May 10, 2021

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, NE

Washington, DC 20549

Attention: | Lily Dang |

| Karl Hiller |

|

|

Re: | Leafbuyer Technologies, Inc. Form 10-K for the Fiscal Year Ended June 30, 2020 Filed September 25, 2020 File No. 000-55855 |

Ladies and Gentlemen:

Please accept this letter as the responses of Leafbuyer Technologies, Inc. (the “Company”) to the comments of the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) set forth in the letter from the Division of Corporation Finance dated March 25, 2021 (the “Comment Letter”) with respect to Leafbuyer Technologies, Inc. Form 10-K for the fiscal year ended June 30, 2020 (the “Form 10-K”).

For ease of reference, we have repeated each of the Staff’s comments below, followed by the corresponding response of the Company.

Form 10-K for the Fiscal Year Ended June 30, 2020

Part IV

Exhibit and Financial Statement Schedules, page 27

| 1. | We see that you plan to amend your filing to include some of the missing exhibits in response to prior comment 1. However, among the exhibits that you have identified for inclusion, we do not see the debt agreements required by Item 601(b)(4)(iii)(A), where the total amount of securities authorized exceeds 10 percent of total assets, nor the material contracts required by Item 601(b)(10)(i) and (ii)(A), (B) and (C). |

|

|

|

|

| Please amend your most recent annual report to include all of the exhibits that would have been required upon filing that report, including exhibits that were required but not provided at each periodic reporting date since your reorganization in 2017. Please also amend your most recent interim report to include any exhibits that were required but not provided, considering events subsequent to your most recently completed fiscal year. |

Answer to Comment 1: The Company will amend the Form 10-K in order to produce Exhibits 3.1 (Articles of Incorporation), 3.2 (Bylaws), 4.1 (Description of Securities), 4.3 (Certificate of Designation for Series A Preferred stock), 4.4 (Certificate of Designation for Series B Preferred stock), and 10.3 (2017 Equity Incentive Plan). Exhibit numbers 3.1, 3.2, 4.3, 4.4, and 10.3 will be incorporated by reference, while Exhibit 4.1 will be filed with the amended Form 10-K. The Company will also amend the exhibit lists in the 10-K and the interim report to produce the exhibits required by Item 601(b)(4)(iii)(A) and 601(b)(10)(i) and (ii)(A), (B) and (C).

| 1 |

Financial Statements

Note 4 – Capital Stock and Equity Transactions, page 41

| 2. | We note your response to prior comment 2 and your proposed revisions indicating the 3 million Series A preferred shares would convert into 46,313,430 common shares based upon 82,892,802 common shares outstanding as of June 30, 2020. However, the conversion provisions described in Section 3(c) of the Certificate of Designation at Exhibit 4.2 to the Form 8-K that you filed on March 29, 2017 states "...upon conversion, the holders of the Series A Preferred Stock would hold shares of Common Stock constituting 55.0% of the Fully-Diluted Shares after giving effect to such conversion." Given this provision, it appears you would need to consider, in addition to the number of issued and outstanding shares, any shares issuable pursuant to other convertible instruments, and the number of shares that would be issued to satisfy conversion of the Series A preferred stock, in determining the number of fully diluted shares to which the prescribed percentage would apply. It also appears that you would need to consider the number of common shares currently held by the three individuals to determine the incremental number of common shares that would be issued to secure their 55% ownership interest, as indicated in the Certificate of Designation. |

|

|

|

|

| However, in response to prior comment 4 you state, "The counterparties do not hold any instruments that are considered in the computation of the conversion of the Series A Preferred stock." If this were correct, then based solely on the number of outstanding common shares as of June 30, 2020, and setting aside for purposes of illustration other convertible instruments that would be counted in a measure of fully diluted shares, you would need to issue 101,313,425 shares to satisfy conversion, which would yield 184,206,227 shares; the number of issuable shares would represent 55% of this total. A similar re-computation would be necessary to correct the number of shares that you indicate were issuable as of June 30, 2019. You indicate the Series A preferred shares were convertible into 5,371,630 common shares, based on 47,914,967 issued and outstanding common shares. In this instance, following the basis for illustration outlined above, you would need to have issued 58,562,737 shares to satisfy conversion.

