Exhibit (c)(ii) Confidential Treatment Requested. Certain portions of this exhibit have been redacted and separately filed with the Securities and Exchange Commission pursuant to a request for confidential treatment. Valuation Materials Underlying Fairness Opinion Project Orange October 10, 2022 PRELIMINARY AND CONFIDENTIAL DRAFT

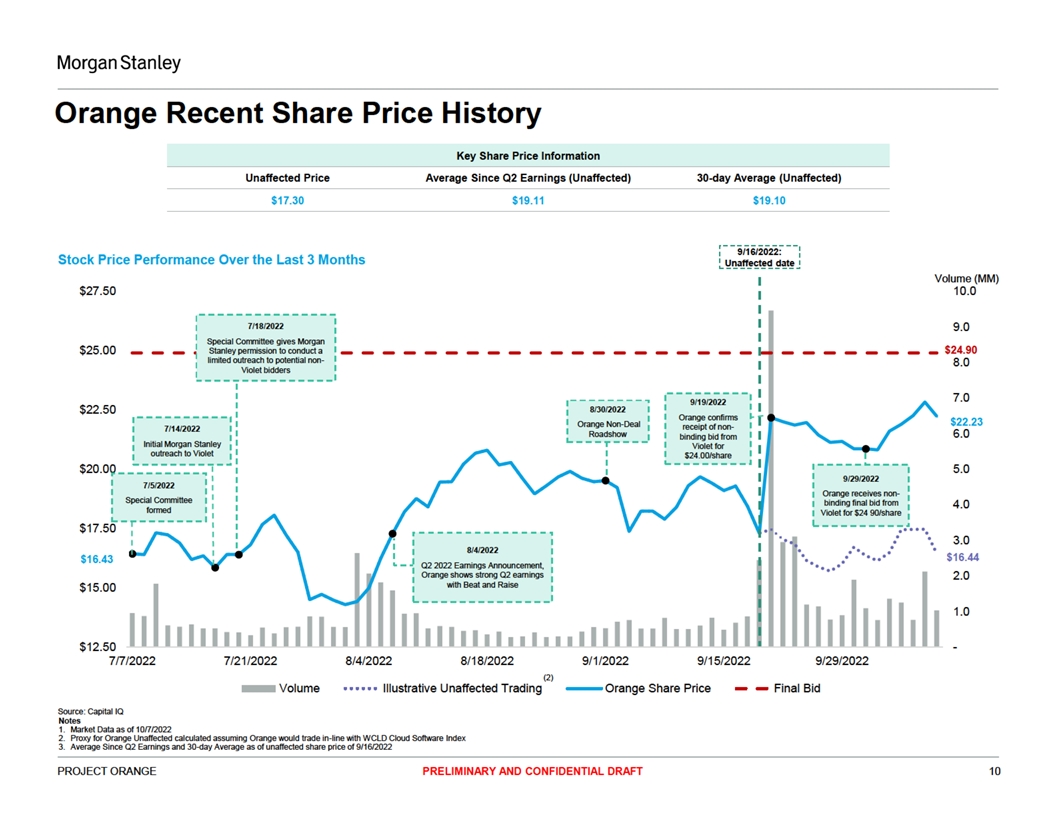

Executive Summary • The Special Committee and, at the Special Committee’s direction, the Company and the Special Committee’s advisors have engaged with “Violet” in response to Violet’s inbound interest and proposal –Following inbound interest from Violet, the Board formed the Special Committee and engaged Morgan Stanley and Potter, Anderson & Corroon LLP as advisors to assist with its evaluation of a potential transaction with Violet and other potential bidders • After negotiations, both sides have indicated interest in moving forward with a transaction at $24.90 per share –10.3x AV / CY2023E Revenue Multiple –44% premium to unaffected share price of $17.30 as of 9/16/2022 • Outreach to 4 strategic parties and 12 financial sponsors pre-13D filing by Violet yielded no other bids –Post-13D filing by Violet, Morgan Stanley conducted additional outreach to certain parties from the total pool listed above. There were no expressions of interest from potential buyers that were contacted or any other potential bidders • The Board resolutions forming the Special Committee provided the Special Committee with broad powers to evaluate a transaction with Violet, as well as a transaction with other potentially interested buyers. The Board resolutions also provided the Special Committee with the “power to say no” and maintain the status quo • The Board resolutions forming the Special Committee indicated that the Company would not effectuate a “Specified Strategic Transaction” if it had not first been –Approved or recommended by the Special Committee, and –Approved by holders of a majority of the voting power of the outstanding shares of the Company held by disinterested stockholders as determined by the Special Committee PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 2

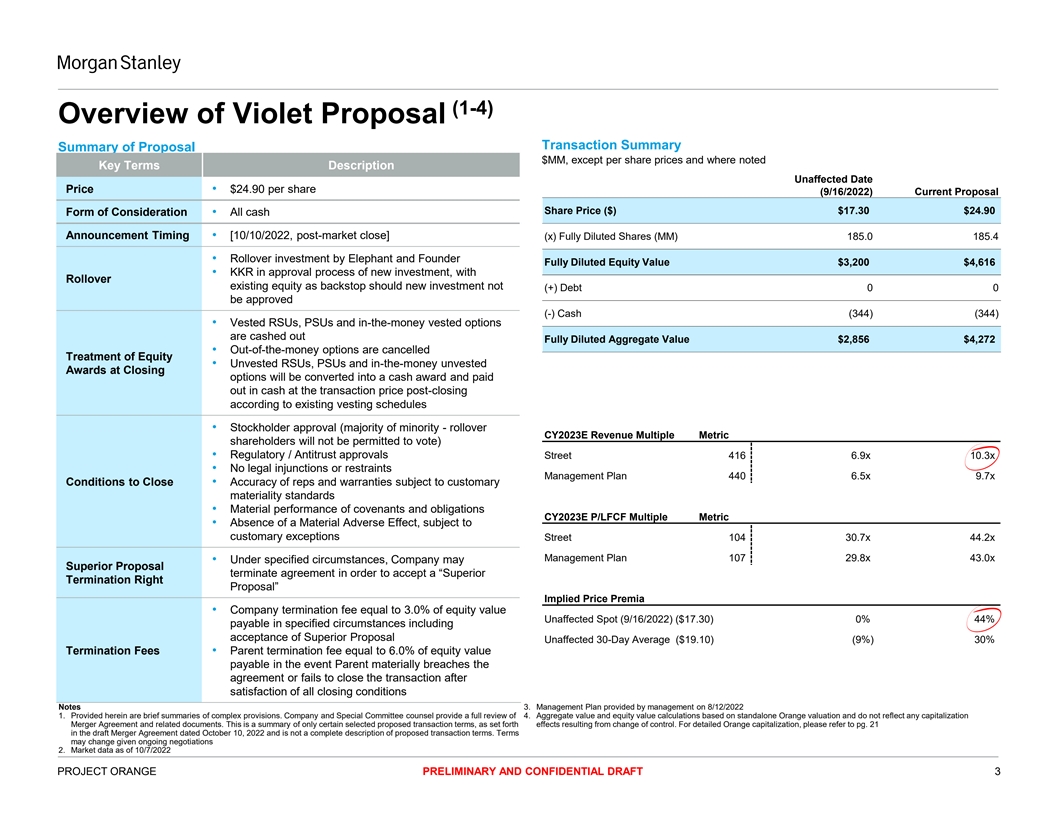

(1-4) Overview of Violet Proposal Transaction Summary Summary of Proposal $MM, except per share prices and where noted Key Terms Description Unaffected Date Price • $24.90 per share (9/16/2022) Current Proposal Share Price ($) $17.30 $24.90 Form of Consideration • All cash Announcement Timing • [10/10/2022, post-market close] (x) Fully Diluted Shares (MM) 185.0 185.4 • Rollover investment by Elephant and Founder Fully Diluted Equity Value $3,200 $4,616 • KKR in approval process of new investment, with Rollover existing equity as backstop should new investment not (+) Debt 0 0 be approved (-) Cash (344) (344) • Vested RSUs, PSUs and in-the-money vested options are cashed out Fully Diluted Aggregate Value $2,856 $4,272 • Out-of-the-money options are cancelled Treatment of Equity • Unvested RSUs, PSUs and in-the-money unvested Awards at Closing options will be converted into a cash award and paid out in cash at the transaction price post-closing according to existing vesting schedules • Stockholder approval (majority of minority - rollover CY2023E Revenue Multiple Metric shareholders will not be permitted to vote) • Regulatory / Antitrust approvals Street 416 6.9x 10.3x • No legal injunctions or restraints Management Plan 440 6.5x 9.7x Conditions to Close • Accuracy of reps and warranties subject to customary materiality standards • Material performance of covenants and obligations CY2023E P/LFCF Multiple Metric • Absence of a Material Adverse Effect, subject to customary exceptions Street 104 30.7x 44.2x Management Plan 107 29.8x 43.0x • Under specified circumstances, Company may Superior Proposal terminate agreement in order to accept a “Superior Termination Right Proposal” Implied Price Premia • Company termination fee equal to 3.0% of equity value Unaffected Spot (9/16/2022) ($17.30) 0% 44% payable in specified circumstances including acceptance of Superior Proposal Unaffected 30-Day Average ($19.10) (9%) 30% Termination Fees • Parent termination fee equal to 6.0% of equity value payable in the event Parent materially breaches the agreement or fails to close the transaction after satisfaction of all closing conditions Notes 3. Management Plan provided by management on 8/12/2022 1. Provided herein are brief summaries of complex provisions. Company and Special Committee counsel provide a full review of 4. Aggregate value and equity value calculations based on standalone Orange valuation and do not reflect any capitalization Merger Agreement and related documents. This is a summary of only certain selected proposed transaction terms, as set forth effects resulting from change of control. For detailed Orange capitalization, please refer to pg. 21 in the draft Merger Agreement dated October 10, 2022 and is not a complete description of proposed transaction terms. Terms may change given ongoing negotiations 2. Market data as of 10/7/2022 PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 3

