October 18, 2021

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, NE

Washington, DC 20549

Attention: | Lily Dang |

| Karl Hiller |

|

|

Re: | Leafbuyer Technologies, Inc. Form 10-K for the Fiscal Year Ended June 30, 2020 Filed September 25, 2020 File No. 000-55855 |

Ladies and Gentlemen:

Please accept this letter as the responses of Leafbuyer Technologies, Inc. (the “Company”) to the comments of the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) set forth in the letter from the Division of Corporation Finance dated September 22, 2021 (the “Comment Letter”) with respect to Leafbuyer Technologies, Inc. Form 10-K for the fiscal year ended June 30, 2020 (the “Form 10-K”).

For ease of reference, we have repeated each of the Staff’s comments below, followed by the corresponding response of the Company.

Form 10-K for the Fiscal Year Ended June 30, 2020

Financial Statements

Note 4 - Capital Stock and Equity Transactions, page 41

1. We understand from your response to reissued comment eight that you increased the number of authorized shares to 700 million on August 11, 2021 and plan to amend the Series A preferred stock Certificate of Designation to remove the conversion provisions, while adjusting and retaining a fixed number of voting rights, as indicated in the draft amendment to the Certificate of Designation submitted as Exhibit B to your response.

Tell us if you have obtained permission from all holders of those instruments for the changes reflected in that document and whether any consideration has been or will be exchanged and if any new agreements with the holders have been or will be introduced in connection with the changes proposed. Please describe any remaining steps that you will need to take to complete the amendment, indicate the timeframe, and provide timely disclosure of the change as appropriate.

There are three holders of the Company’s Series A Convertible Preferred Stock (the “Series A Preferred Stock”) and all three are directors and senior executives of the Company. The Company has obtained the unanimous written consent of the board of directors and a separate written consent of all three holders of the Series A Preferred Stock to the amendment to the Certificate of Designation of the Series A Preferred Stock to change the Series A Preferred Stock form convertible preferred stock to super voting preferred stock (the “Amendment”). No consideration will be exchanged or new agreements executed in connection with the Amendment. The Amendment was filed with the Secretary of State of the state of Nevada on October 13, 2021 and became effective on such date. We have reported the Amendment in Items 3.03 and 5.03 of our Current Report on Form 8-K dated October 18, 2021, which includes the Amendment as filed in Nevada as Exhibit 3.1 thereto.

| 1 |

Financial Statements

Note 4 – Capital Stock and Equity Transactions, page 41

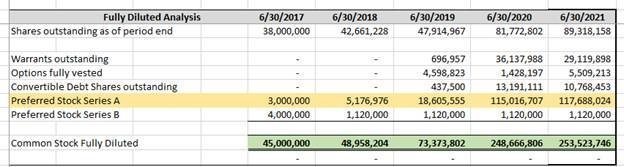

2. We note your response to reissued comments two, four and five, including the tabulation at Exhibit C, reflecting the composition of fully diluted shares and your computation of the number of shares that would be issuable pursuant to the Series A preferred stock, for various periods subsequent to issuance.

We previously referenced in part, information from the Announcement, Agreement and Plan of Merger, and Certificate of Designation filed with the Form 8-K on March 29, 2017, indicating that 21,750,000 common shares were issued to the holders of the Series A preferred stock and would be considered in computing the incremental shares that would become issuable in subsequent periods to maintain their 55% interest; these beneficial interests are also disclosed in Item 12 of your annual report.

However, the figures in Exhibit C and the corresponding disclosures in your draft amendments appear to overstate both the number of issuable shares and the number of fully diluted shares because the common shares already owned were not considered in computing the shares needed to reach the target.

Unless you believe a different computational approach should be used and are able to show how any such other method would be consistent with the numerical illustration in the Certificate of Designation, indicating the number of issuable shares was then 3 million based on 45 million fully diluted shares, please revise accordingly.

We have revised Exhibit C, which is attached hereto as Exhibit A, to revise the calculations of shares underlying the Series A Preferred Stock in the periods presented to be consistent with the numerical illustration in the original certificate of designation.

3. As discussed in our phone conference on September 22, 2021, we have further considered the implications of your Series A preferred stock conversion provisions relative to the requirements in FASB ASC 815-15-25-1, which requires bifurcation of an embedded conversion feature if certain criteria are met, and an exception does not apply.

