UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-23383

LORD ABBETT CREDIT OPPORTUNITIES FUND

(Exact name of Registrant as specified in charter)

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Address of principal executive offices) (Zip code)

Lawrence B. Stoller, Esq.

Vice President, Secretary, and Chief Legal Officer

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 522-2388

Date of fiscal year end: 12/31

Date of reporting period: 12/31/2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1: | Report(s) to Shareholders. |

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Credit Opportunities Fund

For the fiscal year ended December 31, 2022

Table of Contents

Lord Abbett Credit Opportunities Fund

Annual Report

For the fiscal year ended December 31, 2022

From left to right: James L.L. Tullis, Independent Chair of the Lord Abbett Funds and Douglas B. Sieg, Trustee, President, and Chief Executive Officer of the Lord Abbett Funds. | | Dear Shareholders: We are pleased to provide you with this overview of the performance of Lord Abbett Credit Opportunities Fund for the fiscal year ended December 31, 2022. On this page and the following pages, we discuss the major factors that influenced fiscal year performance. For detailed and timely information about the Fund, please visit our website at www.lordabbett.com, where you can also access quarterly commentaries that provide updates on the Fund’s performance and other portfolio related updates. Thank you for investing in Lord Abbett mutual funds. We value the trust that you place in us and look forward to serving your investment needs in the years to come. Best regards,

Douglas B. Sieg

Trustee, President and Chief Executive Officer |

For the fiscal year ended December 31, 2022, the Fund returned -8.58%, reflecting performance at the net asset value (NAV) of Institutional Class shares with all distributions reinvested, compared to its benchmark, the ICE BofA U.S. High Yield Constrained Index1, which returned -11.21%.

The twelve-month period ending December 31, 2022 introduced meaningful headwinds for U.S. markets that led to selloffs in virtually all asset classes. The major risks over the period were inflationary pressures, which reached multi-decade

highs, and the most rapid pace of interest rate hikes implemented in history by the U.S. Federal Reserve (Fed). Rates spiked across the U.S. yield curve as a result, with U.S. Treasury yields at almost all maturities reaching their highest levels in years. Other notable challenges for markets included supply chain dislocations and labor shortages influenced in part by the Omicron variant of COVID-19, as well as escalating geopolitical tensions headlined by Russia’s invasion of Ukraine.

1

The surge in interest rates over the year caused softness in both major fixed income and equity indices. Equities fared the worst amid the sell-off, with the S&P 5002 returning -18.11% over the period and experiencing its worst year since the Global Financial Crisis (GFC) of 2008. The tech-heavy NASDAQ3 also logged its worst year since 2008, declining -32.54% over the period as growth-related stocks in semiconductor and software sectors suffered in the face of inflationary pressures. Within fixed income, higher rates caused underperformance in longer duration bonds. These included U.S. Treasuries4 and investment grade bonds5 which returned -12.46% and -15.76% over the period, respectively. However, high yield bond6 and leveraged loan7 indexes outperformed the investment grade index for the period because of their lower duration profiles. Notably, high yield bonds and leveraged loans returned -11.21% and -1.06%, respectively, outperforming higher quality bonds despite recessionary fears in the U.S. economy contributing to wider spreads. Leveraged loans in particular were able to significantly outperform relative to other assets given their insulation from interest rate volatility due to their floating-rate coupons.

Inflationary concerns began to take focus towards the end of 2021 before becoming a dominant storyline in 2022. Headline consumer price index (CPI) readings had hovered a little above 5% year-over-year for most of 2021, which led

investors to question whether this period of rising prices would be more persistent than originally thought. This debate intensified in the beginning of the year as inflation readings continued as climb throughout the first half of 2022, with CPI peaking at 9.1% year-over-year in June. The surge in prices was due primarily to an imbalance between supply and demand dynamics across multiple industries, including energy, food, and used cars.

Inflationary pressures throughout the period were most evident in energy costs, which rose more than 30% year-over-year by the end of June. The energy sector, which had been subject to rising consumer demand as global economies reopened from lockdowns induced by COVID-19, faced added friction with Russia’s invasion of Ukraine as Russia had been a large exporter of oil and certain minerals. Various sanctions were instilled on Russia from Western nations in response to their aggression towards Ukraine, which contributed to surging prices. Crude oil specifically reached over $100 per barrel, the highest value since 2014.

The Fed pivoted towards a much more hawkish stance on monetary policy during the period given the surge in inflation. After remaining mostly consistent in its messaging around expectations that price pressures would be transitory, elevated and more persistent inflation pressures caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the

2

federal funds rate at the March Federal Open Market Committee (FOMC) meeting, the first hike in more than three years. Six additional rate hikes followed in the succeeding months, one of 50 bps, and four consecutive hikes of 75 bps and an additional one of 50 bps as inflation prints continued to come mostly in hotter than expected, resulting in a federal funds rate at a range of 4.25% – 4.50% by the end of 2022. Bond yields shot up amid this aggressive policy, leading to a bearish curve flattening and ultimately periods of significant yield curve inversion, with the spread between the 2-year and 10-year Treasury yields hitting its most negative level in more than 40 years.

Key macroeconomic indicators trended lower throughout the period. Most notably, the U.S. reported real GDP decline of -1.6% in the first quarter of 2022 and -0.9% in the second quarter before returning to growth in the third quarter. Worries of an impending recession resulted in consumer sentiment dropping to levels worse than during the height of the COVID-19 pandemic and the GFC of 2008, according to the U.S. Consumer Confidence Index.

Despite rising recessionary signs, select bright spots in the U.S. economy supported the idea that a potential recession would be shallow. One of the most positive developments seemed to be the traction behind the peak inflation narrative, which gained momentum in the fourth quarter from lower-than-expected CPI prints in both October and November. In addition,

energy prices retracted from their multi-year highs, rent prices began to stabilize, and wage growth showed signs of softening. Job growth also remained strong in the period, and the U.S. national unemployment rate continued to hover around pre-COVID lows. Companies also cited relatively stable demand in both second and third quarter earnings seasons as consumers remained resilient despite higher prices. Separately, labor shortages eased, and supply chain frictions moderated, providing added benefits for companies managing generally higher input costs.

The Fund seeks to deliver total return by investing across a broad range of credit sectors. Our strategy focuses on identifying idiosyncratic credit ideas that possess a catalyst for price appreciation we believe is unrecognized by market participants. This flexible strategy utilizes a bottom-up approach and seeks investment candidates that possess favorable potential for return-for-risk characteristics. Portfolio construction focuses on balancing the most favorable opportunities while seeking prudent diversification.

The Fund’s allocation to select U.S. high yield bonds were some of the primary detractors from relative performance. These holdings were in certain sectors such as Retail and Leisure that exhibited greater sensitivity from elevated inflationary pressures given its effect on consumer spending and operating costs. An example of this was AMC Entertainment, Inc. (AMC),

3

one of the largest theater operators around the world. AMC’s operating performance has been impacted by a weak box office driven by both lower attendance and weak supply of movies to theaters due to both production disruptions and many studios preferring to distribute movies exclusively on streaming products than through theaters. However, we began to notice an improvement in movie attendance towards the end of the year and we believe that there are indications that movie supply should begin to normalize in 2024, although perhaps never reaching pre-pandemic levels. Party City, a large party supply retailer in the U.S., also underperformed and dragged on the Fund’s returns. The company faced challenges like helium price inflation and a weak macro-outlook from depressed demand by the lower income consumer. To partially offset these headwinds, the company has been executing on a cost reduction program, including workforce layoffs.

Performance was also impacted by the Fund’s position in Emerging Market bonds. Specifically, several China property developers such as Shimao Group Holdings and Sunac China Holdings, both companies that specialize in the property development of Chinese real estate markets, were detractors from performance. Our initial thesis in the sector had come under pressure given some of the specific headwinds in the sector, including escalated leverage and regulatory challenges, which forced us to reduce this

allocation. However, the fourth quarter of 2022 brought about modest easing of these headwinds. The most prominent was the removal of China’s Zero-COVID policy, which helped to positively reset near-term downside risks in the region. Additionally, the Chinese government indicated support for the property sector, creating additional tailwinds.

Although the Fund yielded negative returns for the year, there were select holdings in U.S. high yield bonds that were significant contributors to performance. These holdings were primarily in energy-related high yield issuers, which continued to be supported by a positive relationship to resilient commodity prices as well as more disciplined approaches to capital allocation. This helped energy companies, particularly those in the Exploration and Production (E&P) subsector, experience what we believe to be meaningful deleveraging and stronger balance sheets. Examples of these holdings included Callon Petroleum, Nabors Industries, and Oceaneering International. All three issuers are oil and natural gas E&P companies, and we believed they boasted strong reserve asset coverage, sufficient liquidity and operational flexibility. The Fund’s relative performance also benefited from Energy exposure through various bank loan and convertible holdings, two of which being BEP Ulterra Holdings, Inc and Permian Resources. The Fund’s investment in Scorpio Tankers (Scorpio) had also contributed to performance over the period. We initiated a convertible bond

4

position in March 2021 having owned a prior bond that restructured into this higher coupon, higher delta instrument. With the rise in oil prices and the premiums being paid for storage options, Scorpio saw day rates increase significantly along with earnings. We ultimately exercised our sell discipline by exiting the investment as our upside targets were met.

