FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

| For the month of …. | February | ………………………………………… , | 2023 |

CANON INC. | ||||

(Translation of registrant’s name into English) | ||||

30-2, Shimomaruko 3-Chome, Ohta-ku, Tokyo 146-8501, Japan | ||||

(Address of principal executive offices) | ||||

[Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

| Form 20-F | X | Form 40-F |

|

[Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

| Yes |

| No | X |

[If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b):82-....................

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

CANON INC. | ||

| (Registrant) |

| Date…. | February 27, 2023 | By ……/s/……… Sachiho Tanino………………… | ||||

| (Signature)* |

Sachiho Tanino | ||

General Manager | ||

Consolidated Accounting Division | ||

Canon Inc. |

*Print the name and title of the signing officer under his signature.

The following materials are included.

1. Notice of Convocation of the Ordinary General Meeting of Shareholders for the 122nd Business Term

2. Matters omitted from the Notice of Convocation of the Ordinary General Meeting of Shareholders for the 122nd Business Term

TRANSLATION Securities Code: 7751 Notice of Convocation of the Ordinary Photograph location: Fujikawaguchiko-machi, Minamitsuru-gun, Yamanashi Pref. General Meeting of Shareholders Photographed using: EOS R5 for the 122nd Business Term RF24-105mm F4 L IS USM DATE AND TIME March 30 (Thursday), 2023 at 10:00 a.m. (Japan time) (The reception will commence at 9:00 a.m.) PLACE Headquarters of the Company 30-2, Shimomaruko 3-chome, Ohta-ku, Tokyo MATTERS TO BE Item No.1 Dividend from Surplus RESOLVED Item No.2 Election of Five Directors Item No.3 Election of Two Audit & Supervisory Board Members Item No.4 Grant of Bonus to Directors

| Based on our philosophies of “a respect for humanity” and “an emphasis on original technology,” Canon was founded in 1937 as a camera manufacturer and continued to grow for 30 years under the high ideal of “building the world’s best cameras using our own technology.”

During the age of internationalization in the 1960s, we achieved further growth through structural transformation aimed at “globalization” and “diversification.”

In addition, as internationalization continued to expand around the world, we marked our 50th anniversary of the founding of the Company in 1987. In 1988, we announced our second inauguration and introduced the new corporate philosophy of “kyosei” (harmoniously living and working together with all people of the world).

In accordance with this philosophy of “kyosei,” Canon will continue its business activities aimed at corporate growth and development in the interest of world prosperity and the happiness of humankind.

|

Index |

NOTICE OF CONVOCATION OF THE ORDINARY GENERAL MEETING OF SHAREHOLDERS FOR THE 122ND BUSINESS TERM | P. 3 | |||||

Guidance Notes on the Exercise of Voting Rights via the Internet or in Writing | P. 5 | |||||

REFERENCE DOCUMENTS FOR | ||||||

GENERAL MEETING OF SHAREHOLDERS | ||||||

Propositions: | ||||||

Item No.1 - Dividend from Surplus | P. 7 | |||||

Item No.2 - Election of Five Directors | P. 8 | |||||

Item No.3 - Election of Two Audit & Supervisory Board Members | P. 12 | |||||

Item No.4 - Grant of Bonus to Directors | P. 14 | |||||

BUSINESS REPORT | ||||||

1. Current Conditions of the Canon Group | P. 15 | |||||

2. Shares of the Company | P. 28 | |||||

3. Directors and Audit & Supervisory Board Members | P. 29 | |||||

4. Accounting Auditor | P. 34 | |||||

5. Systems Necessary to Ensure the Properness of Operations | P. 35 | |||||

| CONSOLIDATED FINANCIAL STATEMENTS | ||||||

Consolidated Balance Sheets | P. 39 | |||||

Consolidated Statements of Income | P. 40 | |||||

| NON-CONSOLIDATED FINANCIAL STATEMENTS | ||||||

Non-Consolidated Balance Sheets | P. 41 | |||||

Non-Consolidated Statements of Income | P. 42 | |||||

| AUDIT REPORTS | ||||||

AUDIT REPORT OF ACCOUNTING AUDITOR | ||||||

ON CONSOLIDATED FINANCIAL STATEMENTS | P. 43 | |||||

AUDIT REPORT OF ACCOUNTING AUDITOR | P. 45 | |||||

AUDIT REPORT OF AUDIT & SUPERVISORY BOARD | P. 47 | |||||

| REFERENCE | ||||||

Sustainability Efforts | P. 49 | |||||

Topics | P. 51 | |||||

Information for Shareholders

|

| P. 53

|

| |||

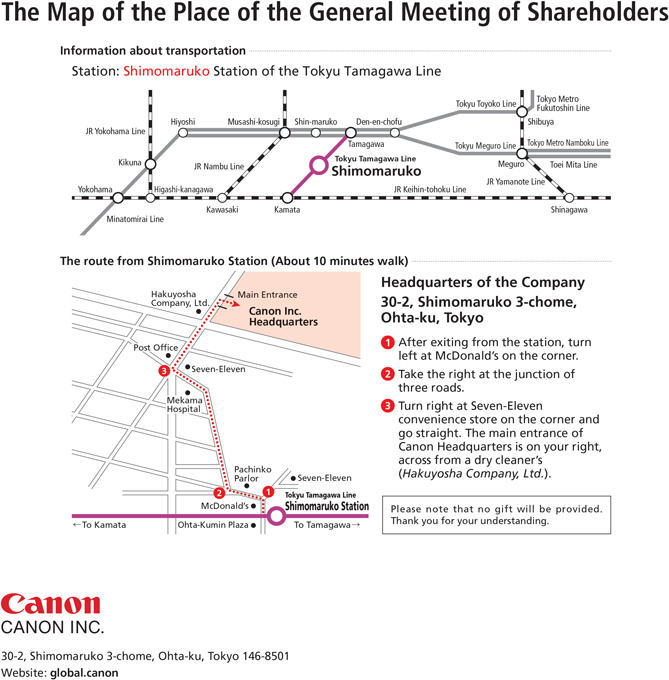

The Map of the Place of the General Meeting of Shareholders | ||||||

To Our Shareholders

|

| |||

We are pleased to present our notice of convocation of the Ordinary General Meeting of Shareholders for the 122nd Business Term (from January 1, 2022 to December 31, 2022). The global economy under the COVID-19 pandemic was, since the beginning of 2021, on a track of steady recovery, in terms of both demand and supply. In 2022, however, we encountered signs of economic slowdown emerging from the latter half of the year, due to factors that included soaring resource and energy prices prompted by Russia’s invasion of Ukraine, rising inflation due to shortages of goods and labor, and tightening of monetary policy undertaken to contain inflation.

Even under this challenging business environment, demand for our products remained firm overall, and by leveraging the collective strength of the entire Canon Group to supply products while contending with component supply shortages and logistical constraints, we recorded unit sales growth in each of our business groups. In addition to this, due to our high ratio of overseas sales, which is roughly 80%, and moving production back to Japan, a measure promoted even before the COVID-19 pandemic, the weaker yen acted as a tailwind. These factors led to significant sales and profit growth for the second consecutive year, and net sales surpassing the 4 trillion yen mark for the first time in five years.

For the year-end dividend, in appreciation for the continued support of our shareholders, we will propose a distribution of 60.00 yen per share at the Ordinary General Meeting of Shareholders for the 122nd Business Term. As such, our dividend for the year, including our interim dividend of 60.00 yen per share, will amount to 120.00 yen per share, thereby constituting an increase of 20.00 yen relative to our annual dividend for the 121st Business Term. |

Regarding the global economy in 2023, amid the persistent threat of COVID-19 and mounting geopolitical tensions, we project low growth, due to moves to tighten monetary policy in respective regions to rein in high prices. Although navigating the Company’s business through this difficult phase will continue, the Canon Group will work in a concerted effort to meet the challenges, and to achieve the goals of its five-year management plan, Phase VI (2021 to 2025) of the “Excellent Global Corporation Plan,” while aiming for its third consecutive year of sales and profit growth.

We look forward to our shareholders’ continued support and encouragement.

