UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-23285

| Name of Fund: | | BlackRock Multi-Sector Opportunities Trust |

| Fund Address: | | 100 Bellevue Parkway, Wilmington, DE 19809 |

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock Multi-Sector Opportunities Trust, 50 Hudson Yards, New York, NY 10001

Registrant’s telephone number, including area code: (800) 882-0052, Option 4

Date of fiscal year end: 12/31/2023

Date of reporting period: 12/31/2023

Item 1 – Report to Stockholders

(a) The Report to Shareholders is attached herewith.

| | |

| | DECEMBER 31, 2023 |

BlackRock Multi-Sector Opportunities Trust

|

| Not FDIC Insured • May Lose Value • No Bank Guarantee |

The Markets in Review

Dear Shareholder,

The combination of continued economic growth and cooling inflation provided a supportive backdrop for investors during the 12-month reporting period ended December 31, 2023. Significantly tighter monetary policy helped to rein in inflation, and the Consumer Price Index decelerated substantially in the first half of the year before stalling between 3% and 4% in the second half. A moderating labor market helped ease inflationary pressure, although wages continued to grow. Wage and job growth powered robust consumer spending, backstopping the economy. On October 7, 2023, Hamas launched a horrific attack on Israel. The ensuing war will have a significant humanitarian impact and could lead to heightened economic and market volatility. We see geopolitics as a structural market risk going forward. See our geopolitical risk dashboard at blackrock.com for more details.

Equity returns were robust during the period, as interest rates stabilized and the economy proved to be more resilient than many investors expected. The U.S. economy continued to show strength, and growth further accelerated in the third quarter of 2023. Large-capitalization U.S. stocks posted particularly substantial gains, supported by the performance of a few notable technology companies and small-capitalization U.S. stocks also advanced. Meanwhile, international developed market equities and emerging market stocks posted solid gains.

The 10-year U.S. Treasury yield ended 2023 where it began despite an eventful year that saw significant moves in bond markets. Overall, U.S. Treasuries gained as investors began to anticipate looser financial conditions. The corporate bond market benefited from improving economic sentiment, although high-yield corporate bond prices fared significantly better than investment-grade bonds as demand from yield-seeking investors remained strong.

The U.S. Federal Reserve (the “Fed”), attempting to manage persistent inflation, raised interest rates four times during the 12-month period, but paused its tightening in the second half of the period. The Fed also wound down its bond-buying programs and incrementally reduced its balance sheet by not replacing securities that reach maturity.

Supply constraints appear to have become an embedded feature of the new macroeconomic environment, making it difficult for developed economies to increase production without sparking higher inflation. Geopolitical fragmentation and an aging population risk further exacerbating these constraints, keeping the labor market tight and wage growth high. Although the Fed has stopped tightening for now, we believe that the new economic regime means that the Fed will need to maintain high rates for an extended period despite the market’s hopes for interest rate cuts, as reflected in the recent rally. In this new regime, we anticipate greater volatility and dispersion of returns, creating more opportunities for selective portfolio management.

We believe developed market equities have priced in an optimistic scenario for rate cuts, which we view as premature, so we prefer an underweight stance in the near term. Nevertheless, we are overweight on Japanese stocks as shareholder-friendly policies generate increased investor interest. We also believe that stocks with an AI tilt should benefit from an investment cycle that is set to support revenues and margins. In credit, there are selective opportunities in the near term despite tighter credit and financial conditions. For fixed income investing with a six- to twelve-month horizon, we see the most attractive investments in short-term U.S. Treasuries, U.S. mortgage-backed securities, and hard-currency emerging market bonds.

Overall, our view is that investors need to think globally, position themselves to be prepared for a decarbonizing economy, and be nimble as market conditions change. We encourage you to talk with your financial advisor and visit blackrock.com for further insight about investing in today’s markets.

Sincerely,

Rob Kapito

President, BlackRock Advisors, LLC

Rob Kapito

President, BlackRock Advisors, LLC

| | | | |

| Total Returns as of December 31, 2023 |

| | | 6-Month | | 12-Month |

U.S. large cap equities

(S&P 500® Index) | | 8.04% | | 26.29% |

U.S. small cap equities

(Russell 2000® Index) | | 8.18 | | 16.93 |

International equities

(MSCI Europe, Australasia, Far East Index) | | 5.88 | | 18.24 |

Emerging market equities (MSCI Emerging Markets Index) | | 4.71 | | 9.83 |

3-month Treasury bills

(ICE BofA 3-Month

U.S. Treasury Bill Index) | | 2.70 | | 5.02 |

U.S. Treasury securities

(ICE BofA 10-Year

U.S. Treasury Index) | | 1.11 | | 2.83 |

U.S. investment grade bonds (Bloomberg U.S. Aggregate Bond Index) | | 3.37 | | 5.53 |

Tax-exempt municipal bonds (Bloomberg Municipal Bond Index) | | 3.63 | | 6.40 |

U.S. high yield bonds (Bloomberg U.S. Corporate High Yield 2%

Issuer Capped Index) | | 7.65 | | 13.44 |

|

Past performance is not an indication of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. |

| | |

| 2 | | THIS PAGE IS NOT PART OF YOUR FUND REPORT |

Table of Contents

| | |

| The Benefits and Risks of Leveraging | | BlackRock Multi-Sector Opportunities Trust (MSO) |

The Trust may utilize leverage to seek to enhance the distribution rate on, and net asset value (“NAV”) of, its common shares (“Common Shares”). However, there is no guarantee that these objectives can be achieved in all interest rate environments.

In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is normally lower than the income earned by the Trust on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of the Trust (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, the Trust’s shareholders benefit from the incremental net income. The interest earned on securities purchased with the proceeds from leverage (after paying the leverage costs) is paid to shareholders in the form of dividends, and the value of these portfolio holdings (less the leverage liability) is reflected in the per share NAV.

To illustrate these concepts, assume the Trust’s capitalization is $100 million and it utilizes leverage for an additional $30 million, creating a total value of $130 million available for investment in longer-term income securities. If prevailing short-term interest rates are 3% and longer-term interest rates are 6%, the yield curve has a strongly positive slope. In this case, the Trust’s financing costs on the $30 million of proceeds obtained from leverage are based on the lower short-term interest rates. At the same time, the securities purchased by the Trust with the proceeds from leverage earn income based on longer-term interest rates. In this case, the Trust’s financing cost of leverage is significantly lower than the income earned on the Trust’s longer-term investments acquired from such leverage proceeds, and therefore the holders of Common Shares (“Common Shareholders”) are the beneficiaries of the incremental net income.

However, in order to benefit shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the leverage. If interest and other costs of leverage exceed the Trust’s return on assets purchased with leverage proceeds, income to shareholders is lower than if the Trust had not used leverage. Furthermore, the value of the Trust’s portfolio investments generally varies inversely with the direction of long-term interest rates, although other factors can influence the value of portfolio investments. In contrast, the amount of the Trust’s obligations under its leverage arrangement generally does not fluctuate in relation to interest rates. As a result, changes in interest rates can influence the Trust’s NAV positively or negatively. Changes in the future direction of interest rates are very difficult to predict accurately, and there is no assurance that the Trust’s intended leveraging strategy will be successful.

The use of leverage also generally causes greater changes in the Trust’s NAV, market price and dividend rates than comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV and market price of the Trust’s shares than if the Trust were not leveraged. In addition, the Trust may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of leverage instruments, which may cause the Trust to incur losses. The use of leverage may limit the Trust’s ability to invest in certain types of securities or use certain types of hedging strategies. The Trust incurs expenses in connection with the use of leverage, all of which are borne by shareholders and may reduce income to the shareholders. Moreover, to the extent the calculation of the Trust’s investment advisory fees includes assets purchased with the proceeds of leverage, the investment advisory fees payable to the Trust’s investment adviser will be higher than if the Trust did not use leverage.

The Trust may utilize leverage through reverse repurchase agreements as described in the Notes to Financial Statements, if applicable.

Under the Investment Company Act of 1940, as amended (the “1940 Act”), the Trust is permitted to borrow money (including through the use of TOB Trusts) or issue debt securities up to 33 1/3% of its total managed assets. The Trust may voluntarily elect to limit its leverage to less than the maximum amount permitted under the 1940 Act.

Derivative Financial Instruments

The Trust may invest in various derivative financial instruments. These instruments are used to obtain exposure to a security, commodity, index, market, and/or other assets without owning or taking physical custody of securities, commodities and/or other referenced assets or to manage market, equity, credit, interest rate, foreign currency exchange rate, commodity and/or other risks. Derivative financial instruments may give rise to a form of economic leverage and involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty to the transaction or illiquidity of the instrument. Pursuant to Rule 18f-4 under the 1940 Act, among other things, the Trust must either use derivative financial instruments with embedded leverage in a limited manner or comply with an outer limit on fund leverage risk based on value-at-risk. The Trust’s successful use of a derivative financial instrument depends on the investment adviser’s ability to predict pertinent market movements accurately, which cannot be assured. The use of these instruments may result in losses greater than if they had not been used, may limit the amount of appreciation the Trust can realize on an investment and/or may result in lower distributions paid to shareholders. The Trust’s investments in these instruments, if any, are discussed in detail in the Notes to Financial Statements.

| | |

| 4 | | 2 0 2 3 BLACK ROCK ANNUAL REPORT TO SHAREHOLDERS |

| | |

| Trust Summary as of December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) |

Investment Objective

BlackRock Multi-Sector Opportunities Trust’s (MSO) (the “Trust”) investment objective is to seek to provide high income and total return. The Trust seeks to achieve its investment objective by investing at least 80% of its total assets in fixed income securities and other financial instruments that pay periodic income. The Trust may invest any amount of its assets in securities of any credit quality, including securities that are rated at the time of investment below investment grade — i.e., ‘‘Ba’’ or ‘‘BB’’ or below by Moody’s Investor’s Service, Inc. (“Moody’s”), S&P Global Ratings or Fitch Ratings, or securities that are judged to be of comparable quality by the Trust’s investment advisers. It is anticipated that the Trust will terminate on or around February 22, 2024 (the “Termination Date”). The Trust may invest directly in securities or synthetically through the use of derivatives.

