UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-23247

(Investment Company Act File Number)

XAI Octagon Floating Rate & Alternative Income Term Trust

(Exact Name of Registrant as Specified in Charter)

321 North Clark Street, Suite 2430

Chicago, IL 60654

(Address of Principal Executive Offices)

John P. McGarrity, Esq.

XA Investments LLC

321 North Clark Street, Suite 2430

Chicago, IL 60654

(Name and Address of Agent for Service)

(312) 374-6930

(Registrant’s Telephone Number)

Date of Fiscal Year End:September 30

Date of Reporting Period:March 31, 2019

| Item 1. | Reports to Stockholders. |

TABLE OF CONTENTS

| Shareholder Letter | 1 |

| Questions & Answers | 2 |

| Trust Portfolio Information | 8 |

| Schedule of Investments | 10 |

| Statement of Assets and Liabilities | 17 |

| Statement of Operations | 18 |

| Statements of Changes In Net Assets | 19 |

| Statement of Cash Flows | 20 |

| Financial Highlights | 21 |

| Notes to Financial Statements | 22 |

| Additional Information | 31 |

Beginning on January 1, 2021, as permitted by regulations adopted by the SEC, paper copies of XAI Octagon Floating Rate & Alternative Income Term Trust’s (“the Trust”) annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Trust or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Trust’s website (www.xainvestments.com/XFLT), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Trust by contacting your financial intermediary, such as a broker-dealer or bank.

Beginning January 1, 2019, you may elect to receive all future reports in paper free of charge. If you own these shares through a financial intermediary, such as a broker-dealer or bank, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Trust, you can inform the Trust that you wish to continue receiving paper copies of your shareholder reports by calling (888) 903-3358. Your election to receive reports in paper will apply to all funds held with the fund complex if you invest directly with the Trust or to all funds held in your account if you invest through your financial intermediary.

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Shareholder Letter |

March 31, 2019 (Unaudited)

Dear Shareholder:

We thank you for your investment in XAI Octagon Floating Rate & Alternative Income Term Trust (the “Trust”). This semi-annual report covers the six-month period ended March 31, 2019.

XA Investments LLC (“XAI”) serves as the investment adviser to the Trust. Octagon Credit Investors, LLC (“Octagon”) serves as the Trust’s investment sub-adviser and is responsible for the management of the Trust’s portfolio of investments. The investment objective of the Trust is to seek attractive total return with an emphasis on income generation across multiple stages of the credit cycle. The Trust seeks to achieve its investment objective by investing in a dynamically managed portfolio of opportunities primarily within the private credit markets. Under normal market conditions, the Trust will invest at least 80% of its Managed Assets in floating-rate credit instruments and other structured credit investments. There can be no assurance that the Trust will achieve its investment objective.

The last six-months were characterized by market turbulence as retail loan fund outflows accelerated in the fourth quarter of 2018 and continued into 2019, reflecting investor concerns over the U.S. Federal Reserve’s (the “Fed”) more dovish stance on interest rates. Loan and collateralized loan obligation (“CLO”) prices rebounded in early 2019, as institutional investors perceived the most compelling yields and appreciation potential in senior loans in quite some time. In the context of healthy credit fundamentals, we expect the loan asset class to remain an attractive allocation within fixed income markets, despite technical volatility. The stable U.S. economic outlook further supports the case for loans and CLO debt and equity. We expect continued institutional demand for floating rate products given attractive relative yields compared to other fixed income asset classes without the attendant interest rate duration risk. Though we recognize the potential for bouts of market volatility owing to exogenous issues such as trade policy, interest rate movements, and other political/international uncertainties, we remain constructive on the fundamental soundness of the U.S. credit markets. Nevertheless, we will continue to closely monitor these risks, which may also potentially create attractive buying opportunities for the Trust.

For the six-months ended March 31, 2019, the S&P 500 Index, the Bloomberg Barclays U.S. High Yield 1% Issuer Capped Index and the Trust’s benchmark, the S&P/LSTA Leveraged Loan 100 Index, generated returns of 1.75%, -2.27%, and -0.40%1, respectively.

For the six-months ended March 31, 2019, the Trust experienced a decline in net assets resulting from operations of approximately $2.4 million, or -$0.30 per average common share (inclusive of unrealized gains). This represents an annualized return on the Trust’s common equity of approximately -2.88% since September 30, 2018.

From October 1, 2018 through March 31, 2019, the Trust’s net asset value (“NAV”) decreased by 7.47% from $9.50 per common share to $8.79 per common share largely reflecting unrealized losses due to valuation changes for the Trust’s investments in CLO debt, CLO equity, and opportunistic loan segments. As described below, during the last six-months, the Trust paid aggregate distributions totaling $0.414 per common share with respect to distributions declared. The distribution declared April 1, 2019 represents an annualized distribution rate of 9.54% based on the Trust’s closing market price of $8.68 per common share on March 29, 2019.

The closing price per share of the Trust’s common shares was $8.68 on March 29, 2019, representing a 1.25% discount to NAV per common share as of such date. From the Trust’s IPO on September 27, 2017 through March 31, 2019, the Trust’s common shares have traded on average at a 0.77% discount to NAV.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Trust’s website at www.xainvestments.com/XFLT.

Sincerely,

Kimberly Flynn

Managing Director

XA Investments LLC

May 21, 2019

| Semi-Annual Report | March 31, 2019 | 1 |

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Questions & Answers |

March 31, 2019 (Unaudited)

Lauren M. Basmadjian, Senior Portfolio Manager at Octagon Credit Investors, LLC (“Octagon”) and a member of the firm’s Investment Committee, serves as lead portfolio manager of XAI Octagon Floating Rate & Alternative Income Term Trust (the “Trust”). Ms. Basmadjian is supported by a team of Octagon investment professionals in the day-to-day management of the Trust’s portfolio, including the following members of the firm’s Investment Committee: Andrew D. Gordon (Octagon’s co-founder, Chief Executive Officer and Co-Chief Investment Officer), Michael B. Nechamkin (Co-Chief Investment Officer and Senior Portfolio Manager), Gretchen M. Lam (Senior Portfolio Manager) and Lauren B. Law (Portfolio Manager). Herein, Ms. Basmadjian discusses the market environment and the Trust’s performance for the six-month period ended March 31, 2019.

What is the Trust’s investment objective and how is it pursued?

The Trust’s investment objective is to seek attractive total return with an emphasis on income generation across multiple stages of the credit cycle. The Trust seeks to achieve its investment objective by investing in a dynamically managed portfolio of opportunities primarily within the private credit markets. Under normal market conditions, the Trust will invest at least 80% of its Managed Assets in floating rate credit instruments and other structured credit investments.

The Trust’s investments include (i) structured credit investments, including collateralized loan obligation (“CLO”) debt and subordinated (i.e., residual or equity) securities; (ii) traditional corporate credit investments, including leveraged loans and high yield bonds; (iii) opportunistic credit investments, including stressed and distressed credit situations and long/short credit investments; and (iv) other credit-related instruments.

Leveraged loans are debt obligations (also commonly referred to as “senior loans” or “floating rate loans”) issued by a bank to a corporation that generally holds legal claim to the borrower’s assets above all other debt obligations. Leveraged loans have floating rates that typically fluctuate according to LIBOR. LIBOR stands for London Interbank Offered Rate and is the benchmark rate that most of the world’s leading banks charge each other for short-term loans.

CLOs are a type of structured credit vehicle which typically invest in a diverse portfolio of broadly syndicated leveraged loans. CLOs finance this pool of loans with a capital structure that consists of debt and equity. CLO debt includes senior and mezzanine debt (collectively, “liabilities”) of a CLO structure with tranches rated from AAA down to BB or B. Interest earned from the underlying loan collateral pool of a CLO is used to pay the coupon interest on the CLO liabilities. CLO debt investors earn returns based on spreads above 3-month LIBOR. CLO equity represents a residual stake in the CLO structure and is the first loss position in the event of defaults and credit losses. CLO equity investors receive the excess spread between the CLO assets and liabilities and expenses. CLO equity is junior in priority of payment and is subject to certain payment restrictions generally set forth in an indenture governing the notes.

The Trust pursues its investment objective by investing primarily in below investment grade credit instruments but may invest without limitation in investment grade credit instruments. Below investment grade credit instruments are regarded as having predominantly speculative characteristics with respect to capacity to pay interest and to repay principal. The Trust may invest without limitation in credit instruments that are illiquid.

The Trust uses leverage to seek to enhance total return and income. The Trust uses leverage through borrowing from a financial institution. Although leverage may create an opportunity for increased return and income for shareholders, it also results in additional risks and can magnify the effect of any losses. There is no assurance that the strategy will be successful. If income and gains on securities purchased with leverage proceeds are greater than the cost of the leverage, common shareholders’ return will be greater than if leverage had not been used. Conversely, if the income or gains from the securities purchased with the proceeds of leverage are less than the cost of leverage, common shareholders’ return will be less than if leverage had not been used.

What were the significant events affecting the economy and market environment over the past six months?

Global financial markets experienced pronounced volatility during the fourth quarter of 2018 in response to mounting macro concerns, notably escalating U.S./China trade war tensions, weaker economic data and slowing growth in the EU, China, and Japan, sharp declines in commodity prices, and shifting interest rate expectations. The uncertain economic outlook arrested expectations for forecasted rate hikes that were reflected in the flattening of the yield curve (with temporary inversions between the two-year and the five-year) and the 10-year moving from a 3.26% peak in October to a sub-2.6% trough by year-end. In mid-December, the U.S. Federal Reserve (the “Fed”) delivered its ninth rate hike in three years but also made a dovish pivot, and subsequently reinforced its stance at the Federal Open Market Committee meeting in March by indicating no expected rate hikes in 2019. As a result, investors rotated to a “duration on” positioning in fixed rate assets and shifted away from floating rate products, which led to retail outflows from the loan asset class. The Fed is currently targeting 2.25-2.50% on its benchmark rate, and we expect inflation perceptions and interest rate movements will remain at the forefront of investor concerns. Financing the 2018 tax act will increase budget deficits; as quantitative easing ends, incremental government debt will need to be issued and financed, which could pressure interest rates.

