Exhibit 99.2

Financials & Notes

(Unaudited)

Contents

Condensed Consolidated Statements of |

| |||||

| 53 | ||||||

| 54 | ||||||

| 55 | ||||||

| 56 | ||||||

| 57 | ||||||

Business and Environment |

| |||||

| Description of Business | 59 | |||||

| Basis of Presentation | 60 | |||||

Income, Expenses and Cash Flows |

| |||||

| Business Combination | 61 | |||||

| Segment Information | 63 | |||||

| Provincial Mining and Other Taxes | 68 | |||||

| Other Expenses | 68 | |||||

| Finance Costs | 68 | |||||

| Income Taxes | 69 | |||||

| Net Earnings per Share | 71 | |||||

| Consolidated Statements of Cash Flows | 72 | |||||

Operating Assets and Liabilities |

| |||||

| Receivables | 73 | |||||

| Inventories | 74 | |||||

| Property, Plant and Equipment | 75 | |||||

| Other Assets | 77 | |||||

| Goodwill and Other Intangible Assets | 77 | |||||

| Payables and Accrued Charges | 79 | |||||

| Derivative Instruments | 79 | |||||

Asset Retirement Obligations and Accrued Environmental Costs | 81 | |||||

Investments, Financing and Capital Structure |

| |||||

| Investments | 84 | |||||

| Short-Term Debt | 87 | |||||

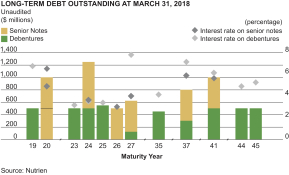

| Long-Term Debt | 87 | |||||

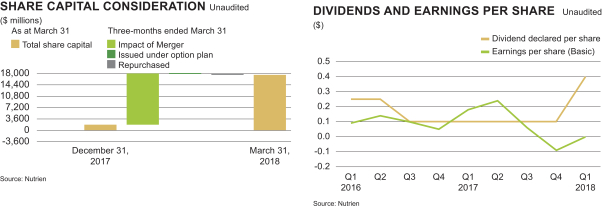

| Share Capital | 90 | |||||

| Capital Management | 91 | |||||

| Commitments | 92 | |||||

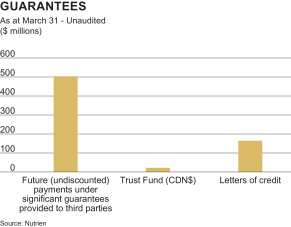

| Guarantees | 93 | |||||

Personnel |

| |||||

| Pension and Other Post-Retirement Benefits | 94 | |||||

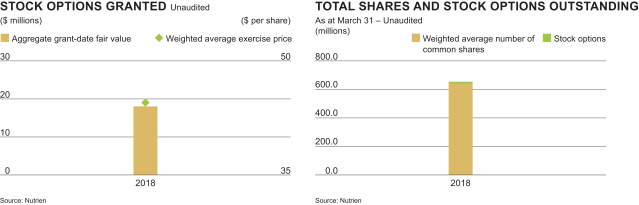

| Share-Based Compensation | 98 | |||||

Other |

| |||||

| Related Party Transactions | 102 | |||||

| 103 | ||||||

| Contingencies and Other Matters | 108 | |||||

| 109 | ||||||

| Comparative Figures | 115 | |||||

| 52 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

|

| Three Months Ended March 31 | ||||||||

| 2018 | 2017 | |||||||||

|

|

| (Note 32) | |||||||

Sales | Note 4 | $ | 3,695 | $ | 1,112 | |||||

Freight, transportation and distribution | (208 | ) | (133 | ) | ||||||

Cost of goods sold | (2,640 | ) | (706 | ) | ||||||

Gross Margin | 847 | 273 | ||||||||

Selling expenses | (532 | ) | (9 | ) | ||||||

General and administrative expenses | (119 | ) | (41 | ) | ||||||

Provincial mining and other taxes | Note 5 | (48 | ) | (33 | ) | |||||

Earnings of equity-accounted investees | Note 19 | 7 | – | |||||||

Other expenses | Note 6 | (79 | ) | (15 | ) | |||||

Earnings before Finance Costs and Income Taxes | 76 | 175 | ||||||||

Finance costs | Note 7 | (119 | ) | (59 | ) | |||||

(Loss) Earnings Before Income Taxes | (43 | ) | 116 | |||||||

Income tax recovery (expense) | Note 8 | 42 | (10 | ) | ||||||

Net (Loss) Earnings from Continuing Operations | $ | (1 | ) | $ | 106 | |||||

Net earnings from discontinued operations | Note 19 | – | 43 | |||||||

Net (Loss) Earnings | $ | (1 | ) | $ | 149 | |||||

Net Earnings per Share from Continuing Operations | Note 9 | |||||||||

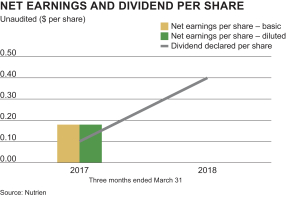

Basic | $ | – | $ | 0.13 | ||||||

Diluted | $ | – | $ | 0.13 | ||||||

Net Earnings per Share from Continuing and Discontinued Operations | Note 9 | |||||||||

Basic | $ | – | $ | 0.18 | ||||||

Diluted | $ | – | $ | 0.18 | ||||||

Weighted average shares outstanding for basic EPS | Note 9 | 642,690,000 | 839,911,000 | |||||||

Weighted average shares outstanding for diluted EPS | Note 9 | 643,218,000 | 840,211,000 | |||||||

(See Notes to the Condensed Consolidated Financial Statements)

| • | Merger of Potash Corporation of Saskatchewan Inc. (“PotashCorp”) and Agrium Inc. (“Agrium”) occurred on January 1, 2018. |

| • | 2017 figures throughout are the financial results of PotashCorp only, the accounting acquirer. |

| • | Gross margin was earned in the retail segment – $408; potash segment – $295; nitrogen segment – $148 and phosphate and sulfate segment – $29. |

| • | Earnings from Sociedad Quimica y Minera de Chile S.A. (“SQM”) and Arab Potash Company (“APC”) and income from Israel Chemicals Ltd. (“ICL”) are presented as discontinued operations for the periods presented to reflect required divestitures of these investments. The company sold its equity interest in ICL on January 24, 2018. |

| Nutrien 2018 First Quarter Interim Report | 53 |

| Unaudited | in millions of US dollars except as otherwise noted |

2018

HIGHLIGHTS

| • | The company adopted IFRS 9, Financial Instruments, beginning January 1, 2018.Available-for-sale investments were reclassified as financial instruments measured at fair value through other comprehensive income (“FVTOCI”). |

Condensed Consolidated Statements of Comprehensive (Loss) Income

The condensed consolidated statements of comprehensive (loss) income present changes in net assets during the period other than transactions with shareholders. Amounts recorded in other comprehensive (loss) income may be subsequently reclassified to net (loss) earnings or may not pass through net (loss) earnings.

| Three Months Ended March 31 | ||||||||

| 2018 | 2017 | |||||||

| (net of related income taxes) | (Note 32) | |||||||

Net (Loss) Earnings | $ | (1 | ) | $ | 149 | |||

Other comprehensive (loss) income | ||||||||

Items that will not be reclassified to net (loss) earnings: | ||||||||

Net actuarial gain on defined benefit plans1 | 57 | – | ||||||

Financial instruments measured at FVTOCI2 | ||||||||

Net fair value (loss) gain on investments | (83 | ) | 33 | |||||

Items that have been or may be subsequently reclassified to net (loss) earnings: | ||||||||

Cash flow hedges | ||||||||

Net fair value loss during the period3 | (2 | ) | (5 | ) | ||||

Reclassification to earnings of net loss4 | – | 8 | ||||||

Foreign currency translation | ||||||||

Loss on translation of net foreign operations | (41 | ) | – | |||||

Equity-accounted investees | ||||||||

Share of comprehensive (loss) income | (1 | ) | 3 | |||||

Other Comprehensive (Loss) Income | (70 | ) | 39 | |||||

Comprehensive (Loss) Income | $ | (71 | ) | $ | 188 | |||

| 1 | Net of income taxes of $(17) (2017 – $NIL). |

| 2 | As at March 31, 2018, financial instruments measured at FVTOCI are comprised of shares in Sinofert Holdings Limited (“Sinofert”) and other (March 31, 2017 – ICL, Sinofert and other). The company’s investment in ICL was classified as held for sale at December 31, 2017 and the divestiture of all equity interests in ICL was completed on January 24, 2018. |

| 3 | Cash flow hedges are comprised of natural gas derivative instruments and were net of income taxes of $1 (2017 – $3). |

| 4 | Net of income taxes of $NIL (2017 – $(5)). See Note 31 for impact of adoption of new standard. |

(See Notes to the Condensed Consolidated Financial Statements)

| 54 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

Condensed Consolidated Statements of Cash Flows

The condensed consolidated statements of cash flows start with net (loss) earnings adjusted fornon-cash items affecting net (loss) earnings to arrive at cash flows from operating activities, and present cash provided by or used in investing and financing activities.

