UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-23100

BERNSTEIN FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: September 30, 2016

Date of reporting period: September 30, 2016

ITEM 1. REPORTS TO STOCKHOLDERS.

BERNSTEIN FUND, INC.

Small Cap Core Portfolio

International Small Cap Portfolio

International Strategic Equities Portfolio

ANNUAL REPORT

SEPTEMBER 30, 2016

Table of Contents

Before investing in any portfolio of the Bernstein Fund, Inc., a prospective investor should consider carefully the portfolio’s investment objectives and policies, charges, expenses and risks. These and other matters of importance to prospective investors are contained in the portfolios’ prospectus, an additional copy of which may be obtained by visiting our website at www.bernstein.com and clicking on “Investments”, then “Mutual Fund Information—Prospectuses, SAIs and Shareholder Reports” or by calling your financial advisor or by calling Bernstein’s mutual fund shareholder help line at 212.756.4097. Please read the prospectus carefully before investing.

For performance information current to the most recent month-end, please call (collect) (212) 486-5800.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, 2016, without charge. Simply visit www.abglobal.com, or go to the Securities and Exchange Commission’s website at www.sec.gov, or call AllianceBernstein at 800.227.4618.

This shareholder report must be preceded or accompanied by the Bernstein Fund, Inc. prospectus for individuals who are not shareholders of the Fund.

The Fund will file its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Form N-Q is available on the Commission’s website at www.sec.gov. The Fund’s Form N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C.; information on the operation of the Public Reference Room may be obtained by calling 800.SEC.0330.

Investment Products Offered: · Are Not FDIC Insured · May Lose Value · Are Not Bank Guaranteed

Portfolio Adviser Commentary (Unaudited)

To Our Shareholders—November 7, 2016

On the following pages, you will find the 2016 Annual Report for the Portfolios of the Bernstein Fund, Inc. (the “Fund”). The Annual Report covers the six-month and since-inception periods ended September 30, 2016 and includes financial statements as well as notes to the financial statements, information about the recent performance of the Portfolios and a listing of each Portfolio’s holdings as of the period end.

Global equity markets have been volatile over the last six months. The second quarter was marked by multiple large swings up and down, driven by concerns over slow global economic growth, and the surprise Brexit vote near quarter-end triggered a dramatic sell-off that swiftly reversed within a week. The third quarter built on that recovery but volatility reappeared with the arrival of September and fears of a potential interest rate increase by the Federal Reserve. For the six-month period as a whole, returns were strongly positive for the emerging markets and positive for the US and international developed markets. US small cap stocks in particular, delivered very strong performance over the period, increasing over 12%.

If you have any questions about your investments in the Portfolios, please contact your Bernstein Advisor by calling 212.756.4097, or visit www.bernstein.com. As always, we are firmly dedicated to your investment success. Thank you for your continued interest in the Portfolios.

Sincerely,

Seth J. Masters

President

Bernstein Fund, Inc.

Bernstein Small Cap Core Portfolio

Investment Objectives and Strategy

The Portfolio seeks to provide long-term growth of capital.

The Portfolio invests, under normal circumstances, at least 80% of its net assets (plus any borrowings for investment purposes) in equity securities of small-capitalization companies or other securities or instruments with similar economic characteristics, including derivatives related to equity securities. Equity securities will primarily be common stocks, although, for purposes of the 80% policy, equity securities may also include preferred stocks, warrants, convertible securities, sponsored or unsponsored American Depositary Receipts (“ADRs”) and Global Depositary Receipts (“GDRs”) and equity real estate investment trusts (“REITs”). You will be notified at least 60 days prior to any change to the Portfolio’s 80% investment policy.

AllianceBernstein L.P. serves as the Portfolio’s investment manager (the “Manager”). The Manager will invest the assets of the Portfolio primarily in a diversified portfolio of equity securities of small-capitalization companies located in the U.S. The Portfolio defines small-capitalization companies as those that, at the time of investment, fall within the capitalization range between the smallest company in the Russell 2000 Index (the “Russell 2000”) and the largest company in the Russell 2000. The market capitalization of the companies included in the Portfolio’s definition of “small-capitalization” companies will change over time as the capitalization of the securities included in the Russell 2000 change.

The Manager utilizes both quantitative analysis and fundamental research to determine which securities will be held by the Portfolio and to manage risk. The Manager applies quantitative analysis to all of the securities in the Portfolio’s research universe, which is composed primarily of securities in the Portfolio’s benchmark (the Russell 2000 Index). Those securities that score highly on this quantitative analysis are then screened to eliminate those securities that the Manager is recommending against purchasing based on its fundamental research, and a portfolio is constructed from the remaining highly ranked securities based on diversification and risk considerations. In its quantitative analysis, the Manager will consider a number of metrics that have historically provided some indication of favorable future returns, including metrics relating to valuation, quality, investor behavior and corporate behavior. In general, stocks are purchased when, in the view of the Manager, they provide the highest expected returns, considering their contribution to the estimated risk of the Portfolio’s existing investments. Typically, growth in the size of a company’s market capitalization relative to other domestically traded companies will not cause the Manager to dispose of the security. The Manager expects to seek to manage the overall portfolio volatility of the Portfolio relative

(Portfolio Advisor Commentary continued on next page)

Portfolio Adviser Commentary (continued)

to the Russell 2000 by favoring securities that offer the best balance between return and targeted risk.

The Portfolio may also invest in exchange-traded funds (“ETFs”) and other investment companies from time to time.

The Portfolio expects to utilize derivatives, such as options, futures contracts, forwards and swaps. For example, the Portfolio may use stock index futures contracts to equitize cash. Derivatives may provide a more efficient and economical exposure to market segments than direct investments, and may also be a more efficient way to alter the Portfolio’s exposure.

Investment Results

Despite outperforming in the earlier part of the year, all share classes (SCB class, Advisor class, and Z class) of the Portfolio underperformed its benchmark for the period ended September 30, 2016, as shown in the table on page 8. This performance pattern matches the reversal in US market returns and factor premia during this period. US markets started the year with recession fears and concerns about China. The Russell 2000 Index was down 15.9% for calendar 2016 as of February 11, 2016 when momentum, quality factors, and defensive sectors outperformed. Subsequently, stronger than expected economic data led to a risk-on market, where the Russell 2000 Index rallied sharply, and was up 11.5% for the calendar year to date period ended September 30, 2016. During the latter period deep-value factors, low-quality stocks, and cyclical sectors outperformed. This was a volatile and challenging period for factor-based systematic investing. The Portfolio seeks to maintain controlled exposure to high-profitability, momentum, and valuation factors. Outperformance early in the year and the subsequent underperformance was attributable mostly to the swings in the return performance of positive-momentum and high-profitability cohorts. Valuation exposure contributed positively to performance. Healthcare underweight, energy overweight, and real estate underweight contributed to performance; Financials and Consumer Staples underweights detracted.

For the six-month period, the Portfolio’s positive exposure to valuation factors, overweight in Energy and underweight in Utilities and Real Estate sectors contributed to performance, whereas the positive exposure to the momentum factor (which failed), lack of exposure to the low-quality stock cohort, and unfavorable stock selection in Healthcare and Information Technology detracted.

The Portfolios utilized derivatives in the form of Treasury futures for investment purposes which added to performance for both the six-month and since-inception periods.

Bernstein International Small Cap Portfolio

Investment Objective and Strategy

The Portfolio seeks to provide long-term growth of capital.

The Portfolio invests, under normal circumstances, at least 80% of its net assets (plus any borrowings for investment purposes) in equity securities of small-capitalization companies or other securities or instruments with similar economic characteristics, including derivatives related to equity securities. Equity securities will primarily be common stocks, although, for purposes of the 80% policy, equity securities may also include preferred stocks, warrants, convertible securities, sponsored or unsponsored ADRs and GDRs and equity REITs. You will be notified at least 60 days prior to any change to the Portfolio’s 80% investment policy.

AllianceBernstein L.P. serves as the Portfolio’s investment manager. The Manager will invest the assets of the Portfolio primarily in a diversified portfolio of equity securities of small-capitalization companies located outside of the United States. Under normal circumstances, at least 65% of the Portfolio’s net assets will be invested in companies located outside of the United States. The Portfolio defines small-capitalization companies as those that, at the time of investment, have market capitalizations within the market capitalization range of the Portfolio’s benchmark, the Morgan Stanley Capital International (“MSCI”) All Country World Index (“ACWI”) ex-US Small Cap Index. The market capitalization of the companies included in the Portfolio’s definition of “small-capitalization” companies will change over time as the capitalization of the securities included in the MSCI ACWI ex-US Small Cap Index change.

The Portfolio’s exposure to non-U.S. companies may change over time based on the Manager’s assessment of market conditions and the investment merit of non-U.S. issuers. Under normal circumstances, the Manager will invest in companies located in at least three countries other than the United States and, at times, may have exposure to issuers in several different countries. In determining a company’s location for purposes of the Portfolio’s investment policies and restrictions, the Manager may consider: (1) the place of domicile; (2) where the company has an established presence and conducts its business; and (3) where the company conducts a significant part of its economic activities. The Portfolio may invest in both developed and emerging market countries and, at times, may invest significantly in emerging markets.

