EXHIBIT 13

APPENDIX

CATERPILLAR INC.

GENERAL AND FINANCIAL INFORMATION

2003

A-1

TABLE OF CONTENTS

A-2

REPORT OF MANAGEMENT

Caterpillar Inc.

The management of Caterpillar Inc. has prepared the accompanying financial statements for the years ended December 31, 2003, 2002 and 2001, and is responsible for their integrity and objectivity. The statements were prepared in conformity with generally accepted accounting principles, applying certain estimates and judgments as required.

Management maintains a system of internal accounting controls which has been designed to provide reasonable assurance that: transactions are executed in accordance with proper authorization, transactions are properly recorded and summarized to produce reliable financial records and reports, assets are safeguarded and the accountability for assets is maintained.

The system of internal controls includes statements of policies and business practices, widely communicated to employees, which are designed to require them to maintain high ethical standards in their conduct of company affairs. The internal controls are augmented by careful selection and training of supervisory and other management personnel, by organizational arrangements that provide for appropriate delegation of authority and division of responsibility and by an extensive program of internal audit with management follow-up. The company's adoption of 6 Sigma has improved processes leading to enhanced internal controls.

The financial statements have been audited by PricewaterhouseCoopers LLP, independent auditors, in accordance with auditing standards generally accepted in the United States of America. They have made similar annual audits since the initial incorporation of our company. Their role is to render an opinion on management's financial statements. Their report appears below.

Through its Audit Committee, the board of directors reviews our financial and accounting policies, practices and reports. The Audit Committee consists exclusively of six directors who are not salaried employees and who are, in the opinion of the board of directors, free from any relationship that would interfere with the exercise of independent judgment as a committee member. The Audit Committee meets several times each year with representatives of management, including the internal auditing department and the independent auditors to review the activities of each and satisfy itself that each is properly discharging its responsibilities. Both the independent auditors and the internal auditors have free access to the Audit Committee and meet with it periodically, with and without management representatives in attendance, to discuss, among other things, their opinions as to the adequacy of internal controls and to review the quality of financial reporting.

| ||

| Chairman of the Board | ||

| ||

| Chief Financial Officer | ||

January 27, 2004 |

REPORT OF INDEPENDENT AUDITORS

![]()

TO THE BOARD OF DIRECTORS AND STOCKHOLDERS OF CATERPILLAR INC.:

In our opinion, the accompanying statements of consolidated financial position and the related statements of consolidated results of operations, changes in consolidated stockholders' equity and consolidated cash flow present fairly, in all material respects, the financial position of Caterpillar Inc. and its subsidiaries at December 31, 2003, 2002 and 2001, and the results of their operations and their cash flow for each of the three years in the period ended December 31, 2003 in conformity with accounting principles generally accepted in the United States of America. These financial statements are the responsibility of the Company's management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these statements in accordance with auditing standards generally accepted in the United States of America, which require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

As discussed in Note 9 to the consolidated financial statements, effective January 1, 2002 the Company changed the manner in which it accounts for goodwill and other intangible assets upon the adoption of Statement of Financial Accounting Standards No. 142 "Goodwill and Other Intangible Assets."

![]()

Peoria, Illinois

January 27, 2004

A-3

STATEMENT 1

Consolidated Results of Operations for the Years Ended December 31

(Dollars in millions except per share data)

| | 2003 | 2002 | 2001 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales and revenues: | |||||||||||

| Sales of Machinery and Engines | $ | 21,048 | $ | 18,648 | $ | 19,027 | |||||

| Revenues of Financial Products | 1,715 | 1,504 | 1,423 | ||||||||

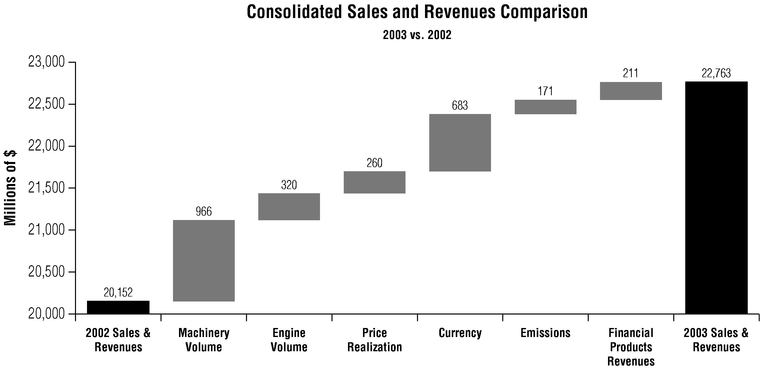

| Total sales and revenues | 22,763 | 20,152 | 20,450 | ||||||||

| Operating costs: | |||||||||||

| Cost of goods sold | 16,945 | 15,146 | 15,179 | ||||||||

| Selling, general and administrative expenses | 2,470 | 2,094 | 2,140 | ||||||||

| Research and development expenses | 669 | 656 | 696 | ||||||||

| Interest expense of Financial Products | 470 | 521 | 657 | ||||||||

| Other operating expenses | 521 | 411 | 467 | ||||||||

| Total operating costs | 21,075 | 18,828 | 19,139 | ||||||||

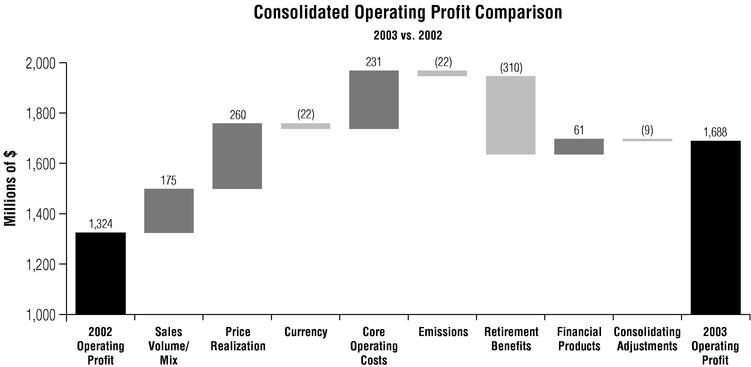

| Operating profit | 1,688 | 1,324 | 1,311 | ||||||||

| Interest expense excluding Financial Products | 246 | 279 | 285 | ||||||||

| Other income (expense) | 35 | 69 | 143 | ||||||||

| Consolidated profit before taxes | 1,477 | 1,114 | 1,169 | ||||||||

| Provision for income taxes | 398 | 312 | 367 | ||||||||

| Profit of consolidated companies | 1,079 | 802 | 802 | ||||||||

| Equity in profit (loss) of unconsolidated affiliated companies | 20 | (4 | ) | 3 | |||||||

| Profit | $ | 1,099 | $ | 798 | $ | 805 | |||||

| Profit per common share | $ | 3.18 | $ | 2.32 | $ | 2.35 | |||||

| Profit per common share—diluted(1) | $ | 3.13 | $ | 2.30 | $ | 2.32 | |||||

| Weighted-average common shares (millions) | 345.2 | 344.0 | 343.3 | ||||||||

| Weighted-average common shares—diluted (millions)(1) | 351.4 | 346.9 | 347.1 | ||||||||

| Cash dividends declared per common share | $ | 1.420 | $ | 1.400 | $ | 1.390 | |||||

- (1)

- Diluted by assumed exercise of stock options, using the treasury stock method.

See accompanying Notes to Consolidated Financial Statements.

A-4

STATEMENT 2

Changes in Consolidated Stockholders' Equity for the Years Ended December 31

(Dollars in millions)

| | 2003 | 2002 | 2001 | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Common stock: | |||||||||||||||||||||

| Balance at beginning of year | $ | 1,034 | $ | 1,043 | $ | 1,048 | |||||||||||||||

| Shares issued from treasury stock | 25 | (9 | ) | (5 | ) | ||||||||||||||||

| Balance at year-end | 1,059 | 1,034 | 1,043 | ||||||||||||||||||

| Treasury stock: | |||||||||||||||||||||

| Balance at beginning of year | $ | (2,669 | ) | $ | (2,696 | ) | $ | (2,676 | ) | ||||||||||||

| Shares issued: 2003—4,956,973; 2002—878,623; 2001—916,634 | 160 | 27 | 23 | ||||||||||||||||||

| Treasury shares purchased: 2003—5,450,000; 2001—937,000 | (405 | ) | — | (43 | ) | ||||||||||||||||

| Balance at year-end | (2,914 | ) | (2,669 | ) | (2,696 | ) | |||||||||||||||

| Profit employed in the business: | |||||||||||||||||||||

| Balance at beginning of year | 7,849 | 7,533 | 7,205 | ||||||||||||||||||

| Profit | 1,099 | $ | 1,099 | 798 | $ | 798 | 805 | $ | 805 | ||||||||||||

| Dividends declared | (498 | ) | (482 | ) | (477 | ) | |||||||||||||||

| Balance at year-end | 8,450 | 7,849 | 7,533 | ||||||||||||||||||

| Accumulated other comprehensive income: | |||||||||||||||||||||

| Foreign currency translation adjustment: | |||||||||||||||||||||

| Balance at beginning of year | 86 | (17 | ) | 55 | |||||||||||||||||

| Aggregate adjustment for year | 262 | 262 | 103 | 103 | (72 | ) | (72 | ) | |||||||||||||

