See Accompanying Notes to the Financial Statements.

Ellington Income Opportunities Fund (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a continuously offered, non-diversified, closed-end management company. The Fund is an interval fund that will offer to make quarterly repurchases of shares at the net asset value (“NAV”) of Class A shares, Class C shares, Class I shares, and Class M shares. The Fund offers four classes of shares: Class A, Class C, Class I, and Class M. Class A shares are offered at NAV plus a maximum sales charge of 5.75%. Class C, I, and M are offered at NAV.

Princeton Fund Advisors, LLC (the “Adviser”) serves as the Fund’s investment adviser. Ellington Global Asset Management, LLC (the “Sub-Adviser” or “Ellington”) serves as the Fund’s investment sub-adviser. The Fund’s investment objective is to seek total return, including capital gains and current income.

The Fund is organized as a statutory trust under the laws of the State of Delaware. The Fund commenced operations on November 13, 2018.

2. SIGNIFICANT ACCOUNTING POLICIES

The Fund’s financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The Fund is an investment company and, accordingly, follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services - Investment Companies including FASB Accounting Standards Update (“ASU”) 2013-08. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates and such differences could be material to the financial statements.

The following is a summary of the significant accounting policies followed by the Fund:

(A) Investments: In accordance with the authoritative guidance on fair value measurements and disclosures under GAAP, the Fund discloses the fair value of its investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to valuations based upon unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to valuations based upon unobservable inputs that are significant to the valuation (Level 3 measurements).

(B) Investment Transactions, Investment Income and Expense Recognition: Investment transactions are recorded on the trade date. Realized and unrealized gains and losses are calculated based on identified cost. Principal write-offs are treated as realized losses. Interest income is recorded as earned unless ultimate collection is in doubt. Generally, the Fund accretes market discounts and amortizes market premiums on debt securities using the effective yield method. Accretion of market discount and amortization of market premiums requires the use of a significant amount of judgment and the application of several assumptions including, but not limited to, prepayment assumptions and default rate assumptions. Expenses that are directly attributable to the Fund (the “Fund Expenses”) consist of permitted expenses determined in accordance with the terms of the governing documents. Fund Expenses are charged when incurred. Fund Expenses include, but are not limited to, operational expenses and other expenses associated with the operation of the Fund. The Fund’s expenses (other than class specific distribution fees) and realized and unrealized gains and losses are allocated proportionately each day based upon the relative net assets of each class.

(C) Cash: Cash and cash equivalents include cash. Cash is maintained at U.S. Bank National Association, member of FDIC. Balances might exceed federally insured limits.

Ellington Income Opportunities Fund

NOTES TO FINANCIAL STATEMENTS

June 30, 2019 (Unaudited)

(D) Income Taxes: The Fund has elected to be treated as, and to qualify each year for special tax treatment afforded to, a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code (“IRC”). In order to qualify as a RIC, the Fund must, among other things, satisfy income, asset diversification and distribution requirements. As long as it so qualifies, the Fund will not be subject to U.S. federal income tax to the extent that it distributes annually its investment company taxable income and its net capital gain. The Fund intends to distribute at least annually all or substantially all of such income and gain. If the Fund retains any investment company taxable income or net capital gain, it will be subject to U.S. federal income tax on the retained amount at regular corporate tax rates. In addition, if the Fund fails to qualify as a RIC for any taxable year, it will be subject to U.S. federal income tax on all of its income and gains at regular corporate tax rates.

(E) Distributions to Shareholders: Distributions from investment income are declared and paid quarterly. Distributions from net realized capital gains, if any, are declared and paid annually and are recorded on the ex‐dividend date. The character of income and gains to be distributed is determined in accordance with income tax regulations, which may differ from GAAP.

(F) Indemnifications: In the normal course of business, the Fund enters into contracts that contain a variety of representations which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. However, the Fund expects the risk of loss to be remote.

(G) Recent Accounting Pronouncements: In August 2018, FASB issued Accounting Standards Update (“ASU”) 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework—Changes to the Disclosure Requirements for Fair Value Measurement (“ASU 2018-13”). The primary focus of ASU 2018-13 is to improve the effectiveness of the disclosure requirements for fair value measurements, specifically, removing the requirement to disclose the amount and reasons for transfers between level 1 and level 2 securities of the fair value hierarchy and the policy for timing of transfers. The changes affect all companies that are required to include fair value measurement disclosures. In general, the amendments in ASU 2018-13 are effective for all entities for fiscal years and interim periods within those fiscal years, beginning after December 15, 2019. An entity is permitted to early adopt the removed or modified disclosures upon the issuance of ASU 2018-13 and may delay adoption of the additional disclosures, which are required for public companies only, until their effective date.

