Registration Statement Nos. 333 - 270004 and 333 - 270004 - 01 Dated August 8, 2024 Rule 424(b)(3) Index supplement to underlying supplement no. 22 - I dated May 12, 2023 and the prospectus and prospectus supplement, each dated April 13, 2023 Investing in the notes involves a number of risks. See “Selected risks associated with the Index” beginning on page 5 of this document, “Risk Factors” in the relevant product supplement and underlying supplement and “Selected Risk Considerations” in the relevant pricing supplement. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the notes or passed upon the accuracy or the adequacy of this document or the accompanying pricing supplement, product supplement, underlying supplement, prospectus supplement and prospectus. Any representation to the contrary is a criminal offense. The notes are not bank deposits, are not insured by the Federal Deposit Insurance Corporation or any other governmental agency and are not obligations of, or guaranteed by, a bank. J.P. Morgan Total Return SM Index August 2024

IMPORTANT INFORMATION The information contained in this document is for discussion purposes only . Any information relating to performance contained in these materials is illustrative and no assurance is given that any indicative returns, performance or results, whether historical or hypothetical, will be achieved . All information herein is subject to change without notice, however, J . P . Morgan undertakes no duty to update this information . In the event of any inconsistency between the information presented herein and any offering document, the offering document shall govern . USE OF HYPOTHETICAL BACKTESTED RETURNS Any backtested historical performance and weighting information included herein is hypothetical . The Constituents may not have traded in the manner shown in the hypothetical backtest of the Index (as defined below) included herein, and no representation is being made that the Index will achieve similar performance . There are frequently significant differences between hypothetical backtested performance and actual subsequent performance . The results obtained from backtesting information should not be considered indicative of the actual results that might be obtained from an investment in notes referencing the Index . J . P . Morgan provides no assurance or guarantee that notes linked to the Index will operate or would have operated in the past in a manner consistent with these materials . The hypothetical historical levels presented herein have not been verified by an independent third party, and such hypothetical historical levels have inherent limitations . Alternative simulations, techniques, modeling or assumptions might produce significantly different results and prove to be more appropriate . Actual results will vary, perhaps materially, from the hypothetical backtested returns and allocations presented in this document . HISTORICAL AND BACKTESTED PERFORMANCE AND ALLOCATIONS ARE NOT INDICATIVE OF FUTURE RESULTS . USE OF ALTERNATIVE PERFORMANCE The information provided herein uses “backtesting” and considers other hypothetical circumstances to estimate how the Index may have performed and how Constituents (as defined below) may have been allocated prior to the actual existence of the Index . Prior to 7 / 13 / 2017 , the Index’s hypothetical backtested performance relies on, and its weights are applied to, alternative “proxy” performance for some of the Constituents identified below . Additionally, alternative performance information for certain Constituents may have been considered in determining hypothetical weight allocations for such Constituents after this date . Prior to each such Constituent’s launch and satisfaction of a minimum liquidity standard, the backtesting uses (in lieu of actual performance) alternative performance derived from the reference index tracked by that Constituent as of the Index’s live date, after deduction of hypothetical fund expenses (in each case, as specified in the accompanying parenthetical) equal to that Constituent’s expense ratio as of the Index’s live date, as follows : the Barclays U . S . 