| Balance at year-end | 348 | 86 | (17 | ) | |||||||||||||||||

| Minimum pension liability adjustment—consolidated companies: | |||||||||||||||||||||

| Balance at beginning of year (net of tax of: 2003—$383; 2002—$82; 2001—$1) | (771 | ) | (161 | ) | (1 | ) | |||||||||||||||

| Aggregate adjustment for year (net of tax of: 2003—$77; 2002—$301; 2001—$81) | (163 | ) | (163 | ) | (610 | ) | (610 | ) | (160 | ) | (160 | ) | |||||||||

| Balance at year-end (net of tax of: 2003—$460; 2002—$383; 2001—$82) | (934 | ) | (771 | ) | (161 | ) | |||||||||||||||

| Minimum pension liability adjustment—unconsolidated affiliates: | |||||||||||||||||||||

| Balance at beginning of year | (37 | ) | (41 | ) | (31 | ) | |||||||||||||||

| Aggregate adjustment for year | (11 | ) | (11 | ) | 4 | 4 | (10 | ) | (10 | ) | |||||||||||

| Balance at year-end | (48 | ) | (37 | ) | (41 | ) | |||||||||||||||

| Derivative financial instruments: | |||||||||||||||||||||

| Balance at beginning of year (net of tax of: 2003—$5; 2002—$17) | 11 | (26 | ) | — | |||||||||||||||||

| Gains/(losses) deferred during year (net of tax of: 2003—$29; 2002—$10; 2001—$24) | 53 | 53 | 15 | 15 | (39 | ) | (39 | ) | |||||||||||||

| (Gains)/losses reclassified to earnings during year (net of tax of: 2003—$20; 2002—$11; 2001—$7) | 40 | 40 | 22 | 22 | 13 | 13 | |||||||||||||||

| Balance at year-end (net of tax of: 2003—$54; 2002—$4; 2001—$17) | 104 | 11 | (26 | ) | |||||||||||||||||

| Available-for-sale securities: | |||||||||||||||||||||

| Balance at beginning of year (net of tax of: 2003—$17; 2002—$13) | (31 | ) | (24 | ) | — | ||||||||||||||||

| Gains/(losses) deferred during year (net of tax of: 2003—$12; 2002—$16; 2001—$14) | 23 | 23 | (29 | ) | (29 | ) | (26 | ) | (26 | ) | |||||||||||

| (Gains)/losses reclassified to earnings during year (net of tax of: 2003—$11; 2002—$12; 2001—$1) | 21 | 21 | 22 | 22 | 2 | 2 | |||||||||||||||

| Balance at year-end (net of tax of: 2003—$7; 2002—$17; 2001—$13) | 13 | (31 | ) | (24 | ) | ||||||||||||||||

| Total accumulated other comprehensive income | (517 | ) | (742 | ) | (269 | ) | |||||||||||||||

| Comprehensive income | $ | 1,324 | $ | 325 | $ | 513 | |||||||||||||||

| Stockholders' equity at year-end | $ | 6,078 | $ | 5,472 | $ | 5,611 | |||||||||||||||

See accompanying Notes to Consolidated Financial Statements.

A-5

STATEMENT 3

Consolidated Financial Position at December 31

(Dollars in millions)

| | 2003 | 2002 | 2001 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Assets | |||||||||||||

| Current assets: | |||||||||||||

| Cash and short-term investments | $ | 342 | $ | 309 | $ | 400 | |||||||

| Receivables—trade and other | 3,666 | 2,838 | 2,592 | ||||||||||

| Receivables—finance | 7,605 | 6,748 | 5,849 | ||||||||||

| Deferred and refundable income taxes | 707 | 781 | 434 | ||||||||||

| Prepaid expenses | 1,424 | 1,224 | 1,139 | ||||||||||

| Inventories | 3,047 | 2,763 | 2,925 | ||||||||||

| Total current assets | 16,791 | 14,663 | 13,339 | ||||||||||

| Property, plant and equipment—net | 7,290 | 7,046 | 6,603 | ||||||||||

| Long-term receivables—trade and other | 82 | 66 | 55 | ||||||||||

| Long-term receivables—finance | 7,822 | 6,714 | 6,267 | ||||||||||

| Investments in unconsolidated affiliated companies | 800 | 747 | 787 | ||||||||||

| Deferred income taxes | 616 | 711 | 927 | ||||||||||

| Intangible assets | 239 | 281 | 274 | ||||||||||

| Goodwill | 1,398 | 1,402 | 1,397 | ||||||||||

| Other assets | 1,427 | 1,117 | 936 | ||||||||||

| Total assets | $ | 36,465 | $ | 32,747 | $ | 30,585 | |||||||

| Liabilities | |||||||||||||

| Current liabilities: | |||||||||||||

| Short-term borrowings: | |||||||||||||

| —Machinery and Engines | $ | 72 | $ | 64 | $ | 219 | |||||||

| —Financial Products | 2,685 | 2,111 | 1,961 | ||||||||||

| Accounts payable | 3,100 | 2,269 | 2,123 | ||||||||||

| Accrued expenses | 1,638 | 1,620 | 1,419 | ||||||||||

| Accrued wages, salaries and employee benefits | 1,802 | 1,779 | 1,403 | ||||||||||

| Dividends payable | 127 | 120 | 120 | ||||||||||

| Deferred and current income taxes payable | 216 | 70 | 11 | ||||||||||

| Long-term debt due within one year: | |||||||||||||

| —Machinery and Engines | 32 | 258 | 73 | ||||||||||

| —Financial Products | 2,949 | 3,654 | 3,058 | ||||||||||

| Total current liabilities | 12,621 | 11,945 | 10,387 | ||||||||||

| Long-term debt due after one year: | |||||||||||||

| —Machinery and Engines | 3,367 | 3,403 | 3,492 | ||||||||||

| —Financial Products | 10,711 | 8,193 | 7,799 | ||||||||||

| Liability for postemployment benefits | 3,172 | 3,333 | 2,920 | ||||||||||

| Deferred income taxes and other liabilities | 516 | 401 | 376 | ||||||||||

| Total liabilities | 30,387 | 27,275 | 24,974 | ||||||||||

| Contingencies (Note 21) | |||||||||||||

| Stockholders' equity | |||||||||||||

| Common stock of $1.00 par value: | |||||||||||||

| Authorized shares: 900,000,000 Issued shares (2003, 2002 and 2001—407,447,312) at paid-in amount | 1,059 | 1,034 | 1,043 | ||||||||||

| Treasury stock (2003—63,685,272 shares; 2002—63,192,245 shares; and 2001—64,070,868 shares) at cost | (2,914 | ) | (2,669 | ) | (2,696 | ) | |||||||

| Profit employed in the business | 8,450 | 7,849 | 7,533 | ||||||||||

| Accumulated other comprehensive income | (517 | ) | (742 | ) | (269 | ) | |||||||

| Total stockholders' equity | 6,078 | 5,472 | 5,611 | ||||||||||

| Total liabilities and stockholders' equity | $ | 36,465 | $ | 32,747 | $ | 30,585 | |||||||

See accompanying Notes to Consolidated Financial Statements.

A-6

STATEMENT 4

Consolidated Statement of Cash Flow for the Years Ended December 31

(Millions of dollars)

| | 2003 | 2002 | 2001 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Cash flow from operating activities: | ||||||||||||

| Profit | $ | 1,099 | $ | 798 | $ | 805 | ||||||

| Adjustments for non-cash items: | ||||||||||||

| Depreciation and amortization | 1,347 | 1,220 | 1,169 | |||||||||

| Other charges | — | — | 153 | |||||||||

| Other | (15 | ) | 363 | 245 | ||||||||

| Changes in assets and liabilities: | ||||||||||||

| Receivables—trade and other | (521 | ) | (50 | ) | 99 | |||||||

| Inventories | (286 | ) | 162 | (211 | ) | |||||||

| Accounts payable and accrued expenses | 617 | 164 | (160 | ) | ||||||||

| Other—net | (175 | ) | (291 | ) | (113 | ) | ||||||

| Net cash provided by operating activities | 2,066 | 2,366 | 1,987 | |||||||||

| Cash flow from investing activities: | ||||||||||||

| Capital expenditures—excluding equipment leased to others | (682 | ) | (728 | ) | (1,100 | ) | ||||||

| Expenditures for equipment leased to others | (1,083 | ) | (1,045 | ) | (868 | ) | ||||||

| Proceeds from disposals of property, plant and equipment | 761 | 561 | 356 | |||||||||

| Additions to finance receivables | (17,146 | ) | (15,338 | ) | (16,284 | ) | ||||||

| Collections of finance receivables | 13,882 | 11,866 | 12,367 | |||||||||

| Proceeds from sale of finance receivables | 1,760 | 2,310 | 3,079 | |||||||||

| Investments and acquisitions | (36 | ) | (294 | ) | (405 | ) | ||||||

| Other—net | (17 | ) | (40 | ) | (72 | ) | ||||||

| Net cash used for investing activities | (2,561 | ) | (2,708 | ) | (2,927 | ) | ||||||