March, 2023

Chairman & CEO FUJIO MITARAI

|

Securities Code: 7751 March 6, 2023 |

TO OUR SHAREHOLDERS

| CANON INC. | ||||||

30-2, Shimomaruko 3-chome, Ohta-ku, Tokyo Chairman & CEO Fujio Mitarai |

NOTICE OF CONVOCATION OF THE ORDINARY GENERAL MEETING OF SHAREHOLDERS FOR THE 122ND BUSINESS TERM

Notice is hereby given that the Ordinary General Meeting of Shareholders for the 122nd Business Term of Canon Inc. (the “Company”) will be held as described below. Although we will hold the Meeting upon having appropriately taken measures to prevent the spread of COVID-19, please consider refraining from traveling to the Meeting venue on the date of the Meeting, taking into consideration your own physical condition and the situation regarding the spread of infection. As you can exercise your voting rights via the Internet or in writing, we strongly encourage you to do so if choosing not to travel to the Meeting venue on the date of the Meeting. The voting deadline via the Internet or in writing is 5:00 p.m. on March 29 (Wednesday), 2023 (Japan time). (If exercising your voting rights in writing, your vote must arrive at the manager of the register of shareholders no later than the aforementioned deadline). | ||||||

1. DATE AND TIME: |

March 30 (Thursday), 2023 at 10:00 a.m. (Japan time) | |||||

(The reception will commence at 9:00 a.m.)

| ||||||

2. PLACE: |

Headquarters of the Company | |||||

| 30-2, Shimomaruko 3-chome, Ohta-ku, Tokyo | ||||||

(Please see the map at the end of this notice.)

| ||||||

3. MATTERS CONSTITUTING |

Matters to be Reported: | |||||

1.���Reports on the contents of the Business Report and Consolidated Financial Statements for the 122nd Business Term (from January 1, 2022 to December 31, 2022), and reports on the Auditing Results of Accounting Auditor and Audit & Supervisory Board regarding the Consolidated Financial Statements. | ||||||

2. Reports on the content of the Non-Consolidated Financial Statements for the 122nd Business Term (from January 1, 2022 to December 31, 2022). | ||||||

| Matters to be Resolved upon: | ||||||

Propositions: | ||||||

Item No.1 - Dividend from Surplus | ||||||

Item No.2 - Election of Five Directors | ||||||

Item No.3 - Election of Two Audit & Supervisory Board Members | ||||||

Item No.4 - Grant of Bonus to Directors

|

3

| 1. | Measures for Electronic Provision of the Shareholders Meeting Reference Documents |

Upon convening the Meeting, the Company takes Measures for Electronic Provision (on the websites listed below) of the information that includes the contents of Reference Documents for General Meeting of Shareholders, Business Report, Consolidated Financial Statements and Non-Consolidated Financial Statements pursuant to provisions of the Companies Act and the Company’s Articles of Incorporation. Please note, however, that regardless of whether or not a Request for Delivery of Documents is made pursuant to the Companies Act, the Company sends this information to shareholders in paper-based form as before. |

(1) Company’s website (“Shareholders’ Meeting” page of the “Investor Relations” section) | ||

Please access the website below and see “The Ordinary General Meeting of Shareholders for the 122nd Business Term (March 30, 2023)” https://global.canon/en/ir/share/meeting.html | ||

(2) Tokyo Stock Exchange website (Listed Company Search) | ||

Please access the website below, input “Canon” into “Issue name (company name)” or “7751” into “Code,” click “Search,” then “Basic information” of Canon Inc. and select “Documents for public inspection/PR information,” “Notice of General Shareholders Meeting/Informational Materials for a General Shareholders Meeting.” https://www2.jpx.co.jp/tseHpFront/JJK020010Action.do?Show=Show |

| 2. | Documents not included in this Notice of Convocation |

The following documents are not included in this Notice of Convocation: “Stock Acquisition Rights etc. of the Company” of the Business Report; “Consolidated Statement of Equity” and “Notes to Consolidated Financial Statements” of the Consolidated Financial Statements; and “Non-Consolidated Statement of Changes in Net Assets” and “Notes to Non-Consolidated Financial Statements” of the Non-Consolidated Financial Statements. These documents are posted on each of the websites described in 1. above as “Matters Omitted from the Notice of Convocation of the Ordinary General Meeting of Shareholders for the 122nd Business Term.” Please access one of the websites to read them. |

These matters have been subject to audit, whereby the Audit & Supervisory Board Members have prepared the Audit Report of Audit & Supervisory Board and the Accounting Auditor has prepared the Audit Report of Accounting Auditor. |

| 3. | Changes in the contents of Shareholders Meeting Reference Documents |

Any changes in information that includes the contents of Reference Documents for General Meeting of Shareholders, Business Report, Consolidated Financial Statements and Non-Consolidated Financial Statements will be posted on each of the websites described in 1. above. |

| 4. | Cautionary matters concerning attending the Meeting in person |

| (1) | Upon attending the Meeting, please present the Voting Form delivered by the Company to the receptionist at the place of the Meeting. |

| (2) | Shareholders at the Meeting will be subject to temperature checks performed prior to reception. Please be aware that those showing signs of fever or poor physical health may be refused to enter the Meeting venue. |

| (3) | Shareholders in attendance will be asked to use hand sanitizer and wear a face mask. |

| (4) | There is to be extra distance between seating at the Meeting venue. Also, the number of shareholders allowed entry into the Meeting venue may be limited depending on the number of shareholders who visit. We appreciate your understanding in this regard. |

| (5) | Please note that no commemorative items or gifts, etc. will be provided for shareholders attending the Meeting in person. |

| 5. | Exercise of voting rights via the Internet or in writing |

Please refer to “Guidance Notes on the Exercise of Voting Rights via the Internet or in Writing” on the following page. |

4

Guidance Notes on the Exercise of Voting Rights via the Internet or in Writing

Shareholders may exercise their voting rights prior to the Meeting via the Internet or in writing (using the Voting Form), instead of attending the Meeting in person.

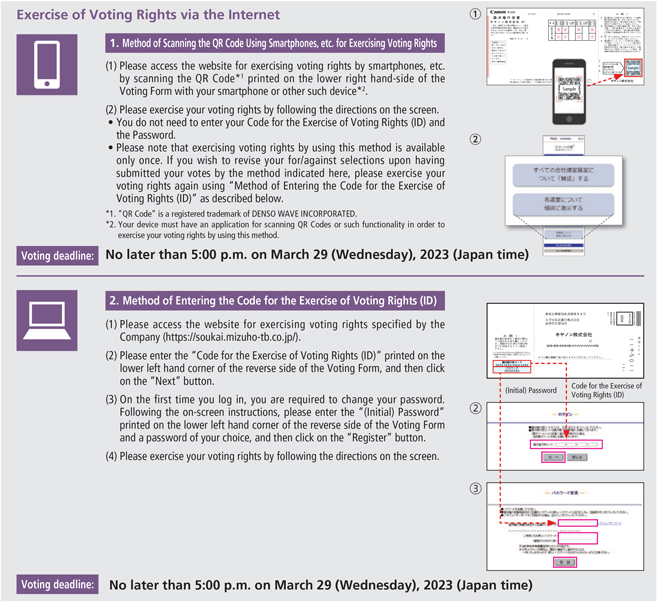

Exercise of Voting Rights via the Internet 1. Method of Scanning the QR Code Using Smartphones, etc. for Exercising Voting Rights (1) Please access the website for exercising voting rights by smartphones, etc. by scanning the QR Code*1 printed on the lower right hand-side of the Voting Form with your smartphone or other such device*2. (2) Please exercise your voting rights by following the directions on the screen. • You do not need to enter your Code for the Exercise of Voting Rights (ID) and the Password. • Please note that exercising voting rights by using this method is available only once. If you wish to revise your for/against selections upon having submitted your votes by the method indicated here, please exercise your voting rights again using “Method of Entering the Code for the Exercise of Voting Rights (ID)” as described below. *1. “QR Code” is a registered trademark of DENSO WAVE INCORPORATED. *2. Your device must have an application for scanning QR Codes or such functionality in order to exercise your voting rights by using this method. Voting deadline: No later than 5:00 p.m. on March 29 (Wednesday), 2023 (Japan time) 2. Method of Entering the Code for the Exercise of Voting Rights (ID) Please access the website for exercising voting rights specified by the Company (https://soukai.mizuho-tb.co.jp/). Please enter the “Code for the Exercise of Voting Rights (ID)” printed on the lower left hand corner of the reverse side of the Voting Form, and then click on the “Next” button. On the first time you log in, you are required to change your password. Following the on-screen instructions, please enter the “(Initial) Password” printed on the lower left hand corner of the reverse side of the Voting Form and a password of your choice, and then click on the “Register” button. Please exercise your voting rights by following the directions on the screen. Voting deadline: No later than 5:00 p.m. on March 29 (Wednesday), 2023 (Japan time)

5

Exercise of Voting Rights in Writing (Using the Voting Form) Please indicate your for/against for each of the propositions on the Voting Form and send it to us by postal mail. (1) Please indicate your for/against for each of the propositions here. • Item No.2 and Item No.3 If you approve of all of the candidates: Mark the “” (for) box with a “” If you are opposed to all of the candidates: Mark the “” (against) box with a “” If you are opposed to some of the candidates: Mark the “” (for) box with a “,” and indicate the numbers for the candidates that you are opposed to In the event that your for/against of any proposition is not indicated on the Voting Form, the proposition shall be considered as an indication of for. (2) Please cut the form at the dotted line, and send this portion of the form by postal mail. (Please use the personal information security sticker on the Voting Form before sending it by postal mail.) Voting deadline: To arrive no later than 5:00 p.m. on March 29 (Wednesday), 2023 (Japan time) (Voting Forms that arrive at our manager of the register of shareholders (Mizuho Trust & Banking Co., Ltd.) no later the aforementioned deadline shall be deemed valid.)

| 1. | Treatment of Voting Rights Which Are Exercised More Than Once |

| • | If you exercise your voting rights twice, via the Internet and in writing, we will only accept the exercise of your voting rights via the Internet as effective. |

| • | If you exercise your voting rights more than once via the Internet, we will only accept the last exercise of your voting rights as effective. |

| 2. | Other Notes Regarding the Exercise of Voting Rights via the Internet |

| • | The cost of Internet access (access fees to providers, telecommunications fees, etc.) shall be borne by the shareholders. |

| • | Although each of the methods concerning the exercise of voting rights via the Internet has been operationally verified on standard devices connected to the Internet, in some cases, it may not be possible to gain access using certain devices or due to certain circumstances. |

| 3. | For Inquiries with Respect to the Exercise of Voting Rights via the Internet |

Please contact: |

Stock Transfer Agency Department of Mizuho Trust & Banking Co., Ltd.

