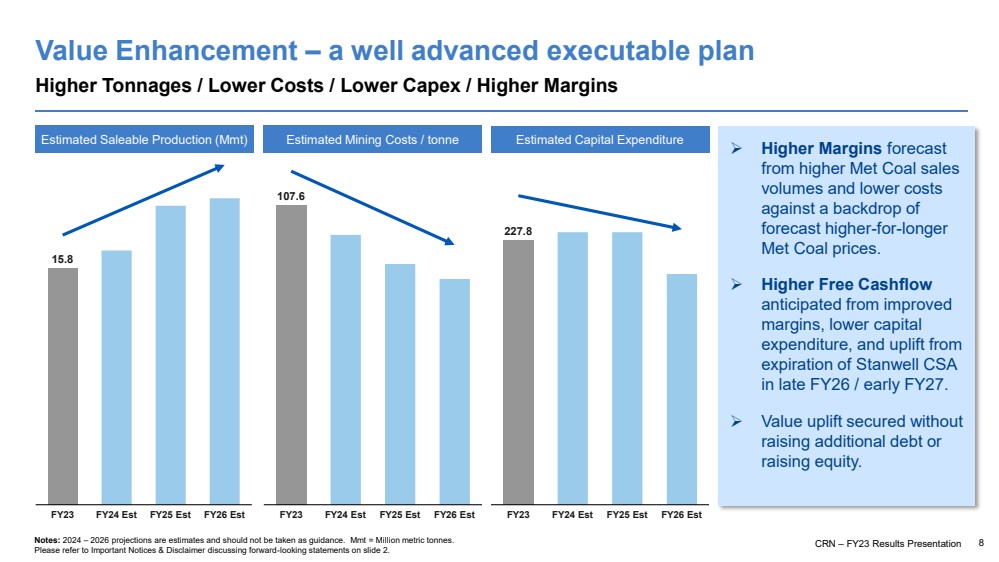

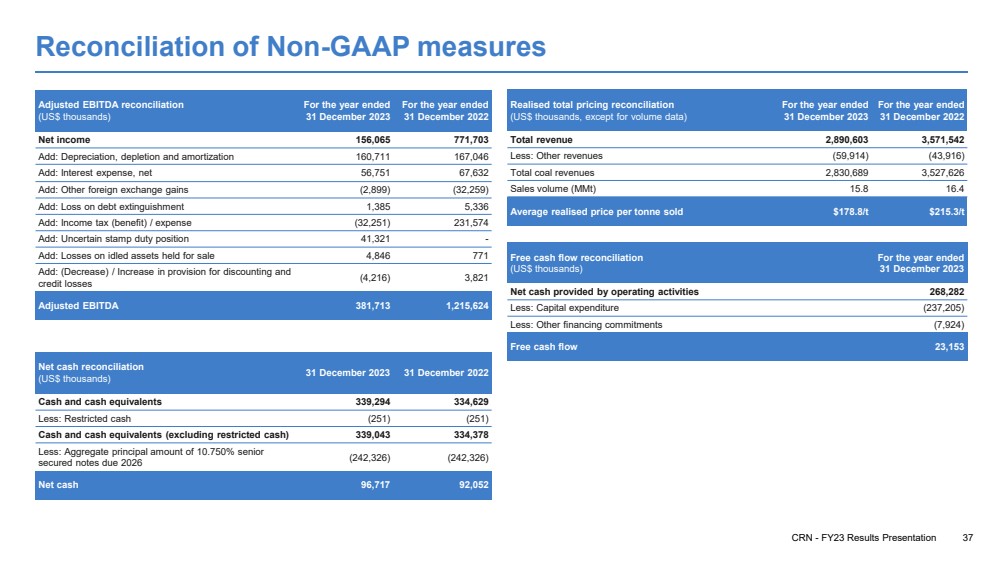

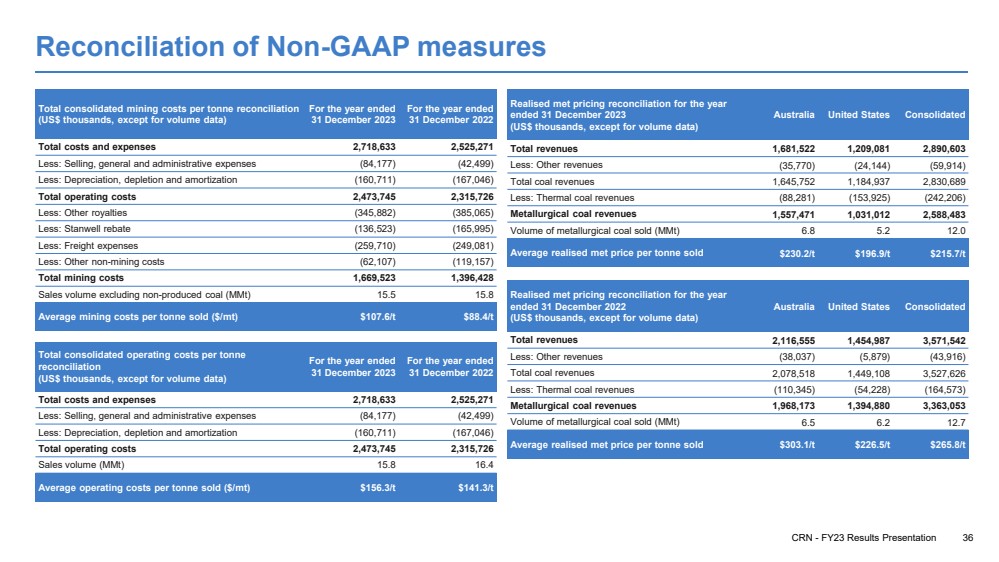

| CRN - FY23 Results Presentation 36 Reconciliation of Non-GAAP measures Total consolidated mining costs per tonne reconciliation (US$ thousands, except for volume data) For the year ended 31 December 2023 For the year ended 31 December 2022 Total costs and expenses 2,718,633 2,525,271 Less: Selling, general and administrative expenses (84,177) (42,499) Less: Depreciation, depletion and amortization (160,711) (167,046) Total operating costs 2,473,745 2,315,726 Less: Other royalties (345,882) (385,065) Less: Stanwell rebate (136,523) (165,995) Less: Freight expenses (259,710) (249,081) Less: Other non-mining costs (62,107) (119,157) Total mining costs 1,669,523 1,396,428 Sales volume excluding non-produced coal (MMt) 15.5 15.8 Average mining costs per tonne sold ($/mt) $107.6/t $88.4/t Realised met pricing reconciliation for the year ended 31 December 2023 (US$ thousands, except for volume data) Australia United States Consolidated Total revenues 1,681,522 1,209,081 2,890,603 Less: Other revenues (35,770) (24,144) (59,914) Total coal revenues 1,645,752 1,184,937 2,830,689 Less: Thermal coal