UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number | | 811-23262 |

Nuveen Emerging Markets Debt 2022 Target Term Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Gifford R. Zimmerman

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: December 31

Date of reporting period: December 31, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Closed-End Funds

31 December

2018

Nuveen Closed-End Funds

| | |

| JEMD | | Nuveen Emerging Markets Debt 2022 Target Term Fund |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website (www.nuveen.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you have already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically anytime by contacting the financial intermediary (such as a broker-dealer or bank) through which you hold your Fund shares or, if you are a direct investor, by enrolling at www.nuveen.com/e-reports.

You may elect to receive all future shareholder reports in paper free of charge at any time by contacting your financial intermediary or, if you are a direct investor, (i) by calling 800-257-8787 and selecting option #2 or (ii) by logging into your Investor Center account at www.computershare.com/investor and clicking on “Communication Preferences.” Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary or, if you are a direct investor, to all your directly held Nuveen Funds and any other directly held funds within the same group of related investment companies.

Annual Report

Life is Complex.

Nuveen makes things e-simple.

It only takes a minute to sign up fore-Reports. Once enrolled, you’ll receive ane-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within thee-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your email!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

Table of Contents

3

Chairman’s Letter to Shareholders

Dear Shareholders,

The global economy seemed to reach a turning point in 2018. Growth was peaking in the U.S. and slowing elsewhere. Deregulation and tax law changes, which lowered corporate and individual tax rates and encouraged companies to repatriate overseas profits, helped boost U.S. economic growth and amplify corporate earnings during 2018. Meanwhile, a weakening housing market and a flattening yield curve in the U.S. and disappointing economic growth across Europe, China and Japan signaled caution. As the year developed, future corporate profit growth was looking less certain than at the start of the year. Adding to the uncertainty were the removal of U.S. central bank monetary stimulus, rising interest rates, a stronger U.S. dollar, trade negotiations and unpredictable politics, including Brexit and a prolonged U.S. government shutdown. Bearish sentiment intensified at the end of 2018, pressuring stocks, corporate bonds and commodities alike.

Although downside risks have been rising, the likelihood of a near-term recession remains low. Global growth is indeed slowing, but it’s still positive. The U.S. economy remains strong, even in the face of late-cycle pressures. Low unemployment and firming wages should continue to support consumer spending, and the Novembermid-term elections resulted in change, but no major surprises. In China, the government remains committed to using fiscal stimulus to offset softening exports. Europe also remains vulnerable to trade policy as well as Brexit uncertainty, but underlying strengths in European economies, including low unemployment that drives domestic demand, remain supportive of a mild expansion. In a slower growth environment, there are opportunities for investors who seek them more selectively.

We expect volatility and challenging conditions to persist in 2019 but also think there is potential for upside. You can prepare your investment portfolio by working with your financial advisor to review your goals, timeline and risk tolerance. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Terence J. Toth

Chairman of the Board

February 22, 2018

4

Portfolio Managers’ Comments

Nuveen Emerging Markets Debt 2022 Target Term Fund (JEMD)

The Fund features portfolio management by Teachers Advisors, LLC, an affiliate of Nuveen Fund Advisors, LLC. Portfolio managers Anupam Damani, CFA, and Katherine Renfrew discuss U.S. economic and global market conditions, key investment strategies and the twelve-month performance of JEMD. Anupam and Katherine have managed the Fund since its inception.

What factors affected the U.S. economy and global markets during the twelve-month reporting period ended December 31, 2018?

The U.S. economy accelerated in this reporting period, with gross domestic product (GDP) growth reaching 4.2% (annualized) in the second quarter of 2018, the fastest pace since 2014, then receding to a still relatively robust 3.4% annualized rate in the third quarter of 2018, according to the Bureau of Economic Analysis “third” estimate. GDP is the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. The boost in economic activity during the second quarter of 2018 was attributed to robust spending by consumers, businesses and the government, as well as a temporary increase in exports, as farmers rushed soybean shipments ahead of China’s retaliatory tariffs. While consumer and government spending continued to drive economic growth in the third quarter, the export contribution declined as expected and both business spending and housing investment weakened. The government’s fourth quarter 2018 GDP growth estimate was not yet available due to the partial government shutdown from late December 2018 to late January 2019.

Consumer spending, the largest driver of the economy, remained well supported by low unemployment, wage gains and tax cuts. As reported by the Bureau of Labor Statistics, the unemployment rate fell to 3.9% in December 2018 from 4.1% in December 2017 and job gains averaged around 219,000 per month for the past twelve months. The jobs market has continued to tighten, while average hourly earnings grew at an annualized rate of 3.2% in December 2018. The Consumer Price Index (CPI) increased 1.9% over the twelve-month reporting period ended December 31, 2018 on a seasonally adjusted basis, as reported by the Bureau of Labor Statistics.

Low mortgage rates and low inventory drove home prices higher during this recovery cycle. But the price momentum slowed in recent months as mortgage rates began to drift higher and homes have become less affordable. The S&P CoreLogic Case-Shiller U.S. National Home Price Index, which covers all nine U.S. census divisions, was up 5.2% year-over-year in November 2018 (most recent data available at the time this report was prepared). The10-City and20-City Composites reported year-over-year increases of 4.3% and 4.7%, respectively.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Fund disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

5

Portfolio Managers’ Comments(continued)

With the U.S. economy delivering a sustainable growth rate and employment strengthening, the Federal Reserve’s (Fed) policy making committee continued to incrementally raise its main benchmark interest rate. The most recent increase, in December 2018, was the fourth rate hike in 2018 and the ninth rate hike since December 2015. Fed Chair Janet Yellen’s term expired in February 2018, and the new Chairman Jerome Powell maintained the Fed’s gradual pace of interest rate hikes. However, amid signs that economic growth might have peaked, the markets’ unease about the future pace of monetary tightening, along with other factors, drove sharp volatility in the final months of 2018. Additionally, the Fed continued reducing its balance sheet by allowing a small amount of maturing Treasury and mortgage securities to roll off each month without reinvestment.

During the twelve-month reporting period, geopolitical news remained a prominent market driver. The U.S. moved forward with tariffs on imported goods from China, as well as on steel and aluminum from Canada, Mexico and Europe. These countries announced retaliatory measures in kind, intensifying concerns about a trade war, although there have been some positive developments. In July 2018, the U.S. and the European Union announced they would refrain from further tariffs while they negotiate trade terms, and in October 2018, the U.S., Mexico and Canada agreed to a new trade deal to replace the North American Free Trade Agreement. At the November 2018G-20 summit, the U.S. and China agreed to a90-day trade truce, although the details were murky. Brexit negotiations continued to be uncertain and Prime Minister Theresa May faced significant difficulty getting a plan approved in Parliament. Elsewhere in Europe, markets remained nervous about Italy’s new euroskeptic coalition government, immigration policy and political risk in Turkey. The U.S. Treasury issued additional sanctions on Russia in April 2018 andre-imposed sanctions on Iran following the U.S. withdrawal from the 2015 nuclear agreement. Bearish crude oil supply news, along with heightened tensions between the U.S. and Saudi Arabia after the disappearance of a Saudi journalist, drove oil price volatility. On the Korean peninsula, the leaders of South Korea and North Korea met during April 2018 and jointly announced a commitment toward peace, while the U.S.-North Korea summit yielded an agreement with few additional details. In the final week of the reporting period, the U.S. government began a prolonged partial shutdown due to an impasse on border security funding (which ended in late January, subsequent to the close of the reporting period, when a temporary funding measure was passed).

