EXHIBIT 13

CATERPILLAR INC.

GENERAL AND FINANCIAL INFORMATION

2013

TABLE OF CONTENTS

MANAGEMENT’S REPORT ON

INTERNAL CONTROL OVER FINANCIAL REPORTING

The management of Caterpillar Inc. (company) is responsible for establishing and maintaining adequate internal control over financial reporting as such term is defined in Rule 13a-15(f) under the Exchange Act. Our internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of our financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. Our internal control over financial reporting includes those policies and procedures that (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Management assessed the effectiveness of the company’s internal control over financial reporting as of December 31, 2013. In making this assessment, we used the criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) in Internal Control—Integrated Framework (1992). Based on our assessment we concluded that, as of December 31, 2013, the company’s internal control over financial reporting was effective based on those criteria.

The effectiveness of the company’s internal control over financial reporting as of December 31, 2013 has been audited by PricewaterhouseCoopers LLP, an independent registered public accounting firm. Their report appears on page A-4.

|

| | |

| | /s/Douglas R. Oberhelman | |

| | Douglas R. Oberhelman | |

| | Chairman of the Board | |

| | and Chief Executive Officer | |

| | |

| | | |

| | /s/Bradley M. Halverson | |

| | Bradley M. Halverson | |

| | Group President | |

| | and Chief Financial Officer | |

| | | |

| | | |

| | February 18, 2014 | |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of Caterpillar Inc.:

In our opinion, the accompanying consolidated statement of financial position and the related consolidated statements of results of operations, comprehensive income, changes in stockholders' equity, and of cash flow, including pages A-5 through A-101, present fairly, in all material respects, the financial position of Caterpillar Inc. and its subsidiaries at December 31, 2013, 2012 and 2011, and the results of their operations and their cash flows for each of the three years in the period ended December 31, 2013 in conformity with accounting principles generally accepted in the United States of America. Also in our opinion, the Company maintained, in all material respects, effective internal control over financial reporting as of December 31, 2013, based on criteria established in Internal Control - Integrated Framework (1992) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). The Company's management is responsible for these financial statements, for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting, included in Management's Report on Internal Control Over Financial Reporting appearing on page A-3. Our responsibility is to express opinions on these financial statements and on the Company's internal control over financial reporting based on our integrated audits. We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement and whether effective internal control over financial reporting was maintained in all material respects. Our audits of the financial statements included examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our audit of internal control over financial reporting included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based on the assessed risk. Our audits also included performing such other procedures as we considered necessary in the circumstances. We believe that our audits provide a reasonable basis for our opinions.

A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial reporting includes those policies and procedures that (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

