,523 | ) | $ | (96,596 | ) | ||||

| EBITDA | (51,900 | ) | (23,253 | ) | (3,217 | ) | 96,924 | |||||||||

| Adjusted EBITDA | 72,938 | 9,091 | 12,799 | 294,799 | ||||||||||||

| Weighted average shares outstanding | ||||||||||||||||

| Basic | 171,838 | 171,838 | 171,838 | |||||||||||||

| Diluted | 171,838 | 171,838 | 171,838 | |||||||||||||

| Loss per ordinary share | ||||||||||||||||

| Basic | (0.79 | ) | (0.23 | ) | (0.17 | ) | ||||||||||

| Diluted | (0.79 | ) | (0.23 | ) | (0.17 | ) | ||||||||||

* Represents combined Globe and FerroAtlantica results on a pro forma basis.

9

Ferroglobe PLC and Subsidiaries

Unaudited Condensed Consolidated Statement of Financial Position

(in thousands of U.S. dollars)

| December 31, | September 30, | December 31, | ||||||||||

| 2016 | 2016 | 2015 | ||||||||||

| ASSETS | ||||||||||||

| Non-current assets | ||||||||||||

| Goodwill | $ | 402,491 | 402,491 | 403,929 | ||||||||

| Other intangible assets | 62,838 | 70,130 | 71,619 | |||||||||

| Property, plant and equipment | 900,199 | 929,217 | 1,012,367 | |||||||||

| Non-current financial assets | 15,668 | 10,541 | 9,672 | |||||||||

| Deferred tax assets | 49,242 | 55,228 | 36,098 | |||||||||

| Non-current receivables from related parties | 2,108 | 2,233 | - | |||||||||

| Other non-current assets | 20,828 | 21,302 | 20,615 | |||||||||

| Total non-current assets | 1,453,374 | 1,491,142 | 1,554,300 | |||||||||

| Current assets | ||||||||||||

| Inventories | 312,800 | 369,996 | 425,372 | |||||||||

| Trade and other receivables | 213,427 | 197,817 | 275,254 | |||||||||

| Current receivables from related parties | 14,763 | 10,312 | 10,950 | |||||||||

| Current income tax assets | 43,264 | 30,826 | 9,273 | |||||||||

| Current financial assets | 4,049 | 14,204 | 4,112 | |||||||||

| Other current assets | 24,521 | 13,236 | 10,134 | |||||||||

| Cash and cash equivalents | 196,982 | 119,166 | 116,666 | |||||||||

| Total current assets | 809,806 | 755,557 | 851,761 | |||||||||

| Total assets | $ | 2,263,180 | 2,246,699 | 2,406,061 | ||||||||

| EQUITY AND LIABILITIES | ||||||||||||

| Equity | $ | 1,093,353 | 1,170,774 | 1,294,973 | ||||||||

| Non-current liabilities | ||||||||||||

| Deferred income | 3,949 | 5,259 | 4,389 | |||||||||

| Provisions | 81,836 | 85,846 | 81,853 | |||||||||

| Bank borrowings | 179,879 | 96,870 | 223,676 | |||||||||

| Obligations under finance leases | 74,261 | 79,780 | 89,768 | |||||||||

| Other financial liabilities | 92,043 | 7,748 | 7,549 | |||||||||

| Other non-current liabilities | 5,737 | 4,295 | 4,517 | |||||||||

| Deferred tax liabilities | 159,142 | 178,577 | 206,648 | |||||||||

| Total non-current liabilities | 596,847 | 458,375 | 618,400 | |||||||||

| Current liabilities | ||||||||||||

| Provisions | 16,868 | 17,688 | 9,010 | |||||||||

| Bank borrowings | 241,412 | 357,004 | 182,554 | |||||||||

| Obligations under finance leases | 12,359 | 15,118 | 13,429 | |||||||||

| Other financial liabilities | 1,592 | - | - | |||||||||

| Payables to related parties | 8,320 | 6,220 | 7,827 | |||||||||

| Trade and other payables | 163,832 | 150,733 | 147,073 | |||||||||

| Current income tax liabilities | 5,300 | 4,987 | 10,887 | |||||||||

| Other current liabilities | 123,297 | 65,800 | 121,908 | |||||||||

| Total current liabilities | 572,980 | 617,550 | 492,688 | |||||||||

| Total equity and liabilities | $ | 2,263,180 | 2,246,699 | 2,406,061 | ||||||||