| Cash flow from financing activities: | ||||||||||||

| Dividends paid | (491 | ) | (481 | ) | (474 | ) | ||||||

| Common stock issued, including treasury shares reissued | 157 | 10 | 6 | |||||||||

| Treasury shares purchased | (405 | ) | — | (43 | ) | |||||||

| Proceeds from long-term debt issued: | ||||||||||||

| —Machinery and Engines | 128 | 248 | 681 | |||||||||

| —Financial Products | 5,274 | 3,889 | 3,381 | |||||||||

| Payments on long-term debt: | ||||||||||||

| —Machinery and Engines | (463 | ) | (225 | ) | (354 | ) | ||||||

| —Financial Products | (3,774 | ) | (3,114 | ) | (2,599 | ) | ||||||

| Short-term borrowings—net | 87 | (102 | ) | 420 | ||||||||

| Net cash provided by financing activities | 513 | 225 | 1,018 | |||||||||

| Effect of exchange rate changes on cash | 15 | 26 | (12 | ) | ||||||||

| Increase (decrease) in cash and short-term investments | 33 | (91 | ) | 66 | ||||||||

| Cash and short-term investments at beginning of period | 309 | 400 | 334 | |||||||||

| Cash and short-term investments at end of period | $ | 342 | $ | 309 | $ | 400 | ||||||

All short-term investments, which consist primarily of highly liquid investments with original maturities of three months or less, are considered to be cash equivalents.

See accompanying Notes to Consolidated Financial Statements.

A-7

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Operations and summary of significant accounting policies

A. Nature of operations

We operate in three principal lines of business:

(1) Machinery—A principal line of business which includes the design, manufacture and marketing of construction, mining, agricultural and forestry machinery—track and wheel tractors, track and wheel loaders, pipelayers, motor graders, wheel tractor-scrapers, track and wheel excavators, backhoe loaders, mining shovels, log skidders, log loaders, off-highway trucks, articulated trucks, paving products, telescopic handlers, skid steer loaders and related parts. Also includes logistics services for other companies.

(2) Engines—A principal line of business including the design, manufacture and marketing of engines for Caterpillar machinery, electric power generation systems; on-highway vehicles and locomotives; marine, petroleum, construction, industrial, agricultural and other applications; and related parts. Reciprocating engines meet power needs ranging from 5 to over 22,000 horsepower (4 to over 16 200 kilowatts). Turbines range from 1,600 to 19,500 horsepower (1 000 to 14 500 kilowatts).

(3) Financial Products—A principal line of business consisting primarily of Caterpillar Financial Services Corporation (Cat Financial), Caterpillar Insurance Holdings, Inc. (Cat Insurance) and their subsidiaries. Cat Financial provides a wide range of financing alternatives for Caterpillar machinery and engines, Solar gas turbines, as well as other equipment and marine vessels. Cat Financial also extends loans to customers and dealers. Cat Insurance provides various forms of insurance to customers and dealers to help support the purchase and lease of our equipment.

Our Machinery and Engines operations are highly integrated. Throughout the Notes, Machinery and Engines represents the aggregate total of these principal lines of business.

Our products are sold primarily under the brands "Caterpillar," "Cat," "Solar Turbines," "MaK," "Perkins," "FG Wilson" and "Olympian."

We conduct operations in our Machinery and Engines lines of business under highly competitive conditions, including intense price competition. We place great emphasis on the high quality and performance of our products and our dealers' service support. Although no one competitor is believed to produce all of the same types of machines and engines that we do, there are numerous companies, large and small, which compete with us in the sale of each of our products.

Machines are distributed principally through a worldwide organization of dealers (dealer network), 56 located in the United States and 151 located outside the United States. Worldwide, these dealers serve 178 countries and operate 3,263 places of business, including 1,391 dealer rental outlets. Reciprocating engines are sold principally through the dealer network and to other manufacturers for use in products manufactured by them. Some of the reciprocating engines manufactured by Perkins are also sold through a worldwide network of 166 distributors located in 148 countries. Most of the electric power generation systems manufactured by FG Wilson are sold through a worldwide network of 250 dealers located in 170 countries. Our dealers do not deal exclusively with our products; however, in most cases sales and servicing of our products are the dealers' principal business. Turbines and large marine reciprocating engines are sold through sales forces employed by Solar and MaK, respectively. Occasionally, these employees are assisted by independent sales representatives.

Manufacturing activities of the Machinery and Engines lines of business are conducted in 44 plants in the United States; 10 in the United Kingdom; eight in Italy; five in Mexico; four in China; three each in France, India and Northern Ireland; two each in Australia, Canada, Germany, Brazil and Japan; and one each in Belgium, Hungary, Indonesia, The Netherlands, Poland, Russia, South Africa and Sweden. Fourteen parts distribution centers are located in the United States and 12 are located outside the United States.

The Financial Products line of business also conducts operations under highly competitive conditions. Financing for users of Caterpillar products is available through a variety of competitive sources, principally commercial banks and finance and leasing companies. We emphasize prompt and responsive service to meet customer requirements and offer various financing plans designed to increase the opportunity for sales of our products and generate financing income for our company. Financial Products activity is conducted primarily in the United States, with additional offices in Asia, Australia, Canada, Europe and Latin America.

B. Basis of consolidation

The financial statements include the accounts of Caterpillar Inc. and its subsidiaries. Investments in companies that are owned 20% to 50% or are less than 20% owned and for which we have significant influence are accounted for by the equity method (see Note 8 on page A-15). We consolidate all variable interest entities where Caterpillar Inc. is the primary beneficiary.

Certain amounts for prior years have been reclassified to conform with the current-year financial statement presentation. In the second quarter of 2003, we revised our policy regarding the classification of certain costs related to distributing replacement parts. Previously, these costs were included in selling, general and administrative expenses and now are included in cost of goods sold. This classification is more consistent with industry practice. The parts distribution costs include shipping and handling (including warehousing) along with related support costs such as information technology, purchasing and inventory management. Prior period amounts have been revised to conform to the new classification. In 2002 and 2001, the amounts reclassified from selling, general and administrative expenses to cost of goods sold were $437 million and $427 million, respectively. This amount was $443 million for 2003. The reclassification had no impact on operating profit.

C. Sales and revenue recognition

Sales of Machinery and Engines are recognized when title transfers and the risks and rewards of ownership have passed to customers or independently owned and operated dealers.

Our standard invoice terms are established by marketing region. The dealer is responsible for payment even if the product is not sold to an end customer and must make payment within the standard terms to avoid interest costs. Interest at or above prevailing market rates is charged on any past due balance. Interest is not forgiven. In 2003, 2002 and 2001, terms were extended to not more than one year for $54 million, $193 million and $224 million of receivables, respectively. For 2003, this amount represents less than 1% of consolidated sales. For 2002 and 2001, these amounts represent approximately 1% of consolidated sales.

A-8

Sales with payment terms of two months or more were as follows:

| | 2003 | 2002 | 2001 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Payment Terms (months) | Sales | Percent of Sales | Sales | Percent of Sales | Sales | Percent of Sales | ||||||||||

| | (Dollars in millions) | |||||||||||||||

| 2 | $ | 116 | 0.6 | % | $ | 62 | 0.3 | % | $ | 28 | 0.2 | % | ||||

| 3 | 27 | 0.1 | % | 118 | 0.6 | % | 177 | 0.9 | % | |||||||

| 4 | 28 | 0.1 | % | 11 | 0.1 | % | 6 | 0.0 | % | |||||||

| 5 | 594 | 2.8 | % | 447 | 2.4 | % | 422 | 2.2 | % | |||||||

| 6 | 4,104 | 19.5 | % | 3,503 | 18.8 | % | 4,056 | 21.3 | % | |||||||

| 7-12 | 671 | 3.2 | % | 465 | 2.5 | % | 218 | 1.2 | % | |||||||

| $ | 5,540 | 26.3 | % | $ | 4,606 | 24.7 | % | $ | 4,907 | 25.8 | % | |||||

Revenues of Financial Products represent primarily finance and lease revenues of Cat Financial. Finance revenues are recognized over the term of the contract at a constant rate of return on the scheduled uncollected principal balance. Lease revenues are recognized in the period earned. Recognition of income is suspended when collection of future income is not probable. Accrual is resumed, and previously suspended income is recognized, when the receivable becomes contractually current and/or collection doubts are removed.

D. Inventories

Inventories are stated at the lower of cost or market. Cost is principally determined using the last-in, first-out (LIFO) method. The value of inventories on the LIFO basis represented about 80% of total inventories at December 31, 2003, 2002 and 2001.

If the FIFO (first-in, first-out) method had been in use, inventories would have been $1,863 million, $1,977 million and $1,923 million higher than reported at December 31, 2003, 2002 and 2001, respectively.