| Three Months Ended March 31 | ||||||||||||

| 2018 | 2017 | |||||||||||

Operating Activities | ||||||||||||

Net (loss) earnings | $ | (1 | ) | $ | 149 | |||||||

Adjustments to reconcile net (loss) earnings to cash (used in) provided by operating activities | Note 10 | 401 | 144 | |||||||||

Changes innon-cash operating working capital | Note 10 | (740 | ) | (70 | ) | |||||||

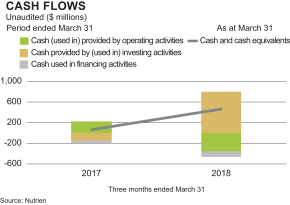

Cash (used in) provided by operating activities | (340 | ) | 223 | |||||||||

Investing Activities | ||||||||||||

Business acquisitions, net of cash acquired | (185 | ) | – | |||||||||

Additions to property, plant and equipment | (238 | ) | (133 | ) | ||||||||

Cash acquired in Merger | Note 3 | 466 | – | |||||||||

Proceeds from disposal of discontinued operations | Note 19 | 752 | – | |||||||||

Other | 1 | 1 | ||||||||||

Cash provided by (used in) investing activities | 796 | (132 | ) | |||||||||

Financing Activities | ||||||||||||

Finance costs on long-term debt | (6 | ) | (1 | ) | ||||||||

Proceeds from short-term debt | 496 | 21 | ||||||||||

Dividends paid | (205 | ) | (82 | ) | ||||||||

Repurchase of common shares | Note 22 | (401 | ) | – | ||||||||

Issuance of common shares | 1 | 1 | ||||||||||

Cash used in financing activities | (115 | ) | (61 | ) | ||||||||

Effect of exchange rate changes on cash and cash equivalents | 3 | – | ||||||||||

Increase in Cash and Cash Equivalents | 344 | 30 | ||||||||||

Cash and Cash Equivalents, Beginning of Period | 116 | 32 | ||||||||||

Cash and Cash Equivalents, End of Period | $ | 460 | $ | 62 | ||||||||

Cash and cash equivalents comprised of: | ||||||||||||

Cash | $ | 325 | $ | 44 | ||||||||

Short-term investments | 135 | 18 | ||||||||||

| $ | 460 | $ | 62 | |||||||||

(See Notes to the Condensed Consolidated Financial Statements)

2018

HIGHLIGHTS

| • | Cash provided by investing activitieswas impacted by net proceeds on the sale of the company’s shares in ICL ($685) and Conda and North Bend facilities ($67). |

| • | Cash used in financing activitieswas primarily impacted by net disbursements on the repurchase of common shares through the company’s normal course issuer bid ($401) and payment of dividends ($205) partially offset by the proceeds from short-term debt ($496). |

| Nutrien 2018 First Quarter Interim Report | 55 |

| Unaudited | in millions of US dollars except as otherwise noted |

Condensed Consolidated Statements of Changes in Shareholders’ Equity

The condensed consolidated statements of changes in shareholders’ equity show the movements in shareholders’ equity.

| Accumulated Other Comprehensive Income (Loss) | ||||||||||||||||||||||||||||||||||||||||

Share Capital | Contributed Surplus | Net fair value loss on investments 1,2 | Net loss on derivatives designated as cash flow hedges | Net actuarial gain on defined benefit plans | Translation (Note 32) | Comprehensive (Note 32) | Total Accumulated Other Comprehensive Income (Loss) | Retained Earnings | Total Equity 3 | |||||||||||||||||||||||||||||||

Balance – December 31, 2017 | $ | 1,806 | $ | 230 | $ | 73 | $ | (43 | ) | $ | – | 4 | $ | (2 | ) | $ | (3 | ) | $ | 25 | $ | 6,242 | $ | 8,303 | ||||||||||||||||

Merger impact (Note 3) | 15,898 | 7 | – | – | – | – | – | – | (1 | ) | 15,904 | |||||||||||||||||||||||||||||

Net loss | – | – | – | – | – | – | – | – | (1 | ) | (1 | ) | ||||||||||||||||||||||||||||

Other comprehensive (loss) income | – | – | (83 | ) | (2 | ) | 57 | (41 | ) | (1 | ) | (70 | ) | – | (70 | ) | ||||||||||||||||||||||||

Shares repurchased | (256 | ) | (23 | ) | – | – | – | – | – | – | (178 | ) | (457 | ) | ||||||||||||||||||||||||||

Dividends declared | – | – | – | – | – | – | – | – | (258 | ) | (258 | ) | ||||||||||||||||||||||||||||

Effect of share-based compensation including issuance of common shares | 1 | – | – | – | – | – | – | – | – | 1 | ||||||||||||||||||||||||||||||

Transfer of net actuarial gain on defined benefit plans | – | – | – | – | (57 | ) | – | – | (57 | ) | 57 | – | ||||||||||||||||||||||||||||

Transfer of net loss on sale of investment | – | – | 19 | – | – | – | – | 19 | (19 | ) | – | |||||||||||||||||||||||||||||

Transfer of net loss on cash flow hedges 5 | – | – | – | 9 | – | – | – | 9 | – | 9 | ||||||||||||||||||||||||||||||

Balance – March 31, 2018 | $ | 17,449 | $ | 214 | $ | 9 | $ | (36 | ) | $ | – | 4 | $ | (43 | ) | $ | (4 | ) | $ | (74 | ) | $ | 5,842 | $ | 23,431 | |||||||||||||||

Balance – December 31, 2016 | $ | 1,798 | $ | 222 | $ | 43 | $ | (60 | ) | $ | – | 4 | $ | (2 | ) | $ | (6 | ) | $ | (25 | ) | $ | 6,204 | $ | 8,199 | |||||||||||||||

Net earnings | – | – | – | – | – | – | – | – | 149 | 149 | ||||||||||||||||||||||||||||||

Other comprehensive income | – | – | 33 | 3 | – | 1 | 2 | 39 | – | 39 | ||||||||||||||||||||||||||||||

Dividends declared | – | – | – | – | – | – | – | – | (84 | ) | (84 | ) | ||||||||||||||||||||||||||||

Effect of share-based compensation including issuance of common shares | 2 | 1 | – | – | – | – | – | – | – | 3 | ||||||||||||||||||||||||||||||

Shares issued for dividend reinvestment plan | 2 | – | – | – | – | – | – | – | – | 2 | ||||||||||||||||||||||||||||||

Balance – March 31, 2017 | $ | 1,802 | $ | 223 | $ | 76 | $ | (57 | ) | $ | – | 4 | $ | (1 | ) | $ | (4 | ) | $ | 14 | $ | 6,269 | $ | 8,308 | ||||||||||||||||

| 1 | The company adopted IFRS 9 in 2018 and reclassifiedavailable-for-sale investments as financial instruments measured at FVTOCI. |

| 2 | The company divested its equity interests in the investment in ICL on January 24, 2018. The loss on sale of ICL of $(19) was transferred to retained earnings at March 31, 2018. The cumulative net unrealized gain at March 31, 2017 was $44. |

| 3 | All equity transactions were attributable to common shareholders. |

| 4 | Any amounts incurred during a period were closed out to retained earnings at eachperiod-end. Therefore, no balance exists at the beginning or end of period. |

| 5 | Net of income taxes of $(2). |

(See Notes to the Condensed Consolidated Financial Statements)

| 56 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

Condensed Consolidated Balance Sheets

The condensed consolidated balance sheets present assets, liabilities and shareholders’ equity.

| March 31, 2018 | December 31, 2017 (Note 32) | |||||||||||

Assets | ||||||||||||

Current assets | ||||||||||||

Cash and cash equivalents | $ | 460 | $ | 116 | ||||||||

Receivables | Note 11 | 3,230 | 489 | |||||||||

Inventories | Note 12 | 5,915 | 788 | |||||||||

Prepaid expenses and other current assets | 546 | 72 | ||||||||||

| 10,151 | 1,465 | |||||||||||

Assets held for sale | Note 19 | 1,150 | 1,858 | |||||||||

| 11,301 | 3,323 | |||||||||||

Non-current assets | ||||||||||||

Property, plant and equipment | Note 13 | 20,576 | 12,971 | |||||||||

Goodwill | Note 15 | 10,576 | 97 | |||||||||

Other intangible assets | Note 15 | 2,333 | 69 | |||||||||

Investments | Note 19 | 778 | 292 | |||||||||

Other assets | Note 14 | 474 | 246 | |||||||||

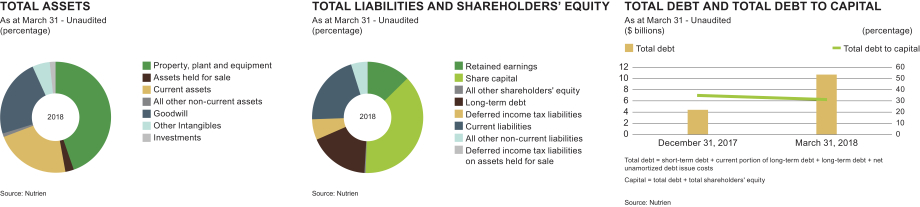

Total Assets | $ | 46,038 | $ | 16,998 | ||||||||

(See Notes to the Condensed Consolidated Financial Statements)

| March 31, 2018 | December 31, 2017 (Note 32) | |||||||||||

Liabilities | ||||||||||||

Current liabilities | ||||||||||||

Short-term debt | Note 20 | $ | 2,091 | $ | 730 | |||||||

Current portion of long-term debt | Note 21 | 524 | – | |||||||||

Payables and accrued charges | Note 16 | 6,920 | 836 | |||||||||

| 9,535 | 1,566 | |||||||||||

Deferred income tax liabilities on assets held for sale | Note 19 | 36 | 36 | |||||||||

| 9,571 | 1,602 | |||||||||||

Non-current liabilities | ||||||||||||

Long-term debt | Note 21 | 8,091 | 3,711 | |||||||||

Deferred income tax liabilities | Note 8 | 2,762 | 2,205 | |||||||||

Pension and other post-retirement benefit liabilities | Note 26 | 519 | 440 | |||||||||