The broader markets rallied in January and February, supported by increasingly accommodative central bank actions, positive macroeconomic developments, and better-than-expected corporate earnings. Loan prices rebounded in January and February but retreated in March, as the pace of retail loan fund outflows accelerated over the month following the Fed’s announcement to maintain benchmark rates. In the absence of mounting credit stress (as indicated by low default rates and generally healthy corporate earnings), we welcome such technically-driven market movements. At current trading levels, we believe loans offer meaningful risk-adjusted yields and convexity and alpha opportunities for fundamental credit pickers.

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Questions & Answers |

March 31, 2019 (Unaudited)

The imposition of tariffs and escalating concerns of a trade war with China also represented a significant development within the past year. Given the heightened threat of increased tariffs against China and the EU, and potential retaliatory actions, trade policy has become a greater concern for the borrowers in the U.S. loan market. The risks surrounding trade policy will likely translate to higher cost of goods sold in some industries, although projections are difficult due to the uncertainty of the ultimate/final policy, increased complexity of many supply chains, moves to alternate sourcing in cheaper countries, foreign exchange fluctuations, and the ability to increase prices in a strong U.S. economy. We are carefully monitoring and analyzing the impact of these developments on specific sectors and credits in the market.

We also continue to witness secular changes in several industry sectors, driven by increasingly available technological innovation. In certain instances, the pace and implementation of technological change(s) has impacted the risk profile of borrowers in the U.S. loan markets. Technological advancements may augur the decline of existing business models, or new and improved technology can represent a substantial advantage, possibly best illustrated in the retail industry. Although we remain in the “expansion” phase of the credit cycle, we also have seen “rolling recessions” in certain sectors in recent years, including energy and metals and mining. Retail represents the latest sector recession, and we anticipate concerns over traditional brick-and-mortar retail may spill over into commercial real estate in the medium term (owing to store closings, rent negotiations, etc.). Mini-default cycles in the energy and retail sectors have provided the Trust with select attractive opportunistic loan investment opportunities, and Octagon remains focused on sourcing idiosyncratic opportunities with strong return potential in the context of a relatively benign fundamental credit environment.

How does Octagon view covenant-lite or “cov-lite” loans in today’s marketplace?

Covenant-lite or “cov-lite” loans are a type of loan that is issued with fewer restrictions on the borrower and fewer protections for the lender than historically required by credit markets. Covenant-lite loan issuance is the norm in today’s loan markets, and currently represent nearly 80% of total outstanding loan issuance.1 Fewer covenants can offer more flexibility for struggling companies to work out of their stress, but also result in a lower recovery for lenders in the event of a default.

It is important to consider the loan holder’s security within the asset collateral pool. Recoveries are driven by collateral quality, not covenants, in the event of default. We believe that the perception that cov-lite loans are more likely to default than loans with financial maintenance covenants is misplaced, as evidenced by lower historical default rates for cov-lite loans compared to cov-heavy loans (S&P Global Market Intelligence has reported that loans with traditional protections barely fare any better in recovery than cov-lite loans issued before 20102). While any measure of lender protection is preferred, Octagon is thoroughly capable of evaluating the creditworthiness of a cov-lite borrower and assessing relative value. We believe it is more important to focus on certain covenant terms such as restricted payment baskets, unrestricted subsidiaries, and incremental debt incurrence terms, among others. While we have seen deterioration of credit agreements for new issue loans in the recent past, market corrections within the past six months have brought some level of increased discipline in issuer terms.

Describe the current market conditions for the leveraged loan market and Octagon’s outlook.

Leveraged loan market conditions have improved over the first few months of 2019, following a turbulent fourth quarter of 2018 driven by technical disruptions. Amid broader market turmoil, loan prices began to soften in late-October due to outflows from retail loan investors (mutual funds and exchange traded funds (“ETFs”)). The uncertain economic outlook precipitated changes to forecasted rate hikes that were reflected in the flattening yield curve. We believe that shifting rate expectations and yield curve movements were the major driver of loans’ negative performance through year-end. All told, retail loan investors withdrew $19.7 billion in the fourth quarter, including $14.6 billion in December – a period when liquidity is typically limited.3 Retail fund managers sold their most liquid loans to meet investor redemptions, resulting in heightened price volatility for those assets. Forced sellers created compelling relative value opportunities in the secondary market, and Octagon took advantage of price weakness to buy performing credits at prices we considered attractive (bid price range of $95 - $98). As of April 3, 2019, retail loan funds have reported 20 straight weeks of net outflows, and retail buyers’ share of the loan market has decreased to roughly 10%.4 It bears noting that periods of technically driven market volatility tend to create buying opportunities for the Trust, as has been the case over the past six months.

Looking at another key technical driver for the loan market, the pace of new CLO formation has picked up after a slow start in January. Improving loan prices over the first quarter brought many open warehouses back to breakeven levels following the late-2018 market sell-off. New CLO issuance totaled $29.3 billion in the first quarter of 2019, on track to meet full-year primary supply forecasts of $110-125 billion.5 Importantly, CLOs comprise roughly 60% of the primary institutional loan market investor base and represent stable, locked-up pools of capital that are not subject to redemptions or forced selling. While CLOs trade loans in smaller increments compared to loan mutual funds which transact in larger blocks that can meaningfully move asset prices, increased CLO demand for loans should help offset price pressures during periods of retail fund outflows.

| Semi-Annual Report | March 31, 2019 | 3 |

XAI Octagon Floating Rate &

Alternative Income Term Trust | Questions & Answers |

March 31, 2019 (Unaudited)

With respect to new issue loan supply, over the past six months, primary loan issuance was driven by M&A transactions, with significantly less refinancing and repricing activity than in prior quarters due to spread widening. Despite a turbulent fourth quarter, M&A-related institutional loan issuance reached an all-time record in 2018. New issue institutional loan volume in the first quarter of 2019 totaled $77.9 billion, slightly above that of the previous quarter, but representing the second lightest quarter since the first quarter of 2016.6 We believe the relatively light forward new issue calendar should provide support for loan prices.

Although recent news articles have focused on increasing leverage levels and deteriorating lending standards in the U.S. loan market, we believe the loan asset class remains fundamentally sound. Recent LBOs have typically been for well-performing companies demonstrating growth trends, and the higher purchase price multiples for these transactions have usually reflected increased equity contributions from sponsors rather than excessive leverage as seen in previous cycles, creating additional subordination for lenders. Moreover, borrowers in the U.S. loan markets have been supported by strong earnings growth, which helped offset rising interest expense and bolstered cash flow coverage (or the number of times financial obligations of a company are covered by its earnings, which has increased to over 3.6x on average as of year-end 2018, compared to 2.1x in 20077(even incorporating nine increases in the Fed Funds rate within the past three years)). On average, below investment grade issuers reported revenue growth of 6.4% in the fourth quarter of 2018, which represented the tenth consecutive quarter of year-over-year increases.8 Meanwhile, EBITDA for below investment grade borrowers grew 13.5% year-over-year as of December 31, 2018.8 Leverage for below investment grade borrowers declined for the tenth consecutive quarter to a six-year low of 3.98x in the fourth quarter of 2018.8 Despite strong earnings growth, some companies are facing inflationary pressures from both wage growth and raw material price increases. We believe many borrowers will attempt to find new efficiencies or try to raise prices to pass through these costs. Furthermore, consumer spending should increase as more jobs are created and wages move higher, to the benefit of the overall economy.

We do not anticipate a significant downturn in the business cycle in the medium term, and we expect defaults to remain low and concentrated in certain industries. We agree with economists’ consensus estimates that U.S. GDP will grow at a healthy (albeit likely slower) rate in 2019.9 While overall corporate earnings are positive, we expect increased dispersion among issuers. We recognize the potential for wage inflation, commodity price increases, and the strong U.S. dollar/trade policy (among other factors) to impact margins for certain borrowers in the U.S. credit markets. We also continue to monitor the risks of weaker deal terms and protections (including the loosening of covenant structures), as well as the higher amount of pro forma adjustments to EBITDA/add-backs that could understate true borrower leverage.

Describe the current market conditions for the CLO market and Octagon’s outlook.

2018 was the busiest year so far in the CLO 2.0 era (post 2008 financial crisis issuance), with $127 billion of new CLO issuances, as well as $122 billion of refinancing or reset deals.10 However, CLO liability spreads ended 2018 meaningfully wider on the year, as spread widening intensified in the fourth quarter in tandem with the loan market sell-off. Primary CLO liability spreads continued to widen in the first quarter of 2019 due to reduced investor demand as LIBOR decreased. CLO equity investors saw lower distributions over the past year due to weighted average spread compression for the underlying loan assets in CLOs, and the basis risk between 1-month and 3-month LIBOR (CLOs finance at 3-month LIBOR, while underlying borrowers have the option to pay 1-month versus 3-month LIBOR). As the weighted average spread for underlying collateral portfolios has widened, CLO equity distributions should increase, a major positive development for equity following months of loan spread tightening.

