| WP Large Cap Income Plus Fund | | |

| | | |

| Statement of Cash Flows | | |

| For the fiscal year ended November 30, 2024 | | |

| | | |

| Increase (Decrease) in cash: | | |

| Cash flows from operating activities: | | |

| Net Increase (Decrease) in Net Assets from Operations | $ 6,271,154 | |

| Adjustments to Reconcile Net Increase (Decrease) in Net Assets from | | |

| Operations to Net Cash (used in) Provided from Operating Activities: | | |

| Purchase of Investments and Options | (393,523) | |

| Proceeds from Disposition of Investments and Options | 3,110,718 | |

| (Purchase) Sales of Short-Term Investment Securities, Net | (196,943) | |

| (Increase) Decrease in Dividends and Interest Receivable | 14,979 | |

| (Increase) Decrease in Receivables for Securities Sold | 201,238 | |

| (Increase) Decrease in Prepaid Expenses | (945) | |

| Premiums Received from Options Written | 284,182 | |

| Payments to Cover Options Written | (156,676) | |

| Increase (Decrease) in Accrued Distribution (12b-1) Fees | 8,781 | |

| Increase (Decrease) in Accrued Expenses | 3,984 | |

| Increase (Decrease) in Payable to Broker | 2,778 | |

| Return of Capital Received from Investments | 8,750 | |

| Net Change in Unrealized (Appreciation) Depreciation on Investments | |

| and Options | (5,276,170) | |

| Net Realized (Gain) Loss on Investments and Options | (1,116,770) | |

| Net Cash (used in)/Provided from Operating Activities | 2,765,537 | |

| | | |

| Cash flows from financing activities: | | |

| Proceeds from Fund Shares Sold | 346,941 | |

| Payment on Fund Shares Redeemed | (3,142,985) | * |

| Cash Distributions Paid | - | |

| Net Cash (used in)/Provided from Financing Activities | (2,796,044) | |

| | | |

| Net Increase (Decrease) in Cash | (30,507) | |

| | | |

| Cash: | | |

| Beginning of Year | 31,507 | |

| End of Year | $ 1,000 | |

| | | |

| Supplemental disclosure of cash flow information: | | |

| | | |

| Reconciliation of restricted and unrestricted cash at the beginning of the | |

| year to the Statement of Assets and Liabilities: | | |

| Cash | $ 1,000 | |

| Deposits at Broker for Written Options | $ 30,507 | |

| | | |

| Reconciliation of restricted and unrestricted cash at the end of the year | |

| to the Statement of Assets and Liabilities: | | |

| Cash | $ 1,000 | |

| Deposits at Broker for Written Options | $ - | |

| | | |

| | | |

| | | |

| Interest paid by the Fund was $13,444. | | |

| * Noncash financing activities not included herein consist of a decrease in payable for Fund Shares redeemed of $11,000. |

| The accompanying notes are an integral part of these financial statements. | | |

| NOTES TO FINANCIAL STATEMENTS | |

| WP LARGE CAP INCOME PLUS FUND | |

| November 30, 2024 | |

| | |

| | | | | | | | | | | | | | | | | |

| 1.) ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES | | | | | |

The WP Large Cap Income Plus Fund (the “Fund”) is a series of WP Trust (the “Trust”). The Trust was organized on June 4, 2015, as a Delaware statutory trust. The Trust is registered as an open-end management investment company under the Investment Company Act of 1940 (the “1940 Act”). As of November 30, 2024, there were two series authorized by the Trust. The Fund is a diversified Fund. The Fund’s investment objective is total return. The Fund’s investment adviser is Winning Points Advisors, LLC (the “Adviser”). The Fund currently offers one class of shares, Institutional Class shares. The Fund commenced operations on October 10, 2013.

|

| | | | | | | | | | | | | | | | | |

The Fund is an investment company that follows the investment company accounting and reporting guidance of Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946 Financial Services - Investment Companies. The financial statements are prepared in conformity with accounting principals generally accepted in the United States of America ("GAAP"). The Fund follows the significant accounting policies described in this section.

