UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-23494

T. Rowe Price Exchange-Traded Funds, Inc.

(Exact name of registrant as specified in charter)

100 East Pratt Street, Baltimore, MD 21202

(Address of principal executive offices)

David Oestreicher

100 East Pratt Street, Baltimore, MD 21202

(Name and address of agent for service)

Registrant’s telephone number, including area code: (410) 345-2000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2023

Item 1. Reports to Shareholders

(a) Report pursuant to Rule 30e-1

ANNUAL REPORT

December 31, 2023

| | T. ROWE PRICE |

| TVAL | Value ETF |

| | For more insights from T. Rowe Price investment professionals, go to troweprice.com. |

HIGHLIGHTS

| ■ | U.S. stocks rose in the second half of 2023 as a resilient economy and signs of cooling inflation raised hopes that the Federal Reserve was nearing an end to its tightening cycle. |

| ■ | The Value Exchange-Traded Fund outperformed its benchmark, the Russell 1000 Value Index, on a net asset value basis and on a market price basis from its inception on June 14, 2023, until December 31, 2023. |

| ■ | The fund seeks to invest in quality companies that appear to be undervalued by various measures and temporarily out of favor but have good potential for capital appreciation. Health care was the largest overweight sector at year-end, while real estate represented the most underweight sector. |

| ■ | Given the concentration of the market’s leadership and growth stocks’ significant outperformance over value in 2023, we believe that valuation will be a more important component of market returns. |

Go Paperless

Going paperless offers a host of benefits, which include:

| ■ | Timely delivery of important documents |

| ■ | Convenient access to your documents anytime, anywhere |

| ■ | Strong security protocols to safeguard sensitive data |

If you invest through a financial intermediary such as an investment advisor, a bank, or a brokerage firm, please contact that organization and ask if it can provide electronic documentation.

T. ROWE PRICE VALUE ETF

Market Commentary

Dear Shareholder

Global stock and bond indexes were broadly positive during 2023 as most economies managed to avoid the recession that was widely predicted at the start of the year. Technology companies benefited from investor enthusiasm for artificial intelligence developments and led the equity rally, while fixed income benchmarks rebounded late in the year amid falling interest rates.

For the 12-month period, the technology-oriented Nasdaq Composite Index rose about 43%, reaching a record high and producing the strongest result of the major benchmarks. Growth stocks outperformed value shares, and developed market stocks generally outpaced their emerging markets counterparts. Currency movements were mixed over the period, although a weaker dollar versus major European currencies was beneficial for U.S. investors in European securities.

Within the S& P 500 Index, which finished the year just short of the record level it reached in early 2022, the information technology, communication services, and consumer discretionary sectors were all lifted by the tech rally and recorded significant gains. A small group of tech-oriented mega-cap companies helped drive much of the market’s advance. Conversely, the defensive utilities sector had the weakest returns in the growth-focused environment, and the energy sector also lost ground amid declining oil prices. The financials sector bounced back from the failure of three large regional banks in the spring and was one of the top-performing segments in the second half of the year.

The U.S. economy was the strongest among the major markets during the period, with gross domestic product growth coming in at 4.9% in the third quarter, the highest since the end of 2021. Corporate fundamentals were also broadly supportive. Year-over-year earnings growth contracted in the first and second quarters of 2023, but results were better than expected, and earnings growth turned positive again in the third quarter. Markets remained resilient despite a debt ceiling standoff in the U.S., the outbreak of war in the Middle East, the continuing conflict between Russia and Ukraine, and a sluggish economic recovery in China.

Inflation remained a concern, but investors were encouraged by the slowing pace of price increases as well as the possibility that the Federal Reserve was nearing the end of its rate-hiking cycle. The Fed held rates steady after raising its short-term lending benchmark rate to a target range of 5.25% to 5.50% in July,

the highest level since March 2001, and at its final meeting of the year in December, the central bank indicated that there could be three 25-basis-point rate cuts in 2024.

The yield of the benchmark 10-year U.S. Treasury note briefly reached 5.00% in October for the first time since late 2007 before falling back to 3.88% by period-end, the same level where it started the year, amid cooler-than-expected inflation readings and less-hawkish Fed rhetoric. Fixed income benchmarks were lifted late in the year by falling yields. Investment-grade and high yield corporate bonds produced solid returns, supported by the higher coupons that have become available over the past year, as well as increasing hopes that the economy might be able to avoid a recession.

Global economies and markets showed surprising resilience in 2023, but considerable uncertainty remains as we look ahead. Geopolitical events, the path of monetary policy, and the impact of the Fed’s rate hikes on the economy all raise the potential for additional volatility. We believe this environment makes skilled active management a critical tool for identifying risks and opportunities, and our investment teams will continue to use fundamental research to help identify securities that can add value to your portfolio over the long term.

Thank you for your continued confidence in T. Rowe Price.

Sincerely,

Robert Sharps

CEO and President

T. ROWE PRICE VALUE ETF

Management’s Discussion of Fund Performance

INVESTMENT OBJECTIVE

The fund seeks to provide long-term capital growth.

FUND COMMENTARY

How did the fund perform over the reporting period?

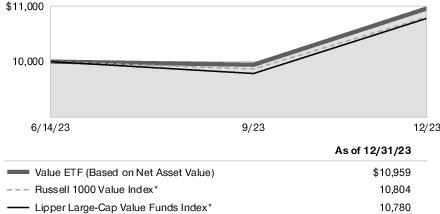

The Value Exchange-Traded Fund (ETF) returned 9.59% (based on net asset value) and 9.59% (at market price) from its inception on June 14, 2023, until December 31, 2023. The fund outperformed the Russell 1000 Value Index, which returned 8.04%, on a net asset value and a market price basis. It performed roughly in line with its Lipper peer group. (Past performance cannot guarantee future results.)

What factors influenced the fund’s performance?

Health care contributed the most to relative performance owing to strong stock selection in the sector. Eli Lilly led contributors amid investor excitement about the blockbuster potential of its diabetes drug Mounjaro, which received

PERFORMANCE COMPARISON

| | Total Return |

| Periods Ended 12/31/23 | 6 Months | Since

Inception

6/14/23 |

| Value ETF (Based on Net Asset Value) | 7.61% | 9.59% |

| Value ETF (At Market Price)* | 7.53 | 9.59 |

| Russell 1000 Value Index | 6.03 | 8.04 |

| Lipper Large-Cap Value Funds Index | 7.80 | 9.68 |

*Market returns are based on the midpoint of the bid/ask spread at market close (typically, 4 p.m. ET) and do not represent returns an investor would have received if shares were traded at other times.

regulatory approval for treating obesity and helped push the drugmaker’s shares to a record high in November. McKesson, the leading U.S. drug distributor, also helped relative returns after it reported better-than-expected quarterly earnings and raised its full-year earnings guidance in August, driven by higher revenue from distributing GLP-1 drugs. The financials sector added value due to positive stock selection. Regional lenders Fifth Third Bancorp and U.S. Bancorp helped relative performance as both significantly outperformed the financials sector based on strong earnings and an improving economic backdrop. (Please refer to the portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

Turning to detractors, energy weighed the most on relative returns due to our overweight allocation to the sector, which lagged the benchmark. Stock selection in energy, however, was broadly neutral as we benefited from strong performance in French oil and gas major TotalEnergies, one of the fund’s largest holdings. Consumer staples detracted from relative performance owing to a large overweight to the sector, which recorded a negative return over the period as investors favored higher-growth names in the second half of 2023. The industrials and business services sector also weighed on relative returns due to adverse stock selection. Siemens, a diversified German industrial group and a core holding, detracted from performance due to weakness in its digital industries business, particularly in China automation. However, Siemens’ shares performed well toward year-end after the company reported strong fourth-quarter results.