In our view, today’s environment represents an opportunity for CLO managers to capture price appreciation in loans (or “build par” in CLO parlance), compared to prior quarters. CLO debt and equity investors should continue to benefit from CLO managers’ ability to successfully build par through discounted purchases of performing loan assets. The median annualized equity distribution for reinvesting U.S. CLOs is 14.6% as of mid-March 2019.11 Wider loan spreads and relatively favorable CLO liability spreads combined with par building opportunities should significantly benefit CLO equity investors over the long-term. Potential bouts of market turbulence may also benefit CLO equity. When credit spreads widen, loan prepayments and amortizations are recycled into discounted/higher yielding assets during periods of market volatility, while CLO liability spreads are fixed, resulting in higher CLO equity distributions. We therefore believe CLO equity continues to offer compelling risk-adjusted returns to long-term investors seeking income strategies, especially in more volatile loan markets.

CLO primary demand has been impacted by a dovish Fed outlook and investors’ recalibrated rate expectations, resulting in wider CLO liability spreads particularly at the top of the CLO liability stack (AAA rated debt tranches). After a slow start to the year, the pace of new CLO issuance picked up later in the first quarter of 2019, and the large pipeline of deals (100+ open warehouses as of March 31) suggests new CLO formation should continue to be healthy in the second quarter, further supported by compelling relative value of CLO AAA paper for Japanese buyers due to lower JPY/USD hedging costs, an influx of capital from dedicated CLO equity investment vehicles raised in 2016-2018, and new/debut CLO managers with large internal equity commitments continuing to enter the market. Higher new issue deal supply, relatively muted domestic AAA demand, and investor focus away from floating rate assets should limit any sustained tightening in CLO debt tranches in the near-to medium-term. We currently see attractive value in BB rated CLO debt tranches, with all-in yields for new issue BB notes coming at an L+700 bps context. In our view, CLO debt has become more compelling as trading prices now present greater convexity and total return potential than in prior quarters.

XAI Octagon Floating Rate &

Alternative Income Term Trust | Questions & Answers |

March 31, 2019 (Unaudited)

How did the Trust perform for the six months ended March 31, 2019?

For the six-month period ended March 31, 2019, the Trust provided a total return on market price of -7.03% and a total return based on NAV of -2.88%. NAV return includes the deduction of management fees, operating expenses, and all other Trust expenses. All Trust returns cited – whether based on net asset value (“NAV”) or market price – assume the reinvestment of all distributions. As of March 31, 2019, the Trust’s market price of $8.68 represented a discount of 1.25% to its NAV of $8.79. The market value of the Trust’s shares fluctuates from time-to-time and may be higher or lower than the Trust’s NAV. Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted.

What were the distributions over the period?

From October 1, 2018 through March 31, 2019, the Trust paid a monthly distribution of $0.069 per share. The Trust declared its first distribution for the period on September 4, 2018 which was payable on October 1, 2018. The distribution declared April 1, 2019 represents an annualized distribution rate of 9.54% based on the Trust’s closing market price of $8.68 on March 29, 2019. The Trust’s distribution rate is not constant, and the amount of distributions, when declared by the Trust’s Board of Trustees, is subject to change based on the performance of the Trust. Please see Note 4 on page 25, and the “Distributions” section of Additional Information on page 32 for more information on distributions for the period.

What influenced the Trust’s performance for the six-months ended March 31, 2019?

Pronounced volatility in the fourth quarter was reflected in lower valuations across most assets, which negatively impacted the Trust’s performance for the six-month period ended March 31, 2019. While the Trust generated strong returns in the first quarter of 2019 as asset prices improved, performance for the six-month period was weighed down by outsized unrealized losses in the prior quarter. During the six-month period, the Trust’s portfolio generated a net gain in its senior loan segment (first lien and second lien loans) driven by interest income, but experienced net investment losses in all other asset class segments, including CLO equity, CLO debt, high yield bonds & equity, and opportunistic loans. The Trust’s CLO equity, CLO debt, and opportunistic loan segments experienced the largest net losses; for the period, approximate net losses for each segment were ($0.04) per share, or ($0.12) per share on a combined basis. The majority of the Trust’s largest performance detractors during the period were CLO equity positions. As asset prices decreased and loan spreads widened in the second half of the fourth quarter, CLO equity NAVs decreased. The Trust’s CLO equity positions collected quarterly distribution payments totaling $3,615,901, or $0.43 per share, during the six-month period, which were offset by market value losses of $2,283,258, or ($.27) per share. It bears noting that the recent market volatility may help boost quarterly equity payments, to the benefit of the Trust.

Relevant indices for the markets in which the Trust invests include the Trust’s benchmark, the S&P/LSTA 100 Leveraged Loan Index, which returned -0.40% for the six-month period, the Bloomberg Barclays U.S. High Yield 1% Issuer Capped Index, which returned -2.27% for the six-month period, and the JP Morgan BB/B CLO Debt Index, which returned 0.54% for the six-month period.12 There is no representative benchmark index for CLO equity in the marketplace.

How is the Trust positioned for the remainder of 2019?

Looking ahead, we believe that the Trust is well-positioned across its primary investment segments to meet its investment objective. As of March 31, 2019, the Trust is invested in floating-rate first lien loans (40.9% of the total portfolio on a market value basis), second lien loans (7.9%), CLO equity (33.4%) and CLO debt securities (15.0%). In the current market environment, we are focused on loans offering attractive spreads and call protection. We believe the Trust’s loan positions are well diversified across industry sectors, with health care providers and services, software, and hotels, restaurants & leisure representing the largest exposures as of March 31, 2019. We generally expect to maintain the Trust’s current allocations to CLO equity and CLO debt. The Trust’s CLO debt investments are presently skewed towards BB-rated tranches versus single-B tranches. We maintain a generally constructive view of CLO equity over the longer term. Lastly, the Trust has maintained low exposure to high yield bonds over the period; as of March 31, 2019, high yield bond positions represented approximately 1.1% of the Trust’s portfolio on a market value basis. We expect to keep the Trust’s bond exposure relatively low, as we continue to prefer loans that offer comparable all-in yields, with lower duration risk, seniority, collateral, and floating rate coupons.

How is the Trust positioned to perform the current interest rate environment?

The Trust is positioned conservatively in terms of duration, with predominantly all of the Trust’s investments in floating-rate or adjustable securities based on changes in LIBOR. Over 95% of the Trust’s portfolio as of March 31, 2019 was invested in leveraged loans, CLO debt and CLO equity.13 We will continue to actively position the Trust to take advantage of a relatively benign credit environment.

The Fed is undoubtedly more dovish today than it appeared towards the end of 2018. From a fundamental perspective, we believe a dovish Fed and lower rates will improve the loan market over time by helping to keep defaults low and supporting economic growth. However, a dovish Fed could have negative implications on market technicals in the near-term, as the probability of rate hikes recedes. At present, we think many asset prices and new issue deals are attractive, and we continue to believe it is still a good time to buy loans. Nevertheless, we do perceive crosswinds in the coming months, such as continued retail loan fund outflows and possible first quarter earnings surprises on a credit-by-credit basis creating opportunities for credit pickers. In today’s environment, we believe active portfolio management and strong fundamental credit work will be key to outperformance.

| Semi-Annual Report | March 31, 2019 | 5 |

XAI Octagon Floating Rate &

Alternative Income Term Trust | Questions & Answers |

March 31, 2019 (Unaudited)

Credit spreads currently remain attractive relative to post-crisis levels, and all-in loan coupons have increased to a high of 5.98% for the S&P/LSTA Leveraged Loan Index.14 Current loan yields are at the widest levels since 2009, save for in 2016 when defaults were higher due to increased stress in certain industry sectors. In March, the trailing 12-month loan default rate dropped to 0.93% - the lowest level in nearly seven years.1 We expect defaults to increase modestly as the year progresses, but in the near-term we do not anticipate defaults to reach 2016 levels. Defaults are likely to be more idiosyncratic, as opposed to widespread across the loan market.

Leveraged loan investors earn returns based on spreads above LIBOR. The rates on leveraged loans typically reset at fixed intervals, usually a monthly or quarterly basis. Leveraged loans do not move in tandem with U.S. Treasuries, but rather with LIBOR. The benefit of the floating rate is that it provides an element of protection against duration risk resulting from rising short-term interest rates.

CLOs are floating-rate instruments designed to mitigate duration risk and therefore may not directly suffer the same adverse effects from rising rates as traditional fixed income investments. As LIBOR increases, CLO debt distributions increase (notwithstanding any fixed rate tranches). CLO equity is more nuanced; once LIBOR has risen above a specified floor, “the spread” paid to equity holders increases as interest rates rise. In contrast, interest rates on traditional fixed income investments are locked and adversely impacted by a rising rate environment. Given the floating-rate nature of their coupon payments, CLOs are well-positioned for a rising interest rate environment.

Discuss the Trust’s use of leverage.

The Trust uses leverage as part of its investment strategy, to finance the purchase of additional securities that may provide increased income and greater appreciation potential to common shareholders than could be achieved from a portfolio that is unlevered. With the low cost of borrowing and relatively low default rates generally among U.S. companies, the amount of leverage used by the Trust is highly accretive to income generation. The Trust currently employs leverage through bank borrowing. As of March 31, 2019, the amount of leverage was approximately 32.88% of the Trust’s Managed Assets (including proceeds of leverage). While leverage increases the income of the Trust in yield terms, it also amplifies the effects of changing market prices in the portfolio and can cause the Trust’s NAV to change to a greater degree than the market as a whole. This change in NAV can create volatility in Trust pricing but should not affect the Trust’s ability to pay distributions under normal circumstances.

Index Definitions

The Trust does not seek to track any index. Index returns are for illustrative purposes only, do not reflect the deduction of fees and expenses and do not represent the performance of the Trust. It is not possible to invest directly in an index.

Bloomberg Barclays U.S. High Yield 1% Issuer Capped Index measures the performance of high-yield bonds, with an individual issuer cap of 1%.