10

Ferroglobe PLC and Subsidiaries

Unaudited Condensed Consolidated Statement of Cash Flows

(in thousands of U.S. dollars)

Year Ended December 31, 2016 | Quarter Ended December 31, 2016 | Quarter Ended September 30, 2016 | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||||||

| Loss for the period | $ | (156,738 | ) | $ | (44,442 | ) | $ | (31,068 | ) | |||

| Adjustments to reconcile net loss to net cash provided by operating activities: | ||||||||||||

| Income tax benefit | (57,556 | ) | (19,137 | ) | (10,158 | ) | ||||||

| Depreciation and amortization charges, operating allowances and write-downs | 130,172 | 32,200 | 30,440 | |||||||||

| Finance income | (1,554 | ) | (321 | ) | (548 | ) | ||||||

| Finance expense | 30,269 | 7,820 | 7,241 | |||||||||

| Exchange differences | 3,507 | 627 | 876 | |||||||||

| Impairment losses | 75,089 | 7,458 | 9,044 | |||||||||

| Loss on disposals of non-current and financial assets | 308 | (100 | ) | 217 | ||||||||

| Other adjustments | (1,851 | ) | (6,099 | ) | 3,269 | |||||||

| Changes in operating assets and liabilities | ||||||||||||

| Decrease in inventories | 103,243 | 43,412 | 2,135 | |||||||||

| Decrease in trade receivables | 36,888 | (34,895 | ) | 17,547 | ||||||||

| Increase in trade payables | 30,662 | 29,569 | 9,834 | |||||||||

| Other* | (27,651 | ) | 31,853 | (603 | ) | |||||||

| Income taxes (paid) received | (23,437 | ) | (3,249 | ) | (8,911 | ) | ||||||

| Interest paid | (26,925 | ) | (6,619 | ) | (6,837 | ) | ||||||

| Net cash provided by operating activities | 114,426 | 38,077 | 22,478 | |||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||||||

| Payments due to investments: | ||||||||||||

| Other intangible assets | (4,184 | ) | (1,641 | ) | (2,020 | ) | ||||||

| Property, plant and equipment | (71,037 | ) | (17,748 | ) | (10,805 | ) | ||||||

| Non-current financial assets | (7,659 | ) | (6,975 | ) | (411 | ) | ||||||

| Current financial assets | (6 | ) | 9,924 | 3,988 | ||||||||

| Disposals: | ||||||||||||

| Intangible assets | - | - | - | |||||||||

| Property, plant and equipment | - | - | - | |||||||||

| Current financial assets | - | - | (99 | ) | ||||||||

| Interest received | 1,825 | (212 | ) | 1,328 | ||||||||

| Net cash used by investing activities | (81,061 | ) | (16,652 | ) | (8,019 | ) | ||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||||||

| Dividends paid | (54,988 | ) | (13,745 | ) | (27,496 | ) | ||||||

| Increase/(decrease) in bank borrowings: | ||||||||||||

| Borrowings | 200,182 | 94,851 | 22,362 | |||||||||

| Payments | (81,237 | ) | (23,539 | ) | (19,623 | ) | ||||||

| Other amounts paid due to financing activities | (14,040 | ) | (5,727 | ) | (3,750 | ) | ||||||

| Net cash provided (used) by financing activities | 49,917 | 51,840 | (28,507 | ) | ||||||||

| TOTAL NET CASH FLOWS FOR THE PERIOD | 83,282 | 73,265 | (14,048 | ) | ||||||||

| Beginning balance of cash and cash equivalents | 116,666 | 119,166 | 135,774 | |||||||||

| Exchange differences on cash and cash equivalents in foreign currencies | (2,966 | ) | 4,551 | (2,560 | ) | |||||||

| Ending balance of cash and cash equivalents | $ | 196,982 | $ | 196,982 | $ | 119,166 | ||||||

* Includes the cash outflow impact of the $32.5M shareholder settlement during the quarter ended March 31, 2016.