The following is a description of the valuation methodologies used for the Fund’s financial instruments. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

Level 1 valuation methodologies include the observation of quoted prices (unadjusted) for identical assets or liabilities in active markets.

Level 2 valuation methodologies include the observation of (i) quoted prices for similar assets or liabilities in active markets, (ii) inputs other than quoted prices that are observable for the asset or liability (for example, interest rates and yield curves) in active markets and (iii) quoted prices for identical or similar assets or liabilities in markets that are not active.

Level 3 fair value methodologies include (i) the solicitation of valuations from third parties (typically, broker-dealers), (ii) the use of proprietary models that require the use of a significant amount of judgment and the application of various assumptions including, but not limited to, prepayment assumptions and default rate assumptions, and (iii) the assessment of observable or reported recent trading activity. The Fund utilizes such information to assign a good faith fair value (the estimated price that would be received to sell an asset or paid to transfer a liability in an orderly transaction at the valuation date) to each such financial instrument.

The Adviser seeks to obtain at least one third-party indicative valuation for each instrument, and obtains multiple indicative valuations when available. Third-party valuation providers often utilize proprietary models that are highly subjective and also require the use of a significant amount of judgment and the application of various assumptions including, but not limited to, prepayment and default rate assumptions. The Adviser has been able to obtain third-party indicative valuations on the vast majority of the Fund’s investments and expects to continue to solicit third-party valuations on substantially all investments in the future to the extent practical. The Adviser generally values each financial instrument at the average of all third-party valuations received. However, such third-party valuations are not binding, and while the Adviser generally does not adjust such valuations, the Adviser may challenge or reject a valuation when, based on validation criteria, the Adviser determines that such valuation is unreasonable or erroneous. Furthermore, the Adviser may determine, based on validation criteria, that for a given instrument the average of the third-party valuations received does not result in what the Adviser believes to be fair value, and in such circumstances the Adviser may override this average with their own good faith valuation. The validation criteria include the use of the Adviser’s own models, recent trading activity in the same or similar instruments, and valuations received from third parties.

Ellington Income Opportunities Fund

NOTES TO FINANCIAL STATEMENTS

June 30, 2019 (Unaudited)

The Adviser’s valuation process, including the application of validation criteria, is overseen and periodically reviewed by the Fund’s valuation committee. Because of the inherent uncertainty of valuations, these estimated values may differ significantly from the values that would have been used had a ready market for the financial instruments existed, and the differences could be material to the financial statements.

The table below reflects the value of the Fund’s Level 1, Level 2 and Level 3 financial instruments measured at fair value as of June 30, 2019:

| Description | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Investments | | | | | | | | | | | | |