(Portfolio Advisor Commentary continued on next page)

Portfolio Adviser Commentary (continued)

The Portfolio will consist of securities selected using three separate strategies—international growth, international value, and quantitative. Under the growth strategy, the Manager will seek companies with strong franchises and competitive positioning, as well as companies where the Manager believes that a positive change is underway that will drive growth and returns in the medium term. Under the value strategy, the Manager will seek to exploit controversies and enduring market behaviors of focusing too heavily on recent information and fearing loss more than valuing potential gains. Under the quantitative strategy, the Manager will consider a number of metrics that have historically provided some indication of favorable future returns, including metrics relating to valuation, quality, investor behavior and corporate behavior. Utilizing these resources, the Manager expects to allocate the Portfolio’s assets among industries and geographic locations to attempt to create a diversified portfolio of investments.

The Portfolio may invest in established companies and also in new and less-seasoned issuers. The Portfolio may also invest in ETFs and other investment companies from time to time.

The Portfolio expects to utilize derivatives, such as options, futures contracts, forwards and swaps. For example, the Portfolio may invest in currency derivatives as discussed below and in futures contracts to gain exposure to certain markets. Derivatives may provide a more efficient and economical exposure to market segments than direct investments, and may also be a more efficient way to alter the Portfolio’s exposure.

Fluctuations in currency exchange rates can have a dramatic impact on the returns of foreign equity securities. The Manager may employ currency hedging strategies, including the use of currency-related derivatives, to seek to reduce currency risk in the Portfolio, but it is not required to do so. The Manager may also take long and short positions in currencies or related derivatives for investment purposes, independent of any security positions. The Manager may use stock index futures contracts to gain access to certain markets.

Investment Results

International small cap stocks recovered strongly in the third quarter of 2016 after selling off in the first part of the year due to growth concerns in China and fears about the outcomes of Brexit, leaving both the six-month and since inception periods with strong positive returns for the Portfolio above large cap markets.

As shown in the table on page 8, during the six-month period, all share classes of the Portfolio outperformed its benchmarks, the MSCI ACWI ex-US Small Cap Index and the Lipper International Small/Mid-Cap Core Funds Average. Strong stock selection in consumer discretionary and industrials drove the outperformance and more than offset the drag from being underweight the materials sector and poor stock selection within Japan. Since inception, the Portfolio is trailing the benchmark but is outperforming the Lipper International Small/Mid-Cap Core Funds Average. Poor stock selection in Canada and our underweight to the materials sector have been detractors to performance.

The Portfolio utilized derivatives in the form of currency forwards for hedging purposes, which had an immaterial effect on performance in both the six-month and since-inception periods.

Bernstein International Strategic Equities Portfolio

Investment Objective and Strategy

The Portfolio seeks to provide long-term growth of capital.

The Portfolio invests, under normal circumstances, at least 80% of its net assets (plus any borrowings for investment purposes) in equity securities or other securities or instruments with similar economic characteristics, including derivatives related to equity securities. Equity securities will primarily be common stocks, although, for purposes of the 80% policy, equity securities may also include preferred stocks, warrants, convertible securities, sponsored or unsponsored ADRs and GDRs and equity REITs. You will be notified at least 60 days prior to any change to the Portfolio’s 80% investment policy.

AllianceBernstein L.P. serves as the Portfolio’s investment manager. The Manager will invest the assets of the Portfolio primarily (under normal circumstances, at least 65% of net assets) in equity securities of issuers in countries that make up the MSCI ACWI ex-US Index, which includes both developed and emerging market countries. The Portfolio will focus on securities of large-cap and mid-cap companies. The Manager expects to allocate fund assets among issuers in many foreign countries, but not necessarily in the same proportion that the countries are represented in the MSCI ACWI ex-US Index and may invest in issuers in countries outside of the MSCI ACWI ex-US Index. The Portfolio’s exposure among non-U.S. countries may change over time based on the Manager’s assessment of market conditions and the investment merit of particular non-U.S. issuers. Under normal circumstances, the Manager will invest in companies located in at least three

(Portfolio Advisor Commentary continued on next page)

Portfolio Adviser Commentary (continued)

countries other than the United States and expects to have exposure to issuers in many different countries. In determining a company’s location for purposes of the Portfolio’s investment policies and restrictions, the Manager may consider: (1) the place of domicile; (2) where the company has an established presence and conducts its business; and (3) where the company conducts a significant part of its economic activities. The Portfolio may, at times, invest significantly in emerging markets.

The Manager utilizes both fundamental and quantitative research to both determine which securities will be held by the Portfolio and to manage risk. Specifically, the Portfolio’s management team will use the universe of securities selected by the Manager’s various fundamental investment teams focusing on international equity securities, and apply its quantitative analysis to these securities. In applying its quantitative analysis, the Manager will consider a number of metrics that have historically provided some indication of favorable future returns, including metrics relating to valuation, quality, investor behavior and corporate behavior. Utilizing these resources, the Manager expects to allocate the Portfolio’s assets among industries and geographic locations to attempt to create a diversified portfolio of investments.

The Portfolio may also invest in ETFs and other investment companies from time to time.

The Portfolio expects to utilize derivatives, such as options, futures contracts, forwards and swaps. For example, the Portfolio may invest in currency derivatives as discussed below and in futures contracts to gain exposure to certain markets. Derivatives may provide a more efficient and economical exposure to market segments than direct investments, and may also be a more efficient way to alter the Portfolio’s exposure.

Fluctuations in currency exchange rates can have a dramatic impact on the returns of foreign equity securities. The Manager may employ currency hedging strategies, including the use of currency-related derivatives, to seek to reduce currency risk in the Portfolio, but it is not required to do so. The Manager may also take long and short positions in currencies or related derivatives for investment purposes, independent of any security positions. The Manager may use stock index futures contracts to gain access to certain markets.

Investment Results

The international equity markets rose during both the six-month and since inception reporting periods, as risk appetite returned following the high volatility experienced in the first quarter of 2016. The Brexit vote at the end of June did not prove to be as disruptive as feared, and this, combined with solid growth in China and stable monetary policy in Japan and the US, led to more of a risk-on environment. As shown in the table on page 8, all share classes of the Portfolio recorded positive absolute performance but lagged the MSCI ACWI ex-US Index in both periods. All share classes of the Portfolio were ahead of the Lipper International Large-Cap Core Average for the since inception period, but lagged over the 6-month period. Positive sector selection was offset by negative country and security selection in both periods.

For the six-month period, the overweight to Technology stocks was the largest sector contributor. Positive stock selection in the Financials and Materials sectors was offset by underperformance of stock selection in Industrials and Utilities. For the since inception period, underweight positions in the Financials and Healthcare sectors contributed positively, in addition to the Technology overweight. Favorable stock selection in Consumer Staples, in addition to Financials and Materials, was offset by underperformance in Industrials, Utilities and Energy stocks. At a country level, for the six-month period, an overweight to Hong Kong and underweight to South Africa contributed positively, but underweights to China and the United Kingdom detracted. For the since inception period, a Hong Kong overweight and Spain underweight were the largest contributors, and an Israel overweight and United Kingdom underweight were the largest detractors.

The Portfolio utilized derivatives in the form of currency forwards for hedging and investment purposes, which detracted from performance for both the six-month and since-inception periods. In addition, the Portfolio utilized Treasury futures for both hedging and investment purposes, which added to performance for both periods.

Disclosures and Risks (Unaudited)

Benchmark Disclosures

None of the following indices or averages reflects fees and expenses associated with the active management of a mutual fund portfolio. The MSCI ACWI ex-US Index measures the performance of the large- and mid-cap market segment across 22 developed markets (excluding the U.S.) and 23 emerging market countries. The MSCI ACWI ex-US Small Cap Index measures the performance of the small-cap market segment across 22 developed markets (excluding the U.S.) and 23 emerging market countries. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. Investors cannot invest directly in indices, and their results are not indicative of the performance for any specific investment, including the Portfolios.

A Word About Risk

All Bernstein Portfolios:

The share price of the Portfolios will fluctuate and you may lose money. There is no guarantee that the Portfolios will achieve their investment objectives.

Market Risk: The Portfolio is subject to market risk, which is the risk that stock prices in general may decline over short or extended periods. In the past several years, financial markets in the United States, Europe and elsewhere have experienced increased volatility, decreased liquidity and heightened uncertainty. Recently, some securities markets, particularly in Europe and Asia, have been very volatile and have declined in value significantly. These market conditions may continue, worsen, or spread. The U.S. Government and the Federal Reserve, as well as certain foreign governments and central banks, have taken steps to support financial markets, including by keeping interest rates low. Other governments have tried to support markets by buying stocks and through other market interventions. Government intervention may not work as intended, particularly if the efforts are perceived by investors as being unlikely to achieve the desired results. The Federal Reserve has terminated certain of its market support activities. Further reduction or withdrawal of Federal Reserve or other U.S. or non-U.S. governmental or central bank support could negatively affect financial markets generally, raise interest rates, increase market volatility, and reduce the value and liquidity of securities in which the Portfolio invests.

Current political uncertainty surrounding the European Union (EU) and its membership may increase market volatility. The financial instability of some countries in the EU, including Greece, Italy and Spain, together with the risk of that financial instability impacting other more stable countries, may increase the risk of investing in companies in Europe and worldwide. In addition, policy and legislative changes in the United States and in other countries are affecting many aspects of financial regulation, and may in some instances contribute to decreased liquidity and increased volatility in the financial markets. The impact of these changes, and the practical implications for market participants, may not be fully known for some time.