How is the fund positioned?

The T. Rowe Price Value ETF invests in mostly large-cap U.S. companies that appear to be undervalued by various measures but have strong prospects for capital appreciation. The portfolio management team relies on an active investment approach emphasizing bottom-up stock selection based on the fundamental research into each holding performed by T. Rowe Price’s equity analysts. The team uses various measures to identify potential investments, including price/earnings ratio, price/book value ratio, dividend yield, undervalued assets, and restructuring opportunities. Companies that are temporarily out of favor; have durable businesses or assets that are currently underappreciated; and trade at a discount versus their history, industry, or overall market are a key focus for the fund.

Sector allocations are driven by bottom-up stock selection. At the end of December, health care was the second-largest sector in absolute terms and the largest overweight sector relative to the benchmark. Our exposure was concentrated in the health care providers and services industry due to our core

holding in Elevance Health, the health insurer formerly known as Anthem. Elevance Health sells Anthem Blue Cross and Blue Shield coverage in 14 U.S. states, which affords it advantages of scale and market share. The company also has a promising earnings growth driver in its health care services unit Carelon, which offers pharmacy benefits management, data analytics, and a range of other services. In the pharmaceuticals industry, we held relatively large positions in Eli Lilly and Elanco Animal Health, which develops and markets medicines and services for pets and farm animals. We also maintained exposure to the health care equipment and supplies industry through owning medical technology company Becton Dickinson, which has a diversified and defensive portfolio of businesses that should allow it to outperform even in a rocky economy.

SECTOR DIVERSIFICATION

| | Percent of

Net Assets |

| | 6/30/23 | 12/31/23 |

| Financials | 18.6% | 20.6% |

| Health Care | 18.2 | 16.4 |

| Industrials and Business Services | 12.3 | 13.6 |

| Information Technology | 8.1 | 10.2 |

| Consumer Staples | 9.8 | 9.1 |

| Energy | 8.6 | 8.8 |

| Communication Services | 5.5 | 4.8 |

| Utilities | 5.8 | 4.6 |

| Consumer Discretionary | 4.6 | 4.2 |

| Materials | 3.9 | 3.7 |

| Real Estate | 4.1 | 3.7 |

| Other and Reserves | 0.5 | 0.3 |

| Total | 100.0% | 100.0% |

Historical weightings reflect current industry/sector classifications.

Consumer staples was the second-largest overweight sector against the benchmark at period-end. Our largest position in the sector was Wal-Mart. In addition to having a defensive business and a reasonable valuation, we believe that Wal-Mart’s focus on its third-party marketplace will increasingly drive e-commerce sales and other revenue streams that can create value, such as online advertising, financial services, and third-party fulfillment. Philip Morris International, the world’s leading tobacco company, was another key staples holding. The maker of Marlboro cigarettes has led an industry shift from combustibles toward smoke-free products, such as heated tobacco and nicotine pouches, a strategic move that we believe will pay off in volume growth and improved margins. Moreover, the company’s IQOS heated tobacco product has a significant market share lead and technological edge over competing products thanks to the company’s early investment in developing tobacco alternatives.

Financials accounted for the fund’s largest sector in absolute terms but a modest underweight versus the benchmark at year-end. Banks represented our largest absolute financial industry exposure, anchored by core positions in money center banks Wells Fargo and Bank of America, as well as a sizable position in Ohio-based regional lender Fifth Third Bancorp. We also remained positive on insurance companies, our largest relative industry position within financials. Chubb, Hartford Financial Services, and American International Group were significant holdings based on our view that each company offered a strong mix of attractive valuation and earnings growth potential.

Real estate was the largest underweight and the second-smallest sector in absolute terms after materials as we found better opportunities in other sectors. Nevertheless, we maintained exposure to the sector through a sizable position in AvalonBay Communities, a real estate investment trust that owns apartment buildings in affluent suburban locations on the East and West coasts where houses are expensive and in limited supply. We regard AvalonBay’s development platform as the best in the business and think that its earnings growth will outpace its peers in the coming years, supported by the attractive location of its apartment buildings and the company’s strong management team and balance sheet.

What is portfolio management’s outlook?

U.S. stocks produced strong returns in 2023, with high-beta names receiving a strong bid in the fourth quarter. Given the concentration of the market’s leadership and growth stocks’ significant outperformance over value, we believe that valuation will be a more important component of market returns in 2024.

The past year’s rally in higher-beta stocks has left behind more defensive holdings, presenting an opportunity to lean into those names, which we believe will help support longer-term performance.

As always, we are focused on finding high-quality companies with solid fundamentals and attractive valuations. Bottom-up stock selection based on rigorous company research continues to be the cornerstone of our investment philosophy and process. We are confident that our disciplined, fundamentals-based approach to value investing, combined with the substantial resources of T. Rowe Price’s equity research platform, will allow us to navigate a highly uncertain macro environment and add value for our shareholders.

The views expressed reflect the opinions of T. Rowe Price as of the date of this report and are subject to change based on changes in market, economic, or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

PRINCIPAL RISKS

Value investing. The fund’s value approach to investing could cause it to underperform other stock funds that employ a different investment style. The intrinsic value of a stock with value characteristics may not be fully recognized by the market for a long time (or at all) or a stock judged to be undervalued may actually be appropriately priced at a low level. Value stocks may fail to appreciate for long periods and may never reach what the adviser believes are their full market values.

Market conditions. The value of the fund’s investments may decrease, sometimes rapidly or unexpectedly, due to factors affecting an issuer held by the fund, particular industries, or the overall securities markets. A variety of factors can increase the volatility of the fund’s holdings and markets generally, including political or regulatory developments, recessions, inflation, rapid interest rate changes, war, military conflict, or acts of terrorism, natural disasters, and outbreaks of infectious illnesses or other widespread public health issues such as the coronavirus pandemic and related governmental and public responses (including sanctions). Certain events may cause instability across global markets, including reduced liquidity and disruptions in trading markets, while some events may affect certain geographic regions, countries, sectors, and industries more significantly than others. Government intervention in markets may impact interest rates, market volatility, and security pricing. These adverse developments may cause broad declines in market value due to short-term market movements or for significantly longer periods during more prolonged market downturns.

BENCHMARK INFORMATION

Note: London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2024. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication.

Note: Portions of the mutual fund information contained in this report was supplied by Lipper, a Refinitiv Company, subject to the following: Copyright 2024 © Refinitiv. All rights reserved. Any copying, republication or redistribution of Lipper content is expressly prohibited without the prior written consent of Lipper. Lipper shall not be liable for any errors or delays in the content, or for any actions taken in reliance thereon.

PORTFOLIO HIGHLIGHTS

TWENTY-FIVE LARGEST HOLDINGS

| | Percent of

Net Assets |

| | 12/31/23 |

| Wells Fargo | 2.4% |

| Bank of America | 2.3 |

| ExxonMobil | 2.0 |

| Southern Company | 2.0 |

| Elevance Health | 1.9 |

| Wal-Mart | 1.9 |

| Chubb | 1.8 |

| Qualcomm | 1.8 |

| TotalEnergies | 1.8 |

| Philip Morris International | 1.7 |

| AvalonBay Communities | 1.6 |

| Hartford Financial Services | 1.6 |

| Johnson & Johnson | 1.6 |

| Fiserv | 1.4 |

| American International Group | 1.3 |

| News Corp | 1.3 |

| ConocoPhillips | 1.2 |

| Eli Lilly and Co | 1.2 |

| Fifth Third Bancorp | 1.2 |

| L3Harris Technologies | 1.2 |

| Siemens | 1.2 |

| Western Digital | 1.2 |

| Intel | 1.1 |

| JPMorgan Chase | 1.1 |

| Merck | 1.1 |

| Total | 38.9% |

Note: The information shown does not reflect any exchange-traded funds (ETFs), cash reserves, or collateral for securities lending that may be held in the portfolio.

