UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________

Form 20-F

__________________________________

|

| |

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2018 |

| OR |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR |

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 333-228667

__________________________________

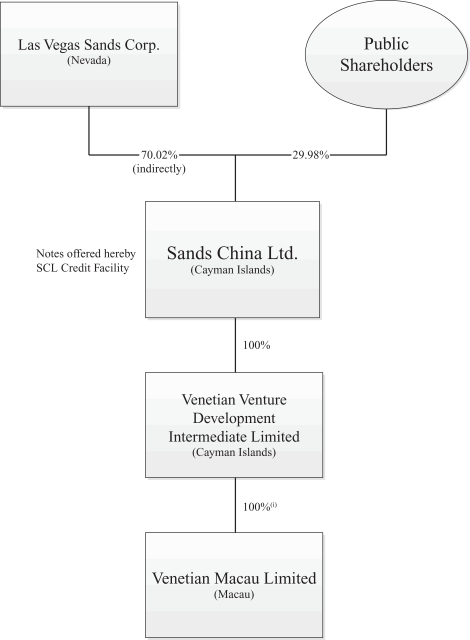

Sands China Ltd.

(Exact name of Registrant as specified in its charter)

__________________________________

Cayman Islands

(Jurisdiction of Incorporation or Organization)

__________________________________

The Venetian Macao Resort Hotel, L2 Executive Offices

Estrada da Baía de N. Senhora da Esperança, s/n

Macao SAR

(Address of principal executive offices)

__________________________________

Dylan Williams, Company Secretary

Sands China Ltd.

The Venetian Macao Resort Hotel, Legal Department, L2 Executive Offices

Estrada da Baía de N. Senhora da Esperança, s/n

Macao SAR

Telephone: +853 8118-2888 Facsimile: +853 2888-3382

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

__________________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of Each Class | | Name of Each Exchange on Which Registered |

| N/A | | N/A |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

__________________________________

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

4.600% Notes Due August 8, 2023

5.125% Notes Due August 8, 2025

5.400% Notes Due August 8, 2028

__________________________________

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

8,080,603,691 ordinary shares outstanding as of December 31, 2018

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | | | | | | |

| Large accelerated filer | ¨ | | Accelerated filer | ¨ | | Non-Accelerated filer | x | | Emerging growth company | ¨ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

| | | | | | | |

| U.S. GAAP | ¨ | | International Financial Reporting Standards as issued by the International Accounting Standards Board | x | | Other | ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ¨ No ¨

TABLE OF CONTENTS

PART I

ITEM 1. — IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. — OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. — KEY INFORMATION

A. SELECTED FINANCIAL INFORMATION

The following selected historical financial and other data as of and for the years ended December 31, 2018 and 2017, and for the year ended December 31, 2016, have been derived from our audited consolidated financial statements included elsewhere in this annual report. The following selected historical financial and other data as of December 31, 2016, and as of and for the years ended December 31, 2015 and 2014, have been derived from our audited consolidated financial statements not included in this annual report. Our audited consolidated financial statements are prepared in accordance with IFRS.

We adopted IFRS 15, Revenue from Contracts with Customers, effective January 1, 2018, by applying the full retrospective method. See Note 2 (b) “Summary of Significant Accounting Policies — Change in Accounting Policies and Disclosures” to our audited consolidated financial statements included in this annual report for further information regarding these changes. Revenues and operating expenses for the year ended December 31, 2014 were not revised and are presented in accordance with International Accounting Standard 18, Revenue, and related interpretations.

You should read this section in conjunction with “Item 4 — Information on the Company — B. Business Overview” and those financial statements and the notes to those statements included elsewhere in this annual report. The results for any historical period are not necessarily indicative of the results of operations to be expected in any future period.

|

| | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, |

| | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

| | (US$ in millions, except per share data) |

| Consolidated income statement data | | | | | | | | | |

| Net revenues | $ | 8,665 |

| | $ | 7,586 |

| | $ | 6,543 |

| | $ | 6,683 |

| | $ | 9,505 |

|

| Operating profit | $ | 2,154 |

| | $ | 1,773 |

| | $ | 1,352 |

| | $ | 1,519 |

| | $ | 2,624 |

|

| Profit attributable to equity holders of the Company | $ | 1,875 |

| | $ | 1,603 |

| | $ | 1,224 |

| | $ | 1,459 |

| | $ | 2,548 |

|

| Earnings per share for profit attributable to equity holders of the Company | | | | | | | | | |

| - Basic | US23.21 cents |

| | US19.86 cents |

| | US15.17 cents |

| | US18.09 cents |

| | US31.59 cents |

|

| - Diluted | US23.19 cents |

| | US19.85 cents |

| | US15.17 cents |

| | US18.08 cents |

| | US31.56 cents |

|

| Dividends declared per share (HK$) | HK$1.99 |

| | HK$1.99 |

| | HK$1.99 |

| | HK$1.99 |

| | HK$1.99 |

|

Dividends declared per share (US$)(i) | US25.40

cents |

| | US25.40

cents |

| | US25.70

cents |

| | US25.70 cents |

| | US25.70 cents |

|

| Consolidated balance sheet and other financial data (at year end) | | | | | | | | | |

| Total assets | $ | 12,058 |

| | $ | 10,647 |

| | $ | 11,183 |

| | $ | 10,772 |

| | $ | 11,348 |

|

| Share capital | $ | 81 |

| | $ | 81 |

| | $ | 81 |

| | $ | 81 |

| | $ | 81 |

|

| Total equity | $ | 4,409 |

| | $ | 4,538 |

| | $ | 5,007 |

| | $ | 5,839 |

| | $ | 6,429 |

|

| Weighted average number of shares | | | | | | | | | |

| - Basic (thousand shares) | 8,078,946 |

| | 8,072,709 |

| | 8,070,042 |

| | 8,068,742 |

| | 8,065,321 |

|

| - Diluted (thousand shares) | 8,086,274 |

| | 8,077,253 |

| | 8,071,651 |

| | 8,070,572 |

| | 8,072,743 |

|

| | | | | | | | | | |

____________________

| |

| (i) | The translation of dividends declared per share from HK$ amounts into US$ amounts has been made at the exchange rates in effect at the time of the transaction. |

B. CAPITALIZATION AND INDEBTEDNESS

Not applicable.

C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not applicable.

D. RISK FACTORS

You should carefully consider the risks described below and the other information contained in this annual report in connection with evaluating the Company. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also have a material adverse effect on the business, financial condition, results of operations and cash flows.

The Macao Government could grant additional rights to conduct gaming in the future.

We hold a subconcession under one of only six gaming concessions and subconcessions authorized by the Macao Government to operate casinos in Macao. No additional concessions or subconcessions have been granted since 2002; however, if the Macao Government were to allow additional gaming operators in Macao, we would face additional competition, which could have a material adverse effect on our financial condition, results of operations and cash flows.

Our business is particularly sensitive to reductions in discretionary consumer and corporate spending as a result of downturns in the economy.

Consumer demand for hotel/casino resorts, trade shows and conventions and for the type of luxury amenities we offer is particularly sensitive to downturns in the economy and the corresponding impact on discretionary spending. Changes in discretionary consumer spending or corporate spending on conventions and business travel could be driven by many factors, such as: perceived or actual general economic conditions; any weaknesses in the job or housing market, additional credit market disruptions; high energy, fuel and food costs; the increased cost of travel; the potential for bank failures; perceived or actual disposable consumer income and wealth; fears of recession and changes in consumer confidence in the economy; or fears of war and future acts of terrorism. These factors could reduce consumer and corporate demand for the luxury amenities and leisure and business activities we offer, thus imposing additional limits on pricing and harming our operations.