Asset retirement obligations and accrued environmental costs | Note 18 | 1,486 | 651 | |||||||||

Othernon-current liabilities | 178 | 86 | ||||||||||

Total Liabilities | 22,607 | 8,695 | ||||||||||

Shareholders’ Equity | ||||||||||||

Share capital | Note 22 | 17,449 | 1,806 | |||||||||

Contributed surplus | 214 | 230 | ||||||||||

Accumulated other comprehensive (loss) income | (74 | ) | 25 | |||||||||

Retained earnings | 5,842 | 6,242 | ||||||||||

Total Shareholders’ Equity | 23,431 | 8,303 | ||||||||||

Total Liabilities and Shareholders’ Equity | $ | 46,038 | $ | 16,998 | ||||||||

(See Notes to the Condensed Consolidated Financial Statements)

| Nutrien 2018 First Quarter Interim Report | 57 |

| Unaudited | in millions of US dollars except as otherwise noted |

2018

HIGHLIGHTS

Highlights to the condensed consolidated balance sheets

| • | Increase in assets and liabilities primarily relates to theMerger of PotashCorp and Agrium, Inc. effective as of January 1, 2018, as well as, the fair value increase from the purchase price allocation. |

| • | Thecurrent ratio1 was 1.18 as at March 31, 2018 (December 31, 2017 – 2.07). |

| • | As at March 31, 2018, the company’sproperty, plant and equipmentaccounted for 45 percent of total assets (December 31, 2017 – 76 percent). |

| • | Thetotaldebt-to-capital ratio2 was 31 percent as at March 31, 2018 (December 31, 2017 – 35 percent). |

| • | Nutrien notes issued after March 31, 2018 in conjunction with the completion of an obligor exchange – no significant change in the economic terms of the consolidated notes outstanding as described in Note 20 and 21. |

| 1 | Current assets / current liabilities. |

| 2 | Total debt / (total debt + total shareholders’ equity). |

| 58 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

| Description of Business |

Nutrien Ltd. is a provider of crop nutrients, inputs and services and plays a critical role in helping growers around the globe increase food production in a sustainable manner. The company’s retail operations supply key products and services directly to growers – including crop nutrients, crop protection and seed, as well as agronomic and application services. The company produces the three essential nutrients – potash, nitrogen and phosphate – required to help farmers grow healthier, more abundant crops.

On January 1, 2018, after receiving all required regulatory approvals, Potash Corporation of Saskatchewan Inc. (“PotashCorp”) and Agrium Inc. (“Agrium”) combined their businesses in a transaction by way of a plan of arrangement (the “Merger”) by becoming wholly owned subsidiaries of a new parent company named Nutrien Ltd.

With its subsidiaries, Nutrien Ltd. (together known as “Nutrien” or “the company” except where the context otherwise requires) is the world’s largest provider of crop inputs and services. The company is a corporation organized under the laws of Canada and its registered head office is located at Suite 500, 122 – 1st Avenue South, Saskatoon, Saskatchewan, Canada. As at March 31, 2018, the company had assets as follows:

R Retail

| • | approximately 1,600 retail facilities across the US, Canada, Australia and key areas of South America |

Production

(Owned)

KPotash

| • | six operations in the province of Saskatchewan |

| • | one operation in the province of New Brunswick (indefinitely suspended in early 2016 and placed incare-and-maintenance mode) |

NNitrogen

| • | eight production facilities in North America, four in the province of Alberta and one located in each of the states of Texas, Georgia, Louisiana and Ohio |

| • | one large-scale operation in the country of Trinidad |

| • | seven upgrade facilities in North America, three in the province of Alberta and one in each of the states of Washington, Missouri, Georgia, and Alabama |

| • | 50 percent investment in Profertil S.A. (“Profertil”), a nitrogen producer based in the country of Argentina |

| • | 26 percent investment in Misr Fertilizers Production Company S.A.E. (“MOPCO”), a nitrogen producer based in the country of Egypt |

PPhosphate and Sulfate

| • | two mines and processing plants, one in each of the states of North Carolina and Florida |

| • | a production facility in the province of Alberta |

| • | phosphate feed plants in the states of Illinois, Missouri, and Nebraska |

| • | an industrial phosphoric acid plant in the state of Ohio |

Others

| • | a processing plant in the state of Louisiana |

| • | investment in Canpotex Ltd. (“Canpotex”), a Canadian potash export, sales and marketing company owned in equal shares by Nutrien and another potash producer |

| • | investments in Sociedad Quimica y Minera de Chile S.A. (“SQM”), Chile and Arab Potash Company (“APC”), Jordan, each currently classified as held for sale |

| • | investment in Sinofert Holdings Limited (“Sinofert”), China |

See Note 19 for additional information.

Transportation and Distribution (excluding Retail)

(Leased and Owned)

| • | leased or owned 403 terminals and warehouses (543 multi-product distribution points) in North America |

| • | leased or owned approximately 15,300 railcars in North America |

| • | leased a warehouse in Malaysia |

| • | ownership in a joint venture that leases a dry bulk fertilizer port terminal in Brazil |

| • | leased four vessels for ammonia transportation |

| • | owned one multi-purpose vessel used for molten sulfur and phosphoric acid transportation |

| Nutrien 2018 First Quarter Interim Report | 59 |

| Unaudited | in millions of US dollars except as otherwise noted |

| Basis of Presentation |

These unaudited interim condensed consolidated financial statements (“interim financial statements”) are based on International Financial Reporting Standards as issued by the International Accounting Standards Board (IFRS), and have been prepared in accordance with International Accounting Standard (IAS) 34, “Interim Financial Reporting.” The accounting policies and methods of computation used in preparing these unaudited interim condensed consolidated financial statements are consistent with those used in the preparation of PotashCorp’s, the accounting acquirer, 2017 annual consolidated financial statements, with the exception of IFRS 9 “Financial Instruments” and IFRS 15 “Revenue from Contracts with Customers” which were adopted effective January 1, 2018. PotashCorp is the acquirer for accounting purposes, and as a result, figures for 2017 and

prior reflect the historical operations of PotashCorp. The financial statements and related notes of Nutrien in 2018 and beyond reflect the operations of Nutrien.

These interim financial statements include the accounts of Nutrien and its subsidiaries; however, they do not include all disclosures normally provided in annual consolidated financial statements. In management’s opinion, the interim financial statements include all adjustments necessary to fairly present such information in all material respects. Interim results are not necessarily indicative of the results expected for any other interim period or the fiscal year.

These interim financial statements were authorized by the audit committee of the Board of Directors for issue on May 7, 2018.

These interim financial statements were prepared under the historical cost convention, except for certain items as discussed in the applicable accounting policies.

Where an accounting policy is applicable to a specific note to the statements, the policy is described within that note, with the related financial disclosures by major caption as noted in the table below. Certain of the company’s accounting policies that relate to the financial statements as a whole, as well as estimates and judgments it has made and how they affect the amounts reported in the consolidated financial statements, are disclosed in Note 31. New standards and amendments or interpretations that were either effective and applied by the company during the first three months of 2018 or that were not yet effective are described in Note 31.

| Note | Topic | Accounting Policies | Accounting Estimates and Judgments | Page | ||||||

| 3 | Business combination | X | X | 61 | ||||||

| 4 | Revenue recognition | X | X | 63 | ||||||

| 8 | Income taxes | X | X | 69 | ||||||

| 10 | Cash equivalents | X | 72 | |||||||

| 11 | Receivables | X | X | 73 | ||||||

| 12 | Inventories | X | X | 74 | ||||||

| 13 | Property, plant and equipment | X | X | 75 | ||||||

| 14 | Other assets | X | 77 | |||||||

| 15 | Goodwill and other intangible assets | X | X | 77 | ||||||

| 17 | Derivative instruments | X | X | 79 | ||||||

| Note | Topic | Accounting Policies | Accounting Estimates and Judgments | Page | ||||||

| 18 | Asset retirement obligations and accrued environmental costs | X | X | 81 | ||||||

| 19 | Investments | X | X | 84 | ||||||

| 21 | Long-term debt | X | 87 | |||||||

| 24 | Commitments | X | X | 92 | ||||||

| 25 | Guarantees | X | 93 | |||||||

| 26 | Pension and other post-retirement benefits | X | X | 94 | ||||||

| 27 | Share-based compensation | X | X | 98 | ||||||

| 28 | Related party transactions | X | 102 | |||||||

| 29 | Fair value and offsetting of financial instruments | X | X | 103 | ||||||

| 30 | Contingencies | X | X | 108 | ||||||

| 60 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

| Business Combinations |

| Accounting Policies | Accounting Estimates and Judgments | |||

Business combinations are recognized as follows:

• Acquisitions of subsidiaries and businesses are accounted for using the acquisition method.

