UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-23499

Goldman Sachs Real Estate Diversified Income Fund

(Exact name of registrant as specified in charter)

200 West Street, New York, New York 10282

(Address of principal executive offices) (Zip code)

| Caroline Kraus, Esq. | Copies to: | |

| Goldman Sachs & Co. LLC | Stephen H. Bier, Esq. | |

| 200 West Street | William J. Bielefeld, Esq. | |

| New York, New York 10282 | Dechert LLP | |

1095 Avenue of the Americas | ||

New York, NY 10036 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (212) 902-1000

Date of fiscal year end: September 30

Date of reporting period: September 30, 2020

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

The Annual Report to Shareholders is filed herewith. |

Goldman Sachs Interval Fund

| Annual Report | September 30, 2020 | |||

Real Estate Diversified Income Fund | ||||

It is our intention that beginning on January 1, 2021, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. At any time, you may elect to receive reports and certain communications from the Fund electronically by calling the applicable toll-free number below or by contacting your financial intermediary.

You may elect to receive all future shareholder reports in paper free of charge. If you hold shares of the Fund directly with the Fund’s transfer agent, you can inform the transfer agent that you wish to receive paper copies of reports by calling toll-free 800-526-7384. If you hold shares of the Fund through a financial intermediary, please contact your financial intermediary to make this election. Your election to receive reports in paper will apply to all Goldman Sachs Funds held in your account if you invest through your financial intermediary or all Goldman Sachs Funds held with the Fund’s transfer agent if you invest directly with the transfer agent.

Goldman Sachs Real Estate Diversified Income Fund

| 1 | ||||

| 9 | ||||

| 12 | ||||

| 16 | ||||

| 21 | ||||

| 35 | ||||

| 36 | ||||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||

PORTFOLIO RESULTS

Goldman Sachs Real Estate Diversified Income Fund

Investment Objective

The Fund seeks to produce income and achieve capital appreciation with low to moderate volatility and low to moderate correlation to the broader equity markets.

Portfolio Management Discussion and Analysis

After the close of business on May 15, 2020, Resource Real Estate Diversified Income Fund (the “Predecessor Fund”) was reorganized with and into the Goldman Sachs Real Estate Diversified Income Fund (the “Fund”). The Fund has assumed the Predecessor Fund’s historical performance. Therefore, the performance information reported below for the Fund is the combined performance of the Fund and the Predecessor Fund, which was managed by another investment adviser. The performance information shown in this report for periods through May 15, 2020 reflects the performance of the Predecessor Fund. Below, the Goldman Sachs Real Estate Securities Investment Team provides an overview of the U.S. real estate securities market for the 12 months ended September 30, 2020 and discusses the Fund’s performance and positioning for the period from May 18, 2020 through September 30, 2020 (the “GSAM Managed Reporting Period”).

| Q | How did the Fund perform during the 12 months ended September 30, 2020? |

| A | During the 12 months ended September 30, 2020, the Fund’s Class A, Class C, Class I, Class L and Class W Shares generated average annual total returns, without sales charges, of -5.20%, -5.94%, -5.05%, -5.46% and -5.31%, respectively. |

| During the period from October 1, 2019 through May 15, 2020, the Fund’s Class A, Class C, Class I Class L and Class W Shares generated cumulative total returns, without sales charges, of -6.88%, -7.33%, -6.79%, -7.09%, and -7.00%, and respectively. |

| During the GSAM Managed Reporting Period, i.e. since Goldman Sachs assumed management of the Fund through September 30, 2020, the Fund’s Class A, Class C, Class I, Class L and Class W Shares generated cumulative total returns, without sales charges, of 1.79%, 1.48%, 1.85%, 1.73% and 1.80%, respectively. |

| As of September 30, 2020, the Fund’s net asset value (“NAV”) for Class A, Class C, Class I, Class L and Class W Shares was $9.38, $9.38, $9.78, $9.39 and $9.52, respectively. |

| Q | What distributions did the Fund make during the 12 months ended September 30, 2020? |

| A | The Fund’s Class A Shares declared dividends totaling $0.71 per unit. The 12-Month Distribution Yield for Class A Shares was 6.40%. The Fund’s Class C Shares declared dividends totaling $0.63 per unit. The 12-Month Distribution Yield for Class C Shares was 5.59%. The Fund’s Class I Shares declared dividends totaling $0.75 per unit. The 12-Month Distribution Yield for Class I Shares was 6.53%. The Fund’s Class L Shares declared dividends totaling $0.68 per unit. The 12-Month Distribution Yield for Class L Shares was 6.09%. The Fund’s Class W Shares declared dividends totaling $0.72 per unit. The 12-Month Distribution Yield for Class W Shares was 6.38%. |

| Q | What economic and market factors most influenced the U.S. real estate securities market as a whole during the 12 months ended September 30, 2020? |

| A | The fourth calendar quarter of 2019 was characterized by the U.S. real estate securities market underperforming the broader U.S. equity market, following significant outperformance in the prior quarter. As the broad U.S. equity market surged, the real estate sector was negatively affected by rising yields, with the bellwether 10-year U.S. Treasury yield increasing approximately 24 basis points during the quarter to end December 2019 at 1.92%. (A basis point is 1/100th of a percentage point.) Also, growth expectations improving in more economically sensitive, cyclical sectors, combined with real estate securities generally trading at a slight premium to the value of the underlying property portfolios at the start of the fourth quarter, may have negatively impacted returns for the sector. Investors moved away from traditionally defensive and yield-oriented sectors, such as real estate, during these months. |

For the remainder of the 12 months ended September 30, 2020, the primary factor influencing the U.S. real estate securities market was the global COVID-19 pandemic that plagued the world and fundamentally altered the way we go about our daily lives. Most notably within the real estate market, small retail businesses and restaurants were shuttered and larger |

1

PORTFOLIO RESULTS

corporations who occupied office buildings across the U.S. pivoted to a nearly complete work-from-home dynamic. Additionally, there was a rapid acceleration in the adoption of online retail as families isolated from the world and remained indoors. Near-term uncertainty heightened around large segments of the commercial and residential real estate tenant base being able to pay rent as the spread of the COVID-19 crisis shut down the economy. Longer-term uncertainty arose around both the depth and duration of the economic downturn and the demand for space in what might be called the “new normal.” That said, the massive stimulus injected by both the U.S. Federal Reserve (the “Fed”) and the U.S. government in an attempt to cushion the economic impact of the pandemic did create liquidity in the economy and capital markets during the second and third quarters of 2020, which benefited the U.S. real estate securities market as a whole. |

| Still, there was significant performance divergence among different property types, depending on how they were impacted by the effects of the pandemic. Overall, underlying real estate fundamentals softened. More specifically, the closure of brick-and-mortar stores and restaurants severely hurt the retail subsector, with businesses of all sizes facing bankruptcy as expenses piled up and little, if any, revenue came in—and with only minimal support from the federal and local governments. Hotels were also among the worst performing subsectors within the U.S. real estate market during the 12 months ended September 30, 2020. Due to the pandemic, global travel of all kinds, including business and leisure, came to a near halt. This, in turn, caused hotel revenues to drop nearly 90%, with some properties having to shut down completely on a temporary basis. Providing significant headwinds to the multi-family/apartment subsector were both tenants losing the income needed to afford their monthly rent payments and the trend seen during the GSAM Managed Reporting Period of city-dwellers seeking to move away from the density and constrained space of apartments to more suburban settings. On the surface, the office subsector was also negatively impacted by the pandemic. As companies were forced to operate with their workforce at home, many found they were functioning well despite the virtual environment and thus began to reevaluate their needs for expensive office space. On the other hand, some companies that do want or need to maintain office space began looking to expand their footprint to provide additional space per person for better distancing between employees, a sharp reversal of the office densification we have seen over the last decade. |

| Conversely, the industrials subsector performed well, as the rapid acceleration of online shopping has meant online retailers need more warehouse space for increased inventory and larger logistical operations. Similarly, data centers were among the best performing subsectors of the U.S. real estate market during the 12 months ended September 30, 2020. Data centers benefited from increased demand, as work-from-home conditions and online classrooms became more ubiquitous, thereby exponentially increasing demand for bandwidth. Other aspects of life, such as shopping, social events, conferences and even family “get-togethers,” have also moved online, increasing the need for the data infrastructure to move and store the amount of data being generated. |

| The other major factor affecting the U.S. real estate securities market during the 12 months ended September 30, 2020 was interest rates. Following the outbreak of COVID-19, capital markets spiraling downward drove the Fed to step in to provide monetary policy support. Among other initiatives, the Fed lowered the targeted federal funds rate to near zero, similar to the action it took amid the 2008-2009 financial crisis. Historically, with interest rates lower, financing becomes less expensive and therefore more heavily accessed, which should, in theory, stimulate transaction volumes. However, this interest rate cut by the Fed in March 2020 coincided with a severely weakening economic backdrop and increased uncertainty around both commercial and residential tenants’ ability to pay rents, thereby introducing significant hesitancy around acquisitions for the near term. |

| Commercial mortgage-backed securities posted mixed performance during the 12 months ended September 30, 2020, with bonds linked to retail and hotels generally weaker and bonds linked to office and multi-family properties generally stronger. |

| Real estate preferred stocks came under pressure during the worst of the pandemic in the spring of 2020 but rebounded meaningfully since, as the strength of real estate investment trust (“REIT”) balance sheets became more apparent and as liquidity returned to the capital markets. |

| Q | What key factors were responsible for the Fund’s performance during the GSAM Managed Reporting Period? |

| A | Public credit investments contributed most positively to the Fund’s performance during the GSAM Managed Reporting Period. The Fund’s allocation to public credit consists of preferred stock investments and mortgage REITs. While struggling early in 2020, they rebounded along with the broader U.S. equity markets in the second and third quarters of 2020 as it became increasingly clear the U.S. government was going to provide substantial relief from the threat of bankruptcy. Credit investments also provided diversification within the asset allocation of the Fund. When the potential for tenants not to make rent payments was still unclear, the Fund’s credit investments, which are placed in a more senior position in the capital stack, were not at the same level of potential risk as their equity counterparts. (The “capital stack” refers to the legal |