For example, the exception outlined in FASB ASC 815-10-15-74(a) would be available if the contract were indexed to your own stock and classified in equity. However, FASB ASC 815-10-15-75(b) clarifies that if a contract that could be settled by issuing your common shares is indexed in part or in full to something other than your own stock, it does not qualify for the exception and if it meets the definition of a derivative would need to be accounted for as a liability or asset.

FASB ASC 815-40-15-7 through 15-8A provide guidance on determining whether the conversion feature is indexed to your stock. Paragraphs 15-7D, 7E, and 7F clarify that if settlement amounts are affected by variables that are extraneous to the pricing of a fixed- for-fixed option or forward contract on equity shares, the conversion feature would not be considered indexed to your stock, while paragraph 8A stipulates that if not indexed, it shall be accounted for as a liability or asset.

Given that settlement amounts pursuant to the conversion provisions of the Series A preferred stock are affected by changes in the number of fully diluted shares, which is not an input to the pricing of a fixed-for-fixed option or forward contract on equity shares, the embedded feature would not be considered indexed to your stock.

| 2 |

With regard to FASB ASC 815-15-25-1(a), considering the economic characteristics of the conversion feature compared to those of the preferred share host, where the economic value of the conversion feature (as represented by the number of issuable shares) changes by a multiple of about 1.2 (or 0.55/0.45) for all changes in the number of fully diluted shares (excluding change in the number of issuable shares), and that the value of a preferred share absent this conversion feature would not be correlated in this manner, the “not clearly and closely related” criteria appears to characterize the relationship.

With regard to FASB ASC 815-15-25-1(c), and that aspect of the derivative definition described in FASB ASC 815-10-15-83(c), considering that the conversion provision is oriented entirely to securing shares to achieve the specified ownership percentage, and that conversion does not require any payment of cash, it also appears the net share settlement criteria would be met, following the guidance in FASB ASC 815-10-15-102.

Based on the observations outlined above, it appears that you would need to bifurcate and account for the embedded conversion feature as a derivative at fair value, consistent with the guidance in FASB ASC 815-10-30-1 and 35-1. However, if you have an alternate view, please address the guidance cited above and submit your analysis for review.

We have incorporated an Error Correction Footnote in our June 30, 2021 10-K filing which states the following:

Series A convertible feature not accounted properly

The Series A Preferred Shares are convertible into a number of shares of Common Stock so that the holders of Series A Convertible Preferred Stock would hold 55% of the number of outstanding shares of Common Stock on a fully diluted basis after giving effect to such conversion. The Series A Convertible Preferred Stock vote on an “as-converted” basis.

The Company has determined that the Series A Preferred Stock conversion provisions meet the accounting requirements of FASB ASC 815 which requires a bifurcation of an embedded conversion feature and classification of the derivative as a liability on the balance sheet at the end of each reporting period. The fair value of the derivative liability is estimated each period as a Level 3 – Significant Unobservable Inputs based upon the numbers of common shares stock at an estimated conversion price.

The following table represents the value of the derivative and number of shares of common stock issuable for the holders to obtain 55% of the number of outstanding shares of common stock:

Balance Sheet – June 30, 2020

|

| As Computed - Restated |

|

| As Reported |

|

| Effect of Change |

| |||

Derivative liability |

| $ | 3,775,678 |

|

| $ | - |

|

| $ | 3,775,678 |

|

Total current liabilities |

| $ | 7,032,322 |

|

| $ | 3,256,644 |

|

| $ | 3,775,678 |

|

Total liabilities |

| $ | 8,199,949 |

|

| $ | 4,424,271 |

|

| $ | 3,775,678 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accumulated deficit |