E. Securitized receivables

When finance receivables are securitized, we retain interest in the receivables in the form of interest-only strips, servicing rights, cash reserve accounts and subordinated certificates. Gains or losses on the securitization are dependent on the purchase price being allocated between the carrying value of the securitized receivables and the retained interests based on their relative fair value. We estimate fair value based on the present value of future expected cash flows using key assumptions for credit losses, pre-payment speeds, forward yield curves and discount rates (see Note 5 on pages A-13 to A-15).

F. Depreciation and amortization

Depreciation of plant and equipment is computed principally using accelerated methods. Depreciation on equipment leased to others, primarily for Financial Products, is computed using the straight-line method over the term of the lease. The depreciable basis is the original cost of the equipment less the estimated residual value of the equipment at the end of the lease term. In 2003, 2002 and 2001, Financial Products depreciation on equipment leased to others was $527 million, $415 million and $314 million, respectively, and was included in "Other operating expenses" in Statement 1. Amortization of purchased intangibles is computed using the straight-line method, generally over a period of 15 years or less. Accumulated amortization was $44 million, $47 million and $32 million at December 31, 2003, 2002 and 2001, respectively.

G. Foreign currency translation

The functional currency for most of our Machinery and Engines consolidated companies is the U.S. dollar. The functional currency for most of our Financial Products and equity basis companies is the respective local currency. Gains and losses resulting from the translation of foreign currency amounts to the functional currency are included in "Other income (expense)" in Statement 1. Gains and losses resulting from translating assets and liabilities from the functional currency to U.S. dollars are included in "Accumulated other comprehensive income."

H. Derivative financial instruments

Our earnings and cash flow are subject to fluctuations due to changes in foreign currency exchange rates, interest rates and commodity prices. Our Risk Management Policy (policy) allows for the use of derivative financial instruments to prudently manage foreign currency exchange rate, interest rate and commodity price exposure. Our policy specifies that derivatives are not to be used for speculative purposes. Derivatives that we use are primarily foreign currency forward and option contracts, interest rate swaps and commodity forward and option contracts. Our derivative activities are subject to the management, direction and control of our financial officers. Risk management practices, including the use of financial derivative instruments, are presented to the Audit Committee of the board of directors at least annually.

All derivatives are recognized on the financial position at their fair value. On the date the derivative contract is entered, we designate the derivative as (1) a hedge of the fair value of a recognized liability ("fair value" hedge), (2) a hedge of a forecasted transaction or the variability of cash flow to be paid ("cash flow" hedge), or (3) an "undesignated" instrument. Changes in the fair value of a derivative that is qualified, designated and highly effective as a fair value hedge, along with the gain or loss on the hedged liability that is attributable to the hedged risk, are recorded in current earnings. Changes in the fair value of a derivative that is qualified, designated and highly effective as a cash flow hedge are recorded in other comprehensive income until earnings are affected by the forecasted transaction or the variability of cash flow and are then reported in current earnings. Changes in the fair value of undesignated derivative instruments and the ineffective portion of designated derivative instruments are reported in current earnings.

We formally document all relationships between hedging instruments and hedged items, as well as the risk-management objective and strategy for undertaking various hedge transactions. This process includes linking all derivatives that are designated as fair value hedges to specific liabilities on the balance sheet and linking cash flow hedges to specific forecasted transactions or variability of cash flow.

We also formally assess, both at the hedge's inception and on an ongoing basis, whether the derivatives that are used in hedging transactions are highly effective in offsetting changes in fair values or cash flow of hedged items. When it is determined that a derivative is not highly effective as a hedge or that it has ceased to be a highly effective hedge, we discontinue hedge accounting prospectively, in accordance with Statement of Financial Accounting Standards No. 133 (SFAS 133). Please refer to Note 2 on pages A-11 to A-12 for more information on derivatives.

I. Impairment of available-for-sale securities

Available-for-sale securities are reviewed monthly to identify market values below cost of 20% or more. If a decline for a debt security is in excess of 20% for six months, the investment is

A-9

evaluated to determine if the decline is due to general declines in the marketplace or if the investment has been impaired and should be written down to market value pursuant to Statement of Financial Accounting Standards No. 115, "Accounting for Certain Investments in Debt and Equity Securities (SFAS 115)." After the six-month period, debt securities with declines from cost in excess of 20% are evaluated monthly for impairment. For equity securities, if a decline from cost of 20% or more continues for a 12-month period, an other than temporary impairment is recognized without continued analysis.

J. Income taxes

The provision for income taxes is determined using the asset and liability approach for accounting for income taxes. Tax laws require items to be included in tax filings at different times than the items are reflected in the financial statements. A current liability is recognized for the estimated taxes payable for the current year. Deferred taxes represent the future tax consequences expected to occur when the reported amounts of assets and liabilities are recovered or paid. Deferred taxes are adjusted for enacted changes in tax rates and tax laws. Valuation allowances are recorded to reduce deferred tax assets when it is more likely than not that a tax benefit will not be realized.

K. Estimates in financial statements

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect reported amounts. The more significant estimates include: residual values for leased assets, fair market values for goodwill impairment tests, and reserves for warranty, product liability and insurance losses, postemployment benefits, post-sale discounts, credit losses and income taxes.

L. Accounting changes

In June 2001, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standards No. 143 (SFAS 143), "Accounting for Asset Retirement Obligations." SFAS 143 addresses financial accounting and reporting for obligations associated with the retirement of tangible, long-lived assets and the associated asset retirement costs. This Statement requires that the fair value of a liability for an asset retirement obligation be recognized in the period in which it is incurred by capitalizing it as part of the carrying amount of the long-lived assets. As required by SFAS 143, we adopted this new accounting standard on January 1, 2003. The adoption of SFAS 143 did not have any impact on our financial statements.

In November 2002, the FASB issued Interpretation No. 45 (FIN 45), "Guarantor's Accounting and Disclosure Requirements for Guarantees, Including Indirect Guarantees of Indebtedness of Others." FIN 45 elaborates on the disclosures to be made by a guarantor about its obligations under certain guarantees. It also clarifies that a guarantor is required to recognize, at the inception of a guarantee, a liability for the fair value of the obligation undertaken in issuing the guarantee. As required by FIN 45, on January 1, 2003, we adopted the initial recognition and measurement provisions on a prospective basis for guarantees issued or modified after December 31, 2002. The adoption of the recognition/measurement provisions did not have any impact on our financial statements.

In January 2003, the FASB issued Interpretation No. 46 (FIN 46), "Consolidation of Variable Interest Entities—an Interpretation of ARB No. 51." FIN 46 addresses consolidation by business enterprises of variable interest entities that have certain characteristics. Transferors to qualifying special-purpose entities and "grandfathered" qualifying special-purpose entities subject to the reporting requirements of SFAS 140, "Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities," are excluded from the scope of FIN 46. FIN 46 is applicable immediately to variable interest entities created or obtained after January 31, 2003 (none created or obtained in 2003). For variable interest entities, which we acquired before February 1, 2003, FIN 46 is applicable to us as of December 31, 2003. In December 2003, the FASB issued Interpretation No. 46—revised 2003 (FIN 46R). We adopted FIN 46 and FIN 46R during 2003. The adoption of these interpretations did not have a material impact on our financial statements.

In April 2003, the FASB issued Statement of Financial Accounting Standards No. 149 (SFAS 149), "Amendment of Statement 133 on Derivative Instruments and Hedging Activities." SFAS 149 amends SFAS 133, "Accounting for Derivative Instruments and Hedging Activities" to provide clarification on the financial accounting and reporting for derivative instruments and hedging activities and requires similar accounting treatment for contracts with comparable characteristics. The adoption of SFAS 149, effective primarily for contracts entered into or modified after June 30, 2003, and for hedging relationships designated after June 30, 2003, had no impact on our financial statements.

In May 2003, the FASB issued Statement of Financial Accounting Standards No. 150 (SFAS 150), "Accounting for Certain Financial Instruments with Characteristics of both Liabilities and Equity." SFAS 150 addresses financial accounting and reporting for certain financial instruments with characteristics of both liabilities and equity. This statement requires that an issuer classify a financial instrument that is within its scope as a liability (or an asset in some circumstances) because that financial instrument embodies an obligation of the issuer. As required by SFAS 150, we adopted this new accounting standard effective July 1, 2003. The adoption of SFAS 150 did not have any impact on our financial statements.

In December 2003, the FASB issued Statement of Financial Accounting Standards No. 132 (revised 2003) "Employers' Disclosures about Pensions and Other Postretirement Benefits." SFAS 132 (revised 2003) retains the disclosure requirements of SFAS 132, which it replaces, and addresses the need for additional annual disclosures related to a company's pensions and other postretirement benefits. SFAS 132 (revised 2003) does not change the measurement or recognition criteria of SFAS 87, "Employers' Accounting for Pensions," SFAS 88, "Employers' Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for Termination Benefits," or SFAS 106, "Employers' Accounting for Postretirement Benefits Other Than Pensions." SFAS 132 (revised 2003) requires new annual disclosures about the types of plan assets, investment strategy, measurement date, plan obligations and cash flows related to a company's pensions and other postretirement benefits. It also requires disclosure of the components of net periodic benefit cost recognized in interim periods and, if significantly different from previously

A-10

disclosed amounts, the projected contributions to fund pension and other postretirement benefit plans. We adopted the disclosure requirements of SFAS 132 (revised 2003) in December 2003.