The number of visitors to Macao, particularly visitors from mainland China, may decline or travel to Macao may be disrupted.

Our VIP and mass market gaming customers typically come from nearby destinations in Asia, including mainland China, Hong Kong, South Korea and Japan. Increasingly, a significant number of gaming customers come to our casinos from mainland China. Any slowdown in economic growth or changes of China’s current restrictions on travel and currency movements could further disrupt the number of visitors from mainland China to our properties as well as the amounts they are willing and able to spend while at our properties.

Policies and measures adopted from time to time by the Chinese government include restrictions imposed on exit visas granted to residents of mainland China for travel to Macao and Hong Kong. These measures have, and any future policy developments implemented may have, the effect of reducing the number of visitors to Macao from mainland China, which could adversely impact tourism and the gaming industry in Macao.

Our operations face intense competition.

The hotel, resort and casino businesses are highly competitive. Our operations currently compete with numerous other casinos located in Macao. Additional Macao facilities announced by our competitors and the increasing capacity of hotel rooms in Macao could add to the competitive dynamic of the market.

Our operations will also compete to some extent with casinos located elsewhere in Asia, including Singapore, South Korea, Malaysia, Philippines, Australia, Cambodia and elsewhere in the world, including Las Vegas, as well as online gaming and cruise ships that offer gaming. Our operations also face increased competition from new developments in Malaysia, Australia and South Korea. In addition, certain countries have legalized, and others may in the future legalize, casino gaming, including Japan, Taiwan, Thailand and Vietnam.

The proliferation of gaming venues, especially in Southeast Asia, could have a significant and adverse effect on our financial condition, results of operations and cash flows.

Our business could be adversely affected by the limitations of the pataca exchange markets and restrictions on the export of the Renminbi.

Our revenues in Macao are denominated in patacas, the legal currency of Macao, and HK dollars. The Macao pataca is pegged to the HK dollar (which is pegged to the US$) and, in many cases, is used interchangeably with the HK dollar in Macao. Although currently

permitted, we cannot assure you patacas will continue to be freely exchangeable into U.S. dollars. Also, our ability to convert large amounts of patacas into U.S. dollars over a relatively short period may be limited.

We are currently prohibited from accepting wagers in Renminbi, the legal currency of China. There are also restrictions on the remittance of the Renminbi from mainland China and the amount of Renminbi that can be converted into foreign currencies, including the pataca and HK dollar. Restrictions on the remittance of the Renminbi from mainland China may impede the flow of gaming customers from mainland China to Macao, inhibit the growth of gaming in Macao and negatively impact our gaming operations. There is no assurance incremental mainland Chinese regulations will not be promulgated in the future that have the effect of restricting or eliminating the remittance of Renminbi from mainland China. Further, if any new mainland Chinese regulations are promulgated in the future that have the effect of permitting or restricting (as the case may be) the remittance of Renminbi from mainland China, then such remittances will need to be made subject to the specific requirements or restrictions set out in such rules.

Conducting business in Macao has certain political and economic risks.

Our operations in Macao include The Venetian Macao, Sands Cotai Central, The Parisian Macao, The Plaza Macao and Sands Macao. Accordingly, our business development plans, financial condition, results of operations and cash flows may be materially and adversely affected by significant political, social and economic developments in Macao, and by changes in policies of the government or changes in laws and regulations or their interpretations. Our operations in Macao are also exposed to the risk of changes in laws and policies that govern operations of companies based in Macao. Jurisdictional tax laws and regulations may also be subject to amendment or different interpretation and implementation, thereby having an adverse effect on our profitability after tax. These changes may have a material adverse effect on our financial condition, results of operations and cash flows.

Current Macao laws and regulations concerning gaming and gaming concessions and licenses are, for the most part, fairly recent and there is little precedent on the interpretation of these laws and regulations. We believe our organizational structure and operations are in compliance in all material respects with all applicable laws and regulations of Macao. These laws and regulations are complex and a court or an administrative or regulatory body may in the future render an interpretation of these laws and regulations, or issue regulations, which differs from our interpretation and could have a material adverse effect on our financial condition, results of operations and cash flows.

In addition, our activities in Macao are subject to administrative review and approval by various government agencies. We cannot assure you we will be able to obtain all necessary approvals, which may have a material adverse effect on our long-term business strategy and operations. Macao laws permit redress to the courts with respect to administrative actions; however, such redress is largely untested in relation to gaming issues.

On October 6, 2014, the Macao Government approved smoking control legislation, which prohibits smoking in casinos. This legislation, as amended on July 14, 2017 and effective as of January 1, 2018, permits casinos to maintain designated smoking rooms opened to the public, as long as such rooms comply with certain conditions, including no gaming equipment is installed within a three-meter radius from their entrance doors, they are physically separated from the remaining areas, and no activity other than smoking is conducted inside the rooms including gaming. Such legislation may deter potential gaming customers who are smokers from frequenting casinos in jurisdictions with smoking bans such as Macao. Such laws and regulations could change or could be interpreted differently in the future. We cannot predict the future likelihood or outcome of similar legislation or referendums or the magnitude of any decrease in revenues as a result of such regulations, though any smoking ban could have an adverse effect on our business, financial condition, results of operations and cash flows.

Our business is sensitive to the willingness of our customers to travel. Acts of terrorism, regional political events and developments in the conflicts in certain countries could cause severe disruptions in air travel that reduce the number of visitors to our facilities.

We are dependent on the willingness of our customers to travel. Only a small amount of our business is and will be generated by local residents. Most of our customers travel to reach our properties. Acts of terrorism may severely disrupt domestic and international travel, which would result in a decrease in customer visits to Macao, including our properties. Regional political events, including those resulting in travelers perceiving areas as unstable or an unwillingness of governments to grant visas, regional conflicts or an outbreak of hostilities or war could have a similar effect on domestic and international travel. Management cannot predict the extent to which disruptions in air or other forms of travel as a result of any further terrorist acts, regional political events, regional conflicts or outbreak of hostilities or war would have a material adverse effect on our business, financial condition, results of operations and cash flows.

Our failure to maintain the integrity of our information and information systems, which contain legally protected information about us and others, could happen in a variety of ways, including as a result of unauthorized access, breach of our cybersecurity systems and measures, or other disruption or corruption of our information systems, software or data, or access to information stored outside of our information systems, and could impair our ability to conduct our business operations, delay our ability to

recognize revenue, compromise the integrity of our business and services, result in significant data losses and the theft of our intellectual property, damage our reputation, expose us to liability to third parties, regulatory fines and penalties, and require us to incur significant costs to maintain the privacy and security of our information, network and data.

We face global cybersecurity and information security threats, which may range from uncoordinated individual attempts to sophisticated and targeted measures directed at us. Cyber-attacks and information security breaches may include, but are not limited to, attempts to access information, including legally protected information about people including customers and company information, computer malware such as viruses, denial of service, ransomware attacks that encrypt, exfiltrate, or otherwise render data unusable or unavailable in an effort to extort money or other consideration as a condition to purportedly returning the data to a usable form, operator errors or misuse, or inadvertent releases of data or documents, and other forms of electronic and non-electronic information security breaches.

Our business requires the collection and retention of large volumes of data and non-electronic information, including credit card numbers and other legally protected information about people in various information systems we maintain and in those maintained by third parties with whom we contract and may share data. We also maintain important internal company information such as legally protected information about our employees and information relating to our operations. The integrity and protection of that legally protected information about people and company information are important to us. Our collection of such legally protected information about people and company information is subject to extensive regulation by private groups such as the payment card industry as well as domestic and foreign governmental authorities, including gaming authorities. If a cybersecurity or privacy event occurs, we may be unable to satisfy applicable laws and regulations or the expectation of regulators, employees, customers or other impacted individuals.