GROWTH OF $10,000

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which include a broad-based market index and may also include a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

Value ETF

Note: See the Average Annual Compound Total Return table.

*Since 6/30/23.

AVERAGE ANNUAL COMPOUND TOTAL RETURN

| Period Ended 12/31/23 | Since

Inception

6/14/23 |

| Value ETF (Based on Net Asset Value) | 9.59%* |

| Value ETF (At Market Price) | 9.59* |

The fund's performance information represents only past performance and is not necessarily an indication of future results. Current performance may be lower or higher than the performance data cited. Share price, principal value, and return will vary, and you may have a gain or loss when you sell your shares. For the most recent month-end performance, please visit our website (troweprice.com).

This table shows how the fund would have performed each year if its actual (or cumulative) returns for the periods shown had been earned at a constant rate. Average annual total return figures include changes in principal value, reinvested dividends, and capital gain distributions. Returns do not reflect taxes that the shareholder may pay on fund distributions or the redemption of fund shares. When assessing performance, investors should consider both short- and long-term returns. Past performance cannot guarantee future results. Market returns are based on the midpoint of the bid/ask spread at market close (typically, 4 p.m. ET) and do not represent returns an investor would have received if shares were traded at other times.

*Returns for periods of less than one year are not annualized.

PREMIUM/DISCOUNT INFORMATION

The frequency at which the daily market prices were at a discount or premium to the fund’s net asset value is available on the fund’s website (troweprice.com).

EXPENSE RATIO

The expense ratio shown is as of the fund’s most recent prospectus. This number may vary from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, includes acquired fund fees and expenses but does not include fee or expense waivers.

FUND EXPENSE EXAMPLE

As a shareholder, you may incur two types of costs: (1) transaction costs, such as brokerage commissions on purchases and sales, and (2) ongoing costs, including management fees and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Actual Expenses

The first line of the following table (Actual) provides information about actual account values and expenses based on the fund’s actual returns. You may use the information on this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number on the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (Hypothetical) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as brokerage commissions paid on purchases and sales of shares. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

Value ETF

| | Beginning

Account Value

7/1/23 | Ending

Account Value

12/31/23 | Expenses Paid

During Period*

7/1/23 to 12/31/23 |

| Actual | $1,000.00 | $1,076.10 | $1.73 |

| Hypothetical (assumes 5% return before expenses) | 1,000.00 | 1,023.54 | 1.68 |

| * | Expenses are equal to the fund’s annualized expense ratio for the 6-month period (0.33%), multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), and divided by the days in the year (365) to reflect the half-year period. |

For a share outstanding throughout the period

| | 6/14/23 (1)

Through |

| | 12/31/23 |

| NET ASSET VALUE | |

| Beginning of period | $ 25.00 |

| Investment activities | |

| Net investment income(2) (3) | 0.34 |

| Net realized and unrealized gain/loss | 2.05 |

| Total from investment activities | 2.39 |

| Distributions | |

| Net investment income | (0.17) |

| NET ASSET VALUE | |

| End of period | $ 27.22 |

| Ratios/Supplemental Data |

| Total return, based on NAV(3) (4) | 9.59% |

Ratios to average net

assets:(3) | |

Gross expenses before

waivers/payments by

Price Associates | 0.33% (5) |

Net expenses after

waivers/payments by

Price Associates | 0.33% (5) |

| Net investment income | 2.43% (5) |

| Portfolio turnover rate(6) | 8.8% |

Net assets, end of period

(in thousands) | $ 57,159 |

| (1) | Inception date |

| (2) | Per share amounts calculated using average shares outstanding method. |

| (3) | See Note 6 for details to expense-related arrangements with Price Associates. |

| (4) | Total return reflects the rate that an investor would have earned on an investment in the fund during the period, assuming reinvestment of all distributions. Total return is not annualized for periods less than one year. |

| (5) | Annualized |

| (6) | Portfolio turnover excludes securities received or delivered through in-kind share transactions. |

The accompanying notes are an integral part of these financial statements.

T. ROWE PRICE VALUE ETF

December 31, 2023

| PORTFOLIO OF INVESTMENTS‡ | Shares | $ Value |

| (Cost and value in $000s) | | |

| | | |

| COMMON STOCKS 99.7% |

| COMMUNICATION SERVICES 4.8% |

| Diversified Telecommunication Services 0.8% | | |

| Verizon Communications | 12,008 | 453 |

| | | 453 |

| Interactive Media & Services 1.7% | | |

| Alphabet, Class C (1) | 3,760 | 530 |

| Meta Platforms, Class A (1) | 1,219 | 431 |

| | | 961 |

| Media 1.3% | | |

| News, Class A | 29,932 | 735 |

| | | 735 |

| Wireless Telecommunication Services 1.0% | | |

| T-Mobile US | 3,752 | 602 |

| | | 602 |

| Total Communication Services | | 2,751 |

| CONSUMER DISCRETIONARY 4.2% |

| Hotels Restaurants & Leisure 2.3% | | |

| Las Vegas Sands | 4,543 | 224 |

| Marriott International, Class A | 1,209 | 273 |

| McDonald's | 1,163 | 345 |

| MGM Resorts International (1) | 3,467 | 155 |

| Starbucks | 1,211 | 116 |

| Yum! Brands | 1,738 | 227 |

| | | 1,340 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| Household Durables 0.5% | | |

| Lennar, Class A | 1,753 | 261 |

| | | 261 |

| Specialty Retail 1.4% | | |

| AutoZone (1) | 124 | 320 |

| Home Depot | 868 | 301 |

| TJX | 1,660 | 156 |

| | | 777 |

| Total Consumer Discretionary | | 2,378 |

| CONSUMER STAPLES 9.1% |

| Beverages 0.9% | | |

| Coca-Cola | 5,679 | 335 |

| Keurig Dr Pepper | 6,250 | 208 |

| | | 543 |

| Consumer Staples Distribution & Retail 1.9% | | |

| Walmart | 6,771 | 1,067 |

| | | 1,067 |

| Food Products 1.6% | | |

| Conagra Brands | 12,475 | 357 |

| Mondelez International, Class A | 5,615 | 407 |

| Tyson Foods, Class A | 3,136 | 169 |

| | | 933 |

| Household Products 2.2% | | |

| Colgate-Palmolive | 5,954 | 474 |

| Kimberly-Clark | 2,862 | 348 |

| Procter & Gamble | 2,980 | 437 |

| | | 1,259 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| Personal Care Products 0.8% | | |

| Kenvue | 20,645 | 445 |

| | | 445 |

| Tobacco 1.7% | | |

| Philip Morris International | 10,091 | 949 |

| | | 949 |

| Total Consumer Staples | | 5,196 |

| ENERGY 8.8% |

| Energy Equipment & Services 0.7% | | |

| Baker Hughes | 2,814 | 96 |

| Halliburton | 9,074 | 328 |

| | | 424 |

| Oil, Gas & Consumable Fuels 8.1% | | |

| Chevron | 3,065 | 457 |

| ConocoPhillips | 5,774 | 670 |

| EOG Resources | 4,465 | 540 |

| EQT | 7,253 | 280 |

| Exxon Mobil | 11,317 | 1,132 |

| Pioneer Natural Resources | 1,279 | 288 |

| TotalEnergies, ADR | 15,110 | 1,018 |

| Williams | 6,689 | 233 |

| | | 4,618 |

| Total Energy | | 5,042 |

| FINANCIALS 20.6% |

| Banks 8.7% | | |

| Bank of America | 38,376 | 1,292 |

| Fifth Third Bancorp | 19,407 | 669 |

| Huntington Bancshares | 33,686 | 429 |

| JPMorgan Chase | 3,811 | 648 |

| US Bancorp | 12,276 | 531 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| Wells Fargo | 28,167 | 1,387 |

