UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

☐ Preliminary Proxy Statement

☐Confidential, for Use of the Commission Only (as permitted by Rule14a-6(e)(2))

☐ Definitive Proxy Statement

☒ Definitive Additional Materials

☐ Soliciting Material Pursuant to§240.14a-12

CAMPBELL SOUP COMPANY

(Name of the Registrant as Specified In Its Charter)

THIRD POINT LLC

DANIEL S. LOEB

THIRD POINT PARTNERS QUALIFIED L.P.

THIRD POINT PARTNERS L.P.

THIRD POINT OFFSHORE MASTER FUND L.P.

THIRD POINT ULTRA MASTER FUND L.P.

THIRD POINT ENHANCED LP

THIRD POINT ADVISORS LLC

THIRD POINT ADVISORS II LLC

FRANCI BLASSBERG

MATTHEW COHEN

SARAH HOFSTETTER

MUNIB ISLAM

LAWRENCE KARLSON

BOZOMA SAINT JOHN

KURT SCHMIDT

RAYMOND SILCOCK

DAVID SILVERMAN

MICHAEL SILVERSTEIN

GEORGE STRAWBRIDGE, JR.

WILLIAM TOLER

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

| ☒ | No fee required. | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials. | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

Third Point Sends Letter to Shareholders Regarding Campbell’s Record of Putting the Interests of Billionaire, Insider Heirs Ahead of Independent Shareholders

Asserts Shareholders and Employees Have Been Repeatedly Misled About the Consequences of Share Buyback Programs and the Implications of Certain Disastrous Acquisitions

Believes Twenty Years of Buybacks Occurred Without Disclosing That One Result Was to Give the Two Billionaire Dorrance Siblings on the Board Almost Total Control Over the Company’s Direction

Reminds Shareholders that the Entrenched Board’s Legacy of Value Destruction Includes an Approximately 20% Drop in Share Price This Year Alone

After Considering the Current Board’s History of Destroying Your Value, We Urge Shareholders to VOTE THE WHITE CARD to Elect the Independent Slate and End This Reign of Error

NEW YORK—(BUSINESS WIRE)—Third Point LLC (LSE: TPOU) (“Third Point”), a New York-based investment firm managing approximately $17 billion in assets and a holder of approximately 7% of the outstanding common shares of Campbell Soup Company (NYSE: CPB) (“Campbell” or the “Company”), has mailed a detailed letter to shareholders regarding Campbell’s record of putting the interests of billionaire, insider heirs ahead of independent shareholders. Thefull text of the letter can be found here and below.

As a reminder, we encourage all shareholders to also reviewour Case for Change to understand more about why the Independent Slate will respect shareholder voices, end the Entrenched Board’s reign of error, and set Campbell on a new and profitable path. We urge all shareholders toVOTE THE WHITE CARD to elect the Independent Slate.

***

November 5, 2018

Dear Fellow Campbell Soup Company Shareholder:

Campbell’s shareholders and employees have been misled about the consequences of the Company’s share buyback programs and the implications of some of its purchases. Campbell has done twenty years of stock buybacks without disclosing that one result was to give the two billionaire Dorrance siblings on the Board almost total control over the Company and the practical ability to block any important decisions they do not like. The Company’s recentall-cash acquisition ofSnyder’s-Lance has saddled Campbell’s with massive debt that is now heavily weighing on the Company but benefitted the billionaire siblings by allowing them to keep their control that could otherwise have been diluted. We find ourselves asking:

Is this Company run for ALL Shareholders or for the Benefit of Two Billionaire Insiders?

We believe SHAREHOLDERS DESERVE THE FACTS and the Incumbent Board and the Company should answer these tough questions.

The Facts on Buybacks:

| • | The Company touts that it hasmade $11.3 billion in share buybacks since 1988 following programs authorized by the Board. |

| • | In 1996, the year the Company started its first largebuy-back, the Dorrance siblings beneficially owned 107 million shares, which was 21.5% of the outstanding stock. Today, they own only 100 million shares after disposing of almost 7% of their shares over the past 22 years. Yet because of the share repurchase programs, their percentage ownership has swelled to 32.8%.This is a 52%increase in control despite areduction in ownership! |

| • | The Company’s charter requires atwo-thirds supermajority to approve major corporate transactions like important mergers and sales. |

| • | Based on the supermajority requirements, the buybacks have provided the Dorrance siblings withblocking rights over any major decision shareholders may be asked to make. Allowing this creeping control to happen was not fair to other shareholders and shows the Board has been asleep at the switch. |