The Trust’s common shares are not listed on any securities exchange. Investors should consider that they may not have access to their investment until the Termination Date. The Trust is designed for long-term investors and an investment in the common shares, unlike an investment in a traditional listed closed-end fund, should be considered illiquid.

On November 15, 2023, the Board of Trustees of the Trust (the “Board”), approved the adoption of a Plan of Liquidation in accordance with the Trust’s strategy of terminating on or around February 22, 2024. Under the Plan of Liquidation which was effective on November 30, 2023, the Trust will begin the process of liquidating portfolio assets and unwinding its affairs. The Trust expects to make a final liquidating distribution on or before February 29, 2024.

No assurance can be given that the Trust’s investment objective will be achieved.

Trust Information

| | |

| | |

Initial Offering Date | | February 23, 2018 |

Termination Date(a) | | February 22, 2024 |

Current Quarterly Distribution per Common Share(b) | | $1.521000 |

Current Annualized Distribution per Common Share(b) | | $6.084000 |

| | (a) | It is anticipated that the Trust will terminate on or around February 22, 2024. | |

| | (b) | The distribution rate is not constant and is subject to change. A portion of the distribution may be deemed a return of capital or net realized gain. | |

Net Asset Value Per Share Summary

| | | | | | | | | | | | | | | | | | | | |

| | | 12/31/23 | | | 12/31/22 | | | Change | | | High | | | Low | |

| | | | | |

Net Asset Value | | $ | 65.34 | | | $ | 66.67 | | | | (1.99 | )% | | $ | 69.46 | | | $ | 64.83 | |

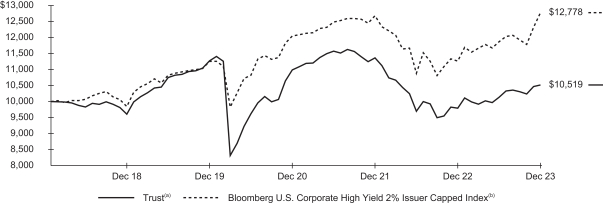

GROWTH OF $10,000 INVESTMENT

MSO commenced operations on February 23, 2018.

| | (a) | Represents the Trust’s NAV and reflects the reinvestment of dividends and/or distributions at NAV on the payable date. | |

| | (b) | An unmanaged index comprised of issuers that meet the following criteria: at least $150 million par value outstanding; maximum credit rating of Ba1; at least one year to maturity; and no issuer represents more than 2% of the index. | |

| | |

| Trust Summary as of December 31, 2023 (continued) | | BlackRock Multi-Sector Opportunities Trust (MSO) |

Performance

Returns for the period ended December 31, 2023 were as follows:

| | | | | | | | | | | | |

| | | Average Annual Total Returns | |

| | | |

| | | | 1 Year | | | | 5 Years | | |

| Since

Inception |

(a) |

| | | |

Trust at NAV(b) | | | 7.40 | % | | | 1.83 | % | | | 0.87 | % |

| | | |

Bloomberg U.S. Corporate High Yield 2% Issuer Capped Index | | | 13.44 | | | | 5.35 | | | | 4.28 | |

| | (a) | MSO commenced operations on February 23, 2018. | |

| | (b) | All returns reflect reinvestment of dividends and/or distributions at NAV on the payable date. Performance results reflect the Trust’s use of leverage, if any. | |

Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles.

Past performance is not an indication of future results.

The Trust is presenting the performance of one or more indices for informational purposes only. The Trust is actively managed and does not seek to track or replicate the performance of any index. The index performance shown is not intended to be indicative of the Trust’s investment strategies, portfolio components or past or future performance.

More information about the Trust’s historical performance can be found in the “Closed End Funds” section of blackrock.com.

The following discussion relates to the Trust’s absolute performance based on NAV:

What factors influenced performance?

Positive contributors to the Trust’s performance during the reporting period included exposures to U.S. high yield corporate bonds, securitized assets including collateralized loan obligations (“CLOs”), emerging market debt, and European corporate credit. The Trust also held private investments that contributed to performance over the period.

The Trust’s duration and yield curve positioning detracted from performance during the period.

The Trust used Treasury futures during the period to hedge duration and yield curve exposure. The use of derivatives did not have a material impact on performance for the period. The Trust’s cash position had no material impact on performance.

Describe recent portfolio activity.

The Trust was positioned defensively over the period as the market had been dealing with persistent inflation and heightened volatility. The Trust held core allocations in U.S. high yield corporate bonds, emerging market debt, structured products including CLOs, and European corporate credit. The Trust maintained an allocation to U.S. high yield corporate credit while remaining cautious within the space and patient in seeking idiosyncratic opportunities given continued performance dispersion across both sectors and quality buckets. Within emerging market debt, the Trust tactically decreased exposure on reduced conviction given less compelling valuations, heightened macro uncertainty, and less favorable technical factors. Within securitized assets, commercial mortgage-backed security holdings were reduced due to a more cautious view on fundamentals, in favor of select, top-of-the-capital structure CLOs with strong levels of protection.

Describe portfolio positioning at period end.

As of December 31, 2023, the Trust’s portfolio had an effective duration of 0.43 years with zero leverage and a nominal yield of 6.29%. The Trust maintained a diversified exposure within spread sectors, including emerging markets, high yield corporate bonds, and securitized assets.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| 6 | | 2 0 2 3 BLACK ROCK ANNUAL REPORT TO SHAREHOLDERS |

| | |

| Trust Summary as of December 31, 2023 (continued) | | BlackRock Multi-Sector Opportunities Trust (MSO) |

Overview of the Trust’s Total Investments

PORTFOLIO COMPOSITION

| | | | |

| | |

| Asset Type | | Percentage of

Total Investments | |

| |

Short-Term Securities | | | 65.7 | % |

Corporate Bonds | | | 20.2 | |

Asset-Backed Securities | | | 7.7 | |

Non-Agency Mortgage-Backed Securities | | | 2.0 | |

Foreign Agency Obligations | | | 1.7 | |

Floating Rate Loan Interests | | | 1.1 | |

Other* | | | 1.6 | |

CREDIT QUALITY ALLOCATION

| | | | |

| | |

| Credit Rating(a)(b) | | Percentage of

Total Investments | |

| |

AAA/Aaa(c) | | | 1.5 | % |

A | | | 0.6 | |

BBB/Baa | | | 16.9 | |

BB/Ba | | | 45.2 | |

B | | | 17.2 | |

CCC/Caa | | | 1.5 | |

CC | | | 0.4 | |

N/R | | | 16.7 | |

| (a) | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P Global Ratings or Moody’s Investors Service, Inc. if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| (b) | Excludes short-term securities. |

| (c) | Includes U.S. Government Sponsored Agency Securities which are deemed AAA/Aaa by the investment adviser. |

| * | Includes one or more investment categories that individually represents less than 1.0% of the Trust’s total investments. Please refer to the Schedule of Investments for details. |

| | |

Schedule of Investments December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) (Percentages shown are based on Net Assets) |

| | | | | | | | | | | | |

| Security | | | | | Par (000) | | | Value | |

| | | |

Asset-Backed Securities | | | | | | | | | | | | |

BankAmerica Manufactured Housing Contract Trust, Series 1997-2, Class B1, 7.07%, 02/10/22(a) | | | USD | | | | 2,300 | | | $ | 480,480 | |

CarVal CLO II Ltd., Series 2019-1A, Class DR, (3-mo. CME Term SOFR + 3.46%), 8.88%, 04/20/32(a)(b) | | | | | | | 250 | | | | 240,966 | |

Cedar Funding XIV CLO Ltd.(a)(b) | | | | | | | | | | | | |

Series 2021-14A, Class D, (3-mo. CME Term SOFR + 3.51%), 8.91%, 07/15/33 | | | | | | | 1,000 | | | | 980,329 | |

Series 2021-14A, Class E, (3-mo. CME Term SOFR + 6.60%), 12.00%, 07/15/33 | | | | | | | 750 | | | | 706,717 | |

Series 2021-14A, Class SUB, 0.00%, 07/15/33 | | | | | | | 750 | | | | 360,225 | |

Deer Creek CLO Ltd., Series 2017-1A, Class E, (3- mo. CME Term SOFR + 6.61%), 12.03%, 10/20/30(a)(b) | | | | | | | 1,000 | | | | 981,818 | |

Fairstone Financial Issuance Trust I, Series 2020-1A, Class D, 6.87%, 10/20/39(b) | | | CAD | | | | 210 | | | | 147,324 | |

Gilbert Park CLO Ltd., Series 2017-1A, Class D, (3-mo. CME Term SOFR + 3.21%), 8.61%, 10/15/30(a)(b) | | | USD | | | | 550 | | | | 536,870 | |

GoldenTree Loan Management U.S. CLO Ltd., Series 2017-2A, Class E, (3-mo. CME Term SOFR + 4.96%),

10.38%, 11/28/30(a)(b) | | | | | | | 1,500 | | | | 1,424,475 | |

GoldenTree Loan Opportunities IX Ltd., Series 2014- 9A, Class ER2, (3-mo. CME Term SOFR + 5.92%),

11.31%, 10/29/29(a)(b) | | | | | | | 500 | | | | 495,398 | |

Lending Funding Trust, Series 2020-2A, Class D, 6.77%, 04/21/31(b) | | | | | | | 315 | | | | 286,356 | |