Telephone: 0120-768-524 (toll-free, available in Japan only)

Operating Hours: 9:00 a.m. to 9:00 p.m. (excluding the New Year holidays)

| To Institutional Investors |

The electronic voting platform for institutional investors operated by Investor Communications Japan Inc. is available for institutional investors that have applied to use such platform in advance.

6

REFERENCE DOCUMENTS FOR GENERAL MEETING OF SHAREHOLDERS

Item No.1: Dividend from Surplus

The basic policy of the Company is to provide a stable return and actively return profits to shareholders, mainly in the form of a dividend, taking into consideration medium-term profit forecasts along with planned future investments, cash flow and other factors.

Taking into account this basic policy and the progress of recovery of our business performance for the current business term, we propose a term- end dividend of 60.00 yen per share for the current business term, an increase of 5.00 yen relative to term-end dividend of the previous term.

As we have already paid an interim dividend of 60.00 yen per share, the full-year dividend will be 120.00 yen per share (an increase of 20.00 yen from the previous term).

1. Kind of the dividend property

|

Cash

| |

2. Matters regarding allocation of the dividend property and its total amount

|

60.00 yen per one common share of the Company Total amount of dividend 60,930,802,080 yen

| |

3. Effective date of the distribution of the dividend from surplus

|

March 31, 2023

|

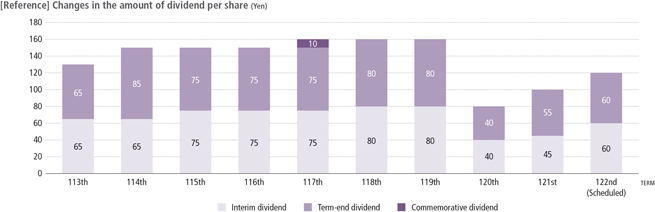

[Reference] Changes in the amount of dividend per share (Yen)

180 160 140 120 100 80 60 40 20 0 65 65 85 65 75 75 75 75 10 75 75 80 80 80 80 40 40 55 45 60 60113th 114th 115th 116tg 117th 118th 119th 120th 121st 122nd (sheduled) TERM

Interin dividend Term-end dividend Commemorative dividend

7

Item No.2: Election of Five Directors

The terms of office of all of the five Directors will expire at the end of this Meeting. Accordingly, we propose the election of five Directors.

The Company has a basic policy that the focus of the organizational structure of the Board of Directors is on the Directors that oversee company-wide business strategies or execution and the Directors that oversee multiple business fields or headquarters functions, while at least two Independent Outside Directors are appointed while also assuring that they account for one third or more of the total number of Directors, in order to secure sound management.

The candidates for Directors, based on this basic policy, are as follows:

Candidate No.

|

Name

|

Current Position, Business in Charge, etc. at the Company

|

Board of

| |||||||||

1

|

Fujio Mitarai

|  |

Chairman & CEO

|

100% (10/10)

| ||||||||

2

|

Toshizo Tanaka

| |

Executive Vice President & CFO Group Executive of Public Affairs Headquarters Group Executive of Facilities Management Headquarters

|

100% (10/10)

| ||||||||

3

|

Toshio Homma

| |

Executive Vice President & CTO Head of Printing Group Chief Executive of Digital Printing Business Operations

|

100% (10/10)

| ||||||||

4

|

Kunitaro Saida

|

|

Director

|

100% (10/10)

| ||||||||

5

|

Yusuke Kawamura

|

|

Director

|

100% (10/10)

| ||||||||

Note: The attendance figures above constitute attendance of the Board of Directors meetings by the respective candidates for Directors during the 122nd business term.

8

Candidate No. 1 Reappointed Candidate No. 1 |

Fujio Mitarai

Date of birth Sep. 23, 1935

Number of the Company’s shares held 148,344 shares

|

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||

As of | ||||||||||||

Apr. 1961: Entered the Company | ||||||||||||

Mar. 1981: Director | ||||||||||||

Mar. 1985: Managing Director | ||||||||||||

Mar. 1989: Senior Managing Director | ||||||||||||

Mar. 1993: Executive Vice President | ||||||||||||

Sep. 1995: President | ||||||||||||

Mar. 2006: Chairman, President & CEO | ||||||||||||

May 2006: Chairman & CEO (daihyō torishimariyaku kaichō) | ||||||||||||

Mar. 2012: Chairman & CEO (daihyō torishimariyaku kaichō ken shachō) | ||||||||||||

Mar. 2016: Chairman & CEO (daihyō torishimariyaku kaichō) | ||||||||||||

May 2020: Chairman & CEO (daihyō torishimariyaku kaichō ken shachō) (present) | ||||||||||||

[Important concurrent posts] | ||||||||||||

● Audit & Supervisory Board Member of The Yomiuri Shimbun Holdings | ||||||||||||

| ||||||||||||

| Candidate No. 1 | [Reasons for being selected as a candidate] | |||||||||||

Mr. Fujio Mitarai has supervised the Company’s management as a CEO over the course of many years and has accomplished many things, such as significantly increasing profitability through management reform including production reform, and building a foundation for the transformation of the Company’s business structure for new areas where growth is expected. The Company has selected him as a candidate for Director upon determining that his wealth of expertise and ability related to management, gained from being chairman of Keidanren (“Japan Business Federation”), and holding many important positions in other organizations, are vital to the Company’s management. | ||||||||||||

Candidate No. 2 Reappointed Candidate No. 2 |

Toshizo Tanaka

Date of birth Oct. 8, 1940

Number of the Company’s shares held 24,910 shares |

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||

As of | ||||||||||||

Apr. 1964: Entered the Company | ||||||||||||

Mar. 1995: Director | ||||||||||||

Mar. 1997: Managing Director | ||||||||||||

Mar. 2001: Senior Managing Director | ||||||||||||

Mar. 2007: Executive Vice President & Director | ||||||||||||

Mar. 2008: Executive Vice President & CFO (present) | ||||||||||||

Apr. 2011: Group Executive of Finance & Accounting Headquarters | ||||||||||||

Mar. 2014: Group Executive of Human Resources Management & Organization Headquarters | ||||||||||||

Apr. 2017: Group Executive of Facilities Management Headquarters (present) | ||||||||||||

Mar. 2018: Group Executive of Public Affairs Headquarters (present) | ||||||||||||

Apr. 2018: Group Executive of Finance & Accounting Headquarters | ||||||||||||

| ||||||||||||

| Candidate No. 2 | [Reasons for being selected as a candidate] | |||||||||||

Mr. Toshizo Tanaka has contributed greatly to building the Company’s strong financial position while working for many years as CFO. The Company has selected him as a candidate for Director upon determining that his extensive expertise, insight, and wide range of experience, gained from managing overall corporate administration, are vital to the Company’s management. | ||||||||||||

9

Candidate No. 3 Candidate No. 3 Reappointed Candidate No. 4 |

Toshio Homma

Date of birth Mar. 10, 1949

Number of the Company’s shares held 72,652 shares

|

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||

As of | ||||||||||||

Apr. 1972: Entered the Company | ||||||||||||

Jan. 1995: Senior General Manager of Copying Machine Development Center | ||||||||||||

Mar. 2003: Director | ||||||||||||

Apr. 2003: Group Executive of Business Promotion Headquarters | ||||||||||||

Jan. 2007: Chief Executive of L Printer Products Operations | ||||||||||||

Mar. 2008: Managing Director | ||||||||||||

Mar. 2012: Senior Managing Director | ||||||||||||

| Group Executive of Procurement Headquarters | ||||||||||||

Mar. 2016: Executive Vice President | ||||||||||||

Apr. 2016: Chief Executive of Office Imaging Products Operations | ||||||||||||

Mar. 2017: Executive Vice President & In charge of Office Business | ||||||||||||

Apr. 2020: Executive Vice President & CTO & In charge of Printing Business | ||||||||||||

| Chief Executive of Digital Printing Business Operations (present) | ||||||||||||

Apr. 2021: Executive Vice President & CTO (present) | ||||||||||||

| Head of Printing Group (present) | ||||||||||||

| ||||||||||||

| [Reasons for being selected as a candidate] | ||||||||||||

Mr. Toshio Homma accomplished great things in the commercialization of large-format printing systems after being engaged in the development and commercialization of copying machines over the course of many years. Also, he led procurement reform and contributed to creating a structure to support reducing the cost-of-sales ratio. He is currently in charge of and managing the overall printing business including commercial printing, while also managing the Company’s technological R&D as CTO. The Company has selected him as a candidate for Director upon determining that his broad knowledge and experience are vital to the Company’s management. | ||||||||||||

Candidate No. 4 Reappointed Outside Director Independent Director |

Kunitaro Saida

Date of birth May 4, 1943

Number of the Company’s shares held 12,800 shares

|

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||

As of | ||||||||||||

Apr. 1969: Appointed as Public Prosecutor | ||||||||||||

Feb. 2003: Superintending Prosecutor of Takamatsu High Public Prosecutors Office | ||||||||||||

Jun. 2004: Superintending Prosecutor of Hiroshima High Public Prosecutors Office | ||||||||||||