During the first half of 2018, emerging markets came into the crosshairs of volatility arising from higher U.S. interest rates, a stronger U.S. dollar, trade tensions and home-grown problems in some countries. As a result, asset class returns suffered as spreads widened. However, as the second half of 2018 progressed, the pressure of many of these macro-driven catalysts ebbed. For example, dollar strength appeared to peak, trade tensions between China and the U.S. cooled modestly and many of the idiosyncratic country-specific issues (i.e., Turkey and Argentina) mitigated. As a result, some of the losses from earlier in the year were retraced, although the asset class still had a negative total return for the year. From a credit ratings perspective, investment grade debt outperformed high yield debt for the reporting period overall.

What strategies were used to manage the Fund during the twelve-month reporting period ended December 31, 2018?

The Fund seeks to provide a high level of current income and return the original $9.85 net asset value (NAV) per common share on or about December 1, 2022.

JEMD seeks to provide high current income from a portfolio of shorter maturity, emerging market sovereign, quasi-sovereign and corporate debt securities, including high yield securities. The Fund invests at least 80% of its managed assets in emerging market debt securities and may invest without limit in investment grade securities and securities rated below investment grade (BB+/Ba1 or lower). However, the Fund invests no more than 10% of its managed assets in securities rated belowB-/B3 or that are unrated but judged by the managers to be of comparable quality. The Fund invests 100% of its managed assets in U.S. dollar denominated securities. No more than 25% is invested in securities of issuers located in a single country.

6

In seeking to return the original NAV on or about December 1, 2022, the Fund intends to utilize various portfolio and cash flow management techniques, including setting aside a portion of its net investment income, possibly retaining gains and limiting the longest effective maturity on any holding to no later than June 1, 2023. This Fund uses leverage. Leverage is discussed in more detail later in the Fund Leverage Section of this report.

How did the Fund perform during the twelve-month reporting period ended December 31, 2018?

The table in the Performance Overview and Holding Summaries section of this report provides total return performance for the Fund for theone-year reporting and since inception periods ended December 31, 2018. The Fund’s total returns at net asset value (NAV) are compared with the performance of a corresponding market index. For the twelve-month reporting period ended December 31, 2018, the Fund underperformed the JP Morgan EMBI Global Diversified Index.

The Fund lagged the benchmark as the bulk of the securities the Fund holds are high yield in nature (with an average portfolio rating of B+), which hurt the Fund as the high yield segment underperformed in this reporting period. However, the Fund’s shorter duration posture (due to its shorter maturity mandate) versus the benchmark helped alleviate a portion of the deficit as longer-dated credits underperformed.

At a country level, the largest detractors were Barbados, Argentina, Zambia and Turkey. Barbados sovereign debt was the single biggest cause for underperformance due to the newly elected government announcing it will suspend payments on external debt while it negotiated with the International Monetary Fund on a program and concluded wider restructuring. Argentina sovereign paper and Turkish bank paper also contributed negatively due to challenging economic, political and policy environments. The largest detractor on the corporate debt side was Digicel, a pan-Caribbean telecom, where holding company debt prices suffered as investors became increasingly concerned over an upcoming maturity. Other country-level detractors included Ukraine, Ecuador and Lebanon. On the positive side, our African selections (outside of Zambia) performed well, including Ghana (both sovereign and corporate), Rwanda and Nigeria (both sovereign and banks).

7

Fund Leverage

IMPACT OF THE FUND’S LEVERAGE STRATEGIES ON PERFORMANCE

One important factor impacting the returns of the Fund’s common shares relative to its comparative benchmark was the Fund’s use of leverage through the use of reverse repurchase agreements. The Fund uses leverage because our research has shown that, over time, leveraging provides opportunities for additional income and total return, particularly in the recent market environment where short-term market rates are at or near historical lows, meaning that the short-term rates the Fund has been paying on its leveraging instruments in recent years have been much lower than the interest the Fund has been earning on its portfolio securities that it has bought with the proceeds of that leverage.

However, use of leverage can expose Fund common shares to additional price volatility. When the Fund uses leverage, the Fund common shares will experience a greater increase in their net asset value if the securities acquired through the use of leverage increase in value, but will also experience a correspondingly larger decline in their net asset value if the securities acquired through leverage decline in value, which will make the shares’ net asset value more volatile, and total return performance more variable, over time.

In addition, common share income in levered funds will typically decrease in comparison to unlevered funds when short-term interest rates increase and increase when short-term interest rates decrease. Over the last few quarters, short-term interest rates have indeed increased from their extended lows after the 2007-09 financial crisis. This increase has reduced common share net income, and also reduced potential for long-term total returns. Nevertheless, the ability to effectively borrow at current short-term rates is still resulting in enhanced common share income, and management believes that the advantages of continuation of leverage outweigh the associated increase in risk and volatility described above.

The Fund’s use of leverage had a negative impact on total return performance during this reporting period.

As of December 31, 2018, the Fund’s percentages of leverage are as shown in the accompanying table.

| | | | |

| | | JEMD | |

Effective Leverage* | | | 28.00 | % |

Regulatory Leverage* | | | 0.00 | % |

| * | Effective leverage is the Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative and other investments in the Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of borrowings of the Fund, which is part of the Fund’s capital structure. The Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of the Fund’s effective leverage ratio. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

THE FUND’S LEVERAGE

Reverse Repurchase Agreements

As noted above, the Fund utilized reverse repurchase agreements. The Fund’s transactions in reverse repurchase agreements are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

| January 1, 2018 | | | Purchases | | | Sales | | | December 31, 2018 | | | Average Balance

Outstanding | | | | | | Purchases | | | Sales | | | February 28, 2019 | |

| | $47,000,000 | | | $ | — | | | $ | — | | | $ | 47,000,000 | | | $ | 47,000,000 | | | | | | | $ | — | | | $ | — | | | $ | 47,000,000 | |

Refer to Notes to Financial Statements, Note 8 – Fund Leverage for further details.

8

Common Share Information

DISTRIBUTION INFORMATION

The following information regarding the Fund’s distributions is current as of December 31, 2018. The Fund’s distribution levels may vary over time based on the Fund’s investment activity and portfolio investment value changes.

During the current reporting period, the Fund’s distributions to shareholders were as shown in the accompanying table.

| | | | |

| Monthly Distributions(Ex-Dividend Date) | | Per

Share

Amounts | |

January 2018 | | $ | 0.0435 | |

February | | | 0.0435 | |

March | | | 0.0435 | |

April | | | 0.0435 | |

May | | | 0.0435 | |

June | | | 0.0435 | |

July | | | 0.0435 | |

August | | | 0.0435 | |

September | | | 0.0435 | |

October | | | 0.0435 | |

November | | | 0.0375 | |

December 2018 | | | 0.0375 | |

Total Distributions | | $ | 0.5100 | |

| |

Current Distribution Rate* | | | 5.90 | % |

| * | Current distribution rate is based on the Fund’s current annualized monthly distribution divided by the Fund’s current market price. The Fund’s monthly distributions to its shareholders may be comprised of ordinary income, net realized capital gains and, if at the end of the fiscal year the Fund’s cumulative net ordinary income and net realized gains are less than the amount of the Fund’s distributions, a return of capital for tax purposes. |

The Fund seeks to pay regular monthly dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit the Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net income actually earned by the Fund during the period. Distributions to shareholders are determined on a tax basis, which may differ from amounts recorded in the accounting records. In instances where the monthly dividend exceeds the earned net investment income, the Fund would report a negative undistributed net ordinary income. Refer to Note 6 – Income Tax Information for additional information regarding the amounts of undistributed net ordinary income and undistributed net long-term capital gains and the character of the actual distributions paid by the Fund during the period.