| | | 4,956 |

| Capital Markets 3.0% | | |

| Ares Management | 1,465 | 174 |

| BlackRock | 254 | 206 |

| Cboe Global Markets | 954 | 170 |

| Charles Schwab | 7,289 | 501 |

| CME Group | 707 | 149 |

| Morgan Stanley | 3,598 | 336 |

| S&P Global | 338 | 149 |

| | | 1,685 |

| Consumer Finance 0.2% | | |

| Capital One Financial | 1,040 | 136 |

| | | 136 |

| Financial Services 3.2% | | |

| Apollo Global Management | 2,475 | 231 |

| Equitable Holdings | 15,822 | 527 |

| Fiserv (1) | 6,115 | 812 |

| FleetCor Technologies (1) | 889 | 251 |

| | | 1,821 |

| Insurance 5.5% | | |

| American International Group | 11,357 | 769 |

| Arthur J Gallagher | 461 | 104 |

| Chubb | 4,588 | 1,037 |

| Hartford Financial Services Group | 11,678 | 939 |

| Marsh & McLennan | 1,699 | 322 |

| | | 3,171 |

| Total Financials | | 11,769 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| HEALTH CARE 16.4% |

| Biotechnology 1.4% | | |

| AbbVie | 1,916 | 297 |

| Amgen | 451 | 130 |

| Regeneron Pharmaceuticals (1) | 268 | 235 |

| Vertex Pharmaceuticals (1) | 418 | 170 |

| | | 832 |

| Health Care Equipment & Supplies 2.6% | | |

| Baxter International | 5,430 | 210 |

| Becton Dickinson | 2,550 | 622 |

| Medtronic | 2,615 | 215 |

| Zimmer Biomet Holdings | 3,716 | 452 |

| | | 1,499 |

| Health Care Providers & Services 6.0% | | |

| Cigna | 1,851 | 554 |

| CVS Health | 2,603 | 206 |

| Elevance Health | 2,329 | 1,098 |

| HCA Healthcare | 747 | 202 |

| Humana | 307 | 141 |

| McKesson | 1,127 | 522 |

| Molina Healthcare (1) | 629 | 227 |

| UnitedHealth Group | 869 | 458 |

| | | 3,408 |

| Life Sciences Tools & Services 1.7% | | |

| Agilent Technologies | 1,489 | 207 |

| Danaher | 1,569 | 363 |

| Thermo Fisher Scientific | 746 | 396 |

| | | 966 |

| Pharmaceuticals 4.7% | | |

| Bristol-Myers Squibb | 1,623 | 83 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| Elanco Animal Health (1) | 15,160 | 226 |

| Eli Lilly | 1,131 | 659 |

| Johnson & Johnson | 6,010 | 942 |

| Merck | 5,925 | 646 |

| Zoetis | 627 | 124 |

| | | 2,680 |

| Total Health Care | | 9,385 |

| INDUSTRIALS & BUSINESS SERVICES 13.6% |

| Aerospace & Defense 3.3% | | |

| Boeing (1) | 2,366 | 617 |

| Howmet Aerospace | 4,497 | 243 |

| L3Harris Technologies | 3,331 | 701 |

| TransDigm Group | 326 | 330 |

| | | 1,891 |

| Air Freight & Logistics 0.4% | | |

| United Parcel Service, Class B | 1,379 | 217 |

| | | 217 |

| Building Products 0.4% | | |

| Trane Technologies | 953 | 232 |

| | | 232 |

| Commercial Services & Supplies 0.6% | | |

| Republic Services | 2,075 | 342 |

| | | 342 |

| Electrical Equipment 0.9% | | |

| AMETEX | 707 | 116 |

| Hubbell | 1,170 | 385 |

| | | 501 |

| Ground Transportation 1.8% | | |

| Canadian Pacific Kansas City | 4,059 | 321 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| CSX | 9,392 | 325 |

| Norfolk Southern | 989 | 234 |

| Union Pacific | 594 | 146 |

| | | 1,026 |

| Industrial Conglomerates 3.0% | | |

| General Electric | 4,270 | 545 |

| Honeywell International | 1,417 | 297 |

| Roper Technologies | 355 | 194 |

| Siemens, ADR | 7,465 | 698 |

| | | 1,734 |

| Machinery 2.8% | | |

| Caterpillar | 604 | 179 |

| Cummins | 2,108 | 505 |

| Deere | 246 | 98 |

| Otis Worldwide | 1,913 | 171 |

| Stanley Black & Decker | 6,326 | 621 |

| | | 1,574 |

| Passenger Airlines 0.1% | | |

| United Airlines Holdings (1) | 1,421 | 59 |

| | | 59 |

| Trading Companies & Distributors 0.3% | | |

| United Rentals | 334 | 192 |

| | | 192 |

| Total Industrials & Business Services | | 7,768 |

| INFORMATION TECHNOLOGY 10.2% |

| Communications Equipment 0.4% | | |

| Motorola Solutions | 785 | 246 |

| | | 246 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| Electronic Equipment, Instruments & Components 0.6% | | |

| CDW | 1,034 | 235 |

| TE Connectivity | 820 | 115 |

| | | 350 |

| IT Services 0.6% | | |

| Accenture, Class A | 916 | 322 |

| | | 322 |

| Semiconductors & Semiconductor Equipment 6.0% | | |

| Applied Materials | 1,959 | 317 |

| Entegris | 1,156 | 139 |

| Intel | 12,535 | 630 |

| Marvell Technology | 2,831 | 171 |

| Microchip Technology | 2,278 | 205 |

| Micron Technology | 3,291 | 281 |

| ON Semiconductor (1) | 2,184 | 182 |

| QUALCOMM | 7,103 | 1,027 |

| Taiwan Semiconductor Manufacturing, ADR | 1,914 | 199 |

| Texas Instruments | 1,581 | 270 |

| | | 3,421 |

| Software 0.7% | | |

| Microsoft | 1,005 | 378 |

| | | 378 |

| Technology Hardware, Storage & Peripherals 1.9% | | |

| Samsung Electronics, GDR | 270 | 403 |

| Western Digital (1) | 13,075 | 685 |

| | | 1,088 |

| Total Information Technology | | 5,805 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| MATERIALS 3.7% |

| Chemicals 2.6% | | |

| CF Industries Holdings | 7,123 | 566 |

| Linde | 1,166 | 479 |

| RPM International | 3,943 | 440 |

| | | 1,485 |

| Containers & Packaging 0.9% | | |

| Avery Dennison | 989 | 200 |

| International Paper | 9,063 | 328 |

| | | 528 |

| Metals & Mining 0.2% | | |

| BHP Group, ADR | 1,632 | 111 |

| | | 111 |

| Total Materials | | 2,124 |

| REAL ESTATE 3.7% |

| Industrial REITs 0.4% | | |

| Prologis, REIT | 1,780 | 237 |

| | | 237 |

| Residential REITs 1.6% | | |

| AvalonBay Communities, REIT | 4,818 | 902 |

| | | 902 |

| Specialized REITs 1.7% | | |

| Equinix, REIT | 122 | 98 |

| Lamar Advertising, Class A, REIT | 1,484 | 158 |

| Public Storage, REIT | 583 | 178 |

| Weyerhaeuser, REIT | 16,297 | 567 |

| | | 1,001 |

| Total Real Estate | | 2,140 |

| | Shares | $ Value |

| (Cost and value in $000s) | | |

| UTILITIES 4.6% |

| Electric Utilities 2.3% | | |

| Entergy | 1,125 | 114 |

| NextEra Energy | 556 | 34 |

| Southern | 16,309 | 1,143 |

| | | 1,291 |

| Independent Power & Renewable Electricity Producer 0.3% | | |

| Vistra | 3,985 | 154 |

| | | 154 |

| Multi-Utilities 2.0% | | |

| Ameren | 4,090 | 296 |

| Dominion Energy | 6,997 | 329 |

| DTE Energy | 1,780 | 196 |

| Sempra | 4,647 | 347 |

| | | 1,168 |

| Total Utilities | | 2,613 |

| Total Common Stocks (Cost $50,975) | | 56,971 |

| SHORT-TERM INVESTMENTS 0.2% |

| Money Market Funds 0.2% | | |

| State Street Institutional U.S. Government Money Market Fund, 5.32% (2) | 109,666 | 110 |