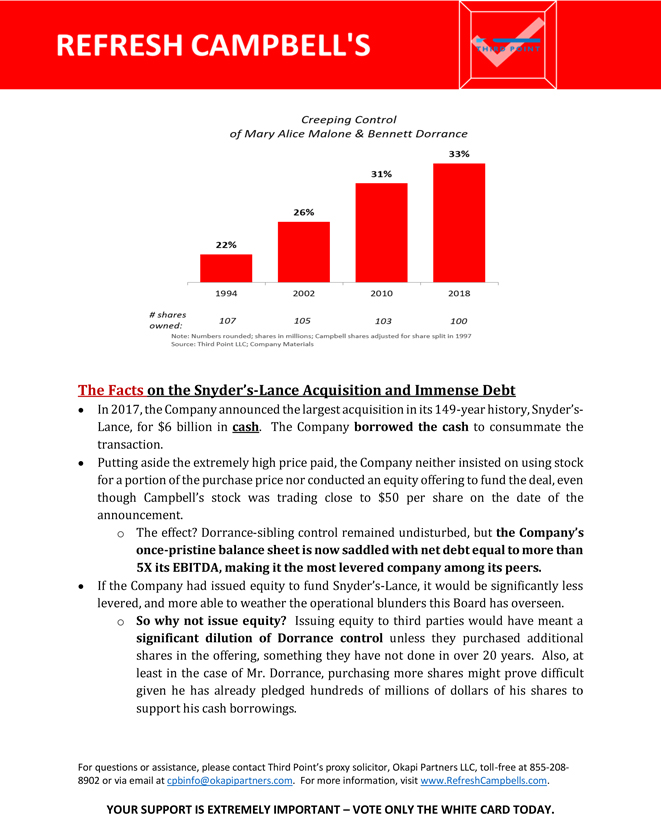

The Facts on theSnyder’s-Lance Acquisition and Immense Debt:

| • | In 2017, the Company announced the largest acquisition in its149-year history,Snyder’s-Lance, for $6 billion incash. The Companyborrowed the cash to consummate the transaction. |

| • | Putting aside the extremely high price paid, the Company neither insisted on using stock for a portion of the purchase price nor conducted an equity offering to fund the deal, even though Campbell’s stock was trading close to $50 per share on the date of the announcement. |

| • | The effect? Dorrance-sibling control remained undisturbed, butthe Company’s once-pristine balance sheet is now saddled with net debt equal to more than 5X its EBITDA, making it the most levered company among its peers. |

| • | If the Company had issued equity to fundSnyder’s-Lance, it would be significantly less levered, and more able to weather the operational blunders this Board has overseen. |

| • | So why not issue equity?Issuing equity to third parties would have meant asignificant dilution of Dorrance control unless they purchased additional shares in the offering, something they have not done in over 20 years. Also, at least in the case of Mr. Dorrance, purchasing more shares might prove difficult given he has already pledged hundreds of millions of dollars of his shares to support his cash borrowings. |

The Facts on Corporate Governance and Disclosures:

| • | Mr. Dorrance wasCo-Chair of the Finance and Corporate Development Committee in 1996, and directly responsible for approving these buybacks. Ms. Dorrance Malone served on the Finance and Corporate Development Committee when theSnyder’s-Lance transaction was structured as all cash. |

| • | The Company never disclosed the conflict of interest inherent in thebuy-back program, nor the risk to investors that, thanks to the supermajority provision and thebuy-backs, investors would effectively have no say in the Company’s most important transactions. |

| • | The Company has not disclosed whether the desire to retain control was a factor in its decisions relating to the funding of theSnyder’s-Lance acquisition. |

The Two Key Questions:

| • | How could the Board of Campbell’s, who are duty bound to look after your interests, fail to protect independent shareholders? |

| • | We believe not insisting on protective provisions (such as permitting buybacks to benefit all shareholders but not increasing the billionaire insiders’ incremental vote) to prevent the “creeping control” by the Dorrance siblings is a breach of the fundamental duties of this board. |

| • | Why was this “creeping control” never listed as a risk factor associated with the buyback policy? |

| • | Did the Board not offer stock or conduct an equity offering to fund its largest acquisition ever, saddling the Company with unprecedented debt, because the Dorrance siblings wanted to retain their blocking position? |

Does this Board really represent you or does it represent the Two Billionaire Insiders?

The Independent Slate is running to replace the Entrenched Board because we believe that with a flat stock price over 20 years, Campbell has been focused on serving someone other than its public shareholders and employees.

VOTE THE WHITE CARD TO LEARN THE ANSWERS TO THESE QUESTIONS AND END THE BOARD’S REIGN OF ERROR. Learn more about our plans atwww.refreshcampbells.com.