All monthly dividends paid by the Fund during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions is sourced or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders will be notified of those sources. For financial reporting purposes, the per share amounts of the Fund’s distributions for the reporting period are presented in this report’s Financial Highlights. For income tax purposes, distribution information for the Fund as of its most recent tax year end is presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

COMMON SHARE REPURCHASES

During August 2018, the Fund’s Board of Trustees authorized the Fund to participate in Nuveen’s closed-end fund complex-wide share repurchase program, allowing the Fund to repurchase an aggregate of up to approximately 10% of its outstanding shares.

9

Common Share Information(continued)

As of December 31, 2018, and since the inception of the Fund’s repurchase program, the Fund has cumulatively repurchased and retired its outstanding common shares as shown in the accompanying table.

| | | | |

| | | JEMD | |

Common shares cumulatively repurchased and retired | | | — | |

Common shares authorized for repurchase | | | 1,425,000 | |

OTHER SHARE INFORMATION

As of December 31, 2018, and during the current reporting period, the Fund’s common share price was trading at a premium/(discount) to its NAV as shown in the accompanying table.

| | | | |

Common share NAV | | $ | 8.49 | |

Common share price | | $ | 7.63 | |

Premium/(Discount) to NAV | | | (10.13 | )% |

12-month average premium/(discount) to NAV | | | (5.58 | )% |

The Fund has an investment objective to return $9.85 (the original net asset value following the Fund’s initial public offering (the “Original NAV”)) to shareholders on or about the end of the Fund’s term. There can be no assurance that the Fund will be able to return the Original NAV to shareholders, and such return is not backed or otherwise guaranteed by the Fund’s investment adviser, Nuveen Fund Advisors, LLC (the “Adviser”), or any other entity.

The Fund’s ability to return Original NAV to shareholders on or about its termination date will depend on market conditions and the success of various portfolio and cash flow management techniques. The Fund currently intends to set aside and retain in its net assets a portion of its net investment income and possibly all or a portion of its gains. This will reduce the amounts otherwise available for distribution prior to the liquidation of the Fund, and the Fund may incur taxes on such retained amount, which will reduce the overall amounts that the Fund would have otherwise been able to distribute. Such retained income or gains, net of any taxes, would constitute a portion of the liquidating distribution returned to investors at the end of the Fund’s term. In addition, the Fund’s investment in shorter term and lower yielding securities, especially as the Fund nears the end of its term, may reduce investment income and, therefore, the monthly dividends during the period prior to termination. Investors that purchase shares in the secondary market (particularly if their purchase price differs meaningfully from the Original NAV) may receive more or less than their original investment.

10

Risk Considerations

Fund shares are not guaranteed or endorsed by any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation.

Nuveen Emerging Markets Debt 2022 Target Term Fund (JEMD)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value.Emerging markets, particularly including frontier markets,involve additional risks, including smaller capitalization, illiquidity, price volatility, political and economic instability that could lead to diminished security values, and different legal and accounting standards.Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, derivatives risk, liquidity risk, and income risk. As interest rates rise, bond prices fall.Lower creditdebt securities may be more likely to fail to make timely interest or principal payments.Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. These and other risk considerations such aslimited term riskare described in more detail on the Fund’s web page atwww.nuveen.com/JEMD.

11

| | |

| JEMD | | Nuveen Emerging Markets Debt 2022 Target Term Fund Performance Overview and Holding Summaries as of December 31, 2018 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of December 31, 2018

| | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | Since

Inception | |

| JEMD at Common Share NAV | | | (8.71)% | | | | (6.39)% | |

| JEMD at Common Share Price | | | (13.85)% | | | | (14.78)% | |

| JP Morgan EMBI Global Diversified Index | | | (4.26)% | | | | (2.55)% | |

Since inception returns are from 9/26/17. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

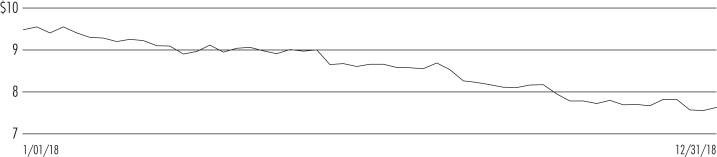

Common Share Price Performance —Weekly Closing Price

12

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Emerging Markets Debt | | | 73.6% | |

| Corporate Bonds | | | 61.5% | |

| U.S. Government and Agency Obligations | | | 1.4% | |

| Other Assets Less Liabilities | | | 2.4% | |

Net Assets Plus Reverse Repurchase Agreements | | | 138.9% | |

| Reverse Repurchase Agreements | | | (38.9)% | |

Net Assets | | | 100% | |

Portfolio Credit Quality

(% of total investments)

| | | | |

| BBB | | | 1.9% | |

| BB or Lower | | | 97.1% | |

| N/R | | | 1.0% | |

Total | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Emerging Markets Debt | | | 54.0% | |

| Banks | | | 17.4% | |

| Oil, Gas & Consumable Fuels | | | 4.9% | |

| Metals & Mining | | | 3.9% | |

| Electric Utilities | | | 2.9% | |

| Real Estate Management & Development | | | 2.8% | |

| Other | | | 13.1% | |

| U.S. Government and Agency Obligations | | | 1.0% | |

Total | | | 100% | |

Top Five Issuers

(% of total investments)

| | | | |

| Republic of Rwanda | | | 5.0% | |

| Republic of Lebanon | | | 4.6% | |

| Republic of Ecuador | | | 4.5% | |

| Republic of Iraq | | | 4.3% | |

| Republic of Ukraine | | | 4.2% | |

Country Allocation¹

(% of total investments)

| | | | |

Ukraine | | | 8.4% | |

| Turkey | | | 7.6% | |

| South Africa | | | 6.6% | |

| Rwanda | | | 5.0% | |

| Nigeria | | | 4.8% | |

| Lebanon | | | 4.6% | |

| Ecuador | | | 4.5% | |

| Iraq | | | 4.3% | |

| El Salvador | | | 4.0% | |

| Argentina | | | 3.7% | |

| Ghana | | | 3.7% | |

| Egypt | | | 3.4% | |

| Zambia | | | 3.3% | |

| United States | | | 3.2% | |

| Barbados | | | 2.9% | |

| China | | | 2.8% | |

| Mongolia | | | 2.7% | |

| Russia | | | 2.6% | |

| Kazakhstan | | | 2.3% | |

| Other | | | 19.6% | |

Total | | | 100% | |

| 1 | Includes 95.6% (as a percentage of total investments) in emerging markets countries. |

13

Report of Independent Registered

Public Accounting Firm

To the Shareholders and Board of Trustees of

Nuveen Emerging Markets Debt 2022 Target Term Fund:

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of Nuveen Emerging Markets Debt 2022 Target Term Fund (the “Fund”) as of December 31, 2018, the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for the year then ended and the period from September 26, 2017 (commencement of operations) to December 31, 2017, and the related notes (collectively, the “financial statements”) and the financial highlights for the year then ended and the period from September 26, 2017 to December 31, 2017. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Fund as of December 31, 2018, the results of its operations and its cash flows for the year then ended, and the changes in its net assets and the financial highlights for the year then ended and the period from September 26, 2017 to December 31, 2017, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Such procedures also included confirmation of securities owned as of December 31, 2018, by correspondence with the custodian and brokers or other appropriate auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. We believe that our audits provide a reasonable basis for our opinion.

/s/ KPMG LLP

We have served as the auditor of one or more Nuveen investment companies since 2014.