| Total Short-Term Investments (Cost $110) | | 110 |

Total Investments in Securities

99.9% of Net Assets (Cost $51,085) | | $57,081 |

| | |

| ‡ | Shares are denominated in U.S. dollars unless otherwise noted. |

| (1) | Non-income producing. |

| (2) | Seven-day yield |

| ADR | American Depositary Receipts |

| GDR | Global Depositary Receipts |

| REIT | A domestic Real Estate Investment Trust whose distributions pass-through with original tax character to the shareholder |

The accompanying notes are an integral part of these financial statements.

T. ROWE PRICE VALUE ETF

December 31, 2023

STATEMENT OF ASSETS AND LIABILITIES

($000s, except shares and per share amounts)

| Assets | |

| Investments in securities, at value (cost $51,085) | $ 57,081 |

| Dividends receivable | 94 |

| Total assets | 57,175 |

| Liabilities | |

| Investment management and administrative fees payable | 16 |

| Total liabilities | 16 |

| NET ASSETS | $ 57,159 |

| Net assets consists of: | |

| Total distributable earnings (loss) | $ 5,809 |

Paid-in capital applicable to 2,100,000 shares of $0.0001 par value

capital stock outstanding; 4,000,000,000 shares authorized | 51,350 |

| NET ASSETS | $57,159 |

| NET ASSET VALUE PER SHARE | $ 27.22 |

The accompanying notes are an integral part of these financial statements.

STATEMENT OF OPERATIONS

($000s)

| | 6/14/23

Through |

| | 12/31/23 |

| Investment Income (Loss) | |

| Dividend income (net of foreign taxes of $4) | $ 411 |

| Investment management and administrative expense | 49 |

| Net investment income | 362 |

| Realized and Unrealized Gain / Loss | |

| Net realized loss on securities | (187) |

| Change in net unrealized gain / loss on securities | 5,996 |

| Net realized and unrealized gain / loss | 5,809 |

| INCREASE IN NET ASSETS FROM OPERATIONS | $6,171 |

The accompanying notes are an integral part of these financial statements.

STATEMENT OF CHANGES IN NET ASSETS

($000s)

| | 6/14/23

Through |

| | 12/31/23 |

| Increase (Decrease) in Net Assets | |

| Operations | |

| Net investment income | $ 362 |

| Net realized loss | (187) |

| Change in net unrealized gain / loss | 5,996 |

| Increase in net assets from operations | 6,171 |

| Distributions to shareholders | |

| Net earnings | (367) |

| Capital share transactions* | |

| Shares sold | 51,355 |

| Increase in net assets from capital share transactions | 51,355 |

| Net Assets | |

| Increase during period | 57,159 |

| Beginning of period | - |

| End of period | $57,159 |

| *Share information | |

| Shares sold | 2,100 |

| Increase in shares outstanding | 2,100 |

The accompanying notes are an integral part of these financial statements.

NOTES TO FINANCIAL STATEMENTS

T. Rowe Price Exchange-Traded Funds, Inc. (the corporation) is registered under the Investment Company Act of 1940 (the 1940 Act). The Value ETF (the fund) is a diversified, open-end management investment company established by the corporation. The fund incepted on June 14, 2023. The fund seeks to provide long-term capital growth.

NOTE 1 – SIGNIFICANT ACCOUNTING POLICIES

Basis of Preparation

The fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 (ASC 946). The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (GAAP), including, but not limited to, ASC 946. GAAP requires the use of estimates made by management. Management believes that estimates and valuations are appropriate; however, actual results may differ from those estimates, and the valuations reflected in the accompanying financial statements may differ from the value ultimately realized upon sale or maturity.

Investment Transactions, Investment Income, and Distributions

Investment transactions are accounted for on the trade date basis. Income and expenses are recorded on the accrual basis. Realized gains and losses are reported on the identified cost basis. Income tax-related interest and penalties, if incurred, are recorded as income tax expense. Dividends received from other investment companies are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Distributions from REITs are initially recorded as dividend income and, to the extent such represent a return of capital or capital gain for tax purposes, are reclassified when such information becomes available. Non-cash dividends, if any, are recorded at the fair market value of the asset received. Proceeds from litigation payments, if any, are included in either net realized gain (loss) or change in net unrealized gain/loss from securities. Distributions to shareholders are recorded on the ex-dividend date. Income distributions, if any, are declared and paid annually. A capital gain distribution, if any, may also be declared and paid by the fund annually. Dividends and distributions cannot be automatically reinvested in additional shares of the fund.

Currency Translation

Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as provided by an outside pricing service. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the respective date of such transaction. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is not bifurcated from the portion attributable to changes in market prices.

Capital Transactions

The fund issues and redeems shares at its net asset value (NAV) only with Authorized Participants and only in large blocks of 50,000 shares (each, a “Creation Unit”). The fund’s NAV per share is computed at the close of the New York Stock Exchange (NYSE). However, the NAV per share may be calculated at a time other than the normal close of the NYSE if trading on the NYSE is restricted, if the NYSE closes earlier, or as may be permitted by the SEC. Individual fund shares may not be purchased or redeemed directly with the fund. An Authorized Participant may purchase or redeem a Creation Unit of the fund each business day that the fund is open in exchange for the delivery of a designated portfolio of in-kind securities and/or cash. When purchasing or redeeming Creation Units, Authorized Participants are also required to pay a fixed and/or variable purchase or redemption transaction fee as well as any applicable additional variable charge to defray the transaction cost to a fund.

Individual fund shares may be purchased and sold only on a national securities exchange through brokers. Shares are listed for trading on NYSE Arca, Inc. (NYSE Arca) and because the shares will trade at market prices rather than NAV, shares may trade at prices greater than NAV (at a premium), at NAV, or less than NAV (at a discount). The fund’s shares are ordinarily valued as of the close of regular trading (normally 4:00 p.m. Eastern time) on each day that the NYSE Arca is open.

New Accounting Guidance

In June 2022, the FASB issued Accounting Standards Update (ASU), ASU 2022-03, Fair Value Measurement (Topic 820) – Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions, which clarifies that a contractual restriction on the sale of an equity security is not considered part of the unit of account of the equity security and, therefore, is not considered in measuring fair value. The amendments under this ASU are effective for fiscal years beginning after December 15, 2023; however, the fund opted to early adopt, as permitted, effective December 1, 2022. Adoption of the guidance did not have a material impact on the fund’s financial statements.

Indemnification

In the normal course of business, the fund may provide indemnification in connection with its officers and directors, service providers, and/or private company investments. The fund’s maximum exposure under these arrangements is unknown; however, the risk of material loss is currently considered to be remote.

NOTE 2 – VALUATION

Fair Value

The fund’s financial instruments are valued at the close of the NYSE and are reported at fair value, which GAAP defines as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fund’s Board of Directors (the Board) has designated T. Rowe Price Associates, Inc. as the fund’s valuation designee (Valuation Designee). Subject to oversight by the Board, the Valuation Designee performs the following functions in performing fair value determinations: assesses and manages valuation risks; establishes and applies fair value methodologies; tests fair value methodologies; and evaluates pricing vendors and pricing agents. The duties and responsibilities of the Valuation Designee are performed by its Valuation Committee. The Valuation Designee provides periodic reporting to the Board on valuation matters.