Economies and financial markets throughout the world are becoming increasingly interconnected. As a result, whether or not the Portfolio invests in securities of issuers located in or with significant exposure to countries experiencing economic and financial difficulties, the value and liquidity of the Portfolio’s investments may be negatively affected.

Liquidity Risk: Liquidity risk exists when particular investments are difficult to purchase or sell, possibly preventing the Portfolio from selling out of these illiquid securities at an advantageous price. Illiquid securities may also be difficult to value. Derivatives and securities involving substantial market and credit risk tend to involve greater liquidity risk.

Redemption Risk: The Portfolio may experience heavy redemptions that could cause the Portfolio to liquidate its assets at inopportune times or at a loss or depressed value, which could cause the value of your investment to decline.

Capitalization Risk: Investments in small- and mid-capitalization companies may be more volatile than investments in large-capitalization companies. Investments in small- and mid-capitalization companies may have additional risks because these companies may have limited product lines, markets or financial resources.

Allocation Risk: The Portfolio may seek to focus on different investment disciplines or factors at different times as means to achieve its investment objective. In the event that the investment disciplines or factors to which the Portfolio has greater exposure perform worse than the investment disciplines or factors with less exposure, the Portfolio’s returns may be negatively affected.

Derivatives Risk: The Portfolio may use derivatives in currency hedging strategies as well as for direct investments to gain access to certain markets, earn income, enhance return and broaden portfolio diversification, which entail greater risk than if used solely for hedging purposes. In addition to other risks such as the credit risk of the counterparty, derivatives involve the risk that changes in the value of the derivative may not

Disclosures and Risks continued on next page

Disclosures and Risks (continued)

correlate with relevant assets, rates or indices. Derivatives may be illiquid and difficult to price or unwind, and small changes may produce disproportionate losses for the Portfolio. Certain derivatives have the potential for unlimited loss, regardless of the size of the initial investment. Assets required to be set aside or posted to cover or secure derivatives positions may themselves go down in value, and these collateral and other requirements may limit investment flexibility. Some derivatives involve leverage, which can make the Portfolio more volatile and can compound other risks. The U.S. Government and foreign governments are in the process of adopting and implementing regulations governing derivatives markets, including mandatory clearing of certain derivatives, margin, reporting and registration requirements. The ultimate impact of the regulations remains unclear. Additional regulation may make derivatives more costly, may limit their availability or utility or otherwise adversely affect their performance, or may disrupt markets.

Management Risk: The Portfolio is subject to management risk because it is an actively managed investment portfolio. The Manager will apply its investment techniques and risk analyses in making investment decisions for the Portfolio, but its decisions may not produce the desired results. In some cases, derivative and other investment techniques may be unavailable or the Manager may determine not to use them, possibly even under market conditions where their use could benefit the Portfolio. In addition, the Manager may change the Portfolio’s investment strategies or policies from time to time. Those changes may not lead to the results intended by the Manager and could have an adverse effect on the Manager and could have an adverse effect on the value or performance of the Portfolio.

REIT Risk: Investing in REITs involves certain unique risks in addition to those risks associated with investing in the real estate industry in general. REITs are dependent upon management skills, are not diversified, and are subject to heavy cash flow dependency, default by borrowers and self-liquidation. Investing in REITs also involves risks similar to those associated with investing in small-capitalization companies. REITs may have limited financial resources, may trade less frequently and in a limited volume and may be subject to more abrupt or erratic price movements than larger company securities.

Investment in Other Investment Companies Risk: As with other investments, investments in other investment companies, including other AB Mutual Funds and ETFs, are subject to market and selection risk. In addition, if the Portfolio acquires shares of investment companies, shareholders bear both their proportionate share of expenses in the Portfolio (including management and advisory fees) and, indirectly, the expenses of the investment companies.

International Strategic Equities and International Small Cap Portfolios

Foreign (Non-U.S.) Securities Risk: Investments in foreign securities entail significant risks in addition to those customarily associated with investing in U.S. securities. These risks include risks related to adverse market, economic, political and regulatory factors and social instability, all of which could disrupt the financial markets in which the Portfolio invests and adversely affect the value of the Portfolio’s assets.

Country Concentration Risk: The Portfolio may not always be diversified among countries or regions and the effect on the share price of the Portfolio of specific risks identified above such as political, regulatory and currency may be magnified due to concentration of the Portfolio’s investments in a particular country or region.

Emerging Markets Securities Risk: The risks of investing in foreign (non-U.S.) securities are heightened with respect to issuers in emerging-market countries because the markets are less developed and less liquid and there may be a greater amount of economic, political and social uncertainty. In addition, the value of the Portfolio’s investments may decline because of factors such as unfavorable or unsuccessful government actions and reduction of government or central bank support.

Foreign Currency Risk: This is the risk that changes in foreign (non-U.S.) currency exchange rates may negatively affect the value of the Portfolio’s investments or reduce the returns of the Portfolio. For example, the value of the Portfolio’s investments in foreign securities and foreign currency positions may decrease if the U.S. Dollar is strong (i.e., gaining value relative to other currencies) and other currencies are weak (i.e., losing value relative to the U.S. Dollar).

Actions by a Few Major Investors: In certain countries, volatility may be heightened by actions of a few major

Disclosures and Risks continued on next page

Disclosures and Risks (continued)

investors. For example, substantial increases or decreases in cash flows of mutual funds investing in these markets could significantly affect local stock prices and, therefore, share prices of the Portfolio.

These risks are fully discussed in the Fund’s prospectus.

An Important Note About Historical Performance

The performance shown on page 8 represents past performance and does not guarantee future results. Performance information is as of the dates shown. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by calling 212.756.4097. The investment return and principal value of an investment in the Portfolios will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost.

Investors should consider the investment objectives, risks, charges and expenses of the Fund/Portfolios carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit www.bernstein.com, click on “Investments”, then “Mutual Fund Information—Prospectuses, SAIs and Shareholder Reports” or by calling Bernstein’s mutual fund shareholder help line at 212.756.4097 or contact your Bernstein Adviser. Please read the prospectus and/or summary prospectus carefully before investing.

Historical Performance (Unaudited)

Bernstein Fund Portfolios vs. Their Benchmarks and Lipper Averages

| | | | | | | | |

| | | TOTAL RETURNS | |

| THROUGH SEPTEMBER 30, 2016 | | PAST 6

MONTHS | | | SINCE

INCEPTION* | |

Small Cap Core Portfolio—SCB Class1 | | | 9.79 | % | | | 5.45 | % |

Small Cap Core Portfolio—Advisor Class | | | 10.00 | % | | | 5.65 | % |

Small Cap Core Portfolio—Class Z | | | 10.00 | % | | | 5.65 | % |

Russell 2000 Index | | | 13.18 | % | | | 9.11 | % |

Lipper Small-Cap Growth Funds | | | 12.27 | % | | | 4.78 | % |

| | | | | | | | | |

International Small Cap Portfolio—SCB Class2 | | | 7.37 | % | | | 9.20 | % |

International Small Cap Portfolio—Advisor Class | | | 7.58 | % | | | 9.30 | % |

International Small Cap Portfolio—Class Z | | | 7.58 | % | | | 9.30 | % |

MSCI ACWI ex USA Small Cap Index | | | 6.97 | % | | | 9.93 | % |

Lipper International Small/Mid-Cap Core | | | 5.52 | % | | | 6.68 | % |

| | | | | | | | | |

International Strategic Equities Portfolio—SCB Class3 | | | 4.65 | % | | | 5.75 | % |

International Strategic Equities Portfolio—Advisor Class | | | 4.76 | % | | | 5.75 | % |

International Strategic Equities Portfolio—Class Z | | | 4.75 | % | | | 5.85 | % |

MSCI ACWI ex-US Index | | | 6.22 | % | | | 7.56 | % |

Lipper International Large-Cap Core | | | 5.12 | % | | | 3.98 | % |

| * | | Inception date: 12/21/2015 for International Small Cap Portfolio and International Strategic Equities Portfolio, 12/29/15 for Small Cap Portfolio. |

| 1 | | The current prospectus table shows the total annual operating expense ratios for the Small Cap Core Portfolio as 1.15%, 0.90% and 0.90% for SCB Class, Advisor Class and Z Class shares, respectively. |

| 2 | | The current prospectus table shows the total annual operating expense ratios for the International Small Cap Portfolio as 1.39%, 1.16% and 1.14% for SCB Class, Advisor Class and Z Class shares, respectively, gross of any fee waiver or expense reimbursements. Contractual fee waivers and/or expense reimbursements limit the Fund’s annual operating expense ratios exclusive of acquired fund fees and expenses other than the advisory fees of any registered funds advised by the Adviser in which the Fund may invest, interest expense, taxes, extraordinary expenses, and brokerage commissions and other transaction costs to 1.35%, 1.10% and 1.10% for SCB Class, Advisor Class and Z Class shares, respectively. These waivers may not be terminated prior to January 4, 2017. Any fees waived and expenses borne by the Adviser may be reimbursed by the Fund until the end of the third fiscal year after the fiscal period in which the fee was waived or the expense was borne, provided that no reimbursement payment will be made that would cause the Portfolio’s total annual fund operating expenses to exceed the expense limitations. Absent reimbursements or waivers, performance would have been lower. The Financial Highlights section of this report sets forth expense ratio data for the current reporting period; the expense ratios shown above may differ from the expense ratios in the Financial Highlights section since they are based on different time periods. |

| 3 | | The current prospectus table shows the total annual operating expense ratios for the International Strategic Equities Portfolio as 1.29%, 1.05% and 1.05% for SCB Class, Advisor Class and Z Class shares, respectively, gross of any fee waiver or expense reimbursements. Contractual fee waivers and/or expense reimbursements limit the Fund’s annual operating expense ratios exclusive of acquired fund fees and expenses other than the advisory fees of any registered funds advised by the Adviser in which the Fund may invest, interest expense, taxes, extraordinary expenses, and brokerage commissions and other transaction costs), on an annualized basis, from exceeding 1.20%, 0.95% and 0.95% of average daily net assets for SCB Class, Advisor Class and Z Class shares (“expense limitations”), respectively. These waivers may not be terminated prior to January 4, 2017. Any fees waived and expenses borne by the Manager may be reimbursed by the Portfolio until the end of the third fiscal year after the fiscal period in which the fee was waived or the expense was borne, provided that no reimbursement payment will be made that would cause the Portfolio’s total annual portfolio operating expenses to exceed the expense limitations. This contractual agreement may be terminated by the Board of Directors of Bernstein Fund, Inc. at its discretion prior to the expiration date. The Adviser has contractually agreed to waive 0.05% of the management fee through December 21, 2016. |