Privacy and cybersecurity laws and regulations are developing and changing frequently, and vary significantly by jurisdiction. Many applicable laws and regulations protecting privacy and addressing cybersecurity have not yet been interpreted by regulators or courts, which causes uncertainty. We may incur significant costs in our efforts to comply with the various applicable privacy and cybersecurity laws and regulations as they emerge and change. Also, privacy and cybersecurity laws and regulations may limit our ability to protect individuals, including customers and employees. For example, these laws and regulations may restrict information sharing in ways that make it more difficult to obtain or share information concerning at-risk individuals. Compliance with applicable privacy laws and regulations also may adversely impact our ability to market our products, properties, and services to our guests and patrons. In addition, non-compliance by us, or potentially by third parties with which we share information, with any applicable privacy and cybersecurity law or regulation, including accidental loss, inadvertent disclosure, unauthorized access or dissemination, or breach of security may result in damage to our reputation and could subject us to fines, penalties, required corrective actions, lawsuits, payment of damages, or restrictions on our use or transfer of data. We are subject to different regulators' and others' interpretations of our compliance with these new and changing laws and regulations.

In addition, LVS, our parent, has experienced a sophisticated criminal cybersecurity attack in the past, including a breach of its information technology systems in which customer and company information was compromised and certain company data may have been destroyed, and LVS or we may experience additional cybersecurity attacks in the future, potentially with more frequency or sophistication. We rely on proprietary and commercially available systems, software, tools, and monitoring to provide security for processing, transmission, and storage of customer and employee information, such as payment card and other confidential or proprietary information. We also rely extensively on computer systems to process transactions, maintain information, and manage our businesses. Disruptions in the availability of our computer systems, through cyber-attacks or otherwise, could impact our ability to service our customers and adversely affect our revenues and results of operations. For instance, there has been an increase in criminal cybersecurity attacks against companies where customer and company information has been compromised and company data has been destroyed. Our information systems and records, including those we maintain with third-party service providers, as well as the systems of other third parties that share data with us under contractual agreements, may be subject to cyber-attacks and information security breaches. Our third-party information system service providers and other third parties that share data with us pursuant to contractual agreements face risks relating to cybersecurity and privacy similar to ours, and we do not directly control any of such parties' information security or privacy operations. For example, the systems currently used for the transmission and approval of payment card transactions, and the technology utilized in payment cards themselves, all of which can put payment card data at risk, are determined and controlled by the payment card industry, not us.

A significant theft, destruction, loss or fraudulent use of legally protected information about people or company information maintained by us or by a third-party service provider or other third party that shares data with us pursuant to contractual agreement could have an adverse effect on our reputation, cause a material disruption to our operations and management team and result in remediation expenses (including liability for stolen assets or information, repairing system damage and offering incentives to customers or business partners to maintain their relationships after an attack) and regulatory fines, penalties and corrective actions, or lawsuits by regulators, third-party service providers, third parties that share data with us pursuant to contractual agreements and/or people whose data is or may be impacted. Such theft, destruction, loss or fraudulent use could also result in litigation by shareholders alleging our privacy protections and protections against cyber-attacks were insufficient, our response to an attack was faulty or insufficient care was taken in ensuring we were able to comply with cybersecurity, privacy or data protection regulations, protect information, identify risks and attacks, or

respond to and recover from a cyber-attack, or by customers and other parties whose information was subject to such attacks. Advances in computer software capabilities and encryption technology, new tools, and other developments, including continuously evolving attack methods that may exploit vulnerabilities based on these advances, may increase the risk of a security breach or other intrusion. In addition, we may incur increased cybersecurity and privacy protection costs that may include organizational changes, deploying additional personnel and protection technologies, training employees and engaging third-party experts and consultants. There can be no assurance the insurance we have in place relating to cybersecurity and privacy risks will be sufficient in the event of a major cybersecurity or privacy event. Any of these events could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are subject to extensive regulation and the cost of compliance or failure to comply with such regulations.

We are required to obtain and maintain licenses from various jurisdictions in order to operate certain aspects of our business, and we are subject to extensive background investigations and suitability standards in our gaming business. We also will become subject to regulation in any other jurisdiction where we choose to operate in the future. There can be no assurance we will be able to obtain new licenses or renew any of our existing licenses, or if such licenses are obtained, such licenses will not be conditioned, suspended or revoked; and the loss, denial or non-renewal of any of our licenses could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are a subsidiary of LVS and are therefore subject to certain Nevada gaming laws, which apply to our gaming activities and associations in jurisdictions outside the State of Nevada. We are required to comply with certain reporting requirements concerning our current and proposed gaming activities and associations occurring outside the State of Nevada, including Macao. Also, as we are required to provide any other information the Nevada Commission may require concerning our gaming activities and associations in jurisdictions outside the State of Nevada, we could be subject to disciplinary action by the Nevada Commission if our current reporting is determined to be unsatisfactory due to Macao regulations regarding personal data protection prohibiting us from satisfying certain reporting requirements of the Nevada Commission.

We are also subject to regulations imposed by the FCPA, which generally prohibits U.S. companies and their intermediaries from making improper payments to foreign officials for the purpose of obtaining or retaining business. LVS entered into a comprehensive civil administrative settlement with the SEC on April 7, 2016, and a non-prosecution agreement with the DOJ on January 19, 2017, which resolved all inquiries related to these government investigations and include ongoing reporting obligations to the DOJ through January 2020. Any violation of the FCPA could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We also deal with significant amounts of cash in our operations and are subject to various reporting and anti-money laundering regulations. Recently, various governmental authorities have evidenced an increased focus on the gaming industry and compliance with anti-money laundering laws and regulations. For instance, we are subject to regulation which, among other things, requires us to report to the various government authorities certain currency transactions in excess of applicable thresholds and certain suspicious activities where we know, suspect or have reason to suspect such transactions involve funds from illegal activity or are intended to violate certain laws or regulations or are designed to evade reporting requirements or have no business or lawful purpose. In addition, we are subject to various other rules and regulations involving reporting, recordkeeping and retention. Our compliance with these requirements is subject to periodic audits, and we may be subject to substantial civil and criminal penalties, including fines, if we fail to comply with applicable regulations. We are also subject to regulations set forth by the gaming authorities in the areas in which we operate. Any such laws and regulations could change or could be interpreted differently in the future, or new laws and regulations could be enacted. Any violation of anti-money laundering laws or regulations, or any accusations of money laundering or regulatory investigations into possible money laundering activities, by any of our properties, employees or customers could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are currently not required to pay corporate income taxes on our casino gaming operations in Macao. Additionally, we currently have an agreement with the Macao Government providing for a fixed annual payment as a substitution for a 12% tax otherwise due from VML’s shareholders on dividends distributed from our gaming operations. These tax arrangements expire on June 26, 2022, the date our subconcession agreement expires.

We have had the benefit of a corporate tax exemption in Macao, which exempts us from paying the 12% corporate income tax on profits generated by the operation of casino games. This exemption does not apply to our non-gaming activities. We will continue to benefit from this tax exemption through June 26, 2022, the date our subconcession agreement expires. Additionally, we entered into an agreement with the Macao Government in April 2019, effective through June 26, 2022, providing for an annual payment as a substitution for a 12% tax otherwise due from VML shareholders on dividend distributions paid from VML gaming profits. There is no certainty these agreements will be extended beyond their expiration dates, which could have a material adverse effect on our financial condition, results of operations and cash flows.

