CERTAIN CONFIDENTIAL PORTIONS OF THIS EXHIBIT HAVE BEEN OMITTED AND REPLACED WITH [ XYZ ] . SUCH IDENTIFIED INFORMATION HAS BEEN EXCLUDED FROM THIS EXHIBIT BECAUSE IT (I) IS NOT MATERIAL AND (II) IS THE TYPE THAT THE REGISTRANT TREATS AS PRIVATE OR CONFIDENTIAL. Exhibit (c)(8)

[ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

PROJECT PACIFIC HOW PRIORITIZED COUNTERPARTIES ARE VALUING PACIFIC AND THEMSELVES $ IN USD MILLIONS. SORTED ALPHABETICALLY. PACIFIC VALUATION COUNTERPARTY PF OWNERSHIP PROPOSED TRANSACTION RETURN OF CASH ASSETS / PRO FORMA TARGET PIPE PARTY STRUCTURE CAPITAL DELIVERED LISTING TECHNOLOGY CVR TOTAL VALUATION STEP-UP CASH RUNWAY (INSIDER COMMITMENT) PACIFIC PARTY PIPE ACTIVE (1) (1) Sign-and-close $100 $40 $10 - None $50 $257 1.00x Until early 2026 $110 (68%) 12.0% 61.6% 26.4% (2) (2) S-4 110 30 15 - None 45 257 1.00x Until early 2026 120 (63%) 10.7% 60.9% 28.4% (3) S-4 - 140 15 - None 155 310 1.00x Through 2027 - 33.3% 66.7% - (4) (5) (3) S-4 60 80 15 - None 95 310 1.00x [Through 2027] - 23.5% 76.5% - PASSED FOLLOWING SPECIAL COMMITTEE FEEDBACK PROVIDED ON 06/07/23 S-4 - $140 - - None $140 402-434 1.50-1.62x Into 2H 2026 - 24.4-25.8% 74.2-75.6% - (6) (5) S-4 $40 100 - - None 100 402-434 1.50-1.62x [Into 2H 2026] - 18.7-19.9% 80.1-81.3% - (1): plans to announce a share buyback upon announcement of the transaction for up to $100M to provide liquidity to PACIFIC stockholders seeking to exit the transaction. (2): revised its proposed share buyback to return up to $110M to PACIFIC stockholders. (3): Ongoing discussions with investors to extend , which would increase post-money for and valuation for proposed transac ion accordingly. would not require a concurrent financing for the transaction. (4): would be open to returning $60M of the $140M available estimated net cash at close to the shareholders of PACIFIC. (5): Pro forma runway per initial indication of interest. The company has since proposed a return of capital mechanism and has not given guidance on how hat may impact the pro forma runway. (6): would consider a scenario that dividends any cash net of $100M from the PACIFIC balance sheet back to PACIFIC shareholders. Note: Green shading denotes revised proposal communicated following further feedback from PACIFIC’s special committee. Blue shading denotes revised proposal communicated following initial feedback from PACIFIC’s special committee. Confidential 2 [ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