|

| | | | | | | | | | | | | | | | | |

SHARE VALUATION: The net asset value (“NAV”) is generally calculated as of the close of trading on the New York Stock Exchange (the “Exchange”) (normally 4:00 p.m. Eastern time) every day the Exchange is open. The NAV is calculated by taking the total value of the Fund’s assets, subtracting its liabilities, and then dividing by the total number of shares outstanding, rounded to the nearest cent. For the Institutional Class, the offering price and redemption price per share is equal to the NAV per share.

|

| | | | | | | | | | | | | | | | | |

SECURITY VALUATION: All investments in securities are recorded at their estimated fair value, as described in note 2.

|

| | | | | | | | | | | | | | | | | |

OPTIONS: The Fund’s option strategy consists of selling and purchasing put and call options on equity indices and exchange traded funds (“ETFs”). The sale of put options generates income for the Fund, but exposes it to the risk of declines in the value of the underlying assets. The risk in purchasing options is limited to the premium paid by the Fund for the options. The sale of call options generates income for the Fund, but may limit the Fund's participation in equity market gains. The Fund’s Adviser seeks to reduce the overall volatility of returns by managing a portfolio of options. When the Fund writes or purchases an option, an amount equal to the premium received or paid by the Fund is recorded as a liability or an asset and is subsequently adjusted to the current value of the option written or purchased. Premiums received or paid from writing or purchasing options which expire unexercised are treated by the Fund on the expiration date as realized gains or losses. The difference between the premium and the amount paid or received on effecting a closing purchase or sale transaction, including brokerage commissions, is also treated as a realized gain or loss. If an option is exercised, the premium paid or received is added to the cost of the purchase or proceeds from the sale in determining whether the Fund has realized a gain or a loss on investment transactions.

|

| | | | | | | | | | | | | | | | | |

Purchasing and selling put and call options are highly specialized activities and entail greater than ordinary investment risks. The successful use of options depends in part on the ability of the Adviser to manage future price fluctuations and the degree of correlation between the options and securities (or currency) markets. By selling call options on equity securities or indices, the Fund gives up the opportunity to benefit from potential increases in the value of the underlying securities above the strike prices of the sold call options, but continues to bear the risks of declines in the value of the markets, including the underlying indices for the puts as well, if different, as the securities that are held by the Fund. The premium received from the sold options may not be sufficient to offset any losses sustained from the volatility of the underlying equity indices over time.

|

| | | | | | | | | | | | | | | | | |

FEDERAL INCOME TAXES: The Fund has qualified and intends to continue to qualify as a regulated investment company (“RIC’) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). It is the policy of the Fund to comply with the requirements of the Code applicable to regulated investment companies and to distribute substantially all of its net investment company taxable income and net capital gains. Therefore, no provision for federal income taxes is required.

|

| | | | | | | | | | | | | | | | | |

As of and during the fiscal year ended November 30, 2024, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax liability as income tax expense in the Statement of Operations. During the fiscal year ended November 30, 2024, the Fund did not incur any interest or penalties. The Fund identifies its major tax jurisdictions as U.S. Federal and the state of Delaware.

|

| | | | | | | | | | | | | | | | | |

In addition, GAAP requires management of the Fund to analyze all open tax years, as defined by IRS statute of limitations, including federal tax authorities and certain state tax authorities. Management has analyzed the Fund’s tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax years. The Fund has no examination in progress and is not aware of any tax positions for which it is reasonably possible that the total tax amounts of unrecognized tax benefits will significantly change in the next twelve months.

|

| | | | | | | | | | | | | | | | | |

DISTRIBUTIONS TO SHAREHOLDERS: Dividends from net investment income and distributions of net realized capital gains, if any, will be declared and paid at least annually. Income and capital gain distributions, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. GAAP requires that permanent financial reporting differences relating to shareholder distributions be reclassified to paid-in capital or net realized gains.

|

| | | | | | | | | | | | | | | | | |

USE OF ESTIMATES: The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

|

| | | | | | | | | | | | | | | | | |

EXPENSES: Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund's relative net assets or another appropriate basis (as determined by the Board of Trustees (the “Board”)). The allocations are dependent upon the nature of the services performed and the relative applicability to each Fund. Other allocations may also be approved from time to time by the Trustees.