revenues (88,281) (153,925) (242,206) Metallurgical coal revenues 1,557,471 1,031,012 2,588,483 Volume of metallurgical coal sold (MMt) 6.8 5.2 12.0 Average realised met price per tonne sold $230.2/t $196.9/t $215.7/t Total consolidated operating costs per tonne reconciliation (US$ thousands, except for volume data) For the year ended 31 December 2023 For the year ended 31 December 2022 Total costs and expenses 2,718,633 2,525,271 Less: Selling, general and administrative expenses (84,177) (42,499) Less: Depreciation, depletion and amortization (160,711) (167,046) Total operating costs 2,473,745 2,315,726 Sales volume (MMt) 15.8 16.4 Average operating costs per tonne sold ($/mt) $156.3/t $141.3/t Realised met pricing reconciliation for the year ended 31 December 2022 (US$ thousands, except for volume data) Australia United States Consolidated Total revenues 2,116,555 1,454,987 3,571,542 Less: Other revenues (38,037) (5,879) (43,916) Total coal revenues 2,078,518 1,449,108 3,527,626 Less: Thermal coal revenues (110,345) (54,228) (164,573) Metallurgical coal revenues 1,968,173 1,394,880 3,363,053 Volume of metallurgical coal sold (MMt) 6.5 6.2 12.7 Average realised met price per tonne sold $303.1/t $226.5/t $265.8/t |