/s/PricewaterhouseCoopers LLP

Peoria, Illinois

February 18, 2014

|

| | | | | | | | | | | |

| STATEMENT 1 | | | Caterpillar Inc. | |

| Consolidated Results of Operations for the Years Ended December 31 | | | | | |

| (Dollars in millions except per share data) | | | | | |

| | 2013 | | 2012 | | 2011 |

| Sales and revenues: | |

| | |

| | |

|

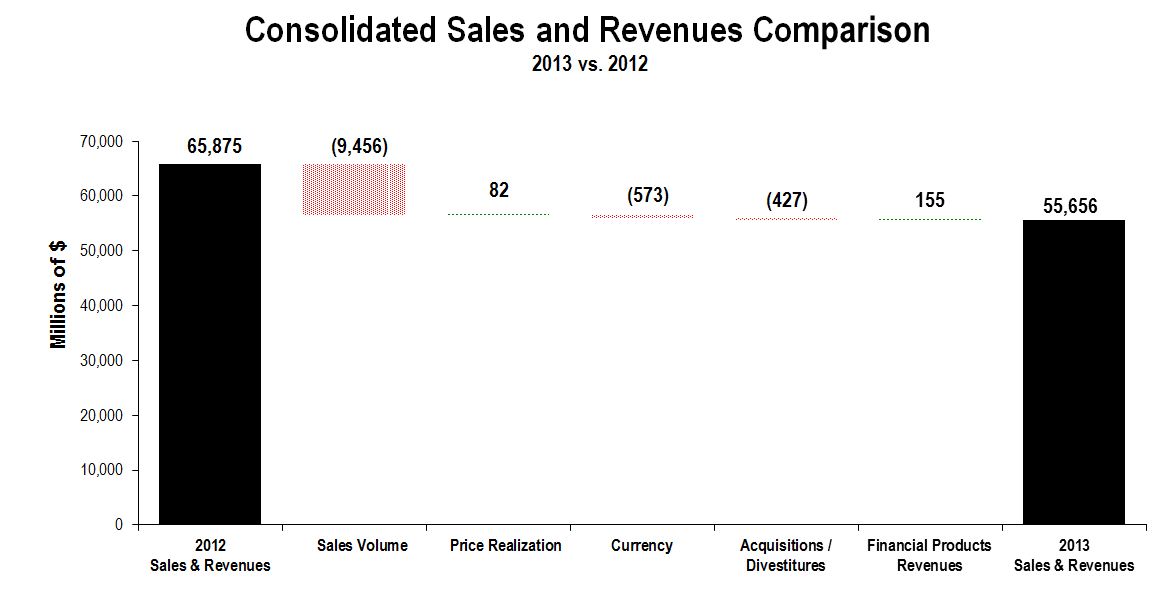

| Sales of Machinery and Power Systems | $ | 52,694 |

| | $ | 63,068 |

| | $ | 57,392 |

|

| Revenues of Financial Products | 2,962 |

| | 2,807 |

| | 2,746 |

|

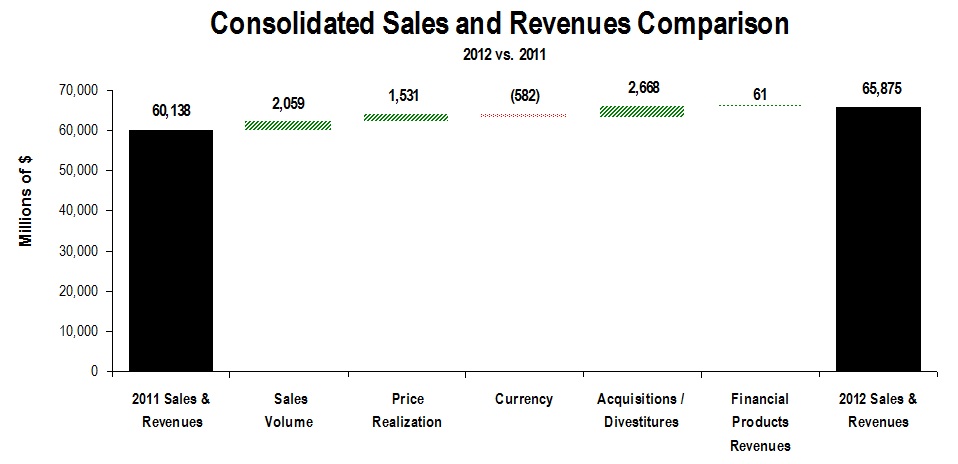

| Total sales and revenues | 55,656 |

| | 65,875 |

| | 60,138 |

|

| | | | | | |

| Operating costs: | |

| | |

| | |

|

| Cost of goods sold | 40,727 |

| | 47,055 |

| | 43,578 |

|

| Selling, general and administrative expenses | 5,547 |

| | 5,919 |

| | 5,203 |

|

| Research and development expenses | 2,046 |

| | 2,466 |

| | 2,297 |

|

| Interest expense of Financial Products | 727 |

| | 797 |

| | 826 |

|

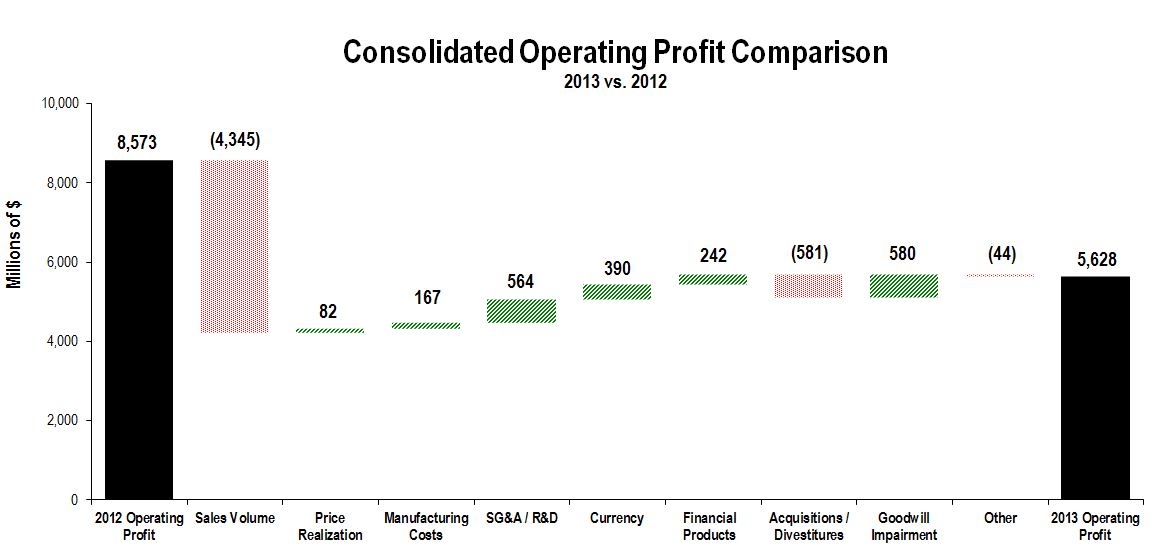

| Goodwill impairment charge | — |

| | 580 |

| | — |

|

| Other operating (income) expenses | 981 |

| | 485 |

| | 1,081 |

|

| Total operating costs | 50,028 |

| | 57,302 |

| | 52,985 |

|

| | | | | | |

| Operating profit | 5,628 |

| | 8,573 |

| | 7,153 |

|

| | | | | | |

| Interest expense excluding Financial Products | 465 |

| | 467 |

| | 396 |

|

| Other income (expense) | (35 | ) | | 130 |

| | (32 | ) |

| | | | | | |

| Consolidated profit before taxes | 5,128 |

| | 8,236 |

| | 6,725 |

|

| | | | | | |

| Provision (benefit) for income taxes | 1,319 |

| | 2,528 |

| | 1,720 |

|

| Profit of consolidated companies | 3,809 |

| | 5,708 |

| | 5,005 |

|

| | | | | | |

| Equity in profit (loss) of unconsolidated affiliated companies | (6 | ) | | 14 |

| | (24 | ) |

| | | | | | |

| Profit of consolidated and affiliated companies | 3,803 |

| | 5,722 |

| | 4,981 |

|

| | | | | | |

| Less: Profit (loss) attributable to noncontrolling interests | 14 |

| | 41 |

| | 53 |

|

| | | | | | |

Profit 1 | $ | 3,789 |

| | $ | 5,681 |

| | $ | 4,928 |

|

| | | | | | |

| Profit per common share | $ | 5.87 |

| | $ | 8.71 |

| | $ | 7.64 |

|

| | | | | | |

Profit per common share — diluted 2 | $ | 5.75 |

| | $ | 8.48 |

| | $ | 7.40 |

|

| | | | | | |

| Weighted-average common shares outstanding (millions) | |

| | |

| | |

|

| - Basic | 645.2 |

| | 652.6 |

| | 645.0 |

|

- Diluted 2 | 658.6 |

| | 669.6 |

| | 666.1 |

|

| | | | | | |

| Cash dividends declared per common share | $ | 2.32 |

| | $ | 2.02 |

| | $ | 1.82 |

|

| |

1 | Profit attributable to common stockholders. |

| |

2 | Diluted by assumed exercise of stock-based compensation awards, using the treasury stock method. |

|

| | | | |

| See accompanying notes to Consolidated Financial Statements. |

|

| | | | | | | | | | | |

| STATEMENT 2 | | | Caterpillar Inc. | |

| Consolidated Comprehensive Income for the Years Ended December 31 |

| (Millions of dollars) | | | | | |

| | 2013 | | 2012 | | 2011 |

| | | | | | |

| Profit of consolidated and affiliated companies | $ | 3,803 |

| | $ | 5,722 |

| | $ | 4,981 |

|

| Other comprehensive income (loss), net of tax: | | | | | |

| Foreign currency translation, net of tax (provision)/benefit of: 2013 - $57; 2012 - $9; 2011 - $3 | (277 | ) | | 60 |

| | (312 | ) |

| | | | | | |

| Pension and other postretirement benefits: | | | | | |

| Current year actuarial gain (loss), net of tax (provision)/benefit of: 2013 - $(1,232); 2012 - $372; 2011 - $1,276 | 2,277 |

| | (731 | ) | | (2,364 | ) |

| Amortization of actuarial (gain) loss, net of tax (provision)/benefit of: 2013 - $(265); 2012 - $(243); 2011 - $(221) | 516 |

| | 458 |

| | 412 |

|

| Current year prior service credit (cost), net of tax (provision)/benefit of: 2013 - $(2); 2012 - $(12); 2011 - $(51) | 3 |

| | 23 |

| | 95 |

|

| Amortization of prior service (credit) cost, net of tax (provision)/benefit of: 2013 - $19; 2012 - $17; 2011 - $11 | (35 | ) | | (31 | ) | | (21 | ) |

| Amortization of transition (asset) obligation, net of tax (provision)/benefit of: 2013 - $(1); 2012 - $(1); 2011 - $(1) | 1 |

| | 1 |

| | 1 |

|

| | | | | | |

| Derivative financial instruments: | | | | | |

| Gains (losses) deferred, net of tax (provision)/benefit of: 2013 - $2; 2012 - $29; 2011 - $12 | (4 | ) | | (48 | ) | | (21 | ) |

| (Gains) losses reclassified to earnings, net of tax (provision)/benefit of: 2013 - $(25); 2012 - $(10); 2011 - $21 | 41 |

| | 16 |

| | (34 | ) |

| | | | | | |

| Available-for-sale securities: | | | | | |

| Gains (losses) deferred, net of tax (provision)/benefit of: 2013 - $(15); 2012 - $(13); 2011 - $2 | 29 |

| | 26 |

| | (5 | ) |

| (Gains) losses reclassified to earnings, net of tax (provision)/benefit of: 2013 - $6; 2012 - $1; 2011 - $(1) | (13 | ) | | (3 | ) | | 1 |

|

| Total other comprehensive income (loss), net of tax | 2,538 |

| | (229 | ) | | (2,248 | ) |

| Comprehensive income | 6,341 |

| | 5,493 |

| | 2,733 |

|

| Less: comprehensive income attributable to the noncontrolling interests | (17 | ) | | (24 | ) | | (82 | ) |