We will stop generating any gaming revenues from our operations if we cannot secure an extension of our subconcession in 2022 or if the Macao Government exercises its redemption right.

Our subconcession agreement expires on June 26, 2022. Unless our subconcession is extended, all of VML’s casino premises and gaming-related equipment will be transferred automatically to the Macao Government on that date without compensation to us and we will cease to generate gaming revenues from these operations. Beginning on December 26, 2017, the Macao Government may redeem the subconcession agreement by providing us at least one-year prior notice. In the event the Macao Government exercises this redemption right, we are entitled to fair compensation or indemnity. The amount of this compensation or indemnity will be determined based on the amount of gaming and non-gaming revenue generated by VML during the tax year prior to the redemption multiplied by the number of remaining years before expiration of the subconcession. We cannot assure you we will be able to renew or extend our subconcession agreement on terms favorable to us or at all. We also cannot assure you if our subconcession is redeemed, the compensation paid will be adequate to compensate us for the loss of future revenues.

Our subconcession can be terminated under certain circumstances without compensation to us.

The Macao Government has the right, after consultation with Galaxy Casino S.A. (one of the three Concessionaires), to unilaterally terminate our subconcession in the event of VML’s serious non-compliance with its basic obligations under the subconcession and applicable Macao laws. Upon termination of our subconcession, our casinos and gaming-related equipment would automatically be transferred to the Macao Government without compensation to us and we would cease to generate any revenues from these operations. The loss of our subconcession would prohibit us from conducting gaming operations in Macao, which would have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are dependent upon gaming promoters for a portion of our gaming revenues in Macao.

Gaming promoters, which promote gaming and draw VIP patrons to casinos, are responsible for a portion of our gaming revenues in Macao. With the increased number of gaming facilities in Macao, the competition for relationships with gaming promoters has increased. There can be no assurance we will be able to maintain, or grow, our relationships with gaming promoters. If we are unable to maintain or grow our relationships with gaming promoters, or if the gaming promoters experience financial difficulties or are unable to develop or maintain relationships with our VIP patrons, our ability to grow our gaming revenues will be hampered.

If gaming promoters attempt to negotiate changes to our operational agreements, including higher commissions, it could result in higher costs for us, loss of business to a competitor or loss of relationships with gaming promoters. Given regulatory requirements and certain economic and other factors occurring in the region, gaming promoters may encounter difficulties in attracting patrons to come to Macao, resulting in decreased gaming volume at our properties. Credit already extended by gaming promoters to their patrons may become increasingly difficult for them to collect. This inability to attract sufficient patrons, grant credit and collect amounts due in a timely manner could negatively affect gaming promoters’ activities, cause gaming promoters to wind up or liquidate their operations or result in gaming promoters leaving Macao. The above factors affecting gaming promoters could have a material adverse effect on our business, financial condition, results of operations and cash flows.

In addition, the quality of gaming promoters with whom we have relationships is important to our reputation and our ability to continue to operate in compliance with our gaming license. While we strive for excellence in our associations with gaming promoters, we cannot assure you the gaming promoters with whom we are associated will meet the high standards we insist upon. If a gaming promoter falls below our standards, we may suffer reputational harm, as well as worsening relationships with, and possible sanctions from, gaming regulators with authority over our operations. In the event a gaming promoter does not meet its financial obligations, there can be no assurance we may not incur financial exposure.

We extend credit to a large portion of our customers and we may not be able to collect gaming receivables from our credit players.

We conduct our gaming activities on a credit and cash basis. Any such credit we extend is unsecured. Table games players typically are extended more credit than slot players, and high-stakes players typically are extended more credit than players who tend to wager lesser amounts. High-end gaming is more volatile than other forms of gaming, and variances in win-loss results attributable to high-end gaming may have a significant positive or negative impact on cash flow and earnings in a particular quarter.

During the year ended December 31, 2018, approximately 15.3% of our table games drop, was from credit-based wagering. We extend credit to those customers whose level of play and financial resources warrant, in the opinion of management, an extension of credit. These large receivables could have a significant impact on our results of operations if deemed uncollectible.

In particular, we expect our operations will be able to enforce gaming debts only in a limited number of jurisdictions, including Macao. To the extent our gaming customers and gaming promoters are from other jurisdictions, our operations may not have access to a forum in which it will be possible to collect all gaming receivables because, among other reasons, courts of many jurisdictions do not

enforce gaming debts and our operations may encounter forums that will refuse to enforce such debts. Moreover, under applicable law, our operations remain obligated to pay taxes on uncollectible winnings from customers.

Even where gaming debts are enforceable, they may not be collectible. Our inability to collect gaming debts could have a significant adverse effect on our results of operations and cash flows.

We face the risk of fraud and cheating.

Our gaming customers may attempt or commit fraud or cheat in order to increase winnings. Acts of fraud or cheating could involve the use of counterfeit chips or other tactics, possibly in collusion with our employees. Internal acts of cheating could also be conducted by employees through collusion with dealers, surveillance staff, floor managers or other casino or gaming area staff. Failure to discover such acts or schemes in a timely manner could result in losses in our gaming operations. In addition, negative publicity related to such schemes could have an adverse effect on our reputation, potentially causing a material adverse effect on our business, financial condition, results of operations and cash flows.

We depend on the continued services of key managers and employees. If we do not retain our key personnel or attract and retain other highly skilled employees, our business will suffer.

Our ability to maintain our competitive position is dependent to a large degree on the services of our senior management team, including Mr. Sheldon Gary Adelson, Dr. Wong Yin Wai (Wilfred), Mr. Chum Kwan Lock (Grant) and Mr. Sun MinQi (Dave). The loss of their services or the services of our other senior managers, or the inability to attract and retain additional senior management personnel could have a material adverse effect on our business.

We compete for limited management and labor resources in Macao, and policies of government may also affect our ability to employ imported managers or labor.

Our success depends in large part upon our ability to attract, retain, train, manage and motivate skilled managers and employees at our properties. The Macao Government requires we only hire Macao residents in our casinos for certain employee roles, such as dealers. In addition, we are required to obtain visas and work permits for managers and employees we seek to employ from other countries. There is significant competition for managers and employees with the skills required to perform the services we offer and competition for these individuals in Macao is likely to increase as other competitors expand their operations.

We may have to recruit managers and employees from other countries to adequately staff and manage our properties and certain Macao Government policies affect our ability to hire non-resident managers and employees in certain job classifications. Despite our coordination with the Macao labor and immigration authorities to ensure our management and labor needs are satisfied, we may not be able to recruit and retain a sufficient number of qualified managers or employees for our operations or the Macao labor and immigration authorities may not grant us the necessary visas or work permits.

If we are unable to obtain, attract, retain and train skilled managers and employees, and obtain any required visas or work permits for our skilled managers and employees, our ability to adequately manage and staff our existing properties and planned development projects could be impaired, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

The transportation infrastructure in Macao may not be adequate to accommodate increased future demand of visitors to Macao.

Macao is in the process of expanding its transportation infrastructure to service the increased number of visitors to Macao. If the planned expansions of transportation facilities to and from Macao are delayed or not completed, and Macao’s transportation infrastructure is insufficient to meet the demands of an increased volume of visitors to Macao, the desirability of Macao as a leisure and business tourism destination, as well as the results of operations of our properties, could be negatively impacted.

Our gaming operations rely heavily on technology services provided by third parties. In the event there is an interruption of these services to us, it may significantly impact us.