However, if holders of the Series A preferred shares also hold 21,750,000 shares of common stock, which would be considered based on the formula utilized in establishing the initial conversion rate in the Certificate of Designation, the issuable number of shares would appear to have been 52,980,091 to yield a 55% interest as of June 30, 2020, and 10,229,404 to yield a 55% as of June 30, 2019, before considering other convertible instruments which would increase the numbers of issuable shares.

Please revise your disclosures as necessary to reflect an accurate computation of the number of shares issuable pursuant to the Series A preferred stock conversion provisions, also to include the conversion price and description of events that could change the number of issuable shares, as previously requested. Please refer to FASB ASC 505-10-50-6 though 50-9 for additional disclosure requirements. |

| 2 |

Answer to Comment 2: The Company will amend the Series A Preferred Certificate of Designation, in order remove the variable conversion feature. The new Certificate of Designation will provide for the same voting preferences as the current Certificate of Designation, but the conversion ability will be modified to only allow for a conversion to common stock on a 1:1 basis. The Company believes that by removing the variable conversion feature, many of the comments from the Staff can be resolved, and the Company believes that it will be able to present its capital stock structure in a way that is more easily understood by our shareholders and potential investors.

| 3. | We note that you have not addressed the specific accounting requirements for beneficial conversion features as requested in prior comment 3. Given the adjustable conversion rates associated with your Series A preferred stock, it appears that you would need to recognize the value of the adjustments as they occur upon each transaction that increases the number of Fully Diluted Shares, as described in Section 3(c) of the Certificate of Designation, to comply with FASB ASC 470-20-35-1, 30-5, and 35-7(c)(1), applicable pursuant to FASB ASC 470-20-15-2. Please also disclose the beneficial conversion amounts recognized along with the change in conversion prices for each period since origination. In conjunction with the foregoing, unless you believe this guidance does not apply to you, please also adhere to FASB ASC 260-10-45-11 and 12, and SAB Topic 6:B, in accounting for the deemed dividends in your EPS computations and in presenting income available to common stockholders on your Statements of Operations. |

Answer to Comment 3: The Company believes that by removing the variable conversion feature of the Series A Preferred Stock through an amendment to the Certificate of Designation, the Company believes that the issues raised in Comment 3 would be resolved, as there would be no need to address specific accounting requirements related to a beneficial conversion feature.

| 4. | We note that you did not comply with prior comment 4 in which we asked you to provide further disclosure in your periodic reports of the conversion provisions pertaining to the Series A preferred stock, including the implications of any change in common shares or common share equivalents held by the preferred share holders. On this point, you state "The counterparties do not hold any instruments that are considered in the computation of the conversion of the Series A Preferred stock." Please reconcile your statement with the description of the Conversion Rate in Section 3(c) of the Certificate of Designation, which explains that the initial conversion rate of 1:1 was based on 45 million shares outstanding on a Fully-Diluted Basis, "consisting of (i) 38,000,000 shares of Common Stock, (ii) 3,000,000 shares of Common Stock issuable upon conversion of Series A Convertible Preferred Stock, and (iii) 4,000,000 shares of Common Stock issuable upon conversion of Series B Convertible Preferred Stock, so that upon conversion, the holders of the Series A Preferred Stock would hold shares of Common Stock constituting 55.0% of the Fully-Diluted Shares after giving effect to such conversion." This formula, as described, indicates an initial conversion rate of 1:1 would yield the desired result, i.e. with 3 million Series A preferred shares converting into 3 million common shares; and since 55% of the 45 million Fully Diluted Shares would be 24.75 million, this implies that your three officers held 21,750,000 common shares that were being counted in establishing the initial conversion rate. |

| 3 |

|

| This is confirmed on page 3 of the Form 8-K that you filed March 29, 2017, in the tabulation and footnote clarifying that 891,894 beneficial shares attributed to each of your three officers includes one-third of the 324,327 pre-split Series A preferred shares, thereby indicating common shareholdings of 783,785 pre-split shares each, or 2,351,355 in total which is approximately 21,750,034 after the 9.25 for 1 stock split that you conducted in March 2017.

If you believe these provisions are invalid or no longer apply due to subsequent changes in the Certificate of Designation, explain your rationale and provide us with any supporting documentation. Otherwise, it appears that you should provide the disclosures required by FASB ASC 505-10-50-6 in your periodic reports, as previously requested. Please address those requirements relative to the provisions in the Certificate of Designation, notwithstanding the intent of your officers.