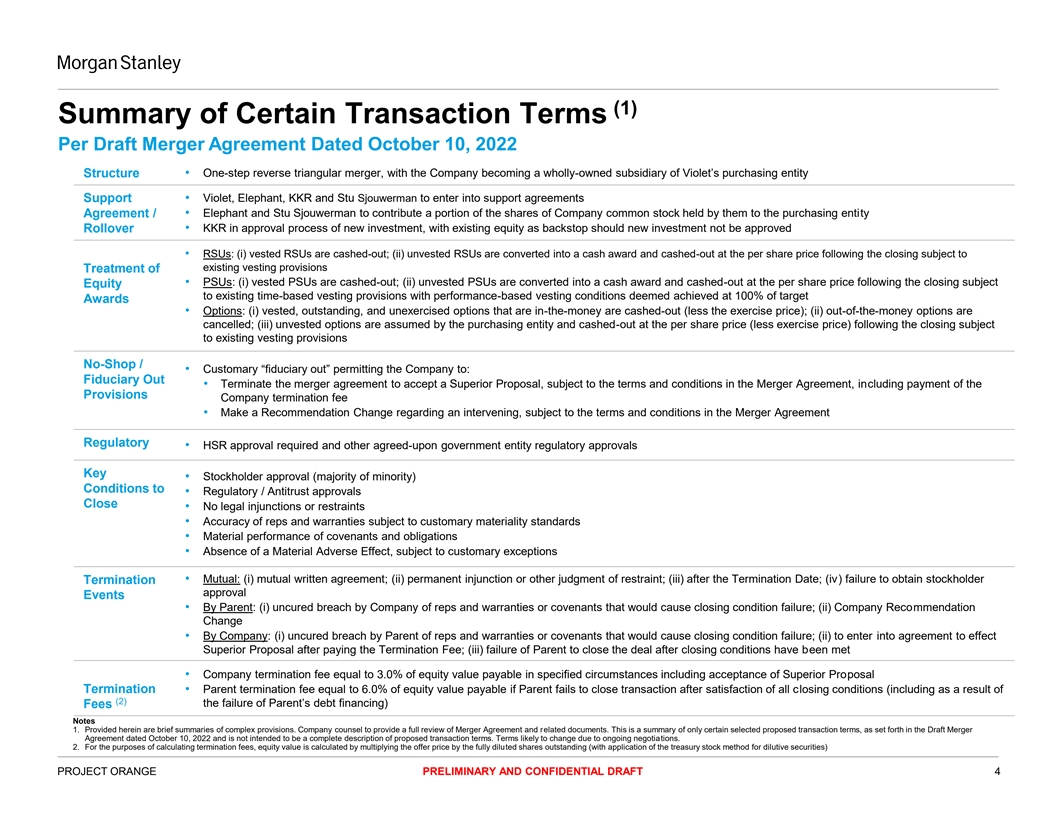

(1) Summary of Certain Transaction Terms Per Draft Merger Agreement Dated October 10, 2022 Structure • One-step reverse triangular merger, with the Company becoming a wholly-owned subsidiary of Violet’s purchasing entity Support • Violet, Elephant, KKR and Stu Sjouwerman to enter into support agreements Agreement / • Elephant and Stu Sjouwerman to contribute a portion of the shares of Company common stock held by them to the purchasing entity • KKR in approval process of new investment, with existing equity as backstop should new investment not be approved Rollover • RSUs: (i) vested RSUs are cashed-out; (ii) unvested RSUs are converted into a cash award and cashed-out at the per share price following the closing subject to existing vesting provisions Treatment of • PSUs: (i) vested PSUs are cashed-out; (ii) unvested PSUs are converted into a cash award and cashed-out at the per share price following the closing subject Equity to existing time-based vesting provisions with performance-based vesting conditions deemed achieved at 100% of target Awards • Options: (i) vested, outstanding, and unexercised options that are in-the-money are cashed-out (less the exercise price); (ii) out-of-the-money options are cancelled; (iii) unvested options are assumed by the purchasing entity and cashed-out at the per share price (less exercise price) following the closing subject to existing vesting provisions No-Shop / • Customary “fiduciary out” permitting the Company to: Fiduciary Out • Terminate the merger agreement to accept a Superior Proposal, subject to the terms and conditions in the Merger Agreement, including payment of the Provisions Company termination fee • Make a Recommendation Change regarding an intervening, subject to the terms and conditions in the Merger Agreement Regulatory • HSR approval required and other agreed-upon government entity regulatory approvals Key • Stockholder approval (majority of minority) Conditions to • Regulatory / Antitrust approvals Close • No legal injunctions or restraints • Accuracy of reps and warranties subject to customary materiality standards • Material performance of covenants and obligations • Absence of a Material Adverse Effect, subject to customary exceptions • Mutual: (i) mutual written agreement; (ii) permanent injunction or other judgment of restraint; (iii) after the Termination Date; (iv) failure to obtain stockholder Termination approval Events • By Parent: (i) uncured breach by Company of reps and warranties or covenants that would cause closing condition failure; (ii) Company Recommendation Change • By Company: (i) uncured breach by Parent of reps and warranties or covenants that would cause closing condition failure; (ii) to enter into agreement to effect Superior Proposal after paying the Termination Fee; (iii) failure of Parent to close the deal after closing conditions have been met • Company termination fee equal to 3.0% of equity value payable in specified circumstances including acceptance of Superior Proposal Termination • Parent termination fee equal to 6.0% of equity value payable if Parent fails to close transaction after satisfaction of all closing conditions (including as a result of (2) the failure of Parent’s debt financing) Fees Notes 1. Provided herein are brief summaries of complex provisions. Company counsel to provide a full review of Merger Agreement and related documents. This is a summary of only certain selected proposed transaction terms, as set forth in the Draft Merger Agreement dated October 10, 2022 and is not intended to be a complete description of proposed transaction terms. Terms likely to change due to ongoing negotiations. 2. For the purposes of calculating termination fees, equity value is calculated by multiplying the offer price by the fully diluted shares outstanding (with application of the treasury stock method for dilutive securities) PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 4

