Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-258754

COTTONWOOD COMMUNITIES, INC.

SUPPLEMENT NO. 8 DATED MARCH 31, 2022

TO THE PROSPECTUS DATED NOVEMBER 4, 2021

This document supplements, and should be read in conjunction with, the prospectus of Cottonwood Communities, Inc. dated November 4, 2021, as supplemented by supplement no. 1 dated November 16, 2021, supplement no. 2 dated November 22, 2021, supplement no. 3 dated November 30, 2021, supplement no. 4 dated December 15, 2021, supplement no. 5 dated January 18, 2022, supplement no. 6 dated February 16, 2022 and supplement no. 7 dated March 15, 2022. As used herein, the terms “we,” “our” and “us” refer to Cottonwood Communities, Inc. and, as required by context, Cottonwood Residential O.P., LP, which we refer to as our “Operating Partnership” or “CROP,” and to their subsidiaries. Capitalized terms used in this supplement have the same meanings as set forth in the prospectus. The purpose of this supplement is to disclose:

| • | the status of this offering; |

| • | information regarding our portfolio; |

| • | information regarding our distributions; |

| • | information regarding repurchases; |

| • | information regarding fees and expenses payable to our advisor and its affiliates; |

| • | updated risks related to this offering; |

| • | information regarding compensation to our named executive officers; |

| • | updated information regarding related party transactions; |

| • | “Management’s Discussion and Analysis of Financial Condition and Results of Operations” similar to that filed in our Annual Report on Form 10-K for the year ended December 31, 2021; |

| • | updated experts information; and |

| • | our audited financial statements and the notes thereto as of and for the year ended December 31, 2021. |

Status of this Offering

As of March 31, 2022, we have raised gross proceeds of approximately $36.0 million from the sale of approximately 2.0 million shares in this offering, including proceeds from our distribution reinvestment plan of approximately $0.6 million. As of March 31, 2022, approximately $964.0 million in shares remain available for sale pursuant to this offering, including approximately $99.4 million in shares available for sale through our distribution reinvestment plan.

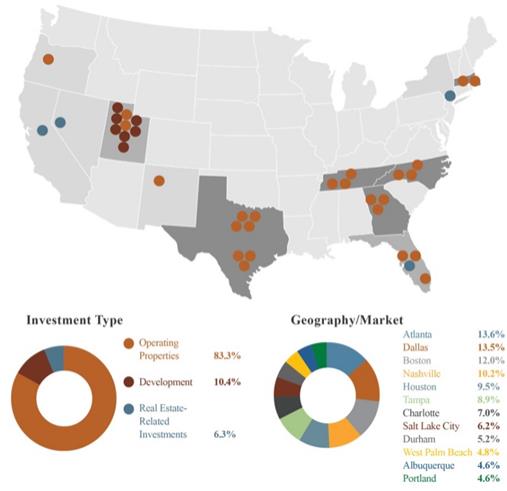

Real Estate Investments

As of December 31, 2021, we had a portfolio of $2.1 billion in total assets, with 83.3% of our equity value in operating properties, 10.4% in development and 6.3% in real estate-related investments. We also currently manage approximately 9,800 units in stabilized assets, including approximately 7,300 units in stabilized properties we own or have ownership interests in. The graphic below presents our real estate portfolio by market and investment type by fair value as of December 31, 2021. Refer to the section of this supplement titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Our Investments” for additional detail regarding our portfolio.

1

Table of Contents

Distribution Information

On March 22, 2022, our board of directors authorized a distribution for the month of March of 0.05916667, or $0.71 annually, reduced for any class-specific expense allocated to the class, for each class of our common stock to holders of record on March 31, 2022, to be paid in April 2022.

Refer to the section of this supplement titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources” for additional detail regarding our distributions paid for the year ended December 31, 2021.

Repurchases

During the year ended December 31, 2021, we received and repurchased in full eligible repurchase requests for 203,537 shares of Class A common stock for $2.6 million, at an average repurchase price of $12.90. We funded our repurchases with cash available from operations, financing activities and capital raising activities.

Fees and Expenses Payable to Our Advisor and its Affiliates

The table below provides information regarding fees and expenses paid to our advisor and its affiliates in connection with their services provided to us pursuant to the terms of the agreements with them in effect at such times. The table includes amounts incurred for the year ended December 31, 2021. We entered an amended and restated advisory agreement on May 7, 2021 at the effective time of our merger with Cottonwood Residential II, Inc. (the “CRII Merger”). The fees paid prior to May 7, 2021 were earned under our prior advisory agreement (amounts in thousands).

2

Table of Contents

| Year Ended December 31, 2021 | ||||

Form of Compensation | ||||

Operational Stage | ||||

Asset management fees(1) | $ | 8,052 | ||

Asset management fees waived by our advisor(2) | (27) | |||

Property management fee(3) | 151 | |||

Reimbursable operating expenses(4) | 331 | |||

Performance participation allocation(5) | 51,761 | |||

|

| |||

| $ | 60,268 | |||

| (1) | Under our advisory agreement in effect through May 6, 2021, we paid our advisor an annual asset management fee, paid monthly, in an amount equal to 1.25% per annum of our gross assets as of the last day of the prior month. Under the amended and restated advisory agreement entered May 7, 2021, our Operating Partnership pays our advisor a monthly management fee equal to 0.0625% of GAV (gross asset value of our Operating Partnership, calculated pursuant to our valuation guidelines and reflective of the ownership interest held by our Operating Partnership in such gross assets), subject to a cap of 0.125% of net asset value of our Operating Partnership. |

| (2) | In connection with our initial public offering, our advisor agreed to waive its asset management fee each month in an amount equivalent to the 6.0% discount provided to those who purchased Class A shares through certain distribution channels. This was to ensure that we received proceeds equivalent to those received for sales of shares outside of these channels. |

| (3) | Through May 7, 2021, we paid Cottonwood Communities Management, LLC (our subsidiary following the CRII Merger) a property management fee in an amount up to 3.5% of the annual gross revenues of our multifamily apartment communities that it manages. Cottonwood Communities Management, LLC could subcontract the performance of its property management duties to third parties and Cottonwood Communities Management, LLC would pay a portion of its property management fee to the third parties with whom it subcontracts for these services. |

| (4) | Under our advisory agreement in effect through May 7, 2021, we reimbursed our advisor or its affiliates for all actual expenses paid or incurred by our advisor or its affiliates in connection with the services provided to us; provided, however, that we did not reimburse our advisor or its affiliates for salaries, wages and related benefits of personnel who performed investment advisory services for us or served as our executive officers. Under the amended and restated advisory agreement entered into on May 7, 2021, subject to the limitations on total operating expenses, our advisor is entitled to reimbursement of all costs and expenses incurred by it or its affiliates on our behalf, provided that our advisor is responsible for the expenses related to any and all of our advisor’s personnel who provide investment advisory services pursuant to the amended and restated advisory agreement (including, without limitation, each of our executive officers and any directors who are also directors, officers or employees of our advisor or any of its affiliates), including, without limitation, salaries, bonuses and other wages, payroll taxes and the cost of employee benefit plans of such personnel, and costs of insurance with respect to such personnel; provided that we will be responsible for the personnel costs of our employees even if they are also directors or officers of our advisor or any of its affiliates except as provided for in the Reimbursement and Cost Sharing Agreement. |

| (5) | As of May 7, 2021, the “Special Limited Partner,” an affiliate of our advisor, is entitled to receive a 12.5% promotional interest, subject to a 5% hurdle and certain limitations, under the terms of the amended and restated limited partnership agreement of CROP as amended to date. The performance participation allocation is an annual distribution to be made following the end of each year and accrues on a monthly basis. On January 31, 2022, the accrued $51.8 million performance participation allocation was paid in cash to the Special Limited Partner. |

Risk Factors

The following risk factors supplement the risk factors and/or supersede and replace the similar risk factors contained in the prospectus and all similar disclosure in the prospectus.

We have paid distributions from offering proceeds. In the future we may continue to fund distributions with offering proceeds. To the extent we fund distributions from sources other than our cash flow from operations, we will have less funds available for investment in multifamily apartment communities and multifamily real estate-related assets and the overall return to our stockholders may be reduced.