The Fund’s portfolio is actively managed and, therefore, its holdings and the weightings of a particular issuer or particular sector as a percentage of portfolio assets are subject to change. Sectors may include many industries.

1 The ICE BofA U.S. High Yield Constrained Index is a capitalization weighted index of all U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market.

2 The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

3 The Nasdaq Composite Index is the market capitalization-weighted index of over 2,500 common equities listed on the Nasdaq stock exchange.

4 As represented by the U.S. Treasury component of the Bloomberg U.S. Government Index as of 12/31/2022.

5 As represented by the Bloomberg US Corp Investment Grade Index as of 12/31/2022.

6 As represented by the ICE BofA U.S. High Yield Constrained Index as of 12/31/2022.

7 As represented by the Credit Suisse Leveraged Loan Index as of 12/31/2022.

Unless otherwise specified, indexes reflect total return, with all dividends reinvested. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Important Performance and Other Information Performance data quoted in the following pages reflect past performance and are no guarantee of future results. Current performance may be higher or lower than the performance quoted. The investment return and principal value of an investment in the Fund will fluctuate so that shares, on any given day or when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling Lord Abbett at 888-522-2388 or referring to www.lordabbett.com.

Except where noted, comparative Fund performance does not account for the deduction of sales charges and would be different if sales charges were included. The Fund offers classes of shares with distinct pricing options. For a full description of the differences in pricing alternatives, please see the Fund’s prospectus.

During certain periods shown, expense waivers and reimbursements were in place. Without such expense waivers and reimbursements, the Fund’s returns would have been lower.

The annual commentary above discusses the views of the Fund’s management and various portfolio holdings of the Fund as of December 31, 2022. These views and portfolio holdings may have changed after this date. Information provided in the commentary is not a recommendation to buy or sell securities. Because the Fund’s portfolio is actively managed and may change significantly, the Fund may no longer own the securities described above or may have otherwise changed its position in the securities. For more recent information about the Fund’s portfolio holdings, please visit www.lordabbett.com.

A Note about Risk: See Notes to Financial Statements for a discussion of investment risks. For a more detailed discussion of the risks associated with the Fund, please see the Fund’s prospectus.

Mutual funds are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by, banks, and are subject to investment risks including possible loss of principal amount invested.

5

Credit Opportunities Fund

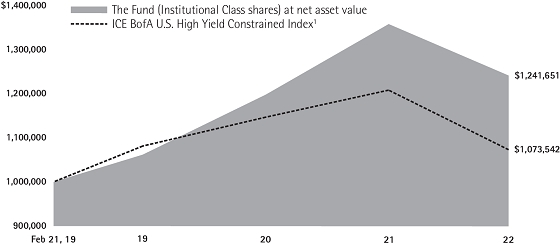

Investment Comparison

Below is a comparison of a $1 million investment in Institutional Class shares with the same investment in the ICE BofA U.S. High Yield Constrained Index, assuming reinvestment of all dividends and distributions. The performance of the other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such class. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Net Asset Value

for the Periods Ended December 31, 2022 |

| | | 1 Year | | Life of Class | |

| Institutional Class2 | | -8.58% | | 5.77% | |

| Class A3 | | -11.28% | | 4.27% | |

| Class U4 | | -9.24% | | 7.76% | |

1 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance.

2 Institutional Class shares commenced operations on February 15, 2019 and performance began on February 21, 2019. Performance is at net asset value.

3 Class A shares commenced operations and performance began on September 13, 2019. Total return, which is the

percentage change in net asset value, after deduction of the maximum initial sales charge of 2.50% applicable to Class A shares, with all dividends and distributions reinvested for the periods shown ended December 31, 2022, is calculated using the SEC-required uniform method to compute such return.

4 Class U shares commenced operations and performance began on June 18, 2020. Performance is at net asset value.

6

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments (these charges vary among the share classes); and (2) ongoing costs, including management fees; distribution and service fees (these charges vary among the share classes); and other Fund expenses. You may also incur transaction costs in the form of a repurchase fee of up to 2% which the Fund may (but does not currently) impose on shares that have been accepted for repurchase that have been held for less than one year. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2022 through December 31, 2022).

Actual Expenses

For each class of the Fund, the first line of the table on the following page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading titled “Expenses Paid During Period 7/1/22 – 12/31/22” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class of the Fund, the second line of the table on the following page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

7

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | 7/1/22 | | 12/31/22 | | 7/1/22 -

12/31/22 | |

| Institutional Class | | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,014.60 | | | $ | 7.11 | | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,018.15 | | | $ | 7.12 | | |

| Class A | | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,010.70 | | | $ | 10.90 | | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,014.37 | | | $ | 10.92 | | |

| Class U | | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,009.70 | | | $ | 10.89 | | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,014.37 | | | $ | 10.92 | | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (1.40% for Institutional Class, 2.15% for Class A and 2.15% for Class U) multiplied by the average account value over the period, multiplied by 184/365 (to reflect one-half year period). |

Portfolio Holdings Presented by Sector

December 31, 2022

| Sector* | %** | |

| Asset Backed Securities | 12.77 | % |

| Basic Materials | 0.81 | % |

| Communications | 2.13 | % |

| Consumer Cyclical | 14.22 | % |

| Consumer Non-cyclical | 6.95 | % |

| Energy | 30.20 | % |

| Financials | 9.53 | % |

| Industrials | 14.57 | % |

| Manufacturing | 0.18 | % |

| Mortgage-Backed Securities | 5.35 | % |

| Technology | 0.60 | % |

| Utilities | 1.32 | % |

| Repurchase Agreements | 1.37 | % |

| Total | 100.00 | % |

| * | | A sector may comprise of several industries. |

| ** | | Represents percent of total investments, which excludes derivatives. |

8

Schedule of Investments

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| LONG-TERM INVESTMENTS 86.52% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| ASSET-BACKED SECURITIES 12.25% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Automobiles 4.66% | | | | | | | | | | | | |

| Carvana Auto Receivables Trust 2021-N1 R† | | Zero Coupon | | 1/10/2028 | | $ | 10,000 | (a) | | $ | 2,086,347 | (b) |

| Exeter Automobile Receivables Trust 2021-4A R† | | Zero Coupon | | 12/15/2033 | | | 18,050 | (a) | | | 9,937,664 | (b) |

| Flagship Credit Auto Trust 2020 4 R† | | Zero Coupon | | 7/17/2028 | | | 17,826 | (a) | | | 3,295,302 | |

| PenFed Auto Receivables Owner Trust 2022-A R1† | | Zero Coupon | | 6/17/2030 | | | 30,000 | | | | 6,345,558 | (b) |

| Santander Bank Auto Credit-Linked Notes 2022-C D† | | 8.197% | | 12/15/2032 | | | 3,750,000 | | | | 3,752,266 | |

| Santander Bank Auto Credit-Linked Notes 2022-C E† | | 11.366% | | 12/15/2032 | | | 4,500,000 | | | | 4,503,823 | |

| Santander Bank Auto Credit-Linked Notes 2022-C F† | | 14.592% | | 12/15/2032 | | | 20,000,000 | | | | 20,003,408 | |

| Tricolor Auto Securitization Trust 2021-1A F† | | 5.08% | | 5/15/2028 | | | 5,250,000 | | | | 4,901,065 | |

| Total | | | | | | | | | | | 54,825,433 | |

| | | | | | | | | | | | | |

| Credit Card 0.80% | | | | | | | | | | | | |

| Continental Finance Credit Card ABS Master Trust 2020-1A C† | | 5.75% | | 12/15/2028 | | | 6,500,000 | | | | 5,910,786 | |

| Genesis Sales Finance Master Trust 2021-AA F† | | 5.59% | | 12/21/2026 | | | 4,000,000 | | | | 3,530,264 | |

| Total | | | | | | | | | | | 9,441,050 | |

| | | | | | | | | | | | | |

| Other 6.79% | | | | | | | | | | | | |

| AMMC CLO Ltd. 2020 23A ER† | | 10.479%

(3 Mo. LIBOR + 6.40% | )# | 10/17/2031 | | | 7,500,000 | | | | 6,894,339 | |

| Anchorage Capital CLO 25 Ltd. 2022-25A SUB† | | Zero Coupon | # | 4/20/2035 | | | 8,000,000 | | | | 5,910,914 | |

| Ares XLVI CLO Ltd. 2017-46A E† | | 9.379%

(3 Mo. LIBOR + 5.30% | )# | 1/15/2030 | | | 250,000 | | | | 208,684 | |

| Avant Loans Funding Trust 2021-REV1 E† | | 6.41% | | 7/15/2030 | | | 3,931,000 | | | | 3,369,362 | |

| Carlyle US CLO Ltd. 2021-10A E† | | 10.743%

(3 Mo. LIBOR + 6.50% | )# | 10/20/2034 | | | 5,000,000 | | | | 4,095,658 | |

| Dryden 45 Senior Loan Fund 2016-45A ER† | | 9.929%

(3 Mo. LIBOR + 5.85% | )# | 10/15/2030 | | | 7,763,000 | | | | 6,500,581 | |

| Dryden 65 CLO Ltd. 2018-65A E† | | 9.944%

(3 Mo. LIBOR + 5.75% | )# | 7/18/2030 | | | 3,000,000 | | | | 2,628,611 | |

| Encina Equipment Finance LLC 2021-1A E† | | 4.36% | | 3/15/2029 | | | 3,733,000 | | | | 3,531,837 | |

