FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

| For the month of …. | February | ………………………………………… , | 2022 |

CANON INC. | ||||

(Translation of registrant’s name into English) | ||||

30-2, Shimomaruko 3-Chome, Ohta-ku, Tokyo 146-8501, Japan | ||||

(Address of principal executive offices) | ||||

[Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

| Form 20-F | X | Form 40-F |

|

[Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

| Yes |

| No | X |

[If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b):82-....................

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

CANON INC. | ||

| (Registrant) |

| Date…. | February 25, 2022 | By ……/s/……… Sachiho Tanino………………… | ||||

| (Signature)* |

Sachiho Tanino | ||

General Manager | ||

Consolidated Accounting Division | ||

Canon Inc. |

*Print the name and title of the signing officer under his signature.

The following materials are included.

1. Notice of Convocation of the Ordinary General Meeting of Shareholders for the 121st Business Term

2. Internet Disclosure for Notice of Convocation of the Ordinary General Meeting of Shareholders for the 121st Business Term

Notice of Convocation of the Ordinary General Meeting of Shareholders for the 121st Business Term

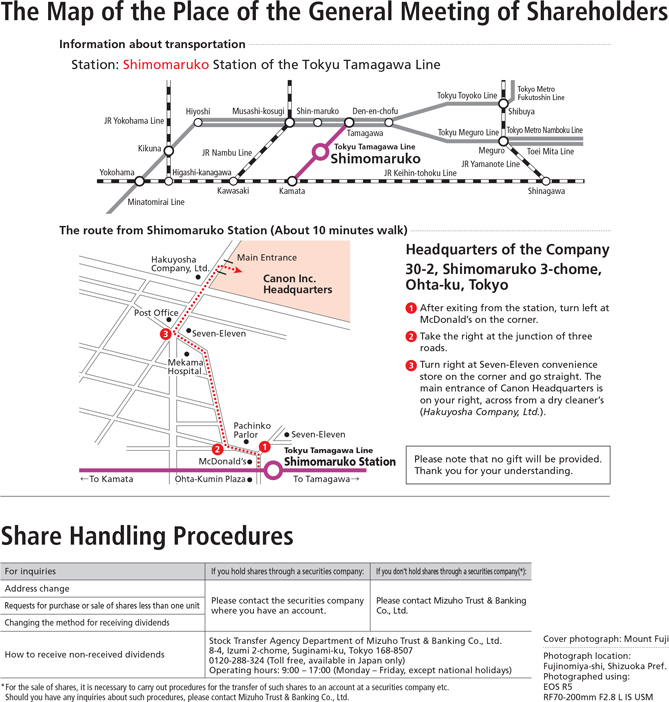

DATE AND TIME March 30 (Wednesday), 2022 at 10:00 a.m. (Japan time) From the perspective of preventing the spread of the novel (The reception will commence at 9:00 a.m.) coronavirus disease (COVID-19), we ask that you to refrain from traveling to the Meeting venue on the date of the PLACE Headquarters of the Company Meeting if at all possible and instead consider the option of 30-2, Shimomaruko 3-chome, Ohta-ku, Tokyo exercising your voting rights in writing or via the Internet. MATTERS TO BE Item No.1 Dividend from Surplus RESOLVED Item No.2 Partial Amendment to the Articles of Incorporation Item No.3 Election of Five Directors Item No.4 Election of Two Audit & Supervisory Board Members Item No.5 Grant of Bonus to Directors

Notice of Convocation of the Ordinary General Meeting of Shareholders for the 121st Business Term DATE AND TIME March 30 (Wednesday), 2022 at 10:00 a.m. (Japan time) (The reception will commence at 9:00 a.m.) PLACE Headquarters of the Company 30-2, Shimomaruko 3-chome, Ohta-ku, Tokyo MATTERS TO BE Item No.1 Dividend from Surplus RESOLVED Item No.2 Partial Amendment to the Articles of Incorporation Item No.3 Election of Five Directors Item No.4 Election of Two Audit & Supervisory Board Members Item No.5 Grant of Bonus to Directors From the perspective of preventing the spread of the novel coronavirus disease (COVID-19), we ask that you to refrain from traveling to the Meeting venue on the date of the Meeting if at all possible and instead consider the option of exercising your voting rights in writing or via the Internet.

| Based on our philosophies of “a respect for humanity” and “an emphasis on original technology,” Canon was founded in 1937 as a camera manufacturer and continued to grow for 30 years under the high ideal of “building the world’s best cameras using our own technology.”

During the age of internationalization in the 1960s, we achieved further growth through structural transformation aimed at “globalization” and “diversification.”

In addition, as internationalization continued to expand around the world, we marked our 50th anniversary of the founding of the Company in 1987. In 1988, we announced our second inauguration and introduced the new corporate philosophy of “kyosei” (harmoniously living and working together with all people of the world).

In accordance with this philosophy of “kyosei,” Canon will continue its business activities aimed at corporate growth and development in the interest of world prosperity and the happiness of humankind.

|

Index |

NOTICE OF CONVOCATION OF THE ORDINARY GENERAL MEETING OF SHAREHOLDERS FOR THE 121ST BUSINESS TERM | P. 3 | |||||

Guidance Notes on the Exercise of Voting Rights Prior to the Meeting | P. 4 | |||||

REFERENCE DOCUMENTS FOR | ||||||

GENERAL MEETING OF SHAREHOLDERS | ||||||

Propositions: | ||||||

Item No.1 - Dividend from Surplus | P. 6 | |||||

Item No.2 - Partial Amendment to the Articles of Incorporation | P. 7 | |||||

Item No.3 - Election of Five Directors | P. 9 | |||||

Item No.4 - Election of Two Audit & Supervisory Board Members | P. 13 | |||||

Item No.5 - Grant of Bonus to Directors | P. 16 | |||||

(Materials delivered pursuant to Article 437 and Article 444 of the Corporation Law of Japan)

|

|

|

| |||

BUSINESS REPORT | ||||||

1. Current Conditions of the Canon Group | P. 17 | |||||

2. Shares of the Company | P. 30 | |||||

3. Directors and Audit & Supervisory Board Members | P. 31 | |||||

4. Accounting Auditor | P. 36 | |||||

5. Systems Necessary to Ensure the Properness of Operations | P. 37 | |||||

| CONSOLIDATED FINANCIAL STATEMENTS | ||||||

Consolidated Balance Sheets | P. 41 | |||||

Consolidated Statements of Income | P. 42 | |||||

| NON-CONSOLIDATED FINANCIAL STATEMENTS | ||||||

Non-Consolidated Balance Sheets | P. 43 | |||||

Non-Consolidated Statements of Income | P. 44 | |||||

| AUDIT REPORTS | ||||||

AUDIT REPORT OF ACCOUNTING AUDITOR | ||||||

ON CONSOLIDATED FINANCIAL STATEMENTS | P. 45 | |||||

AUDIT REPORT OF ACCOUNTING AUDITOR | P. 47 | |||||

AUDIT REPORT OF AUDIT & SUPERVISORY BOARD

|

| P. 49

|

| |||

| REFERENCE | ||||||

Activities of Sustainability | P. 51 | |||||

Topics

|

| P. 53

|

| |||

The Map of the Place of the General Meeting of Shareholders / Share Handling Procedures | ||||||

To Our Shareholders

|

| |||

We are pleased to present our notice of convocation of the Ordinary General Meeting of Shareholders for the 121st Business Term (from January 1, 2021 to December 31, 2021). The global economy has remained on track toward recovery overall during the current business term, albeit the trend has varied depending on the country and region, amid progress achieved in implementing measures to address COVID-19 in respective countries along with easing movement restrictions. Meanwhile, production lulls of companies due to a shortage of materials, mainly for semiconductors, arose and pressured distribution systems emerged.

Amid this environment, though the Company encountered difficulties in production of some products, we achieved steady gains in net sales and profits as a result of efforts geared to increasing sales of products and services and generating earnings upon having resumed full-scale sales activities, which had been hampered due to the COVID-19 pandemic.

For the term-end dividend, taking into account our improved performance and our outlook going forward, and also in appreciation for the continued support of our shareholders, we will propose a distribution of 55.00 yen per share at the Ordinary General Meeting of Shareholders for the 121st Business Term. As such, our dividend for the year, including our interim dividend of 45.00 yen per share, will amount to 100.00 yen per share, thereby constituting an increase of 20.00 yen relative to our annual dividend for the 120th Business Term.