Aug. 2005: Superintending Prosecutor of Osaka High Public Prosecutors Office | ||||||||||||

May 2006: Retired from Superintending Prosecutor of Osaka High Public Prosecutors Office | ||||||||||||

Registered as an attorney (present) | ||||||||||||

Jun. 2007: Audit & Supervisory Board Member of NICHIREI CORPORATION | ||||||||||||

Jun. 2008: Director of Sumitomo Osaka Cement Co., Ltd. | ||||||||||||

Jun. 2010: Director of HEIWA REAL ESTATE CO., LTD. | ||||||||||||

Mar. 2014: Director (present) | ||||||||||||

[Important concurrent posts] | ||||||||||||

● Attorney

| ||||||||||||

| ||||||||||||

| [Reasons for being selected as a candidate and expected roles] | ||||||||||||

Mr. Kunitaro Saida has been serving as an attorney in corporate legal affairs subsequent to his distinguished career as Superintending Prosecutor of High Public Prosecutors Offices (in Takamatsu, Hiroshima and Osaka), and also has experience serving as an Outside Director and an Outside Audit & Supervisory Board Member for other companies. The Company has selected him as a candidate for Outside Director in hopes that he will furnish particularly useful advice drawing on his wealth of experience and high level of expertise regarding legal affairs when taking part in discussions on internal control mechanisms and corporate governance, including from the perspective of ensuring compliance.

| ||||||||||||

10

Candidate No.5 Reappointed Outside Director Independent Director |

Yusuke Kawamura

Date of birth Dec. 5, 1953

Number of the Company’s shares held 1,300 shares

|

Brief personal record, position, business in charge and important concurrent posts

| ||||||||||||||

As of | ||||||||||||||||

Apr. 1977: Entered Daiwa Securities Co. Ltd. | ||||||||||||||||

Jan. 1997: General Manager of Syndicate Department of Daiwa Securities Co. Ltd. | ||||||||||||||||

Apr. 2000: Professor of Faculty of Economics and the Graduate School of Economics of Nagasaki University | ||||||||||||||||

Apr. 2010: Senior Managing Director of Daiwa Institute of Research Ltd. | ||||||||||||||||

Jan. 2011: Commissioner of Fiscal System Council of Ministry of Finance | ||||||||||||||||

Apr. 2012: Deputy Chairman of Daiwa Institute of Research Ltd. | ||||||||||||||||

Feb. 2013: Commissioner of Business Accounting Council of Financial Services Agency (present) | ||||||||||||||||

Jun. 2017: Director of Mitsui Sugar Co., Ltd. (currently Mitsui DM Sugar Holdings Co., Ltd.) (present) | ||||||||||||||||

Apr. 2019: Executive Counselor of Japan Securities Dealers Association | ||||||||||||||||

Apr. 2020: Chairman & CEO of Institute of Glocal Policy Research (present) | ||||||||||||||||

Mar. 2021: Director (present) | ||||||||||||||||

[Important concurrent posts] ● Director of Mitsui DM Sugar Holdings Co., Ltd. ● Chairman & CEO of Institute of Glocal Policy Research | ||||||||||||||||

| ||||||||||||||||

[Reasons for being selected as a candidate and expected roles] | ||||||||||||||||

Mr. Yusuke Kawamura has a wealth of experience as an Outside Director along with capacity as an expert with respect to financial and securities systems as well as strategy for managing financial institutions, given that he worked at a securities company and subsequently served in various positions, including as a university professor, a commissioner of councils of Japan’s Ministry of Finance and Financial Services Agency, and an Executive Counselor of the Japan Securities Dealers Association. The Company has selected him as a candidate for Outside Director in hopes that he will furnish particularly useful advice drawing on his wealth of experience and high level of expertise regarding finance and securities, especially when taking part in discussions on M&A and ESG-related topics from a shareholder and investor perspective.

| ||||||||||||||||

Notes: | 1. | None of the candidates for the Directors have any special interest in the Company. | ||

2. | Mr. Kunitaro Saida and Mr. Yusuke Kawamura are candidates for Outside Directors defined by Item 7, Paragraph 3, Article 2 of the Enforcement Regulations of the Corporation Law of Japan. | |||

3. | At HEIWA REAL ESTATE CO., LTD. where Mr. Kunitaro Saida served as External Director until June 24, 2020, employee misconduct relating to real estate transactions was discovered, resulting in the aforesaid company’s recording of extraordinary loss in the second quarter of the fiscal year ended March 31, 2020, in association with that misconduct. Whereas he had been unaware of the misconduct up until its discovery, Mr. Kunitaro Saida has expressed his opinions on measures to prevent recurrence of any such incident, and otherwise has been appropriately making recommendations at the aforesaid company from the perspective of legal adherence and compliance-oriented management. | |||

4. | Although Mr. Kunitaro Saida and Mr. Yusuke Kawamura do not have the experience of being involved in the management of a company other than in a position of an outside director or outside audit & supervisory board member, the Company judges that they will appropriately perform their duties as Outside Director as outlined above in “Reasons for being selected as a candidate and expected roles.” | |||

5. | Mr. Kunitaro Saida will have served as Outside Director of the Company for nine years as of the end of this Meeting. Mr. Yusuke Kawamura will have served as Outside Director of the Company for two years as of the end of this Meeting. | |||

6. | The Company has entered into contracts with Mr. Kunitaro Saida and Mr. Yusuke Kawamura limiting the amount of their damage compensation liabilities defined in Paragraph 1, Article 423 of the Corporation Law of Japan to the limit prescribed by laws and regulations. Should they be elected to the position of Director, the Company will continue the aforementioned contract with them. | |||

7. | The Company has entered into a directors and officers liability insurance contract with an insurance company as specified in the provision of Paragraph 1, Article 430-3 of the Corporation Law of Japan, whereby the Company’s Directors serve as the insured parties. The insurance covers damages that could arise under situations where an insured party bears liability in regard to performance of his or her duties or where the insured party becomes subject to a claim seeking to hold him or her liable in that regard. Every Director candidate is to be insured under the directors and officers liability insurance contract should they be elected. The contract is to be renewed in September 2023. | |||

8. | The Company has notified Mr. Kunitaro Saida and Mr. Yusuke Kawamura as independent directors to each stock exchange in Japan on which the Company is listed as provided under the regulations of each stock exchange. Should they be elected to the position of Director, the Company will continue to make both of them independent directors. Although the Company has compensated Mr. Kunitaro Saida for his advisory services rendered prior to him having assumed the post of Director of the Company, the remuneration was not substantial given that it amounted to no more than 12 million yen annually, and his contract in that regard has already expired. Accordingly, the Company judges that his independence is not affected by the aforesaid circumstances. | |||

Additional Note for English Translation: | ||||

Mr. Fujio Mitarai, Mr. Toshizo Tanaka and Mr. Toshio Homma are Representative Directors. | ||||

11

Item No.3: Election of Two Audit & Supervisory Board Members

The terms of office of Audit & Supervisory Board Members Mr. Hiroaki Sato and Mr. Yutaka Tanaka will expire at the end of this Meeting. Accordingly, we propose the election of two Audit & Supervisory Board Members.

The Company has a basic policy to have Audit & Supervisory Board Members that are familiar with the Company’s businesses or its management structure, or that have extensive knowledge in specialized areas such as law, finance and accounting, and internal controls. The candidates for Audit & Supervisory Board Member, based on this basic policy, are as follows:

Prior to our proposal of this item, we have already obtained the consent of the Audit & Supervisory Board.

Candidate No. 1 Newly appointed |

Hideya Hatamochi

Date of birth Oct. 4, 1960

Number of the Company’s shares held 0 shares

|

Brief personal record, position and important concurrent posts

| ||||||||||||||

As of

| ||||||||||||||||

Apr. 1983: Entered the Company

| ||||||||||||||||

Apr. 2009: General Manager of Office Imaging Products Electrical Parts Engineering Division of Office Imaging Products Operations

| ||||||||||||||||

May. 2012: General Manager of Office Imaging Products Manufacturing Division of Office Imaging Products Operations

| ||||||||||||||||

Jan. 2014: General Manager in charge of Corporate Audit Center

| ||||||||||||||||

Feb. 2015: President of Canon (Suzhou) Inc. (present)

| ||||||||||||||||

| ||||||||||||||||

[Reasons for being selected as a candidate] | ||||||||||||||||

Mr. Hideya Hatamochi was engaged for many years in the process design of office multifunction devices (MFDs) and was in charge of improving production efficiency and designing quality assurance systems. Subsequently, he served as General Manager of a manufacturing division. Then, after gaining experience at the Corporate Audit Center, performing auditing for subsidiaries of the Company, he served as President of a manufacturing subsidiary in China, which is one of the Group’s major overseas manufacturing plants, for approximately eight years. The Company has selected him as a candidate for Audit & Supervisory Board Member premised on the notion that his experience and knowledge described above will help bring about audits that are more effective.