Various valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value hierarchy that categorizes the inputs used to measure fair value:

Level 1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting date

Level 2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to, quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive markets, interest rates and yield curves, implied volatilities, and credit spreads)

Level 3 – unobservable inputs (including the Valuation Designee’s assumptions in determining fair value)

Observable inputs are developed using market data, such as publicly available information about actual events or transactions, and reflect the assumptions that market participants would use to price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best information available about

the assumptions that market participants would use to price the financial instrument. GAAP requires valuation techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. When multiple inputs are used to derive fair value, the financial instrument is assigned to the level within the fair value hierarchy based on the lowest-level input that is significant to the fair value of the financial instrument. Input levels are not necessarily an indication of the risk or liquidity associated with financial instruments at that level but rather the degree of judgment used in determining those values.

Valuation Techniques

Equity securities, including exchange-traded funds, listed or regularly traded on a securities exchange or in the over-the-counter (OTC) market are valued at the last quoted sale price or, for certain markets, the official closing price at the time the valuations are made. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Listed securities not traded on a particular day are valued at the mean of the closing bid and asked prices for domestic securities.

Investments in mutual funds are valued at the mutual fund’s closing NAV per share on the day of valuation. Assets and liabilities other than financial instruments, including short-term receivables and payables, are carried at cost, or estimated realizable value, if less, which approximates fair value.

Investments for which market quotations are not readily available or deemed unreliable are valued at fair value as determined in good faith by the Valuation Designee. The Valuation Designee has adopted methodologies for determining the fair value of investments for which market quotations are not readily available or deemed unreliable, including the use of other pricing sources. Factors used in determining fair value vary by type of investment and may include market or investment specific considerations. The Valuation Designee typically will afford greatest weight to actual prices in arm’s length transactions, to the extent they represent orderly transactions between market participants, transaction information can be reliably obtained, and prices are deemed representative of fair value. However, the Valuation Designee may also consider other valuation methods such as market-based valuation multiples; a discount or premium from market value of a similar, freely traded security of the same issuer; discounted cash flows; yield to maturity; or some combination. Fair value determinations are reviewed on a regular basis. Because any fair value determination involves a significant amount of judgment, there is a degree of subjectivity inherent in such pricing decisions. Fair value prices determined by the Valuation Designee could differ from those of other market participants, and it is possible that the fair value determined for a security may be materially different from the value that could be realized upon the sale of that security.

Valuation Inputs

The following table summarizes the fund’s financial instruments, based on the inputs used to determine their fair values on December 31, 2023 (for further detail by category, please refer to the accompanying Portfolio of Investments):

| ($000s) | Level 1 | Level 2 | Level 3 | Total Value |

| Assets | | | | |

| Common Stocks | $56,568 | $403 | $— | $56,971 |

| Short-Term Investments | 110 | — | — | 110 |

| Total | $56,678 | $403 | $— | $57,081 |

NOTE 3 – OTHER INVESTMENT TRANSACTIONS

Purchases and sales of portfolio securities excluding in-kind transactions and short-term securities aggregated $15,475,000 and $2,722,000, respectively, for the period ended December 31, 2023. Portfolio securities received and delivered through in-kind transactions aggregated $38,409,000 and $0, respectively, for the period ended December 31, 2023.

NOTE 4 – FEDERAL INCOME TAXES

Generally, no provision for federal income taxes is required since the fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Distributions determined in accordance with federal income tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes.

The fund files U.S. federal, state, and local tax returns as required. The fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return but which can be extended to six years in certain circumstances.

Capital accounts within the financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences. The permanent book/tax adjustments, if any, have no impact on results of operations or net assets.

The tax character of distributions paid for the periods presented was as follows:

| ($000s) | |

| | December 31, |

| | 2023 |

| Ordinary income (including short-term capital gains, if any) | $367 |

At December 31, 2023, the tax-basis cost of investments, (including derivatives, if any) and gross unrealized appreciation and depreciation were as follows:

| ($000s) | |

| Cost of investments | $51,085 |

| Unrealized appreciation | $ 6,312 |

| Unrealized depreciation | (316) |

| Net unrealized appreciation (depreciation) | $ 5,996 |

At December 31, 2023, the tax-basis components of accumulated net earnings (loss) were as follows:

| ($000s) | |

| Net unrealized appreciation (depreciation) | $5,996 |

| Loss carryforwards and deferrals | (187) |

| Total distributable earnings (loss) | $5,809 |

Temporary differences between book-basis and tax-basis components of total distributable earnings (loss) arise when certain items of income, gain, or loss are recognized in different periods for financial statement purposes versus for tax purposes; these differences will reverse in a subsequent reporting period. The temporary differences relate primarily to the deferral of losses from wash sales. The loss carryforwards and deferrals primarily relate to capital loss carryforwards and late-year ordinary loss deferrals. Capital loss carryforwards are available indefinitely to offset future realized capital gains. The fund has elected to defer certain losses to the first day of the following fiscal year for late-year ordinary loss deferrals.

NOTE 5 – FOREIGN TAXES

The fund is subject to foreign income taxes imposed by certain countries in which it invests. Additionally, capital gains realized upon disposition of securities issued in or by certain foreign countries are subject to capital gains tax imposed by those countries. All

taxes are computed in accordance with the applicable foreign tax law, and, to the extent permitted, capital losses are used to offset capital gains. Taxes attributable to income are accrued by the fund as a reduction of income. Current and deferred tax expense attributable to capital gains is reflected as a component of realized or change in unrealized gain/loss on securities in the accompanying financial statements. To the extent that the fund has country specific capital loss carryforwards, such carryforwards are applied against net unrealized gains when determining the deferred tax liability. Any deferred tax liability incurred by the fund is included in either Other liabilities or Deferred tax liability on the accompanying Statement of Assets and Liabilities.

NOTE 6 – RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. (Price Group). The investment management and administrative agreement between the fund and Price Associates provides for an all-inclusive annual fee equal to 0.33% of the fund’s average daily net assets. The fee is computed daily and paid monthly. The all-inclusive fee covers investment management services and ordinary, recurring operating expenses but does not cover interest and borrowing expenses; taxes; brokerage commissions and other transaction costs; fund proxy expenses; and nonrecurring and extraordinary expenses. All costs related to organization and offering of the fund are borne by Price Associates.

T. Rowe Price Investment Services, Inc. (Investment Services) serves as distributor to the fund. Pursuant to an underwriting agreement, no compensation for any distribution services provided is paid to Investment Services by the fund.

As of December 31, 2023, T. Rowe Price Group, Inc., or its wholly owned subsidiaries, owned 1,998,577 shares of the fund, representing 95% of the fund’s net assets.

The fund may participate in securities purchase and sale transactions with other funds or accounts advised by Price Associates (cross trades), in accordance with procedures adopted by the fund’s Board and Securities and Exchange Commission rules, which require, among other things, that such purchase and sale cross trades be effected at the independent current market price of the security. During the period ended December 31, 2023, the fund had no purchases or sales cross trades with other funds or accounts advised by Price Associates.

NOTE 7 – OTHER MATTERS

Unpredictable events such as environmental or natural disasters, war and conflict, terrorism, geopolitical events, and public health epidemics and similar public health threats may significantly affect the economy and the markets and issuers in which the fund invests. Certain events may cause instability across global markets, including reduced liquidity and disruptions in trading markets, while some events may affect certain geographic regions, countries, sectors, and industries more significantly than others, and exacerbate other pre-existing political, social, and economic risks.