| Fairstone Financial Issuance Trust I 2020-1A D†(c) | | 6.873% | | 10/20/2039 | | CAD | 6,570,000 | | | | 4,755,889 | |

| Galaxy XVIII CLO Ltd. 2018-28A E† | | 10.079%

(3 Mo. LIBOR + 6.00% | )# | 7/15/2031 | | $ | 3,550,000 | | | | 2,930,839 | |

| | | |

| | See Notes to Financial Statements. | 9 |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Other (continued) | | | | | | | | | | | | |

| Galaxy XXVI CLO Ltd. 208-26A E† | | 10.515%

(3 Mo. LIBOR + 5.85% | )# | 11/22/2031 | | $ | 4,400,000 | | | $ | 3,775,340 | |

| Lending Funding Trust 2020-2A D† | | 6.77% | | 4/21/2031 | | | 3,335,000 | | | | 2,844,233 | |

| Lendmark Funding Trust 2019-2A A† | | 2.78% | | 4/20/2028 | | | 8,977,288 | | | | 8,715,901 | |

| Lendmark Funding Trust 2021-2A D† | | 4.46% | | 4/20/2032 | | | 2,000,000 | | | | 1,470,281 | |

| OCP CLO Ltd. 2014-6A DR† | | 10.599%

(3 Mo. LIBOR + 6.52% | )# | 10/17/2030 | | | 6,087,000 | | | | 4,928,963 | |

| Pagaya AI Debt Selection Trust 2020-1 CERT† | | Zero Coupon | | 7/15/2027 | | | 2,000,000 | (a) | | | 591,574 | (b) |

| Pagaya AI Debt Selection Trust 2021-1 CERT† | | Zero Coupon | # | 11/15/2027 | | | 2,153,846 | (a) | | | 80,399 | |

| Perimeter Master Note Business | | 8.13% | | 5/15/2027 | | | 15,000,000 | | | | 13,696,665 | |

| Regatta XIV Funding Ltd. 2018-3A E† | | 10.308%

(3 Mo. LIBOR + 5.95% | )# | 10/25/2031 | | | 3,400,000 | | | | 2,840,536 | |

| Total | | | | | | | | | | | 79,770,606 | |

| Total Asset-Backed Securities (cost $180,738,815) | | | | | | | | | | | 144,037,089 | |

| | | | | | | | | | | | | |

| | | | | | | Shares | | | | | |

| | | | | | | | | | | | | |

| COMMON STOCKS 0.01% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Transportation Infrastructure | | | | | | | | | | | | |

ACBL Holdings Corp.

(cost $132,392) | | | | | | | 4,355 | | | | 172,022 | |

| | | | | | | | | | | | | |

| | | | | | | Principal

Amount | | | | | |

| | | | | | | | | | | | | |

| CONVERTIBLE BONDS 3.65% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Airlines 0.86% | | | | | | | | | | | | |

| JetBlue Airways Corp. | | 0.50% | | 4/1/2026 | | $ | 13,694,000 | | | | 10,052,451 | |

| | | | | | | | | | | | | |

| Chemicals 0.13% | | | | | | | | | | | | |

| Danimer Scientific, Inc.† | | 3.25% | | 12/15/2026 | | | 4,000,000 | | | | 1,554,000 | |

| | | | | | | | | | | | | |

| Commercial Services 1.05% | | | | | | | | | | | | |

| Chegg, Inc. | | 0.125% | | 3/15/2025 | | | 13,500,000 | | | | 12,386,250 | |

| | | | | | | | | | | | | |

| Internet 0.93% | | | | | | | | | | | | |

| Airbnb, Inc. | | Zero Coupon | | 3/15/2026 | | | 7,500,000 | | | | 6,191,250 | |

| Uber Technologies, Inc. | | Zero Coupon | | 12/15/2025 | | | 5,583,000 | | | | 4,730,233 | |

| Total | | | | | | | | | | | 10,921,483 | |

| | |

| 10 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Trucking & Leasing 0.68% | | | | | | | | | | | | |

| Greenbrier Cos., Inc. | | 2.875% | | 4/15/2028 | | $ | 9,000,000 | | | $ | 7,978,500 | |

| Total Convertible Bonds (cost $53,026,702) | | | | | | | | | | | 42,892,684 | |

| | | | | | | | | | | | | |

| CORPORATE BONDS 55.55% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Advertising 0.35% | | | | | | | | | | | | |

| National CineMedia LLC† | | 5.875% | | 4/15/2028 | | | 17,765,000 | | | | 4,114,818 | |

| | | | | | | | | | | | | |

| Auto Parts & Equipment 1.01% | | | | | | | | | | | | |

| Real Hero Merger Sub 2, Inc.† | | 6.25% | | 2/1/2029 | | | 17,300,000 | | | | 11,881,640 | |

| | | | | | | | | | | | | |

| Building Materials 4.39% | | | | | | | | | | | | |

| Eco Material Technologies, Inc.† | | 7.875% | | 1/31/2027 | | | 12,242,000 | | | | 11,710,184 | |

| Oscar AcquisitionCo LLC/Oscar Finance, Inc.† | | 9.50% | | 4/15/2030 | | | 31,931,000 | | | | 28,696,390 | |

| Victors Merger Corp.† | | 6.375% | | 5/15/2029 | | | 20,393,000 | | | | 11,242,661 | |

| Total | | | | | | | | | | | 51,649,235 | |

| | | | | | | | | | | | | |

| Chemicals 0.65% | | | | | | | | | | | | |

| Kobe US Midco 2, Inc. PIK 10.0%† | | 9.25% | | 11/1/2026 | | | 10,760,000 | | | | 7,585,800 | |

| | | | | | | | | | | | | |

| Commercial Services 3.57% | | | | | | | | | | | | |

| BCP V Modular Services Finance plc(c) | | 6.75% | | 11/30/2029 | | EUR | 23,000,000 | | | | 18,314,454 | |

| Limak Iskenderun Uluslararasi Liman Isletmeciligi AS (Turkey)(d) | | 9.50% | | 7/10/2036 | | $ | 6,388,273 | | | | 5,523,045 | |

| Sabre GLBL, Inc.† | | 7.375% | | 9/1/2025 | | | 18,851,000 | | | | 18,147,764 | |

| Total | | | | | | | | | | | 41,985,263 | |

| | | | | | | | | | | | | |

| Diversified Financial Services 7.30% | | | | | | | | | | | | |

| Advisor Group Holdings, Inc.† | | 10.75% | | 8/1/2027 | | | 13,161,000 | | | | 13,342,261 | |

| Armor Holdco, Inc.† | | 8.50% | | 11/15/2029 | | | 7,500,000 | | | | 5,642,496 | |

| Global Aircraft Leasing Co. Ltd. (Cayman Islands)†(d) | | 6.50% | | 9/15/2024 | | | 32,038,729 | | | | 26,781,310 | |

| SCF Preferred Equity LLC† | | 7.50%

(5 Yr. Treasury CMT + 6.73% | )# | – | (e) | | 15,000,000 | | | | 13,152,751 | |

| VistaJet Malta Finance plc/XO Management Holding, Inc. (Malta)†(d) | | 6.375% | | 2/1/2030 | | | 33,459,000 | | | | 26,871,759 | |

| Total | | | | | | | | | | | 85,790,577 | |

| | | | | | | | | | | | | |

| Entertainment 0.77% | | | | | | | | | | | | |

| AMC Entertainment Holdings, Inc.† | | 10.00% | | 6/15/2026 | | | 22,428,687 | | | | 9,019,696 | |

| | | | | | | | | | | | | |

| Environmental Control 0.40% | | | | | | | | | | | | |

| Madison IAQ LLC† | | 5.875% | | 6/30/2029 | | | 6,867,000 | | | | 4,719,544 | |

| | | | | | | | | | | | | |

| Home Builders 0.37% | | | | | | | | | | | | |

| STL Holding Co. LLC† | | 7.50% | | 2/15/2026 | | | 4,964,000 | | | | 4,400,338 | |

| | | |

| | See Notes to Financial Statements. | 11 |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Lodging 0.86% | | | | | | | | | | | | |

| Full House Resorts, Inc.† | | 8.25% | | 2/15/2028 | | $ | 11,439,000 | | | $ | 10,141,360 | |

| | | | | | | | | | | | | |

| Machinery-Diversified 3.81% | | | | | | | | | | | | |

| Granite US Holdings Corp.† | | 11.00% | | 10/1/2027 | | | 16,162,000 | | | | 17,054,304 | |

| SPX FLOW, Inc.† | | 8.75% | | 4/1/2030 | | | 35,148,000 | | | | 27,765,514 | |

| Total | | | | | | | | | | | 44,819,818 | |

| | | | | | | | | | | | | |

| Oil & Gas 20.43% | | | | | | | | | | | | |

| Berry Petroleum Co. LLC† | | 7.00% | | 2/15/2026 | | | 29,570,000 | | | | 27,204,860 | |

| Callon Petroleum Co.† | | 8.00% | | 8/1/2028 | | | 6,750,000 | | | | 6,443,407 | |

| Civitas Resources, Inc.† | | 5.00% | | 10/15/2026 | | | 13,892,000 | | | | 12,718,205 | |