| Comprehensive income attributable to stockholders | $ | 6,324 |

| | $ | 5,469 |

| | $ | 2,651 |

|

| | | | | | |

|

| | | | |

| See accompanying notes to Consolidated Financial Statements. |

|

| | | | | | | | | | | |

| STATEMENT 3 | | | Caterpillar Inc. | |

| Consolidated Financial Position at December 31 | | | | | |

| (Dollars in millions) | | | | | |

| | 2013 | | 2012 | | 2011 |

| Assets | |

| | |

| | |

|

| Current assets: | |

| | |

| | |

|

| Cash and short-term investments | $ | 6,081 |

| | $ | 5,490 |

| | $ | 3,057 |

|

| Receivables - trade and other | 8,413 |

| | 9,706 |

| | 10,057 |

|

| Receivables - finance | 8,763 |

| | 8,860 |

| | 7,668 |

|

| Deferred and refundable income taxes | 1,553 |

| | 1,547 |

| | 1,580 |

|

| Prepaid expenses and other current assets | 900 |

| | 988 |

| | 994 |

|

| Inventories | 12,625 |

| | 15,547 |

| | 14,544 |

|

| Total current assets | 38,335 |

| | 42,138 |

| | 37,900 |

|

| | | | | | |

| Property, plant and equipment - net | 17,075 |

| | 16,461 |

| | 14,395 |

|

| Long-term receivables - trade and other | 1,397 |

| | 1,316 |

| | 1,130 |

|

| Long-term receivables - finance | 14,926 |

| | 14,029 |

| | 11,948 |

|

| Investments in unconsolidated affiliated companies | 272 |

| | 272 |

| | 133 |

|

| Noncurrent deferred and refundable income taxes | 594 |

| | 2,011 |

| | 2,157 |

|

| Intangible assets | 3,596 |

| | 4,016 |

| | 4,368 |

|

| Goodwill | 6,956 |

| | 6,942 |

| | 7,080 |

|

| Other assets | 1,745 |

| | 1,785 |

| | 2,107 |

|

| Total assets | $ | 84,896 |

| | $ | 88,970 |

| | $ | 81,218 |

|

| | | | | | |

| Liabilities | |

| | |

| | |

|

| Current liabilities: | |

| | |

| | |

|

| Short-term borrowings: | |

| | |

| | |

|

| Machinery and Power Systems | $ | 16 |

| | $ | 636 |

| | $ | 93 |

|

| Financial Products | 3,663 |

| | 4,651 |

| | 3,895 |

|

| Accounts payable | 6,560 |

| | 6,753 |

| | 8,161 |

|

| Accrued expenses | 3,493 |

| | 3,667 |

| | 3,386 |

|

| Accrued wages, salaries and employee benefits | 1,622 |

| | 1,911 |

| | 2,410 |

|

| Customer advances | 2,360 |

| | 2,638 |

| | 2,487 |

|

| Dividends payable | 382 |

| | — |

| | 298 |

|

| Other current liabilities | 1,849 |

| | 2,055 |

| | 1,967 |

|

| Long-term debt due within one year: | |

| | |

| | |

|

| Machinery and Power Systems | 760 |

| | 1,113 |

| | 558 |

|

| Financial Products | 6,592 |

| | 5,991 |

| | 5,102 |

|

| Total current liabilities | 27,297 |

| | 29,415 |

| | 28,357 |

|

| Long-term debt due after one year: | |

| | |

| | |

|

| Machinery and Power Systems | 7,999 |

| | 8,666 |

| | 8,415 |

|

| Financial Products | 18,720 |

| | 19,086 |

| | 16,529 |

|

| Liability for postemployment benefits | 6,973 |

| | 11,085 |

| | 10,956 |

|

| Other liabilities | 3,029 |

| | 3,136 |

| | 3,559 |

|

| Total liabilities | 64,018 |

| | 71,388 |

| | 67,816 |

|

| Commitments and contingencies (Notes 21 and 22) |

|

| |

|

| |

|

|

| Redeemable noncontrolling interest (Note 25) | — |

| | — |

| | 473 |

|

| Stockholders’ equity | |

| | |

| | |

|

| Common stock of $1.00 par: | |

| | |

| | |

|

Authorized shares: 2,000,000,000

Issued shares: (2013, 2012 and 2011 – 814,894,624) at paid-in amount | 4,709 |

| | 4,481 |

| | 4,273 |

|

| Treasury stock: (2013 – 177,072,282; 2012 – 159,846,131 shares; and 2011 – 167,361,280 shares) at cost | (11,854 | ) | | (10,074 | ) | | (10,281 | ) |

| Profit employed in the business | 31,854 |

| | 29,558 |

| | 25,219 |

|

| Accumulated other comprehensive income (loss) | (3,898 | ) | | (6,433 | ) | | (6,328 | ) |

| Noncontrolling interests | 67 |

| | 50 |

| | 46 |

|

| Total stockholders’ equity | 20,878 |

| | 17,582 |

| | 12,929 |

|

| Total liabilities, redeemable noncontrolling interest and stockholders’ equity | $ | 84,896 |

| | $ | 88,970 |

| | $ | 81,218 |

|

| | | | | | |

|

| | | | |

| See accompanying notes to Consolidated Financial Statements. |

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| STATEMENT 4 | | Caterpillar Inc. | | |

| Changes in Consolidated Stockholders’ Equity for the Years Ended December 31 | |

| (Dollars in millions) | | | | | | | | | | | | |

| | Common stock | | Treasury stock | | Profit employed in the business | | Accumulated other comprehensive income (loss) | | Noncontrolling interests | | Total | |

| Balance at January 1, 2011 | $ | 3,888 |

| | $ | (10,397 | ) | | $ | 21,384 |

| | $ | (4,051 | ) | | $ | 40 |

| | $ | 10,864 |

| |

| Profit of consolidated and affiliated companies | — |

| | — |

| | 4,928 |

| | — |

| | 53 |

| | 4,981 |

| |

| Foreign currency translation, net of tax | — |

| | — |

| | — |

| | (345 | ) | | 33 |

| | (312 | ) | |

| Pension and other postretirement benefits, net of tax | — |

| | — |

| | — |

| | (1,873 | ) | | (4 | ) | | (1,877 | ) | |

| Derivative financial instruments, net of tax | — |

| | — |

| | — |

| | (55 | ) | | — |

| | (55 | ) | |

| Available-for-sale securities, net of tax | — |

| | — |

| | — |

| | (4 | ) | | — |

| | (4 | ) | |

| Change in ownership from noncontrolling interests | (1 | ) | | — |

| | — |

| | — |

| | (7 | ) | | (8 | ) | |

| Dividends declared | — |

| | — |

| | (1,176 | ) | | — |

| | — |

| | (1,176 | ) | |

| Distribution to noncontrolling interests | — |

| | — |

| | — |

| | — |

| | (3 | ) | | (3 | ) | |

| Common shares issued from treasury stock for stock-based compensation: 8,710,630 | 7 |

| | 116 |

| | — |

| | — |

| | — |

| | 123 |

| |

| Stock-based compensation expense | 193 |

| | — |

| | — |

| | — |

| | — |

| | 193 |

| |

| Net excess tax benefits from stock-based compensation | 186 |

| | — |

| | — |

| | — |

| | — |

| | 186 |

| |

Cat Japan share redemption 1 | — |

| | — |

| | 83 |

| | — |

| | (66 | ) | | 17 |

| |

| Balance at December 31, 2011 | $ | 4,273 |

| | $ | (10,281 | ) | | $ | 25,219 |

| | $ | (6,328 | ) | | $ | 46 |

| | $ | 12,929 |

| |

| Profit of consolidated and affiliated companies | — |

| | — |

| | 5,681 |

| | — |

| | 41 |

| | 5,722 |

| |

| Foreign currency translation, net of tax | — |

| | — |

| | — |

| | 83 |

| | (23 | ) | | 60 |

| |

| Pension and other postretirement benefits, net of tax | — |

| | — |

| | — |

| | (285 | ) | | 5 |

| | (280 | ) | |

| Derivative financial instruments, net of tax | — |

| | — |

| | — |

| | (32 | ) | | — |

| | (32 | ) | |

| Available-for-sale securities, net of tax | — |

| | — |

| | — |

| | 22 |

| | 1 |

| | 23 |

| |

| Change in ownership from noncontrolling interests | — |

| | — |

| | — |

| | — |

| | (4 | ) | | (4 | ) | |

| Dividends declared | — |

| | — |

| | (1,319 | ) | | — |

| | — |

| | (1,319 | ) | |

| Distribution to noncontrolling interests | — |

| | — |

| | — |

| | — |

| | (6 | ) | | (6 | ) | |

| Common shares issued from treasury stock for stock-based compensation: 7,515,149 | (155 | ) | | 207 |

| | — |

| | — |

| | — |

| | 52 |

| |

| Stock-based compensation expense | 245 |

| | — |

| | — |

| | — |

| | — |

| | 245 |

| |

| Net excess tax benefits from stock-based compensation | 192 |

| | — |

| | — |

| | — |

| | — |

| | 192 |

| |

Cat Japan share redemption 1 | (74 | ) | | — |

| | (23 | ) | | 107 |

| | (10 | ) | | — |

| |

| Balance at December 31, 2012 | $ | 4,481 |

| | $ | (10,074 | ) | | $ | 29,558 |

| | $ | (6,433 | ) | | $ | 50 |

| | $ | 17,582 |

| |

(Continued)