Chicago, Illinois

February 28, 2019

14

| | |

| JEMD | | Nuveen Emerging Markets Debt

2022 Target Term Fund Portfolio of Investments December 31, 2018 |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | LONG-TERM INVESTMENTS – 135.1% (99.0% of Total Investments) | | | | | |

| | |

| | | | EMERGING MARKETS DEBT – 73.6% (54.0% of Total Investments) | | | | |

| | | | | |

| | | | Argentina – 5.0% | | | | | | | | | | | | |

| | | | | |

| $ | 7,575 | | | Province of Buenos Aires, 144A | | | 6.500% | | | | 2/15/23 | | | | B | | | $ | 6,097,875 | |

| | | | | |

| | | | Bahrain – 1.4% | | | | | | | | | | | | |

| | | | | |

| | 1,675 | | | Kingdom of Bahrain, 144A, (3) | | | 6.125% | | | | 7/05/22 | | | | BB– | | | | 1,706,825 | |

| | | | | |

| | | | Barbados – 3.9% | | | | | | | | | | | | |

| | | | | |

| | 650 | | | Barbados Government, 144A | | | 7.250% | | | | 12/15/21 | | | | Caa3 | | | | 356,687 | |

| | 7,500 | | | Barbados Government, 144A | | | 7.000% | | | | 8/04/22 | | | | D | | | | 4,115,625 | |

| | 517 | | | Barbados Government, Reg S | | | 7.000% | | | | 8/04/22 | | | | D | | | | 283,704 | |

| | 8,667 | | | Total Barbados | | | | | | | | | | | | | | | 4,756,016 | |

| | | | | |

| | | | Belarus – 0.6% | | | | | | | | | | | | |

| | | | | |

| | 750 | | | Republic of Belarus, 144A | | | 6.875% | | | | 2/28/23 | | | | B | | | | 764,055 | |

| | | | | |

| | | | Costa Rica – 1.8% | | | | | | | | | | | | |

| | | | | |

| | 2,400 | | | Republic of Costa Rica, 144A, (3) | | | 4.250% | | | | 1/26/23 | | | | BB | | | | 2,112,000 | |

| | | | | |

| | | | Dominican Republic – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 600 | | | Dominican Republic, 144A, (3) | | | 7.500% | | | | 5/06/21 | | | | BB– | | | | 619,500 | |

| | | | | |

| | | | Ecuador – 6.1% | | | | | | | | | | | | |

| | | | | |

| | 7,350 | | | Republic of Ecuador, 144A | | | 10.750% | | | | 3/28/22 | | | | B– | | | | 7,414,312 | |

| | | | | |

| | | | Egypt – 4.7% | | | | | | | | | | | | |

| | | | | |

| | 5,775 | | | Arab Republic of Egypt, 144A, (3) | | | 6.125% | | | | 1/31/22 | | | | B | | | | 5,665,737 | |

| | | | | |

| | | | El Salvador – 5.4% | | | | | | | | | | | | |

| | | | | |

| | 6,375 | | | Republic of El Salvador, 144A, (3) | | | 7.750% | | | | 1/24/23 | | | | B– | | | | 6,558,281 | |

| | | | | |

| | | | Ghana – 3.4% | | | | | | | | | | | | |

| | | | | |

| | 3,750 | | | Republic of Ghana, 144A, (3) | | | 9.250% | | | | 9/15/22 | | | | B | | | | 4,128,975 | |

| | | | | |

| | | | Honduras – 0.9% | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Honduras Government, 144A | | | 8.750% | | | | 12/16/20 | | | | BB– | | | | 1,062,250 | |

| | | | | |

| | | | Iraq – 5.9% | | | | | | | | | | | | |

| | | | | |

| | 7,500 | | | Republic of Iraq, 144A, (3) | | | 6.752% | | | | 3/09/23 | | | | B– | | | | 7,123,740 | |

| | | | | |

| | | | Lebanon – 6.3% | | | | | | | | | | | | |

| | | | | |

| | 5,000 | | | Republic of Lebanon, Reg S | | | 6.000% | | | | 1/27/23 | | | | B– | | | | 4,222,800 | |

| | 4,000 | | | Republic of Lebanon | | | 6.400% | | | | 5/26/23 | | | | B– | | | | 3,385,680 | |

| | 9,000 | | | Total Lebanon | | | | | | | | | | | | | | | 7,608,480 | |

| | | | | |

| | | | Mongolia – 3.6% | | | | | | | | | | | | |

| | | | | |

| | 3,000 | | | Mongolia Government International Bond, 144A, (3) | | | 5.125% | | | | 12/05/22 | | | | B | | | | 2,813,007 | |

| | 1,650 | | | Mongolia Government International Bond, 144A | | | 5.625% | | | | 5/01/23 | | | | B | | | | 1,559,336 | |

| | 4,650 | | | Total Mongolia | | | | | | | | | | | | | | | 4,372,343 | |

| | | | | |

| | | | Nigeria – 1.2% | | | | | | | | | | | | |

| | | | | |

| | 1,500 | | | Nigerian Government International Bond, (3) | | | 5.625% | | | | 6/27/22 | | | | B+ | | | | 1,451,580 | |

| | | | | |

| | | | Pakistan – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Third Pakistan International Sukuk Co Ltd., 144A | | | 5.625% | | | | 12/05/22 | | | | B | | | | 944,522 | |

15

| | |

| |

| JEMD | | Nuveen Emerging Markets Debt 2022 Target Term Fund(continued) |

| | Portfolio of Investments December 31, 2018 |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Paraguay – 0.4% | | | | | | | | | | | | |

| | | | | |

| $ | 500 | | | Republic of Paraguay, 144A, (3) | | | 4.625% | | | | 1/25/23 | | | | Ba1 | | | $ | 500,750 | |

| | | | | |

| | | | Rwanda – 6.9% | | | | | | | | | | | | |

| | | | | |

| | 8,400 | | | Republic of Rwanda, 144A, (3) | | | 6.625% | | | | 5/02/23 | | | | B+ | | | | 8,316,000 | |

| | | | | |

| | | | Senegal – 1.0% | | | | | | | | | | | | |

| | | | | |

| | 925 | | | Republic of Senegal, 144A | | | 8.750% | | | | 5/13/21 | | | | Ba3 | | | | 980,796 | |

| | 235 | | | Republic of Senegal, Reg S | | | 8.750% | | | | 5/13/21 | | | | Ba3 | | | | 249,175 | |

| | 1,160 | | | Total Senegal | | | | | | | | | | | | | | | 1,229,971 | |

| | | | | |

| | | | Sri Lanka – 2.8% | | | | | | | | | | | | |

| | | | | |

| | 600 | | | Republic of Sri Lanka, 144A, (3) | | | 5.875% | | | | 7/25/22 | | | | B | | | | 561,103 | |

| | 3,000 | | | Sri Lanka Government International Bond, 144A, (3) | | | 5.750% | | | | 4/18/23 | | | | B | | | | 2,760,570 | |

| | 3,600 | | | Total Sri Lanka | | | | | | | | | | | | | | | 3,321,673 | |

| | | | | |

| | | | Turkey – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Export Credit Bank of Turkey, 144A | | | 4.250% | | | | 9/18/22 | | | | BB– | | | | 903,232 | |

| | | | | |

| | | | Ukraine – 5.8% | | | | | | | | | | | | |

| | | | | |

| | 7,650 | | | Republic of Ukraine, 144A, (3) | | | 7.750% | | | | 9/01/22 | | | | B– | | | | 7,010,154 | |

| | | | | |

| | | | Zambia – 4.4% | | | | | | | | | | | | |

| | | | | |

| | 7,500 | | | Republic of Zambia, 144A, (3) | | | 5.375% | | | | 9/20/22 | | | | B– | | | | 5,362,200 | |

| $ | 99,377 | | | Total Emerging Markets Debt (cost $101,541,425) | | | | | | | | | | | | | | | 89,030,471 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | CORPORATE BONDS – 61.5% (45.0% of Total Investments) | | | | | |