| Crescent Energy Finance LLC† | | 7.25% | | 5/1/2026 | | | 26,302,000 | | | | 24,818,962 | |

| Earthstone Energy Holdings LLC† | | 8.00% | | 4/15/2027 | | | 25,939,000 | | | | 24,846,968 | |

| Gulfport Energy Corp.† | | 8.00% | | 5/17/2026 | | | 10,890,000 | | | | 10,631,635 | |

| Kosmos Energy Ltd.† | | 7.50% | | 3/1/2028 | | | 11,580,000 | | | | 9,312,414 | |

| Kosmos Energy Ltd.† | | 7.75% | | 5/1/2027 | | | 5,300,000 | | | | 4,432,631 | |

| Laredo Petroleum, Inc.† | | 7.75% | | 7/31/2029 | | | 26,555,000 | | | | 23,936,250 | |

| Laredo Petroleum, Inc. | | 10.125% | | 1/15/2028 | | | 4,657,000 | | | | 4,548,652 | |

| Nabors Industries Ltd.† | | 7.25% | | 1/15/2026 | | | 28,653,000 | | | | 27,047,829 | |

| Permian Resources Operating LLC† | | 5.375% | | 1/15/2026 | | | 6,949,000 | | | | 6,336,548 | |

| Precision Drilling Corp. (Canada)†(d) | | 6.875% | | 1/15/2029 | | | 10,977,000 | | | | 10,233,931 | |

| Precision Drilling Corp. (Canada)†(d) | | 7.125% | | 1/15/2026 | | | 6,586,000 | | | | 6,382,361 | |

| ROCC Holdings LLC† | | 9.25% | | 8/15/2026 | | | 15,714,000 | | | | 15,664,509 | |

| Tap Rock Resources LLC† | | 7.00% | | 10/1/2026 | | | 27,600,000 | | | | 25,705,260 | |

| Total | | | | | | | | | | | 240,264,422 | |

| | | | | | | | | | | | | |

| Oil & Gas Services 4.86% | | | | | | | | | | | | |

| Nine Energy Service, Inc.† | | 8.75% | | 11/1/2023 | | | 9,750,000 | | | | 9,570,405 | |

| Oceaneering International, Inc. | | 6.00% | | 2/1/2028 | | | 28,410,000 | | | | 26,211,584 | |

| Welltec International ApS (Denmark)†(d) | | 8.25% | | 10/15/2026 | | | 18,924,000 | | | | 18,494,709 | |

| Welltec International ApS (Denmark)(d) | | 8.25% | | 10/15/2026 | | | 2,930,000 | | | | 2,863,533 | |

| Total | | | | | | | | | | | 57,140,231 | |

| | | | | | | | | | | | | |

| Real Estate 0.76% | | | | | | | | | | | | |

| CIFI Holdings Group Co. Ltd. (China)(d) | | 5.25% | | 5/13/2026 | | | 1,800,000 | | | | 475,755 | |

| CIFI Holdings Group Co. Ltd. (China)(d) | | 6.00% | | 7/16/2025 | | | 3,000,000 | | | | 788,369 | |

| Logan Group Co. Ltd. (China)(d) | | 4.50% | | 1/13/2028 | | | 4,000,000 | | | | 932,740 | |

| Shimao Group Holdings Ltd. (Hong Kong)(d) | | 3.45% | | 1/11/2031 | | | 5,277,000 | | | | 986,862 | |

| Shimao Group Holdings Ltd. (Hong Kong)(d)(f) | | 4.75% | | 7/3/2022 | | | 338,000 | | | | 65,065 | |

| Shimao Group Holdings Ltd. (Hong Kong)(d) | | 5.20% | | 1/16/2027 | | | 13,885,000 | | | | 2,638,147 | |

| Sunac China Holdings Ltd. (China)(d)(f) | | 5.95% | | 4/26/2024 | | | 10,500,000 | | | | 2,299,904 | |

| | |

| 12 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Real Estate (continued) | | | | | | | | | | | | |

| Sunac China Holdings Ltd. (China)(d)(f) | | 6.80% | | 10/20/2024 | | $ | 2,500,000 | | | $ | 557,013 | |

| Sunac China Holdings Ltd. (China)(d) | | 7.50% | | 2/1/2024 | | | 1,000,000 | | | | 221,924 | |

| Total | | | | | | | | | | | 8,965,779 | |

| | | | | | | | | | | | | |

| Retail 6.02% | | | | | | | | | | | | |

| BCPE Ulysses Intermediate, Inc. PIK 8.50%† | | 7.75% | | 4/1/2027 | | | 39,531,000 | | | | 24,476,045 | |

| Carrols Restaurant Group, Inc.† | | 5.875% | | 7/1/2029 | | | 27,746,000 | | | | 19,482,187 | |

| GPS Hospitality Holding Co. LLC/GPS Finco, Inc.† | | 7.00% | | 8/15/2028 | | | 38,025,000 | | | | 24,113,554 | |

| Party City Holdings, Inc.† | | 6.625% | | 8/1/2026 | | | 12,075,000 | | | | 301,875 | |

| Party City Holdings, Inc.† | | 8.75% | | 2/15/2026 | | | 8,402,000 | | | | 2,436,580 | |

| Total | | | | | | | | | | | 70,810,241 | |

| Total Corporate Bonds (cost $757,112,128) | | | | | | | | | | | 653,288,762 | |

| | | | | | | | | | | | | |

| FLOATING RATE LOANS(g) 9.72% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Building & Construction 0.70% | | | | | | | | | | | | |

| USIC Holdings, Inc. 2021 2nd Lien Term Loan | | 10.884%

(1 Mo. LIBOR + 6.50% | ) | 5/14/2029 | | | 8,726,238 | | | | 8,217,237 | |

| | | | | | | | | | | | | |

| Building Materials 1.36% | | | | | | | | | | | | |

| ACProducts, Inc. 2021 Term Loan B | | 8.98%

(3 Mo. LIBOR + 4.25%

(6 Mo. LIBOR + 4.25% | )

) | 5/17/2028 | | | 21,220,763 | | | | 16,027,724 | |

| | | | | | | | | | | | | |

| Entertainment 1.00% | | | | | | | | | | | | |

| Vue International Bidco p.l.c. 2019 EUR Term Loan B(c) | | - | (h) | 7/3/2026 | | EUR | 15,930,448 | | | | 9,762,694 | |

| Vue International Bidco p.l.c. 2022 EUR Term Loan(c) | | 9.766%

(3 Mo. EURIBOR + 8.00% | ) | 6/30/2027 | | EUR | 2,105,399 | | | | 2,062,156 | |

| Total | | | | | | | | | | | 11,824,850 | |

| | | | | | | | | | | | | |

| Financial 1.03% | | | | | | | | | | | | |

| NEXUS Buyer LLC 2021 Second Lien Term Loan | | 10.634%

(1 Mo. LIBOR + 6.25% | ) | 11/5/2029 | | $ | 13,000,001 | | | | 12,079,211 | |

| | | | | | | | | | | | | |

| Gaming/Leisure 1.09% | | | | | | | | | | | | |

| Silk Bidco AS EUR Term Loan B(c) | | 4.908%

(3 Mo. EURIBOR + 4.00% | ) | 2/24/2025 | | EUR | 15,089,300 | | | | 12,767,935 | |

| | | | | | | | | | | | | |

| Manufacturing 0.78% | | | | | | | | | | | | |

| ABG Intermediate Holdings 2 LLC 2021 2nd Lien Term Loan | | - | (h) | 12/20/2029 | | $ | 9,978,802 | | | | 9,168,024 | |

| | | |

| | See Notes to Financial Statements. | 13 |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Oil & Gas Services 1.73% | | | | | | | | | | | | |

| Ulterra Drilling Technologies, LP Term Loan B | | 9.634%

(1 Mo. LIBOR + 5.25% | ) | 11/26/2025 | | $ | 21,151,381 | | | $ | 20,340,543 | |

| | | | | | | | | | | | | |

| Pharmaceuticals 0.23% | | | | | | | | | | | | |

| Canopy Growth Corporation Term Loan (Canada)(d) | | 12.854%

(1 Mo. LIBOR + 8.50% | ) | 3/18/2026 | | | 3,205,149 | | | | 2,697,133 | |

| | | | | | | | | | | | | |

| Recreation & Travel 0.07% | | | | | | | | | | | | |

| United PF Holdings, LLC 2019 2nd Lien Term Loan | | 13.23%

(3 Mo. LIBOR + 8.50% | ) | 12/30/2027 | | | 1,000,000 | | | | 835,000 | |

| | | | | | | | | | | | | |

| Retail 0.57% | | | | | | | | | | | | |

| Miller’s Ale House, Inc. 2018 Term Loan | | 9.48% - 11.25%

(Prime Rate + 3.75%

(3 Mo. LIBOR + 4.75% | )