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| STATEMENT 4 | | Caterpillar Inc. | | |

| Changes in Consolidated Stockholders’ Equity for the Years Ended December 31 | |

| (Dollars in millions) | | | | | | | | | | | | |

| | Common stock | | Treasury stock | | Profit employed in the business | | Accumulated other comprehensive income (loss) | | Noncontrolling interests | | Total | |

| Balance at December 31, 2012 | $ | 4,481 |

| | $ | (10,074 | ) | | $ | 29,558 |

| | $ | (6,433 | ) | | $ | 50 |

| | $ | 17,582 |

| |

| Profit of consolidated and affiliated companies | — |

| | — |

| | 3,789 |

| | — |

| | 14 |

| | 3,803 |

| |

| Foreign currency translation, net of tax | — |

| | — |

| | — |

| | (280 | ) | | 3 |

| | (277 | ) | |

| Pension and other postretirement benefits, net of tax | — |

| | — |

| | — |

| | 2,762 |

| | — |

| | 2,762 |

| |

| Derivative financial instruments, net of tax | — |

| | — |

| | — |

| | 37 |

| | — |

| | 37 |

| |

| Available-for-sale securities, net of tax | — |

| | — |

| | — |

| | 16 |

| | — |

| | 16 |

| |

| Change in ownership from noncontrolling interests | (6 | ) | | — |

| | — |

| | — |

| | 13 |

| | 7 |

| |

| Dividends declared | — |

| | — |

| | (1,493 | ) | | — |

| | — |

| | (1,493 | ) | |

| Distribution to noncontrolling interests | — |

| | — |

| | — |

| | — |

| | (13 | ) | | (13 | ) | |

| Common shares issued from treasury stock for stock-based compensation: 6,258,692 | (92 | ) | | 220 |

| | — |

| | — |

| | — |

| | 128 |

| |

| Stock-based compensation expense | 231 |

| | — |

| | — |

| | — |

| | — |

| | 231 |

| |

| Net excess tax benefits from stock-based compensation | 95 |

| | — |

| | — |

| | — |

| | — |

| | 95 |

| |

Common shares repurchased: 23,484,843 2 | — |

| | (2,000 | ) | | — |

| | — |

| | — |

| | (2,000 | ) | |

| Balance at December 31, 2013 | $ | 4,709 |

| | $ | (11,854 | ) | | $ | 31,854 |

| | $ | (3,898 | ) | | $ | 67 |

| | $ | 20,878 |

| |

| |

1 | See Note 25 regarding the Cat Japan share redemption. |

| |

2 | See Note 16 regarding shares repurchased. |

|

| | | | |

| See accompanying notes to Consolidated Financial Statements. |

|

| | | | | | | | | | | |

| STATEMENT 5 | | Caterpillar Inc. | |

| Consolidated Statement of Cash Flow for the Years Ended December 31 | | | | | |

| (Millions of dollars) | | | | | |

| | 2013 | | 2012 | | 2011 |

| Cash flow from operating activities: | |

| | |

| | |

|

| Profit of consolidated and affiliated companies | $ | 3,803 |

| | $ | 5,722 |

| | $ | 4,981 |

|

| Adjustments for non-cash items: | |

| | |

| | |

|

| Depreciation and amortization | 3,087 |

| | 2,813 |

| | 2,527 |

|

| Net gain from sale of businesses and investments | (68 | ) | | (630 | ) | | (128 | ) |

| Goodwill impairment charge | — |

| | 580 |

| | — |

|

| Other | 550 |

| | 439 |

| | 585 |

|

| Changes in assets and liabilities, net of acquisitions and divestitures: | |

| | |

| | |

|

| Receivables - trade and other | 835 |

| | (15 | ) | | (1,409 | ) |

| Inventories | 2,658 |

| | (1,149 | ) | | (2,927 | ) |

| Accounts payable | 134 |

| | (1,868 | ) | | 1,555 |

|

| Accrued expenses | (108 | ) | | 126 |

| | 255 |

|

| Accrued wages, salaries and employee benefits | (279 | ) | | (490 | ) | | 619 |

|

| Customer advances | (301 | ) | | 83 |

| | 237 |

|

| Other assets - net | (49 | ) | | 252 |

| | (91 | ) |

| Other liabilities - net | (71 | ) | | (679 | ) | | 753 |

|

| Net cash provided by (used for) operating activities | 10,191 |

| | 5,184 |

| | 6,957 |

|

| | | | | | |

| Cash flow from investing activities: | |

| | |

| | |

|

| Capital expenditures - excluding equipment leased to others | (2,522 | ) | | (3,350 | ) | | (2,515 | ) |

| Expenditures for equipment leased to others | (1,924 | ) | | (1,726 | ) | | (1,409 | ) |

| Proceeds from disposals of leased assets and property, plant and equipment | 844 |

| | 1,117 |

| | 1,354 |

|

| Additions to finance receivables | (11,422 | ) | | (12,010 | ) | | (10,001 | ) |

| Collections of finance receivables | 9,567 |

| | 8,995 |

| | 8,874 |

|

| Proceeds from sale of finance receivables | 220 |

| | 132 |

| | 207 |

|

| Investments and acquisitions (net of cash acquired) | (195 | ) | | (618 | ) | | (8,184 | ) |

| Proceeds from sale of businesses and investments (net of cash sold) | 365 |

| | 1,199 |

| | 376 |

|

| Proceeds from sale of available-for-sale securities | 449 |

| | 306 |

| | 247 |

|

| Investments in available-for-sale securities | (402 | ) | | (402 | ) | | (336 | ) |

| Other - net | (26 | ) | | 167 |

| | (40 | ) |

| Net cash provided by (used for) investing activities | (5,046 | ) | | (6,190 | ) | | (11,427 | ) |

| | | | | | |

| Cash flow from financing activities: | |

| | |

| | |

|

| Dividends paid | (1,111 | ) | | (1,617 | ) | | (1,159 | ) |

| Distribution to noncontrolling interests | (13 | ) | | (6 | ) | | (3 | ) |

| Common stock issued, including treasury shares reissued | 128 |

| | 52 |

| | 123 |

|

| Treasury shares purchased | (2,000 | ) | | — |

| | — |

|

| Excess tax benefit from stock-based compensation | 96 |

| | 192 |

| | 189 |

|

| Acquisitions of redeemable noncontrolling interests | — |

| | (444 | ) | | — |

|

| Acquisitions of noncontrolling interests | — |

| | (5 | ) | | (8 | ) |

| Proceeds from debt issued (original maturities greater than three months): | |

| | |

| | |

|

| - Machinery and Power Systems | 195 |

| | 2,209 |

| | 4,587 |

|

| - Financial Products | 9,133 |

| | 13,806 |

| | 10,873 |

|

| Payments on debt (original maturities greater than three months): | |

| | |

| | |

|

| - Machinery and Power Systems | (1,769 | ) | | (1,107 | ) | | (2,269 | ) |

| - Financial Products | (9,101 | ) | | (9,940 | ) | | (8,277 | ) |

| Short-term borrowings - net (original maturities three months or less) | (69 | ) | | 466 |

| | (37 | ) |

| Net cash provided by (used for) financing activities | (4,511 | ) | | 3,606 |

| | 4,019 |

|

| Effect of exchange rate changes on cash | (43 | ) | | (167 | ) | | (84 | ) |

| Increase (decrease) in cash and short-term investments | 591 |

| | 2,433 |

| | (535 | ) |

| Cash and short-term investments at beginning of period | 5,490 |

| | 3,057 |

| | 3,592 |

|

| Cash and short-term investments at end of period | $ | 6,081 |

| | $ | 5,490 |

| | $ | 3,057 |

|

All short-term investments, which consist primarily of highly liquid investments with original maturities of three months or less, are considered to be cash equivalents.