• Consideration for each acquisition is measured at the aggregate of the fair values of assets given, liabilities incurred or assumed, and equity instruments issued in exchange for control of the acquiree at the acquisition date.

• The acquisition date is the date the company obtains control over the acquiree and is generally the day the purchase consideration transfers.

• At the acquisition date, the identifiable assets acquired and liabilities assumed are recognized at their fair values with the exception of contingent liabilities, deferred taxes, employee benefit arrangements, replaced acquiree share-based compensation awards and assets held for sale, where IFRS provides exceptions to recording amounts at fair value.

• Acquisition-related costs are recognized in net (loss) earnings as incurred.

• The excess of total consideration for each acquisition plusnon-controlling interest in the acquiree, over the fair value of the identifiable net assets acquired, is recorded as goodwill. If the total consideration plusnon-controlling interest is less than the fair value of the net assets acquired, a purchase gain is recognized in net (loss) earnings.

• If the initial accounting for a business combination is incomplete by the end of the reporting period in which the combination occurs, provisional amounts are recorded for the incomplete items. The measurement period is the period from the date of acquisition to the date complete information about facts and circumstances that existed as of the acquisition date is received, subject to a maximum of one year. Provisional amounts are retrospectively adjusted during the measurement period, or recognized as additional assets or liabilities to reflect new information obtained about facts and circumstances that existed as of the acquisition date that, if known, would have affected the amounts recognized as of that date. | • Estimation is required to allocate the purchase consideration to the fair value of the identifiable tangible and intangible assets acquired and liabilities assumed.

• Judgment is required to determine which entity is the acquirer in a merger of equals. PotashCorp is treated as the acquiring entity for accounting purposes. In identifying PotashCorp as the acquirer, the companies considered the voting rights of all equity instruments, the intended corporate governance structure of the combined company, the intended composition of senior management of the combined company and the size of each of the companies. In assessing the size of each of the companies, the companies evaluated various metrics. No single factor was the sole determinant in the overall conclusion that PotashCorp is the acquirer for accounting purposes; rather all factors were considered in arriving at the conclusion. | |||

Merger with Agrium

As described in Note 1, PotashCorp and Agrium combined their businesses in a merger of equals. Expected benefits of the acquisition include operating synergies, primarily from the distribution and retail integration, production and expense optimization, and procurement savings.

Agrium was a retail distributor of agricultural crop inputs, providing growers with fertilizer, crop protection products, seed, services and solutions. Agrium was also one of the largest manufacturers of fertilizer in the world producing and marketing all three major crop nutrients – nitrogen, potash and phosphate.

On January 2, 2018, the first day Nutrien began trading, shareholders of PotashCorp received 0.400 common shares of Nutrien for each PotashCorp share held and shareholders of Agrium received 2.230 common shares of Nutrien for each Agrium share held. The exchange ratios represent the respective closing share prices of each company’s common shares at market close on the NYSE on August 29, 2016, the last trading day prior to when the companies announced that they were in preliminary discussions regarding a merger of equals, which is consistent with the weighted average prices through that date. The outstanding share-based compensation awards of PotashCorp and Agrium were replaced by Nutrien share-based compensation awards with substantially equivalent terms after adjusting for the applicable exchange ratio (refer to Note 27). The purchase consideration was $16 billion. Merger and related costs of $66 for the three months ended March 31, 2018 are included in other expenses (2017 – $9). | The company has engaged independent valuation experts to assist in determining the fair value of certain assets acquired and liabilities assumed and related deferred income tax impacts. The purchase price allocation is not final as the company is continuing to obtain and verify information required to determine the fair value of certain assets and liabilities and the amount of deferred income taxes arising on their recognition. The company expects to finalize the amounts recognized as it obtains the information necessary to complete the analysis, not later than December 31, 2018. | |||

| Nutrien 2018 First Quarter Interim Report | 61 |

| Unaudited | in millions of US dollars except as otherwise noted |

Due to the inherent complexity associated with valuations and the timing of the acquisition, the numbers below are provisional. The preliminary value that was allocated to Agrium’s assets and liabilities based upon fair values is as follows:

January 1, 2018 | ||||||||||||||||

Cash and cash equivalents | $ | 466 | ||||||||||||||

Receivables1 | 2,424 | |||||||||||||||

Inventories | 3,321 | |||||||||||||||

Prepaid expenses and other current assets | 1,124 | |||||||||||||||

Assets held for sale2 | 105 | |||||||||||||||

Property, plant and equipment3 | 7,783 | |||||||||||||||

Goodwill 4 | 10,455 | |||||||||||||||

Other intangible assets 5 | 2,318 | |||||||||||||||

Investments | 522 | |||||||||||||||

Other assets | 123 | |||||||||||||||

Total assets | $ | 28,641 | ||||||||||||||

Short-term debt | $ | 867 | ||||||||||||||

Payables and accrued charges | 5,223 | |||||||||||||||

Long-term debt | 4,941 | |||||||||||||||

Deferred income tax liabilities | 498 | |||||||||||||||

Pension and other post-retirement benefit liabilities | 142 | |||||||||||||||

Asset retirement obligations and accrued environmental costs6 | 888 | |||||||||||||||

Othernon-current liabilities | 72 | |||||||||||||||

Total liabilities | $ | 12,631 | ||||||||||||||

Net assets (consideration for the merger) | $ | 16,010 | ||||||||||||||

| 1 | This includes trade receivables with gross contractual trade receivables of $2,247, of which $78 are considered to be uncollectible. |

| 2 | This relates to the assets held at Conda phosphate and North Bend nitric acid operations. The sale was completed on January 12, 2018. |

| 3 | Refer to Note 13 for detailed information of property, plant and equipment acquired. |

| 4 | Goodwill resulting from the acquisition is attributed to the strategic and financial benefits expected to be realized, including the increased post-acquisition scale of operations, purchasing and distribution capability, and the assembled workforce. The portion of goodwill deductible for income tax purposes, if any, will be determined when the purchase allocation is finalized. |

| 5 | Refer to Note 15 for detailed information of other intangible assets acquired. |

| 6 | Refer to Note 18 for detailed information of asset retirement obligations and accrued environmental costs acquired. Included in payables and accrued charges is $39 related to the current portion of asset retirement obligations and accrued environmental costs. |

The significant fair value considerations included in the preliminary allocation of purchase price are discussed below:

Property, plant and equipment

The preliminary estimated fair value was primarily determined using a market approach for land and certain types of personal property, and a replacement cost approach for the remainder. The market approach for land and certain types of personal property represents a sales comparison that measures the value of an asset through an analysis of sales and offerings of comparable assets. The replacement cost approach used for all other depreciable property, plant and equipment measures the value of an asset by estimating the cost to acquire or construct comparable assets and adjusts for age and condition of the asset.

Other intangible assets

Other intangible assets primarily consist of acquired customer relationships, brands, proprietary technology, trademarks and tradenames. The preliminary fair value of customer-related assets was determined using the excess earnings method, an income approach.

Long-term debt

The fair value of debentures was determined based on comparable debt instruments with similar maturities, adjusted where necessary to Agrium’s credit spread, based on information published by financial institutions.

Accrued environmental costs

The preliminary fair value for environmental costs was determined using a decision-tree approach of future costs and a risk premium to capture the compensation sought by risk-averse market participants for bearing the uncertainty inherent in the cash flows of the liability. Accrued environmental costs are expected to be paid over a period extending up to 30 years and were discounted using a credit adjusted risk free rate.

Financial information related to the acquired operations of Agrium

The following table provides “Gross sales” and “earnings (loss) from continuing operations before income taxes”:

Summary results of acquired operations of Agrium1 | ||||||

Gross sales | $ | 2,488 | ||||

Net loss | $ | (243 | ) | |||

| 1 | Results of acquired operations included in the company’s condensed consolidated statements of (loss) earnings for the period from January 1, 2018 to March 31, 2018. |

| 62 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

| Segment Information |

The company has four reportable operating segments: retail, potash, nitrogen and phosphate and sulfate. The retail segment distributes crop nutrients, crop protection products, seed and merchandise and provides services directly to growers through a network of farm centers in North and South America and Australia. The potash, nitrogen and phosphate and sulfate segments are differentiated by the chemical nutrient contained in the products that each produces.

| Accounting Policies | Accounting Estimates and Judgments | |||

Operating Segments

Prior to the Merger, the company identified the Chief Executive Officer as the Chief Operating Decision Maker (“CODM”) and used gross margin to measure the segments’ profit or loss. The operating segments were limited to the following: potash, nitrogen, and phosphate. The changes in the structure of the company’s internal organization as a result of the Merger caused the composition of the operating segments to change as well as who the company has identified to be the CODM.