2

PORTFOLIO RESULTS

organization of all of the capital placed into a company or secured by an asset through investment or borrowing. The capital stack determines who has legal rights to certain assets and income, who receives priority of payment in the event of an uncured default, and in which order each party may be repaid or given authority to take over or liquidate assets in the event of a bankruptcy. The more senior one is in the capital stack, i.e., the more secure, the better.) Therefore, public credit investments played an important role in reducing the overall risk of the Fund’s portfolio during the GSAM Managed Reporting Period. |

| Private equity contributed least to the Fund’s performance during the GSAM Managed Reporting Period, not unexpected given the lag in pricing experienced in the private markets. The publicly traded markets reprice daily on the exchanges and therefore can reflect real-time changing investor sentiment, which rapidly evolved during the 12 months ended September 30, 2020. For example, during the first quarter of 2020, the macroeconomic backdrop deteriorated substantially and then saw rapid recovery in select segments of the economy during the second and third quarters of 2020. Public investments had already taken part in and reflected both the decline and subsequent rebound, while the private markets were still experiencing the early effects of the pandemic. That said, despite their lag in pricing, the private equity investments worked to dampen volatility in the Fund, as they did not experience price movements during the GSAM Managed Reporting Period as severe as public equity investments did in March 2020. |

| Q | What were some of the Fund’s best-performing individual holdings during the GSAM Managed Reporting Period? |

| A | The top contributors to the Fund’s performance during the GSAM Managed Reporting Period were Starwood Property Trust, ARES Commercial Real Estate Corporation and MFA Financial, Inc. Preferred. |

| Starwood Property Trust is the largest commercial mortgage REIT in the U.S. Ares Commercial Real Estate Corporation, a specialty finance company, originates and invests in commercial real estate loans and related investments in the U.S. In each case, the stock rebounded strongly during the GSAM Managed Reporting Period along with the broad U.S. equity market and as the liquidity situation for each improved. MFA Financial, Inc. operates as a REIT primarily engaged in the business of investing, on a leveraged basis, in residential mortgage assets, including residential mortgage-backed securities and residential whole loans. Generally, residential credit-focused assets rebounded strongly during the GSAM Managed Reporting Period as strength in the housing market grew. Also, MFA Financial, Inc. as a company was recapitalized in a manner particularly beneficial to investors in its preferred stock. |

| Q | Which positions detracted significantly from the Fund’s performance during the GSAM Managed Reporting Period? |

| A | The positions that detracted most from the Fund’s performance during the GSAM Managed Reporting Period were Harrison Street Core Property Fund, LP; Clarion Lion Properties Fund, LP; and Broadstone Net Lease Inc. |

| Harrison Street Core Property Fund, LP was created to provide investment in stabilized, cash flow-producing real estate with demographic-driven demand. The fund invests in student housing, both on and off campus, and other education-related real estate investments; senior housing, including independent living, assisted living and memory care communities; medical office buildings and other health care-related real estate investments; life science buildings and storage properties. During the GSAM Managed Reporting Period, it experienced weakness due primarily to its exposure to health care and senior living properties, two areas of the real estate market impacted especially heavily by COVID-19 but also property types where we have conviction around values over the longer term. |

| Clarion Lion Properties Fund, LP is a diversified core real estate fund with a portfolio of primarily institutional quality real estate assets located throughout the U.S. The fund is focused on maintaining diversification across four core property types—office, retail, industrial and multi-family residential. The portfolio is actively managed through a continuous evaluation of the 50 largest metropolitan statistical areas with respect to each major property type to identify relative sectors of value and does tilt toward the largest and most liquid markets. (Metropolitan statistical areas are delineated by the U.S. Office of Management and Budget as having at least one urbanized area with a minimum population of 50,000.) During the GSAM Managed Reporting Period, the fund’s exposure to the retail subsector drove its performance weakness most. |

Broadstone Net Lease Inc. is a REIT that acquires, owns and manages primarily single-tenant commercial real estate properties that are net leased on a long-term basis to a diversified group of tenants. (Commonly used in commercial real estate, the term net lease refers to a contractual agreement where a lessee pays a portion or all of the taxes, insurance fees and maintenance costs for a property in addition to rent. In the purest form of a net lease, the tenant is expected to pay for all the costs related to a piece of property |

3

PORTFOLIO RESULTS

as if the tenant were the actual owner. A net lease is the opposite of a gross lease, where the tenant pays a flat rental fee while the landlord is responsible for the other costs.) Approximately 15% of Broadstone Net Lease’s portfolio is in restaurants, which experienced extreme pressure amidst the COVID-19 pandemic, leading to the REIT’s performance weakness during the GSAM Managed Reporting Period. |

| Q | How did the Fund use derivatives and similar instruments during the GSAM Managed Reporting Period? |

| A | The Fund did not use derivatives during the GSAM Managed Reporting Period. |

| Q | Did the Fund make any significant purchases or sales during the GSAM Managed Reporting Period? |

| A | During the GSAM Managed Reporting Period, we established Fund positions in self-storage REITs Life Storage and CubeSmart because we believed their stocks were trading at a significant discount to their respective NAVs and felt the self-storage subsector’s fundamentals were poised to improve. These purchases proved prudent, as the self-storage subsector benefited from increased demand amidst pandemic-driven secular trends developing during the GSAM Managed Reporting Period. For example, the subsector saw an acceleration in demand from a robust residential real estate market, wherein more urban dwellers sought to move away from cities to the suburbs and needed storage for their belongings during the gap time between the two. Demand was also boosted by college students and younger workers who chose to live at home rather than in dorms or their own apartments, thus creating less turnover and higher occupancies for self-storage units. |

| We initiated a Fund position in PennyMac Mortgage Investment Trust, a specialty finance company, during the GSAM Managed Reporting Period, as we viewed its risk/reward profile and valuation as attractive when its stock was at 80% of book value. We subsequently sold the position when its corporate earnings results came in as the market expected, and its stock was re-rated. (When the market changes its view of a company sufficiently to make calculation ratios, such as price/earnings ratios, substantially higher or lower, this a re-rating.) |

| We sold a number of Fund positions in preferred stock investments to reallocate the proceeds to public common equity positions. |

| Q | Were there any changes made in the Fund’s investment strategy during the GSAM Managed Reporting Period? |

| A | Since acquiring and assuming management of the Fund in mid-May 2020, we made no material changes to the Fund’s investment strategy. However, we opportunistically increased the Fund’s exposure to more secular growth-oriented property types, such as self-storage, and to the multi-family subsector, all in the public equity markets given what we saw as their compelling, attractive valuations. We also added to the self-storage subsector based on our view of its improving fundamentals, as discussed earlier. We reduced exposure to preferred securities, such as certain office and hotel preferred stocks, as we felt we could find more attractive risk/reward profiles elsewhere, and used the proceeds to fund the aforementioned common equity purchases. |

| Q | How was the Fund positioned at the end of the GSAM Managed Reporting Period? |

| A | At the end of the GSAM Managed Reporting Period, the Fund was invested with approximately 44% of its total net assets in private equity, approximately 29% of its total net assets in private credit, approximately 13% of its total net assets in public equity, approximately 10% of its total net assets in public credit, and approximately 4% of its total net assets in cash and cash equivalents. |

Within the Fund’s overall net equity, approximately 36% of assets were invested in higher growth property types benefiting from near-term secular trends, including industrials, towers/digital storage, life science-focused offices, single-family housing, manufactured housing and self-storage. Approximately 30% of assets within the Fund’s overall net equity was invested in multi-family properties, where we believe valuations, long-term demand, demographics and necessity are favoring the property type over the longer term. For example, at the end of the GSAM Managed Reporting Period, about 52% of 18 to 29 year olds, a key demographic for multi-family rentals, were living with their parents, the highest level on record since the Great Depression. We believe this is poised to reverse and may well be met with more muted new construction/supply, translating to improved occupancy and rents when conditions allow. The Fund’s positioning within the multi-family subsector was focused at the end of the GSAM Managed Reporting Period on the suburbs and lower tax states, which we believe could see greater demand than cities in high tax states. Approximately 19% of the Fund’s overall net equity was invested in office properties at the end of the GSAM Managed Reporting Period. Despite facing headwinds from |