Non-cash activities: In 2012, $1,325 million of debentures with varying interest rates and maturity dates were exchanged for $1,722 million of 3.803% debentures due in 2042 and $179 million of cash. The $179 million of cash paid is included in Other liabilities – net in the operating activities section of the Consolidated Statement of Cash Flow.

|

| | | | |

| See accompanying notes to Consolidated Financial Statements. |

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

| |

| 1. | Operations and summary of significant accounting policies |

Information in our financial statements and related commentary are presented in the following categories:

Machinery and Power Systems – Represents the aggregate total of Construction Industries, Resource Industries, Power Systems, and the All Other segment and related corporate items and eliminations.

Financial Products – Primarily includes the company’s Financial Products Segment. This category includes Caterpillar Financial Services Corporation (Cat Financial), Caterpillar Financial Insurance Services (Insurance Services) and their respective subsidiaries.

Our products are sold primarily under the brands “Caterpillar,” “CAT,” design versions of “CAT” and “Caterpillar,” “Electro-Motive,” “FG Wilson,” “MaK,” “MWM,” “Perkins,” “Progress Rail,” “SEM” and “Solar Turbines”.

We conduct operations in our Machinery and Power Systems lines of business under highly competitive conditions, including intense price competition. We place great emphasis on the high quality and performance of our products and our dealers’ service support. Although no one competitor is believed to produce all of the same types of machines and engines that we do, there are numerous companies, large and small, which compete with us in the sale of each of our products.

Our machines are distributed principally through a worldwide organization of dealers (dealer network), 48 located in the United States and 130 located outside the United States, serving 182 countries and operating 3,454 places of business, including 1,202 dealer rental outlets. Reciprocating engines are sold principally through the dealer network and to other manufacturers for use in products. Some of the reciprocating engines manufactured by our subsidiary Perkins Engines Company Limited, are also sold through a worldwide network of 100 distributors located in 180 countries. Most of the electric power generation systems manufactured by our subsidiary Caterpillar Northern Ireland Limited, formerly known as F.G. Wilson Engineering Limited, are sold through its worldwide network of 264 distributors located in 145 countries. Some of the large, medium speed reciprocating engines are also sold under the MaK brand through a worldwide network of 19 distributors located in 130 countries. Our dealers do not deal exclusively with our products; however, in most cases sales and servicing of our products are the dealers’ principal business. Turbines, locomotives and certain global mining products are sold directly to end customers through sales forces employed by the company. At times, these employees are assisted by independent sales representatives.

The Financial Products line of business also conducts operations under highly competitive conditions. Financing for users of Caterpillar products is available through a variety of competitive sources, principally commercial banks and finance and leasing companies. We emphasize prompt and responsive service to meet customer requirements and offer various financing plans designed to increase the opportunity for sales of our products and generate financing income for our company. A significant portion of Financial Products activity is conducted in North America, with additional offices in Asia/Pacific, Europe and Latin America.

The consolidated financial statements include the accounts of Caterpillar Inc. and its subsidiaries where we have a controlling financial interest.

We consolidate all variable interest entities (VIEs) where Caterpillar Inc. is the primary beneficiary. For VIEs, we assess whether we are the primary beneficiary as prescribed by the accounting guidance on the consolidation of VIEs. The primary beneficiary of a VIE is the party that has both the power to direct the activities that most significantly impact the entity’s economic performance, and the obligation to absorb losses or the right to receive benefits that could potentially be significant to the VIE.

Investments in companies that are owned 20 percent to 50 percent or are less than 20 percent owned and for which we have significant influence are accounted for by the equity method. See Note 9 for further discussion.

Certain amounts for prior years have been reclassified to conform with the current-year financial statement presentation.

We have revised previously reported cash flows from operating and financing activities on Statement 5 for the years ended December 31, 2012 and 2011 to correct for the impact of interest payments on certain Cat Financial bank borrowings. Cash provided by operating activities decreased from the amounts previously reported by $57 million and $53 million for the years ended December 31, 2012 and 2011, respectively. Cash provided by financing activities increased by the same amounts for the respective periods. Management has concluded that the impact was not material to any annual period.

We have also revised previously reported balances on Statement 3 as of December 31, 2012 and 2011 to correct for customer advances invoiced but not yet paid. Receivables - trade and other decreased from the amounts previously reported by $386 million and $228 million as of December 31, 2012 and 2011, respectively. Customer advances decreased from the amounts previously reported by $340 million and $204 million as of December 31, 2012 and 2011, respectively. Other (long-term) liabilities also decreased from the amounts previously reported by $46 million and $24 million as of December 31, 2012 and 2011, respectively. Although the revision did not impact Net cash provided by (used for) operating activities on Statement 5, we have revised the impacted operating cash flow line items for the years ended December 31, 2012 and 2011. Management has concluded that the impact was not material to any period presented.

Shipping and handling costs are included in Cost of goods sold in Statement 1. Other operating (income) expenses primarily include Cat Financial’s depreciation of equipment leased to others, Insurance Services’ underwriting expenses, gains (losses) on disposal of long-lived assets and business divestitures, long-lived asset impairment charges, legal settlements, employee separation charges and benefit plan curtailment, settlement and contractual termination benefits.

Prepaid expenses and other current assets in Statement 3 include prepaid rent, prepaid insurance, assets held for sale, core to be returned for remanufacturing, restricted cash and other short-term investments, and other prepaid items.

| |

| C. | Sales and revenue recognition |

Sales of Machinery and Power Systems are recognized and earned when all the following criteria are satisfied: (a) persuasive evidence of a sales arrangement exists; (b) price is fixed and determinable; (c) collectability is reasonably assured; and (d) delivery has occurred. Persuasive evidence of an arrangement and a fixed or determinable price exist once we receive an order or contract from a customer or independently owned and operated dealer. We assess collectability at the time of the sale and if collectability is not reasonably assured, the sale is deferred and not recognized until collectability is probable or payment is received. Typically, where product is produced and sold in the same country, title and risk of ownership transfer when the product is shipped. Products that are exported from a country for sale typically pass title and risk of ownership at the border of the destination country.

Sales of certain turbine machinery units, draglines, large shovels and long wall roof supports are recognized under accounting for construction-type contracts, primarily using the percentage-of-completion method. Revenue is recognized based upon progress towards completion, which is estimated and continually updated over the course of construction. We provide for any loss that we expect to incur on these contracts when that loss is probable.