J.P. Morgan CLO Debt Index represents the post-crisis J.P. Morgan Collateralized Loan Obligation Index (“CLOIE”). The CLOIE is a benchmark to track the market for U.S. dollar denominated broadly-syndicated, arbitrage CLOs. The CLOIE is divided by origination (pre- versus post-crisis) and is broken out further into six original rating classes (AAA, AA, A, BBB, BB, B).

S&P/LSTA U.S. Leveraged Loan 100 Index is a market value-weighted index designed to measure the performance of the U.S. leveraged loan market. In conjunction with Standard & Poor's/LCD, the Leveraged Syndications & Trading Association (“LSTA”) developed the S&P/LSTA U.S. Leveraged Loan 100 Index (“L100”). The L100 is designed to reflect the largest loan facilities in the leveraged loan market. It mirrors the market-value-weighted performance of the 100 largest institutional leveraged loans based upon actual market weightings, spreads and interest payments. The L100 utilizes LSTA/LPC Mark-to-Market Pricing, which is based on bid/ask quotes gathered from dealers and is not based upon derived pricing models. The index uses the average bid for its market value calculation. Each loan facility’s total return is calculated by aggregating the interest return (reflecting the return due to interest paid and accrued interest), and price return (reflecting the gains or losses due to changes in the end of day prices and principal repayments). The return of each loan facility is weighted in the index based upon its market value outstanding, which reflects both the prior period’s prices as well as accrued interest. The overall index return is the aggregate of each component loan facility’s return multiplied by the market value outstanding from the prior time period.

Risks and Other Considerations

Investing involves risk, including the possible loss of principal and fluctuation of value.

The views expressed in this report reflect those of the portfolio managers only through the report period as stated on the cover. These views are expressed for informational purposes only and are subject to change at any time, based on market and other conditions, and may not come to pass. These views should not be construed as research, investment advice or a recommendation of any kind regarding the Trust or any issuer or security, do not constitute a solicitation to buy or sell any security and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation or particular needs of any specific investor.

XAI Octagon Floating Rate &

Alternative Income Term Trust | Questions & Answers |

March 31, 2019 (Unaudited)

The views expressed in this report may also include forward-looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass. Actual results or events may differ materially from those projected, estimated, assumed or anticipated in any such forward looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include general economic conditions such as inflation, recession and interest rates. Neither XAI or Octagon has any obligation to update or otherwise revise any forward-looking statements, including any revision to reflect changes in any circumstances arising after the date hereof relating to any assumptions or otherwise.

There can be no assurance that the Trust will achieve its investment objective or that any investment strategies or techniques discussed herein will be effective. The value of the Trust will fluctuate with the value of the underlying securities. Historically, closed-end funds often trade at a discount to their net asset value.

Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted.

Please see www.xainvestments.com/XFLT for a detailed discussion of the Trust’s risks and considerations. The Trust regularly updates performance and certain other data and publishes material information as necessary from time to time on its website. Investors and others are advised to check the website for updated performance information and the release of other material information about the Trust. References herein to the Trust’s website are intended to allow investors public access to information regarding the Trust and does not, and is not intended to, incorporate the Trust’s website in this report.

This material is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

| 1 | As of March 31, 2019. Sources: S&P Global Market Intelligence and S&P/LSTA Leveraged Loan Index. |

| 2 | Sufficient data is not available at this time for loans issued after 2010. |

| 3 | Source: S&P Global Market Intelligence LCD News “US leveraged loans lose 2.54% in December rout, gain 0.44% in 2018” (January 2, 2019). |

| 4 | Source: J.P. Morgan US High Yield & Leveraged Loan Strategy Credit Strategy Weekly Update (April 12, 2019). |

| 5 | Wells Fargo Securities CLO and Commercial ABS Research team projects $110B in full-year 2019 (“FY”) new CLO issuance (Source: CLO Monthly Market Overview, April 1, 2019). JPMorgan CLO Research team projects $115-125B for FY new CLO issuance (Source: JPMorgan CLO Research, April 1, 2019). |

| 6 | Source: S&P Global Market Intelligence LCD Quarterly Review – First Quarter 2019. |

| 7 | Represents average cash flow coverage of outstanding loans, which is a ratio calculated as EBITDA less capital expenditures to cash interest. Source: S&P Capital IQ/SNL Financial LCD News (April 1, 2019). |

| 8 | Based on a quarterly analysis of 489 U.S. high yield companies, excluding the financials and utilities sectors. The financial data is derived from JPMorgan High Yield Credit analysts and Capital IQ. Source: J.P. Morgan North America Credit Research Credit Strategy Weekly Update (March 22, 2019). |

| 9 | Source: Bloomberg Article “Big Start to Year for U.S. Growth Seen Fizzling Later in 2019” (May 9, 2019). |

| 10 | Source: Wells Fargo Research “The CLO Salmagundi: US CLO 2018 Year in Review” (January 7, 2019). |

| 11 | Source: Wells Fargo Securities Structured Products Research, The U.S. CLO Manager Style Guide, March 25, 2019. Past performance has been achieved during a period of relative economic stability, and is not necessarily indicative of future results. |

| 12 | Sources: S&P/LSTA Leveraged Loan Index and S&P Capital IQ/SNL Financial Leveraged Commentary & Data, Bloomberg, J.P. Morgan Markets DataQuery. |

| 13 | As calculated by Octagon Credit Investors, LLC. Represents unaudited figures. |

| 14 | Sources: S&P/LSTA Leveraged Loan Index and S&P Capital IQ/SNL Financial Leveraged Commentary & Data. All-in Rate is calculated as the sum of the nominal spread plus the average LIBOR contract rate for all outstanding loans in the S&P/LSTA Leveraged Loan Index. |

| Semi-Annual Report | March 31, 2019 | 7 |

XAI Octagon Floating Rate &

Alternative Income Term Trust | Trust Portfolio Information |

March 31, 2019 (Unaudited)

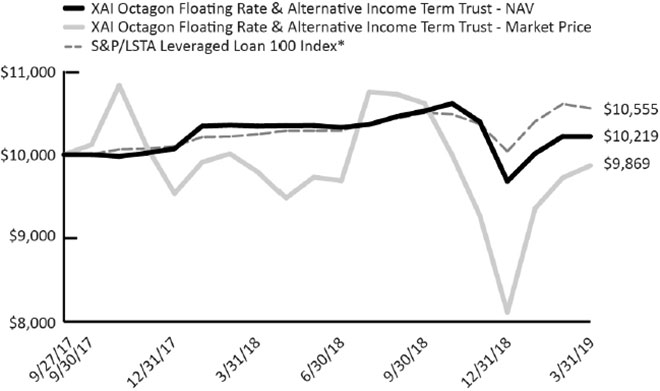

Growth of a $10,000 Investment(as of March 31, 2019)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Trust since inception.Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Trust distributions or the redemption of Trust shares. The chart assumes that distributions from the Trust are reinvested.

Summary Performance(as of March 31, 2019)

| | 1 Month | 3 Months | 6 Months | 1 Year | Since the Trust’s Inception (September 27, 2017)^ |

| XAI Octagon Floating Rate & Alternative Income Term Trust - NAV | -0.01% | 5.54% | -2.88% | -1.21% | 1.44% |

| XAI Octagon Floating Rate & Alternative Income Term Trust – Market Price | 1.49% | 21.61% | -7.03% | 0.76% | -0.87% |

| S&P/LSTA Leveraged Loan 100 Index* | -0.48% | 5.13% | 0.49% | 3.03% | 3.64% |

| * | The S&P/LSTA (Loan Syndications and Trading Association) U.S. Leveraged Loan 100 Index was the first to track the investable senior loan market. This rules-based index consists of the 100 largest loan facilities in the benchmark S&P/LSTA Leveraged Loan Index (LLI). |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than performance data quoted.

XAI Octagon Floating Rate &

Alternative Income Term Trust | Trust Portfolio Information |

March 31, 2019 (Unaudited)

Top Ten Portfolio Holdings(as a % of Total Investments)*

| Name | | Type | | |

| Madison Park Funding XVIII, Ltd. | | CLO Equity | | | 2.87% |

| CIFC Funding 2018-I, Ltd. | | CLO Equity | | | 2.78% |

| Apidos CLO XXVIII | | CLO Equity | | | 2.59% |

| THL Credit Wind River 2016-1 CLO, Ltd. | | CLO Equity | | | 2.50% |

| OZLM XIX, Ltd. | | CLO Equity | | | 2.35% |

| CIFC Funding 2017-V, Ltd. | | CLO Equity | | | 2.21% |

| Carlyle Global Market Strategies CLO 2013-1, Ltd. | | CLO Equity | | | 2.04% |

| Marble Point CLO XI, Ltd. | | CLO Equity | | | 1.96% |

| Thacher Park CLO, Ltd. | | CLO Equity | | | 1.84% |

| Asurion LLC | | Secured Second Lien Loan | | | 1.55% |

| Total | | | | | 22.69% |

| * | Holdings are subject to change |

Asset Allocation(as a % of Total Investments)

| Senior Secured First Lien Loans | | | 40.86% |

| CLO Equity | | | 33.36% |

| CLO Debt | | | 14.98% |

| Secured Second Lien Loans | | | 7.86% |

| Corporate Bonds | | | 1.10% |

| Money Market Mutual Funds | | | 1.84% |

| Semi-Annual Report | March 31, 2019 | 9 |

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Schedule of Investments |

March 31, 2019 (Unaudited)

| | | Coupon(a) | | Reference Rate & Spread | | Maturity Date | | Principal Amount | | | Value | |

| CORPORATE BONDS - 1.67%* (1.10% of Total Investments) |

| Health Care Providers & Services - 0.74% (0.49% of Total Investments) |

| Envision Healthcare Corp., Senior Unsecured(b) | | 8.75% | | N/A | | 10/15/2026 | | $ | 333,000 | | | $ | 296,370 | |