M. Stock based compensation

We use the intrinsic value method of accounting for stock-based employee compensation in accordance with Accounting Principles Board Opinion No. 25, "Accounting for Stock Issued to Employees." No compensation expense is recognized in association with our options. We adopted the disclosure requirements of SFAS 148, "Accounting for Stock-Based Compensation-Transition and Disclosure," in December 2002.

Pro forma net income and earnings per share were:

| | Years ended December 31, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | |||||||||

| | (Dollars in millions except per share data) | |||||||||||

| Net income, as reported | $ | 1,099 | $ | 798 | $ | 805 | ||||||

| Deduct: Total stock-based employee compensation expense determined under fair value based method for all awards, net of related tax effects | (69 | ) | (65 | ) | (57 | ) | ||||||

| Pro forma net income | $ | 1,030 | $ | 733 | $ | 748 | ||||||

| Profit per share of common stock: | ||||||||||||

| As reported: | ||||||||||||

| Basic | $ | 3.18 | $ | 2.32 | $ | 2.35 | ||||||

| Assuming dilution | $ | 3.13 | $ | 2.30 | $ | 2.32 | ||||||

| Pro forma: | ||||||||||||

| Basic | $ | 2.98 | $ | 2.13 | $ | 2.18 | ||||||

| Assuming dilution | $ | 2.93 | $ | 2.13 | $ | 2.17 | ||||||

2. Derivative financial instruments and risk management

A. Adoption of SFAS 133

We adopted SFAS 133, "Accounting for Derivative Instruments and Hedging Activities," and Financial Accounting Standards No. 138 effective January 1, 2001. Adoption of these new accounting standards resulted in cumulative after-tax reductions to profit and accumulated other comprehensive income of $2 million and $12 million, respectively, in the first quarter of 2001. The adoption also immaterially impacted both assets and liabilities recorded on the balance sheet. During 2002 and 2001, we reclassified $1 million and $5 million of the transition adjustment from accumulated other comprehensive income to current earnings, respectively.

B. Foreign currency exchange rate risk

Foreign currency exchange rate movements create a degree of risk by affecting the U.S. dollar value of sales made and costs incurred in foreign currencies. Movements in foreign currency rates also affect our competitive position as these changes may affect business practices and/or pricing strategies of non-U.S.-based competitors. Additionally, we have balance sheet positions denominated in foreign currency, thereby creating exposure to movements in exchange rates.

Machinery and Engines operations purchase, manufacture and sell products in many locations around the world. As we have a diversified revenue and cost base, we manage our future foreign currency cash flow exposure on a net basis. We use foreign currency forward and option contracts to manage unmatched foreign currency cash inflow and outflow. Our objective is to minimize the risk of exchange rate movements that would reduce the U.S. dollar value of our foreign currency cash flow. Our policy allows for managing anticipated foreign currency cash flow for up to four years.

We generally designate as cash flow hedges at inception of the contract any Australian dollar, Brazilian real, British pound, Canadian dollar, euro, Japanese yen, Mexican peso or Singapore dollar forward or option contracts that exceed 90 days in duration. Designation is performed on a specific exposure basis to support hedge accounting. The remainder of Machinery and Engines foreign currency contracts are undesignated.

As of December 31, 2003, $70 million of deferred net gains included in equity ("Accumulated other comprehensive income" in Statement 3), related to Machinery and Engines foreign currency contracts, is expected to be reclassified to current earnings ["Other income (expense)"] over the next twelve months. There were no circumstances where hedge treatment was discontinued during 2003, 2002 or 2001.

In managing foreign currency risk for our Financial Products operations, our objective is to minimize earnings volatility resulting from conversion and the remeasurement of net foreign currency balance sheet positions. Our policy allows the use of foreign currency forward contracts to offset the risk of currency mismatch between our receivable and debt portfolio. All such foreign currency forward contracts are undesignated.

Gains/(losses) included in current earnings [Other income (expense)]:

| | 2003 | 2002 | 2001 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | (Millions of dollars) | ||||||||||

| Machinery and Engines: | |||||||||||

| On undesignated contracts | $ | (1 | ) | $ | — | $ | (2 | ) | |||

| Due to changes in time and volatility value on options | — | $ | (1 | ) | $ | — | |||||

| Financial Products: | |||||||||||

| On undesignated contracts | $ | (121 | ) | $ | (96 | ) | $ | 43 | |||

| $ | (122 | ) | $ | (97 | ) | $ | 41 | ||||

Gains and losses on the Financial Products contracts above are substantially offset by balance sheet remeasurement and conversion gains and losses.

C. Interest rate risk

Interest rate movements create a degree of risk by affecting the amount of our interest payments and the value of our fixed rate debt. Our policy is to use interest rate swap agreements and forward rate agreements to manage our exposure to interest rate changes and lower the cost of borrowed funds.

Machinery and Engines operations generally use fixed rate debt as a source of funding. Our objective is to minimize the cost of borrowed funds. Our policy allows us to enter fixed-to-floating interest rate swaps and forward rate agreements to meet that objective with the intent to designate as fair value hedges at inception of the contract all fixed-to-floating interest rate swaps. Designation as a hedge of the fair value of our fixed rate debt is performed to support hedge accounting. During 2001, our Machinery and Engines operations liquidated all fixed-to-floating interest rate swaps. Deferred gains on liquidated fixed-to-floating interest rate swaps, which were previously designated as fair value hedges, are being amortized to earnings ratably over the remaining life of the hedged debt. We designate as cash flow hedges at inception of the contract all forward rate agreements. Designation as a hedge of the anticipated issuance of debt is performed to support hedge accounting. Machinery and Engines forward rate agreements are 100% effective.

Financial Products operations have a "match funding" objective whereby, within specified boundaries, the interest rate profile

A-11

(fixed rate or floating rate) of their debt portfolio largely matches the interest rate profile of their receivable, or asset, portfolio. In connection with that objective, we use interest rate derivative instruments to modify the debt structure to match the receivable portfolio. This "match funding" reduces the risk of deteriorating margins between interest-bearing assets and interest-bearing liabilities, regardless of which direction interest rates move. We also use these instruments to gain an economic and/or competitive advantage through a lower cost of borrowed funds. This is accomplished by changing the characteristics of existing debt instruments or entering into new agreements in combination with the issuance of new debt.

Our policy allows us to issue floating-to-fixed, fixed-to-floating and floating-to-floating interest rate swaps to meet the "match funding" objective. We designate as fair value hedges, at inception of the contract, all fixed-to-floating interest rate swaps. Designation as a hedge of the fair value of our fixed rate debt is performed to support hedge accounting. As Financial Products fixed-to-floating interest rate swaps are 100% effective, gains on designated interest rate derivatives were offset completely by losses on hedged debt. Financial Products policy is to designate as cash flow hedges, at inception of the contract, most floating-to-fixed interest rate swaps. Designation as a hedge of the variability of cash flow is performed to support hedge accounting. During the second quarter of 2002, Financial Products liquidated four fixed-to-floating interest rate swaps. Deferred gains on these swaps, which were previously designated as fair value hedges, are being amortized to earnings ratably over the remaining life of the hedged debt.

Gains (losses) included in current earnings [Other income (expense)]:

| | 2003 | 2002 | 2001 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | (Millions of dollars) | |||||||||||

| Fixed-to-floating interest rate swaps | ||||||||||||

| Machinery and Engines: | ||||||||||||

| Gain/(loss) on designated interest rate derivatives | $ | — | $ | — | $ | 23 | ||||||

| Gain/(loss) on hedged debt | — | — | (18 | ) | ||||||||

| Gain/(loss) on liquidated swaps | 6 | 8 | 6 | |||||||||

| Financial Products: | ||||||||||||

| Gain/(loss) on designated interest rate derivatives | (20 | ) | 17 | 44 | ||||||||

| Gain/(loss) on hedged debt | 20 | (17 | ) | (44 | ) | |||||||

| Gain/(loss) on liquidated swaps—included in interest expense | 2 | 1 | — | |||||||||

| Floating-to-fixed interest rate swaps | ||||||||||||

| Financial Products: | ||||||||||||

| Gain/(loss) due to ineffectiveness | $ | — | $ | — | $ | (1 | ) | |||||

| $ | 8 | $ | 9 | $ | 10 | |||||||

As of December 31, 2003, $16 million of deferred net losses included in equity ("Accumulated other comprehensive income" in Statement 3), related to Financial Products floating-to-fixed interest rate swaps, is expected to be reclassified to current earnings ("Interest expense of Financial Products") over the next twelve months. There were no circumstances where hedge treatment was discontinued during 2003, 2002 or 2001 in either Machinery and Engines or Financial Products.

D. Commodity price risk

Commodity price movements create a degree of risk by affecting the price we must pay for certain raw material. Our policy is to use commodity forward and option contracts to manage the commodity risk and reduce the cost of purchased materials.