| ||||||||||||||||

Candidate No. 2 Reappointed Outside Audit & Supervisory Board Member Independent Audit & Supervisory Board Member

|

|

Yutaka Tanaka

Date of birth Mar. 11, 1949

Number of the Company’s shares held 3,400 shares

|

Brief personal record, position and important concurrent posts

| |||||||||||||

As of

| ||||||||||||||||

Apr. 1975: Assistant Judge of the Tokyo District Court

| ||||||||||||||||

Apr. 1986: Judge of the Tokyo District Court

| ||||||||||||||||

Apr. 1987: Instructor of the Legal Training & Research Institute, the Supreme Court of Japan

| ||||||||||||||||

Apr. 1992: Judicial Research Official, the Supreme Court of Japan

| ||||||||||||||||

Apr. 1996: Resignation as a Judge Registered as an attorney (present)

| ||||||||||||||||

Apr. 2004: Professor of Keio University Law School

| ||||||||||||||||

Mar. 2019: Audit & Supervisory Board Member (present)

[Important concurrent posts] ● Attorney ● Director of Laws & Ordinances Compliance Investigation Office, Financial Services Agency of Japan

| ||||||||||||||||

| ||||||||||||||||

[Reasons for being selected as a candidate] | ||||||||||||||||

Mr. Yutaka Tanaka had for many years served as a judge in charge of civil cases, and subsequently has been engaging in corporate legal affairs as an attorney and as a law school professor. The Company has selected him as a candidate for Outside Audit & Supervisory Board Member as it desires to leverage his considerable experience and high level of expert knowledge about legal affairs to further enhance the Company’s auditing system.

| ||||||||||||||||

12

Notes: | 1. | None of the candidates have any special interest in the Company. | ||

2. | Brief personal record of Mr. Hideya Hatamochi is based on the information as of January 30, 2023. | |||

3. | Mr. Yutaka Tanaka is a candidate for Outside Audit & Supervisory Board Member defined by Item 8, Paragraph 3, Article 2 of the Enforcement Regulations of the Corporation Law of Japan. | |||

4. | Although Mr. Yutaka Tanaka does not have the experience of being involved in the management of a company other than in a position of an outside audit & supervisory board member, the Company judges that he will appropriately perform his duties as Outside Audit & Supervisory Board Member by utilizing his considerable experience and high level of expert knowledge about legal affairs, as outlined above. | |||

5. | Mr. Yutaka Tanaka will have served as Audit & Supervisory Board Member of the Company for four years as of the end of this Meeting. | |||

6. | The Company has entered into a contract with Mr. Yutaka Tanaka limiting the amount of his damage compensation liabilities defined in Paragraph 1, Article 423 of the Corporation Law of Japan to the limit prescribed by laws and regulations. Should he be elected to the position of Audit & Supervisory Board Member, the Company will continue the aforementioned contract with him. | |||

7. | The Company has entered into a directors and officers liability insurance contract with an insurance company as specified in the provision of Paragraph 1, Article 430-3 of the Corporation Law of Japan, whereby the Company’s Audit & Supervisory Board Members serve as the insured parties. The insurance covers damages that could arise under situations where an insured party bears liability in regard to performance of his or her duties or where the insured party becomes subject to a claim seeking to hold him or her liable in that regard. Should each candidate be elected to the position of Audit & Supervisory Board Member, each person is to be insured under the directors and officers liability insurance contract. The contract is to be renewed in September 2023. | |||

8. | The Company has notified Mr. Yutaka Tanaka as an independent audit & supervisory board member to each stock exchange in Japan on which the Company is listed as provided under the regulations of each stock exchange. Should he be elected to the position of Audit & Supervisory Board Member, the Company will continue to make him an independent audit & supervisory board member. |

[Reference]

“Independence Standards for Independent Directors/Audit and Supervisory Board Members” of the Company

The Company has established the “Independence Standards for Independent Directors/Audit and Supervisory Board Members” resolved by the Board of Directors with the consent of all Audit and Supervisory Board Members, in order to clarify the standards for ensuring independence of Independent Directors/Audit and Supervisory Board Members of the Company, taking into consideration Japan’s Corporate Governance Code (Principle 4.9) and the independence criteria set by securities exchanges in Japan.

Independence Standards for

Independent Directors/Audit and Supervisory Board Members

Canon Inc. deems that a person who satisfies the requirements for Outside Directors/Audit and Supervisory Board Members prescribed by the Corporation Law of Japan, and meets the independence criteria set by securities exchanges in Japan, and does not fall into any of the items below, is an “Independent Director/Audit and Supervisory Board Member” (a person who is independent from the management of Canon Inc. and unlikely to have conflicts of interest with general shareholders).

1. | A person/organization for which Canon Group (Canon Inc. and its subsidiaries; hereinafter the same) is a major client, or a major client of Canon Group, or an executing person of such organization or client | |||||

2. | A major lender to Canon Group, or an executing person of such lender | |||||

3. | A large shareholder of Canon Inc., or an executing person of such shareholder | |||||

4. | A person/organization receiving large amounts of contributions from Canon Group, or an executing person of such organization | |||||

5. | A consultant, accounting professional or legal professional who has received a large amount of money or other properties from Canon Group, other than as compensation for being a director/Audit and Supervisory Board Member (if the recipient is a corporation, partnership or any other organization, this item applies to any person belonging to said organization.) |

13

6. | A certified public accountant belonging to the audit firm engaged to conduct the statutory audit of Canon Group (including any such accountant to whom this item has applied in the last 3 business years) | |||||

7. | An executing person of another company in cases where an executing person of Canon Group is an outside director/Audit and Supervisory Board Member of such other company | |||||

8. | An immediate family member (spouse and a relative within the second degree of kinship) of any of the persons listed in each of items 1 to 7; provided, however that the persons to whom this is applicable shall be limited to key executing persons such as directors, executive officers of companies and partners of advisory firms | |||||

(Notes) | ||||||

* | In item 1, “major” means in cases where the total amount (for any business year during the last 3 business years) of transactions between Canon Group and such client exceeds 1% of the consolidated sales of Canon Group or such client. | |||||

* | In item 2, “major” means in cases where the debt outstanding exceeds 1% of the consolidated total assets of Canon Inc. for any business year during the last 3 business years. | |||||

* | In item 3, “a large shareholder” means a shareholder who directly or indirectly holds 5% or more of the total voting rights of Canon Inc. | |||||

* | In item 4, “a large amount” means in cases where the total amount of contributions exceeds JPY 12 million (in cases where the recipient is an individual) or 1% of the annual gross income of such recipient (in cases where the recipient is an organization), for any business year during the last 3 business years of Canon Inc. | |||||

* | In items 1 to 4 and 7, an “executing person” means an executive director, executive officer and employee including manager (in items 1 to 4, including a person to whom this item has applied in any business year during the last 3 business years). | |||||

* | In item 5, “a large amount” means in cases where the total amount of money or other properties received by said consultant, etc., exceeds JPY 12 million (in cases where the recipient is a person) or 1% of the annual gross sales of such consultant, etc. (in cases where the recipient is an organization), for any business year during the last 3 business years of Canon Inc. |

Item No.4: Grant of Bonus to Directors

We propose that bonus be granted to the three Directors excluding Outside Directors as of the end of this term, which totals 275,800,000 yen.

Remuneration for Directors consists of a basic remuneration, a bonus, and stock-type compensation stock options.

The Nomination and Remuneration Advisory Committee has furnished its confirmation with respect to the aforementioned bonus amount, in accordance with the “Policy on Decisions on the Content of Remunerations for Individual Directors” (pages 31 to 32), stipulated at the meeting of the Board of Directors held on January 18, 2021.

14

BUSINESS REPORT (From January 1, 2022 to December 31, 2022)

1. Current Conditions of the Canon Group

(1) Business Progress and Results

General Business Conditions

The global economy during the 122nd Business Term (from January 1, 2022 to December 31, 2022) was marked by rising inflation due to shortages of goods and labor, and increasing energy prices prompted by the COVID-19 pandemic and Russia’s invasion of Ukraine. We encountered a decelerating trend in economic growth across a wide area amid a rapid tightening of monetary policy in areas around the world to curb historically high rates of inflation.

As for exchange rates, although the yen began sharply depreciating in March and reached a level of 151 yen to the U.S. dollar in October for

the first time in 32 years, before subsequently appreciating somewhat, the yen was significantly weaker against both the U.S. dollar and the euro, relative to last year.

Demand for our products remained firm overall, even amidst the volatile economic environment. We addressed prevailing issues such as product supply shortages and pressures on distribution, in part by steadily implementing measures that entailed changing designs and procuring alternative parts to contend with shortages of semiconductors and other components, and by promptly securing cargo

15

space and making use of alternative transportation routes. As a result, we managed to increase our supply of products from one quarter to the next and achieved greater sales volume in each of our businesses. Although costs rose significantly, due to inflation, the tight supply of components, and pressures on distribution, we partially absorbed the impact as we appropriately reflected them in selling prices.