During the current business term, the Canon Group started on a new five-year management plan, Phase VI (2021 to 2025) of the “Excellent Global Corporation Plan,” under which we have reorganized our operations into four industry-oriented business groups of Printing, Imaging, Medical, and Industrial. Under the new business group structure, we will seek to improve productivity and fortify our competitive strengths while also taking on challenges of further creating new businesses. |

When it comes to the global economy in 2022, the business environment does not warrant optimism amid concerns arising from the prospect of slowing growth due to the spread of COVID-19 variants and the expectation that the semiconductor shortage will be further prolonged. Nevertheless, the Canon Group will make united efforts to overcome this difficulty and further strive to improve our business performance.

We look forward to our shareholders’ continued support and encouragement.

March, 2022

Chairman & CEO FUJIO MITARAI

|

Securities Code: 7751 March 4, 2022 |

TO OUR SHAREHOLDERS

| CANON INC. | ||||||

30-2, Shimomaruko 3-chome, Ohta-ku, Tokyo Chairman & CEO Fujio Mitarai |

NOTICE OF CONVOCATION OF THE ORDINARY GENERAL MEETING OF SHAREHOLDERS FOR THE 121ST BUSINESS TERM

Notice is hereby given that the Ordinary General Meeting of Shareholders for the 121st Business Term of Canon Inc. (the “Company”) will be held as described below. Although we will hold the Meeting upon having appropriately taken measures to prevent the spread of COVID-19, from the perspective of preventing further transmission of infection, we ask that you to refrain from traveling to the Meeting venue on the date of the Meeting if at all possible and instead consider the option of exercising your voting rights in writing or via the Internet. The voting deadline in writing or via the Internet is 5:00 p.m. on March 29 (Tuesday), 2022 (Japan time). | ||||||

1. DATE AND TIME: |

March 30 (Wednesday), 2022 at 10:00 a.m. (Japan time) | |||||

(The reception will commence at 9:00 a.m.)

| ||||||

2. PLACE: |

Headquarters of the Company | |||||

| 30-2, Shimomaruko 3-chome, Ohta-ku, Tokyo | ||||||

(Please see the map at the end of this notice.)

| ||||||

3. MATTERS CONSTITUTING |

Matters to be Reported: | |||||

1. Reports on the contents of the Business Report and Consolidated Financial Statements for the 121st Business Term (from January 1, 2021 to December 31, 2021), and reports on the Auditing Results of Accounting Auditor and Audit & Supervisory Board regarding the Consolidated Financial Statements. | ||||||

2. Reports on the content of the Non-Consolidated Financial Statements for the 121st Business Term (from January 1, 2021 to December 31, 2021). | ||||||

| Matters to be Resolved upon: | ||||||

Propositions: | ||||||

Item No.1 - Dividend from Surplus | ||||||

Item No.2 - Partial Amendment to the Articles of Incorporation | ||||||

Item No.3 - Election of Five Directors | ||||||

Item No.4 - Election of Two Audit & Supervisory Board Members | ||||||

Item No.5 - Grant of Bonus to Directors

|

3

| · | Upon attending the Meeting, please present the enclosed Voting Form to the receptionist at the place of the Meeting. |

| · | Shareholders at the Meeting will be subject to temperature checks performed prior to reception. Please be aware that those showing signs of fever or poor physical health may be refused to enter the Meeting venue. |

| · | Shareholders in attendance will be asked to use hand sanitizer and wear a face mask. |

| · | There is to be extra distance between seating at the Meeting venue. Also, the number of shareholders allowed entry into the Meeting venue may be limited depending on the number of shareholders who visit. We appreciate your understanding in this regard. |

| · | Please note that no gift will be provided at the Meeting. |

| · | Of the documents to be provided upon Notice of Convocation, the following documents have been posted on our website on the Internet (https://global.canon/en/ir/) in accordance with laws and regulations and provisions of the Company’s Articles of Incorporation, and therefore have not been included in this Notice of Convocation: “Stock Acquisition Rights etc. of the Company” of the Business Report; “Consolidated Statement of Equity” and “Notes to Consolidated Financial Statements” of the Consolidated Financial Statements, and; “Non-Consolidated Statement of Changes in Net Assets” and “Notes to Non-Consolidated Financial Statements” of the Non-Consolidated Financial Statements. Documents posted on the aforementioned website have been subject to audit, whereby the Audit & Supervisory Board Members have prepared the Audit Report and the Accounting Auditor has prepared the Audit Report of Accounting Auditor. |

| · | Any changes in the matters described in Reference Documents for General Meeting of Shareholders, Business Report, Consolidated Financial Statements and Non-Consolidated Financial Statements will be posted on our website on the Internet (https://global.canon/en/ir/). |

Guidance Notes on the Exercise of Voting Rights Prior to the Meeting

Shareholders may exercise their voting rights prior to the Meeting in writing (using the Voting Form) or via the Internet as explained below, instead of attending the Meeting in person.

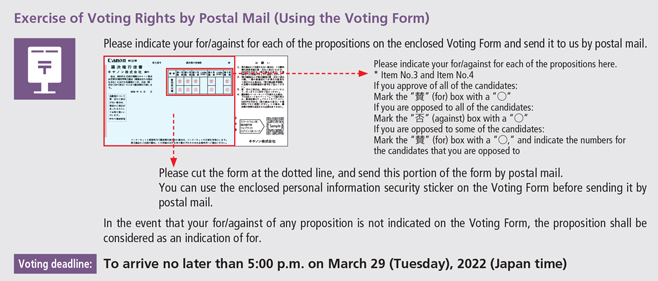

Exercise of Voting Rights by Postal Mail (Using the Voting Form) Please indicate your for/against for each of the propositions on the enclosed Voting Form and send it to us by postal mail. Please indicate your for/against for each of the propositions here. * Item No.3 and Item No.4 If you approve of all of the candidates: Mark the “賛” (for) box with a “○” If you are opposed to all of the candidates: Mark the “否” (against) box with a “○” If you are opposed to some of the candidates: Mark the “賛” (for) box with a “○,” and indicate the numbers for the candidates that you are opposed to Please cut the form at the dotted line, and send this portion of the form by postal mail. You can use the enclosed personal information security sticker on the Voting Form before sending it by postal mail. In the event that your for/against of any proposition is not indicated on the Voting Form, the proposition shall be considered as an indication of for. Voting deadline: To arrive no later than 5:00 p.m. on March 29 (Tuesday), 2022 (Japan time)

4

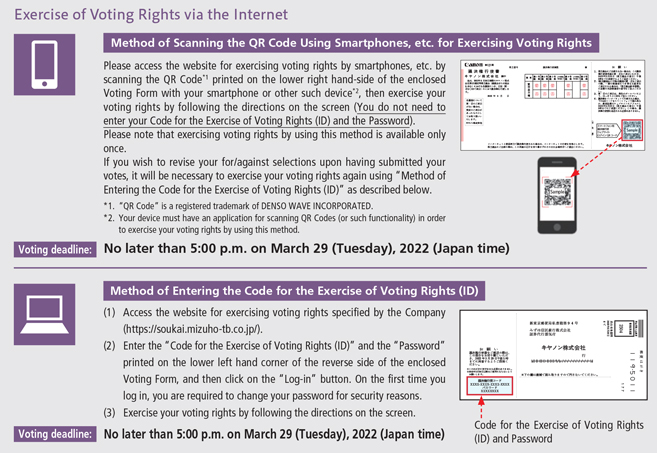

Exercise of Voting Rights via the Internet Method of Scanning the QR Code Using Smartphones, etc. for Exercising Voting Rights Please access the website for exercising voting rights by smartphones, etc. by scanning the QR Code*1 printed on the lower right hand-side of the enclosed Voting Form with your smartphone or other such device*2, then exercise your voting rights by following the directions on the screen (You do not need to enter your Code for the Exercise of Voting Rights (ID) and the Password). Please note that exercising voting rights by using this method is available only once. If you wish to revise your for/against selections upon having submitted your votes, it will be necessary to exercise your voting rights again using “Method of Entering the Code for the Exercise of Voting Rights (ID)” as described below. *1. “QR Code” is a registered trademark of DENSO WAVE INCORPORATED. *2. Your device must have an application for scanning QR Codes (or such functionality) in order to exercise your voting rights by using this method Voting deadline: No later than 5:00 p.m. on March 29 (Tuesday), 2022 (Japan time) Method of Entering the Code for the Exercise of Voting Rights (ID) (1) Access the website for exercising voting rights specified by the Company (https://soukai.mizuho-tb.co.jp/). (2) Enter the “Code for the Exercise of Voting Rights (ID)” and the “Password” printed on the lower left hand corner of the reverse side of the enclosed Voting Form, and then click on the “Log-in” button. On the first time you log in, you are required to change your password for security reasons. (3) Exercise your voting rights by following the directions on the screen. Voting deadline: No later than 5:00 p.m. on March 29 (Tuesday), 2022 (Japan time) Code for the Exercise of Voting Rights (ID) and Password

| • | Items Required to be Agreed on for the Exercise of Voting Rights via the Internet |

| (1) | If you exercise your voting rights twice, in writing and via the Internet, we will only accept the exercise of your voting rights via the Internet as effective. |

| (2) | If you exercise your voting rights more than once via the Internet, we will only accept the last exercise of your voting rights as effective. |

| (3) | The cost of Internet access (access fees to providers, telecommunications fees, etc.) shall be borne by the shareholders. |

| (4) | Although each of the methods concerning the exercise of voting rights via the Internet has been operationally verified on standard devices connected to the Internet, in some cases, it may not be possible to gain access using certain devices or due to certain circumstances. |

| • | For Inquiries with Respect to the Exercise of Voting Rights via the Internet |

Please contact: |

Stock Transfer Agency Department of Mizuho Trust & Banking Co., Ltd.