For example, although you indicate there is no intention to conduct partial conversions, Section 3(a) of the Certificate of Designation states that "Each Holder shall have the right to convert, at any time and from time to time, all or any part of the Series A Preferred Stock held by such Holder...." We reissue prior comment 4. |

Answer to Comment 4: As provided in the answers to Comments 2 and 3, the Company believes that by removing the variable conversion feature of the Series A Preferred Stock through an amendment to the Certificate of Designation, which the Company will file upon approval of these comment responses, allowing for only a 1:1 conversion ability, the issues raised in Comment 4 would be resolved, as there would be no need to address specific accounting requirements related to a beneficial conversion feature.

| 5. | We note that you have listed various figures in your response to prior comment 5 along with an assertion that the total represents fully diluted shares and does not exceed your current 150 million authorized common shares. |

|

|

|

|

| Please tabulate the figures listed in your response and augment as necessary to illustrate, with separate columns for each fiscal year-end subsequent to issuing the Series A preferred shares, and as of the end of your most recently completed interim period, your computations of fully diluted shares and of common shares issuable pursuant to the Series A preferred stock. Include cross references with your tabulation to the specific pages of your financial reports for each component associated with a convertible instrument, and your calculations of shares issuable to settle those instruments, including detailed explanations of your approach and rationale. Tell us how you define Fully Diluted Shares for the purpose of conducting these computations.

Please demonstrate how the shares that you believe would be issuable to settle the Series A preferred shares at the end of each period would provide the holders with 55% of the fully diluted share amounts you have calculated. Please refer to the second comment in this letter for additional perspective on your computational approach. |

| 4 |

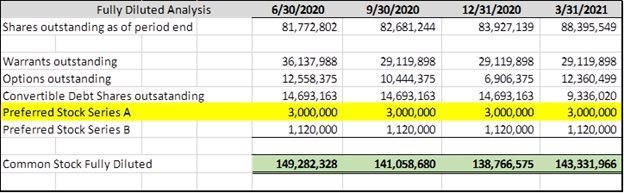

Answer to Comment 5: Please see the below table listing the outstanding shares computed on a fully diluted basis, assuming an amendment to the Series A Preferred Certificate of Designation that would only allow conversion to common shares on a 1:1 basis.

| 6. | We note that in response to prior comment 6, pertaining to various discrepancies in reporting your outstanding preferred shares, you state that in the June 30, 2017 Form 10-K, since the Series B preferred shares had a conversion feature of 16:1, you "elected to report these shares as converted and increased the number of Series B Preferred shares outstanding by 3,750,000" and that the 7,000,000 preferred shares outstanding at that date "represented 3,000,000 series A and 4,000,000, Series B." |

|

|

|

|

| Please reconcile your statement with the disclosure on the corresponding balance sheet describing the composition of the 7,000,000 shares as "6,750,000 shares issued and outstanding for class A convertible preferred stock and 250,000 shares issued and outstanding for class B convertible preferred stock at June 30, 2017," also your equity presentation for 2017, labeling the 3,750,000 shares added during the period as stock

subscriptions, the disclosure on page 33 of that filing stating "During the six months ended June 30, 2017, an additional 3,750,000 shares of post-split Series A Convertible Preferred Stock were purchased from the Company," and your inclusion of the corresponding value ascribed in the equity statement to those shares in "Proceeds from issuance of stock" in your 2017 Statements of Cash Flow.

Please separate the presentations of the Series A and Series B preferred shares and values in your Balance Sheets and Statements of Equity to comply with FASB ASC 505-10-50-2. Tell us whether you have amended the Certificate of Designation for the Series B preferred stock to eliminate the 1:16 conversion ratio, and if not explain why you believe presenting these securities on a converted basis is appropriate, as it appears this would represent a departure from the legal framework under which rights of the security holders are established and understood. We reissue prior comment 6. |

| 5 |

Answer to Comment 6: As disclosed in Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations on page 12 of the June 30, 2017 Form 10-K, “Simultaneously with the Merger,……..The Company also accepted a subscription from a single investor in the amount of Two Hundred Fifty Thousand Dollars ($250,000 for 27,027 shares of the Registrants Series B Convertible Preferred Stock, par value $0.001 per share (the “Series B Shares”) also in accordance with Rule 506 of Regulation D of the Securities Act. The Series B Shares convert, following six months after issuance, into shares of Common Stock at the post-Split rate of sixteen (16) votes per share. The Series B Shares cannot be converted by the investor if such conversion would result in the investor owning more than 4.99% of the outstanding common stock.” Please note that the 27,027 were the number of shares before the 9.25:1 reverse split, that number is 250,000 shares post-split.