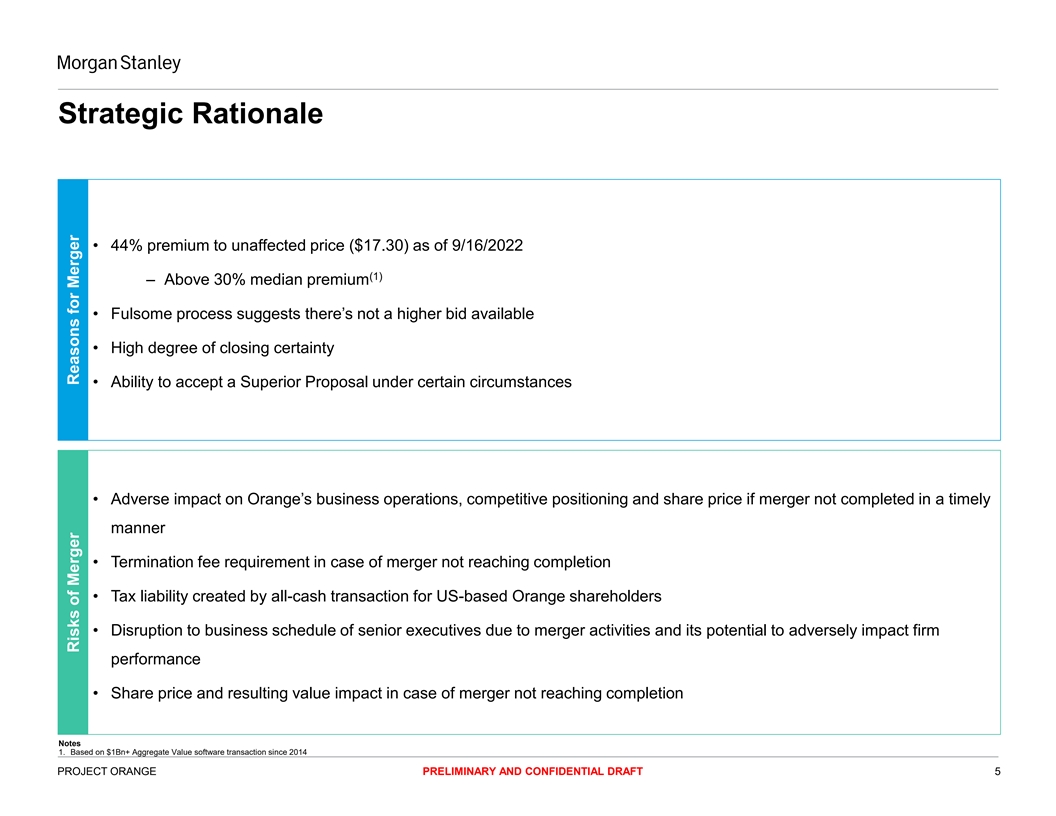

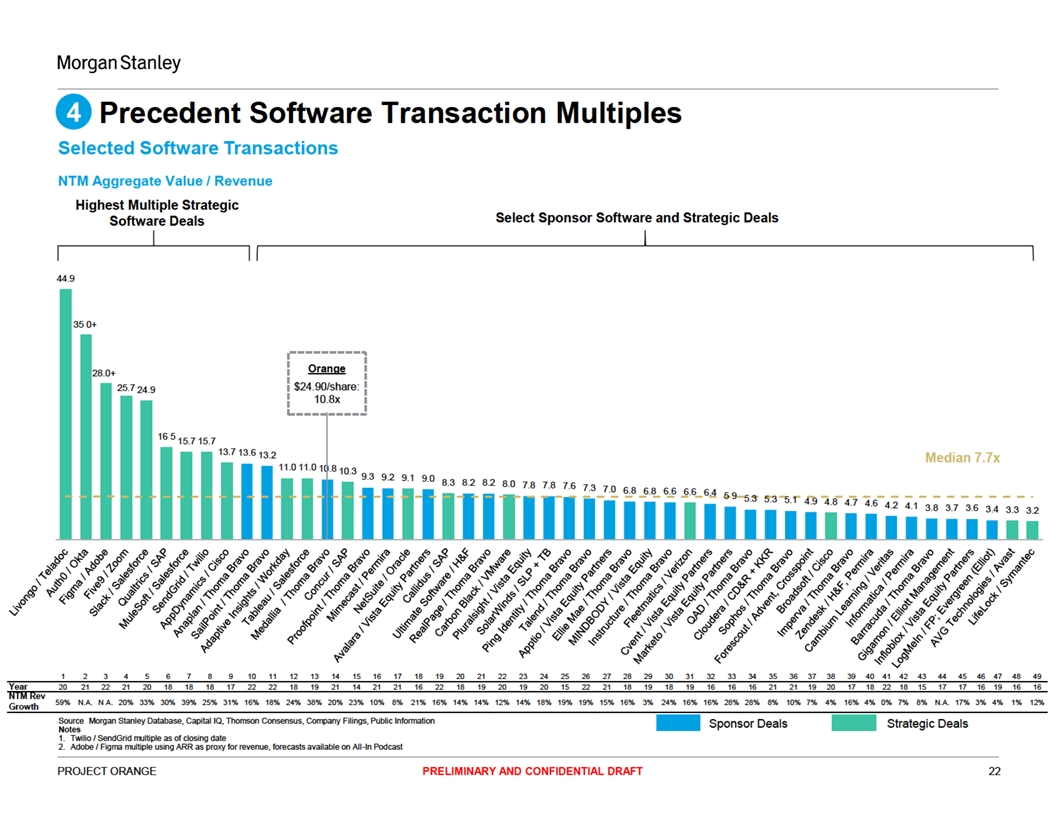

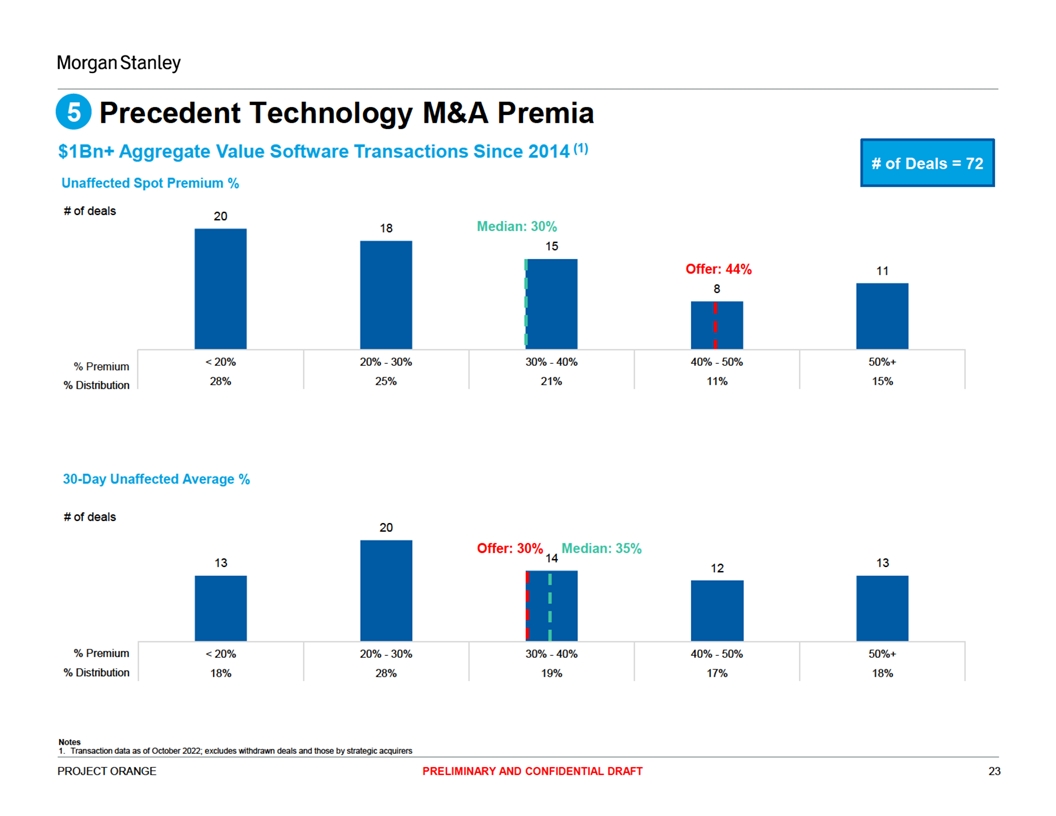

Strategic Rationale • 44% premium to unaffected price ($17.30) as of 9/16/2022 (1) ‒ Above 30% median premium • Fulsome process suggests there’s not a higher bid available • High degree of closing certainty • Ability to accept a Superior Proposal under certain circumstances • Adverse impact on Orange’s business operations, competitive positioning and share price if merger not completed in a timely manner • Termination fee requirement in case of merger not reaching completion • Tax liability created by all-cash transaction for US-based Orange shareholders • Disruption to business schedule of senior executives due to merger activities and its potential to adversely impact firm performance • Share price and resulting value impact in case of merger not reaching completion Notes 1. Based on $1Bn+ Aggregate Value software transaction since 2014 PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 5 Risks of Merger Reasons for Merger

Shareholder Voting Analysis (Majority of the Disinterested Parties) • Assumes current Class A and Class B Top 10 Aggregate Voting Power Shareholders (Non-Board Members / Insiders) shareholders hold their shares through Class B Total (A+B) Class A (1) to the shareholder vote Class A Shares Class B Shares Aggregate Voting Aggregate Voting Economic Economic Shareholder Voting Power Held Held Power Power % Ownership Ownership % Kevin Mitnick 2.5 4.9 49.0 51.5 31% 7.4 4% Legacy Marlin Holdings - 1.2 12.5 12.5 7% 1.2 1% • Assumes rollover / new investment RadWit Inc - 1.2 11.9 11.9 7% 1.2 1% Sanabil Private Equity Investments Company - 0.8 8.3 8.3 5% 0.8 0% current shareholders are prohibited Voya Financial, Inc. 5.7 - - 5.7 3% 5.7 3% from voting (i.e. Vista, KKR, Elephant, Invesco Ltd. 4.9 - - 4.9 3% 4.9 3% FMR LLC 4.9 - - 4.9 3% 4.9 3% Stu Sjouwerman) BlackRock Institutional Trust Company NA 4.7 - - 4.7 3% 4.7 3% Eventide Asset Management, LLC 4.2 - - 4.2 3% 4.2 2% The Vanguard Group 3.4 - - 3.4 2% 3.4 2% Other Common Shareholders Excl. Affiliated 53.4 0.2 1.7 55.0 33% 147.0 79% • Assumes no RSU or Option holders Totals 83.6 8.3 83.3 166.9 100% 185.4 100% exercise and convert into Class A or B Board Member / Insider Assumed Voting Power shares and vote Class A Class B Total (A+B) Potential Potential (2) (1) Class A Shares Outstanding Vested Options Economic Economic Shareholder Aggregate Voting Aggregate Voting Convertible Into Shares of Class B Held and RSU Ownership Ownership % Power Power % Krish Venkataraman 0.2 - 0.2 0% 0.2 0% Lars Letonoff 0.8 - 0.8 1% 0.8 0% Kevin Klausmeyer - - 0.0 0% 0.0 0% Gerhard Watzinger - 0.7 7.0 4% 0.7 0% Kara Wilson - 0.7 7.0 4% 0.7 0% 1.4 Total Additional Votes 0.8 15.0 9% 2.4 1% Current Shareholders Assumed Conflicted For the Vote Class A Class B Total (A+B) (1) Class A Shares Class B Shares Aggregate Voting Aggregate Voting Economic Economic Shareholder Voting Power Held Held Power Power % Ownership Ownership % Emerald - 37.1 37.1 20% Khaki - 26.1 26.1 14% Violet 1.9 14.6 16.4 9% Stu Sjouwerman 0.1 4.4 4.5 2% Totals 2.0 82.1 84.1 45% Notes 1. Economic ownership calculated off of fully diluted share count of 185.4M inclusive of affiliated shares 2. Assumes Total Potential Diluted Aggregate Voting Power of 166 9MM votes 7

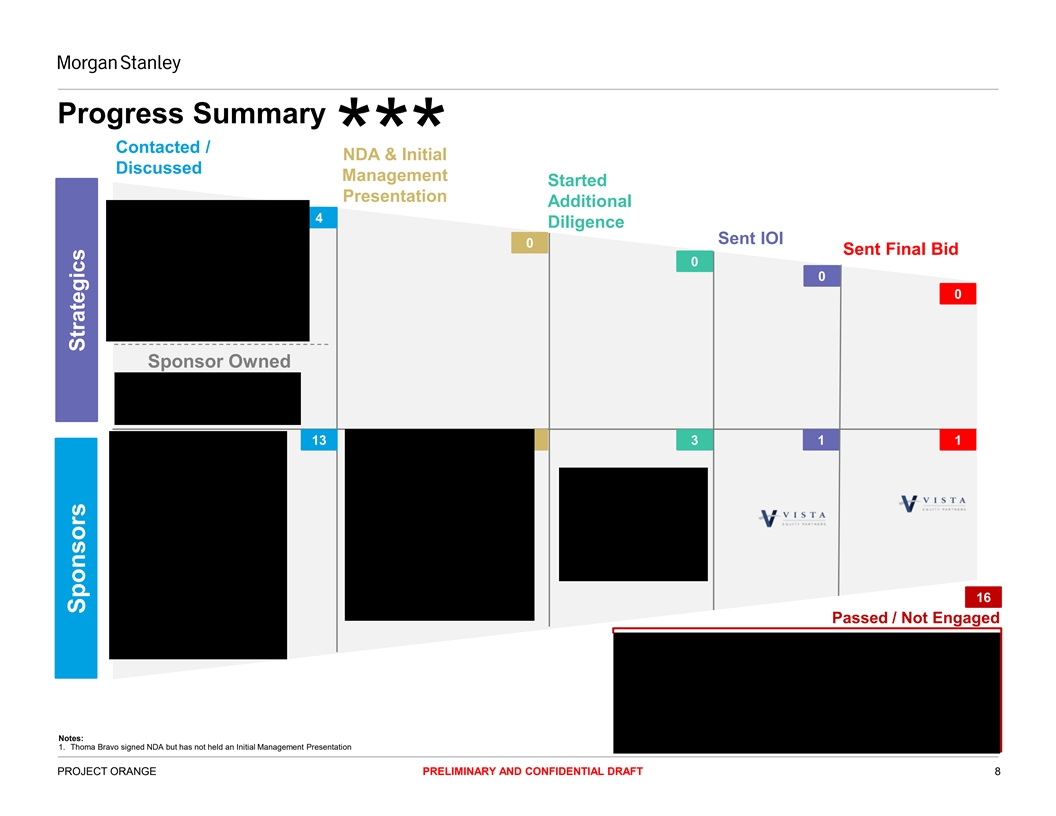

Progress Summary Contacted / NDA & Initial *** Discussed Management Started Presentation Additional 4 Diligence Sent IOI 0 Sent Final Bid 0 0 0 Sponsor Owned 13 3 1 1 16 Passed / Not Engaged Notes: 1. Thoma Bravo signed NDA but has not held an Initial Management Presentation PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 8 Sponsors Strategics

***

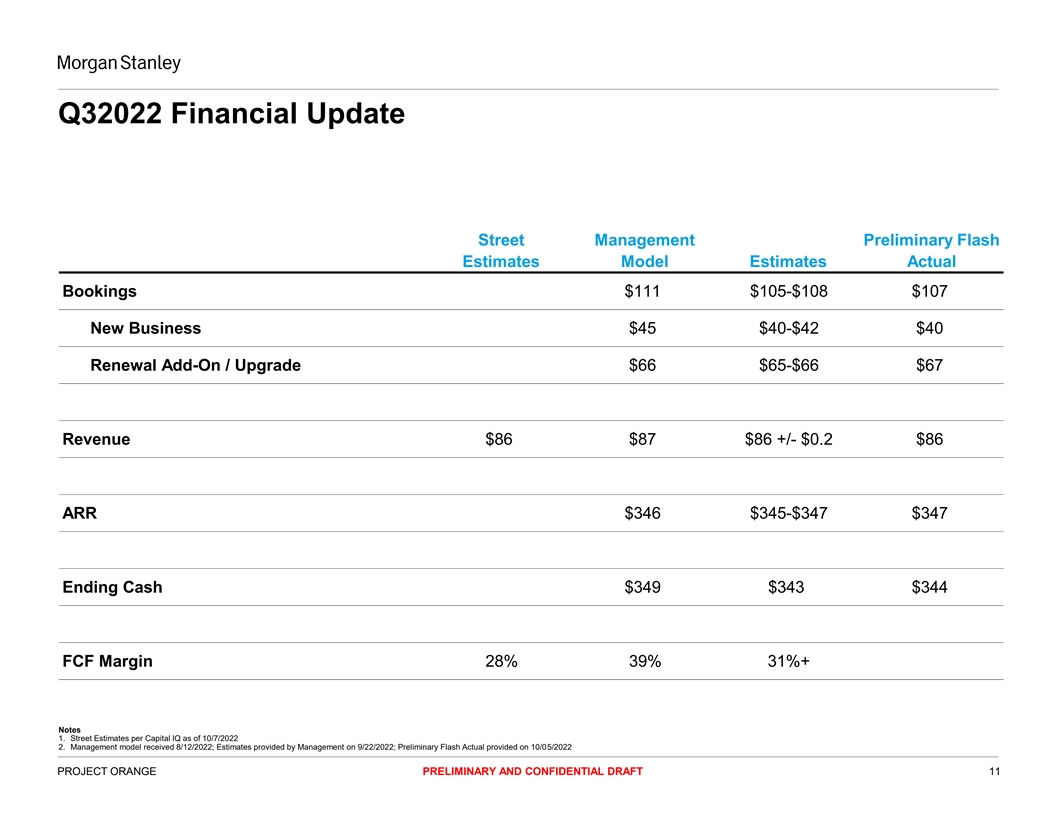

Q32022 Financial Update Street Management Preliminary Flash Estimates Model Estimates Actual Bookings $111 $105-$108 $107 New Business $45 $40-$42 $40 Renewal Add-On / Upgrade $66 $65-$66 $67 Revenue $86 $87 $86 +/- $0.2 $86 ARR $346 $345-$347 $347 Ending Cash $349 $343 $344 FCF Margin 28% 39% 31%+ Notes 1. Street Estimates per Capital IQ as of 10/7/2022 2. Management model received 8/12/2022; Estimates provided by Management on 9/22/2022; Preliminary Flash Actual provided on 10/05/2022 PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 11

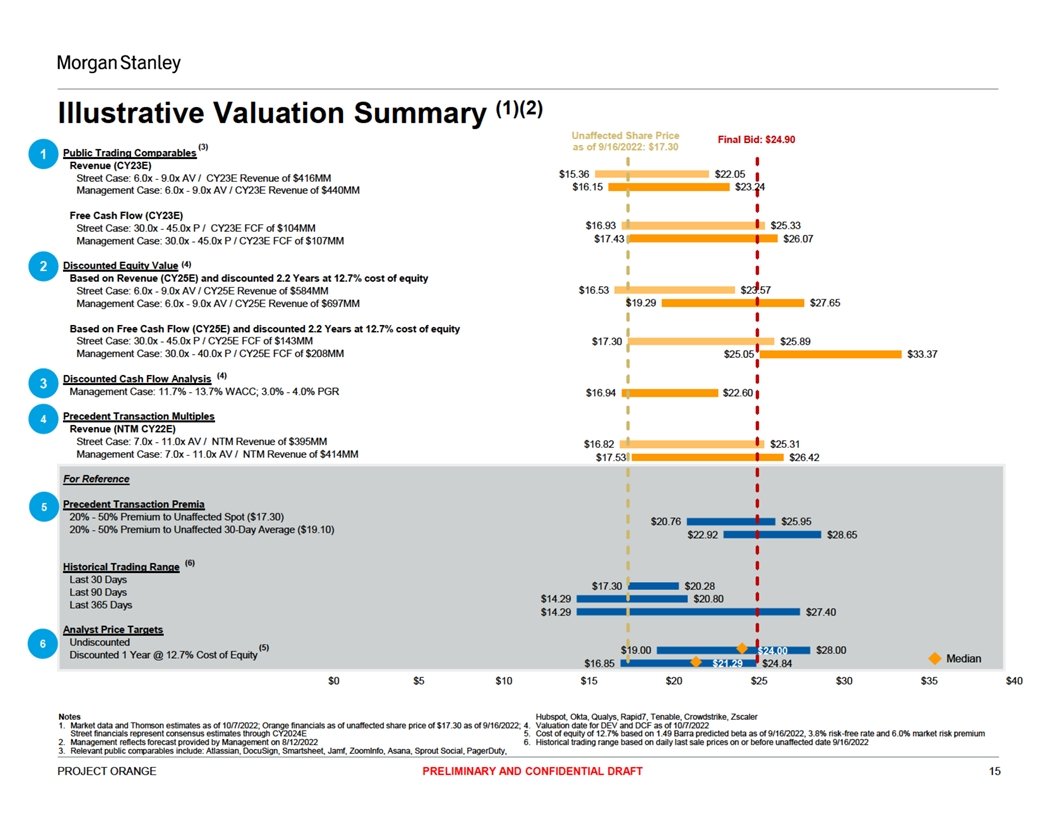

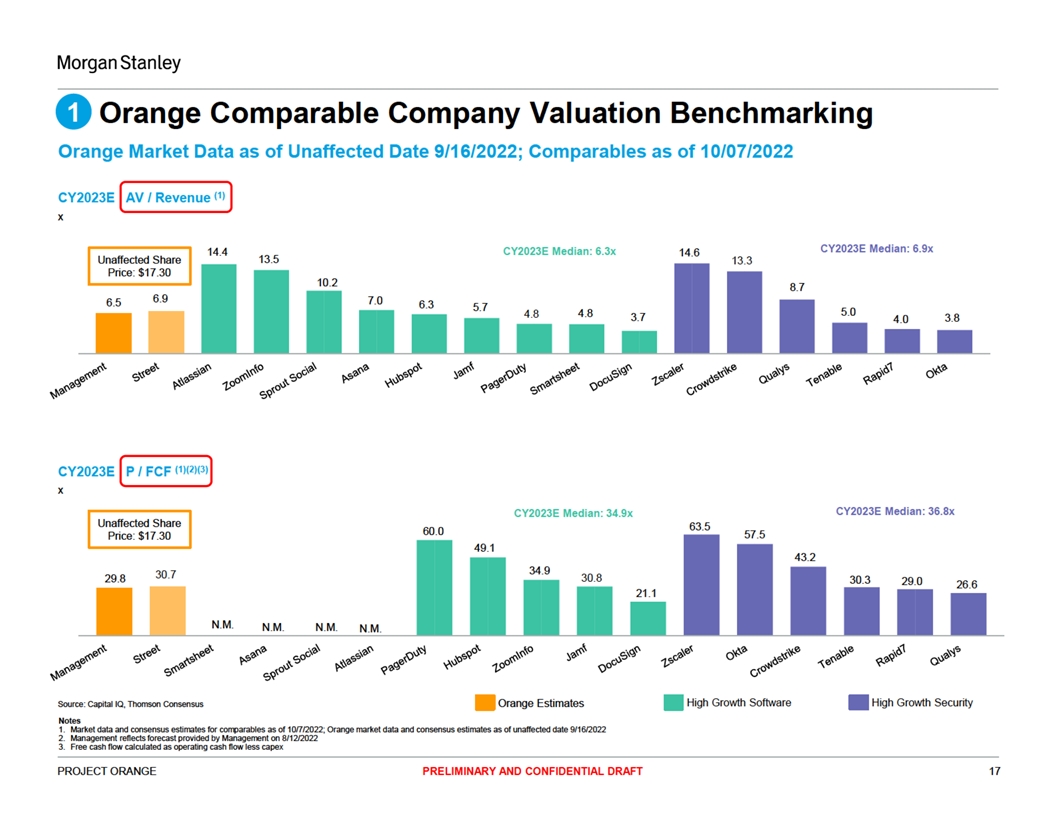

Illustrative Valuation Matrix $MM other than per share data, unless otherwise noted Management Case Street Case Premium / (Discount) To AV / Revenue P / FCF AV / Revenue P / FCF Fully Diluted Agg. Value Price Unaffected 30-Day Avg. 52 Wk. High EV CY2022E CY2023E CY2022E CY2023E CY2022E CY2023E CY2022E CY2023E Metric $17.30 $19.10 $27.40 $3,200 $2,856 $334 $416 $80 $104 $336 $440 $92 $107 Growth Rate / Margin 36% 25% 24% 25% 36% 31% 28% 24% $17.30 0% (9%) (37%) $3,200 $2,856 8.6x 6.9x 40x 31x 8.5x 6.5x 35x 30x Unaffected $22.00 27% 15% (20%) $4,076 $3,732 11.2x 9.0x 51x 39x 11.1x 8.5x 44x 38x $23.00 33% 20% (16%) $4,262 $3,918 11.7x 9.4x 53x 41x 11.7x 8.9x 46x 40x Violet IOI $24.00 39% 26% (12%) $4,449 $4,105 12.3x 9.9x 56x 43x 12.2x 9.3x 48x 41x $24.25 40% 27% (11%) $4,495 $4,151 12.4x 10.0x 56x 43x 12.4x 9.4x 49x 42x $24.50 42% 28% (11%) $4,542 $4,198 12.6x 10.1x 57x 44x 12.5x 9.5x 49x 42x Violet $24.60 42% 29% (10%) $4,561 $4,217 12.6x 10.1x 57x 44x 12.6x 9.6x 49x 42x Revised IOI 1 Violet $24.80 43% 30% (9%) $4,598 $4,254 12.7x 10.2x 58x 44x 12.7x 9.7x 50x 43x Revised IOI 2 Current $24.90 44% 30% (9%) $4,616 $4,272 12.8x 10.3x 58x 44x 12.7x 9.7x 50x 43x Proposal $25.00 45% 31% (9%) $4,635 $4,291 12.9x 10.3x 58x 44x 12.8x 9.7x 50x 43x Orange Counter $25.75 49% 35% (6%) $4,775 $4,431 13.3x 10.7x 60x 46x 13.2x 10.1x 52x 44x Proposal 2 $26.00 50% 36% (5%) $4,821 $4,477 13.4x 10.8x 60x 46x 13.3x 10.2x 52x 45x Orange Counter $26.50 53% 39% (3%) $4,915 $4,571 13.7x 11.0x 62x 47x 13.6x 10.4x 53x 46x Proposal 1 Source: CapIQ, Thomson Consensus Notes 1. Market data and consensus estimates as of unaffected share price date 9/16/2022 2. FCF defined as operating cash flow less capital expenditures PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 12

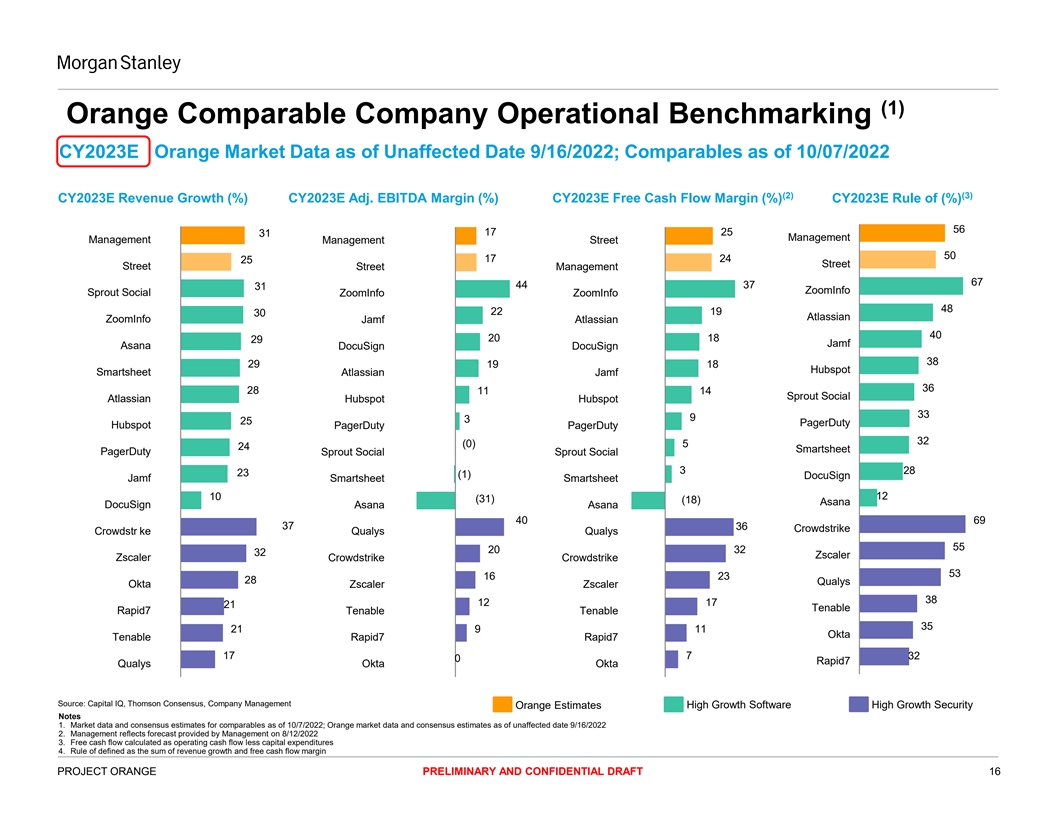

(1) Orange Comparable Company Operational Benchmarking CY2023E Orange Market Data as of Unaffected Date 9/16/2022; Comparables as of 10/07/2022 (2) (3) CY2023E Revenue Growth (%) CY2023E Adj. EBITDA Margin (%) CY2023E Free Cash Flow Margin (%) CY2023E Rule of (%) 56 17 25 31 Management Management Management Street 50 17 24 25 Street Street Street Management 67 44 37 31 ZoomInfo Sprout Social ZoomInfo ZoomInfo 48 22 19 30 Atlassian ZoomInfo Jamf Atlassian 40 20 18 29 Jamf Asana DocuSign DocuSign 38 29 19 18 Hubspot Smartsheet Atlassian Jamf 36 28 11 14 Sprout Social Atlassian Hubspot Hubspot 33 9 3 25 PagerDuty Hubspot PagerDuty PagerDuty 32 (0) 5 24 Smartsheet PagerDuty Sprout Social Sprout Social 3 28 23 (1) DocuSign Jamf Smartsheet Smartsheet 10 12 (31) (18) Asana DocuSign Asana Asana 40 69 37 36 Crowdstrike Crowdstr ke Qualys Qualys 55 20 32 32 Zscaler Zscaler Crowdstrike Crowdstrike 53 16 23 28 Qualys Okta Zscaler Zscaler 38 12 17 21 Tenable Rapid7 Tenable Tenable 35 21 9 11 Okta Tenable Rapid7 Rapid7 17 7 32 0 Rapid7 Qualys Okta Okta Source: Capital IQ, Thomson Consensus, Company Management Orange Estimates High Growth Software High Growth Security Notes 1. Market data and consensus estimates for comparables as of 10/7/2022; Orange market data and consensus estimates as of unaffected date 9/16/2022 2. Management reflects forecast provided by Management on 8/12/2022 3. Free cash flow calculated as operating cash flow less capital expenditures 4. Rule of defined as the sum of revenue growth and free cash flow margin PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 16