Our Machinery and Engines operations purchase aluminum, copper and nickel embedded in the components we purchase from suppliers. Our suppliers pass on to us price changes in the commodity portion of the component cost.

Our objective is to reduce the cost of purchased materials. Our policy allows us to enter commodity forward and option contracts to lock in the purchase price of the commodities within a four-year horizon. All such commodity forward and option contracts are undesignated. Gains/(losses) on the undesignated contracts of $27 million, $1 million and $(8) million were recorded in current earnings ["Other income (expense)"] for 2003, 2002 and 2001, respectively.

3. Other income (expense)

| | Years ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2001 | 2002 | |||||||

| | (Millions of dollars) | |||||||||

| Investment and interest income | $ | 49 | $ | 31 | $ | 96 | ||||

| Foreign exchange (losses) gains | 35 | 13 | (29 | ) | ||||||

| Charge for early retirement of debt | (55 | ) | — | — | ||||||

| Miscellaneous income | 6 | 25 | 76 | |||||||

| $ | 35 | $ | 69 | $ | 143 | |||||

4. Income taxes

The components of profit before taxes were:

| | Years ended December 31, | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2001 | 2002 | ||||||

| | (Millions of dollars) | ||||||||

| U.S. | $ | 489 | $ | 343 | $ | 741 | |||

| Non-U.S. | 988 | 771 | 428 | ||||||

| $ | 1,477 | $ | 1,114 | $ | 1,169 | ||||

Profit before taxes, as shown above, is based on the location of the entity to which such earnings are attributable. However, since such earnings are subject to taxation in more than one country, the income tax provision shown below as U.S. or non-U.S. may not correspond to the earnings shown above.

The components of the provision for income taxes were:

| | Years ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | ||||||||

| | (Millions of dollars) | ||||||||||

| Current tax provision: | |||||||||||

| U.S. Federal | $ | 24 | $ | (62 | ) | $ | 150 | ||||

| Non-U.S. | 196 | 210 | 174 | ||||||||

| State (U.S.) | 10 | 1 | 11 | ||||||||

| $ | 230 | $ | 149 | $ | 335 | ||||||

| Deferred tax provision (credit): | |||||||||||

| U.S. Federal | 182 | 172 | 65 | ||||||||

| Non-U.S. | (21 | ) | (20 | ) | (34 | ) | |||||

| State (U.S.) | 7 | 11 | 1 | ||||||||

| 168 | 163 | 32 | |||||||||

| Total provision for income taxes | $ | 398 | $ | 312 | $ | 367 | |||||

Reconciliation of the U.S. federal statutory rate to effective rate:

| | Years ended December 31, | |||||||

|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | |||||

| U.S. statutory rate | 35.0 | % | 35.0 | % | 35.0 | % | ||

| (Decreases) increases in taxes resulting from: | ||||||||

| Benefit of foreign sales corporation/extraterritorial income exclusion | (4.9 | )% | (4.4 | )% | (4.9 | )% | ||

| Non-U.S. subsidiaries taxed at other than 35% | (4.0 | )% | (3.4 | )% | (0.1 | )% | ||

| Other—net | 0.9 | % | 0.8 | % | 1.4 | % | ||

| Provision for income taxes | 27.0 | % | 28.0 | % | 31.4 | % | ||

A-12

We paid income taxes of $55 million, $124 million and $379 million in 2003, 2002 and 2001, respectively.

We have recorded income tax expense at U.S. tax rates on all profits, except for undistributed profits of non-U.S. companies which are considered permanently invested. Determination of the amount of unrecognized deferred tax liability related to permanently invested profits is not feasible.

Certain subsidiaries operating in China qualify for holidays from income tax, which consist of a two-year full exemption from tax followed by a three-year 50% reduction in the applicable tax rate. The tax holiday begins the first year the subsidiary generates taxable income after utilization of any carryforward losses. The dollar effect in 2003 was $10 million or $.03 per share.

Deferred income tax assets and liabilities:

| | December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | ||||||||

| | (Millions of dollars) | ||||||||||

| Deferred income tax assets: | |||||||||||

| Postemployment benefits other than pensions | $ | 1,147 | $ | 1,130 | $ | 1,112 | |||||

| Warranty reserves | 163 | 204 | 186 | ||||||||

| Unrealized profit excluded from inventories | 242 | 219 | 212 | ||||||||

| Tax carryforwards | 370 | 230 | 130 | ||||||||

| Inventory valuation method | 37 | 60 | 50 | ||||||||

| Pension | — | 39 | — | ||||||||

| Other | 133 | 128 | 275 | ||||||||

| 2,092 | 2,010 | 1,965 | |||||||||

| Deferred income tax liabilities: | |||||||||||

| Capital assets | (673 | ) | (538 | ) | (437 | ) | |||||

| Pension | (102 | ) | — | (182 | ) | ||||||

| (775 | ) | (538 | ) | (619 | ) | ||||||

| Valuation allowance for deferred tax assets | (37 | ) | (34 | ) | (27 | ) | |||||

| Deferred income taxes—net | $ | 1,280 | $ | 1,438 | $ | 1,319 | |||||

SFAS 109 requires that individual tax-paying entities of the company offset all current deferred tax liabilities and assets within each particular tax jurisdiction and present them as a single amount in the Statement of Financial Position. A similar procedure is followed for all noncurrent deferred tax liabilities and assets. Amounts in different tax jurisdictions cannot be offset against each other. The amount of deferred income taxes at December 31, included on the following lines in Statement 3, are as follows:

| | 2003 | 2002 | 2001 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | (Millions of dollars) | |||||||||

| Assets: | ||||||||||

| Deferred and refundable income taxes | $ | 702 | $ | 777 | $ | 434 | ||||

| Deferred income taxes | 616 | 711 | 927 | |||||||

| $ | 1,318 | $ | 1,488 | $ | 1,361 | |||||

| Liabilities: | ||||||||||

| Deferred and current income taxes payable | $ | 18 | $ | 8 | $ | 6 | ||||

| Deferred income taxes and other liabilities | 20 | 42 | 36 | |||||||

| Deferred income taxes—net | $ | 1,280 | $ | 1,438 | $ | 1,319 | ||||

A valuation allowance has been recorded at certain non-U.S. subsidiaries that have not yet demonstrated consistent and/or sustainable profitability to support the recognition of net deferred tax assets.

As of December 31, 2003, amounts and expiration dates of net operating loss carryforwards in various non-U.S. taxing jurisdictions were:

| 2004 | 2005 | 2006 | 2007 | 2008-2014 | Unlimited | Total | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Millions of dollars) | |||||||||||||||||||

| $ | 7 | $ | 9 | $ | 8 | $ | 13 | $ | 123 | $ | 528 | $ | 688 | ||||||

As of December 31, 2003, approximately $365 million of state tax net operating loss carryforwards were available. Of these, 82% expire after 2014.

As of December 31, 2003, approximately $148 million of regular foreign tax credits and $18 million of credit for increasing research activities were available to carry forward in the United States. Of the foreign tax credits, $108 million will expire in 2008, and $40 million will expire in 2009. The research credits will begin to expire in 2023.

5. Finance receivables

Finance receivables are receivables of Cat Financial, which generally can be repaid or refinanced without penalty prior to contractual maturity. Total finance receivables reported in Statement 3 are net of an allowance for credit losses. The average interest rate on these receivables was 6.3%, 7.1% and 8.7% for 2003, 2002 and 2001, respectively.

Caterpillar Inc. utilizes inventory merchandising programs for its North American dealers. Certain dealer receivables, which arise from the sale of goods, are sold to Cat Financial. Some of these receivables are then securitized by Cat Financial into private-placement, revolving securitization facilities. Cat Financial services the dealer receivables, which are held in a securitization trust and receives an annual servicing fee of 1% of the average outstanding principal balance. Securitization of receivables is a cost-effective means of financing the business. Consolidated net discounts of $6 million, $10 million and $24 million were recognized on securitization of dealer receivables during 2003, 2002 and 2001, respectively, and are included in "Other income (expense)" in Statement 1. Significant assumptions used to estimate the fair value of dealer receivables securitized during 2003, 2002 and 2001 include a discount rate of 4.1%, 4.8% and 7.2%, respectively. These rates reflect declining market interest rates. Other assumptions include a one-month weighted-average maturity, a weighted-average prepayment rate of 0% and expected credit losses of 0% for 2003, 2002 and 2001. Expected credit losses are assumed to be 0% because dealer receivables have historically had no losses and none are expected in the future. The net dealer receivables retained were $1,550 million, $1,145 million and $772 million as of December 31, 2003, 2002 and 2001, respectively, and are included in "Receivables—finance" in Statement 3 and "Wholesale Notes" in Table I on page A-14.