The disclosure on page 33 of that filing incorrectly states the additional 3,750,000 shares of post-split as Series A when in fact they are not and should have been reference as Series B. We will correct this statement in a subsequent refilling of the June 30, 2017 10-K.

We will separate the presentations of Series A and Series B preferred shares and value in our Balance sheet and Statement of Equity.

We did not amend the Certificate of Designation for the Series preferred stock to eliminate the 1:16 conversion feature because as stated above the Series B covert into common shares six months after issuance. The Company will eliminate any reference or mention of the conversion feature as this feature is no longer relevant.

| 7. | We note the following provision regarding Rank and Liquidation in Section 2 of your Series A Preferred Stock Certificate of Designation, which we would like you to explain - "All shares of the Series A Preferred Stock shall rank, both as the payment of dividends and as to distributions of assets upon liquidation or winding up of the Corporation, whether voluntary or involuntary, (x) junior to: the shares of the Corporation’s shares of common stock, par value $0.01 per share (the “Common Stock”), and (y) prior to (ii) all of the Corporation’s hereafter issued capital stock ranking junior to the Series A Preferred Stock, both as to payment of dividends and as to distribution of assets upon liquidation, dissolution or winding up of the Corporation, whether voluntary or involuntary, when and if issued (any junior capital stock being herein referred to as “Junior Stock”)." |

|

|

|

|

| This provision appears to establish a senior position for the Series A preferred stock relative to subsequently issued common stock, and a subordinate position relative to common stock that was outstanding at origination. Please clarify the full scope and meaning of this provision, including "prior to (ii)"and elaborate on the rationale for, and ownership of, any common shares having differing liquidation preferences. Explain how the "Liquidation Value," and the holders’ rights thereto, as referenced in Section 3(f) of the Certificate of Designation, would be established. |

| 6 |

Answer to Comment 7: The amended Certificate of Designation for the Series A Preferred Stock as discussed in answers to other Comments in this letter, will no longer include language related to multiple liquidation preferences for the same class of common stock, in order to further clarify the rights of such stock.

| 8. | We understand that you will be recalculating the number of common shares issuable pursuant to the Series A preferred stock to address certain disclosure and accounting concerns raised in the other comments in this letter. As the conversion provision is based on the number of fully diluted shares, which include, among other components, common shares issuable upon the exercise of stock options, warrants, and convertible debt, as indicated in your response to prior comment 5, and considering that the number of shares needed to settle your convertible debt is both variable and indeterminate, according to your disclosures in Note 5, it does not appear you would be able to conclude that you have a sufficient number of authorized and unissued common shares to settle the Series A preferred stock, or that the ability to settle in shares is within your control. |

|

|

|

|

| Please refer to FASB ASC 480-10-S99-3A(6), FASB ASC 815-40-25-10(b), 25-20, and 25-26. Unless you are able to show why this guidance would not apply to you, under the circumstances, it appears you will need to classify these instruments as temporary equity and follow the measurement guidance in FASB ASC 480-10-S99-3A(14). |

Answer to Comment 8: Please note the table provided as part of the response to Comment 5, which assumes a 1:1 conversion feature following an amendment to the Series A Preferred Certificate of Designation.

The Company acknowledges that:

| · | The Company is responsible for the adequacy and accuracy of the disclosures contained in the Form 10-K; |

|

|

|

| · | Staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the Form 10-K; |

|

|

|

| · | The Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

The Company believes the foregoing is responsive to the comments and questions raised by the Staff in its Comment Letter. If you have further questions or require additional clarifying information, please contact the undersigned at 720-235-0099. Thank you.

Sincerely,

/s/ Mark Breen

Mark Breen

Chief Financial Officer

| 7 |