See Disclosures, Risks and Note about Historical Performance on pages 5–7.

(Historical Performance continued on next page)

Historical Performance (continued from previous page)

| | | | |

| Small Cap Core | | | | |

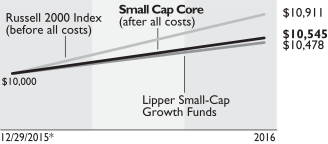

Growth of a $10,000 Investment in the Portfolio

12/29/15* to 9/30/16 | | | | |

| | | | |

| | | | |

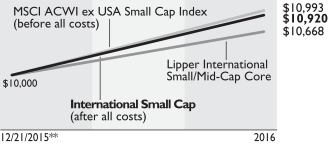

| International Small Cap | | | | |

Growth of a $10,000 Investment in the Portfolio

12/21/15** to 9/30/16 | | | | |

| | | | |

| | | | |

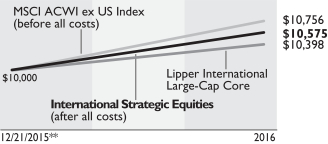

| International Strategic Equities | | | | |

Growth of a $10,000 Investment in the Portfolio

12/21/15** to 9/30/16 | | | | |

| | | | |

| * | | Inception date: 12/29/2015 |

| ** | | Inception date: 12/21/2015 |

| | | Past performance is no guarantee of future results and an investment in the portfolios described could lose value. Each chart illustrates the total value of an assumed $10,000 investment as compared to the performance of the Portfolio’s benchmark. |

See Disclosures, Risks and Note about Historical Performance on pages 5–7.

Expense Example—September 30, 2016 (Unaudited)

As a shareholder of the Portfolio, you incur various ongoing costs, including management fees and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses—The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes—The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | |

| | | BEGINNING

ACCOUNT VALUE

APRIL 1, 2016 | | | ENDING

ACCOUNT VALUE

SEPTEMBER 30, 2016 | | | EXPENSES

PAID DURING

PERIOD* | | | ANNUALIZED

EXPENSE

RATIO* | |

Small Cap Core Portfolio | | | | | | | | | | | | | | | | |

SCB Class | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,097.90 | | | $ | 6.82 | | | | 1.30 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,018.50 | | | $ | 6.56 | | | | 1.30 | % |

Advisor Class | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,100.00 | | | $ | 5.51 | | | | 1.05 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,019.75 | | | $ | 5.30 | | | | 1.05 | % |

Class Z | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,100.00 | | | $ | 5.51 | | | | 1.05 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,019.75 | | | $ | 5.30 | | | | 1.05 | % |

| |

International Small Cap Portfolio | | | | | | | | | | | | | | | | |

SCB Class | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,073.70 | | | $ | 7.00 | | | | 1.35 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,018.25 | | | $ | 6.81 | | | | 1.35 | % |

Advisor Class | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,075.80 | | | $ | 5.71 | | | | 1.10 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,019.50 | | | $ | 5.55 | | | | 1.10 | % |

Class Z | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,075.80 | | | $ | 5.71 | | | | 1.10 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,019.50 | | | $ | 5.55 | | | | 1.10 | % |

| |

International Strategic Equities Portfolio | | | | | | | | | | | | | | | | |

SCB Class | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,046.50 | | | $ | 6.14 | | | | 1.20 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,019.00 | | | $ | 6.06 | | | | 1.20 | % |

Advisor Class | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,047.60 | | | $ | 4.86 | | | | 0.95 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,020.25 | | | $ | 4.80 | | | | 0.95 | % |

Class Z | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 1,047.50 | | | $ | 4.86 | | | | 0.95 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,020.25 | | | $ | 4.80 | | | | 0.95 | % |

| |

| * | | Expenses are equal to each classes’ annualized expense ratios, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the since inception period). |

| ** | | Assumes 5% annual return before expenses. |

Portfolio Summary—September 30, 2016 (Unaudited)

| | | | | | | | | | |

| Small Cap Core Portfolio | |

| Sector Breakdown* | | | | |

Information Technology | | | 19.6 | % | | | | | | |

Industrials | | | 16.0 | | | | | | | |

Financials | | | 15.4 | | | | | | | |

Health Care | | | 14.9 | | | | | | | |

Consumer Discretionary | | | 11.2 | | | | | | | |

Real Estate | | | 6.9 | | | | | | | |

Energy | | | 5.1 | | | | | | | |

Materials | | | 4.9 | | | | | | | |

Consumer Staples | | | 2.9 | | | | | | | |

Utilities | | | 1.8 | | | | | | | |

Telecommunication Services | | | 1.3 | | | | | | | |

| | | | | | | | | | |

| | | | | | |

| | | | | | |

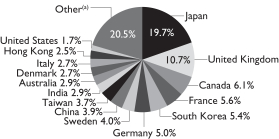

| International Small Cap Portfolio | |

| Country Breakdown* | | Sector Breakdown* | |

| | Consumer Discretionary | | | 23.5 | % |

| | Industrials | | | 16.0 | |

| | Information Technology | | | 13.0 | |

| | Consumer Staples | | | 12.2 | |

| | Materials | | | 7.7 | |

| | Health Care | | | 7.4 | |

| | Financials | | | 6.3 | |

| | Real Estate | | | 6.3 | |

| | Utilities | | | 2.6 | |

| | Energy | | | 2.4 | |

| | Telecommunication Services | | | 1.8 | |

| | Funds and Investment Trusts | | | 0.8 | |

| | | | | | |

| International Strategic Equities Portfolio | |

| Country Breakdown* | | Sector Breakdown* | |

| | Financials | | | 17.4 | % |

| | Information Technology | | | 13.8 | |

| | Materials | | | 10.4 | |

| | Consumer Discretionary | | | 10.3 | |

| | Industrials | | | 10.1 | |

| | Consumer Staples | | | 9.8 | |

| | Energy | | | 7.5 | |

| | Health Care | | | 7.0 | |

| | Real Estate | | | 6.0 | |

| | Utilities | | | 4.0 | |

| | Telecommunication Services | | | 3.7 | |

| | | | | | |

| * | | All data are as of September 30, 2016. The Portfolio’s country and sector breakdowns are expressed as a percentage of each Portfolio’s long-term investments and may vary over time. Each Portfolio may also invest in other financial instruments, including derivative instruments, which provide investment exposure to a variety of asset classes (see “Schedule of Investments” section of the report for the Small Cap Core, International Small Cap and International Strategic Equities Portfolios). |

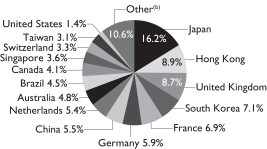

| (a) | | “Other” represents 11.3% in MSCI EM Index countries and 8.1% in MSCI EAFE Index countries and 1.1% in other emerging market countries. |

| (b) | | “Other” represents 2.5% in MSCI EM Index countries and 8.1% in MSCI EAFE Index countries. |

| | | Please note: The sector classifications presented herein are based on the Global Industry Classification Standard (GICS) which was developed by Morgan Stanley Capital International and Standard & Poor’s. The components are divided into sector, industry group, and industry sub-indices as classified by the GICS for each of the market capitalization indices in the broad market. These sector classifications are broadly defined. The “Schedule of Investments” section of the report reflects more specific industry information and is consistent with the investment restrictions discussed in the Portfolio’s prospectus. |

Schedule of Investments

Bernstein Fund, Inc.