We engage a number of third parties to provide gaming operating systems for the facilities we operate. As a result, we rely on such third parties to provide uninterrupted services to us in order to run our business efficiently and effectively. In the event one of these third parties experiences a disruption in its ability to provide such services to us (whether due to technological difficulties or power problems), this may result in a material disruption at the gaming facilities in which we operate and have a material adverse effect on our business, financial condition, results of operations and cash flows.

Any unscheduled interruption in our technology services is likely to result in an immediate, and possibly substantial, loss of revenues due to a shutdown of our gaming operations, cloud computing and gaming systems. Such interruptions may occur as a result of, for example, catastrophic events or rolling blackouts. Our systems are also vulnerable to damage or interruption from earthquakes, floods, typhoons, fires, telecommunication failures, terrorist attacks, computer viruses, computer denial-of-service attacks and similar events.

Natural or man-made disasters, an outbreak of highly infectious disease, terrorist activity or war could adversely affect the number of visitors to our facilities and disrupt our operations.

So called “Acts of God,” such as typhoons and rainstorms, particularly in Macao, and other natural disasters, man-made disasters, outbreaks of highly infectious diseases, terrorist activity or war may result in decreases in travel to and from, and economic activity in, areas in which we operate, and may adversely affect the number of visitors to our properties. Any of these events also may disrupt our ability to staff our business adequately, could generally disrupt our operations and could have a material adverse effect on our business, financial condition, results of operations and cash flows. Although we have insurance coverage with respect to some of these events, we cannot assure you any such coverage will be sufficient to indemnify us fully against all direct and indirect costs, including any loss of business that could result from substantial damage to, or partial or complete destruction of, any of our properties.

VML may have financial and other obligations to foreign workers managed by its contractors under government labor quotas.

In January 2019, the Macao Government has granted VML a quota to permit it to hire foreign workers. VML has effectively assigned the management of this quota to its contractors for the construction of our Cotai Strip projects. VML, however, remains ultimately liable for all employer obligations relating to these employees, including for payment of wages and taxes and compliance with labor and workers’ compensation laws. VML requires each contractor to whom it has assigned the management of part of its labor quota to indemnify VML for any costs or liabilities VML incurs as a result of such contractor’s failure to fulfill employer obligations. VML’s agreements with its contractors also contain provisions that permit it to retain some payments for up to one year after the contractors’ complete work on the projects. We cannot assure you VML’s contractors will fulfill their obligations to employees hired under the labor quotas or to VML under the indemnification agreements, or the amount of any indemnification payments received will be sufficient to pay for any obligations VML may owe to employees managed by contractors under VML’s quotas. Until we make final payments to our contractors, we have offset rights to collect amounts they may owe us, including amounts owed under the indemnities relating to employer obligations. After we have made the final payments, it may be more difficult for us to enforce any unpaid indemnity obligations.

There are significant risks associated with our construction projects.

In 2018, we announced the renovation, expansion and rebranding of Sands Cotai Central into The Londoner Macao, the addition of approximately 370 luxury suites within the tower also occupied by the St. Regis hotel and the development of approximately 290 additional premium quality suites in the Four Seasons Tower Suites Macao. These development projects and any other construction projects we undertake will entail significant risks. Construction activity requires us to obtain qualified contractors and subcontractors, the availability of which may be uncertain. Construction projects are subject to cost overruns and delays caused by events outside of our control or, in certain cases, our contractors’ control, such as shortages of materials or skilled labor, unforeseen engineering, environmental and/or geological problems, work stoppages, weather interference, unanticipated cost increases and unavailability of construction materials or equipment. Construction, equipment or staffing problems or difficulties in obtaining any of the requisite materials, licenses, permits, allocations and authorizations from governmental or regulatory authorities could increase the total cost, delay, jeopardize, prevent the construction or opening of our projects, or otherwise affect the design and features. Construction contractors or counterparties for our current projects may be required to bear certain cost overruns for which they are contractually liable, and if such counterparties are unable to meet their obligations, we may incur increased costs for such developments. If our management is unable to manage successfully our construction projects, it could have a material adverse effect on our financial condition, results of operations and cash flows.

The anticipated costs and completion dates for our current projects are based on budgets, designs, development and construction documents. Schedule estimates are prepared with the assistance of architects and other construction development consultants and are subject to change as the design, development and construction documents are finalized and as actual construction work is performed. A failure to complete our projects on budget or on schedule may have a material adverse effect on our financial condition, results of operations and cash flows.

Our debt instruments, current debt service obligations and substantial indebtedness may restrict our current and future operations, particularly our ability to timely refinance existing indebtedness, finance additional growth, respond to changes or take some actions that may otherwise be in our best interests.

Our current debt service obligations contain, or any future debt service obligations and instruments may contain, a number of restrictive covenants that impose significant operating and financial restrictions on us, including restrictions on our ability to:

| |

| • | incur additional debt, including providing guarantees or credit support; |

| |

| • | incur liens securing indebtedness or other obligations; |

| |

| • | dispose of certain assets; |

| |

| • | make certain acquisitions; |

| |

| • | pay dividends or make distributions and make other restricted payments, such as purchasing equity interests, repurchasing junior indebtedness or making investments in third parties; |

| |

| • | enter into sale and leaseback transactions; |

| |

| • | engage in any new businesses; |

| |

| • | issue preferred stock; and |

| |

| • | enter into transactions with our stockholders and our affiliates. |

In addition, our credit agreements contain various financial covenants. See “Notes to the Consolidated Financial Statements — 24. Borrowings” further description of these covenants.

At December 31, 2018, we had US$5.56 billion of long-term debt outstanding, net of original issue discount, deferred offering costs and cumulative fair value adjustments. This indebtedness could have important consequences to us. For example, it could:

| |

| • | make it more difficult for us to satisfy our debt service obligations; |

| |

| • | increase our vulnerability to general adverse economic and industry conditions; |

| |

| • | impair our ability to obtain additional financing in the future for working capital needs, capital expenditures, development projects, acquisitions or general corporate purposes; |

| |

| • | require us to dedicate a significant portion of our cash flow from operations to the payment of principal and interest on our debt, which would reduce the funds available for our operations and development projects; |

| |

| • | limit our flexibility in planning for, or reacting to, changes in the business and the industry in which we operate; |

| |

| • | require us to repurchase our Senior Notes (as defined in Item 5 - “A. Operating Results”) upon certain events, such as any change in gaming law or any action by a gaming authority after which none of the Group members owns or manages casino or gaming areas or operates casino games of fortune and chance in Macao in substantially the same matter as the Group was at the issue date of the Senior Notes for a period of 30 consecutive days or more; |

| |

| • | place us at a competitive disadvantage compared to our competitors that have less debt; and |

| |

| • | subject us to higher interest expense in the event of increases in interest rates. |

Our ability to timely refinance and replace our indebtedness in the future will depend upon general economic and credit market conditions, approval required by local government regulators, adequate liquidity in the global credit markets, the particular circumstances of the gaming industry and prevalent regulations and our cash flow and operations, in each case as evaluated at the time of such potential refinancing or replacement. If we are unable to refinance or generate sufficient cash flow from operations to repay our indebtedness on a timely basis, we might be forced to seek alternate forms of financing, dispose of certain assets or minimize capital expenditures and other investments, or reduce dividend payments. There is no assurance any of these alternatives would be available to us, if at all, on satisfactory terms, on terms that would not be disadvantageous to us, or on terms that would not require us to breach the terms and conditions of our existing or future debt agreements.