Our charter permits us to make distributions from any source, including offering proceeds or borrowings (which may constitute a return of capital), and our charter does not limit the amount of funds we may use from any source to pay such distributions. We intend to make distributions on our common stock on a per share basis with each share receiving the same

3

Table of Contents

distribution, subject to any class-specific expenses such as distribution fees on our Class T and Class D shares. If we fund distributions from financings, our offerings or other sources, we will have less funds available for investment in multifamily apartment communities and other multifamily real estate-related assets and the number of real estate properties that we invest in and the overall return to our stockholders may be reduced. If we fund distributions from borrowings, our interest expense and other financing costs, as well as the repayment of such borrowings, will reduce our earnings and cash flow from operations available for distribution in future periods. If we fund distributions from the sale of assets or the maturity, payoff or settlement of multifamily real estate-related assets, this will affect our ability to generate cash flows from operations in future periods.

During the early stages of our operations, it is likely that we will use sources of funds, which may constitute a return of capital to fund distributions. During our offering stage, when we may raise capital more quickly than we acquire income-producing assets, and for some period after, we may not be able to make distributions solely from our cash flow from operations. Further, because we may receive income from our investments at various times during our fiscal year and because we may need cash flow from operations during a particular period to fund capital expenditures and other expenses, we expect that at least during the early stages of our existence and from time to time during our operational stage, we will declare distributions in anticipation of cash flow that we expect to receive during a later period and we will make these distributions in advance of our actual receipt of these funds. In addition, to the extent our investments are in development or redevelopment projects or in properties that have significant capital requirements, our ability to make distributions may be negatively impacted, especially during our early periods of operation. In these instances, we expect to look to third party borrowings to fund our distributions. We may also fund such distributions from the sale of assets. To the extent distributions exceed cash flow from operations, a stockholder’s basis in our stock will be reduced and, to the extent distributions exceed a stockholder’s basis, the stockholder may recognize capital gain.

For the years ended December 31, 2021 and 2020, we paid aggregate distributions to common stockholders and limited partnership unitholders of $20.2 million and $5.2 million, including $20.1 million and $4.1 million of distributions paid in cash and $0.1 million and $1.1 million of distributions reinvested through our distribution reinvestment plan, respectively. Our net loss for the years ended December 31, 2021 and 2020 was $106.9 million and $8.6 million. Cash flows provided by operating activities were $5.4 million for the year ended December 31, 2021 and cash flows used in operating activities was $2.8 million during the year ended December 31, 2020. We funded our total distributions paid during 2021, which includes net cash distributions and distributions reinvested by stockholders, with $11.0 million prior period cash provided by operating activities, $5.0 million from our revolving credit facility, and $4.0 million of offering proceeds. We funded our total distributions paid during 2020, which includes net cash distributions and distributions reinvested by stockholders, with $0.6 million prior period cash provided by operating activities and $3.6 million of offering proceeds.

Generally, for purposes of determining the source of our distributions paid, we assume first that we use cash flow from operating activities from the relevant or prior periods to fund distribution payments. To the extent that we pay distributions from sources other than our cash flow from operating activities, we will have less funds available for the acquisition of real estate investments, the overall return to our stockholders may be reduced and subsequent investors will experience dilution. In addition, to the extent distributions exceed cash flow from operating activities, a stockholder’s basis in our stock will be reduced and, to the extent distributions exceed a stockholder’s basis, the stockholder may recognize capital gain.

We have incurred net losses under GAAP in the past and may incur net losses in the future, and we have an accumulated deficit and may continue to have an accumulated deficit in the future.

For the years ended December 31, 2021 and 2020, we had consolidated net losses of $106.9 million and $8.6 million, respectively. As of December 31, 2021 and 2020, we had accumulated deficit of $55.9 million and $11.9 million, respectively. These amounts largely reflect the expense of real estate depreciation and amortization in accordance with GAAP, which was $63.4 million and $7.0 million during these periods. In addition, the year ended December 31, 2021, also included $51.8 million of charges related to the performance participation allocation.

Net loss and accumulated deficit are calculated and presented in accordance with GAAP, which, among other things, requires depreciation of real estate investments to be calculated on a straight-line basis. As a result, our operating results imply

4

Table of Contents

that the value of our real estate investments will decrease evenly over a set time period. However, we believe that the value of real estate investments will fluctuate over time based on market conditions. Thus, in addition to GAAP financial metrics, management reviews certain non-GAAP financial metrics, funds from operations, or FFO and Core FFO. FFO measures operating performance that excludes gains or losses from sales of depreciable properties, real estate-related depreciation and amortization and after adjustments for our share of consolidated and unconsolidated entities.

Our success is dependent on general market and economic conditions.

The real estate industry generally and the success of our investment activities in particular will both be affected by global and national economic and market conditions generally and by the local economic conditions where our properties are located. These factors may affect the level and volatility of real estate prices, which could impair our profitability or result in losses. In addition, general fluctuations in the market prices of securities and interest rates may affect our investment opportunities and the value of our investments. Our sponsor’s financial condition may be adversely affected by a significant economic downturn and it may be subject to legal, regulatory, reputational and other unforeseen risks that could have a material adverse effect on its businesses and operations (including our advisor).

A recession, slowdown and/or sustained downturn in the U.S. real estate market, and to a lesser extent, the global economy (or any particular segment thereof) would have a pronounced impact on us, the value of our assets and our profitability, impede the ability of our assets to perform under or refinance their existing obligations, and impair our ability to effectively deploy our capital or realize upon investments on favorable terms. We could also be affected by any overall weakening of, or disruptions in, the financial markets. Any of the foregoing events could result in substantial losses to our business, which losses will likely be exacerbated by the presence of leverage in our investments capital structures.

For example, during the financial crisis, the availability of debt financing secured by commercial real estate was significantly restricted as a result of a prolonged tightening of lending standards. Due to the uncertainties created in the credit market, real estate investors were unable to obtain debt financing on attractive terms, which adversely affected investment returns on acquisitions and their ability to even make acquisitions or tenant improvements to existing holdings. Any future financial market disruptions may force us to use a greater proportion of our offering proceeds to finance our acquisitions and fund tenant improvements, reducing the number of acquisitions we would otherwise make.

In addition, the recent invasion by the Russian Federation of the Ukraine on February 24, 2022 has caused a significant rise in geopolitical tensions and the United States, the United Kingdom and EU member states and other countries have imposed economic sanctions on the Russian Federation, parts of Ukraine, as well as various designated parties. As further military conflicts and economic sanctions continue to evolve, it has become increasingly difficult to predict the impact of these events or how long they will last. Depending on direction and timing, the Russian Federation-Ukraine conflict may significantly adversely affect economic and market conditions.

CROP may be subject to tax indemnification obligations upon the taxable sale of certain of its properties. CROP will not have control of the assets that will be subject to an in-kind redemption transaction under the CROP Tax Protection Agreement.

Pursuant to the tax protection agreement between CROP and High Traverse Holdings, LLC (“HT Holdings”), a Delaware limited liability company, which is beneficially owned by Daniel Shaeffer, Chad Christensen, Gregg Christensen and Eric Marlin, each of who are our executive officers and some of whom are our directors, (the “CROP Tax Protection Agreement”), CROP has agreed, until May 7, 2031, to indemnify HT Holdings (including Daniel Shaeffer, Chad Christensen, Gregg Christensen and Eric Marlin, as beneficial owners of HT Holdings, and their affiliated trusts and certain other entities) (collectively, the “protected partners”) against certain tax consequences of a taxable transfer of all or any portion of the properties that are owned by CROP or any of its subsidiaries as of the closing date of our merger with CROP, subject to certain conditions and limitations. These indemnification obligations could prevent CROP from selling its properties at times and on terms that are in the best interest of CROP, us and the respective equity owners of CROP and us and any indemnification payments that may become payable could be a significant expense for CROP and us. In addition, at any time after the closing

5

Table of Contents

(including after expiration of the tax protection term), each protected partner and CROP will have the right to exercise an in-kind redemption transaction (i.e., a redemption of all of the protected partner’s interest in CROP in exchange for one or more assets of CROP at the then-current market price). This would eliminate CROP’s indemnification obligations to the protected partner(s). The protected partners will have the right to select the assets of CROP necessary to effectuate the in-kind redemption transaction, subject to certain limitations. If an in-kind redemption transaction is effectuated, CROP’s portfolio may become less geographically diverse and thus subject to greater market risk, and CROP may be required to transfer some of its prime assets to the protected partner(s).