Post-Merger, the company identified the Executive Leadership Team (“ELT”) as the CODM. The CODM uses net (loss) earnings from continuing operations before finance costs, income tax (recovery) expense, and depreciation and amortization (“EBITDA”) to measure performance and allocate resources to the operating segments. The CODM believes EBITDA to be an important measure as it excludes the effects of items that primarily reflect the impact of long-term investment and financing decisions, rather than the performance of the company’s day-to-day operations.

Accounting policies of the segments are the same as those described in Note 2 and Note 31; and measured in a manner consistent with the financial statements.

Revenue

The company follows a policy of recognizing revenue when it satisfies the performance obligations in its contracts by transferring control of a product or service to a customer.

Retail

The company generates revenue through the sale of goods and the provision of services in the retail product lines which include crop protection products, crop nutrients, seed, merchandise and services throughout the US, Canada, Australia and South America.

Sales revenue consists primarily of:

• Crop Nutrients – sales of dry and liquid macronutrient products which include nitrogen, potash and phosphates, proprietary liquid micronutrient products and nutrient application services;

• Crop Protection products – sales of various third-party supplier and proprietary products designed to maintain crop quality and manage plant diseases, weeds, and other pests;

• Seed – various third-party supplier seed brands and proprietary seed product lines;

• Merchandise – sales of fencing, feed supplements, livestock-related animal health products, storage and irrigation equipment, and other products; and

• Services and other revenues – sales of product application, soil and leaf testing, crop scouting and precision agriculture services and financial services.

Sales revenue for the sale of goods is recognized at the point in time when the product is picked up by the customer at the company’s retail farm center or delivered to the customer’s farm. Sales revenue for the sale of services is recognized when the promised service is delivered. The company sells certain retail products to end customers with a right of return. A refund liability and a right to the returned goods (included in inventory) are recognized for the products expected to be returned. Provisions for returns, trade discounts and rebates are deducted from revenue. Returns and incentives are estimated based on historical and | Operating Segments

The ELT, comprised of officers at the Executive Vice President level and above, are responsible for strategic decision making, resource allocation and assessing financial performance and is identified as the company’s CODM for the purposes of reporting segment operations under IFRS. The CODM reviews the results of the company’s operations and financial position on consolidated and operating segment levels. The company’s operating segments are defined by the organization and reporting structure through which the company’s business operates.

Revenue

Accumulated experience is used to estimate and provide for product sales which contain volume rebates, using the most likely method, and revenue is recognized to the extent that it is highly probable that significant reversals will not occur. Estimates on rebates are described in Note 11. |

| Nutrien 2018 First Quarter Interim Report | 63 |

| Unaudited | in millions of US dollars except as otherwise noted |

| Accounting Policies continued | Accounting Estimates and Judgments continued | |||

forecasted data, contractual terms and current conditions. Due to the nature of goods and services sold, any single estimate would have only a negligible impact on revenue recognition.

Potash, Nitrogen, and Phosphate and Sulfate

The company manufactures and sells potash, nitrogen and phosphate and sulfate products. While agriculture is the company’s primary market, it also produces products for animal nutrition and industrial uses. Sales from contracts with customers are recognized at the point in time when control of products have transferred to the customer, which is when the related goods are loaded for shipping or delivered to the customer, depending on the contractual terms. Indicators of transfer of control depend on the contractual terms with the company’s customers and include when the customer is obliged to pay for the products, has legal title of the products, has physical possession of the products, has assumed the significant risks and rewards of ownership of the products, has accepted the products and any other relevant indicators.

The company’s sales revenue is recorded and measured based on the freight on board mine, plant, warehouse or terminal price specified in the contract (except for certain vessel sales or specific product sales that are shipped and recorded on a delivered basis) which reflects the consideration the company expects to be entitled to in exchange for the goods or services, net of any variable consideration (e.g. any trade discounts or estimated volume rebates). Where volume rebates are provided for in customer contracts, the company estimates revenue at the earlier of the most likely amount of consideration expected to receive or when the consideration becomes fixed. The company’s customer contracts may provide certain product quality specification guarantees but do not generally provide for refunds or returns. No significant element of financing is deemed present due to the short-term nature of the company’s sales contracts.

Sales prices are based on North American and International benchmark market prices which are variable and subject to global supply and demand and competitive factors. Potash international prices are referenced at the mine site thereby excluding transportation and distributions costs while North American prices are referenced at delivered prices and include transportation and distribution costs. Nitrogen products primarily consist of urea, ammonia, urea ammonium nitrate, and industrial-grade ammonium nitrate where realized selling prices are impacted by global energy costs and supply. Phosphate products primarily consist of solid fertilizer, liquid fertilizer, industrial products and feed products where realized selling prices are impacted by global sulfur and ammonia costs and supply.

Other

The company does not provide general warranties. Intersegment sales are made under terms that approximate market value. Transportation costs are recovered from the customer through sales pricing.

Seasonality in the company’s business results from increased demand for products during planting season. Sales are generally higher in spring and fall. |

| 64 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

Supporting Information

Financial information on each of these segments, consistent with the company’s disaggregated revenue information under IFRS 15, is summarized in the following tables:

| Three Months Ended March 31, 2018 | ||||||||||||||||||||||||||||

| Retail | Potash | Nitrogen | Phosphate and Sulfate | Others | Eliminations | Consolidated | ||||||||||||||||||||||

Sales – third party | $ | 2,088 | $ | 602 | $ | 624 | $ | 381 | $ | – | $ | – | $ | 3,695 | ||||||||||||||

– intersegment | 11 | 68 | 122 | 81 | – | (282 | ) | – | ||||||||||||||||||||

Sales – total | 2,099 | 670 | 746 | 462 | – | (282 | ) | 3,695 | ||||||||||||||||||||

Freight, transportation and distribution | – | (95 | ) | (74 | ) | (58 | ) | – | 19 | (208 | ) | |||||||||||||||||

Net sales | 2,099 | 575 | 672 | 404 | – | (263 | ) | |||||||||||||||||||||

Cost of goods sold | (1,691 | ) | (280 | ) | (524 | ) | (375 | ) | – | 230 | (2,640 | ) | ||||||||||||||||

Gross margin | 408 | 295 | 148 | 29 | – | (33 | ) | 847 | ||||||||||||||||||||

Selling expenses | (523 | ) | (3 | ) | (8 | ) | (3 | ) | 5 | – | (532 | ) | ||||||||||||||||

General and administrative expenses | (23 | ) | (3 | ) | (6 | ) | (3 | ) | (84 | ) | – | (119 | ) | |||||||||||||||

Provincial mining and other taxes | – | (48 | ) | – | – | – | – | (48 | ) | |||||||||||||||||||

Earnings of equity-accounted investees | 2 | – | 4 | – | 1 | – | 7 | |||||||||||||||||||||

Other income (expenses) | 3 | (4 | ) | (6 | ) | – | (72 | ) | – | (79 | ) | |||||||||||||||||

(Loss) Earnings before finance costs and income taxes | (133 | ) | 237 | 132 | 23 | (150 | ) | (33 | ) | 76 | ||||||||||||||||||

Depreciation and amortization | 123 | 91 | 129 | 51 | 17 | – | 411 | |||||||||||||||||||||

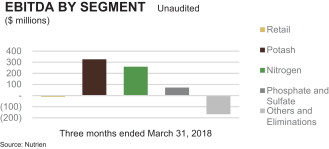

EBITDA1 | (10 | ) | 328 | 261 | 74 | (133 | ) | (33 | ) | 487 | ||||||||||||||||||

Assets2 | 13,709 | 13,360 | 5,615 | 2,493 | 10,861 | – | 46,038 | |||||||||||||||||||||

| 1 | EBITDA is a non-IFRS measure calculated as net (loss) earnings from continuing operations before finance costs, income taxes and depreciation and amortization. Nutrien uses EBITDA as a supplemental measure. EBITDA is frequently used by investors and analysts for valuation purposes when multiplied by a factor to estimate the enterprise value of a company. EBITDA is also used in determining annual incentive compensation for certain management employees and in calculating certain of the company’s debt covenants. Generally, this measure is a numerical measure of a company’s performance, financial position or cash flows that either excludes or includes amounts that are not normally excluded or included in the most directly comparable measure calculated and presented in accordance with IFRS. EBITDA is not a measure of financial performance (nor does it have a standardized meaning) under IFRS. In evaluating this measure, investors should consider that the methodology applied in calculating such measures may differ among companies and analysts. The company uses both IFRS and certain non-IFRS measures to assess performance. Management believes the non-IFRS measures provide useful supplemental information to investors in order that they may evaluate Nutrien’s financial performance using the same measures as management. Management believes that, as a result, the investor is afforded greater transparency in assessing the financial performance of the company. These non-IFRS financial measures should not be considered as a substitute for, nor superior to, measures of financial performance prepared in accordance with IFRS. |

| 2 | Included in the total assets relating to the others segment are $1,150 relating to the investments held for sale as described in Note 19. Goodwill related to the Merger is not allocated due to the timing of close and the provisional status of the purchase price allocation. |