) | 5/30/2025 | | | 6,877,820 | | | | 6,673,205 | |

| | | | | | | | | | | | | |

| Software 0.58% | | | | | | | | | | | | |

| ECL Entertainment, LLC Term Loan | | 11.884%

(1 Mo. LIBOR + 7.50% | ) | 5/1/2028 | | | 6,830,369 | | | | 6,824,700 | |

| | | | | | | | | | | | | |

| Support: Services 0.58% | | | | | | | | | | | | |

| KUEHG Corp. 2017 2nd Lien Term Loan | | 12.98%

(3 Mo. LIBOR + 8.25% | ) | 8/22/2025 | | | 7,090,000 | | | | 6,852,485 | |

| Total Floating Rate Loans (cost $129,393,346) | | | | | | | | | | | 114,308,047 | |

| | | | | | | | | | | | | |

| NON-AGENCY COMMERCIAL MORTGAGE-BACKED SECURITIES 5.24% | | | | | | | | |

| BX Trust 2018-GW MZ MC† | | 9.806%

(1 Mo. LIBOR + 5.49% | )# | 5/15/2037 | | | 4,000,000 | | | | 3,841,416 | |

| CF Trust 2019-BOSS B1A | | 13.00% | | 12/15/2024 | | | 1,100,000 | | | | 1,059,842 | (b) |

| Commercial Mortgage Pass-Through Certificates 2015-DC1 D† | | 4.297% | #(i) | 2/10/2048 | | | 5,000,000 | | | | 3,589,478 | |

| GS Mortgage Securities Corp. Trust 2021-RENT G† | | 10.054%

(1 Mo. LIBOR + 5.70% | )# | 11/21/2035 | | | 8,214,886 | | | | 7,399,471 | |

| GS Mortgage Securities Corp. Trust 2021-RSMZ MZ† | | 13.818%

(1 Mo. LIBOR + 9.50% | )# | 6/15/2026 | | | 11,250,000 | | | | 10,789,927 | |

| GS Mortgage Securities Trust 2013-GC12 E† | | 3.25% | | 6/10/2046 | | | 10,790,000 | | | | 10,235,887 | |

| JPMorgan Chase Commercial Mortgage Securities Trust 2014-DSTY D† | | 3.805% | #(i) | 6/10/2027 | | | 614,619 | | | | 30,515 | |

| JPMorgan Chase Commercial Mortgage Securities Trust 2020-1 F† | | 13.451%

(1 Mo. Term SOFR + 9.11% | )# | 9/15/2029 | | | 850,000 | | | | 430,312 | (b) |

| | |

| 14 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| NON-AGENCY COMMERCIAL MORTGAGE-BACKED SECURITIES (continued) | | | | | | | | |

| JPMorgan Chase Commercial Mortgage Securities Trust 2021-1 XCP† | | Zero Coupon | #(i) | 9/15/2029 | | $ | 67,025,943 | | | $ | 1 | (j) |

| JPMorgan Chase Commercial Mortgage Securities Trust 2021-1440 F† | | 9.168%

(1 Mo. LIBOR + 4.85% | )# | 3/15/2036 | | | 6,025,000 | | | | 5,867,136 | |

| JPMorgan Chase Commercial Mortgage Securities Trust 2021-BOLT D† | | 11.018%

(1 Mo. LIBOR + 6.70% | )# | 8/15/2033 | | | 15,790,000 | (a) | | | 15,305,127 | |

| Laurel Road Prime Student Loan Trust 2019-A R† | | Zero Coupon | | 10/25/2048 | | | 4,049,632 | | | | 871,481 | |

| Palisades Center Trust 2016-PLSD A† | | 2.713% | | 4/13/2033 | | | 3,200,000 | | | | 2,144,000 | |

| Palisades Center Trust 2016-PLSD D† | | 4.737% | | 4/13/2033 | | | 225,000 | | | | 35,438 | |

| Total Non-Agency Commercial Mortgage-Backed Securities (cost $61,769,800) | | | | | | | 61,600,031 | |

| | �� | | | | | | | | | | | |

| | Dividend

Rate | | | | Shares | | | | | |

| | | | | | | | | | | | | |

| PREFERRED STOCKS 0.10% | | | | | | | | | | | | |

| Transportation Infrastructure | | | | | | | | | | | | |

| ACBL Holdings Corp. | | Zero Coupon | | | | | 14,619 | | | | 376,439 | |

| ACBL Holdings Corp. | | Zero Coupon | | | | | 15,891 | | | | 802,496 | |

| Total Preferred Stocks (cost $762,750) | | | | | | | | | | | 1,178,935 | |

| | | | | | | | | | | | | |

| | | Exercise

Price | | Expiration

Date | | | | | | | | |

| | | | | | | | | | | | | |

| WARRANTS 0.00% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Specialty Retail | | | | | | | | | | | | |

Chinos Intermediate Holdings A, Inc.*

(cost $34,898) | | $3.20 | | | | | 9,971 | | | | 31,907 | |

| Total Long-Term Investments (cost $1,182,970,831) | | | | | | | | | | | 1,017,509,477 | |

| | | | | | | | | | | | | |

| | | Interest

Rate | | Maturity

Date | | | Principal

Amount | | | | | |

| | | | | | | | | | | | | |

| SHORT-TERM INVESTMENTS 10.00% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| COMMERCIAL PAPER 8.67% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Electric 1.27% | | | | | | | | | | | | |

| Electricite de France SA | | 4.871% | | 1/5/2023 | | $ | 15,000,000 | | | | 14,992,000 | |

| | | |

| | See Notes to Financial Statements. | 15 |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Electronics 2.72% | | | | | | | | | | | | |

| Arrow Electronics, Inc. | | 5.00% | | 1/5/2023 | | $ | 12,000,000 | | | $ | 11,993,400 | |

| Jabil, Inc. | | 5.194% | | 1/3/2023 | | | 20,000,000 | | | | 19,994,311 | |

| Total | | | | | | | | | | | 31,987,711 | |

| | | | | | | | | | | | | |

| Food 1.28% | | | | | | | | | | | | |

| Mccormick Co. | | 4.514% | | 1/3/2023 | | | 15,000,000 | | | | 14,996,292 | |

| | | | | | | | | | | | | |

| Home Furnishings 1.28% | | | | | | | | | | | | |

| Leggett & Platt, Inc. | | 4.697% | | 1/3/2023 | | | 15,000,000 | | | | 14,996,142 | |

| | | | | | | | | | | | | |

| Oil & Gas 0.85% | | | | | | | | | | | | |

| Ovintiv, Inc. | | 5.225% | | 1/3/2023 | | | 10,000,000 | | | | 9,997,139 | |

| | | | | | | | | | | | | |

| Pipelines 1.27% | | | | | | | | | | | | |

| Energy Transfer Partners | | 5.05% | | 1/3/2023 | | | 14,995,833 | | | | 14,995,833 | |

| Total Commercial Paper (cost $101,965,117) | | | | | | | | | | | 101,965,117 | |

| | | | | | | | | | | | | |

| REPURCHASE AGREEMENTS 1.33% | | | | | | | | | | | | |

Repurchase Agreement dated 12/30/2022, 2.050% due 1/3/2023 with Fixed Income Clearing Corp. collateralized by $15,784,300 of U.S. Treasury Note at 4.275% due 4/30/2024; value: $15,860,949; proceeds: $15,553,435

(cost $15,549,893) | | | | | | | 15,549,893 | | | | 15,549,893 | |

| Total Short-Term Investments (cost $117,515,010) | | | | | | | | | 117,515,010 | |

| Total Investments in Securities 96.52% (cost $1,300,485,841) | | | | | | | | | 1,135,024,487 | |

| Other Assets and Liabilities – Net(k) 3.48% | | | | | | | | | | | 40,981,633 | |

| Net Assets 100.00% | | | | | | | | | | $ | 1,176,006,120 | |

| | |

| CAD | Canadian Dollar. |

| EUR | Euro. |

| CMT | Constant Maturity Rate. |

| EURIBOR | Euro Interbank Offered Rate. |

| LIBOR | London Interbank Offered Rate. |

| PIK | Payment-in-kind. |

| SOFR | Secured Overnight Financing Rate. |

| † | | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and, unless registered under such Act or exempted from registration, may only be resold to qualified institutional buyers. At December 31, 2022, the total value of Rule 144A securities was $779,296,328, which represents 66.27% of net assets. |

| # | | Variable rate security. The interest rate represents the rate in effect at December 31, 2022. |

| * | | Non-income producing security. |

| (a) | | Principal amount represents ownership shares of the Trust. |

| (b) | | Level 3 Investment as described in Note 2(o) in the Notes to Financials. Security valued utilizing third party pricing information without adjustment. Such valuations are based on unobservable inputs. A significant change in third party information could result in a significantly lower or higher value of such Level 3 investments. |

| (c) | | Investment in non-U.S. dollar denominated securities. |

| (d) | | Foreign security traded in U.S. dollars. |

| | |

| 16 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| (e) | | Security is perpetual in nature and has no stated maturity. |

| (f) | | Defaulted (non-income producing security). |

| (g) | | Floating Rate Loans in which the Fund invests generally pay interest at rates which are periodically re-determined at a margin above the London Interbank Offered Rate (“LIBOR”) or the prime rate offered by major U.S. banks. The rate(s) shown is the rate(s) in effect at December 31, 2022. |

| (h) | | Interest Rate to be determined. |

| (i) | | Interest rate is based on the weighted average interest rates of the underlying mortgages within the mortgage pool. |

| (j) | | Level 3 Investment as described in Note 2(o) in the Notes to Financials. Security fair valued by the Pricing Committee. |

| (k) | | Other Assets and Liabilities – Net include net unrealized appreciation/depreciation on forward foreign currency exchange contracts and swaps as follows: |