Telephone: 0120-768-524 (toll-free, available in Japan only)

Operating Hours: 9:00 a.m. to 9:00 p.m. (excluding the New Year holidays)

| To Institutional Investors |

The electronic voting platform for institutional investors operated by Investor Communications Japan Inc. is available for institutional investors that have applied to use such platform in advance.

5

REFERENCE DOCUMENTS FOR GENERAL MEETING OF SHAREHOLDERS

Item No.1: Dividend from Surplus

The basic policy of the Company is to provide a stable return and actively return profits to shareholders, mainly in the form of a dividend, taking into consideration medium-term profit forecasts along with planned future investments, cash flow and other factors.

We accordingly propose a term-end dividend of 55.00 yen per share for the current business term, an increase of 15.00 yen relative to term-end dividend of the previous term, upon having taken into account steady recovery of our business performance despite adverse effects of COVID-19 culminating in production reductions and logistics disruptions, and in view of our performance outlook going forward.

As we have already paid an interim dividend of 45.00 yen per share, the full-year dividend will be 100.00 yen per share (an increase of 20.00 yen from the previous term).

1. Kind of the dividend property

|

Cash

| |

2. Matters regarding allocation of the dividend property and its total amount

|

55.00 yen per one common share of the Company Total amount of dividend 57,517,446,745 yen

| |

3. Effective date of the distribution of the dividend from surplus

|

March 31, 2022

|

[Reference] Changes in the amount of dividend per share (Yen)

Interim dividend Term-end dividend Commemorative dividend

| 6 |

Item No.2: Partial Amendment to the Articles of Incorporation

1. Reasons for Proposal

Since the system for providing informational materials for the general meeting of shareholders in electronic format has been established as provided for in the Act Partially Amending the Companies Act (Act No. 70 of 2019), and the provisions of the amended Companies Act that stipulates the system are to be enforced on September 1, 2022, the Company will make the following changes to the Articles of Incorporation in preparation for the introduction of the system.

| (1) | The proposed amendment to Paragraph 1, Article 14 will newly stipulate that the Company shall take measures for providing information that constitutes the content of informational materials for the general meeting of shareholders of reference documents, etc. for the general meeting of shareholders in electronic format. |

| (2) | The proposed amendment to Paragraph 2, Article 14 will establish provisions to limit the scope of the items to be stated in the paper-based documents to be delivered to shareholders who requested the delivery of paper-based documents pertaining to informational materials for the general meeting of shareholders pursuant to the amended Companies Act. |

| (3) | Since Article 14 of the current Articles of Incorporation for Disclosure through Internet and Deemed Delivery of Reference Documents, etc. for General Meetings of Shareholders under the current Companies Act will no longer be required, it will be deleted. |

| (4) | Accompanying the aforementioned new establishment and deletion, supplementary provisions regarding the effective date, etc. will be established. |

2. Substance of Amendment

The substance of the amendment is as follows:

(The amended parts are underlined.)

Current Articles of Incorporation

|

Proposed Amendment

| |||||||||

Article 1. - Article 13. |

(Text omitted)

|

| Article 1. - Article 13. |

(Same as present text)

|

| |||||

Disclosure through Internet and Deemed Delivery of Reference Documents, etc. for General Meetings of Shareholders | ||||||||||

Article 14. Upon convening a general meeting of shareholders, the Company may deem that the information required to be described or indicated in the reference documents for the general meeting of shareholders, business reports, financial statements and consolidated financial statements has been provided to the shareholders in the event that such information is disclosed, pursuant to ordinances of the Ministry of Justice, through a method that uses the Internet. | (Deleted) | |||||||||

Measures for Providing Information in Electronic Format, etc. | ||||||||||

| (Newly established) | Article 14. When the Company convenes a general meeting of shareholders, the Company shall take measures for providing information that constitutes the content of reference documents, etc. for the general meeting of shareholders in electronic format stipulated in Article 325-2 of the Corporation Law. | |||||||||

2. Among items for which the measures for providing information in electronic format will be taken, the Company may exclude all or some of those items designated by ordinances of the Ministry of Justice from statements in the paper-based documents to be delivered to shareholders who requested the delivery of paper-based documents stipulated in Article 325-5 of the Corporation Law by the record date of voting rights.

| ||||||||||

7

Current Articles of Incorporation

|

Proposed Amendment

| |||||||||

Article 15. - Article 39. |

(Text omitted)

|

| Article 15. - Article 39. |

(Same as present text)

|

| |||||

| (Newly established) | Supplementary Provisions | |||||||||

| (Newly established) | 1. The deletion of Article 14 (Disclosure through Internet and Deemed Delivery of Reference Documents, etc. for General Meetings of Shareholders) of the current Articles of Incorporation and the new establishment of Article 14 (Measures for Providing Information in Electronic Format, etc.) of the proposed amendment shall be effective from the date of enforcement of the revised provisions provided for in the proviso to Article 1 of the Supplementary Provisions of the Act Partially Amending the Companies Act (Act No. 70 of 2019) (hereinafter “Date of Enforcement”). | |||||||||

2. Notwithstanding the provision of the preceding paragraph, Article 14 of the current Articles of Incorporation shall remain effective regarding any general meeting of shareholders held on a date within six months from the Date of Enforcement. | ||||||||||

3. These Supplementary Provisions shall be deleted on the date when six months have elapsed from the Date of Enforcement or three months have elapsed from the date of the general meeting of shareholders in the preceding paragraph, whichever is later.

| ||||||||||

8

Item No.3: Election of Five Directors

The terms of office of all of the five Directors will expire at the end of this Meeting. Accordingly, we propose the election of five Directors.

The Company has a basic policy that the focus of the organizational structure of the Board of Directors is on the Directors that oversee company-wide business strategies or execution and the Directors that oversee multiple business fields or headquarters functions, while at least two Independent Outside Directors are appointed while also assuring that they account for one third or more of the total number of Directors, in order to secure sound management.

The candidates for Directors, based on this basic policy, are as follows:

Candidate No.

|

Name

|

Current Position, Business in Charge, etc. at the Company

|

Board of

| |||||||||

1

|

Fujio Mitarai

|  |

Chairman & CEO

|

100% (12/12)

| ||||||||

2

|

Toshizo Tanaka

| |

Executive Vice President & CFO Group Executive of Finance & Accounting Headquarters Group Executive of Public Affairs Headquarters Group Executive of Facilities Management Headquarters

|

100% (12/12)

| ||||||||

3

|

Toshio Homma

| |

Executive Vice President & CTO Head of Printing Group Chief Executive of Digital Printing Business Operations

|

100% (12/12)

| ||||||||

4

|

Kunitaro Saida

|

|

Director

|

100% (12/12)

| ||||||||

5

|

Yusuke Kawamura

|

|

Director

|

100% (9/9)

| ||||||||

Note: The attendance figures above constitute attendance of the Board of Directors meetings by the respective candidates for Directors during the 121st business term.

reappointed outside director independent director

9

Candidate No. 1 |

Fujio Mitarai

Date of birth Sep. 23, 1935

Number of the Company’s shares held 144,444 shares

|

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||

As of | ||||||||||||

Apr. 1961: Entered the Company | ||||||||||||

Mar. 1981: Director | ||||||||||||

Mar. 1985: Managing Director | ||||||||||||

Mar. 1989: Senior Managing Director | ||||||||||||

Mar. 1993: Executive Vice President | ||||||||||||

Sep. 1995: President | ||||||||||||

Mar. 2006: Chairman, President & CEO | ||||||||||||

May 2006: Chairman & CEO (daihyō torishimariyaku kaichō) | ||||||||||||

Mar. 2012: Chairman & CEO (daihyō torishimariyaku kaichō ken shachō) | ||||||||||||

Mar. 2016: Chairman & CEO (daihyō torishimariyaku kaichō) | ||||||||||||

May 2020: Chairman & CEO (daihyō torishimariyaku kaichō ken shachō) (present) | ||||||||||||