11

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Date: March 16, 2017 | |||

| FERROGLOBE PLC | |||

| By: | /s/ Nick Deeming | ||

| Name: Nick Deeming | |||

| Title: Corporate Secretary | |||

12

Advancing Materials Innovation NASDAQ: GSM Fourth Quarter 2016

Forward-Looking Statement This presentation contains forward-looking statements within the meaning of Section 27A of the United States Securities Act of 1933, as amended, and Section 21E of the United States Securities Exchange Act of 1934, as amended. Forward-looking statements are not historical facts but are based on certain assumptions of management and describe our future plans, strategies and expectations. Forward-looking statements can generally be identified by the use of forward-looking terminology, including, but not limited to, "may," “could,” “seek,” “guidance,” “predict,” “potential,” “likely,” "believe," "will," "expect," "anticipate," "estimate," "plan," "intend," "forecast," or variations of these terms and similar expressions, or the negative of these terms or similar expressions. Forward-looking statements contained in this presentation are based on information presently available to us and assumptions that we believe to be reasonable, but are inherently uncertain. As a result, our actual results, performance or achievements may differ materially from those expressed or implied by these forward-looking statements, which are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors that are, in some cases, beyond our control. You are cautioned that all such statements involve risks and uncertainties, including without limitation, risks that the businesses of Globe Specialty Metals Inc. and Grupo FerroAtlántica (together, “we,” “us,” “Ferroglobe,” the “Company”) will not be integrated successfully or that we will not realize estimated cost savings, value of certain tax assets, synergies and growth, or that such benefits may take longer to realize than expected. Important factors that may cause actual results to differ include, but are limited to: (i) risks relating to unanticipated costs of integration, including operating costs, customer loss and business disruption being greater than expected; (ii) our organizational and governance structure; (iii) the ability to hire and retain key personnel; (iv) regional, national or global political, economic, business, competitive, market and regulatory conditions including, among others, changes in metals prices; (v) increases in the cost of raw materials or energy; (vi) competition in the metals and foundry industries; (vii) environmental and regulatory risks; (viii) ability to identify liabilities associated with acquired properties prior to their acquisition; (ix) ability to manage price and operational risks including industrial accidents and natural disasters; (x) ability to manage foreign operations; (xi) changes in technology; (xii) ability to acquire or renew permits and approvals; (xiii) changes in legislation or governmental regulations affecting Ferroglobe; (xiv) conditions in the credit markets; (xv) risks associated with assumptions made in connection with critical accounting estimates and legal proceedings; (xvi) Ferroglobe's international operations, which are subject to the risks of currency fluctuations and foreign exchange controls; and (xvii) the potential of international unrest, economic downturn or effects of currencies, tax assessments, tax adjustments, anticipated tax rates, raw material costs or availability or other regulatory compliance costs. The foregoing list is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties that affect our business, including those described in the “Risk Factors” section of our Registration Statement on Form F-1, Annual Reports on Form 20-F, Current Reports on Form 6-K and other documents we file from time to time with the United States Securities and Exchange Commission. We do not give any assurance (1) that we will achieve our expectations or (2) concerning any result or the timing thereof, in each case, with respect to any regulatory action, administrative proceedings, government investigations, litigation, warning letters, consent decree, cost reductions, business strategies, earnings or revenue trends or future financial results. Forward- looking financial information and other metrics presented herein represent our key goals and are not intended as guidance or projections for the periods presented herein or any future periods. We do not undertake or assume any obligation to update publicly any of the forward- looking statements in this presentation to reflect actual results, new information or future events, changes in assumptions or changes in other factors affecting forward-looking statements. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements. We caution you not to place undue reliance on any forward-looking statements, which are made only as of the date of this presentation.