|

| | | | | | | | | | | | | | | | | |

OTHER: Investment and shareholder transactions are recorded on trade date. The Fund determines the gain or loss realized from the investment transactions by comparing the original cost of the security lot sold with the net sales proceeds using the identified cost method. Dividend income is recognized on the ex-dividend date or as soon as information is available to the Fund. Interest income and interest expenses, if any, are recognized on an accrual basis. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

|

| | | | | | | | | | | | | | | | | |

| 2.) SECURITIES VALUATIONS | | | | | | | | | | | |

PROCESSES AND STRUCTURE: The Fund’s Board has adopted guidelines for valuing securities and other derivative instruments including in circumstances in which market quotes are not readily available, and has delegated authority to the Valuation Designee to apply those guidelines in determining fair value prices, subject to review by the Board.

|

| | | | | | | | | | | | | | | | | |

HIERARCHY OF FAIR VALUE INPUTS: The Fund utilizes various methods to measure the fair value of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation techniques used to measure fair value. The three levels of inputs are as follows:

|

| | | | | | | | | | | | | | | | | |

Level 1 - Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access.

|

| | | | | | | | | | | | | | | | | |

Level 2 - Observable inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

|

| | | | | | | | | | | | | | | | | |

Level 3 - Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s best information about the assumptions a market participant would use in valuing the assets or liabilities.

|

| | | | | | | | | | | | | | | | | |

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

|

| | | | | | | | | | | | | | | | | |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

|

| | | | | | | | | | | | | | | | | |

FAIR VALUE MEASUREMENTS: A description of the valuation techniques applied to the Fund’s major categories of assets and liabilities measured at fair value on a recurring basis follows.

|

| | | | | | | | | | | | | | | | | |

Equity securities (common stocks). Securities that are traded on any stock exchange or on the NASDAQ over-the-counter market are generally valued by the pricing service at the last quoted sale price on the primary exchange or market on which the security trades. Lacking a last sale price, an equity security is generally valued by the pricing service at its last bid price. In the event of a short sale of an equity security, lacking a last sale price, an equity security is generally valued by the pricing service at its last ask price. Generally, if the security is traded in an active market and is valued at the last sale price, the security is categorized as a level 1 security, and if an equity security is valued by the pricing service at its last bid or ask, it is generally categorized as a level 2 security. When market quotations are not readily available or when a Valuation Designee determines that the market quotation or the price provided by the pricing service does not accurately reflect the current market value, or when restricted or illiquid securities are being valued, such securities are valued pursuant to the fair value pricing procedures and are categorized as level 2 or level 3, as appropriate.

|

| | | | | | | | | | | | | | | | | |

Money market funds. Money market funds are valued at net asset value and are classified in Level 1 of the fair value hierarchy.

|

| | | | | | | | | | | | | | | | | |

Derivative instruments. Listed derivatives, including purchased options and written options, will be valued at the mean of the bid and ask price on the primary exchange on which the option trades and are categorized as level 1 of the fair value hierarchy. If there is not a bid and ask price on the primary exchange on which the option trades, or if the Valuation Designee determines that the mean of the bid and ask price does not accurately reflect the current value, the option will be valued at fair value as determined under the fair value pricing procedures and may be categorized as level 2 or level 3, as appropriate.

|

| | | | | | | | | | | | | | | | | |

In accordance with the Trust's fair value pricing guidelines, the Fund's Valuation Committee, which includes the Valuation Designee, shall consider all appropriate factors relevant to the value of securities for which market quotations are not readily available. No single standard for determining fair value can be established, since fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued by a Fund's Valuation Committee is the price at which the security could reasonably be sold in a current market transaction. Methods that are in accord with this principle may, for example, be based on a multiple of earnings; a discount from market of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or yield to maturity and credit spread with respect to debt issues, or a combination of these and other methods. The Board maintains responsibilities for the fair value determinations under Rule 2a-5 under the 1940 Act and oversees the Valuation Designee.