7 - 10 Year Treasury Bond Index was used as a proxy for iShares ® 7 - 10 Year Treasury Bond ETF through 4 / 23 / 2004 ( - 0 . 15 % p . a . ) ; the Barclays U . S . 20 + Year Treasury Bond Index was used as a proxy for iShares ® 20 + Year Treasury Bond ETF through 4 / 16 / 2004 ( - 0 . 15 % p . a . ) ; the Bloomberg Barclays US 1 - 3 Year Credit Bond Index was used as a proxy for iShares ® 1 - 5 Year Investment Grade Corporate Bond ETF through 1 / 13 / 2009 ( - 0 . 20 % p . a . ) ; the Bloomberg Barclays US Intermediate Credit Bond Index was used as a proxy for iShares ® 5 - 10 Year Investment Grade Corporate Bond ETF through 4 / 6 / 2009 ( - 0 . 20 % p . a . ) ; the Bloomberg Barclays US Long Credit Index was used as a proxy for iShares ® 10 + Year Investment Grade Corporate Bond ETF through 6 / 25 / 2014 ( - 0 . 20 % p . a . ) ; the Bloomberg Barclays US Mortgage - Backed Securities (MBS) Index was used as a proxy for iShares ® MBS ETF through 9 / 11 / 2008 ( - 0 . 29 % p . a . ) ; the Bloomberg Barclays US Treasury Inflation Protected Securities (TIPS) Index (Series - L) was used as a proxy for iShares ® TIPS Bond ETF through 5 / 27 / 2004 ( - 0 . 20 % p . a . ) ; the J . P . Morgan EMBI SM Global Core Index was used as a proxy for iShares ® J . P . Morgan USD Emerging Markets Bond ETF through 11 / 17 / 2009 ( - 0 . 40 % p . a . ) ; the Markit iBoxx ® USD Liquid High Yield Index was used as a proxy for iShares ® iBoxx ® $ High Yield Corporate Bond ETF through 5 / 23 / 2008 ( - 0 . 50 % p . a . ) ; the Bloomberg Barclays US Floating Rate Note < 5 Years Index was used as a proxy for iShares ® Floating Rate Bond ETF through 1 / 15 / 2013 ( - 0 . 20 % p . a . ) ; the S&P U . S . Preferred Stock Index was used as a proxy for iShares ® Preferred and Income Securities ETF through 10 / 20 / 2008 ( - 0 . 47 % p . a . ) . Investment suitability must be determined individually for each investor, and investments linked to the Index may not be suitable for all investors . This material is not a product of J . P . Morgan Research Departments . Copyright © 2024 JPMorgan Chase & Co . All rights reserved . For additional regulatory disclosures, please consult : www . jpmorgan . com/disclosures . Information contained on this website is not incorporated by reference in, and should not be considered part of, this document .

Executive summary 1 The J.P. Morgan Total Return SM Index (the “Index”) was launched as J.P. Morgan Investable Indices’ flagship “smart beta” fixed income index with more than six years of live track record The Index applies a rules - based methodology to evaluate recent market conditions and allocate dynamically across up to twelve ETFs that each track a U.S. dollar fixed income sector By looking at recent ETF returns and volatility, the Index indirectly uses cross - sectoral momentum to vary its duration, credit and liquidity risk profiles based on market conditions The Index can allocate opportunistically to ETFs that provide exposure to alternative fixed income assets (e.g., TIPS, high yield, emerging markets, floating - rate notes) Over its live period, the Index has outperformed the Bloomberg US Aggregate Bond Index by 1.41% p.a. 1 with outperformance in both rising and declining rate environments J.P. Morgan can provide exposure to the Index in delta - one notes STRENGTHS Live track record delivering 1.41% p.a. 1 outperformance over the Bloomberg US Aggregate Bond Index Systematic portfolio construction CONSIDERATIONS Notes linked to the Index are subject to the credit risk of JPMorgan Chase Financial Company LLC, as issuer of the notes, and JPMorgan Chase & Co., as guarantor of the notes Notes linked to the Index are not listed on any exchange Greater perceived market acceptance of ETFs 1 Note: Past performance is no guarantee of future performance. Based on the historical live close levels of the J.P. Morgan Total Return SM Index and the Bloomberg US Aggregate Bond Index from July 13, 2017 through July 31, 2024.