During 2003, 2002 and 2001, Cat Financial securitized retail installment sale contracts and finance leases into public asset-backed securitization facilities. These finance receivables, which are being held in securitization trusts, are secured by new and used equipment. Cat Financial retained servicing responsibilities and subordinated interests related to these securitizations. For 2003, subordinated interests included $9 million in subordinated certificates, an interest in certain future cash flow (excess) with an initial fair value of $14 million and a reserve account with an initial fair value of $10 million. For 2002, subordinated interests included $8 million in subordinated certificates, an interest in certain future cash flow (excess) with an initial fair value of $11 million and a reserve account with an initial fair value of $10 million. For 2001, subordinated interests included $10 million in subordinated certificates, an interest in certain future cash flow (excess) with an initial fair value of $20 million and a reserve account with an initial fair value of $5 million. The company's retained interests

A-13

generally are subordinate to the investors' interests. Net gains of $22 million, $18 million and $21 million were recognized on these transactions in 2003, 2002 and 2001, respectively.

Significant assumptions used to estimate the fair value of the subordinated certificates were:

| | 2003 | 2002 | 2001 | ||||

|---|---|---|---|---|---|---|---|

| Discount rate | 5.0 | % | 4.8 | % | 6.3 | % | |

| Weighted-average prepayment rate | 14.0 | % | 14.0 | % | 14.0 | % | |

| Expected credit losses | 1.0 | % | 1.0 | % | 0.6 | % |

Significant assumptions used to estimate the fair value of the excess and the reserve accounts were:

| | 2003 | 2002 | 2001 | ||||

|---|---|---|---|---|---|---|---|

| Discount rate | 14.0 | % | 14.0 | % | 13.6 | % | |

| Weighted-average prepayment rate | 14.0 | % | 14.0 | % | 14.0 | % | |

| Expected credit losses | 1.0 | % | 1.0 | % | 0.6 | % |

The company receives annual servicing fees of approximately 1% of the unpaid note value.

As of December 31, 2003, 2002 and 2001, the subordinated retained interests in the public securitizations totaled $73 million, $47 million and $51 million, respectively. Key assumptions used to determine the fair value of the retained interests were:

| | 2003 | 2002 | 2001 | ||||

|---|---|---|---|---|---|---|---|

| Cash flow discount rates on subordinated tranches | 4.8-6.3 | % | 4.8-6.3 | % | 6.3-6.9 | % | |

| Cash flow discount rates on other retained interests | 13.6-14.0 | % | 13.6-14.0 | % | 13.6 | % | |

| Weighted-average maturity | 27 months | 29 months | 27 months | ||||

| Average prepayment rate | 14.0 | % | 14.0 | % | 14.0 | % | |

| Expected credit losses | 1.0 | % | 1.0 | % | 0.5 | % |

The investors and the securitization trusts have no recourse to Cat Financial's other assets for failure of debtors to pay when due.

TABLE I—Finance Receivables Information (Millions of dollars)

Contractual maturities of outstanding receivables:

| | December 31, 2003 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Amounts Due In | Installment Contracts | Wholesale and Retail Finance Leases | Wholesale and Retail Notes | Total | ||||||||

| 2004 | $ | 1,848 | $ | 1,664 | $ | 3,704 | $ | 7,216 | ||||

| 2005 | 1,310 | 1,136 | 918 | 3,364 | ||||||||

| 2006 | 818 | 683 | 567 | 2,068 | ||||||||

| 2007 | 399 | 345 | 303 | 1,047 | ||||||||

| 2008 | 157 | 159 | 517 | 833 | ||||||||

| Thereafter | 44 | 174 | 784 | 1,002 | ||||||||

| 4,576 | 4,161 | 6,793 | 15,530 | |||||||||

| Residual value | — | 932 | — | 932 | ||||||||

| Less: Unearned income | 287 | 467 | 40 | 794 | ||||||||

| Total | $ | 4,289 | $ | 4,626 | $ | 6,753 | $ | 15,668 | ||||

Impaired loans and leases:

| | 2003 | 2002 | 2001 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Average recorded investment | $ | 321 | $ | 292 | $ | 323 | ||||

| At December 31: | ||||||||||

| Recorded investment | $ | 275 | $ | 366 | $ | 259 | ||||

| Less: Impaired loans/finance leases for which there is no related allowance for credit losses (due to the fair value of underlying collateral) | 177 | 233 | 167 | |||||||

| Impaired loans/finance leases for which there is a related allowance for credit losses | $ | 98 | $ | 133 | $ | 92 | ||||

Allowance for credit loss activity:

| | 2003 | 2002 | 2001 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Balance at beginning of year | $ | 207 | $ | 177 | $ | 163 | ||||

| Provision for credit losses | 101 | 109 | 97 | |||||||

| Receivables written off | (104 | ) | (103 | ) | (82 | ) | ||||

| Recoveries on receivables previously written off | 22 | 18 | 10 | |||||||

| Other—net | 15 | 6 | (11 | ) | ||||||

| Balance at end of year | $ | 241 | $ | 207 | $ | 177 | ||||

In estimating the allowance for credit losses, we review accounts that are past due, non-performing or in bankruptcy.

Cat Financial's net investment in financing leases:

| | December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | |||||||

| Total minimum lease payments receivable | $ | 4,161 | $ | 3,794 | $ | 3,607 | ||||

| Estimated residual value of leased assets: | ||||||||||

| Guaranteed | 369 | 306 | 272 | |||||||

| Unguaranteed | 563 | 604 | 682 | |||||||

| 5,093 | 4,704 | 4,561 | ||||||||

| Less: Unearned income | 467 | 479 | 514 | |||||||

| Net investment in financing leases | $ | 4,626 | $ | 4,225 | $ | 4,047 | ||||

| | 2003 | 2002 | 2001 | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Dealer Receivables | Finance Receivables | Dealer Receivables | Finance Receivables | Dealer Receivables | Finance Receivables | |||||||||||||

| Cash flow from securitizations: | |||||||||||||||||||

| Proceeds from initial sales of receivables | $ | — | $ | 661 | $ | — | $ | 614 | $ | — | $ | 600 | |||||||

| Proceeds from subsequent sales of receivables into revolving facility | 1,099 | — | 1,696 | — | 2,479 | — | |||||||||||||

| Servicing fees received | 2 | 8 | 3 | 7 | 5 | 6 | |||||||||||||

Characteristics of securitized receivables: | |||||||||||||||||||

| At December 31: | |||||||||||||||||||

| Total securitized principal balance | $ | 240 | $ | 813 | $ | 240 | $ | 726 | $ | 500 | $ | 616 | |||||||

| Loans more than 30 days past due | — | 34 | — | 32 | — | 31 | |||||||||||||

| Weighted average maturity (in months) | 1 | 27 | 1 | 28 | 1 | 26 | |||||||||||||

| For the year ended December 31: | |||||||||||||||||||

| Average securitized principal balance | 240 | 1,073 | 324 | 619 | 504 | 836 | |||||||||||||

| Net credit losses | — | 6 | — | 5 | — | 3 | |||||||||||||

A-14

We estimated the impact of individual 10% and 20% changes to the key economic assumptions used to determine the fair value of residual cash flow in retained interests on our income. An independent, adverse change to each key assumption had an immaterial impact on the fair value of residual cash flow.

The securitization facilities involved in Cat Financial's securitizations are qualifying special purpose entities and thus, in accordance with Statement of Financial Standards No. 140 (SFAS 140), "Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities," are not consolidated.

We consider an account past due if any portion of an installment is due and unpaid for more than 30 days. Recognition of income is suspended when management determines that collection of future income is not probable (generally after 120 days past due). Accrual is resumed, and previously suspended income is recognized, when the receivable becomes contractually current and/or collection doubts are removed. Investment in loans/finance leases on non-accrual status were $233 million and $370 million and past due over 90 days and still accruing were $25 million and $72 million as of December 31, 2003 and 2002, respectively.

Cat Financial provides financing only when acceptable criteria are met. Credit decisions are based on, among other things, the customer's credit history, financial strength and intended use of equipment. Cat Financial typically maintains a security interest in retail financed equipment and requires physical damage insurance coverage on financed equipment.

Please refer to Table I on page A-14 for additional finance receivables information and Note 17 and Table III on pages A-22 to A-23 for fair value information.

6. Inventories

| | December 31, | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | ||||||

| | (Millions of dollars) | ||||||||

| Raw materials | $ | 1,105 | $ | 900 | $ | 954 | |||

| Work-in-process | 377 | 311 | 214 | ||||||

| Finished goods | 1,381 | 1,365 | 1,575 | ||||||

| Supplies | 184 | 187 | 182 | ||||||

| $ | 3,047 | $ | 2,763 | $ | 2,925 | ||||

We had long-term material purchase obligations of approximately $857 million at December 31, 2003.

7. Property, plant and equipment

| | | December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | Useful Lives (Years) | ||||||||||

| | 2003 | 2002 | 2001 | ||||||||

| | | (Dollars in millions) | |||||||||

| Land | — | $ | 149 | $ | 149 | $ | 149 | ||||

| Buildings and land improvements | 20-45 | 3,006 | 3,039 | 3,077 | |||||||

| Machinery, equipment and other | 3-10 | 7,039 | 7,015 | 6,658 | |||||||

| Equipment leased to others | — | 3,648 | 3,033 | 2,270 | |||||||

| Construction-in-process | — | 487 | 305 | 636 | |||||||

| Total property, plant and equipment, at cost | 14,329 | 13,541 | 12,790 | ||||||||

| Less: Accumulated depreciation | 7,039 | 6,495 | 6,187 | ||||||||

| Property, plant and equipment—net | $ | 7,290 | $ | 7,046 | $ | 6,603 | |||||

We had commitments for the purchase or construction of capital assets of approximately $218 million at December 31, 2003.