Table of contents Q4 overviewSelected financial highlights

Q4 overview

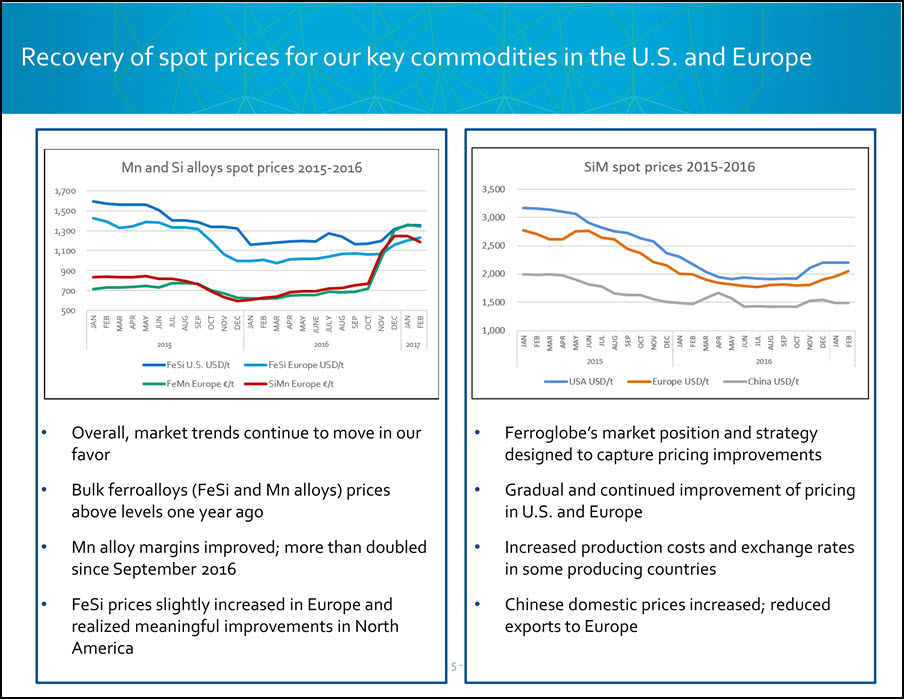

Source: Company information Silicon metal price of $0.94 per pound, down 0.7% Silicon-based alloys price of $0.61 per pound, down 3.3% Manganese alloys price of $0.40 per pound, up 3.1% Silicon metal (35% of sales): meaningful stabilization of prices Silicon alloy (33% of sales): Sales mix of lower-priced products impacted Q4 Manganese alloy (32% of sales): pricing continues to strengthen into 2017 Spot prices for key products stabilized in Q4

Recovery of spot prices for our key commodities in the U.S. and Europe Overall, market trends continue to move in our favorBulk ferroalloys (FeSi and Mn alloys) prices above levels one year agoMn alloy margins improved; more than doubled since September 2016 FeSi prices slightly increased in Europe and realized meaningful improvements in North America Ferroglobe’s market position and strategy designed to capture pricing improvements Gradual and continued improvement of pricing in U.S. and EuropeIncreased production costs and exchange rates in some producing countries Chinese domestic prices increased; reduced exports to Europe

Positive market outlook for 2017 Signs of meaningful improvements, with spot prices for key products in U.S. and Europe gaining momentum, driven by:Market starting to adjust to increased production costs in importing countries due to increased energy costs and to exchange ratesTight supply conditions in most of our products and geographiesContinued strong demand from our key end-markets due to global trends:For silicon metal: light-weighting of auto vehicles and increased demand for solar energyFor other products: infrastructure development and increased industrial activity Market trends Actions Ferroglobe is taking: our strategy Taking legal action to address unfairly priced silicon metal importsPrices well above reported indexesAchieved prices 10% above indexEntered into sales contracts for 2017 that are 15-20% above Q4 spot pricesSimilar trends across all geographies Removing all discounts to index in contract structure for silicon metalCapitalizing on supply shortage Favoring fixed prices, with shorter term if necessary Observing gradual price improvements in silicon metal and silicon alloys and a dramatic increase in manganese alloys margins

Recent business updates Antidumping and countervailing duty actions filed in the U.S. and Canada against Australia, Brazil, Kazakhstan, Malaysia, Norway and ThailandPetitions outlines deliberate practices by producers from these countries to sell silicon metal at artificially low prices in North AmericaFavorable decisions will positively impact our profitabilitySale of Spanish hydro-electric assets for ~$270m in gross proceedsContinuing to work diligently to obtain approvals and progress toward closing

Reported EBITDA loss of $(23.3) million for the quarter1 Adjusted EBITDA of $9.1 million for the quarterGenerated $20.3 million of free cash flow2 in Q4 2016 and $75.9 million for FY 2016Generated $191 million in working capital synergies for FY 2016, well ahead of original three-year projection of $100 million$54.7 million improvement in working capital in Q4 2016 Maintained strong balance sheetNet debt of $404.6 million at end of Q4; flat versus end of 2015 1 Reported EBITDA, which includes executive severance expense of $24.4 million and impairment losses of $7.9 million2 Free cash flow defined as “Net cash provided by operating activities” minus “Payments for property, plant and equipment.” Source: Company information Financial discipline combined with approach to sales delivering results

