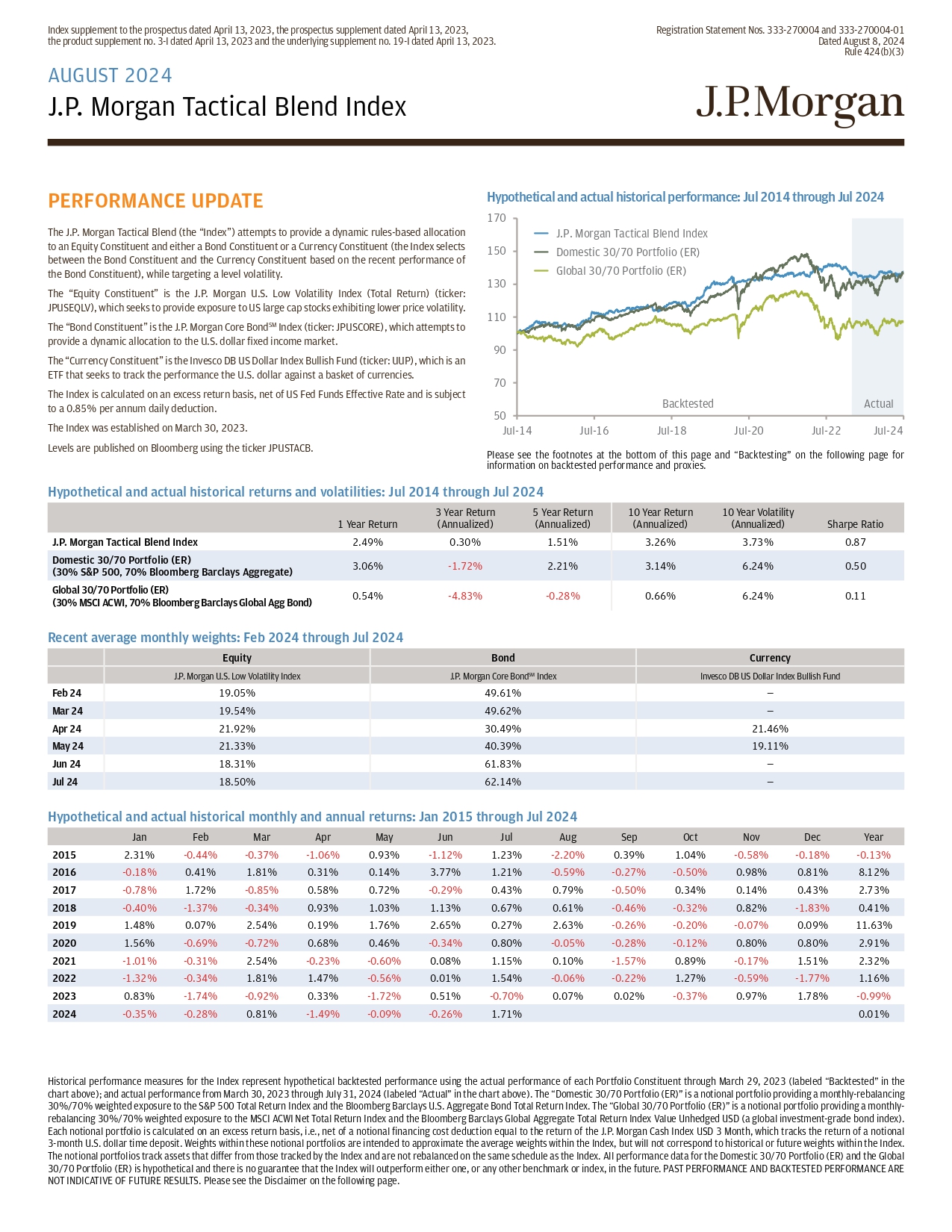

Index supplement to the prospectus dated April 13, 2023, the prospectus supplement dated April 13, 2023, the product supplement no. 3 - I dated April 13, 2023 and the underlying supplement no. 19 - I dated April 13, 2023. Registration Statement Nos. 333 - 270004 and 333 - 270004 - 01 Dated August 8, 2024 Rule 424(b)(3) PERFORMANCE UPDATE The J . P . Morgan Tactical Blend (the “Index”) attempts to provide a dynamic rules - based allocation to an Equity Constituent and either a Bond Constituent or a Currency Constituent (the Index selects between the Bond Constituent and the Currency Constituent based on the recent performance of the Bond Constituent), while targeting a level volatility . The “Equity Constituent” is the J . P . Morgan U . S . Low Volatility Index (Total Return) (ticker : JPUSEQLV), which seeks to provide exposure to US large cap stocks exhibiting lower price volatility . The “Bond Constituent” is the J . P . Morgan Core Bond SM Index (ticker : JPUSCORE), which attempts to provide a dynamic allocation to the U . S . dollar fixed income market . The “Currency Constituent” is the Invesco DB US Dollar Index Bullish Fund (ticker : UUP), which is an ETF that seeks to track the performance the U . S . dollar against a basket of currencies . The Index is calculated on an excess return basis, net of US Fed Funds Etfective Rate and is subject to a 0 . 85 % per annum daily deduction . The Index was established on March 30 , 2023 . Levels are published on Bloomberg using the ticker JPUSTACB . Hypothetical and actual historical performance: Jul 2014 through Jul 2024 Please see the footnotes at the bottom of this page and “Backtesting” on the following page for information on backtested performance and proxies. 70 90 110 130 150 170 Jul - 20 Jul - 22 Jul - 24 J.P. Morgan Tactical Blend Index Domestic 30/70 Portfolio (ER) Global 30/70 Portfolio (ER) Actual Backtested 50 Jul - 14 Jul - 16 Jul - 18 Hypothetical and actual historical returns and volatilities: Jul 2014 through Jul 2024 Sharpe Ratio 10 Year Volatility (Annualized) 10 Year Return (Annualized) 5 Year Return (Annualized) 3 Year Return (Annualized) 1 Year Return 0.87 3.73% 3.26% 1.51% 0.30% 2.49% J.P. Morgan Tactical Blend Index 0.50 6.24% 3.14% 2.21% - 1.72% 3.06% Domestic 30/70 Portfolio (ER) (30% S&P 500, 70% Bloomberg Barclays Aggregate) 0.11 6.24% 0.66% - 0.28% - 4.83% 0.54% Global 30/70 Portfolio (ER) (30% MSCI ACWI, 70% Bloomberg Barclays Global Agg Bond) Recent average monthly weights: Feb 2024 through Jul 2024 Currency Bond Equity Invesco DB US Dollar Index Bullish Fund J.P. Morgan Core Bond SM Index J.P. Morgan U.S. Low Volatility Index — 49.61% 19.05% Feb 24 — 49.62% 19.54% Mar 24 21.46% 30.49% 21.92% Apr 24 19.11% 40.39% 21.33% May 24 — 61.83% 18.31% Jun 24 — 62.14% 18.50% Jul 24 Hypothetical and actual historical monthly and annual returns: Jan 2015 through Jul 2024 Year Dec Nov Oct Sep Aug Jul Jun May Apr Mar Feb Jan - 0.13% - 0.18% - 0.58% 1.04% 0.39% - 2.20% 1.23% - 1.12% 0.93% - 1.06% - 0.37% - 0.44% 2.31% 