Assets recorded under capital leases(1):

| | December 31, | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | ||||||

| | (Millions of dollars) | ||||||||

| Gross capital leases(2) | $ | 321 | $ | 259 | $ | 444 | |||

| Less: Accumulated depreciation | 213 | 170 | 318 | ||||||

| Net capital leases | $ | 108 | $ | 89 | $ | 126 | |||

- (1)

- Included in Property, plant and equipment table above.

- (2)

- Consists primarily of machinery and equipment.

Equipment leased to others (primarily by Financial Products):

| | December 31, | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | ||||||

| | (Millions of dollars) | ||||||||

| Equipment leased to others—at original cost | $ | 3,648 | $ | 3,033 | $ | 2,270 | |||

| Less: Accumulated depreciation | 1,074 | 809 | 629 | ||||||

| Equipment leased to others—net | $ | 2,574 | $ | 2,224 | $ | 1,641 | |||

At December 31, 2003, scheduled minimum rental payments to be received for equipment leased to others were:

| 2004 | 2005 | 2006 | 2007 | 2008 | After 2008 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Millions of dollars) | ||||||||||||||||

| $ | 565 | $ | 398 | $ | 237 | $ | 116 | $ | 47 | $ | 22 | |||||

8. Investment in unconsolidated affiliated companies

The company's investment in affiliated companies accounted for by the equity method consists primarily of a 50% interest in Shin Caterpillar Mitsubishi Ltd. (SCM) located in Japan. Combined financial information of the unconsolidated affiliated companies accounted for by the equity method (generally on a three-month lag, e.g., SCM results reflect the periods ending September 30) was as follows:

| | Years ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | |||||||

| | (Millions of dollars) | |||||||||

| Results of Operations: | ||||||||||

| Sales | $ | 2,946 | $ | 2,734 | $ | 2,493 | ||||

| Cost of sales | 2,283 | 2,168 | 1,971 | |||||||

| Gross profit | 663 | 566 | 522 | |||||||

| Profit (loss) | $ | 48 | $ | (1 | ) | $ | 9 | |||

| Caterpillar's profit (loss) | $ | 20 | $ | (4 | ) | $ | 3 | |||

| | December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | ||||||||

| | (Millions of dollars) | ||||||||||

| Financial Position: | |||||||||||

| Assets: | |||||||||||

| Current assets | $ | 1,494 | $ | 1,389 | $ | 1,451 | |||||

| Property, plant and equipment—net | 961 | 1,209 | 986 | ||||||||

| Other assets | 202 | 493 | 290 | ||||||||

| 2,657 | 3,091 | 2,727 | |||||||||

| Liabilities: | |||||||||||

| Current liabilities | $ | 1,247 | $ | 1,117 | $ | 1,257 | |||||

| Long-term debt due after one year | 343 | 808 | 414 | ||||||||

| Other liabilities | 257 | 249 | 281 | ||||||||

| 1,847 | 2,174 | 1,952 | |||||||||

| Ownership | $ | 810 | $ | 917 | $ | 775 | |||||

Caterpillar's investment in unconsolidated affiliated companies:

| Investment in equity method companies | $ | 432 | $ | 437 | $ | 437 | |||

| Plus: Investment in cost method companies | 368 | 310 | 350 | ||||||

| Investment in unconsolidated affiliated companies | $ | 800 | $ | 747 | $ | 787 | |||

A-15

At December 31, 2003, consolidated "Profit employed in the business" in Statement 2 included $70 million representing undistributed profit of the unconsolidated affiliated companies. In 2003, 2002 and 2001, we received $25 million, $4 million and $4 million, respectively, in dividends from unconsolidated affiliated companies.

Certain investments in unconsolidated affiliated companies are accounted for using the cost method. During first quarter 2001, Cat Financial invested for a limited partnership interest in a venture financing structure associated with Caterpillar's rental strategy in the United Kingdom.

9. Intangible assets and goodwill

In July 2001, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 142 (SFAS 142), "Goodwill and Other Intangible Assets." SFAS 142 addresses financial accounting and reporting for intangible assets and goodwill. The Statement requires that goodwill and intangible assets having indefinite useful lives not be amortized, but rather be tested at least annually for impairment. Intangible assets that have finite useful lives will continue to be amortized over their useful lives. As required by SFAS 142, we adopted this new accounting standard on January 1, 2002. Upon adoption, we performed the required transitional impairment tests of goodwill and indefinite-lived intangible assets. Application of the transitional impairment provisions of SFAS 142 did not result in an impairment loss.

Intangible assets

| | 2003 | 2002 | |||||

|---|---|---|---|---|---|---|---|

| | (Millions of dollars) | ||||||

| Intellectual property | $ | 126 | $ | 137 | |||

| Pension-related | 157 | 191 | |||||

| Total intangible assets—gross | 283 | 328 | |||||

| Less: Accumulated amortization of intellectual property | (44 | ) | (47 | ) | |||

| Intangible assets—net | $ | 239 | $ | 281 | |||

Amortization expense was $15 million and $13 million for 2003 and 2002, respectively.

Amortization expense related to intangible assets is expected to be:

| 2004 | 2005 | 2006 | 2007 | 2008 | Thereafter | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Millions of dollars) | ||||||||||||||||

| $ | 15 | $ | 14 | $ | 13 | $ | 12 | $ | 8 | $ | 20 | |||||

During the years ended December 31, 2003 and 2002, no goodwill was acquired or impaired. During the year ended December 31, 2003, we disposed of assets with related goodwill of $3 million. No goodwill was disposed of during 2002. Goodwill amortization expense was $85 million for 2001. Excluding goodwill amortization expense, profit for 2001 was $863 million ($2.51 per share-basic, $2.49 per share-diluted).

10. Available-for-sale securities

Cat Insurance and Caterpillar Investment Management Ltd. had investments in certain debt and equity securities at December 31, 2003, 2002 and 2001, that have been classified as available-for-sale in accordance with Statement of Financial Accounting Standards No. 115 (SFAS 115) and recorded at fair value based upon quoted market prices. These fair values are included in "Other assets" in Statement 3. Gains and losses arising from the revaluation of available-for-sale securities are included, net of applicable deferred income taxes, in equity ("Accumulated other comprehensive income" in Statement 3). Realized gains and losses on sales of investments are determined using the average cost method for debt instruments and the FIFO method for equity securities.

| | December 31, 2003 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | Cost Basis | Pre-Tax Net Gains (Losses) | Fair Value | ||||||

| | (Millions of dollars) | ||||||||

| Government debt | $ | 102 | $ | — | $ | 102 | |||

| Corporate bonds | 288 | 3 | 291 | ||||||

| Equity securities | 191 | 21 | 212 | ||||||

| $ | 581 | $ | 24 | $ | 605 | ||||

| | December 31, 2002 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | Cost Basis | Pre-Tax Net Gains (Losses) | Fair Value | ||||||

| | (Millions of dollars) | ||||||||

| Government debt | $ | 89 | $ | — | $ | 89 | |||

| Corporate bonds | 208 | 1 | 209 | ||||||

| Equity securities | 220 | (51 | ) | 169 | |||||

| $ | 517 | $ | (50 | ) | $ | 467 | |||

| | December 31, 2001 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| | Cost Basis | Pre-Tax Net Gains (Losses) | Fair Value | ||||||

| | (Millions of dollars) | ||||||||

| Government debt | $ | 80 | $ | — | $ | 80 | |||

| Corporate bonds | 157 | 1 | 158 | ||||||

| Equity securities | 200 | (40 | ) | 160 | |||||

| $ | 437 | $ | (39 | ) | $ | 398 | |||

Investments in an unrealized loss position that are not other-than-temporarily impaired

| | December 31, 2003 | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Less than 12 months(1) | More than 12 months(1) | Total | |||||||||||||||||

| | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | ||||||||||||||

| | (Millions of dollars) | |||||||||||||||||||

| Corporate bonds | 93 | (2 | ) | 13 | (1 | ) | 106 | (3 | ) | |||||||||||

| Equity securities | — | — | 25 | (1 | ) | 25 | (1 | ) | ||||||||||||

| Total | $ | 93 | $ | (2 | ) | $ | 38 | $ | (2 | ) | $ | 131 | $ | (4 | ) | |||||

- (1)

- Indicates length of time that individual securities have been in a continuous unrealized loss position.

The fair value of available-for-sale debt securities at December 31, 2003, by contractual maturity, is shown below. Expected maturities will differ from contractual maturities because borrowers may have the right to call or prepay obligations.

| | Fair Value | ||

|---|---|---|---|

| | (Millions of dollars) | ||

| Due in one year or less | $ | 7 | |

| Due after one year through five years | $ | 229 | |

| Due after five years through ten years | $ | 14 | |

| Due after ten years | $ | 143 | |