| | | | | |

| | | | Banks – 23.8% | | | | | | | | | | | | |

| | | | | |

| $ | 750 | | | Akbank TAS, 144A | | | 5.000% | | | | 10/24/22 | | | | B1 | | | $ | 701,218 | |

| | 600 | | | Banco De Bogota, 144A | | | 5.375% | | | | 2/19/23 | | | | BBB– | | | | 595,500 | |

| | 750 | | | Banco Do Brasil, 144A | | | 5.875% | | | | 1/19/23 | | | | Ba3 | | | | 768,750 | |

| | 2,500 | | | Credit Bank of Moscow Via CBOM Finance PLC, 144A | | | 5.875% | | | | 11/07/21 | | | | BB– | | | | 2,453,780 | |

| | 2,000 | | | Credit Bank of Moscow Via CBOM Finance PLC, 144A | | | 5.550% | | | | 2/14/23 | | | | BB– | | | | 1,871,616 | |

| | 3,900 | | | Kazkommertsbank, 144A | | | 5.500% | | | | 12/21/22 | | | | BB | | | | 3,821,922 | |

| | 4,000 | | | TC Ziraat Bankasi AS, 144A, (3) | | | 5.125% | | | | 5/03/22 | | | | B1 | | | | 3,662,320 | |

| | 1,200 | | | Trade and Development Bank of Mongolia, 144A, (3) | | | 9.375% | | | | 5/19/20 | | | | B | | | | 1,249,225 | |

| | 300 | | | Turkiye IS Bankasi (Isbank), 144A | | | 5.250% | | | | 9/13/22 | | | | BB– | | | | 282,127 | |

| | 5,000 | | | Turkiye IS Bankasi (Isbank), 144A, (3) | | | 6.000% | | | | 10/24/22 | | | | B | | | | 4,137,550 | |

| | 3,304 | | | Turkiye Vakiflar Bankasi T.A.O, 144A | | | 6.000% | | | | 11/01/22 | | | | B | | | | 2,786,798 | |

| | 3,000 | | | United Bank for Africa PLC, 144A, (3) | | | 7.750% | | | | 6/08/22 | | | | B+ | | | | 2,962,380 | |

| | 3,500 | | | Zenith Bank PLC, 144A, (3) | | | 7.375% | | | | 5/30/22 | | | | B+ | | | | 3,470,229 | |

| | 30,804 | | | Total Banks | | | | | | | | | | | | | | | 28,763,415 | |

| | | | | |

| | | | Commercial Services & Supplies – 2.0% | | | | | | | | | | | | |

| | | | | |

| | 2,500 | | | Atento Luxco 1 SA, 144A | | | 6.125% | | | | 8/10/22 | | | | BB | | | | 2,425,000 | |

| | | | | |

| | | | Communications Equipment – 2.7% | | | | | | | | | | | | |

| | | | | |

| | 3,250 | | | IHS Netherlands Holdco B.V, 144A, (3) | | | 9.500% | | | | 10/27/21 | | | | B+ | | | | 3,268,083 | |

| | | | | |

| | | | Diversified Financial Services – 3.5% | | | | | | | | | | | | |

| | | | | |

| | 4,300 | | | Ukreximbank Via Biz Finance PLC, 144A | | | 9.625% | | | | 4/27/22 | | | | B– | | | | 4,206,260 | |

| | | | | |

| | | | Diversified Telecommunication Services – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Colombia Telecommunicaciones S.A. ESP, 144A, (3) | | | 5.375% | | | | 9/27/22 | | | | BB+ | | | | 995,000 | |

| | | | | |

| | | | Electric Utilities – 3.9% | | | | | | | | | | | | |

| | | | | |

| | 5,000 | | | Esckom Holdings Limited, 144A, (3) | | | 5.750% | | | | 1/26/21 | | | | B3 | | | | 4,710,240 | |

16

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Food Products – 2.1% | | | | | | | | | | | | |

| | | | | |

| $ | 2,700 | | | Kernel Holding SA, 144A, (3) | | | 8.750% | | | | 1/31/22 | | | | B+ | | | $ | 2,586,568 | |

| | |

| | | | Independent Power & Renewable Electricity Producers – 1.7% | | | | |

| | | | | |

| | 2,250 | | | Azure Power Energy Ltd, 144A, (3) | | | 5.500% | | | | 11/03/22 | | | | Ba3 | | | | 2,109,825 | |

| | | | | |

| | | | Metals & Mining – 5.3% | | | | | | | | | | | | |

| | | | | |

| | 3,000 | | | Petra Diamonds US Treasury PLC, 144A, (3) | | | 7.250% | | | | 5/01/22 | | | | B | | | | 2,775,000 | |

| | 4,000 | | | Vedanta Resources PLC, 144A, (3) | | | 7.125% | | | | 5/31/23 | | | | B+ | | | | 3,592,000 | |

| | 7,000 | | | Total Metals & Mining | | | | | | | | | | | | | | | 6,367,000 | |

| | | | | |

| | | | Oil, Gas & Consumable Fuels – 6.7% | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | Azerbaijan State Oil Company, Reg S | | | 4.750% | | | | 3/13/23 | | | | BB+ | | | | 1,990,520 | |

| | 1,500 | | | Medco Straits Services PTE LTD, 144A | | | 8.500% | | | | 8/17/22 | | | | B | | | | 1,461,234 | |

| | 2,800 | | | Petrobras Global Finance BV | | | 4.375% | | | | 5/20/23 | | | | Ba2 | | | | 2,670,836 | |

| | 2,000 | | | Tullow Oil PLC, 144A | | | 6.250% | | | | 4/15/22 | | | | B+ | | | | 1,925,000 | |

| | 8,300 | | | Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | | | 8,047,590 | |

| | | | | |

| | | | Pharmaceuticals – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 1,100 | | | Teva Pharmaceutical Finance Company B.V., Series D | | | 2.950% | | | | 12/18/22 | | | | BB | | | | 972,743 | |

| | | | | |

| | | | Real Estate Management & Development – 3.9% | | | | | | | | | | | | |

| | | | | |

| | 3,200 | | | China Evergrande Group, Reg S | | | 8.250% | | | | 3/23/22 | | | | B+ | | | | 3,072,474 | |

| | 1,750 | | | Country Garden Holding Company, Reg S | | | 4.750% | | | | 7/25/22 | | | | BBB– | | | | 1,589,214 | |

| | 4,950 | | | Total Real Estate Management & Development | | | | | | | | | | | | | | | 4,661,688 | |

| | | | | |

| | | | Road & Rail – 0.9% | | | | | | | | | | | | |

| | | | | |

| | 1,100 | | | Transnet SOC Limited, 144A | | | 4.000% | | | | 7/26/22 | | | | Baa3 | | | | 1,029,195 | |

| | | | | |

| | | | Wireless Telecommunication Services – 3.4% | | | | | | | | | | | | |

| | | | | |

| | 3,700 | | | Digicel Group, Limited, 144A | | | 7.125% | | | | 4/01/22 | | | | Caa3 | | | | 1,720,500 | |

| | | | | |

| | 2,525 | | | MTN Mauritius Investments Ltd, 144A, (3) | | | 5.373% | | | | 2/13/22 | | | | BB+ | | | | 2,448,720 | |

| | 6,225 | | | Total Wireless Telecommunication Services | | | | | | | | | | | | | | | 4,169,220 | |

| $ | 80,479 | | | Total Corporate Bonds (cost $81,744,510) | | | | | | | | | | | | | | | 74,311,827 | |

| | | | Total Long-Term Investments (cost $183,285,935) | | | | | | | | | | | | | | | 163,342,298 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | SHORT-TERM INVESTMENTS – 1.4% (1.0% of Total Investments) | | | | | |

| | | |

| | | | U.S. GOVERNMENT AND AGENCY OBLIGATIONS – 1.4% (1.0% of Total Investments) | | | | | | | |

| | | | | |

| $ | 1,630 | | | Federal Home Loan Bank Discount Notes | | | 0.000% | | | | 1/02/19 | | | | N/R | | | $ | 1,629,903 | |

| | | | Total Short-Term Investments (cost $1,629,903) | | | | | | | | | | | | | | | 1,629,903 | |

| | | | Total Investments (cost $184,915,838) – 136.5% | | | | | | | | | | | | | | | 164,972,201 | |

| | | | Reverse Repurchase Agreements – (38.9)% (4) | | | | | | | | | | | | | | | (47,000,000 | ) |

| | | | Other Assets Less Liabilities – 2.4% | | | | | | | | | | | | | | | 2,898,387 | |

| | | | Net Assets Applicable to Common Shares – 100% | | | | | | | | | | | | | | $ | 120,870,588 | |