The global outbreak of COVID-19 and related governmental and public responses have led and may continue to lead to increased market volatility and the potential for illiquidity in certain classes of securities and sectors of the market either in specific countries or worldwide.

In February 2022, Russian forces entered Ukraine and commenced an armed conflict, leading to economic sanctions imposed on Russia that target certain of its citizens and issuers and sectors of the Russian economy, creating impacts on Russian-related stocks and debt and greater volatility in global markets.

In March 2023, the banking industry experienced heightened volatility, which sparked concerns of potential broader adverse market conditions. The extent of impact of these events on the US and global markets is highly uncertain.

These are recent examples of global events which may have a negative impact on the values of certain portfolio holdings or the fund’s overall performance. Management is actively monitoring the risks and financial impacts arising from these events.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors of T. Rowe Price Exchange-Traded Funds, Inc. and Shareholders of T. Rowe Price Value ETF

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of T. Rowe Price Value ETF (one of the funds constituting T. Rowe Price Exchange-Traded Funds, Inc., referred to hereafter as the "Fund") as of December 31, 2023, and the related statements of operations and changes in net assets, including the related notes, and the financial highlights for the period June 14, 2023 (inception) through December 31, 2023 (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2023, and the results of its operations, changes in its net assets, and the financial highlights for the period June 14, 2023 (inception) through December 31, 2023 in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

(CONTINUED)

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of December 31, 2023 by correspondence with the custodian. We believe that our audit provides a reasonable basis for our opinion.

/s/ PricewaterhouseCoopers LLP

Baltimore, Maryland

February 16, 2024

We have served as the auditor of one or more investment companies in the T. Rowe Price group of investment companies since 1973.

TAX INFORMATION (UNAUDITED) FOR THE TAX YEAR ENDED 12/31/23

We are providing this information as required by the Internal Revenue Code. The amounts shown may differ from those elsewhere in this report because of differences between tax and financial reporting requirements. The fund’s distributions to shareholders included:

For taxable non-corporate shareholders, $382,000 of the fund’s income represents qualified dividend income subject to a long-term capital gains tax rate of not greater than 20%.

For corporate shareholders, $348,000 of the fund’s income qualifies for the dividends-received deduction.

INFORMATION ON PROXY VOTING POLICIES, PROCEDURES, AND RECORDS

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information. You may request this document by calling 1-800-638-5660 or by accessing the SEC’s website, sec.gov.

The description of our proxy voting policies and procedures is also available on our corporate website. To access it, please visit the following Web page:

https://www.troweprice.com/corporate/en/utility/policies.html

Scroll down to the section near the bottom of the page that says, “Proxy Voting Policies.” Click on the Proxy Voting Policies link in the shaded box.

Each fund’s most recent annual proxy voting record is available on our website and through the SEC’s website. To access it through T. Rowe Price, visit the website location shown above, and scroll down to the section near the bottom of the page that says, “Proxy Voting Records.” Click on the Proxy Voting Records link in the shaded box.

HOW TO OBTAIN QUARTERLY PORTFOLIO HOLDINGS

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission (SEC) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The fund’s Form N-PORT is available electronically on the SEC’s website (sec.gov). In addition, most T. Rowe Price funds disclose their first and third fiscal quarter-end holdings on troweprice.com.

TAILORED SHAREHOLDER REPORTS FOR MUTUAL FUNDS AND EXCHANGE TRADED FUNDS

In October 2022, the Securities and Exchange Commission (SEC) adopted rule and form amendments requiring Mutual Funds and Exchange-Traded Funds to transmit concise and visually engaging streamlined annual and semiannual reports that highlight key information to shareholders. Other information, including financial statements, will no longer appear in

the funds’ shareholder reports but will be available online, delivered free of charge upon request, and filed on a semiannual basis on Form N-CSR. The rule and form amendments have a compliance date of July 24, 2024.

Liquidity Risk Management Program

In accordance with Rule 22e-4 (Liquidity Rule) under the Investment Company Act of 1940, as amended, the fund has established a liquidity risk management program (Liquidity Program) reasonably designed to assess and manage the fund’s liquidity risk, which generally represents the risk that the fund would not be able to meet redemption requests without significant dilution of remaining investors’ interests in the fund. The fund’s Board of Directors (Board) has appointed the fund’s investment adviser, T. Rowe Price Associates, Inc. (Adviser), as the administrator of the Liquidity Program. As administrator, the Adviser is responsible for overseeing the day-to-day operations of the Liquidity Program and, among other things, is responsible for assessing, managing, and reviewing with the Board at least annually the liquidity risk of each T. Rowe Price fund. The Adviser has delegated oversight of the Liquidity Program to a Liquidity Risk Committee (LRC), which is a cross-functional committee composed of personnel from multiple departments within the Adviser.

The Liquidity Program’s principal objectives include supporting the T. Rowe Price funds’ compliance with limits on investments in illiquid assets and mitigating the risk that the fund will be unable to timely meet its redemption obligations. The Liquidity Program also includes a number of elements that support the management and assessment of liquidity risk, including an annual assessment of factors that influence the fund’s liquidity and the periodic classification and reclassification of a fund’s investments into categories that reflect the LRC’s assessment of their relative liquidity under current market conditions. Under the Liquidity Program, every investment held by the fund is classified at least monthly into one of four liquidity categories based on estimations of the investment’s ability to be sold during designated time frames in current market conditions without significantly changing the investment’s market value.

As required by the Liquidity Rule, at a meeting held on July 24, 2023, the Board was presented with an annual assessment that was prepared by the LRC on behalf of the Adviser and addressed the operation of the Liquidity Program and assessed its adequacy and effectiveness of implementation, including any material changes to the Liquidity Program and the determination of each fund’s Highly Liquid Investment Minimum (HLIM). The annual assessment included consideration of the following factors, as applicable: the fund’s investment strategy and liquidity of portfolio investments during normal and reasonably foreseeable stressed conditions, including whether the investment strategy is appropriate for an open-end fund, the extent to which the strategy involves a relatively concentrated portfolio or large positions in particular issuers, and the use of borrowings for investment purposes and derivatives; short-term and long-term cash flow projections covering both normal and reasonably foreseeable stressed conditions; and holdings of cash and cash equivalents, as well as available borrowing arrangements.

For the fund and other T. Rowe Price funds, the annual assessment incorporated a report related to a fund’s holdings, shareholder and portfolio concentration, any borrowings during the period, cash flow projections, and other relevant data for the period of April 1, 2022, through March 31, 2023. The report described the methodology for classifying a fund’s investments (including any derivative transactions) into one of four liquidity

categories, as well as the percentage of a fund’s investments assigned to each category. It also explained the methodology for establishing a fund’s HLIM and noted that the LRC reviews the HLIM assigned to each fund no less frequently than annually.

During the period covered by the annual assessment, the LRC has concluded, and reported to the Board, that the Liquidity Program continues to operate adequately and effectively and is reasonably designed to assess and manage the fund’s liquidity risk.

ABOUT THE FUND’S DIRECTORS AND OFFICERS

Your fund is overseen by a Board of Directors (Board) that meets regularly to review a wide variety of matters affecting or potentially affecting the fund, including performance, investment programs, compliance matters, advisory fees and expenses, service providers, and business and regulatory affairs. The Board elects the fund’s officers, who are listed in the final table. The directors who are also employees or officers of T. Rowe Price are considered to be “interested” directors as defined in Section 2(a)(19) of the 1940 Act because of their relationships with T. Rowe Price Associates, Inc. (T. Rowe Price), and its affiliates. The business address of each director and officer is 100 East Pratt Street, Baltimore, Maryland 21202. The Statement of Additional Information includes additional information about the fund directors and is available without charge by calling a T. Rowe Price representative at 1-800-638-5660.

