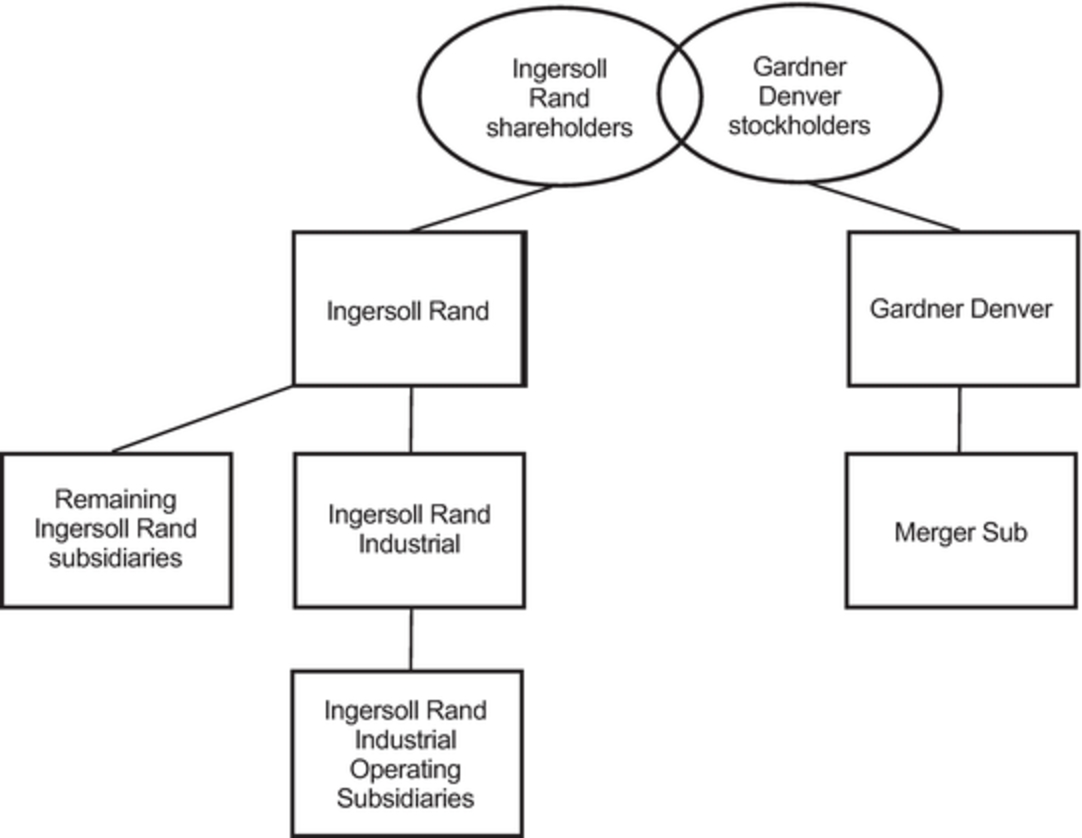

Background of the Merger

As part of their ongoing consideration and evaluation of Gardner Denver’s long-term prospects and strategies, the Gardner Denver board of directors and management regularly review the performance, strategy, competitive position, opportunities and prospects of Gardner Denver in light of the then-current business and economic environments. The Gardner Denver board of directors and management also monitor developments in the industrials sector and the industries Gardner Denver supplies, as well as the opportunities and challenges facing participants in those industries. Since Gardner Denver completed its initial public offering in May 2017, these reviews have involved, among other things, assessing potential strategic alternatives aimed at maximizing Gardner Denver stockholder value. The range of potential strategic alternatives that have been considered include, but are not limited to, business combinations, divestitures of non-core businesses, and other strategic transactions, as well as the potential to remain an independent, stand-alone company.

From time to time, in connection with these reviews, Vicente Reynal, the chief executive officer of Gardner Denver, and Peter Stavros, the chairman of the Gardner Denver board of directors, have had discussions with directors and chief executive officers of various industry participants and with various financial advisors regarding industry developments and various potential strategic and commercial opportunities involving Gardner Denver. During this time period, Mr. Stavros and Michael Lamach, the Chief Executive Officer of Ingersoll Rand, corresponded and had numerous discussions about a number of potential transactions and different structures, including discussions about Gardner Denver purchasing businesses within Ingersoll Rand’s Industrials segment; however, these discussions did not result in any agreements or transactions.

During the course of these periodic discussions, in the summer of 2018 Mr. Lamach suggested that he and Mr. Reynal meet in person. Over the course of the next few months, Messrs. Lamach and Reynal corresponded regarding the best time and place to meet. Ultimately, they decided to meet for dinner on December 13, 2018, at which time Mr. Lamach first broached the possibility of some type of business combination between Ingersoll Rand and Gardner Denver. Messrs. Lamach and Reynal agreed to schedule a meeting in January 2019 for the two companies to learn more about each other. Following the dinner, Mr. Reynal discussed with Mr. Stavros the details of the conversation and the plan for a subsequent meeting.

On December 21, 2018, Gardner Denver and Ingersoll Rand entered into a mutual confidentiality agreement with respect to a potential business combination. Thereafter, representatives of Ingersoll Rand and Gardner Denver set up a meeting to discuss further a potential business combination for late January 2019.

In early January, Neil Snyder, chief financial officer of Gardner Denver, and Mark Majocha, vice president, corporate development, of Ingersoll Rand, discussed plans for the meeting and an agenda. Prior to the meeting, Mr. Majocha sent Mr. Snyder an initial assessment prepared by Ingersoll Rand with respect to the potential synergies from a potential business combination and an agenda to review in advance of the meeting, both of which were shared with certain other members of Gardner Denver management and Mr. Stavros and Josh Weisenbeck, a member of the Gardner Denver board of directors. Mr. Snyder and Mr. Majocha continued to share thoughts on the materials for the meeting during this period.

Also, in mid-January, Mr. Stavros communicated with Mr. Lamach about beginning discussions regarding a potential transaction and also discussed with Mr. Lamach retaining financial advisors, confirming which firms each company intended to hire.

Shortly following this communication, Gardner Denver requested the assistance of Citigroup Global Markets Inc. (“Citi”), which had served as a lead underwriter in Gardner Denver’s initial public offering and recent secondary offerings and as a lender in various financing transactions for Gardner Denver, and thereafter Citi assisted members of Gardner Denver management in preparing for the meeting with Ingersoll Rand.

In late January, Ingersoll Rand was being advised by Goldman Sachs & Co. LLC (“Goldman Sachs”) and Lazard Frères & Co. LLC (“Lazard”) as financial advisors with respect to the proposed transaction.

On January 31, 2019, members of Gardner Denver management, including Messrs. Reynal and Snyder, met in person in St. Louis with members of Ingersoll Rand management, including Mr. Lamach, Sue Carter, chief financial officer of Ingersoll Rand, and Dave Regnery, executive vice president of Ingersoll Rand to discuss a potential business combination involving Gardner Denver and Ingersoll Rand. At the meeting, the parties