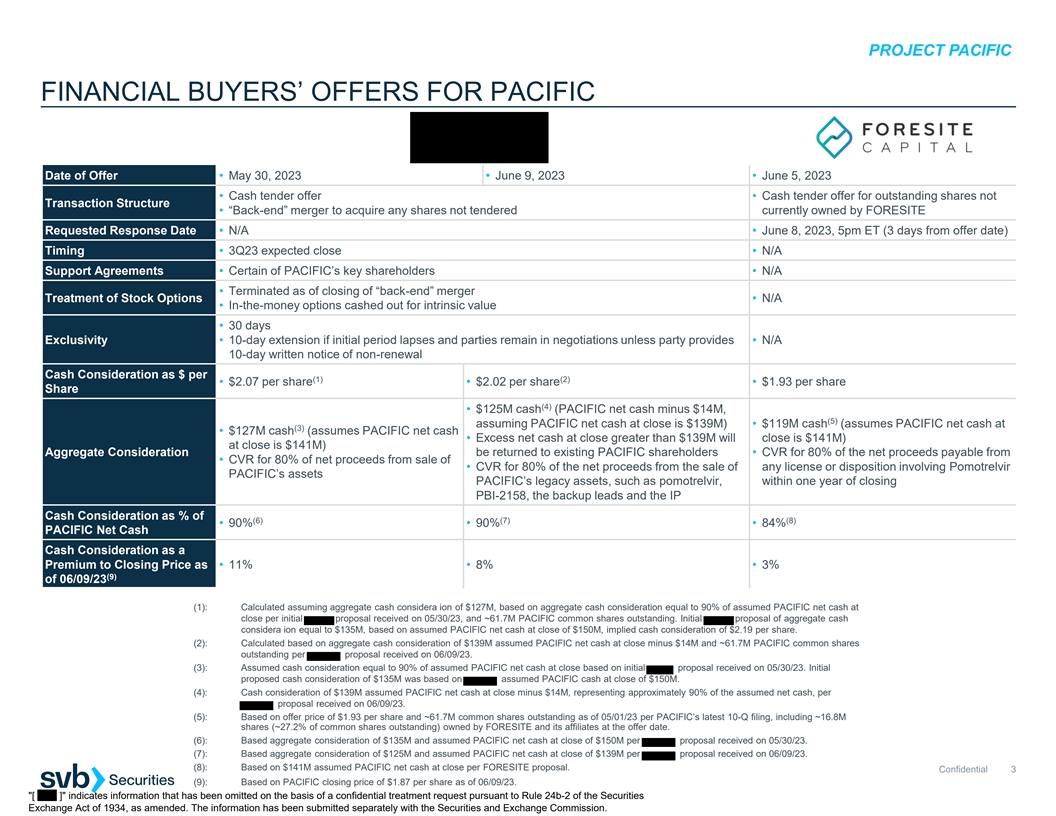

PROJECT PACIFIC FINANCIAL BUYERS’ OFFERS FOR PACIFIC Date of Offer • May 30, 2023 • June 9, 2023 • June 5, 2023 • Cash tender offer • Cash tender offer for outstanding shares not Transaction Structure • “Back-end” merger to acquire any shares not tendered currently owned by FORESITE Requested Response Date • N/A • June 8, 2023, 5pm ET (3 days from offer date) Timing • 3Q23 expected close • N/A Support Agreements • Certain of PACIFIC’s key shareholders • N/A • Terminated as of closing of “back-end” merger Treatment of Stock Options • N/A • In-the-money options cashed out for intrinsic value • 30 days Exclusivity • 10-day extension if initial period lapses and parties remain in negotiations unless party provides • N/A 10-day written notice of non-renewal Cash Consideration as $ per (1) (2) • $2.07 per share • $2.02 per share • $1.93 per share Share (4) • $125M cash (PACIFIC net cash minus $14M, (5) assuming PACIFIC net cash at close is $139M) • $119M cash (assumes PACIFIC net cash at (3) • $127M cash (assumes PACIFIC net cash • Excess net cash at close greater than $139M will close is $141M) at close is $141M) Aggregate Consideration be returned to existing PACIFIC shareholders • CVR for 80% of the net proceeds payable from • CVR for 80% of net proceeds from sale of • CVR for 80% of the net proceeds from the sale of any license or disposition involving Pomotrelvir PACIFIC’s assets PACIFIC’s legacy assets, such as pomotrelvir, within one year of closing PBI-2158, the backup leads and the IP Cash Consideration as % of (6) (7) (8) • 90% • 90% • 84% PACIFIC Net Cash Cash Consideration as a Premium to Closing Price as • 11% • 8% • 3% (9) of 06/09/23 (1): Calculated assuming aggregate cash considera ion of $127M, based on aggregate cash consideration equal to 90% of assumed PACIFIC net cash at close per initial proposal received on 05/30/23, and ~61.7M PACIFIC common shares outstanding. Initial proposal of aggregate cash considera ion equal to $135M, based on assumed PACIFIC net cash at close of $150M, implied cash consideration of $2.19 per share. (2): Calculated based on aggregate cash consideration of $139M assumed PACIFIC net cash at close minus $14M and ~61.7M PACIFIC common shares outstanding per proposal received on 06/09/23. (3): Assumed cash consideration equal to 90% of assumed PACIFIC net cash at close based on initial proposal received on 05/30/23. Initial proposed cash consideration of $135M was based on assumed PACIFIC cash at close of $150M. (4): Cash consideration of $139M assumed PACIFIC net cash at close minus $14M, representing approximately 90% of the assumed net cash, per proposal received on 06/09/23. (5): Based on offer price of $1.93 per share and ~61.7M common shares outstanding as of 05/01/23 per PACIFIC’s latest 10-Q filing, including ~16.8M shares (~27.2% of common shares outstanding) owned by FORESITE and its affiliates at the offer date. (6): Based aggregate consideration of $135M and assumed PACIFIC net cash at close of $150M per proposal received on 05/30/23. (7): Based aggregate consideration of $125M and assumed PACIFIC net cash at close of $139M per proposal received on 06/09/23. (8): Based on $141M assumed PACIFIC net cash at close per FORESITE proposal. Confidential 3 (9): Based on PACIFIC closing price of $1.87 per share as of 06/09/23. [ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

PROJECT PACIFIC DISCOUNTS TO NET CASH IMPLIED BY RECENT FINANCIAL BUYERS’ PROPOSALS ($ in millions, except per share values) Terms of Proposal Cash Consideration Non-Contingent Offer Target As a % of Premium to Ann. Financial Cash per Equity Total per Aggregate Contingent Net Cash Net Cash Unaffected Offer (1) Date Company Buyer Share per Share Share Value Value Rights at Close at Close Price Accepted 80% of the net proceeds payable from any (2) 05/30/23 $8.00 - $8.00 $53 license or disposition of the MEI's clinical $76 70% 11% O assets 80% of the net proceeds payable from any 05/22/23 5.75 - 5.75 480 570 84% 55% O license or disposition of Atea’s programs Echo Lake (3) 03/21/23 1.60 - 1.60 58 None 87 67% 90% O Capital 80% of the net proceeds for ten years post- closing from any license or disposition of (4) 03/14/23 1.85 - 1.85 96 Jounce’s programs effected within two years 115 85% 75% P of closing and 100% of the potential aggregate value of certain potential cost savings Mean: 76% 58% Median: 77% 65% 25th Percentile: 69% 44% 75th Percentile: 84% 78% (1): Estimated net cash at close per offer filing unless otherwise noted. (2): Expected net cash of ~$93M at 06/30/23 per the S-4 filing, net of ~$17M of total minimum operating lease payments (carrying value of $13M due to present value discounting) as of 03/31/23. (3): $90M cash and cash equivalents net of $3M total liabilities as of 03/31/23. (4): Represents final offer accepted on 03/27/23, increased from the 03/14/23 offer of $1.80 per share + CVR. Note: Includes unsolicited offers from financial buyers for biopharma companies trading below net cash. Excludes unsolicited offers for companies which total liabilities exceeded cash and cash equivalents at he time of the offer. Source: Company press releases and filings. Confidential 4