[Important concurrent posts] | ||||||||||||

● Audit & Supervisory Board Member of The Yomiuri Shimbun Holdings | ||||||||||||

| ||||||||||||

| Candidate No. 1 | [Reasons for being selected as a candidate] | |||||||||||

Mr. Fujio Mitarai has supervised the Company’s management as a CEO over the course of many years and has accomplished many things, such as significantly increasing profitability through management reform including production reform, and building a foundation for the transformation of the Company’s business structure for new areas where growth is expected. The Company has selected him as a candidate for Director upon determining that his wealth of expertise and ability related to management, gained from being chairman of Keidanren (“Japan Business Federation”), and holding many important positions in other organizations, are vital to the Company’s management. | ||||||||||||

Candidate No. 2 |

Toshizo Tanaka

Date of birth Oct. 8, 1940

Number of the Company’s shares held 24,510 shares |

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||

As of | ||||||||||||

Apr. 1964: Entered the Company | ||||||||||||

Mar. 1995: Director | ||||||||||||

Mar. 1997: Managing Director | ||||||||||||

Mar. 2001: Senior Managing Director | ||||||||||||

Mar. 2007: Executive Vice President & Director | ||||||||||||

Mar. 2008: Executive Vice President & CFO (present) | ||||||||||||

Apr. 2011: Group Executive of Finance & Accounting Headquarters | ||||||||||||

Mar. 2014: Group Executive of Human Resources Management & Organization Headquarters | ||||||||||||

Apr. 2017: Group Executive of Facilities Management Headquarters (present) | ||||||||||||

Mar. 2018: Group Executive of Public Affairs Headquarters (present) | ||||||||||||

Apr. 2018: Group Executive of Finance & Accounting Headquarters (present) | ||||||||||||

| ||||||||||||

| Candidate No. 2 | [Reasons for being selected as a candidate] | |||||||||||

Mr. Toshizo Tanaka has contributed greatly to building the Company’s strong financial position while working for many years as CFO. The Company has selected him as a candidate for Director upon determining that his extensive expertise, insight, and wide range of experience, gained from managing overall corporate administration, are vital to the Company’s management. | ||||||||||||

10

Candidate No. 3 |

Toshio Homma

Date of birth Mar. 10, 1949

Number of the Company’s shares held 68,752 shares

|

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||

As of | ||||||||||||

Apr. 1972: Entered the Company | ||||||||||||

Jan. 1995: Senior General Manager of Copying Machine Development Center | ||||||||||||

Mar. 2003: Director | ||||||||||||

Apr. 2003: Group Executive of Business Promotion Headquarters | ||||||||||||

Jan. 2007: Chief Executive of L Printer Products Operations | ||||||||||||

Mar. 2008: Managing Director | ||||||||||||

Mar. 2012: Senior Managing Director | ||||||||||||

| Group Executive of Procurement Headquarters | ||||||||||||

Mar. 2016: Executive Vice President | ||||||||||||

Apr. 2016: Chief Executive of Office Imaging Products Operations | ||||||||||||

Mar. 2017: Executive Vice President & In charge of Office Business | ||||||||||||

Apr. 2020: Executive Vice President & CTO & In charge of Printing Business | ||||||||||||

| Chief Executive of Digital Printing Business Operations (present) | ||||||||||||

Apr. 2021: Executive Vice President & CTO (present) | ||||||||||||

| Head of Printing Group (present) | ||||||||||||

| ||||||||||||

| [Reasons for being selected as a candidate] | ||||||||||||

Mr. Toshio Homma accomplished great things in the commercialization of large-format printing systems after being engaged in the development and commercialization of copying machines over the course of many years. Also, he led procurement reform and contributed to creating a structure to support reducing the cost-of-sales ratio. He is currently in charge of and managing the overall printing business including commercial printing, while also managing the Company’s technological R&D as CTO. The Company has selected him as a candidate for Director upon determining that his broad knowledge and experience are vital to the Company’s management. | ||||||||||||

|

Kunitaro Saida

Date of birth May 4, 1943

Number of the Company’s shares held 11,200 shares

|

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||

As of | ||||||||||||

Apr. 1969: Appointed as Public Prosecutor | ||||||||||||

Feb. 2003: Superintending Prosecutor of Takamatsu High Public Prosecutors Office | ||||||||||||

Jun. 2004: Superintending Prosecutor of Hiroshima High Public Prosecutors Office | ||||||||||||

Aug. 2005: Superintending Prosecutor of Osaka High Public Prosecutors Office | ||||||||||||

May 2006: Retired from Superintending Prosecutor of Osaka High Public Prosecutors Office | ||||||||||||

Registered as an attorney (present) | ||||||||||||

Jun. 2007: Audit & Supervisory Board Member of NICHIREI CORPORATION | ||||||||||||

Jun. 2008: Director of Sumitomo Osaka Cement Co., Ltd. | ||||||||||||

Jun. 2010: Director of HEIWA REAL ESTATE CO., LTD. | ||||||||||||

Mar. 2014: Director (present) | ||||||||||||

[Important concurrent posts] | ||||||||||||

● Attorney

| ||||||||||||

| ||||||||||||

| [Reasons for being selected as a candidate and expected roles] | ||||||||||||

Mr. Kunitaro Saida has been serving as an attorney in corporate legal affairs subsequent to his distinguished career as Superintending Prosecutor of High Public Prosecutors Offices (in Takamatsu, Hiroshima and Osaka), and also has experience serving as an Outside Director and an Outside Audit & Supervisory Board Member for other companies. The Company has selected him as a candidate for Outside Director in hopes that he will furnish particularly useful advice drawing on his wealth of experience and high level of expertise regarding legal affairs when taking part in discussions on internal control mechanisms and corporate governance, including from the perspective of ensuring compliance.

| ||||||||||||

11

|

Yusuke Kawamura

Date of birth Dec. 5, 1953

Number of the Company’s shares held 500 shares

|

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||||||

As of | ||||||||||||||||

Apr. 1977: Entered Daiwa Securities Co. Ltd. | ||||||||||||||||

Jan. 1997: General Manager of Syndicate Department of Daiwa Securities Co. Ltd. | ||||||||||||||||

Apr. 2000: Professor of Faculty of Economics and the Graduate School of Economics of Nagasaki University | ||||||||||||||||

Apr. 2010: Senior Managing Director of Daiwa Institute of Research Ltd. | ||||||||||||||||

Jan. 2011: Commissioner of Fiscal System Council of Ministry of Finance | ||||||||||||||||

Apr. 2012: Deputy Chairman of Daiwa Institute of Research Ltd. | ||||||||||||||||

Feb. 2013: Commissioner of Business Accounting Council of Financial Services Agency (present) | ||||||||||||||||

Jun. 2017: Director of Mitsui Sugar Co., Ltd. (currently Mitsui DM Sugar Holdings Co., Ltd.) (present) | ||||||||||||||||

Apr. 2019: Executive Counselor of Japan Securities Dealers Association | ||||||||||||||||

Apr. 2020: Chairman & CEO of Institute of Glocal Policy Research (present) | ||||||||||||||||

Mar. 2021: Director (present) | ||||||||||||||||

[Important concurrent posts] ● Director of Mitsui DM Sugar Holdings Co., Ltd. ● Chairman & CEO of Institute of Glocal Policy Research | ||||||||||||||||

| ||||||||||||||||

[Reasons for being selected as a candidate and expected roles] | ||||||||||||||||

Mr. Yusuke Kawamura has a wealth of experience as an Outside Director along with capacity as an expert with respect to financial and securities systems as well as strategy for managing financial institutions, given that he worked at a securities company and subsequently served in various positions, including as a university professor, a commissioner of councils of Japan’s Ministry of Finance and Financial Services Agency, and an Executive Counselor of the Japan Securities Dealers Association. The Company has selected him as a candidate for Outside Director in hopes that he will furnish particularly useful advice drawing on his wealth of experience and high level of expertise regarding finance and securities, especially when taking part in discussions on M&A and ESG-related topics from a shareholder and investor perspective.

| ||||||||||||||||

Notes: | 1. | None of the candidates for the Directors have any special interest in the Company. | ||

2. | Mr. Kunitaro Saida and Mr. Yusuke Kawamura are candidates for Outside Directors defined by Item 7, Paragraph 3, Article 2 of the Enforcement Regulations of the Corporation Law of Japan. | |||

3. | At HEIWA REAL ESTATE CO., LTD. where Mr. Kunitaro Saida served as External Director until June 24, 2020, employee misconduct relating to real estate transactions was discovered, resulting in the aforesaid company’s recording of extraordinary loss in the second quarter of the fiscal year ended March 31, 2020, in association with that misconduct. Whereas he had been unaware of the misconduct up until its discovery, Mr. Kunitaro Saida has expressed his opinions on measures to prevent recurrence of any such incident, and otherwise has been appropriately making recommendations at the aforesaid company from the perspective of legal adherence and compliance-oriented management. | |||