We may attempt to arrange additional financing to fund the remainder of our planned, and any future, development projects. If such additional financing is necessary, we cannot assure you we will be able to obtain all the financing required for the construction and opening of these projects on suitable terms, if at all.

Our insurance coverage may not be adequate to cover all possible losses our properties could suffer. In addition, our insurance costs may increase and we may not be able to obtain the same insurance coverage, or the scope of insurance coverage we deem necessary, in the future.

We have comprehensive property and liability insurance policies for our properties in operation, as well as those in the course of construction, with coverage features and insured limits we believe are customary in their breadth and scope. Market forces beyond our control may nonetheless limit the scope of the insurance coverage we can obtain or our ability to obtain coverage at reasonable rates. Certain types of losses, generally of a catastrophic nature, such as earthquakes, typhoons and floods, or terrorist acts, or certain liabilities may be uninsurable or too expensive to justify obtaining insurance. As a result, we may not be successful in obtaining insurance without increases in cost or decreases in coverage levels. In addition, in the event of a substantial loss, the insurance coverage we carry may not be sufficient to pay the full market value or replacement cost of our lost investment or in some cases could result in certain losses being

totally uninsured. As a result, we could lose some or all of the capital we have invested in a property, as well as the anticipated future revenue from the property, and we could remain obligated for debt or other financial obligations related to the property.

Our debt instruments and other material agreements require us to maintain a certain level of insurance. Failure to satisfy these requirements could result in an event of default under these debt instruments or material agreements.

The Senior Notes could face risks which could have important consequences for the holders of the Senior Notes and significant effects on our business and future operations.

We may incur secured indebtedness or other secured obligations in the future. The claims of the holders of the Senior Notes will be effectively subordinated to any secured indebtedness and other secured obligations of the Company to the extent of the value of the assets securing such indebtedness or other obligations.

The Senior Notes are structurally subordinated to the liabilities of our subsidiaries and our subsidiaries do not have any obligations to pay amounts due under the Senior Notes or to make funds available for that purpose. In the event any of our subsidiaries becomes insolvent, is liquidated, reorganized or dissolved, or is otherwise wound up other than as a part of a solvent transaction, the holders of the Senior Notes will have no right to proceed against the assets of such subsidiary. Additionally, as a holding company, we depend on the receipt of dividends and the interest or principal payments on intercompany loans or advances from our subsidiaries to satisfy our obligations, including our obligations under the Senior Notes. The ability of our subsidiaries to pay dividends and make payments on intercompany loans or advances to their shareholders is subject to, among other things, distributable earnings, cash flow conditions, restrictions contained in the articles of association of our subsidiaries and applicable laws. Certain of our subsidiaries have incurred debt in their own name and may do so again in the future, and the instruments governing such debt may require the lenders’ consent prior to the subsidiaries declaring dividends or otherwise restrict dividends or other distributions on their equity interests to us. These restrictions could reduce the amounts we receive from our subsidiaries, which would restrict our ability to meet our payment obligations under the Senior Notes.

The Senior Notes have limited covenants that may not protect against developments that may impair their trading price or our ability to repay them.

Upon the occurrence of certain triggering events prescribed by the Senior Notes, we must offer to purchase the Senior Notes. The sources of funds for any such purchases is limited to our available cash or third-party financing. We may not have enough funds to make the required purchase, thus triggering an event of default under the Senior Notes. This event of default may, in turn, trigger an event of default on other indebtedness for which we may not have sufficient funds to purchase the Senior Notes and repay the other indebtedness.

ITEM 4. — INFORMATION ON THE COMPANY

A. HISTORY AND DEVELOPMENT OF THE COMPANY

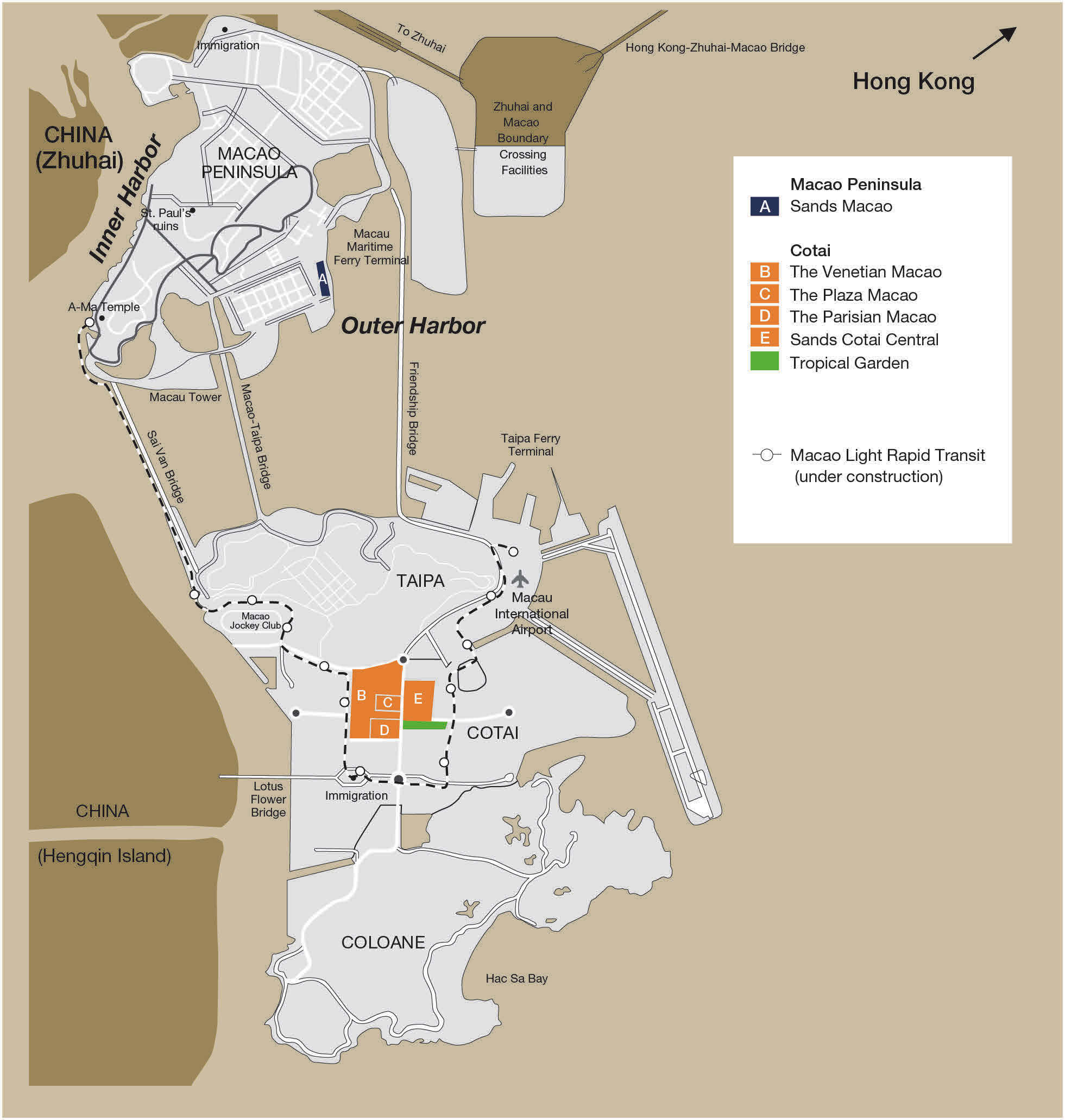

Sands China Ltd. was incorporated in the Cayman Islands on July 15, 2009 as an exempted company with limited liability under the Companies Law, Cap 22 (Law 3 of 1961, as consolidated and revised) of the Cayman Islands. Our principal executive offices are located at The Venetian Macao Resort Hotel, L2 Executive Offices, Estrada da Baía de N. Senhora da Esperança, s/n, Macao SAR. Our telephone number at this address is +853 8118-2888. Our registered office in the Cayman Islands is located at the offices of Intertrust Corporate Services (Cayman) Limited, 190 Elgin Avenue, George Town, Grand Cayman KY1-9005, Cayman Islands. Our principal place of business is Level 54, Hopewell Centre, 183 Queen’s Road East, Hong Kong. Our agent for service of process in the United States is Corporation Service Company located at 1180 Avenue of the Americas, Suite 210, New York, New York 10036. Our corporate website is www.sandschina.com. The information contained on our website is not a part of this annual report. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that site is www.sec.gov.

