Table of Contents

As filed with the Securities and Exchange Commission on December 17, 2021

Registration No. 333-259887

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2 TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CLAIRE’S HOLDINGS LLC

to be converted as described herein into a corporation named

CLAIRE’S INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 5600 | 36-4609619 | ||

| (State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) | ||

2400 West Central Road (847) 765-1100 | ||||

| (Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices) | ||||

Brendan McKeough Claire’s Holdings LLC (847) 765-4319 |

| (Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service) |

| Copies to: | ||

John B. Meade, Esq. Pedro J. Bermeo, Esq. | Craig E. Marcus, Esq. (617) 951-7000 | |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||||

| Emerging growth company | ☒ | |||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| ||||

| Title Of Each Class Of Securities To Be Registered | Proposed Maximum Aggregate Offering Price(1)(2) | Amount Of Registration Fee(3) | ||

Common stock, par value $0.01 per share | $100,000,000 | $9,270 | ||

| ||||

| ||||

| (1) | Includes additional shares of common stock which the underwriters have the right to purchase to cover over-allotments. |

| (2) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to 457(o) under the Securities Act of 1933, as amended. |

| (3) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

Claire’s Holdings LLC, the registrant whose name appears on the cover of this registration statement, is a Delaware limited liability company. Prior to the effectiveness of this registration statement, Claire’s Holdings LLC will convert into a Delaware corporation pursuant to a statutory conversion and change its name to Claire’s Inc. as described in the section captioned “Corporate Conversion” of the accompanying prospectus. Except as disclosed in the prospectus, the historical consolidated financial statements and selected historical consolidated financial data and other financial information included in this registration statement are those of Claire’s Holdings LLC, and do not give effect to the Corporate Conversion. Shares of the common stock of Claire’s Inc. are being offered by the prospectus included in this registration statement.

i

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED DECEMBER 17, 2021

PRELIMINARY PROSPECTUS

Shares

Claire’s Inc.

Common Stock

This is the initial public offering of shares of common stock of Claire’s Inc.

We are offering shares of common stock in this offering, and if the underwriters exercise their option to purchase additional shares of common stock, we will sell up to additional shares of common stock and the selling stockholders identified in this prospectus will sell up to additional shares of common stock. We will not receive any proceeds from any sale of shares of common stock by the selling stockholders pursuant to the underwriters’ option to purchase additional shares. Prior to this offering, there has been no public market for our common stock. We anticipate that the initial public offering price will be between $ and $ per share. We have applied to list our common stock on the New York Stock Exchange under the symbol “CLRS”.

After giving effect to the Corporate Conversion (as defined in this prospectus), and the completion of this offering, affiliates of each of Elliott Investment Management L.P. (together with its affiliates, “Elliott”) and Monarch Alternative Capital LP (“Monarch”) will control approximately % and %, respectively, of the outstanding voting power of our company (assuming no exercise of the underwriters’ option to purchase additional shares of common stock from us or the selling stockholders). As such, each of Elliott and Monarch may individually have the ability to exercise significant influence over all corporate actions requiring stockholder approval, irrespective of how our other stockholders may vote, and may have interests that may not align with the interests of each other or of our other stockholders. See “Risk Factors—Risks related to our common stock and this offering—Affiliates of each of Elliott Investment Management L.P. and Monarch Alternative Capital LP may each continue to have significant influence over us after this offering, which could limit your ability to influence the outcome of matters submitted to stockholders for a vote.”

The underwriters have a 30-day option to purchase up to additional shares of common stock from us and up to additional shares of common stock from the selling stockholders at the initial public offering price, less the underwriting discounts and commissions.

| Price to Public | Underwriting Discounts and Commissions(1) | Proceeds before Expenses, to Us(2) | Proceeds before Expenses, to the Selling Stockholders(3) | |||||||||||||

Per Share | $ | $ | $ | $ | ||||||||||||

Total | $ | $ | $ | $ | ||||||||||||

| (1) | See “Underwriting (Conflicts of Interest)” for a description of all compensation payable to the underwriters. |

| (2) | Assumes no exercise of the underwriters’ option to purchase additional shares of common stock from us. |

| (3) | Assumes the exercise in full of the underwriters’ option to purchase additional shares of common stock from the selling stockholders. |

Investing in our common stock involves risks.

See “Risk Factors” beginning on page 26.

We are an “emerging growth company” as defined under the federal securities laws and, as such, may elect, and have elected, to comply with certain reduced public company reporting requirements for future filings. See “Prospectus Summary—Implications of Being an Emerging Growth Company.”

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2022.

Joint Book-Running Managers

| Goldman Sachs & Co. LLC | Citigroup |

| Cowen | Guggenheim Securities | Piper Sandler | Telsey Advisory Group |

Co-Manager

Siebert Williams Shank

Prospectus dated , 2022

Table of Contents

claire’s

Table of Contents

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

| 18 | ||||

| 21 | ||||

| 26 | ||||

| 56 | ||||

| 58 | ||||

| 59 | ||||

| 60 | ||||

| 64 | ||||

| 66 | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 69 | |||

| 96 | ||||

| 115 | ||||

| 122 | ||||

| 139 | ||||

| 141 | ||||

| 145 | ||||

Material U.S. Federal Tax Considerations for Non-U.S. Holders of Common Stock | 152 | |||

| 155 | ||||

| 157 | ||||

| 165 | ||||

| 165 | ||||

| 165 | ||||

| F-1 | ||||

Unless otherwise indicated, references in this prospectus to “Claire’s,” “our company,” “we,” “our” and “us,” or like terms, refer, prior to the Corporate Conversion discussed elsewhere in this prospectus, to Claire’s Holdings LLC, a Delaware limited liability company and its consolidated subsidiaries, and, after the Corporate Conversion, to Claire’s Inc., a Delaware corporation and its subsidiaries. Neither we, the selling stockholders nor the underwriters have authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. Neither we, the selling stockholders nor the underwriters take any responsibility for, and can provide no assurance as to the reliability of, any other information that others may provide you. We and the selling stockholders are offering to sell, and seeking offers to buy, shares of common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the shares of common stock.

No action is being taken in any jurisdiction outside the United States to permit a public offering of common stock. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restriction as to this offering and the distribution of this prospectus applicable to those jurisdictions.

i

Table of Contents

Market Share and Other Information

This prospectus includes certain market, statistical and industry data and forecasts. Although we are responsible for all of the disclosure contained in this prospectus, in some cases we rely on and refer to market, statistical and industry data, estimates and forecasts that were obtained from third-party surveys, market research, consultant surveys, publicly available information and industry publications and surveys that we believe to be reliable. Unless otherwise indicated, all market, statistical and industry data and forecasts contained in this prospectus are based on independent industry publications, government publications, reports by market research firms or other independent sources and other externally obtained data, such as Green Street Advisors, Euromonitor International Limited and The Morning Consult LLC, that we believe to be reliable. Some market and industry data, and statistical information and forecasts, are also based on management’s estimates, which are derived from our review of internal surveys as well as the independent sources referred to above. Any such market data, information or forecast may prove to be inaccurate because of the method by which we obtain it or because it cannot always be verified with complete certainty given the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process, and other limitations and uncertainties, including those discussed under the caption “Risk Factors.” As a result, although we believe that these sources are reliable, we have not independently verified the information.