In addition, CROP has entered and may in the future into tax indemnification agreements with certain persons who contributed their interests in properties to CROP in exchange for CROP Common Units. These current agreements provide that CROP will indemnify such contributors against certain tax consequences of a taxable sale of the property contributed by such contributors through 2025, subject to certain conditions and limitations. Future tax indemnification agreements entered by CROP may extend such obligations beyond 2025. The obligations of CROP under these and future indemnification agreements may constrain CROP with respect to deciding to dispose of a particular property and may also result in financial obligations for us.

Holders of our preferred stock will have dividend, liquidation and other rights that are senior to the rights of the holders of our common stock.

We have classified and designated 12,800,000 shares of our authorized but unissued preferred stock as shares of non-voting Series 2019 preferred stock. In connection with the CRII Merger, we classified and designated 14,500,000 shares of our authorized but unissued preferred stock as shares of non-voting Series 2016 preferred stock, and designated 5,000,000 shares of our authorized but unissued preferred stock as shares of non-voting Series 2017 preferred stock. We issued one share of our Series 2016 preferred stock for each share of CRII Series 2016 preferred stock outstanding prior to the effective time of the CRII Merger and one share of Series 2017 preferred stock for each share of CRII Series 2017 preferred stock outstanding prior to the effective time of the CRII Merger.

The outstanding shares of our Series 2019 preferred stock are entitled to receive a preferred dividend equal to a 5.5% (subject to an increase to 6.0% in certain circumstances) per annum cumulative but not compounded return. The outstanding shares of our Series 2016 preferred stock are entitled to receive a preferential dividend equal to a 7% cumulative but not compounded annual return. The outstanding shares of our Series 2017 preferred stock are entitled to receive a preferential dividend equal to a 7.5% cumulative but not compounded annual return (subject to an increase to 8% in certain circumstances). As of March 22, 2022, we had 13,983,810 shares of our Series 2016 preferred stock outstanding, which was issued in connection with the CRII Merger and 12,733,485 shares of Series 2019 preferred stock outstanding. We had no Series 2017 preferred stock outstanding.

Holders of the Series 2016 preferred stock and Series 2019 preferred stock are entitled to cumulative dividends before any dividends may be declared or set aside on our common stock, or the redemption of our common stock and a liquidation preference of $10.00 per share plus any accrued and unpaid distributions before any payment is made to holders of our common stock upon our voluntary or involuntary liquidation, dissolution or winding up. This will reduce the remaining amount of our assets, if any, available to distribute to holders of our common stock.

Military conflict may affect the markets in which we operate, our operations and our profitability.

The Russian Federation invaded Ukraine on February 24, 2022. Geopolitical tensions have risen significantly in response and the United States, the United Kingdom, EU member states, and other countries have imposed economic sanctions on the Russian Federation, parts of Ukraine, as well as various designated parties. As further military conflicts and economic sanctions continue to evolve, it has become increasingly difficult to predict the impact of these events or how long they will last. Depending on direction and timing, the Russian Federation-Ukraine conflict may significantly exacerbate the normal risks associated with an investment in real estate and result in adverse changes to, among other things: (i) general economic and market conditions; (ii) shipping and transportation costs and supply chain constraints; (iii) interest rates, currency exchange rates, and expenses associated with currency management transactions; (iv) demand for real estate; (v) available credit in

6

Table of Contents

certain markets; (vi) import and export activity from certain markets; and (vii) laws, regulations, treaties, pacts, accords, and governmental policies. Economic and military sanctions related to the Russian Federation-Ukraine conflict, or other conflicts, have the potential to gravely impact markets, global supply and demand, import/export policies, and the availability of labor in certain markets. There is no guarantee that such sanctions and economic actions will abate or that more restrictive measures will not be put in place in the near term. Moreover, it is expected that the Russian Federation-Ukraine military conflict could spark further sanctions and/or military conflicts which will impact other regions. The foregoing could impact our operations and our ability to realize out investment objectives.

Rent control and other changes in applicable laws, or noncompliance with applicable laws, could adversely affect our portfolio of residential properties.

Lower revenue growth or significant unanticipated expenditures may result from changes in rent control or rent stabilization laws or other residential landlord/tenant laws. Municipalities may implement, consider or be urged by advocacy groups to consider rent control or rent stabilization laws and regulations or take other actions that could limit our ability to raise rents based on market conditions. For example, in 2016 in Mountain View, California, voters passed a referendum that limits rent increases on existing tenants (but not on new move-ins) in communities built before 1995. These initiatives and any other future enactments of rent control or rent stabilization laws or other laws regulating residential housing, as well as any lawsuits against us arising from such rent control or other laws, may reduce rental revenues or increase operating costs. Such laws and regulations may limit our ability to charge market rents, increase rents, evict tenants or recover increases in our operating costs and could make it more difficult for us to dispose of properties in certain circumstances. Expenses associated with investments in residential properties, such as debt service, real estate taxes, insurance and maintenance costs, are generally not reduced when circumstances cause a reduction in rental income from such properties.

Our multifamily apartment communities and multifamily real estate-related assets may be cross-collateralized.

At December 31, 2021, we had $213.0 million of fixed rate debt and $543.7 million of variable rate debt, including our revolving credit facility and including $116.7 million of variable rate debt related to construction loans; $407.0 million, or 74.9% of our variable rate debt is accompanied by interest rate cap hedging instruments as required by the lenders. In addition, CROP has issued unsecured promissory notes in several private placement offerings, in an aggregate amount of $43.5 million at December 31, 2021. We may obtain additional lines of credit or other debt financing, or take additional advances on our existing lines of credit, which we may utilize to acquire multifamily apartment communities and multifamily real estate-related assets and fund our operations. Thus, our assets may be cross-collateralized. Information about the amount and terms of any new lines of credit are uncertain and will be negotiated by our officers. No assurance can be given that future cash flow will be sufficient to make the debt service payments on any loans and to cover all operating expenses.

If our revenues are insufficient to pay debt service and operating costs, we may be required to seek additional working capital. There can be no assurance that such additional funds will be available. The degree to which we are leveraged could have an adverse impact on us, including (i) increased vulnerability to adverse general economic and market conditions, (ii) impaired ability to expand and to respond to increased competition, (iii) impaired ability to obtain additional financing for future working capital, capital expenditures, general corporate or other purposes and (iv) requiring that a significant portion of cash provided by operating activities be used for the payment of debt obligations, thereby reducing funds available for operations and future business opportunities.

Increases in interest rates and the future discontinuation of LIBOR could increase the amount of our interest payments and could reduce the amount of distributions our shareholders receive.

At December 31, 2021, we had $543.7 million of variable rate debt, including our revolving credit facility and including $116.7 million of variable rate debt related to construction loans; $407.0 million, or 74.9% of our variable rate debt is accompanied by interest rate cap hedging instruments as required by the lenders. We may incur additional indebtedness in the future. Interest we pay reduces our cash flows. Since we have incurred and may continue to incur variable rate debt, increases

7

Table of Contents

in interest rates raise our interest costs, which reduces our cash flows. In addition, if we need to repay existing debt during periods of rising interest rates, we could be required to sell one or more of our properties at times or on terms which may not permit realization of the maximum return on such investments. Increases in interest rates may cause our operations to suffer and the amount of distributions our shareholders receive and their overall return on investment may decline.

We currently pay interest under our variable rate debt at an interest rate that is determined based on a US Dollar London Interbank Offered Rate (“LIBOR”). In July 2017, the United Kingdom’s Financial Conduct Authority (the “FCA”), which regulates LIBOR, announced that it will stop encouraging or requiring banks to submit rates for the calculation of LIBOR after December 31, 2021. On March 5, 2021, the FCA announced that all LIBOR settings will either cease to be provided by any administrator or no longer be representative (i) immediately after December 31, 2021, in the case of the 1-week and 2-month US dollar settings; and (ii) immediately after June 30, 2023, in the case of the remaining US dollar settings. The tenors that were extended to June 30, 2023 are more widely used and are the tenors used in our LIBOR-based debt.