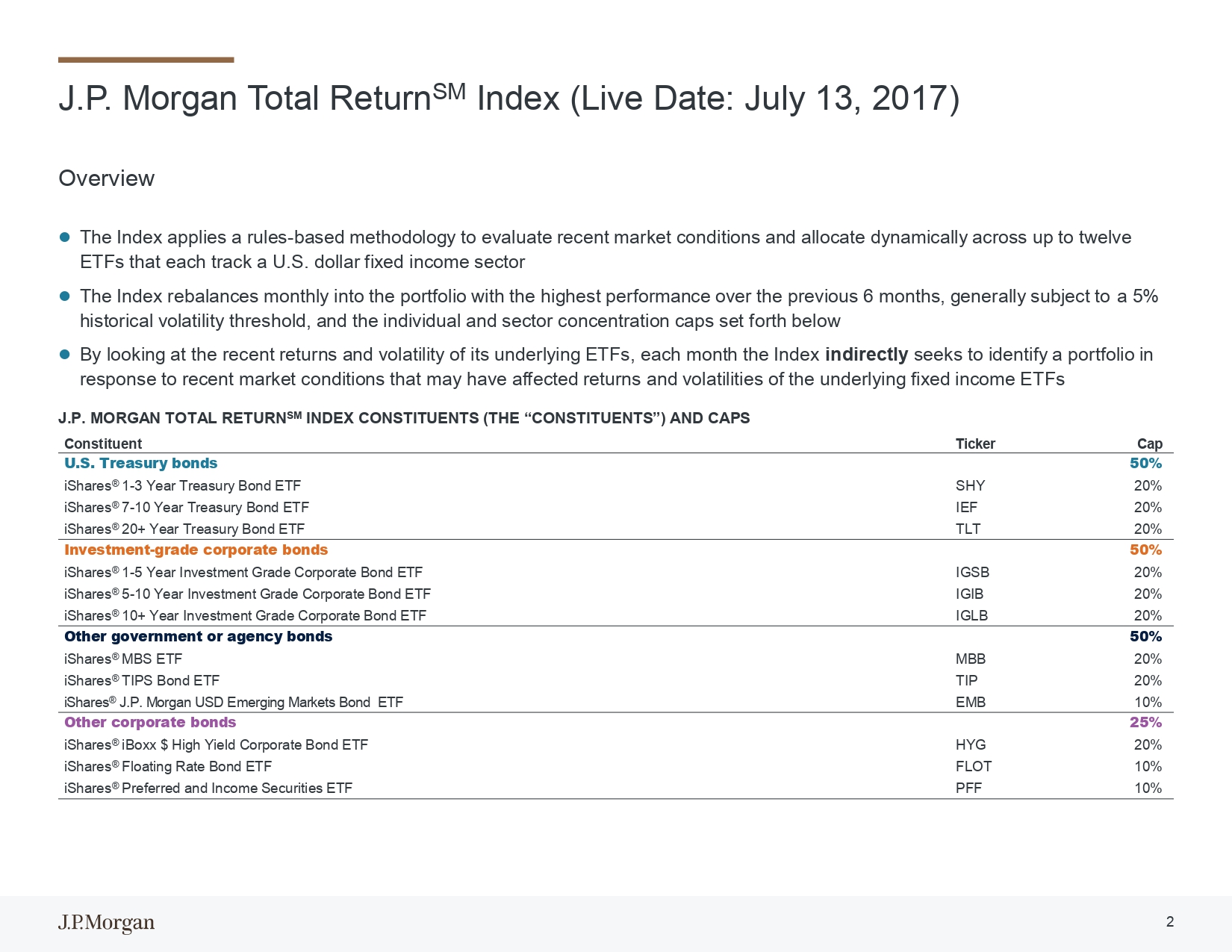

J.P. Morgan Total Return SM Index (Live Date: July 13, 2017) 2 Overview The Index applies a rules - based methodology to evaluate recent market conditions and allocate dynamically across up to twelve ETFs that each track a U.S. dollar fixed income sector The Index rebalances monthly into the portfolio with the highest performance over the previous 6 months, generally subject to a 5% historical volatility threshold, and the individual and sector concentration caps set forth below By looking at the recent returns and volatility of its underlying ETFs, each month the Index indirectly seeks to identify a portfolio in response to recent market conditions that may have affected returns and volatilities of the underlying fixed income ETFs J.P. MORGAN TOTAL RETURN SM INDEX CONSTITUENTS (THE “CONSTITUENTS”) AND CAPS Cap Ticker Constituent 50% U.S. Treasury bonds 20% SHY iShares ® 1 - 3 Year Treasury Bond ETF 20% IEF iShares ® 7 - 10 Year Treasury Bond ETF 20% TLT iShares ® 20+ Year Treasury Bond ETF 50% Investment - grade corporate bonds 20% IGSB iShares ® 1 - 5 Year Investment Grade Corporate Bond ETF 20% IGIB iShares ® 5 - 10 Year Investment Grade Corporate Bond ETF 20% IGLB iShares ® 10+ Year Investment Grade Corporate Bond ETF 50% Other government or agency bonds 20% MBB iShares ® MBS ETF 20% TIP iShares ® TIPS Bond ETF 10% EMB iShares ® J.P. Morgan USD Emerging Markets Bond ETF 25% Other corporate bonds 20% HYG iShares ® iBoxx $ High Yield Corporate Bond ETF 10% FLOT iShares ® Floating Rate Bond ETF 10% PFF iShares ® Preferred and Income Securities ETF

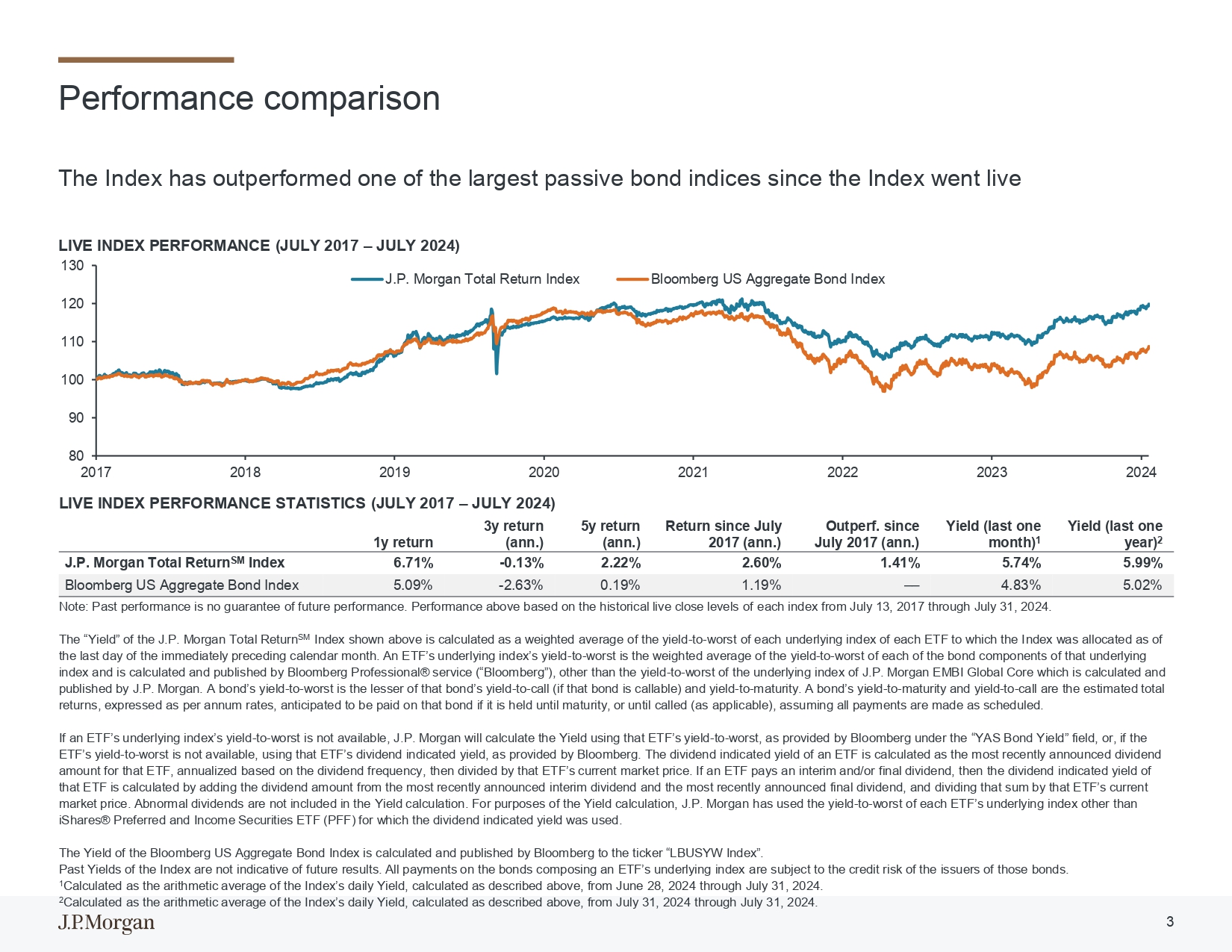