Madison Park Funding XXX Ltd.(a) | | | | | | | | | | | | |

Series 2018-30A, Class E, (3-mo. CME Term SOFR + 5.21%), 10.61%, 04/15/29(b) | | | | | | | 1,250 | | | | 1,197,881 | |

Series 2018-30X, Class E, (3-mo. CME Term SOFR + 5.21%), 10.61%, 04/15/29 | | | | | | | 250 | | | | 239,576 | |

Mosaic Solar Loan Trust, Series 2018-2GS, Class C, 5.97%, 02/22/44(b) | | | | | | | 197 | | | | 167,441 | |

OCP CLO Ltd., Series 2013-4A, Class CRR, (3-mo. CME Term SOFR + 3.26%), 8.66%, 04/24/29(a)(b) | | | | | | | 600 | | | | 594,826 | |

Palmer Square CLO Ltd.(a)(b) | | | | | | | | | | | | |

Series 2015-2A, Class CR2, (3-mo. CME Term SOFR + 3.01%), 8.43%, 07/20/30 | | | | | | | 250 | | | | 248,460 | |

Series 2018-2A, Class D, (3-mo. CME Term SOFR + 5.86%), 11.26%, 07/16/31 | | | | | | | 1,500 | | | | 1,469,501 | |

Republic Finance Issuance Trust, Series 2020-A, Class D, 7.00%, 11/20/30(b) | | | | | | | 700 | | | | 653,760 | |

Strata CLO I Ltd.(a)(b) | | | | | | | | | | | | |

Series 2018-1A, Class E, (3-mo. CME Term SOFR + 7.34%), 12.74%, 01/15/31 | | | | | | | 500 | | | | 500,794 | |

Series 2018-1A, Class USUB, 0.00%, 01/15/2118 | | | | | | | 1,750 | | | | 875,368 | |

| | | | | | | | |

| | |

Total Asset-Backed Securities — 7.6%

(Cost: $15,620,486) | | | | | | | | 12,588,565 | |

| | | | | | | | |

| | | |

| | | | | | Shares | | | | |

| | | |

Common Stocks | | | | | | | | | | | | |

| | | |

| Oil, Gas & Consumable Fuels — 0.7% | | | | | | | | | |

California Resources Corp.(c) | | | | | | | 19,725 | | | | 1,078,563 | |

| | | | | | | | |

| | | | | | | | | | | | |

| Security | | | | | Shares | | | Value | |

| | |

| Real Estate Management & Development — 0.0% | | | | | | | |

ADLER Group SA | | | | | | | 3,319 | | | $ | 1,877 | |

| | | | | | | | |

| | |

Total Common Stocks — 0.7%

(Cost: $340,930) | | | | | | | | 1,080,440 | |

| | | | | | | | |

| | | |

| | | | | | Par

(000) | | | | |

| | | |

Corporate Bonds | | | | | | | | | | | | |

| | | |

| Automobile Components — 0.2% | | | | | | | | | |

Clarios Global LP/Clarios U.S. Finance Co., 6.25%, 05/15/26(b) | | | USD | | | | 71 | | | | 71,092 | |

Forvia SE, 3.75%, 06/15/28(d) | | | EUR | | | | 200 | | | | 216,074 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 287,166 | |

| | | |

| Automobiles(d) — 0.3% | | | | | | | | | |

RCI Banque SA | | | | | | | | | | | | |

4.63%, 07/13/26 | | | | | | | 75 | | | | 84,607 | |

(5-year EUR Swap + 2.85%), 2.63%, 02/18/30(a) | | | | | | | 400 | | | | 427,008 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 511,615 | |

| | | |

| Banks — 0.7% | | | | | | | | | |

Banco BPM SpA, (5-year EUR Swap + 3.40%), 3.38%, 01/19/32(a)(d) | | | | | | | 200 | | | | 208,479 | |

Banco Votorantim SA, 4.50%, 09/24/24(d) | | | USD | | | | 207 | | | | 203,390 | |

Cooperatieve Rabobank UA, (3-mo. EURIBOR + 1.15%), 4.23%, 04/25/29(a)(d) | | | EUR | | | | 100 | | | | 113,574 | |

Intesa Sanpaolo SpA, 5.15%, 06/10/30(d) | | | GBP | | | | 250 | | | | 288,121 | |

Phoenix PIB Dutch Finance BV, 2.38%, 08/05/25(d) | | | EUR | | | | 100 | | | | 107,254 | |

UniCredit SpA, (5-year USD ICE Swap + 4.91%), 7.30%, 04/02/34(a)(b) | | | USD | | | | 200 | | | | 205,617 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 1,126,435 | |

| | | |

| Capital Markets — 0.3% | | | | | | | | | |

SURA Asset Management SA, 4.88%, 04/17/24(d) | | | | | | | 417 | | | | 413,276 | |

| | | | | | | | |

| | | |

| Chemicals — 1.0% | | | | | | | | | |

Braskem Netherlands Finance BV, 8.50%, 01/12/31(b) | | | | | | | 245 | | | | 228,462 | |

Chemours Co., 4.00%, 05/15/26 | | | EUR | | | | 100 | | | | 108,325 | |

Kronos International, Inc., 3.75%, 09/15/25(d) | | | | | | | 100 | | | | 105,510 | |

NOVA Chemicals Corp., 4.88%, 06/01/24(b) | | | USD | | | | 661 | | | | 655,223 | |

OCI NV, 3.63%, 10/15/25(d) | | | EUR | | | | 90 | | | | 98,365 | |

Olympus Water U.S. Holding Corp., 9.63%, 11/15/28(d) | | | | | | | 100 | | | | 118,123 | |

Sasol Financing USA LLC, 4.38%, 09/18/26 | | | USD | | | | 200 | | | | 186,000 | |

SCIL IV LLC/SCIL USA Holdings LLC, 9.50%, 07/15/28(d) | | | EUR | | | | 100 | | | | 117,571 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 1,617,579 | |

| | | |

| Commercial Services & Supplies — 0.4% | | | | | | | | | |

Allied Universal Holdco LLC/Allied Universal Finance Corp./Atlas Luxco 4 SARL, 3.63%, 06/01/28(d) | | | | | | | 120 | | | | 116,064 | |

AMN Healthcare, Inc., 4.63%, 10/01/27(b) | | | USD | | | | 210 | | | | 198,713 | |

DAE Funding LLC, 1.55%, 08/01/24(d) | | | | | | | 212 | | | | 206,038 | |

Q-Park Holding I BV, 1.50%, 03/01/25(d) | | | EUR | | | | 100 | | | | 107,940 | |

Techem Verwaltungsgesellschaft 675 mbH, 2.00%, 07/15/25(d) | | | | | | | 100 | | | | 107,788 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 736,543 | |

| | | |

| Construction Materials — 0.4% | | | | | | | | | |

Cemex SAB de CV, 3.13%, 03/19/26(d) | | | | | | | 300 | | | | 324,237 | |

Emerald Debt Merger Sub LLC, 6.38%, 12/15/30(d) | | | | | | | 100 | | | | 117,907 | |

| | |

| 8 | | 2 0 2 3 BLACK ROCK ANNUAL REPORT TO SHAREHOLDERS |

| | |

Schedule of Investments (continued) December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) (Percentages shown are based on Net Assets) |

| | | | | | | | | | | | |

| Security | | | | | Par

(000) | | | Value | |

| | | |

Construction Materials (continued) | | | | | | | | | | | | |

HT Troplast GmbH, 9.38%, 07/15/28 | | | EUR | | | | 100 | | | $ | 111,981 | |

OPENLANE, Inc., 5.13%, 06/01/25(b) | | | USD | | | | 97 | | | | 95,303 | |

Standard Industries, Inc./New Jersey, 4.75%, 01/15/28(b) | | | | | | | 46 | | | | 44,284 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 693,712 | |

| | | |

| Consumer Discretionary — 0.1% | | | | | | | | | |

Techem Verwaltungsgesellschaft 674 mbH, 6.00%, 07/30/26(d) | | | EUR | | | | 88 | | | | 96,574 | |

| | | | | | | | |

| | | |

| Consumer Finance — 0.4% | | | | | | | | | |

Ford Motor Credit Co. LLC, 5.58%, 03/18/24 | | | USD | | | | 612 | | | | 611,163 | |

Worldline SA/France, 0.00%, 07/30/25(d)(e)(f) | | | EUR | | | | 19 | | | | 22,586 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 633,749 | |

| | |

| Consumer Staples Distribution & Retail(d) — 0.2% | | | | | | | |

Bellis Acquisition Co. PLC, 3.25%, 02/16/26 | | | GBP | | | | 200 | | | | 236,043 | |

Premier Foods Finance PLC, 3.50%, 10/15/26 | | | | | | | 100 | | | | 118,326 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 354,369 | |

| | | |

| Containers & Packaging — 0.7% | | | | | | | | | |

Ardagh Metal Packaging Finance USA LLC/Ardagh Metal Packaging Finance PLC, 2.00%, 09/01/28(d) | | | EUR | | | | 200 | | | | 195,496 | |

Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc., 2.13%, 08/15/26(d) | | | | | | | 100 | | | | 98,120 | |

Mauser Packaging Solutions Holding Co., 7.88%, 08/15/26(b) | | | USD | | | | 160 | | | | 162,829 | |

OI European Group BV, 2.88%, 02/15/25(d) | | | EUR | | | | 260 | | | | 283,382 | |