17

| | |

| |

| JEMD | | Nuveen Emerging Markets Debt 2022 Target Term Fund(continued) |

| | Portfolio of Investments December 31, 2018 |

Summary of Investments in Emerging Markets Countries

| | | | |

| Ukraine | | | 8.4% | |

| Turkey | | | 7.6% | |

| South Africa | | | 6.6% | |

| Rwanda | | | 5.0% | |

| Nigeria | | | 4.8% | |

| Lebanon | | | 4.6% | |

| Ecuador | | | 4.5% | |

| Iraq | | | 4.3% | |

| El Salvador | | | 4.0% | |

| Argentina | | | 3.7% | |

| Ghana | | | 3.7% | |

| Egypt | | | 3.4% | |

| Zambia | | | 3.3% | |

| Barbados | | | 2.9% | |

| China | | | 2.8% | |

| Mongolia | | | 2.7% | |

| Russia | | | 2.6% | |

| Kazakhstan | | | 2.3% | |

| Bahamas | | | 2.2% | |

| | | | |

| Brazil | | | 2.1% | |

| Sri Lanka | | | 2.0% | |

| Mauritius | | | 2.0% | |

| Costa Rica | | | 1.3% | |

| India | | | 1.3% | |

| Azerbaijan | | | 1.2% | |

| Bermuda | | | 1.0% | |

| Bahrain | | | 1.0% | |

| Indonesia | | | 0.9% | |

| Senegal | | | 0.7% | |

| Honduras | | | 0.6% | |

| Pakistan | | | 0.6% | |

| Belarus | | | 0.5% | |

| Dominican Republic | | | 0.4% | |

| Colombia | | | 0.3% | |

| Paraguay | | | 0.3% | |

Total Emerging Markets Countries | | | 95.6% | |

Total Developed Countries | | | 4.4% | |

Total Investments | | | 100% | |

For Fund portfolio compliance purposes, the Fund’s industry classifications refer to any one or more of the industrysub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industrysub-classifications into sectors for reporting ease.

| (1) | All percentages shown in the Portfolio of Investments are based on net assets applicable to common shares unless otherwise noted. |

| (2) | For financial reporting purposes, the ratings disclosed are the highest of Standard & Poor’s Group (“Standard & Poor’s”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch, Inc. (“Fitch”) rating. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Ratings below BBB by Standard & Poor’s, Baa by Moody’s or BBB by Fitch are considered to be below investment grade. Holdings designated N/R are not rated by any of these national rating agencies. Ratings are not covered by the report of independent registered public accounting firm. |

| (3) | Investment, or portion of investment, has been pledged to collateralize the net payment obligations for investments in reverse repurchase agreements. |

| (4) | Reverse repurchase agreements as a percentage of Total Investments is 28.5%. |

| 144A | Investment is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These investments may only be resold in transactions exempt from registration, which are normally those transactions with qualified institutional buyers. |

| Reg S | Regulation S allows U.S. companies to sell securities to persons or entities located outside of the United States without registering those securities with the Securities and Exchange Commission. Specifically, Regulation S provides a safe harbor from the registration requirements of the Securities Act for the offers and sales of securities by both foreign and domestic issuers that are made outside the United States. |

See accompanying notes to financial statements.

18

Statement of Assets and Liabilities

December 31, 2018

| | | | |

Assets | | | | |

Long-term investments, at value (cost $183,285,935) | | $ | 163,342,298 | |

Short-term investments, at value (cost approximates value) | | | 1,629,903 | |

Receivable for interest | | | 3,289,100 | |

Other assets | | | 1,237 | |

Total assets | | | 168,262,538 | |

Liabilities | | | | |

Reverse repurchase agreements | | | 47,000,000 | |

Cash overdraft | | | 101,904 | |

Accrued expenses: | | | | |

Interest | | | 86,106 | |

Management fees | | | 137,026 | |

Trustees fees | | | 1,067 | |

Other | | | 65,847 | |

Total liabilities | | | 47,391,950 | |

Net assets applicable to common shares | | $ | 120,870,588 | |

Common shares outstanding | | | 14,235,550 | |

Net asset value (“NAV”) per common share outstanding | | $ | 8.49 | |

Net assets applicable to common shares consist of: | | | | |

Common shares, $0.01 par value per share | | $ | 142,356 | |

Paid-in surplus | | | 139,777,946 | |

Total distributable earnings | | | (19,049,714 | ) |

Net assets applicable to common shares | | $ | 120,870,588 | |

Authorized common shares | | | Unlimited | |

See accompanying notes to financial statements.

19

Statement of Operations

Year Ended December 31, 2018

| | | | |

Investment Income | | $ | 10,814,821 | |

Expenses | | | | |

Management fees | | | 1,691,015 | |

Interest expense | | | 1,220,091 | |

Custodian fees | | | 33,888 | |

Trustees fees | | | 4,503 | |

Professional fees | | | 81,266 | |

Shareholder reporting expenses | | | 25,592 | |

Shareholder servicing agent fees | | | 167 | |

Stock exchange listing fees | | | 6,771 | |

Investor relations expense | | | 12,434 | |

Other | | | 5,415 | |

Total expenses | | | 3,081,142 | |

Net investment income (loss) | | | 7,733,679 | |

Realized and Unrealized Gain (Loss) | | | | |

Net realized gain (loss) from investments | | | (37,508 | ) |

Change in net unrealized appreciation (depreciation) of investments | | | (19,642,595 | ) |

Net realized and unrealized gain (loss) | | | (19,680,103 | ) |

Net increase (decrease) in net assets from operations | | $ | (11,946,424 | ) |

See accompanying notes to financial statements.

20

Statement of Changes in Net Assets

| | | | | | | | |

| | | Year Ended 12/31/18 | | | For the period September 26, 2017(1)

(commencement of operations)

through December 31, 2017 | |

Operations | | | | | | | | |

Net investment income (loss) | | $ | 7,733,679 | | | $ | 1,655,173 | |

Net realized gain (loss) from investments | | | (37,508 | ) | | | 25,841 | |

Change in net unrealized appreciation (depreciation) of investments | | | (19,642,595 | ) | | | (301,042 | ) |

Net increase (decrease) in net assets applicable to common shares from operations | | | (11,946,424 | ) | | | 1,379,972 | |

Distributions to Common Shareholders(2) | | | | | | | | |

Dividends(3) | | | (7,260,130 | ) | | | (1,238,476 | ) |

Decrease in net assets applicable to common shares from distributions to common shareholders | | | (7,260,130 | ) | | | (1,238,476 | ) |

Capital Share Transactions | | | | | | | | |

Proceeds from sale of common shares, net of offering costs | | | — | | | | 139,831,750 | |

Proceeds from common shares issued to shareholders due to reinvestment of distributions | | | — | | | | 3,820 | |

Net increase (decrease) in net assets applicable to common shares from capital share transactions | | | — | | | | 139,835,570 | |

Net increase (decrease) in net assets applicable to common shares | | | (19,206,554 | ) | | | 139,977,066 | |

Net assets applicable to common shares at the beginning of period | | | 140,077,142 | | | | 100,076 | |

Net assets applicable to common shares at the end of period | | $ | 120,870,588 | | | $ | 140,077,142 | |

| (1) | Prior period amounts have been conformed to current year presentation. See Notes to Financial Statements, Note 10 – New Accounting Pronouncements for further details. |

| (2) | The composition and per share amounts of the Fund’s distributions are presented in the Financial Highlights. The distribution information for the Fund as of its most recent tax year end is presented within the Notes to Financial Statements, Note 6 – Income Tax Information. |

| (3) | For the period September 26, 2017 (commencement of operations) through December 31, 2017, the Fund’s distributions to shareholders were paid from net investment income and accumulated net realized gains. |

See accompanying notes to financial statements.