Our remanufacturing operations are primarily focused on the remanufacture of Cat engines and components and rail related products. In this business, used engines and related components (core) are inspected, cleaned and remanufactured. In connection with the sale of most of our remanufactured product, we collect a deposit from the dealer that is repaid if the dealer returns an acceptable core within a specified time period. Caterpillar owns and has title to the cores when they are returned from dealers. The rebuilt engine or component (the core plus any new content) is then sold as a remanufactured product to dealers and customers. Revenue is recognized pursuant to the same criteria as machinery and power systems sales noted above (title to the entire remanufactured product passes to the dealer upon sale). At the time of sale, the deposit is recognized in Other current liabilities in Statement 3. In addition, the core to be returned is recognized as an asset in Prepaid expenses and other current assets in Statement 3 at the estimated replacement cost (based on historical experience with useable cores). Upon receipt of an acceptable core, we repay the deposit and relieve the liability. The returned core is then included in inventory. In the event that the deposit is forfeited (i.e. upon failure by the dealer to return an acceptable core in the specified time period), we recognize the core deposit and the cost of the core in Sales and Cost of goods sold, respectively.

No right of return exists on sales of equipment. Replacement part returns are estimable and accrued at the time a sale is recognized.

We provide discounts to dealers through merchandising programs. We have numerous programs that are designed to promote the sale of our products. The most common dealer programs provide a discount when the dealer sells a product to a targeted end user. The cost of these discounts is estimated based on historical experience and known changes in merchandising programs and is reported as a reduction to sales when the product sale is recognized.

Our standard dealer invoice terms are established by marketing region. Our invoice terms for end-user customer sales are established by the responsible business unit. When a sale is made to a dealer, the dealer is responsible for payment even if the product is not sold to an end customer. Dealers and customers must make payment within the established invoice terms to avoid potential interest costs. Interest at or above prevailing market rates may be charged on any past due balance, and generally our practice is to not forgive this interest. In 2013, terms were extended to not more than one year for $706 million of receivables, which represent approximately 1 percent of consolidated sales. In 2012 and 2011, terms were extended to not more than one year for $354 million and $341 million of receivables, respectively, which represent less than 1 percent of consolidated sales.

We establish a bad debt allowance for Machinery and Power Systems receivables when it becomes probable that the receivable will not be collected. Our allowance for bad debts is not significant.

Revenues of Financial Products primarily represent the following Cat Financial revenues:

| |

| • | Retail finance revenue on finance leases and installment sale contracts is recognized over the term of the contract at a constant rate of return on the scheduled outstanding principal balance. Revenue on retail notes is recognized based on the daily balance of retail receivables outstanding and the applicable effective interest rate. |

| |

| • | Operating lease revenue is recorded on a straight-line basis in the period earned over the life of the contract. |

| |

| • | Cat Financial provides wholesale inventory financing to dealers. Wholesale finance revenue on installment sale contracts and finance leases related to financing dealer inventory and rental fleets is recognized over the term of the contract at a constant rate of return on the scheduled outstanding principal balance. Revenue on wholesale notes is recognized based on the daily balance of wholesale receivables outstanding and the applicable effective interest rate. |

| |

| • | Loan origination and commitment fees are deferred and amortized to revenue using the interest method over the life of the finance receivables. |

Recognition of income is suspended and the loan or finance lease is placed on non-accrual status when management determines that collection of future income is not probable (generally after 120 days past due except in locations where local regulatory requirements dictate a different method, or instances in which relevant information is known that warrants placing the loan or finance lease on non-accrual status). Accrual is resumed, and previously suspended income is recognized, when the receivable becomes contractually current and/or collection doubts are removed. See Note 6 for more information.

Sales and revenues are presented net of sales and other related taxes.

Inventories are stated at the lower of cost or market. Cost is principally determined using the last-in, first-out (LIFO) method. The value of inventories on the LIFO basis represented about 60 percent of total inventories at December 31, 2013 and 2012, and about 65 percent at December 31, 2011.

If the FIFO (first-in, first-out) method had been in use, inventories would have been $2,504 million, $2,750 million and $2,422 million higher than reported at December 31, 2013, 2012 and 2011, respectively.

| |

| E. | Depreciation and amortization |

Depreciation of plant and equipment is computed principally using accelerated methods. Depreciation on equipment leased to others, primarily for Financial Products, is computed using the straight-line method over the term of the lease. The depreciable basis is the original cost of the equipment less the estimated residual value of the equipment at the end of the lease term. In 2013, 2012 and 2011, Cat Financial depreciation on equipment leased to others was $768 million, $688 million and $690 million, respectively, and was included in Other operating (income) expenses in Statement 1. In 2013, 2012 and 2011, consolidated depreciation expense was $2,710 million, $2,421 million and $2,240 million, respectively. Amortization of purchased finite-lived intangibles is computed principally using the straight-line method, generally not to exceed a period of 20 years.

| |

| F. | Foreign currency translation |

The functional currency for most of our Machinery and Power Systems consolidated companies is the U.S. dollar. The functional currency for most of our Financial Products and affiliates accounted for under the equity method is the respective local currency. Gains and losses resulting from the remeasurement of foreign currency amounts to the functional currency are included in Other income (expense) in Statement 1. Gains and losses resulting from translating assets and liabilities from the functional currency to U.S. dollars are included in Accumulated other comprehensive income (loss) in Statement 3.

| |

| G. | Derivative financial instruments |

Our earnings and cash flow are subject to fluctuations due to changes in foreign currency exchange rates, interest rates and commodity prices. Our Risk Management Policy (policy) allows for the use of derivative financial instruments to prudently manage foreign currency exchange rate, interest rate and commodity price exposures. Our policy specifies that derivatives are not to be used for speculative purposes. Derivatives that we use are primarily foreign currency forward, option, and cross currency contracts, interest rate swaps, and commodity forward and option contracts. All derivatives are recorded at fair value. See Note 3 for more information.

The provision for income taxes is determined using the asset and liability approach taking into account guidance related to uncertain tax positions. Tax laws require items to be included in tax filings at different times than the items are reflected in the financial statements. A current liability is recognized for the estimated taxes payable for the current year. Deferred taxes represent the future tax consequences expected to occur when the reported amounts of assets and liabilities are recovered or paid. Deferred taxes are adjusted for enacted changes in tax rates and tax laws. Valuation allowances are recorded to reduce deferred tax assets when it is more likely than not that a tax benefit will not be realized.

| |

| I. | Estimates in financial statements |

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect reported amounts. The more significant estimates include: residual values for leased assets, fair values for goodwill impairment tests, impairment of available-for-sale securities, warranty liability, stock-based compensation and reserves for product liability and insurance losses, postretirement benefits, post-sale discounts, credit losses and income taxes.

| |

| J. | New accounting guidance |

Presentation of comprehensive income – In June 2011, the Financial Accounting Standards Board (FASB) issued accounting guidance on the presentation of comprehensive income. The guidance provides two options for presenting net income and other comprehensive income. The total of comprehensive income, the components of net income, and the components of other comprehensive income may be presented in either a single continuous statement of comprehensive income or in two separate but consecutive statements. We elected to present two separate statements. This guidance was effective January 1, 2012.

Goodwill impairment testing – In September 2011, the FASB issued accounting guidance on the testing of goodwill for impairment. The guidance allows entities testing goodwill for impairment the option of performing a qualitative assessment to determine the likelihood of goodwill impairment and whether it is necessary to perform the two-step impairment test currently required. This guidance was effective for annual and interim goodwill impairment tests performed for fiscal years beginning after December 15, 2011. Early adoption was permitted. We elected to early adopt this guidance for the year ended December 31, 2011 and the guidance did not have a material impact on our financial statements.

Disclosures about offsetting assets and liabilities – In December 2011, the FASB issued accounting guidance on disclosures about offsetting assets and liabilities. The guidance requires entities to disclose both gross and net information about instruments and transactions that are offset in the statement of financial position, as well as instruments and transactions that are subject to an enforceable master netting arrangement or similar agreement. In January 2013, the FASB issued guidance clarifying the scope of the disclosures to apply only to derivatives, including bifurcated embedded derivatives, repurchase and reverse repurchase agreements, and securities lending and securities borrowing transactions. This guidance was effective January 1, 2013, with retrospective application required. The guidance did not have a material impact on our financial statements. See Note 3 for additional information.