Trivium Packaging Finance BV, 5.50%, 08/15/26(b) | | | USD | | | | 446 | | | | 437,574 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 1,177,401 | |

| | | |

| Diversified REITs(b) — 1.2% | | | | | | | | | |

VICI Properties LP/VICI Note Co., Inc. | | | | | | | | | | | | |

5.63%, 05/01/24 | | | | | | | 1,895 | | | | 1,888,833 | |

4.63%, 06/15/25 | | | | | | | 123 | | | | 120,817 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 2,009,650 | |

| | |

| Diversified Telecommunication Services(d) — 0.4% | | | | | | | |

Cellnex Telecom SA | | | | | | | | | | | | |

1.00%, 04/20/27 | | | EUR | | | | 200 | | | | 203,710 | |

Series CLNX, 0.75%, 11/20/31(e) | | | | | | | 200 | | | | 183,708 | |

Global Switch Holdings Ltd., 2.25%, 05/31/27 | | | | | | | 100 | | | | 107,295 | |

SoftBank Group Corp., 3.88%, 07/06/32 | | | | | | | 100 | | | | 94,150 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 588,863 | |

| | | |

| Electric Utilities — 0.4% | | | | | | | | | |

Diamond II Ltd., 7.95%, 07/28/26(b) | | | USD | | | | 200 | | | | 200,750 | |

EDP - Energias de Portugal SA, (5-year EUR Swap + 1.84%), 1.70%, 07/20/80(a)(d) | | | EUR | | | | 400 | | | | 421,647 | |

Electricite de France SA, (12-year EUR Swap + 3.04%), 5.00%(a)(d)(g) | | | | | | | 100 | | | | 110,021 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 732,418 | |

|

| Electronic Equipment, Instruments & Components — 0.1% | |

Belden, Inc., 3.88%, 03/15/28(d) | | | | | | | 200 | | | | 214,166 | |

| | | | | | | | |

| | | |

| Energy Equipment & Services — 0.0% | | | | | | | | | |

Vallourec SACA, 8.50%, 06/30/26(d) | | | | | | | 42 | | | | 46,592 | |

| | | | | | | | |

| |

| Environmental, Maintenance & Security Service — 0.0% | | | | |

Covanta Holding Corp., 4.88%, 12/01/29(b) | | | USD | | | | 22 | | | | 19,221 | |

| | | | | | | | |

| | | |

| Financial Services — 0.4% | | | | | | | | | |

Intrum AB, 4.88%, 08/15/25(d) | | | EUR | | | | 100 | | | | 102,943 | |

| | | | | | | | | | | | |

| Security | | | | | Par

(000) | | | Value | |

| | | |

| Financial Services (continued) | | | | | | | | | |

Nationstar Mortgage Holdings, Inc., 6.00%, 01/15/27(b) | | | USD | | | | 24 | | | $ | 23,820 | |

Rocket Mortgage LLC/Rocket Mortgage Co-Issuer, Inc., 2.88%, 10/15/26(b) | | | | | | | 179 | | | | 165,128 | |

United Wholesale Mortgage LLC, 5.75%, 06/15/27(b) | | | | | | | 374 | | | | 366,561 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 658,452 | |

| | | |

| Gas Utilities — 0.1% | | | | | | | | | |

UGI International LLC, 2.50%, 12/01/29(d) | | | EUR | | | | 100 | | | | 93,572 | |

| | | | | | | | |

| | | |

| Health Care Providers & Services — 0.5% | | | | | | | | | |

Select Medical Corp., 6.25%, 08/15/26(b) | | | USD | | | | 780 | | | | 783,880 | |

| | | | | | | | |

| | | |

| Hotel & Resort REITs — 0.1% | | | | | | | | | |

Service Properties Trust, 7.50%, 09/15/25 | | | | | | | 69 | | | | 69,767 | |

XHR LP, 6.38%, 08/15/25(b) | | | | | | | 148 | | | | 147,625 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 217,392 | |

| | | |

| Hotels, Restaurants & Leisure — 1.7% | | | | | | | | | |

Affinity Interactive, 6.88%, 12/15/27(b) | | | | | | | 367 | | | | 327,083 | |

Caesars Entertainment, Inc.(b) | | | | | | | | | | | | |

6.25%, 07/01/25 | | | | | | | 486 | | | | 487,321 | |

8.13%, 07/01/27 | | | | | | | 314 | | | | 321,881 | |

Carnival Corp., 7.63%, 03/01/26(d) | | | EUR | | | | 100 | | | | 111,941 | |

Cedar Fair LP/Canada’s Wonderland Co./Magnum Management Corp./Millennium Op, 5.50%, 05/01/25(b) | | | USD | | | | 220 | | | | 218,894 | |

Churchill Downs, Inc., 5.75%, 04/01/30(b) | | | | | | | 9 | | | | 8,775 | |

Cirsa Finance International SARL, 4.75%, 05/22/25(d) | | | EUR | | | | 100 | | | | 110,174 | |

Dave & Buster’s, Inc., Series B, 7.63%, 11/01/25(b) | | | USD | | | | 35 | | | | 35,438 | |

Food Service Project SA, 5.50%, 01/21/27(d) | | | EUR | | | | 100 | | | | 110,034 | |

Full House Resorts, Inc., 8.25%, 02/15/28(b) | | | USD | | | | 29 | | | | 27,260 | |

IRB Holding Corp., 7.00%, 06/15/25(b) | | | | | | | 151 | | | | 151,000 | |

Lottomatica SpA/Roma, (3-mo. EURIBOR + 4.13%), 8.10%, 06/01/28(a)(d) | | | EUR | | | | 109 | | | | 121,395 | |

SeaWorld Parks & Entertainment, Inc., 8.75%, 05/01/25(b) | | | USD | | | | 669 | | | | 672,345 | |

Travel & Leisure Co., 6.63%, 07/31/26(b) | | | | | | | 189 | | | | 190,655 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 2,894,196 | |

| | | |

| Household Durables — 3.0% | | | | | | | | | |

Ashton Woods USA LLC/Ashton Woods Finance Co.(b) | | | | | | | | |

Series B, 6.63%, 01/15/28 | | | | | | | 495 | | | | 480,366 | |

Series B, 4.63%, 08/01/29 | | | | | | | 66 | | | | 58,691 | |

Brookfield Residential Properties, Inc./Brookfield Residential U.S. LLC(b) | | | | | | | | | | | | |

6.25%, 09/15/27 | | | | | | | 541 | | | | 524,168 | |

5.00%, 06/15/29 | | | | | | | 27 | | | | 23,966 | |

Century Communities, Inc., 6.75%, 06/01/27 | | | | | | | 27 | | | | 27,291 | |

Forestar Group, Inc.(b) | | | | | | | | | | | | |

3.85%, 05/15/26 | | | | | | | 560 | | | | 533,442 | |

5.00%, 03/01/28 | | | | | | | 669 | | | | 643,584 | |

Taylor Morrison Communities, Inc.(b) | | | | | | | | | | | | |

5.88%, 06/15/27 | | | | | | | 647 | | | | 650,235 | |

5.75%, 01/15/28 | | | | | | | 1,500 | | | | 1,506,881 | |

Tri Pointe Homes, Inc. | | | | | | | | | | | | |

5.25%, 06/01/27 | | | | | | | 505 | | | | 496,162 | |

5.70%, 06/15/28 | | | | | | | 38 | | | | 37,478 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 4,982,264 | |

| | |

SCHEDULE OF INVESTMENTS | | 9 |

| | |

Schedule of Investments (continued) December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) (Percentages shown are based on Net Assets) |

| | | | | | | | | | | | |

| Security | | | | | Par

(000) | | | Value | |

| | | |

Insurance — 0.2% | | | | | | | | | | | | |

Galaxy Bidco Ltd., 6.50%, 07/31/26(d) | | | GBP | | | | 220 | | | $ | 270,608 | |

| | | | | | | | |

| | | |

| Internet Software & Services — 0.1% | | | | | | | | | |

Gen Digital, Inc., 6.75%, 09/30/27(b) | | | USD | | | | 120 | | | | 122,079 | |

| | | | | | | | |

| | | |

| IT Services(d) — 0.2% | | | | | | | | | |

Engineering - Ingegneria Informatica - SpA, 11.13%, 05/15/28 | | | EUR | | | | 100 | | | | 117,844 | |

La Financiere Atalian SASU, 6.63%, 05/15/25 | | | GBP | | | | 200 | | | | 186,077 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 303,921 | |

| | | |

| Machinery(d) — 0.3% | | | | | | | | | |

Loxam SAS, 3.75%, 07/15/26 | | | EUR | | | | 200 | | | | 217,931 | |

Renk AG/Frankfurt am Main, 5.75%, 07/15/25 | | | | | | | 200 | | | | 219,146 | |

TK Elevator Midco GmbH, 4.38%, 07/15/27 | | | | | | | 115 | | | | 122,739 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 559,816 | |

| | | |

| Media — 1.1% | | | | | | | | | |

Altice Financing SA, 2.25%, 01/15/25(d) | | | | | | | 116 | | | | 124,232 | |

Clear Channel Outdoor Holdings, Inc., 5.13%, 08/15/27(b) | | | USD | | | | 738 | | | | 704,485 | |

Nexstar Media, Inc., 5.63%, 07/15/27(b) | | | | | | | 733 | | | | 708,775 | |

Pinewood Finance Co. Ltd., 3.25%, 09/30/25(d) | | | GBP | | | | 100 | | | | 123,570 | |

Sirius XM Radio, Inc., 5.00%, 08/01/27(b) | | | USD | | | | 70 | | | | 67,620 | |

Tele Columbus AG, 3.88%, 05/02/25(d) | | | EUR | | | | 100 | | | | 69,880 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 1,798,562 | |

| | | |

| Metals & Mining — 0.5% | | | | | | | | | |

Metinvest BV(d) | | | | | | | | | | | | |

8.50%, 04/23/26 | | | USD | | | | 296 | | | | 205,720 | |

7.65%, 10/01/27 | | | | | | | 400 | | | | 256,000 | |

POSCO, 5.63%, 01/17/26(b) | | | | | | | 200 | | | | 201,634 | |

Vedanta Resources Finance II PLC, 8.95%, 03/11/25(b) | | | | | | | 320 | | | | 237,165 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 900,519 | |

| | | |

| Oil, Gas & Consumable Fuels — 2.7% | | | | | | | | | |

California Resources Corp., 7.13%, 02/01/26(b) | | | | | | | 378 | | | | 383,362 | |