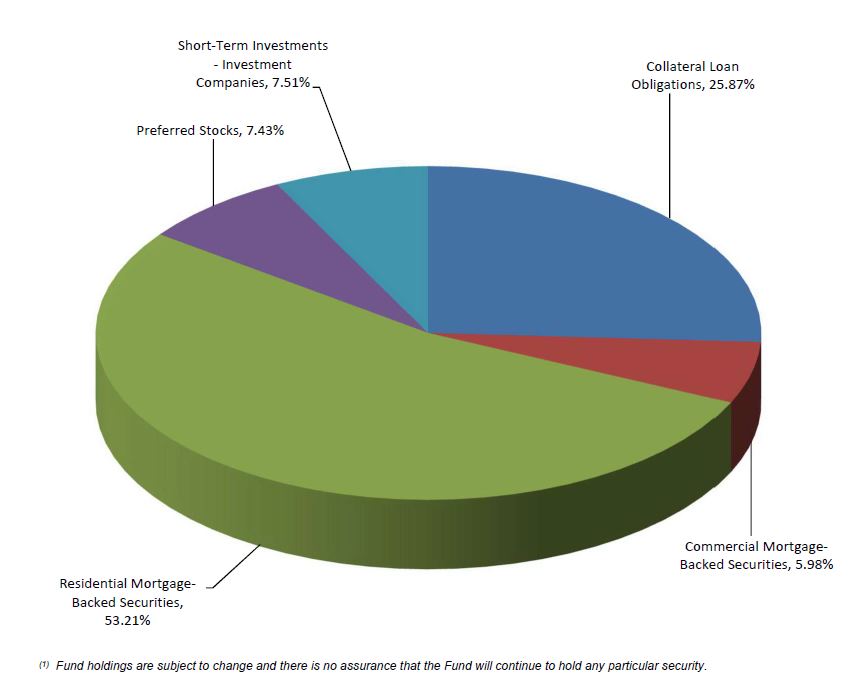

| Collateralized Loan Obligations | | $ | - | | | $ | 5,072,985 | | | $ | - | | | $ | 5,072,985 | |

| Commercial Mortgage-Backed Securities | | | - | | | | 1,172,762 | | | | - | | | | 1,172,762 | |

Residential Mortgage-Backed Securities | | | - | | | | 2,847,203 | | | | 7,585,962 | | | | 10,433,165 | |

Preferred Stocks | | | 1,457,909 | | | | - | | | | - | | | | 1,472,909 | |

Short-Term Investments | | | 1,471,898 | | | | - | | | | - | | | | 1,471,898 | |

| Total Investments | | $ | 2,929,807 | | | $ | 9,092,950 | | | $ | 7,585,962 | | | $ | 19,608,719 | |

| | | | | | | | | | | | | | | | | |

| Other Financial Instruments* | | | | | | | | | | | | | | | | |

| Swap Contracts | | $ | - | | | $ | 152,369 | | | $ | - | | | $ | 152,369 | |

*Other financial instruments are derivative instruments, such as swap contacts, which are reported at market value. | |

The Fund generally uses prices provided by an independent pricing service, broker, or agent bank, which provide non-binding indicative prices on or near the valuation date as the primary basis for fair value determinations for certain instruments. The independent pricing services typically value such securities based on one or more inputs, including but not limited to benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities, and pricing models such as yield measurers calculated using factors such as cash flows, financial or collateral performance and other reference data. In addition to these inputs, mortgage-backed and asset-backed obligations may utilize cash flows, prepayment information, default rates, delinquency and loss assumptions, collateral characteristics, credit enhancements, and specific deal information. These values are non-binding, and may not be determinative of fair value. Values are evaluated during the Fund's valuation process by management in conjunction with additional information about the instrument, similar instruments, market indicators and other information.

4. RELATED PARTY AGREEMENTS AND FEES

The Adviser serves as the investment adviser to the Fund. Under the terms of the management agreement between the Fund and the Adviser dated October 17, 2018 (the “Agreement”), the Adviser, subject to the oversight of the Board of Trustees (the “Board”), provides or arranges to be provided to the Fund such investment advice as it deems advisable and will furnish or arrange to be furnished a continuous investment program for the Fund consistent with the Fund’s investment objectives and policies. As compensation for its management services, the Fund agrees to pay to the Adviser a monthly fee in dollars at the annual rate of 1.85% of the Fund’s average daily net assets.

Ellington Income Opportunities Fund

NOTES TO FINANCIAL STATEMENTS

June 30, 2019 (Unaudited)

The Adviser and the Fund have entered into an expense limitation and reimbursement agreement under which the Adviser has agreed, until at least October 31, 2020, to waive its management fees and to pay or absorb the ordinary operating expenses of the Fund (excluding (i) interest expense, and any fees and expenses incurred in connection with credit facilities, if any, obtained by the Fund; (ii) transaction costs and other expenses incurred in connection with the acquisition, financing, maintenance, and disposition of the Fund’s investments and prospective investments, including without limitation bank and custody fees, brokerage commissions, legal, data, consulting and due diligence costs, servicing and property management costs; (iii) acquired fund fees and expenses; (iv) taxes; and (v) extraordinary expenses), to the extent that its management fees plus applicable distribution and shareholder servicing fees and the Fund’s ordinary operating expenses would otherwise exceed, on a year-to-date basis, 2.85%, 3.60%, 2.60%, and 2.20% per annum of the Fund’s average daily net assets attributable to Class A, Class C, Class I, and Class M shares, respectively. The Expense Limitation Agreement may not be terminated by the Adviser, but it may be terminated by the Board, on 60 days written notice to the Adviser. Any waiver or reimbursement by the Adviser is subject to repayment by the Fund within the three years from the date the Adviser waived any payment or reimbursed any expense, if (after taking the repayment into account) the Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or at the time of the reimbursement payment. The Adviser’s waived fees and reimbursed expenses that are subject to potential recoupment are as follows:

| Fiscal Year Incurred | | Amount Waived | | Amount Recouped | | Amount Subject to Potential Reimbursement | | Expiration Date |

| December 31, 2018 | | $185,928 | | $ - | | $185,928 | | December 31, 2021 |

| December 31, 2019 | | $281,438 | | $ - | | $281,438 | | December 31, 2022 |

The Adviser engaged Ellington, an investment adviser registered with the U.S. Securities & Exchange Commission, to act as the Fund’s sub-adviser pursuant to a Subadvisory Agreement dated October 17, 2018 between Ellington and the Adviser (the “Subadvisory Agreement”). Under the terms of the Subadvisory Agreement, the Sub-Advisor is paid directly by the Adviser.

Under Administration, Fund Accounting and Transfer Agent Servicing Agreements between the Fund and U.S. Bancorp Fund Services, LLC doing business as U.S. Bancorp Global Fund Services, LLC (“Global Fund Services”), Global Fund Services is paid a monthly fee based on the net asset value of the Fund. Global Fund Services acts as fund administrator, fund accountant, registrar and transfer agent to the Fund.

For the period ended June 30, 2019, the Fund used U.S. Bank National Association (“U.S. Bank”) as its custodian pursuant to a Custody Agreement between U.S. Bank and the Fund.

Northern Lights Compliance Services, LLC (“NLCS”) provides a Chief Compliance Officer to the Fund as well as related compliance services pursuant to a consulting agreement between NLCS and the Fund.

Two Trustees and certain Officers of the Fund are also Officers of the Adviser or Sub-Adviser. Trustees and Officers, other than the Chief Compliance Officer, affiliated with the Adviser are not compensated by the Fund for their services.

5. INVESTMENT TRANSACTIONS

The cost of purchases and proceeds from the sale of securities, other than short-term securities, for the period ended June 30, 2019 amounted to $11,834,928 and $3,897,026, respectively.

Ellington Income Opportunities Fund

NOTES TO FINANCIAL STATEMENTS

June 30, 2019 (Unaudited)

6. DERIVATIVE INSTRUMENTS

The Fund uses derivative instruments as part of its investment strategy to achieve its stated investment objective. The Fund’s derivative contracts held at period end are not accounted for as hedging instruments under GAAP. For financial reporting purposes, the Fund does not offset derivative assets and liabilities across derivative types that are subject to a master netting arrangement in the Statement of Assets and Liabilities.

The following table lists the fair value of derivative instruments held by the Fund by primary underlying risk and contracted type:

| | | Assets | | Liabilities |

Primary Underlying Risk: | | Swaps at Value | | Swaps at Value |

| Credit Risk | | $163,571 | | $(11,202) |

The following table lists the effect of derivative instruments held by the Fund by primary underlying risk and contract type on the Statement of Operations for the period ended June 30, 2019:

| | | Realized Gain/(Loss) on Derivatives recognized as a result of Operations | | Net Change in Unrealized Appreciation / (Depreciation) on

Derivatives recognized as a result of Operations |

Primary Underlying Risk: | | Swaps | | Swaps |

| Credit Risk | | $73,483 | | $56,135 |

The following table, as of June 30, 2019, discloses the Fund’s over-the-counter (“OTC”) derivative assets by counterparty and contract type, showing gross and net information about instruments and transactions available for a master netting agreement and the related collateral received or pledge by the Fund:

| | | | | Gross Amounts of

Assets Presented in the Statements of Assets & Liabilities | | | | | | Gross Amounts not offset in the Statement of Assets & Liabilities | | | |

| Counterparty | | Investment Type | | | Gross Amounts Available for Offset | | Net Amounts | | Financial Instruments | | Collateral Received | | Net Amount | |

| Morgan Stanley | | Credit Default Swap Contracts | | $163,571 | | $- | | $163,571 | | $- | | $- | | $163,571 |

As of June 30, 2019, the Fund did not have any OTC derivative liabilities to offset derivative assets or to disclose any gross and net information about.