APPENDIX

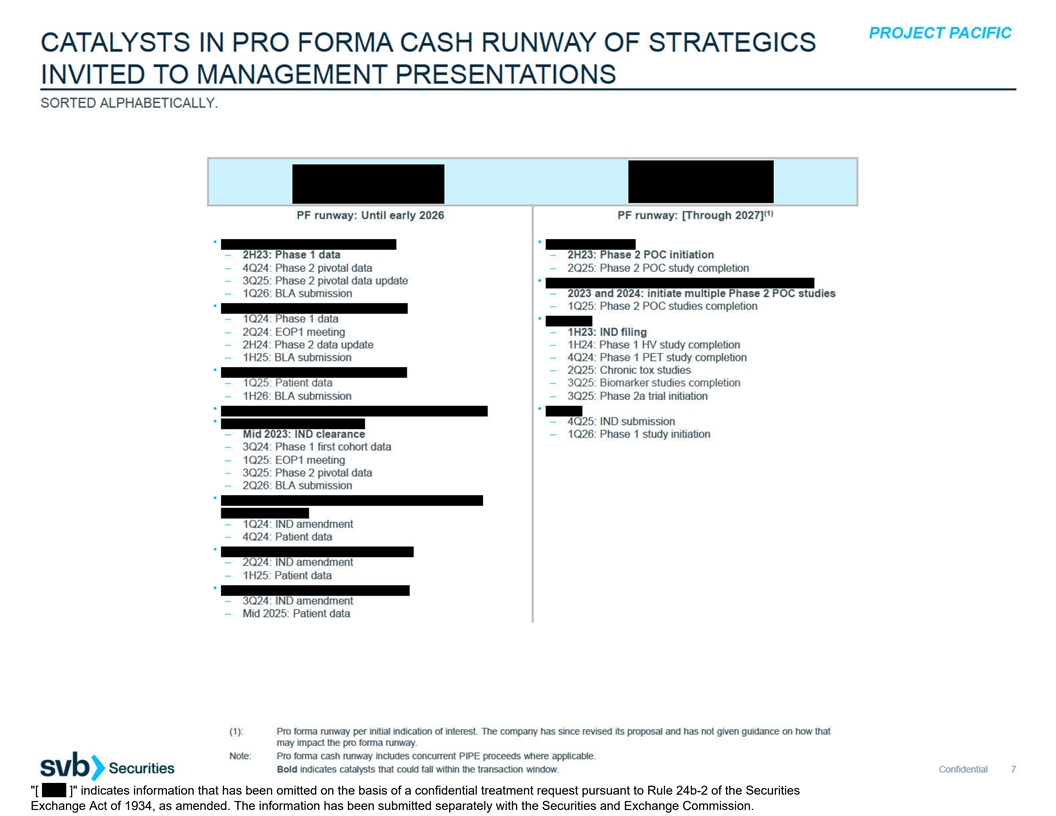

A. CATALYSTS IN PRO FORMA CASH RUNWAY OF STRATEGICS THAT HAVE SUBMITTED INDICATIONS OF INTEREST

[ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

[ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

[ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

B. INITIAL INDICATIONS OF INTEREST FROM STRATEGICS INVITED TO MANAGEMENT PRESENTATIONS

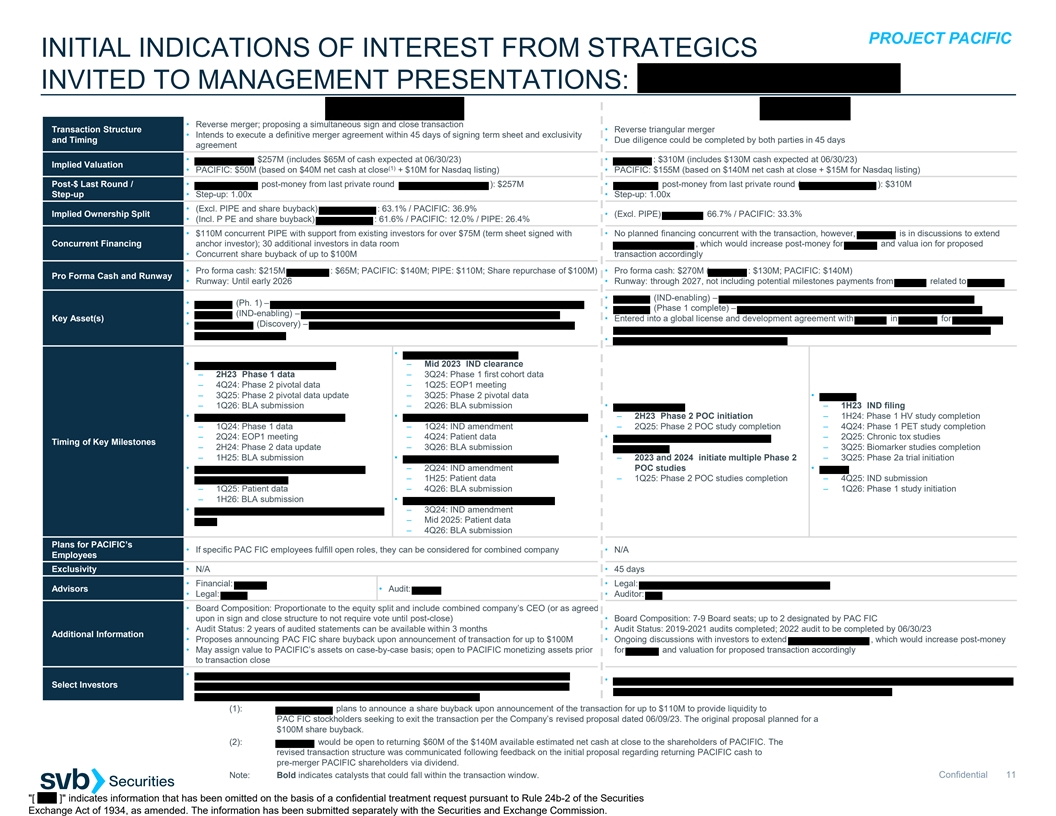

PROJECT PACIFIC INITIAL INDICATIONS OF INTEREST FROM STRATEGICS INVITED TO MANAGEMENT PRESENTATIONS: • Reverse merger; proposing a simultaneous sign and close transaction Transaction Structure • Reverse triangular merger • Intends to execute a definitive merger agreement within 45 days of signing term sheet and exclusivity and Timing • Due diligence could be completed by both parties in 45 days agreement • $257M (includes $65M of cash expected at 06/30/23) • : $310M (includes $130M cash expected at 06/30/23) Implied Valuation (1) • PACIFIC: $50M (based on $40M net cash at close + $10M for Nasdaq listing) • PACIFIC: $155M (based on $140M net cash at close + $15M for Nasdaq listing) Post-$ Last Round / • post-money from last private round ): $257M • post-money from last private round ( ): $310M Step-up • Step-up: 1.00x • Step-up: 1.00x • (Excl. PIPE and share buyback) : 63.1% / PACIFIC: 36.9% Implied Ownership Split • (Excl. PIPE) 66.7% / PACIFIC: 33.3% • (Incl. P PE and share buyback) : 61.6% / PACIFIC: 12.0% / PIPE: 26.4% • $110M concurrent PIPE with support from existing investors for over $75M (term sheet signed with • No planned financing concurrent with the transaction, however, is in discussions to extend Concurrent Financing anchor investor); 30 additional investors in data room , which would increase post-money for and valua ion for proposed • Concurrent share buyback of up to $100M transaction accordingly • Pro forma cash: $215M : $65M; PACIFIC: $140M; PIPE: $110M; Share repurchase of $100M) • Pro forma cash: $270M ( : $130M; PACIFIC: $140M) Pro Forma Cash and Runway • Runway: Until early 2026 • Runway: through 2027, not including potential milestones payments from related to • (IND-enabling) – • (Ph. 1) – • (Phase 1 complete) – • (IND-enabling) – Key Asset(s) • Entered into a global license and development agreement with in for • (Discovery) – • • • – Mid 2023 IND clearance – 2H23 Phase 1 data – 3Q24: Phase 1 first cohort data – 4Q24: Phase 2 pivotal data – 1Q25: EOP1 meeting – 3Q25: Phase 2 pivotal data update – 3Q25: Phase 2 pivotal data • – 1Q26: BLA submission – 2Q26: BLA submission • – 1H23 IND filing • • – 2H23 Phase 2 POC initiation – 1H24: Phase 1 HV study completion – 1Q24: Phase 1 data – 1Q24: IND amendment – 2Q25: Phase 2 POC study completion – 4Q24: Phase 1 PET study completion – 2Q24: EOP1 meeting – 4Q24: Patient data • – 2Q25: Chronic tox studies Timing of Key Milestones – 2H24: Phase 2 data update – 3Q26: BLA submission – 3Q25: Biomarker studies completion – 1H25: BLA submission • – 2023 and 2024 initiate multiple Phase 2 – 3Q25: Phase 2a trial initiation • – 2Q24: IND amendment POC studies • – 1H25: Patient data – 1Q25: Phase 2 POC studies completion – 4Q25: IND submission – 1Q25: Patient data – 4Q26: BLA submission – 1Q26: Phase 1 study initiation – 1H26: BLA submission • • – 3Q24: IND amendment – Mid 2025: Patient data – 4Q26: BLA submission Plans for PACIFIC’s • If specific PAC FIC employees fulfill open roles, they can be considered for combined company • N/A Employees Exclusivity • N/A • 45 days • Financial: • Legal: Advisors • Audit: • Legal: • Auditor: • Board Composition: Proportionate to the equity split and include combined company’s CEO (or as agreed upon in sign and close structure to not require vote until post-close) • Board Composition: 7-9 Board seats; up to 2 designated by PAC FIC • Audit Status: 2 years of audited statements can be available within 3 months • Audit Status: 2019-2021 audits completed; 2022 audit to be completed by 06/30/23 Additional Information • Proposes announcing PAC FIC share buyback upon announcement of transaction for up to $100M • Ongoing discussions with investors to extend , which would increase post-money • May assign value to PACIFIC’s assets on case-by-case basis; open to PACIFIC monetizing assets prior for and valuation for proposed transaction accordingly to transaction close • • Select Investors (1): plans to announce a share buyback upon announcement of the transaction for up to $110M to provide liquidity to PAC FIC stockholders seeking to exit the transaction per the Company’s revised proposal dated 06/09/23. The original proposal planned for a $100M share buyback. (2): would be open to returning $60M of the $140M available estimated net cash at close to the shareholders of PACIFIC. The revised transaction structure was communicated following feedback on the initial proposal regarding returning PACIFIC cash to pre-merger PACIFIC shareholders via dividend. Note: Bold indicates catalysts that could fall within the transaction window. Confidential 11 [ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