The Alternative Reference Rates Committee (“ARRC”), a steering committee comprised of U.S. financial market participants, published model LIBOR replacement language for use in bilateral and syndicated loan facilities. ARRC selected the Secured Overnight Financing Rate (“SOFR”) as the replacement to LIBOR. SOFR is a broad measure of the cost of borrowing cash in the overnight U.S. treasury repo market and is a rate published by the Federal Reserve Bank of New York. Our variable rate note remains indexed to LIBOR and not SOFR and includes LIBOR transition language that generally aligns with ARRC recommendations. The transition from LIBOR to SOFR could result in higher all-in interest costs and could reduce the amount of distributions to our shareholders.

Management Compensation

The following discussion supplements the disclosure regarding executive compensation contained in the prospectus.

This section discusses the components of the compensation we provide to our “named executive officers” who are listed in the “Summary Compensation Table” below. In 2021, our named executive officers were Daniel Shaeffer, our Chief Executive Officer; Gregg Christensen, our Chief Legal Officer and Secretary; and Glenn Rand, our Chief Operating Officer.

Prior to the effective time of the CRII Merger on May 7, 2021, we had no employees, and all of our executive officers were employed by our advisor and its affiliates. As such, all of our executive officers were compensated by these entities, in part, for their services to us and our subsidiaries, and except for grants of equity incentive compensation that we made commencing with the fiscal year 2020, we did not provide compensation to our executive officers prior to May 7, 2021.

Following the CRII Merger, we employ certain of our executive officers, including two of our named executive officers, Mr. G. Christensen and Mr. Rand. Because we employed certain of our executive officers for less than a full year in 2021, the discussion below regarding executive compensation reflects the compensation approved by our compensation committee that we expect to pay for a full year commencing in 2022 with our executive compensation tables reflecting only those amounts paid in 2021.

Mr. Shaeffer, along with certain other of our executive officers, continues to be employed by our advisor and its affiliates. Except for grants of equity incentive compensation that we make to all of our executive officers, Mr. Shaeffer and those executive officers employed by our advisor and its affiliates are compensated by these entities (and not us), in part, for their service to us and our subsidiaries. See “Fees and Expenses Payable to Our Advisor and its Affiliates” above and “Compensation” in the prospectus for a discussion of the fees paid to our advisor and its affiliates. All of our named executive officers are officers and/or employees of, or hold an indirect ownership interest in, our advisor and/or its affiliates.

We are a “smaller reporting company” as defined in Rule 12b-2 under the Exchange Act and an “emerging growth company” as defined under the JOBS Act. As such, we are permitted to take advantage of certain reduced reporting requirements that are otherwise applicable generally to public companies.

8

Table of Contents

Compensation of Executive Officers

Executive Compensation Process

Our compensation committee, which is composed of all of our independent directors, discharges our board of directors’ responsibilities relating to the compensation that we pay to our named executive officers. This includes equity incentive compensation grants we make to all of our executive officers as well as additional compensation we pay to those named executive officers employed by us. Prior to the CRII Merger, except for annual grants of LTIP Units and Special LTIP Units (for purposes of our executive compensation discussion, referred to as required by context, collectively as the “LTIP Units”) under our partnership agreement in effect at the time of the award, our named executive officers did not receive any compensation from us.

Our compensation committee acknowledges that the real estate industry is highly competitive and that experienced professionals have significant career mobility. Commencing with fiscal year 2020, our compensation committee determined that through the annual grant of LTIP Units under our partnership agreement, we will attract, motivate and retain highly skilled executive officers who are committed to our core values of prudent risk-taking and integrity. Each year our compensation committee determines, in its sole discretion, the aggregate amount, type and terms of any equity grants to our executive officers, including our employees and employees of our advisor and its affiliates. For the initial grants of LTIP Units in 2020 our compensation committee consulted Ferguson Partners Consulting L.P., f/k/a FPL Associates, L.P. (“FPC”), a nationally recognized compensation consulting firm specializing in the real estate industry.

In making initial compensation decisions following the CRII Merger, the compensation committee reviewed market-based compensation data provided by FPC. The compensation committee also evaluated the performance of our Chief Executive Officer and, together with our Chief Executive Officer, assessed the individual performance of the other executive and senior officers. While the compensation committee considers these recommendations, along with data provided by its other advisors, it retains full discretion to set all compensation to our named executive officers that we pay directly.

Engagement of Compensation Consultant

The compensation committee is authorized to retain the services of one or more executive compensation consultants, in its discretion, to assist with the establishment and review of our compensation programs and related policies. The compensation committee has sole authority to hire, terminate and set the terms of any future engagement of FPC or any other compensation consultant.

For compensation advice following the CRII Merger, the compensation committee engaged FPC to provide market-based compensation data to assist the committee in the implementation of a comprehensive executive compensation program for those executive officers that we employ and an equity incentive compensation program for all of our executive officers that complements the compensation provided to our executive officers by our advisor and its affiliates. In connection with these efforts, FPC prepared for the compensation committee reports that included compensation analyses for each executive position, including those executive positions that are held by employees of our advisor and its affiliates, an analysis of a recommended peer group for the company and a description of the methodology used to provide the compensation analyses. FPC researched competitive market practices, reviewed the proxy statements of its recommended peer group and checked its own proprietary information data bases. The compensation committee reviewed the information provided to the company and approved the executive compensation program which included equity incentive compensation for all of our executive officers and full compensation for those executive officers that we employ.

9

Table of Contents

Components of Executive Compensation

The key elements of our executive compensation program for our executive officers include annual cash compensation, short-term incentive plan compensation as well as equity incentive compensation in the form of time-based and performance-based LTIP Units. Each element is discussed in detail below.

Base Salary. Compensation for each executive officer we employ was established by our compensation committee. We believe that our executive officers’ base salary levels are commensurate with their positions and are expected to provide a steady source of income sufficient to permit these officers to focus their time and attention on their work duties and responsibilities. Base salaries of our named executive officers periodically will be reviewed by the compensation committee. Information about base salary for our named executive officers for 2022 is as follows.

Name and Principal Position | Base Salary | |||

Daniel Shaeffer, Chief Executive Officer | (1) | |||

Gregg Christensen, Chief Legal Officer and Secretary | $ | 400,000 | ||

Glenn Rand, Chief Operating Officer | $ | 400,000 | ||

| (1) | Mr. Shaeffer, along with certain other of our executive officers, is employed by our advisor and its affiliates. Except for grants of equity incentive compensation that we make to all of our executive officers, Mr. Shaeffer is compensated by these entities, in part, for his service to us and our subsidiaries. See “Fees and Expenses Payable to Our Advisor and its Affiliates” above for a discussion of the fees paid to our advisor and its affiliates for the year ended December 31, 2021. |

Short-Term Incentive Plan. The short-term incentive plan is intended to compensate our executive officers for achieving annual company and strategic performance goals. The compensation committee believes that the opportunity to earn an annual cash bonus encourages our executive officers to achieve company and strategic performance goals, which fosters a performance-driven company culture that aligns the executives’ interests with the stockholders’ interests.

The short-term incentive plan allows our executive officers to earn a cash bonus based on various pre-defined and pre-weighted company and strategic performance goals established by the compensation committee (at least 50% of which are objective, calculable company performance measurements). Strategic performance goals are assessed subjectively.

The annual cash incentive bonus is the product of the named executive officer’s target bonus (which is a percentage of his base salary) and a formula number that is based on the achievement of predetermined targets. Depending on the achievement of the predetermined targets, the actual annual cash incentive bonus may be less than, but not greater than the target bonus. The compensation committee set Mr. G. Christensen’s target bonus at 90% of his base salary and Mr. Rand’s target bonus at 85% of his base salary.