Performance comparison 120 110 100 90 2021 2022 2023 2024 J.P. Morgan Total Return Index Bloomberg US Aggregate Bond Index 3 LIVE INDEX PERFORMANCE (JULY 2017 – JULY 2024) 130 80 2017 2018 2019 2020 LIVE INDEX PERFORMANCE STATISTICS (JULY 2017 – JULY 2024) The Index has outperformed one of the largest passive bond indices since the Index went live Yield (last one year) 2 Yield (last one month) 1 Outperf. since July 2017 (ann.) Return since July 2017 (ann.) 5y return (ann.) 3y return (ann.) 1y return 5.99% 5.74% 1.41% 2.60% 2.22% - 0.13% 6.71% J.P. Morgan Total Return SM Index 5.02% 4.83% –– 1.19% 0.19% - 2.63% 5.09% Bloomberg US Aggregate Bond Index Note: Past performance is no guarantee of future performance. Performance above based on the historical live close levels of each index from July 13, 2017 through July 31, 2024. The “Yield” of the J.P. Morgan Total Return SM Index shown above is calculated as a weighted average of the yield - to - worst of each underlying index of each ETF to which the Index was allocated as of the last day of the immediately preceding calendar month. An ETF’s underlying index’s yield - to - worst is the weighted average of the yield - to - worst of each of the bond components of that underlying index and is calculated and published by Bloomberg Professional® service (“Bloomberg”), other than the yield - to - worst of the underlying index of J.P. Morgan EMBI Global Core which is calculated and published by J.P. Morgan. A bond’s yield - to - worst is the lesser of that bond’s yield - to - call (if that bond is callable) and yield - to - maturity. A bond’s yield - to - maturity and yield - to - call are the estimated total returns, expressed as per annum rates, anticipated to be paid on that bond if it is held until maturity, or until called (as applicable), assuming