Indefinite-lived intangible assets impairment testing – In July 2012, the FASB issued accounting guidance on the testing of indefinite-lived intangible assets for impairment. The guidance allows entities to first perform a qualitative assessment to determine the likelihood of an impairment for an indefinite-lived intangible asset and whether it is necessary to perform the quantitative impairment assessment currently required. This guidance was effective January 1, 2013 and did not have a material impact on our financial statements.

Reporting of amounts reclassified out of accumulated other comprehensive income – In February 2013, the FASB issued accounting guidance on the reporting of reclassifications out of accumulated other comprehensive income. The guidance requires an entity to present, either on the face of the statement where net income is presented or in the notes, significant amounts reclassified out of accumulated other comprehensive income by the respective line items of net income if the amount is reclassified to net income in its entirety in the same reporting period. For other amounts not required to be reclassified in their entirety to net income in the same reporting period, a cross reference to other disclosures that provide additional detail about the reclassification amounts is required. This guidance was effective January 1, 2013 and did not have a material impact on our financial statements. See Note 17 for additional information.

Joint and several liability arrangements – In February 2013, the FASB issued accounting guidance on the recognition, measurement and disclosure of obligations resulting from joint and several liability arrangements. The guidance requires an entity to measure obligations resulting from joint and several liability arrangements for which the total amount of the obligation within the scope of this guidance is fixed at the reporting date, as the sum of the amount the reporting entity agreed to pay on the basis of its arrangement among its co-obligors and any additional amount the reporting entity expects to pay on behalf of its co-obligors. The entity is also required to disclose the nature and amount of the obligation as well as any other information about those obligations. This guidance is effective January 1, 2014, with retrospective application required. We do not expect the adoption to have a material impact on our financial statements.

Parent's accounting for the cumulative translation adjustment upon derecognition of certain subsidiaries or groups of assets within a foreign entity or of an investment in a foreign entity – In March 2013, the FASB issued accounting guidance on the parent's accounting for the cumulative translation adjustment (CTA) upon derecognition of certain subsidiaries or groups of assets within a foreign entity or of an investment in a foreign entity. The new standard clarifies existing guidance regarding when the CTA should be released into earnings upon various deconsolidation and consolidation transactions. This guidance is effective January 1, 2014. We do not expect the adoption to have a material impact on our financial statements.

Presentation of an unrecognized tax benefit when a net operating loss carryforward, a similar tax loss, or a tax credit carryforward exists – In July 2013, the FASB issued accounting guidance on the financial statement presentation of an unrecognized tax benefit when a net operating loss carryforward, a similar tax loss, or a tax credit carryforward exists. The guidance requires an unrecognized tax benefit, or a portion of an unrecognized tax benefit, to be presented as a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss, or a tax credit carryforward in the financial statements if available under the applicable tax jurisdiction. The guidance is effective January 1, 2014. We do not expect the adoption to have a material impact on our financial statements.

For acquisitions accounted for as a business combination, goodwill represents the excess of the cost over the fair value of the net assets acquired. We are required to test goodwill for impairment, at the reporting unit level, annually and when events or circumstances indicate the fair value of a reporting unit may be below its carrying value. A reporting unit is an operating segment or one level below an operating segment (referred to as a component) to which goodwill is assigned when initially recorded. We assign goodwill to reporting units based on our integration plans and the expected synergies resulting from the acquisition. Because Caterpillar is a highly integrated company, the businesses we acquire are sometimes combined with or integrated into existing reporting units. When changes occur in the composition of our operating segments or reporting units, goodwill is reassigned to the affected reporting units based on their relative fair values.

We test goodwill for impairment annually and whenever events or circumstances make it more likely than not that an impairment may have occurred. We perform our annual goodwill impairment test as of October 1 and monitor for interim triggering events on an ongoing basis. Goodwill is reviewed for impairment utilizing a qualitative assessment or a two-step process. We have an option to make a qualitative assessment of a reporting unit’s goodwill for impairment. If we choose to perform a qualitative assessment and determine the fair value more likely than not exceeds the carrying value, no further evaluation is necessary. For reporting units where we perform the two-step process, the first step requires us to compare the fair value of each reporting unit, which we primarily determine using an income approach based on the present value of discounted cash flows, to the respective carrying value, which includes goodwill. If the fair value of the reporting unit exceeds its carrying value, the goodwill is not considered impaired. If the carrying value is higher than the fair value, there is an indication that an impairment may exist and the second step is required. In step two, the implied fair value of goodwill is calculated as the excess of the fair value of a reporting unit over the fair values assigned to its assets and liabilities. If the implied fair value of goodwill is less than the carrying value of the reporting unit’s goodwill, the difference is recognized as an impairment loss. See Note 10 for further details.

For those businesses where management has committed to a plan to divest, which is typically demonstrated by approval from the Board of Directors or Group President, each business is valued at the lower of its carrying amount or estimated fair value less cost to sell. If the carrying amount of the business exceeds its estimated fair value, an impairment loss is recognized. The fair values are estimated using accepted valuation techniques such as a discounted cash flow model, valuations performed by third parties, or indicative bids, when available. A number of significant estimates and assumptions are involved in the application of these techniques, including the forecasting of markets and market share, sales volumes and prices, costs and expenses, and multiple other factors. Management considers historical experience and all available information at the time the estimates are made; however, the fair values that are ultimately realized upon the sale of the businesses to be divested may differ from the estimated fair values reflected in the Consolidated Financial Statements.

| |

| 2. | Stock-based compensation |

Our stock-based compensation plans primarily provide for the granting of stock options, stock-settled stock appreciation rights (SARs) and restricted stock units (RSUs) to Officers and other key employees, as well as non-employee Directors. Stock options permit a holder to buy Caterpillar stock at the stock’s price when the option was granted. SARs permit a holder the right to receive the value in shares of the appreciation in Caterpillar stock that occurred from the date the right was granted up to the date of exercise. A restricted stock unit (RSU) is an agreement to issue shares of Caterpillar stock at the time of vesting.

Our long-standing practices and policies specify all stock-based compensation awards are approved by the Compensation Committee (the Committee) of the Board of Directors on the date of grant. The stock-based award approval process specifies the number of awards granted, the terms of the award and the grant date. The same terms and conditions are consistently applied to all employee grants, including Officers. The Committee approves all individual Officer grants. The number of stock-based compensation awards included in an individual’s award is determined based on the methodology approved by the Committee. In 2007, under the terms of the Caterpillar Inc. 2006 Long-Term Incentive Plan (approved by stockholders in June of 2006), the Compensation Committee approved the exercise price methodology to be the closing price of the Company stock on the date of the grant.

Common stock issued from Treasury stock under the plans totaled 6,258,692 for 2013, 7,515,149 for 2012 and 8,710,630 for 2011.

Awards generally vest three years after the date of grant. At grant, SARs and option awards have a term life of ten years. Upon separation from service, if the participant is 55 years of age or older with more than five years of service, the participant meets the criteria for a “Long Service Separation”. If the “Long Service Separation” criteria are met, the vested options/SARs will have a life that is the lesser of ten years from the original grant date or five years from the separation date.

Our stock-based compensation plans allow for the immediate vesting upon separation for employees who meet the criteria for a “Long Service Separation” and who have fulfilled the requisite service period of six months. Compensation expense is recognized over the period from the grant date to the end date of the requisite service period for employees who meet the immediate vesting upon retirement requirements. For those employees who become eligible for immediate vesting upon retirement subsequent to the requisite service period and prior to the completion of the vesting period, compensation expense is recognized over the period from grant date to the date eligibility is achieved.