The annual cash incentive bonus formula number for 2021 consists of the following components: (i) 25% capital formation, (ii) 25% capital deployment efficiency, (iii) 25% portfolio characteristics and objectives, (iv) 15% same store net operating income (NOI) growth relative to the same store NOI growth of a pre-selected peer group, and (v) 10% completion of development projects. With respect to the specific formula components for 2021, the named executive officers received 93% of their target bonus based on the achievement of the predetermined targets.

Equity Incentive Compensation. The compensation committee has made and may make certain awards to the named executive officers in the form of LTIP units. LTIP units are a separate series of limited partnership units of our Operating Partnership, which are convertible into common units upon achieving certain vesting and performance requirements. Awards of LTIP units are subject to the conditions and restrictions determined by our compensation committee, including continued employment or service, computation of financial metrics and/or achievement of pre-established performance goals and objectives. If the conditions and/or restrictions included in an LTIP unit award agreement are not attained, holders will forfeit the LTIP units granted under such agreement. Unless otherwise provided, the LTIP unit awards (whether vested or unvested) will entitle the holder to receive current distributions from our Operating Partnership, and the Special LTIP units (whether vested or unvested) will entitle the holder to receive 10% of the current distributions from our Operating Partnership during the applicable performance period. When the LTIP units have vested and sufficient income has been allocated to the holder of the vested LTIP units, the LTIP units will automatically convert to common units in our Operating Partnership on a one-for-one basis.

10

Table of Contents

The compensation committee has deemed LTIP unit awards to be an effective means to ensure alignment of the executives’ interests with those of the stockholders. LTIP units are structured as “profits interests” for U.S. federal income tax purposes, and we do not expect the grant, vesting or conversion of LTIP units to produce a tax deduction for us based on current U.S. federal income tax law. As profits interests, the LTIP units initially will not have full parity, on a per unit basis, with the common units with respect to liquidating distributions. Upon the occurrence of specified events, the LTIP units can, over time, achieve full parity with the common units in our Operating Partnership and therefore, accrete to an economic value for the holder equivalent to the common units. If such parity is achieved, the LTIP units may be converted, subject to the satisfaction of applicable vesting conditions, on a one-for-one basis into common units, which in turn may be exchanged, upon the occurrence of certain events, by the holder for a cash amount based on the value of a share of our common stock or for shares of our common stock, on a one-for-one basis, at our election. However, there are circumstances under which the LTIP units will not achieve parity with the common units, and until such parity is reached, the value that a holder could realize for a given number of LTIP units will be less than the value of an equal number of shares of our common stock and may be zero. The compensation committee believes that this characteristic of the LTIP units, that they achieve real value only if our share value appreciates, links executive compensation to our performance.

Our compensation committee has approved grants of LTIP units to certain executive officers for fiscal year 2020 and 2021; however, none of our named executive officers received a grant of LTIP units from our compensation committee for 2021 compensation and none have outstanding equity awards as of December 31, 2021.

Our compensation committee currently expects to continue to grant LTIP units awards to our named executive officers annually on the same terms and conditions; however, the committee’s decision whether to approve any such awards in the future will depend on our performance, market trends and practices and other considerations.

Time-Based LTIP Units. The following table sets forth the number and value of the time-based LTIP Units granted to our named executive officers in January 2022. The time-based LTIP Units were issued on January 7, 2022 based on the grant date fair value determined in accordance with the Financial Accounting Standards Board’s Accounting Standards Codification 718, Compensation—Stock Compensation (“ASC Topic 718”). The time-based LTIP Units vest annually in equal installments over a four-year period with the first 25% vesting on January 1, 2023, subject to continued service. Time based LTIP Units (whether vested or unvested) receive the same distribution per unit as the CROP Common Units.

Executive Officer | Date of Grant | Number of Time- Based LTIP Units | Value of Time-Based LTIP Units | |||||||

Daniel Shaeffer | January 7, 2022 | 23,589 | $ | 407,710 | ||||||

Gregg Christensen | January 7, 2022 | 7,959 | $ | 137,563 | ||||||

Glenn Rand | January 7, 2022 | 6,201 | $ | 107,177 | ||||||

Performance-Based LTIP Units. The following table sets forth the number and value of the performance-based LTIP Units granted to our named executive officers in January 2022. The performance-based LTIP Units were issued on January 7, 2022 based on the grant date fair value determined in accordance with ASC Topic 718. The actual amount of each award will be determined at the conclusion of the three-year performance period on December 31, 2024, and will depend on our internal rate of return (as defined in the award agreements).

Executive Officer | Date of Grant | Number of Performance-Based LTIP Units | Value of Performance-Based LTIP Units | |||||||

Daniel Shaeffer | January 7, 2022 | 43,809 | $ | 757,190 | ||||||

Gregg Christensen | January 7, 2022 | 14,780 | $ | 255,456 | ||||||

Glenn Rand | January 7, 2022 | 11,517 | $ | 199,059 | ||||||

11

Table of Contents

Pursuant to the terms of the applicable award agreements, our named executive officers may earn up to 100% of the number of performance-based LTIP Units granted, plus deemed dividends on earned units, based on our internal rate of return during the performance period in accordance with the following schedule, with linear interpolation for performance between levels:

Internal Rate of Return | Percentage Earned | |||

Less than 6% | — | % | ||

6% | 50 | % | ||

10% or greater | 100 | % | ||

None of the performance-based LTIP Units will be earned if our internal rate of return for the performance period is less than 6%, and the maximum number of performance-based LTIP Units will only be earned if our internal rate of return for the performance period is 10% or greater. The earned performance-based LTIP Units will become fully vested on the first anniversary of the last day of the performance period, subject to continued employment with us, or our advisor or its affiliates. During the performance period, performance based LTIP Units (whether vested or unvested) will entitle the holder to receive 10% of the current distribution per unit paid to holders of the CROP Common Units (based on the total number of performance-based LTIP Units granted). At the end of the performance period, if the internal rate of return equals or exceeds the performance threshold (6%), the holder will be entitled to receive an additional grant of LTIP Units equivalent to 90% of distributions that would have been paid on the earned performance-based LTIP Units during the performance period.

Executive Officer Compensation Tables

Summary Compensation Table

The following table sets forth the information required by Item 402 of Regulation S-K promulgated by the SEC. Prior to the effective time of the CRII Merger on May 7, 2021, we had no employees, and all of our executive officers were employed by our advisor and its affiliates. As such, all of our executive officers were compensated by these entities, in part, for their services to us and our subsidiaries and except for grants of equity incentive compensation that we made to certain of our executive officers commencing for the fiscal year 2020, we did not compensate our executive officers prior to May 7, 2021. Therefore, the table below reflect executive compensation that we paid for the partial year commencing May 7, 2021.

Name and Principal Position | Year | Salary | Non-Equity Incentive Plan Compensation | Total | ||||||||||

Daniel Shaeffer | 2021 | (1) | (1) | (1) | ||||||||||

Gregg Christensen | 2021 | $ | 375,000 | $ | 315,000 | $ | 690,000 | |||||||

Glenn Rand | 2021 | $ | 380,000 | $ | 250,000 | $ | 630,000 | |||||||

| (1) | Mr. Shaeffer is an officer and employee of our advisor and its affiliates, and is compensated by these entities, in part, for his services to us or our subsidiaries. We do not directly compensate Mr. Shaeffer other than through stock awards. See “Fees and Expenses Payable to Our Advisor and its Affiliates” above for a discussion of the fees paid to our advisor and its affiliates for the year ended December 31, 2021. |

Termination and Change in Control Arrangements

Accelerated Vesting of Time-Based LTIP-Units. Pursuant to award agreements with our named executive officers, upon a “change in control” (as defined in the award agreements) or in the event of a termination of the executive officer’s employment by the executive officer for “good reason” (as defined in the award agreements), by the company without “cause” (as defined in the award agreements), or by reason of death or disability, all outstanding time-based LTIP Units will become fully vested.