21

Statement of Cash Flows

Year Ended December 31, 2018

| | | | |

Cash Flows from Operating Activities: | | | | |

Net Increase (Decrease) in Net Assets Applicable to Common Shares from Operations | | $ | (11,946,424 | ) |

Adjustments to reconcile the net increase (decrease) in net assets applicable to common shares from operations

to net cash provided by (used in) operating activities: | | | | |

Purchases of investments | | | (12,816,005 | ) |

Proceeds from sales and maturities of investments | | | 12,671,550 | |

Proceeds from (Purchases of) short-term investments, net | | | (1,629,903 | ) |

Taxes paid | | | (15,344 | ) |

Amortization (Accretion) of premiums and discounts, net | | | 989,067 | |

(Increase) Decrease in: | | | | |

Receivable for interest | | | 104,654 | |

Receivable for investments sold | | | 421,179 | |

Other assets | | | (1,237 | ) |

Increase (Decrease) in: | | | | |

Payable for investments purchased | | | (1,133,291 | ) |

Accrued interest | | | 24,372 | |

Accrued management fees | | | (15,159 | ) |

Accrued Trustees fees | | | (425 | ) |

Accrued other expenses | | | (7,036 | ) |

Net realized (gain) loss from investments | | | 37,508 | |

Change in net unrealized (appreciation) depreciation of investments | | | 19,642,595 | |

Net cash provided by (used in) operating activities | | | 6,326,101 | |

Cash Flows from Financing Activities: | | | | |

Cash distributions paid to common shareholders | | | (7,260,130 | ) |

Increase (Decrease) in cash overdraft | | | 101,904 | |

Net cash provided by (used in) financing activities | | | (7,158,226 | ) |

Net Increase (Decrease) in Cash | | | (832,125 | ) |

Cash at the beginning of period | | | 832,125 | |

Cash at the end of period | | $ | — | |

| |

| Supplemental Disclosure of Cash Flow Information | | | |

Cash paid for interest (excluding costs) | | $ | 1,195,719 | |

See accompanying notes to financial statements.

22

THIS PAGE INTENTIONALLY LEFT BLANK

23

Financial Highlights

Selected data for a common share outstanding throughout each period:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | Investment Operations | | | Less Distributions to

Common Shareholders | | | | | | Common Share | |

| | | Beginning

Common

Share

NAV | | | Net

Investment

Income (Loss)(a) | | | Net

Realized/

Unrealized

Gain (Loss) | | | Total | | | From Net

Investment

Income | | | From

Accumulated

Net Realized

Gains | | | Total | | | Offering

Costs | | | Ending

NAV | | | Ending

Share

Price | |

Year Ended 12/31: | |

2018 | | $ | 9.84 | | | $ | 0.54 | | | $ | (1.38 | ) | | $ | (0.84 | ) | | $ | (0.51 | ) | | $ | — | | | $ | (0.51 | ) | | $ | — | | | $ | 8.49 | | | $ | 7.63 | |

2017(e) | | | 9.85 | | | | 0.12 | | | | (0.02 | ) | | | 0.10 | | | | (0.09 | ) | | | — | * | | | (0.09 | ) | | | (0.02 | ) | | | 9.84 | | | | 9.40 | |

24

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Common Share Supplemental Data/

Ratios Applicable to Common Shares | |

Common Share

Total Returns | | | | | | Ratios to Average Net Assets(c) | | | | |

Based

on

NAV(b) | | | Based

on

Share

Price(b) | | | Ending

Net

Assets

(000) | | | Expenses | | | Net

Investment

Income (Loss) | | | Portfolio

Turnover

Rate(d) | |

| | | | | | | | | | | | | | | | | | | | | | |

| | (8.71 | )% | | | (13.85 | )% | | $ | 120,871 | | | | 2.38 | % | | | 5.98 | % | | | 9 | % |

| | 0.79 | | | | (5.15 | ) | | | 140,077 | | | | 1.85 | ** | | | 4.70 | ** | | | 7 | |

| (a) | Per share Net Investment Income (Loss) is calculated using the average daily shares method. |

| (b) | Total Return Based on Common Share NAV is the combination of changes in common share NAV, reinvested dividend income at NAV and reinvested capital gains distributions at NAV, if any. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending NAV. The actual reinvest price for the last dividend declared in the period may often be based on the Fund’s market price (and not its NAV), and therefore may be different from the price used in the calculation. Total returns are not annualized. |

Total Return Based on Common Share Price is the combination of changes in the market price per share and the effect of reinvested dividend income and reinvested capital gains distributions, if any, at the average price paid per share at the time of reinvestment. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending market price. The actual reinvestment for the last dividend declared in the period may take place over several days, and in some instances may not be based on the market price, so the actual reinvestment price may be different from the price used in the calculation. Total returns are not annualized.

| | | | |

| (c) | | • | | Net Investment Income (Loss) ratios reflect income earned and expense incurred on assets attributable to reverse repurchase agreements (as described in Note 8 – Fund Leverage, Reverse Repurchase Agreements), where applicable. |

| | • | | Each ratio includes the effect of all interest expenses paid and other costs related to reverse repurchase agreements, where applicable, as follows: |

| | | | |

Ratio of Interest Expense to Average Net Assets Applicable to Common Shares | |

Year Ended 12/31: | |

2018 | | | 0.94 | % |

2017(e) | | | 0.48 | ** |

| (d) | Portfolio Turnover Rate is calculated based on the lesser of long-term purchases or sales (as disclosed in Note 5 – Investment Transactions) divided by the average long-term market value during the period. |

| (e) | For the period September 26, 2017 (commencement of operations) through December 31, 2017. |

| * | Rounds to less than $0.01 per share. |

See accompanying notes to financial statements.

25

Notes to Financial Statements

1. General Information and Significant Accounting Policies

General Information

Fund Information

Nuveen Emerging Markets Debt 2022 Target Term Fund (the “Fund”) is registered under the Investment Company Act of 1940, as amended, as anon-diversified,closed-end management investment company. The Fund’s shares are listed on the New York Stock Exchange (“NYSE”) and trade under the ticker symbol “JEMD.” The Fund was organized as a Massachusetts business trust on June 1, 2017.

The end of the reporting period for the Fund is December 31, 2018, and the period covered by these Notes to Financial Statements is for the fiscal year ended December 31, 2018 (the “current fiscal period”).

Investment Adviser

The Fund’s investment adviser is Nuveen Fund Advisors, LLC (the “Adviser”), a subsidiary of Nuveen, LLC (“Nuveen”). Nuveen is the investment management arm of Teachers Insurance and Annuity Association of America (TIAA). The Adviser has overall responsibility for management of the Fund, oversees the management of the Fund’s portfolio, manages the Fund’s business affairs and provides certain clerical, bookkeeping and other administrative services, and, if necessary, asset allocation decisions. The Adviser has entered into asub-advisory agreement with Teachers Advisors, LLC (the“Sub-Adviser”), an affiliate of the Adviser, under which theSub-Adviser manages the Fund’s investment portfolio.

