Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

Filing tables

Filing exhibits

Associated filings

- 28 Apr 23 SC 13G Trean Insurance / Percy Rockdale ownership change

- 21 Apr 23 SC 13E3/A Going private transaction (amended)

- 12 Apr 23 SC 13E3/A Going private transaction (amended)

- 16 Mar 23 SC 13E3/A Going private transaction (amended)

- 14 Feb 23 SC 13G/A Trean Insurance / Baker Blake ownership change

- 13 Feb 23 SC 13G/A Trean Insurance / Altaris Partners ownership change

- 27 Jan 23 SC 13G/A Trean Insurance / ROYCE & ASSOCIATES ownership change

-

19 Jan 23 SC 13E3 Going private transaction

- 2 Feb 22 SC 13G/A Trean Insurance / Baker Blake ownership change

- 25 Jan 22 SC 13G Trean Insurance / ROYCE & ASSOCIATES ownership change

- 14 Jan 22 SC 13G/A Trean Insurance / Altaris Partners ownership change

- 24 Mar 21 SC 13G Trean Insurance / Baker Blake ownership change

- 14 Jan 21 SC 13G/A Trean Insurance / Altaris Partners ownership change

- 11 Aug 20 SC 13G Trean Insurance / Altaris Partners ownership change

TIG similar filings

Filing view

External links

Exhibit (c)(2)

Project Twins DISCUSSION MATERIALS FOR THE SPECIAL COMMITTEE OF THE BOARD OF DIRECT ORS DECEMBER 15, 2022 | CONFIDENTIAL

CONFIDENTIAL Table of Contents 2 Page 3 5 10 20 21 23 30 33 Executive Summary Selected Updates Since Prior Discussion Materials Financial Analyses Appendices Selected Cost of Equity Considerations Supplemental Financial Information Illustrative Selected Company Multiple Trendlines Supplemental Public Company & Market Observations

Page 1. Executive Summary 3 Selected Updates Since Prior Discussion Materials Financial Analyses Appendices 5 10 20

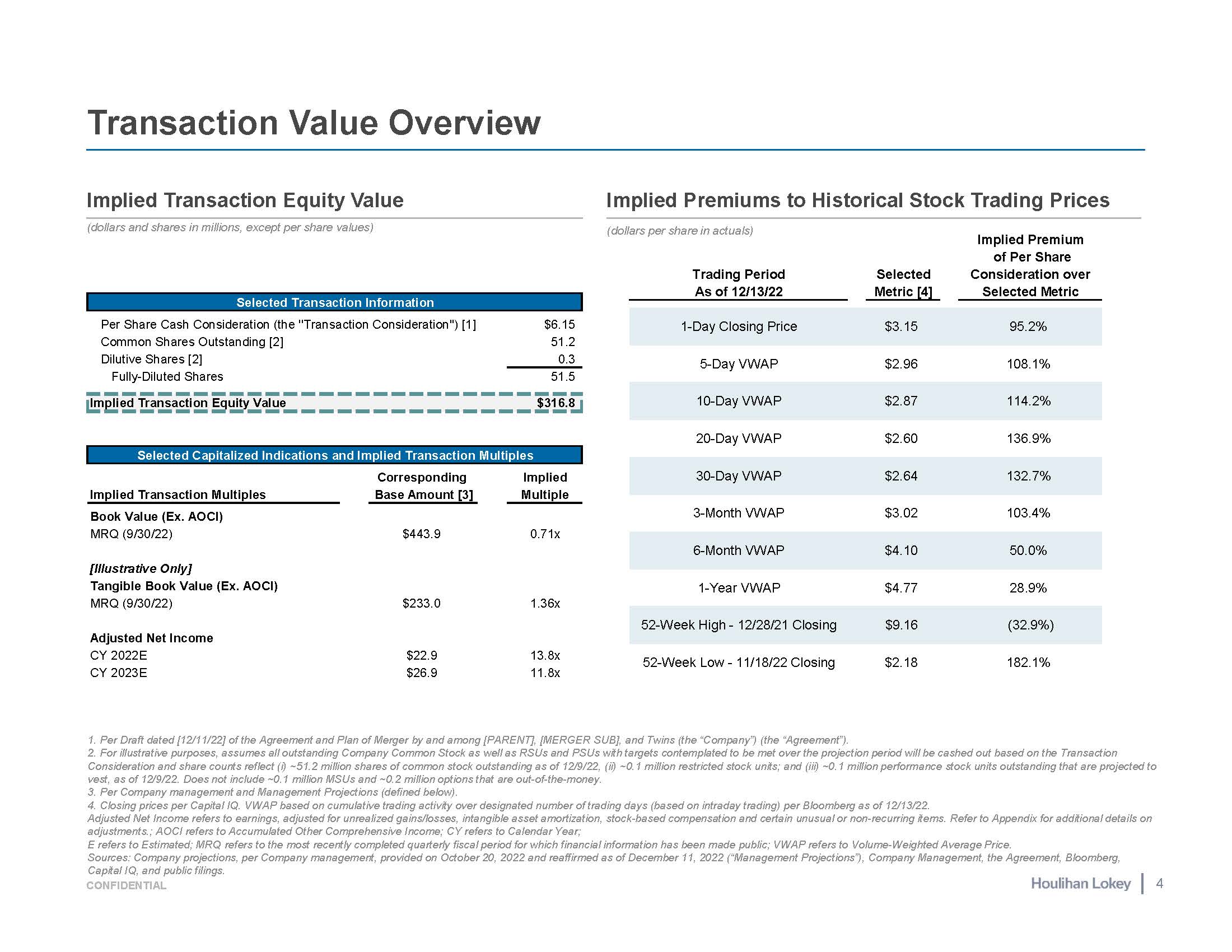

Transaction Value Overview Per Draft dated [12/11/22] of the Agreement and Plan of Merger by and among [PARENT], [MERGER SUB], and Twins (the “Company”) (the “Agreement”). For illustrative purposes, assumes all outstanding Company Common Stock as well as RSUs and PSUs with targets contemplated to be met over the projection period will be cashed out based on the Transaction Consideration and share counts reflect (i) ~51.2 million shares of common stock outstanding as of 12/9/22, (ii) ~0.1 million restricted stock units; and (iii) ~0.1 million performance stock units outstanding that are projected to vest, as of 12/9/22. Does not include ~0.1 million MSUs and ~0.2 million options that are out-of-the-money. Per Company management and Management Projections (defined below). Closing prices per Capital IQ. VWAP based on cumulative trading activity over designated number of trading days (based on intraday trading) per Bloomberg as of 12/13/22. Adjusted Net Income refers to earnings, adjusted for unrealized gains/losses, intangible asset amortization, stock-based compensation and certain unusual or non-recurring items. Refer to Appendix for additional details on adjustments.; AOCI refers to Accumulated Other Comprehensive Income; CY refers to Calendar Year; E refers to Estimated; MRQ refers to the most recently completed quarterly fiscal period for which financial information has been made public; VWAP refers to Volume-Weighted Average Price. Sources: Company projections, per Company management, provided on October 20, 2022 and reaffirmed as of December 11, 2022 (“Management Projections”), Company Management, the Agreement, Bloomberg, Capital IQ, and public filings. (dollars and shares in millions, except per share values) Implied Transaction Equity Value Implied Premiums to Historical Stock Trading Prices (dollars per share in actuals) Selected Transaction Information Per Share Cash Consideration (the ''Transaction Consideration'') [1] Common Shares Outstanding [2] Dilutive Shares [2] Fully-Diluted Shares $6.15 51.2 0.3 51.5 Implied Transaction Equity Value $316.8 Selected Capitalized Indications and Implied Transaction Multiples Corresponding Base Amount [3] Implied Multiple Implied Transaction Multiples Book Value (Ex. AOCI) MRQ (9/30/22) $443.9 0.71x [Illustrative Only] Tangible Book Value (Ex. AOCI) MRQ (9/30/22) $233.0 1.36x Adjusted Net Income CY 2022E $22.9 13.8x CY 2023E $26.9 11.8x Implied Premium of Per Share Consideration over Selected Metric 4 CONFIDENTIAL Trading Period As of 12/13/22 Selected Metric [4] 1-Day Closing Price $3.15 95.2% 5-Day VWAP $2.96 108.1% 10-Day VWAP $2.87 114.2% 20-Day VWAP $2.60 136.9% 30-Day VWAP $2.64 132.7% 3-Month VWAP $3.02 103.4% 6-Month VWAP $4.10 50.0% 1-Year VWAP $4.77 28.9% 52-Week High - 12/28/21 Closing $9.16 (32.9%) 52-Week Low - 11/18/22 Closing $2.18 182.1%

Page 3 1. Executive Summary 2. Selected Updates Since Prior Discussion Materials 5 Financial Analyses Appendices 10 20

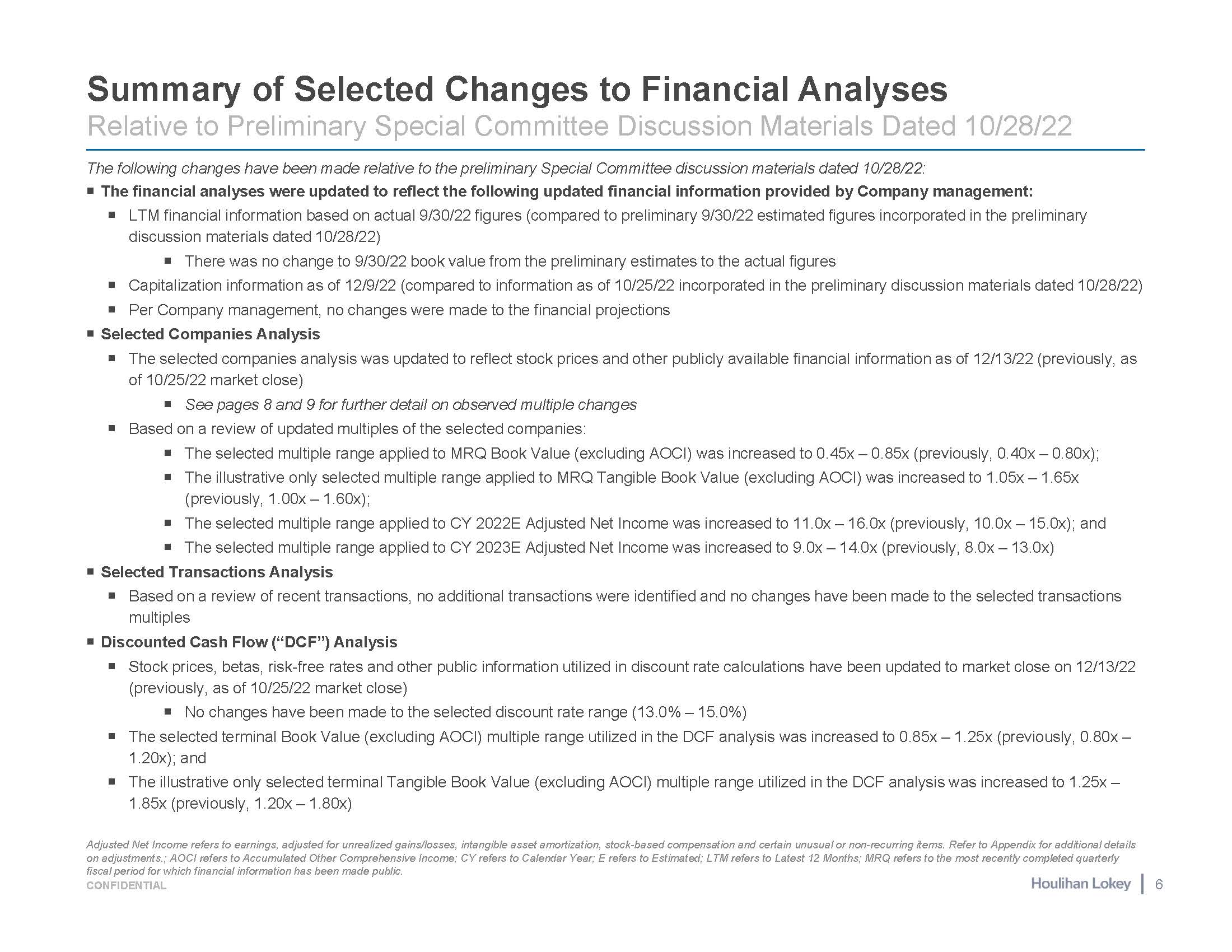

Summary of Selected Changes to Financial Analyses fiscal period for which financial information has been made public. CONFIDENTIAL 6 Relative to Preliminary Special Committee Discussion Materials Dated 10/28/22 The following changes have been made relative to the preliminary Special Committee discussion materials dated 10/28/22: The financial analyses were updated to reflect the following updated financial information provided by Company management: LTM financial information based on actual 9/30/22 figures (compared to preliminary 9/30/22 estimated figures incorporated in the preliminary discussion materials dated 10/28/22) There was no change to 9/30/22 book value from the preliminary estimates to the actual figures Capitalization information as of 12/9/22 (compared to information as of 10/25/22 incorporated in the preliminary discussion materials dated 10/28/22) Per Company management, no changes were made to the financial projections Selected Companies Analysis The selected companies analysis was updated to reflect stock prices and other publicly available financial information as of 12/13/22 (previously, as of 10/25/22 market close) See pages 8 and 9 for further detail on observed multiple changes Based on a review of updated multiples of the selected companies: The selected multiple range applied to MRQ Book Value (excluding AOCI) was increased to 0.45x – 0.85x (previously, 0.40x – 0.80x); The illustrative only selected multiple range applied to MRQ Tangible Book Value (excluding AOCI) was increased to 1.05x – 1.65x (previously, 1.00x – 1.60x); The selected multiple range applied to CY 2022E Adjusted Net Income was increased to 11.0x – 16.0x (previously, 10.0x – 15.0x); and The selected multiple range applied to CY 2023E Adjusted Net Income was increased to 9.0x – 14.0x (previously, 8.0x – 13.0x) Selected Transactions Analysis Based on a review of recent transactions, no additional transactions were identified and no changes have been made to the selected transactions multiples Discounted Cash Flow (“DCF”) Analysis Stock prices, betas, risk-free rates and other public information utilized in discount rate calculations have been updated to market close on 12/13/22 (previously, as of 10/25/22 market close) No changes have been made to the selected discount rate range (13.0% – 15.0%) The selected terminal Book Value (excluding AOCI) multiple range utilized in the DCF analysis was increased to 0.85x – 1.25x (previously, 0.80x – 1.20x); and The illustrative only selected terminal Tangible Book Value (excluding AOCI) multiple range utilized in the DCF analysis was increased to 1.25x – 1.85x (previously, 1.20x – 1.80x) Adjusted Net Income refers to earnings, adjusted for unrealized gains/losses, intangible asset amortization, stock-based compensation and certain unusual or non-recurring items. Refer to Appendix for additional details on adjustments.; AOCI refers to Accumulated Other Comprehensive Income; CY refers to Calendar Year; E refers to Estimated; LTM refers to Latest 12 Months; MRQ refers to the most recently completed quarterly

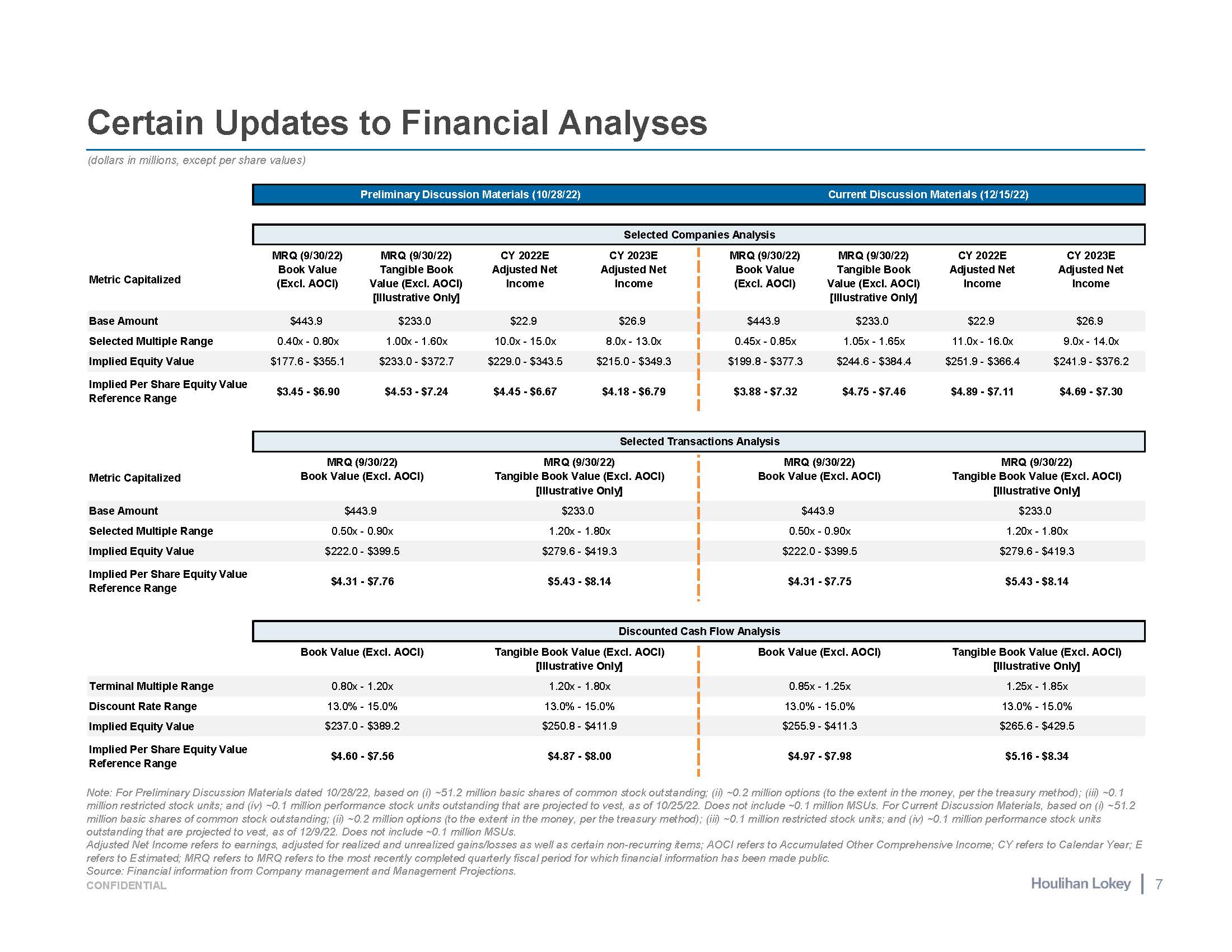

Certain Updates to Financial Analyses Note: For Preliminary Discussion Materials dated 10/28/22, based on (i) ~51.2 million basic shares of common stock outstanding; (ii) ~0.2 million options (to the extent in the money, per the treasury method); (iii) ~0.1 million restricted stock units; and (iv) ~0.1 million performance stock units outstanding that are projected to vest, as of 10/25/22. Does not include ~0.1 million MSUs. For Current Discussion Materials, based on (i) ~51.2 million basic shares of common stock outstanding; (ii) ~0.2 million options (to the extent in the money, per the treasury method); (iii) ~0.1 million restricted stock units; and (iv) ~0.1 million performance stock units outstanding that are projected to vest, as of 12/9/22. Does not include ~0.1 million MSUs. Adjusted Net Income refers to earnings, adjusted for realized and unrealized gains/losses as well as certain non-recurring items; AOCI refers to Accumulated Other Comprehensive Income; CY refers to Calendar Year; E refers to Estimated; MRQ refers to MRQ refers to the most recently completed quarterly fiscal period for which financial information has been made public. Source: Financial information from Company management and Management Projections. (dollars in millions, except per share values) Selected Companies Analysis Metric Capitalized MRQ (9/30/22) Book Value (Excl. AOCI) MRQ (9/30/22) Tangible Book Value (Excl. AOCI) [Illustrative Only] CY 2022E Adjusted Net Income CY 2023E Adjusted Net Income MRQ (9/30/22) Book Value (Excl. AOCI) MRQ (9/30/22) Tangible Book Value (Excl. AOCI) [Illustrative Only] CY 2022E Adjusted Net Income CY 2023E Adjusted Net Income Base Amount $443.9 $233.0 $22.9 $26.9 $443.9 $233.0 $22.9 $26.9 Selected Multiple Range 0.40x - 0.80x 1.00x - 1.60x 10.0x - 15.0x 8.0x - 13.0x 0.45x - 0.85x 1.05x - 1.65x 11.0x - 16.0x 9.0x - 14.0x Implied Equity Value $177.6 - $355.1 $233.0 - $372.7 $229.0 - $343.5 $215.0 - $349.3 $199.8 - $377.3 $244.6 - $384.4 $251.9 - $366.4 $241.9 - $376.2 Implied Per Share Equity Value Reference Range $3.45 - $6.90 $4.53 - $7.24 $4.45 - $6.67 $4.18 - $6.79 $3.88 - $7.32 $4.75 - $7.46 $4.89 - $7.11 $4.69 - $7.30 Selected Transactions Analysis Metric Capitalized MRQ (9/30/22) Book Value (Excl. AOCI) MRQ (9/30/22) Tangible Book Value (Excl. AOCI) [Illustrative Only] MRQ (9/30/22) Book Value (Excl. AOCI) MRQ (9/30/22) Tangible Book Value (Excl. AOCI) [Illustrative Only] Base Amount $443.9 $233.0 $443.9 $233.0 Selected Multiple Range 0.50x - 0.90x 1.20x - 1.80x 0.50x - 0.90x 1.20x - 1.80x Implied Equity Value $222.0 - $399.5 $279.6 - $419.3 $222.0 - $399.5 $279.6 - $419.3 Implied Per Share Equity Value Reference Range $4.31 - $7.76 $5.43 - $8.14 $4.31 - $7.75 $5.43 - $8.14 Discounted Cash Flow Analysis Book Value (Excl. AOCI) Tangible Book Value (Excl. AOCI) [Illustrative Only] Book Value (Excl. AOCI) Tangible Book Value (Excl. AOCI) [Illustrative Only] Terminal Multiple Range 0.80x - 1.20x 1.20x - 1.80x 0.85x - 1.25x 1.25x - 1.85x Discount Rate Range 13.0% - 15.0% 13.0% - 15.0% 13.0% - 15.0% 13.0% - 15.0% Implied Equity Value $237.0 - $389.2 $250.8 - $411.9 $255.9 - $411.3 $265.6 - $429.5 Implied Per Share Equity Value Reference Range $4.60 - $7.56 $4.87 - $8.00 $4.97 - $7.98 $5.16 - $8.34 Preliminary Discussion Materials (10/28/22) Current Discussion Materials (12/15/22) 7 CONFIDENTIAL

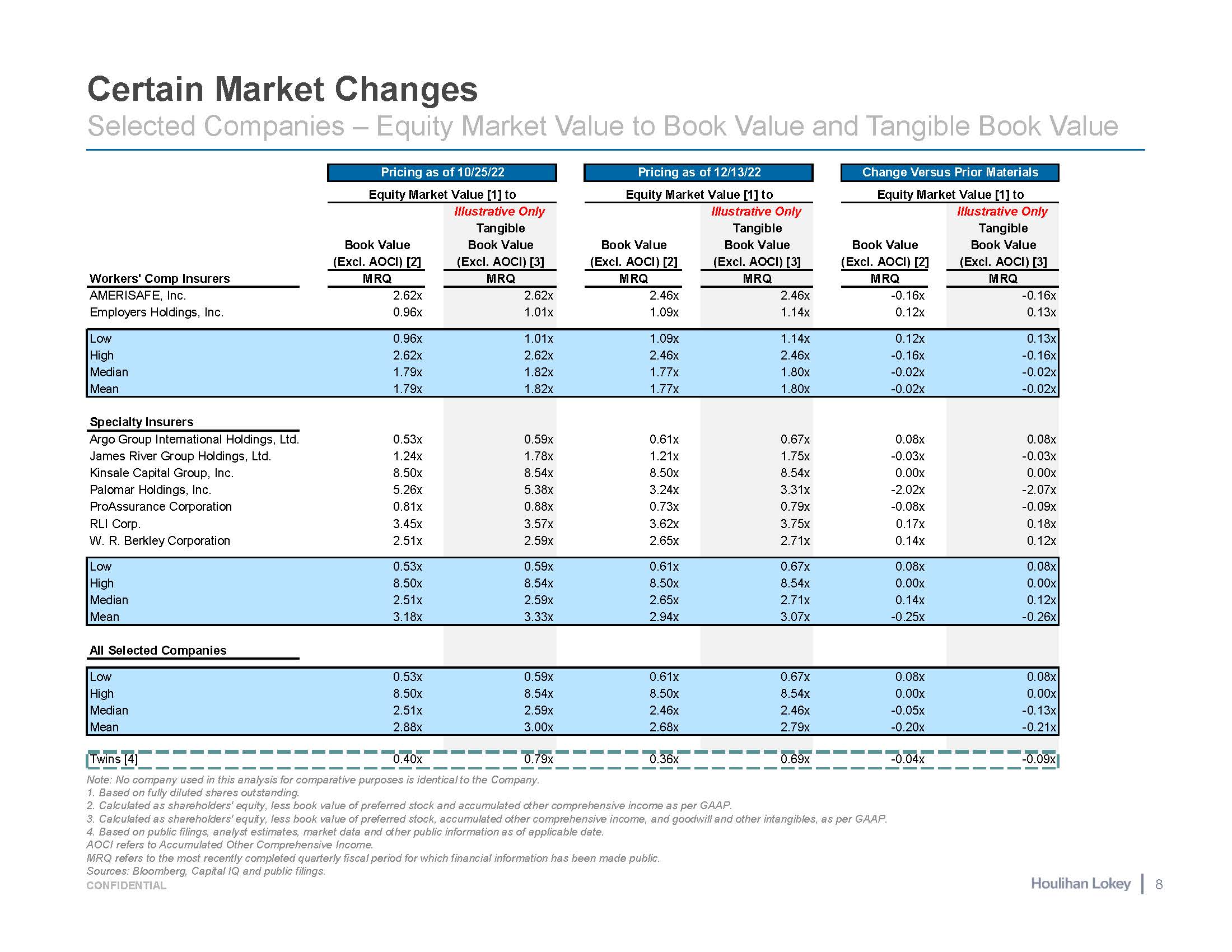

Certain Market Changes Selected Companies – Equity Market Value to Book Value and Tangible Book Value Note: No company used in this analysis for comparative purposes is identical to the Company. Based on fully diluted shares outstanding. Calculated as shareholders' equity, less book value of preferred stock and accumulated other comprehensive income as per GAAP. Calculated as shareholders' equity, less book value of preferred stock, accumulated other comprehensive income, and goodwill and other intangibles, as per GAAP. Based on public filings, analyst estimates, market data and other public information as of applicable date. AOCI refers to Accumulated Other Comprehensive Income. Pricing as of 10/25/22 Pricing as of 12/13/22 Change Versus Prior Materials Equity Market Value [1] to Equity Market Value [1] to Equity Market Value [1] to Workers' Comp Insurers AMERISAFE, Inc. Employers Holdings, Inc. Book Value (Excl. AOCI) [2] Illustrative Only Tangible Book Value (Excl. AOCI) [3] Book Value (Excl. AOCI) [2] MRQ 2.46x 1.09x Illustrative Only Tangible Book Value (Excl. AOCI) [3] Book Value (Excl. AOCI) [2] MRQ -0.16x 0.12x Illustrative Only Tangible Book Value (Excl. AOCI) [3] MRQ MRQ MRQ MRQ 2.62x 0.96x 2.62x 1.01x 2.46x 1.14x -0.16x 0.13x Low 0.96x 1.01x 1.09x 1.14x 0.12x 0.13x High 2.62x 2.62x 2.46x 2.46x -0.16x -0.16x Median 1.79x 1.82x 1.77x 1.80x -0.02x -0.02x Mean 1.79x 1.82x 1.77x 1.80x -0.02x -0.02x Specialty Insurers Argo Group International Holdings, Ltd. 0.53x 0.59x 0.61x 0.67x 0.08x 0.08x James River Group Holdings, Ltd. 1.24x 1.78x 1.21x 1.75x -0.03x -0.03x Kinsale Capital Group, Inc. 8.50x 8.54x 8.50x 8.54x 0.00x 0.00x Palomar Holdings, Inc. 5.26x 5.38x 3.24x 3.31x -2.02x -2.07x ProAssurance Corporation 0.81x 0.88x 0.73x 0.79x -0.08x -0.09x RLI Corp. 3.45x 3.57x 3.62x 3.75x 0.17x 0.18x W. R. Berkley Corporation 2.51x 2.59x 2.65x 2.71x 0.14x 0.12x Low 0.53x 0.59x 0.61x 0.67x 0.08x 0.08x High 8.50x 8.54x 8.50x 8.54x 0.00x 0.00x Median 2.51x 2.59x 2.65x 2.71x 0.14x 0.12x Mean 3.18x 3.33x 2.94x 3.07x -0.25x -0.26x All Selected Companies Low 0.53x 0.59x 0.61x 0.67x 0.08x 0.08x High 8.50x 8.54x 8.50x 8.54x 0.00x 0.00x Median 2.51x 2.59x 2.46x 2.46x -0.05x -0.13x Mean 2.88x 3.00x 2.68x 2.79x -0.20x -0.21x Twins [4] 0.40x 0.79x 0.36x 0.69x -0.04x -0.09x MRQ refers to the most recently completed quarterly fiscal period for which financial information has been made public. Sources: Bloomberg, Capital IQ and public filings. CONFIDENTIAL 8

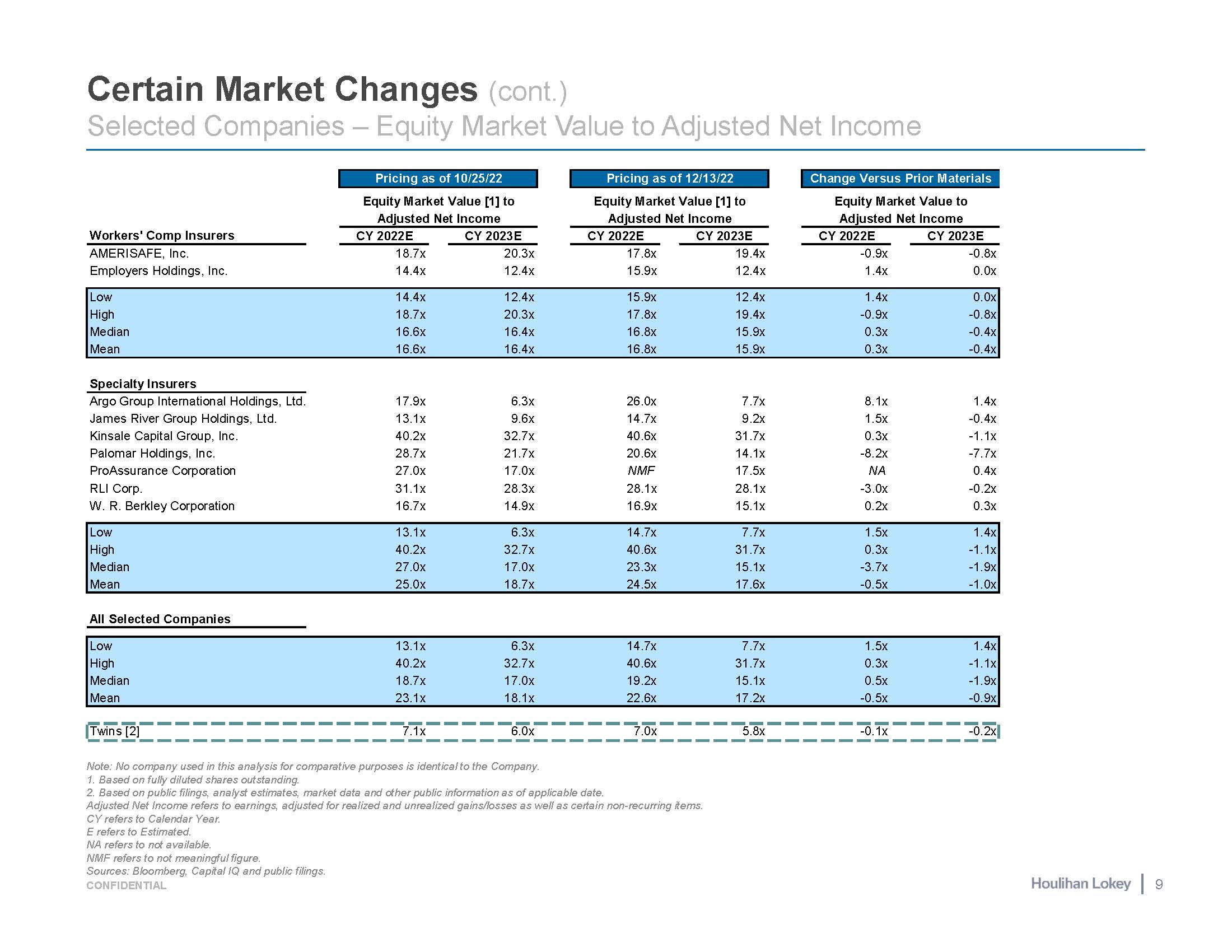

Certain Market Changes (cont.) Selected Companies – Equity Market Value to Adjusted Net Income Note: No company used in this analysis for comparative purposes is identical to the Company. Based on fully diluted shares outstanding. Based on public filings, analyst estimates, market data and other public information as of applicable date. Adjusted Net Income refers to earnings, adjusted for realized and unrealized gains/losses as well as certain non-recurring items. CY refers to Calendar Year. E refers to Estimated. NA refers to not available. Pricing as of 10/25/22 Pricing as of 12/13/22 Change Versus Prior Materials Workers' Comp Insurers Equity Market Value [1] to Adjusted Net Income CY 2022E CY 2023E Equity Market Value [1] to Adjusted Net Income CY 2022E CY 2023E Equity Market Value to Adjusted Net Income CY 2022E CY 2023E AMERISAFE, Inc. 18.7x 20.3x 17.8x 19.4x -0.9x -0.8x Employers Holdings, Inc. 14.4x 12.4x 15.9x 12.4x 1.4x 0.0x Low 14.4x 12.4x 15.9x 12.4x 1.4x 0.0x High 18.7x 20.3x 17.8x 19.4x -0.9x -0.8x Median 16.6x 16.4x 16.8x 15.9x 0.3x -0.4x Mean 16.6x 16.4x 16.8x 15.9x 0.3x -0.4x Specialty Insurers Argo Group International Holdings, Ltd. 17.9x 6.3x 26.0x 7.7x 8.1x 1.4x James River Group Holdings, Ltd. 13.1x 9.6x 14.7x 9.2x 1.5x -0.4x Kinsale Capital Group, Inc. 40.2x 32.7x 40.6x 31.7x 0.3x -1.1x Palomar Holdings, Inc. 28.7x 21.7x 20.6x 14.1x -8.2x -7.7x ProAssurance Corporation 27.0x 17.0x NMF 17.5x NA 0.4x RLI Corp. 31.1x 28.3x 28.1x 28.1x -3.0x -0.2x W. R. Berkley Corporation 16.7x 14.9x 16.9x 15.1x 0.2x 0.3x Low 13.1x 6.3x 14.7x 7.7x 1.5x 1.4x High 40.2x 32.7x 40.6x 31.7x 0.3x -1.1x Median 27.0x 17.0x 23.3x 15.1x -3.7x -1.9x Mean 25.0x 18.7x 24.5x 17.6x -0.5x -1.0x All Selected Companies Low 13.1x 6.3x 14.7x 7.7x 1.5x 1.4x High 40.2x 32.7x 40.6x 31.7x 0.3x -1.1x Median 18.7x 17.0x 19.2x 15.1x 0.5x -1.9x Mean 23.1x 18.1x 22.6x 17.2x -0.5x -0.9x Twins [2] 7.1x 6.0x 7.0x 5.8x -0.1x -0.2x NMF refers to not meaningful figure. Sources: Bloomberg, Capital IQ and public filings. CONFIDENTIAL 9

Page 3 5 Executive Summary Selected Updates Since Prior Discussion Materials 3. Financial Analyses 10 4. Appendices 20

Flow Analysis Selected Companies Analysis MRQ (9/30/22) Book Value (Excl. AOCI): $443.9 million Selected Multiple Range: 0.45x – 0.85x MRQ (9/30/22) Tangible Book Value (Excl. AOCI): $233.0 million Selected Multiple Range: 1.05x – 1.65x CY 2022E Adjusted Net Income: $22.9 million Selected Multiple Range: 11.0x – 16.0x CY 2023E Adjusted Net Income: $26.9 million Selected Multiple Range: 9.0x – 14.0x Selected Transaction Analysis MRQ (9/30/22) Book Value (Excl. AOCI): $443.9 million Selected Multiple Range: 0.50x – 0.90x MRQ (9/30/22) Tangible Book Value (Excl. AOCI): $233.0 million Selected Multiple Range: 1.20x – 1.80x Discounted Cash Book Value (Excl. AOCI) [3] Terminal Multiple: 0.85x – 1.25x Discount Rate: 13.0% – 15.0% Tangible Book Value (Excl. AOCI) [4] Terminal Multiple: 1.25x – 1.85x Discount Rate: 13.0% – 15.0% $2 Financial Analyses Summary Implied Per Share Value Reference Ranges (dollars per share in actuals) .00 $3.00 $4.00 $5.00 $6.00 $7.00 $8.00 $9.00 $10.00 Note: No particular weight has been attributed to any analysis. Note: Based on (i) ~51.2 million basic shares of common stock outstanding; (ii) ~0.2 million options (to the extent in the money, per the treasury method); (iii) ~0.1 million restricted stock units; and (iv) ~0.1 million performance stock units outstanding that are projected to vest, as of 12/9/22. Does not include ~0.1 million MSUs. Based on the Agreement. Reflects 10-day volume-weighted average price per share of common stock as of 12/13/22. Per Company management, at this time the Company is not contemplating making cash distributions over the projection period. For illustrative purposes only and based on discussions with Company management, assuming distributions of 75% of distributable cash at Twins Corporation of $4.2 million in 2022, $5.9 million in 2023, $6.5 million in 2024, $8.2 million in 2025, $9.1 million in 2026 and $10.5 million in 2027, corresponding reduction in book value, and the same discount rate range and terminal multiple range used in the discounted cash flow analysis, the implied equity value per share reference range would be $5.22 - $8.04. Per Company management, at this time the Company is not contemplating making cash distributions over the projection period. For illustrative purposes only and based on discussions with Company management, assuming distributions of 75% of distributable cash at Twins Corporation of $4.2 million in 2022, $5.9 million in 2023, $6.5 million in 2024, $8.2 million in 2025, $9.1 million in 2026 and $10.5 million in 2027, corresponding reduction in tangible book value, and the same discount rate range and terminal multiple range used in the illustrative discounted cash flow analysis, the implied equity value per share reference range would be $5.24 - $8.12. Adjusted Net Income refers to earnings, adjusted, among other things, for unrealized gains/losses and certain unusual or non-recurring items; AOCI refers to Accumulated Other Comprehensive Income; CY refers to Calendar Year; E refers to Estimated; MRQ refers to the most recently completed quarterly fiscal period for which financial information has been made public; VWAP refers to Volume-Weighted Average Price. Source: Company management, Management Projections, Capital IQ, Bloomberg, and public filings. lllustrative Only lllustrative Only lllustrative Only $5.16 $4.97 $5.43 $4.31 $4.69 $4.89 $4.75 $3.88 $8.34 $7.98 $8.14 $7.75 $7.30 $7.11 $7.46 $7.32 Transaction Consideration¹: $6.15 10-Day VWAP²: $2.87 12 CONFIDENTIAL

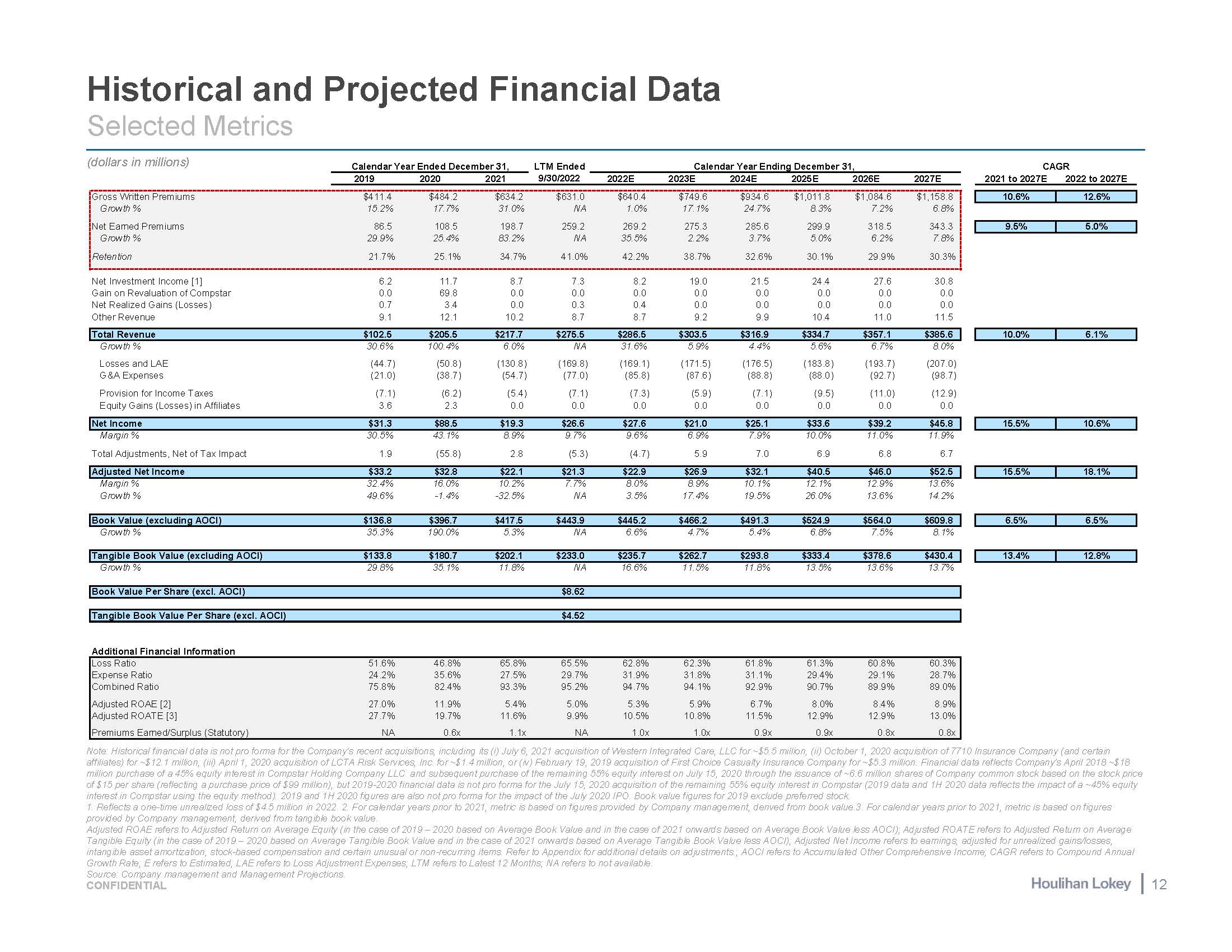

Historical and Projected Financial Data Selected Metrics Note: Historical financial data is not pro forma for the Company's recent acquisitions, including its (i) July 6, 2021 acquisition of Western Integrated Care, LLC for ~$5.5 million, (ii) October 1, 2020 acquisition of 7710 Insurance Company (and certain affiliates) for ~$12.1 million, (iii) April 1, 2020 acquisition of LCTA Risk Services, Inc. for ~$1.4 million, or (iv) February 19, 2019 acquisition of First Choice Casualty Insurance Company for ~$5.3 million. Financial data reflects Company's April 2018 ~$18 million purchase of a 45% equity interest in Compstar Holding Company LLC and subsequent purchase of the remaining 55% equity interest on July 15, 2020 through the issuance of ~6.6 million shares of Company common stock based on the stock price of $15 per share (reflecting a purchase price of $99 million), but 2019-2020 financial data is not pro forma for the July 15, 2020 acquisition of the remaining 55% equity interest in Compstar (2019 data and 1H 2020 data reflects the impact of a ~45% equity interest in Compstar using the equity method). 2019 and 1H 2020 figures are also not pro forma for the impact of the July 2020 IPO. Book value figures for 2019 exclude preferred stock. 1. Reflects a one-time unrealized loss of $4.5 million in 2022. 2. For calendar years prior to 2021, metric is based on figures provided by Company management, derived from book value.3. For calendar years prior to 2021, metric is based on figures provided by Company management, derived from tangible book value. Adjusted ROAE refers to Adjusted Return on Average Equity (in the case of 2019 – 2020 based on Average Book Value and in the case of 2021 onwards based on Average Book Value less AOCI); Adjusted ROATE refers to Adjusted Return on Average Tangible Equity (in the case of 2019 – 2020 based on Average Tangible Book Value and in the case of 2021 onwards based on Average Tangible Book Value less AOCI); Adjusted Net Income refers to earnings, adjusted for unrealized gains/losses, intangible asset amortization, stock-based compensation and certain unusual or non-recurring items. Refer to Appendix for additional details on adjustments.; AOCI refers to Accumulated Other Comprehensive Income; CAGR refers to Compound Annual Growth Rate; E refers to Estimated; LAE refers to Loss Adjustment Expenses; LTM refers to Latest 12 Months; NA refers to not available. Source: Company management and Management Projections. (dollars in millions) Calendar Year Ended December 31, LTM Ended Calendar Year Ending December 31, 2019 2020 2021 9/30/2022 2022E 2023E 2024E 2025E 2026E 2027E CAGR 2021 to 2027E 2022 to 2027E Gross Written Premiums $411.4 $484.2 $634.2 $631.0 $640.4 $749.6 $934.6 $1,011.8 $1,084.6 $1,158.8 10.6% 12.6% Growth % 15.2% 17.7% 31.0% NA 1.0% 17.1% 24.7% 8.3% 7.2% 6.8% Net Earned Premiums 86.5 108.5 198.7 259.2 269.2 275.3 285.6 299.9 318.5 343.3 9.5% 5.0% Growth % 29.9% 25.4% 83.2% NA 35.5% 2.2% 3.7% 5.0% 6.2% 7.8% Retention 21.7% 25.1% 34.7% 41.0% 42.2% 38.7% 32.6% 30.1% 29.9% 30.3% Net Investment Income [1] 6.2 11.7 8.7 7.3 8.2 19.0 21.5 24.4 27.6 30.8 Gain on Revaluation of Compstar 0.0 69.8 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Net Realized Gains (Losses) 0.7 3.4 0.0 0.3 0.4 0.0 0.0 0.0 0.0 0.0 Other Revenue 9.1 12.1 10.2 8.7 8.7 9.2 9.9 10.4 11.0 11.5 Total Revenue $102.5 $205.5 $217.7 $275.5 $286.5 $303.5 $316.9 $334.7 $357.1 $385.6 10.0% 6.1% Growth % 30.6% 100.4% 6.0% NA 31.6% 5.9% 4.4% 5.6% 6.7% 8.0% Losses and LAE (44.7) (50.8) (130.8) (169.8) (169.1) (171.5) (176.5) (183.8) (193.7) (207.0) G&A Expenses (21.0) (38.7) (54.7) (77.0) (85.8) (87.6) (88.8) (88.0) (92.7) (98.7) Provision for Income Taxes (7.1) (6.2) (5.4) (7.1) (7.3) (5.9) (7.1) (9.5) (11.0) (12.9) Equity Gains (Losses) in Affiliates 3.6 2.3 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Net Income $31.3 $88.5 $19.3 $26.6 $27.6 $21.0 $25.1 $33.6 $39.2 $45.8 15.5% 10.6% Margin % 30.5% 43.1% 8.9% 9.7% 9.6% 6.9% 7.9% 10.0% 11.0% 11.9% Total Adjustments, Net of Tax Impact 1.9 (55.8) 2.8 (5.3) (4.7) 5.9 7.0 6.9 6.8 6.7 Adjusted Net Income $33.2 $32.8 $22.1 $21.3 $22.9 $26.9 $32.1 $40.5 $46.0 $52.5 15.5% 18.1% Margin % 32.4% 16.0% 10.2% 7.7% 8.0% 8.9% 10.1% 12.1% 12.9% 13.6% Growth % 49.6% -1.4% -32.5% NA 3.5% 17.4% 19.5% 26.0% 13.6% 14.2% Book Value (excluding AOCI) $136.8 $396.7 $417.5 $443.9 $445.2 $466.2 $491.3 $524.9 $564.0 $609.8 6.5% 6.5% Growth % 35.3% 190.0% 5.3% NA 6.6% 4.7% 5.4% 6.8% 7.5% 8.1% Tangible Book Value (excluding AOCI) $133.8 $180.7 $202.1 $233.0 $235.7 $262.7 $293.8 $333.4 $378.6 $430.4 13.4% 12.8% Growth % 29.8% 35.1% 11.8% NA 16.6% 11.5% 11.8% 13.5% 13.6% 13.7% Book Value Per Share (excl. AOCI) $8.62 Tangible Book Value Per Share (excl. AOCI) $4.52 Additional Financial Information Loss Ratio 51.6% 46.8% 65.8% 65.5% 62.8% 62.3% 61.8% 61.3% 60.8% 60.3% Expense Ratio 24.2% 35.6% 27.5% 29.7% 31.9% 31.8% 31.1% 29.4% 29.1% 28.7% Combined Ratio 75.8% 82.4% 93.3% 95.2% 94.7% 94.1% 92.9% 90.7% 89.9% 89.0% Adjusted ROAE [2] 27.0% 11.9% 5.4% 5.0% 5.3% 5.9% 6.7% 8.0% 8.4% 8.9% Adjusted ROATE [3] 27.7% 19.7% 11.6% 9.9% 10.5% 10.8% 11.5% 12.9% 12.9% 13.0% Premiums Earned/Surplus (Statutory) NA 0.6x 1.1x NA 1.0x 1.0x 0.9x 0.9x 0.8x 0.8x 12 CONFIDENTIAL

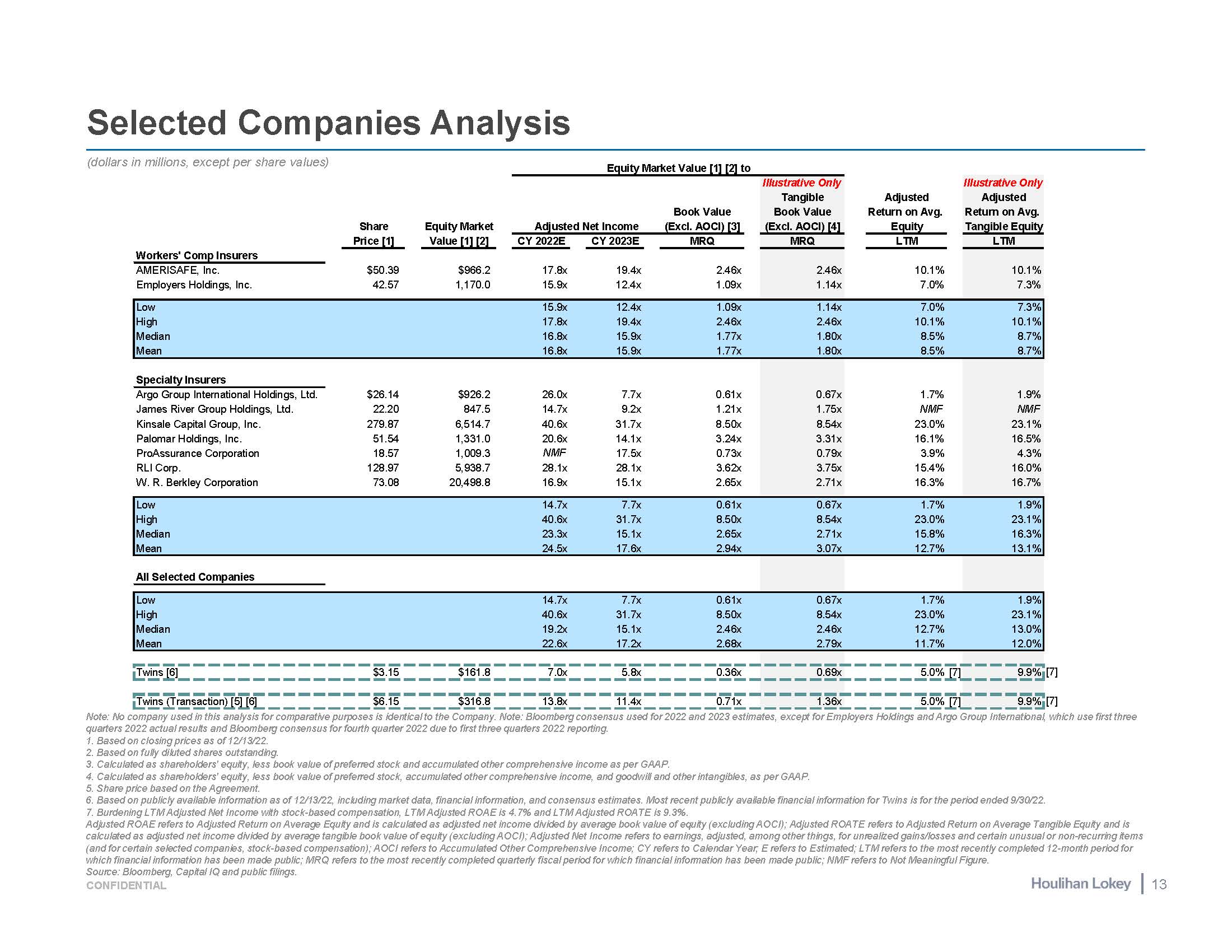

Selected Companies Analysis (dollars in millions, except per share values) Equity Market Value [1] [2] to N Workers' Comp Insurers AMERISAFE, Inc. Employers Holdings, Inc. Share Price [1] $50.39 42.57 Equity Market Value [1] [2] $966.2 1,170.0 Adjusted Net Income Book Value (Excl. AOCI) [3] Illustrative Only Tangible Book Value (Excl. AOCI) [4] Adjusted Return on Avg. Equity LTM 10.1% 7.0% Illustrative Only Adjusted Return on Avg. Tangible Equity CY 2022E CY 2023E MRQ MRQ LTM 17.8x 15.9x 19.4x 12.4x 2.46x 1.09x 2.46x 1.14x 10.1% 7.3% Low 15.9x 12.4x 1.09x 1.14x 7.0% 7.3% High 17.8x 19.4x 2.46x 2.46x 10.1% 10.1% Median 16.8x 15.9x 1.77x 1.80x 8.5% 8.7% Mean 16.8x 15.9x 1.77x 1.80x 8.5% 8.7% Specialty Insurers Argo Group International Holdings, Ltd. $26.14 $926.2 26.0x 7.7x 0.61x 0.67x 1.7% 1.9% James River Group Holdings, Ltd. 22.20 847.5 14.7x 9.2x 1.21x 1.75x NMF NMF Kinsale Capital Group, Inc. 279.87 6,514.7 40.6x 31.7x 8.50x 8.54x 23.0% 23.1% Palomar Holdings, Inc. 51.54 1,331.0 20.6x 14.1x 3.24x 3.31x 16.1% 16.5% ProAssurance Corporation 18.57 1,009.3 NMF 17.5x 0.73x 0.79x 3.9% 4.3% RLI Corp. 128.97 5,938.7 28.1x 28.1x 3.62x 3.75x 15.4% 16.0% W. R. Berkley Corporation 73.08 20,498.8 16.9x 15.1x 2.65x 2.71x 16.3% 16.7% Low 14.7x 7.7x 0.61x 0.67x 1.7% 1.9% High 40.6x 31.7x 8.50x 8.54x 23.0% 23.1% Median 23.3x 15.1x 2.65x 2.71x 15.8% 16.3% Mean 24.5x 17.6x 2.94x 3.07x 12.7% 13.1% All Selected Companies Low 14.7x 7.7x 0.61x 0.67x 1.7% 1.9% High 40.6x 31.7x 8.50x 8.54x 23.0% 23.1% Median 19.2x 15.1x 2.46x 2.46x 12.7% 13.0% Mean 22.6x 17.2x 2.68x 2.79x 11.7% 12.0% Twins [6] $3.15 $161.8 7.0x 5.8x 0.36x 0.69x 5.0% [7] 9.9% Twins (Transaction) [5] [6] $6.15 $316.8 13.8x 11.4x 0.71x 1.36x 5.0% [7] 9.9% [7] [7] Note: No company used in this analysis for comparative purposes is identical to the Company. Note: Bloomberg consensus used for 2022 and 2023 estimates, except for Employers Holdings and Argo Group International, which use first three quarters 2022 actual results and Bloomberg consensus for fourth quarter 2022 due to first three quarters 2022 reporting. Based on closing prices as of 12/13/22. Based on fully diluted shares outstanding. Calculated as shareholders' equity, less book value of preferred stock and accumulated other comprehensive income as per GAAP. Calculated as shareholders' equity, less book value of preferred stock, accumulated other comprehensive income, and goodwill and other intangibles, as per GAAP. Share price based on the Agreement. Based on publicly available information as of 12/13/22, including market data, financial information, and consensus estimates. Most recent publicly available financial information for Twins is for the period ended 9/30/22. Burdening LTM Adjusted Net Income with stock-based compensation, LTM Adjusted ROAE is 4.7% and LTM Adjusted ROATE is 9.3%. Adjusted ROAE refers to Adjusted Return on Average Equity and is calculated as adjusted net income divided by average book value of equity (excluding AOCI); Adjusted ROATE refers to Adjusted Return on Average Tangible Equity and is calculated as adjusted net income divided by average tangible book value of equity (excluding AOCI); Adjusted Net Income refers to earnings, adjusted, among other things, for unrealized gains/losses and certain unusual or non-recurring items (and for certain selected companies, stock-based compensation); AOCI refers to Accumulated Other Comprehensive Income; CY refers to Calendar Year; E refers to Estimated; LTM refers to the most recently completed 12-month period for which financial information has been made public; MRQ refers to the most recently completed quarterly fiscal period for which financial information has been made public; NMF refers to Not Meaningful Figure. Source: Bloomberg, Capital IQ and public filings. CONFIDENTIAL 13

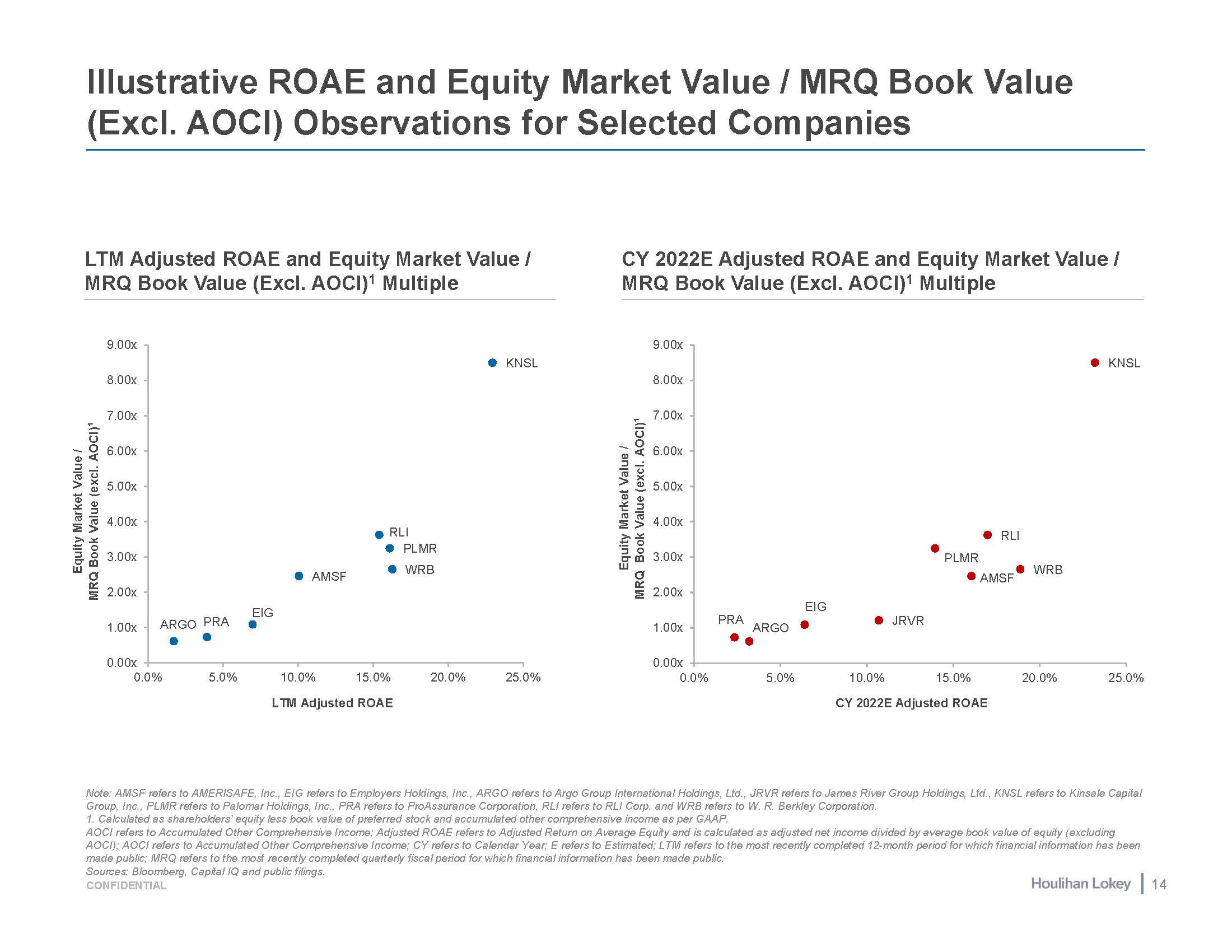

Note: AMSF refers to AMERISAFE, Inc., EIG refers to Employers Holdings, Inc., ARGO refers to Argo Group International Holdings, Ltd., JRVR refers to James River Group Holdings, Ltd., KNSL refers to Kinsale Capital Group, Inc., PLMR refers to Palomar Holdings, Inc., PRA refers to ProAssurance Corporation, RLI refers to RLI Corp. and WRB refers to W. R. Berkley Corporation. 1. Calculated as shareholders’ equity less book value of preferred stock and accumulated other comprehensive income as per GAAP. AOCI refers to Accumulated Other Comprehensive Income; Adjusted ROAE refers to Adjusted Return on Average Equity and is calculated as adjusted net income divided by average book value of equity (excluding AOCI); AOCI refers to Accumulated Other Comprehensive Income; CY refers to Calendar Year; E refers to Estimated; LTM refers to the most recently completed 12-month period for which financial information has been made public; MRQ refers to the most recently completed quarterly fiscal period for which financial information has been made public. Illustrative ROAE and Equity Market Value / MRQ Book Value (Excl. AOCI) Observations for Selected Companies LTM Adjusted ROAE and Equity Market Value / MRQ Book Value (Excl. AOCI)1 Multiple CY 2022E Adjusted ROAE and Equity Market Value / MRQ Book Value (Excl. AOCI)1 Multiple AMSF EIG KNSL ARGO PRA RLI PLMR WRB 0.00x 1.00x 2.00x 3.00x 4.00x 5.00x 6.00x 7.00x 8.00x 9.00x 0.0% 5.0% 10.0% 15.0% LTM Adjusted ROAE 20.0% 25.0% Equity Market Value / MRQ Book Value (excl. AOCI)¹ AMSF Sources: Bloomberg, Capital IQ and public filings. CONFIDENTIAL 14 EIG JRVR KNSL PLMR PRA ARGO RLI WRB 0.00x 1.00x 2.00x 3.00x 4.00x 5.00x 6.00x 7.00x 8.00x 9.00x 0.0% 5.0% 10.0% 15.0% CY 2022E Adjusted ROAE 20.0% 25.0% Equity Market Value / MRQ Book Value (excl. AOCI)¹

Benchmarking Data Note: No company used in this analysis for comparative purposes is identical to the Company. Based on financial information for Twins for the period ended 9/30/22 per Company management. Ratings represent the latest available (as of 12/13/2022) AM Best Financial Strength Rating for each company's largest insurance subsidiary as measured by 9/30/2022 LTM Direct Premiums Written. Represents calendar year 2021 figure, given Kinsale Capital Group, Inc. only files annual statutory statements. Calculated excluding AOCI. Burdening Adjusted Net Income with stock-based compensation, Twins LTM Adj. ROATE is 9.3%, LTM Adj. ROAE is 4.7%, CY 2022E Adj. ROAE is 5.0%, and CY 2023E Adj. ROAE is 5.5%. Adjusted Net Income refers to earnings, adjusted, among other things, for unrealized gains/losses and certain unusual or non-recurring items. Adjusted ROAE refers to Adjusted Return on Average Equity and is calculated as adjusted net income divided by average book value of equity (excluding AOCI). Adjusted ROATE refers to Adjusted Return on Average Tangible Equity and is calculated as adjusted net income divided by average tangible book value of equity (excluding AOCI). AOCI refers to Accumulated Other Comprehensive Income. CY refers to Calendar Year. E refers to Estimated. LTM refers to the most recently completed 12-month period for which financial information has been made public. MRQ refers to the most recently completed fiscal quarter for which financial information has been made public. Size & Financial Strength Profitability (Adjusted ROAE and Adjusted ROATE) Leverage (LTM Net Premiums Written / Average Capital and Surplus) Workers' Comp Insurers Employers Holdings, Inc. 0.7x AMERISAFE, Inc. 1.0x Twins - FY 2022E 1.0x Specialty Insurers ProAssurance Corporation 0.7x RLI Corp. 1.0x Twins - FY 2022E 1.0x Argo Group International Holdings, Ltd. 1.1x Kinsale Capital Group, Inc. [3] 1.2x Palomar Holdings, Inc. 1.2x W. R. Berkley Corporation 1.3x James River Group Holdings, Ltd. 2.1x Financial Strength (AM Best Financial Strength Rating) [2] Workers' Comp Insurers AMERISAFE, Inc. A Twins A Employers Holdings, Inc. A- Specialty Insurers RLI Corp. A+ W. R. Berkley Corporation A+ Kinsale Capital Group, Inc. A Twins A Argo Group International Holdings, Ltd. A- James River Group Holdings, Ltd. A- Palomar Holdings, Inc. A- ProAssurance Corporation A- Size (MRQ Book Value of Equity (Excl. AOCI), millions) Workers' Comp Insurers Employers Holdings, Inc. $1,077.9 Twins [1] $443.9 AMERISAFE, Inc. $393.0 Specialty Insurers W. R. Berkley Corporation $7,731.9 RLI Corp. $1,638.6 Argo Group International Holdings, Ltd. $1,513.8 ProAssurance Corporation $1,390.2 Kinsale Capital Group, Inc. $766.8 James River Group Holdings, Ltd. $702.1 Twins [1] $443.9 Palomar Holdings, Inc. $410.5 Size (MRQ Tangible Book Value of Equity (Excl. AOCI), millions) Workers' Comp Insurers Employers Holdings, Inc. $1,028.1 AMERISAFE, Inc. $393.0 Twins [1] $233.0 Specialty Insurers W. R. Berkley Corporation $7,562.2 RLI Corp. $1,585.0 Argo Group International Holdings, Ltd. $1,377.7 ProAssurance Corporation $1,272.2 Kinsale Capital Group, Inc. $763.3 James River Group Holdings, Ltd. $484.5 Palomar Holdings, Inc. $401.9 Twins [1] $233.0 Profitability (LTM Adjusted ROATE) [4] [5] Workers' Comp Insurers AMERISAFE, Inc. 10.1% Twins [1] 9.9% Employers Holdings, Inc. 7.3% Specialty Insurers Kinsale Capital Group, Inc. 23.1% W. R. Berkley Corporation 16.7% Palomar Holdings, Inc. 16.5% RLI Corp. 16.0% Twins [1] 9.9% ProAssurance Corporation 4.3% Argo Group International Holdings, Ltd. 1.9% James River Group Holdings, Ltd. NMF Profitability (LTM Adjusted ROAE) [4] [5] Workers' Comp Insurers AMERISAFE, Inc. 10.1% Employers Holdings, Inc. 7.0% Twins [1] 5.0% Specialty Insurers Kinsale Capital Group, Inc. 23.0% W. R. Berkley Corporation 16.3% Palomar Holdings, Inc. 16.1% RLI Corp. 15.4% Twins [1] 5.0% ProAssurance Corporation 3.9% Argo Group International Holdings, Ltd. 1.7% James River Group Holdings, Ltd. NMF Profitability (CY 2022E Adjusted ROAE) [5] Workers' Comp Insurers AMERISAFE, Inc. 16.0% Employers Holdings, Inc. 6.4% Twins 5.3% Specialty Insurers Kinsale Capital Group, Inc. 23.2% W. R. Berkley Corporation 18.9% RLI Corp. 17.0% Palomar Holdings, Inc. 13.9% James River Group Holdings, Ltd. 10.7% Twins 5.3% Argo Group International Holdings, Ltd. 3.2% ProAssurance Corporation 2.3% Profitability (CY 2023E Adjusted ROAE) [5] Workers' Comp Insurers AMERISAFE, Inc. 17.4% Employers Holdings, Inc. 7.6% Twins 5.9% Specialty Insurers Kinsale Capital Group, Inc. 25.9% Palomar Holdings, Inc. 20.8% W. R. Berkley Corporation 19.9% RLI Corp. 14.5% James River Group Holdings, Ltd. 14.1% Argo Group International Holdings, Ltd. 10.3% Twins 5.9% ProAssurance Corporation 5.5% NMF refers to not meaningful figure. Source: Bloomberg, Capital IQ, Company management, Management Projections and public filings. CONFIDENTIAL 15

Benchmarking Data (cont.) Note: No company used in this analysis for comparative purposes is identical to the Company. 1. In 1999, company entered into a LPT Agreement with third party reinsurers. The figures above do not reflect the impact of that agreement. If those are reflected, 2019-2021 average and LTM loss ratios would be 52.2% and 56.9%, respectively and the 2019-2021 average and LTM combined ratios would be 93.2% and 95.5%, respectively. 2. Based on financial information for Twins for the period ended 9/30/22 per Company management. Adjusted Net Income refers to earnings, adjusted, among other things, for unrealized gains/losses and certain unusual or non-recurring items. CY refers to Calendar Year. E refers to Estimated. NA refers to not available. NMF refers to not meaningful figure. Profitability (Loss & Combined Ratios) Growth (Adjusted Net Income) Projected Growth (CY 2022E to CY 2023E Adjusted Net Income) Workers' Comp Insurers Employers Holdings, Inc. 27.6% Twins 17.4% AMERISAFE, Inc. (8.2%) Specialty Insurers James River Group Holdings, Ltd. 60.5% Palomar Holdings, Inc. 46.3% Kinsale Capital Group, Inc. 28.0% Twins 17.4% W. R. Berkley Corporation 11.7% RLI Corp. (0.0%) Argo Group International Holdings, Ltd. NMF ProAssurance Corporation NMF Projected Growth (CY 2021 to CY 2022E Adjusted Net Income) Workers' Comp Insurers Employers Holdings, Inc. 8.7% Twins 3.5% AMERISAFE, Inc. (1.0%) Specialty Insurers W. R. Berkley Corporation 27.4% Kinsale Capital Group, Inc. 21.3% Palomar Holdings, Inc. 21.0% RLI Corp. 19.4% Twins 3.5% Argo Group International Holdings, Ltd. (14.2%) ProAssurance Corporation (87.5%) James River Group Holdings, Ltd. NMF Projected Growth (CY 2021 to CY 2023E Adjusted Net Income) Workers' Comp Insurers Employers Holdings, Inc. 17.8% Twins 10.2% AMERISAFE, Inc. (4.6%) Specialty Insurers Argo Group International Holdings, Ltd. 70.4% Palomar Holdings, Inc. 33.1% Kinsale Capital Group, Inc. 24.6% W. R. Berkley Corporation 19.3% Twins 10.2% RLI Corp. 9.2% ProAssurance Corporation (12.7%) James River Group Holdings, Ltd. NA Projected Growth (CY 2020 to CY 2022E Adjusted Net Income) Workers' Comp Insurers Employers Holdings, Inc. (11.2%) Twins (16.4%) AMERISAFE, Inc. (18.9%) Specialty Insurers Palomar Holdings, Inc. 170.0% W. R. Berkley Corporation 66.3% James River Group Holdings, Ltd. 64.9% Kinsale Capital Group, Inc. 49.0% RLI Corp. 34.1% Twins (16.4%) Argo Group International Holdings, Ltd. NA ProAssurance Corporation NA Combined Ratio (CY 2019 to CY 2021 Average) Workers' Comp Insurers AMERISAFE, Inc. 79.6% Twins 83.9% Employers Holdings, Inc. [1] 95.1% Specialty Insurers Kinsale Capital Group, Inc. 82.9% Twins 83.9% RLI Corp. 90.2% Palomar Holdings, Inc. 93.4% W. R. Berkley Corporation 96.7% Argo Group International Holdings, Ltd. 106.7% ProAssurance Corporation 112.4% James River Group Holdings, Ltd. 114.6% Net Loss Ratio (CY 2019 to CY 2021 Average) Workers' Comp Insurers Employers Holdings, Inc. [1] 54.1% AMERISAFE, Inc. 54.3% Twins 54.8% Specialty Insurers Palomar Holdings, Inc. 21.6% RLI Corp. 49.0% Twins 54.8% Kinsale Capital Group, Inc. 59.8% W. R. Berkley Corporation 62.6% Argo Group International Holdings, Ltd. 69.1% ProAssurance Corporation 83.3% James River Group Holdings, Ltd. 91.5% Net Loss Ratio (LTM) Workers' Comp Insurers Employers Holdings, Inc. [1] 58.7% AMERISAFE, Inc. 64.0% Twins [2] 65.5% Specialty Insurers Palomar Holdings, Inc. 23.3% RLI Corp. 44.5% Kinsale Capital Group, Inc. 58.1% W. R. Berkley Corporation 61.3% Twins [2] 65.5% Argo Group International Holdings, Ltd. 68.3% ProAssurance Corporation 74.9% James River Group Holdings, Ltd. 86.1% Combined Ratio (LTM) Workers' Comp Insurers AMERISAFE, Inc. 91.2% Twins [2] 95.2% Employers Holdings, Inc. [1] 97.3% Specialty Insurers Kinsale Capital Group, Inc. 78.7%�� Palomar Holdings, Inc. 81.8% RLI Corp. 84.2% W. R. Berkley Corporation 91.9% Twins [2] 95.2% ProAssurance Corporation 103.4% Argo Group International Holdings, Ltd. 103.9% James River Group Holdings, Ltd. 108.6% LTM refers to the most recently completed 12-month period for which financial information has been made public. Source: Bloomberg, Capital IQ, Company management, Management Projections and public filings. CONFIDENTIAL 16

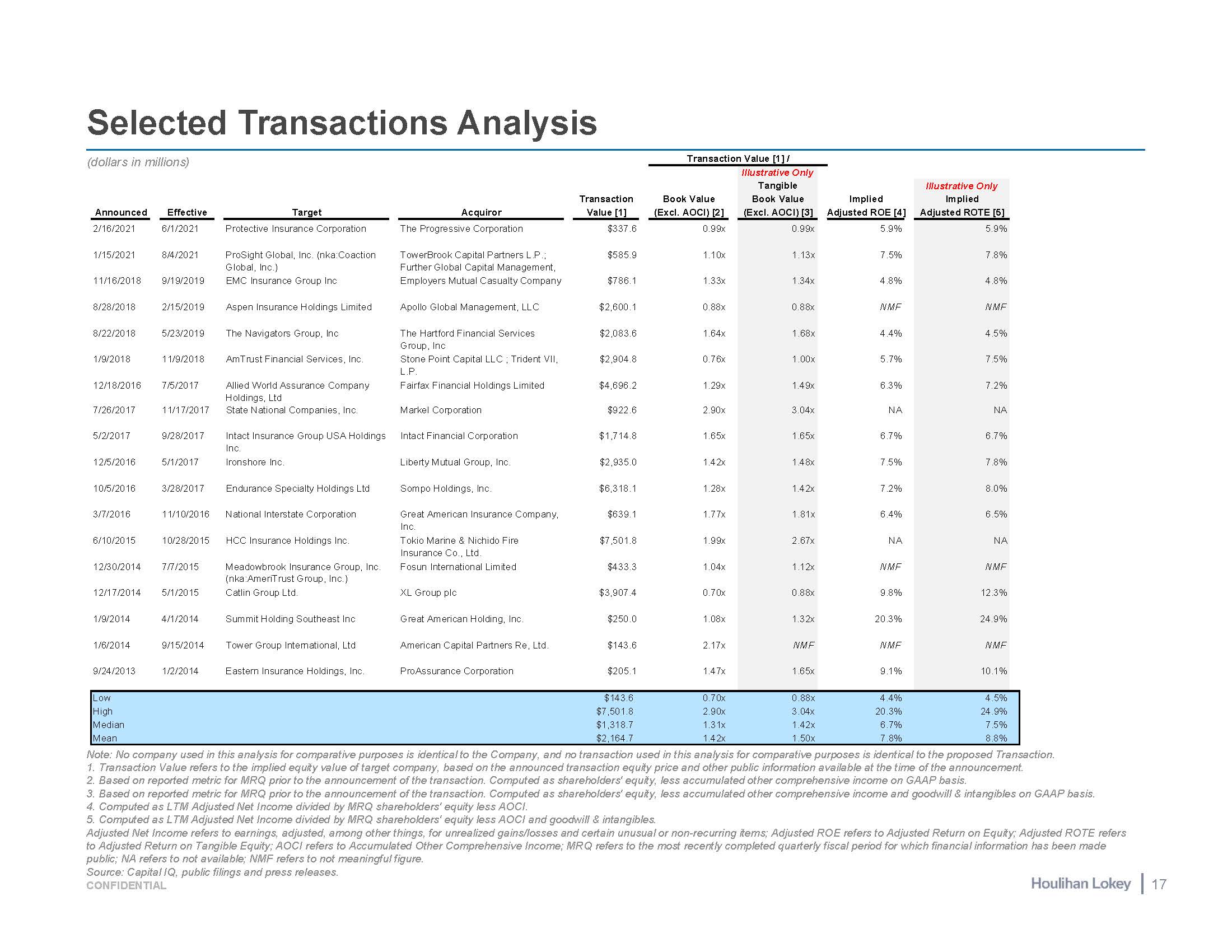

Selected Transactions Analysis Source: Capital IQ, public filings and press releases. CONFIDENTIAL 17 Note: No company used in this analysis for comparative purposes is identical to the Company, and no transaction used in this analysis for comparative purposes is identical to the proposed Transaction. Transaction Value refers to the implied equity value of target company, based on the announced transaction equity price and other public information available at the time of the announcement. Based on reported metric for MRQ prior to the announcement of the transaction. Computed as shareholders' equity, less accumulated other comprehensive income on GAAP basis. Based on reported metric for MRQ prior to the announcement of the transaction. Computed as shareholders' equity, less accumulated other comprehensive income and goodwill & intangibles on GAAP basis. Computed as LTM Adjusted Net Income divided by MRQ shareholders' equity less AOCI. Computed as LTM Adjusted Net Income divided by MRQ shareholders' equity less AOCI and goodwill & intangibles. Adjusted Net Income refers to earnings, adjusted, among other things, for unrealized gains/losses and certain unusual or non-recurring items; Adjusted ROE refers to Adjusted Return on Equity; Adjusted ROTE refers to Adjusted Return on Tangible Equity; AOCI refers to Accumulated Other Comprehensive Income; MRQ refers to the most recently completed quarterly fiscal period for which financial information has been made public; NA refers to not available; NMF refers to not meaningful figure. (dollars in millions) Transaction Value [1] / Illustrative Only Transaction Book Value Tangible Book Value Implied Illustrative Only Implied Announced Effective Target Acquiror Value [1] (Excl. AOCI) [2] (Excl. AOCI) [3] Adjusted ROE [4] Adjusted ROTE [5] 2/16/2021 6/1/2021 Protective Insurance Corporation The Progressive Corporation $337.6 0.99x 0.99x 5.9% 5.9% 1/15/2021 8/4/2021 ProSight Global, Inc. (nka:Coaction Global, Inc.) TowerBrook Capital Partners L.P.; Further Global Capital Management, $585.9 1.10x 1.13x 7.5% 7.8% 11/16/2018 9/19/2019 EMC Insurance Group Inc Employers Mutual Casualty Company $786.1 1.33x 1.34x 4.8% 4.8% 8/28/2018 2/15/2019 Aspen Insurance Holdings Limited Apollo Global Management, LLC $2,600.1 0.88x 0.88x NMF NMF 8/22/2018 5/23/2019 The Navigators Group, Inc The Hartford Financial Services Group, Inc $2,083.6 1.64x 1.68x 4.4% 4.5% 1/9/2018 11/9/2018 AmTrust Financial Services, Inc. Stone Point Capital LLC ; Trident VII, L.P. $2,904.8 0.76x 1.00x 5.7% 7.5% 12/18/2016 7/26/2017 7/5/2017 11/17/2017 Allied World Assurance Company Holdings, Ltd State National Companies, Inc. Fairfax Financial Holdings Limited Markel Corporation $4,696.2 $922.6 1.29x 2.90x 1.49x 3.04x 6.3% NA 7.2% NA 5/2/2017 9/28/2017 Intact Insurance Group USA Holdings Inc. Intact Financial Corporation $1,714.8 1.65x 1.65x 6.7% 6.7% 12/5/2016 5/1/2017 Ironshore Inc. Liberty Mutual Group, Inc. $2,935.0 1.42x 1.48x 7.5% 7.8% 10/5/2016 3/28/2017 Endurance Specialty Holdings Ltd Sompo Holdings, Inc. $6,318.1 1.28x 1.42x 7.2% 8.0% 3/7/2016 11/10/2016 National Interstate Corporation Great American Insurance Company, Inc. $639.1 1.77x 1.81x 6.4% 6.5% 6/10/2015 10/28/2015 HCC Insurance Holdings Inc. Tokio Marine & Nichido Fire Insurance Co., Ltd. $7,501.8 1.99x 2.67x NA NA 12/30/2014 7/7/2015 Meadowbrook Insurance Group, Inc. (nka:AmeriTrust Group, Inc.) Fosun International Limited $433.3 1.04x 1.12x NMF NMF 12/17/2014 5/1/2015 Catlin Group Ltd. XL Group plc $3,907.4 0.70x 0.88x 9.8% 12.3% 1/9/2014 4/1/2014 Summit Holding Southeast Inc Great American Holding, Inc. $250.0 1.08x 1.32x 20.3% 24.9% 1/6/2014 9/15/2014 Tower Group International, Ltd American Capital Partners Re, Ltd. $143.6 2.17x NMF NMF NMF 9/24/2013 1/2/2014 Eastern Insurance Holdings, Inc. ProAssurance Corporation $205.1 1.47x 1.65x 9.1% 10.1% Low $143.6 0.70x 0.88x 4.4% 4.5% High $7,501.8 2.90x 3.04x 20.3% 24.9% Median $1,318.7 1.31x 1.42x 6.7% 7.5% Mean $2,164.7 1.42x 1.50x 7.8% 8.8%

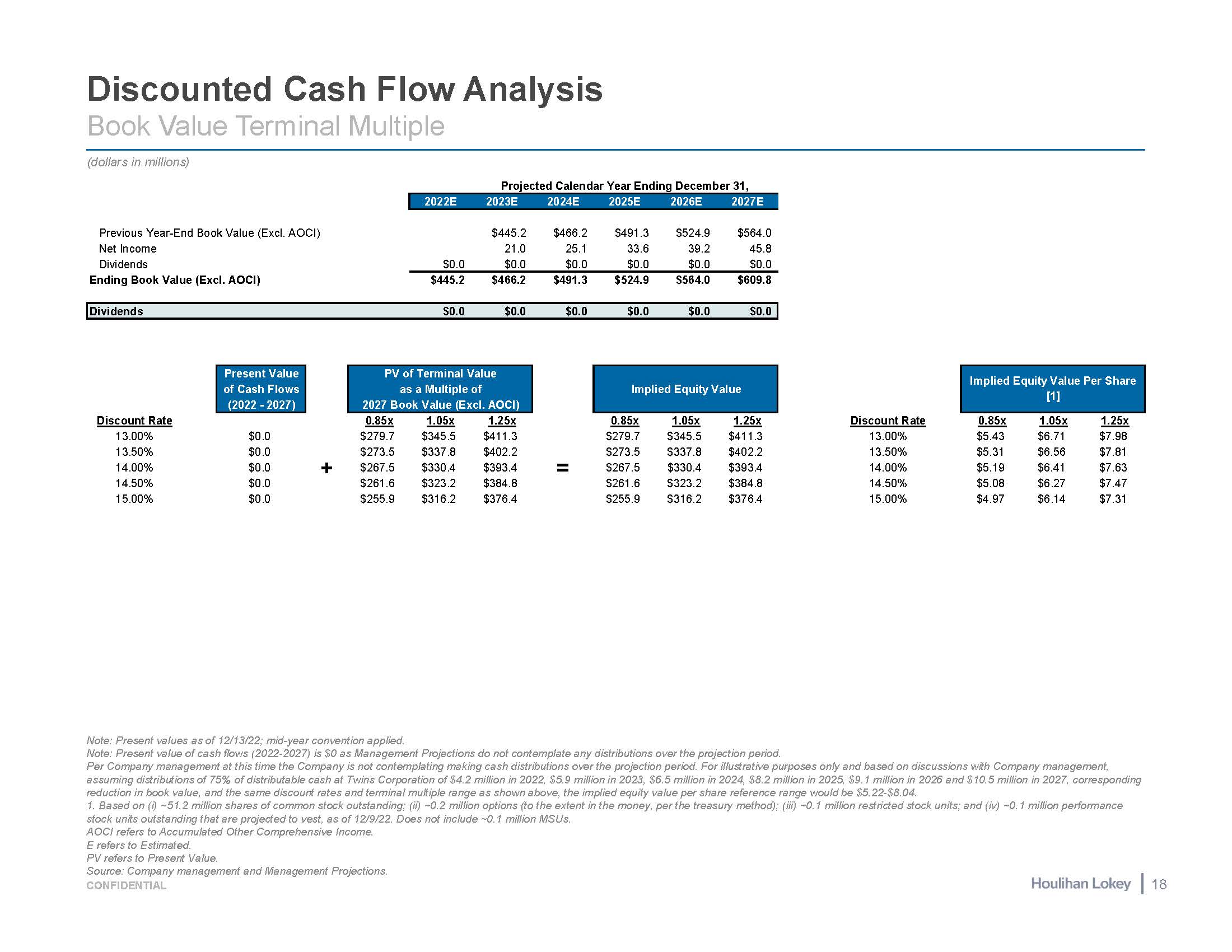

Discounted Cash Flow Analysis Book Value Terminal Multiple (dollars in millions) Previous Year-End Book Value (Excl. AOCI) $445.2 $466.2 $491.3 $524.9 $564.0 Net Income 21.0 25.1 33.6 39.2 45.8 Dividends $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 Ending Book Value (Excl. AOCI) $445.2 $466.2 $491.3 $524.9 $564.0 $609.8 Dividends $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 Present Value of Cash Flows (2022 - 2027) Projected Calendar Year Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E PV of Terminal Value as a Multiple of 2027 Book Value (Excl. AOCI) Implied Equity Value Discount Rate 13.00% 13.50% 14.00% 14.50% 15.00% 0.85x $279.7 $273.5 $267.5 $261.6 $255.9 1.05x $345.5 $337.8 $330.4 $323.2 $316.2 1.25x $411.3 $402.2 $393.4 $384.8 $376.4 0.85x $279.7 $273.5 $267.5 $261.6 $255.9 1.05x $345.5 $337.8 $330.4 $323.2 $316.2 1.25x $411.3 $402.2 $393.4 $384.8 $376.4 Discount Rate 13.00% 13.50% 14.00% 14.50% 15.00% 0.85x $5.43 $5.31 $5.19 $5.08 $4.97 1.05x $6.71 $6.56 $6.41 $6.27 $6.14 1.25x $7.98 $7.81 $7.63 $7.47 $7.31 $0.0 $0.0 $0.0 $0.0 $0.0 + = Implied Equity Value Per Share [1] Note: Present values as of 12/13/22; mid-year convention applied. Note: Present value of cash flows (2022-2027) is $0 as Management Projections do not contemplate any distributions over the projection period. Per Company management at this time the Company is not contemplating making cash distributions over the projection period. For illustrative purposes only and based on discussions with Company management, assuming distributions of 75% of distributable cash at Twins Corporation of $4.2 million in 2022, $5.9 million in 2023, $6.5 million in 2024, $8.2 million in 2025, $9.1 million in 2026 and $10.5 million in 2027, corresponding reduction in book value, and the same discount rates and terminal multiple range as shown above, the implied equity value per share reference range would be $5.22-$8.04. 1. Based on (i) ~51.2 million shares of common stock outstanding; (ii) ~0.2 million options (to the extent in the money, per the treasury method); (iii) ~0.1 million restricted stock units; and (iv) ~0.1 million performance stock units outstanding that are projected to vest, as of 12/9/22. Does not include ~0.1 million MSUs. AOCI refers to Accumulated Other Comprehensive Income. E refers to Estimated. PV refers to Present Value. Source: Company management and Management Projections. CONFIDENTIAL 18

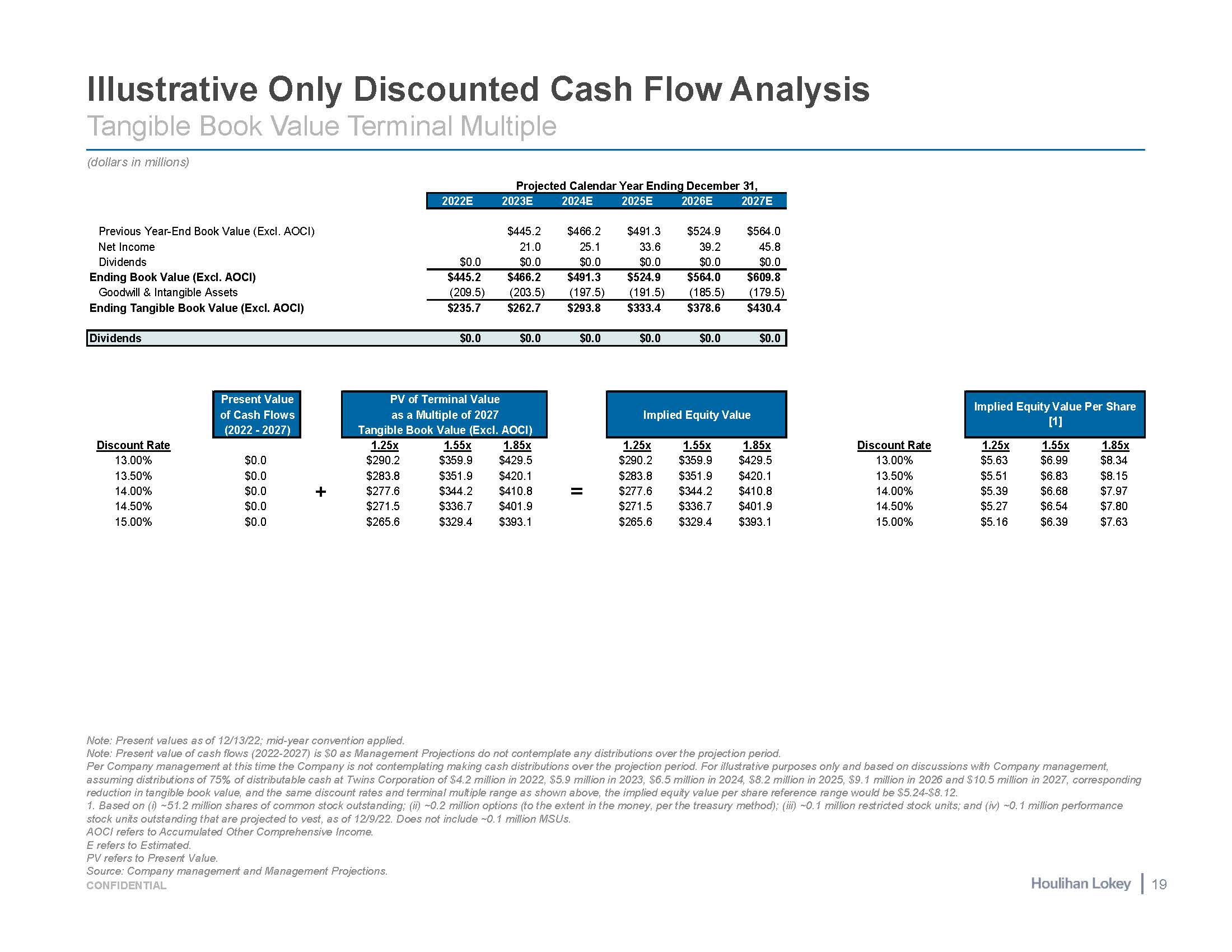

Illustrative Only Discounted Cash Flow Analysis Tangible Book Value Terminal Multiple (dollars in millions) Previous Year-End Book Value (Excl. AOCI) $445.2 $466.2 $491.3 $524.9 $564.0 Net Income 21.0 25.1 33.6 39.2 45.8 Dividends $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 Ending Book Value (Excl. AOCI) $445.2 $466.2 $491.3 $524.9 $564.0 $609.8 Goodwill & Intangible Assets (209.5) (203.5) (197.5) (191.5) (185.5) (179.5) Ending Tangible Book Value (Excl. AOCI) $235.7 $262.7 $293.8 $333.4 $378.6 $430.4 Dividends $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 Present Value of Cash Flows (2022 - 2027) Projected Calendar Year Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E PV of Terminal Value as a Multiple of 2027 Tangible Book Value (Excl. AOCI) Implied Equity Value Discount Rate 13.00% 13.50% 14.00% 14.50% 15.00% 1.25x $290.2 $283.8 $277.6 $271.5 $265.6 1.55x $359.9 $351.9 $344.2 $336.7 $329.4 1.85x $429.5 $420.1 $410.8 $401.9 $393.1 1.25x $290.2 $283.8 $277.6 $271.5 $265.6 1.55x $359.9 $351.9 $344.2 $336.7 $329.4 1.85x $429.5 $420.1 $410.8 $401.9 $393.1 Discount Rate 13.00% 13.50% 14.00% 14.50% 15.00% 1.25x $5.63 $5.51 $5.39 $5.27 $5.16 1.55x $6.99 $6.83 $6.68 $6.54 $6.39 1.85x $8.34 $8.15 $7.97 $7.80 $7.63 $0.0 $0.0 $0.0 $0.0 $0.0 + = Implied Equity Value Per Share [1] Note: Present values as of 12/13/22; mid-year convention applied. Note: Present value of cash flows (2022-2027) is $0 as Management Projections do not contemplate any distributions over the projection period. Per Company management at this time the Company is not contemplating making cash distributions over the projection period. For illustrative purposes only and based on discussions with Company management, assuming distributions of 75% of distributable cash at Twins Corporation of $4.2 million in 2022, $5.9 million in 2023, $6.5 million in 2024, $8.2 million in 2025, $9.1 million in 2026 and $10.5 million in 2027, corresponding reduction in tangible book value, and the same discount rates and terminal multiple range as shown above, the implied equity value per share reference range would be $5.24-$8.12. 1. Based on (i) ~51.2 million shares of common stock outstanding; (ii) ~0.2 million options (to the extent in the money, per the treasury method); (iii) ~0.1 million restricted stock units; and (iv) ~0.1 million performance stock units outstanding that are projected to vest, as of 12/9/22. Does not include ~0.1 million MSUs. AOCI refers to Accumulated Other Comprehensive Income. E refers to Estimated. PV refers to Present Value. Source: Company management and Management Projections. CONFIDENTIAL 19

Page 3 5 10 Executive Summary Selected Updates Since Prior Discussion Materials Financial Analyses 4. Appendices 20 Selected Cost of Equity Considerations Supplemental Financial Information Illustrative Selected Company Multiple Trendlines Supplemental Public Company & Market Observations 21 23 30 33

Page 3 5 10 20 Executive Summary Selected Updates Since Prior Discussion Materials Financial Analyses Appendices Selected Cost of Equity Considerations 21 Supplemental Financial Information Illustrative Selected Company Multiple Trendlines Supplemental Public Company & Market Observations 23 30 33

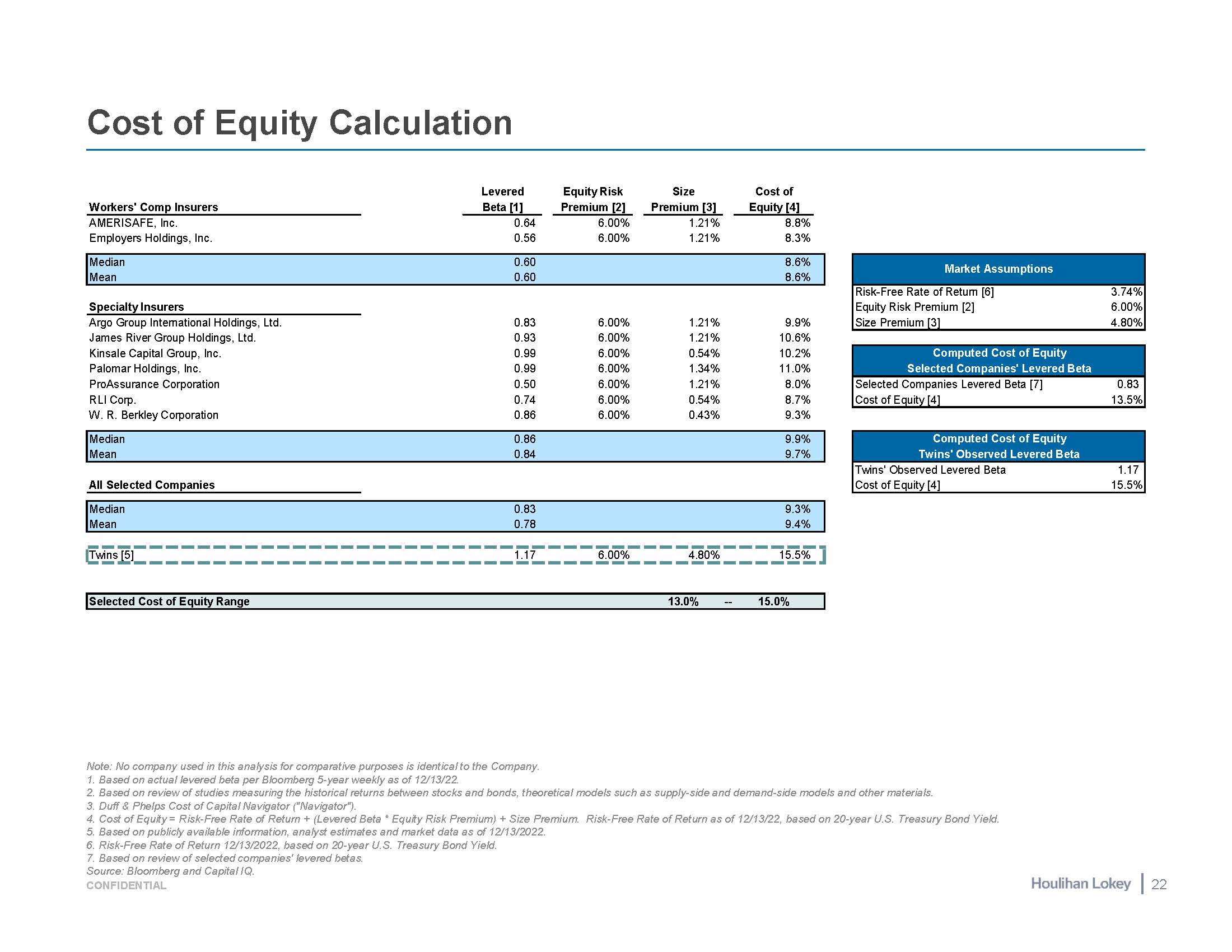

Cost of Equity Calculation Note: No company used in this analysis for comparative purposes is identical to the Company. Based on actual levered beta per Bloomberg 5-year weekly as of 12/13/22. Based on review of studies measuring the historical returns between stocks and bonds, theoretical models such as supply-side and demand-side models and other materials. Duff & Phelps Cost of Capital Navigator ("Navigator"). Cost of Equity = Risk-Free Rate of Return + (Levered Beta * Equity Risk Premium) + Size Premium. Risk-Free Rate of Return as of 12/13/22, based on 20-year U.S. Treasury Bond Yield. Based on publicly available information, analyst estimates and market data as of 12/13/2022. Risk-Free Rate of Return 12/13/2022, based on 20-year U.S. Treasury Bond Yield. Based on review of selected companies' levered betas. Source: Bloomberg and Capital IQ. Workers' Comp Insurers Levered Beta [1] Equity Risk Premium [2] Size Premium [3] Cost of Equity [4] AMERISAFE, Inc. 0.64 6.00% 1.21% 8.8% Employers Holdings, Inc. 0.56 6.00% 1.21% 8.3% Median 0.60 8.6% Mean 0.60 8.6% Specialty Insurers Argo Group International Holdings, Ltd. 0.83 6.00% 1.21% 9.9% Risk-Free Rate of Return [6] Equity Risk Premium [2] Size Premium [3] 3.74% 6.00% 4.80% James River Group Holdings, Ltd. 0.93 6.00% 1.21% 10.6% Kinsale Capital Group, Inc. 0.99 6.00% 0.54% 10.2% Computed Cost of Equity Palomar Holdings, Inc. 0.99 6.00% 1.34% 11.0% Selected Companies' Levered Beta ProAssurance Corporation 0.50 6.00% 1.21% 8.0% Selected Companies Levered Beta [7] 0.83 RLI Corp. 0.74 6.00% 0.54% 8.7% Cost of Equity [4] 13.5% W. R. Berkley Corporation 0.86 6.00% 0.43% 9.3% Median 0.86 9.9% Computed Cost of Equity Mean 0.84 9.7% Twins' Observed Levered Beta Twins' Observed Levered Beta 1.17 All Selected Companies Cost of Equity [4] 15.5% Median 0.83 9.3% Mean 0.78 9.4% Twins [5] 1.17 6.00% 4.80% 15.5% Selected Cost of Equity Range 13.0% -- 15.0% Market Assumptions 22 CONFIDENTIAL

Page 3 5 10 20 21 Executive Summary Selected Updates Since Prior Discussion Materials Financial Analyses Appendices Selected Cost of Equity Considerations Supplemental Financial Information 23 Illustrative Selected Company Multiple Trendlines Supplemental Public Company & Market Observations 30 33

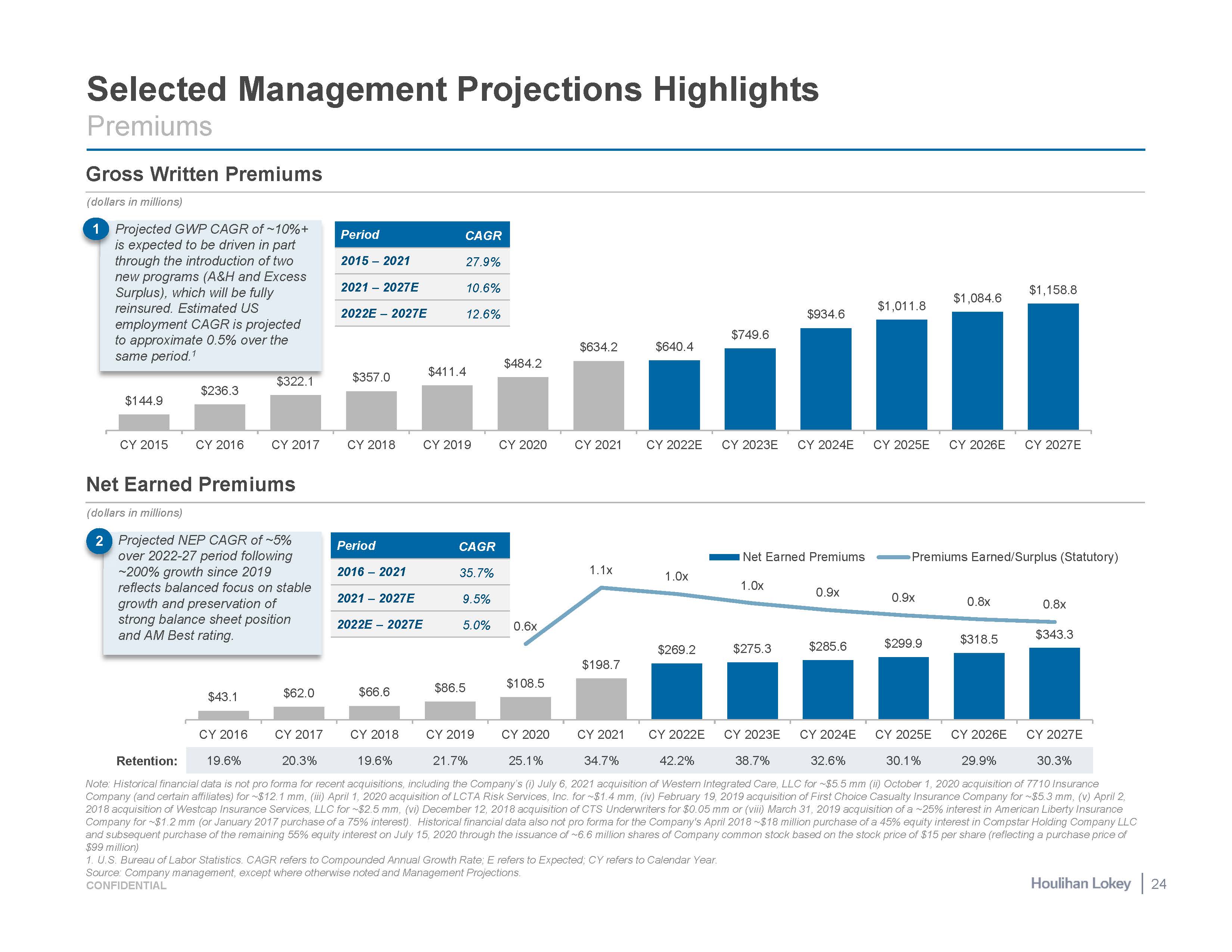

$43.1 $62.0 $66.6 $86.5 $108.5 $198.7 $269.2 $275.3 $285.6 $299.9 $318.5 $343.3 0.6x 1.1x 1.0x 1.0x 0.9x 0.9x 0.8x 0.8x CY 2016 CY 2017 CY 2018 CY 2019 CY 2020 CY 2021 CY 2022E CY 2023E CY 2024E CY 2025E CY 2026E CY 2027E Net Earned Premiums Premiums Earned/Surplus (Statutory) $144.9 $236.3 $322.1 $357.0 $411.4 $484.2 $634.2 $640.4 $749.6 $934.6 $1,011.8 $1,084.6 $1,158.8 CY 2015 CY 2016 CY 2017 Net Earned Premiums CY 2018 CY 2019 CY 2020 CY 2021 CY 2022E CY 2023E CY 2024E CY 2025E CY 2026E CY 2027E Selected Management Projections Highlights Premiums Gross Written Premiums (dollars in millions) (dollars in millions) 2 Projected NEP CAGR of ~5% over 2022-27 period following ~200% growth since 2019 reflects balanced focus on stable growth and preservation of strong balance sheet position and AM Best rating. Period CAGR 2015 – 2021 27.9% 2021 – 2027E 10.6% 2022E – 2027E 12.6% Period CAGR 2016 – 2021 35.7% 2021 – 2027E 9.5% 2022E – 2027E 5.0% Retention: 19.6% 20.3% 19.6% 21.7% 25.1% 34.7% 42.2% 38.7% 32.6% 30.1% 29.9% 30.3% Note: Historical financial data is not pro forma for recent acquisitions, including the Company’s (i) July 6, 2021 acquisition of Western Integrated Care, LLC for ~$5.5 mm (ii) October 1, 2020 acquisition of 7710 Insurance Company (and certain affiliates) for ~$12.1 mm, (iii) April 1, 2020 acquisition of LCTA Risk Services, Inc. for ~$1.4 mm, (iv) February 19, 2019 acquisition of First Choice Casualty Insurance Company for ~$5.3 mm, (v) April 2, 2018 acquisition of Westcap Insurance Services, LLC for ~$2.5 mm, (vi) December 12, 2018 acquisition of CTS Underwriters for $0.05 mm or (viii) March 31, 2019 acquisition of a ~25% interest in American Liberty Insurance Company for ~$1.2 mm (or January 2017 purchase of a 75% interest). Historical financial data also not pro forma for the Company's April 2018 ~$18 million purchase of a 45% equity interest in Compstar Holding Company LLC and subsequent purchase of the remaining 55% equity interest on July 15, 2020 through the issuance of ~6.6 million shares of Company common stock based on the stock price of $15 per share (reflecting a purchase price of $99 million) 1. U.S. Bureau of Labor Statistics. CAGR refers to Compounded Annual Growth Rate; E refers to Expected; CY refers to Calendar Year. Source: Company management, except where otherwise noted and Management Projections. employment CAGR is projected to approximate 0.5% over the same period.1 1 Projected GWP CAGR of ~10%+ is expected to be driven in part through the introduction of two new programs (A&H and Excess Surplus), which will be fully reinsured. Estimated US 24 CONFIDENTIAL

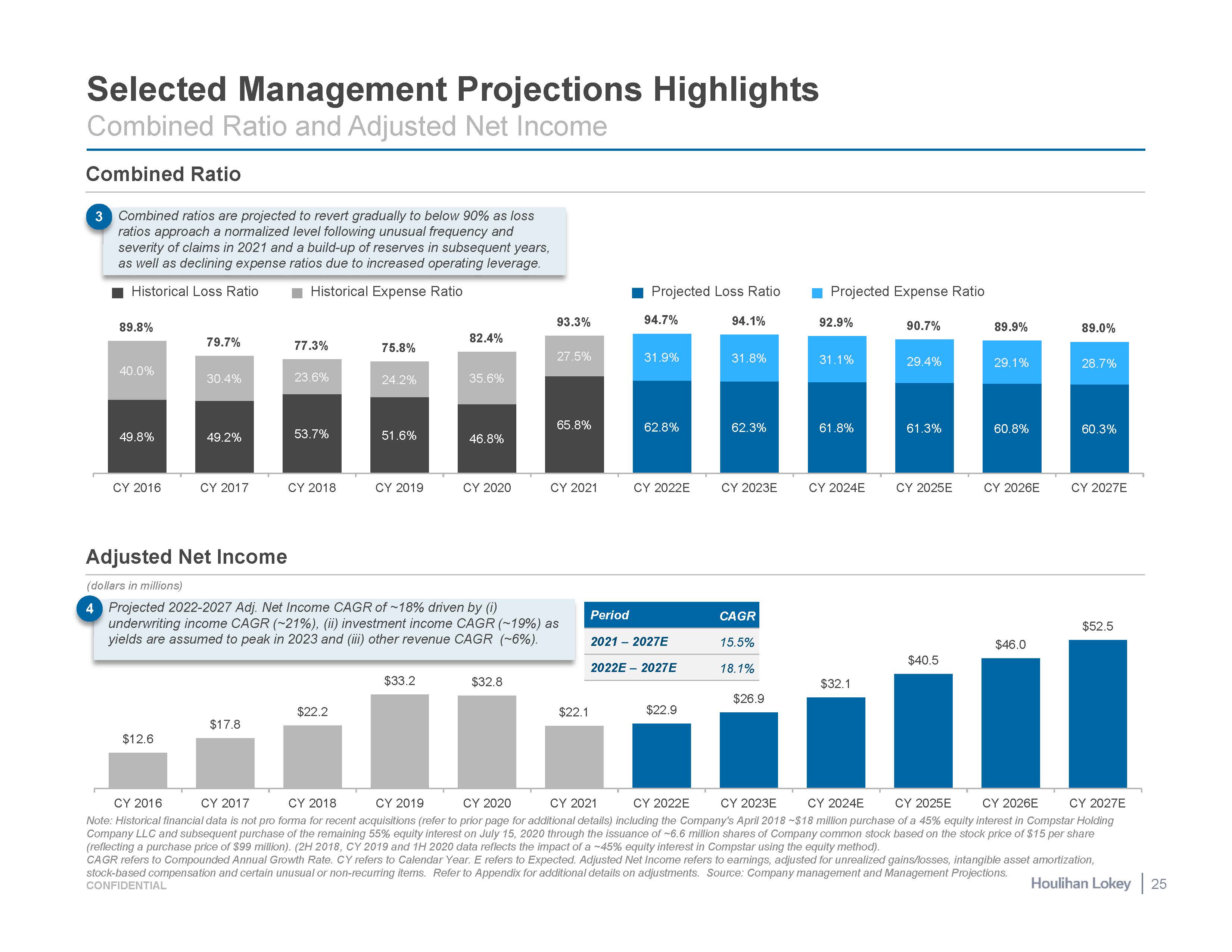

(dollars in millions) $17.8 $12.6 $22.2 $33.2 $32.8 $22.1 $22.9 $26.9 $32.1 $40.5 $46.0 $52.5 CY 2016 CY 2017 CY 2018 CY 2019 CY 2020 CY 2021 CY 2022E CY 2023E CY 2024E CY 2025E CY 2026E CY 2027E Note: Historical financial data is not pro forma for recent acquisitions (refer to prior page for additional details) including the Company's April 2018 ~$18 million purchase of a 45% equity interest in Compstar Holding Company LLC and subsequent purchase of the remaining 55% equity interest on July 15, 2020 through the issuance of ~6.6 million shares of Company common stock based on the stock price of $15 per share (reflecting a purchase price of $99 million). (2H 2018, CY 2019 and 1H 2020 data reflects the impact of a ~45% equity interest in Compstar using the equity method). CAGR refers to Compounded Annual Growth Rate. CY refers to Calendar Year. E refers to Expected. Adjusted Net Income refers to earnings, adjusted for unrealized gains/losses, intangible asset amortization, 49.8% 49.2% 53.7% 51.6% 46.8% 65.8% 62.8% 62.3% 61.8% 61.3% 60.8% 60.3% 40.0% 30.4% 23.6% 24.2% 35.6% 27.5% 31.1% 29.4% 29.1% 28.7% 89.8% 79.7% 77.3% 75.8% 82.4% 93.3% 92.9% 90.7% 89.9% 89.0% CY 2016 CY 2017 CY 2018 CY 2019 CY 2020 CY 2021 CY 2022E CY 2023E CY 2024E CY 2025E CY 2026E CY 2027E Selected Management Projections Highlights Combined Ratio and Adjusted Net Income Combined Ratio Adjusted Net Income Projected 2022-2027 Adj. Net Income CAGR of ~18% driven by (i) underwriting income CAGR (~21%), (ii) investment income CAGR (~19%) as yields are assumed to peak in 2023 and (iii) other revenue CAGR (~6%). 4 Period CAGR 2021 – 2027E 15.5% 2022E – 2027E 18.1% 3 Projected Loss Ratio 94.7% 94.1% 31.9% 31.8% Projected Expense Ratio Combined ratios are projected to revert gradually to below 90% as loss ratios approach a normalized level following unusual frequency and severity of claims in 2021 and a build-up of reserves in subsequent years, as well as declining expense ratios due to increased operating leverage. Historical Loss Ratio Historical Expense Ratio stock-based compensation and certain unusual or non-recurring items. Refer to Appendix for additional details on adjustments. Source: Company management and Management Projections. CONFIDENTIAL 25

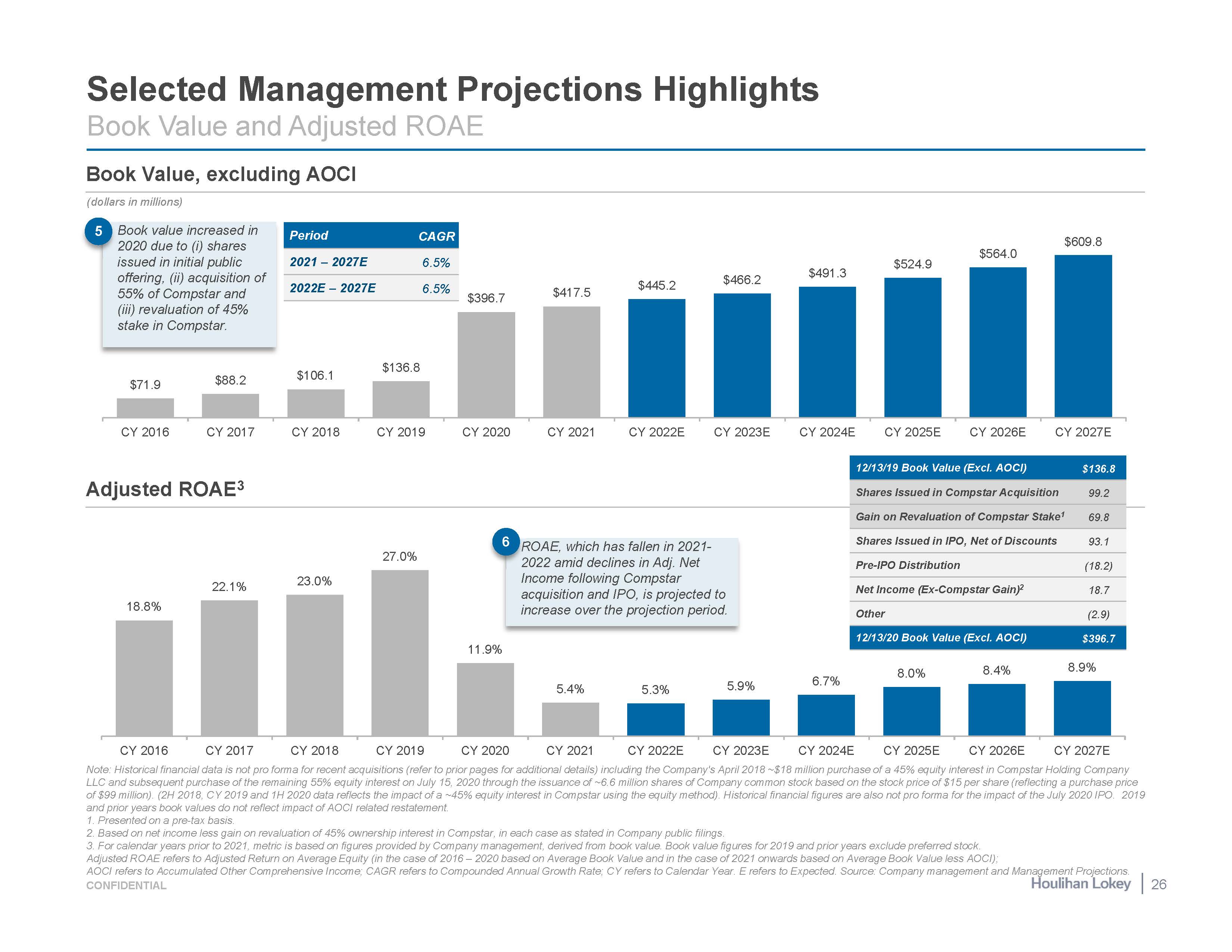

5.4% 5.3% 5.9% 6.7% 8.0% 8.4% 8.9% CY 2016 CY 2017 CY 2018 CY 2019 CY 2020 CY 2021 CY 2022E CY 2023E CY 2024E CY 2025E CY 2026E CY 2027E Note: Historical financial data is not pro forma for recent acquisitions (refer to prior pages for additional details) including the Company's April 2018 ~$18 million purchase of a 45% equity interest in Compstar Holding Company LLC and subsequent purchase of the remaining 55% equity interest on July 15, 2020 through the issuance of ~6.6 million shares of Company common stock based on the stock price of $15 per share (reflecting a purchase price of $99 million). (2H 2018, CY 2019 and 1H 2020 data reflects the impact of a ~45% equity interest in Compstar using the equity method). Historical financial figures are also not pro forma for the impact of the July 2020 IPO. 2019 and prior years book values do not reflect impact of AOCI related restatement. Presented on a pre-tax basis. Based on net income less gain on revaluation of 45% ownership interest in Compstar, in each case as stated in Company public filings. For calendar years prior to 2021, metric is based on figures provided by Company management, derived from book value. Book value figures for 2019 and prior years exclude preferred stock. Adjusted ROAE refers to Adjusted Return on Average Equity (in the case of 2016 – 2020 based on Average Book Value and in the case of 2021 onwards based on Average Book Value less AOCI); $71.9 $88.2 $106.1 $136.8 $396.7 $417.5 $445.2 $466.2 $491.3 $524.9 $564.0 $609.8 CY 2016 CY 2017 CY 2018 CY 2019 CY 2020 CY 2021 CY 2022E CY 2023E CY 2024E CY 2025E CY 2026E CY 2027E Selected Management Projections Highlights Book Value and Adjusted ROAE Book Value, excluding AOCI (dollars in millions) Period CAGR 2021 – 2027E 6.5% 2022E – 2027E 6.5% Book value increased in 2020 due to (i) shares issued in initial public offering, (ii) acquisition of 55% of Compstar and (iii) revaluation of 45% stake in Compstar. 5 R 2 Adjusted ROAE3 12/13/19 Book Value (Excl. AOCI) $136.8 Shares Issued in Compstar Acquisition 99.2 OAE, which has fallen in 2021- 022 amid declines in Adj. Net Income following Compstar acquisition and IPO, is projected to increase over the projection period. Gain on Revaluation of Compstar Stake1 69.8 18.8% 22.1% 23.0% 27.0% 6 Shares Issued in IPO, Net of Discounts 93.1 Pre-IPO Distribution (18.2) Net Income (Ex-Compstar Gain)2 18.7 Other (2.9) 11.9% 12/13/20 Book Value (Excl. AOCI) $396.7 AOCI refers to Accumulated Other Comprehensive Income; CAGR refers to Compounded Annual Growth Rate; CY refers to Calendar Year. E refers to Expected. Source: Company management and Management Projections. CONFIDENTIAL 26

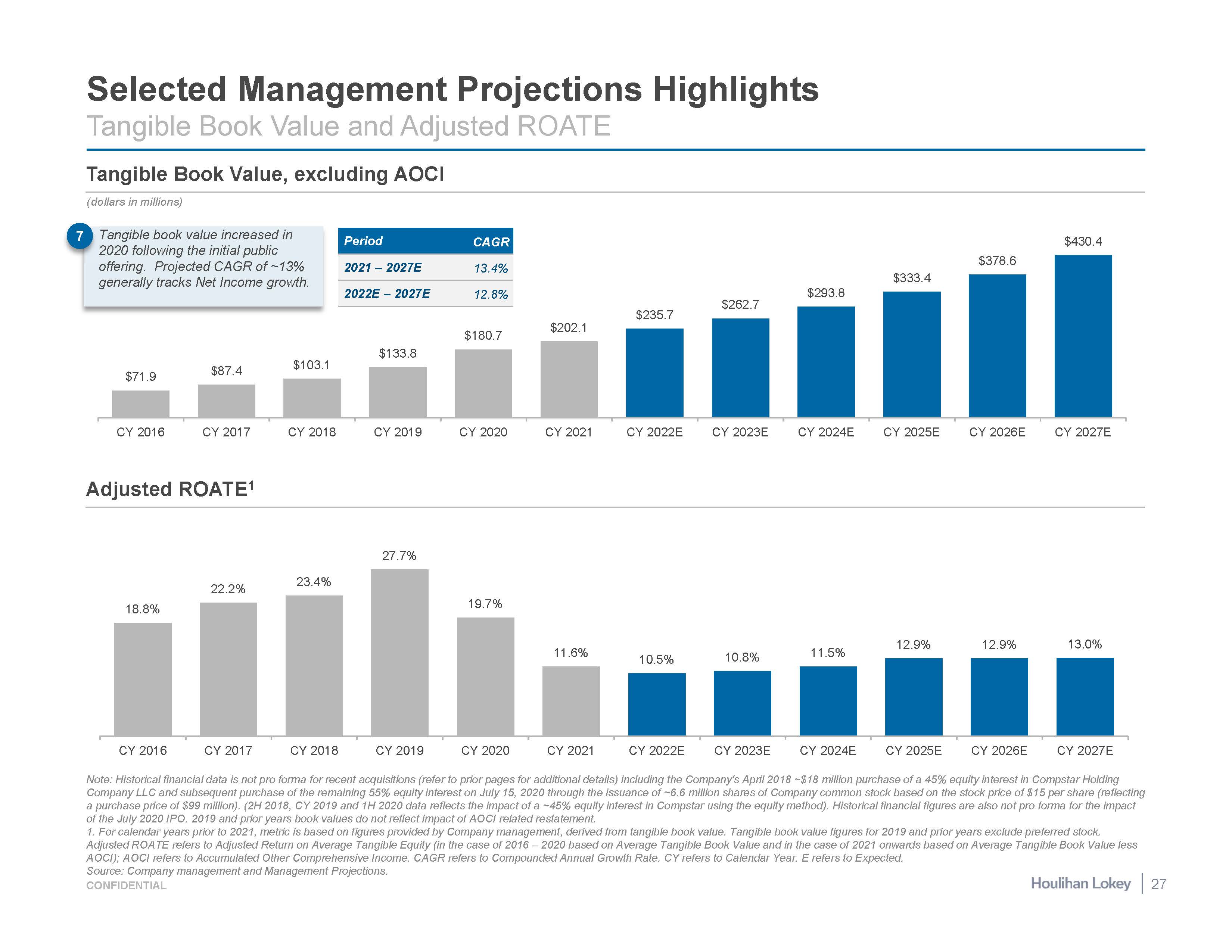

$71.9 $87.4 $103.1 $133.8 $180.7 $202.1 $235.7 $262.7 $293.8 $333.4 $378.6 $430.4 CY 2016 CY 2017 CY 2018 CY 2019 CY 2020 CY 2021 CY 2022E CY 2023E CY 2024E CY 2025E CY 2026E CY 2027E 18.8% 22.2% 23.4% 27.7% 19.7% 11.6% 10.5% 10.8% 11.5% 12.9% 12.9% 13.0% CY 2016 CY 2017 CY 2018 CY 2019 CY 2020 CY 2021 CY 2022E CY 2023E CY 2024E CY 2025E CY 2026E CY 2027E Note: Historical financial data is not pro forma for recent acquisitions (refer to prior pages for additional details) including the Company's April 2018 ~$18 million purchase of a 45% equity interest in Compstar Holding Company LLC and subsequent purchase of the remaining 55% equity interest on July 15, 2020 through the issuance of ~6.6 million shares of Company common stock based on the stock price of $15 per share (reflecting a purchase price of $99 million). (2H 2018, CY 2019 and 1H 2020 data reflects the impact of a ~45% equity interest in Compstar using the equity method). Historical financial figures are also not pro forma for the impact of the July 2020 IPO. 2019 and prior years book values do not reflect impact of AOCI related restatement. 1. For calendar years prior to 2021, metric is based on figures provided by Company management, derived from tangible book value. Tangible book value figures for 2019 and prior years exclude preferred stock. Adjusted ROATE refers to Adjusted Return on Average Tangible Equity (in the case of 2016 – 2020 based on Average Tangible Book Value and in the case of 2021 onwards based on Average Tangible Book Value less Selected Management Projections Highlights Tangible Book Value and Adjusted ROATE Tangible Book Value, excluding AOCI Adjusted ROATE1 (dollars in millions) Period CAGR 2021 – 2027E 13.4% 2022E – 2027E 12.8% Tangible book value increased in 2020 following the initial public offering. Projected CAGR of ~13% generally tracks Net Income growth. 7 AOCI); AOCI refers to Accumulated Other Comprehensive Income. CAGR refers to Compounded Annual Growth Rate. CY refers to Calendar Year. E refers to Expected. Source: Company management and Management Projections. CONFIDENTIAL 27

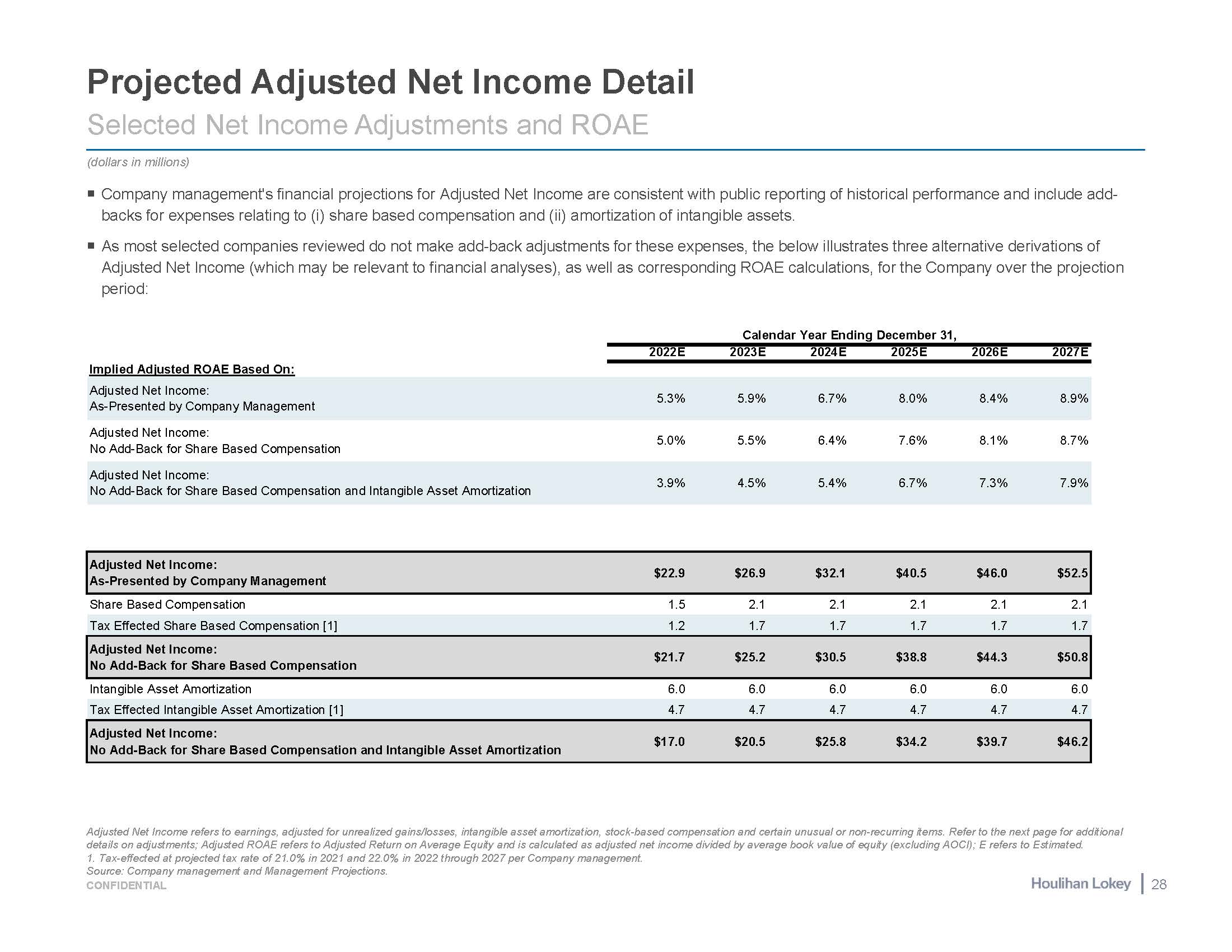

Projected Adjusted Net Income Detail Selected Net Income Adjustments and ROAE Adjusted Net Income refers to earnings, adjusted for unrealized gains/losses, intangible asset amortization, stock-based compensation and certain unusual or non-recurring items. Refer to the next page for additional details on adjustments; Adjusted ROAE refers to Adjusted Return on Average Equity and is calculated as adjusted net income divided by average book value of equity (excluding AOCI); E refers to Estimated. (dollars in millions) Company management's financial projections for Adjusted Net Income are consistent with public reporting of historical performance and include add- backs for expenses relating to (i) share based compensation and (ii) amortization of intangible assets. As most selected companies reviewed do not make add-back adjustments for these expenses, the below illustrates three alternative derivations of Adjusted Net Income (which may be relevant to financial analyses), as well as corresponding ROAE calculations, for the Company over the projection period: Tax Effected Share Based Compensation [1] 1.2 1.7 1.7 1.7 1.7 1.7 Adjusted Net Income: No Add-Back for Share Based Compensation $21.7 $25.2 $30.5 $38.8 $44.3 $50.8 Tax Effected Intangible Asset Amortization [1] 4.7 4.7 4.7 4.7 4.7 4.7 Adjusted Net Income: No Add-Back for Share Based Compensation and Intangible Asset Amortization $17.0 $20.5 $25.8 $34.2 $39.7 $46.2 As-Presented by Company Management No Add-Back for Share Based Compensation No Add-Back for Share Based Compensation and Intangible Asset Amortization Calendar Year Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E Implied Adjusted ROAE Based On: Adjusted Net Income: 5.3% 5.9% 6.7% 8.0% 8.4% 8.9% Adjusted Net Income: 5.0% 5.5% 6.4% 7.6% 8.1% 8.7% Adjusted Net Income: 3.9% 4.5% 5.4% 6.7% 7.3% 7.9% Adjusted Net Income: $22.9 $26.9 $32.1 $40.5 $46.0 $52.5 As-Presented by Company Management Share Based Compensation 1.5 2.1 2.1 2.1 2.1 2.1 Intangible Asset Amortization 6.0 6.0 6.0 6.0 6.0 6.0 1. Tax-effected at projected tax rate of 21.0% in 2021 and 22.0% in 2022 through 2027 per Company management. Source: Company management and Management Projections. CONFIDENTIAL 28

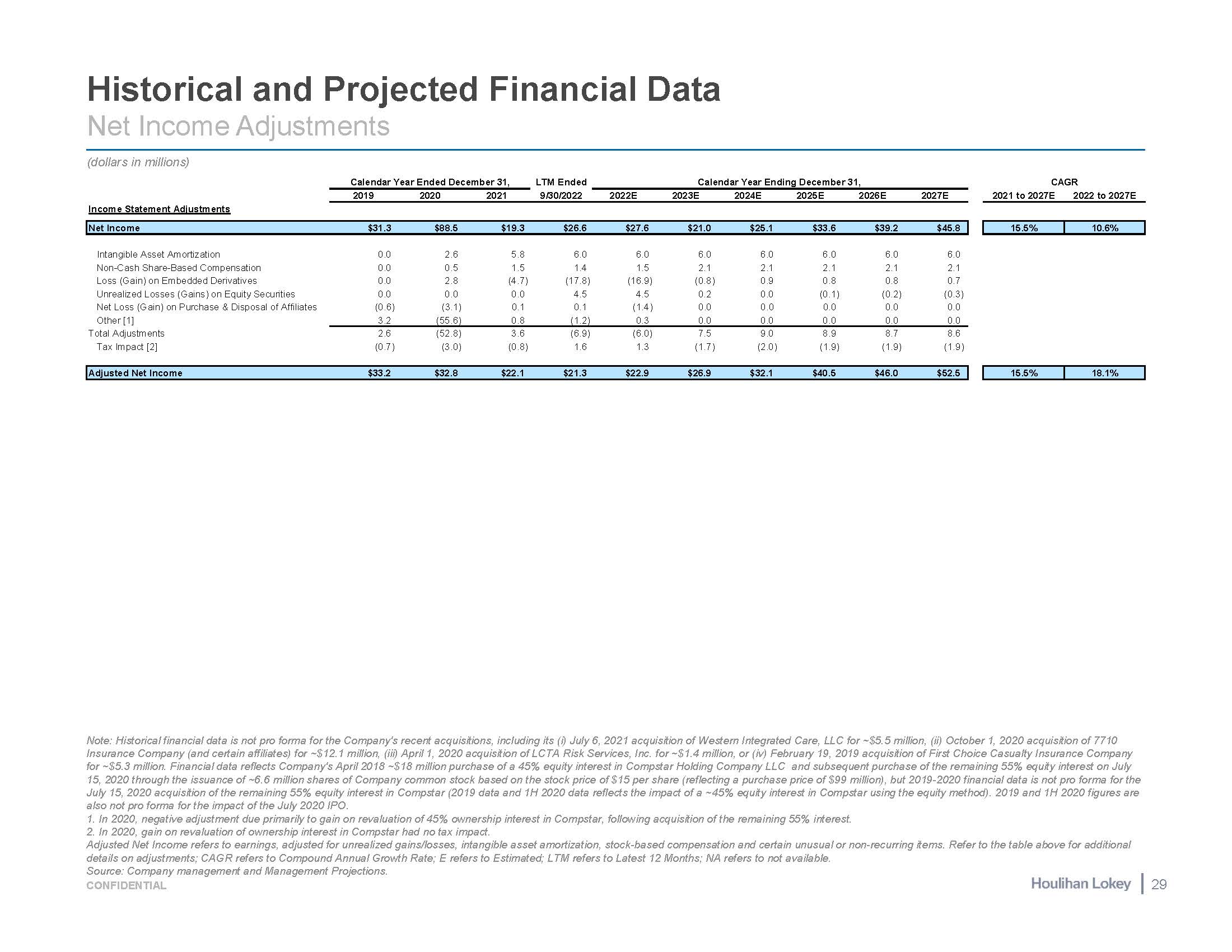

Historical and Projected Financial Data Net Income Adjustments Note: Historical financial data is not pro forma for the Company's recent acquisitions, including its (i) July 6, 2021 acquisition of Western Integrated Care, LLC for ~$5.5 million, (ii) October 1, 2020 acquisition of 7710 Insurance Company (and certain affiliates) for ~$12.1 million, (iii) April 1, 2020 acquisition of LCTA Risk Services, Inc. for ~$1.4 million, or (iv) February 19, 2019 acquisition of First Choice Casualty Insurance Company for ~$5.3 million. Financial data reflects Company's April 2018 ~$18 million purchase of a 45% equity interest in Compstar Holding Company LLC and subsequent purchase of the remaining 55% equity interest on July 15, 2020 through the issuance of ~6.6 million shares of Company common stock based on the stock price of $15 per share (reflecting a purchase price of $99 million), but 2019-2020 financial data is not pro forma for the July 15, 2020 acquisition of the remaining 55% equity interest in Compstar (2019 data and 1H 2020 data reflects the impact of a ~45% equity interest in Compstar using the equity method). 2019 and 1H 2020 figures are also not pro forma for the impact of the July 2020 IPO. In 2020, negative adjustment due primarily to gain on revaluation of 45% ownership interest in Compstar, following acquisition of the remaining 55% interest. In 2020, gain on revaluation of ownership interest in Compstar had no tax impact. Adjusted Net Income refers to earnings, adjusted for unrealized gains/losses, intangible asset amortization, stock-based compensation and certain unusual or non-recurring items. Refer to the table above for additional (dollars in millions) Calendar Year Ended December 31, LTM Ended Calendar Year Ending December 31, CAGR 2019 2020 2021 9/30/2022 2022E 2023E 2024E 2025E 2026E 2027E 2021 to 2027E 2022 to 2027E Income Statement Adjustments Net Income $31.3 $88.5 $19.3 $26.6 $27.6 $21.0 $25.1 $33.6 $39.2 $45.8 15.5% 10.6% Intangible Asset Amortization 0.0 2.6 5.8 6.0 6.0 6.0 6.0 6.0 6.0 6.0 Non-Cash Share-Based Compensation 0.0 0.5 1.5 1.4 1.5 2.1 2.1 2.1 2.1 2.1 Loss (Gain) on Embedded Derivatives 0.0 2.8 (4.7) (17.8) (16.9) (0.8) 0.9 0.8 0.8 0.7 Unrealized Losses (Gains) on Equity Securities 0.0 0.0 0.0 4.5 4.5 0.2 0.0 (0.1) (0.2) (0.3) Net Loss (Gain) on Purchase & Disposal of Affiliates (0.6) (3.1) 0.1 0.1 (1.4) 0.0 0.0 0.0 0.0 0.0 Other [1] 3.2 (55.6) 0.8 (1.2) 0.3 0.0 0.0 0.0 0.0 0.0 Total Adjustments 2.6 (52.8) 3.6 (6.9) (6.0) 7.5 9.0 8.9 8.7 8.6 Tax Impact [2] (0.7) (3.0) (0.8) 1.6 1.3 (1.7) (2.0) (1.9) (1.9) (1.9) Adjusted Net Income $33.2 $32.8 $22.1 $21.3 $22.9 $26.9 $32.1 $40.5 $46.0 $52.5 15.5% 18.1% details on adjustments; CAGR refers to Compound Annual Growth Rate; E refers to Estimated; LTM refers to Latest 12 Months; NA refers to not available. Source: Company management and Management Projections. CONFIDENTIAL 29

Page 3 5 10 20 21 23 Executive Summary Selected Updates Since Prior Discussion Materials Financial Analyses Appendices Selected Cost of Equity Considerations Supplemental Financial Information Illustrative Selected Company Multiple Trendlines 30 Supplemental Public Company & Market Observations 33

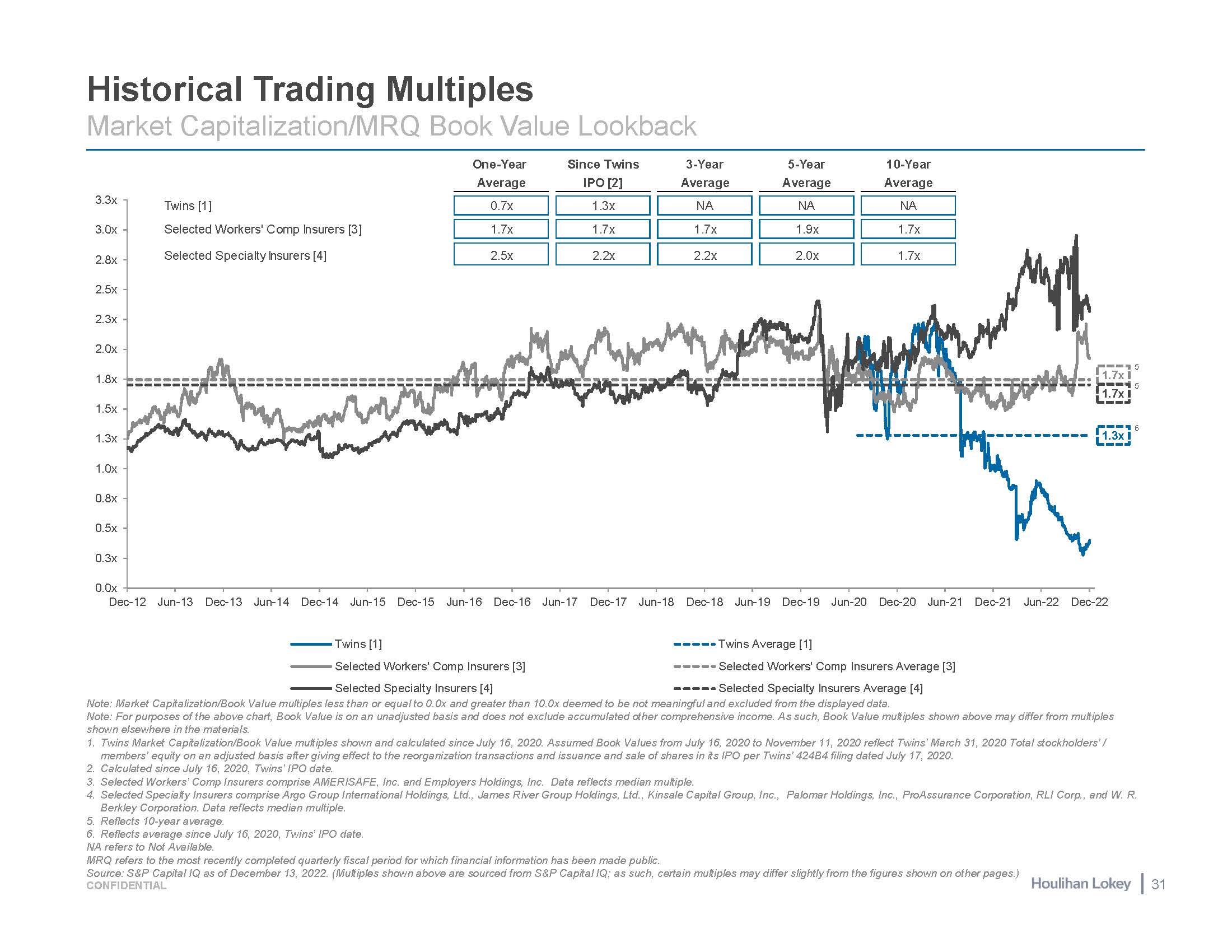

1.7x 1.7x 1.0x 0.8x 0.5x 0.3x 0.0x 1.3x 1.5x 1.8x 2.5x 2.3x 2.0x 2.8x 3.0x 3.3x Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-21 Jun-22 Dec-22 Twins [1] Selected Workers' Comp Insurers [3] Selected Specialty Insurers [4] Dec-18 Jun-19 Dec-19 Jun-20 Dec-20 Jun-21 Twins Average [1] Selected Workers' Comp Insurers Average [3] Selected Specialty Insurers Average [4] Source: S&P Capital IQ as of December 13, 2022. (Multiples shown above are sourced from S&P Capital IQ; as such, certain multiples may differ slightly from the figures shown on other pages.) CONFIDENTIAL 31 Historical Trading Multiples Market Capitalization/MRQ Book Value Lookback Note: Market Capitalization/Book Value multiples less than or equal to 0.0x and greater than 10.0x deemed to be not meaningful and excluded from the displayed data. Note: For purposes of the above chart, Book Value is on an unadjusted basis and does not exclude accumulated other comprehensive income. As such, Book Value multiples shown above may differ from multiples shown elsewhere in the materials. Twins Market Capitalization/Book Value multiples shown and calculated since July 16, 2020. Assumed Book Values from July 16, 2020 to November 11, 2020 reflect Twins’ March 31, 2020 Total stockholders’ / members’ equity on an adjusted basis after giving effect to the reorganization transactions and issuance and sale of shares in its IPO per Twins’ 424B4 filing dated July 17, 2020. Calculated since July 16, 2020, Twins’ IPO date. Selected Workers’ Comp Insurers comprise AMERISAFE, Inc. and Employers Holdings, Inc. Data reflects median multiple. Selected Specialty Insurers comprise Argo Group International Holdings, Ltd., James River Group Holdings, Ltd., Kinsale Capital Group, Inc., Palomar Holdings, Inc., ProAssurance Corporation, RLI Corp., and W. R. Berkley Corporation. Data reflects median multiple. Reflects 10-year average. Reflects average since July 16, 2020, Twins’ IPO date. NA refers to Not Available. MRQ refers to the most recently completed quarterly fiscal period for which financial information has been made public. One-Year Average Since Twins IPO [2] 3-Year Average 5-Year Average 10-Year Average Twins [1] Selected Workers' Comp Insurers [3] Selected Specialty Insurers [4] 0.7x 1.3x NA NA NA 1.7x 1.7x 1.7x 1.9x 1.7x 2.5x 2.2x 2.2x 2.0x 1.7x 6 1.3x 5 5

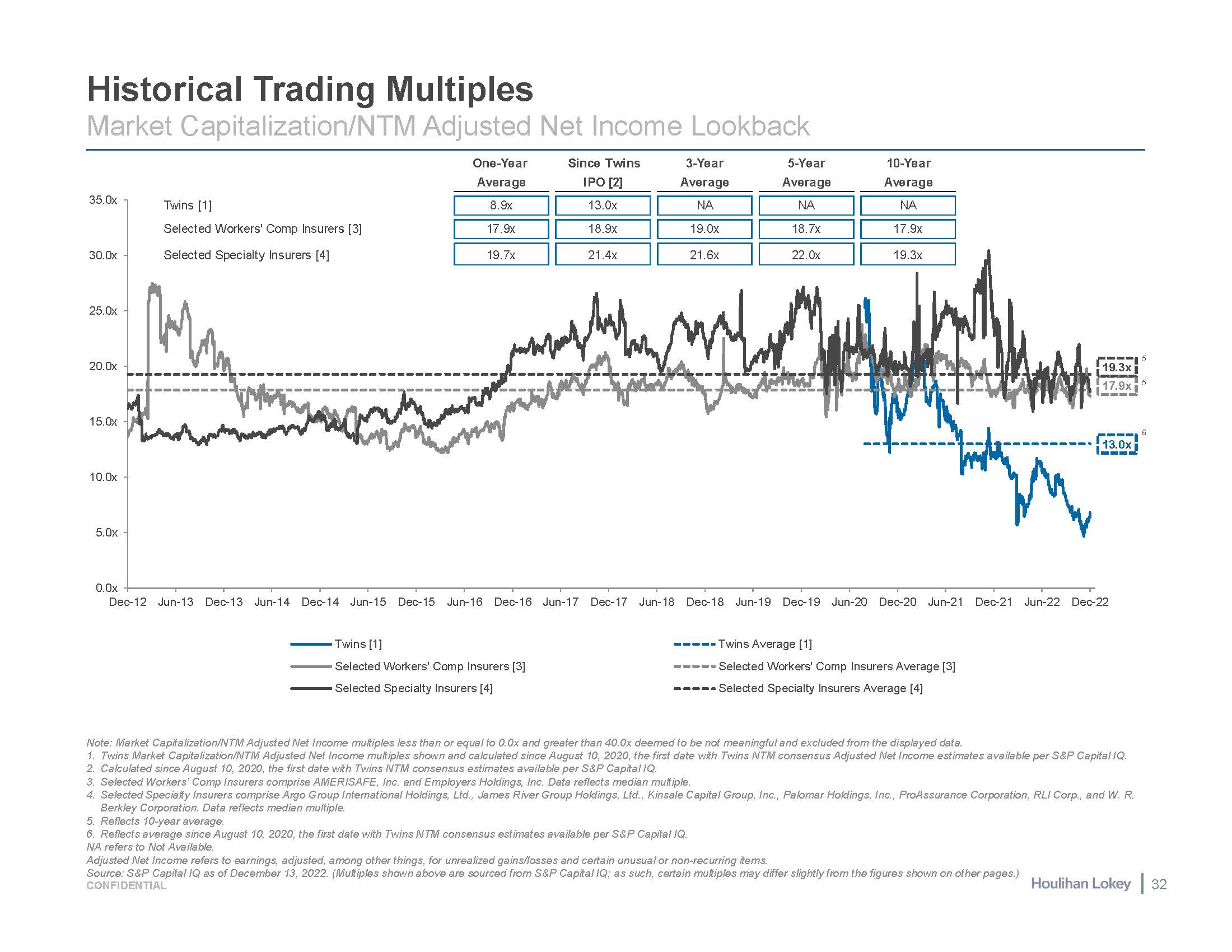

Historical Trading Multiples Market Capitalization/NTM Adjusted Net Income Lookback Note: Market Capitalization/NTM Adjusted Net Income multiples less than or equal to 0.0x and greater than 40.0x deemed to be not meaningful and excluded from the displayed data. Twins Market Capitalization/NTM Adjusted Net Income multiples shown and calculated since August 10, 2020, the first date with Twins NTM consensus Adjusted Net Income estimates available per S&P Capital IQ. Calculated since August 10, 2020, the first date with Twins NTM consensus estimates available per S&P Capital IQ. Selected Workers’ Comp Insurers comprise AMERISAFE, Inc. and Employers Holdings, Inc. Data reflects median multiple. Selected Specialty Insurers comprise Argo Group International Holdings, Ltd., James River Group Holdings, Ltd., Kinsale Capital Group, Inc., Palomar Holdings, Inc., ProAssurance Corporation, RLI Corp., and W. R. Berkley Corporation. Data reflects median multiple. Reflects 10-year average. Reflects average since August 10, 2020, the first date with Twins NTM consensus estimates available per S&P Capital IQ. NA refers to Not Available. Adjusted Net Income refers to earnings, adjusted, among other things, for unrealized gains/losses and certain unusual or non-recurring items. 6 13.0x 5 19.3x 17.9x 5 0.0x Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20 Dec-20 Jun-21 Dec-21 Jun-22 Dec-22 5.0x 10.0x 15.0x 20.0x 25.0x 30.0x 35.0x Twins [1] Selected Workers' Comp Insurers [3] Selected Specialty Insurers [4] Twins Average [1] Selected Workers' Comp Insurers Average [3] Selected Specialty Insurers Average [4] One-Year Average Source: S&P Capital IQ as of December 13, 2022. (Multiples shown above are sourced from S&P Capital IQ; as such, certain multiples may differ slightly from the figures shown on other pages.) CONFIDENTIAL 31 Since Twins IPO [2] 3-Year Average 5-Year Average 10-Year Average Twins [1] Selected Workers' Comp Insurers [3] Selected Specialty Insurers [4] 8.9x 13.0x NA NA NA 17.9x 18.9x 19.0x 18.7x 17.9x 19.7x 21.4x 21.6x 22.0x 19.3x

Page 3 5 10 20 21 23 30 Executive Summary Selected Updates Since Prior Discussion Materials Financial Analyses Appendices Selected Cost of Equity Considerations Supplemental Financial Information Illustrative Selected Company Multiple Trendlines Supplemental Public Company & Market Observations 33

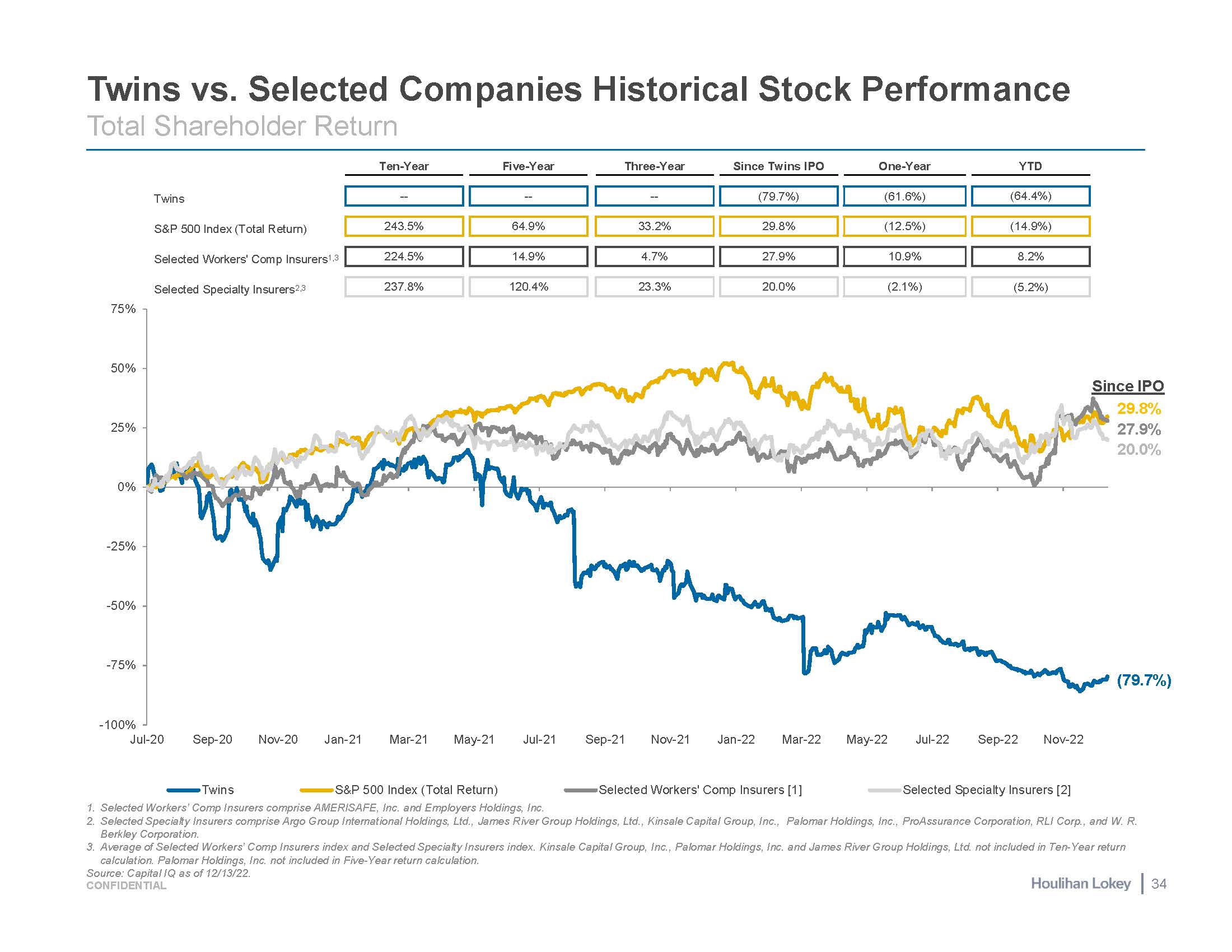

Twins vs. Selected Companies Historical Stock Performance (79.7%) 29.8% 27.9% 20.0% -- -- -- (79.7%) (61.6%) (64.4%) 243.5% 64.9% 33.2% 29.8% (12.5%) (14.9%) 224.5% 14.9% 4.7% 27.9% 10.9% 8.2% 237.8% 120.4% 23.3% 20.0% (2.1%) (5.2%) Since IPO Total Shareholder Return Ten-Year Five-Year Three-Year Since Twins IPO One-Year YTD Twins S&P 500 Index (Total Return) Selected Workers' Comp Insurers1,3 Selected Specialty Insurers2,3 75% -100% -75% -50% -25% 0% 25% 50% Jul-20 Sep-20 Nov-20 Jan-21 Mar-21 May-21 Jul-21 Sep-21 Nov-21 Jan-22 Mar-22 May-22 Jul-22 Sep-22 Nov-22 Twins S&P 500 Index (Total Return) Selected Workers' Comp Insurers [1] Selected Specialty Insurers [2] Selected Workers’ Comp Insurers comprise AMERISAFE, Inc. and Employers Holdings, Inc. Selected Specialty Insurers comprise Argo Group International Holdings, Ltd., James River Group Holdings, Ltd., Kinsale Capital Group, Inc., Palomar Holdings, Inc., ProAssurance Corporation, RLI Corp., and W. R. Berkley Corporation. Average of Selected Workers’ Comp Insurers index and Selected Specialty Insurers index. Kinsale Capital Group, Inc., Palomar Holdings, Inc. and James River Group Holdings, Ltd. not included in Ten-Year return calculation. Palomar Holdings, Inc. not included in Five-Year return calculation. Source: Capital IQ as of 12/13/22. 34 CONFIDENTIAL

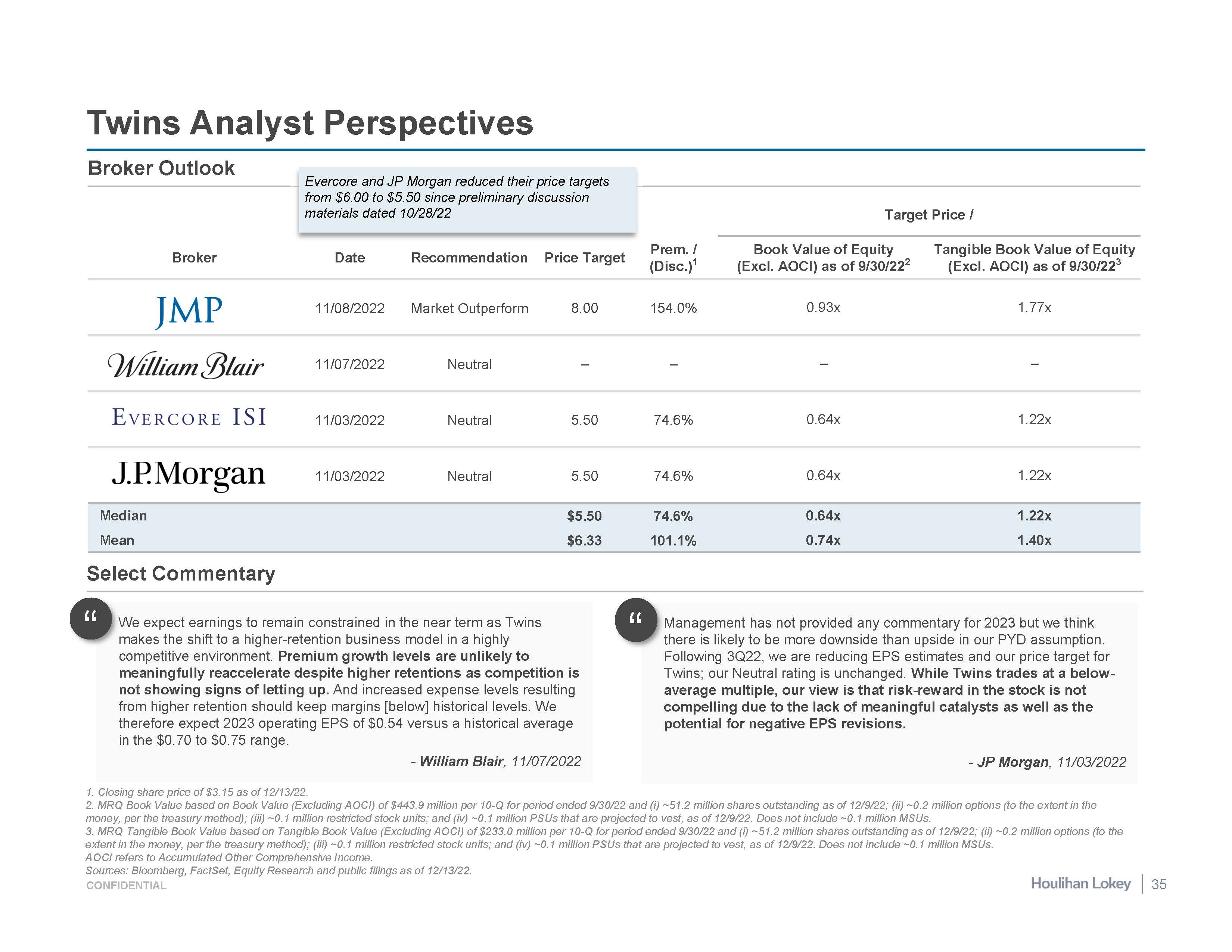

Twins Analyst Perspectives M t anagement has not provided any commentary for 2023 but we think here is likely to be more downside than upside in our PYD assumption. Following 3Q22, we are reducing EPS estimates and our price target for Twins; our Neutral rating is unchanged. While Twins trades at a below- average multiple, our view is that risk-reward in the stock is not compelling due to the lack of meaningful catalysts as well as the potential for negative EPS revisions. - JP Morgan, 11/03/2022 “ Target Price / Broker Date Recommendation Price Target Prem. / (Disc.)1 Book Value of Equity (Excl. AOCI) as of 9/30/222 Tangible Book Value of Equity (Excl. AOCI) as of 9/30/223 11/08/2022 Market Outperform 8.00 154.0% 0.93x 1.77x 11/07/2022 Neutral – – – – 11/03/2022 Neutral 5.50 74.6% 0.64x 1.22x 11/03/2022 Neutral 5.50 74.6% 0.64x 1.22x Median $5.50 74.6% 0.64x 1.22x Mean $6.33 101.1% 0.74x 1.40x Closing share price of $3.15 as of 12/13/22. MRQ Book Value based on Book Value (Excluding AOCI) of $443.9 million per 10-Q for period ended 9/30/22 and (i) ~51.2 million shares outstanding as of 12/9/22; (ii) ~0.2 million options (to the extent in the money, per the treasury method); (iii) ~0.1 million restricted stock units; and (iv) ~0.1 million PSUs that are projected to vest, as of 12/9/22. Does not include ~0.1 million MSUs. MRQ Tangible Book Value based on Tangible Book Value (Excluding AOCI) of $233.0 million per 10-Q for period ended 9/30/22 and (i) ~51.2 million shares outstanding as of 12/9/22; (ii) ~0.2 million options (to the extent in the money, per the treasury method); (iii) ~0.1 million restricted stock units; and (iv) ~0.1 million PSUs that are projected to vest, as of 12/9/22. Does not include ~0.1 million MSUs. AOCI refers to Accumulated Other Comprehensive Income. Sources: Bloomberg, FactSet, Equity Research and public filings as of 12/13/22. Select Commentary Broker Outlook m We expect earnings to remain constrained in the near term as Twins akes the shift to a higher-retention business model in a highly competitive environment. Premium growth levels are unlikely to meaningfully reaccelerate despite higher retentions as competition is not showing signs of letting up. And increased expense levels resulting from higher retention should keep margins [below] historical levels. We therefore expect 2023 operating EPS of $0.54 versus a historical average in the $0.70 to $0.75 range. - William Blair, 11/07/2022 “ 34 CONFIDENTIAL Evercore and JP Morgan reduced their price targets from $6.00 to $5.50 since preliminary discussion materials dated 10/28/22

Last Twelve Months Last Six Months Last Three Months Since Release of 3Q Earnings (11/2/22 After Hours) Volume1: 15.2 million (67.8% of float)2 Twins Selected Historical Trading Activity Volume1: 9.0 million (40.0% of float)2 Volume1: 35.1 million (156.7% of float)2 Volume1: 4.7 million (20.8% of float)2 Based on VWAP volume, per Bloomberg. Public float calculated as total shares less primarily shares held by Angels and Company insiders. ADTV refers to Average Daily Trading Volume. VWAP refers to Volume-Weighted Average Price. Selected VWAP Data 52-Week Range 12-Month 9-Month 6-Month 3-Month 30-Day 20-Day 10-Day 5-Day $2.18 – $9.16 $4.77 $4.42 $4.10 $3.02 $2.64 $2.60 $2.87 $2.96 Current Trading Stats: Float2: 22.4mm (43.8% of common) 90-Day ADTV: 138k 90-Day Avg. Value Traded: $0.5mm 12.6% 34.3% 17.6% 6.2% 15.1% 7.8% 6.2% 0.2% $2.00- $3.00- $4.00- $5.00- $6.00- $7.00- $8.00- $9.00- $2.00- $3.00- $4.00- $5.00- $6.00- $7.00- $8.00- $9.00- $2.99 $3.99 $4.99 $5.99 $6.99 $7.99 $8.99 $9.99 $2.99 $3.99 $4.99 $5.99 $6.99 $7.99 $8.99 $9.99 29.1% 29.9% 11.7% 10.2% 19.1% 0.0% 0.0% 0.0% 49.3% 50.7% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% $2.00- $2.99 $3.00- $3.99 $4.00- $4.99 $5.00- $5.99 $6.00- $6.99 $7.00- $7.99 $8.00- $8.99 $9.00- $9.99 95.0% Source: Bloomberg as of 12/13/22. CONFIDENTIAL 36 5.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% $2.00- $2.99 $3.00- $3.99 $4.00- $4.99 $5.00- $5.99 $6.00- $6.99 $7.00- $7.99 $8.00- $8.99 $9.00- $9.99

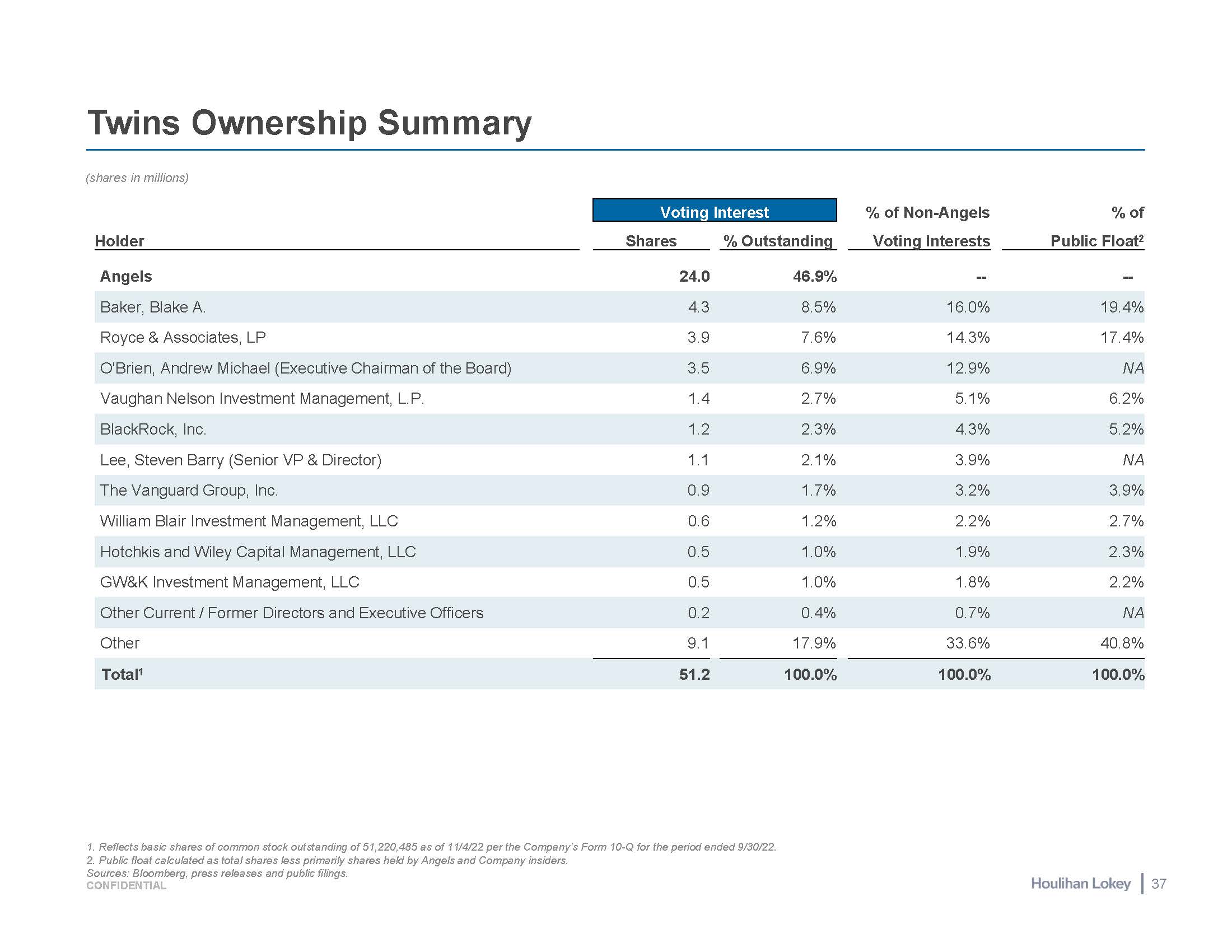

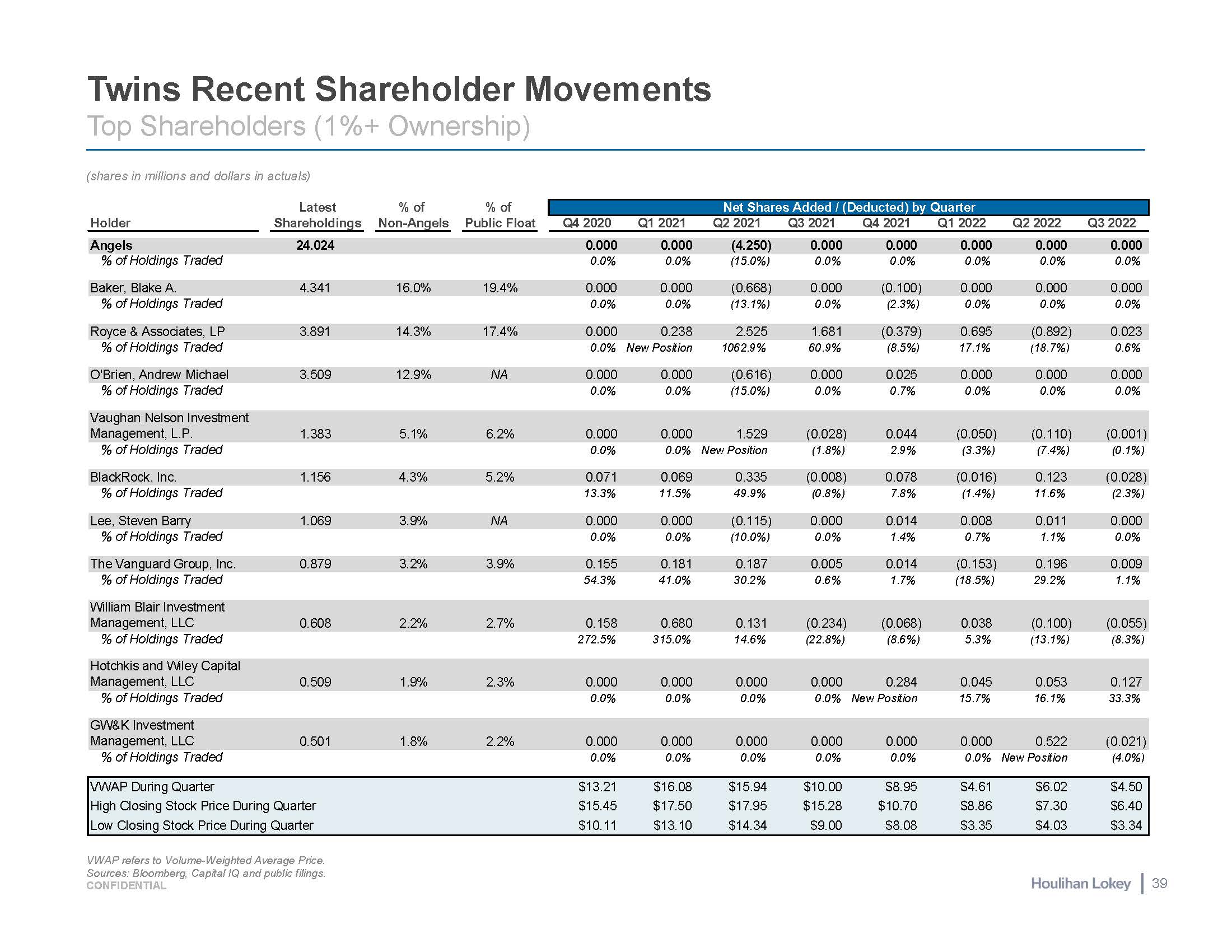

Twins Ownership Summary (shares in millions) Reflects basic shares of common stock outstanding of 51,220,485 as of 11/4/22 per the Company’s Form 10-Q for the period ended 9/30/22. Public float calculated as total shares less primarily shares held by Angels and Company insiders. Holder Shares % Outstanding Voting Interests Public Float2 Angels 24.0 46.9% -- -- Baker, Blake A. 4.3 8.5% 16.0% 19.4% Royce & Associates, LP 3.9 7.6% 14.3% 17.4% O'Brien, Andrew Michael (Executive Chairman of the Board) 3.5 6.9% 12.9% NA Vaughan Nelson Investment Management, L.P. 1.4 2.7% 5.1% 6.2% BlackRock, Inc. 1.2 2.3% 4.3% 5.2% Lee, Steven Barry (Senior VP & Director) 1.1 2.1% 3.9% NA The Vanguard Group, Inc. 0.9 1.7% 3.2% 3.9% William Blair Investment Management, LLC 0.6 1.2% 2.2% 2.7% Hotchkis and Wiley Capital Management, LLC 0.5 1.0% 1.9% 2.3% GW&K Investment Management, LLC 0.5 1.0% 1.8% 2.2% Other Current / Former Directors and Executive Officers 0.2 0.4% 0.7% NA Other 9.1 17.9% 33.6% 40.8% Total1 51.2 100.0% 100.0% 100.0% Voting Interest Sources: Bloomberg, press releases and public filings. CONFIDENTIAL 37 % of Non-Angels % of

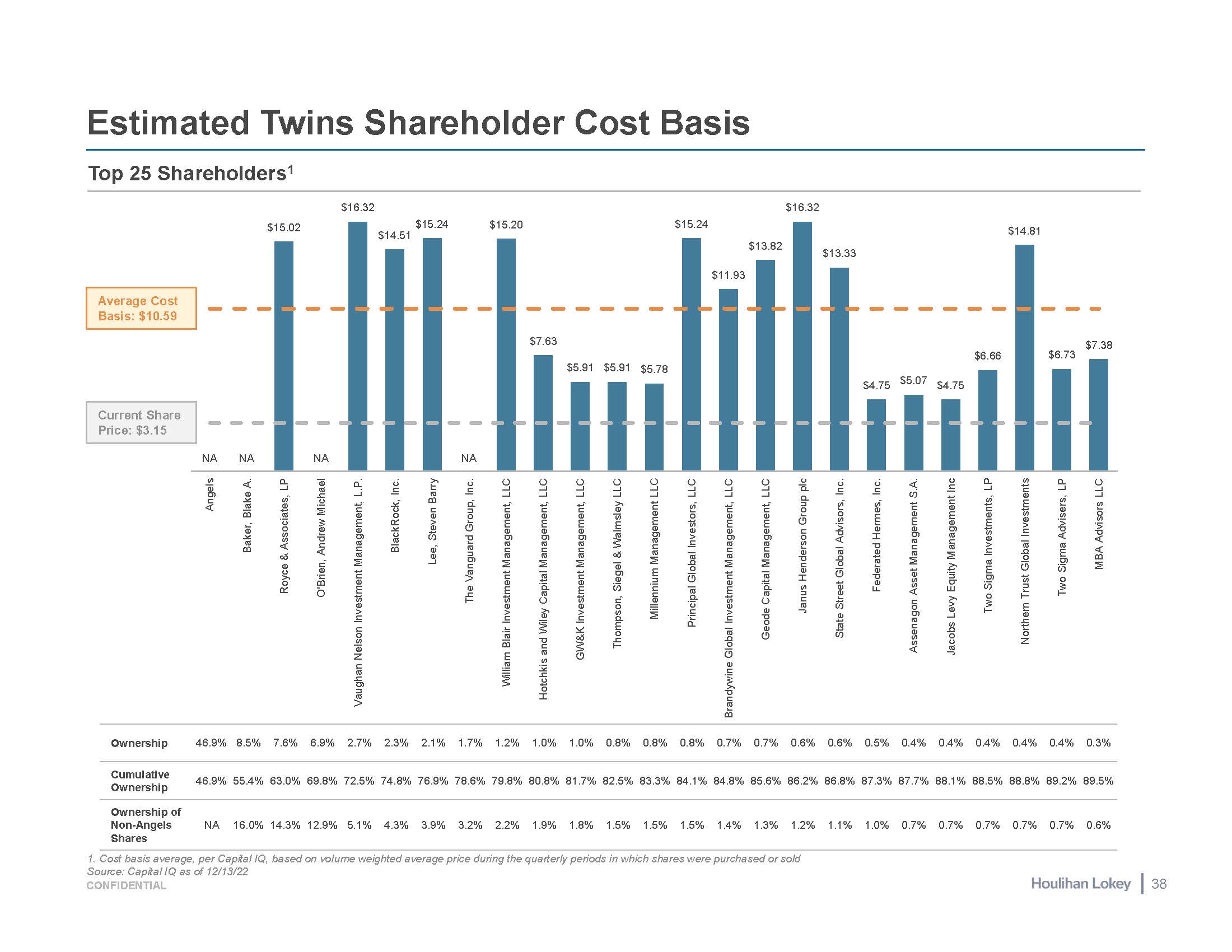

Estimated Twins Shareholder Cost Basis Current Share Price: $3.15 1. Cost basis average, per Capital IQ, based on volume weighted average price during the quarterly periods in which shares were purchased or sold Source: Capital IQ as of 12/13/22 Ownership 46.9% 8.5% 7.6% 6.9% 2.7% 2.3% 2.1% 1.7% 1.2% 1.0% 1.0% 0.8% 0.8% 0.8% 0.7% 0.7% 0.6% 0.6% 0.5% 0.4% 0.4% 0.4% 0.4% 0.4% 0.3% Cumulative Ownership 46.9% 55.4% 63.0% 69.8% 72.5% 74.8% 76.9% 78.6% 79.8% 80.8% 81.7% 82.5% 83.3% 84.1% 84.8% 85.6% 86.2% 86.8% 87.3% 87.7% 88.1% 88.5% 88.8% 89.2% 89.5% Ownership of Non-Angels Shares NA 16.0% 14.3% 12.9% 5.1% 4.3% 3.9% 3.2% 2.2% 1.9% 1.8% 1.5% 1.5% 1.5% 1.4% 1.3% 1.2% 1.1% 1.0% 0.7% 0.7% 0.7% 0.7% 0.7% 0.6% Average Cost Basis: $10.59 Top 25 Shareholders1 NA 38 CONFIDENTIAL NA $15.02 NA $16.32 $15.24 $14.51 NA $15.20 $7.63 $5.91 $5.91 $5.78 $15.24 $11.93 $13.82 $16.32 $13.33 $4.75 $5.07 $4.75 $6.66 $14.81 $6.73 $7.38 Angels Baker, Blake A. Royce & Associates, LP O'Brien, Andrew Michael Vaughan Nelson Investment Management, L.P. BlackRock, Inc. Lee, Steven Barry The Vanguard Group, Inc. William Blair Investment Management, LLC Hotchkis and Wiley Capital Management, LLC GW&K Investment Management, LLC Thompson, Siegel & Walmsley LLC Millennium Management LLC Principal Global Investors, LLC Brandywine Global Investment Management, LLC Geode Capital Management, LLC Janus Henderson Group plc State Street Global Advisors, Inc. Federated Hermes, Inc. Assenagon Asset Management S.A. Jacobs Levy Equity Management Inc Two Sigma Investments, LP Northern Trust Global Investments Two Sigma Advisers, LP MBA Advisors LLC