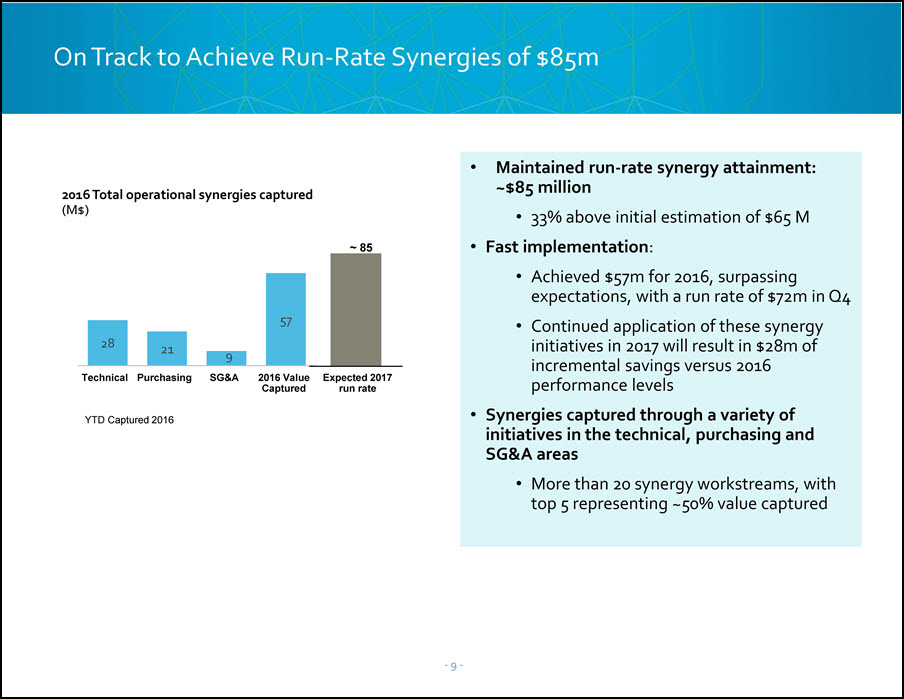

Maintained run-rate synergy attainment: ~$85 million33% above initial estimation of $65 MFast implementation:Achieved $57m for 2016, surpassing expectations, with a run rate of $72m in Q4Continued application of these synergy initiatives in 2017 will result in $28m of incremental savings versus 2016 performance levelsSynergies captured through a variety of initiatives in the technical, purchasing and SG&A areasMore than 20 synergy workstreams, with top 5 representing ~50% value captured On Track to Achieve Run-Rate Synergies of $85m Purchasing SG&A 2016 Value Captured Technical YTD Captured 2016 Expected 2017 run rate 2016 Total operational synergies captured(M$) 9

Opportunities for long-term value creation Strong balance sheet gives company ability to grow organically and inorganically Generating cash flow, even in down cycle and identifying non-core asset divestitures Strong market position and multiple levers to pull given diversified products, end markets & geographies Tight cost control puts the company in the optimal position for a price recovery

Selected financial highlights

Q4 key performance indicators and overview 1 Free cash flow defined as “Net cash provided by operating activities” minus “Payments for property, plant and equipment.”Source: Company information Key performance indicators FY 2016 Q4 2016 Q3 2016 Pro Forma CY 2015 Sales ($m) 1,580.5 394.4 364.7 2,039.6 Operating Profit ($m) -182.1 -55.5 -33.7 -44.2 Profit Attributable to the Parent ($m) -136.6 -40.1 -28.5 -96.6 Adjusted EBITDA ($m) 72.9 9.1 12.8 294.8 Adjusted EBITDA Margin 4.6% 2.3% 3.5% 14.5% Working capital ($m) 191.2 54.7 417.1 553.6 Free Cash Flow1 ($m) 75.9 20.3 11.7 113.3

Silicon metal sales (ton) FeSi sales (ton) Other Silicon Alloys* sales (ton) Manganese Alloys sales (ton) Quarterly sales volumes (tons) (CY 2016) *Includes CaSi, MgFeSi and Foundry.

Refinancing Update Issued senior notes due 2022 bearing 9.375% interest rate$350m aggregate principal amount Issued at 100% nominal value Amendment to GSM’s existing revolving credit facility $200 million aggregate principal amount Expiring in 2018

Balance sheet summary ($mm) 12/31/20161 Q3 20161 12/31/2015 Total Assets 2,263 2,247 2,406 Net Debt2 405 430 393 Book Equity 1,093 1,171 1,295 Net Debt2 / Total Assets 17.9% 19.5% 16.3% Net Debt2 / Capital3 27.0% 27.2% 23.3% Financial results are unauditedNet Debt includes finance lease obligationsCapital is calculated as book equity plus net debt

Q&A

Advancing Materials Innovation NASDAQ: GSM Fourth Quarter 2016