Schedule of Investments

Small Cap Core Portfolio

September 30, 2016

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| COMMON STOCKS–97.9% | |

| Information Technology–19.2% | |

| Communications Equipment–2.1% | |

F5 Networks, Inc.(a) | | | 37,980 | | | $ | 4,733,827 | |

InterDigital, Inc./PA | | | 43,060 | | | | 3,410,352 | |

NETGEAR, Inc.(a) | | | 83,500 | | | | 5,050,915 | |

Sonus Networks, Inc.(a) | | | 287,880 | | | | 2,239,706 | |

| | | | | | | | |

| | | | | | | 15,434,800 | |

| | | | | | | | |

| Electronic Equipment, Instruments & Components–3.6% | |

Anixter International, Inc.(a) | | | 50,490 | | | | 3,256,605 | |

Benchmark Electronics, Inc.(a) | | | 164,530 | | | | 4,105,024 | |

Celestica, Inc. (Toronto)(a) | | | 155,410 | | | | 1,683,090 | |

Insight Enterprises, Inc.(a) | | | 66,680 | | | | 2,170,434 | |

Sanmina Corp.(a) | | | 161,320 | | | | 4,592,780 | |

SYNNEX Corp. | | | 60,190 | | | | 6,868,281 | |

Tech Data Corp.(a) | | | 44,200 | | | | 3,744,182 | |

| | | | | | | | |

| | | | | | | 26,420,396 | |

| | | | | | | | |

| Internet Software & Services–1.5% | |

Cimpress NV(a) | | | 39,050 | | | | 3,951,079 | |

Shutterstock, Inc.(a) | | | 66,170 | | | | 4,215,029 | |

Web.com Group, Inc.(a) | | | 159,010 | | | | 2,746,103 | |

| | | | | | | | |

| | | | | | | 10,912,211 | |

| | | | | | | | |

| IT Services–4.6% | |

Booz Allen Hamilton Holding Corp. | | | 89,990 | | | | 2,844,584 | |

Cardtronics PLC–Class A(a) | | | 49,890 | | | | 2,225,094 | |

Convergys Corp. | | | 176,900 | | | | 5,381,298 | |

CSG Systems International, Inc. | | | 71,550 | | | | 2,957,161 | |

EVERTEC, Inc. | | | 169,840 | | | | 2,849,915 | |

Hackett Group, Inc. (The) | | | 218,680 | | | | 3,612,594 | |

Lionbridge Technologies, Inc.(a) | | | 547,050 | | | | 2,735,250 | |

ManTech International Corp./VA–Class A | | | 108,420 | | | | 4,086,350 | |

Perficient, Inc.(a) | | | 94,930 | | | | 1,912,840 | |

Science Applications International Corp. | | | 78,160 | | | | 5,421,959 | |

| | | | | | | | |

| | | | | | | 34,027,045 | |

| | | | | | | | |

| Semiconductors & Semiconductor Equipment–4.7% | |

Advanced Energy Industries, Inc.(a) | | | 122,100 | | | | 5,777,772 | |

Cavium, Inc.(a) | | | 20,997 | | | | 1,222,025 | |

Cirrus Logic, Inc.(a) | | | 83,230 | | | | 4,423,674 | |

Integrated Device Technology, Inc.(a) | | | 226,261 | | | | 5,226,629 | |

IXYS Corp. | | | 182,740 | | | | 2,202,017 | |

Mellanox Technologies Ltd.(a) | | | 41,780 | | | | 1,806,985 | |

ON Semiconductor Corp.(a) | | | 333,030 | | | | 4,102,930 | |

Silicon Laboratories, Inc.(a) | | | 57,760 | | | | 3,396,288 | |

Synaptics, Inc.(a) | | | 61,450 | | | | 3,599,741 | |

Tessera Technologies, Inc. | | | 69,440 | | | | 2,669,274 | |

| | | | | | | | |

| | | | | | | 34,427,335 | |

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| Software–2.3% | |

Aspen Technology, Inc.(a) | | | 117,420 | | | $ | 5,494,082 | |

Atlassian Corp. PLC–Class A(a) | | | 95,010 | | | | 2,847,450 | |

Barracuda Networks, Inc.(a) | | | 145,850 | | | | 3,716,258 | |

Manhattan Associates, Inc.(a) | | | 32,580 | | | | 1,877,259 | |

Mentor Graphics Corp. | | | 110,530 | | | | 2,922,413 | |

| | | | | | | | |

| | | | | | | 16,857,462 | |

| | | | | | | | |

| Technology Hardware, Storage & Peripherals–0.4% | |

NCR Corp.(a) | | | 89,930 | | | | 2,894,847 | |

| | | | | | | | |

| | | | | | | 140,974,096 | |

| | | | | | | | |

| | | | | | | | |

| |

| Industrials–15.7% | |

| Aerospace & Defense–0.4% | |

Engility Holdings, Inc.(a) | | | 95,300 | | | | 3,001,950 | |

| | | | | | | | |

| Air Freight & Logistics–0.3% | |

Hub Group, Inc.–Class A(a) | | | 51,140 | | | | 2,084,467 | |

| | | | | | | | |

| Building Products–2.4% | |

Gibraltar Industries, Inc.(a) | | | 54,320 | | | | 2,017,988 | |

Insteel Industries, Inc. | | | 66,400 | | | | 2,406,336 | |

NCI Building Systems, Inc.(a) | | | 167,310 | | | | 2,441,053 | |

Patrick Industries, Inc.(a) | | | 32,650 | | | | 2,021,688 | |

Ply Gem Holdings, Inc.(a) | | | 199,910 | | | | 2,670,798 | |

Trex Co., Inc.(a) | | | 53,650 | | | | 3,150,328 | |

Universal Forest Products, Inc. | | | 26,060 | | | | 2,566,649 | |

| | | | | | | | |

| | | | | | | 17,274,840 | |

| | | | | | | | |

| Commercial Services & Supplies–1.8% | |

ABM Industries, Inc. | | | 56,120 | | | | 2,227,964 | |

ACCO Brands Corp.(a) | | | 127,300 | | | | 1,227,172 | |

Deluxe Corp. | | | 43,480 | | | | 2,905,334 | |

Herman Miller, Inc. | | | 38,770 | | | | 1,108,822 | |

Quad/Graphics, Inc. | | | 121,430 | | | | 3,244,609 | |

Tetra Tech, Inc. | | | 70,900 | | | | 2,514,823 | |

| | | | | | | | |

| | | | | | | 13,228,724 | |

| | | | | | | | |

| Construction & Engineering–3.0% | |

AECOM(a) | | | 89,450 | | | | 2,659,348 | |

Comfort Systems USA, Inc. | | | 68,250 | | | | 2,000,408 | |

EMCOR Group, Inc. | | | 68,150 | | | | 4,063,103 | |

Jacobs Engineering Group, Inc.(a) | | | 53,040 | | | | 2,743,229 | |

MYR Group, Inc.(a) | | | 101,240 | | | | 3,047,324 | |

Quanta Services, Inc.(a) | | | 204,250 | | | | 5,716,957 | |

Valmont Industries, Inc. | | | 14,010 | | | | 1,885,326 | |

| | | | | | | | |

| | | | | | | 22,115,695 | |

| | | | | | | | |

| Electrical Equipment–0.7% | |

Babcock & Wilcox Enterprises, Inc.(a) | | | 151,350 | | | | 2,497,275 | |

EnerSys | | | 41,930 | | | | 2,901,137 | |

| | | | | | | | |

| | | | | | | 5,398,412 | |

| | | | | | | | |

| Machinery–1.7% | | | | | | | | |

Briggs & Stratton Corp. | | | 116,810 | | | | 2,178,507 | |

Chart Industries, Inc.(a) | | | 69,592 | | | | 2,284,705 | |

Global Brass & Copper Holdings, Inc. | | | 116,280 | | | | 3,359,329 | |

Kadant, Inc. | | | 44,730 | | | | 2,330,880 | |

Lincoln Electric Holdings, Inc. | | | 32,900 | | | | 2,060,198 | |

| | | | | | | | |

| | | | | | | 12,213,619 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| Company | | Shares | | | U.S. $ Value | |

| Professional Services–2.4% | | | | | | | | |

Huron Consulting Group, Inc.(a) | | | 72,350 | | | $ | 4,323,636 | |

Insperity, Inc. | | | 52,620 | | | | 3,822,317 | |

Kforce, Inc. | | | 202,980 | | | | 4,159,060 | |

TrueBlue, Inc.(a) | | | 223,670 | | | | 5,068,362 | |

| | | | | | | | |

| | | | | | | 17,373,375 | |

| | | | | | | | |

| Road & Rail–0.6% | | | | | | | | |

Saia, Inc.(a) | | | 69,490 | | | | 2,081,920 | |

Werner Enterprises, Inc. | | | 109,110 | | | | 2,538,990 | |

| | | | | | | | |

| | | | | | | 4,620,910 | |

| | | | | | | | |

| Trading Companies & Distributors–2.4% | | | | | | | | |

Applied Industrial Technologies, Inc. | | | 103,000 | | | | 4,814,220 | |

MRC Global, Inc.(a) | | | 381,090 | | | | 6,261,309 | |

MSC Industrial Direct Co., Inc.–Class A | | | 46,580 | | | | 3,419,438 | |

WESCO International, Inc.(a) | | | 56,590 | | | | 3,479,719 | |

| | | | | | | | |

| | | | | | | 17,974,686 | |

| | | | | | | | |

| | | | | | | 115,286,678 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| Financials–15.1% | | | | | | | | |