Centrally Cleared Credit Default Swaps on Issuers - Buy Protection at December 31, 2022(1):

Referenced

Issuer | | Central

Clearing

Party | | Fund Pays

(Quarterly) | | Termination

Date | | Notional

Amount | | Payments

Upfront(2) | | | Value | | | Unrealized

Appreciation(3) | |

| Federal Republic of Germany(4)(5) | | Bank of America | | 0.25% | | 12/20/2026 | | $ | 35,000,000 | | | $ | (133,911 | ) | | $ | (129,815 | ) | | $ | 4,096 | |

| Johnson & Johnson(4)(5) | | Bank of America | | 1.00% | | 12/20/2026 | | | 15,000,000 | | | | (429,680 | ) | | | (423,376 | ) | | | 6,304 | |

| | | | | | | | | | | | | $ | (563,591 | ) | | $ | (553,191 | ) | | $ | 10,400 | |

| | | | | | | | | | | | | | | | | | | |

Referenced

Issuer | | Central

Clearing

Party | | Fund Pays

(Quarterly) | | Termination

Date | | Notional

Amount | | | Payments

Upfront(2) | | | Value | | | Unrealized

Depreciation(3) | |

| Federal Republic of Germany(4)(5) | | Bank of America | | 0.25% | | 12/20/2027 | | $ | 10,000,000 | | | | $(15,677 | ) | | | $(30,550 | ) | | $(14,873 | ) |

| | | | | | | | | | | | | | | | | | | | | | |

Centrally Cleared Credit Default Swaps on Index/Issuers - Sell Protection at December 31, 2022(1): |

| | | | | | | | | | | | | | | | | | | | | | |

Referenced

Index | | Central

Clearing

Party | | Fund

Receives

(Quarterly) | | Termination

Date | | Notional

Amount | | | Payments

Upfront(2) | | | Value | | | Unrealized

Appreciation(3) | |

| CDX.NA.HY.S39(4)(6) | | Bank of America | | 5.00% | | 12/20/2027 | | $ | 47,500,000 | | | | $125,346 | | | | $276,641 | | | $151,295 | |

| | | | | | | | | | | | | | | | | | | |

Referenced

Issuer | | Central

Clearing

Party | | Fund

Receives

(Quarterly) | | Termination

Date | | Notional

Amount | | | Payments

Upfront(2) | | | Value | | | Unrealized

Depreciation(3) | |

| American Airlines Group Inc.(4)(5) | | Bank of America | | 5.00% | | 12/20/2024 | | $ | 31,950,000 | | $(2,579,543 | ) | | $(2,947,006 | ) | | $(367,463 | ) |

| | | |

| (1) | | If the Fund is a buyer of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) receive from the seller of protection an amount equal to the notional amount of the swap and make delivery of the referenced obligation or underlying securities comprising the referenced index or (ii) receive net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation or underlying securities. If the Fund is a seller of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) pay to the buyer of protection an amount equal to the notional amount of the swap and take delivery of the referenced obligation or underlying securities comprising the referenced index or (ii) pay a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation or underlying securities. |

| (2) | | Upfront payments paid (received) by Central Clearing Party are presented net of amortization. |

| (3) | | Total unrealized appreciation on Centrally Cleared Credit Default Swaps on Index/Issuers amounted to $161,695. Total unrealized depreciation on Centrally Cleared Credit Default Swaps on Index/Issuers amounted to $382,336. |

| (4) | | Central Clearinghouse: Intercontinental Exchange (ICE). |

| (5) | | Moody’s Credit Rating: Baa3. |

| (6) | | The Referenced Index is for the Centrally Cleared Credit Default Swaps on Indexes, which is comprised of a basket of high yield securities. |

| | | |

| | See Notes to Financial Statements. | 17 |

Schedule of Investments (continued)

December 31, 2022

Credit Default Swaps on Issuer - Buy Protection at December 31, 2022(1):

Referenced

Issuer | | Swap

Counterparty | | Fund

Pays

(Quarterly) | | Termination

Date | | Notional

Amount | | | Payments

Upfront(2) | | | Unrealized

Appreciation/

Depreciation(3) | | | Credit

Default

Swap

Agreements

Payable at

Fair Value(4) | |

| Swedbank AB(5) | | Barclays Bank plc | | 1.000% | | 6/20/2027 | | | EUR18,000,000 | | | | $(200,697 | ) | | | $(44,306 | ) | | | $(245,003 | ) |

| | | |

| (1) | | If the Fund is a buyer of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) receive from the seller of protection an amount equal to the notional amount of the swap and make delivery of the referenced obligation or underlying securities comprising the referenced index or (ii) receive a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation or underlying securities. |

| (2) | | Upfront payments paid (received) are presented net of amortization. |

| (3) | | Total unrealized appreciation on Credit Default Swaps on Issuer amounted to $0. Total unrealized depreciation on Credit Default Swaps on Issuer amounted to $44,306. |

| (4) | | Includes upfront payments paid (received). |

| (5) | | Moody’s Credit Rating: Baa3. |

Forward Foreign Currency Exchange Contracts at December 31, 2022:

Forward

Foreign

Currency

Exchange

Contracts | | Transaction

Type | | Counterparty | | Expiration

Date | | Foreign

Currency | | U.S. $

Cost on

Origination

Date | | | U.S. $

Current

Value | | | Unrealized

Appreciation | |

| Euro | | Buy | | Morgan Stanley | | 3/13/2023 | | 330,000 | | | $353,792 | | | | $354,891 | | | | | $1,099 | |

| Euro | | Buy | | State Street Bank and Trust | | 3/13/2023 | | 440,000 | | | 469,416 | | | | 473,188 | | | | | 3,772 | |

| Total Unrealized Appreciation on Forward Foreign Currency Exchange Contracts | | | | | | | | | | | | $4,871 | |

| | | | | | | | | | | | | | |

Forward

Foreign

Currency

Exchange

Contracts | | Transaction

Type | | Counterparty | | Expiration

Date | | Foreign

Currency | | U.S. $

Cost on

Origination

Date | | | U.S. $

Current

Value | | | Unrealized

Depreciation | |

| Canadian dollar | | Sell | | Toronto | | | | | | | | | | | | | | | | | |

| | | | | Dominion Bank | | 1/20/2023 | | 6,375,000 | | | $ 4,632,186 | | | | $ 4,708,658 | | | | | $ (76,472 | ) |

| Euro | | Sell | | State Street Bank and Trust | | 3/13/2023 | | 37,938,000 | | | 40,305,559 | | | | 40,799,572 | | | | | (494,013 | ) |

| Total Unrealized Depreciation on Forward Foreign Currency Exchange Contracts | | | | | | | | | | | | $(570,485 | ) |

| | |

| 18 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

The following is a summary of the inputs used as of December 31, 2022 in valuing the Fund’s investments carried at fair value(1):

| Investment Type(2) | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Long-Term Investments | | | | | | | | | | | | | | | | |

| Asset-Backed Securities | | | | | | | | | | | | | | | | |

| Automobiles | | $ | – | | | $ | 36,455,864 | | | $ | 18,369,569 | | | $ | 54,825,433 | |

| Other | | | – | | | | 79,179,032 | | | | 591,574 | | | | 79,770,606 | |

| Remaining Industries | | | – | | | | 9,441,050 | | | | – | | | | 9,441,050 | |

| Common Stocks | | | – | | | | 172,022 | | | | – | | | | 172,022 | |

| Convertible Bonds | | | – | | | | 42,892,684 | | | | – | | | | 42,892,684 | |

| Corporate Bonds | | | – | | | | 653,288,762 | | | | – | | | | 653,288,762 | |

| Floating Rate Loans | | | – | | | | 114,308,047 | | | | – | | | | 114,308,047 | |

| Non-Agency Commercial Mortgage-Backed Securities | | | – | | | | 60,109,876 | | | | 1,490,155 | | | | 61,600,031 | |

| Preferred Stocks | | | – | | | | 1,178,935 | | | | – | | | | 1,178,935 | |

| Warrants | | | – | | | | 31,907 | | | | – | | | | 31,907 | |

| Short-Term Investments | | | | | | | | | | | | | | | | |

| Commercial Paper | | | – | | | | 101,965,117 | | | | – | | | | 101,965,117 | |

| Repurchase Agreements | | | – | | | | 15,549,893 | | | | – | | | | 15,549,893 | |

| Total | | $ | – | | | $ | 1,114,573,189 | | | $ | 20,451,298 | | | $ | 1,135,024,487 | |

| | | | | | | | | | | | | | | | | |

| Other Financial Instruments | | | | | | | | | | | | | | | | |

| Centrally Cleared Credit Default Swap Contracts | | | | | | | | | | | | | | | | |

| Assets | | $ | – | | | $ | 276,641 | | | $ | – | | | $ | 276,641 | |

| Liabilities | | | – | | | | (3,530,747 | ) | | | – | | | | (3,530,747 | ) |

| Credit Default Swap Contracts | | | | | | | | | | | | | | | | |

| Assets | | | – | | | | – | | | | – | | | | – | |

| Liabilities | | | – | | | | (245,003 | ) | | | – | | | | (245,003 | ) |

| Forward Foreign Currency Exchange Contracts | | | | | | | | | | | | | | | | |

| Assets | | | – | | | | 4,871 | | | | – | | | | 4,871 | |

| Liabilities | | | – | | | | (570,485 | ) | | | – | | | | (570,485 | ) |

| Total | | $ | – | | | $ | (4,064,723 | ) | | $ | – | | | $ | (4,064,723 | ) |

| (1) | | Refer to Note 2(o) for a description of fair value measurements and the three-tier hierarchy of inputs. |

| (2) | | See Schedule of Investments for fair values in each industry and identification of foreign issuers and/or geography. The table above is presented by Investment Type. Industries are presented within an Investment Type should such Investment Type include securities classified as two or more levels within the three-tier fair value hierarchy. When applicable, each Level 3 security is identified on the Schedule of Investments along with the valuation technique utilized. |