| $ | 19,776,802 |

|

| $ | 16,001,124 |

|

| $ | 3,775,678 |

|

Total equity (deficit) |

| $ | (3,223,148 | ) |

| $ | 552,530 |

|

| $ | (3,775,678 | ) |

| 3 |

Income Statement – June 30, 2020

|

| As Computed - Restated |

|

| As Reported |

|

| Effect of Change |

| |||

Unrealized gain(loss) on derivative |

| $ | 6,811,623 |

|

| $ | - |

|

| $ | 6,811,623 |

|

Other income/ (expense) |

| $ | 5,794,379 |

|

| $ | (1,017,244 | ) |

| $ | 6,811,623 |

|

Net (loss) income |

| $ | 1,302,375 |

|

| $ | (5,509,248 | ) |

| $ | 6,811,623 |

|

Earnings (loss) per share - Basic |

| $ | 0.02 |

|

| $ | (0.07 | ) |

| $ | 0.09 |

|

Earnings (loss) per share - Basic |

| $ | 0.01 |

|

| $ | (0.07 | ) |

| $ | 0.08 |

|

Statement of Cash Flow – June 30, 2020

|

| As Computed - Restated |

|

| As Reported |

|

| Effect of Change |

| |||

Net (loss) income |

| $ | 1,302,375 |

|

| $ | 5,509,248 |

|

| $ | 6,811,623 |

|

Loss (gain) on derivative liability |

| $ | (6,811,623 | ) |

| $ | - |

|

| $ | (6,811,623 | ) |

Statement of Equity – June 30, 2020

|

| As Computed - Restated |

|

| As Reported |

|

| Effect of Change |

| |||

June 30, 2019 – Accumulated Deficit |

| $ | (21,079,177 | ) |

| $ | (10,491,876 | ) |

| $ | (10,587,301 | ) |

4. We note that disclosures proposed in Note 1 to each of the draft amendments reference the Series A preferred shares and states that you are “required to evaluate the fair market value of these shares as of the Balance Sheet date” and that you have determined that the par value represents the fair value of the Series A stock “because of the accumulated deficit” and because there is not enough liquidity in the public market.

We do not believe that you have described an approach to valuing the Series A preferred stock that would be consistent with GAAP, considering the conversion feature, an established market for your common shares, and various issuances of shares in exchange for cash both concurrently with and subsequent to origination.

As indicated in the preceding comment, we believe that you will need to account for the embedded derivative at fair value to comply with FASB ASC 815. Please refer to the definition of readily determinable fair value in FASB ASC 820-10-20 and the associated guidance in FASB ASC 820-10-35-36B, as it pertains to the underlying common shares.

Please further revise your proposed disclosures pertaining to the required accounting and valuation methodology accordingly. Please also expand your proposed disclosures to address the error correction accounting and disclosure requirements in FASB ASC 250- 10-45-22 through 28, and 50-7 through 50-11.

| 4 |

We repeat here our response to Comment 3 above.

5. We note that you have submitted draft amendments to your annual report and the three subsequent interim reports, and that each draft amendment includes error correction disclosures covering revisions to the numbers of Series A and Series B preferred shares outstanding, and clarifying certain conversion provisions. In addition to the revisions that

will be required to address the other comments in this letter, please revise to address the following inconsistencies.

| · | Note 4 on page 12 of both the second and third quarter reports continues to indicate the company has 3,000,000 Series A shares outstanding and 1,120,000 Series B shares outstanding (in the first paragraph); these should be revised to remove the effect of the stock split. |

|

|

|

| · | Note 4 to each of the draft amendments indicates that because the Series A preferred shares would convert into more common shares than the company has available “the Company needs to present the Series A Convertible Preferred Stock separate as a mezzanine equity” while the error correction disclosures in Note 1 indicate you would not be reporting the instruments in this manner; please revise the language in Note 1 and Note 4 to address the requirements of FASB ASC 815, which would preclude any change in the classification of your Series A preferred stock. |

|

|

|

| · | Note 4 to each of the interim reports references the issuable and fully diluted shares that you calculated for June 30, 2020 and are not consistent with the corresponding references in Note 1; both references should be revised to include the revised numbers that pertain to the interim reporting dates. |

|

|

|

| · | The March 31, 2021 APIC balance in the third quarter Statement of Stockholders’ Equity of 17,24,509 appears to be missing a digit. |

|

|

|

| · | The explanatory notes to each of the interim reports appear to pertain to the annual report rather than to the specific interim reports. |

As stated above, we have incorporated an Error Correction Footnote in our June 30, 2021 10-K filing, which restates information from our June 30, 2020 10-K filing and have restated the Balance Sheet, Statement of Operations, Statement of Cash Flow and Statement of Equity. We do not plan to amend filings for prior periods, but will continue to disclose the error footnote and the impact it has on our quarterly and annual financial information.

The Company believes the foregoing is responsive to the comments and questions raised by the Staff in its Comment Letter. If you have further questions or require additional clarifying information, please contact the undersigned at 720-235-0099. Thank you.

Sincerely,

/s/ Mark Breen |

|

Mark Breen |

|

Chief Financial Officer |

|

| 5 |

EXHIBIT A

6 |