$847

Gross Margin

Earned from all

nutrients

in the first quarter of 2018

| Nutrien 2018 First Quarter Interim Report | 65 |

| Unaudited | in millions of US dollars except as otherwise noted |

| Three Months Ended March 31, 2017 | ||||||||||||||||||||||||

| Potash | Nitrogen | Phosphate and Sulfate | Others | Eliminations | Consolidated | |||||||||||||||||||

Sales – third party | $ | 429 | $ | 375 | $ | 308 | $ | – | $ | – | $ | 1,112 | ||||||||||||

– intersegment | – | 22 | – | – | (22 | ) | – | |||||||||||||||||

Sales – total | 429 | 397 | 308 | – | (22 | ) | 1,112 | |||||||||||||||||

Freight, transportation and distribution | (64 | ) | (32 | ) | (37 | ) | – | – | (133 | ) | ||||||||||||||

Net sales | 365 | 365 | 271 | – | (22 | ) | ||||||||||||||||||

Cost of goods sold | (200 | ) | (268 | ) | (260 | ) | – | 22 | (706 | ) | ||||||||||||||

Gross margin | 165 | 97 | 11 | – | – | 273 | ||||||||||||||||||

Selling expenses | (2 | ) | (4 | ) | (2 | ) | (1 | ) | – | (9 | ) | |||||||||||||

General and administrative expenses | (2 | ) | (1 | ) | (1 | ) | (37 | ) | – | (41 | ) | |||||||||||||

Provincial mining and other taxes | (33 | ) | – | – | – | – | (33 | ) | ||||||||||||||||

Other expenses | (5 | ) | (2 | ) | (1 | ) | (7 | ) | – | (15 | ) | |||||||||||||

Earnings (loss) before finance costs and income taxes | 123 | 90 | 7 | (45 | ) | – | 175 | |||||||||||||||||

Depreciation and amortization | 55 | 50 | 58 | 9 | – | 172 | ||||||||||||||||||

EBITDA | 178 | 140 | 65 | (36 | ) | – | 347 | |||||||||||||||||

Assets1 | 9,784 | 2,510 | 2,324 | 2,693 | – | 17,311 | ||||||||||||||||||

| 1 | Included in the total assets relating to the others segment are $1,969 relating to the investments held for sale as described in Note 19. |

| 66 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

The company has disaggregated revenue from contracts with customers by product line or geographic location for each reportable segment, as it believes this best depicts how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.

| Three Months Ended | ||||||||

| Retail sales by product line | March 31, 2018 | March 31, 2017 | ||||||

Crop nutrients | $ | 684 | $ | – | ||||

Crop protection products | 774 | – | ||||||

Seed | 341 | – | ||||||

Merchandise | 149 | – | ||||||

Services and other | 151 | – | ||||||

| $ | 2,099 | $ | – | |||||

| Manufactured Potash sales by geography | ||||||||

North America | $ | 346 | $ | 231 | ||||

Offshore | 324 | 198 | ||||||

| $ | 670 | $ | 429 | |||||

| Nitrogen sales by product line | ||||||||

Manufactured Product | ||||||||

Ammonia | $ | 236 | $ | 169 | ||||

Urea | 232 | 97 | ||||||

Solutions and nitrates | 155 | 125 | ||||||

Other nitrogen and purchased products | 123 | 6 | ||||||

| $ | 746 | $ | 397 | |||||

| Phosphate and Sulfate sales by product line | ||||||||

Manufactured Product | ||||||||

Fertilizer | $ | 276 | $ | 161 | ||||

Feed and Industrial | 118 | 146 | ||||||

Ammonium sulfate | 20 | – | ||||||

Other phosphate and purchased products | 48 | 1 | ||||||

| $ | 462 | $ | 308 | |||||

| Nutrien 2018 First Quarter Interim Report | 67 |

| Unaudited | in millions of US dollars except as otherwise noted |

| Provincial Mining and Other Taxes |

Under Saskatchewan provincial legislation, the company is subject to resource taxes, including the potash production tax and the resource surcharge.

| For the Three Months Ended March 31, | ||||||||

| 2018 | 2017 | |||||||

Potash production tax | $ | 28 | $ | 22 | ||||

Saskatchewan resource surcharge and other | 20 | 11 | ||||||

| $ | 48 | $ | 33 | |||||

| Other Expenses |

| For the Three Months Ended March 31, | ||||||||

| 2018 | 2017 | |||||||

| (Note 32) | ||||||||

Foreign exchange gain | $ | 2 | $ | 1 | ||||

Merger and related costs | (66 | ) | (9 | ) | ||||

Other expenses | (15 | ) | (7 | ) | ||||

| $ | (79 | ) | $ | (15 | ) | |||

| Finance Costs |

Finance costs mainly arise from interest expense on long-term senior notes and debentures.

| For the Three Months Ended March 31, | ||||||||

| 2018 | 2017 | |||||||

Interest expense on | ||||||||

Short-term debt | $ | 18 | $ | 1 | ||||

Long-term debt | 92 | 52 | ||||||

Interest on net defined benefit pension and other post-retirement plan obligations (Note 26) | 5 | 5 | ||||||

Unwinding of discount on asset retirement obligations (Note 18) | 7 | 4 | ||||||

Borrowing costs capitalized to property, plant and equipment | (2 | ) | (3 | ) | ||||

Other interest income | (1 | ) | – | |||||

| $ | 119 | $ | 59 | |||||

Borrowing costs capitalized to property, plant and equipment during the three months ended March 31, 2018 were calculated by applying an average capitalization rate of 4.5 percent (2017 – 4.4 percent) to expenditures on qualifying assets.

See Note 10 for interest paid.

| 68 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

| Note 8 | Income Taxes |

This note explains the company’s income tax recovery (expense) andtax-related balances within the interim financial statements.

Accounting Policies |

The company operates in a specialized industry and in several tax jurisdictions. As a result, its income is subject to various rates of taxation. Taxation on items recognized in the condensed consolidated statements of (loss) earnings, other comprehensive income (“OCI”) or contributed surplus is recognized in the same location as those items.

Taxation on earnings is comprised of current and deferred income tax.

| Current income tax is: | Deferred income tax is: | |

• the expected tax payable on the taxable earnings for the period;

• calculated using rates enacted or substantively enacted at the condensed consolidated balance sheet date in the countries where the company’s subsidiaries, held for sale investees and equity-accounted investees operate and generate taxable earnings; and

• inclusive of any adjustment to income tax payable or recoverable in respect of previous years. | • recognized using the liability method;

• based on temporary differences between financial statements’ carrying amounts of assets and liabilities and their respective income tax bases; and

• determined using tax rates that have been enacted or substantively enacted by the condensed consolidated balance sheet date and are expected to apply when the related deferred income tax asset is realized or the deferred income tax liability is settled. |

The realized and unrealized excess tax benefit from share-based compensation arrangements is recognized in contributed surplus as current and deferred tax, respectively.

Uncertain income tax positions are accounted for using the standards applicable to current income tax liabilities and assets; i.e., both liabilities and assets are recorded when probable and measured at the amount expected to be paid to (recovered from) the taxation authorities using the company’s best estimate of the amount.

Deferred income tax is not accounted for:

| • | with respect to investments in subsidiaries and equity-accounted investees where the company is able to control the reversal of the temporary difference and that difference is not expected to reverse in the foreseeable future; and |

| • | if arising from initial recognition of an asset or liability in a transaction, other than a business combination, that at the time of the transaction affects neither accounting nor taxable profit or loss. |

Deferred income tax assets are reviewed at each balance sheet date and amended to the extent that it is no longer probable that the related tax benefit will be realized.

Accounting Estimates and Judgments |

Estimates and judgments to determine the company’s taxes are impacted by:

| • | the breadth of the company’s operations; and |

| • | global complexity of tax regulations. |

The final taxes paid, and potential adjustments to tax assets and liabilities, are dependent upon many factors including:

| • | negotiations with taxation authorities in various jurisdictions; |

| • | outcomes of tax litigation; and |

| • | resolution of disputes arising from federal, provincial, state and local tax audits. |

Estimates and judgments are used to recognize the amount of deferred tax assets, which:

| • | includes the probability that future taxable profit will be available to use deductible temporary differences; and |

| • | could be reduced if projected earnings are not achieved or increased if earnings previously not projected becomes probable. |

| Nutrien 2018 First Quarter Interim Report | 69 |

| Unaudited | in millions of US dollars except as otherwise noted |

Accounting Policies continued

Income tax assets and liabilities are offset when:

| For current income taxes, the company has: | For deferred income taxes: | |

• a legally enforceable right 1 to offset the recognized amounts; and

• the intention to settle on a net basis or realize the asset and settle the liability simultaneously. | • the company has a legally enforceable right to set off current tax assets against current tax liabilities; and

• they relate to income taxes levied by the same taxation authority on either: (1) the same taxable entity; or (2) different taxable entities intending to settle current tax liabilities and assets on a net basis, or realize assets and settle liabilities simultaneously in each future period. 2 | |

1 For income taxes levied by the same taxation authority and the authority permits the company to make or receive a single net payment or receipt.