| Banks–8.3% | | | | | | | | |

1st Source Corp. | | | 78,060 | | | | 2,786,352 | |

Bank of the Ozarks, Inc. | | | 26,910 | | | | 1,033,344 | |

Cathay General Bancorp | | | 159,470 | | | | 4,908,487 | |

City Holding Co. | | | 49,090 | | | | 2,468,736 | |

Community Trust Bancorp, Inc. | | | 64,170 | | | | 2,381,349 | |

Fidelity Southern Corp. | | | 109,810 | | | | 2,019,406 | |

First Citizens BancShares, Inc./NC–Class A | | | 8,670 | | | | 2,548,026 | |

First Community Bancshares, Inc./VA | | | 73,880 | | | | 1,832,224 | |

First Financial Corp./IN | | | 108,310 | | | | 4,406,051 | |

Flushing Financial Corp. | | | 102,530 | | | | 2,432,012 | |

Great Southern Bancorp, Inc. | | | 58,710 | | | | 2,389,497 | |

Great Western Bancorp, Inc. | | | 43,370 | | | | 1,445,088 | |

Hanmi Financial Corp. | | | 148,520 | | | | 3,912,017 | |

Hilltop Holdings, Inc.(a) | | | 147,720 | | | | 3,317,791 | |

Hope Bancorp, Inc. | | | 117,411 | | | | 2,039,429 | |

International Bancshares Corp. | | | 177,510 | | | | 5,286,248 | |

Prosperity Bancshares, Inc. | | | 28,150 | | | | 1,545,153 | |

Republic Bancorp, Inc./KY–Class A | | | 75,930 | | | | 2,359,904 | |

Sierra Bancorp | | | 116,900 | | | | 2,193,044 | |

Texas Capital Bancshares, Inc.(a) | | | 47,040 | | | | 2,583,437 | |

Triumph Bancorp, Inc.(a) | | | 235,422 | | | | 4,670,772 | |

Western Alliance Bancorp(a) | | | 62,870 | | | | 2,360,140 | |

| | | | | | | | |

| | | | | | | 60,918,507 | |

| | | | | | | | |

| Capital Markets–0.6% | |

Cohen & Steers, Inc. | | | 49,050 | | | | 2,096,888 | |

MarketAxess Holdings, Inc. | | | 12,500 | | | | 2,069,875 | |

| | | | | | | | |

| | | | | | | 4,166,763 | |

| | | | | | | | |

| Consumer Finance–0.3% | |

Nelnet, Inc.–Class A | | | 57,260 | | | | 2,311,586 | |

| | | | | | | | |

| Insurance–2.2% | |

Ambac Financial Group, Inc.(a) | | | 286,770 | | | | 5,273,700 | |

Heritage Insurance Holdings, Inc. | | | 105,450 | | | | 1,519,535 | |

| Company | | Shares | | | U.S. $ Value | |

MBIA, Inc.(a) | | | 307,960 | | | $ | 2,399,008 | |

State Auto Financial Corp. | | | 130,840 | | | | 3,115,301 | |

Universal Insurance Holdings, Inc. | | | 166,070 | | | | 4,184,964 | |

| | | | | | | | |

| | | | | | | 16,492,508 | |

| | | | | | | | |

| Mortgage Real Estate Investment Trusts (REITs)–1.8% | |

American Capital Mortgage Investment Corp. | | | 122,180 | | | | 2,100,274 | |

Ares Commercial Real Estate Corp. | | | 179,730 | | | | 2,264,598 | |

Invesco Mortgage Capital, Inc. | | | 128,640 | | | | 1,959,187 | |

New Residential Investment Corp. | | | 176,420 | | | | 2,436,360 | |

PennyMac Mortgage Investment Trust | | | 139,040 | | | | 2,166,243 | |

Redwood Trust, Inc. | | | 147,010 | | | | 2,081,662 | |

| | | | | | | | |

| | | | | | | 13,008,324 | |

| | | | | | | | |

| Thrifts & Mortgage Finance–1.9% | |

Flagstar Bancorp, Inc.(a) | | | 132,750 | | | | 3,683,812 | |

MGIC Investment Corp.(a) | | | 746,370 | | | | 5,970,960 | |

Radian Group, Inc. | | | 333,960 | | | | 4,525,158 | |

| | | | | | | | |

| | | | | | | 14,179,930 | |

| | | | | | | | |

| | | | | | | 111,077,618 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| Health Care–14.5% | | | | | | | | |

| Biotechnology–4.7% | |

AMAG Pharmaceuticals, Inc.(a) | | | 117,840 | | | | 2,888,258 | |

ARIAD Pharmaceuticals, Inc.(a) | | | 269,380 | | | | 3,687,812 | |

Cepheid(a) | | | 87,000 | | | | 4,584,030 | |

Enanta Pharmaceuticals, Inc.(a) | | | 115,190 | | | | 3,065,206 | |

FibroGen, Inc.(a) | | | 70,170 | | | | 1,452,519 | |

Five Prime Therapeutics, Inc.(a) | | | 56,550 | | | | 2,968,310 | |

Genomic Health, Inc.(a) | | | 54,040 | | | | 1,562,837 | |

Insys Therapeutics, Inc.(a) | | | 105,330 | | | | 1,241,841 | |

Lexicon Pharmaceuticals, Inc.(a) | | | 123,760 | | | | 2,236,343 | |

Myriad Genetics, Inc.(a) | | | 24,740 | | | | 509,149 | |

Neurocrine Biosciences, Inc.(a) | | | 31,520 | | | | 1,596,173 | |

Repligen Corp.(a) | | | 78,930 | | | | 2,382,897 | |

Vanda Pharmaceuticals, Inc.(a) | | | 217,350 | | | | 3,616,704 | |

Xencor, Inc.(a) | | | 108,690 | | | | 2,661,818 | |

| | | | | | | | |

| | | | | | | 34,453,897 | |

| | | | | | | | |

| Health Care Equipment & Supplies–3.1% | |

Align Technology, Inc.(a) | | | 34,410 | | | | 3,225,938 | |

AngioDynamics, Inc.(a) | | | 134,800 | | | | 2,364,392 | |

Atrion Corp. | | | 3,730 | | | | 1,591,218 | |

Exactech, Inc.(a) | | | 70,630 | | | | 1,909,129 | |

Halyard Health, Inc.(a) | | | 80,500 | | | | 2,790,130 | |

Masimo Corp.(a) | | | 27,080 | | | | 1,610,989 | |

OraSure Technologies, Inc.(a) | | | 385,920 | | | | 3,075,782 | |

Orthofix International NV(a) | | | 106,810 | | | | 4,568,264 | |

West Pharmaceutical Services, Inc. | | | 27,110 | | | | 2,019,695 | |

| | | | | | | | |

| | | | | | | 23,155,537 | |

| | | | | | | | |

| Health Care Providers & Services–2.1% | |

Chemed Corp. | | | 21,550 | | | | 3,040,058 | |

HealthSouth Corp. | | | 56,110 | | | | 2,276,383 | |

Molina Healthcare, Inc.(a) | | | 98,530 | | | | 5,746,270 | |

WellCare Health Plans, Inc.(a) | | | 38,550 | | | | 4,513,819 | |

| | | | | | | | |

| | | | | | | 15,576,530 | |

| | | | | | | | |

Schedule of Investments (continued)