Trademarks and Trade Names

We own or have rights to trademarks, service marks and trade names that we use in connection with the operation of our business. Other trademarks, service marks and trade names appearing in this prospectus are the property of their respective owners. Solely for convenience, some of the trademarks, service marks and trade names referred to in this prospectus are listed without the ® or ™ symbols, but we will assert, to the fullest extent under applicable law, our rights to our trademarks, service marks and trade names.

Presentation of Financial Information

We report on the basis of a 52- or 53-week fiscal year, which ends on the Saturday closest to January 31. References to “fiscal year” mean the year in which that fiscal year began. For example, references to “fiscal year 2020” and “fiscal year 2019” relate to our fiscal years ended January 30, 2021 and February 1, 2020, respectively.

We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that precede them. As used in this prospectus, unless the context otherwise requires, references to “U.S. dollars,” “dollars,” “U.S. $” and “$” are to the lawful currency of the United States of America.

This prospectus contains “non-GAAP financial measures,” which are financial measures that are not calculated and presented in accordance with U.S. generally accepted accounting principles (“GAAP”). See “Summary Historical Consolidated Financial and Other Data—Non-GAAP Financial Measures.”

ii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that you should consider before deciding to invest in our common stock. You should read this entire prospectus carefully, including the “Risk Factors” and the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections and our consolidated financial statements and the notes thereto included elsewhere in this prospectus.

Who We Are

We are a fully integrated global fashion brand powerhouse committed to inspiring self-expression through the creation and delivery of exclusive, well-curated products and experiences. We offer an immersive, experience-driven shopping environment for our consumers, with product offerings including jewelry, fashion accessories, tech accessories, cosmetics and more. Our trend-forward products are distributed in Claire’s®-operated stores, via e-commerce and through our broad base of concession partners. For over 50 years, Claire’s® has been a destination for the curious, creative and influential. Our entire ecosystem is anchored by our legacy in dynamic merchandising and our core piercing expertise and is informed by our unique understanding of and loyal relationship with our consumers worldwide.

We have two brands, Claire’s®, our flagship brand, and Icing®. Claire’s® has a powerful following with the highly influential Generation Z audience, which consists of over 2.5 billion individuals globally. Based on customer feedback, we have a reputation for delivering a differentiated, trendsetting and diverse assortment of products, many of which are proprietary designs, that help young minds style and define themselves. We believe that we are the market share leader in retail piercing services in North America and the world’s largest ear piercing service provider, having pierced the ears of millions of customers over our 40-plus year history of piercing. Piercing services and related product sales represent a meaningful part of our revenue and serve as an important customer acquisition vehicle that draws new consumers to our stores every year. The dynamic combination of strong brand equity, unique and diverse product offerings and revenue from services offered in our stores creates a highly differentiated financial profile with attractive margins.

Claire’s® offers an omni-present, multi-dimensional shopping experience, creating unique touchpoints with our consumers where they live and shop. Our offering is anchored in a strong physical retail presence which includes a global network of company-operated stores—consisting of conventional retail formats (which we refer to as standalone stores) and Claire’s® stores we operate inside a retail partner’s stores (which we refer to as store-in-stores)—and franchised stores. In addition, we operate in over 10,500 concessions located within approximately 30 retail partners in North America and Europe, including Walmart, CVS, Asda, Tesco and Matalan. In our concession formats, Claire’s® owns, merchandises and manages the inventory located in our partners’ stores and pays a sales-based variable fee for the right to operate in the concession.

Our retail stores offer a fun “treasure hunt” shopping experience that encourages our customers to explore and find the latest trends to create their own unique looks. We merchandize our stores with the intention of delighting and surprising our customers at every visit, which we believe encourages them to return to our stores frequently. We operate stores averaging 1,200 square feet in North America and 835 square feet in Europe in a broad variety of retail formats including mall, outlet, lifestyle, high street, strip centers and store-in-stores. As of October 30, 2021, there were 1,448 company-operated Claire’s® stores in North America, 885 company-operated Claire’s® stores in Europe across 15 countries and 296 franchised Claire’s® stores primarily located in the Middle East and South Africa. We believe our

1

Table of Contents

service-led retail model and attractive target consumer makes us a desirable tenant for commercial real estate operators, allowing us to be selective in choosing retail locations.

We use our Claire’s® and Icing® websites and the Claire’s® app for commerce and community, promoting and selling the latest products available at Claire’s® and Icing® and connecting with our customers, including educating them on recent trends, current offerings and our ear piercing service process and options. We continue to invest in our digital offerings to enable seamless and consistent brand interactions across every channel. We are enhancing our Buy Online, Pick-Up in Store (“BOPIS”) capability, which we began to pilot in the United States in September 2021 and in the United Kingdom in October 2021, with full rollout in the United States and the United Kingdom completed in November 2021, and pilot programs in other countries expected to follow in the coming months. We launched our Claire’s® Rewards loyalty program in the United States in November 2020 and in the United Kingdom and Ireland in September 2021, and are in the process of expanding the program to additional countries. As of October 30, 2021, we had approximately 8.7 million loyalty members and sales to Claire’s® Rewards members which represented half of our total U.S. Retail sales (including e-commerce) for the first nine months of fiscal year 2021. In September 2021, we launched our subscription program in the United States, offering curated boxes of jewelry and accessories to our subscription members.

We also operate our sister brand, Icing®, which had 191 stores in North America as of October 30, 2021. Icing® offers an inspiring merchandise assortment of fashionable products, as well as piercing services, targeting young women looking to express themselves. Our product offering includes jewelry, beauty, hair, fashion and bridal accessories. We believe Icing® allows us to reach age groups beyond our Claire’s® core customer demographic, including the over 76 million Millennial consumers in North America, and retain Claire’s® customers as they age. Many of our customers later introduce their children or other family members to the Claire’s® brand as they become mothers, aunts and grandmothers. Our Icing® product offering leverages our brand merchandising capabilities, consumer trend insights and other core expertise, including our product development and sourcing expertise.

Our Recent Transformation

Our management team has identified and enacted initiatives to leverage our strong brand equity and recognition in service and product excellence to accelerate growth, amplify brand value, expand our offerings and optimize our operating structure. By the end of fiscal year 2021, we expect to have invested over $150 million in the business to better align our offering with consumer trends, augment our physical and digital presence and enhance growth. These investments include the following:

Growth investments across all aspects of our business:

| • | Assembling a growth-oriented management team with deep experience across all aspects of our company |

| • | Expanding and upgrading our retail footprint to meet our customers where they prefer to shop |

| • | Investing in new formats and channels to increase consumer interaction and access new customers |

| • | Building e-commerce capabilities to drive a seamless omni-channel experience and personalization at scale |

| • | Improving our ear piercing experience through digital enhancements and service expansion |

| • | Launching a consumer loyalty program to create more rewarding customer relationships with deeper insights |

2

Table of Contents

| • | Designing subscription services to offer curated products with more frequent consumer interaction |

| • | Enhancing our buying and merchandise systems, including localizing assortment |

Operational investments:

| • | Redesigning our supply chain and developing improved planning and allocation capabilities |

| • | Upgrading our store network and IT to support our growth |

| • | Developing data analysis excellence to drive decision making across all areas of the organization, including consumer trends, promotion management, real estate strategy and cost optimization |

Our Recent Financial Performance

Since reopening our stores as COVID-19-related operating restrictions eased, we have experienced strong performance in North America and improving performance in Europe as the COVID-19 vaccine roll-out gains traction across the continent. We believe our operating results for the first nine months of fiscal year 2021 highlight the strength of our brand and unique nature of our business model, which combines growth potential with robust operating metrics.