Chesapeake Energy Corp., 5.50%, 02/01/26(b) | | | | | | | 110 | | | | 109,047 | |

CrownRock LP/CrownRock Finance, Inc., 5.63%, 10/15/25(b) | | | | | | | 54 | | | | 53,928 | |

Ecopetrol SA, 4.13%, 01/16/25 | | | | | | | 440 | | | | 428,175 | |

Geopark Ltd., 5.50%, 01/17/27(b) | | | | | | | 205 | | | | 180,582 | |

Permian Resources Operating LLC(b) | | | | | | | | | | | | |

5.38%, 01/15/26 | | | | | | | 1,841 | | | | 1,816,484 | |

6.88%, 04/01/27 | | | | | | | 127 | | | | 126,913 | |

Petroleos Mexicanos | | | | | | | | | | | | |

3.75%, 02/21/24(d) | | | EUR | | | | 190 | | | | 208,545 | |

4.25%, 01/15/25 | | | USD | | | | 209 | | | | 202,599 | |

6.50%, 03/13/27 | | | | | | | 703 | | | | 653,351 | |

SM Energy Co., 6.75%, 09/15/26 | | | | | | | 341 | | | | 340,112 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 4,503,098 | |

| | | |

| Paper & Forest Products — 0.1% | | | | | | | | | |

Ahlstrom-Munksjo Holding 3 Oy, 3.63%, 02/04/28(d) | | | EUR | | | | 100 | | | | 99,631 | |

| | | | | | | | |

| | | |

| Passenger Airlines — 0.0% | | | | | | | | | |

Allegiant Travel Co., 7.25%, 08/15/27(b) | | | USD | | | | 56 | | | | 54,793 | |

| | | | | | | | |

| | | |

| Pharmaceuticals — 0.5% | | | | | | | | | |

Cheplapharm Arzneimittel GmbH, 4.38%, 01/15/28(d) | | | EUR | | | | 331 | | | | 355,428 | |

Gruenenthal GmbH, 3.63%, 11/15/26(d) | | | | | | | 200 | | | | 217,534 | |

| | | | | | | | | | | | |

| Security | | | | | Par

(000) | | | Value | |

| | | |

Pharmaceuticals (continued) | | | | | | | | | | | | |

Teva Pharmaceutical Finance Netherlands II BV | | | | | | | | | | | | |

7.38%, 09/15/29 | | | EUR | | | | 101 | | | $ | 121,780 | |

4.38%, 05/09/30 | | | | | | | 100 | | | | 103,478 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 798,220 | |

| |

| Real Estate Management & Development — 1.0% | | | | |

Agps Bondco PLC, 5.50%, 11/13/26(d)(h)(i) | | | | | | | 100 | | | | 38,086 | |

Five Point Operating Co. LP/Five Point Capital Corp., Series C, 7.88%, 11/15/25(b) | | | USD | | | | 750 | | | | 742,500 | |

Howard Hughes Corp., 5.38%, 08/01/28(b) | | | | | | | 981 | | | | 942,864 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 1,723,450 | |

| | | |

| Software — 0.2% | | | | | | | | | |

Cedacri Mergeco SpA, (3-mo. EURIBOR + 5.50%), 9.50%, 05/15/28(a)(d) | | | EUR | | | | 100 | | | | 108,739 | |

Cloud Software Group, Inc., 6.50%, 03/31/29(b) | | | USD | | | | 239 | | | | 227,633 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 336,372 | |

| | |

| Wireless Telecommunication Services — 0.4% | | | | | | | |

Altice France SA/France(d) | | | | | | | | | | | | |

2.50%, 01/15/25 | | | EUR | | | | 141 | | | | 149,577 | |

5.88%, 02/01/27 | | | | | | | 100 | | | | 98,034 | |

Cellnex Finance Co. SA, 2.00%, 02/15/33(d) | | | | | | | 100 | | | | 93,987 | |

Kenbourne Invest SA, 6.88%, 11/26/24(b) | | | USD | | | | 249 | | | | 172,355 | |

Vmed O2 U.K. Financing I PLC, 3.25%, 01/31/31(d) | | | EUR | | | | 133 | | | | 134,712 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 648,665 | |

| | | | | | | | |

| | |

Total Corporate Bonds — 19.9%

(Cost: $33,943,438) | | | | | | | | 33,008,819 | |

| | | | | | | | |

| | | |

Floating Rate Loan Interests(a) | | | | | | | | | | | | |

|

Commercial Services & Supplies — 0.6% | |

Interface Security Systems LLC, Term Loan, (1-mo. CME Term SOFR at 1.75% Floor + 7.00%, 1.00% PIK),

13.43%, 08/07/24(h)(i)(j)(k) | | | USD | | | | 1,326 | | | | 984,427 | |

| | | | | | | | |

| | | |

| Financial Services — 0.5% | | | | | | | | | |

Colorado Plaza, Term Loan,

05/15/24(h)(i)(j)(l) | | | | | | | 4,118 | | | | 818,763 | |

| | | | | | | | |

| | | |

| Passenger Airlines — 0.0% | | | | | | | | | |

WestJet Airlines Ltd., Term Loan B, 12/11/26(l) | | | | | | | — | (m) | | | 408 | |

| | | | | | | | |

| | |

Total Floating Rate Loan Interests — 1.1%

(Cost: $5,440,682) | | | | | | | | 1,803,598 | |

| | | | | | | | |

| | | |

Foreign Agency Obligations | | | | | | | | | | | | |

| | | |

Bahrain — 0.2% | | | | | | | | | | | | |

Bahrain Government International Bond, 7.00%, 01/26/26(d) | | | | | | | 295 | | | | 300,439 | |

| | | | | | | | |

| | | |

| Colombia — 0.6% | | | | | | | | | |

Colombia Government International Bond | | | | | | | | | | | | |

4.50%, 01/28/26 | | | | | | | 411 | | | | 402,780 | |

3.88%, 04/25/27 | | | | | | | 573 | | | | 545,962 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 948,742 | |

| | | |

| Dominican Republic — 0.4% | | | | | | | | | |

Dominican Republic International Bond(d) | | | | | | | | | | | | |

6.88%, 01/29/26 | | | | | | | 279 | | | | 283,659 | |

5.95%, 01/25/27 | | | | | | | 379 | | | | 379,789 | |

| | | | | | | | |

| | | |

| | | | | | | | | | | 663,448 | |

| | |

| 10 | | 2 0 2 3 BLACK ROCK ANNUAL REPORT TO SHAREHOLDERS |

| | |

Schedule of Investments (continued) December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) (Percentages shown are based on Net Assets) |

| | | | | | | | | | | | |

| Security | | Par (000) | | | Value | |

| |

| | | |

Hungary — 0.0% | | | | | | | | | | | | |

Hungary Government International Bond, 5.38%, 03/25/24 | | | USD | | | | 56 | | | $ | 55,986 | |

| | | | | | | | | | | | |

| | | |

| Jordan — 0.1% | | | | | | | | | |

Jordan Government International Bond, 4.95%, 07/07/25(d) | | | | | | | 200 | | | | 195,375 | |

| | | | | | | | | | | | |

| | | |

| Morocco — 0.1% | | | | | | | | | |

Morocco Government International Bond, 2.38%, 12/15/27(b) | | | | | | | 217 | | | | 194,079 | |

| | | | | | | | | | | | |

| | | |

| Oman — 0.1% | | | | | | | | | |

Oman Sovereign Sukuk Co., 4.40%, 06/01/24(d) | | | | | | | 205 | | | | 203,398 | |

| | | | | | | | | | | | |

| | | |

| Romania — 0.1% | | | | | | | | | |

Romanian Government International Bond, 5.25%, 11/25/27(b) | | | | | | | 202 | | | | 200,164 | |

| | | | | | | | | | | | |

| | | |

| Ukraine — 0.1% | | | | | | | | | |

Ukraine Government International Bond, 8.99%, 02/01/26(d)(h)(i) | | | | | | | 243 | | | | 71,199 | |

| | | | | | | | | | | | |

| | | |

Total Foreign Agency Obligations — 1.7%

(Cost: $2,989,661) | | | | | | | | | | | 2,832,830 | |

| | | | | | | | | | | | |

| | | |

Municipal Bonds | | | | | | | | | | | | |

| | | |

| Puerto Rico(a) — 0.2% | | | | | | | | | |

Commonwealth of Puerto Rico, GO 0.00%, 11/01/51 | | | | | | | 532 | | | | 217,331 | |

Series A-1, 0.00%, 11/01/43 | | | | | | | 47 | | | | 25,407 | |

Commonwealth of Puerto Rico, RB, 0.00%, 11/01/51 | | | | | | | 227 | | | | 79,344 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | 322,082 | |

| | | | | | | | | | | | |

| | | |

Total Municipal Bonds — 0.2%

(Cost: $338,291) | | | | | | | | | | | 322,082 | |

| | | | | | | | | | | | |

|

Non-Agency Mortgage-Backed Securities | |

|

| Collateralized Mortgage Obligations(a)(b) — 1.7% | |

BCAP LLC Trust, Series 2012-RR3, Class 1A5, 5.28%, 12/26/37 | | | | | | | 951 | | | | 742,017 | |

Cascade Funding Mortgage Trust, Series 2019-RM3, Class C, 4.00%, 06/25/69 | | | | | | | 2,250 | | | | 2,055,282 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | 2,797,299 | |

|

| Commercial Mortgage-Backed Securities(b) — 0.3% | |

Morgan Stanley Capital I Trust, Series 2018-MP, Class E, 4.28%, 07/11/40(a) | | | | | | | 551 | | | | 329,134 | |