| | | | | | | | |

| | | |

| Company | | Shares | | | U.S. $ Value | |

| Life Sciences Tools & Services–1.1% | |

ICON PLC(a) | | | 55,010 | | | $ | 4,256,124 | |

INC Research Holdings, Inc.–Class A(a) | | | 49,140 | | | | 2,190,661 | |

PAREXEL International Corp.(a) | | | 20,910 | | | | 1,452,199 | |

| | | | | | | | |

| | | | | | | 7,898,984 | |

| | | | | | | | |

| Pharmaceuticals–3.5% | | | | | | | | |

Akorn, Inc.(a) | | | 68,980 | | | | 1,880,395 | |

Amphastar Pharmaceuticals, Inc.(a) | | | 158,820 | | | | 3,012,815 | |

ANI Pharmaceuticals, Inc.(a) | | | 41,100 | | | | 2,726,985 | |

Aratana Therapeutics, Inc.(a) | | | 157,100 | | | | 1,470,456 | |

Corcept Therapeutics, Inc.(a) | | | 315,640 | | | | 2,051,660 | |

Depomed, Inc.(a) | | | 162,570 | | | | 4,062,624 | |

Impax Laboratories, Inc.(a) | | | 91,780 | | | | 2,175,186 | |

Prestige Brands Holdings, Inc.(a) | | | 54,730 | | | | 2,641,817 | |

SciClone Pharmaceuticals, Inc.(a) | | | 237,480 | | | | 2,434,170 | |

Supernus Pharmaceuticals, Inc.(a) | | | 140,790 | | | | 3,481,737 | |

| | | | | | | | |

| | | | | | | 25,937,845 | |

| | | | | | | | |

| | | | | | | 107,022,793 | |

| | | | | | | | |

| | | | | | | | |

| |

| Consumer Discretionary–10.9% | |

| Auto Components–1.8% | | | | | | | | |

Dana, Inc. | | | 349,670 | | | | 5,451,355 | |

Stoneridge, Inc.(a) | | | 99,290 | | | | 1,826,936 | |

Tenneco, Inc.(a) | | | 96,170 | | | | 5,603,826 | |

| | | | | | | | |

| | | | | | | 12,882,117 | |

| | | | | | | | |

| Automobiles–0.5% | | | | | | | | |

Winnebago Industries, Inc. | | | 145,310 | | | | 3,424,957 | |

| | | | | | | | |

| Diversified Consumer Services–0.8% | |

Capella Education Co. | | | 50,260 | | | | 2,917,090 | |

Strayer Education, Inc.(a) | | | 63,300 | | | | 2,954,844 | |

| | | | | | | | |

| | | | | | | 5,871,934 | |

| | | | | | | | |

| Hotels, Restaurants & Leisure–3.1% | |

Bloomin’ Brands, Inc. | | | 239,460 | | | | 4,128,291 | |

Brinker International, Inc. | | | 72,810 | | | | 3,671,808 | |

Denny’s Corp.(a) | | | 400,660 | | | | 4,283,056 | |

Jack in the Box, Inc. | | | 20,910 | | | | 2,006,105 | |

Papa John’s International, Inc. | | | 49,030 | | | | 3,866,016 | |

Potbelly Corp.(a) | | | 174,710 | | | | 2,171,645 | |

Ruth’s Hospitality Group, Inc. | | | 183,360 | | | | 2,589,043 | |

| | | | | | | | |

| | | | | | | 22,715,964 | |

| | | | | | | | |

| Household Durables–0.2% | |

NACCO Industries, Inc.–Class A | | | 21,530 | | | | 1,463,179 | |

| | | | | | | | |

| Leisure Products–0.3% | |

JAKKS Pacific, Inc.(a) | | | 182,400 | | | | 1,575,936 | |

Smith & Wesson Holding Corp.(a) | | | 28,610 | | | | 760,740 | |

| | | | | | | | |

| | | | | | | 2,336,676 | |

| | | | | | | | |

| Media–0.7% | | | | | | | | |

New Media Investment Group, Inc. | | | 178,660 | | | | 2,769,230 | |

New York Times Co. (The)–Class A | | | 224,820 | | | | 2,686,599 | |

| | | | | | | | |

| | | | | | | 5,455,829 | |

| | | | | | | | |

| Multiline Retail–0.2% | | | | | | | | |

Big Lots, Inc. | | | 38,600 | | | | 1,843,150 | |

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| Specialty Retail–2.8% | | | | | | | | |

Caleres, Inc. | | | 169,720 | | | $ | 4,292,219 | |

Children’s Place, Inc. (The) | | | 56,260 | | | | 4,493,486 | |

Citi Trends, Inc. | | | 168,380 | | | | 3,355,813 | |

Francesca’s Holdings Corp.(a) | | | 201,970 | | | | 3,116,397 | |

Michaels Cos., Inc. (The)(a) | | | 56,140 | | | | 1,356,904 | |

Urban Outfitters, Inc.(a) | | | 108,080 | | | | 3,730,922 | |

| | | | | | | | |

| | | | | | | 20,345,741 | |

| | | | | | | | |

| Textiles, Apparel & Luxury Goods–0.5% | |

Perry Ellis International, Inc.(a) | | | 86,560 | | | | 1,668,877 | |

Wolverine World Wide, Inc. | | | 101,220 | | | | 2,331,096 | |

| | | | | | | | |

| | | | | | | 3,999,973 | |

| | | | | | | | |

| | | | | | | 80,339,520 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| Real Estate–6.8% | | | | | | | | |

| Equity Real Estate Investment Trusts (REITs)–6.8% | |

Chesapeake Lodging Trust | | | 101,650 | | | | 2,327,785 | |

CorEnergy Infrastructure Trust, Inc. | | | 102,840 | | | | 3,016,297 | |

DCT Industrial Trust, Inc. | | | 42,530 | | | | 2,064,832 | |

Education Realty Trust, Inc. | | | 88,100 | | | | 3,800,634 | |

EPR Properties | | | 31,750 | | | | 2,499,995 | |

First Industrial Realty Trust, Inc. | | | 38,970 | | | | 1,099,733 | |

Franklin Street Properties Corp. | | | 160,880 | | | | 2,027,088 | |

Getty Realty Corp. | | | 143,000 | | | | 3,421,990 | |

Gramercy Property Trust | | | 467,570 | | | | 4,507,375 | |

Highwoods Properties, Inc. | | | 36,140 | | | | 1,883,617 | |

Independence Realty Trust, Inc. | | | 339,010 | | | | 3,051,090 | |

iStar, Inc.(a) | | | 266,690 | | | | 2,861,584 | |

Medical Properties Trust, Inc. | | | 173,350 | | | | 2,560,379 | |

National Health Investors, Inc. | | | 28,180 | | | | 2,211,566 | |

One Liberty Properties, Inc. | | | 56,280 | | | | 1,359,725 | |

Select Income REIT | | | 111,180 | | | | 2,990,742 | |

Summit Hotel Properties, Inc. | | | 227,280 | | | | 2,991,005 | |

Sun Communities, Inc. | | | 21,020 | | | | 1,649,650 | |

Sunstone Hotel Investors, Inc. | | | 153,790 | | | | 1,966,974 | |

Xenia Hotels & Resorts, Inc. | | | 93,090 | | | | 1,413,106 | |

| | | | | | | | |

| | | | | | | 49,705,167 | |

| | | | | | | | |

| | | | | | | | |

| |

| Energy–5.0% | |

| Energy Equipment & Services–2.8% | |

Archrock, Inc. | | | 156,360 | | | | 2,045,189 | |

Dril-Quip, Inc.(a) | | | 45,820 | | | | 2,554,007 | |

Matrix Service Co.(a) | | | 148,490 | | | | 2,785,672 | |

McDermott International, Inc.(a) | | | 918,090 | | | | 4,599,631 | |

Oil States International, Inc.(a) | | | 149,140 | | | | 4,708,350 | |

RPC, Inc.(a) | | | 244,370 | | | | 4,105,416 | |

| | | | | | | | |

| | | | | | | 20,798,265 | |

| | | | | | | | |

| Oil, Gas & Consumable Fuels–2.2% | |

Gulfport Energy Corp.(a) | | | 77,050 | | | | 2,176,662 | |

Matador Resources Co.(a) | | | 138,330 | | | | 3,366,952 | |

QEP Resources, Inc. | | | 114,390 | | | | 2,234,037 | |

REX American Resources Corp.(a) | | | 48,470 | | | | 4,108,317 | |

SM Energy Co. | | | 112,070 | | | | 4,323,661 | |

| | | | | | | | |

| | | | | | | 16,209,629 | |

| | | | | | | | |

| | | | | | | 37,007,894 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| Company | | Shares | | | U.S. $ Value | |

| Materials–4.7% | |

| Chemicals–1.9% | |

Huntsman Corp. | | | 191,890 | | | $ | 3,122,050 | |

Koppers Holdings, Inc.(a) | | | 88,730 | | | | 2,855,332 | |

PolyOne Corp. | | | 78,390 | | | | 2,650,366 | |

Trinseo SA | | | 89,620 | | | | 5,068,907 | |

| | | | | | | | |

| | | | | | | 13,696,655 | |

| | | | | | | | |

| Containers & Packaging–0.8% | |

Bemis Co., Inc. | | | 63,560 | | | | 3,242,196 | |

Graphic Packaging Holding Co. | | | 210,260 | | | | 2,941,537 | |

| | | | | | | | |

| | | | | | | 6,183,733 | |

| | | | | | | | |

| Metals & Mining–2.0% | |

Commercial Metals Co. | | | 189,810 | | | | 3,073,024 | |

Reliance Steel & Aluminum Co. | | | 21,850 | | | | 1,573,855 | |

Schnitzer Steel Industries, Inc.–Class A | | | 180,350 | | | | 3,769,315 | |

Steel Dynamics, Inc. | | | 118,500 | | | | 2,961,315 | |

Worthington Industries, Inc. | | | 77,430 | | | | 3,718,963 | |

| | | | | | | | |

| | | | | | | 15,096,472 | |

| | | | | | | | |

| | | | | | | 34,976,860 | |

| | | | | | | | |

| | | | | | | | |

| |

| Consumer Staples–2.9% | |

| Food & Staples Retailing–0.5% | |

SpartanNash Co. | | | 135,730 | | | | 3,925,312 | |

| | | | | | | | |

| Food Products–1.5% | |

Fresh Del Monte Produce, Inc. | | | 80,610 | | | | 4,828,539 | |

Sanderson Farms, Inc. | | | 33,910 | | | | 3,266,550 | |

Seaboard Corp.(a) | | | 810 | | | | 2,786,400 | |

| | | | | | | | |

| | | | | | | 10,881,489 | |

| | | | | | | | |

| Personal Products–0.4% | |

Natural Health Trends Corp. | | | 100,870 | | | | 2,850,586 | |

| | | | | | | | |

| Tobacco–0.5% | | | | | | | | |

Universal Corp./VA | | | 58,530 | | | | 3,407,617 | |

| | | | | | | | |

| | | | | | | 21,065,004 | |

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| Utilities–1.8% | |

| Gas Utilities–0.9% | |

ONE Gas, Inc. | | | 43,910 | | | $ | 2,715,394 | |

Southwest Gas Corp. | | | 53,750 | | | | 3,754,975 | |

| | | | | | | | |

| | | | | | | 6,470,369 | |

| | | | | | | | |

| Independent Power and Renewable Electricity Producers–0.9% | |

Atlantic Power Corp. | | | 883,260 | | | | 2,181,652 | |

Talen Energy Corp.(a) | | | 318,790 | | | | 4,415,242 | |

| | | | | | | | |

| | | | | | | 6,596,894 | |

| | | | | | | | |

| | | | | | | 13,067,263 | |

| | | | | | | | |

| | | | | | | | |

| |

| Telecommunication Services–1.3% | |

| Diversified Telecommunication Services–1.1% | |

IDT Corp.–Class B | | | 202,060 | | | | 3,483,514 | |

Vonage Holdings Corp.(a) | | | 729,460 | | | | 4,821,731 | |

| | | | | | | | |

| | | | | | | 8,305,245 | |

| | | | | | | | |

| Wireless Telecommunication Services–0.2% | |

Spok Holdings, Inc. | | | 59,370 | | | | 1,057,973 | |

| | | | | | | | |

| | | | | | | 9,363,218 | |

| | | | | | | | |

Total Common Stocks

(cost $678,869,061) | | | | | | | 719,886,111 | |

| | | | | | | | |

| | | | | | | | |

| |

| SHORT-TERM INVESTMENTS–1.6% | |

| Investment Companies–1.6% | |

AB Fixed Income Shares, Inc.–

Government Money Market Portfolio–

Class AB, 0.28%(b)(c)