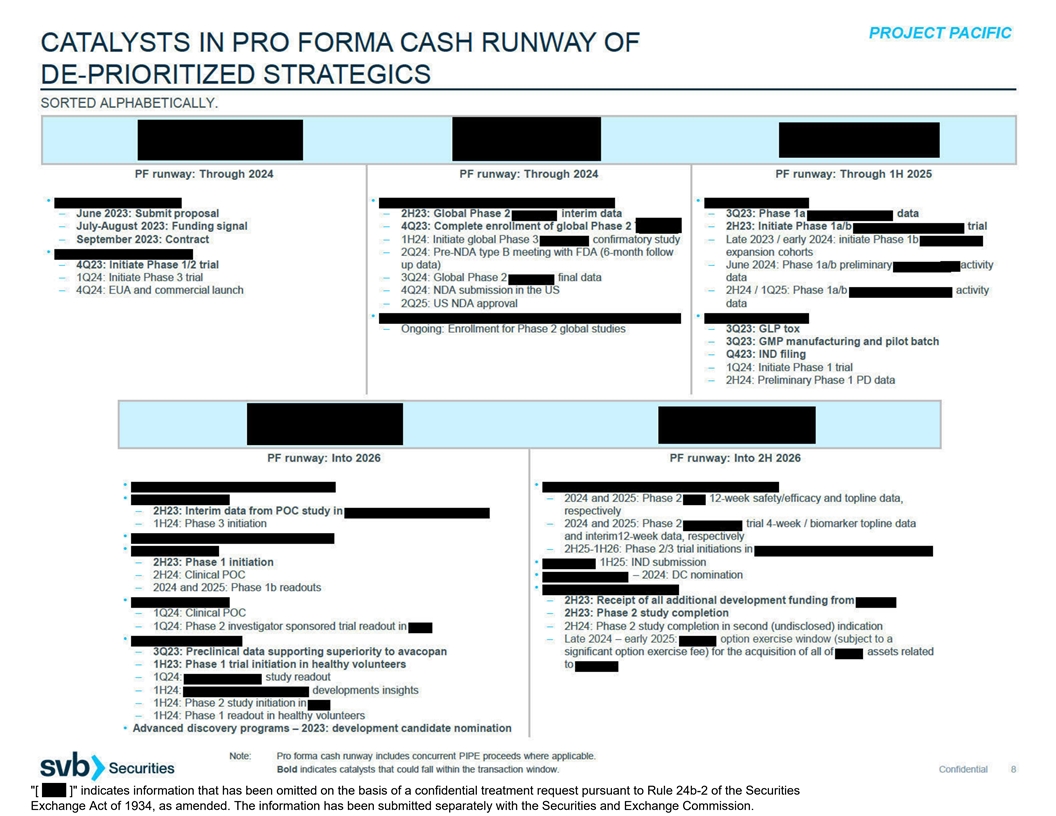

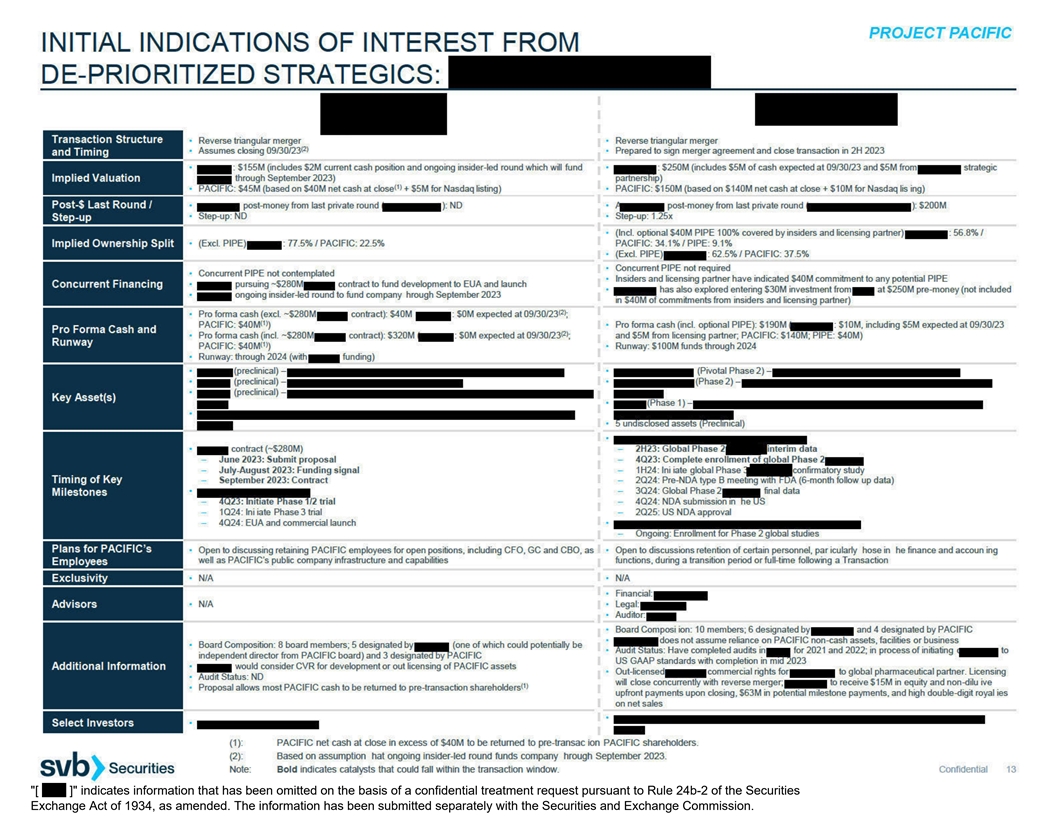

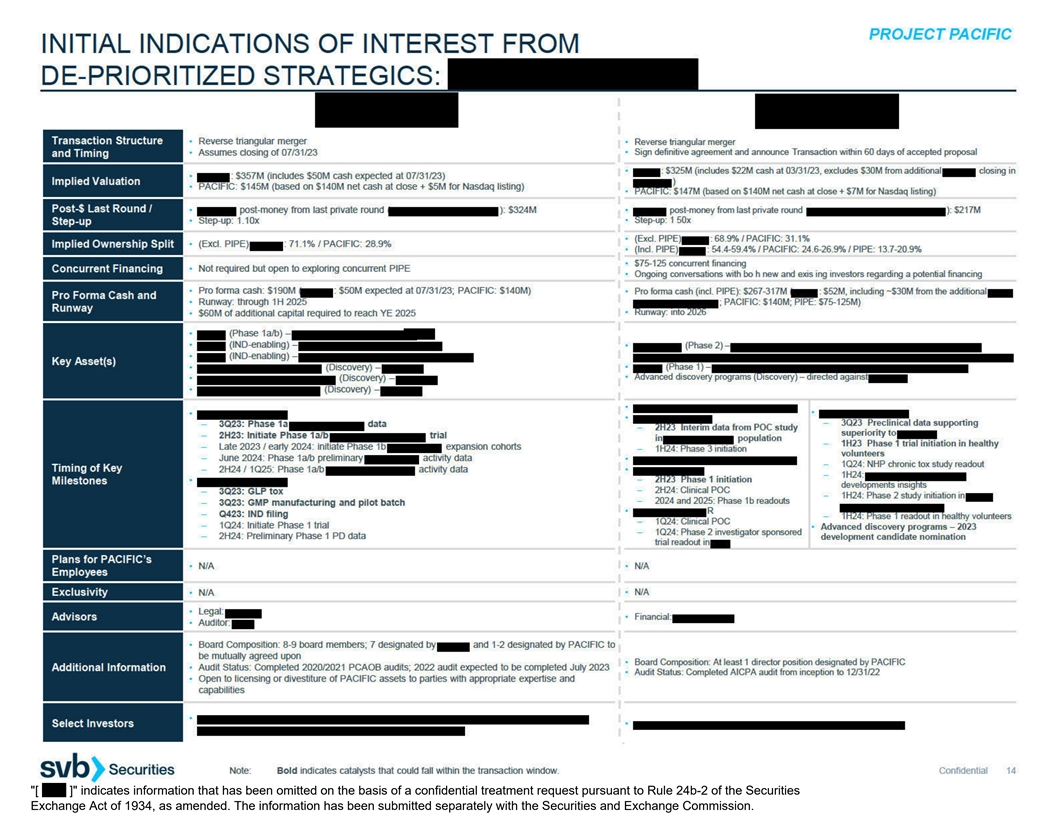

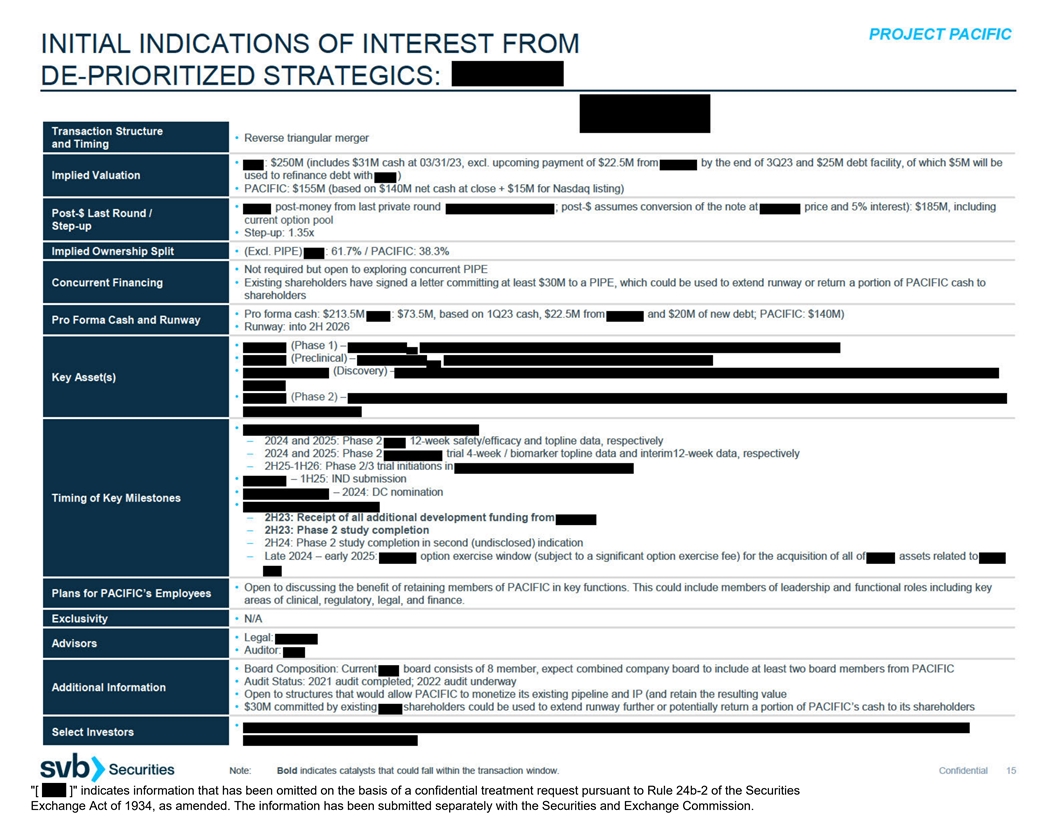

C. INITIAL INDICATIONS OF INTEREST FROM DE-PRIORITIZED STRATEGICS

[ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

[ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

[ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

D. INITIAL INDICATION OF INTEREST FROM STRATEGIC WHO HAS PASSED

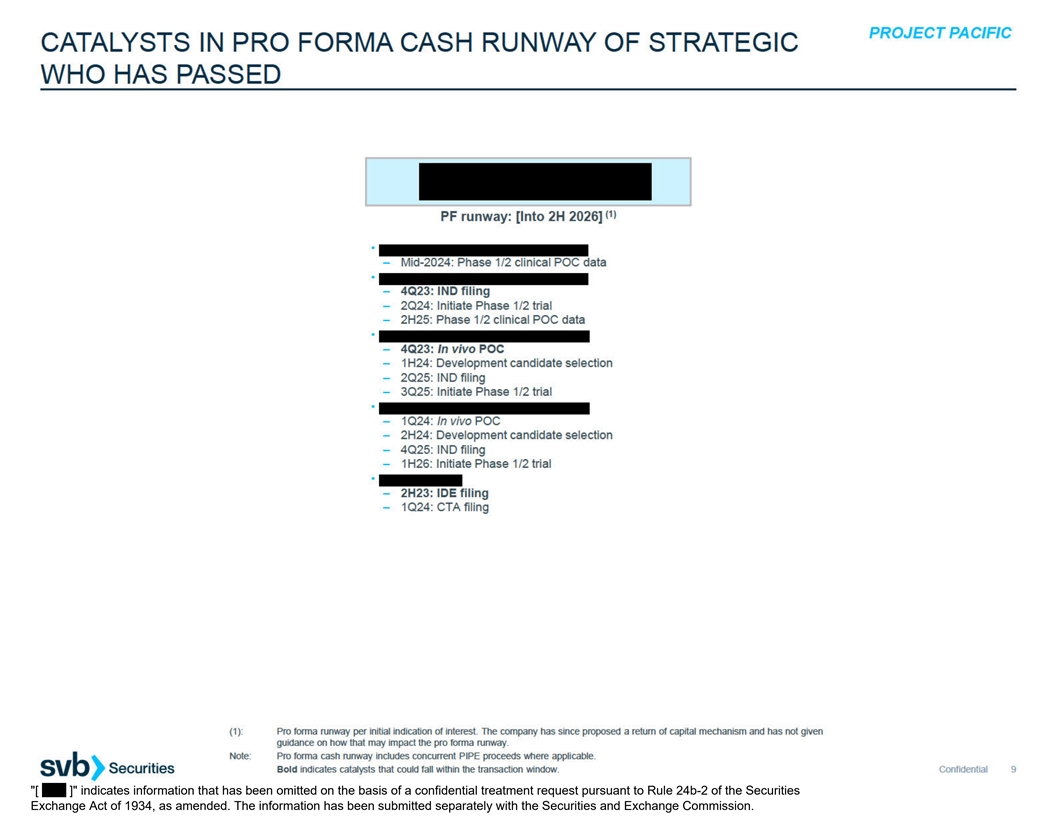

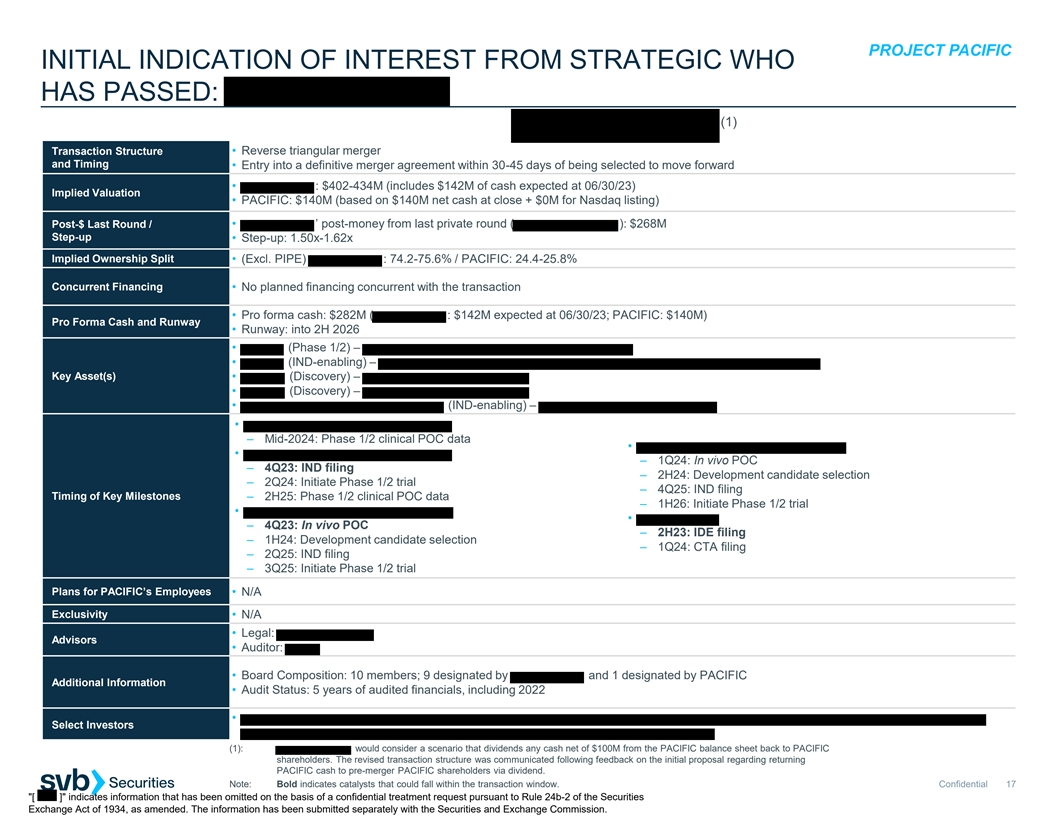

PROJECT PACIFIC INITIAL INDICATION OF INTEREST FROM STRATEGIC WHO HAS PASSED: (1) Transaction Structure • Reverse triangular merger and Timing • Entry into a definitive merger agreement within 30-45 days of being selected to move forward • : $402-434M (includes $142M of cash expected at 06/30/23) Implied Valuation • PACIFIC: $140M (based on $140M net cash at close + $0M for Nasdaq listing) Post-$ Last Round / • ’ post-money from last private round ( ): $268M Step-up • Step-up: 1.50x-1.62x Implied Ownership Split • (Excl. PIPE) : 74.2-75.6% / PACIFIC: 24.4-25.8% Concurrent Financing • No planned financing concurrent with the transaction • Pro forma cash: $282M ( : $142M expected at 06/30/23; PACIFIC: $140M) Pro Forma Cash and Runway • Runway: into 2H 2026 • (Phase 1/2) – • (IND-enabling) – Key Asset(s) • (Discovery) – • (Discovery) – • (IND-enabling) – • – Mid-2024: Phase 1/2 clinical POC data • • – 1Q24: In vivo POC – 4Q23: IND filing – 2H24: Development candidate selection – 2Q24: Initiate Phase 1/2 trial – 4Q25: IND filing Timing of Key Milestones – 2H25: Phase 1/2 clinical POC data – 1H26: Initiate Phase 1/2 trial • • – 4Q23: In vivo POC – 2H23: IDE filing – 1H24: Development candidate selection – 1Q24: CTA filing – 2Q25: IND filing – 3Q25: Initiate Phase 1/2 trial Plans for PACIFIC’s Employees • N/A Exclusivity • N/A • Legal: Advisors • Auditor: • Board Composition: 10 members; 9 designated by and 1 designated by PACIFIC Additional Information • Audit Status: 5 years of audited financials, including 