Velocity Commercial Capital Loan Trust | | | | | | | | | | | | |

Series 2018-1, Class M5, 6.26%, 04/25/48 | | | | | | | 128 | | | | 95,089 | |

Series 2018-1, Class M6, 7.26%, 04/25/48 | | | | | | | 182 | | | | 121,764 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | 545,987 | |

| | | | | | | | | | | | |

| |

Total Non-Agency Mortgage-Backed Securities — 2.0%

(Cost: $3,876,645) | | | | 3,343,286 | |

| | | | | | | | | | | | |

| | | |

Preferred Securities | | | | | | | | | | | | |

| | | |

| Capital Trusts — 0.2%(a)(d)(g) | | | | | | | | | |

| | | |

| Banks — 0.0% | | | | | | | | | |

HSBC Bank Capital Funding Sterling 1 LP, Series 1, 5.84% | | | GBP | | | | 20 | | | | 26,513 | |

| | | | | | | | | | | | |

|

| Diversified Telecommunication Services — 0.1% | |

Koninklijke KPN NV, 2.00% | | | EUR | | | | 100 | | | | 107,039 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Security | | Par (000) | | | Value | |

| |

| | | |

| Electric Utilities — 0.1% | | | | | | | | | |

Naturgy Finance BV, 2.37% | | | EUR | | | | 100 | | | $ | 100,459 | |

| | | | | | | | | | | | |

|

| Real Estate Management & Development — 0.0% | |

Heimstaden Bostad AB, 2.63% | | | | | | | 100 | | | | 37,038 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | 271,049 | |

| | | | | | | | | | | | |

| | |

Total Preferred Securities — 0.2%

(Cost: $360,970) | | | | | | | | 271,049 | |

| | | | | | | | | | | | |

|

U.S. Government Sponsored Agency Securities | |

|

| Mortgage-Backed Securities — 0.5% | |

Uniform Mortgage-Backed Securities, 3.50%, 01/16/54(n) | | | USD | | | | 900 | | | | 825,609 | |

| | | | | | | | | | | | |

| |

Total U.S. Government Sponsored Agency

Securities — 0.5%

(Cost: $783,602) | | | | 825,609 | |

| | | | | | | | | | | | |

| | |

Total Long-Term Investments — 33.9%

(Cost: $63,694,705) | | | | | | | | 56,076,278 | |

| | | | | | | | | | | | |

| | | |

Short-Term Securities | | | | | | | | | | | | |

| | | |

| Commercial Paper — 0.5% | | | | | | | | | |

AT&T, Inc., 5.93%, 02/21/24(o) | | | | | | | 590 | | | | 585,078 | |

Societe Generale SA, 5.70%, 03/06/24(o) | | | | | | | 250 | | | | 247,406 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | | | | | 832,484 | |

| | | | | | | | | | | | |

| | | |

| | | | | | Shares | | | | |

| |

| | | |

| Money Market Funds — 64.3% | | | | | | | | | |

BlackRock Liquidity Funds, T-Fund, Institutional Class, 5.26%(p)(q) | | | | | | | 106,485,015 | | | | 106,485,015 | |

| | | | | | | | | | | | |

| | |

Total Short-Term Securities — 64.8%

(Cost: $107,318,031) | | | | | | | | 107,317,499 | |

| | | | | | | | | | | | |

| |

Total Investments Before TBA Sale

Commitments — 98.7%

(Cost: $171,012,736) | | | | 163,393,777 | |

| | | | | | | | | | | | |

| | | |

| | | | | | Par (000) | | | | |

| |

| | | |

TBA Sale Commitments | | | | | | | | | | | | |

|

| Mortgage-Backed Securities — (0.5)% | |

Uniform Mortgage-Backed Securities, 3.50%, 01/16/54(n) | | | USD | | | | (900 | ) | | | (825,609 | ) |

| | | | | | | | | | | | |

| |

Total TBA Sale Commitments — (0.5)%

(Proceeds: $(789,917)) | | | | (825,609 | ) |

| | | | | | | | | | | | |

| |

Total Investments, Net of TBA Sale

Commitments — 98.2%

(Cost: $170,222,819) | | | | 162,568,168 | |

| | |

Other Assets Less Liabilities — 1.8% | | | | | | | | 2,966,510 | |

| | | | | | | | | | | | |

| | |

Net Assets — 100.0% | | | | | | | $ | 165,534,678 | |

| | | | | | | | | | | | |

| (a) | Variable rate security. Interest rate resets periodically. The rate shown is the effective interest rate as of period end. Security description also includes the reference rate and spread if published and available. |

| (b) | Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration to qualified institutional investors. |

| (c) | All or a portion of the security has been pledged and/or segregated as collateral in connection with outstanding exchange-traded options written. |

| | |

SCHEDULE OF INVESTMENTS | | 11 |

| | |

Schedule of Investments (continued) December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) |

| (d) | This security may be resold to qualified foreign investors and foreign institutional buyers under Regulation S of the Securities Act of 1933. |

| (e) | Convertible security. |

| (g) | Perpetual security with no stated maturity date. |

| (h) | Issuer filed for bankruptcy and/or is in default. |

| (i) | Non-income producing security. |

| (j) | Security is valued using significant unobservable inputs and is classified as Level 3 in the fair value hierarchy. |

| (k) | Payment-in-kind security which may pay interest/dividends in additional par/shares and/or in cash. Rates shown are the current rate and possible payment rates. |

| (l) | Represents an unsettled loan commitment at period end. Certain details associated with this purchase are not known prior to the settlement date, including coupon rate. |

| (m) | Rounds to less than 1,000. |

| (n) | Represents or includes a TBA transaction. |

| (o) | Rates are discount rates or a range of discount rates as of period end. |

| (p) | Affiliate of the Trust. |

| (q) | Annualized 7-day yield as of period end. |

For Trust compliance purposes, the Trust’s industry classifications refer to one or more of the industry sub-classifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such industry sub-classifications for reporting ease.

Affiliates

Investments in issuers considered to be affiliate(s) of the Trust during the year ended December 31, 2023 for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as amended, were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | Affiliated Issuer | | Value at 12/31/22 | | | Purchases at Cost | | | Proceeds from Sale | | | Net Realized Gain (Loss) | | | | | | Change in Unrealized Appreciation (Depreciation) | | | Value at 12/31/23 | | | Shares Held at 12/31/23 | | | Income | | | Capital Gain Distributions from Underlying Funds | | | | |

| | | | | | | | | | | | |

| | BlackRock Liquidity Funds, T-Fund, Institutional Class | | $ | 8,842,853 | | | $ | 97,642,162 | (a) | | $ | — | | | $ | — | | | | | | | $ | — | | | $ | 106,485,015 | | | | 106,485,015 | | | $ | 1,637,121 | | | $ | — | | | | | |

| | | | | | | | | | | | |

| | iShares iBoxx $ High Yield Corporate Bond ETF(b) | | | 1,656,675 | | | | — | | | | (1,641,157 | ) | | | (146,421 | ) | | | | | | | 130,903 | | | | — | | | | — | | | | 75,042 | | | | — | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | | | | $ | (146,421 | ) | | | | | | $ | 130,903 | | | $ | 106,485,015 | | | | | | | $ | 1,712,163 | | | $ | — | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (a) | Represents net amount purchased (sold). | |

| | (b) | As of period end, the entity is no longer held. | |

Derivative Financial Instruments Outstanding as of Period End

Forward Foreign Currency Exchange Contracts

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| Currency Purchased | | | | | | Currency Sold | | | Counterparty | | Settlement Date | | | Unrealized Appreciation (Depreciation) | |

| | | | | | | |

EUR | | | 18,221 | | | | | | | | USD | | | | 20,121 | | | State Street Bank and Trust Co. | | | 02/22/24 | | | $ | 33 | |

EUR | | | 3,785,000 | | | | | | | | USD | | | | 4,108,712 | | | UBS AG | | | 02/22/24 | | | | 77,966 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | 77,999 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

USD | | | 124,717 | | | | | | | | CAD | | | | 169,000 | | | Deutsche Bank AG | | | 02/22/24 | | | | (2,914 | ) |

USD | �� | | 2,389,584 | | | | | | | | EUR | | | | 2,171,823 | | | HSBC Bank PLC | | | 02/22/24 | | | | (12,721 | ) |

USD | | | 1,998 | | | | | | | | EUR | | | | 1,809 | | | Societe Generale | | | 02/22/24 | | | | (3 | ) |

USD | | | 127,753 | | | | | | | | EUR | | | | 115,682 | | | Societe Generale | | | 02/22/24 | | | | (206 | ) |

USD | | | 205,866 | | | | | | | | EUR | | | | 186,415 | | | Societe Generale | | | 02/22/24 | | | | (332 | ) |

USD | | | 9,533,791 | | | | | | | | EUR | | | | 8,633,000 | | | Societe Generale | | | 02/22/24 | | | | (15,374 | ) |

USD | | | 1,883,718 | | | | | | | | GBP | | | | 1,482,000 | | | Standard Chartered Bank | | | 02/22/24 | | | | (5,812 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | (37,362 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | $ | 40,637 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| 12 | | 2 0 2 3 BLACK ROCK ANNUAL REPORT TO SHAREHOLDERS |

| | |

Schedule of Investments (continued) December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) |