A reconciliation of Level 3 investments is presented when the Fund has a material amount of Level 3 investments at the beginning or end of the year in relation to the Fund’s net assets.

| | See Notes to Financial Statements. | 19 |

Schedule of Investments (concluded)

December 31, 2022

The following is a reconciliation of investments with unobservable inputs (Level 3) that were used in determining fair value:

| | | Asset-Backed | | | Non-Agency Commercial | |

| Investment Type | | Securities | | | Mortgage-Backed Securities | |

| Balance as of January 1, 2022 | | | $ | 16,325,250 | | | | $ | 1,943,093 | |

| Accrued Discounts (Premiums) | | | | (7,700 | ) | | | | – | |

| Realized Gain (Loss) | | | | – | | | | | (24,277 | ) |

| Change in Unrealized Appreciation (Depreciation) | | | | (15,549,279 | ) | | | | (428,661 | ) |

| Purchases | | | | 28,487,180 | | | | | – | |

| Sales | | | | – | | | | | – | |

| Transfers into Level 3(a) | | | | – | | | | | – | |

| Transfers out of Level 3(a) | | | | (10,294,308 | ) | | | | – | |

| Balance as of December 31, 2022 | | | $ | 18,961,143 | | | | $ | 1,490,155 | |

| Change in unrealized appreciation/ depreciation for the year ended December 31, 2022, related to Level 3 investments held at December 31, 2022 | | | $ | (15,549,279 | ) | | | $ | (428,661 | ) |

| (a) | | The fund recognizes transfers within the fair value hierarchy as of the beginning of the period. Transfers into and out of Level 3 were primarily related to the availability of market quotations in accordance with valuation methodology. |

| | |

| 20 | See Notes to Financial Statements. |

Statement of Assets and Liabilities

December 31, 2022

| ASSETS: | | | | |

| Investments in securities, at cost | | $ | 1,300,485,841 | |

| Investments in securities, at fair value | | $ | 1,135,024,487 | |

| Cash | | | 51,808 | |

| Deposit with brokers for forwards and swaps collateral | | | 27,034,520 | |

| Receivables: | | | | |

| Interest and dividends | | | 21,172,228 | |

| Capital shares sold | | | 6,545,805 | |

| Investment securities sold | | | 3,825,069 | |

| From broker | | | 109,642 | |

| Variation margin for centrally cleared credit default swap agreements | | | 710,241 | |

| Unrealized appreciation on forward foreign currency exchange contracts | | | 4,871 | |

| Prepaid expenses and other assets | | | 64,076 | |

| Total assets | | | 1,194,542,747 | |

| LIABILITIES: | | | | |

| Payables: | | | | |

| Investment securities purchased | | | 5,170,995 | |

| Management fee | | | 1,231,631 | |

| Distribution and Servicing plan | | | 308,011 | |

| Credit default swap agreements payable, at fair value (including upfront payments of $200,697) | | | 245,003 | |

| Fund administration | | | 39,412 | |

| Trustees’ fees | | | 17,361 | |

| Unrealized depreciation on forward foreign currency exchange contracts | | | 570,485 | |

| Foreign currency overdraft (cost $3,186,044) | | | 3,239,033 | |

| Distributions payable | | | 7,556,375 | |

| Accrued expenses and other liabilities | | | 158,321 | |

| Total liabilities | | | 18,536,627 | |

| NET ASSETS | | $ | 1,176,006,120 | |

| COMPOSITION OF NET ASSETS: | | | | |

| Paid-in capital | | $ | 1,339,188,563 | |

| Total distributable earnings (loss) | | | (163,182,443 | ) |

| Net Assets | | $ | 1,176,006,120 | |

| Net assets by class: | | | | |

| Institutional Class Shares | | $ | 684,810,008 | |

| Class A Shares | | $ | 466,140,901 | |

| Class U Shares | | $ | 25,055,211 | |

| Outstanding shares by class (unlimited number of authorized shares of beneficial interest): | | | | |

| Institutional Class Shares | | | 77,892,031 | |

| Class A Shares | | | 53,017,441 | |

| Class U Shares | | | 2,848,614 | |

| Net asset value, offering and redemption price per share (Net assets divided by outstanding shares): | | | | |

| Institutional Class Shares-Net asset value | | | $8.79 | |

| Class A Shares-Net asset value | | | $8.79 | |

| Class A Shares-Maximum offering price (Net asset value plus sales charge of 2.50%) | | | $9.02 | |

| Class U Shares-Net asset value | | | $8.80 | |

| | | |

| | See Notes to Financial Statements. | 21 |

Statement of Operations

For the Year Ended December 31, 2022

| Investment income: | | | | |

| Dividends | | $ | 68,624 | |

| Interest and other | | | 93,230,990 | |

| Total investment income | | | 93,299,614 | |

| Expenses: | | | | |

| Management fee | | | 12,498,758 | |

| Distribution and Servicing plan–Class A | | | 3,399,693 | |

| Distribution and Servicing plan–Class U | | | 56,167 | |

| Shareholder servicing | | | 518,817 | |

| Fund administration | | | 399,960 | |

| Reports to shareholders | | | 161,670 | |

| Registration | | | 112,261 | |

| Professional | | | 100,570 | |

| Custody | | | 33,232 | |

| Trustees’ fees | | | 16,524 | |

| Other | | | 105,241 | |

| Gross expenses | | | 17,402,893 | |

| Fees waived and expenses reimbursed (See Note 3) | | | (33,232 | ) |

| Net expenses | | | 17,369,661 | |

| Net investment income | | | 75,929,953 | |

| Net realized and unrealized gain (loss): | | | | |

| Net realized gain (loss) on investments | | | 8,851,421 | |

| Net realized gain (loss) on futures contracts | | | 121,766 | |

| Net realized gain (loss) on forward foreign currency exchange contracts | | | 4,042,854 | |

| Net realized gain (loss) on swap contracts | | | 4,076,051 | |

| Net realized gain (loss) on foreign currency related transactions | | | 62,540 | |

| Net change in unrealized appreciation/depreciation on investments | | | (182,549,799 | ) |

| Net change in unrealized appreciation/depreciation on forward foreign currency exchange contracts | | | (765,316 | ) |

| Net change in unrealized appreciation/depreciation on swap contracts | | | (780,557 | ) |

| Net change in unrealized appreciation/depreciation on translation of assets and liabilities denominated in foreign currencies | | | (43,128 | ) |

| Net realized and unrealized gain (loss) | | | (166,984,168 | ) |

| Net Decrease in Net Assets Resulting From Operations | | $ | (91,054,215 | ) |

| | |

| 22 | See Notes to Financial Statements. |

Statements of Changes in Net Assets

| | | For the Year Ended | | | For the Year Ended | |

| INCREASE (DECREASE) IN NET ASSETS | | December 31, 2022 | | | December 31, 2021 | |

| Operations: | | | | | | | | | | |

| Net investment income | | | $ | 75,929,953 | | | | $ | 39,582,110 | |

| Net realized gain (loss) on investments, futures contracts, forward foreign currency exchange contracts, swap contracts and foreign currency related transactions | | | | 17,154,632 | | | | | 28,708,539 | |

| Net change in unrealized appreciation/depreciation on investments, forward foreign currency exchange contracts, swap contracts and translation of assets and liabilities denominated in foreign currencies | | | | (184,138,800 | ) | | | | (8,632,435 | ) |

| Net increase (decrease) in net assets resulting from operations | | | | (91,054,215 | ) | | | | 59,658,214 | |

| Distributions to shareholders: | | | | | | | | | | |

| Institutional Class | | | | (53,534,524 | ) | | | | (32,169,191 | ) |

| Class A | | | | (39,750,401 | ) | | | | (34,566,142 | ) |

| Class U | | | | (909,175 | ) | | | | (1,171 | ) |

| Total distributions to shareholders | | | | (94,194,100 | ) | | | | (66,736,504 | ) |

| Capital share transactions (See Note 15): | | | | | | | | | | |

| Net proceeds from sales of shares | | | | 569,650,851 | | | | | 473,919,305 | |

| Reinvestment of distributions | | | | 39,331,874 | | | | | 37,212,909 | |

| Cost of shares reacquired | | | | (95,594,188 | ) | | | | (18,748,480 | ) |

| Net increase in net assets resulting from capital share transactions | | | | 513,388,537 | | | | | 492,383,734 | |

| Net increase in net assets | | | | 328,140,222 | | | | | 485,305,444 | |

| NET ASSETS: | | | | | | | | | | |

| Beginning of year | | | $ | 847,865,898 | | | | $ | 362,560,454 | |

| End of year | | | $ | 1,176,006,120 | | | | $ | 847,865,898 | |

| | | |

| | See Notes to Financial Statements. | 23 |

Financial Highlights

| | | | | | Per Share Operating Performance: |

| | | | | | Investment operations: | | | Distributions to

shareholders from: |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | Total | | | | | | | | | |