2022 • Select Investors (1): would consider a scenario that dividends any cash net of $100M from the PACIFIC balance sheet back to PACIFIC shareholders. The revised transaction structure was communicated following feedback on the initial proposal regarding returning PACIFIC cash to pre-merger PACIFIC shareholders via dividend. Note: Bold indicates catalysts that could fall within the transaction window. Confidential 17 [ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Securities Exchange Act of 1934, as amended. The information has been submitted separately with the Securities and Exchange Commission.

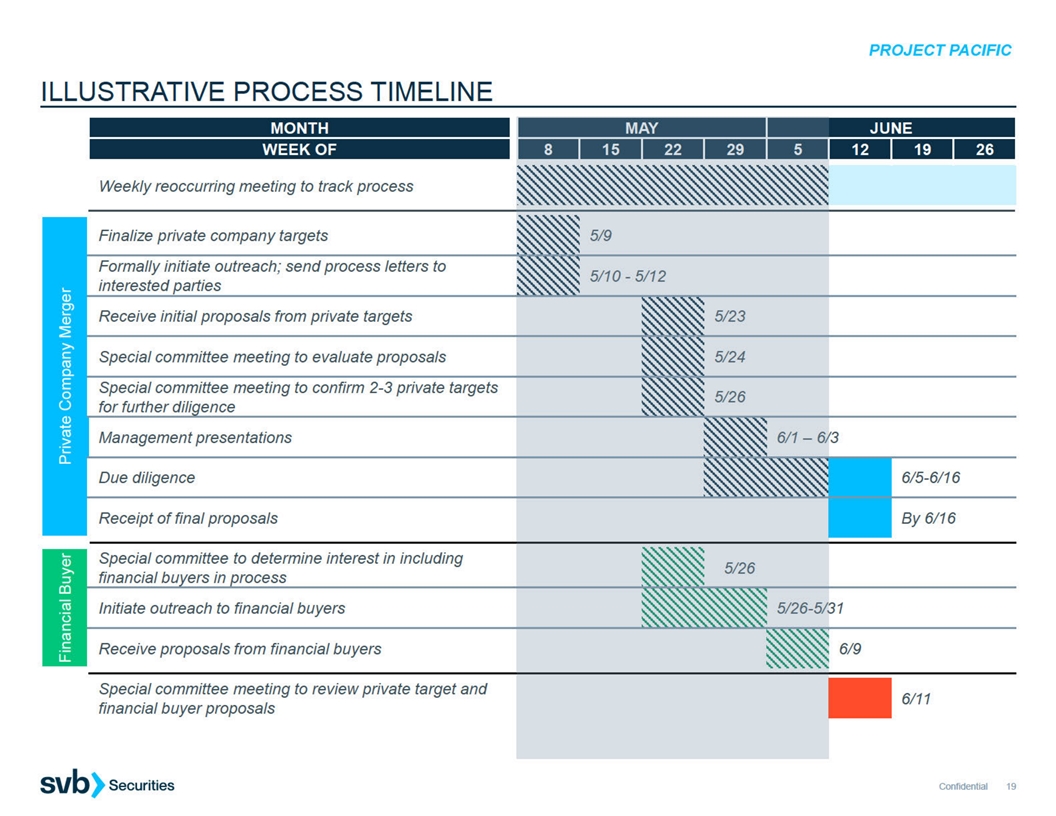

E. ILLUSTRATIVE PROCESS TIMELINE