***

Your Vote Is Important, No Matter How Many or How Few Shares You Own!

PLEASE REMEMBER TO CAN THE COMPANY’S CARD! If you return a Campbell’s proxy card – even by simply indicating “withhold” on the Company’s slate – you will revoke any vote you had previously submitted for the Third Point nominees on the WHITE proxy card.

IMPORTANT INFORMATION

On September 28, 2018, Third Point LLC filed a definitive proxy statement and on October 1, 2018 filed Supplement No. 1 thereto and on October 9, 2018 filed Supplement No. 2 thereto (collectively, the “Definitive Proxy Statement”) with the U.S. Securities and Exchange Commission (“SEC”) to solicit proxies from stockholders of Campbell Soup Company (the “Company”) for use at the Company’s 2018 annual meeting of stockholders. THIRD POINT STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE DEFINITIVE PROXY STATEMENT BECAUSE IT CONTAINS IMPORTANT INFORMATION. THE DEFINITIVE PROXY STATEMENT ALSO INCLUDES INFORMATION ABOUT THE IDENTITY OF THE PARTICIPANTS IN THE THIRD POINT SOLICITATION AND A DESCRIPTION OF THEIR DIRECT OR INDIRECT INTERESTS THEREIN. The Definitive Proxy Statement is available at no charge on the SEC’s website athttp://www.sec.gov and is also available, without charge, on request from Third Point LLC’s proxy solicitor, Okapi Partners LLC, at (855)208-8902 or via email atCPBinfo@okapipartners.com.

CONTACTS

For Media:

Third Point LLC

Elissa Doyle,917-748-8533

Chief Marketing Officer

edoyle@thirdpoint.com

###

REFRESH CAMPBELL’S THIRD POINT How Did the Billionaire Dorrance Siblings Come to Control Campbell’s Soup Over the Past Two Decades? How Did They Increase Their Voting Power by 52% Despite Disposing Some of Their Holdings as the Stock Stalled for Shareholders? Shareholders Deserve Answers Learn the Facts and Vote the White Card for the Independent Slate to Put Shareholder Interests Above Those of Billionaire Insiders

November 5, 2018 Dear Fellow Campbell Soup Company Shareholder: Campbell’s shareholders and employees have been misled about the consequences of the Company’s share buyback programs and the implications of some of its purchases. Campbell has done twenty years of stock buybacks without disclosing that one result was to give the two billionaire Dorrance siblings on the Board almost total control over the Company and the practical ability to block any important decisions they do not like. The Company’s recent all-cash acquisition of Snyder’s-Lance has saddled Campbell’s with massive debt that is now heavily weighing on the Company but benefitted the billionaire siblings by allowing them to keep their control that could otherwise have been diluted. We find ourselves asking: Is this Company run for ALL Shareholders or for the Benefit of Two Billionaire Insiders? We believe SHAREHOLDERS DESERVE THE FACTS and the Incumbent Board and the Company should answer these tough questions. The Facts on Buybacks: • The Company touts that it has made $11.3 billion in share buybacks since 1988 following programs authorized by the Board. • In 1996, the year the Company started its first largebuy-back, the Dorrance siblings beneficially owned 107 million shares, which was 21.5% of the outstanding stock. Today, they own only 100 million shares after disposing of almost 7% of their shares over the past 22 years. Yet because of the share repurchase programs, their percentage ownership has swelled to 32.8%. This is a 52% increase in control despite a reduction in ownership! • The Company’s charter requires atwo-thirds supermajority to approve major corporate transactions like important mergers and sales. o Based on the supermajority requirements, the buybacks have provided the Dorrance siblings with blocking rights over any major decision shareholders may be asked to make. Allowing this creeping control to happen was not fair to other shareholders and shows the Board has been asleep at the switch.

Creeping Control of Mary Alice Malone & Bennett Dorrance 22% 26% 31% 33% 1994 2002 2010 2018 #shares owned: 107 105 103 100 Note: Numbers rounded; shares in millions; Campbell shares adjusted for share split in 1997 Source: Third Point LLC; Company Materials The Facts on the Snyder’s-Lance Acquisition and Immense Debt • In 2017, the Company announced the largest acquisition in its149-year history,Snyder’s-Lance, for $6 billion in cash. The Company borrowed the cash to consummate the transaction. • Putting aside the extremely high price paid, the Company neither insisted on using stock for a portion of the purchase price nor conducted an equity offering to fund the deal, even though Campbell’s stock was trading close to $50 per share on the date of the announcement. o The effect? Dorrance-sibling control remained undisturbed, but the Company’s once-pristine balance sheet is now saddled with net debt equal to more than 5X its EBITDA, making it the most levered company among its peers. • If the Company had issued equity to fundSnyder’s-Lance, it would be significantly less levered, and more able to weather the operational blunders this Board has overseen. o So why not issue equity? Issuing equity to third parties would have meant a significant dilution of Dorrance control unless they purchased additional shares in the offering, something they have not done in over 20 years. Also, at least in the case of Mr. Dorrance, purchasing more shares might prove difficult given he has already pledged hundreds of millions of dollars of his shares to support his cash borrowings.