2 In which significant amounts of deferred tax liabilities or assets expected are to be settled or recovered. | ||

Accounting Estimates and Judgments continued

Supporting Information

A separate estimated average annual effective income tax rate was determined for each taxing jurisdiction and applied individually to the interim periodpre-tax income from continuing operations for each jurisdiction.

| Three Months Ended March 31 | Ordinary earnings for the three months ended March 31, 2018 were negative as compared to positive earnings for the three months ended March 31, 2017. This produced very different weightings between jurisdictions on a quarter-over-quarter basis. This resulted in an increase in the actual effective tax rate on ordinary earnings. Compared to the same period last year, earnings were significantly lower in the United States and Canada and higher in lower-tax jurisdictions resulting in overall lower income taxes. | |||||||||

| Income Tax Related to Continuing Operations | 2018 | 2017 | ||||||||

Income tax recovery (expense) | $ | 42 | $ | (10 | ) | |||||

Actual effective tax rate on ordinary earnings | 89 | % | 12 | % | ||||||

Actual effective tax rate including discrete items | 95 | % | 8 | % | ||||||

Discrete tax adjustments that impacted the tax rate | $ | 3 | $ | 5 | ||||||

Income Tax Balances

Income tax balances within the condensed consolidated balance sheet were comprised of the following:

| Income Tax Assets (Liabilities) | Balance Sheet Location | March 31, 2018 | December 31, 2017 | |||||||

Current income tax assets | ||||||||||

Current | Receivables (Note 11) | $ | 152 | $ | 24 | |||||

Non-current | Other assets (Note 14) | 63 | 64 | |||||||

Deferred income tax assets | Other assets (Note 14) | 149 | 18 | |||||||

Total income tax assets | $ | 364 | $ | 106 | ||||||

Current income tax liabilities | ||||||||||

Current | Payables and accrued charges (Note 16) | $ | (57 | ) | $ | (16 | ) | |||

Non-current | Othernon-current liabilities | (81 | ) | (43 | ) | |||||

Deferred income tax liabilities | Deferred income tax liabilities | (2,762 | ) | (2,205 | ) | |||||

Total income tax liabilities | $ | (2,900 | ) | $ | (2,264 | ) | ||||

| 70 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

Amounts and expiry dates of unused tax losses and unused tax credits as at January 1, 2018 were:

| Amount | Expiry Date | Subsequent to March 31, 2018, capital losses totaling $675 were realized upon completion of a debt restructuring in Canada. Deferred tax assets will not be recognized for these capital losses. | ||||||

Unused operating losses | $ | 314 | 2018 – Indefinite | |||||

Unused tax credits | $ | 59 | 2018 – Indefinite | |||||

Unused capital losses | $ | 17 | None | |||||

| Net Earnings per Share |

Basic net earnings per share provides a measure of the interests of each ordinary common share in the company’s performance over the period.

Diluted net earnings per share adjusts basic net earnings per share for the effects of all dilutive potential common shares.

| For the Three Months Ended March 31, | ||||||||

| 20182 | 2017 | |||||||

Basic net earnings per share1 | ||||||||

Net (loss) earnings from continuing operations available to common shareholders | $ | (1 | ) | $ | 106 | |||

Net earnings from discontinued operations available to common shareholders | – | 43 | ||||||

Net (Loss) Earnings | $ | (1 | ) | $ | 149 | |||

Weighted average number of common shares | 642,690,000 | 839,911,000 | ||||||

Basic net earnings per share from continuing operations | $ | – | $ | 0.13 | ||||

Basic net earnings per share from discontinued operations | $ | – | $ | 0.05 | ||||

Basic net earnings per share from continuing and discontinued operations | $ | – | $ | 0.18 | ||||

Diluted net earnings per share1 | ||||||||

Net (loss) earnings from continuing operations available to common shareholders | $ | (1 | ) | $ | 106 | |||

Net earnings from discontinued operations available to common shareholders | – | 43 | ||||||

Net (Loss) Earnings | $ | (1 | ) | $ | 149 | |||

Weighted average number of common shares | 642,690,000 | 839,911,000 | ||||||

Dilutive effect of stock options | 521,000 | 251,000 | ||||||

Dilutive effect of share-settled performance share units (“PSUs”) | 7,000 | 49,000 | ||||||

Weighted average number of diluted common shares | 643,218,000 | 840,211,000 | ||||||

Diluted net earnings per share from continuing operations | $ | – | $ | 0.13 | ||||

Diluted net earnings per share from discontinued operations | $ | – | $ | 0.05 | ||||

Diluted net earnings per share from continuing and discontinued operations | $ | – | $ | 0.18 | ||||

| 1 | Net earnings per share calculations are based on dollar and share amounts each rounded to the nearest thousand. |

| 2 | The number of shares, stock options and share-settled PSUs reflect the Merger. Refer to Note 3 for details. |

Net earnings per share = net earnings available to common shareholders / weighted average number of common shares issued and outstanding during the period. Diluted net earnings per share incorporated the following adjustments. The denominator was:

Ù | increased by the total of the additional common shares that would have been issued assuming exercise of all stock options with exercise prices at or below the average market price for the period; |

Ù | increased by the total of the additional share-settled PSUs that could be issued if vesting criteria are achieved; and |

Ú | decreased by the number of shares that the company could have repurchased if it had used the assumed proceeds from the exercise of stock options to repurchase them on the open market at the average share price for the period. |

For performance-based stock option plans, the number of contingently issuable common shares included in the calculation was based on the number of shares, if any, that would be issuable if the end of the reporting period was the end of the performance period and the effect was dilutive.

Options excluded from the calculation of diluted net earnings per share due to the option exercise prices being greater than the average market price of common shares were as follows:

| For the Three Months Ended March 31, | ||||||||

| 2018 | 2017 | |||||||

Number of options excluded | 7,472,060 | 13,151,912 | ||||||

Performance option plan years fully excluded |

| 2008 – 2015 | | 2008 – 2014, | | |||

Stock option plan years fully excluded | 2015, 2018 | – | ||||||

| Nutrien 2018 First Quarter Interim Report | 71 |

| Unaudited | in millions of US dollars except as otherwise noted |

| Consolidated Statements of Cash Flows |

| Accounting Policy | ||||||||

| Highly liquid investments with a maturity of three months or less from the date of purchase are considered to be cash equivalents. | ||||||||

| For the Three Months Ended March 31 | 2018 | 2017 | ||||||||||||||

| (Note 32) | ||||||||||||||||

Reconciliation of cash (used in) provided by operating activities | ||||||||||||||||

Net (loss) earnings | $ | (1 | ) | $ | 149 | |||||||||||

Adjustments to reconcile net (loss) earnings to cash (used in) provided by operating activities | ||||||||||||||||

Depreciation and amortization | 411 | 172 | ||||||||||||||

Net undistributed earnings of equity-accounted investees (Note 19) | (6 | ) | (37 | ) | ||||||||||||

Share-based compensation (Note 27) | 16 | 5 | ||||||||||||||

Recovery of deferred income tax (Note 8) | (8 | ) | (14 | ) | ||||||||||||

Asset retirement obligations and accrued environmental costs (Note 18) | (18 | ) | (1 | ) | ||||||||||||

Other long-term liabilities and miscellaneous | 6 | 19 | ||||||||||||||

|

|

|

| |||||||||||||

Subtotal of adjustments | 401 | 144 | ||||||||||||||

Changes innon-cash operating working capital | ||||||||||||||||

Receivables | (187 | ) | 15 | |||||||||||||

Inventories | (1,701 | ) | (49 | ) | ||||||||||||

Prepaid expenses and other current assets | 645 | (5 | ) | |||||||||||||

Payables and accrued charges | 503 | (31 | ) | |||||||||||||

|

|

|

| |||||||||||||

Subtotal of changes innon-cash operating working capital | (740 | ) | (70 | ) | ||||||||||||

Cash (used in) provided by operating activities | $ | (340 | ) | $ | 223 | |||||||||||

Supplemental cash flows disclosure | ||||||||||||||||

Interest paid | $ | 114 | $ | 29 | ||||||||||||

Income taxes paid | $ | 29 | $ | 15 | ||||||||||||

The following is a summary of changes in liabilities arising from financing activities:

| Short-term debt and current portion of Long-term debt 1 | Long-term debt | Total | ||||||||||

Balance – December 31, 2017 | $ | 730 | $ | 3,711 | $ | 4,441 | ||||||

Cash flows1 | 494 | (4 | ) | 490 | ||||||||

Non-cash changes | (5 | ) | (27 | ) | (32 | ) | ||||||

Reclassifications | 518 | (518 | ) | – | ||||||||

Debt acquired in Merger (Note 3) | 878 | 4,930 | 5,808 | |||||||||

Foreign currency translation | – | (1 | ) | (1 | ) | |||||||

Balance – March 31, 2018 | $ | 2,615 | $ | 8,091 | $ | 10,706 | ||||||

Balance – December 31, 2016 | $ | 884 | $ | 3,707 | $ | 4,591 | ||||||

Cash flows1 | 21 | – | 21 | |||||||||

Balance – March 31, 2017 | $ | 905 | $ | 3,707 | $ | 4,612 | ||||||

| 1 | Cash inflows and cash outflows arising from short-term debt transactions are presented on a net basis. |

| 72 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

| Receivables |

Receivables represent amounts the company expects to collect from other parties. Trade receivables consist mainly of amounts owed to Nutrien by its customers, the largest individual customer being the related party, Canpotex.