4. | Although Mr. Kunitaro Saida and Mr. Yusuke Kawamura do not have the experience of being involved in the management of a company other than in a position of an outside director or outside audit & supervisory board member, the Company judges that they will appropriately perform their duties as Outside Director as outlined above in “Reasons for being selected as a candidate and expected roles.” | |||

5. | Mr. Kunitaro Saida will have served as Outside Director of the Company for eight years as of the end of this Meeting. Mr. Yusuke Kawamura will have served as Outside Director of the Company for one year as of the end of this Meeting. | |||

6. | The Company has entered into contracts with Mr. Kunitaro Saida and Mr. Yusuke Kawamura limiting the amount of their damage compensation liabilities defined in Paragraph 1, Article 423 of the Corporation Law of Japan to the limit prescribed by laws and regulations. Should they be elected to the position of Director, the Company will continue the aforementioned contract with them. | |||

7. | The Company has entered into a directors and officers liability insurance contract with an insurance company as specified in the provision of Paragraph 1, Article 430-3 of the Corporation Law of Japan, whereby the Company’s Directors serve as the insured parties. The insurance covers damages that could arise under situations where an insured party bears liability in regard to performance of his or her duties or where the insured party becomes subject to a claim seeking to hold him or her liable in that regard. Every Director candidate is to be insured under the directors and officers liability insurance contract should they be elected. The contract is to be renewed in September 2022. | |||

8. | The Company has notified Mr. Kunitaro Saida and Mr. Yusuke Kawamura as independent directors to each stock exchange in Japan on which the Company is listed as provided under the regulations of each stock exchange. Should they be elected to the position of Director, the Company will continue to make both of them independent directors. Although the Company has compensated Mr. Kunitaro Saida for his advisory services rendered prior to him having assumed the post of Director of the Company, the remuneration was not substantial given that it amounted to no more than 12 million yen annually, and his contract in that regard has already expired. Accordingly, the Company judges that his independence is not affected by the aforesaid circumstances. | |||

Additional Note for English Translation: | ||||

Mr. Fujio Mitarai, Mr. Toshizo Tanaka and Mr. Toshio Homma are Representative Directors. | ||||

Candidate no. 5 outside director independent director reappointed

12

Item No.4: Election of Two Audit & Supervisory Board Members

The terms of office of Audit & Supervisory Board Members Mr. Ryuichi Ebinuma and Mr. Koichi Kashimoto will expire at the end of this Meeting. Accordingly, we propose the election of two Audit & Supervisory Board Members.

The Company has a basic policy to have Audit & Supervisory Board Members that are familiar with the Company’s businesses or its management structure, or that have extensive knowledge in specialized areas such as law, finance and accounting. The candidates for Audit & Supervisory Board Member, based on this basic policy, are as follows:

Prior to our proposal of this item, we have already obtained the consent of the Audit & Supervisory Board.

|

|

Katsuhito Yanagibashi

Date of birth Aug. 25, 1957

Number of the Company’s shares held 4,200 shares

|

Brief personal record, position and important concurrent posts

| |||||||||||||

As of

| ||||||||||||||||

Apr. 1980: Entered the Company

| ||||||||||||||||

Jan. 2007: General Manager of Consolidated Accounting Division of Finance & Accounting Headquarters

| ||||||||||||||||

Jan. 2010: Senior General Manager of Global Accounting Planning Administration Center of Finance & Accounting Headquarters

| ||||||||||||||||

Jan. 2013: Senior General Manager of Accounting Standards & System Promotion Center of Finance & Accounting Headquarters

| ||||||||||||||||

Jan. 2017: Senior Principal of Finance & Accounting Headquarters

| ||||||||||||||||

Newly appointed

| Jun. 2017: Audit & Supervisory Board Member of Toshiba Medical Systems Corporation (currently Canon Medical Systems Corporation) | |||||||||||||||

Aug. 2017: Left the Company

| ||||||||||||||||

Mar. 2021: Advisor of Canon Medical Systems Corporation (present) | ||||||||||||||||

| ||||||||||||||||

[Reasons for being selected as a candidate] | ||||||||||||||||

Mr. Katsuhito Yanagibashi engaged in practical aspects of consolidated financial settlement and other such duties of the Company’s accounting operations over many years, and has furthermore served as a supervisor in charge of developing and promoting internal control systems related to group-wide finance, and as Audit & Supervisory Board Member of a core company of the Canon Group. Given that he has a wealth of expertise related to finance, corporate accounting and internal controls based on such experience, the Company has selected him as a candidate for Audit & Supervisory Board Member in hopes that he will utilize such expertise in improving the appropriateness of audits.

| ||||||||||||||||

|

|

Koichi Kashimoto

Date of birth Jul. 2, 1961

Number of the Company’s shares held 2,900 shares

|

Brief personal record, position and important concurrent posts

| |||||||||||||

As of

| ||||||||||||||||

Apr. 1984: Entered The Dai-ichi Mutual Life Insurance Company

| ||||||||||||||||

Apr. 1997: Manager of Government Relations Dept. of The Dai-ichi Mutual Life Insurance Company

| ||||||||||||||||

Apr. 2005: General Manager of Corporate Administration Center of The Dai-ichi Mutual Life Insurance Company

| ||||||||||||||||

Apr. 2009: Managing Director of Dai-ichi Life International (Europe) Limited

| ||||||||||||||||

Apr. 2012: General Manager of Secretarial Dept. of The Dai-ichi Life Insurance Company, Limited

| ||||||||||||||||

Apr. 2016: Senior General Manager of Secretarial Dept. (in charge of Secretarial Dept. and General Affairs Dept.), and Senior General Manager of Group General Affairs Unit of The Dai-ichi Life Insurance Company, Limited

| ||||||||||||||||

Outside Audit & Supervisory Board Member | Oct. 2016: Senior General Manager of Secretarial Dept. (in charge of Secretarial Dept. and General Affairs Dept.) of The Dai-ichi Life Insurance Company, Limited, and Senior General Manager and Chief of General Affairs Unit of Dai-ichi Life Holdings, Inc.

Mar. 2018: Audit & Supervisory Board Member (present) | |||||||||||||||

| ||||||||||||||||

Independent Audit & Supervisory Board Member | ||||||||||||||||

| ||||||||||||||||

[Reasons for being selected as a candidate] | ||||||||||||||||

Mr. Koichi Kashimoto has, over many years, been involved in business management of a major life insurance company, has served as a supervisor of general affairs including legal affairs, and furthermore has extensive international experience. The Company has selected him as a candidate for Outside Audit & Supervisory Board Member given expectations that he will utilize such knowledge and experience in performing audits encompassing the Canon Group, including its overseas operations.

| ||||||||||||||||

Candidate no. 1 Candidate no. 2 outside director independent director

13

Notes: | 1. | None of the candidates have any special interest in the Company. | ||

2. | Mr. Koichi Kashimoto is a candidate for Outside Audit & Supervisory Board Member defined by Item 8, Paragraph 3, Article 2 of the Enforcement Regulations of the Corporation Law of Japan. | |||

3. | Although Mr. Koichi Kashimoto does not have the experience of being involved in the management of a company other than in a position of an outside audit & supervisory board member, the Company judges that he will appropriately perform his duties as Outside Audit & Supervisory Board Member by utilizing experience and expertise he has gained in having served as a supervisor in charge of general affairs including legal affairs, in addition to his having engaged in business management of a major life insurance company, as outlined above. | |||

4. | Mr. Koichi Kashimoto will have served as Outside Audit & Supervisory Board Member of the Company for four years as of the end of this Meeting. | |||

5. | The Company has entered into a contract with Mr. Koichi Kashimoto limiting the amount of his damage compensation liabilities defined in Paragraph 1, Article 423 of the Corporation Law of Japan to the limit prescribed by laws and regulations. Should he be elected to the position of Audit & Supervisory Board Member, the Company will continue the aforementioned contract with him. | |||

6. | The Company has entered into a directors and officers liability insurance contract with an insurance company as specified in the provision of Paragraph 1, Article 430-3 of the Corporation Law of Japan, whereby the Company’s Audit & Supervisory Board Members serve as the insured parties. The insurance covers damages that could arise under situations where an insured party bears liability in regard to performance of his or her duties or where the insured party becomes subject to a claim seeking to hold him or her liable in that regard. Should each candidate be elected to the position of Audit & Supervisory Board Member, each person is to be insured under the directors and officers liability insurance contract. The contract is to be renewed in September 2022. | |||