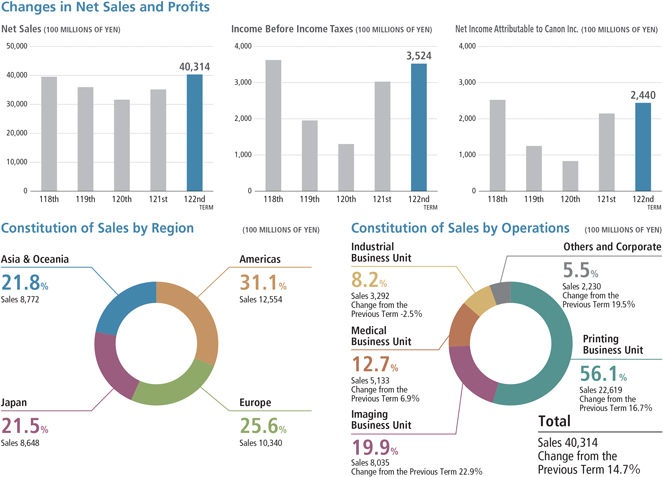

With the added benefit of the weak yen, consolidated net sales for this term was 4,031.4 billion yen (up 14.7% from the previous term). Consolidated income before income taxes was 352.4 billion yen (up

16.4% from the previous term). Consolidated net income attributable to Canon Inc. was 244.0 billion yen (up 13.6% from the previous term). This marked the second consecutive year of sales and profit growth.

Compared to 2017, the year in which we last achieved consolidated net sales of over 4 trillion yen, sales of existing businesses declined. However, we are making steady progress in transforming our business portfolio as sales of new businesses, such as medical and network cameras, grew significantly to exceed 1 trillion yen, and now account for a larger portion of total sales from 22% to 27%.

16

Highlights of Results

· During this term, whereas the global economy exhibited signs of a slowdown from the latter half of the year, demand for our products remained firm overall. As a result, consolidated net sales grew by 14.7% compared to the previous term, as we achieved sales volume growth through company-wide efforts to address the tight supply of components and pressures on distribution.

· Due to growth in sales volume, and in part, depreciation of the yen, consolidated net income attributable to Canon Inc. increased by 13.6% compared to the previous term.

Changes in Net Sales and Profits Net Sales (100 MILLIONS OF YEN) Income Before Income Taxes (100 MILLIONS OF YEN) Net Income Attributable to Canon Inc. (100 MILLIONS OF YEN) 50,000 40,000 30,000 20,000 10,000 0 118th 119th 120th 121st 122nd TERM 40,314 4,000 3,000 2,000 1,000 0 118th 119th 120th 121st 122nd TERM 3,524 4,000 3,000 2,000 1,000 0 118th 119th 120th 121st 122nd TERM 2,440 Constitution of Sales by Region (100 MILLIONS OF YEN) Constitution of Sales by Operations (100 MILLIONS OF YEN) Asia & Oceania Americas 21.8% Sales 8,772 31.1% Sales 12,554 Japan 21.5% Sales 8,648 Europe 25.6% Sales 10,340 Industrial Business Unit 8.2% Sales 3,292 Change from the Previous Term -2.5% Medical Business Unit 12.7% Sales 5,133 Change from the Previous Term 6.9% Imaging Business Unit 19.9% Sales 8,035 Change from the Previous Term 22.9% Others and Corporate 5.5% Sales 2,230 Change from the Previous Term 19.5% Printing Business Unit 56.1% Sales 22,619 Change from the Previous Term 16.7% Total Sales 40,314 Change from the Previous Term 14.7%

Notes: | 1. | From this term, Canon has changed the name and structure of segments to Printing Business Unit, Imaging Business Unit, Medical Business Unit, and Industrial Business Unit, and Others and Corporate. Accordingly, the same restatement has been applied in relation to the previous terms. | ||

| 2. | The totals do not amount to 100% because the consolidated sales of each business unit include the sales relating to intersegment transactions. | |||

17

Business Conditions by Operations

Printing Business Unit

In the office MFD market, the recovery in the number of people coming into the office prompted the replacement of equipment, which had previously stagnated amid the COVID-19 pandemic. Meanwhile, printing demand has also been on a moderate trajectory toward recovery. The Company achieved a recovery in product supply volume and increased unit sales mainly for medium- and high-speed models with high print volume, while sales of services and consumable supplies also exceeded the previous term’s levels.

Laser printers and inkjet printers saw significant growth in both unit sales and net sales, resulting from a recovery in product supply volume, which had suffered shortages due to the impact of plant shutdowns in 2021, linked to the spread of COVID-19.

Sales of production printers for commercial and industrial printing increased significantly, amid the accelerating shift to digital printing that offers cost and labor savings, as unit sales of continuous feed presses, high-speed sheet-fed presses, and large format printers each increased from the previous term.

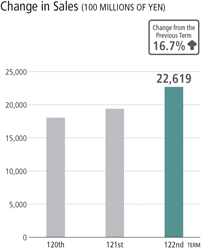

As a result, on a consolidated basis, sales for this business unit increased by 16.7% to 2,261.9 billion yen in comparison to the previous term.

Change in Sales (100 MILLIONS OF YEN) Change from the Previous Term 16.7% 25,000 20,000 15,000 10,000 5,000 0 120th 121st 122nd TERM 22,619

18

Imaging Business Unit

The market for interchangeable-lens digital cameras was firm as camera manufacturers introduced appealing products. Meanwhile, unit sales of our interchangeable-lens digital cameras exceeded those of the previous year, thanks to continued strong sales of our EOS R5 and EOS R6, full-frame mirrorless cameras released in 2020, and the addition to our lineup of the EOS R7 and EOS R10, which are new products equipped with the EOS R system’s first ever APS-C size image sensor. Moreover, we also achieved growth in sales of interchangeable lenses amid our efforts to meet diverse user needs by launching six new models for the EOS R system.

For network cameras, people’s needs for safety and security are strong, and the market is returning to its original growth trajectory as restrictions on economic activities due to the spread of COVID-19 have eased. Accordingly, sales were up significantly, thanks to not only an increase in camera unit sales, but software sales as well.

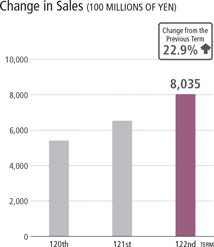

As a result, on a consolidated basis, sales for this business unit increased by 22.9% to 803.5 billion yen in comparison to the previous term.

Change from the Previous Term 22.9% 10,000 8,000 6,000 4,000 2,000 0 120th 121st 122nd TERM 8,035 Change in Sales (100 MILLIONS OF YEN)

19

Medical Business Unit

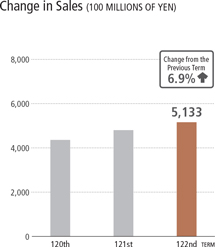

In the medical equipment market, investment, which was restricted due to the COVID-19 pandemic, in large diagnostic imaging systems such as computed tomography (CT) systems and magnetic resonance imaging (MRI) systems, particularly in Europe and the United States, recovered. As for the Company, we generated strong orders amid a favorable market reception, particularly for our Aquilion Serve CT system and our Vantage Fortian MRI system, which are new products that utilize technologies of the Imaging Group to reduce the burdens of testing incurred by healthcare professionals and patients. We achieved steady sales by addressing the tight supply of components against a backdrop of record-high orders. As a result, on a consolidated basis, sales for this business unit exceeded 500.0 billion yen for the first time, increasing by 6.9% to 513.3 billion yen in comparison to the previous term, thanks to significant growth in sales in the U.S. and other overseas markets where we have strengthened our sales capabilities.

Change in Sales (100 MILLIONS OF YEN) 8,000 6,000 4,000 2,000 0 120th 121st 122nd TERM change from the previous term 6.9% 5,133

20

Industrial Business Unit

Demand for semiconductors and displays has been rising across a wide range of fields amid a societal shift to smart technologies brought about by AI, IoT, 5G, and other technological innovations. Unit sales of the Company’s semiconductor lithography equipment exceeded those of the previous term amid very strong performance in terms of inquiries regarding such equipment. We have made the decision to increase such production capacity by building a new manufacturing facility within the Canon Utsunomiya Office to meet demand for semiconductor lithography equipment, which is poised for further growth going forward.

Conversely, unit sales of FPD (Flat Panel Display) lithography equipment declined compared to the previous term, when there was a high level of sales in response to pent-up demand for the installation of equipment, which was delayed due to the COVID-19 pandemic. As for OLED display manufacturing equipment, sales were lower than in the previous term as customers continued to adjust the level of their capital investment.

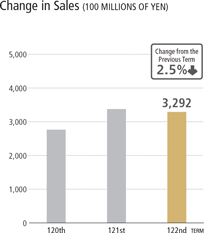

As a result, on a consolidated basis, sales for this business unit decreased by 2.5% to 329.2 billion yen in comparison to the previous term.

Change in Sales (100 MILLIONS OF YEN) 5,000 4,000 3,000 2,000 1,000 0 120th 121st 122nd TERM 3,292 change from the previous term 2.5%

21

(2) Facilities Investment

The investment in facilities by the Canon Group during this term totaled 156.6 billion yen (52.3 billion yen by the Company), which are mainly as follows:

Main facilities under construction for establishment / expansion as of the end of this term | Main facilities under planning for establishment / expansion as of the end of this term | |||

Canon Inc.: | Canon Inc.: | |||

| New Production Base of Hiratsuka Plant | New Production Base of Utsunomiya Optical Products Plant | |||

| (Others and Corporate) | (Industrial Business Unit) | |||

| Location: Hiratsuka-shi, Kanagawa Pref., Japan | Location: Utsunomiya-shi, Tochigi Pref., Japan | |||

(3) Business Challenges and Countermeasures

Under Phase V of the “Excellent Global Corporation Plan,” which covered the years from 2016 to 2020, the four new businesses to serve as Canon’s new growth drivers, namely, Commercial Printing, Network Cameras, Medical, and Industrial Equipment fully emerged and the basic framework for promoting transformation of the business portfolio was completed. Then in 2021, the initial year of Phase VI of the Excellent Global Corporation Plan, we sought to further facilitate the transformation of our business portfolio by reorganizing our product-oriented business divisions into industry-oriented business groups, thereby establishing a framework for enhancing business competitiveness and creating new drivers of growth.