|

| | | | | | | | | | | | | | | | | |

The following tables summarize the inputs used to value the Fund’s assets and liabilities measured at fair value as of November 30, 2024:

|

| | | | | | | | | | | | | | | | | |

| Valuation Inputs of Assets | | | | | Level 1 | | | Level 2 | | Level 3 | | Total | |

| Common Stock | | | | | | $ 24,642,791 | | | $ - | | $ - | | $ 24,642,791 | |

| Money Market Funds | | | | | 431,915 | | | - | | - | | 431,915 | |

| Total | | | | | | | | $ 25,074,706 | | | $ - | | $ - | | $ 25,074,706 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Valuation Inputs of Liabilities | | | | Level 1 | | | Level 2 | | Level 3 | | Total | |

| Put Options Written | | | | | $ 58,200 | | | $ - | | $ - | | $ 58,200 | |

| Total | | | | | | | | $ 58,200 | | | $ - | | $ - | | $ 58,200 | |

| | | | | | | | | | | | | | | | | |

Refer to the Fund’s Schedule of Investments for a listing of securities by industry. The Fund did not hold any level 3 assets or liabilities during the fiscal year ended November 30, 2024.

|

| | | | | | | | | | | | | | | | | |

| 3. DERIVATIVES TRANSACTIONS | | | | | | | | | | | |

The Fund has adopted a derivative risk management program under Rule 18f-4 of the 1940 Act which governs the Fund's use of derivative transactions. As part of the program, the Board has appointed a member of the Fund's Adviser as the derivatives risk manager. As of November 30, 2024, portfolio securities valued at $24,642,791, were held in a segregated account by the custodian as collateral for options written.

|

| | | | | | | | | | | | | | | | | |

The average monthly notional value of options contracts purchased and written by the Fund for the fiscal year ended November 30, 2024, were as follows:

|

| | | | | | | | | | | | | | | | | |

| Derivative Type | | | | | | | | | | Average Notional Value |

| Call Options Purchased | | | | | | | | | | $923,077 | |

| Put Options Purchased | | | | | | | | | | $7,692,308 | |

| Put Options Written | | | | | | | | | | ($6,276,923) | |

| | | | | | | | | | | | | | | | | |

As of November 30, 2024, the location on the Statement of Assets and Liabilities for financial derivative instrument fair values is as follows:

|

| | | | | | | | | | | | | | | | | |

| Liabilities | | | | | | | | Location | | Equity Contracts/Total | |

| Put Options Written | | | | | Options Written at Fair Value | | $ 58,200 | |

| Total Liabilities | | | | | | | | | | | $ 58,200 | |

| | | | | | | | | | | | | | | | | |

Realized and unrealized gains and losses on derivatives contracts entered into by the Fund during the fiscal year ended November 30, 2024, are recorded in the following location in the Statement of Operations:

|

| | | | | | | | | | | | | | | | | |

| Net Change in Unrealized | | | | | | | | | | | | |

| Appreciation (Depreciation) on: | | | Location | | Equity Contracts/Total | |

| Call Options Purchased | | | | | Options Purchased | | $ 35,045 | |

| Put Options Written | | | | | Options Written | | $ 3,368 | |

| | | | | | | | | | | | | | $ 38,413 | |

| | | | | | | | | | | | | | | |

| Net Realized Gain (Loss) on: | | | Location | | Equity Contracts/Total | |

| Call Options Purchased | | | | | Options Purchased | | $ (107,230) | |

| Put Options Purchased | | | | | Options Purchased | | $ (27,662) | |

| Put Options Written | | | | | Options Written | | $ 108,038 | |

| | | | | | | | | | | | | | $ (26,854) | |

| | | | | | | | | | | |

All open derivative positions at November 30, 2024, are reflected on the Fund's Schedule of Options Written.

|

| | | | | | | | | | | | | | | | | |

The following tables present the Fund’s asset and liability derivatives available for offset under a master netting arrangement as of November 30, 2024.

|

| | | | | | | | | | | | | | | | | |

| Liabilities: | | | | Gross Amount of Assets Presented in the Statement of Assets & Liabilities | |

| | | | | | | | | | | | Gross Amounts Not Offset in the Statement of Assets and Liabilities | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | Gross Amounts Offset in the Statement of Assets and Liabilities | | Net Amount of Liabilities Presented in the Statement of Assets and Liabilities(1) | | | | | | | |

| | | | | | | | | | | | | |

| | | Gross Amounts of Recognized Liabilities(1) | | | | | | Cash Collateral Pledged(2) | | | |

| | | | | | Financial Instruments Pledged(2) | | | | |

| | | | | | | | Net Amount of Liabilities | |

| Description | | | | | | |

| Options | | | | | | | | | | | | | | | |

| Written | $ 58,200 | | $ - | | $ 58,200 | | $ 58,200 | | $ - | | $ - | |

| | | | | | | | | | | | | | | | | |

(1) Written options at value as presented in the Fund’s Schedule of Options Written.