7. | The Company has notified Mr. Koichi Kashimoto as an independent audit & supervisory board member to each stock exchange in Japan on which the Company is listed as provided under the regulations of each stock exchange. Should he be elected to the position of Audit & Supervisory Board Member, the Company will continue to make him an independent audit & supervisory board member. Moreover, The Dai-ichi Life Insurance Company, Limited, to which he belonged in the past, is a shareholder of the Company, and its shareholding ratio is approximately 2.3% (the shareholding ratio is calculated by deducting the number of treasury shares from total shares issued). In addition, although there are transactions based on insurance contracts between the aforesaid company and the Company, the annual gross amount of these transactions is less than 1% of either the Company’s or the aforesaid company’s annual net sales. Accordingly, the Company judges that his independence is not affected by the aforesaid circumstances. |

14

[Reference]

“Independence Standards for Independent Directors/Audit and Supervisory Board Members” of the Company

The Company has established the “Independence Standards for Independent Directors/Audit and Supervisory Board Members” resolved by the Board of Directors with the consent of all Audit and Supervisory Board Members, in order to clarify the standards for ensuring independence of Independent Directors/Audit and Supervisory Board Members of the Company, taking into consideration Japan’s Corporate Governance Code (Principle 4.9) and the independence criteria set by securities exchanges in Japan.

Independence Standards for

Independent Directors/Audit and Supervisory Board Members

Canon Inc. deems that a person who satisfies the requirements for Outside Directors/Audit and Supervisory Board Members prescribed by the Corporation Law of Japan, and meets the independence criteria set by securities exchanges in Japan, and does not fall into any of the items below, is an “Independent Director/Audit and Supervisory Board Member” (a person who is independent from the management of Canon Inc. and unlikely to have conflicts of interest with general shareholders).

1. | A person/organization for which Canon Group (Canon Inc. and its subsidiaries; hereinafter the same) is a major client, or a major client of Canon Group, or an executing person of such organization or client | |||||

2. | A major lender to Canon Group, or an executing person of such lender | |||||

3. | A large shareholder of Canon Inc., or an executing person of such shareholder | |||||

4. | A person/organization receiving large amounts of contributions from Canon Group, or an executing person of such organization | |||||

5. | A consultant, accounting professional or legal professional who has received a large amount of money or other properties from Canon Group, other than as compensation for being a director/Audit and Supervisory Board Member (if the recipient is a corporation, partnership or any other organization, this item applies to any person belonging to said organization.) | |||||

6. | A certified public accountant belonging to the audit firm engaged to conduct the statutory audit of Canon Group (including any such accountant to whom this item has applied in the last 3 business years) | |||||

7. | An executing person of another company in cases where an executing person of Canon Group is an outside director/Audit and Supervisory Board Member of such other company | |||||

8. | An immediate family member (spouse and a relative within the second degree of kinship) of any of the persons listed in each of items 1 to 7; provided, however that the persons to whom this is applicable shall be limited to key executing persons such as directors, executive officers of companies and partners of advisory firms | |||||

(Notes) | ||||||

* | In item 1, “major” means in cases where the total amount (for any business year during the last 3 business years) of transactions between Canon Group and such client exceeds 1% of the consolidated sales of Canon Group or such client. | |||||

* | In item 2, “major” means in cases where the debt outstanding exceeds 1% of the consolidated total assets of Canon Inc. for any business year during the last 3 business years. | |||||

* | In item 3, “a large shareholder” means a shareholder who directly or indirectly holds 5% or more of the total voting rights of Canon Inc. | |||||

* | In item 4, “a large amount” means in cases where the total amount of contributions exceeds JPY 12 million (in cases where the recipient is an individual) or 1% of the annual gross income of such recipient (in cases where the recipient is an organization), for any business year during the last 3 business years of Canon Inc. | |||||

* | In items 1 to 4 and 7, an “executing person” means an executive director, executive officer and employee including manager (in items 1 to 4, including a person to whom this item has applied in any business year during the last 3 business years). | |||||

* | In item 5, “a large amount” means in cases where the total amount of money or other properties received by said consultant, etc., exceeds JPY 12 million (in cases where the recipient is a person) or 1% of the annual gross sales of such consultant, etc. (in cases where the recipient is an organization), for any business year during the last 3 business years of Canon Inc. |

15

Item No.5: Grant of Bonus to Directors

We propose that bonus be granted to the three Directors excluding Outside Directors as of the end of this term, which totals 231,900,000 yen.

Remuneration for Directors consists of a basic remuneration, a bonus, and stock-type compensation stock options.

The Nomination and Remuneration Advisory Committee has furnished its confirmation with respect to the aforementioned bonus amount, in accordance with the “Policy on Decisions on the Content of Remunerations for Individual Directors” (pages 33 to 34), stipulated at the meeting of the Board of Directors held on January 18, 2021.

16

(Materials delivered pursuant to Article 437 and Article 444 of the Corporation Law of Japan)

BUSINESS REPORT (From January 1, 2021 to December 31, 2021)

1. Current Conditions of the Canon Group

(1) Business Progress and Results

General Business Conditions

The global economy during the 121st Business Term (from January 1, 2021 to December 31, 2021) remained on track toward recovery overall, albeit the trend has varied depending on the country and region, amid a gradual turnaround in economic activity associated with progress achieved with measures taken to address COVID-19 in respective countries along with easing of restrictions imposed on freedom of movement. However, inflation has risen worldwide given the emergence of pressure on distribution due to labor shortages and other such factors, in addition to stagnating production affecting numerous manufacturers largely due to shortages of materials.

As for exchange rates, the yen depreciated against both the U.S. dollar and the euro on an annual average basis compared with the previous term.

Amid such circumstances, the Canon Group endeavored to secure sales and profits in part by raising prices and focusing on sales of products with high profit margins in an attempt to offset adverse effects of production reductions and higher costs of procurement and distribution.

Turning to the state of our businesses, unit sales of office multifunction devices (MFDs) exceeded those of the previous term despite our having encountered shortages of semiconductor components. Meanwhile, sales of related services and consumable supplies mounted a recovery in alignment with a situation where business activities have gradually normalized.

Laser printers and inkjet printers achieved higher sales despite the emergence of difficulties in supplying products due to production reductions brought about by the resurgence of COVID-19 infections in Southeast Asia.

Four New Businesses Where Future Growth is Expected

| ||||

Commercial Printing

| Network Cameras

|

|

| |||

Sheet-fed presses that realize high image quality with a wide variety of media |

Network cameras that meet safety and security needs |

17

Interchangeable-lens digital cameras encountered an increase in sales, backed by continuing strong sales of full-frame mirrorless cameras along with strong results from interchangeable lenses amid expansion of the product lineup. Sales of network cameras also increased as a result of efforts to increase sales in terms of tapping growing demand brought about by an increasingly diverse range of applications.

In medical equipment, sales increased due to factors that include growing demand in Japan against a backdrop of government measures to support medical institutions, rising demand in North America, and sales of equipment such as computed tomography (CT) systems and diagnostic ultrasound systems. In September, the Company brought Redlen Technologies Inc. of Canada into the Canon Group, thereby gaining access to its cutting-edge semiconductor technology, instrumental in developing next-generation CT systems that will lead to dramatic progress in tomography capabilities.

Unit sales of semiconductor lithography equipment exceeded those of the previous term amid firm performance underpinned by aggressive capital investment among semiconductor manufacturers. Meanwhile, against a backdrop of steady panel demand, unit sales of FPD (Flat Panel Display) lithography equipment also greatly surpassed those of the previous term as restrictions on installation activities in the previous term were eased.

As a result of the above, consolidated net sales for this term was 3,513.4 billion yen (up 11.2% from the previous term). Consolidated income before income taxes was 302.7 billion yen (up 132.4% from the previous term). Consolidated net income attributable to Canon Inc. was 214.7 billion yen (up 157.7% from the previous term).