Derivative Financial Instruments Categorized by Risk Exposure

As of period end, the fair values of derivative financial instruments located in the Statement of Assets and Liabilities were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | | Commodity Contracts | | | Credit Contracts | | | Equity Contracts | | | Foreign Currency Exchange Contracts | | | Interest Rate Contracts | | | Other Contracts | | | Total | |

| | | | | | | |

Assets — Derivative Financial Instruments | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Forward foreign currency exchange contracts | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Unrealized appreciation on forward foreign currency exchange contracts | | $ | — | | | $ | — | | | $ | — | | | $ | 77,999 | | | $ | — | | | $ | — | | | $ | 77,999 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Liabilities — Derivative Financial Instruments | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Forward foreign currency exchange contracts | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Unrealized depreciation on forward foreign currency exchange contracts | | $ | — | | | $ | — | | | $ | — | | | $ | 37,362 | | | $ | — | | | $ | — | | | $ | 37,362 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

For the period ended December 31, 2023, the effect of derivative financial instruments in the Statement of Operations was as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | | Commodity

Contracts | | | Credit

Contracts | | | Equity

Contracts | | | Foreign

Currency

Exchange

Contracts | | | Interest

Rate

Contracts | | | Other

Contracts | | | Total | |

| | | | | | | |

Net Realized Gain (Loss) from: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Futures contracts | | $ | — | | | $ | — | | | $ | (672 | ) | | $ | — | | | $ | (366,228 | ) | | $ | — | | | $ | (366,900 | ) |

Forward foreign currency exchange contracts | | | — | | | | — | | | | — | | | | 603,710 | | | | — | | | | — | | | | 603,710 | |

Options purchased(a) | | | — | | | | — | | | | (14,069 | ) | | | — | | | | — | | | | — | | | | (14,069 | ) |

Options written | | | — | | | | — | | | | 6,325 | | | | — | | | | — | | | | — | | | | 6,325 | |

Swaps | | | — | | | | 919,908 | | | | (3,629 | ) | | | — | | | | (1,013,659 | ) | | | — | | | | (97,380 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | $ | — | | | $ | 919,908 | | | $ | (12,045 | ) | | $ | 603,710 | | | $ | (1,379,887 | ) | | $ | — | | | $ | 131,686 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Net Change in Unrealized Appreciation (Depreciation) on: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Futures contracts | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | (165,573 | ) | | $ | — | | | $ | (165,573 | ) |

Forward foreign currency exchange contracts | | | — | | | | — | | | | — | | | | 19,756 | | | | — | | | | — | | | | 19,756 | |

Swaps | | | — | | | | (641,501 | ) | | | 4,626 | | | | — | | | | 851,698 | | | | — | | | | 214,823 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | $ | — | | | $ | (641,501 | ) | | $ | 4,626 | | | $ | 19,756 | | | $ | 686,125 | | | $ | — | | | $ | 69,006 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (a) | Options purchased are included in net realized gain (loss) from investments — unaffiliated. | |

Average Quarterly Balances of Outstanding Derivative Financial Instruments

| | | | |

| | |

Futures contracts: | | | | |

Average notional value of contracts — long | | $ | 32,597,214 | |

Average notional value of contracts — short | | $ | 33,868,483 | |

Forward foreign currency exchange contracts: | | | | |

Average amounts purchased — in USD | | $ | 28,206,875 | |

Average amounts sold — in USD | | $ | 2,057,501 | |

Options: | | | | |

Average value of option contracts purchased | | $ | 1,386 | |

Average value of option contracts written | | $ | 362 | |

Credit default swaps: | | | | |

Average notional value — sell protection | | $ | 23,296,354 | |

Interest rate swaps: | | | | |

Average notional value — pays fixed rate | | $ | 3,730,200 | |

Average notional value — receives fixed rate | | $ | 14,588,808 | |

Total return swaps: | | | | |

Average notional value | | $ | 245,718 | |

For more information about the Trust’s investment risks regarding derivative financial instruments, refer to the Notes to Financial Statements.

| | |

SCHEDULE OF INVESTMENTS | | 13 |

| | |

Schedule of Investments (continued) December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) |

Derivative Financial Instruments — Offsetting as of Period End

The Trust’s derivative assets and liabilities (by type) were as follows:

| | | | | | | | |

| | | |

| | | Assets | | | Liabilities | |

| | |

Derivative Financial Instruments | | | | | | | | |

Forward foreign currency exchange contracts | | $ | 77,999 | | | $ | 37,362 | |

| | | | | | | | |

| | |

Total derivative assets and liabilities in the Statement of Assets and Liabilities | | | 77,999 | | | | 37,362 | |

| | | | | | | | |

| | |

Derivatives not subject to a Master Netting Agreement or similar agreement (“MNA”) | | | — | | | | — | |

| | |

| | | | | | | | |

| | |

Total derivative assets and liabilities subject to an MNA | | $ | 77,999 | | | $ | 37,362 | |

| | | | | | | | |

The following table presents the Trust’s derivative assets and liabilities by counterparty net of amounts available for offset under an MNA and net of the related collateral received and pledged by the Trust:

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Counterparty | |

| Derivative

Assets Subject to an MNA by Counterparty |

| |

| Derivatives

Available for Offset |

(a) | |

| Non-Cash

Collateral Received |

| |

| Cash

Collateral Received |

| |

| Net Amount

of Derivative Assets |

(b)(c) |

| | | | | |

State Street Bank and Trust Co. | | $ | 33 | | | $ | — | | | $ | — | | | $ | — | | | $ | 33 | |

UBS AG | | | 77,966 | | | | — | | | | — | | | | — | | | | 77,966 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | $ | 77,999 | | | $ | — | | | $ | — | | | $ | — | | | $ | 77,999 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Counterparty | |

| Derivative

Liabilities Subject to an MNA by Counterparty |

| |

| Derivatives

Available for Offset |

(a) | |

| Non-Cash

Collateral Pledged |

| |

| Cash

Collateral Pledged |

| |

| Net Amount

of Derivative Liabilities |

(b)(d) |

| | | | | |

Deutsche Bank AG | | $ | 2,914 | | | $ | — | | | $ | — | | | $ | — | | | $ | 2,914 | |

HSBC Bank PLC | | | 12,721 | | | | — | | | | — | | | | — | | | | 12,721 | |

Societe Generale | | | 15,915 | | | | — | | | | — | | | | — | | | | 15,915 | |

Standard Chartered Bank | | | 5,812 | | | | — | | | | — | | | | — | | | | 5,812 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | $ | 37,362 | | | $ | — | | | $ | — | | | $ | — | | | $ | 37,362 | |

| | | | | | | | | | | | | | | | | | | | |

| | (a) | The amount of derivatives available for offset is limited to the amount of derivative asset and/or liabilities that are subject to an MNA. | |

| | (b) | Net amount may also include forward foreign currency exchange contracts that are not required to be collateralized. | |

| | (c) | Net amount represents the net amount receivable from the counterparty in the event of default. | |

| | (d) | Net amount represents the net amount payable due to counterparty in the event of default. | |

Fair Value Hierarchy as of Period End

Various inputs are used in determining the fair value of financial instruments. For a description of the input levels and information about the Trust’s policy regarding valuation of financial instruments, refer to the Notes to Financial Statements.

The following table summarizes the Trust’s financial instruments categorized in the fair value hierarchy. The breakdown of the Trust’s financial instruments into major categories is disclosed in the Schedule of Investments above.

| | | | | | | | | | | | | | | | |

| | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| | | | |

Assets | | | | | | | | | | | | | | | | |

Investments | | | | | | | | | | | | | | | | |

Long-Term Investments | | | | | | | | | | | | | | | | |

Asset-Backed Securities | | $ | — | | | $ | 12,588,565 | | | $ | — | | | $ | 12,588,565 | |

Common Stocks | | | | | | | | | | | | | | | | |

Oil, Gas & Consumable Fuels | | | 1,078,563 | | | | — | | | | — | | | | 1,078,563 | |

Real Estate Management & Development | | | — | | | | 1,877 | | | | — | | | | 1,877 | |

Corporate Bonds | | | | | | | | | | | | | | | | |

Automobile Components | | | — | | | | 287,166 | | | | — | | | | 287,166 | |

Automobiles | | | — | | | | 511,615 | | | | — | | | | 511,615 | |

Banks | | | — | | | | 1,126,435 | | | | — | | | | 1,126,435 | |

Capital Markets | | | — | | | | 413,276 | | | | — | | | | 413,276 | |

Chemicals | | | — | | | | 1,617,579 | | | | — | | | | 1,617,579 | |

Commercial Services & Supplies | | | — | | | | 736,543 | | | | — | | | | 736,543 | |

| | |

| 14 | | 2 0 2 3 BLACK ROCK ANNUAL REPORT TO SHAREHOLDERS |

| | |

Schedule of Investments (continued) December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) |

Fair Value Hierarchy as of Period End (continued)

| | | | | | | | | | | | | | | | |

| | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| | | | |

Corporate Bonds (continued) | | | | | | | | | | | | | | | | |

Construction Materials | | $ | — | | | $ | 693,712 | | | $ | — | | | $ | 693,712 | |

Consumer Discretionary | | | — | | | | 96,574 | | | | — | | | | 96,574 | |

Consumer Finance | | | — | | | | 633,749 | | | | — | | | | 633,749 | |

Consumer Staples Distribution & Retail | | | — | | | | 354,369 | | | | — | | | | 354,369 | |

Containers & Packaging | | | — | | | | 1,177,401 | | | | — | | | | 1,177,401 | |

Diversified REITs | | | — | | | | 2,009,650 | | | | — | | | | 2,009,650 | |

Diversified Telecommunication Services | | | 183,708 | | | | 405,155 | | | | — | | | | 588,863 | |

Electric Utilities | | | — | | | | 732,418 | | | | — | | | | 732,418 | |

Electronic Equipment, Instruments & Components | | | — | | | | 214,166 | | | | — | | | | 214,166 | |