| Verscend Escrow Corp., Senior Unsecured(b) | | 9.75% | | N/A | | 08/31/2026 | | | 250,000 | | | | 248,594 | |

| Total Health Care Providers & Services | | | | | | | | | 583,000 | | | | 544,964 | |

| | | | | | | | | | | | | | | |

| Internet Software & Services - 0.61% (0.40% of Total Investments) |

| Veritas US, Inc. / Veritas Bermuda, Ltd., Senior Unsecured(b) | | 10.50% | | N/A | | 02/01/2024 | | | 500,000 | | | | 445,312 | |

| | | | | | | | | | | | | | | |

| Wireless Telecommunication Services - 0.32% (0.21% of Total Investments) |

| Digicel Group One, Ltd., Senior Secured First Lien(b) | | 8.25% | | N/A | | 12/30/2022 | | | 257,000 | | | | 154,200 | |

| Digicel Group Two, Ltd., Senior Unsecured(b) | | 8.25% | | N/A | | 09/30/2022 | | | 243,000 | | | | 82,620 | |

| Total Wireless Telecommunication Services | | | | | | | | | 500,000 | | | | 236,820 | |

| | | | | | | | | | | | | | | |

| Total Corporate Bonds (Cost $1,553,891) | | | | | | | | $ | 1,583,000 | | | $ | 1,227,096 | |

| | | | | | | | | | | | | | | |

| SECURED SECOND LIEN LOANS(c)- 11.88% (7.86% of Total Investments) |

| Commercial Services & Supplies - 1.02% (0.68% of Total Investments) |

| AVSC Holding Corp., Initial | | 9.99% | | 3M US L + 7.25% | | 09/01/2025 | | | 805,556 | | | | 751,181 | |

| | | | | | | | | | | | | | | |

| Communications Equipment - 0.46% (0.30% of Total Investments) |

| Global Tel*Link Corp. | | 10.75% | | 1M US L + 8.25% | | 11/29/2026 | | | 347,222 | | | | 339,121 | |

| | | | | | | | | | | | | | | |

| Construction & Engineering - 0.68% (0.45% of Total Investments) |

| Brookfield WEC Holdings, Inc., Initial | | 9.25% | | 1M US L + 6.75% | | 08/03/2026 | | | 498,810 | | | | 498,312 | |

| | | | | | | | | | | | | | | |

| Health Care Providers & Services - 1.35% (0.89% of Total Investments) |

| Albany Molecular Research, Inc., Initial | | 9.50% | | 1M US L + 7.00% | | 08/30/2025 | | | 126,466 | | | | 124,569 | |

| CVS Holdings I LP, Initial | | 9.25% | | 1M US L + 6.75% | | 02/06/2026 | | | 102,612 | | | | 100,303 | |

| Gentiva Health Services, Inc., Initial | | 9.50% | | 3M US L + 7.00% | | 07/02/2026 | | | 752,980 | | | | 768,040 | |

| Total Health Care Providers & Services | | | | | | | | | 982,058 | | | | 992,912 | |

| | | | | | | | | | | | | | | |

| Hotels, Restaurants & Leisure - 0.51% (0.34% of Total Investments) |

| Affinity Gaming, Initial | | 10.75% | | 1M US L + 8.25% | | 01/31/2025 | | | 392,857 | | | | 374,852 | |

| | | | | | | | | | | | | | | |

| Insurance - 2.34% (1.55% of Total Investments) |

| Asurion LLC, Replacement B-2 | | 9.00% | | 1M US L + 6.50% | | 08/04/2025 | | | 1,700,000 | | | | 1,720,536 | |

| | | | | | | | | | | | | | | |

| Real Estate Investment Trusts (REITs) - 1.10% (0.73% of Total Investments) |

| Capital Automotive LP, Initial Tranche B | | 8.50% | | 1M US L + 6.00% | | 03/24/2025 | | | 807,643 | | | | 806,133 | |

| | | | | | | | | | | | | | | |

| Software - 4.42% (2.92% of Total Investments) |

| EagleView Technology Corp. | | 9.98% | | 3M US L + 7.50% | | 08/14/2026 | | | 442,623 | | | | 430,451 | |

| McAfee LLC, Initial | | 11.00% | | 1M US L + 8.50% | | 09/29/2025 | | | 916,667 | | | | 922,167 | |

| MH Sub I LLC, Amendment No. 2 Initial | | 9.99% | | 1M US L + 7.50% | | 09/15/2025 | | | 750,000 | | | | 735,937 | |

See Notes to Financial Statements.

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Schedule of Investments |

March 31, 2019 (Unaudited)

| | | Coupon(a) | | Reference Rate & Spread | | Maturity Date | | Principal Amount | | | Value | |

| SECURED SECOND LIEN LOANS(c)(continued) |

| Software (continued) |

| Misys, Ltd., Dollar Term Loan | | 9.85% | | 1M US L + 7.25% | | 06/13/2025 | | $ | 1,200,000 | | | $ | 1,153,752 | |

| Total Software | | | | | | | | | 3,309,290 | | | | 3,242,307 | |

| | | | | | | | | | | | | | | |

| Total Secured Second Lien Loans (Cost $8,929,911) | | | | | | | | $ | 8,843,436 | | | $ | 8,725,354 | |

| | | | | | | | | | | | | | | |

| SENIOR SECURED FIRST LIEN LOANS(c)- 61.81% (40.86% of Total Investments) |

| Aerospace & Defense - 1.48% (0.98% of Total Investments) |

| Constellis Holdings LLC, B | | 7.74% | | 3M US L + 5.00% | | 04/21/2024 | | | 760,577 | | | | 722,549 | |

| Maxar Technologies, Inc., Initial B | | 5.25% | | 1M US L + 2.75% | | 10/04/2024 | | | 468,472 | | | | 362,733 | |

| Total Aerospace & Defense | | | | | | | | | 1,229,049 | | | | 1,085,282 | |

| | | | | | | | | | | | | | | |

| Airlines - 0.73% (0.48% of Total Investments) |

| Allegiant Travel Co., Class B | | 7.23% | | 3M US L + 4.50% | | 02/05/2024 | | | 392,758 | | | | 390,794 | |

| LifeMiles Finance, LLC (LifeMiles, Ltd.), Initial Term Loan | | 8.00% | | 3M US L + 5.50% | | 08/18/2022 | | | 146,653 | | | | 147,203 | |

| Total Airlines | | | | | | | | | 539,411 | | | | 537,997 | |

| | | | | | | | | | | | | | | |

| Auto Components - 0.66% (0.44% of Total Investments) |

| Panther BF Aggregator 2 L P, B(d) | | N/A | | L + 3.50% | | 03/18/2026 | | | 490,196 | | | | 484,377 | |

| | | | | | | | | | | | | | | |

| Automobiles - 1.55% (1.03% of Total Investments) |

| Thor Industries, Inc., Initial USD | | 6.25% | | 1M US L + 3.75% | | 02/01/2026 | | | 777,568 | | | | 739,903 | |

| Truck Hero, Inc., Initial | | 6.25% | | 1M US L + 3.75% | | 04/22/2024 | | | 414,268 | | | | 398,861 | |

| Total Automobiles | | | | | | | | | 1,191,836 | | | | 1,138,764 | |

| | | | | | | | | | | | | | | |

| Building Products - 1.80% (1.19% of Total Investments) |

| Ply Gem Midco, Inc., Initial | | 6.55% | | 3M US L + 3.75% | | 04/12/2025 | | | 492,657 | | | | 471,104 | |

| SRS Distribution, Inc., Initial | | 5.75% | | 2M US L + 3.25% | | 05/23/2025 | | | 894,382 | | | | 852,086 | |

| Total Building Products | | | | | | | | | 1,387,039 | | | | 1,323,190 | |

| | | | | | | | | | | | | | | |

| Chemicals - 1.83% (1.21% of Total Investments) |

| Innovative Water Care Global Corp., Initial | | 7.60% | | 3M US L + 5.00% | | 02/27/2026 | | | 742,857 | | | | 707,571 | |

| Solenis Holdings LLC, Initial Dollar | | 6.63% | | 3M US L + 4.00% | | 06/26/2025 | | | 644,481 | | | | 633,203 | |

| Total Chemicals | | | | | | | | | 1,387,338 | | | | 1,340,774 | |

| | | | | | | | | | | | | | | |

| Commercial Services & Supplies - 2.24% (1.48% of Total Investments) |

| Belfor Holdings, Inc., B(d) | | N/A | | L + 4.00% | | 02/13/2026 | | | 153,121 | | | | 154,270 | |

| Dun & Bradstreet Corp., Initial Borrowing | | 7.49% | | 1M US L + 5.00% | | 02/06/2026 | | | 961,744 | | | | 948,520 | |

| Harland Clarke Holdings Corp., Initial | | 7.35% | | 3M US L + 4.75% | | 11/03/2023 | | | 609,875 | | | | 545,838 | |

| Total Commercial Services & Supplies | | | | | | | | | 1,724,740 | | | | 1,648,628 | |

| | | | | | | | | | | | | | | |

| Communications Equipment - 0.62% (0.41% of Total Investments) |

| Global Tel*Link Corp. | | 6.75% | | 1M US L + 4.25% | | 11/29/2025 | | | 462,920 | | | | 459,217 | |

| | | | | | | | | | | | | | | |

| Construction & Engineering - 1.17% (0.77% of Total Investments) |

| Brand Energy & Infrastructure Services, Inc., Initial | | 6.96% | | 3M US L + 4.25% | | 06/21/2024 | | | 330,937 | | | | 316,365 | |

See Notes to Financial Statements.