all payments are made as scheduled. If an ETF’s underlying index’s yield - to - worst is not available, J.P. Morgan will calculate the Yield using that ETF’s yield - to - worst, as provided by Bloomberg under the “YAS Bond Yield” field, or, if the ETF’s yield - to - worst is not available, using that ETF’s dividend indicated yield, as provided by Bloomberg. The dividend indicated yield of an ETF is calculated as the most recently announced dividend amount for that ETF, annualized based on the dividend frequency, then divided by that ETF’s current market price. If an ETF pays an interim and/or final dividend, then the dividend indicated yield of that ETF is calculated by adding the dividend amount from the most recently announced interim dividend and the most recently announced final dividend, and dividing that sum by that ETF’s current market price. Abnormal dividends are not included in the Yield calculation. For purposes of the Yield calculation, J.P. Morgan has used the yield - to - worst of each ETF’s underlying index other than iShares® Preferred and Income Securities ETF (PFF) for which the dividend indicated yield was used. The Yield of the Bloomberg US Aggregate Bond Index is calculated and published by Bloomberg to the ticker “LBUSYW Index”. Past Yields of the Index are not indicative of future results. All payments on the bonds composing an ETF’s underlying index are subject to the credit risk of the issuers of those bonds. 1 Calculated as the arithmetic average of the Index’s daily Yield, calculated as described above, from June 28, 2024 through July 31, 2024. 2 Calculated as the arithmetic average of the Index’s daily Yield, calculated as described above, from July 31, 2024 through July 31, 2024.