Energy Equipment & Services | | | — | | | | 46,592 | | | | — | | | | 46,592 | |

Environmental, Maintenance & Security Service | | | — | | | | 19,221 | | | | — | | | | 19,221 | |

Financial Services | | | — | | | | 658,452 | | | | — | | | | 658,452 | |

Gas Utilities | | | — | | | | 93,572 | | | | — | | | | 93,572 | |

Health Care Providers & Services | | | — | | | | 783,880 | | | | — | | | | 783,880 | |

Hotel & Resort REITs | | | — | | | | 217,392 | | | | — | | | | 217,392 | |

Hotels, Restaurants & Leisure | | | — | | | | 2,894,196 | | | | — | | | | 2,894,196 | |

Household Durables | | | — | | | | 4,982,264 | | | | — | | | | 4,982,264 | |

Insurance | | | — | | | | 270,608 | | | | — | | | | 270,608 | |

Internet Software & Services | | | — | | | | 122,079 | | | | — | | | | 122,079 | |

IT Services | | | — | | | | 303,921 | | | | — | | | | 303,921 | |

Machinery | | | — | | | | 559,816 | | | | — | | | | 559,816 | |

Media | | | — | | | | 1,798,562 | | | | — | | | | 1,798,562 | |

Metals & Mining | | | — | | | | 900,519 | | | | — | | | | 900,519 | |

Oil, Gas & Consumable Fuels | | | — | | | | 4,503,098 | | | | — | | | | 4,503,098 | |

Paper & Forest Products | | | — | | | | 99,631 | | | | — | | | | 99,631 | |

Passenger Airlines | | | — | | | | 54,793 | | | | — | | | | 54,793 | |

Pharmaceuticals | | | — | | | | 798,220 | | | | — | | | | 798,220 | |

Real Estate Management & Development | | | — | | | | 1,723,450 | | | | — | | | | 1,723,450 | |

Software | | | — | | | | 336,372 | | | | — | | | | 336,372 | |

Wireless Telecommunication Services | | | — | | | | 648,665 | | | | — | | | | 648,665 | |

Floating Rate Loan Interests | | | — | | | | 408 | | | | 1,803,190 | | | | 1,803,598 | |

Foreign Agency Obligations | | | — | | | | 2,832,830 | | | | — | | | | 2,832,830 | |

Municipal Bonds | | | — | | | | 322,082 | | | | — | | | | 322,082 | |

Non-Agency Mortgage-Backed Securities | | | — | | | | 3,343,286 | | | | — | | | | 3,343,286 | |

Preferred Securities | | | | | | | | | | | | | | | | |

Capital Trusts | | | — | | | | 271,049 | | | | — | | | | 271,049 | |

U.S. Government Sponsored Agency Securities | | | — | | | | 825,609 | | | | — | | | | 825,609 | |

Short-Term Securities | | | | | | | | | | | | | | | | |

Commercial Paper | | | — | | | | 832,484 | | | | — | | | | 832,484 | |

Money Market Funds | | | 106,485,015 | | | | — | | | | — | | | | 106,485,015 | |

Liabilities | | | | | | | | | | | | | | | | |

Investments | | | | | | | | | | | | | | | | |

TBA Sale Commitments | | | — | | | | (825,609 | ) | | | — | | | | (825,609 | ) |

| | | | | | | | | | | | | | | | |

| | | | |

| | $ | 107,747,286 | | | $ | 53,017,692 | | | $ | 1,803,190 | | | $ | 162,568,168 | |

| | | | | | | | | | | | | | | | |

Derivative Financial Instruments(a) | | | | | | | | | | | | | | | | |

Assets | | | | | | | | | | | | | | | | |

Foreign Currency Exchange Contracts | | $ | — | | | $ | 77,999 | | | $ | — | | | $ | 77,999 | |

Liabilities | | | | | | | | | | | | | | | | |

Foreign Currency Exchange Contracts | | | — | | | | (37,362 | ) | | | — | | | | (37,362 | ) |

| | | | | | | | | | | | | | | | |

| | | | |

| | $ | — | | | $ | 40,637 | | | $ | — | | | $ | 40,637 | |

| | | | | | | | | | | | | | | | |

| | (a) | Derivative financial instruments are forward foreign currency exchange contracts. Forward foreign currency exchange contracts are valued at the unrealized appreciation (depreciation) on the instrument. | |

| | |

SCHEDULE OF INVESTMENTS | | 15 |

| | |

Schedule of Investments (continued) December 31, 2023 | | BlackRock Multi-Sector Opportunities Trust (MSO) |

A reconciliation of Level 3 financial instruments is presented when the Trust had a significant amount of Level 3 investments and derivative financial instruments at the beginning and/or end of the year in relation to net assets. The following table is a reconciliation of Level 3 investments for which significant unobservable inputs were used in determining fair value:

| | | | | | | | | | | | | | | | |

| |

| | | | |

| | | Asset-Backed

Securities | | | Corporate

Bonds | | | Floating

Rate Loan

Interests | | | Total | |

| |

| | | | |

Assets | | | | | | | | | | | | | | | | |

Opening balance, as of December 31, 2022 | | $ | 1,003,006 | | | $ | 2,503,178 | | | $ | 14,067,820 | | | $ | 17,574,004 | |

Transfers into Level 3 | | | — | | | | — | | | | — | | | | — | |

Transfers out of Level 3 | | | (191,535 | ) | | | — | | | | — | | | | (191,535 | ) |

Other(a) | | | (811,471 | ) | | | 3,687,893 | | | | (2,876,422 | ) | | | — | |

Accrued discounts/premiums | | | — | | | | (8,875 | ) | | | 6,427 | | | | (2,448 | ) |

Net realized gain (loss) | | | — | | | | (632,953 | ) | | | (5,853,838 | ) | | | (6,486,791 | ) |

Net change in unrealized appreciation (depreciation)(b)(c) | | | — | | | | 455,455 | | | | 4,954,647 | | | | 5,410,102 | |

Purchases | | | — | | | | 54,561 | | | | 191,520 | | | | 246,081 | |

Sales | | | — | | | | (6,059,259 | ) | | | (8,686,964 | ) | | | (14,746,223 | ) |

| | | | | | | | | | | | | | | | |

| | | | |

Closing balance, as of December 31, 2023 | | $ | — | | | $ | — | | | $ | 1,803,190 | | | $ | 1,803,190 | |

| | | | | | | | | | | | | | | | |

| | | | |

Net change in unrealized appreciation (depreciation) on investments still held at December 31, 2023(c) | | $ | — | | | $ | — | | | $ | (1,558,146 | ) | | $ | (1,558,146 | ) |

| | | | | | | | | | | | | | | | |

| | (a) | Certain Level 3 investments were re-classified between Asset-Backed Securities, Corporate Bonds and Floating Rate Loan Interests. | |

| | (b) | Included in the related net change in unrealized appreciation (depreciation) in the Statement of Operations. | |

| | (c) | Any difference between net change in unrealized appreciation (depreciation) and net change in unrealized appreciation (depreciation) on investments still held at December 31, 2023 is generally due to investments no longer held or categorized as Level 3 at period end. | |

The following table summarizes the valuation approaches used and unobservable inputs utilized by the BlackRock Valuation Committee (the “Valuation Committee”) to determine the value of certain of the Trust’s Level 3 financial instruments as of period end.

| | | | | | | | | | | | | | | | |

| | | | | | |

| | | | Value | | | Valuation

Approach | | Unobservable Inputs | |

| Range of

Unobservable Inputs Utilized |

(a) | |

| Weighted

Average of Unobservable Inputs Based on Fair Value |

|

| | | | | |

Assets | | | | | | | | | | | | | | | | |

Floating Rate Loan Interests(b) | | $ | 1,803,190 | | | Income | | Estimated Recovery Value | | | 20% | | | | — | |

| | | | | | Market | | EBITDA Multiple | | | 14.50x | | | | — | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | |

| | $ | 1,803,190 | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | (a) | A significant change in unobservable input would have resulted in a correlated (inverse) significant change to value. | |

| | (b) | For the period end December 31, 2023, the valuation technique for investments classified as Floating Rate Loan Interests amounting to $984,427 changed to a Market approach. The investments were previously valued utilizing a Discounted Cash Flow approach. The change was due to consideration of the information that was available at the time the investments were valued. | |

See notes to financial statements.

| | |

| 16 | | 2 0 2 3 BLACK ROCK ANNUAL REPORT TO SHAREHOLDERS |

Statement of Assets and Liabilities

December 31, 2023

| | | | |

| | | BlackRock Multi-Sector Opportunities Trust | |

| |

|

ASSETS | |

Investments, at value — unaffiliated(a) | | $ | 56,908,762 | |

Investments, at value — affiliated(b) | | | 106,485,015 | |

Foreign currency, at value(c) | | | 995,680 | |

Receivables: | | | | |

Investments sold | | | 849,175 | |

TBA sale commitments | | | 789,917 | |

Dividends — affiliated | | | 467,389 | |

Interest — unaffiliated | | | 1,040,615 | |

Unrealized appreciation on forward foreign currency exchange contracts | | | 77,999 | |

Prepaid expenses | | | 1,708 | |

| | | | |

| |

Total assets | | | 167,616,260 | |

| | | | |

| |

LIABILITIES | | | | |

TBA sale commitments, at value(d) | | | 825,609 | |

Payables: | | | | |

Investments purchased | | | 787,609 | |

Accounting services fees | | | 14,927 | |

Custodian fees | | | 11,619 | |

Investment advisory fees | | | 170,862 | |

Trustees’ and Officer’s fees | | | 3,142 | |

Other accrued expenses | | | 30,167 | |

Principal payups | | | 100,327 | |

Professional fees | | | 83,373 | |

Transfer agent fees | | | 16,585 | |

Unrealized depreciation on forward foreign currency exchange contracts | | | 37,362 | |

| | | | |

| |