| Semi-Annual Report | March 31, 2019 | 11 |

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Schedule of Investments |

March 31, 2019 (Unaudited)

| | | Coupon(a) | | Reference Rate & Spread | | Maturity Date | | Principal Amount | | | Value | |

| SENIOR SECURED FIRST LIEN LOANS(c)(continued) |

| Construction & Engineering (continued) |

| Brookfield WEC Holdings, Inc., Initial | | 6.25% | | 1M US L + 3.75% | | 08/01/2025 | | $ | 541,629 | | | $ | 539,901 | |

| Total Construction & Engineering | | | | | | | | | 872,566 | | | | 856,266 | |

| | | | | | | | | | | | | | | |

| Distributors - 1.17% (0.77% of Total Investments) |

| United Natural Foods, Inc., Initial | | 6.75% | | 1M US L + 4.25% | | 10/22/2025 | | | 1,000,000 | | | | 859,000 | |

| | | | | | | | | | | | | | | |

| Diversified Consumer Services - 2.17% (1.43% of Total Investments) |

| Staples, Inc., Closing Date | | 6.49% | | 1M US L + 4.00% | | 09/12/2024 | | | 735,849 | | | | 729,145 | |

| Travelport Finance S.à r.l., Initial(d) | | N/A | | L + 5.00% | | 03/18/2026 | | | 886,897 | | | | 861,399 | |

| Total Diversified Consumer Services | | | | | | | | | 1,622,746 | | | | 1,590,544 | |

| | | | | | | | | | | | | | | |

| Diversified Financial Services - 0.84% (0.55% of Total Investments) |

| Financial & Risk US Holdings, Inc., Initial Dollar | | 6.25% | | 1M US L + 3.75% | | 10/01/2025 | | | 634,562 | | | | 615,639 | |

| | | | | | | | | | | | | | | |

| Diversified Telecommunication Services - 3.27% (2.16% of Total Investments) |

| Altice France S.A., USD TLB-13 Incremental | | 6.48% | | 3M US L + 4.00% | | 08/14/2026 | | | 816,137 | | | | 780,226 | |

| Sorenson Communications LLC(d) | | N/A | | L + 6.50% | | 03/15/2024 | | | 229,770 | | | | 226,611 | |

| Syniverse Holdings, Inc., Tranche C | | 7.48% | | 1M US L + 5.00% | | 03/09/2023 | | | 774,303 | | | | 709,261 | |

| WideOpenWest Finance LLC, Eighth Amendment B | | 5.74% | | 1M US L + 3.25% | | 08/18/2023 | | | 714,125 | | | | 686,453 | |

| Total Diversified Telecommunication Services | | | | | | | | | 2,534,335 | | | | 2,402,551 | |

| | | | | | | | | | | | | | | |

| Electrical Equipment - 0.45% (0.30% of Total Investments) |

| AI Ladder Subco S.a r.l., Facility B | | 7.10% | | 3M US L + 4.50% | | 07/09/2025 | | | 105,593 | | | | 103,416 | |

| Energy Acquisition LP, Initial | | 6.85% | | 3M US L + 4.25% | | 06/26/2025 | | | 240,123 | | | | 230,518 | |

| Total Electrical Equipment | | | | | | | | | 345,716 | | | | 333,934 | |

| | | | | | | | | | | | | | | |

| Electronic Equipment, Instruments & Components - 3.09% (2.05% of Total Investments) |

| ConvergeOne Holdings, Corp., Initial | | 7.50% | | 1M US L + 5.00% | | 01/04/2026 | | | 875,091 | | | | 836,263 | |

| Mavenir Systems, Inc., Initial | | 8.50% | | 1M US L + 6.00% | | 05/08/2025 | | | 743,753 | | | | 738,175 | |

| Triton Solar US Acquisition Co., Initial | | 8.50% | | 1M US L + 6.00% | | 10/29/2024 | | | 293,393 | | | | 270,288 | |

| Ultra Clean Holdings, Inc., B | | 7.00% | | 1M US L + 4.50% | | 08/27/2025 | | | 445,685 | | | | 427,582 | |

| Total Electronic Equipment, Instruments & Components | | | | | | | | | 2,357,922 | | | | 2,272,308 | |

| | | | | | | | | | | | | | | |

| Energy Equipment & Services - 2.32% (1.54% of Total Investments) |

| KCA Deutag US Finance LLC, 2018 Extended | | 9.35% | | 3M US L + 6.75% | | 02/28/2023 | | | 988,816 | | | | 841,117 | |

| McDermott International, Inc. | | 7.50% | | 1M US L + 5.00% | | 05/12/2025 | | | 904,327 | | | | 864,862 | |

| Total Energy Equipment & Services | | | | | | | | | 1,893,143 | | | | 1,705,979 | |

| | | | | | | | | | | | | | | |

| Food Products - 1.65% (1.09% of Total Investments) |

| Chobani LLC, New | | 6.00% | | 1M US L + 3.50% | | 10/10/2023 | | | 508,763 | | | | 486,505 | |

| Give and Go Prepared Foods Corp., 2017 | | 6.85% | | 3M US L + 4.25% | | 07/29/2023 | | | 258,773 | | | | 235,807 | |

| H-Food Holdings LLC, 2018 Incremental B-2 | | 6.50% | | 1M US L + 4.00% | | 05/23/2025 | | | 498,750 | | | | 490,127 | |

| Total Food Products | | | | | | | | | 1,266,286 | | | | 1,212,439 | |

| | | | | | | | | | | | | | | |

| Health Care Equipment & Supplies - 1.20% (0.79% of Total Investments) |

| Femur Buyer, Inc., Initial | | 7.10% | | 3M US L + 4.50% | | 03/05/2026 | | | 437,321 | | | | 437,867 | |

See Notes to Financial Statements.

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Schedule of Investments |

March 31, 2019 (Unaudited)

| | | Coupon(a) | | Reference Rate & Spread | | Maturity Date | | Principal Amount | | | Value | |

| SENIOR SECURED FIRST LIEN LOANS(c)(continued) |

| Health Care Equipment & Supplies (continued) |

| Lanai Holdings II, Inc., Initial | | 7.49% | | 3M US L + 4.75% | | 08/29/2022 | | $ | 462,430 | | | $ | 442,777 | |

| Total Health Care Equipment & Supplies | | | | | | | | | 899,751 | | | | 880,644 | |

| | | | | | | | | | | | | | | |

| Health Care Providers & Services - 8.41% (5.56% of Total Investments) |

| Air Medical Group Holdings, Inc. | | | | | | | | | | | | | | |

| 2018 | | 5.56% | | 1M US L + 3.25% | | 04/28/2022 | | | 465,392 | | | | 437,665 | |

| 2018 New | | 6.74% | | 1M US L + 4.25% | | 03/14/2025 | | | 248,741 | | | | 233,505 | |

| BW NHHC Holdco, Inc., Initial | | 7.49% | | 1M US L + 5.00% | | 05/15/2025 | | | 870,778 | | | | 845,377 | |

| Envision Healthcare Corp., Initial | | 6.25% | | 1M US L + 3.75% | | 10/10/2025 | | | 785,852 | | | | 734,120 | |

| Gentiva Health Services, Inc., Closing Date Initial | | 6.25% | | 3M US L + 3.75% | | 07/02/2025 | | | 786,803 | | | | 787,786 | |

| Phoenix Guarantor, Inc., Initial(e) | | 6.98% | | 1M US L + 4.50% | | 03/05/2026 | | | 963,121 | | | | 946,989 | |

| Radiology Partners, Inc., B | | 7.42% | | 3M US L + 4.75% | | 07/09/2025 | | | 96,727 | | | | 96,807 | |

| Regionalcare Hospital Partners Holdings, Inc., B | | 6.98% | | 1M US L + 4.50% | | 11/16/2025 | | | 1,026,467 | | | | 1,014,119 | |

| Verscend Holding Corp., B | | 7.00% | | 1M US L + 4.50% | | 08/27/2025 | | | 1,090,711 | | | | 1,081,167 | |

| Total Health Care Providers & Services | | | | | | | | | 6,334,592 | | | | 6,177,535 | |

| | | | | | | | | | | | | | | |

| Health Care Technology - 1.34% (0.89% of Total Investments) |

| athenahealth, Inc., B | | 7.20% | | 3M US L + 4.50% | | 02/11/2026 | | | 997,586 | | | | 982,622 | |

| | | | | | | | | | | | | | | |

| Hotels, Restaurants & Leisure - 2.97% (1.96% of Total Investments) |

| AMC Entertainment Holdings, Inc., B(d) | | N/A | | L + 3.00% | | 03/20/2026 | | | 436,919 | | | | 433,424 | |

| Bulldog Purchaser, Inc., Initial(e) | | 6.25% | | 1M US L + 3.75% | | 09/05/2025 | | | 84,942 | | | | 83,615 | |

| Casablanca US Holdings, Inc., Amendment No. 2 Initial | | 6.74% | | 3M US L + 4.00% | | 03/29/2024 | | | 837,759 | | | | 808,438 | |

| NPC International, Inc., Initial | | 6.05% | | 1M US L + 3.50% | | 04/19/2024 | | | 130,519 | | | | 116,596 | |

| Red Lobster Management LLC, Initial | | 7.75% | | 1M US L + 5.25% | | 07/28/2021 | | | 745,454 | | | | 736,136 | |

| Total Hotels, Restaurants & Leisure | | | | | | | | | 2,235,593 | | | | 2,178,209 | |

| | | | | | | | | | | | | | | |

| Household Products - 0.62% (0.41% of Total Investments) |

| American Greetings Corp., Initial | | 7.00% | | 1M US L + 4.50% | | 04/06/2024 | | | 454,397 | | | | 453,261 | |

| | | | | | | | | | | | | | | |

| Industrial Conglomerates - 0.74% (0.49% of Total Investments) |

| WireCo WorldGroup, Inc., Initial | | 7.50% | | 1M US L + 5.00% | | 09/29/2023 | | | 543,806 | | | | 542,615 | |