(cost $12,157,406) | | | 12,157,406 | | | | 12,157,406 | |

| | | | | | | | |

Total Investments—99.5%

(cost $691,026,467) | | | | | | | 732,043,517 | |

| | |

Other assets less liabilities—0.5% | | | | | | | 3,468,532 | |

| | | | | | | | |

| Net Assets—100.0% | | | | | | $ | 735,512,049 | |

| | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| |

| FUTURES (see Note 3) | |

| Type | | Number of Contracts | | | Expiration Month | | Original Value | | | Value at September 30, 2016 | | | Unrealized Appreciation/

(Depreciation) | |

| Purchased Contracts | | | | | | | | | | | | | | | |

Russell 2000 Mini Futures | | | 343 | | | December 2016 | | $ | 42,307,947 | | | $ | 42,816,690 | | | $ | 508,743 | |

| (a) | | Non-income producing security. |

| (b) | | Investment in affiliated money market mutual fund. The rate shown represents the 7-day yield as of period end. |

| (c) | | To obtain a copy of the fund’s financial statements, please go to the Securities and Exchange Commission’s website at www.sec.gov, or call AB at (800) 227-4618. |

Glossary:

REIT—Real Estate Investment Trust

See notes to financial statements.

Schedule of Investments

Bernstein Fund, Inc.

Schedule of Investments

International Small Cap Portfolio

September 30, 2016

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| | | | | | | | |

| COMMON STOCKS–93.3% | |

| Consumer Discretionary–22.2% | |

| Auto Components–4.4% | | | | | | | | |

Aisan Industry Co., Ltd. | | | 102,100 | | | $ | 810,257 | |

Brembo SpA | | | 13,757 | | | | 820,904 | |

Faurecia | | | 64,828 | | | | 2,544,022 | |

Hankook Tire Co., Ltd. | | | 97,269 | | | | 5,258,983 | |

Hanon Systems | | | 217,900 | | | | 2,465,401 | |

Linamar Corp. | | | 84,038 | | | | 3,508,977 | |

Nexen Tire Corp. | | | 209,869 | | | | 2,828,390 | |

Nexteer Automotive Group Ltd. | | | 4,968,288 | | | | 6,495,996 | |

Plastic Omnium SA | | | 92,105 | | | | 3,056,457 | |

Showa Corp. | | | 104,500 | | | | 550,639 | |

Tianneng Power International Ltd. | | | 874,000 | | | | 748,170 | |

| | | | | | | | |

| | | | | | | 29,088,196 | |

| | | | | | | | |

| Distributors–0.1% | |

John Menzies PLC | | | 44,625 | | | | 337,211 | |

| | | | | | | | |

| Diversified Consumer Services–1.1% | |

Navitas Ltd. | | | 171,541 | | | | 688,165 | |

TAL Education Group (ADR)(a) | | | 79,146 | | | | 5,606,703 | |

Tarena International, Inc. (ADR) | | | 90,908 | | | | 1,316,348 | |

| | | | | | | | |

| | | | | | | 7,611,216 | |

| | | | | | | | |

| Hotels, Restaurants & Leisure–3.0% | |

Alsea SAB de CV | | | 188,310 | | | | 637,193 | |

CVC Brasil Operadora e Agencia de Viagens SA | | | 146,319 | | | | 1,082,045 | |

Domino’s Pizza Group PLC | | | 501,492 | | | | 2,427,840 | |

Elior Group(b) | | | 82,014 | | | | 1,877,880 | |

IMAX China Holding, Inc.(a)(b) | | | 824,800 | | | | 4,058,672 | |

Jollibee Foods Corp. | | | 1,147,430 | | | | 5,850,159 | |

Lion Travel Service Co., Ltd. | | | 197,000 | | | | 497,866 | |

Plenus Co., Ltd. | | | 18,700 | | | | 341,933 | |

Round One Corp. | | | 99,700 | | | | 676,197 | |

Tabcorp Holdings Ltd. | | | 527,884 | | | | 2,021,448 | |

| | | | | | | | |

| | | | | | | 19,471,233 | |

| | | | | | | | |

| Household Durables–1.1% | |

Auto Trader Group PLC(b) | | | 448,388 | | | | 2,357,161 | |

Bovis Homes Group PLC | | | 161,648 | | | | 1,832,785 | |

De’ Longhi SpA | | | 5,309 | | | | 128,584 | |

Dorel Industries, Inc.–Class B | | | 27,460 | | | | 739,272 | |

Fujitsu General Ltd. | | | 18,000 | | | | 389,991 | |

SEB SA | | | 5,961 | | | | 841,890 | |

Token Corp. | | | 9,000 | | | | 670,586 | |

| | | | | | | | |

| | | | | | | 6,960,269 | |

| | | | | | | | |

| | | | | | | | |

| Internet & Direct Marketing Retail–0.6% | |

ASKUL Corp. | | | 90,800 | | | $ | 3,444,177 | |

GS Home Shopping, Inc. | | | 4,701 | | | | 703,483 | |

| | | | | | | | |

| | | | | | | 4,147,660 | |

| | | | | | | | |

| Leisure Products–1.6% | |

Amer Sports Oyj | | | 93,020 | | | | 2,845,048 | |

Bandai Namco Holdings, Inc. | | | 73,800 | | | | 2,258,877 | |

Playmates Toys Ltd. | | | 4,528,000 | | | | 698,795 | |

Thule Group AB(b) | | | 277,360 | | | | 4,730,579 | |

| | | | | | | | |

| | | | | | | 10,533,299 | |

| | | | | | | | |

| Media–3.1% | | | | | | | | |

Asatsu-DK, Inc. | | | 31,200 | | | | 831,044 | |

IPSOS | | | 24,661 | | | | 805,553 | |

Loen Entertainment, Inc.(a) | | | 77,536 | | | | 5,506,737 | |

Mediaset Espana Comunicacion SA | | | 41,860 | | | | 496,214 | |

Megacable Holdings SAB de CV | | | 503,409 | | | | 1,933,437 | |

Metropole Television SA | | | 185,802 | | | | 3,352,350 | |

NOS SGPS SA | | | 352,306 | | | | 2,397,331 | |

TV Asahi Holdings Corp. | | | 293,800 | | | | 5,418,613 | |

| | | | | | | | |

| | | | | | | 20,741,279 | |

| | | | | | | | |

| Multiline Retail–1.5% | | | | | | | | |

Dollarama, Inc. | | | 40,650 | | | | 3,173,733 | |

Harvey Norman Holdings Ltd. | | | 686,329 | | | | 2,747,324 | |

Myer Holdings Ltd. | | | 628,730 | | | | 564,168 | |

Poya International Co., Ltd. | | | 25,200 | | | | 375,415 | |

Seria Co., Ltd. | | | 39,900 | | | | 3,207,841 | |

| | | | | | | | |

| | | | | | | 10,068,481 | |

| | | | | | | | |

| Specialty Retail–3.6% | | | | | | | | |

Ace Hardware Indonesia Tbk PT | | | 36,585,100 | | | | 2,456,998 | |

Clas Ohlson AB–Class B | | | 39,767 | | | | 619,069 | |

Delek Automotive Systems Ltd. | | | 79,040 | | | | 691,303 | |

EDION Corp. | | | 82,200 | | | | 688,572 | |

Geo Holdings Corp. | | | 52,400 | | | | 678,055 | |

Giordano International Ltd. | | | 1,426,000 | | | | 736,883 | |

Groupe Fnac SA(a) | | | 11,930 | | | | 876,387 | |

Halfords Group PLC | | | 117,221 | | | | 531,342 | |

JB Hi-Fi Ltd. | | | 40,222 | | | | 895,231 | |

JD Sports Fashion PLC | | | 7,020 | | | | 134,218 | |

KappAhl AB | | | 158,090 | | | | 805,828 | |

Mobilezone Holding AG | | | 51,769 | | | | 759,350 | |

Motorpoint Group PLC(a)(b) | | | 676,257 | | | | 1,730,800 | |

Mr Price Group Ltd. | | | 143,285 | | | | 1,585,075 | |

Nishimatsuya Chain Co., Ltd. | | | 50,700 | | | | 770,635 | |

PAL GROUP Holdings Co., Ltd. | | | 13,000 | | | | 301,888 | |

Senao International Co., Ltd. | | | 125,000 | | | | 209,579 | |

Shimamura Co., Ltd. | | | 19,400 | | | | 2,361,782 | |