4

PORTFOLIO RESULTS

telecommuting trends, we believe there is good value and select pockets of opportunity located in “innovation cities” or low tax states where job growth is and will likely remain, in our view, higher. Additionally, the Fund’s exposure to this subsector at the end of the GSAM Managed Reporting Period had limited near-term maturities. (An “innovation city” is one where leading-edge anchor institutions and companies cluster and connect with start-ups, business incubators and accelerators.) At the end of the GSAM Managed Reporting Period, approximately 12% of the Fund’s overall net equity were invested in health care properties that, in our view, offer higher predictability of cash flows due to inelastic yet growing demand drivers, such as aging demographics, and longer lease terms. Approximately 3% of the Fund’s overall net equity were invested in retail properties at the end of the GSAM Managed Reporting Period, focused on those with necessity-based tenants, such as grocery-anchored centers, which we find better insulated from obsolescence. There were no holdings within the public equity sleeve in hotel properties at the end of the GSAM Managed Reporting Period. |

| At the end of the GSAM Managed Reporting Period, the Fund’s positioning within the public credit sleeve was broadly diversified across numerous property types that we believed would provide attractive yield, low volatility and equity-like returns. |

| Q | What is the Fund’s tactical view and strategy for the months ahead? |

| A | By the end of the GSAM Managed Reporting Period, it had become clear to us that some real estate property types had been struggling pre-pandemic due to the disruptive impact of technology, and the pandemic served to accelerate that disruption. For example, online and other e-commerce spending trends translated to less demand for brick-and-mortar retail, requiring an even more vigilant view toward retail than was the case before the COVID-19 outbreak. Other real estate property types were affected directly by the COVID-19 crisis and must be managed carefully. Due to greater efficiency of space usage plus increased telecommuting trends, for instance, there is now less demand for commodity office buildings. (A commodity office building is a standard, “run of the mill” office building, as opposed to a specialty office building.) Also, due to reduced business travel and increased remote work driven by concerns around COVID-19, corporate/group-oriented hotels have struggled. |

| Conversely, some property types have either benefited from changes in behavior or can grow despite it, in our view. At the end of the GSAM Managed Reporting Period, we were focused on areas like industrial and logistics real estate, towers, digital storage, self-storage, single-family housing and manufactured housing. Some of these property types have secular demand drivers tied to powerful innovation trends. The proliferation of data and an increased need to store it has buoyed digital storage properties. Similarly, the proliferation of data and an increased need to transport it has boosted towers. Biotechnology innovation-driven demand has made life-sciences offices an attractive area of the market, in our opinion. Online spending trends translating to increased demand for logistics to get the box from the warehouse to the end consumer has supported the industrial property subsector. The “content gold rush” in southern California and the growth of the information technology sector, especially on the west coast of the U.S., has created demand for technology-driven office space. |

| Other property types have secular demand drivers tied to powerful demographic trends. For health care properties, we look at aging demographics as a demand driver. Leisure, hotels and gaming properties benefited prior to the pandemic from an increased desire for experience over things, partially driven by the millenial generation, a trend we believe will resume in a post-pandemic scenario. Manufactured housing may be driven by aging demographics and a push toward affordable housing post COVID-19. Multi-family housing properties, in our view, may well be supported going forward by population growth and an increased demand for renting over buying, especially pronounced in low tax states. Similarly, single-family rentals’ performance may be driven by strong household formation and increased desire to rent as well as by a move toward the suburbs amidst stay-at-home conditions. As discussed earlier, self-storage, we believe, should continue to perform well due to increased life changes, including job loss, job change, divorce, remote learning, adult children living with parents and more. |

| In short, we believe it will be increasingly critical in the months ahead to distinguish between property types that have had a temporary cyclical impact from the pandemic, either positive or negative, and those that have more secular and/or long-term headwinds and tailwinds. As we move forward, we intend to maintain our approach that aims to balance the need for attractive income and capital appreciation with low to moderate volatility relative to equity and public real estate markets by investing primarily in income-producing real estate equity and debt securities. Through this actively managed closed-end interval fund, we will continue seeking to provide access to both private and public real estate diversified across property types, geography and asset class (equity and debt). |

5

PORTFOLIO RESULTS

| Q | How did the Fund use leverage during the GSAM Managed Reporting Period? |

| A | The line of credit established by the Fund under GSAM’s management is a bilateral, fully committed, revolving credit facility. (A revolving credit facility is a line of credit arranged between a bank and a business. It comes with an established maximum amount, and the business can access the funds at any time when needed.) The Fund, while under the management of Resource, had access to financing via its prime brokerage agreement, which was accompanied by certain risks that are now mitigated by our establishment of a fully committed credit facility. |

| Sector, subsector and property type designations throughout this shareholder report are defined by GSAM. |

6

FUND BASICS

Real Estate Diversified Income Fund

as of September 30, 2020

| TOP TEN HOLDINGS AS OF 9/30/201 | ||||||||

| Holding | % of Net Assets | Asset Class | ||||||

| Heitman Core Real Estate Debt Income Trust, LP | 8.6 | % | Private REITs & Private Investment Funds | |||||

| Carlyle Property Investors, LP | 5.8 | Private REITs & Private Investment Funds | ||||||

| Menlo Equities Absolute Return Fund, LP | 5.1 | Private REITs & Private Investment Funds | ||||||

| Harrison Street Core Property Fund, LP | 4.9 | Private REITs & Private Investment Funds | ||||||

| Clarion Ventures 4, LP | 4.9 | Private REITs & Private Investment Funds | ||||||

| Brookfield Premier Real Estate Partners, LP | 4.7 | Private REITs & Private Investment Funds | ||||||

| Clarion Lion Properties Fund, LP | 4.1 | Private REITs & Private Investment Funds | ||||||

| ACRES Capital Debt Opportunity Fund, LP | 4.1 | Private REITs & Private Investment Funds | ||||||

| Brookfield Real Estate Finance Fund V, LP | 3.9 | Private REITs & Private Investment Funds | ||||||

| Prologis Targeted U.S. Logistics Holdings II, LP | 3.5 | Private REITs & Private Investment Funds | ||||||

| 1 | The top 10 holdings may not be representative of the Fund’s future investments. |

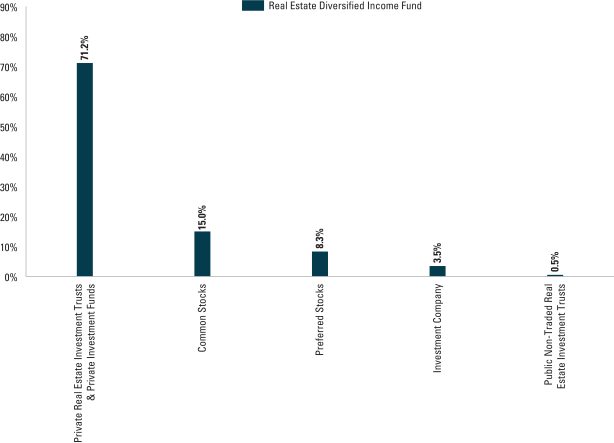

| ASSET CLASS ALLOCATION2 |

| As of September 30, 2020 |

| 2 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall allocations may differ from percentages contained in the graph above. Figures in the above graph may not sum to 100% due to the exclusion of other assets and liabilities. |

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance.

7

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Performance Summary

September 30, 2020

Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when repurchased, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

| Average Annual Total Return through September 30, 2020*,** | One Year | Five Years | Since Inception | |||||||

Class A (Commenced March 12, 2013) | ||||||||||

Excluding sales charges | -5.20% | 5.56% | 5.41% | |||||||

Including sales charges | -11.09% | 4.31% | 4.59% | |||||||

| ||||||||||

Class C (Commenced August 1, 2014) | ||||||||||

Excluding sales charges | -5.94% | 4.76% | 4.47% | |||||||

Including sales charges | -6.87% | 4.76% | 4.47% | |||||||

| ||||||||||

Class l (Commenced August 1, 2014) | -5.05% | 5.47% | 5.10% | |||||||

| ||||||||||

Class L (Commenced July 10, 2017) | ||||||||||

Excluding sales charges | -5.46% | N/A | 3.49% | |||||||

Including sales charges | -9.45% | N/A | 2.11% | |||||||

| ||||||||||

Class W (Commenced November 21, 2014) | -5.31% | 5.41% | 4.86% | |||||||

| ||||||||||

| * | These returns assume reinvestment of all distributions at NAV and reflect a maximum initial sales charge of 5.75% for Class A and 4.25% for Class L and the assumed contingent deferred sales charge for Class A and C Shares (0.5% and 1%, respectively, if repurchased within 12 months of purchase). Because Class W and Class I Shares do not involve a sales charge, such a charge is not applied to their Average Annual Total Return. |

| ** | After the close of business on May 15, 2020, the Predecessor Fund was reorganized into the Fund. The Fund has assumed the historical performance of the Predecessor Fund, which was managed by another investment adviser. Therefore, the performance information reported above for the Fund is the combined performance of the Fund and the Predecessor Fund. The performance information shown in this report for periods through May 15, 2020 reflects the performance of the Predecessor Fund. As a result, the Fund’s performance may differ substantially from what is shown for periods through May 15, 2020. |

For more information about the Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about the Fund’s investment strategies, holdings, and performance.

8

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Schedule of Investments

September 30, 2020

| Description | Value | |||||||

| Private Real Estate Investment Trusts & Private Investment Funds – 71.2%(a) | ||||||||

| ACRES Capital Debt Opportunity Fund, LP | $ | 11,851,758 | ||||||

| Ares Real Estate Enhanced Income Fund, LP | 9,047,907 | |||||||

| Ares US Real Estate Fund IX, LP | 9,180,578 | |||||||

| Bain Capital Real Estate Fund I-B, LP | 4,097,922 | |||||||

| Brookfield Premier Real Estate Partners, LP | 13,602,734 | |||||||

| Brookfield Real Estate Finance Fund V, LP | 11,322,188 | |||||||

| Carlyle Property Investors, LP | 16,642,543 | |||||||

| Clarion Lion Industrial Trust | 8,819,105 | |||||||

| Clarion Lion Properties Fund, LP | 11,891,253 | |||||||

| Clarion Partners Debt Investment Fund, LP | 6,857,669 | |||||||

| Clarion Ventures 4, LP | 13,989,773 | |||||||

| Harrison Street Core Property Fund, LP | 13,993,270 | |||||||

| Heitman Core Real Estate Debt Income Trust, LP | 24,640,132 | |||||||

| Menlo Equities Absolute Return Fund, LP | 14,792,882 | |||||||

| Nuveen U.S. Core-Plus Real Estate Debt Fund, LP | 4,652,191 | |||||||

| Prologis Targeted U.S. Logistics Holdings II, LP | 10,051,704 | |||||||

| Sculptor Real Estate Credit Fund, LP | 7,018,765 | |||||||

| The Trumbull Property Fund, LP | 6,524,018 | |||||||

| Truman 2016 SC5, LLC | 643,197 | |||||||

| Voya Commercial Mortgage Lending Fund, LP | 5,379,264 | |||||||

|

| |||||||

TOTAL PRIVATE REAL ESTATE INVESTMENT TRUSTS & PRIVATE INVESTMENT FUNDS |

| |||||||

| (Cost $199,179,535) | $ | 204,998,853 | ||||||

|

| |||||||

| Shares | Description | Value | ||||||

| Common Stocks – 15.0% | ||||||||

| Equity Real Estate Investment Trusts (REITs) – 13.0% | ||||||||

| 10,079 | Alexandria Real Estate Equities, Inc. REIT | $ | 1,612,640 | |||||

| 6,219 | American Tower Corp. REIT | 1,503,319 | ||||||

| 94,117 | Broadstone Net Lease, Inc.(a) | 1,277,111 | ||||||

| 57,212 | Camden Property Trust REIT | 5,090,724 | ||||||

| 161,170 | CubeSmart REIT | 5,207,403 | ||||||

| 21,137 | CyrusOne, Inc. REIT | 1,480,224 | ||||||

| 79,322 | Duke Realty Corp. REIT | 2,926,982 | ||||||

| 36,413 | Equity LifeStyle Properties, Inc. REIT | 2,232,117 | ||||||

| 19,880 | Essex Property Trust, Inc. REIT | 3,991,705 | ||||||

| 83,456 | Invitation Homes, Inc. REIT | 2,335,933 | ||||||

| 46,049 | Life Storage, Inc. REIT | 4,847,578 | ||||||

| 26,400 | MGM Growth Properties LLC, Class A REIT | 738,672 | ||||||

| 24,120 | Prologis, Inc. REIT | 2,426,954 | ||||||

| 30,280 | Terreno Realty Corp. REIT | 1,658,133 | ||||||

|

| |||||||

| 37,329,495 | ||||||||

|

| |||||||

| Mortgage Real Estate Investment Trusts (REITs) – 2.0% | ||||||||

| 235,775 | Ares Commercial Real Estate Corp. REIT | 2,154,983 | ||||||

| 140,573 | Starwood Property Trust, Inc. REIT | 2,121,247 | ||||||

| 165,000 | TPG RE Finance Trust, Inc. REIT | 1,395,900 | ||||||

|

| |||||||

| 5,672,130 | ||||||||

|

| |||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $45,244,457) | $ | 43,001,625 | ||||||

|

| |||||||

| Shares | Description | Dividend Rate | Value | |||||||||

| Preferred Stocks – 8.3% | ||||||||||||

| Equity Real Estate Investment Trusts (REITs) – 3.7% | ||||||||||||

| 59,203 | Global Net Lease, Inc., Series A | 7.25 | % | $ | 1,521,517 | |||||||

| 110,690 | SL Green Realty Corp., Series I | 6.50 | % | 2,780,533 | ||||||||

| 112,800 | Sunstone Hotel Investors, Inc., Series E | 6.95 | % | 2,809,848 | ||||||||

| 137,946 | UMH Properties, Inc., Series C | 6.75 | % | 3,472,101 | ||||||||

|

| |||||||||||

| 10,583,999 | ||||||||||||

|

| |||||||||||

| Mortgage Real Estate Investment Trusts (REITs) – 4.6% | ||||||||||||

| 102,679 | AGNC Investment Corp., Series E | 6.50 | % | 2,339,028 | ||||||||

| 105,601 | Annaly Capital Management, Inc., Series F | 6.95 | % | 2,378,134 | ||||||||

| 113,473 | MFA Financial, Inc., Series C | 6.50 | % | 2,085,634 | ||||||||

| 75,401 | New Residential Investment Corp., Series A | 7.50 | % | 1,661,838 | ||||||||

| 66,009 | PennyMac Mortgage Investment Trust, Series A | 8.13 | % | 1,520,187 | ||||||||

| 150,000 | Two Harbors Investment Corp., Series A | 8.13 | % | 3,300,000 | ||||||||

|

| |||||||||||

| 13,284,821 | ||||||||||||

|

| |||||||||||

| TOTAL PREFERRED STOCKS | ||||||||||||

| (Cost $25,765,061) | $ | 23,868,820 | ||||||||||

|

| |||||||||||

| Public Non-Traded Real Estate Investment Trusts – 0.5%(a)(b) | ||||||||||||

| 446,837 | InvenTrust Properties Corp. | $ | 897,685 | |||||||||

| 168,566 | NorthStar Healthcare Income, Inc. | 623,831 | ||||||||||

|

| |||||||||||

| | TOTAL PUBLIC NON-TRADED REAL ESTATE INVESTMENT TRUSTS | | ||||||||||

| (Cost $3,021,726) | $ | 1,521,516 | ||||||||||

|

| |||||||||||

| Shares | Dividend Rate | Value | ||||||

| Investment Company – 3.5%(c) | ||||||||

Goldman Sachs Financial Square Government Fund – Institutional Shares |

| |||||||

| 9,993,327 | 0.027 | % | $ | 9,993,327 | ||||

| (Cost $9,993,327) |

| |||||||

| ||||||||

| TOTAL INVESTMENTS – 98.5% |

| |||||||

| (Cost $283,204,106) |

| $ | 283,384,141 | |||||

| ||||||||

OTHER ASSETS IN EXCESS OF LIABILITIES – 1.5% |

| 4,428,670 | ||||||

| ||||||||

| NET ASSETS – 100.0% |

| $ | 287,812,811 | |||||

| ||||||||

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. | ||

| The accompanying notes are an integral part of these consolidated financial statements. | 9 |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Schedule of Investments (continued)

September 30, 2020

(a) | Restricted securities are not registered under the Securities Act of 1933 and are subject to legal restrictions on sale. These securities generally may be resold in transactions exempt from registration or to the public if the securities are subsequently registered and the registration statement is effective. Disposal of these securities may involve time consuming negotiations and prompt sale at an acceptable price may be difficult. Total market value of restricted securities amounts to $207,797,480, which represents approximately 72.2% of net assets as of September 30, 2020. See additional details below: | |

| Security | Date(s) of Purchase | Cost | ||||||||

ACRES Capital Debt Opportunity Fund, LP | 08/16/18-7/11/19 | $ | 12,000,000 | |||||||

Ares Real Estate Enhanced Income Fund, LP | 10/31/19-08/20/20 | 9,092,877 | ||||||||

Ares US Real Estate Fund IX, LP | 09/19/19-09/23/20 | 9,438,728 | ||||||||

Bain Capital Real Estate Fund I-B, LP | 12/18/19-09/23/20 | 3,968,771 | ||||||||

Broadstone Net Lease, Inc. | 12/30/16 | 1,811,764 | ||||||||

Brookfield Premier Real Estate Partners, LP | 10/01/19-12/30/19 | 14,000,000 | ||||||||

Brookfield Real Estate Finance Fund V, LP | 10/03/19-01/17/20 | 11,730,013 | ||||||||

Carlyle Property Investors, LP | 10/01/19-04/01/20 | 16,987,157 | ||||||||

Clarion Lion Industrial Trust | 12/30/19-04/01/20 | 5,485,051 | ||||||||

Clarion Lion Properties Fund, LP | 01/01/14-05/31/19 | 9,496,610 | ||||||||

Clarion Partners Debt Investment Fund, LP | 02/14/17-05/21/19 | 6,906,873 | ||||||||

Clarion Ventures 4, LP | 07/01/16-07/10/19 | 9,793,571 | ||||||||

Harrison Street Core Property Fund, LP | 07/03/19-10/03/19 | 14,157,423 | ||||||||

Heitman Core Real Estate Debt Income Trust, LP | 07/27/17-11/13/17 | 25,000,000 | ||||||||

InvenTrust Properties Corp. | 02/06/15 | 1,429,240 | ||||||||

Menlo Equities Absolute Return Fund, LP | 06/28/19 | 16,000,000 | ||||||||

NorthStar Healthcare Income, Inc. | 11/27/13-03/12/15 | 1,592,486 | ||||||||

Nuveen U.S. Core-Plus Real Estate Debt Fund, LP | 10/01/19-02/28/20 | 4,792,480 | ||||||||

Prologis Targeted U.S. Logistics Holdings II, LP | 01/03/20-07/15/20 | 10,096,699 | ||||||||

Sculptor Real Estate Credit Fund, LP | 01/21/20-05/12/20 | 7,635,204 | ||||||||

The Trumbull Property Fund, LP | 01/04/16-10/01/18 | 7,101,855 | ||||||||

Truman 2016 SC5, LLC | 10/21/19 | 97,429 | ||||||||

Voya Commercial Mortgage Lending Fund, LP | 10/11/19-12/30/19 | 5,398,794 | ||||||||

| Total | $ | 204,013,025 | ||||||||

(b) | Significant unobservable inputs were used in the valuation of this portfolio security; i.e. Level 3. | |

(c) | Represents an affiliated issuer. | |

| ||

Investment Abbreviations: | ||

LP | —Limited Partnership | |

REIT | —Real Estate Investment Trust | |

| ||

| 10 | The accompanying notes are an integral part of these consolidated financial statements. |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Schedule of Investments (continued)

September 30, 2020

| ADDITIONAL INVESTMENT INFORMATION |

Additional information on investments in private real estate investment funds:

| Security | Value | Redemption Frequency | Redemption Notice (Days) | Unfunded Commitments as of September 30, 2020 | ||||||||||||

ACRES Capital Debt Opportunity Fund, LP | $ | 11,851,758 | N/A | N/A | $ | — | ||||||||||

Ares Real Estate Enhanced Income Fund, LP(a) | 9,047,907 | Quarterly | 90 | 4,907,123 | ||||||||||||

Ares US Real Estate Fund IX, LP | 9,180,578 | N/A | N/A | 3,061,272 | ||||||||||||

Bain Capital Real Estate Fund I-B, LP | 4,097,922 | N/A | N/A | 6,217,735 | ||||||||||||

Brookfield Premier Real Estate Partners, LP(b) | 13,602,734 | Quarterly | 90 | — | ||||||||||||

Brookfield Real Estate Finance Fund V, LP | 11,322,188 | N/A | N/A | 12,752,267 | ||||||||||||

Carlyle Property Investors, LP(c) | 16,642,543 | Quarterly | 90 | — | ||||||||||||

Clarion Lion Industrial Trust | 8,819,105 | Quarterly | 90 | — | ||||||||||||

Clarion Lion Properties Fund, LP | 11,891,253 | Quarterly | 90 | — | ||||||||||||

Clarion Partners Debt Investment Fund, LP | 6,857,669 | N/A | N/A | 5,158,972 | ||||||||||||

Clarion Ventures 4, LP | 13,989,773 | N/A | N/A | 963,242 | ||||||||||||

Harrison Street Core Property Fund, LP | 13,993,270 | Quarterly | 45 | — | ||||||||||||

Heitman Core Real Estate Debt Income Trust, LP(d) | 24,640,132 | Quarterly | 90 | — | ||||||||||||

Menlo Equities Absolute Return Fund, LP(e) | 14,792,882 | Annually | 30 | — | ||||||||||||

Nuveen U.S. Core-Plus Real Estate Debt Fund, LP(f) | 4,652,191 | Quarterly | 45 | 5,207,520 | ||||||||||||

Prologis Targeted U.S. Logistics Holdings II, LP | 10,051,704 | Quarterly | 90 | — | ||||||||||||

Sculptor Real Estate Credit Fund, LP | 7,018,765 | N/A | N/A | 14,449,083 | ||||||||||||

The Trumbull Property Fund, LP | 6,524,018 | Quarterly | 60 | — | ||||||||||||

Truman 2016 SC5, LLC | 643,197 | N/A | N/A | — | ||||||||||||

Voya Commercial Mortgage Lending Fund, LP | 5,379,264 | Quarterly | 90 | — | ||||||||||||

| (a) | Redemptions are subject to a two-year holding period from the underlying fund’s initial capital call on February 22, 2019. |

| (b) | Redemptions are subject to a two-year holding period from the initial capital call on October 1, 2019. |

| (c) | Redemptions are subject to a two-year holding period from the underlying fund’s initial capital call on July 1, 2019. |

| (d) | Redemptions of certain tranches are subject to a three-year holding period from the underlying fund’s latest capital call on November 13, 2017. |

| (e) | Redemptions are subject to a two-year holding period from the underlying fund’s initial capital call on June 28, 2019. |

| (f) | Redemptions are subject to a two-year holding period from the underlying fund’s initial capital call on May 31, 2019. |

| The accompanying notes are an integral part of these consolidated financial statements. | 11 |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Statement of Assets and Liabilities(a)

September 30, 2020

| ||||||

| Assets: |

| |||||

Investments in unaffiliated issuers, at value (cost $273,210,779) | $ | 273,390,814 | ||||

Investments in affiliated issuers, at value (cost $9,993,327) | 9,993,327 | |||||

Cash | 388,460 | |||||

Receivables: | ||||||

Dividends | 4,763,889 | |||||

Fund shares sold | 75,828 | |||||

Investments sold | 45,804 | |||||

Other assets | 3,662 | |||||

| Total assets | 288,661,784 | |||||

| Liabilities: | ||||||

Payables: | ||||||

Management fees | 366,378 | |||||

Distribution and Service fees and Transfer Agency fees | 171,810 | |||||

Interest on borrowings | 17,139 | |||||

Accrued expenses | 293,646 | |||||

| Total liabilities | 848,973 | |||||

| Net Assets: | ||||||

Paid-in capital | 291,013,535 | |||||

Total distributable earnings (loss) | (3,200,724 | ) | ||||

| NET ASSETS | $ | 287,812,811 | ||||

Net Assets: | ||||||

Class A | $ | 87,520,363 | ||||

Class C | 72,825,564 | |||||

Class I | 74,219,760 | |||||

Class L | 5,538,228 | |||||

Class W | 47,708,896 | |||||

Total Net Assets | $ | 287,812,811 | ||||

Shares Outstanding $0.001 par value (unlimited number of shares authorized): | ||||||

Class A | 9,330,754 | |||||

Class C | 7,763,854 | |||||

Class I | 7,586,565 | |||||

Class L | 590,101 | |||||

Class W | 5,009,338 | |||||

Net asset value and offering price per share:(b) | ||||||

Class A | $9.38 | |||||

Class C | 9.38 | |||||

Class I | 9.78 | |||||

Class L | 9.39 | |||||

Class W | 9.52 | |||||

| (a) | Statement of Assets and Liabilities for the Fund is consolidated and includes the balances of wholly owned subsidiaries DIF Investments LLC and DIF Investments II LLC. Accordingly, all interfund balances and transactions have been eliminated. |

| (b) | Maximum public offering price per share for Class A Shares is $9.95 and for Class L is $9.81. Upon repurchase, Class C Shares may be subject to a contingent deferred sales charge, assessed on the amount equal to the lesser of the current net asset value (“NAV”) or the original purchase price of the shares. |

| 12 | The accompanying notes are an integral part of these consolidated financial statements. |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Statement of Operations(a)

For the Fiscal Year Ended September 30, 2020

| ||||||

| Investment income: |

| |||||

Dividends — unaffiliated issuers (net of foreign withholding taxes of $2,887) | $ | 16,522,346 | ||||

Interest — unaffiliated issuers | 34,148 | |||||

Dividends — affiliated issuers | 4,809 | |||||

| Total investment income | 16,561,303 | |||||

| Expenses: |

| |||||

Management fees | 4,067,224 | |||||

Distribution Service fees(b) | 804,674 | |||||

Interest on borrowing | 637,973 | |||||

Custody, accounting and administrative services | 406,599 | |||||

Transfer Agency fees | 524,541 | |||||

Shareholder Services fees(b) | 413,466 | |||||

Professional fees | 283,026 | |||||

Printing and mailing costs | 200,213 | |||||

Compliance fees | 132,927 | |||||

Registration fees | 109,993 | |||||

Trustee fees | 99,349 | |||||

Other | 131,647 | |||||

| Total expenses | 7,811,632 | |||||

Less — expense reductions | (6,892 | ) | ||||

Less — fees waived by investment adviser | (300,041 | ) | ||||

Recoupment of previously waived fees | 40,517 | |||||

| Net expenses | 7,545,216 | |||||

| NET INVESTMENT INCOME | 9,016,087 | |||||

| Realized and unrealized gain (loss): |

| |||||

Net realized gain (loss) from: | ||||||

Investments — unaffiliated issuers | 44,679 | |||||

Purchased options | (2,083,273 | ) | ||||

Written options | (325,501 | ) | ||||

Net change in unrealized gain (loss) on: | ||||||

Investments — unaffiliated issuers | (27,659,390 | ) | ||||

Purchased options | 136,900 | |||||

Written options | 247,584 | |||||

| Net realized and unrealized loss | (29,639,001 | ) | ||||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (20,622,914 | ) | |||

| (a) | Statement of Operations for the Fund is consolidated and includes the balances of wholly owned subsidiaries DIF Investments LLC and DIF Investments II LLC. Accordingly, all interfund balances and transactions have been eliminated. |

| (b) | Class specific Distribution Service and Shareholder Services fees were as follows: |

| Distribution Service Fees | Shareholder Services fees | |||||||||||||||||||||||||||||||||||||||||||||||||

Class A | Class C | Class W | Class L | Class T | Class D | Class A | Class C | Class W | Class L | Class T | Class U | Class D | ||||||||||||||||||||||||||||||||||||||

| $ | 119,137 | $ | 578,113 | $ | 72,716 | $ | 17,306 | $ | 10,949 | $ | 6,453 | $ | 119,137 | $ | 192,704 | $ | 72,716 | $ | 17,306 | $ | 3,650 | $ | 4,726 | $ | 3,227 | |||||||||||||||||||||||||

| The accompanying notes are an integral part of these consolidated financial statements. | 13 |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Statements of Changes in Net Assets(a)

| For the Fiscal Year Ended September 30, 2020 | For the Fiscal Year Ended September 30, 2019 | |||||||||

| From operations: |

| |||||||||

Net investment income | $ | 9,016,087 | $ | 11,154,521 | ||||||

Net realized gain (loss) | (2,364,095 | ) | 7,880,053 | |||||||

Net change in unrealized gain (loss) | (27,274,906 | ) | 5,488,048 | |||||||

| Net increase (decrease) in net assets resulting from operations | (20,622,914 | ) | 24,522,622 | |||||||

| Distributions to shareholders: | ||||||||||

Total distributable earnings: | ||||||||||

Class A Shares | (5,429,382 | ) | (3,994,204 | ) | ||||||

Class C Shares | (3,663,199 | ) | (2,618,689 | ) | ||||||

Class I Shares | (4,472,302 | ) | (1,835,557 | ) | ||||||

Class L Shares | (283,683 | ) | (330,150 | ) | ||||||

Class W Shares | (3,165,247 | ) | (3,730,424 | ) | ||||||

Class U Shares(b) | (62 | ) | (445,458 | ) | ||||||

Class T Shares(c) | (327 | ) | (248,861 | ) | ||||||

Class D Shares(c) | (787 | ) | (255,121 | ) | ||||||

From return of capital: | ||||||||||

Class A Shares | (1,741,207 | ) | (1,153,777 | ) | ||||||

Class C Shares | (1,378,419 | ) | (747,260 | ) | ||||||

Class I Shares | (1,278,114 | ) | (519,261 | ) | ||||||

Class L Shares | (122,826 | ) | (93,724 | ) | ||||||

Class W Shares | (1,167,461 | ) | (1,104,767 | ) | ||||||

Class U Shares(b) | — | (133,691 | ) | |||||||

Class T Shares(c) | — | (78,236 | ) | |||||||

Class D Shares(c) | — | (73,525 | ) | |||||||

| Total distributions to shareholders | (22,703,016 | ) | (17,362,705 | ) | ||||||

| From share transactions: | ||||||||||

Proceeds from sales of shares | 96,310,426 | 87,178,408 | ||||||||

Reinvestment of distributions | 10,456,342 | 9,167,702 | ||||||||

Cost of shares repurchased | (126,528,978 | ) | (22,395,901 | ) | ||||||

Net transferred between share classes | — | * | 482,114 | |||||||

| Net increase (decrease) in net assets resulting from share transactions | (19,762,210 | ) | 74,432,323 | |||||||

| TOTAL INCREASE (DECREASE) | (63,088,140 | ) | 81,592,240 | |||||||

| Net assets: | ||||||||||

Beginning of year | 350,900,951 | 269,308,711 | ||||||||

End of year | $ | 287,812,811 | $ | 350,900,951 | ||||||

| (a) | Statements of Changes in Net Assets for the Fund is consolidated and includes the balances of wholly owned subsidiaries DIF Investments LLC and DIF Investments II LLC. Accordingly, all interfund balances and transactions have been eliminated. |

| (b) | Effective as of January 15, 2020, the Fund terminated operations of its Class U Shares. |

| (c) | Effective as of February 3, 2020, the Fund terminated operations of its Class D and Class T shares. |

| * | For the fiscal year ended September 30, 2020, the fund recognized transfers between share classes as shares sold and shares repurchased. |

| 14 | The accompanying notes are an integral part of these consolidated financial statements. |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Statement of Cash Flows(a)

For the Fiscal Year Ended September 30, 2020

| ||||||

Increase/(Decrease) in cash – Cash flows provided by operating activities:(b) | ||||||

Net decrease in net assets resulting from operations | $ | (20,622,914 | ) | |||

Adjustments to reconcile net increase in net assets from operations to net cash provided by/(used in) operating activities: | ||||||

Payments for purchases of investments | (188,610,161 | ) | ||||

Proceeds from sales of investments | 284,889,906 | |||||

Payment for purchases of option contracts | (972,335 | ) | ||||

Proceeds from sale of option contracts | 107,722 | |||||

Premiums received from written options transactions | 936,738 | |||||

Premiums paid from closing written options transactions | (2,878,406 | ) | ||||

Net (purchase) proceeds from short-term investment securities | (7,777,999 | ) | ||||

Accretion of discount on investments | 26 | |||||

(Increase) Decrease in Assets: | ||||||

Receivable for dividends | (1,240,716 | ) | ||||

Other assets | 25,985 | |||||

Increase (Decrease) in Liabilities: | ||||||

Interest on borrowings | (143,036 | ) | ||||

Management fees | 25,917 | |||||

Distribution and Service fees and Transfer Agency fees | 2,936 | |||||

Accrued expenses | 13,718 | |||||

Net realized (gain) loss on: | ||||||

Investments | (44,679 | ) | ||||

Purchased options | 2,083,273 | |||||

Written options | 325,501 | |||||

Net change in unrealized (gain) loss on: | ||||||

Investments | 27,659,390 | |||||

Purchased options | (136,900 | ) | ||||

Written options | (247,584 | ) | ||||

| Net cash provided by operating activities | 93,396,382 | |||||

| Cash flows provided by financing activities: | ||||||

Repayment of borrowing facility | (43,482,332 | ) | ||||

Proceeds from sale of shares | 36,241,192 | |||||

Cost of shares repurchased | (72,077,693 | ) | ||||

Decrease in payable to custodian | (1,555,642 | ) | ||||

Distributions paid | (12,246,674 | ) | ||||

| Net cash used in financing activities | (93,121,149 | ) | ||||

| NET INCREASE IN CASH | $ | 275,233 | ||||

| Cash (restricted and unrestricted): | ||||||

Beginning of year | $ | 113,227 | ||||

End of year | $ | 388,460 | ||||

Supplemental disclosure: | ||||||

Cash paid for interest and related fees | 732,273 | |||||

Transfers of shares in from other share classes | 54,451,285 | |||||

Transfers of shares out of other share classes | (54,451,285 | ) | ||||

Reinvestment of distributions | 10,456,342 | |||||

| (a) | Statement of Cash Flows for the Fund is consolidated and includes the balances of wholly owned subsidiaries DIF Investments LLC and DIF Investments II LLC. Accordingly, all interfund balances and transactions have been eliminated. |

| (b) | Certain line items in the Increase/Decrease in operating assets and liabilities section of the consolidated statement of cash flows are presented based on the classifications in the September 30, 2020 consolidated statement of assets and liabilities which have been updated from the September 30, 2019 presentation. The classification changes had no impact on total assets, total liabilities, or net assets. |

| The accompanying notes are an integral part of these consolidated financial statements. | 15 |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Financial Highlights

Selected Share Data for a Share Outstanding Throughout Each Year

| Goldman Sachs Real Estate Diversified Income Fund | ||||||||||||||||||||||

| Class A Shares | ||||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data | ||||||||||||||||||||||

Net asset value, beginning of year | $ | 10.69 | $ | 10.47 | $ | 10.19 | $ | 10.26 | $ | 9.81 | ||||||||||||

Net investment income(a) | 0.29 | 0.40 | 0.30 | 0.39 | 0.34 | |||||||||||||||||

Net realized and unrealized gain (loss) | (0.89 | ) | 0.42 | 0.58 | 0.17 | 0.71 | ||||||||||||||||

Total from investment operations | (0.60 | ) | 0.82 | 0.88 | 0.56 | 1.05 | ||||||||||||||||

Distributions to shareholders from net investment income | (0.23 | ) | (0.26 | ) | (0.24 | ) | (0.31 | ) | (0.32 | ) | ||||||||||||

Distributions to shareholders from net realized gains | (0.30 | ) | (0.21 | ) | (0.15 | ) | (0.12 | ) | — | |||||||||||||

Distributions to shareholders from return of capital | (0.18 | ) | (0.13 | ) | (0.21 | ) | (0.20 | ) | (0.28 | ) | ||||||||||||

Total distributions | (0.71 | ) | (0.60 | ) | (0.60 | ) | (0.63 | ) | (0.60 | ) | ||||||||||||

Net asset value, end of year | $ | 9.38 | $ | 10.69 | $ | 10.47 | $ | 10.19 | $ | 10.26 | ||||||||||||

| Total Return(b) | (5.20 | )% | 8.17 | % | 9.00 | % | 5.67 | % | 11.09 | % | ||||||||||||

Net assets, end of year (in 000’s) | $ | 87,520 | $ | 96,114 | $ | 86,965 | $ | 84,231 | $ | 61,470 | ||||||||||||

Ratio of net expenses to average net assets before interest expense | 1.99 | % | 1.99 | % | 1.99 | % | 1.99 | % | 1.99 | % | ||||||||||||

Ratio of net expenses to average net assets after interest expense | 2.19 | % | 2.83 | % | 2.76 | % | 2.69 | % | 2.39 | % | ||||||||||||

Ratio of total expenses to average net assets after interest expense | 2.28 | % | 2.90 | % | 2.97 | % | 2.90 | % | 2.78 | % | ||||||||||||

Ratio of net investment income to average net assets | 2.88 | % | 3.83 | % | 2.97 | % | 3.81 | % | 3.47 | % | ||||||||||||

Portfolio turnover rate(c) | 53 | % | 65 | % | 78 | % | 11 | % | 21 | % | ||||||||||||

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete repurchase of the investment at the NAV at the end of the year and no sales or repurchase charges (if any). Total returns would be reduced if a sales or repurchase charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the repurchase of Fund shares. |

| (c) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| 16 | The accompanying notes are an integral part of these consolidated financial statements. |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout Each Year

| Goldman Sachs Real Estate Diversified Income Fund | ||||||||||||||||||||||

| Class C Shares | ||||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data | ||||||||||||||||||||||

Net asset value, beginning of year | $ | 10.68 | $ | 10.47 | $ | 10.19 | $ | 10.25 | $ | 9.81 | ||||||||||||

Net investment income(a) | 0.20 | 0.32 | 0.23 | 0.32 | 0.28 | |||||||||||||||||

Net realized and unrealized gain (loss) | (0.87 | ) | 0.41 | 0.57 | 0.18 | 0.68 | ||||||||||||||||

Total from investment operations | (0.67 | ) | 0.73 | 0.80 | 0.50 | 0.96 | ||||||||||||||||

Distributions to shareholders from net investment income | (0.16 | ) | (0.22 | ) | (0.20 | ) | (0.27 | ) | (0.27 | ) | ||||||||||||

Distributions to shareholders from net realized gains | (0.29 | ) | (0.18 | ) | (0.14 | ) | (0.12 | ) | — | |||||||||||||

Distributions to shareholders from return of capital | (0.18 | ) | (0.12 | ) | (0.18 | ) | (0.17 | ) | (0.25 | ) | ||||||||||||

Total distributions | (0.63 | ) | (0.52 | ) | (0.52 | ) | (0.56 | ) | (0.52 | ) | ||||||||||||

Net asset value, end of year | $ | 9.38 | $ | 10.68 | $ | 10.47 | $ | 10.19 | $ | 10.25 | ||||||||||||

| Total Return(b) | (5.94 | )% | 7.24 | % | 8.17 | % | 4.97 | % | 10.15 | % | ||||||||||||

Net assets, end of year (in 000’s) | $ | 72,826 | $ | 74,609 | $ | 62,367 | $ | 57,559 | $ | 33,114 | ||||||||||||

Ratio of net expenses to average net assets before interest expense | 2.74 | % | 2.74 | % | 2.74 | % | 2.74 | % | 2.74 | % | ||||||||||||

Ratio of net expenses to average net assets after interest expense | 2.94 | % | 3.58 | % | 3.51 | % | 3.47 | % | 3.14 | % | ||||||||||||

Ratio of total expenses to average net assets after interest expense | 3.04 | % | 3.64 | % | 3.73 | % | 3.71 | % | 3.53 | % | ||||||||||||

Ratio of net investment income to average net assets | 2.04 | % | 3.08 | % | 2.24 | % | 3.11 | % | 2.87 | % | ||||||||||||

Portfolio turnover rate(c) | 53 | % | 65 | % | 78 | % | 11 | % | 21 | % | ||||||||||||

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete repurchase of the investment at the NAV at the end of the year and no sales or repurchase charges (if any). Total returns would be reduced if a sales or repurchase charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the repurchase of Fund shares. |

| (c) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| The accompanying notes are an integral part of these consolidated financial statements. | 17 |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout Each Year

| Goldman Sachs Real Estate Diversified Income Fund | ||||||||||||||||||||||

| Class I Shares | ||||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data | ||||||||||||||||||||||

Net asset value, beginning of year | $ | 11.13 | $ | 10.91 | $ | 10.62 | $ | 10.74 | $ | 10.36 | ||||||||||||

Net investment income(a) | 0.33 | 0.45 | 0.36 | 0.48 | 0.04 | |||||||||||||||||

Net realized and unrealized gain (loss) | (0.93 | ) | 0.42 | 0.59 | 0.09 | 0.97 | ||||||||||||||||

Total from investment operations | (0.60 | ) | 0.87 | 0.95 | 0.57 | 1.01 | ||||||||||||||||

Distributions to shareholders from net investment income | (0.26 | ) | (0.27 | ) | (0.26 | ) | (0.34 | ) | (0.33 | ) | ||||||||||||

Distributions to shareholders from net realized gains | (0.31 | ) | (0.23 | ) | (0.16 | ) | (0.12 | ) | — | |||||||||||||

Distributions to shareholders from return of capital | (0.18 | ) | (0.15 | ) | (0.24 | ) | (0.23 | ) | (0.30 | ) | ||||||||||||

Total distributions | (0.75 | ) | (0.65 | ) | (0.66 | ) | (0.69 | ) | (0.63 | ) | ||||||||||||

Net asset value, end of year | $ | 9.78 | $ | 11.13 | $ | 10.91 | $ | 10.62 | $ | 10.74 | ||||||||||||

| Total Return(b) | (5.05 | )% | 8.35 | % | 9.25 | % | 5.45 | % | 10.12 | % | ||||||||||||

Net assets, end of year (in 000’s) | $ | 74,220 | $ | 55,138 | $ | 22,273 | $ | 8,385 | $ | 0 | (c) | |||||||||||

Ratio of net expenses to average net assets before interest expense | 1.74 | % | 1.74 | % | 1.74 | % | 1.74 | % | 1.74 | % | ||||||||||||

Ratio of net expenses to average net assets after interest expense | 1.94 | % | 2.63 | % | 2.49 | % | 2.56 | % | 2.14 | % | ||||||||||||

Ratio of total expenses to average net assets after interest expense | 2.03 | % | 2.68 | % | 2.75 | % | 3.23 | % | 2.49 | % | ||||||||||||

Ratio of net investment income to average net assets | 3.16 | % | 4.10 | % | 3.35 | % | 4.48 | % | 0.36 | % | ||||||||||||

Portfolio turnover rate(d) | 53 | % | 65 | % | 78 | % | 11 | % | 21 | % | ||||||||||||