For the third quarter of fiscal year 2021, we achieved the following results:

| • | Increase in total same store sales of 17.4% compared to the same period in 2020 and 10.4% compared to the same period in 2019. North America same store sales grew 22.1% compared to 2020 and 19.1% compared to 2019. European same store sales grew 8.3% compared to 2020 and decreased 4.9% compared to 2019. |

| • | Total net sales growth of 25.5% compared to the same period in 2020 and 14.9% compared to the same period in 2019. North America sales grew 31.3% compared to 2020 and 23.1% compared to 2019. European sales grew 14.5% compared to 2020 and 0.5% compared to 2019. |

| • | Net income of $75.3 million, representing a 1,092.6% change compared to the same period in 2020. |

| • | Adjusted EBITDA growth of 40.3% compared to the same period in 2020. Adjusted EBITDA is a non-GAAP measure. See “Summary Historical Consolidated Financial and Other Data—Non-GAAP Financial Measures.” |

| • | Net income margin of 21.1%, compared to 2.2% for the same period in 2020. |

| • | Adjusted EBITDA margin of 19.7%, compared to 17.6% for the same period in 2020. |

| • | Partnered with 16 retail partners to open 288 net new concessions locations. |

For the first nine months of fiscal year 2021, we achieved the following results:

| • | Increase in total same store sales of 23.7% compared to the same period in 2020 and 12.8% compared to the same period in 2019. North America same store sales grew 29.6% compared to 2020 and 20.9% compared to 2019. European same store sales grew 9.7% compared to 2020 and decreased 5.9% compared to 2019. |

3

Table of Contents

| • | Total net sales growth of 61.6% compared to the same period in 2020 and 7.3% compared to the same period in 2019. North America sales grew 81.4% compared to 2020 and 23.2% compared to 2019. European sales grew 23.4% compared to 2020 and decreased 21.5% compared to 2019. |

| • | Net loss of $(32.4) million, representing 69.3% improvement compared to the same period in 2020. |

| • | Adjusted EBITDA growth of 709.6% compared to the same period in 2020. |

| • | Net loss margin of (3.3)%, compared to (17.3)% for the same period in 2020. |

| • | Adjusted EBITDA margin of 20.1%, compared to 4.0% for the same period in 2020. |

| • | Partnered with 22 retail partners to open 2,458 net new concessions. |

Our Competitive Strengths

Global brand powerhouse for self-expression

We are a category leader in the girl’s fashion jewelry and accessories market with strong brand recognition among our core demographic. According to surveys commissioned by Claire’s and conducted by The Morning Consult LLC, we enjoy between 82% and 99% brand awareness among 13 to 17 year-old girls, women 18 and over, and mothers with children aged 3 to 12 in the United States, the United Kingdom and France. Our Claire’s® brand is viewed by many as synonymous with self-expression and while Generation Z is our primary target, our brand appeals to consumers of all ages around the world. Our products are regularly featured in editorial coverage, social media and fashion periodicals relevant for our target audience. We believe there is an opportunity to further leverage our brand by extending into additional categories to capture a larger share of spending from or influenced by Generation Z consumers. In 2020, according to Euromonitor, the total addressable market of the jewelry, apparel accessories, color cosmetics, toys and writing instruments product categories was approximately $450 billion, with jewelry representing approximately $288 billion.

We believe we are the leading retail piercing destination, providing customers with a safe and affordable experience from a brand they trust. Ear piercing is a memorable life experience that we believe establishes a lifelong connection between customers and our brand. We offer piercing in all of our stores in North America and in over 98% of our stores in Europe. We have experienced 26 consecutive quarters of positive same-store sales growth of our ear-piercing business (excluding the first three months of fiscal year 2020 due to shut-downs resulting from the COVID-19 pandemic), although there are no assurances this growth will continue at the same rate or at all. See “Risk Factors.” We believe our highly trained associates and over 40 years of piercing experience have made us a desirable destination worldwide for a variety of piercing services.

Experiential, service-led business model

We are a preferred destination for consumers looking for a safe, fun and affordable ear piercing service. Our specially-trained staff pierce millions of customers’ ears annually. During the nine months ended October 30, 2021, we averaged over 85,000 piercings per week. Revenue generated from our ear piercing experience has consistently accounted for a meaningful part of our Retail sales. For fiscal year 2019 through October 30, 2021, more than 20% of our Retail sales came from ear-piercing-related transactions, with a substantially higher percentage of Retail sales from these transactions in North America than in Europe, and spend per piercing transaction grew at a compound annual growth

4

Table of Contents

rate of approximately 14% during this period. Our ear piercing service also functions as an attractive customer acquisition vehicle and drives significant traffic to our stores. For the first nine months of fiscal year 2021, approximately 55% of all ear piercing customers purchased fashion jewelry or accessories during their visit to our stores. Since the launch of our Claire’s® Rewards loyalty program in the United States, approximately 60% of piercing customers have joined the program. In addition to piercing, we offer other in-store activities, including birthday parties and life event celebrations. Special events represent a small but growing part of our business.

We strategically design the layout of our stores to encourage impulse buying and a “treasure hunt” experience for our customers. We constantly refresh our store merchandise, changing our floor plans eight to ten times per year, ensuring there is a feeling of newness each time a customer visits. We amplify this experience with promotions designed to fuel exploration and discovery of merchandise, such as our “buy three, get three” promotion.

We believe our experiential and service-led model differentiates us from other brick-and-mortar and online competition, given that our ear piercing service and in-store experience cannot be replicated online.

Multichannel flexible distribution strategy

We strive to connect with our customers where they prefer to shop. Reflective of the continuously evolving retail environment, we have strategically created a multichannel shopping experience, which includes a global company-operated and franchised retail store network, store-in-store formats and retail partner concessions, as well as a growing digital presence.

We have a highly flexible and differentiated real estate strategy, which allows us to grow and operate a variety of formats that generate positive store-level four-wall EBITDA. Our company-operated stores average 1,200 square feet in North America and 835 square feet in Europe. Each of our stores is a retail destination that draws in consumers looking for a fun shopping environment and drives foot traffic. Our customers rely on us to highlight new trends and provide them with a deep assortment of products to inspire their self-expression. As of October 30, 2021, we had 1,639 company-operated stores, which included 226 store-in-stores, in North America and 885 company-operated stores, which included 9 store-in-stores, in Europe. For fiscal year 2019, prior to the onset of the COVID-19 pandemic, 96% of our company-operated stores generated positive four-wall EBITDA, and we have experienced strong same-store sales growth in the current fiscal year, further enhancing store performance. We define four-wall EBITDA as store-level operating income before depreciation, including store wages, rent, distribution costs and other store operating expenses, adjusted to exclude corporate overhead expense.

| • | Over one-third of our stores in North America were located in non-mall locations as of October 30, 2021. Our mall stores are located in many of the top malls in the country (with approximately 75% of the malls in which our stores are located graded by Green Street Advisors as mall grades A or grades B (excluding malls not rated by Green Street Advisors)), and are expected to continue to generate strong traffic trends and generate positive four-wall EBITDA. For fiscal year 2019, prior to the onset of the COVID-19 pandemic, 99% of our company-operated stores in North America generated positive four-wall EBITDA. For our stores located in lower-graded malls, the average remaining lease term was approximately 12 months as of October 30, 2021, which provides the opportunity for us to continue to evolve our retail footprint. |

| • | Our European locations are comprised primarily of mall and high street locations, with malls containing some of our top-performing stores. For fiscal year 2019, prior to the onset of the |

5

Table of Contents

COVID-19 pandemic, 93% of our company-operated stores in Europe generated positive four-wall EBITDA, and we closed a number of unprofitable stores in Europe during 2020 and the first nine months of fiscal year 2021. A primary focus of our strategy is to improve the performance of European stores on a four-wall EBITDA basis by optimizing our existing store fleet through strategic relocations or closures of under-performing stores and opening new stores in under-penetrated markets within countries where we currently operate high-performing stores. |

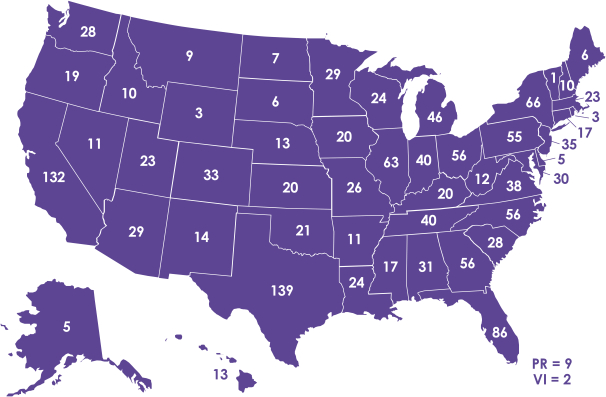

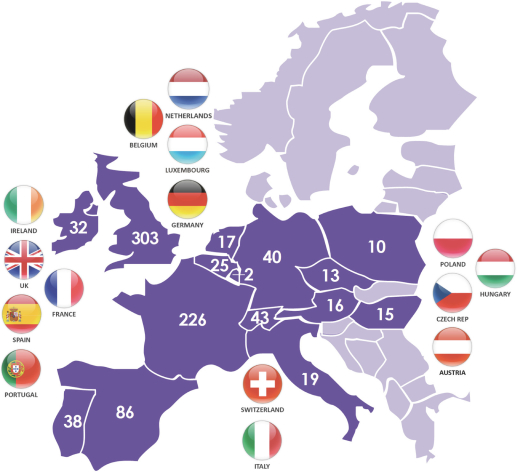

The following graphics summarize our number of company-operated stores by state, territory or country in our North America and Europe segments as of October 30, 2021.

North America:

6

Table of Contents

7

Table of Contents

Europe:

We also operate in over 10,500 concessions globally across approximately 30 retail partners. Further, expansion in the concessions business represents an attractive growth opportunity with low upfront investment.

We also have numerous avenues outside of our physical retail presence that extend our offering to meet our customers where they are, including our Claire’s® and Icing® websites, our Claire’s® app, our presence on third-party marketplaces including Amazon.com and our subscription program, which we launched in September 2021. We believe there is opportunity to grow our digital sales and subscription program by offering convenience, engaging content and a curated selection of merchandise.

Vertical integration resulting in differentiated merchandizing strategy and unique product assortment

Both our design team and sourcing team are vertically integrated. Our design team conceptualizes the vast majority of our merchandise, and over 90% of our merchandise is designed or sourced exclusively for, or otherwise sold exclusively by, Claire’s® or Icing®, including Claire’s® exclusive products from various licensed partners. Our sourcing team is responsible for generating and maintaining vendor relationships. We have solid, long-standing relationships with our approximately

8

Table of Contents

200 vendors, some continuing for over 30 years, resulting in strong collaboration and competitive bidding across our vendor base. We believe that our vertically-integrated design and sourcing model allows us to respond quickly and nimbly to new trends and yields low cost sourcing that results in strong margins for our Claire’s® and Icing® products.

Differentiated financial profile with strong operating margins and many visible growth opportunities

Our differentiated business model combines significant top line growth opportunity with operating margin expansion and operating cash flow generation. Our brand, service-led offering and flexible real estate strategy allow us to continuously expand the market we serve and attract new consumers. We believe our scale, vertical integration and operational excellence allow us to offer consumers a unique and affordable product assortment and popular services while maintaining high operating income margins. Due to our strong operating margins, the relatively low capital investments required to open our stores and concessions and our low run-rate maintenance capital expenditure costs, we are able to generate strong operating cash flow and strong conversion of Adjusted EBITDA to operating cash flow. We believe the combination of our financial profile and strong balance sheet creates significant flexibility for us to capitalize on numerous visible growth opportunities.

Experienced and talented management team

Our senior management team has extensive retail experience and complementary expertise across a broad range of disciplines including merchandising, supply chain, real estate, e-commerce and finance. In total, our senior management team consists of nine members with over 225 years of collective experience in the retail sector. Ryan Vero, who joined as Chief Executive Officer in July of 2019, brings with him a strong track record of propelling retail growth through innovation.

Our Market Opportunity

While we serve customers across multiple generations, we consider the Generation Z audience, which encompasses individuals from 5 to 24 years of age in 2021, to be our core and most important demographic focus. The Generation Z consumer segment is over 2.5 billion strong globally. Relative to older generations, a high proportion of Generation Z spending is discretionary in nature given that much of Generation Z’s essential spending needs are paid by parents or other family members.

We believe there is a significant opportunity to not only grow product sales to our target consumers, but also to continue to enhance long-term brand equity and engagement, creating another generation of loyal and enthusiastic Claire’s® consumers. Our vision is to remain an influencer and creator of youth and fashion culture and a leader in the fashion jewelry and accessories market.

Our Growth Strategies

We believe we have significant opportunities to drive long-term growth in revenue and earnings by further leveraging our brand and dynamic operating platform to expand our physical footprint, attract new consumers and increase our share of wallet with our core demographic while enhancing our digital presence and consumers’ experience. We plan to execute on the following strategies:

Expand our multichannel presence to meet our customers where they are

| • | Continue to grow and evolve our store footprint. Our service-led global retail network serves as an attractive consumer acquisition vehicle and the foundation for our multichannel |

9

Table of Contents

presence and experiential model. Our flexible business model allows us to operate various formats that generate positive store-level four-wall EBITDA, including standalone stores and store-in-store locations. With the exception of the period during the COVID-19 pandemic, we have consistently generated positive store-level four-wall EBITDA across our existing store footprint. For fiscal year 2019, prior to the onset of the COVID-19 pandemic, 96% of our company-operated stores generated positive four-wall EBITDA, and we closed some of our least productive locations during 2020 and in the first nine months of 2021. We set certain targets when we evaluate new store locations. Our mall-based stores are expected to generate $600,000 to $900,000 in sales per year, require approximately $0.2 million of capital and inventory investment and typically have a 15-month payback period. Our off-mall stores are expected to generate $375,000 to $900,000 in sales per year, require approximately $0.2 million of capital and inventory investment and typically have a 14-month payback period. Our store-in-store locations are expected to generate $250,000 to $400,000 in sales per year, require approximately $0.1 million of capital and inventory investment and typically have a 14-month payback period. Although we set these targets for new store openings, such targets may not be reached or obtained. |

| • | Over one-third of our stores in North America were located outside of shopping malls as of October 30, 2021. We have identified over 500 potential new standalone Claire’s® store locations in strip, power, outlet and lifestyle centers and select top-tier mall locations where we are currently not present. In fiscal year 2021, we expect to open 55 to 60 new standalone store locations, of which the majority will be located in non-mall locations. We also expect to close 39 standalone store locations, the majority of which will be located in malls. We further expect to open 165 to 170 new store-in-store locations in fiscal year 2021. At the end of fiscal year 2021, we expect approximately 40% of our stores in North America to be located in non-mall locations, up from approximately 20% from fiscal year 2019. As of October 30, 2021, our average remaining lease commitment on our existing real estate portfolio was less than 24 months in North America. |

| • | In Europe, we expect to improve the performance on a four-wall EBITDA basis of our existing stores as well as open new locations in select markets. We plan to continue to optimize our existing store fleet through strategic relocations or closures of under-performing stores and opening new stores in under-penetrated markets within countries where we currently operate high-performing stores. We expect to open 13 new standalone store locations and close 38 underperforming stores in fiscal year 2021. As of October 30, 2021, our average remaining lease commitment on our existing real estate portfolio was approximately 22 months in Europe. |

| • | Over the next several years, we anticipate annually opening 90 to 110 net-new standalone stores (new stores less closing stores) globally, most of which will be located in non-mall locations. We also expect to open 10 to 15 new store-in-store locations in 2022. We further expect to continue optimizing our real estate portfolio, through strategic relocations, to reduce exposure to lower quality and lower grade mall locations. |

| • | Grow concessions. We currently operate in over 10,500 concessions across approximately 30 retail partners in North America and Europe. During the nine months ended October 30, 2021, our average weekly sales were between $50 and $250 at our small-format concessions locations, between $250 and $650 at our medium-format concessions locations, and between $650 and $3,000 at our large-format concessions locations. We believe we have a significant opportunity to grow and deepen these existing partnerships as well as launch concession offerings with new retail partners. We maintain inventory ownership and only incur minimal fixed operating costs with limited upfront investment for our concessions, which results in a lucrative revenue stream and earnings profile. We currently operate successful concession partnerships in a variety of retail segments across North America and Europe. We focus on |

10

Table of Contents

partnering with large chains where we can scale quickly. We have an existing presence in approximately 30 retailers globally, including Walmart, CVS and Matalan. We believe there are meaningful identified opportunities for our concessions, which we are only in the early stages of addressing, including through continued expansion into new retail partner stores and through the rollout of additional stores with existing partners. We focus on top retailers across a variety of retail segments, including mass, grocery, apparel, department and specialty stores in the United States and Europe. Given the impulse nature of purchases for many of our categories and unique shopping experience, we have not experienced any meaningful cannibalization in our Claire’s® and Icing® banner stores as we have grown our concessions partnerships. We also believe we have numerous incremental opportunities with our retail partners, including expansion of our product offerings and offering ear piercing services in some partners’ stores. |

| • | Expand geographically. We believe there is an opportunity to expand our business in new geographies in the future, including expanding our presence in Central and South America and entering Mexico and the Asia-Pacific region, each of which we believe is an untapped market for the Claire’s® brand. |

Acquire new consumers and increase our share of the customer’s wallet

| • | Enhance and grow our piercing services. We believe we are the world’s largest ear piercing services provider as well as the market share leader in retail piercing services in North America. We have an opportunity to further leverage our piercing experience and reputation for piercing safety to grow our market share and our revenue per piercing by enhancing the consumer piercing experience, including by increasing the product mix of premium offerings. We are investing in capabilities that will allow us to elevate consumers’ pre-appointment, in-store and aftercare piercing experience, including online scheduling and registration, virtual earring try-on and digital aftercare notifications. We are also planning to expand our nose piercing services, which we currently only offer in certain stores in the United Kingdom, Germany and Canada. In addition, we see an opportunity to continue to expand our products to include a higher percentage of premium items in a majority of our stores, including gold and diamond options. |

| • | Localize our merchandise. We are continuously elevating our merchandise to deliver a differentiated selection of proprietary and exclusive products that are highly relevant to our customers. This includes varying our product inventory and assortment across our store base to reflect the unique characteristics of our local markets. We believe this is especially important across our footprint in Europe, which spans several distinct markets. We have invested in a new merchandizing system we are implementing to enable us to further leverage our global consumer insights to customize our offering to local preferences at scale, further enhancing store performance and reducing markdowns. |

| • | Increase consumer lifetime value by expanding our loyalty program. We believe there is an opportunity to capture a larger share of the spend by and for our core demographic by offering a focused and compelling loyalty program. We launched our loyalty program in the United States in November 2020 and, as of October 30, 2021, we had approximately 8.7 million members. Our loyalty program rewards our customers with cash back and exclusive discounts while allowing us to leverage consumer data analytics from the program to employ more personalized consumer messaging and marketing to drive a higher share of our customer’s wallet. For the nine months ended October 30, 2021, half of our U.S. Retail revenue (including e-commerce) was attributable to loyalty members. We plan to expand the loyalty program into our European markets later this year. |

11

Table of Contents

| • | Enhance our digital presence. Our goal is to become the most engaging customer-centric digital destination for discovery, inspiration and purchase of fashion jewelry and accessories. We use our online presence to highlight current trends, provide purchase recommendations as well as interact and transact with our consumers. Since 2018, we have invested over $15 million in enhancing our digital capabilities, resulting in meaningful increases in traffic to Claires.com and Icing.com and improved conversion rates. We believe we have an opportunity to grow our digital business by making the online shopping experience easier, with improvements in website navigation, product pages and checkout experience, as well as by leveraging our expanded Buy Online, Pick-Up in Store (“BOPIS”) capabilities. We also have the opportunity to expand our digital footprint to additional countries where we currently have a retail store presence but where our e-commerce presence is not customized to the local market as well as to capture additional sales through Amazon’s marketplace and similar opportunities globally. We also launched a subscription service in the United States in September 2021 to offer customers access to the latest trends and products from Claire’s®. We believe growth in subscription represents a sizable opportunity. |

Summary Risk Factors

An investment in shares of our common stock involves substantial risks and uncertainties that may adversely affect our business, financial condition and results of operations and cash flows. Some of the more significant challenges and risks relating to an investment in our common stock include those associated with the following:

Risks related to our business and industry

| • | the COVID-19 pandemic; |

| • | our ability to maintain, enhance and protect the value and goodwill of our brands; |

| • | our ability to anticipate, identify and respond to merchandise, marketing and promotional trends or consumer shopping patterns and successfully maintain proper merchandise assortment, and our ability to adequately forecast the demand for our products; |

| • | our ability to recruit, train, motivate and retain suitably qualified store associates, distribution center works and other employees; |

| • | the failure to grow our store (including store-in-store) and concessions businesses or grow our digital business; |

| • | a decline in the number of people who go to shopping malls, especially those where we experience high sales volumes; |

| • | our sourcing of a substantial majority of our products through production arrangements in Asia; |

| • | our ability to source our merchandise efficiently and cost effectively if new trade restrictions are imposed, existing trade restrictions become more burdensome or relationships with manufacturers are impaired or terminated; |

| • | negative publicity that is accelerated by social media or emergent forms of communication and our inability or failure to recognize, respond to and effectively manage the accelerated impact of social media; |

| • | our industry is highly competitive and our ability to effectively compete; |

12

Table of Contents

| • | our ability to deliver our products to market if we encounter problems with distribution; |

| • | our concessions and store-in-store locations are operated under agreements that are subject to revocation or modification; |

| • | we have changed our executive team significantly in the past two years, and our business and future growth prospects may be harmed if we lose key members of our executive team or are unable to integrate, attract and retain the executives and key personnel we need to support our operations and growth; |

| • | our ability to renew or replace our distribution center and store leases, or enter into leases for new distribution centers or stores on favorable terms, or if our current leases are terminated prior to the expiration of their stated term and we cannot find suitable alternate locations; |

| • | fluctuations in foreign currency exchange rates; |

| • | macroeconomic conditions may adversely impact levels of consumer spending; |

| • | litigation matters and regulatory enforcement actions relating to our business could be adversely determined against us or otherwise distract management from our business activities and result in significant liability or damage to our brands; |

| • | natural disasters or unusually adverse weather conditions, public health crises, political crises and other catastrophic events or other events outside of our control; |

| • | the willingness of vendors and service providers to supply us with goods and services pursuant to customary credit arrangements that may not be available to us in the future; |

| • | some of our European workforce is covered by collective bargaining agreements, national collective agreements and/or works councils, and our business could be harmed in the event of a prolonged work stoppage; |

| • | goodwill impairments; |

| • | our ability to use our net operating losses to offset future taxable income; |

| • | additional tax liabilities in connection with our operations or due to future legislation; |

| • | failure to maintain our franchising relationships; and |

| • | our debt agreements contain restrictions that limit our flexibility in operating our business. |

Risks related to information technology, data security and intellectual property

| • | if our or our third-party providers’ information technology systems are interrupted for a significant period of time or fail to perform as designed; |

| • | if we or our third-party providers experience any compromise or breach of our or our third-party service providers’ data security or information technology systems, including the security of customer, associate, third-party or company information, as we have in the past, we may be subject to penalties and liability and experience negative publicity; |

| • | we may be unable to obtain, maintain, protect or enforce our trademarks and other intellectual property rights; |

| • | legal claims alleging that we, our vendors, our franchisees or licensees or the manufacturers of our merchandise infringe, misappropriate or otherwise violate the intellectual property rights of third parties; and |

13

Table of Contents

| • | if our franchisees, vendors and other licensees do not observe our required quality and trademark usage standards. |

Risks related to laws, regulations and industry standards

| • | our business, including our marketing programs, e-commerce initiatives and use of consumer information, is governed by an evolving set of laws and enforcement trends relating to data privacy or security, and any actual or perceived failure by us to comply with any such existing or future laws or with other obligations relating to data privacy and security; |

| • | our cost of doing business could increase as a result of changes in regulations regarding the content and sale of our merchandise and our piercing services; |

| • | failure to comply with standards, rules and laws governing electronic payments; and |

| • | failure to comply with anti-bribery, anti-corruption, economic sanctions, export control, anti-terrorism and anti-money laundering laws. |

Risks related to our common stock and this offering

| • | affiliates of each of Elliott Investment Management L.P. (together with its affiliates, “Elliott”) and Monarch Alternative Capital LP (“Monarch”) may each continue to have significant influence over us after this offering; |

| • | we have no current plans to pay regular cash dividends on our shares of common stock following this offering; and |

| • | we are a holding company with nominal net worth and will depend on dividends and distributions from our subsidiaries to pay any dividends. |

Before you invest in our stock, you should carefully consider all the information in this prospectus, including matters set forth under the heading “Risk Factors” beginning on page 26.

COVID-19

As a result of the public health risk and government-imposed quarantines and other restrictions on commercial activity to contain the spread of COVID-19, the Company’s Retail and Concessions sales were significantly impacted during fiscal year 2020. From March 2020 to May 2020, we temporarily closed all of our stores in North America and Europe; during this period, many of our concessions locations were also closed and in some geographies, non-essential products (including our own) could not be sold at concessions locations that otherwise remained open.

Though we cannot estimate the precise impact of the COVID-19 pandemic on our results of operations, we note that net sales, gross profit and operating income (loss) were $986.4 million, $570.9 million, and $124.9 million, respectively, for the first nine months of fiscal year 2021, compared to $610.5 million, $274.6 million and $(36.0) million, respectively, for the first nine months of fiscal year 2020, compared to $919.3 million, $489.7 million and $98.9 million, respectively, for the first nine months of fiscal year 2019. In addition, segment net sales for North America and Europe were $729.2 million and $257.2 million, respectively for the first nine months of fiscal year 2021, compared to $402.1 million and $208.5 million, respectively for the first nine months of fiscal year 2020, compared to $591.9 million and $327.4 million, respectively for the first nine months of fiscal year 2019. Segment operating income (loss) for North America and Europe were $123.4 million and $1.5 million, respectively, for the first nine months

14

Table of Contents

of fiscal year 2021, compared to $(15.9) million and $(20.1) million, respectively, for the first nine months of fiscal year 2020, compared to $72.6 million and $26.3 million, respectively, for the first nine months of fiscal year 2019. We believe that such reductions in net sales, gross profit, operating income (loss) and segment operating income (loss) were largely attributable to the impact of COVID-19, in particular due to the temporary closure of all of our stores during March 2020 to May 2020, which resulted in no revenues generated at our stores during such period. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—COVID-19” for a description of the impact of COVID-19 on our results.

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion (as adjusted for inflation pursuant to the Securities and Exchange Commission (the “SEC”) rules from time to time) in revenue during our last fiscal year, we qualify as an “emerging growth company” under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An emerging growth company may take advantage of reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. As an emerging growth company:

| • | we may present as few as two years of audited financial statements and two years of related management discussion and analysis of financial condition and results of operations; |

| • | we are exempt from the requirement to obtain an attestation report from our auditors on our internal control over financial reporting under the Sarbanes-Oxley Act of 2002, as amended (the “Sarbanes-Oxley Act”), for up to five years or until we no longer qualify as an emerging growth company; |

| • | we are permitted to provide reduced disclosure regarding our executive compensation arrangements pursuant to the rules applicable to smaller reporting companies, which means we do not have to include a compensation discussion and analysis and certain other disclosures regarding our executive compensation; and |

| • | we are not required to hold non-binding advisory votes on executive compensation or golden parachute arrangements. |

In addition to the relief described above, the JOBS Act permits us an extended transition period for complying with new or revised accounting standards affecting public companies. We have elected to use this extended transition period, which means that our financial statements may not be comparable to the financial statements of public companies that comply with such new or revised accounting standards on a non-delayed basis.

In this prospectus we have elected to present as few as two years of audited financial statements and two years of related management discussion and analysis of financial condition and results of operations, and to take advantage of the reduced disclosure requirements relating to executive compensation. In the future, we may take advantage of any or all of these exemptions for so long as we remain an emerging growth company. We will remain an emerging growth company until the earliest of (i) the end of the fiscal year during which we have total annual gross revenue of $1.07 billion (as adjusted for inflation pursuant to SEC rules from time to time) or more, (ii) the end of the fiscal year following the fifth anniversary of the completion of this offering, (iii) the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt securities or (iv) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended.

15

Table of Contents

Corporate Conversion

We currently operate as a Delaware limited liability company under the name Claire’s Holdings LLC. Prior to the effectiveness of the registration statement of which this prospectus forms a part, Claire’s Holdings LLC will convert into a Delaware corporation pursuant to a statutory conversion and change its name to Claire’s Inc. Prior to the closing of this offering, Claire’s Inc. will effect the other corporate actions described in “Corporate Conversion.” In this prospectus, we refer to all of the transactions related to our conversion to a corporation as the Corporate Conversion.

The purpose of the Corporate Conversion is to convert the top-tier entity in our corporate structure—the entity that is offering common stock to the public in this offering—from a limited liability company to a corporation so that our existing and future investors will own shares of our common stock rather than membership interests in a limited liability company. Immediately prior to the Corporate Conversion, the outstanding limited liability company membership interests of Claire’s Holdings LLC consist of Common Units and Series A Preferred Units. In connection with the closing of the offering, all holders of outstanding membership interests of Claire’s Holdings LLC at the time of its conversion to Claire’s Inc. will receive shares of common stock of Claire’s Inc. See “Corporate Conversion.”

Following the Corporate Conversion, Claire’s Inc. will continue to hold all the property and assets of Claire’s Holdings LLC and continue to be responsible for all of the debts and obligations of Claire’s Holdings LLC. As of the closing of this offering, Claire’s Inc. will be governed by a certificate of incorporation filed with the Delaware Secretary of State and bylaws, the material provisions of which are described in “Description of Capital Stock.”

Except as otherwise noted herein, the consolidated financial statements included elsewhere in this prospectus are those of Claire’s Holdings LLC and its consolidated operations. We do not expect that the Corporate Conversion will have a material effect on the results of our core operations.

Transactions Involving Holders of Series A Preferred Units

At October 30, 2021, the Company had 544,751 Series A Preferred Units issued and outstanding,

without giving effect to the redemption of 46,981 Series A Preferred Units on December 14, 2021 described under “—Redemptions.” The Series A Preferred Units accrue a preferred return at an annual rate equal to 14% of the stated value (the “Preferred Return”). The Preferred Return is paid quarterly within 30 days of each fiscal quarter end. The Preferred Return is payable in additional Series A Preferred Units unless investors that hold a majority of the Series A Preferred Units elect to receive cash. The requisite number of investors have never elected to receive cash. As a result, for the nine months ended October 30, 2021, fiscal year 2020 and fiscal year 2019, the Company issued 54,583, 71,155 and 65,084 Series A Preferred Units, respectively, as payment of the Preferred Return.

The Corporate Conversion and this offering

In connection with the closing of the offering, all holders of outstanding membership interests of Claire’s Holdings LLC at the time of its conversion to Claire’s Inc. will be issued shares of common stock of Claire’s Inc. In addition, former holders of Series A Preferred Units will be issued common shares as part of their make whole premium, as described under “Corporate Conversion—Series A Preferred Unit Make Whole Premium.”

16

Table of Contents

We intend to use the net proceeds from this offering (before any exercise by the underwriters of their option to purchase additional shares of common stock) to pay, in part, the Series A Preferred Unit make whole premium to the former holders of Series A Preferred Units. See “Use of Proceeds.” The make whole premium is required to be paid in cash only to the extent of the net proceeds of the offering (excluding the net proceeds from any exercise by the underwriters of their option to purchase additional shares of common stock), with the remainder of the make whole premium to be paid in common shares.

For details of the number of common shares to be issued in this regard, see “Corporate Conversion—Pricing Sensitivity Analysis.”

Redemptions

On December 14, 2021 the Company redeemed 46,981 Series A Preferred Units at a redemption price of $2,661 per unit for a total redemption amount of $125.0 million, on April 9, 2021 the Company redeemed 28,691 Series A Preferred Units at a redemption price of $2,614 per unit for a total redemption amount of $75.0 million, and on November 6, 2020, the Company redeemed 52,959 Series A Preferred Units at a redemption price of $2,837 per unit for a total redemption amount of $150.3 million. The December 2021, April 2021 and November 2020 redemption prices were equal to the stated value of each unit plus a redemption premium based upon the present value of the Preferred Return due through October 12, 2038.

Debt Exchange

On December 18, 2019, the Company entered into the term loan credit agreement (the “Term Loan Credit Agreement”) among Claire’s Stores, Inc. (“Claire’s Stores”), as borrower, the lenders party thereto and JP Morgan Chase Bank, N.A., as administrative agent and collateral agent, providing for $502.4 million aggregate principal amount of term loan maturing on December 18, 2026 (the “Term Loan”). The Term Loan refinanced the $250.0 million aggregate principal amount of the then-outstanding term loan (the “Refinanced Term Loan”) and consummated an offer to exchange 10,049 of its preferred units, including accrued preferred return for $1,500 of Term Loan for each preferred unit tendered (the “Debt Exchange”).

Our Corporate Information

Claire’s Holdings LLC is a Delaware limited liability company. Prior to the effectiveness of the registration of which this prospectus forms a part, we will convert into a Delaware corporation pursuant to a statutory conversion and be renamed Claire’s Inc. See “Corporate Conversion.”

Our principal executive offices are located at 2400 West Central Road, Hoffman Estates, Illinois, 60192 and our telephone number is (847) 765-1100. Our website is www.claires.com. Our website and the information contained therein or connected thereto are not incorporated into this prospectus or the registration statement of which it forms a part.

17

Table of Contents

This summary highlights information presented in greater detail elsewhere in this prospectus. This summary is not complete and does not contain all the information you should consider before investing in our common stock. You should carefully read this entire prospectus before investing in our common stock, including the “Risk Factors” section and our consolidated financial statements and notes thereto included elsewhere in this prospectus.

Common stock offered by Claire’s Inc. | shares ( shares if the underwriters exercise their option to purchase additional shares of common stock from us in full) | |

Common stock offered by the selling stockholders | shares (assuming the underwriters exercise their option to purchase additional shares of common stock from the selling stockholders in full) | |

Common stock to be outstanding after this offering | shares ( shares if the underwriters exercise their option to purchase additional shares of common stock from us in full) | |

Use of proceeds | We estimate that the net proceeds to us from this offering will be approximately $ , or approximately $ if the underwriters exercise their option to purchase additional shares of common stock from us in full, assuming an initial public offering price of $ per share (the midpoint of the estimated price range set forth on the cover page of this prospectus), after deducting estimated underwriting discounts and commissions. We estimate that the offering expenses (other than the underwriting discounts and commissions) will be approximately $ . We intend to use the net proceeds from this offering to pay, in part, the Series A Preferred Unit make whole premium to the former holders of Series A Preferred Units. See “Corporate Conversion—Series A Preferred Unit make whole premium.” If the underwriters’ option to purchase additional common shares from us is exercised, the net proceeds therefrom are expected to be used for general corporate purposes, including the payment of offering expenses. See “Use of Proceeds.” | |

18

Table of Contents

We will not receive any proceeds from the sale of shares of common stock offered by the selling stockholders pursuant to the underwriters’ option to purchase additional shares from the selling stockholders. | ||

Dividend policy | We do not anticipate paying any cash dividends on our common stock in the near future. The declaration, amount and payment of any dividends will be at the sole discretion of our board of directors and subject to certain considerations. In addition, our credit facilities place certain restrictions on our ability to pay cash dividends. See “Dividend Policy.” | |

Listing | We have applied to list our common stock on the New York Stock Exchange under the trading symbol “CLRS.” | |

Conflicts of interest | Goldman Sachs & Co. LLC, an underwriter of this offering, beneficially owns approximately 5.2% of our outstanding equity securities prior to the consummation of this offering (approximately 4.4% of the Series A Preferred Units and approximately 5.7% of the Common Units of the Company, which will be converted into preferred and common stock, respectively, of the Company pursuant to the Corporate Conversion as described in “Corporate Conversion”). Goldman Sachs & Co. LLC is expected to receive in excess of 5% of the total net proceeds in this offering as a result of the Company’s payment of the make whole premium to holders of Series A Preferred Units as described in “Use of Proceeds.” Therefore, Goldman Sachs & Co. LLC is deemed to have a “conflict of interest” within the meaning of Rule 5121 of the Financial Industry Regulatory Authority (“FINRA”). Accordingly, this offering is being conducted in accordance with FINRA Rule 5121. FINRA Rule 5121 prohibits Goldman Sachs & Co. LLC from making sales to discretionary accounts without the prior written approval of the account holder and requires that a “qualified independent underwriter,” as defined in FINRA Rule 5121, participate in the preparation of the registration statement and exercise its usual standards of due diligence with respect thereto. Citigroup Global Markets Inc. is acting as the “qualified independent underwriter” for this offering. | |

19

Table of Contents

The number of shares of our common stock to be outstanding after this offering:

| • | is based on shares of common stock to be issued to former holders of Series A Preferred Units upon completion of this offering as described in “Corporate Conversion”; |

| • | excludes shares of common stock reserved for future issuance under the Claire’s Holdings LLC 2018 Management Equity Incentive Plan (the “2018 Plan”); and |

| • | excludes shares of common stock reserved for future issuance under the Claire’s Inc. 2021 Long-Term Incentive Plan (the “2021 Plan”). |

Unless we specifically state otherwise, all information in this prospectus, (1) except for our historical consolidated financial statements and notes thereto included elsewhere in this prospectus, assumes the consummation of the Corporate Conversion immediately prior to the effectiveness of the registration statement of which this prospectus forms a part, (2) assumes no exercise of the underwriters’ option to purchase additional shares of common stock from us or the selling stockholders solely to cover overallotments, (3) gives effect to our amended and restated certificate of incorporation and bylaws, which will be in effect prior to the closing of this offering, (4) assumes an initial public offering price of $ per share of our common stock (the midpoint of the estimated price range set forth on the cover page of this prospectus) and (5) assumes a -for- split of our common stock, to occur after the effectiveness of the registration statement of which this prospectus forms a part and prior to the closing of this offering. The share and per share information in the financial statements and the related notes thereto included elsewhere in this prospectus are presented on a historical basis only and therefore do not reflect the Corporate Conversion, the -for- stock split of our common stock or the completion of the offering.

20

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL AND OTHER DATA

The following table presents our summary historical consolidated financial and other data as of the dates and for the periods indicated. The summary historical consolidated financial data as of and for the fiscal years ended January 30, 2021 and February 1, 2020, are derived from the audited historical consolidated financial statements included elsewhere in this prospectus. The summary historical consolidated financial data as of and for the three and nine months ended October 30, 2021 and October 31, 2020 are derived from the interim unaudited historical condensed consolidated financial statements included elsewhere in this prospectus.

Historical results are not necessarily indicative of the results to be expected for future periods. We refer you to the notes to our historical consolidated financial statements for a discussion of the basis on which our historical consolidated financial statements are prepared.

Our fiscal year ends on the Saturday closest to January 31, resulting in fiscal years of either 52 or 53 weeks. All references to a fiscal year refer to the fiscal year ending on the Saturday closest to January 31 of the following year. For example, references to “fiscal year 2020” and “fiscal year 2019” relate to our fiscal years ended January 30, 2021 and February 1, 2020, respectively.

This table should be read in conjunction with the sections entitled “Capitalization” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our historical consolidated financial statements and notes thereto included elsewhere in this prospectus.

| Three Months Ended | Nine Months Ended | Year Ended | ||||||||||||||||||||||

| October 30, 2021 | October 31, 2020 | October 30, 2021 | October 31, 2020 | January 30, 2021 | February 1, 2020 | |||||||||||||||||||

(in thousands) | ||||||||||||||||||||||||

Income Statement Data: | ||||||||||||||||||||||||

Net sales | $ | 357,283 | $ | 284,748 | $ | 986,374 | $ | 610,525 | $ | 910,341 | $ | 1,284,541 | ||||||||||||

Cost of sales, occupancy and buying expense (exclusive of depreciation and amortization shown separately below) | 148,985 | 128,175 | 415,507 | 335,951 | 471,960 | 595,372 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Gross profit | 208,298 | 156,573 | 570,867 | 274,574 | 438,381 | 689,169 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Operating expenses: | ||||||||||||||||||||||||

Selling, general and administrative expense | 149,923 | 111,914 | 402,091 | 264,206 | 387,683 | 489,839 | ||||||||||||||||||

Depreciation and amortization | 16,448 | 14,923 | 48,048 | 49,712 | 66,310 | 59,607 | ||||||||||||||||||

Other income, net | (2,150 | ) | (626 | ) | (4,188 | ) | (3,357 | ) | (6,214 | ) | (8,650 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total operating expenses | $ | 164,221 | $ | 126,211 | $ | 445,951 | $ | 310,561 | $ | 447,779 | $ | 540,796 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Operating income (loss) | 44,077 | 30,362 | 124,916 | (35,987 | ) | (9,398 | ) | 148,373 | ||||||||||||||||

Reorganization items, net | 50 | 60 | 81 | (468 | ) | (372 | ) | 4,871 | ||||||||||||||||

Loss on early debt extinguishment | — | — | — | — | — | 250,588 | ||||||||||||||||||

21

Table of Contents

| Three Months Ended | Nine Months Ended | Year Ended | ||||||||||||||||||||||

| October 30, 2021 | October 31, 2020 | October 30, 2021 | October 31, 2020 | January 30, 2021 | February 1, 2020 | |||||||||||||||||||

(in thousands) | ||||||||||||||||||||||||

Loss (gain) on derivative liability | (12,306 | ) | 6,670 | 143,053 | 55,110 | 41,349 | 55,095 | |||||||||||||||||

Interest expense, net | 9,167 | 8,861 | 28,056 | 31,586 | 41,333 | 28,389 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Income (loss) before income tax (benefit) expense | 47,166 | 14,771 | (46,274 | ) | (122,215 | ) | (91,708 | ) | (190,570 | ) | ||||||||||||||

Income tax (benefit) expense | (28,125 | ) | 8,458 | (13,901 | ) | (16,891 | ) | (24,728 | ) | 7,647 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net income (loss) | $ | 75,291 | $ | 6,313 | $ | (32,373 | ) | $ | (105,324 | ) | $ | (66,980 | ) | $ | (198,217 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Other comprehensive income (loss): | ||||||||||||||||||||||||

Foreign currency translation adjustments | 482 | 223 | 758 | 278 | 1,264 | (1,220 | ) | |||||||||||||||||

Net gain (loss) on intra-entity foreign currency transactions, net of income tax (benefit) expense of $45, $(0), $86, $(270), $(217) and $167 | (2,858 | ) | 14 | (4,032 | ) | 4,132 | 8,836 | (1,993 | ) | |||||||||||||||

|

|

|

|

|

|