| | | | |

| | | | | | | | | | | | | | | | | |

(2) The amounts are limited to the derivative liability balances and accordingly do not include excess collateral pledged.

|

| | | | | | | | | | | | | | | | | |

| 4.) INVESTMENT TRANSACTIONS | | | | | | | | | | | |

For the fiscal year ended November 30, 2024, purchases and sales of investment securities other than U.S. Government obligations and short-term investments were $342,804 and $3,107,346, respectively.

| |

| | | | | | | | | | | | | | | | | |

| 5.) ADVISERY FEES AND OTHER RELATED PARTY TRANSACTIONS | | | | | |

The Fund has entered into an Investment Advisory Agreement (the “Advisory Agreement”) with the Adviser. Pursuant to the Advisory Agreement, the Adviser manages the operations of the Fund and manages the Fund’s investments in accordance with the stated policies of the Fund. As compensation for the investment advisory services provided to the Fund, the Adviser receives a monthly management fee equal to an annual rate of 1.35% of the Fund’s average daily net assets. For the fiscal year ended November 30, 2024, the Adviser earned $309,776 in management fees. At November 30, 2024, the Fund owed the Adviser management fees of $26,787.

| |

| | | | | | | | | | | | | | | | | |

A managing member of the Adviser also serves as an Interested Trustee and Officer of the Trust.

| |

| | | | | | | | | | | | | | | | | |

The Fund has adopted a Distribution Plan (“Plan”) pursuant to Rule 12b-1 under the Investment Company Act of 1940. The Plan allows that the Fund may expend up to 0.25% for Institutional Class shares of the Fund’s average daily net assets annually to pay for any activity primarily intended to result in the sale of shares of the Fund and the servicing of shareholder accounts, provided that the Trustees have approved the category of expenses for which payment is being made. Beginning January 26, 2024, the Board reduced the Institutional shares service fee to 0.10% of average daily net assets. The Fund incurred distribution and service (12b-1) fees of $27,977 for the fiscal year ended November 30, 2024. At November 30, 2024, the Fund had available $21,464 which could be used for qualifying expenses under the Plan.

| |

| | | | | | | | | | | | | | | | | |

Premier Fund Solutions, Inc. (“PFS” or “Administrator”) serves as the Administrator for the Trust pursuant to a written agreement with the Trust. PFS provides day-to-day administrative services to the Fund. For PFS’s services to the Fund, the Fund pays PFS an annualized asset-based fee of 0.07% of average daily net assets up to $200 million, with lower fees at higher asset levels; subject to a minimum monthly fee of $2,800, plus reimbursement of out-of-pocket expenses. For its services, for the fiscal year ended November 30, 2024, PFS earned $33,690. At November 30, 2024, the Fund owed PFS administration fees of $2,887.

| |

| | | | | | | | | | | | | | | | | |

An officer of the Trust is also an officer of the Administrator.

| |

| | | | | | | | | | | | | | | | | |

| 6.) TAX MATTERS | | | | | | | | | | | | | |

For federal income tax purposes, at November 30, 2024, the cost of securities on a tax basis and the composition of gross unrealized appreciation (the excess of value over tax cost) and depreciation (the excess of tax cost over value) including written options were as follows:

| |

| | | | | | | | | | | | | | | | | |

| Cost of Investments | | | | | | | $ 8,885,688 | | | | | |

| | | | | | | | | | | | | | | | | |

| Gross Unrealized Appreciation | | | | | $ 16,190,862 | | | | | |

| Gross Unrealized Depreciation | | | | | (1,844) | | | | | |

| Net Unrealized Appreciation (Depreciation) on Investments | | $ 16,189,018 | | | | | |

| | | | | | | | | | | | | | | | | |

| The difference between book basis and tax basis unrealized appreciation (depreciation) is primarily attributable to the tax treatment of derivatives and the tax deferral of wash sales. | |

| | | | | | | | | | | | | | | | | |

The Fund’s tax basis distributable earnings are determined only at the end of each fiscal year. The tax character of distributable earnings (deficit) at November 30, 2024, the Fund’s most recent fiscal year end, were as follows:

| |

| | | | | | | | | | | | | | | | | |

| Accumulated Capital and Other Losses | $ (6,458,166) | | | | | | | | |

| Net Unrealized Appreciation | | | | 16,189,018 | | | | | | | | |

| | | | | | | | $ 9,730,852 | | | | | | | | |

| | | | | | | | | | | | | | | | | |

As of November 30, 2024, accumulated capital and other losses include the following:

| |

| | | | | | | | | | | | | | | | | |

| Deferred Late Year Ordinary Losses* | | $ 121,575 | | | | | | | | |

| Short Term Capital Loss Carryforward* | $ 6,303,183 | | | | | | | | |

| Long Term Capital Loss Carryforward* | $ 33,408 | | | | | | | | |

| | | | | | | | | | | | | | | | | |

* Under current tax law, late year ordinary losses incurred after December 31 of a fund’s fiscal year may be deferred and treated as occurring on the first business day of the following fiscal year for tax purposes. Available capital loss carryforwards have no expiration. During the fiscal year ended November 30, 2024, the Fund utilized capital loss carryforwards of $1,119,898.

| |

| | | | | | | | | | | | | | | | | |

In accordance with GAAP, the Fund has recorded reclassifications in the capital accounts. The reclassifications listed below have no impact on the net asset value of the Fund and are as a result of net operating losses. As of November 30, 2024, the Fund recorded reclassifications to increase (decrease) the capital account as follows:

| |

| | | | | | | | | | | | | | | | | |

| Paid In Capital | | | | | $ (26,658) | | | | | | | | |

| Total Distributable Earnings | | | | $ 26,658 | | | | | | | | |

| | | | | | | | | | | | | | | | | |

The tax character of distributions paid during the fiscal years ended November 30, 2024 and 2023 were as follows:

| |

| | | | | | | | | | | | | | | | | |

The Fund did not pay any distributions during the fiscal years ended November 30, 2024 and 2023.

| |

| | | | | | | | | | | | | | | | | |

| 7.) COMMITMENTS AND CONTINGENCIES | | | | | | | | | |

In the normal course of business, the Trust may enter into contracts that may contain a variety of representations and warranties and provide general indemnifications. The Fund’s maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, management considers the risk of loss from such claims to be remote.

| |

| | | | | | | | | | | | | | | | | |

| 8.) CONTROL OWNERSHIP | | | | | | | | | | |

| The beneficial ownership, either directly or indirectly, of more than 25% of the voting shares of a fund creates a presumption of control of the fund, under section 2(a)(9) of the 1940 Act. At November 30, 2024, Charles Schwab & Co. Inc., held for the benefit of its customers, in aggregate, 100% of Fund shares. The Trust does not know whether any underlying accounts of Charles Schwab & Co. Inc. owned or controlled 25% or more of the voting securities of the Fund. | |

| | | | | | | | | | | | | | | | | |

| 9.) CONCENTRATION OF SECTOR RISK | | | | | | | | | | |

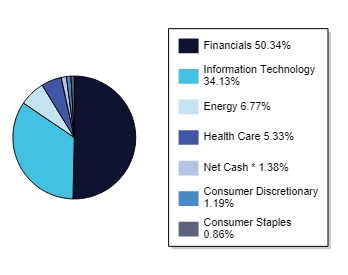

If a Fund has significant investments in the securities of issuers in industries within a particular sector, any development affecting that sector will have a greater impact on the value of the net assets of the Fund than would be the case if the Fund did not have significant investments in that sector. In addition, this may increase the risk of loss of an investment in the Fund and increase the volatility of the Fund’s NAV per share. From time to time, circumstances may affect a particular sector and the companies within such sector. For instance, economic or market factors, regulation or deregulation, and technological or other developments may negatively impact all companies in a particular sector and therefore the value of a Fund’s portfolio will be adversely affected. As of November 30, 2024, the Fund had 50.34% and 34.13%, respectively, of the value of its net assets invested in stocks within the Financials and Information Technology sectors.

| |

| | | | | | | | | | | | | | | | | |

| 10.) SUBSEQUENT EVENTS | | | | | | | | | | | | |

Subsequent events after the date of the Statement of Assets and Liabilities have been evaluated through the date the financial statements were issued. Management has concluded that there are no other subsequent events requiring adjustment to or disclosure in the financial statements.

| |