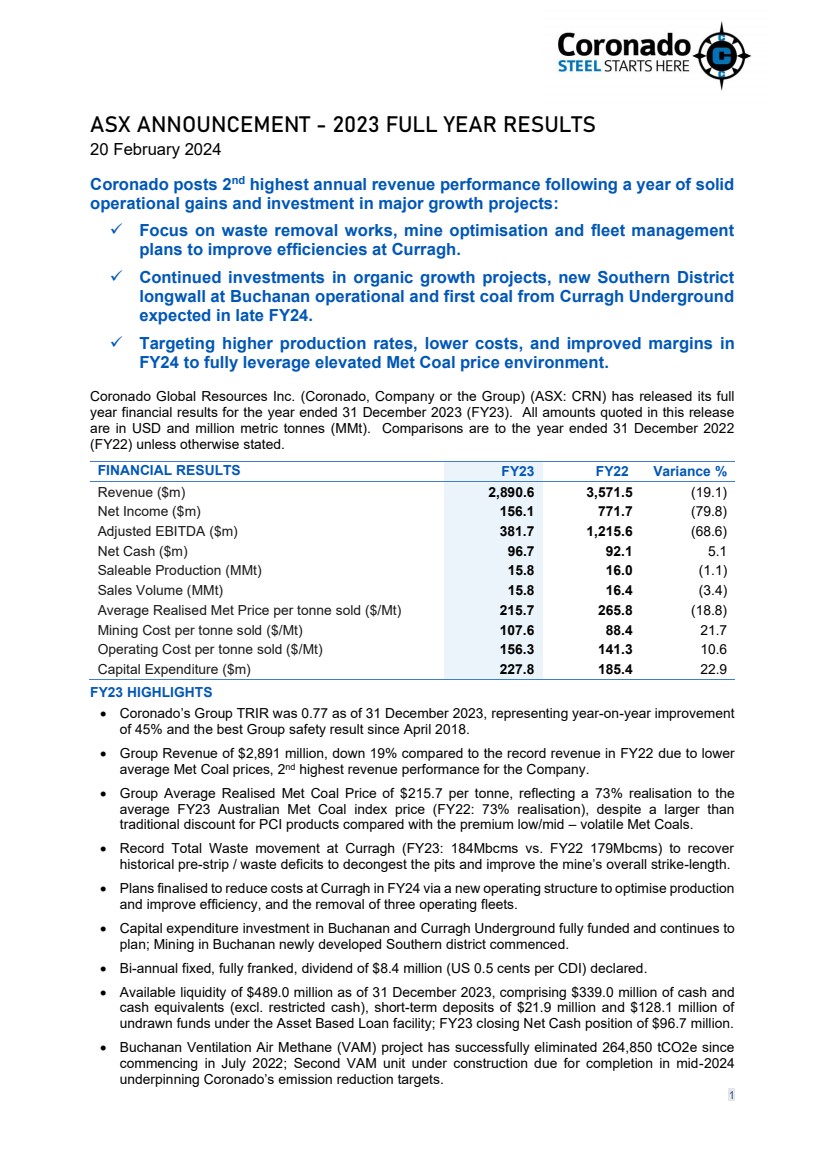

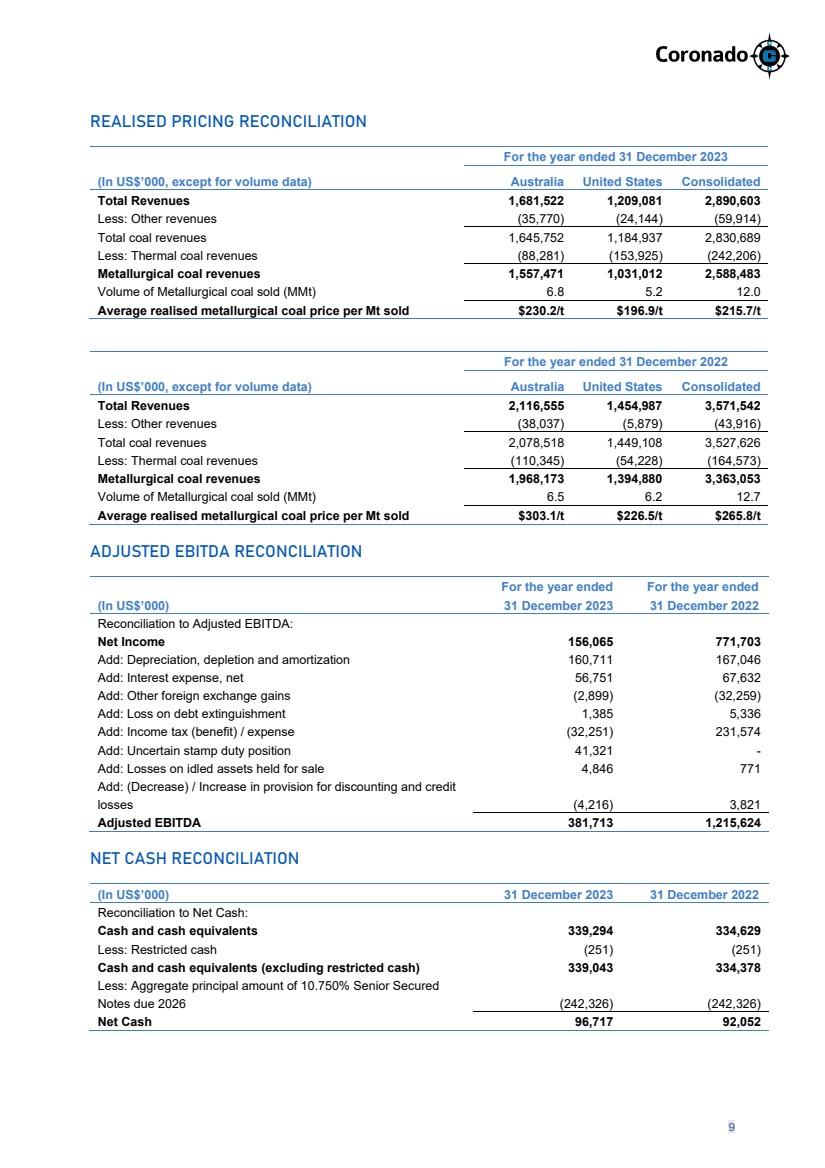

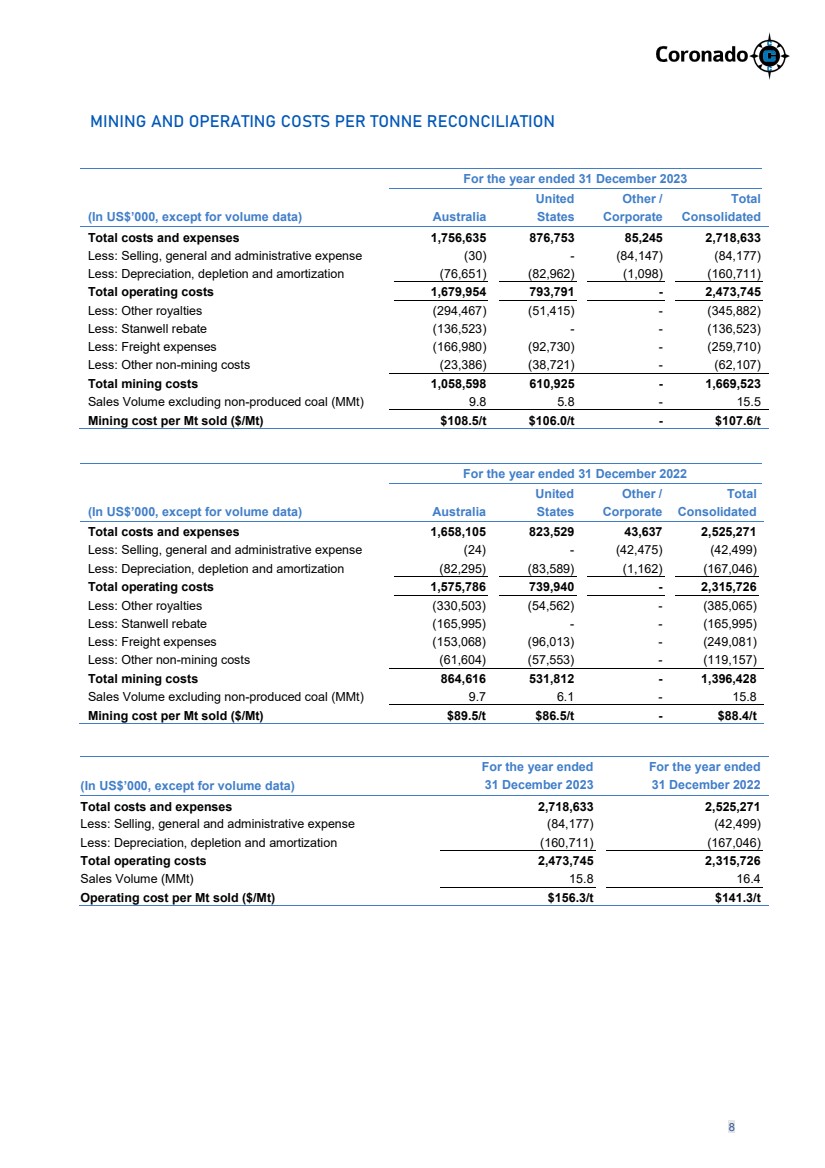

| 8 MINING AND OPERATING COSTS PER TONNE RECONCILIATION For the year ended 31 December 2023 (In US$’000, except for volume data) Australia United States Other / Corporate Total Consolidated Total costs and expenses 1,756,635 876,753 85,245 2,718,633 Less: Selling, general and administrative expense (30) - (84,147) (84,177) Less: Depreciation, depletion and amortization (76,651) (82,962) (1,098) (160,711) Total operating costs 1,679,954 793,791 - 2,473,745 Less: Other royalties (294,467) (51,415) - (345,882) Less: Stanwell rebate (136,523) - - (136,523) Less: Freight expenses (166,980) (92,730) - (259,710) Less: Other non-mining costs (23,386) (38,721) - (62,107) Total mining costs 1,058,598 610,925 - 1,669,523 Sales Volume excluding non-produced coal (MMt) 9.8 5.8 - 15.5 Mining cost per Mt sold ($/Mt) $108.5/t $106.0/t - $107.6/t For the year ended 31 December 2022 (In US$’000, except for volume data) Australia United States Other / Corporate Total Consolidated Total costs and expenses 1,658,105 823,529 43,637 2,525,271 Less: Selling, general and administrative expense (24) - (42,475) (42,499) Less: Depreciation, depletion and amortization (82,295) (83,589) (1,162) (167,046) Total operating costs 1,575,786 739,940 - 2,315,726 Less: Other royalties (330,503) (54,562) - (385,065) Less: Stanwell rebate (165,995) - - (165,995) Less: Freight expenses (153,068) (96,013) - (249,081) Less: Other non-mining costs (61,604) (57,553) - (119,157) Total mining costs 864,616 531,812 - 1,396,428 Sales Volume excluding non-produced coal (MMt) 9.7 6.1 - 15.8 Mining cost per Mt sold ($/Mt) $89.5/t $86.5/t - $88.4/t (In US$’000, except for volume data) For the year ended 31 December 2023 For the year ended 31 December 2022 Total costs and expenses 2,718,633 2,525,271 Less: Selling, general and administrative expense (84,177) (42,499) Less: Depreciation, depletion and amortization (160,711) (167,046) Total operating costs 2,473,745 2,315,726 Sales Volume (MMt) 15.8 16.4 Operating cost per Mt sold ($/Mt) $156.3/t $141.3/t |