Accelerated Vesting of Performance-Based LTIP-Units. Pursuant to the terms of award agreements with our named executive officers, upon a “change in control” (as defined in the award agreements) or in the event of a termination of the executive officer’s employment by the executive officer for “good reason” (as defined in the award agreements), by the

12

Table of Contents

company without “cause” (as defined in the award agreements), or by reason of death or disability (each a “Qualified Termination”), after the grant date, but prior to the end of the performance period, the target number of award LTIP Units shall be deemed earned. Upon a Qualified Termination after the end of the performance period, but prior to the vesting of the earned LTIP Units, all unvested earned LTIP Units will become fully vested.

Director Compensation

The following discussion supplements, and supersedes and replaces as appropriate, the disclosure regarding director compensation contained in the prospectus.

Following the CRII Merger, our compensation committee undertook a review of our director compensation and approved a revised compensation structure for our independent directors. The revised compensation structure was approved following a review of peer board compensation data provided FPC.

Annually, with a prorated amount for 2021 based on three quarters, we will pay a cash retainer of $50,000 to each independent director for their service as a director, as well as an equity grant of time-based LTIP Units in the Operating Partnership with a value of approximately $85,000 at the time of grant. The equity will have a one-year vesting schedule. The independent board members serving as chairperson of each of the audit, compensation and conflicts committees will receive an additional annual cash retainer of $15,000, $10,000 and $10,000, respectively.

Previously, each independent director received an annual retainer of $10,000 and we paid independent directors for attending board and committee meetings as follows, (i) $500 in cash for each board meeting attended (including if by teleconference); and (ii) $500 in cash for each committee meeting attended (if at a different time or place than a board meeting and including if by teleconference).

We also reimburse our directors for their travel expenses incurred in connection with their attendance at board and committee meetings.

In addition, in 2020, the special committee of our board of directors (the “Special Committee”) was formed for the purpose of reviewing, considering, investigating, evaluating and, as determined by the Special Committee, negotiating the Mergers or any alternative extraordinary transaction. The members of the Special Committee were Gentry Jensen, R. Brent Hardy and John Lunt, with Gentry Jensen serving as the chairman of the Special Committee. Effective on the closing date of the CRII Merger, R. Brent Hardy and Gentry Jensen resigned from the board of directors. In 2021, we paid each member of our special committee a $70,000 retainer for their service on the special committee.

The table below provides information regarding compensation paid to or earned by our directors during the year ended December 31, 2021 as required by Item 402(k) of Regulation S-K.

Name | Fees Earned or Paid in Cash | Stock Awards(1)(2) | Total | |||||||||

Daniel Shaeffer(3) | $ | — | $ | — | $ | — | ||||||

Chad Christensen(3) | $ | — | $ | — | $ | — | ||||||

Jonathan Gardner | $ | 37,500 | $ | 65,074 | $ | 102,574 | ||||||

John Lunt | $ | 121,750 | $ | 65,074 | $ | 186,524 | ||||||

Philip White | $ | 37,500 | $ | 65,074 | $ | 102,574 | ||||||

Gentry Jensen(4) | $ | 73,000 | $ | — | $ | 73,000 | ||||||

R. Brent Hardy(4) | $ | 73,000 | $ | — | $ | 73,000 | ||||||

| (1) | As of December 31, 2021, each of Mr. Gardner, Mr. Lunt and Mr. White held 3,765 unvested LTIP units. |

| (2) | Represents 3,765 LTIP units granted to each of Messrs. Gardner, Lunt, and White on January 7, 2022 for compensation for the year ended December 31, 2021. The dollar value is computed in accordance with the Financial Accounting Standards Board’s Accounting Standards Codification 718, Compensation—Stock Compensation (“ASC Topic 718”). See Note 11 to our consolidated financial statements included in our financial statements for the year ended December 31, 2021 included herein, for a discussion of our accounting of LTIP units and the assumptions used. The grant date fair value of each award granted on January 7, 2022 was $17.2839. |

| (3) | Directors who are not independent of us do not receive compensation for their services as a director. |

13

Table of Contents

| (4) | Effective on the closing date of the CRII Merger, R. Brent Hardy and Gentry Jensen, two of our former independent directors, resigned from the board of directors. |

Equity Compensation Plans

As of December 31, 2021, we have granted LTIP Units to certain of our executive officers and registered persons associated with the dealer manager for our public offering. The following table summarizes information, as of December 31, 2021, relating to our equity compensation plans pursuant to which we have granted LTIP units.

Plan Category | Number of securities to be issued upon exercise of outstanding options, warrants and rights(1) | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plans (2) | |||||||||

Equity compensation plans approved by security holders | — | — | — | |||||||||

Equity compensation plans not approved by security holders (3) | 1,099,775 | — | — | |||||||||

|

|

|

|

|

| |||||||

Total | 1,099,775 | — | — | |||||||||

|

|

|

|

|

| |||||||

| (1) | Consists entirely of LTIP units that, upon the satisfaction of certain conditions, are convertible into common units, which may then be redeemed for cash, or at our option, an equal number of shares of common stock, subject to certain restrictions. There is no exercise price associated with LTIP units. |

| (2) | No additional securities have been reserved for issuance. |

| (3) | Our board of directors has granted awards of LTIP units to our executive officers pursuant to the terms of award agreements and as contemplated in the operating partnership agreement for CROP. |

Stock Ownership of Certain Beneficial Owners and Management

The following disclosure supersedes and replaces the disclosure regarding stock ownership of certain beneficial owners and management contained in the prospectus.

The following table sets forth, as of March 31, 2022, the amount of our common stock, CROP’s common units and CROP’s LTIP units beneficially owned (unless otherwise indicated) by (i) any person who is known by us to be the beneficial owner of more than 5% of the outstanding shares of our common stock, (ii) our directors, (iii) our executive officers and (iv) all of our directors and executive officers as a group. Beneficial ownership is determined in accordance with the rules of the SEC and includes securities that a person has the right to acquire within 60 days.

14

Table of Contents

Name and Address of Beneficial Owner(1) | Amount and Nature of Beneficial Ownership (2) | Percent of all Shares (3) | Percent of all Shares and Common Units (4) | |||||||||

Daniel Shaeffer | 4,283,211 | (5) | 16.87 | % | 7.62 | % | ||||||

Chad Christensen | 4,283,211 | (5) | 16.87 | % | 7.62 | % | ||||||

Gregg Christensen | 3,850,024 | (5) | 15.16 | % | 6.85 | % | ||||||

Glenn Rand | 58,225 | (6) | * | * | ||||||||

Enzio Cassinis | 50,607 | (6) | * | * | ||||||||

Adam Larson | 39,069 | (6) | * | * | ||||||||

Paul Fredenberg | 18,412 | (6) | * | * | ||||||||

Susan Hallenberg | 50,509 | (6) | * | * | ||||||||

Stan Hanks | 41,938 | (6) | * | * | ||||||||

Eric Marlin | 3,567,178 | (5) | 14.05 | % | 6.34 | % | ||||||

Jonathan Gardner | 10,625 | (7) | * | * | ||||||||

John Lunt | 8,683 | (7) | * | * | ||||||||

Philip White | 20,865 | (8) | * | * | ||||||||

All directors and executive officers as a group (13 persons) | 5,797,682 | 22.83 | % | 10.31 | % | |||||||

| * | Indicates less than 1% of the outstanding common stock. |

| (1) | The address of each named beneficial owner is 1245 Brickyard Road, Suite 250, Salt Lake City, Utah 84106. |

| (2) | Ownership consists of shares of our common stock, CROP common units and CROP LTIP units. Subject to certain restrictions, common units may be redeemed for cash, or at our option, an equal number of shares of our common stock. Upon achieving parity with the common units and becoming “redeemable” in accordance with the terms of CROP’s partnership agreement, LTIP units may be redeemed for cash, or at our option, an equal number of shares of our common stock, subject to certain restrictions. |

| (3) | Based on 25,394,008 shares of our common stock outstanding as of March 14, 2022. In computing the percentage ownership of a person or group, we have assumed that the common units and LTIP units held by that person or persons in the group have been redeemed for shares of our common stock and that those shares are outstanding, but that no common units or LTIP units held by other persons are redeemed for shares of our common stock, notwithstanding that not all of the LTIP units have vested to date. |