The Facts on Corporate Governance and Disclosures • Mr. Dorrance wasCo-Chair of the Finance and Corporate Development Committee in 1996, and directly responsible for approving these buybacks. Ms. Dorrance Malone served on the Finance and Corporate Development Committee when theSnyder’s-Lance transaction was structured as all cash. • The Company never disclosed the conflict of interest inherent in thebuy-back program, nor the risk to investors that, thanks to the supermajority provision and thebuy-backs, investors would effectively have no say in the Company’s most important transactions. • The Company has not disclosed whether the desire to retain control was a factor in its decisions relating to the funding of theSnyder’s-Lance acquisition. The Two Key Questions • How could the Board of Campbell’s, who are duty bound to look after your interests, fail to protect independent shareholders? • We believe not insisting on protective provisions (such as permitting buybacks to benefit all shareholders but not increasing the billionaire insiders’ incremental vote) to prevent the “creeping control” by the Dorrance siblings is a breach of the fundamental duties of this board. • Why was this “creeping control” never listed as a risk factor associated with the buyback policy? • Did the Board not offer stock or conduct an equity offering to fund its largest acquisition ever, saddling the Company with unprecedented debt, because the Dorrance siblings wanted to retain their blocking position? Does this Board really represent you or does it represent the Two Billionaire Insiders? The Independent Slate is running to replace the Entrenched Board because we believe that with a flat stock price over 20 years, Campbell has been focused on serving someone other than its public shareholders and employees. VOTE THE WHITE CARD TO LEARN THE ANSWERS TO THESE QUESTIONS AND END THE BOARD’S REIGN OF ERROR. Learn more about our plans at www.refreshcampbells.com.

@ThirdPointLLC issued Tweets stating:

7 core products out of stock, 6 months without a CEO, no plan. This photo from a @GiantEagle store shows how much $CPB has suffered at the hands of the current Board. Enough is enough – it’s time to #RefreshTheRecipe (SEC Legend: http://bit.ly/SEC_Legend)

Is $CPB run for ALL shareholders or for the benefit of two billionaire insiders? Today we mailed a letter describing how we believe $CPB shareholders & employees have been grossly misled. Click here to read our letter https://bit.ly/2CVjIIq (SEC Legend: http://bit.ly/SEC_Legend)

****

Third Point LLC also issued the following statement through additional social media outlets:

Is Campbell Soup Company run for ALL shareholders or for the benefit of two billionaire insiders? Today, Third Point mailed a letter asserting that Campbell Soup Company shareholders and employees have been grossly misled. Click here to read our letter https://bit.ly/2CVjIIq and #RefreshTheRecipe (SEC Legend: http://bit.ly/SEC_Legend)

****

Permission to use quotations in this filing neither sought nor obtained.

IMPORTANT INFORMATION

On September 28, 2018, Third Point LLC filed a definitive proxy statement and on October 1, 2018 filed Supplement No. 1 thereto and on October 9, 2018 filed Supplement No. 2 thereto (collectively, the “Definitive Proxy Statement”) with the U.S. Securities and Exchange Commission (“SEC”) to solicit proxies from stockholders of Campbell Soup Company (the “Company”) for use at the Company’s 2018 annual meeting of stockholders. THIRD POINT STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE DEFINITIVE PROXY STATEMENT BECAUSE IT CONTAINS IMPORTANT INFORMATION.THE DEFINITIVE PROXY STATEMENT ALSO INCLUDES INFORMATION ABOUT THE IDENTITY OF THE PARTICIPANTS IN THE THIRD POINT SOLICITATION AND A DESCRIPTION OF THEIR DIRECT OR INDIRECT INTERESTS THEREIN.The Definitive Proxy Statement is available at no charge on the SEC’s website at http://www.sec.gov and is also available, without charge, on request from Third Point LLC’s proxy solicitor, Okapi Partners LLC, at (855)208-8902 or via email atCPBinfo@okapipartners.com.