| | | | | | | | | | | | | | | |

| Internet Software & Services - 1.84% (1.22% of Total Investments) |

| EIG Investors Corp., 2018 Refinancing | | 6.39% | | 3M US L + 3.75% | | 02/09/2023 | | | 443,041 | | | | 440,272 | |

| Veritas US, Inc., New Dollar B | | 7.02% | | 1M US L + 4.50% | | 01/27/2023 | | | 984,925 | | | | 909,361 | |

| Total Internet Software & Services | | | | | | | | | 1,427,966 | | | | 1,349,633 | |

| | | | | | | | | | | | | | | |

| IT Services - 3.46% (2.29% of Total Investments) |

| Avaya, Inc., Tranche B | | 6.78% | | 1M US L + 4.25% | | 12/15/2024 | | | 960,445 | | | | 955,442 | |

| ION Trading Technologies S.a.r.l., 2018 Initial Dollar | | 6.65% | | 3M US L + 4.00% | | 11/21/2024 | | | 930,590 | | | | 901,174 | |

| West Corp., Initial B | | 6.63% | | 1M US L + 4.00% | | 10/10/2024 | | | 727,987 | | | | 681,709 | |

| Total IT Services | | | | | | | | | 2,619,022 | | | | 2,538,325 | |

| | | | | | | | | | | | | | | |

| Media - 1.43% (0.94% of Total Investments) |

| MediArena Acquisition B.V., Dollar B | | 8.55% | | 3M US L + 5.75% | | 08/13/2021 | | | 742,894 | | | | 737,790 | |

See Notes to Financial Statements.

| Semi-Annual Report | March 31, 2019 | 13 |

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Schedule of Investments |

March 31, 2019 (Unaudited)

| | | Coupon(a) | | Reference Rate & Spread | | Maturity Date | | Principal Amount | | | Value | |

| SENIOR SECURED FIRST LIEN LOANS(c)(continued) | | | | | | | | | | | | | | |

| Media (continued) |

| Quad/Graphics, Inc., B | | 7.50% | | 1M US L + 5.00% | | 02/02/2026 | | $ | 310,304 | | | $ | 309,916 | |

| Total Media | | | | | | | | | 1,053,198 | | | | 1,047,706 | |

| | | | | | | | | | | | | | | |

| Oil, Gas & Consumable Fuels - 0.57% (0.38% of Total Investments) |

| Permian Production Partners LLC, Initial Advances | | 8.49% | | 1M US L + 6.00% | | 05/20/2024 | | | 438,786 | | | | 421,235 | |

| | | | | | | | | | | | | | | |

| Personal Products - 0.75% (0.50% of Total Investments) |

| Revlon Consumer Products Corp., Initial B | | 6.13% | | 3M US L + 3.50% | | 09/07/2023 | | | 763,258 | | | | 550,820 | |

| | | | | | | | | | | | | | | |

| Pharmaceuticals - 1.46% (0.96% of Total Investments) |

| Endo Pharmaceuticals Holdings, Inc., Initial Term Loan | | 6.75% | | 1M US L + 4.25% | | 04/29/2024 | | | 967,893 | | | | 948,380 | |

| Mallinckrodt International Finance S.A., 2018 Incremental(d) | | N/A | | L + 3.00% | | 02/24/2025 | | | 128,620 | | | | 121,009 | |

| Total Pharmaceuticals | | | | | | | | | 1,096,513 | | | | 1,069,389 | |

| | | | | | | | | | | | | | | |

| Real Estate Management & Development - 0.63% (0.41% of Total Investments) |

| Forest City Enterprises LP, Initial | | 6.48% | | 1M US L + 4.00% | | 12/08/2025 | | | 458,386 | | | | 459,532 | |

| | | | | | | | | | | | | | | |

| Road & Rail - 0.67% (0.44% of Total Investments) |

| YRC Worldwide, Inc., Term B-1 Loan | | 11.24% | | 1M US L + 8.50% | | 07/26/2022 | | | 499,252 | | | | 490,870 | |

| | | | | | | | | | | | | | | |

| Software - 4.42% (2.92% of Total Investments) |

| Blackboard, Inc., B-4 | | 7.78% | | 3M US L + 5.00% | | 06/30/2021 | | | 122,424 | | | | 120,159 | |

| Datto, Inc., Cov-Lite TLB(d) | | N/A | | L + 4.75% | | 04/02/2026 | | | 143,236 | | | | 143,236 | |

| DiscoverOrg LLC, Initial | | 7.24% | | 3M US L + 4.50% | | 02/02/2026 | | | 739,910 | | | | 728,811 | |

| LegalZoom.com, Inc., 2018 | | 6.99% | | 1M US L + 4.50% | | 11/21/2024 | | | 560,575 | | | | 559,875 | |

| McAfee LLC, B USD | | 6.25% | | 1M US L + 3.75% | | 09/30/2024 | | | 838,820 | | | | 837,420 | |

| Project Alpha Intermediate Holding, Inc., B(d) | | N/A | | L + 4.50% | | 04/26/2024 | | | 374,365 | | | | 370,621 | |

| Project Leopard Holdings, Inc., 2018 Repricing | | 7.00% | | 1M US L + 4.50% | | 07/07/2023 | | | 492,516 | | | | 485,438 | |

| Total Software | | | | | | | | | 3,271,846 | | | | 3,245,560 | |

| | | | | | | | | | | | | | | |

| Specialty Retail - 1.76% (1.16% of Total Investments) |

| Bass Pro Group LLC, Initial | | 7.50% | | 1M US L + 5.00% | | 09/25/2024 | | | 762,294 | | | | 743,999 | |

| Payless, Inc. | | | | | | | | | | | | | | |

| Term Loan(d) | | N/A | | L + 8.00% | | 09/30/2019 | | | 146,987 | | | | 144,782 | |

| Tranche A-1 | | 10.78% | | 3M US L + 9.00% | | 02/10/2022 | | | 359,832 | | | | 178,718 | |

| Tranche A-2 | | 11.78% | | 3M US L + 10.00% | | 08/10/2022 | | | 643,500 | | | | 222,007 | |

| Total Specialty Retail | | | | | | | | | 1,912,613 | | | | 1,289,506 | |

| | | | | | | | | | | | | | | |

| Textiles, Apparel & Luxury Goods - 1.78% (1.18% of Total Investments) |

| Champ Acquisition Corp., Initial | | 8.10% | | 3M US L + 5.50% | | 12/19/2025 | | | 549,391 | | | | 549,051 | |

| Elevate Textiles, Inc., Initial | | 7.49% | | 1M US L + 5.00% | | 05/01/2024 | | | 790,900 | | | | 759,264 | |

| Total Textiles, Apparel & Luxury Goods | | | | | | | | | 1,340,291 | | | | 1,308,315 | |

See Notes to Financial Statements.

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Schedule of Investments |

March 31, 2019 (Unaudited)

| | | Coupon(a) | | Reference Rate & Spread | | Maturity Date | | Principal Amount | | | Value | |

| SENIOR SECURED FIRST LIEN LOANS(c)(continued) |

| Wireless Telecommunication Services - 0.72% (0.48% of Total Investments) |

| Digicel International Finance, Ltd., Initial B | | 5.88% | | 3M US L + 3.25% | | 05/27/2024 | | $ | 599,255 | | | $ | 530,718 | |

| | | | | | | | | | | | | | | |

| Total Senior Secured First Lien Loans (Cost $47,262,288) | | | | | | | | $ | 47,885,916 | | | $ | 45,383,384 | |

| | | | | | | | | | | | | | | |

| CLO DEBT(c)(f)- 22.67% (14.98% of Total Investments) |

| Anchorage Capital CLO 2018-10, Ltd., Series 2018-10A(b) | | 8.18% | | 3M US L + 5.75% | | 10/15/2031 | | | 500,000 | | | | 458,574 | |

| Apidos CLO XXVIII, Series 2017-28A(b) | | 8.26% | | 3M US L + 5.50% | | 01/20/2031 | | | 1,000,000 | | | | 929,345 | |

| Atrium XIV LLC, Series 2018-14A(b) | | 8.43% | | 3M US L + 5.65% | | 08/23/2030 | | | 500,000 | | | | 468,752 | |

| CIFC Funding 2015-I, Ltd., Series 2015-1A(b) | | 8.76% | | 3M US L + 6.00% | | 01/22/2031 | | | 500,000 | | | | 477,037 | |

| CIFC Funding 2017-II, Ltd., Series 2017-2A(b) | | 8.71% | | 3M US L + 5.95% | | 04/20/2030 | | | 500,000 | | | | 478,807 | |

| CIFC Funding 2017-V, Ltd., Series 2017-5A(b) | | 8.87% | | 3M US L + 6.10% | | 11/16/2030 | | | 1,000,000 | | | | 970,411 | |

| Dryden 64 CLO, Ltd., Series 2018-64A(b) | | 8.38% | | 3M US L + 5.60% | | 04/18/2031 | | | 500,000 | | | | 461,965 | |

| GoldenTree Loan Management US CLO 1, Ltd., Series 2017-1A(b) | | 8.36% | | 3M US L + 5.60% | | 04/20/2029 | | | 1,000,000 | | | | 853,243 | |

| GoldenTree Loan Opportunities XI, Ltd., Series 2015-11A(b) | | 8.18% | | 3M US L + 5.40% | | 01/18/2031 | | | 750,000 | | | | 679,165 | |

| Halcyon Loan Advisors Funding 2018-2, Ltd., Series 2018-2A(b) | | 9.75% | | 3M US L + 6.90% | | 01/22/2031 | | | 500,000 | | | | 501,848 | |