2015 8.12% 0.81% 0.98% - 0.50% - 0.27% - 0.59% 1.21% 3.77% 0.14% 0.31% 1.81% 0.41% - 0.18% 2016 2.73% 0.43% 0.14% 0.34% - 0.50% 0.79% 0.43% - 0.29% 0.72% 0.58% - 0.85% 1.72% - 0.78% 2017 0.41% - 1.83% 0.82% - 0.32% - 0.46% 0.61% 0.67% 1.13% 1.03% 0.93% - 0.34% - 1.37% - 0.40% 2018 11.63% 0.09% - 0.07% - 0.20% - 0.26% 2.63% 0.27% 2.65% 1.76% 0.19% 2.54% 0.07% 1.48% 2019 2.91% 0.80% 0.80% - 0.12% - 0.28% - 0.05% 0.80% - 0.34% 0.46% 0.68% - 0.72% - 0.69% 1.56% 2020 2.32% 1.51% - 0.17% 0.89% - 1.57% 0.10% 1.15% 0.08% - 0.60% - 0.23% 2.54% - 0.31% - 1.01% 2021 1.16% - 1.77% - 0.59% 1.27% - 0.22% - 0.06% 1.54% 0.01% - 0.56% 1.47% 1.81% - 0.34% - 1.32% 2022 - 0.99% 1.78% 0.97% - 0.37% 0.02% 0.07% - 0.70% 0.51% - 1.72% 0.33% - 0.92% - 1.74% 0.83% 2023 0.01% 1.71% - 0.26% - 0.09% - 1.49% 0.81% - 0.28% - 0.35% 2024 Historical performance measures for the Index represent hypothetical backtested performance using the actual performance of each Portfolio Constituent through March 29 , 2023 (labeled “Backtested” in the chart above) ; and actual performance from March 30 , 2023 through July 31 , 2024 (labeled “Actual” in the chart above) . The “Domestic 30 / 70 Portfolio (ER)” is a notional portfolio providing a monthly - rebalancing 30 % / 70 % weighted exposure to the S&P 500 Total Return Index and the Bloomberg Barclays U . S . Aggregate Bond Total Return Index . The “Global 30 / 70 Portfolio (ER)” is a notional portfolio providing a monthly - rebalancing 30 % / 70 % weighted exposure to the MSCI ACWI Net Total Return Index and the Bloomberg Barclays Global Aggregate Total Return Index Value Unhedged USD (a global investment - grade bond index) . Each notional portfolio is calculated on an excess return basis, i . e . , net of a notional financing cost deduction equal to the return of the J . P . Morgan Cash Index USD 3 Month, which tracks the return of a notional 3 - month U . S . dollar time deposit . Weights within these notional portfolios are intended to approximate the average weights within the Index, but will not correspond to historical or future weights within the Index . The notional portfolios track assets that ditfer from those tracked by the Index and are not rebalanced on the same schedule as the Index . All performance data for the Domestic 30 / 70 Portfolio (ER) and the Global 30 / 70 Portfolio (ER) is hypothetical and there is no guarantee that the Index will outperform either one, or any other benchmark or index, in the future . PAST PERFORMANCE AND BACKTESTED PERFORMANCE ARE NOT INDICATIVE OF FUTURE RESULTS . Please see the Disclaimer on the following page . AUGUST 2024 J.P. Morgan Tactical Blend Index

AUGUST 2024 | J.P. Morgan Tactical Blend Index Selected Risks J.P. Morgan Securities LLC (“JPMS”), as the Index Sponsor and the Index Calculation Agent, may adjust the Index in a way that atfects its level, and JPMS has no obligation to consider any person’s interests. The Index is calculated on an excess return basis, net of US Fed Funds Etfective Rate and is subject to a 0.85% per annum daily deduction. The Index may not be successful or outperform any alternative strategy that might be employed in respect of the Portfolio Constituents. The Index is not expected to approximate the Target Volatility. The Index should not be compared to any other index or strategy sponsored by any affiliates of JPMorgan Chase & Co. (each, a “J.P. Morgan Index”) and cannot necessarily be considered a revised, enhanced or modified version of any other J.P. Morgan Index. The Index may be significantly uninvested. A significant portion of the Index’s exposure may be allocated to the Selected Defensive Constituent. The Index may be more heavily influenced by the performance of the Equity Constituent than the performance of the Selected Defensive Constituent in general over time. Correlation of performances between the Portfolio Constituents may reduce the performance of the Index. Changes in the values of the Portfolio Constituents may otfset each other. Hypothetical back - tested data relating to the Index do not represent actual historical data and are subject to inherent limitations. If the value of a Portfolio Constituent changes, the level of the Index may not change in the same manner. The Index comprises notional assets and liabilities. The Index has a very limited operating history and may perform in unanticipated ways. The Index is subject to market risks. The investment strategy used to construct the Index involves rebalancing from time to time. The Index determines the Selected Defensive Constituent based on the momentum of the Bond Constituent. There are risks associated with the momentum investment strategy underlying the rebalancing methodology of the Index. A Portfolio Constituent may be replaced by a substitute index or ETF upon the occurrence of certain extraordinary events. The Index seeks to allocate notional exposure between the Equity Constituent and the Selected Defensive Constituent so that the risk associated with each constituent is roughly equal. However, the Index methodology may not be successful at achieving “risk - parity” among the Portfolio Constituents. The Portfolio Constituents will likely be unequally weighted in the Index. The risks identified above are not exhaustive. You should also review carefully the related “Risk Factors” section in the prospectus supplement and the relevant product supplement and underlying supplement and the “Selected Risk Considerations” in the relevant pricing supplement. Disclaimer The information contained in this document is for discussion purposes only . Any information relating to performance contained in these materials is illustrative and no assurance is given that any indicative returns, performance or results, whether historical or hypothetical, will be achieved . J . P . Morgan undertakes no duty to update this information . In the event of any inconsistency between the information presented herein and any otfering documents, the otfering documents shall govern . Backtesting : Hypothetical backtested performance measures have inherent limitations and are designed with the benefit of hindsight . Alternative modelling techniques might produce significantly ditferent results and may prove to be more appropriate . For time periods prior to the launch of each of the Bond Constituent’s underlying ETFs, and prior to that underlying ETF’s satisfaction of a minimum liquidity standard, backtesting uses alternative performance derived from the reference index tracked by that underlying ETF as of the live date of the Bond Constituent (or the reference index originally tracked by that underlying ETF, if the reference index as of the live date of the Bond Constituent was not available for the relevant period), after deducting hypothetical fund expenses equal to such underlying ETF’s expense ratio as of the Bond Constituent’s live date, rather than actual performance of that underlying ETF for that period . For time periods prior to the launch of the Currency Constituent, and prior to the Currency Constituent’s satisfaction of a minimum liquidity standard, backtesting uses alternative performance derived from the reference index tracked by the Currency Constituent as of the live date of the Index, after deducting hypothetical fund expenses equal to the Currency Constituent’s expense ratio as of the live date of the Index, rather than actual performance of the Currency Constituent for that period . The use of alternative “proxy” performance information in the calculation of hypothetical backtested weights and levels may have resulted in ditferent, perhaps significantly ditferent, weights and higher levels than would have resulted from the use of actual performance information of the Portfolio Constituents . Past performance, and especially hypothetical backtested performance, is not indicative of future results . This type of information has inherent limitations and you should carefully consider these limitations before placing reliance on such information . The 10 Year Volatility (Annualized) on the previous page is a measure of market risk, calculated as of the square root of two hundred and fifty - two ( 252 ) multiplied by the sample standard deviation of the daily logarithmic returns of each applicable index or portfolio (considering only days for which levels are available for all three) over the preceding 10 years . The Sharpe Ratio on the previous page is a measure of risk - adjusted performance, calculated as the 10 Year Return (Annualized) divided by the 10 Year Volatility (Annualized) . Investment suitability must be determined individually for each investor, and CDs linked to the Index may not be suitable for all investors . This material is not a product of J . P . Morgan Research Departments . Copyright © 2024 JPMorgan Chase & Co . All rights reserved . For additional regulatory disclosures, please consult : www . jpmorgan . com/disclosures . Information contained on this website is not incorporated by reference in, and should not be considered part of, this document . This monthly update document replaces and supersedes all prior written materials of this type previously provided with respect to the Index .