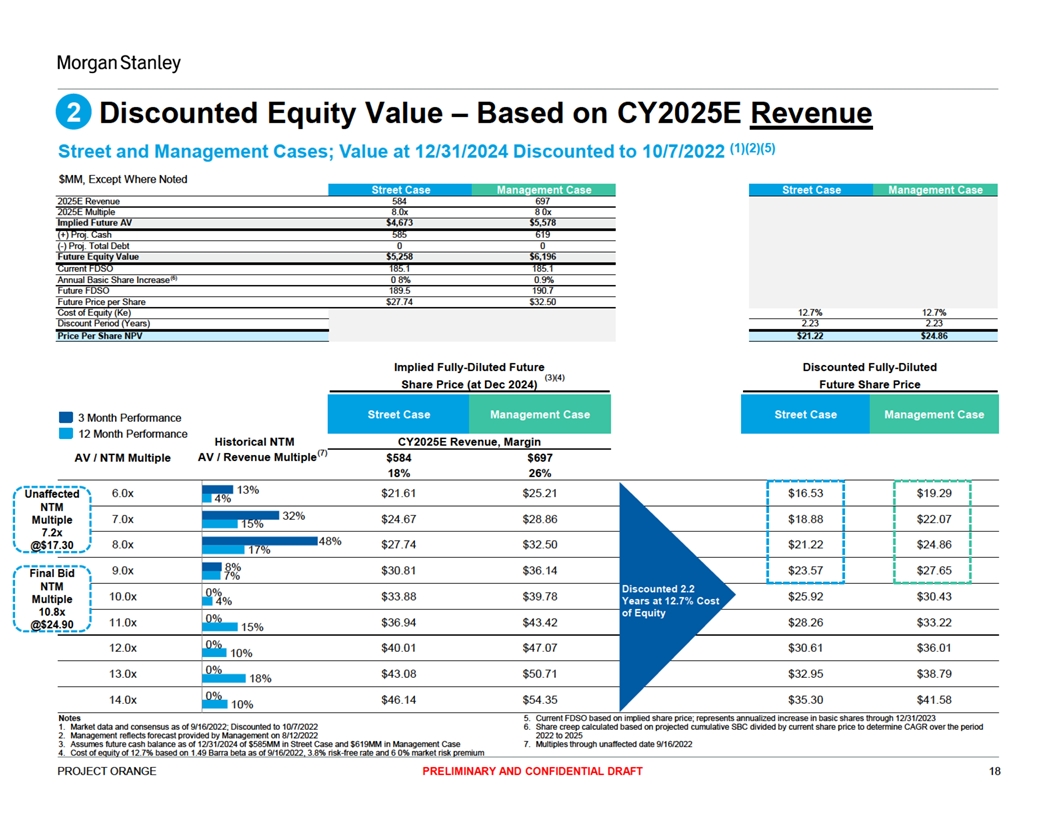

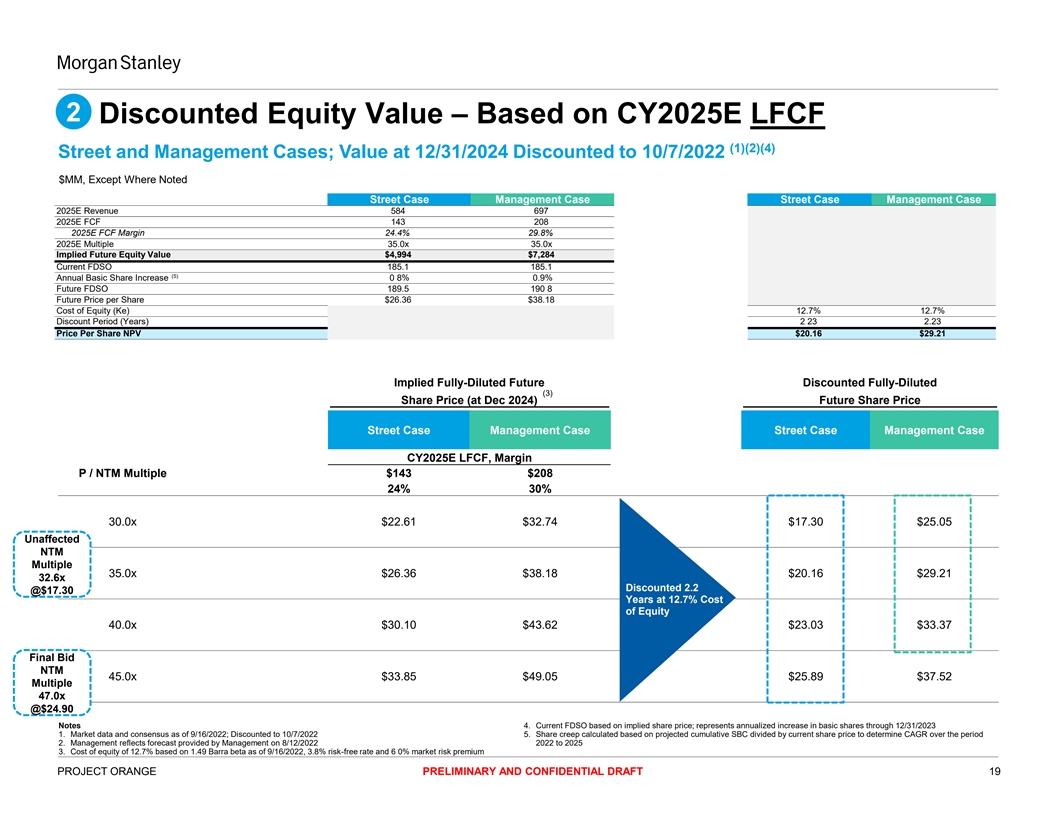

2 Discounted Equity Value – Based on CY2025E LFCF (1)(2)(4) Street and Management Cases; Value at 12/31/2024 Discounted to 10/7/2022 $MM, Except Where Noted Street Case Management Case Street Case Management Case 2025E Revenue 584 697 2025E FCF 143 208 2025E FCF Margin 24.4% 29.8% 2025E Multiple 35.0x 35.0x Implied Future Equity Value $4,994 $7,284 Current FDSO 185.1 185.1 (5) Annual Basic Share Increase 0 8% 0.9% Future FDSO 189.5 190 8 Future Price per Share $26.36 $38.18 Cost of Equity (Ke) 12.7% 12.7% Discount Period (Years) 2 23 2.23 Price Per Share NPV $20.16 $29.21 Implied Fully-Diluted Future Discounted Fully-Diluted (3) Share Price (at Dec 2024) Future Share Price Street Case Management Case Street Case Management Case CY2025E LFCF, Margin P / NTM Multiple $143 $208 24% 30% 30.0x $22.61 $32.74 $17.30 $25.05 Unaffected NTM Multiple 35.0x $26.36 $38.18 $20.16 $29.21 32.6x Discounted 2.2 @$17.30 Years at 12.7% Cost of Equity 40.0x $30.10 $43.62 $23.03 $33.37 Final Bid NTM 45.0x $33.85 $49.05 $25.89 $37.52 Multiple 47.0x @$24.90 Notes 4. Current FDSO based on implied share price; represents annualized increase in basic shares through 12/31/2023 1. Market data and consensus as of 9/16/2022; Discounted to 10/7/2022 5. Share creep calculated based on projected cumulative SBC divided by current share price to determine CAGR over the period 2. Management reflects forecast provided by Management on 8/12/2022 2022 to 2025 3. Cost of equity of 12.7% based on 1.49 Barra beta as of 9/16/2022, 3.8% risk-free rate and 6 0% market risk premium PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 19

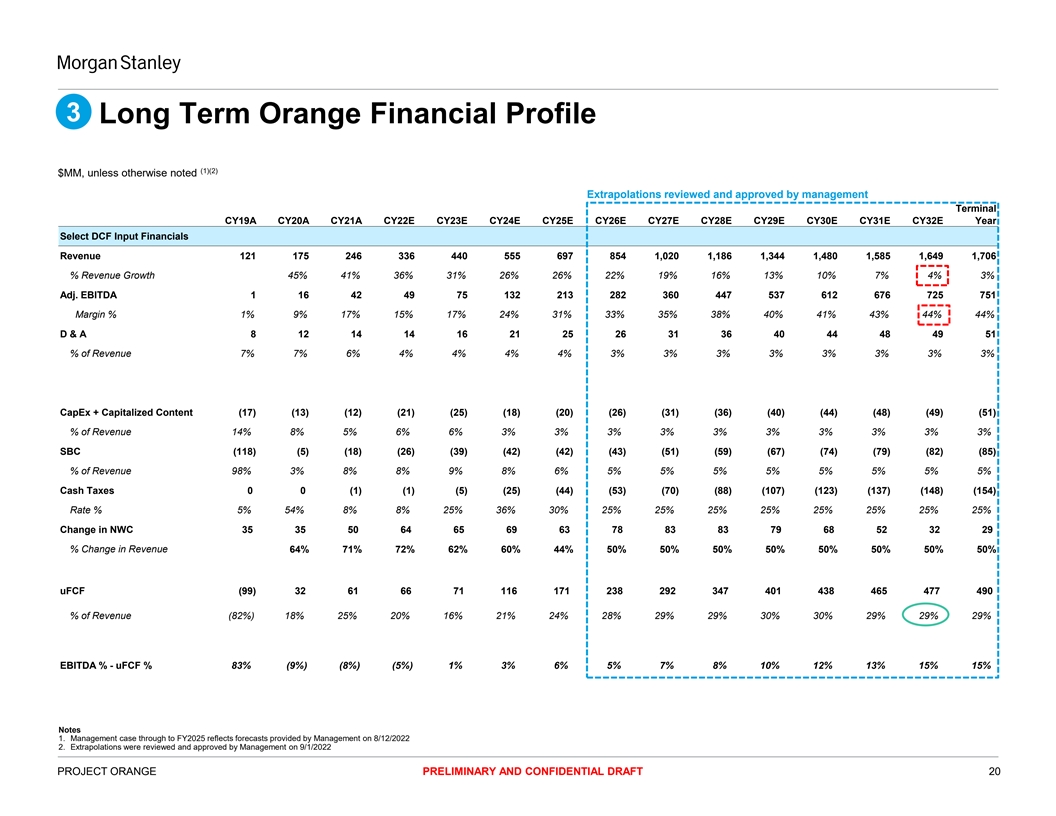

3 Long Term Orange Financial Profile (1)(2) $MM, unless otherwise noted Extrapolations reviewed and approved by management Terminal CY19A CY20A CY21A CY22E CY23E CY24E CY25E CY26E CY27E CY28E CY29E CY30E CY31E CY32E Year Select DCF Input Financials Revenue 121 175 246 336 440 555 697 854 1,020 1,186 1,344 1,480 1,585 1,649 1,706 % Revenue Growth 45% 41% 36% 31% 26% 26% 22% 19% 16% 13% 10% 7% 4% 3% Adj. EBITDA 1 16 42 49 75 132 213 282 360 447 537 612 676 725 751 Margin % 1% 9% 17% 15% 17% 24% 31% 33% 35% 38% 40% 41% 43% 44% 44% D & A 8 12 14 14 16 21 25 26 31 36 40 44 48 49 51 % of Revenue 7% 7% 6% 4% 4% 4% 4% 3% 3% 3% 3% 3% 3% 3% 3% CapEx + Capitalized Content (17) (13) (12) (21) (25) (18) (20) (26) (31) (36) (40) (44) (48) (49) (51) % of Revenue 14% 8% 5% 6% 6% 3% 3% 3% 3% 3% 3% 3% 3% 3% 3% SBC (118) (5) (18) (26) (39) (42) (42) (43) (51) (59) (67) (74) (79) (82) (85) % of Revenue 98% 3% 8% 8% 9% 8% 6% 5% 5% 5% 5% 5% 5% 5% 5% Cash Taxes 0 0 (1) (1) (5) (25) (44) (53) (70) (88) (107) (123) (137) (148) (154) Rate % 5% 54% 8% 8% 25% 36% 30% 25% 25% 25% 25% 25% 25% 25% 25% Change in NWC 35 35 50 64 65 69 63 78 83 83 79 68 52 32 29 % Change in Revenue 64% 71% 72% 62% 60% 44% 50% 50% 50% 50% 50% 50% 50% 50% uFCF (99) 32 61 66 71 116 171 238 292 347 401 438 465 477 490 % of Revenue (82%) 18% 25% 20% 16% 21% 24% 28% 29% 29% 30% 30% 29% 29% 29% EBITDA % - uFCF % 83% (9%) (8%) (5%) 1% 3% 6% 5% 7% 8% 10% 12% 13% 15% 15% Notes 1. Management case through to FY2025 reflects forecasts provided by Management on 8/12/2022 2. Extrapolations were reviewed and approved by Management on 9/1/2022 PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 20