| HPS Loan Management 11-2017, Ltd., Series 2017-11A(b) | | 10.58% | | 3M US L + 7.85% | | 05/06/2030 | | | 1,000,000 | | | | 911,394 | |

| Madison Park Funding XVII, Ltd., Series 2015-17A(b) | | 10.24% | | 3M US L + 7.48% | | 07/21/2030 | | | 1,000,000 | | | | 893,726 | |

| Marble Point CLO XI, Ltd., Series 2017-2A E(b) | | 8.38% | | 3M US L + 5.60% | | 12/18/2030 | | | 1,000,000 | | | | 907,841 | |

| Neuberger Berman CLO XIV, Ltd., Series 2013-14A(b) | | 9.21% | | 3M US L + 6.45% | | 01/28/2030 | | | 1,000,000 | | | | 962,956 | |

| OZLM Funding, Ltd., Series 2012-1A(b) | | 9.43% | | 3M US L + 6.67% | | 07/23/2029 | | | 1,000,000 | | | | 991,428 | |

| OZLM XXII, Ltd., Series 2018-22A(b) | | 8.07% | | 3M US L + 5.30% | | 01/17/2031 | | | 500,000 | | | | 451,216 | |

| Sound Point CLO II, Ltd., Series 2013-1A(b) | | 8.26% | | 3M US L + 5.50% | | 01/26/2031 | | | 250,000 | | | | 233,293 | |

| Sound Point CLO XVIII, Ltd., Series 2017-4A(b) | | 8.26% | | 3M US L + 5.50% | | 01/20/2031 | | | 500,000 | | | | 466,030 | |

| Symphony CLO XVIII, Ltd., Series 2016-18A(b) | | 9.12% | | 3M US L + 6.35% | | 01/23/2028 | | | 1,500,000 | | | | 1,458,071 | |

| THL Credit Wind River 2017-4 CLO, Ltd., Series 2017-4A(b) | | 8.44% | | 3M US L + 5.80% | | 11/20/2030 | | | 500,000 | | | | 469,548 | |

| THL Credit Wind River 2019-1 CLO, Ltd., Series 2019-1A(b) | | N/A | | 3M US L + 6.72% | | 04/20/2031 | | | 750,000 | | | | 738,750 | |

| Voya CLO 2013-1, Ltd., Series 2013-1A(b) | | 9.27% | | 3M US L + 6.48% | | 10/15/2030 | | | 1,000,000 | | | | 965,247 | |

| Voya CLO 2013-2, Ltd., Series 2013-2A(b) | | 8.37% | | 3M US L + 5.60% | | 04/25/2031 | | | 1,000,000 | | | | 915,317 | |

| Total CLO Debt (Cost $17,614,014) | | | | | | | | $ | 17,750,000 | | | $ | 16,643,964 | |

| | | | | | | | | | | | | | | |

| CLO EQUITY(f)(g)- 50.47% (33.36% of Total Investments) |

| ALM V, Ltd., Series 2012-5A(b) | | N/A | | Estimated yield of 11.79% | | 10/18/2027 | | | 2,000,000 | | | | 822,568 | |

| Anchorage Capital CLO 1-R, Ltd., Series 2018-1RA(b) | | N/A | | Estimated yield of 11.53% | | 04/13/2031 | | | 2,000,000 | | | | 1,627,442 | |

| Anchorage Capital CLO 3-R, Ltd., Series 2014-3RA(b) | | N/A | | Estimated yield of 13.41% | | 01/28/2031 | | | 1,400,000 | | | | 1,141,749 | |

| Apidos CLO XXI, Series 2015-21A(b) | | N/A | | Estimated yield of 17.77% | | 07/18/2027 | | | 750,000 | | | | 448,538 | |

| Apidos CLO XXVIII, Series 2017-28A(b) | | N/A | | Estimated yield of 10.68% | | 01/20/2031 | | | 3,500,000 | | | | 2,876,223 | |

| Ares XLIX CLO, Ltd., Series 2018-49A(b) | | N/A | | Estimated yield of 12.79% | | 07/22/2030 | | | 2,000,000 | | | | 1,650,000 | |

| Ares XLVII CLO, Ltd., Series 2018-47A(b) | | N/A | | Estimated yield of 11.57% | | 04/16/2030 | | | 2,000,000 | | | | 1,650,540 | |

| Carlyle Global Market Strategies CLO 2013-1, Ltd., Series 2013-1A(b) | | N/A | | Estimated yield of 19.99% | | 08/14/2030 | | | 3,500,000 | | | | 2,262,935 | |

| Carlyle Global Market Strategies CLO 2016-1, Ltd., Series 2016-1A(b) | | N/A | | Estimated yield of 14.82% | | 04/20/2027 | | | 598,000 | | | | 520,261 | |

| Carlyle US CLO 2018-2, Ltd., Series 2018-2A(b) | | N/A | | Estimated yield of 11.83% | | 10/15/2031 | | | 933,000 | | | | 766,489 | |

| Catamaran CLO 2015-1, Ltd., Series 2015-1A(b) | | N/A | | Estimated yield of 27.49% | | 04/22/2027 | | | 750,000 | | | | 349,692 | |

| CIFC Funding 2017-III, Ltd., Series 2017-3A(b) | | N/A | | Estimated yield of 17.10% | | 07/30/2030 | | | 750,000 | | | | 611,514 | |

| CIFC Funding 2017-V, Ltd., Series 2017-5A(b) | | N/A | | Estimated yield of 13.32% | | 11/16/2030 | | | 3,000,000 | | | | 2,457,279 | |

See Notes to Financial Statements.

| Semi-Annual Report | March 31, 2019 | 15 |

| XAI Octagon Floating Rate & | |

| Alternative Income Term Trust | Schedule of Investments |

March 31, 2019 (Unaudited)

| | | Coupon(a) | | Reference Rate & Spread | | Maturity Date | | Principal Amount | | | Value | |

| CLO EQUITY(f)(g) (continued) |

| CIFC Funding 2018-I, Ltd., Series 2018-1A(b) | | N/A | | Estimated yield of 15.24% | | 04/18/2031 | | $ | 3,250,000 | | | $ | 3,093,512 | |

| Dryden 34 Senior Loan Fund, Series 2014-34A(b) | | N/A | | Estimated yield of 0.00% | | 10/15/2026 | | | 5,000,000 | | | | 65,750 | |

| Madison Park Funding XVIII, Ltd., Series 2015-18A(b) | | N/A | | Estimated yield of 9.61% | | 10/21/2027 | | | 4,000,000 | | | | 3,188,440 | |

| Marble Point CLO XI, Ltd., Series 2017-2A INC(b) | | N/A | | Estimated yield of 14.75% | | 12/18/2030 | | | 3,000,000 | | | | 2,182,500 | |

| OZLM XIX, Ltd., Series 2017-19A(b) | | N/A | | Estimated yield of 12.35% | | 11/22/2030 | | | 3,500,000 | | | | 2,611,907 | |

| OZLM XVI, Ltd., Series 2017-16A(b) | | N/A | | Estimated yield of 10.52% | | 05/16/2030 | | | 1,250,000 | | | | 811,661 | |

| Sound Point CLO III, Ltd., Series 2017-3A(b) | | N/A | | Estimated yield of 17.61% | | 10/20/2030 | | | 1,500,000 | | | | 1,389,933 | |

| Sound Point CLO III-R, Ltd., Series 2013-2RA(b) | | N/A | | Estimated yield of 18.13% | | 04/15/2029 | | | 1,000,000 | | | | 445,964 | |

| Thacher Park CLO, Ltd., Series 2014-1A(b) | | N/A | | Estimated yield of 12.79% | | 10/20/2026 | | | 6,000,000 | | | | 2,042,640 | |

| THL Credit Wind River 2016-1 CLO, Ltd., Series 2016-1A(b) | | N/A | | Estimated yield of 18.76% | | 07/15/2028 | | | 4,000,000 | | | | 2,773,288 | |

| Voya CLO 2017-4, Ltd., Series 2017-4A(b) | | N/A | | Estimated yield of 12.48% | | 10/15/2030 | | | 1,500,000 | | | | 1,267,292 | |

| Total CLO Equity (Cost $41,292,446) | | | | | | | | $ | 57,181,000 | | | $ | 37,058,117 | |

| | | | | | | | | | | | | | | |

| | | Shares | | | | | |

| MONEY MARKET MUTUAL FUNDS - 2.78%(1.84% of Total Investments) | | | | | | | | |

| Invesco Short Term Investments Trust Treasury Portfolio, Institutional Class (2.299% 7-Day Yield) | | | 2,043,080 | | | | 2,043,080 | |

| Total Money Market Mutual Funds (Cost $2,043,080) | | $ | 2,043,080 | | | $ | 2,043,080 | |

| | | | | | | | | |

| Total Investments - 151.28% (Cost $$118,695,630) | | | | | | $ | 111,080,995 | |

| Liabilities in Excess of Other Assets - (2.24)% | | | | | | | (1,649,149 | ) |

| Leverage Facility (Net of 59,107 Deferred Costs) - (49.04)% | | | | | | | (36,005,893 | ) |

| Net Assets - 100.00% | | | | | | $ | 73,425,953 | |

| * | Amounts above are shown as a percentage of net assets as of March 31, 2019. |

| (a) | The rate shown is the coupon as of the end of the reporting period. |

| (b) | Security exempt from registration under Rule 144A of the Securities Act of 1933. Total market value of Rule 144A securities amounts to $54,929,177, which represents approximately 74.81% of net assets as of March 31, 2019. Such securities may normally be sold to qualified institutional buyers in transactions exempt from registration. |

| (c) | Variable rate investment. Interest rates reset periodically. Interest rate shown reflects the rate in effect at March 31, 2019. For securities based on a published reference rate and spread, the reference rate and spread are indicated in the description above. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |