UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

| |

☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2024

OR

| |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from______ to______

Commission File Number: 001-39493

SPIRE GLOBAL, INC.

(Exact Name of Registrant as Specified in its Charter)

| |

Delaware | 85-1276957 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer

Identification No.) |

8000 Towers Crescent Drive Suite 1100 Vienna, Virginia 22182 |

(Address of principal executive offices) (Zip Code) |

(202) 301-5127

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

Class A common stock, par value of $0.0001 per share | | SPIR | | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☐ No ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | |

Large accelerated filer |

| ☐ |

| Accelerated filer |

| ☐ |

Non-accelerated filer |

| ☒ |

| Smaller reporting company |

| ☒ |

Emerging growth company | | ☒ | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The registrant had outstanding 25,734,974 shares of Class A common stock and 1,507,325 shares of Class B common stock as of February 14, 2025.

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains forward-looking statements within the meaning of the federal securities laws, which statements involve substantial risks and uncertainties. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “would,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential,” “seek” or “continue” or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans or intentions. Forward-looking statements contained in this Quarterly Report on Form 10-Q include, but are not limited to, statements about:

•our ability to meet our financial covenants in the future;

•the sufficiency of our working capital in the future;

•changes in our growth, strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, and plans;

•our ability to remedy identified material weaknesses;

•failure to complete the Transactions would have a material adverse effect on us;

•uncertainties associated with the Transactions may result in our losing management and other key personnel, which could adversely affect our business and operations;

•there is no assurance that we will be able to realize the anticipated benefits from the Transactions;

•the implementation, market acceptance, and success of our business model;

•the ability to develop new offerings, services, solutions and features and bring them to market in a timely manner and make enhancements to our business;

•the quality and effectiveness of and advancements in our technology and our ability to accurately and effectively use data and engage in predictive analytics;

•overall level of customer demand for our products and offerings;

•expectations and timing related to product launches;

•expectations of achieving and maintaining profitability;

•projections of total addressable markets, market opportunity, and market share;

•our ability to acquire data sets, software, equipment, satellite components, and regulatory approvals from third parties;

•our expectations concerning relationships with third parties;

•our ability to acquire or develop products or technologies we believe could complement or expand our platform or to expand our products and offerings internationally;

•our ability to obtain and protect patents, trademarks, licenses and other intellectual property rights;

•our ability to utilize potential net operating loss carryforwards;

•developments and projections relating to our competitors and industries, such as the projected growth in demand for space-based data;

•our ability to acquire new customers and partners or obtain renewals, upgrades, or expansions from our existing customers;

•our ability to compete with existing and new competitors in existing and new markets and offerings;

•our ability to retain or recruit officers, key employees or directors;

•the conversion or planned repayment of our debt obligations;

•our future capital requirements and sources and uses of cash;

•our ability to obtain funding for our operations;

•our business, expansion plans, and opportunities;

•our expectations regarding regulatory approvals and authorizations;

•the expectations regarding the effects of existing and developing laws and regulations, including with respect to regulations around satellites, intellectual property law, and privacy and data protection;

•global and domestic economic conditions, including currency exchange rate fluctuations, inflation, rising interest rates and geopolitical uncertainty and instability, and their impact on demand and pricing for our offerings in affected markets; and

•the impact of global health crises on global capital and financial markets, general economic conditions in the United States, and our business and operations.

We caution you that the foregoing list may not contain all of the forward-looking statements made in this Quarterly Report on Form 10-Q. You should not rely upon forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Quarterly Report on Form 10-Q primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations, and prospects. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties, and other factors, including those described in Part I, Item 1A “Risk Factors” of our Annual Report on Form 10-K/A for the year ended December 31, 2023, and in Part II, Item 1A “Risk Factors” of this Quarterly Report on Form 10-Q. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Quarterly Report on Form 10-Q. We cannot assure you that the results, events, and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events, or circumstances could differ materially from those described in the forward-looking statements.

Neither we nor any other person assumes responsibility for the accuracy and completeness of any of these forward-looking statements. Moreover, the forward-looking statements made in this Quarterly Report on Form 10-Q relate only to expectations as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Quarterly Report on Form 10-Q to reflect events or circumstances after the date of this Quarterly Report on Form 10-Q or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments we may make.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Quarterly Report on Form 10-Q, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to rely upon these statements.

PART I—FINANCIAL INFORMATION

Item 1. Unaudited Condensed Consolidated Financial Statements

Spire Global, Inc.

Condensed Consolidated Balance Sheets

(In thousands, except share and per share amounts)

(Unaudited)

| | | | | | | | |

| | June 30, | | | December 31, | |

| | 2024 | | | 2023 | |

Assets | | | | | | |

Current assets | | | | | | |

Cash and cash equivalents | | $ | 23,528 | | | $ | 29,136 | |

Marketable securities | | | 22,271 | | | | 11,726 | |

Accounts receivable, net (including allowance of $406 and $586 as of

June 30, 2024 and December 31, 2023, respectively) | | | 12,423 | | | | 9,911 | |

Contract assets | | | 3,963 | | | | 4,718 | |

Other current assets | | | 9,133 | | | | 16,848 | |

Total current assets | | | 71,318 | | | | 72,339 | |

Property and equipment, net | | | 60,023 | | | | 60,446 | |

Operating lease right-of-use assets | | | 13,454 | | | | 14,921 | |

Goodwill | | | 49,550 | | | | 51,155 | |

Customer relationships | | | 17,809 | | | | 19,363 | |

Other intangible assets | | | 11,484 | | | | 12,660 | |

Other long-term assets, including restricted cash | | | 7,190 | | | | 8,380 | |

Total assets | | $ | 230,828 | | | $ | 239,264 | |

Liabilities and Stockholders’ Equity | | | | | | |

Current liabilities | | | | | | |

Accounts payable | | $ | 7,529 | | | $ | 8,012 | |

Accrued wages and benefits | | | 1,687 | | | | 1,829 | |

Long-term debt, current portion | | | 101,012 | | | | — | |

Contract liabilities, current portion | | | 21,203 | | | | 31,178 | |

Other accrued expenses | | | 8,532 | | | | 8,326 | |

Total current liabilities | | | 139,963 | | | | 49,345 | |

Long-term debt | | | 4,854 | | | | 114,113 | |

Contract liabilities, non-current | | | 21,292 | | | | 17,923 | |

Contingent earnout liability | | | 1,452 | | | | 220 | |

Deferred income tax liabilities | | | 784 | | | | 804 | |

Warrant liability | | | 10,350 | | | | 5,988 | |

Operating lease liabilities, net of current portion | | | 11,791 | | | | 13,079 | |

Other long-term liabilities | | | 8 | | | | 8 | |

Total liabilities | | | 190,494 | | | | 201,480 | |

Commitments and contingencies (Note 9) | | | | | | |

Stockholders’ equity | | | | | | |

Common stock, $0.0001 par value, 1,000,000,000 Class A and 15,000,000 Class

B shares authorized, 24,775,949 Class A and 1,507,325 Class B shares issued

and outstanding at June 30, 2024; 21,097,351 Class A and 1,507,325 Class B shares

issued and outstanding at December 31, 2023 | | | 3 | | | | 2 | |

Additional paid-in capital | | | 524,567 | | | | 477,624 | |

Accumulated other comprehensive loss | | | (6,847 | ) | | | (4,556 | ) |

Accumulated deficit | | | (477,389 | ) | | | (435,286 | ) |

Total stockholders’ equity | | | 40,334 | | | | 37,784 | |

Total liabilities and stockholders’ equity | | $ | 230,828 | | | $ | 239,264 | |

The accompanying notes are an integral part of these unaudited Condensed Consolidated Financial Statements.

Spire Global, Inc.

Condensed Consolidated Statements of Operations

(In thousands, except share and per share amounts)

(Unaudited)

| | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | | Six Months Ended June 30, | |

| | 2024 | | | 2023 | | | 2024 | | | 2023 | |

| | | | | (As Restated) | | | | | | (As Restated) | |

Revenue | | $ | 25,399 | | | $ | 28,065 | | | $ | 60,224 | | | $ | 51,282 | |

Cost of revenue | | | 14,488 | | | | 15,245 | | | | 40,084 | | | | 28,614 | |

Gross profit | | | 10,911 | | | | 12,820 | | | | 20,140 | | | | 22,668 | |

Operating expenses: | | | | | | | | | | | | |

Research and development | | | 7,517 | | | | 7,655 | | | | 13,554 | | | | 14,973 | |

Sales and marketing | | | 5,168 | | | | 6,729 | | | | 10,286 | | | | 13,579 | |

General and administrative | | | 10,009 | | | | 10,718 | | | | 19,853 | | | | 22,541 | |

Loss on decommissioned satellites | | | 529 | | | | 472 | | | | 707 | | | | 472 | |

Allowance for current expected credit loss on notes receivable | | | 40 | | | | — | | | | 80 | | | | — | |

Total operating expenses | | | 23,263 | | | | 25,574 | | | | 44,480 | | | | 51,565 | |

Loss from operations | | | (12,352 | ) | | | (12,754 | ) | | | (24,340 | ) | | | (28,897 | ) |

Other income (expense): | | | | | | | | | | | | |

Interest income | | | 571 | | | | 636 | | | | 1,025 | | | | 1,201 | |

Interest expense | | | (4,773 | ) | | | (4,709 | ) | | | (9,826 | ) | | | (9,287 | ) |

Change in fair value of contingent earnout liability | | | (1,187 | ) | | | 128 | | | | (1,232 | ) | | | 204 | |

Change in fair value of warrant liabilities | | | 2,239 | | | | 357 | | | | (1,963 | ) | | | 1,103 | |

Issuance of stock warrants | | | — | | | | — | | | | (2,399 | ) | | | — | |

Foreign exchange (loss) gain | | | (513 | ) | | | (486 | ) | | | (2,299 | ) | | | 527 | |

Other expense, net | | | (477 | ) | | | (1,130 | ) | | | (1,011 | ) | | | (1,441 | ) |

Total other expense, net | | | (4,140 | ) | | | (5,204 | ) | | | (17,705 | ) | | | (7,693 | ) |

Loss before income taxes | | | (16,492 | ) | | | (17,958 | ) | | | (42,045 | ) | | | (36,590 | ) |

Income tax provision | | | 67 | | | | 414 | | | | 58 | | | | 437 | |

Net loss | | $ | (16,559 | ) | | $ | (18,372 | ) | | $ | (42,103 | ) | | $ | (37,027 | ) |

Basic and diluted net loss per share(1) | | $ | (0.68 | ) | | $ | (0.99 | ) | | $ | (1.82 | ) | | $ | (2.03 | ) |

Weighted-average shares used in computing basic and diluted net loss per share(1) | | | 24,487,484 | | | | 18,468,949 | | | | 23,150,265 | | | | 18,283,958 | |

(1) The shares of the Company's common stock and the per share amounts for the three and six months ended June 30, 2023, have been retroactively adjusted to reflect the 1-for-8 reverse stock split (Note 1)

The accompanying notes are an integral part of these unaudited Condensed Consolidated Financial Statements.

Spire Global, Inc.

Condensed Consolidated Statements of Comprehensive Loss

(In thousands)

(Unaudited)

| | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | | Six Months Ended June 30, | |

| | 2024 | | | 2023 | | | 2024 | | | 2023 | |

| | | | | (As Restated) | | | | | | (As Restated) | |

Net loss | | $ | (16,559 | ) | | $ | (18,372 | ) | | $ | (42,103 | ) | | $ | (37,027 | ) |

Other comprehensive (loss) gain: | | | | | | | | | | | | |

Foreign currency translation adjustments | | | (729 | ) | | | 4,357 | | | | (2,289 | ) | | | 2,743 | |

Net unrealized (loss) gain on investments

(net of tax) | | | — | | | | (7 | ) | | | (2 | ) | | | 37 | |

Comprehensive loss | | $ | (17,288 | ) | | $ | (14,022 | ) | | $ | (44,394 | ) | | $ | (34,247 | ) |

The accompanying notes are an integral part of these unaudited Condensed Consolidated Financial Statements.

Spire Global, Inc.

Condensed Consolidated Statements of Changes in Stockholders’ Equity

(In thousands, except share amounts)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Common Stock | | | Additional

Paid in | | | Accumulated

Other

Comprehensive | | | Accumulated | | | Total

Stockholders' | |

| | | Shares | | | Amount | | | Capital | | | Loss | | | Deficit | | | Equity | |

Balance, March 31, 2024 | | | | 25,822,914 | | | $ | 3 | | | $ | 519,400 | | | $ | (6,118 | ) | | $ | (460,830 | ) | | $ | 52,455 | |

Release of Restricted Stock Units | | | | 380,235 | | | | — | | | | — | | | | — | | | | — | | | | — | |

Issuance of common stock under

Employee Stock Purchase Plan | | | | 79,903 | | | | — | | | | 370 | | | | — | | | | — | | | | 370 | |

Exercise of stock options | | | | 222 | | | | — | | | | 2 | | | | — | | | | — | | | | 2 | |

Stock compensation expense | | | | — | | | | — | | | | 4,795 | | | | — | | | | — | | | | 4,795 | |

Net loss | | | | — | | | | — | | | | — | | | | — | | | | (16,559 | ) | | | (16,559 | ) |

Foreign currency translation

adjustments | | | | — | | | | — | | | | — | | | | (729 | ) | | | — | | | | (729 | ) |

Balance, June 30, 2024 | | | | 26,283,274 | | | $ | 3 | | | $ | 524,567 | | | $ | (6,847 | ) | | $ | (477,389 | ) | | $ | 40,334 | |

| | | | | | | | | | | | | | | | | | | |

| | | Common Stock | | | Additional

Paid in | | | Accumulated

Other

Comprehensive | | | Accumulated | | | Total

Stockholders' | |

| | | Shares | | | Amount | | | Capital | | | Loss | | | Deficit | | | Equity | |

Balance, December 31, 2023 | | | | 22,604,676 | | | $ | 2 | | | $ | 477,624 | | | $ | (4,556 | ) | | $ | (435,286 | ) | | $ | 37,784 | |

Release of Restricted Stock Units | | | | 584,746 | | | | — | | | | — | | | | — | | | | — | | | | — | |

Issuance of common stock under

Employee Stock Purchase Plan | | | | 79,903 | | | | — | | | | 370 | | | | — | | | | — | | | | 370 | |

Exercise of stock options | | | | 37,758 | | | | | | | 269 | | | | | | | | | | 269 | |

Stock compensation expense | | | | — | | | | — | | | | 8,423 | | | | — | | | | — | | | | 8,423 | |

Issuance of common stock under

Securities Purchase Agreements | | | | 2,976,191 | | | | 1 | | | | 37,881 | | | | — | | | | — | | | | 37,882 | |

Net loss | | | | — | | | | — | | | | — | | | | — | | | | (42,103 | ) | | | (42,103 | ) |

Foreign currency translation

adjustments | | | | — | | | | — | | | | — | | | | (2,289 | ) | | | — | | | | (2,289 | ) |

Net unrealized loss on

investments (net of tax) | | | — | | | | — | | | | — | | | | (2 | ) | | | — | | | | (2 | ) |

Balance, June 30, 2024 | | | | 26,283,274 | | | $ | 3 | | | $ | 524,567 | | | $ | (6,847 | ) | | $ | (477,389 | ) | | $ | 40,334 | |

The accompanying notes are an integral part of these unaudited Condensed Consolidated Financial Statements.

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Common Stock | | | Additional

Paid in | | | Accumulated

Other

Comprehensive | | | Accumulated | | | Total

Stockholders' | |

| | | Shares(1) | | | Amount(1) | | | Capital | | | Loss | | | Deficit | | | Equity | |

Balance, March 31, 2023

(As Restated) | | | | 19,763,064 | | | $ | 2 | | | $ | 458,697 | | | $ | (8,478 | ) | | $ | (376,383 | ) | | $ | 73,838 | |

Release of Restricted Stock Units | | | | 173,156 | | | | — | | | | — | | | | — | | | | — | | | | — | |

Issuance of common stock under

Employee Stock Purchase Plan | | | | 83,727 | | | | — | | | | 422 | | | | — | | | | — | | | | 422 | |

Stock compensation expense | | | | — | | | | — | | | | 3,340 | | | | — | | | | — | | | | 3,340 | |

Issuance of common stock under the

Equity Distribution Agreement, net | | | | 2,166,389 | | | | — | | | | 7,866 | | | | — | | | | — | | | | 7,866 | |

Net loss (As Restated) | | | | — | | | | — | | | | — | | | | — | | | | (18,372 | ) | | | (18,372 | ) |

Foreign currency translation

adjustments (As Restated) | | | | — | | | | — | | | | — | | | | 4,357 | | | | — | | | | 4,357 | |

Net unrealized loss on

investments (net of tax) | | | — | | | | — | | | | — | | | | (7 | ) | | | — | | | | (7 | ) |

Balance, June 30, 2023

(As Restated) | | | 22,186,336 | | | $ | 2 | | | $ | 470,325 | | | $ | (4,128 | ) | | $ | (394,755 | ) | | $ | 71,444 | |

| | | | | | | | | | | | | | | | | | | |

| | | Common Stock | | | Additional

Paid in | | | Accumulated

Other

Comprehensive | | | Accumulated | | | Total

Stockholders' | |

| | | Shares(1) | | | Amount(1) | | | Capital | | | Loss | | | Deficit | | | Equity | |

Balance, December 31, 2022 | | | | 19,467,183 | | | $ | 2 | | | $ | 455,765 | | | $ | (6,908 | ) | | $ | (357,728 | ) | | $ | 91,131 | |

Release of Restricted Stock Units | | | | 434,309 | | | | — | | | | — | | | | — | | | | — | | | | — | |

Issuance of common stock under

Employee Stock Purchase Plan | | | | 83,727 | | | | — | | | | 422 | | | | — | | | | — | | | | 422 | |

Stock compensation expense | | | | — | | | | — | | | | 5,986 | | | | — | | | | — | | | | 5,986 | |

Issuance of common stock under the

Equity Distribution Agreement, net | | | | 2,166,389 | | | | — | | | | 7,866 | | | | — | | | | — | | | | 7,866 | |

Conversion of warrants to common

stock | | | | 34,728 | | | | — | | | | 286 | | | | — | | | | — | | | | 286 | |

Net loss (As Restated) | | | | — | | | | — | | | | — | | | | — | | | | (37,027 | ) | | | (37,027 | ) |

Foreign currency translation

adjustments (As Restated) | | | — | | | | — | | | | — | | | | 2,743 | | | | — | | | | 2,743 | |

Net unrealized gain on

investments (net of tax) | | | — | | | | — | | | | — | | | | 37 | | | | — | | | | 37 | |

Balance, June 30, 2023

(As Restated) | | | 22,186,336 | | | $ | 2 | | | $ | 470,325 | | | $ | (4,128 | ) | | $ | (394,755 | ) | | $ | 71,444 | |

(1) The shares of the Company's common stock have been retroactively adjusted to reflect the 1-for-8 reverse stock split (Note 1).

The accompanying notes are an integral part of these unaudited Condensed Consolidated Financial Statements.

Spire Global, Inc.

Condensed Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

| | | | | | | | |

| | Six Months Ended June 30, | |

| | 2024 | | | 2023 | |

| | | | | (As Restated) | |

Cash flows from operating activities | | | | | | |

Net loss | | $ | (42,103 | ) | | $ | (37,027 | ) |

Adjustments to reconcile net loss to net cash used in operating activities: | | | | | | |

Depreciation and amortization | | | 12,489 | | | | 7,883 | |

Stock-based compensation | | | 8,423 | | | | 5,986 | |

Amortization of operating lease right-of-use assets | | | 1,798 | | | | 1,128 | |

Amortization of debt issuance costs | | | 1,800 | | | | 1,086 | |

Change in fair value of warrant liabilities | | | 1,963 | | | | (1,103 | ) |

Change in fair value of contingent earnout liability | | | 1,232 | | | | (204 | ) |

Issuance of stock warrants | | | 2,399 | | | | — | |

Loss on decommissioned satellites and impairment of assets | | | 924 | | | | 472 | |

Other, net | | | (148 | ) | | | (273 | ) |

Changes in operating assets and liabilities: | | | | | | |

Accounts receivable, net | | | (2,689 | ) | | | (6,441 | ) |

Contract assets | | | 712 | | | | (1,307 | ) |

Other current assets | | | 7,656 | | | | (1,654 | ) |

Other long-term assets | | | 965 | | | | 774 | |

Accounts payable | | | (965 | ) | | | (2,465 | ) |

Accrued wages and benefits | | | (117 | ) | | | 413 | |

Contract liabilities | | | (6,161 | ) | | | 4,648 | |

Other accrued expenses | | | 275 | | | | 359 | |

Operating lease liabilities | | | (1,692 | ) | | | (890 | ) |

Net cash used in operating activities | | | (13,239 | ) | | | (28,615 | ) |

Cash flows from investing activities | | | | | | |

Purchases of short-term investments | | | (30,147 | ) | | | (25,845 | ) |

Maturities of short-term investments | | | 20,000 | | | | 28,400 | |

Purchase of property and equipment | | | (12,585 | ) | | | (6,653 | ) |

Net cash used in investing activities | | | (22,732 | ) | | | (4,098 | ) |

Cash flows from financing activities | | | | | | |

Proceeds from Securities Purchase Agreements, net | | | 37,881 | | | | — | |

Proceeds from long-term debt | | | — | | | | 19,886 | |

Proceeds from issuance of common stock under the Equity Distribution Agreement, net | | | — | | | | 7,866 | |

Payments on long-term debt | | | (10,113 | ) | | | — | |

Proceeds from exercise of stock options | | | 269 | | | | — | |

Proceeds from employee stock purchase plan | | | 370 | | | | 422 | |

Net cash provided by financing activities | | | 28,407 | | | | 28,174 | |

Effect of foreign currency translation on cash, cash equivalents and restricted cash | | | 1,947 | | | | 538 | |

Net decrease in cash, cash equivalents and restricted cash | | | (5,617 | ) | | | (4,001 | ) |

Cash, cash equivalents and restricted cash | | | | | | |

Beginning balance | | | 29,633 | | | | 47,569 | |

Ending balance | | $ | 24,016 | | | $ | 43,568 | |

Supplemental disclosure of cash flow information | | | | | | |

Cash paid for interest | | $ | 7,643 | | | $ | 7,927 | |

Income taxes paid | | $ | 42 | | | $ | 585 | |

Noncash operating, investing and financing activities | | | | | | |

Property and equipment purchased but not yet paid | | $ | 1,373 | | | $ | 1,742 | |

Right-of-use assets obtained in exchange for lease liabilities | | $ | 490 | | | $ | 2,925 | |

Issuance of stock warrants with long-term debt (Note 8) | | $ | — | | | $ | 286 | |

The accompanying notes are an integral part of these unaudited Condensed Consolidated Financial Statements.

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

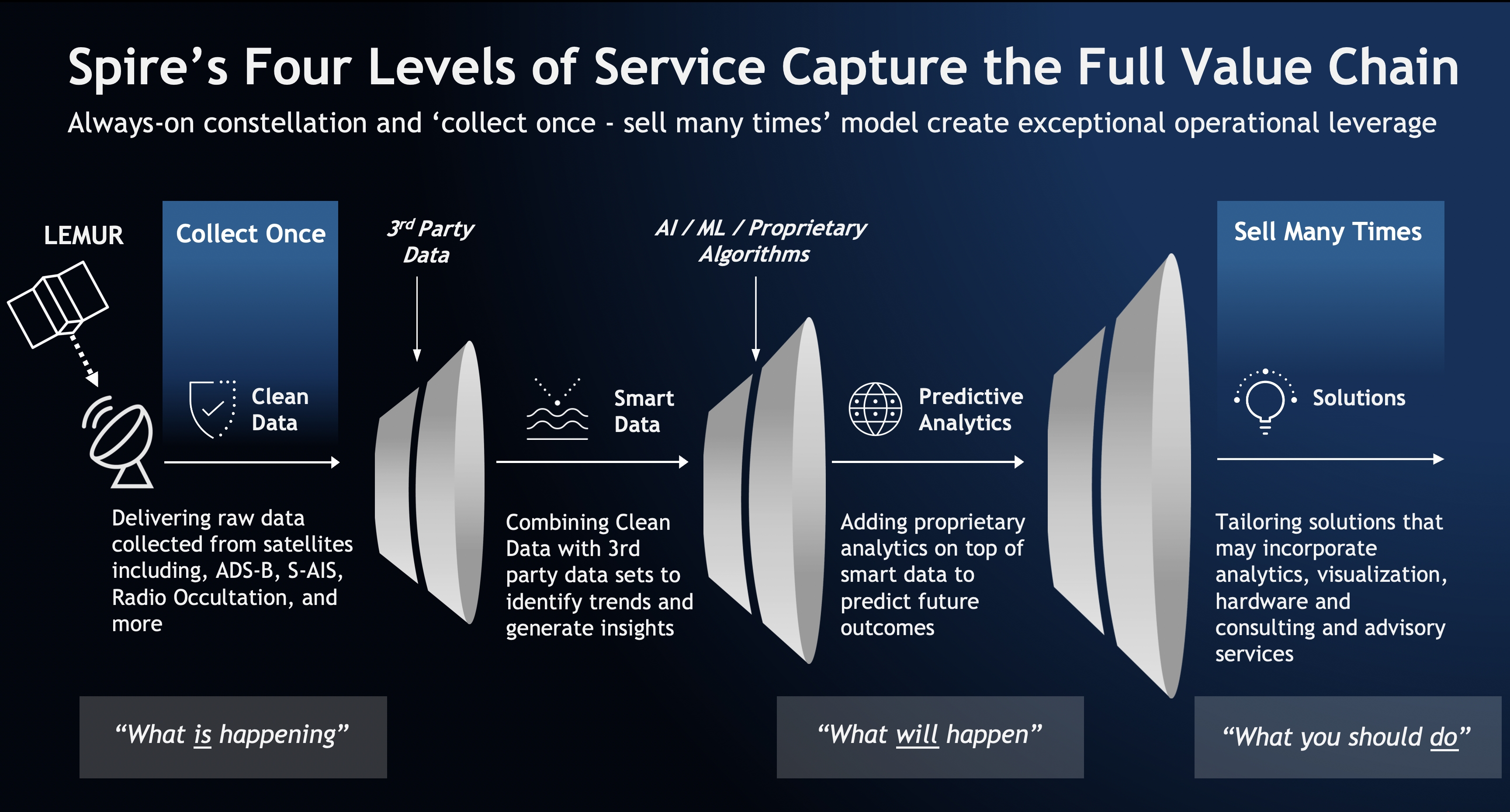

Spire Global, Inc. (“Spire” or the “Company”), founded in August 2012, is a global provider of space-based data and analytics that offers its customers unique datasets and insights about earth from the ultimate vantage point. The Company collects this space-based data through its proprietary constellation of multi-purpose nanosatellites. The Company designs, manufacturers, integrates, and operates its own satellites and ground stations to deliver unique end-to-end comprehensive solutions. The Company offers the following three data solutions to customers: Maritime, Aviation, and Weather and Climate. As a fourth solution, the Company is providing “space-as-a-service” through its Space Services solution.

The Company is headquartered in Vienna, Virginia and has several wholly-owned operating subsidiaries in the United States, United Kingdom, Luxembourg, Singapore, Australia, Germany, and Canada.

On August 16, 2021, Spire Global Subsidiary, Inc. (formerly known as Spire Global, Inc.) (“Legacy Spire”) closed its previously announced merger with NavSight Holdings, Inc. (“NavSight”), a special purpose acquisition company. As a result, Legacy Spire continued as the surviving corporation and a wholly owned subsidiary of NavSight (the “Merger,” and such consummation, the “Closing”). NavSight then changed its name to Spire Global, Inc. and Legacy Spire changed its name to Spire Global Subsidiary, Inc.

On September 14, 2022, the Company entered into an Equity Distribution Agreement (the “Equity Distribution Agreement”) with Canaccord Genuity LLC, as sales agent (the “Agent”). In accordance with the terms of the Equity Distribution Agreement, the Company may offer and sell its Class A common stock, having an aggregate offering price of up to $85,000 from time to time through the Agent pursuant to a registration statement on Form S-3, which became effective on September 26, 2022. Under the Equity Distribution Agreement, the Company sold (i) 2,166,389 shares of its Class A common stock during the year ended December 31, 2023 for gross proceeds of $8,235 and (ii) no shares during the six months ended June 30, 2024.

On March 24, 2023, the Company, was notified by the New York Stock Exchange (“NYSE”) that the Company was not in compliance with Rule 802.01C of the NYSE’s Listed Company Manual (“Rule 802.01C”) relating to the minimum average closing price of the Company’s Class A common stock, par value of $0.0001 per share, required over a consecutive 30 trading-day period. On August 31, 2023, the Company effected a reverse stock split at a ratio of 1-for-8 (the “Reverse Stock Split”) of its common stock. In connection with the Reverse Stock Split, every eight shares of the Company’s Class A and Class B common stock issued and outstanding as of the effective date were automatically combined into one share of Class A or Class B common stock, as applicable. On September 25, 2023, the Company received formal notice from the NYSE that the Company had regained compliance with Rule 802.01C.

On February 4, 2024, the Company and Signal Ocean Ltd (“Signal Ocean”) entered into a securities purchase agreement (the “SPA”) for the issuance and sale of 833,333 shares of the Company’s Class A common stock to Signal Ocean at a price of $12.00 per share (the “Private Placement”). The Private Placement closed on February 8, 2024, resulting in gross proceeds to the Company of $10.0 million.

On March 21, 2024, the Company entered into a Securities Purchase Agreement (the “Securities Purchase Agreement”) with institutional investors (the “Investors”), pursuant to which the Company issued and sold in a registered direct offering (the “Offering”), (i) an aggregate of 2,142,858 shares of Class A common stock and (ii) warrants exercisable for an aggregate of 2,142,858 shares of Class A common stock (“Securities Purchase Agreement Warrants”) to the Investors. Each share of Class A common stock and accompanying Securities Purchase Agreement Warrant to purchase one share of Class A common stock was sold at an offering price of $14.00. The aggregate gross proceeds to the Company from the Offering totaled $30,000 before deducting the placement agent’s fees and related offering expenses. The Securities Purchase Agreement Warrants had an exercise price equal to $14.50 per share of Class A common stock, were exercisable for a term beginning on March 25, 2024, and expired on July 3, 2024, with no warrants exercised.

On March 21, 2024, the Company entered into a placement agency agreement (the “Placement Agency Agreement”) with Alliance Global Partners (“A.G.P” or the “Placement Agent”), pursuant to which the Company engaged A.G.P as the exclusive placement agent in connection with the Offering. The Company paid A.G.P a cash fee equal to 6% of the gross proceeds from

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

the sale of shares and Securities Purchase Agreement Warrants to the Investors, or $1,800, in March 2024. The Company agreed to pay a cash fee equal to 4% of the gross exercise price paid in cash with respect to the exercise of the Securities Purchase Agreement Warrants, which are now expired.

The par value of the common stock remains $0.0001 per share after the Reverse Stock Split. All share and per share information has been retroactively adjusted to reflect the impact of the Reverse Stock Split for applicable periods presented.

On November 13, 2024, the Company entered into a Share Purchase Agreement (the “Purchase Agreement”) with Kpler Holding SA, a Belgian corporation (“Buyer”), pursuant to which the Company agreed to sell its maritime business to Buyer and enter into certain ancillary agreements (the “Transactions”). The maritime business to be sold pursuant to the Transactions does not include any part of the Company’s satellite network or operations. The Purchase Agreement provides that the closing of the Transactions is subject to the satisfaction or waiver of certain closing conditions set forth in the Purchase Agreement. Refer to Note 12, Subsequent Events, for detailed discussion.

Restatement of Financial Statements

On March 3, 2025, the Company filed its Annual Report on Form 10-K/A for the year ended December 31, 2023 (the “Form 10-K/A”), which included audited restated consolidated financial statements as of and for the fiscal years ended December 31, 2023, and December 31, 2022, as well as unaudited restated condensed consolidated financial information as of the quarter ends and for the interim periods in the fiscal years ended December 31, 2023 and 2022 (collectively, the “Affected Periods”) to make corrections related to consideration of embedded leases for a contract in its “Space as a Service” business (the “Space Services Contract”), recognition of an allowance for current expected credit losses related to a note receivable issued to a customer, revenue recognition for contracts in its customer-funded or co-funded research and development arrangements (the “R&D Services Contracts,” and together with the Space Services Contracts, the “Space Services and R&D Services Contracts”) and Space Services Contracts, and income statement classification of costs related to R&D Services Contracts. The Form 10-K/A included corrections to the condensed consolidated financial statements for the Affected Periods presented in this Quarterly Report on Form 10-Q. Therefore, the Company has reflected these corrections to the condensed consolidated financial statements for prior periods presented in this Quarterly Report on Form 10-Q. Additionally, prior period amounts in the applicable notes to the condensed consolidated financial statements have been corrected. Refer also to Note 13 of Notes to Condensed Consolidated Financial Statements of this Quarterly Report on Form 10-Q for unaudited restated condensed consolidated financial information for the three and six months ended June 30, 2023.

2.Summary of Significant Accounting Policies

Basis of Presentation

The condensed consolidated financial statements and accompanying notes are unaudited and have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) and regulations of the U.S. Securities and Exchange Commission (the “SEC") for interim financial reporting.

Certain information and footnote disclosures normally included in consolidated financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to rules and regulations applicable to interim financial reporting. The unaudited condensed consolidated financial statements were prepared on the same basis as the audited consolidated financial statements and, in the opinion of management, contain all adjustments, consisting of normal recurring adjustments, necessary for a fair statement of its financial position, results of operations and cash flows for the periods indicated. These condensed consolidated financial statements should be read in conjunction with the consolidated financial statements included within the Form 10-K/A.

The information as of December 31, 2023, included on the condensed consolidated balance sheets was derived from the Company’s audited consolidated financial statements. All intercompany accounts and transactions have been eliminated in consolidation.

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

Results of operations for the three and six months ended June 30, 2024, are not necessarily indicative of the results that may be expected for any other interim period or for the year ending December 31, 2024.

Reverse Stock Split

For the three and six months ended, and as of, June 30, 2023, reported share amounts, including issued and outstanding shares, per share amounts, and reported issued and outstanding warrants and other securities convertible into common stock in these condensed consolidated financial statements and accompanying notes have been retroactively adjusted for the Reverse Stock Split by applying the Reverse Stock Split ratio. The number of authorized shares of common stock was not impacted by the Reverse Stock Split, and therefore has not been retroactively adjusted.

Liquidity Risks and Uncertainties

The Company has a history of operating losses and negative cash flows from operations since inception. During the six months ended June 30, 2024, net loss was $42,103, cash used in operations was $13,239 and the Company received net proceeds of $9,825 from the Private Placement and $28,056 from the Offering. The Company held cash and cash equivalents of $23,528, excluding restricted cash of $488, and investment in short-term marketable securities of $22,271 as of June 30, 2024.

The Company’s ability to continue as a going concern for the next 12 months from the date of issuance of these condensed consolidated financial statements is dependent upon its ability to obtain sufficient cash to meet its obligations, including the repayment of all amounts owed pursuant to the Blue Torch Financing Agreement (as amended, and as defined below in Note 6). The Company has failed to meet its leverage ratio and minimum liquidity financial covenants and SEC periodic filing requirement non-financial covenant under the Blue Torch Financing Agreement, and therefore Blue Torch Finance LLC (“Blue Torch”) has the right to accelerate and declare all or any portion of the loans outstanding under the Blue Torch Financing Agreement to be due and payable. Further, upon the filing of the Form 10-K/A, the Company failed to comply with the non-financial covenant requiring the Company to have a report or opinion of its auditor without an explanatory paragraph expressing substantial doubt about its ability to continue as a going concern. Based on the Company’s current cash and cash equivalents and investment in marketable securities balances and expected future financial results, if the Transactions (as defined below) do not close, the Company will not have sufficient liquidity to continue operations for at least the next twelve months from the issuance of these condensed consolidated financial statements. Furthermore, the Company will not have sufficient cash to repay the balance of the loans outstanding under the Blue Torch Financing Agreement in the event Blue Torch declares all or any portion of the loans to be due and payable.

The Company entered into a Share Purchase Agreement (the “Purchase Agreement”) with Kpler Holding SA, a Belgian corporation (“Buyer”), pursuant to which the Company agreed to sell its maritime business to Buyer and enter into certain ancillary agreements (the “Transactions”). The maritime business to be sold pursuant to the Transactions does not include any part of the Company’s satellite network or operations. The purchase price to be paid by Buyer to the Company at the closing of the Transactions is a cash payment based upon an enterprise value of $233,500, subject to certain adjustments. The Transactions also include a twelve-month transition service and data provision agreement for $7,500. The Purchase Agreement provides that the closing of the Transactions is subject to the satisfaction or waiver of certain closing conditions set forth in the Purchase Agreement.

On February 10, 2025, the Company filed a complaint in the Delaware Court of Chancery against Buyer seeking a grant of specific performance ordering Buyer to satisfy its obligations under the Purchase Agreement and consummate the closing in accordance with the terms of the Purchase Agreement. In the complaint, the Company also requested a declaratory judgment declaring that Buyer has breached its obligations under the Purchase Agreement and is not excused from performing its obligations under the Purchase Agreement, including proceeding with the closing.

Kpler removed the matter to the District of Delaware, pursuant to a contract term in the Purchase Agreement promising not to contest removal to that court. The District of Delaware initially selected a March 4 trial date, but on February 26, 2025, the court set a trial date of May 28-30, 2025. There is no assurance as to what action the District of Delaware will take with respect to the proceeding initiated by the Company and there is no assurance as to whether or not the Transactions will be consummated on

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

the terms contemplated or at all. The amount of any damages which may be sought or obtained from Buyer cannot be determined at this time.

The Company intends to use the proceeds from the closing of the Transactions to repay all amounts owed under the Blue Torch Financing Agreement. However, as described above, there is currently no assurance that the Transactions will close or when the Transactions may close. Given the expected delay in the closing of the Transactions, the Company intends to seek additional equity or debt financing (including securities convertible or exchangeable for equity) and may seek waivers of or amendments to contractual obligations, delay, limit, reduce, or terminate certain commercial efforts, or pursue merger, disposition or other strategies, any of which could adversely affect its business, results of operations, and financial condition. There is no assurance that the Company will be successful in achieving any of the foregoing. Due to the Company’s projected cash needs, including amounts owed pursuant to the Blue Torch Financing Agreement and the Company’s breach of its covenants under the Blue Torch Financing Agreement, there is substantial doubt about its ability to continue as a going concern for a period of at least 12 months from the date of issuance of these condensed consolidated financial statements. The condensed consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Macroeconomic and Geopolitical

Over the past two years, the Company has been impacted by the macroeconomic environment, such as fluctuations in foreign currencies, increasing interest rates, and geopolitical conflicts like the Russian invasion of Ukraine, Israel's war with Hamas and the increased tensions between China and the United States.

The U.S. Dollar exhibited a modest decrease in strength against the local functional currencies of our foreign subsidiaries for the six months ended June 30, 2024, as compared to the six months ended June 30, 2023. The U.S. Dollar's modest decrease had a marginal positive impact on the Company's revenue, as approximately one-third of the Company's sales are conducted in foreign currencies. Conversely, the decrease in the value of the U.S. Dollar had a marginal unfavorable impact on the Company's expenses, given that a majority of the Company's workforce resides in countries other than the United States.

The macroeconomic environment has caused existing or potential customers to re-evaluate their decision to purchase the Company's offerings, at times resulting in additional customer discounts, extended payment terms, and longer sales cycles.

Increasing interest rates for the six months ended June 30, 2024, compared to the six months ended June 30, 2023, resulted in higher interest expenses as the Company’s credit facility is based on a floating interest rate. The Russian invasion of Ukraine and the continued conflict created additional global sanctions, which caused scheduling shifts or launch cancellations by third-party satellite launch providers, and negatively impacted the availability of launch windows for the Company's constellation replenishment efforts.

If any of these factors continue or worsen, and/or if new macroeconomic or geopolitical issues arise, the Company's results and financial condition could be further negatively impacted. The Company cannot predict the timing, strength, or duration of any economic slowdown, downturn, instability, or recovery, generally or within any particular industry or geography. Any downturn of the general economy or industries in which the Company operates would adversely affect its business, financial condition, and results of operations.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosures of contingent assets and liabilities at the dates of the condensed consolidated financial statements, and the reported amounts of revenues and expenses during the reporting period. Management’s significant estimates include assumptions for revenue recognition, which requires estimates of total costs used in measuring the progress of completion for the cost-based input method, allowance for current expected credit losses, valuation of certain assets and liabilities acquired from the acquisition of exactEarth in November 2021 (the “Acquisition”), realizability of deferred income tax assets, and fair value of equity awards, contingent earnout liabilities, and warrant liabilities. Actual results could differ from those estimates.

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

Based on an evaluation of the lifespans of its in-service satellites and on current capabilities to extend the useful life of in-service satellites via software updates, the Company changed the estimated useful life of its capitalized satellites and related launch costs from three to four years for depreciation purposes. The Company determined it was appropriate to make this change beginning June 2023.

In November 2023, the Company updated the estimated useful lives for 43 capitalized satellites and related launch costs based on updated de-orbit dates. This change represents a change in accounting estimate and the impact of the change was an increase in loss from continuing operations before income taxes of approximately $1,584, or $0.06 per basic and diluted share, and $4,592 or $0.20 per basic and diluted share, for the three and six months ended June 30, 2024, respectively.

Cash, Cash Equivalents, Marketable Securities, and Restricted Cash

The Company considers all highly liquid investments with an original maturity of three months or less to be cash equivalents. Restricted cash included in other long-term assets, including restricted cash on the condensed consolidated balance sheets, represents amounts pledged as guarantees or collateral for financing arrangements and lease agreements, as contractually required.

The Company invests in highly rated securities with the primary objective of minimizing the potential risk of principal loss. The Company’s investment policy generally requires securities to be investment-grade and limits the amount of credit exposure to any one issuer. The Company’s investments in marketable debt securities have been classified and accounted for as available-for-sale. The Company classifies its marketable debt securities as either short-term or long-term based on each instrument’s underlying contractual maturity date. Unrealized gains and losses on marketable debt securities classified as available-for-sale are recognized in accumulated other comprehensive loss. Interest on securities classified as available-for-sale is included in interest income on the condensed consolidated statements of operations.

The following table shows components of cash, cash equivalents, and restricted cash reported on the condensed consolidated balance sheets and in the condensed consolidated statements of cash flows as of the dates indicated:

| | | | | | | | |

| | June 30, | | | December 31, | |

| | 2024 | | | 2023 | |

Cash and cash equivalents | | $ | 23,528 | | | $ | 29,136 | |

Restricted cash included in Other long-term assets | | | 488 | | | | 497 | |

| | $ | 24,016 | | | $ | 29,633 | |

Concentrations of Credit Risk

Financial instruments that potentially subject the Company to concentrations of credit risk consist of cash, cash equivalents and restricted cash, marketable securities, and accounts receivable. The Company typically has cash accounts in excess of Federal Deposit Insurance Corporation insurance coverage limits. The Company has not experienced any losses on such accounts and management believes that the Company’s risk of loss is remote. The Company has a $4,500 note receivable and $551 of accrued interest receivables relating to one customer. The Company has established a $1,298 allowance of current expected credit loss for the note receivable and accrued interest receivable as of June 30, 2024.

The Company has a concentration of contractual revenue arrangements with various government agencies. Entities under common control are reported as a single customer. As of June 30, 2024, and December 31, 2023, the Company did not have any customers that accounted for more than 10% of the Company’s total accounts receivable.

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

The following customers represented 10% or more of the Company’s total revenue for each of the following periods:

| | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, | | | Six Months Ended June 30, | |

| | 2024 | | | 2023 | | | 2024 | | | 2023 | |

| | | | | (As Restated) | | | | | | (As Restated) | |

Customer A(1) | | | 31 | % | | | 33 | % | | | 23 | % | | | 32 | % |

Customer B | | * | | | | 13 | % | | | 16 | % | | * | |

* Revenue from this customer was less than 10% of total revenue during the period.

(1) Consists of multiple U.S. government agencies, of which one government agency represented greater than 10% of total revenue for each of the three and six months ended June 30, 2024 and 2023.

Related Parties

In conjunction with the Company's acquisition of exactEarth in November 2021, Myriota Pty Ltd (“Myriota”), an existing Spire customer, became a related party as a result of exactEarth's approximately 13% ownership of Myriota at the time of acquisition. As of June 30, 2024, the Company had 11.5% ownership of Myriota. The investment in Myriota of $1,556 and $2,216 was included in other long-term assets, including restricted cash on the condensed consolidated balance sheets as of June 30, 2024, and December 31, 2023, respectively. The Company accounts for this investment using the equity method of accounting. The Company's share of earnings or losses on the investment is recorded on a one month lag, due to the timing of receiving financial statements from Myriota, as a component of other expense, net in the condensed consolidated statements of operations. The Company generated $226 and $443 in revenue from Myriota for the three and six months ended June 30, 2024, respectively, and had $54 of accounts receivable, and $180 of contract liabilities, noncurrent from Myriota as of June 30, 2024. The Company generated $238 and $463 in revenue from Myriota for the three and six months ended June 30, 2023, respectively, and had no accounts receivable from Myriota as of December 31, 2023.

Accounting Pronouncements Recently Adopted

In March 2023,the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2023-01, Leases – Common Control Arrangements (Topic 842), to improve the accounting for amortizing leasehold improvements associated with arrangements between entities under common control. The amendment requires that leasehold improvements be amortized by the lessee over the useful life of the leasehold improvements to the common control group (regardless of the lease term) as long as the lessee controls the use of the underlying asset through a lease. Additionally, leasehold improvements should be accounted for as a transfer between entities under common control through an adjustment to equity when the lessee no longer controls the use of the underlying asset. The amendments in this update are effective for financial statements issued for annual periods beginning after December 15, 2023, with early adoption permitted. The adoption of ASU 2023-01 as of January 1, 2024, did not impact the Company’s condensed consolidated financial statements.

In August 2023, the FASB issued ASU 2023-05, Business Combinations – Joint Venture Formations (Subtopic 805-60): Recognition and Initial Measurement. The amendments in this ASU are intended to facilitate consistency in the application of accounting guidance upon the formation of entities qualifying as joint ventures (“JVs”). This ASU generally requires the use of business combinations accounting at the JV formation date, which would result in the contributed assets/liabilities being revalued to fair value and potentially result in the recognition of goodwill and other intangibles on the JV’s financial statements. However, this ASU does not alter the ongoing accounting for the JV’s operations. This guidance is effective for JVs with formation dates on or after January 1, 2025. The adoption of ASU 2023-05 as of January 1, 2024, did not impact the Company’s condensed consolidated financial statements.

Accounting Pronouncements Not Yet Adopted

In November 2023, the FASB issued ASU 2023-07, Segment Reporting - Improvements to Reportable Segment Disclosures (Topic 280), to improve reportable segment disclosure requirements, primarily through enhanced disclosures about significant segment expenses. The amendments enhance interim disclosure requirements, clarify circumstances in which an entity can disclose multiple segment measures of profit or loss, provide new segment disclosure requirements for entities within a single reportable segment, and contain other disclosure requirements. The ASU is effective for fiscal years beginning after December

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted and will be applied retrospectively to all prior periods presented in the financial statements. The Company is currently evaluating the ASU to determine its impact on the Company’s disclosures.

In December 2023, the FASB issued ASU 2023-09, Income Taxes - Improvements to Income Tax Disclosures (Topic 740), to further enhance income tax disclosures to enable investors to better assess how an entity’s operations, related tax risks, tax planning, and operational opportunities affect its tax rate and prospects for future cash flows. The improvements primarily relate to the disaggregation of rate reconciliation categories and income taxes paid by jurisdiction. The other amendments improve the effectiveness and comparability of disclosures by adding disclosures of pretax income (or loss) and income tax expense (or benefit) to be consistent with SEC regulations. The ASU is effective for public business entities for annual reporting periods beginning after December 15, 2024. Early adoption is permitted and should be applied prospectively or retrospectively. The Company is currently evaluating the ASU to determine its impact on the Company’s disclosures.

In March 2024, the SEC adopted final rules under SEC Release No. 33-11275, The Enhancement and Standardization of Climate-Related Disclosures for Investors, which will require registrants to provide certain climate-related information in their annual reports and registration statements. The rules will require disclosure of material climate-related risks, how the board of directors and management oversee and manage such risks, and the actual and potential impact of such risks on the registrant. It will also require disclosure about material climate-related targets and goals, and the financial impact of severe weather events and other natural conditions in the notes to audited financial statements. In April 2024, the SEC voluntarily stayed the final rule as a result of pending legal challenges. The disclosure requirements will apply at the earliest to reports for the Company's fiscal year ended December 31, 2025 (or potentially later depending on the Company's filer status at the time), pending resolution of the stay. The Company is currently evaluating the impact on the Company's disclosures.

In November 2024, the FASB issued ASU 2024-03, Income Statement-Reporting Comprehensive Income-Expense Disaggregation Disclosures (Subtopic 220-40). Additionally, in January 2025, the FASB issued ASU 2025-01 to clarify the effective date of ASU 2024-03. The standard provides guidance to expand disclosures related to the disaggregation of income statement expenses. The standard requires, in the notes to the financial statements, disclosure of specified information about certain costs and expenses, which includes purchases of inventory, employee compensation, depreciation and intangible asset amortization included in each relevant expense caption. This guidance is effective for fiscal years beginning after December 15, 2026, and interim periods within annual reporting periods beginning after December 15, 2027, on a retrospective or prospective basis, with early adoption permitted. The Company is assessing the guidance, noting the adoption impacts disclosure only.

3.Revenue, Contract Assets, Contract Liabilities and Remaining Performance Obligations

Disaggregation of Revenue

Revenue from subscription-based contracts was $19,703 and $37,759, or 78% and 63% of total revenue, for the three and six months ended June 30, 2024, respectively, and was $20,247 and $39,847, or 72% and 78% of total revenue, for the three and six months ended June 30, 2023, respectively. Revenue from non-subscription-based contracts was $5,696 and $22,465, or 22% and 37% of total revenue, for the three and six months ended June 30, 2024, respectively, and was $7,819 and $11,435, or 28% and 22% of total revenue, for the three and six months ended June 30, 2023, respectively.

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

The following revenue disaggregated by geography, derived from billing addresses, was recognized:

| | | | | | | | | | | | | | | | |

| | Three Months Ended June 30, 2024 | | | Six Months Ended June 30, 2024 | |

Americas (1) | | $ | 13,880 | | | | 55 | % | | $ | 36,560 | | | | 61 | % |

EMEA(2) | | | 9,436 | | | | 37 | % | | | 19,395 | | | | 32 | % |

Asia Pacific | | | 2,083 | | | | 8 | % | | | 4,269 | | | | 7 | % |

Total | | $ | 25,399 | | | | 100 | % | | $ | 60,224 | | | | 100 | % |

| | | | | | | | | | | | |

| | Three Months Ended June 30, 2023 | | | Six Months Ended June 30, 2023 | |

| | (As Restated) | | | (As Restated) | |

Americas (1) | | $ | 16,559 | | | | 59 | % | | $ | 28,238 | | | | 55 | % |

EMEA(2) | | | 8,373 | | | | 30 | % | | | 16,592 | | | | 32 | % |

Asia Pacific | | | 3,133 | | | | 11 | % | | | 6,452 | | | | 13 | % |

Total | | $ | 28,065 | | | | 100 | % | | $ | 51,282 | | | | 100 | % |

(1)U.S. represented 49% and 41% of total revenue for the three and six months ended June 30, 2024, respectively, and 43% and 44% of total revenue for the three and six months ended June 30, 2023, respectively. Canada represented 20% and 11% for the six months ended June 30, 2024 and 2023, respectively.

(2)United Kingdom represented 15% and 11% of total revenue for the three and six months ended June 30, 2024 and United Kingdom represented 12% and 11% of total revenue for the three and six months ended June 30, 2023, respectively.

Contract Assets

As of June 30, 2024, contract assets were $4,161, of which $3,963 was reported in contract assets, and $198 was reported in other long-term assets including restricted cash on the Company's condensed consolidated balance sheets. At December 31, 2023, contract assets were $4,917 of which $4,718 was reported in contract assets, and $199 was reported in other long-term assets, including restricted cash on the Company's condensed consolidated balance sheets.

Changes in contract assets for the six months ended June 30, 2024 and 2023 were as follows:

| | | | | | | | |

| | 2024 | | | 2023 | |

| | | | | (As Restated) | |

Balance as of January 1 | | $ | 4,917 | | | $ | 2,881 | |

Contract assets recorded during the period | | | 3,970 | | | | 3,752 | |

Reclassified to accounts receivable during the period | | | (4,685 | ) | | | (2,445 | ) |

Other | | | (41 | ) | | | 40 | |

Balance as of June 30 | | $ | 4,161 | | | $ | 4,228 | |

Contract Liabilities

As of June 30, 2024, contract liabilities were $42,495, of which $21,203 was reported in contract liabilities, current portion, and $21,292 was reported in other long-term liabilities on the Company’s condensed consolidated balance sheets. As of December 31, 2023, contract liabilities were $49,101 of which $31,178 was reported in contract liabilities, current portion, and $17,923 was reported in other long-term liabilities on the Company’s condensed consolidated balance sheets.

Changes in contract liabilities for the six months ended June 30, 2024 and 2023 were as follows:

| | | | | | | | |

| | 2024 | | | 2023 | |

| | | | | (As Restated) | |

Balance as of January 1 | | $ | 49,101 | | | $ | 34,873 | |

Contract liabilities recorded during the period | | | 22,821 | | | | 19,596 | |

Revenue recognized during the period | | | (29,037 | ) | | | (14,962 | ) |

Other | | | (390 | ) | | | 173 | |

Balance as of June 30 | | $ | 42,495 | | | $ | 39,680 | |

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

Remaining Performance Obligations

The Company has performance obligations associated with commitments in customer contracts for future services that have not yet been recognized as revenue. These commitments for future services exclude (i) contracts with an original term of one year or less, and (ii) cancellable contracts. As of June 30, 2024, the amount not yet recognized as revenue from these commitments was $189,689.

The Company expects to recognize its remaining performance obligations as of June 30, 2024, over the following periods:

| | | | | | | | |

| | June 30, 2024 | |

1 to 12 months | | $ | 62,295 | | | | 33 | % |

13 to 24 months | | | 32,268 | | | | 17 | % |

25 to 36 months | | | 26,028 | | | | 14 | % |

Remaining | | | 69,098 | | | | 36 | % |

Total | | $ | 189,689 | | | | 100 | % |

4.Balance Sheet Components

Other current assets consisted of the following:

| | | | | | | | |

| | June 30, | | | December 31, | |

| | 2024 | | | 2023 | |

Technology and other prepaid contracts | | $ | 3,012 | | | $ | 9,874 | |

Notes receivable | | | 3,344 | | | | 3,344 | |

Other receivables | | | 1,376 | | | | 1,476 | |

Prepaid insurance | | | 424 | | | | 487 | |

Deferred contract costs | | | 515 | | | | 1,238 | |

Other | | | 462 | | | | 429 | |

Other current assets | | $ | 9,133 | | | $ | 16,848 | |

Property and equipment, net consisted of the following:

| | | | | | | | |

| | June 30, | | | December 31, | |

| | 2024 | | | 2023 | |

Satellites in-service | | $ | 45,453 | | | $ | 59,751 | |

Internally developed software | | | 1,760 | | | | 2,138 | |

Ground stations in-service | | | 4,439 | | | | 4,444 | |

Leasehold improvements | | | 5,808 | | | | 5,800 | |

Machinery and equipment | | | 4,705 | | | | 4,787 | |

Computer equipment | | | 1,804 | | | | 1,908 | |

Computer software and website development | | | 99 | | | | 99 | |

Furniture and fixtures | | | 1,324 | | | | 1,336 | |

| | | 65,392 | | | | 80,263 | |

Less: Accumulated depreciation and amortization | | | (31,610 | ) | | | (36,326 | ) |

| | | 33,782 | | | | 43,937 | |

Satellite, launch, and ground station work in progress | | | 23,415 | | | | 16,483 | |

Finished satellites not yet placed in-service | | | 2,826 | | | | 26 | |

Property and equipment, net | | $ | 60,023 | | | $ | 60,446 | |

Depreciation and amortization expense related to property and equipment was $5,447 and $11,404 for the three and six months ended June 30, 2024, respectively. Depreciation and amortization expense related to property and equipment was $3,084 and $6,121 for the three and six months ended June 30, 2023, respectively.

The Company recorded losses of $529 and $707 on decommissioned satellite for the three and six months ended June 30, 2024, respectively. The Company recorded a $472 loss on decommissioned satellite for each of the three and six months ended June 30, 2023.

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

Other accrued expenses consisted of the following:

| | | | | | | | |

| | June 30, | | | December 31, | |

| | 2024 | | | 2023 | |

Operating lease liabilities, current | | $ | 3,423 | | | $ | 3,506 | |

Accrued operating costs | | | 1,145 | | | | 913 | |

Professional services | | | 862 | | | | 1,088 | |

Corporate and sales tax | | | 189 | | | | 285 | |

Accrued interest | | | 912 | | | | 853 | |

Software | | | 973 | | | | 754 | |

Other | | | 1,028 | | | | 927 | |

Other accrued expenses | | $ | 8,532 | | | $ | 8,326 | |

5.Goodwill and Intangible Assets

The following table summarizes changes in goodwill balance:

| | | | |

Balance at December 31, 2023 | | $ | 51,155 | |

Impact of foreign currency translation | | | (1,605 | ) |

Balance at June 30, 2024 | | $ | 49,550 | |

Intangible assets consisted of the following:

| | | | | | | | |

| | June 30, 2024 | |

| | Gross Carrying Amount | | | Accumulated Amortization | |

Customer relationships | | $ | 22,692 | | | $ | (4,883 | ) |

Developed technology | | | 12,896 | | | | (2,776 | ) |

Trade names | | | 2,186 | | | | (1,129 | ) |

Patents | | | 419 | | | | (326 | ) |

FCC licenses | | | 480 | | | | (266 | ) |

| | $ | 38,673 | | | $ | (9,380 | ) |

| | | | | | |

| | December 31, 2023 | |

| | Gross Carrying Amount | | | Accumulated Amortization | |

Customer relationships | | $ | 23,427 | | | $ | (4,064 | ) |

Developed technology | | | 13,313 | | | | (2,312 | ) |

Trade names | | | 2,257 | | | | (940 | ) |

Backlog | | | 3,117 | | | | (3,117 | ) |

Patents | | | 419 | | | | (308 | ) |

FCC licenses | | | 480 | | | | (249 | ) |

| | $ | 43,013 | | | $ | (10,990 | ) |

As of June 30, 2024, the weighted-average amortization period for customer relationships and developed technology was 9.4 years, for trade names was 2.4 years, and for patents and FCC licenses was 5.9 years. Amortization expense related to intangible assets was $868 and $1,748 for the three and six months ended June 30, 2024, respectively, and $885 and $1,762 for the three and six months ended June 30, 2023, respectively.

No impairment charges were recognized for the three and six months ended June 30, 2024 and 2023. The patents asset balance included $32 and $57 of capitalized patent costs that will begin amortization upon the issuance of an official patent right to the Company as of June 30, 2024 and December 31, 2023, respectively.

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

As of June 30, 2024, the expected future amortization expense of intangible assets is as follows:

| | | | |

Fiscal year ending December 31, | | Future Amortization Expense | |

Remainder of 2024 | | $ | 1,733 | |

2025 | | | 3,458 | |

2026 | | | 3,413 | |

2027 | | | 3,004 | |

2028 | | | 3,001 | |

Thereafter | | | 14,652 | |

| | | 29,261 | |

Capitalized patent costs, unissued | | | 32 | |

| | $ | 29,293 | |

Long-term debt consisted of the following:

| | | | | | | | |

| | June 30, | | | December 31, | |

| | 2024 | | | 2023 | |

Blue Torch term loan | | $ | — | | | $ | 117,996 | |

Other | | | 4,854 | | | | 5,128 | |

Total long-term debt | | | 4,854 | | | | 123,124 | |

Less: Debt issuance costs | | | — | | | | (9,011 | ) |

Non-current portion of long-term debt | | $ | 4,854 | | | $ | 114,113 | |

The Company recorded interest expense, including amortization of deferred issuance costs from long-term debt of $4,772 and $9,825 for the three and six months ended June 30, 2024, respectively, and $4,709 and $9,283 for the three and six months ended June 30, 2023, respectively.

As of June 30, 2024, the scheduled principal payments of long-term debt was as follows:

| | | | |

Fiscal year ending December 31, | | Future Principal Payments | |

Remainder of 2024 | | $ | — | |

2025 | | | — | |

2026 | | | 270 | |

2027 | | | 324 | |

2028 | | | 324 | |

Thereafter | | | 3,936 | |

Total debt payments | | $ | 4,854 | |

Blue Torch Credit Agreement

On June 13, 2022, the Company, as borrower, and Spire Global Subsidiary, Inc. and Austin Satellite Design, LLC, as guarantors, entered into a financing agreement (the “Blue Torch Financing Agreement”) with Blue Torch Finance LLC, a Delaware limited liability company (“Blue Torch”), as administrative agent and collateral agent, and certain lenders (the “Lenders”). The Blue Torch Financing Agreement provides for, among other things, a term loan facility in an aggregate principal amount of up to $120,000 (the “Blue Torch Credit Facility”). A portion of the proceeds of the term loan was used to repay the Company’s then-existing $70,000 credit facility with FP Credit Partners, L.P., and the remainder of the proceeds of the term loan may be used for general corporate purposes.

The Blue Torch Credit Facility is scheduled to mature on June 13, 2026. Subject to certain exceptions, prepayments of principal under the Blue Torch Credit Facility will be subject to early termination fees in the amount of 3.0%, 2.0% and 1.0% of the principal prepaid if prepayment occurs within the first, second, and third years following the closing date, respectively, plus if prepayment would have occurred on or prior to the first anniversary of the closing date, a make-whole amount equal to the amount of interest that would have otherwise been payable through the maturity date of the Blue Torch Credit Facility.

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)

The $120,000 term loan was available and drawn at closing, of which $19,735 was placed in an escrow account by Blue Torch with such amount to be released upon the Company achieving certain metrics related to annualized recurring revenue and a total annualized recurring revenue leverage ratio. These metrics were achieved and the $19,735 was released from the escrow account and delivered to the Company in February 2023. The term loan accrues interest at a floating rate, to be based, at the Company's election, on either a reference rate or a 3-month Term Secured Overnight Financing Rate (“SOFR”) (subject to a 1.0% floor), plus an interest rate margin of 7.0% for reference rate borrowings and 8.0% for 3-month Term SOFR borrowings, plus an incremental Term SOFR margin of 0.26161%. The Company elected the Term SOFR rate which was 13.6084% as of June 30, 2024. Principal on the term loan is only payable at maturity and interest on the term loan is due and payable quarterly for Term SOFR borrowings. The Company is also required to pay other customary fees and costs in connection with the Blue Torch Credit Facility, including a commitment fee in an amount equal to $2,400 on the closing date, a $250 annual agency fee and an exit fee of $1,800 upon termination of the Blue Torch Financing Agreement.

The Blue Torch Financing Agreement contains customary affirmative covenants and customary negative covenants limiting the Company's ability and the ability of its subsidiaries to, among other things, dispose of assets, undergo a change in control, merge or consolidate, make acquisitions, incur debt, incur liens, pay dividends, repurchase stock, and make investments, in each case subject to certain exceptions. The Company must also comply with a maximum debt to annualized recurring revenue leverage ratio financial covenant tested monthly during the first two years of the Blue Torch Financing Agreement, a maximum debt to EBITDA leverage ratio financial covenant tested monthly during the third and fourth years of the Blue Torch Financing Agreement and a minimum liquidity financial covenant tested at all times.

On June 13, 2022, in connection with the Blue Torch Financing Agreement, the Company issued warrants to Blue Torch, which were exercisable for an aggregate of 437,024 shares of the Company’s Class A common stock with a per share exercise price of $16.08 (the “2022 Blue Torch Warrants”). In addition, in connection with the closing of the financing, the Company paid Urgent Capital LLC, a Delaware limited liability company, a fee for introducing the Company to the Lenders, for the purpose of loan financing, in the amount equal to $600 in cash and a warrant to purchase 24,834 fully paid and non-assessable shares of the Company's Class A common stock with a per share exercise price of $16.88 (the “Urgent Warrants”).

On September 27, 2023, the Company entered into the Waiver and Amendment No. 2 to Financing Agreement (the “Waiver and Amendment”) with Blue Torch and the Lenders, which amends the Blue Torch Financing Agreement to (a) waive an event of default under the Blue Torch Financing Agreement arising out of the total annualized recurring revenue leverage ratio being greater than the permitted ratio, (b) amend the financial covenants to provide covenant relief from the maximum debt to annualized recurring revenue leverage ratio and the maximum debt to EBITDA leverage ratio set forth in the Blue Torch Financing Agreement for future periods, and (c) provide for a second amendment exit fee. The second amendment exit fee is $1,800 (which is an amount equal to one and a half percent (1.50%) of the aggregate outstanding principal balance of the term loans on the effective date of the Waiver and Amendment), bears interest from the date of the Waiver and Amendment at the Adjusted Term SOFR for a 3-month interest period plus the applicable margin under the Financing Agreement, and is payable by the Company in cash upon the termination of the Blue Torch Financing Agreement, either as a result of acceleration of the loans or at the final maturity date. The Waiver and Amendment required a repayment by the Company of $2,500 of the outstanding principal balance of the term loans and a prepayment premium of $50, which were paid on October 2, 2023. The Waiver and Amendment also requires additional reporting if the Company’s liquidity level is less than $35,000 at any time during a month and revises the minimum liquidity covenant to require liquidity of at least $30,000 at all times, commencing on September 30, 2023, which in both cases represent a $5,000 incremental change from the original requirements.

On September 27, 2023, in connection with the Waiver and Amendment, the Company and certain affiliates of Blue Torch amended and restated the 2022 Blue Torch Warrants to reduce the per share exercise price from $16.08 to $5.44. The Company also concurrently issued new warrants to certain Blue Torch affiliates that are exercisable for an additional 597,082 shares of the Company’s Class A common stock at a per share exercise price of $5.44 (the “2023 Blue Torch Warrants" and together with the 2022 Blue Torch Warrants and the Urgent Warrants, the “Credit Agreement Warrants”).

The Company evaluated the Credit Agreement Warrants and concluded that they do not meet the criteria to be classified within stockholders’ equity. The agreements governing the Credit Agreement Warrants include a provision that could result in a different settlement value for the Credit Agreement Warrants depending on their holder. Because the holder of an instrument is

Spire Global, Inc.

Notes to Condensed Consolidated Financial Statements

(In thousands, except shares and per share data, unless otherwise noted)

(Unaudited)