Medical

| Industrial Equipment

| |

|

| |

| MRI systems that realize both high image quality and shorter examination time | OLED display manufacturing equipment that possesses overwhelming competitive strength |

18

Highlights of Results

| · | During this term, the global economy generally remained on a path of recovery, as economic activity gradually recovered, largely due to the progress of measures against COVID-19 in various countries. In such an environment, consolidated net sales increased by 11.2% year on year owing to recovery of demand in each business unit, including ongoing strong demand for mirrorless cameras and lithography equipment. |

| · | In addition, consolidated net income attributable to Canon Inc. increased by 157.7% year on year as a result of structural reforms implemented thus far and group-wide improvements in productivity. |

Notes: | 1. | From this term, Canon has changed the name and structure of segments to Printing Business Unit, Imaging Business Unit, Medical Business Unit, and Industrial and Others Business Unit. The same restatement has been applied in relation to the previous terms. | ||

| 2. | The totals do not amount to 100% because the consolidated sales of each business unit include the sales relating to intersegment transactions. | |||

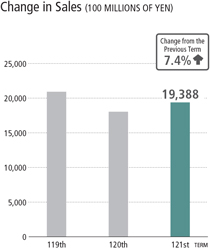

Changes in net sales and profits net sales (100 millions of yen) income before income taxes (100 millions of yen) net income attributable to canon inc. (100 millions of yen) 50,000 40,000 30,000 20,000 10,000 117th 118th 119th 120th 121th 35,134 3,027 2,147 constitution of sales by region constitution of sales by operations 23.3% sales 8,192 americas 27.6% sales 9,688 japan 23.6% sales 8,304 europe 25.5% sales 8,949 industrial and others business unit 15.5% sales 5,457 change from the previous term 18.2% printing business unit 55.2% sales 19,388 change from the previous term 7.4% medical business unit 13.7% sales 4,804 change from the previous term 10.2% imaging business unit 18.6% sales 6,535 change from the previous term 20.7% total sales 35,134 change from the previous term 11.2%

19

Business Conditions by Operations

Printing Business Unit

In office MFDs, we encountered lulls in production largely due to the shortage of semiconductor components, yet sales increased with unit sales having exceeded those of the previous term amid recovering demand that had fallen due to the COVID-19 pandemic, in addition to the recovery in demand for services and consumable supplies in step with a gradual normalization of business activities.

As for products for the Prosumer market, sales in the laser printer category increased due to strong performance of consumable supplies, and despite unit sales having underperformed those of the previous term due to production reductions among Southeast Asian production sites associated with the spread of COVID-19. Likewise with inkjet printers, even with unit sales having decreased due to production reductions, sales exceeded those of the previous term as a result of having been buoyed by firm home-use demand in addition to focus having been placed on sales of products with high profit margins.

Sales increased with respect to products for the production printing market amid firm performance of machines, services and consumable supplies.

As a result, on a consolidated basis, sales for this business unit increased by 7.4% to 1,938.8 billion yen in comparison to the previous term.

change in sales (100 millions of yen)

20

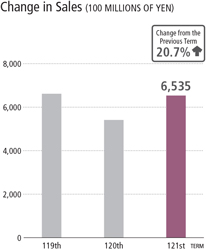

Imaging Business Unit

In interchangeable-lens digital cameras, the EOS R5 and EOS R6 full-frame mirrorless cameras continued to sell well. Launched during the fourth quarter of this term, the EOS R3 featuring the high reliability and performance sought by professional photographers and advanced amateurs was well received. Unit sales of digital cameras overall remained on par with those of the previous term as a result of product supply having been affected by the semiconductor component shortage. However, sales exceeded those of the previous term due to strong performance of highly profitable models and sales of RF-series interchangeable lenses for the EOS R system increased significantly amid expansion of the product lineup.

In network cameras, we encountered issues with product supply against a backdrop of component shortages. However, amid the likelihood of further market expansion against a backdrop of an increasing range of applications for purposes other than crime prevention and disaster monitoring, sales increased as a result of our aggressive engagement in providing video analysis and management software and expanding the visual solutions business, while taking on efforts to enhance sales activities.

As a result, on a consolidated basis, sales for this business unit increased by 20.7% to 653.5 billion yen in comparison to the previous term.

change in sales (100 millions of yen)

21

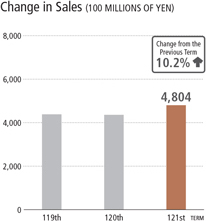

Medical Business Unit

Although the shortage of semiconductors and other components weighed on the production of medical equipment, unit sales of CT systems and diagnostic ultrasound systems increased steadily, particularly in Japan where robust demand was underpinned by the government’s measures to support medical institutions and in North America where a strengthened sales framework contributed to the result, amid ongoing economic recovery there.

Orders have been increasing since the latter half of the year amid recovery in demand for large-scale equipment such as angiography systems and Magnetic Resonance Imaging (MRI) systems, in addition to CT systems and diagnostic ultrasound systems.

We have developed and launched a new generation of CT systems designed to provide minimally invasive, low-noise and super-resolution imaging enlisting technology developed utilizing AI in the fourth quarter.

As a result, on a consolidated basis, sales for this business unit increased by 10.2% in comparison to the previous term to a record-high of 480.4 billion yen.

change in sales (100 millions of yen)

22

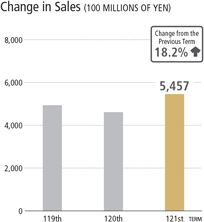

Industrial and Others Business Unit

Unit sales of semiconductor lithography equipment exceeded those of the previous term amid continuance of active capital investment among semiconductor manufacturers against a backdrop of heightening semiconductor demand across a wide range of fields including data centers, electric vehicles (EV), and the IoT-related domain. In addition, unit sales of FPD lithography equipment significantly exceeded those of the previous term, which had been subject to a lull in installations largely due to overseas travel restrictions associated with the spread of COVID-19. The increase in unit sales is attributable to robust demand for display panels for PCs and tablet devices due to remote work arrangements becoming more common and escalating stay-at-home demand. Sales of OLED display manufacturing equipment underperformed those of the previous term partially due to customer adjustments to capital investment schedules.

As a result, on a consolidated basis, sales for this business unit increased by 18.2% to 545.7 billion yen in comparison to the previous term.

change in sales (100 millions of yen)

23

(2) Facilities Investment

The investment in facilities by the Canon Group during this term totaled 151.9 billion yen (57.8 billion yen by the Company), which are mainly as follows:

Main facilities completed during this term | Main facilities under construction for establishment / expansion as of the end of this term | |

Canon Mold Co., Ltd.: | Canon Inc.: | |

| New Production Base | New Production Base of Hiratsuka Plant | |

| (Industrial and Others Business Unit) | (Industrial and Others Business Unit) | |

| Location: Kasama-shi, Ibaraki Pref., Japan | Location: Hiratsuka-shi, Kanagawa Pref., Japan | |

| Date of Completion: April, 2021 | ||

| *Leased to Canon Mold Co., Ltd. by the Company | ||

(3) Business Challenges and Countermeasures

Last year (the 121st Business Term), the Canon Group started a new five-year management plan, Phase VI (2021 to 2025) of the “Excellent Global Corporation Plan,” and under our basic policy to “accelerate our corporate portfolio transformation by improving productivity and creating new businesses,” we reorganized our business divisions and group companies into four industry-oriented business groups of “Printing,” “Imaging,” “Medical,” and “Industrial” in order to further promote the transformation of the business portfolio whose foundation was established in Phase V (2016 to 2020). We also launched a new organization to accelerate the commercialization of, among others, a materials business and sales of components such as sensors to outside businesses.

During the past year, which was the first year of Phase VI, many production sites of the Canon Group closed temporarily due to lockdowns as the global COVID-19 pandemic continued without being contained. We were also forced to reduce production due to shortages of materials, mainly for semiconductors, and logistics disruptions. However, because economic activities resumed with increased availability of vaccinations, we were able to achieve an increase in both sales and profits through responding to a recovery in demand.

As we enter this year, although there are still no projections as to when the COVID-19 pandemic will be brought under control and disruptions in production and logistics are expected to continue, we believe that the fundamentals of the Canon Group’s business environment are sound and have not changed from last year. Accordingly, under the basic policy of Phase VI that we have been carrying out since the past year, we will focus on the following measures.

| 1. | Thoroughly strengthen competitiveness of industry-oriented business groups |

While creating new businesses by combining technologies, revising the business domains, and utilizing M&A and other measures for each industry-oriented business group, as well as by strengthening the development, production, and sales framework, we will thoroughly enhance business competitiveness.

| 1) | Printing Group |

In the age of digital transformation (DX), although the shift to paperless documents will continue in the future given that the volume of printed pages at offices is being reduced as much as possible, printing demand is expected to remain steady based on the need to share ideas and work results. Due to the spread of the COVID-19, the adoption of hybrid working styles that combine office work with teleworking is accelerating and there are demands to utilize cloud computing, etc. for providing printing environments and services not constrained to a certain workplace. The Canon Group aims to be No. 1 in the world in the office and home printing field by utilizing two digital printing technologies, namely electrophotographic technology as well as inkjet technology, and the strengths of its worldwide sales and service network, and by focusing on providing printing solutions that meet the needs of the DX age. |