| (4) | Based on 56,242,685 shares of common stock and common units outstanding as of March 14, 2022 on a fully-diluted basis, comprised of 25,394,008 shares of common stock and 30,848,677 shares of common stock issuable upon exchange or conversion of outstanding common units and LTIP units, respectively. |

| (5) | Includes 93,963, 93,963, 43,850 and 31,339 common units held by each of Messrs. Shaeffer, C. Christensen, G. Christensen and Marlin, respectively, and 687,743, 687,743, 304,669 and 54,334 LTIP units held by each of Messrs. Shaeffer, C. Christensen, G. Christensen and Marlin, respectively. Not all of the LTIP units have vested. Includes 3,481,505 common units held by HT Holdings, an entity owned and controlled by Messrs. Shaeffer, C. Christensen, G. Christensen and Marlin. Also includes 20,000 shares of common stock held by CCA, which is beneficially owned by Messrs. Shaeffer, C. Christensen, G. Christensen and Marlin (through entities they own and control or directly). In addition, Messrs. Shaeffer, C. Christensen and G. Christensen comprise the board of managers of CCA and, as such, may be deemed to have had beneficial ownership of the shares held by CCA. |

| (6) | Includes 3,633, 18,814, 12,543, 7,840, 3,633 and 3,633 common units held by each of Messrs. Rand, Cassinis, Larson, Fredenberg and Hanks and Ms. Hallenberg, respectively, and 54,592, 31,793, 26,526, 10,572, 38,305 and 46,876 LTIP units held by each of Messrs. Rand, Cassinis, Larson, Fredenberg and Hanks and Ms. Hallenberg, respectively. Not all of the LTIP units have vested. |

| (7) | Includes 10,265 and 8,683 LTIP units held by Messrs. Gardner and Lunt, respectively. Not all of the LTIP units have vested. |

| (8) | Includes 10,600 shares of our common stock and 10,265 LTIP units held by Mr. White. Not all of the LTIP units have vested. |

Related Party Transactions

The following discussion supplements the disclosure in the prospectus regarding other related party transactions.

Cottonwood Multifamily Opportunity Fund, Inc.

Cottonwood Capital Property Management II, LLC (“CCPMII”), a wholly owned subsidiary of CROP, acts as the sponsor, property manager and asset manager for Cottonwood Multifamily Opportunity Fund, Inc. (“CMOF”). Daniel Shaeffer, Chad Christensen and Gregg Christensen are each officers and directors of CMOF. Daniel Shaeffer and Chad Christensen are our affiliated directors and two of our executive officers. Gregg Christensen is one of our executive officers. As the property manager and asset manager for CMOF, CCPMII receives compensation for the acquisition, management and disposition of CMOF’s assets. Total compensation paid to CCPMII as the asset manager of CMOF for the years ended December 31, 2021 and December 31, 2020 were $0.8 million and $0.8 million, respectively. We did not receive fees from CMOF until our acquisition of CCPMII at the closing of our merger with CROP on May 7, 2021.

15

Table of Contents

In addition, prior to the CRII Merger, CROP had made three investments through separate joint ventures with CMOF as follows: Park Avenue Joint Venture (development project), Broadway Joint Venture (development project) and Block C Joint Venture (land held for development) with a percentage ownership interest by CROP as of December 31, 2021 of 23.56%, 18.84%), and 37.02%, respectively, and the balance of a majority of the remaining interest held indirectly by CMOF. None of the joint ventures had any operating activity or distributions from inception through December 31, 2021.

Compensation to Executive Officers and Affiliated Directors

As of the effective time of the CRII Merger, we employ certain of our executive officers, including Gregg Christensen, the brother of Chad Christensen, our Executive Chairman of the Board. As our Chief Legal Officer, Mr. G. Christensen receives an annual base salary of $375,000 and received a discretionary bonus of $315,000. In addition, Mr. G. Christensen participates in our general welfare plans and we expect him to participate in annual equity incentive awards grants to our officers as to be determined by our compensation committee.

On January 7, 2022, our compensation committee approved grants of LTIP Units from the Operating Partnership for fiscal year 2022 to our executive officers and certain of our employees. The compensation committee approved awards of time-based LTIP Units to our executive officers in an aggregate amount of $1,537,553, including $134,750 to Gregg Christensen, our Chief Legal Officer. Each award will vest approximately one-quarter of the awarded amount on January 1, 2023, 2024, 2025 and 2026.

The compensation committee also approved awards of performance-based LTIP Units to our executive officers in an aggregate target amount of $2,773,749, including $250,250 to Gregg Christensen, our Chief Legal Officer. The actual amount of each performance-based LTIP Unit award will be determined at the conclusion of a three-year performance period and will depend on the internal rate of return as defined in the award agreement. The earned LTIP Units will become fully vested on the first anniversary of the last day of the performance period, subject to continued employment with the advisor or its affiliates.

The number of units granted were valued by reference to our November 30, 2021 NAV per share as announced on December 15, 2021 of $16.9316.

Investment in 33rd and 13th - Millcreek

On October 26, 2021, we, through a wholly owned subsidiary of our Operating Partnership, entered a real estate purchase contract with 33rd and 13th, LLC (the “Seller”) to purchase a multifamily development project located on 1.76 acres of land and referred to as 33rd and 13th – Millcreek in Millcreek, Utah (the “Project”) for $7.2 million. The Seller is directly or indirectly owned by the following individuals who are also our executive officers: Daniel Shaeffer (11.3636%), Chad Christensen (22.7273%), Gregg Christensen (11.3636%), Glenn Rand (2.2727%), Stan Hanks (2.2727%), Susan Hallenberg (1.8182%) and Eric Marlin (1.3636%). In addition, an unaffiliated third party owns 36.3636% of the Seller and the balance is owned by non-executive employees of the Company or its affiliates. The purchase of the Project was approved by the conflicts committee. In addition, the purchase price for the Project was established based on an appraisal provided by an independent third-party appraisal firm. On October 29, 2021, we acquired the Project.

Membership Interest Purchase Agreement – Sugar House Commons, LLC

On November 1, 2021, we, through a wholly owned subsidiary of our Operating Partnership, entered a Membership Interest Purchase Agreement to sell all of the membership interests of Sugar House Commons, LLC (“Windsor Court”) directly or indirectly to the following individuals who are also our executive officers: Daniel Shaeffer, Chad Christensen, Gregg Christensen and Eric Marlin for $510,000. The sole asset of Sugar House Commons, LLC is a 0.72-acre parcel of land located in Salt Lake City, Utah valued at $510,000 pursuant to a recent third-party appraisal report. The sale was approved by the conflicts committee of the board of directors, which is comprised entirely of independent directors who have no interest in the transaction. The disposition of Windsor Court closed in the fourth quarter of 2021.

16

Table of Contents

Alpha Mill Investment by Related Party

On November 2, 2021, we sold TIC interests in Alpha Mill totaling 43% to certain unaffiliated third parties through a private offering for $34.8 million. Reed Christensen, the father of Chad Christensen, one of our directors and Executive Chairman, and Gregg Christensen, our Chief Legal Officer and Secretary, is expected to invest. Mr. R. Christensen is expected to purchase his shares net of selling commissions in the amount of $244,444. The net proceeds received by us for the sale of the shares will be the same as what we receive from unaffiliated third parties.

Apt Cowork

Certain of our officers and directors expect to have an ownership interest in APT Cowork, LLC (“APT”), an entity recently formed to engage in the business of converting unused common space in multifamily apartment communities or retail space to revenue producing co-working space.

We, through Cottonwood Capital Management, Inc., a wholly owned subsidiary of CROP (“CCMI”), expect to enter into a Reimbursement and Cost Sharing Agreement with APT pursuant to which CCMI will make certain employees available to APT to the extent they are not otherwise occupied in providing services to us and in exchange APT will reimburse CCMI for APT’s allocable share of all direct and indirect costs related to the employees utilized by APT. Under the terms of the agreement as proposed, for any annual period, the amount of reimbursement pursuant to the agreement will not exceed $120,000. In addition, the agreement is expected to have a one-year term, but may be renewed for an unlimited number of successive one-year terms.