INDEPENDENT DIRECTORS(a)

Name

(Year of Birth)

Year Elected

[Number of T. Rowe Price

Portfolios Overseen] | Principal Occupation(s) and Directorships of Public Companies and

Other Investment Companies During the Past Five Years |

Teresa Bryce Bazemore

(1959)

2020

[209] | President and Chief Executive Officer, Federal Home Loan

Bank of San Francisco (2021 to present); Chief Executive Officer,

Bazemore Consulting LLC (2018 to 2021); Director, Chimera

Investment Corporation (2017 to 2021); Director, First Industrial

Realty Trust (2020 to present); Director, Federal Home Loan Bank of

Pittsburgh (2017 to 2019) |

Melody Bianchetto

(1966)

2023

[209] | Vice President for Finance, University of Virginia (2015 to 2023)

|

Bruce W. Duncan

(1951)

2020

[209] | President, Chief Executive Officer, and Director, CyrusOne, Inc. (2020 to

2021); Chair of the Board (2016 to 2020) and President (2009 to 2016),

First Industrial Realty Trust, owner and operator of industrial properties;

Member, Investment Company Institute Board of Governors (2017 to

2019); Member, Independent Directors Council Governing Board (2017

to 2019); Senior Advisor, KKR (2018 to 2022); Director, Boston

Properties (2016 to present); Director, Marriott International, Inc. (2016 to

2020) |

Robert J. Gerrard, Jr.

(1952)

2020

[209] | Chair of the Board, all funds (July 2018 to present)

|

INDEPENDENT DIRECTORS(a) (continued)

Name

(Year of Birth)

Year Elected

[Number of T. Rowe Price

Portfolios Overseen] | Principal Occupation(s) and Directorships of Public Companies and

Other Investment Companies During the Past Five Years |

Paul F. McBride

(1956)

2020

[209] | Advisory Board Member, Vizzia Technologies (2015 to present); Board

Member, Dunbar Armored (2012 to 2018)

|

Mark J. Parrell

(1966)

2023

[209] | Board of Trustees Member and Chief Executive Officer (2019 to

present), President (2018 to present), Executive Vice President and

Chief Financial Officer (2007 to 2018), and Senior Vice President and

Treasurer (2005 to 2007), EQR; Member, Nareit Dividends Through

Diversity, Equity & Inclusion CEO Council and Chair, Nareit 2021 Audit

and Investment Committee (2021); Advisory Board, Ross Business

School at University of Michigan (2015 to 2016); Member, National

Multifamily Housing Council and served as Chair of the Finance

Committee (2015 to 2016); Member, Economic Club of Chicago;

Director, Brookdale Senior Living, Inc. (2015 to 2017); Director, Aviv

REIT, Inc. (2013 to 2015); Director, Real Estate Roundtable and the

2022 Executive Board Nareit; Board of Directors and Chair of the

Finance Committee, Greater Chicago Food Depository |

Kellye L. Walker

(1966)

2021

[209] | Executive Vice President and Chief Legal Officer, Eastman Chemical

Company (April 2020 to present); Executive Vice President and Chief

Legal Officer, Huntington Ingalls Industries, Inc. (January 2015 to March

2020); Director, Lincoln Electric Company (October 2020 to present) |

(a)All information about the independent directors was current as of December 31, 2022, unless otherwise indicated, except for the number of portfolios overseen, which is current as of the date of this report.

INTERESTED DIRECTORS(a)

Name

(Year of Birth)

Year Elected

[Number of T. Rowe Price

Portfolios Overseen] | Principal Occupation(s) and Directorships of Public Companies and

Other Investment Companies During the Past Five Years |

David Oestreicher

(1967)

2020

[209] | Director, Vice President, and Secretary, T. Rowe Price, T. Rowe Price

Investment Services, Inc., T. Rowe Price Retirement Plan Services,

Inc., and T. Rowe Price Services, Inc.; Director and Secretary,

T. Rowe Price Investment Management, Inc. (Price Investment

Management); Vice President and Secretary, T. Rowe Price

International (Price International); Vice President, T. Rowe Price Hong

Kong (Price Hong Kong), T. Rowe Price Japan (Price Japan), and T.

Rowe Price Singapore (Price Singapore); General Counsel, Vice

President, and Secretary, T. Rowe Price Group, Inc.; Chair of the

Board, Chief Executive Officer, President, and Secretary, T. Rowe

Price Trust Company; Principal Executive Officer and Executive Vice

President, all funds |

Eric L. Veiel, CFA

(1972)

2022

[209] | Director and Vice President, T. Rowe Price; Vice President, T. Rowe

Price Group, Inc., and T. Rowe Price Trust Company; Vice President,

Global Funds |

(a)All information about the interested directors was current as of December 31, 2022, unless otherwise indicated, except for the number of portfolios overseen, which is current as of the date of this report.

OFFICERS

Name (Year of Birth)

Position Held With Exchange-Traded Funds, Inc. | Principal Occupation(s) |

Christopher P. Brown (1977)

Executive Vice President | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

Armando (Dino) Capasso (1974)

Chief Compliance Officer and Vice

President | Chief Compliance Officer and Vice President, T. Rowe Price and Price Investment Management; Vice President, T. Rowe Price Group, Inc.; formerly, Chief Compliance Officer, PGIM Investments LLC and AST Investment Services, Inc. (ASTIS) (to 2022); Chief Compliance Officer, PGIM Retail Funds complex and Prudential Insurance Funds (to 2022); Vice President and Deputy Chief Compliance Officer, PGIM Investments LLC and ASTIS (to 2019) |

Timothy Coyne (1967)

Executive Vice President | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

Vincent Michael DeAugustino (1983)

Executive Vice President | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

OFFICERS (continued)

Name (Year of Birth)

Position Held With Exchange-Traded Funds, Inc. | Principal Occupation(s) |

Anna Alexandra Dreyer, Ph.D., CFA (1981)

Executive Vice President | Vice President, T. Rowe Price and T. Rowe Price Group, Inc. |

Alan S. Dupski, CPA (1982)

Principal Financial Officer, Vice

President, and Treasurer | Vice President, Price Investment Management, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

Cheryl Emory (1963)

Assistant Secretary | Assistant Vice President and Assistant Secretary, T. Rowe Price; Assistant Secretary, T. Rowe Price Group, Inc., Price Investment Management, Price International, Price Hong Kong, Price Singapore, T. Rowe Price Investment Services,

Inc., T. Rowe Price Retirement Plan Services, Inc., and T.

Rowe Price Trust Company |

Joseph B. Fath, CPA (1971)

Executive Vice President | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

David Giroux (1975)

Executive Vice President | Vice President, Price Investment Management, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

Paul Greene II (1978)

Executive Vice President | Vice President, T. Rowe Price and T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

Cheryl Hampton, CPA (1969)

Vice President | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company; formerly, Tax Director, Invesco Ltd. (to 2021); Vice President, Oppenheimer Funds, Inc. (to 2019) |

Ann M. Holcomb, CFA (1972)

Executive Vice President | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

Thomas J. Huber, CFA (1966)

Executive Vice President | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

Stephon Jackson, CFA (1962)

Co-president | Director and President, Price Investment Management; Vice President, T. Rowe Price Group, Inc. |

Benjamin Kersse, CPA (1989)

Vice President | Vice President, T. Rowe Price and T. Rowe Price Trust

Company |

Paul J. Krug, CPA (1964)

Vice President | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

Robert M. Larkins, CFA (1973)

Executive Vice President | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

John D. Linehan, CFA (1965)

Executive Vice President | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., and T. Rowe Price Trust Company |

OFFICERS (continued)

Name (Year of Birth)

Position Held With Exchange-Traded Funds, Inc. | Principal Occupation(s) |

Jodi Love (1977)