Selected risks associated with the Index 4 Our affiliate, J.P. Morgan Securities LLC (“JPMS”), is the sponsor and index calculation agent of the Index and may adjust the Index in a way that affects its level — Policies and judgments for which JPMS is responsible could have an impact, positive or negative, on the level of the Index and the value of your investment. JPMS may have interests adverse to your interests as an investor in notes linked to the Index, and JPMS is under no obligation to consider your interests. The securities of JPMorgan Chase & Co. are currently held by several Constituents — JPMC will not, however, have any obligation to consider your interests in taking any corporate action that might affect the level of these Constituents, their reference indices or the Index. There are risks associated with the Index’s momentum allocation strategy — If market conditions do not represent a continuation of prior observed trends, the level of the Index, which is rebalanced monthly based on prior trends, may decline. Additionally, even when the values of the Constituents are trending downwards, the Index will continue to be composed of the downward trending Constituents between monthly rebalancing dates. The Index may not approximate its target volatility. The Index may perform poorly during periods characterized by short - term volatility — The Index’s strategy is based on momentum investing. Momentum investing strategies are effective at identifying the current market direction in trending markets. Consequently, the Index may perform poorly in non - trending, “choppy” markets characterized by short - term volatility. An ETF may not fully replicate its reference index and may hold securities different from those included in its reference index. The performance of an ETF may also not correlate with the performance of its reference index — The performance of each ETF may not correlate with its net asset value per share, which could materially and adversely affect the value of the notes in the secondary market and/or reduce any payment on the notes. At a time when the value of one Constituent increases, the values of the other Constituents may not increase as much or may even decline — The Index may not perform as well as an alternative index that tracks only one Constituent. The Constituents are subject to monthly rebalancing and weighting constraints by asset type and on subsets of assets based on historical volatility — No assurance can be given that the investment strategy used to construct the Index will outperform any alternative investment in the Constituents.

Selected risks associated with the Index 5 The Constituent of the Index may be replaced by a substitute constituent ETF in certain extraordinary events — Changing a Constituent may affect the performance of the Index, and therefore, the return on an investment, as the replacement Constituent may perform significantly better or worse than the original Constituent . Other key risks : The Index comprises notional assets and liabilities. There is no actual portfolio of assets to which any person is entitled or in which any person has any ownership interest. The Index is subject to significant risks associated with fixed - income securities, including interest rate - related risks and credit risk. The Index is subject to significant risks associated with high - yield fixed income securities, including credit risk. The Index is subject to significant risks associated with floating rate notes. The Index is subject to significant risks associated with mortgage - backed securities. The Index is subject to significant risks associated with preferred stock. The Index is subject to significant risks associated with hybrid securities. The Index is subject to risks associated with non - U.S. securities markets, including emerging markets. The Index may not be successful or outperform any alternative strategy that might be employed in respect of the Constituents. The risks identified above are not exhaustive. You should also carefully review the related “Risk Factors” section in the relevant product supplement and underlying supplement and the “Selected Risk Considerations” in the relevant pricing supplement.