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete repurchase of the investment at the NAV at the end of the year and no sales or repurchase charges (if any). Total returns would be reduced if a sales or repurchase charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the repurchase of Fund shares. |

| (c) | Amount less than $500. |

| (d) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| 18 | The accompanying notes are an integral part of these consolidated financial statements. |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout Each Year

| Goldman Sachs Real Estate Diversified Income Fund | ||||||||||||||||||

| Class L Shares | ||||||||||||||||||

| Year Ended September 30, | Period Ended September 30, 2017(a) | |||||||||||||||||

| 2020 | 2019 | 2018 | ||||||||||||||||

| Per Share Data | ||||||||||||||||||

Net asset value, beginning of period | $ | 10.69 | $ | 10.48 | $ | 10.20 | $ | 10.22 | ||||||||||

Net investment income(b) | 0.27 | 0.38 | 0.30 | 0.26 | ||||||||||||||

Net realized and unrealized gain (loss) | (0.89 | ) | 0.40 | 0.55 | (0.14 | )(c) | ||||||||||||

Total from investment operations | (0.62 | ) | 0.78 | 0.85 | 0.12 | |||||||||||||

Distributions to shareholders from net investment income | (0.20 | ) | (0.24 | ) | (0.22 | ) | (0.05 | ) | ||||||||||

Distributions to shareholders from net realized gains | (0.30 | ) | (0.20 | ) | (0.15 | ) | (0.02 | ) | ||||||||||

Distributions to shareholders from return of capital | (0.18 | ) | (0.13 | ) | (0.20 | ) | (0.07 | ) | ||||||||||

Total distributions | (0.68 | ) | (0.57 | ) | (0.57 | ) | (0.14 | ) | ||||||||||

Net asset value, end of period | $ | 9.39 | $ | 10.69 | $ | 10.48 | $ | 10.20 | ||||||||||

| Total Return(d) | (5.46 | )% | 7.79 | % | 8.72 | % | 1.22 | % | ||||||||||

Net assets, end of period (in 000’s) | $ | 5,538 | $ | 10,402 | $ | 4,613 | $ | 836 | ||||||||||

Ratio of net expenses to average net assets before interest expense | 2.24 | % | 2.24 | % | 2.24 | % | 2.24 | %(e) | ||||||||||

Ratio of net expenses to average net assets after interest expense | 2.44 | % | 3.13 | % | 2.99 | % | 3.07 | %(e) | ||||||||||

Ratio of total expenses to average net assets after interest expense | 2.54 | % | 3.17 | % | 3.22 | % | 3.83 | %(e) | ||||||||||

Ratio of net investment income to average net assets | 2.71 | % | 3.60 | % | 2.91 | % | 11.62 | %(e) | ||||||||||

Portfolio turnover rate(f) | 53 | % | 65 | % | 78 | % | 11 | % | ||||||||||

| (a) | The Fund’s Class L Shares commenced operations on July 10, 2017. |

| (b) | Calculated based on the average shares outstanding methodology. |

| (c) | Realized and unrealized losses per share do not correlate to the aggregate of the net realized and unrealized gains on the Statement of Operations for the period ended September 30, 2017, primarily due to the timing of sales and repurchases of the Fund’s shares in relation to fluctuating market values for the Fund’s portfolio. |

| (d) | Assumes investment at the NAV at the beginning of the period, reinvestment of all dividends and distributions, a complete repurchase of the investment at the NAV at the end of the period and no sales or repurchase charges (if any). Total returns would be reduced if a sales or repurchase charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the repurchase of Fund shares. Total returns for periods less than one full year are not annualized. |

| (e) | Annualized. |

| (f) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| The accompanying notes are an integral part of these consolidated financial statements. | 19 |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Financial Highlights (continued)

Selected Share Data for a Share Outstanding Throughout Each Year

| Goldman Sachs Real Estate Diversified Income Fund | ||||||||||||||||||||||

| Class W Shares | ||||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||||

| Per Share Data | ||||||||||||||||||||||

Net asset value, beginning of year | $ | 10.85 | $ | 10.63 | $ | 10.35 | $ | 10.41 | $ | 9.96 | ||||||||||||

Net investment income(a) | 0.31 | 0.41 | 0.31 | 0.39 | 0.32 | |||||||||||||||||

Net realized and unrealized gain (loss) | (0.92 | ) | 0.42 | 0.58 | 0.17 | 0.69 | ||||||||||||||||

Total from investment operations | (0.61 | ) | 0.83 | 0.89 | 0.56 | 1.01 | ||||||||||||||||

Distributions to shareholders from net investment income | (0.24 | ) | (0.26 | ) | (0.23 | ) | (0.30 | ) | (0.30 | ) | ||||||||||||

Distributions to shareholders from net realized gains | (0.30 | ) | (0.21 | ) | (0.16 | ) | (0.12 | ) | — | |||||||||||||

Distributions to shareholders from return of capital | (0.18 | ) | (0.14 | ) | (0.22 | ) | (0.20 | ) | (0.26 | ) | ||||||||||||

Total distributions | (0.72 | ) | (0.61 | ) | (0.61 | ) | (0.62 | ) | (0.56 | ) | ||||||||||||

Net asset value, end of year | $ | 9.52 | $ | 10.85 | $ | 10.63 | $ | 10.35 | $ | 10.41 | ||||||||||||

| Total Return(b) | (5.31 | )% | 8.13 | % | 8.95 | % | 5.64 | % | 10.46 | % | ||||||||||||

Net assets, end of year (in 000’s) | $ | 47,709 | $ | 92,006 | $ | 69,400 | $ | 56,427 | $ | 31,076 | ||||||||||||

Ratio of net expenses to average net assets before interest expense | 1.99 | % | 1.99 | % | 1.99 | % | 2.09 | %(c) | 2.49 | % | ||||||||||||

Ratio of net expenses to average net assets after interest expense | 2.19 | % | 2.84 | % | 2.76 | % | 2.83 | % | 2.89 | % | ||||||||||||

Ratio of total expenses to average net assets after interest expense | 2.23 | % | 2.88 | % | 2.96 | % | 3.06 | % | 3.30 | % | ||||||||||||

Ratio of net investment income to average net assets | 2.99 | % | 3.85 | % | 3.01 | % | 3.79 | % | 3.17 | % | ||||||||||||

Portfolio turnover rate(d) | 53 | % | 65 | % | 78 | % | 11 | % | 21 | % | ||||||||||||

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete repurchase of the investment at the NAV at the end of the year and no sales or repurchase charges (if any). Total returns would be reduced if a sales or repurchase charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the repurchase of Fund shares. |

| (c) | Effective January 5, 2017, the annual expense limitation changed from 2.49% to 1.99%. |

| (d) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| 20 | The accompanying notes are an integral part of these consolidated financial statements. |

GOLDMAN SACHS REAL ESTATE DIVERSIFIED INCOME FUND

Consolidated Notes to Financial Statements

September 30, 2020

| 1 . ORGANIZATION |

Goldman Sachs Real Estate Diversified Income Fund (the “Fund”), is a Delaware statutory trust registered under the Investment Company Act of 1940 (the “Act”), as amended, as a diversified, closed-end management investment company and is structured as an “interval fund,” a type of fund which, in order to provide some liquidity to shareholders, makes quarterly offers to repurchase a percentage of its outstanding shares at NAV, pursuant to Rule 23c-3 under the Act. The Fund was organized as a Delaware statutory trust on December 2, 2019. The Fund offers five classes of shares: Class A, Class C, Class I, Class L, and Class W.

Class A and Class L Shares are sold with front-end sales charges of up to 5.75% and 4.25%, respectively. Class A and Class C Shares are sold with contingent deferred sales charges (“CDSC”) of 0.50% and 1.00%, respectively, which are imposed on repurchases made within 12 months of purchase. Class I and Class W Shares are not subject to a sales charge.

Goldman Sachs Asset Management, L.P. (“GSAM”), an affiliate of Goldman Sachs & Co. LLC, serves as investment adviser to the Fund pursuant to a management agreement (the “Agreement”) with the Fund.

Pursuant to an Agreement and Plan of Reorganization (the “Reorganization Agreement”) approved by the Fund’s Board of Trustees, all of the assets of the Resource Real Estate Diversified Income Fund (“Predecessor Fund”) were transferred to the Fund in exchange for the assumption of the Predecessor Fund’s stated liabilities by the Fund and shares of beneficial interest of the Fund as of the close of business on May 15, 2020 (the “Reorganization”). Holders of Class A, Class C, Class I, Class L, and Class W Shares of the Predecessor Fund received Class A, Class C, Class I, Class L, and Class W Shares of the Fund. The exchange was a tax-free event to shareholders. The Predecessor Fund was the accounting survivor in the Reorganization, and, as such, the financial statements and financial highlights reflect the financial information of the Predecessor Fund through May 15, 2020. Class D, Class T and Class U Shares of the Predecessor Fund were liquidated prior to the Reorganization.

| 2. SIGNIFICANT ACCOUNTING POLICIES |

The financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) and require management to make estimates and assumptions that may affect the reported amounts and disclosures. Actual results may differ from those estimates and assumptions. The Fund is an investment company under GAAP and follows the accounting and reporting guidance applicable to investment companies.