| | | | | | | | | Net | | from | | | | | | | | | |

| | | Net asset | | Net | | realized | | invest- | | Net | | | | | | |

| | | value, | | invest- | | and | | ment | | invest- | | Net | | Total |

| | | beginning | | ment | | unrealized | | oper- | | ment | | realized | | distri- |

| | | of period | | income(a) | | gain (loss) | | ations | | income | | gain | | butions |

| Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 12/31/2022 | | | $10.58 | | | | $0.75 | | | | $(1.64 | ) | | | $(0.89 | ) | | | $(0.76 | ) | | | $(0.14 | ) | | | $(0.90 | ) |

| 12/31/2021 | | | 10.37 | | | | 0.79 | | | | 0.56 | | | | 1.35 | | | | (0.75 | ) | | | (0.39 | ) | | | (1.14 | ) |

| 12/31/2020 | | | 10.00 | | | | 0.74 | | | | 0.34 | | | | 1.08 | | | | (0.71 | ) | | | – | | | | (0.71 | ) |

| 2/15/2019 to 12/31/2019(c) | | | 10.00 | | | | 0.59 | | | | 0.03 | | | | 0.62 | | | | (0.61 | ) | | | (0.01 | ) | | | (0.62 | ) |

| Class A | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 12/31/2022 | | | 10.58 | | | | 0.68 | | | | (1.64 | ) | | | (0.96 | ) | | | (0.69 | ) | | | (0.14 | ) | | | (0.83 | ) |

| 12/31/2021 | | | 10.37 | | | | 0.71 | | | | 0.56 | | | | 1.27 | | | | (0.67 | ) | | | (0.39 | ) | | | (1.06 | ) |

| 12/31/2020 | | | 10.00 | | | | 0.66 | | | | 0.48 | | | | 1.14 | | | | (0.77 | ) | | | – | | | | (0.77 | ) |

| 9/13/2019 to 12/31/2019(f) | | | 9.93 | | | | 0.19 | | | | 0.08 | | | | 0.27 | | | | (0.19 | ) | | | (0.01 | ) | | | (0.20 | ) |

| Class U | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 12/31/2022 | | | 10.58 | | | | 0.68 | | | | (1.62 | ) | | | (0.94 | ) | | | (0.70 | ) | | | (0.14 | ) | | | (0.84 | ) |

| 12/31/2021 | | | 10.37 | | | | 0.70 | | | | 0.57 | | | | 1.27 | | | | (0.67 | ) | | | (0.39 | ) | | | (1.06 | ) |

| 6/18/2020 to 12/31/2020(g) | | | 9.10 | | | | 0.36 | | | | 1.27 | | | | 1.63 | | | | (0.36 | ) | | | – | | | | (0.36 | ) |

| | | |

| (a) | | Calculated based on average shares outstanding during the period. |

| (b) | | Total return for Class A does not consider the effects of sales loads and assumes the reinvestment of all distributions. Total return for Institutional Class and Class U assumes the reinvestment of all distributions. |

| (c) | | Commenced on February 15, 2019. |

| (d) | | Not annualized. |

| (e) | | Annualized. |

| (f) | | Commenced on September 13, 2019. |

| (g) | | Commenced on June 18, 2020. |

| | |

| 24 | See Notes to Financial Statements. |

| | | | | | | Ratios to Average Net Assets: | | Supplemental

Data: |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | Total | | | | | | | | | | | | |

| | | | | | | expenses | | | | | | | | | | | | |

| | | | | | | after | | | | | | | | | | | | |

| Net | | | | | waivers | | | | | | | | Net | | | |

| asset | | | | | and/or | | | | | Net | | assets, | | Portfolio |

| value, | | Total | | reimburse- | | Total | | investment | | end of | | turnover |

| end of | | return | | ments | | expenses | | income | | period | | rate |

| period | | (%)(b) | | (%) | | (%) | | (%) | | (000) | | (%) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | $ 8.79 | | | | (8.58 | ) | | | 1.39 | | | | 1.39 | | | | 7.94 | | | | $ 684,810 | | | | 52 | |

| | 10.58 | | | | 13.35 | | | | 1.39 | | | | 1.40 | | | | 7.23 | | | | 408,536 | | | | 61 | |

| | 10.37 | | | | 12.84 | | | | 1.50 | | | | 1.62 | | | | 7.92 | | | | 177,894 | | | | 119 | |

| | 10.00 | | | | 6.29 | (d) | | | 1.50 | (e) | | | 3.79 | (e) | | | 6.78 | (e) | | | 61,215 | | | | 50 | (d) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 8.79 | | | | (9.26 | ) | | | 2.14 | | | | 2.14 | | | | 7.16 | | | | 466,141 | | | | 52 | |

| | 10.58 | | | | 12.53 | | | | 2.13 | | | | 2.14 | | | | 6.53 | | | | 439,318 | | | | 61 | |

| | 10.37 | | | | 12.02 | | | | 2.25 | | | | 2.30 | | | | 7.01 | | | | 184,655 | | | | 119 | |

| | 10.00 | | | | 2.67 | (d) | | | 2.25 | (e) | | | 5.39 | (e) | | | 6.54 | (e) | | | 10 | | | | 50 | (d) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 8.80 | | | | (9.24 | ) | | | 2.15 | | | | 2.15 | | | | 7.50 | | | | 25,055 | | | | 52 | |

| | 10.58 | | | | 12.54 | | | | 2.13 | | | | 2.13 | | | | 6.46 | | | | 12 | | | | 61 | |

| | 10.37 | | | | 18.33 | (d) | | | 2.25 | (e) | | | 2.30 | (e) | | | 7.01 | (e) | | | 11 | | | | 119 | |

| | | |

| | See Notes to Financial Statements. | 25 |

Notes to Financial Statements

Lord Abbett Credit Opportunities Fund (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “Act”), as a non-diversified, closed-end management investment company that continuously offers its common shares (the “Shares”) and is operated as an interval fund. The Fund was organized as a Delaware statutory trust on September 18, 2018. The Fund had a sale to Lord, Abbett & Co. LLC (“Lord Abbett”) of 10,000 shares of common stock for $100,000 ($10.00 per share). The Fund commenced operations on February 15, 2019.

The Fund’s investment objective is total return. The Fund currently offers three classes of Shares: Institutional Class, Class A and Class U. A front-end sales charge is normally added to the net asset value (“NAV”) for Class A shares. There is no front-end sales charge in the case of Institutional Class and Class U shares. Class U shares commenced operations on June 18, 2020.

The Fund will not list its Shares for trading on any securities exchange. There is currently no secondary market for its Shares and the Fund does not expect any secondary market to develop for its Shares. Shareholders of the Fund are not able to have their Shares redeemed or otherwise sell their Shares on a daily basis because the Fund is an unlisted closed-end fund. In order to provide liquidity to shareholders, the Fund is structured as an interval fund and conducts quarterly repurchase offers for a portion of its outstanding Shares.

The preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”) requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. The Fund is considered an investment company under U.S. GAAP and follows the accounting and reporting guidance applicable to investment companies.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

| (a) | Investment Valuation–Under procedures approved by the Fund’s Board of Trustees (the “Board”), the Board has designated the determination of fair value of the Fund’s portfolio investments to Lord, Abbett & Co. LLC (“Lord Abbett”), as its valuation designee. Accordingly, Lord Abbett is responsible for, among other things, assessing and managing valuation risks, establishing, applying and testing fair value methodologies, and evaluating pricing services. Lord Abbett has formed a Pricing Committee that performs these responsibilities on behalf of Lord Abbett, administers the pricing and valuation of portfolio investments and ensures that prices utilized reasonably reflect fair value. Among other things, these procedures allow Lord Abbett, subject to Board oversight, to utilize independent pricing services, quotations from securities and financial instrument dealers and other market sources to determine fair value. |

| | |

| | Securities actively traded on any recognized U.S. or non-U.S. exchange or on The NASDAQ Stock Market LLC are valued at the last sale price or official closing price on the exchange or system on which they are principally traded. Events occurring after the close of trading on non-U.S. exchanges may result in adjustments to the valuation of foreign securities to reflect their fair value as of the close of regular trading on the New York Stock Exchange. When valuing foreign equity securities that meet certain criteria, the Board has approved the use of an independent fair valuation service that values such securities to reflect market trading that occurs after the close of the applicable foreign markets of comparable securities or other |

26

Notes to Financial Statements (continued)

| | instruments that correlate to the fair-valued securities. Unlisted equity securities are valued at the last quoted sale price or, if no sale price is available, at the mean between the most recently quoted bid and ask prices. Exchange traded options and futures contracts are valued at the last quoted sale price in the market where they are principally traded. If no sale has occurred, the mean between the most recently quoted bid and ask prices is used. Fixed income securities are valued based on evaluated prices supplied by independent pricing services, which reflect broker/dealer supplied valuations and the independent pricing services’ own electronic data processing techniques. Forward foreign currency exchange contracts are valued using daily forward exchange rates. Swaps are valued daily using independent pricing services or quotations from broker/dealers to the extent available. |

| | |