Ellington Income Opportunities Fund

NOTES TO FINANCIAL STATEMENTS

June 30, 2019 (Unaudited)

The Fund’s average monthly notional amount of derivatives during the period ended June 30, 2019 were:

| Derivative Type | | Average Monthly Notional Amount |

| Credit Default Swaps | | |

| Average Amounts – Buy Protection | | $83,333 |

| Average Amounts – Sell Protection | | 8,666,667 |

It is the Fund’s intention to continue to qualify as a RIC under Subchapter M of the IRC and distribute all of its taxable income. Accordingly, no provision for federal income taxes is required in its financial statements.

The tax character of dividends paid to shareholders during the period ended December 31, 2018, was as follows:

Ordinary Income | | Net Long-Term Capital Gains | | Return of Capital | | Total Distributions Paid |

| $ 40,904 | | $ - | | $ - | | $ 40,904 |

The amount and character of income and capital gain distributions to be paid, if any, are determined in accordance with federal income tax regulations, which may differ from U.S. GAAP. These differences are primarily due to differences in the timing of recognition of gains or losses on investments.

The following information is provided on a tax basis as of December 31, 2018:

| | Tax cost of investments | | $ | 11,224,200 | |

| | Gross unrealized appreciation | | | 76,948 | |

| | Gross unrealized depreciation | | | (144,081 | ) |

| | Net unrealized depreciation | | | (67,133 | ) |

| | Undistributed ordinary income | | | 28,889 | |

| | Undistributed long-term gains | | | - | |

| | Other temporary differences | | | - | |

| | Total accumulated losses | | $ | (38,244 | ) |

As of December 31, 2018, for federal income tax purposes, there were no capital loss carryforwards.

There was no difference between book and tax basis net unrealized appreciation.

The Fund follows the authoritative guidance on accounting for and disclosure of uncertainty on tax positions, which requires management to determine whether a tax position of the Fund is more likely than not to be sustained upon examination by the applicable taxing authority, including resolution of any related appeals of litigation process, based on the technical merits of the position. The tax benefit to be recognized is measured as the largest amount of benefit that is greater than fifty percent likely of being realized upon ultimate settlement. The Fund did not have any unrecognized tax benefits or unrecognized tax liabilities as of December 31, 2018. The Fund does not expect any change in unrecognized tax benefits or unrecognized tax liabilities within the next year. In the normal course of business, the Fund may be subject to examination by federal, state, local and foreign jurisdictions, where applicable, for all open tax years.

Ellington Income Opportunities Fund

NOTES TO FINANCIAL STATEMENTS

June 30, 2019 (Unaudited)

8. SHAREHOLDER TRANSACTIONS

The Fund operates as an interval fund pursuant to Rule 23c-3 under the 1940 Act and, as such, has adopted a fundamental policy to make quarterly repurchase offers, at NAV, of no less than 5% and no more than 25% of the Fund’s shares outstanding on the Repurchase Request Deadline (as defined below). There is no guarantee that shareholders will be able to sell all of the shares they desire to sell in a quarterly repurchase offer, although each shareholder will have the right to require the Fund to purchase at least 5% of such shareholder’s shares in each quarterly repurchase. Liquidity will be provided to shareholders only through the Fund’s quarterly repurchases. Shareholders will be notified in writing of each quarterly repurchase offer and the date the repurchase offer ends (the “Repurchase Request Deadline”). Shares will be repurchased at the NAV per share determined as of the close of regular trading on the NYSE no later than the 14th day after the Repurchase Request Deadline, or the next business day if the 14th day is not a business day.

The Fund had 1,732,904 shares outstanding as of June 30, 2019. The Fund issued 591,471 shares through shareholder subscriptions, 17,463 shares through dividend reinvestments and did not repurchase any shares through shareholder redemptions during the period ended June 30, 2019.

Reverse Repurchase Agreements: The Fund may enter into reverse repurchase agreements. In a reverse repurchase agreement, the Fund delivers a security in exchange for cash to a financial institution, the counterparty, with a simultaneous agreement to repurchase the same or substantially the same security at an agreed upon price and date. The Fund is entitled to receive the principal and interest payments, if any, made on the security delivered to the counterparty during the term of the agreement. Cash received in exchange for securities delivered plus accrued interest payments to be made by the Fund to counterparties are reflected as a liability on the Statement of Assets and Liabilities. Interest payments made by the Fund to counterparties are recorded as a component of interest expense on the Statement of Operations. The Fund will segregate assets determined to be liquid by the Adviser or will otherwise cover its obligations under reverse repurchase agreements.