Investment Objectives and Principal Investment Strategies

The Fund seeks to provide a high level of current income and return the original $9.85 net asset value (“NAV”) per share on or about December 1, 2022 (the “Termination Date”). The Fund generally invests in a portfolio of below investment grade emerging market debt securities. At least 80% of the Fund’s managed assets (as defined in Note 7 – Management Fees) will be in emerging market debt securities. However, the Fund invests no more than 10% of its managed assets in securities rated belowB-/B3 or that are unrated but judged by the Sub-Adviser to be of comparable quality. The Fund invests 100% of its managed assets in U.S. dollar denominated securities. No more than 25% is invested in securities of issuers located in a single country.

Significant Accounting Policies

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (ASC) Topic 946 “Financial Services-Investment Companies.” The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”).

Investment Transactions

Investment transactions are recorded on a trade date basis. Realized gains and losses from investment transactions are determined on the specific identification method, which is the same basis used for federal income tax purposes. Investments purchased on a when-issued/delayed delivery basis may have extended settlement periods. Any investments so purchased are subject to market fluctuation during this period. The Fund has earmarked securities in its portfolio with a current value at least equal to the amount of the when-issued/delayed delivery purchase commitments.

As of the end of the reporting period, the Fund did not have any outstanding when-issued/delayed delivery purchase commitments.

Investment Income

Investment income is comprised of interest income, which reflects the amortization of premiums and accretion of discounts for financial reporting purposes, and is recorded on an accrual basis. Investment income also reflectspayment-in-kind (“PIK”) interest, fees earned from reverse repurchase agreements and paydown gains and losses, if any. PIK interest represents income received in the form of securities in lieu of cash.

Professional Fees

Professional fees presented on the Statement of Operations consist of legal fees incurred in the normal course of operations, audit fees, tax consulting fees and, in some cases, workout expenditures. Workout expenditures are incurred in an attempt to protect or enhance an investment or to pursue other claims or legal actions on behalf of Fund shareholders. If a refund is received for workout expenditures paid in a prior reporting period, such amounts will be recognized as “Legal fee refund” on the Statement of Operations.

26

Dividends and Distributions to Common Shareholders

Dividends to common shareholders, if any, are declared monthly. Net realized capital gains from investment transactions, if any, are declared and distributed to shareholders at least annually. However, in seeking to achieve its investment objectives, the Fund currently intends to set aside and retain in its net assets (and therefore its NAV) a portion of its net investment income, and possibly all or a portion of its gains. This will reduce the amounts otherwise available for distribution prior to the liquidation of the Fund, and the Fund may incur taxes on such retained amount. Such retained income or gains, net of any taxes, would constitute a portion of the liquidating distribution returned to investors on or about the Termination Date. Furthermore, capital gains are distributed only to the extent they exceed available capital loss carryforwards.

Distributions to common shareholders are recorded on theex-dividend date. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from U.S. GAAP.

Compensation

The Fund pays no compensation directly to those of its trustees who are affiliated with the Adviser or to its officers, all of whom receive renumeration for their services to the Fund from the Adviser or its affiliates. The Fund’s Board of Trustees (the “Board”) has adopted a deferred compensation plan for independent trustees that enables trustees to elect to defer receipt of all or a portion of the annual compensation they are entitled to receive from certain Nuveen-advised funds. Under the plan, deferred amounts are treated as though equal dollar amounts had been invested in shares of select Nuveen-advised funds.

Indemnifications

Under the Fund’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Fund enters into contracts that provide general indemnifications to other parties. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. However, the Fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

Netting Agreements

In the ordinary course of business, the Fund may enter into transactions subject to enforceable master repurchase agreements, International Swaps and Derivatives Association, Inc. (ISDA) master agreements or other similar arrangements (“netting agreements”). Generally, the right to offset in netting agreements allows the Fund to offset certain securities and derivatives with a specific counterparty, when applicable, as well as any collateral received or delivered to that counterparty based on the terms of the agreements. Generally, the Fund manages its cash collateral and securities collateral on a counterparty basis.

The Fund’s investments subject to netting agreements as of the end of the reporting period, if any, are further described in Note 3 – Portfolio Securities and Investments in Derivatives.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets applicable to common shares from operations during the current fiscal period. Actual results may differ from those estimates.

2. Investment Valuation and Fair Value Measurements

The fair valuation input levels as described below are for fair value measurement purposes.

Fair value is defined as the price that would be received upon selling an investment or transferring a liability in an orderly transaction to an independent buyer in the principal or most advantageous market for the investment. A three-tier hierarchy is used to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability. Observable inputs are based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability. Unobservable inputs are based on the best information available in the circumstances. The following is a summary of the three-tiered hierarchy of valuation input levels.

| | | | |

| Level 1 – | | Inputs are unadjusted and prices are determined using quoted prices in active markets for identical securities. |

| Level 2 – | | Prices are determined using other significant observable inputs (including quoted prices for similar securities, interest rates, credit spreads, etc.). |

| Level 3 – | | Prices are determined using significant unobservable inputs (including management’s assumptions in determining the fair value of investments). |

27

Notes to Financial Statements(continued)

Prices of fixed-income securities are provided by an independent pricing service (“pricing service”) approved by the Board. The pricing service establishes a security’s fair value using methods that may include consideration of the following: yields or prices of investments of comparable quality, type of issue, coupon, maturity and rating, market quotes or indications of value from security dealers, evaluations of anticipated cash flows or collateral, general market conditions and other information and analysis, including the obligor’s credit characteristics considered relevant. These securities are generally classified as Level 2. In pricing certain securities, particularly less liquid and lower quality securities, the pricing service may consider information about a security, its issuer or market activity provided by the Adviser. These securities are generally classified as Level 2 or Level 3 depending on the observability of the significant inputs.

Certain securities may not be able to be priced by thepre-established pricing methods as described above. Such securities may be valued by the Board and/or its appointee at fair value. These securities generally include, but are not limited to, restricted securities (securities which may not be publicly sold without registration under the Securities Act of 1933, as amended) for which a pricing service is unable to provide a market price; securities whose trading has been formally suspended; debt securities that have gone into default and for which there is no current market quotation; a security whose market price is not available from apre-established pricing source; a security with respect to which an event has occurred that is likely to materially affect the value of the security after the market has closed but before the calculation of the Fund’s NAV (as may be the case innon-U.S. markets on which the

security is primarily traded) or make it difficult or impossible to obtain a reliable market quotation; and a security whose price, as provided by the pricing service, is not deemed to reflect the security’s fair value. As a general principle, the fair value of a security would appear to be the amount that the owner might reasonably expect to receive for it in a current sale. A variety of factors may be considered in determining the fair value of such securities, which may include consideration of the following: yields or prices of investments of comparable quality, type of issue, coupon, maturity and rating, market quotes or indications of value from security dealers, evaluations of anticipated cash flows or collateral, general market conditions and other information and analysis, including the obligor’s credit characteristics considered relevant. These securities are generally classified as Level 2 or Level 3 depending on the observability of the significant inputs. Regardless of the method employed to value a particular security, all valuations are subject to review by the Board and/or its appointee.

The inputs or methodologies used for valuing securities are not an indication of the risks associated with investing in those securities. The following is a summary of the Fund’s fair value measurements as of the end of the reporting period:

| | | | | | | | | | | | | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Long-Term Investments*: | | | | | | | | | | | | | | | | |