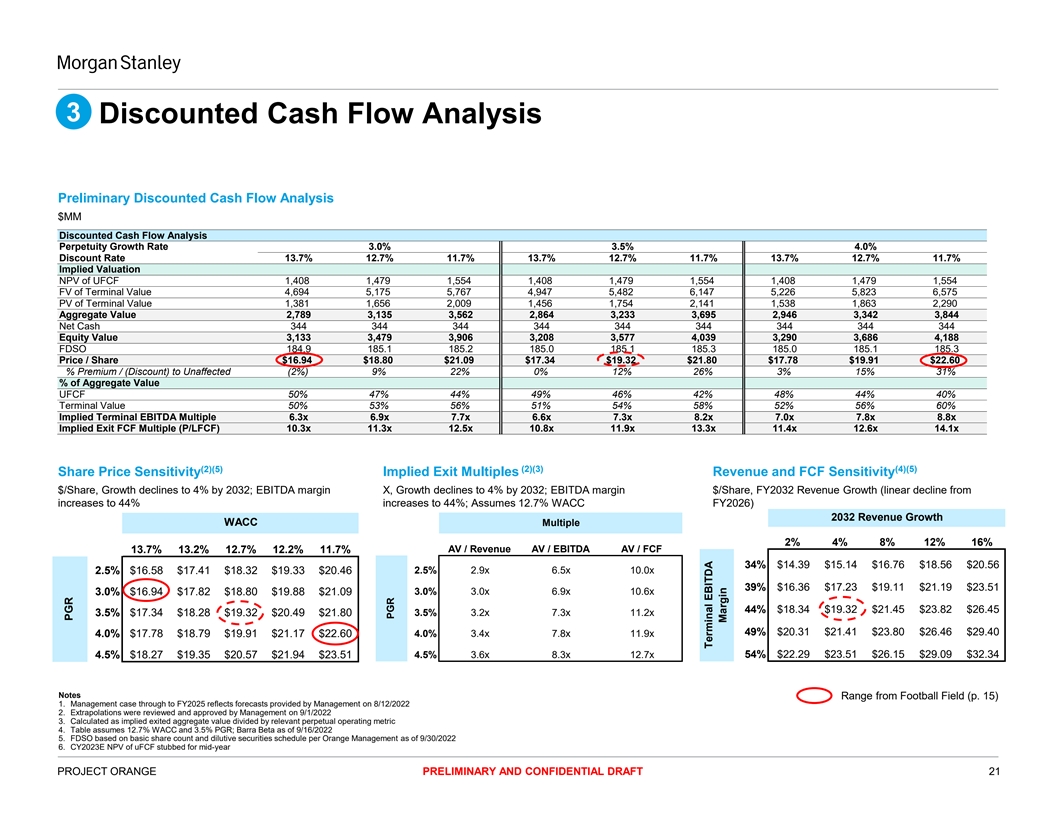

3 Discounted Cash Flow Analysis Preliminary Discounted Cash Flow Analysis $MM Discounted Cash Flow Analysis Perpetuity Growth Rate 3.0% 3.5% 4.0% Discount Rate 13.7% 12.7% 11.7% 13.7% 12.7% 11.7% 13.7% 12.7% 11.7% Implied Valuation NPV of UFCF 1,408 1,479 1,554 1,408 1,479 1,554 1,408 1,479 1,554 FV of Terminal Value 4,694 5,175 5,767 4,947 5,482 6,147 5,226 5,823 6,575 PV of Terminal Value 1,381 1,656 2,009 1,456 1,754 2,141 1,538 1,863 2,290 Aggregate Value 2,789 3,135 3,562 2,864 3,233 3,695 2,946 3,342 3,844 Net Cash 344 344 344 344 344 344 344 344 344 Equity Value 3,133 3,479 3,906 3,208 3,577 4,039 3,290 3,686 4,188 FDSO 184.9 185.1 185.2 185.0 185 1 185.3 185.0 185.1 185.3 Price / Share $16.94 $18.80 $21.09 $17.34 $19.32 $21.80 $17.78 $19.91 $22.60 % Premium / (Discount) to Unaffected (2%) 9% 22% 0% 12% 26% 3% 15% 31% % of Aggregate Value UFCF 50% 47% 44% 49% 46% 42% 48% 44% 40% Terminal Value 50% 53% 56% 51% 54% 58% 52% 56% 60% Implied Terminal EBITDA Multiple 6.3x 6.9x 7.7x 6.6x 7.3x 8.2x 7.0x 7.8x 8.8x Implied Exit FCF Multiple (P/LFCF) 10.3x 11.3x 12.5x 10.8x 11.9x 13.3x 11.4x 12.6x 14.1x (2)(5) (2)(3) (4)(5) Share Price Sensitivity Implied Exit Multiples Revenue and FCF Sensitivity $/Share, Growth declines to 4% by 2032; EBITDA margin X, Growth declines to 4% by 2032; EBITDA margin $/Share, FY2032 Revenue Growth (linear decline from increases to 44% increases to 44%; Assumes 12.7% WACC FY2026) 2032 Revenue Growth WACC Multiple 2% 4% 8% 12% 16% AV / Revenue AV / EBITDA AV / FCF 13.7% 13.2% 12.7% 12.2% 11.7% 34% $14.39 $15.14 $16.76 $18.56 $20.56 2.5% 2.9x 6.5x 10.0x 2.5% $16.58 $17.41 $18.32 $19.33 $20.46 39% $16.36 $17.23 $19.11 $21.19 $23.51 3.0% 3.0x 6.9x 10.6x 3.0% $16.94 $17.82 $18.80 $19.88 $21.09 44% $18.34 $19.32 $21.45 $23.82 $26.45 3.5% $17.34 $18.28 $19.32 $20.49 $21.80 3.5% 3.2x 7.3x 11.2x 49% $20.31 $21.41 $23.80 $26.46 $29.40 4.0% $17.78 $18.79 $19.91 $21.17 $22.60 4.0% 3.4x 7.8x 11.9x 4.5% $18.27 $19.35 $20.57 $21.94 $23.51 4.5% 3.6x 8.3x 12.7x 54% $22.29 $23.51 $26.15 $29.09 $32.34 Notes Range from Football Field (p. 15) 1. Management case through to FY2025 reflects forecasts provided by Management on 8/12/2022 2. Extrapolations were reviewed and approved by Management on 9/1/2022 3. Calculated as implied exited aggregate value divided by relevant perpetual operating metric 4. Table assumes 12.7% WACC and 3.5% PGR; Barra Beta as of 9/16/2022 5. FDSO based on basic share count and dilutive securities schedule per Orange Management as of 9/30/2022 6. CY2023E NPV of uFCF stubbed for mid-year PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 21 PGR PGR Terminal EBITDA Margin

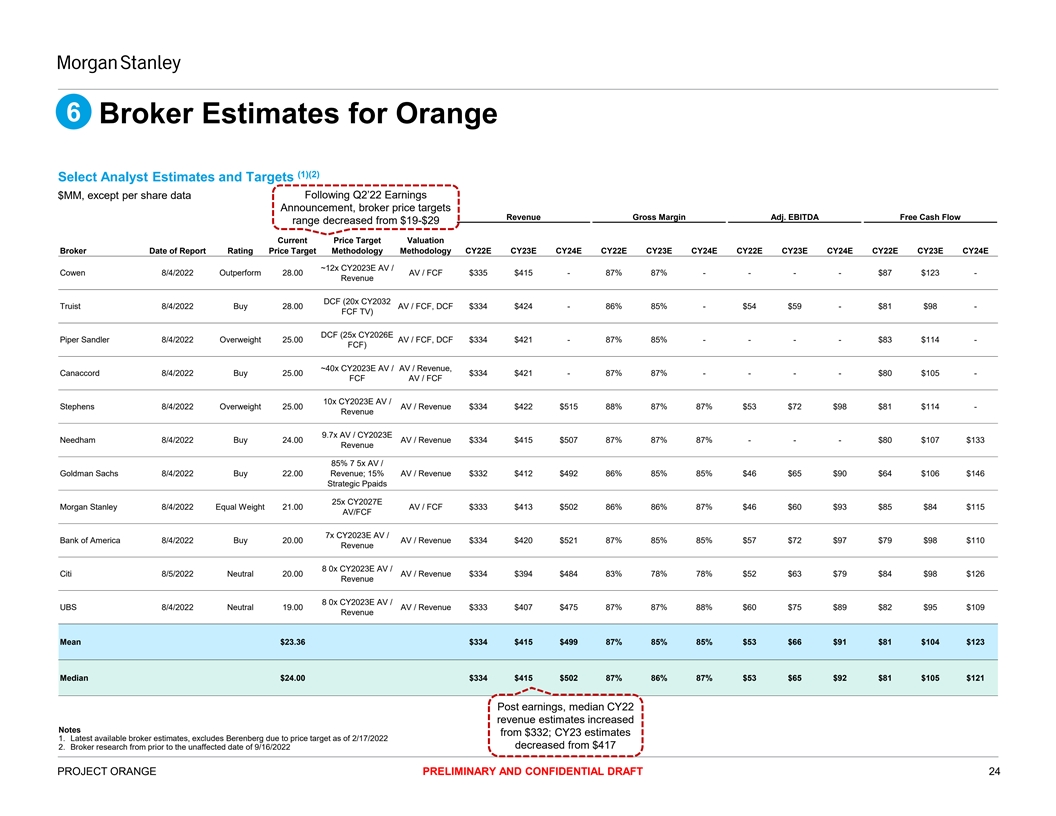

6 Broker Estimates for Orange (1)(2) Select Analyst Estimates and Targets $MM, except per share data Following Q2’22 Earnings Announcement, broker price targets Revenue Gross Margin Adj. EBITDA Free Cash Flow range decreased from $19-$29 Current Price Target Valuation Price Target Methodology Methodology Broker Date of Report Rating CY22E CY23E CY24E CY22E CY23E CY24E CY22E CY23E CY24E CY22E CY23E CY24E ~12x CY2023E AV / Cowen 8/4/2022 Outperform 28.00 AV / FCF $335 $415 - 87% 87% - - - - $87 $123 - Revenue DCF (20x CY2032 Truist 8/4/2022 Buy 28.00 AV / FCF, DCF $334 $424 - 86% 85% - $54 $59 - $81 $98 - FCF TV) DCF (25x CY2026E Piper Sandler 8/4/2022 Overweight 25.00 AV / FCF, DCF $334 $421 - 87% 85% - - - - $83 $114 - FCF) ~40x CY2023E AV / AV / Revenue, Canaccord 8/4/2022 Buy 25.00 $334 $421 - 87% 87% - - - - $80 $105 - FCF AV / FCF 10x CY2023E AV / Stephens 8/4/2022 Overweight 25.00 AV / Revenue $334 $422 $515 88% 87% 87% $53 $72 $98 $81 $114 - Revenue 9.7x AV / CY2023E Needham 8/4/2022 Buy 24.00 AV / Revenue $334 $415 $507 87% 87% 87% - - - $80 $107 $133 Revenue 85% 7 5x AV / Goldman Sachs 8/4/2022 Buy 22.00 Revenue; 15% AV / Revenue $332 $412 $492 86% 85% 85% $46 $65 $90 $64 $106 $146 Strategic Ppaids 25x CY2027E Morgan Stanley 8/4/2022 Equal Weight 21.00 AV / FCF $333 $413 $502 86% 86% 87% $46 $60 $93 $85 $84 $115 AV/FCF 7x CY2023E AV / Bank of America 8/4/2022 Buy 20.00 AV / Revenue $334 $420 $521 87% 85% 85% $57 $72 $97 $79 $98 $110 Revenue 8 0x CY2023E AV / Citi 8/5/2022 Neutral 20.00 AV / Revenue $334 $394 $484 83% 78% 78% $52 $63 $79 $84 $98 $126 Revenue 8 0x CY2023E AV / UBS 8/4/2022 Neutral 19.00 AV / Revenue $333 $407 $475 87% 87% 88% $60 $75 $89 $82 $95 $109 Revenue Mean $23.36 $334 $415 $499 87% 85% 85% $53 $66 $91 $81 $104 $123 Median $24.00 $334 $415 $502 87% 86% 87% $53 $65 $92 $81 $105 $121 Post earnings, median CY22 revenue estimates increased Notes from $332; CY23 estimates 1. Latest available broker estimates, excludes Berenberg due to price target as of 2/17/2022 decreased from $417 2. Broker research from prior to the unaffected date of 9/16/2022 PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 24