Reverse repurchase agreements involve the risk that the market value of the securities retained in lieu of sale by the Fund may decline below the price of the securities the Fund has sold but is obligated to repurchase. In the event the buyer of securities under a reverse repurchase agreement files for bankruptcy or becomes insolvent, such buyer or its trustee or receiver may receive an extension of time to determine whether to enforce the Fund's obligation to repurchase the securities, and the Fund's use of the proceeds of the reverse repurchase agreement may effectively be restricted pending such decision. Also, the Fund would bear the risk of loss to the extent that the proceeds of the reverse repurchase agreement are less than the value of the securities subject to such agreements.

For the six months ended June 30, 2019, the average daily balance and average interest rate in effect for reverse repurchase agreements were $732,348 and 3.88%, respectively. Outstanding reverse repurchase agreements as of June 30, 2019, were equal to 13.24% of the Fund’s net assets. The following is a summary of the reverse repurchase agreements by the type of collateral and the remaining contractual maturity of the agreements:

| | | Overnight and Continuous | | Up to 30 Days | | 30 to 90 Days | | Greater than 90 Days | | Total |

| Collateral Loan Obligation | | $- | | $2,360,000 | | $- | | $- | | $2,360,000 |

Ellington Income Opportunities Fund

NOTES TO FINANCIAL STATEMENTS

June 30, 2019 (Unaudited)

Below is the gross and net information about instruments and transactions eligible for offset in the Statement of Assets and Liabilities as well as instruments and transactions subject to an agreement similar to a master netting arrangement:

| | | | | | | | | Collateral | | |

| Description | | Gross Amounts of Recognized Liabilities | | Gross Amounts Offset in the Statement of Assets and Liabilities | | Net Amounts Presented in the Statement of Assets and Liabilities | | Non-Cash Collateral (Pledged) Received | | Cash Collateral (Pledged) Received | | Net Amount |

Reverse Repurchase Agreements | | $2,360,000 | | $- | | $2,360,000 | | $(2,360,000) | | $- | | $- |

| | | | | | | | | | | | | |

Reverse repurchase transactions are entered into by the Fund under Master Repurchase Agreements (“MRA”) which permit the Fund, under certain circumstances, including an event of default of the Fund (such as bankruptcy or insolvency), to offset payables under the MRA with collateral held with the counterparty and create one single net payment from the Fund. Upon a bankruptcy or insolvency of the MRA counterparty, the Fund is considered an unsecured creditor with respect to excess collateral and, as such, the return of excess collateral may be delayed. In the event the buyer of securities (i.e. the MRA counterparty) under a MRA files for bankruptcy or becomes insolvent, the Fund’s use of the proceeds of the agreement may be restricted while the other party, or its trustee or receiver, determines whether or not to enforce the Fund’s obligation to repurchase the securities.

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates presumption of control of the fund, under Section 2(a)(9) of the 1940 Act. As of June 30, 2019, National Financial Services held approximately 96% of the voting securities of the Fund.

Subsequent events after the date of these financial statements have been evaluated through the date the financial statements were issued.

Management has determined that there were no subsequent events to disclose in the financial statements.

Form N-Q

The Fund files its complete schedule of portfolio holdings for the first and third quarters of each fiscal year with the SEC on Form N-Q. The Fund’s Form N-Q is available without charge by visiting the SEC’s Web site at www.sec.gov.

Proxy Voting

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities owned by the Fund for the most recent 12-month period ended June 30 and information regarding how the Fund voted proxies relating to the portfolio of securities are available to stockholders without charge, upon request by calling the Adviser at (888) 862-3690.

Board of Trustees

The Fund’s prospectus and statement of additional information includes additional information about the Fund’s Trustees and is available upon request without charge by calling the Adviser at (888) 862-3690 or by visiting the SEC’s Web site at www.sec.gov.

Forward-Looking Statements

This report contains “forward-looking statements,’’ which are based on current management expectations. Actual future results, however, may prove to be different from expectations. You can identify forward-looking statements by words such as “may’’, “will’’, “believe’’, “attempt’’, “seem’’, “think’’, “ought’’, “try’’ and other similar terms. The Fund cannot promise future returns. Management’s opinions are a reflection of its best judgment at the time this report is compiled, and it disclaims any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.