For a description of our principal capital expenditures for the years ended December 31, 2018, 2017 and 2016, see “Item 5 - Operating and Financial Review and Prospects — B. Liquidity and Capital Resources.”

B. BUSINESS OVERVIEW

Overview

We are the leading developer, owner and operator of large-scale integrated resorts in Macao. In 2018, we welcomed approximately 99.3 million leisure and business visits at our properties on Cotai and on the Macao peninsula.

Our founder, chairman and chief executive officer, Sheldon G. Adelson, began investing in Macao in 2002 after being awarded a gaming subconcession to operate casino games and other games of chance in Macao. His vision and goal was to develop large-scale integrated resorts with a variety of world-class amenities and create an international tourism destination. This helped support Macao’s objective for long-term economic diversification and growth in tourism.

Today, with nearly 30 million square feet of interconnected facilities on Cotai, we operate the largest integrated resorts in Macao. These integrated resorts contain not only gaming areas, but also the largest number of four- and five-star rated hotel rooms of any other single developer in the market. Our integrated resorts also collectively feature the largest amount of meeting space, convention and exhibition halls, retail and dining areas and entertainment venues. We believe that our integrated resorts are unique to Macao and differentiate us from our competitors due to their size and scale, diversity of non-gaming amenities, and focus on leisure and business tourism.

According to research by the University of Nevada Las Vegas, Macao is the largest gaming market in the world as measured by casino gaming revenue and is the only location in China offering legalized casino gaming. VML, our subsidiary, holds one of six concessions or subconcessions permitted by the Macao Government to operate casinos or gaming areas in Macao.

We developed, own and operate The Venetian Macao, Sands Cotai Central, The Parisian Macao, The Plaza Macao and Sands Macao. We also own Cotai Expo, one of the largest convention and exhibition centers in Asia, as well as Macao’s largest entertainment venue, the Cotai Arena. Our properties collectively feature over 12,300 luxury suites and hotel rooms, more than 150 different restaurants and food outlets, spas, theaters for live performances, as well as other integrated resort amenities.

Our integrated resort brands, including The Venetian Macao and The Parisian Macao, are aspirational and have become recognized throughout China and Asia for quality and service and are designed to ensure a lasting connection with our customers. We believe The Venetian Macao is the most visited integrated resort in Asia, and since its opening in 2007, the property has received over 330 million visitations up to December 31, 2018. We estimate that since 2016, The Parisian Macao digital marketing and social media program has reached over nine billion online impressions up to December 31, 2018, including from platforms within China such as Sina Weibo.

We were the first developer in Macao to feature global hospitality brands for our hotel offerings on Cotai, including the Four Seasons, St. Regis, Conrad, Sheraton and Holiday Inn brands.

Within our integrated resorts, we also operate some of the largest and most profitable retail malls in Asia, showcasing over 820 shops occupying over 2 million square feet of retail space. Our retail malls showcase global luxury brands as well as leading Asian retail brands.

We own and operate CotaiJet, one of two major high speed ferry companies operating between Hong Kong and Macao, with 14 vessels helping leisure and business tourists reach Macao from points in Hong Kong, including the Hong Kong International Airport.

Our Developments in Macao

In May 2004, we opened the Sands Macao, the first Las Vegas style resort in Macao, which was designed for the mass market segment of leisure tourism. The Sands Macao currently contains a mix of gaming areas for mass market, VIP and premium players, entertainment and dining facilities, and hotel suites.

In August 2007, we opened The Venetian Macao, the flagship property of our Cotai Strip development. The Venetian Macao is a themed, large-scale integrated resort, with over 2,900 luxury hotel suites, more than 350 retail shops in one of the largest shopping malls in Asia with approximately 943,000 square feet of retail space, more than 50 restaurants and food outlets, and a state-of-the-art live performance theater with 1,800 seats. In addition, The Venetian Macao contains the Cotai Arena, a 15,000-seat venue directly adjacent to and which adjoins the Cotai Expo center and hosts numerous concerts, live performances, sporting events and corporate events each year. The Cotai Expo is a 1.2 million square foot first-class MICE facility, which includes exhibition and meeting space, including one of the largest column-free ballrooms in Asia.

In August 2008, we opened The Plaza Macao, a boutique luxury integrated resort featuring the Four Seasons Hotel Macao with 360 luxury suites, the Shoppes at Four Seasons with more than 140 shops from the world’s leading luxury retail brands, and the Plaza Casino. In July 2009, we completed and introduced our ultra-exclusive Paiza Mansions at The Plaza Macao.

In April 2012, we completed the first phase of Sands Cotai Central and opened the Conrad and Holiday Inn tower. This tower features approximately 650 five-star rooms and suites under the Conrad brand and approximately 1,200 four-star rooms and suites under the Holiday Inn brand. In September 2012, we opened the next phase of Sands Cotai Central with the completion of the first Sheraton tower, which features approximately 1,800 rooms and suites under the Sheraton brand.

In December 2012, we opened a fully enclosed climate-controlled footbridge between Sands Cotai Central and The Plaza Macao, with moving walkways to enhance the inter-connectivity and accessibility between our Cotai Strip properties.

In January 2013, we opened the second Sheraton tower at Sands Cotai Central, featuring approximately 2,100 additional rooms and suites under the Sheraton brand.

In December 2015, we opened the St. Regis tower at Sands Cotai Central, featuring 400 rooms and suites under the St. Regis brand.

Sands Cotai Central features approximately 367,000 square feet of gaming space, with over 390 table games and more than 1,100 slot machines or similar electronic gaming devices, and includes exclusive VIP rooms designed for VIP and premium players. Sands Cotai Central also has approximately 369,000 square feet of meeting space, a 1,701-seat theater and approximately 520,000 square feet of retail space with more than 150 stores and over 50 restaurants and food outlets.

In September 2016, we opened The Parisian Macao, a themed, iconic, “must-see” integrated resort connected to The Venetian Macao and The Plaza Macao, which includes a 253,000 square-foot casino, a hotel with approximately 2,500 rooms and suites, retail, entertainment, dining and meeting facilities. The Parisian Macao features a half size replica of the Eiffel Tower, providing a landmark attraction to visitors.

In 2018, we announced the renovation, expansion and rebranding of Sands Cotai Central into a new destination integrated resort, The Londoner Macao, by adding extensive thematic elements both externally and internally. The Londoner Macao will feature new attractions and features from London, including some of London’s most recognizable landmarks, and expanded retail and food and beverage venues. We will add approximately 370 luxury suites within the tower also occupied by the St. Regis hotel. Design work is nearing completion and construction is being initiated and will be phased to minimize disruption during the property’s peak periods. We expect the additional suites within the tower also occupied by the St. Regis hotel to be completed in the first quarter of 2020 and The Londoner Macao project to be completed in phases throughout 2020 and 2021.