In addition to the Reimbursement and Cost Sharing Agreement, we expect to enter a Master Coworking Space Lease Agreement between APT and our property-owning limited liability company (“landlord”) to provide for the terms on which APT may lease space from landlord at landlord’s properties to operate its business.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with the consolidated financial statements and notes thereto appearing elsewhere in this supplement. In addition to historical data, this discussion contains forward-looking statements about our business, operations and financial performance based on current expectations that involve risks, uncertainties and assumptions. Our actual results may differ materially from those in this discussion as a result of various factors, including but not limited to those discussed under “Risk Factors” in the prospectus and herein.

Overview

Cottonwood Communities, Inc. invests in a diverse portfolio of multifamily apartment communities and multifamily real estate-related assets throughout the United States. We are externally managed by our advisor, CC Advisors III, a wholly owned subsidiary of our sponsor, Cottonwood Communities Advisors, LLC (“CCA”). We were incorporated in Maryland in 2016. We hold all of our assets through our Operating Partnership. Our Operating Partnership was Cottonwood Communities O.P., LP (“CCOP”) prior to the CRII Merger and is CROP after the CRII Merger. We are the sole member of the sole general partner of the Operating Partnership and own general partner interests in the Operating Partnership alongside third party limited partners.

Cottonwood Communities, Inc. is a non-traded perpetual-life, net asset value (“NAV”), real estate investment trust (“REIT”). We qualified as a REIT for U.S. federal income tax purposes beginning with the taxable year ended December 31, 2019. We generally will not be subject to U.S. federal income taxes on our taxable income to the extent we annually distribute all of our net taxable income to stockholders and maintain our qualification as a REIT.

17

Table of Contents

As December 31, 2021, we had received net proceeds of $124.5 million from the sale of common stock and $111.9 million from the sale of Series 2019 Preferred Stock. We have contributed our net proceeds to CROP in exchange for a corresponding number of mirrored OP units. CROP has primarily used the net proceeds to make investments in real estate, multifamily real estate-related assets, and real estate related operations.

As December 31, 2021, we had a portfolio of $2.1 billion in total assets, with 83.3% of our equity value in operating properties, 10.4% in development and 6.3% in real estate-related investments. Refer to the section “Our Investments” below for further description of our portfolio.

COVID-19 Pandemic

One of the most significant risks and uncertainties facing the real estate industry generally continues to be the effect of the ongoing public health crisis of the novel coronavirus disease (COVID-19) pandemic. During the year ended December 31, 2021 we did not experience significant disruptions in our operations from the COVID-19 pandemic; however, we continue to closely monitor the impact of the COVID-19 pandemic on all aspects of our business, including how the pandemic will impact our tenants and multifamily communities.

2021 Activities

The following highlights activities that occurred during the year ended December 31, 2021:

Merged with Cottonwood Residential II, Inc. (“CRII”), Cottonwood Multifamily REIT I, Inc, and Cottonwood Multifamily REIT II, Inc. (collectively, the “Mergers”)

| • | Acquired $1.5 billion of real estate and real estate-related assets. |

| • | Assumed $622.1 million in property-level financing. |

| • | Assumed $64.1 million in construction loans. |

| • | Assumed $144.0 million in Series 2016 and Series 2017 Preferred Stock. |

| • | Assumed $48.6 million of unsecured promissory notes. |

Implemented an NAV-Based Perpetual-Life Strategy

| • | Restructured the classes of shares we offer. |

| • | Revised our compensation arrangements with our advisor and its affiliates. |

| • | Adopted a monthly NAV policy beginning on May 7, 2021. NAV was $10.8315 per share as of May 7, 2021 compared to $17.2839 as of December 31, 2021. |

| • | Amended our share repurchase program to provide additional liquidity to our stockholders. |

| • | Received shareholder approval to remove liquidation provisions in our charter. |

Invested and Disposed of Real Estate Assets

| • | Invested $81.8 million in seven projects under various stages of development in the Salt Lake City, UT market. |

| • | Contributed $12.4 million of preferred equity to Riverfront, a development in West Sacramento, CA. |

| • | Provided a $13.0 mezzanine loan to Integra Peaks, a development in Reno, NV. |

| • | Acquired an additional 54.9% interest in Melrose Phase II for $10.6 million, increasing our ownership to 79.8%. |

| • | Loaned an additional $1.1 million in B Notes to Dolce Twin Creeks, Phase II prior to being repaid the full $9.3 million of those notes. |

| • | Sold a 43% interest in Alpha Mill for $34.8 million. |

18

Table of Contents

Raised Capital and Managed Financing

| • | Closed an aggregate of $13.4 million in property-level financing and repaid $24.6 million. |

| • | Drew an additional $52.5 million on construction loans. |

| • | Raised $78.9 million of proceeds from the sale of our Series 2019 Preferred Stock. |

| • | Repaid $5.1 million of unsecured promissory notes. |

| • | Launched this offering of up to $1.0 billion of shares of our common stock on November 4, 2021, raising $2.5 million through the end of the year. |

Our Investments

Our portfolio of investments consists of ownership interests or structured investment interests in 33 multifamily apartment communities in 13 states with 9,746 units, including 1,373 units in four multifamily apartment communities in which we have a structured investment interest and another 1,079 units in four multifamily apartment communities under construction. In addition, we have an ownership interest in three parcels of land planned for development.

Information regarding our investments as of December 31, 2021 is as follows:

Stabilized Properties ($ in thousands, except net effective rents)

Property Name | Location | Number of Units | Average Unit Size (Sq Ft) | Purchase Date | Purchase Date Property Value | Mortgage Debt Outstanding (1) | Net Effective Rent | Physical Occupancy Rate | Percentage Owned by CROP | |||||||||||||||||||||||

3800 Main | Houston, TX | 319 | 831 | May 2021 | $ | 58,100 | $ | 35,861 | $ | 1,449 | 93.7 | % | 50.0 | % | ||||||||||||||||||

Alpha Mill | Charlotte, NC | 267 | 830 | May 2021 | 69,500 | 39,044 | 1,438 | 95.5 | % | 57.2 | % | |||||||||||||||||||||

Cason Estates | Murfreesboro, TN | 262 | 1,078 | May 2021 | 51,400 | 33,594 | 1,299 | 98.1 | % | 100.0 | % | |||||||||||||||||||||

Cottonwood | Salt Lake City, UT | 264 | 834 | May 2021 | 47,300 | 21,645 | 1,216 | 96.6 | % | 100.0 | % | |||||||||||||||||||||

Cottonwood Bayview | St. Petersburg, FL | 309 | 805 | May 2021 | 95,900 | 47,205 | 2,163 | 98.1 | % | 71.0 | % | |||||||||||||||||||||

Cottonwood One Upland | Boston, MA | 262 | 1,160 | March 2020 | 103,600 | 20,000 | 2,460 | 93.1 | % | 100.0 | % | |||||||||||||||||||||

Cottonwood Reserve | Charlotte, NC | 352 | 1,021 | May 2021 | 77,500 | 38,314 | 1,299 | 94.3 | % | 91.1 | % | |||||||||||||||||||||

Cottonwood Ridgeview | Plano, TX | 322 | 1,156 | May 2021 | 70,000 | 29,800 | 1,551 | 96.6 | % | 90.5 | % | |||||||||||||||||||||

Cottonwood West Palm | West Palm Beach, FL | 245 | 1,122 | May 2019 | 66,900 | 35,995 | 1,987 | 95.1 | % | 100.0 | % | |||||||||||||||||||||

Cottonwood Westside | Atlanta, GA | 197 | 860 | May 2021 | 47,900 | 25,506 | 1,558 | 92.9 | % | 100.0 | % | |||||||||||||||||||||

Enclave on Golden Triangle | Keller, TX | 273 | 1,048 | May 2021 | 51,600 | 34,000 | 1,443 | 96.0 | % | 98.9 | % | |||||||||||||||||||||

Fox Point | Salt Lake City, UT | 398 | 841 | May 2021 | 79,400 | 46,000 | 1,234 | 95.2 | % | 52.8 | % | |||||||||||||||||||||

Heights at Meridian | Durham, NC | 339 | 997 | May 2021 | 79,900 | 33,750 | 1,379 | 96.5 | % | 100.0 | % | |||||||||||||||||||||