In 2021 and 2022, the business environment remained challenging due to the spread of COVID-19, supply chain disruptions caused by the tight supply of components and pressures on distribution, the conflict between Russia and Ukraine, lockdowns in Shanghai, and accelerating inflation worldwide. However, by harnessing the efforts of the entire Canon Group, including procurement and logistics operations, and backed by strong product competitiveness in each of our businesses, we achieved sales and profit growth for the second consecutive year.

Although it is likely that we will continue to operate under a volatile economic environment this year as well, we will seek to achieve greater performance while leveraging the collective strength of our development, procurement, production, and sales. In so doing, we will accordingly focus on the following measures under the basic policy of Phase VI of striving to “accelerate our corporate portfolio transformation by improving productivity and creating new businesses.”

| 1. | Thoroughly strengthen competitiveness of industry-oriented business groups |

We will strengthen and expand our four industry-oriented business groups to promote business portfolio transformation.

| 1) | Printing Group |

Even though companies have been shifting to paperless documents due to a greater dispersion of workplaces caused by the COVID-19 pandemic, as well as due to advances in digital transformation (DX), we are likely to see solid demand for printing devices given that paper remains an instrumental means of work-related conceptualization and information sharing. |

In order to support hybrid work styles that combine office- and tele-work, there is a need to provide a print environment that is free from restrictions on where to work by utilizing the cloud. Leveraging the advantage of having two digital printing technologies, namely electrophotography and inkjet, the Canon Group will offer new solutions for the DX era in both office and home printing. |

Furthermore, in the field of digital commercial printing of catalogs, posters and other material, which is poised for growth amid a shift from analog to digital, we are expanding sales of our printing presses, recognized for their image quality and productivity, which have been further enhanced by incorporating feedback from printing companies, our customers. Furthermore, in the field of industrial printing, which includes labels and packaging, we plan to fully enter the market by developing new products while taking advantage of the wealth of technology, knowledge and customer relationships held by Edale Limited, a UK-based company that we acquired last year. |

22

| 2) | Imaging Group |

Although the overall market for digital cameras has shrunk significantly due to widespread use of smartphones, we expect demand to remain solid as current users of interchangeable-lens cameras are mainly professionals and enthusiasts who seek high-quality images. To address the needs of these users, we will continuously introduce cameras, from entry-class to professional level models that offer enhanced features as well as interchangeable lenses. In doing so, we, as a leading camera company, seek to stimulate the market. We are currently expanding our lineup of mirrorless cameras with our sights set on establishing our position as No.1 in that field. |

In the network camera field, where surveillance applications are likely to keep driving growth due to escalating needs for safety and security, we also anticipate substantial growth accompanying an expanding range of applications for such cameras in areas other than surveillance. For instance, this is likely to include applications with respect to facilitating in-store marketing, implementing production control at manufacturing sites, and helping people avoid crowds and contact in places where individuals gather. We seek to achieve market-exceeding growth by offering an abundant lineup of camera bodies and solutions with providing total services encompassing everything from video input to video management and analytics, cooperating with Canon Group companies such as Axis, Milestone Systems, BriefCam, and Arcules. |

We will also take steps to create new businesses by coming up with applications for optical-related technologies involving lenses, sensors, and image processing, cultivated by the Company thus far. |

| 3) | Medical Group |

The Company aims to contribute to medical treatment worldwide not only through diagnostic imaging systems, but also by broadening its business sphere, to include healthcare IT and in-vitro diagnostics. |

We are Japan’s leading manufacturer of diagnostic imaging systems and accordingly deem it necessary to establish a similar presence overseas in order to achieve growth going forward. First, to become the No.1 company worldwide in CT systems, we aim to achieve early commercialization of the next-generation of CT scanners that utilize photon-counting technology. To such ends, we developed an X-ray CT system equipped with a photon-counting detector that uses the technology of Canada-based Redlen Technologies, which we acquired two years ago. Having installed it at the National Cancer Center of Japan, we are accelerating the development of this system. Furthermore, with the aim of achieving a market share of over 10% in the United States, which is highly influential market worldwide, we established a new company in January 2023 in the suburbs of Cleveland to focus on marketing. As such, we will work to achieve substantial growth in part by increasing our presence as we engage in joint research with U.S. medical institutions and promote stronger relationships with medical practitioners who serve as key opinion leaders. Moreover, to achieve high growth, we will spread the benefits to markets not only in the United States, but also to markets worldwide. |

In the healthcare IT field, we support the provision of high-quality diagnoses and efficient medical treatment by making it possible to integrate, process, and analyze data collected in clinical settings. Furthermore, in the in-vitro diagnostics field, we will expand our business domain to include testing reagents and other areas around testing equipment. |

| 4) | Industrial Group |

As applications for semiconductors and displays continue to expand, prompted by innovation particularly with respect to AI, IoT, 5G, and other technologies, we anticipate continuing market growth and subsequently expect demand for manufacturing equipment to rise. As for semiconductor lithography equipment, with our sights set on addressing growing demand, we aim to increase our market share by further enhancing product competitiveness and bolstering production capacity. Unlike conventional lithography technology that uses light to expose circuit patterns, the nanoimprint lithography manufacturing equipment being developed by the Company enlists a simple process of stamping a circuit pattern from a mold imprinted with such patterns. Nanoimprint lithography enables semiconductor manufacturers to reduce costs significantly because it eliminates the necessity of complex processes for etching minute circuit patterns. It also helps to reduce impact on the global environment as it consumes significantly less power given that it does not require powerful lasers and it does not need large vacuum systems or cooling systems. |

23

In the panel market, IT panels used in PCs and tablets are likely to drive growth going forward. As such, we will continue to provide FPD lithography equipment and OLED display manufacturing equipment that help panel manufacturers, our customers, boost productivity. Furthermore, we aim to expand the industrial business domain by developing new equipment that integrates core technologies of the group in the areas of ultra-precision positioning, ultra-precision processing and vacuum systems. |

| 2. | Rebuild the global production system |

The Company has been expanding its manufacturing facilities throughout Asia since the 1970s, but is now reviewing and reorganizing such production sites against the backdrop of supply chain interruptions and geopolitical risks. In our return to domestic production, which has been promoted up until now, we have taken a two-pronged approach of shifting to automation and in-house production, effectively achieving thorough cost reduction by integrating design, production technology, and manufacturing sites, thereby gaining competitive edge with respect to costs that is unmatched by overseas production.

| 3. | Strengthen product development based on proprietary technologies |

Whereas we have been turning to M&A initiatives as a means of developing new businesses in recent years, we seek to create new businesses going forward by further reinforcing product development centered on proprietary technologies. Under our framework of business groups largely reorganized by industry, we have been working on developing new products and solutions by combining respective technologies in a manner that gives rise to a sort of chemical reaction. In addition, the Frontier Business Promotion Headquarters has been bringing together Canon’s technologies from across the Canon Group with the aim to create new businesses in the fields of life science, materials, and solutions.

In order to achieve these goals, it is important to develop the technology experts who are responsible for product development, and we will promote this through a system to certify world-class engineers as “Top Scientists” who lead the development of cutting-edge technologies, and a system to train software engineers by reskilling employees.

Through these measures the Canon Group aims to achieve in 2025, the final year of Phase VI, net sales of 4,500.0 billion yen or more, an operating profit ratio of 12% or more, a net income ratio of 8% or more, and, in light of steady increases in shareholders’ equity ratio, a shareholders’ equity ratio of 65% or more.

24

(4) Status of Assets and Earnings

| 118th Business Term (Jan. 1, 2018-Dec. 31, 2018) | 119th Business Term (Jan. 1, 2019-Dec. 31, 2019) | 120th Business Term (Jan. 1, 2020-Dec. 31, 2020) | 121st Business Term (Jan. 1, 2021-Dec. 31, 2021) | 122nd Business Term (Jan. 1, 2022-Dec. 31, 2022) | |||||||||||||||||||||

Net Sales (100 millions of yen)

| 39,519 | 35,933 | 31,602 | 35,134 | 40,314 | ||||||||||||||||||||

Income before Income Taxes (100 millions of yen)

| 3,624 | 1,955 | 1,303 | 3,027 | 3,524 | ||||||||||||||||||||

Net Income Attributable to Canon Inc. (100 millions of yen)

| 2,524 | 1,250 | 833 | 2,147 | 2,440 | ||||||||||||||||||||

Basic Net Income Attributable to Canon Inc. Shareholders Per Share (yen)

| 233.80 | 116.79 | 79.37 | 205.35 | 236.71 | ||||||||||||||||||||

Total Assets (100 millions of yen)

| 49,030 | 47,719 | 46,256 | 47,509 | 50,955 | ||||||||||||||||||||

Total Canon Inc. Shareholders’ Equity (100 millions of yen)

| 28,206 | 26,855 | 25,750 | 28,738 | 31,131 | ||||||||||||||||||||

Notes: | 1. | Canon’s consolidated financial statements are prepared in accordance with U.S. generally accepted accounting principles. | ||

| 2. | Basic net income attributable to Canon Inc. shareholders per share is calculated based on the average number of outstanding common shares during the term. | |||

(5) Main Activities

The Canon Group is engaged in the development, manufacture and sales of the following products.