In 2018, we also announced the Four Seasons Tower Suites Macao, which will feature approximately 290 additional premium quality suites. We have completed the structural work of the tower and have commenced preliminary build out of the suites. We expect the project to be completed in the first quarter of 2020.

We anticipate the total costs associated with these development projects to be approximately US$2.2 billion. The ultimate costs and completion dates for these projects are subject to change as we finalize our planning and design work and complete the projects. See “Item 3 - Key Information D. — Risk Factors — There are significant risks associated with our construction projects, which could have a material adverse effect on our financial condition, results of operations and cash flows.”

Our business strategy is to develop Cotai and to leverage our large-scale integrated resort business model to create Asia’s premier gaming, leisure, convention and meetings destination. Our interconnected integrated resorts, which have a wide range of branded hotel and resort offerings, are designed to attract different segments of the market all year round. We believe our business strategy and development plan will allow us to achieve more consistent demand, longer average length of stay in our hotels, more diversified sources of revenue and higher margins than more gaming-centric facilities.

Key Strengths

We believe we have a number of key strengths that differentiate our business from our competitors, including:

Diversified, high quality integrated resort offerings with substantial non-gaming amenities

Our integrated resorts feature non-gaming attractions and amenities including world-class entertainment, expansive retail offerings and market-leading MICE facilities. These attractions and amenities enhance the appeal of our integrated resorts, contributing to visitation, length of stay and customer expenditure at our resorts. As of December 31, 2018, our hotel inventory represented 47% of the total Macao competitor hotel inventory. The broad appeal of our market-leading integrated resort offerings in Macao enables us to serve the broadest array of customer segments in the Macao market.

Substantial and diversified cash flow from existing operations

We generated cash from operations of US$3.05 billion during the year ended December 31, 2018, from gaming and non-gaming sources, including retail, hotel, food and beverage, entertainment and MICE business.

Market leadership in the growing high-margin mass market gaming segment

We focus on the high-margin mass gaming segment, which has grown at a compound annual growth rate in excess of 11% since fiscal year 2015. During the twelve months ended December 31, 2018, we had the highest percentage of gaming win from mass tables and slots of the Macao operators, with approximately 30% market share. Our management estimates our mass market table revenues typically generate a gross margin that is approximately four times higher than the gross margin on our typical VIP table revenues.

Established brands with broad regional and international market awareness and appeal

Our brands, including The Venetian Macao, The Parisian Macao, Sands Macao, Cotai Expo, Cotai Arena, and CotaiJet enjoy broad regional and international market awareness and appeal. We welcomed approximately 99.3 million visits to our property portfolio in 2018, an increase of 7% compared to the prior year. The Venetian Macao is the most visited integrated resort in Macao, and enjoys broad brand awareness both regionally and globally. We estimate that since 2016, The Parisian Macao digital marketing and social media program has reached over nine billion online impressions up to December 31, 2018, including from platforms within China such as Sina Weibo.

Experienced management team with a proven track record

Mr. Sheldon G. Adelson is our founder, chairman and chief executive officer. Mr. Adelson’s business career spans more than seven decades and has included creating and developing to maturity numerous companies. Mr. Adelson created the MICE-based integrated resort and pioneered its development in the Las Vegas and Singapore markets, as well as in Macao, where he planned and developed the Cotai Strip. Dr. Wong Ying Wai, our President and Chief Operating Officer, Chum Kwan Lock, our Chief of Staff, and Sun Min Qi, our Chief Financial Officer, have substantial business experience and have successfully contributed to the execution of our operating strategies.

Unique MICE and entertainment facilities

Our market-leading MICE and entertainment facilities contribute to Macao’s diversification and appeal to business and leisure travelers while diversifying our cash flows and increasing revenues and profit. Our 1.7 million square feet of MICE space is specifically designed to meet the needs of meeting planners and corporate events and trade show organizers from around the world. Our experience and expertise in this industry continues to drive leisure and business tourism to Macao. Since opening in 2007, our 15,000-seat Cotai Arena has established itself as one of the top live entertainment venues in Southern China. The theaters at The Venetian Macao, Sands Cotai Central and The Parisian Macao offer a variety of ticketed events. The live entertainment program at our properties is a key traffic driver and has established us as the leader in the field of tourism and leisure activities.

Significant benefits from our on-going relationship with LVS

Sands China is approximately 70.0% owned by Las Vegas Sands, the world’s leading developer and operator of MICE-based integrated resorts. The operating experience of Las Vegas Sands in developing and operating MICE-based integrated resorts in the Las Vegas, Singapore and Macao markets is a significant benefit to us.

Business Strategies

Building on our key strengths, we seek to enhance our position as the leading developer and operator of integrated resorts and casinos in Macao by continuing to implement the following business strategies:

Developing and diversifying our integrated resort offerings on Cotai to include a full complement of products and services to cater to different market segments. Our development on Cotai includes four integrated resorts, MICE space, additional retail, dining and entertainment facilities and a range of hotel offerings to cater to different segments of the market. In addition to The Venetian Macao and The Parisian Macao hotel rooms, we have Four Seasons, Conrad, Holiday Inn, Sheraton and St. Regis branded suites and hotel rooms. We are able to leverage the recognition and the sales, marketing and reservation capabilities of these premier hotel brands to attract a wide range of customers in different market segments to our properties. We believe our partnerships with renowned hotel management partners, our diverse integrated resort offerings and the convenience and accessibility of our properties will continue to increase the appeal of our properties to both the business and leisure customer segments.

Leveraging our scale of operations to create and maintain an absolute cost advantage. Management expects to benefit from lower unit costs due to the economies of scale inherent in our operations. Opportunities for lower unit costs include, but are not limited to, lower utility costs; more efficient staffing of hotel and gaming operations; and centralized laundry, transportation, marketing and sales, and procurement. In addition, our scale allows us to consolidate certain back office functions.

Focusing on the high-margin mass market gaming segment, while continuing to provide luxury amenities and high service levels to our VIP and premium players. Our properties cater not only to VIP and premium players, but also to mass market customers, which comprise our most profitable gaming segment. We believe the mass market segment will continue to be a long-term growing segment as a result of the introduction of more high-quality gaming facilities and non-gaming amenities into the market. Our management estimates our mass market table revenues typically generate a gross margin that is approximately four times higher than the gross margin on our typical VIP table revenues.

Identifying targeted investment opportunities to drive growth across our portfolio. We will continue to invest in the expansion of our facilities and the enhancement of the leisure and business tourism appeal of our Cotai property portfolio.

Industry

According to Macao Government statistics issued publicly on a monthly basis by DICJ, annual gaming revenues were US$37.7 billion in 2018, a 13.4% increase compared to 2017. Macao gross gaming revenues had experienced year-over-year growth beginning in August 2016, and Macao continues to be the largest gaming market in the world and the only market in China to offer legalized casino gaming.

In 2018, Macao welcomed 36 million visitors, according to Macao Government Statistics Bureau disclosure. We expect Macao will continue to experience meaningful long-term growth and this growth will be driven by a variety of factors, including the movement of Chinese citizens to urban centers in China, continued growth of the Chinese outbound tourism market, the increased utilization of existing transportation infrastructure, the introduction of new transportation infrastructure and the continued increase in hotel room inventory in Macao and neighboring Hengqin Island. There has been significant investment announced and recently completed by concessionaires and subconcessionaires in new resort development projects on Cotai. These new resorts should help increase the critical mass on Cotai and further drive Macao’s transformation into a leading leisure and business tourism destination in Asia.