24

In addition, in the fields of catalog printing and other commercial printing and label printing, package printing and other industrial printing where there is expected to be a further shift from analog to digital in the future, we will take this opportunity to enhance workflow software that contributes to labor savings and supports increases in added value, as well as to introduce new competitive products to the market one after the other utilizing the collective strengths of the entire group and establish a strong position. |

| 2) | Imaging Group |

Although the overall market for digital cameras has shrunk significantly due to the widespread use of smartphones, sales of mirrorless cameras equipped with full-frame sensors were strong even during the COVID-19 pandemic and demand for high image quality photos was steady. As a company with the world’s leading optical technology, the Company will continue to introduce cameras and interchangeable lenses to the market one after the other according to this demand, and establish its position as No. 1 in the world for mirrorless cameras by focusing on professional photographers and advanced amateurs who value “high image quality.” In addition, given the increasing use and application of virtual reality images, 3D images and 360° images in various fields recently, we are working to capture these new video-experience markets using the Free Viewpoint Video System, the EOS VR System, which was introduced last year, and MREAL, etc., in order to expand the business. |

In the broadcasting and video production field, we will strengthen our lineup of high image quality remote camera systems in accordance with the continuing increase in IP streaming demand. |

In the network camera field, the Company will strengthen its presence in the security field, including for smart cities, utilizing the collective strength of the entire group, which includes Axis, one of the world’s leading manufacturers, Milestone Systems, a video management software vendor, and BriefCam, a video analytics software vendor. At the same time, for quality inspection work at production sites, out-of-stock detection at distribution centers, crowd level detection at shops and exhibition sites and other such uses go beyond the original scope of security, we are working on developing products and services that provide DX solutions that utilize video for various operations. |

In the mobility field which is undergoing tremendous changes, such as autonomous vehicles, we are working on entering the in-vehicle camera and traffic infrastructure businesses by leveraging the optical and network technology that the Company has refined over its long history, and will contribute to the widespread use of driving support and other mobility services. |

| 3) | Medical Group |

In order to respond to medical treatments that are becoming more advanced, we will expand the business domains to include healthcare IT and in vitro diagnostics with the diagnostic imaging business as the core, aiming to contribute to medical treatment around the world. |

In the diagnostic imaging business, we will utilize Redlen, which was acquired last year, in order to promote development of photon-counting CT technology that makes it possible to achieve both unprecedented diagnostic functions and a significant reduction in radiation exposure, and are focused on early commercialization. In addition, by using Quality Electrodynamics’s RF coil technology, which is a core technology for MRI systems, and other original technologies of the group companies, as well as by applying image-processing technologies, etc. that utilize AI, we will develop the next-generation high-performance MRI systems. In diagnostic ultrasound systems, we will work to reduce costs by standardizing platforms, bringing production in-house and utilizing Canon’s production technology. Furthermore, by strengthening the sales network, with a particular focus on the United States, we aim to have the No. 1 global market share for CT systems and be in the world’s top group for other diagnostic imaging systems. |

25

In the healthcare IT field, by enabling medical institutions to integrate image and non-image data collected in clinical settings, analyze and process the data utilizing AI and other technologies and provide the data worldwide, we aim to offer high-quality diagnostic support and facilitate efficient medical treatment. In addition, in the in vitro diagnostics field, we will expand our portfolio into domains on the periphery of diagnostic equipment, such as test reagents for COVID-19, and expand the business. |

In the component business, we will expand the existing business by cultivating new customers, consolidating sales functions, etc., and while also looking at growth opportunities through M&A, we will offer multi-layered solutions, comprised of completed products, modules, processes, services, etc., aiming to expand the BtoB business, whose sales account for 10% or more of the total sales of the Medical Group. |

| 4) | Industrial Group |

Given the widespread use of the 5G communications standard and cloud computing, demand for semiconductors, such as IC and memory chips, is expected to continue growing in the future. In addition, due to the increase in individualized listening, viewing and learning using online distribution and the shift to images with higher resolution, demand for LCD panels and OLED panels is expected to be strong. Production of the Canon Group’s semiconductor manufacturing equipment, FPD lithography equipment and OLED display manufacturing equipment is continuing at almost full capacity. Recognizing that our ability to respond flexibly to increased demand is an important issue, we will enhance the production system utilizing the collective strength of the entire group and strengthen our customer support system. In addition, we will increase our product strengths through improved performance and additional functions that contribute to raising customer productivity, and work to expand our market share. |

At the same time, we will promote technological development with a view to expanding the application of nanoimprint lithography technology, aiming for early commercialization, and focus on establishing next-generation manufacturing technology for OLED displays. Furthermore, we will create new products and services that combine core technologies in the group, such as ultra-precision positioning, ultra-precision processing and vacuum systems, and aim to expand the business domains by providing our customers with new value. |

| 2. | Improve group-wide productivity through extensive reinforcement of Canon’s global headquarter functions |

We will reaffirm our commitment to thorough cash flow management throughout the entire group and further strengthen the financial foundation. In Japan, we will improve the productivity of white-collar employees by redistributing human resources to growth areas in accordance with changes in the business portfolio and promoting highly streamlined work using DX and other measures. In addition, in order to rebuild the production system to create a resilient system integrated horizontally across the group, we are working to further increase automation and in-house production in all businesses through horizontal expansion of production technologies, and will continue striving to achieve thorough cost reductions.

With pursuing the above challenges in particular, the Canon Group aims to achieve net sales of 4,500.0 billion yen or more, an operating profit ratio of 12% or more, a net income ratio of 8% or more, and a shareholders’ equity ratio of 60% or more in 2025, which is the final year of Phase VI.

26

(4) Status of Assets and Earnings

117th Business Term (Jan. 1, 2017-Dec. 31, 2017) | 118th Business Term (Jan. 1, 2018-Dec. 31, 2018) | 119th Business Term (Jan. 1, 2019-Dec. 31, 2019) | 120th Business Term (Jan. 1, 2020-Dec. 31, 2020) | 121st Business Term (Jan. 1, 2021-Dec. 31, 2021) | |||||||||||||||||||||

Net Sales (100 millions of yen)

| 40,800 | 39,519 | 35,933 | 31,602 | 35,134 | ||||||||||||||||||||

Income before Income Taxes (100 millions of yen)

| 3,545 | 3,624 | 1,955 | 1,303 | 3,027 | ||||||||||||||||||||

Net Income Attributable to Canon Inc. (100 millions of yen)

| 2,421 | 2,524 | 1,250 | 833 | 2,147 | ||||||||||||||||||||

Basic Net Income Attributable to Canon Inc. Shareholders Per Share (yen)

| 223.03 | 233.80 | 116.79 | 79.37 | 205.35 | ||||||||||||||||||||

Total Assets (100 millions of yen)

| 52,016 | 49,030 | 47,719 | 46,256 | 47,509 | ||||||||||||||||||||

Total Canon Inc. Shareholders’ Equity (100 millions of yen)

| 28,640 | 28,206 | 26,855 | 25,750 | 28,738 | ||||||||||||||||||||

Notes: | 1. | Canon’s consolidated financial statements are prepared in accordance with U.S. generally accepted accounting principles. | ||

| 2. | Basic net income attributable to Canon Inc. shareholders per share is calculated based on the weighted average number of outstanding shares during the term. | |||

(5) Main Activities

The Canon Group is engaged in the development, manufacture and sales of the following products.

| Operations | Main Products | |||

Printing Business Unit | Office Multifunction Devices (MFDs), Document Solutions, Laser Multifunction Printers (MFPs), Laser Printers, Inkjet Printers, Image Scanners, Calculators, Digital Continuous Feed Presses, Digital Sheet-Fed Presses, Large Format Printers | |||

Imaging Business Unit | Interchangeable-Lens Digital Cameras, Interchangeable Lenses, Digital Compact Cameras, Compact Photo Printers, Network Cameras, Video Management Software, Video Content Analytics Software, Digital Camcorders, Digital Cinema Cameras, Broadcast Equipment, Multimedia Projectors | |||

Medical Business Unit | Computed Tomography (CT) Systems, Diagnostic Ultrasound Systems, Diagnostic X-ray Systems, Magnetic Resonance Imaging (MRI) Systems, Clinical Chemistry Analyzers, Digital Radiography Systems, Ophthalmic Equipment | |||

Industry and Others Business Unit | Semiconductor Lithography Equipment, FPD (Flat Panel Display) Lithography Equipment, OLED Display Manufacturing Equipment, Vacuum Thin-Film Deposition Equipment, Die Bonders, Handy Terminals, Document Scanners | |||

(6) Employees

| Consolidated | (Breakdown by Operation) | |||||||||||||||

Number of Employees | Office Business Unit | Imaging System Business Unit | Medical System Business Unit | Industry and Others Business Unit | Corporate | |||||||||||

| 184,034 persons | (Increase of 2,137 persons from the previous term) | 122,864 persons

| 25,761 persons

| 12,769 persons