We may be adversely affected by natural disasters and other catastrophic events, and byman-made problems such as terrorism, that could disrupt our business operations and our business continuity and disaster recovery plans may not adequately protect us from a serious disaster.

Natural disasters or other catastrophic events may also cause damage or disruption to our operations, international commerce, and the global economy, and could have an adverse effect on our business, operating results, and financial condition. Our business operations are subject to interruption by natural disasters, fire, power shortages, pandemics, and other events beyond our control. In addition, acts of terrorism and othergeo-political unrest could cause disruptions in our business or the businesses of our partners or the economy as a whole. In the event of a natural disaster, including a major earthquake, blizzard, or hurricane, or a catastrophic event such as a fire, power loss, or telecommunications failure, we may be unable to continue our operations and may endure system interruptions, reputational harm, delays in development of our platform, lengthy interruptions in service, breaches of data security, and loss of critical data, all of which could have an adverse effect on our future operating results. For example, our corporate offices are located in California, a state that frequently experiences earthquakes. Additionally, all the aforementioned risks may be further increased if we do not implement a disaster recovery plan or our partners’ disaster recovery plans prove to be inadequate.

Failure to comply with governmental laws and regulations could harm our business.

Our business is subject to regulation by various federal, state, local and foreign governments. In certain jurisdictions, these regulatory requirements may be more stringent than those in the United States. Noncompliance with applicable regulations or requirements could subject us to investigations, sanctions, mandatory product recalls, enforcement actions, disgorgement of profits, fines, damages, civil and criminal penalties, injunctions or other collateral consequences. If any governmental sanctions are imposed, or if we do not prevail in any possible civil or criminal litigation, our business, operating results, and financial condition could be materially adversely affected. In addition, responding to any action will likely result in a significant diversion of management’s attention and resources and an increase in professional fees. Enforcement actions and sanctions could harm our business, reputation, operating results and financial condition.

Changes in laws or regulations relating to privacy or the protection or transfer of personal data, or any actual or perceived failure by us to comply with such laws and regulations or our privacy policies, could adversely affect our business.

Components of our business, including our platform, involve processing, storing, and transmitting confidential data, which is subject to our privacy policies and certain federal, state, and foreign laws and regulations relating to privacy and data protection. The amount of customer and employee data that we store through our platform, networks, and other systems, including personal data, is increasing. In recent years, the collection and use of personal data by companies have come under increased regulatory and public scrutiny.

For example, in the United States, protected health information is subject to the Health Insurance Portability and Accountability Act, or HIPAA. HIPAA has been supplemented by the Health Information Technology for Economic and Clinical Health Act with the result of increased civil and criminal penalties for noncompliance. Under HIPAA, entities performing certain functions and creating, receiving, maintaining, or transmitting protected health information provided by covered entities and other business associates are directly subject to HIPAA. If we have access to protected health information through our platform, we may be obligated to comply with certain privacy rules and data security requirements under HIPAA. Any systems failure or security breach that results in the release of, or unauthorized access to, personal data, or any failure or perceived failure by us to comply with our privacy policies or any applicable laws or regulations relating to privacy or data protection, could result in proceedings against us by governmental entities or others. Such proceedings could result in the imposition of sanctions, fines, penalties, liabilities, or governmental orders requiring that we change our data practices, any of which could have a material adverse effect on our business, operating results, and financial condition.

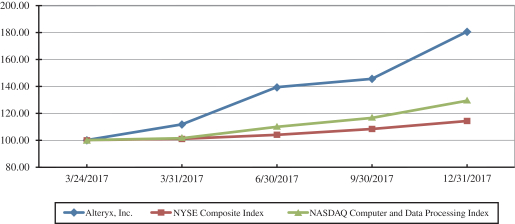

35