Accounting Policies |

Trade receivables are recognized initially at fair value and subsequently measured at amortized cost less provision for impairment of trade accounts receivable. When a trade receivable is uncollectible, it is written off against the provision. Subsequent recoveries of amounts previously written off are credited to the condensed consolidated statements of (loss) earnings.

|

Vendors may offer various incentives to purchase products for resale. Vendor rebates and prepay discounts are accounted for as a reduction of the prices of the suppliers’ products. Rebates based on the amount of materials purchased reduce cost of goods as inventory is sold. Rebates are offset based on sales volume to cost of goods sold if the rebate has been earned based on sales volume of products.

|

| Rebates that are probable and can be reasonably estimated are accrued. Rebates that are not probable or estimable are accrued when certain milestones are achieved. Rebates not covered by binding agreements or published vendor programs are accrued when conclusive documentation of right of receipt is obtained. |

Supporting Information

| March 31, 2018 | December 31, 2017 | ||||||

Trade accounts – third parties | $ | 2,494 | $ | 314 | ||||

– Canpotex (Note 28) | 171 | 82 | ||||||

Less provision for impairment of trade accounts receivable | (19 | ) | (6 | ) | ||||

| 2,646 | 390 | |||||||

Rebates | 271 | – | ||||||

Income taxes receivable (Note 8) | 152 | 24 | ||||||

Othernon-trade accounts | 161 | 75 | ||||||

| $ | 3,230 | $ | 489 | |||||

| Accounting Estimates and Judgments |

Determining when amounts are deemed uncollectible requires judgment.

Vendor arrangements are diverse and can be highly complex. When vendor rebates are probable and can be estimated, a rebate will be accrued by estimating the point at which performance has been completed under an agreement. The amount of the accrual is determined by analyzing and reviewing historical trends to apply negotiated rates to estimated and actual purchase volumes. Estimated amounts accrued throughout the year could be impacted if actual purchase volumes differ from projected volumes.

| Nutrien 2018 First Quarter Interim Report | 73 |

| Unaudited | in millions of US dollars except as otherwise noted |

| Inventories |

Inventories consist of retail inventory (crop nutrients, crop protection products, seed and merchandise products) and products from the potash, nitrogen and phosphate and sulfate segment in varying stages of the production process.

Accounting Policies | ||

Inventories are valued monthly at the lower of cost and net realizable value. Costs, allocated to inventory using the weighted average cost method, include direct acquisition costs, direct costs related to units of production and a systematic allocation of fixed and variable production overhead, as applicable.

Net realizable value is based on:

| ||

| For products for resale, finished goods and raw materials | For materials and supplies | |

• selling price of the finished product (in ordinary course of business); • less the estimated costs of completion; and • less the estimated costs to make the sale. | • replacement cost, considered to be the best available measure of net realizable value. |

| A writedown is recognized if carrying amount exceeds net realizable value, and may be reversed if the circumstances which caused it no longer exist. | ||

Supporting Information

| March 31, 2018 | December 31, 2017 | ||||||

Purchased for resale | $ | 4,513 | $ | – | ||||

Finished products | 557 | 260 | ||||||

Intermediate products | 215 | 202 | ||||||

Raw materials | 248 | 62 | ||||||

Materials and supplies | 382 | 264 | ||||||

| $ | 5,915 | $ | 788 | |||||

Accounting Estimates and Judgments |

Judgment involves determining:

| • | the appropriate measure of net realizable value; |

| • | inputs to the determination of net realizable value, consisting of a combination of interrelated demand and supply variables; and |

| • | the allocation of production overhead to inventories. |

The carrying amount of inventory recorded at net realizable value was $55 as at March 31, 2018 (December 31, 2017 – $45), with the remaining inventory recorded at cost.

| 74 | Nutrien 2018 First Quarter Interim Report |

| Unaudited | in millions of US dollars except as otherwise noted |

| Property, Plant and Equipment |

The majority of the company’s tangible assets are the buildings, machinery and equipment used to produce and/or distribute its products and services. These assets are depreciated over their estimated useful lives.

Accounting Policies |

Property, plant and equipment (which include certain mine development costs,pre-stripping costs and assets under construction) are carried at cost less accumulated depreciation and any recognized impairment loss.

Cost includes all expenditures directly attributable to bringing the asset to the location and installing it in working condition for its intended use, including:

• income or expenses;1

• a reduction for investment tax credits to which the company is entitled;

• additions, betterments and renewals; and

• borrowing costs during construction.2

Each component of an item of property, plant and equipment with a cost that is significant in relation to the item’s total cost is depreciated separately. When the cost of replacing part of an item of property, plant and equipment is capitalized, the carrying amount of the replaced part is derecognized. The cost of major inspections and overhauls is capitalized and depreciated over the period until the next major inspection or overhaul. Maintenance and repair expenditures that do not improve or extend productive life are expensed in the period incurred.

Any gain or loss arising on the disposal or retirement of an item of property, plant and equipment is determined as the difference between the sale proceeds and the carrying amount of the asset and is recognized in earnings before finance costs and income taxes. |

1 Derived from the necessity to bring an asset under construction to the location and condition necessary to be capable of operating in the manner and location intended.

2 The capitalization rate is based on the weighted average interest rate on all of the company’s outstanding third-party debt. Capitalization ceases when assets are substantially ready for their intended use.

|

Accounting Estimates and Judgments |

Judgment involves determining:

| • | which costs are directly attributable (e.g., labor, overhead) and when income or expenses derived from an asset under construction are recognized as part of the asset cost; |

| • | appropriate timing for ceasing costcapitalization1, considering the circumstances and the industry in which the asset is to be operated, normally predetermined by management with reference to such factors as productive capacity; |

| • | the appropriate level of componentization (for individual components for which different depreciation methods or rates are appropriate); |

| • | which repairs and maintenance constitute major inspections and overhauls; and |

| • | the appropriate life over which such costs should be amortized. |

Property, plant and equipment directly related to the potash, nitrogen and phosphate and sulfate operations are depreciated using theunits-of-production method based on the shorter of estimates of reserves or service lives.Pre-stripping costs are depreciated on aunits-of-production basis over the ore mined from the mineable acreage stripped. Land is not depreciated. Other asset classes are depreciated on a straight-line basis.

The following estimated useful lives have been applied to the majority of property, plant and equipment assets as at March 31, 2018:

| Useful Life Range (years) | Weighted Average Useful Life (years) 3 | |||||||

Land improvements | 5 to 70 | 34 | ||||||

Buildings and improvements | 5 to 70 | 44 | ||||||

Machinery and equipment2 | 2 to 60 | 25 | ||||||

Asset residual values and useful lives are reviewed, and adjusted if appropriate, at the end of each reporting period. Changes in the expected useful life or the expected pattern of consumption of future economic benefits embodied in the asset are accounted for by changing the depreciation period or method, as appropriate, and are treated as changes in accounting estimates.

The company assesses its existing assets and their depreciable lives in connection with the review at the end of each reporting period. When it is determined that assigned asset lives do not reflect the expected remaining period of benefit, prospective changes are made to their depreciable lives. Uncertainties are inherent in estimating reserve quantities, particularly as they relate to assumptions regarding future prices, the geology of the company’s mines, the mining methods used, and the related costs incurred to develop and mine its reserves. Changes in these assumptions could result in material adjustments to reserve estimates, which could result in impairments or changes to depreciation expense in future periods, particularly if reserve estimates are reduced.

1 Generally when the asset or asset under construction is substantially complete and in the location and condition necessary for it to be capable of operating in the manner intended by management.

2 Comprised primarily of plant equipment.

3 Weighted by carrying amount as at March 31, 2018. Carrying amounts do not include preliminary fair value adjustments related to the Merger.

|

| Nutrien 2018 First Quarter Interim Report | 75 |

| Unaudited | in millions of US dollars except as otherwise noted |

Accounting policies, estimates and judgments related to impairment of long-lived assets are included within Note 31.

Supporting Information

Land and Improvements | Buildings and Improvements | Machinery and Equipment | Assets Under Construction | Total | ||||||||||||||||

Carrying amount – December 31, 2017 | $ | 1,591 | $ | 4,184 | $ | 6,744 | $ | 452 | $ | 12,971 | ||||||||||

Merger impact 1 | 452 | 2,947 | 3,988 | 396 | 7,783 | |||||||||||||||

Other acquisitions | 14 | (3 | ) | 40 | – | 51 | ||||||||||||||

Additions | 14 | 9 | 21 | 172 | 216 | |||||||||||||||

Disposals | (1 | ) | (1 | ) | (12 | ) | – | (14 | ) | |||||||||||