APPENDIX Reference Materials PRELIMINARY AND CONFIDENTIAL DRAFT 25

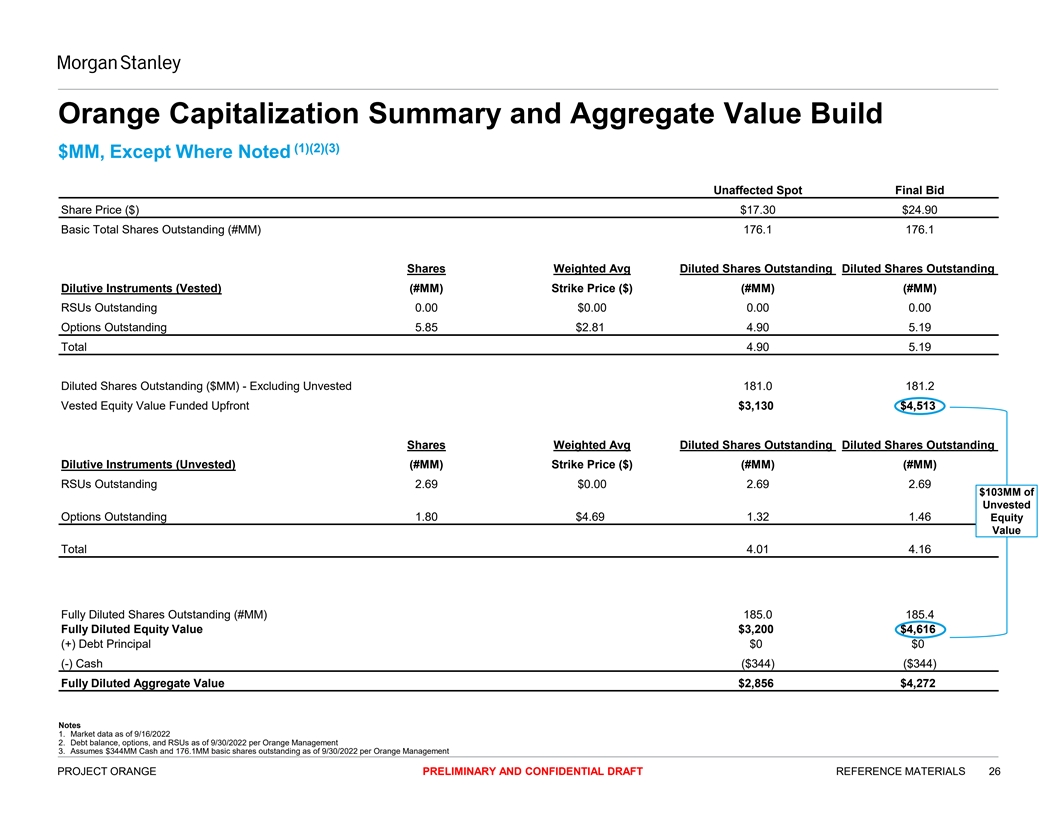

Orange Capitalization Summary and Aggregate Value Build (1)(2)(3) $MM, Except Where Noted Unaffected Spot Final Bid Share Price ($) $17.30 $24.90 Basic Total Shares Outstanding (#MM) 176.1 176.1 Shares Weighted Avg Diluted Shares Outstanding Diluted Shares Outstanding Dilutive Instruments (Vested) (#MM) Strike Price ($) (#MM) (#MM) RSUs Outstanding 0.00 $0.00 0.00 0.00 Options Outstanding 5.85 $2.81 4.90 5.19 Total 4.90 5.19 Diluted Shares Outstanding ($MM) - Excluding Unvested 181.0 181.2 Vested Equity Value Funded Upfront $3,130 $4,513 Shares Weighted Avg Diluted Shares Outstanding Diluted Shares Outstanding Dilutive Instruments (Unvested) (#MM) Strike Price ($) (#MM) (#MM) RSUs Outstanding 2.69 $0.00 2.69 2.69 $103MM of Unvested Options Outstanding 1.80 $4.69 1.32 1.46 Equity Value Total 4.01 4.16 Fully Diluted Shares Outstanding (#MM) 185.0 185.4 Fully Diluted Equity Value $3,200 $4,616 (+) Debt Principal $0 $0 (-) Cash ($344) ($344) Fully Diluted Aggregate Value $2,856 $4,272 Notes 1. Market data as of 9/16/2022 2. Debt balance, options, and RSUs as of 9/30/2022 per Orange Management 3. Assumes $344MM Cash and 176.1MM basic shares outstanding as of 9/30/2022 per Orange Management PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT REFERENCE MATERIALS 26

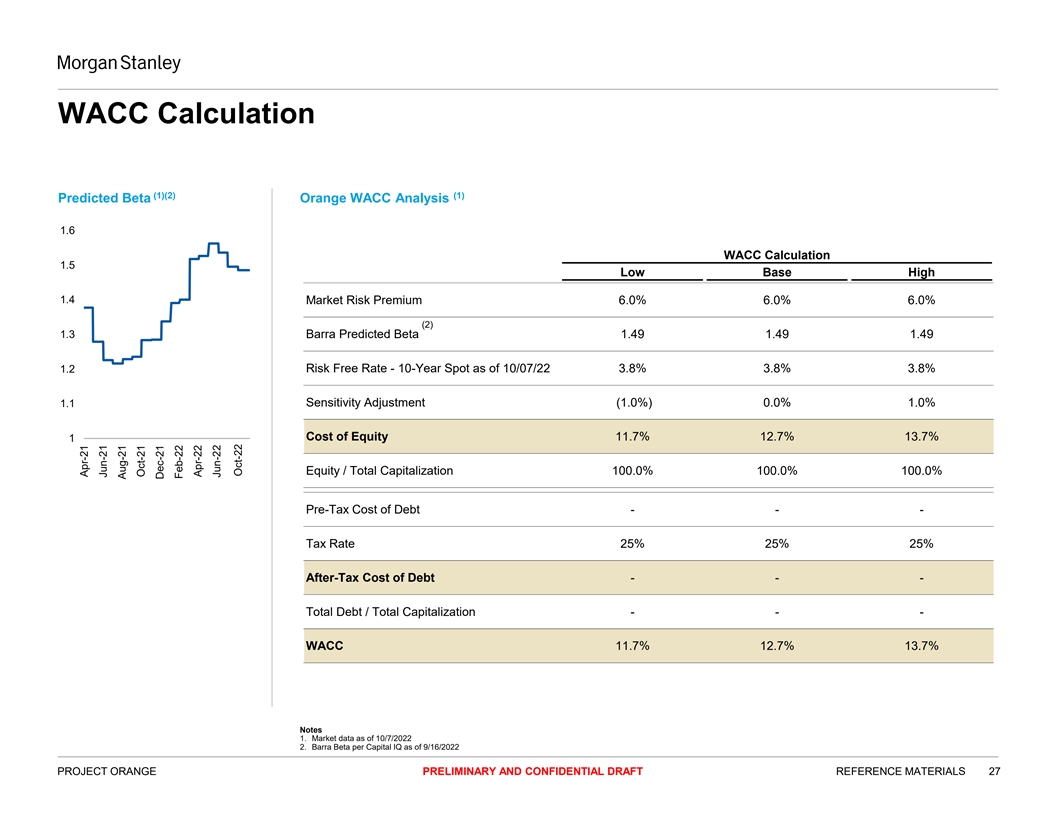

WACC Calculation (1)(2) (1) Predicted Beta Orange WACC Analysis 1.6 WACC Calculation 1.5 Low Base High 1.4 Market Risk Premium 6.0% 6.0% 6.0% (2) 1.3 Barra Predicted Beta 1.49 1.49 1.49 1.2 Risk Free Rate - 10-Year Spot as of 10/07/22 3.8% 3.8% 3.8% Sensitivity Adjustment (1.0%) 0.0% 1.0% 1.1 Cost of Equity 11.7% 12.7% 13.7% 1 Equity / Total Capitalization 100.0% 100.0% 100.0% Pre-Tax Cost of Debt - - - Tax Rate 25% 25% 25% After-Tax Cost of Debt - - - Total Debt / Total Capitalization - - - WACC 11.7% 12.7% 13.7% Notes 1. Market data as of 10/7/2022 2. Barra Beta per Capital IQ as of 9/16/2022 PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT REFERENCE MATERIALS 27 Apr-21 Jun-21 Aug-21 Oct-21 Dec-21 Feb-22 Apr-22 Jun-22 Oct-22

Legal Disclaimer We have prepared this document solely for informational purposes. You should not definitively rely upon it or use it to form the definitive basis for any decision, contract, commitment or action whatsoever, with respect to any proposed transaction or otherwise. You and your directors, officers, employees, agents and affiliates must hold this document and any oral information provided in connection with this document in strict confidence and may not communicate, reproduce, distr bute or disclose it to any other person, or refer to it publicly, in whole or in part at any time except with our prior written consent. If you are not the intended recipient of this document, please delete and destroy all copies immediately. We have prepared this document and the analyses contained in it based, in part, on certain assumptions and information obtained by us from the recipient, its directors, officers, employees, agents, affiliates and/or from other sources. Our use of such assumptions and information does not imply that we have independently verified or necessarily agree with any of such assumptions or information, and we have assumed and relied upon the accuracy and completeness of such assumptions and information for purposes of this document. Neither we nor any of our affiliates, or our or their respective officers, employees or agents, make any representation or warranty, express or implied, in relation to the accuracy or completeness of the information contained in this document or any oral information provided in connection herewith, or any data it generates and accept no responsibility, obligation or liability (whether direct or indirect, in contract, tort or otherwise) in relation to any of such information. We and our affiliates and our and their respective officers, employees and agents expressly disclaim any and all liability which may be based on this document and any errors therein or omissions therefrom. Neither we nor any of our affiliates, or our or their respective officers, employees or agents, make any representation or warranty, express or implied, that any transaction has been or may be effected on the terms or in the manner stated in this document, or as to the achievement or reasonableness of future projections, management targets, estimates, prospects or returns, if any. Any views or terms contained herein are preliminary only, and are based on financial, economic, market and other conditions prevailing as of the date of this document and are therefore subject to change. We undertake no obligation or responsibility to update any of the information contained in this document. Past performance does not guarantee or predict future performance. We have (i) assumed that any forecasted financial information contained herein reflects the best available estimates of future financial performance, and (ii) not made any independent valuation or appraisal of the assets or liabilities of any company involved in any proposed transaction, nor have we been furnished with any such valuations or appraisals. The purpose of this document is to provide the recipient with a preliminary valuation for discussion purposes in connection with a potential transaction. This document and the information contained herein do not constitute an offer to sell or the solicitation of an offer to buy any security, commodity or instrument or related derivative, nor do they constitute an offer or commitment to lend, syndicate or arrange a financing, underwrite or purchase or act as an agent or advisor or in any other capacity with respect to any transaction, or commit capital, or to participate in any trading strategies, and do not constitute legal, regulatory, accounting or tax advice to the recipient. We recommend that the recipient seek independent third party legal, regulatory, accounting and tax advice regarding the contents of this document. This document does not constitute and should not be considered as any form of financial opinion or recommendation by us or any of our affiliates. This document is not a research report and was not prepared by the research department of Morgan Stanley or any of its affiliates. Notwithstanding anything herein to the contrary, each recipient hereof (and their employees, representatives, and other agents) may disclose to any and all persons, without limitation of any kind from the commencement of discussions, the U.S. federal and state income tax treatment and tax structure of the proposed transaction and all materials of any kind (including opinions or other tax analyses) that are provided relating to the tax treatment and tax structure. For this purpose, tax structure is limited to facts relevant to the U.S. federal and state income tax treatment of the proposed transaction and does not include information relating to the identity of the parties, their affiliates, agents or advisors. This document is provided by Morgan Stanley & Co. LLC and/or certain of its affiliates or other applicable entities, which may include Morgan Stanley Realty Incorporated, Morgan Stanley Senior Funding, Inc., Morgan Stanley Bank, N.A., Morgan Stanley & Co. International plc, Morgan Stanley Securities Limited, Morgan Stanley Bank AG, Morgan Stanley MUFG Securities Co., Ltd., Mitsubishi UFJ Morgan Stanley Securities Co., Ltd., Morgan Stanley Asia Limited, Morgan Stanley Australia Securities Limited, Morgan Stanley Australia Limited, Morgan Stanley Asia (Singapore) Pte., Morgan Stanley Services Limited, Morgan Stanley & Co. International plc Seoul Branch and/or Morgan Stanley Canada Limited Unless governing law permits otherwise, you must contact an authorized Morgan Stanley entity in your jurisdiction regarding this document or any of the information contained herein. © Morgan Stanley and/or certain of its affiliates. All rights reserved. PROJECT ORANGE PRELIMINARY AND CONFIDENTIAL DRAFT 28