Operations | Main Products | |||

Printing Business Unit | Office Multifunction Devices (MFDs), Document Solutions, Laser Multifunction Printers (MFPs), Laser Printers, Inkjet Printers, Image Scanners, Calculators, Digital Continuous Feed Presses, Digital Sheet-Fed Presses, Large Format Printers | |||

Imaging Business Unit | Interchangeable-Lens Digital Cameras, Interchangeable Lenses, Digital Compact Cameras, Compact Photo Printers, MR Systems, Network Cameras, Video Management Software, Video Content Analytics Software, Digital Camcorders, Digital Cinema Cameras, Broadcast Equipment, Projectors | |||

Medical Business Unit | Computed Tomography (CT) Systems, Diagnostic Ultrasound Systems, Diagnostic X-ray Systems, Magnetic Resonance Imaging (MRI) Systems, Clinical Chemistry Analyzers, Digital Radiography Systems, Ophthalmic Equipment | |||

Industrial Business Unit | Semiconductor Lithography Equipment, FPD (Flat Panel Display) Lithography Equipment, OLED Display Manufacturing Equipment, Vacuum Thin-Film Deposition Equipment, Die Bonders | |||

Others | Handy Terminals, Document Scanners | |||

(6) Employees

| Consolidated | (Breakdown by Operation) | |||||||||||||||

Number of Employees | Printing Business Unit | Imaging Business Unit | Medical Business Unit | Industry Business Unit | Others and Corporate | |||||||||||

| 180,775 persons | (Decrease of 3,259 persons from the previous term) | 118,971 persons

| 24,917 persons

| 12,801 persons

| 8,005 persons

| 16,081 persons

| ||||||||||

| Non-Consolidated | ||||||||||||||||

Number of Employees | ||||||||||||||||

| 24,717 persons | (Decrease of 660 persons from the previous term) | |||||||||||||||

25

(7) Major Lenders

| ||||||||||||||||

Lenders | Funds Borrowed | |||||||||||||||

Mizuho Bank, Ltd. | 152.4 billion yen | |||||||||||||||

| MUFG Bank, Ltd. | 101.6 billion yen | |||||||||||||||

(8) Principal Subsidiaries

Subsidiaries

| Company Name | Capital Stock | Ratio of Voting Rights of the Company (%) | Main Activities | |||||||

Canon Marketing Japan Inc. | | 73,303 millions of yen |

| 58.5 | Sale of business machines, cameras, etc. in Japan | |||||

Canon Electronics Inc. | | 4,969 millions of yen |

| 55.2 | Manufacture and sale of information related equipment and precision machinery units for cameras | |||||

| Oita Canon Inc. | | 80 millions of yen |

| 100.0 | Manufacture of cameras | |||||

| Canon U.S.A., Inc. | | 204,355 thousands of U.S.$ |

| 100.0 | Sale of business machines, cameras, etc. in the Americas | |||||

| Canon Europa N.V. | | 360,021 thousands of Euro |

| 100.0 | Sale of business machines, cameras, etc. in Europe | |||||

| Canon Singapore Pte. Ltd. | | 7,000 thousands of Singapore $ |

| 100.0 | Sale of business machines, cameras, etc. in Southeast Asia | |||||

| Canon Vietnam Co., Ltd. | | 94,000 thousands of U.S.$ |

| 100.0 | Manufacture of inkjet printers and laser printers | |||||

| Canon Medical Systems Corporation | | 20,700 millions of yen |

| 100.0 | Development, manufacture, and sale of medical equipment | |||||

| Canon Medical Systems USA, Inc. | | 262,250 thousands of U.S.$ |

| 100.0 | Sale of medical equipment in the U.S. | |||||

Notes: | 1. | The ratio of the Company’s voting rights in Canon Marketing Japan Inc. is calculated together with the number of voting rights held by subsidiaries of the Company. Furthermore, the ratios of the Company’s voting rights in Canon Europa N.V. and Canon Medical Systems USA, Inc. are made up of the number of voting rights held by subsidiaries of the Company. | ||

| 2. | The status of the specified wholly-owned subsidiary as of the end of this term was as follows: | |||

Name of specified wholly-owned subsidiary: Canon Medical Systems Corporation | ||||

Address of specified wholly-owned subsidiary: 1385 Shimoishigami, Otawara-shi, Tochigi Pref., Japan | ||||

Book value of shares of specified wholly-owned subsidiary at the Company: 658,304 million yen | ||||

Amount of total assets of the Company: 2,914,232 million yen | ||||

Consolidated Status

The number of consolidated subsidiaries was 330, and the number of affiliated companies accounted for by the equity method was 10 as of the end of this term.

26

(9) Canon Group Global Network

Major Domestic Bases | ||||

| Canon Inc. | R&D, Manufacturing and Marketing | Manufacturing | ||

Headquarters [Tokyo] | Canon Electronics Inc. [Saitama Pref.] | Oita Canon Inc. [Oita Pref.] | ||

Yako Office [Kanagawa Pref.] | Canon Finetech Nisca Inc. [Saitama Pref.] | Nagasaki Canon Inc. [Nagasaki Pref.] | ||

Kawasaki Office [Kanagawa Pref.] | Canon Precision Inc. [Aomori Pref.] | Canon Chemicals Inc. [Ibaraki Pref.] | ||

Tamagawa Office [Kanagawa Pref.] | Canon Components, Inc. [Saitama Pref.] | Oita Canon Materials Inc. [Oita Pref.] | ||

Kosugi Office [Kanagawa Pref.] | Canon ANELVA Corporation [Kanagawa Pref.] | Fukushima Canon Inc. [Fukushima Pref.] | ||

Hiratsuka Plant [Kanagawa Pref.] | Canon Machinery Inc. [Shiga Pref.] | Nagahama Canon Inc. [Shiga Pref.] | ||

Ayase Plant [Kanagawa Pref.] Fuji-Susono Research Park [Shizuoka Pref.] Utsunomiya Office [Tochigi Pref.] Toride Plant [Ibaraki Pref.] Ami Plant [Ibaraki Pref.] Oita Plant [Oita Pref.] | Canon Tokki Corporation [Niigata Pref.] | Miyazaki Canon Inc. [Miyazaki Pref.] | ||

Canon Medical Systems Corporation [Tochigi Pref.] |

Marketing | |||

Canon Marketing Japan Inc. [Tokyo] | ||||

Canon System & Support Inc. [Tokyo]

| ||||

| R&D | ||||

Canon IT Solutions Inc. [Tokyo] | ||||

Major Overseas Bases | ||||

Americas Marketing Canon U.S.A., Inc. [U.S.A.] Canon Solutions America, Inc. [U.S.A.] Canon Canada Inc. [Canada] Canon Mexicana, S.de R.L. de C.V. [Mexico] Canon do Brasil Indústria e Comércio Ltda. [Brazil] Canon Medical Systems USA, Inc. [U.S.A.]

Manufacturing Canon Virginia, Inc. [U.S.A.]

R&D Canon Nanotechnologies, Inc. [U.S.A.]

Europe, Middle East, Africa Marketing Canon Europa N.V. [Netherlands] Canon Europe Ltd. [U.K.] Canon (UK) Ltd. [U.K.] Canon France S.A.S. [France] Canon Deutschland GmbH [Germany] Canon Middle East FZ-LLC [U.A.E.] Canon South Africa (Pty) Ltd. [South Africa]

Manufacturing Canon Bretagne S.A.S. [France] Canon Production Printing Netherlands B.V. [Netherlands]

R&D Canon Research Centre France S.A.S. [France]

R&D, Manufacturing and Marketing Axis Communications AB [Sweden] | Asia, Oceania Marketing Canon (China) Co., Ltd. [China] Canon Hongkong Co., Ltd. [Hong Kong] Canon Singapore Pte. Ltd. [Singapore] Canon India Pvt. Ltd. [India] Canon Australia Pty. Ltd. [Australia]

Manufacturing Canon Dalian Business Machines, Inc. [China] Canon Zhongshan Business Machines Co., Ltd. [China] Canon (Suzhou) Inc. [China] Canon Inc., Taiwan [Taiwan] Canon Hi-Tech (Thailand) Ltd. [Thailand] Canon Prachinburi (Thailand) Ltd. [Thailand] Canon Vietnam Co., Ltd. [Vietnam] Canon Opto (Malaysia) Sdn.Bhd. [Malaysia] Canon Business Machines (Philippines), Inc. [Philippines] | |||

27

2. Shares of the Company

| Number of Shares Issuable | 3,000,000,000 shares |

Issued Shares, Capital Stock, Number of Shareholders

|

As of the end of the Previous Term

|

|

|

Change during This Term

|

|

|

As of the end of This Term

|

| ||||

Issued Shares (share)

|

|

1,333,763,464

|

|

|

0

|

|

|

1,333,763,464

|

| |||

Capital Stock (yen)

|

|

174,761,797,475

|

|

|

0

|

|

|

174,761,797,475

|

| |||

Number of Shareholders (person)

|

|

428,883

|

|

|

Decrease of 9,531

|

|

|