Accounting guidance on share-based payments requires companies to estimate the fair value of options/SARs on the date of grant using an option-pricing model. The fair value of the option/SAR grant was estimated using a lattice-based option-pricing model. The lattice-based option-pricing model considers a range of assumptions related to volatility, risk-free interest rate and historical employee behavior. Expected volatility was based on historical and current implied volatilities from traded options on our stock. The risk-free rate was based on U.S. Treasury security yields at the time of grant. The weighted-average dividend yield was based on historical information. The expected life was determined from the lattice-based model. The lattice-based model incorporated exercise and post vesting forfeiture assumptions based on analysis of historical data. The following table provides the assumptions used in determining the fair value of the stock-based awards for the years ended December 31, 2013, 2012 and 2011, respectively.

|

| | | | | | | | |

| | | | | | |

| | Grant Year |

| | 2013 | | 2012 | | 2011 |

| Weighted-average dividend yield | 2.1 | % | | 2.2 | % | | 2.2 | % |

| Weighted-average volatility | 30.6 | % | | 35.0 | % | | 32.7 | % |

| Range of volatilities | 23.4-40.6% |

| | 33.3-40.4% |

| | 20.9-45.4% |

|

| Range of risk-free interest rates | 0.16-1.88% |

| | 0.17-2.00% |

| | 0.25-3.51% |

|

| Weighted-average expected lives | 8 years |

| | 7 years |

| | 8 years |

|

| | | | | | |

The fair value of the RSU grant was determined by reducing the stock price on the day of grant by the present value of the estimated dividends to be paid during the vesting period. The estimated dividends are based on Caterpillar’s weighted-average dividend yield.

The amount of stock-based compensation expense capitalized for the years ended December 31, 2013, 2012 and 2011 did not have a significant impact on our financial statements.

At December 31, 2013, there was $193 million of total unrecognized compensation cost from stock-based compensation arrangements granted under the plans, which is related to non-vested stock-based awards. The compensation expense is expected to be recognized over a weighted-average period of approximately 1.8 years.

Please refer to Tables I and II below for additional information on our stock-based awards.

|

| | | | | | | | | | | | | | | | | | | | |

| TABLE I — Financial Information Related to Stock-based Compensation |

| | 2013 | | 2012 | | 2011 |

| | Shares | | Weighted- Average Exercise Price | | Shares | | Weighted- Average Exercise Price | | Shares | | Weighted- Average Exercise Price |

| Stock options/SARs activity: | |

| | |

| | |

| | |

| | |

| | |

|

| Outstanding at beginning of year | 45,827,599 |

| | $ | 59.45 |

| | 50,372,991 |

| | $ | 53.01 |

| | 57,882,998 |

| | $ | 48.50 |

|

Granted to officers and key employees 1 | 4,276,060 |

| | $ | 89.75 |

| | 3,318,188 |

| | $ | 110.09 |

| | 2,960,595 |

| | $ | 102.13 |

|

| Exercised | (6,476,082 | ) | | $ | 41.10 |

| | (7,708,343 | ) | | $ | 38.73 |

| | (10,149,476 | ) | | $ | 41.78 |

|

| Forfeited / expired | (251,830 | ) | | $ | 84.64 |

| | (155,237 | ) | | $ | 67.50 |

| | (321,126 | ) | | $ | 48.02 |

|

| Outstanding at end of year | 43,375,747 |

| | $ | 65.03 |

| | 45,827,599 |

| | $ | 59.45 |

| | 50,372,991 |

| | $ | 53.01 |

|

| Exercisable at year-end | 34,200,054 |

| | $ | 55.93 |

| | 33,962,000 |

| | $ | 51.75 |

| | 35,523,057 |

| | $ | 52.66 |

|

| | | | | | | | | | | | |

| RSUs activity: | |

| | |

| | |

| | |

| | |

| | |

|

| Outstanding at beginning of year | 3,580,220 |

| | |

| | 4,281,490 |

| | |

| | 4,650,241 |

| | |

|

| Granted to officers and key employees | 1,614,870 |

| | |

| | 1,429,939 |

| | |

| | 1,082,032 |

| | |

|

| Vested | (1,286,934 | ) | | |

| | (2,077,485 | ) | | |

| | (1,382,539 | ) | | |

|

| Forfeited | (84,828 | ) | | |

| | (53,724 | ) | | |

| | (68,244 | ) | | |

|

| Outstanding at end of year | 3,823,328 |

| | |

| | 3,580,220 |

| | |

| | 4,281,490 |

| | |

|

|

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Stock options/SARs outstanding and exercisable: |

| | | Outstanding | | Exercisable |

| Exercise Prices | | Shares Outstanding at 12/31/13 | | Weighted- Average Remaining Contractual Life (Years) | | Weighted- Average Exercise Price | | Aggregate Intrinsic Value 2 | | Shares Outstanding at 12/31/13 | | Weighted- Average Remaining Contractual Life (Years) | | Weighted- Average Exercise Price | | Aggregate Intrinsic Value 2 |

| $22.17 – 38.63 | | 7,775,953 |

| | 3.20 | | $ | 29.03 |

| | $ | 481 |

| | 7,775,953 |

| | 3.20 | | $ | 29.03 |

| | $ | 481 |

|

| $40.64 – 57.85 | | 11,656,943 |

| | 4.06 | | $ | 52.71 |

| | 444 |

| | 11,656,943 |

| | 4.06 | | $ | 52.71 |

| | 444 |

|

| $63.04 – 72.05 | | 9,687,583 |

| | 2.48 | | $ | 69.05 |

| | 211 |

| | 9,687,583 |

| | 2.48 | | $ | 69.05 |

| | 211 |

|

| $73.20 – 89.75 | | 8,280,894 |

| | 6.69 | | $ | 81.70 |

| | 75 |

| | 4,174,124 |

| | 4.37 | | $ | 73.86 |

| | 71 |

|

| $102.13 – 110.09 | | 5,974,374 |

| | 7.71 | | $ | 106.28 |

| | — |

| | 905,451 |

| | 7.62 | | $ | 105.59 |

| | — |

|

| | | 43,375,747 |

| | | | $ | 65.03 |

| | $ | 1,211 |

| | 34,200,054 |

| | | | $ | 55.93 |

| | $ | 1,207 |

|

| |

1 | No SARS were granted during the years ended December 31, 2013 or 2012. Of the 2,960,595 awards granted during the year ended December 31, 2011, 2,722,689 were SARs. |

| |

2 | The difference between a stock award’s exercise price and the underlying stock’s market price at December 31, 2013, for awards with market price greater than the exercise price. Amounts are in millions of dollars. |

The computations of weighted-average exercise prices and aggregate intrinsic values are not applicable to RSUs since an RSU represents an agreement to issue shares of stock at the time of vesting. At December 31, 2013, there were 3,823,328 outstanding RSUs with a weighted average remaining contractual life of 1.3 years.

|

| | | | | | | | | | | | |

| TABLE II— Additional Stock-based Award Information |

| | | | | | | |

| (Dollars in millions except per share data) | | 2013 | | 2012 | | 2011 |

| Stock Options/SARs activity: | | |

| | |

| | |

|

| Weighted-average fair value per share of stock awards granted | | $ | 28.34 |

| | $ | 39.20 |

| | $ | 36.73 |

|

| Intrinsic value of stock awards exercised | | $ | 312 |

| | $ | 488 |

| | $ | 618 |

|

| Fair value of stock awards vested | | $ | 167 |

| | $ | 66 |

| | $ | 96 |

|

| Cash received from stock awards exercised | | $ | 152 |

| | $ | 112 |

| | $ | 161 |

|

| | | | | | | |

| RSUs activity: | | |

| | |

| | |

|

| Weighted-average fair value per share of stock awards granted | | $ | 84.05 |

| | $ | 104.61 |

| | $ | 97.51 |

|

| Fair value of stock awards vested | | $ | 117 |

| | $ | 229 |

| | $ | 143 |

|

| | | | | | | |

Before tax, stock-based compensation expense for 2013, 2012 and 2011 was $231 million, $245 million and $193 million, respectively, with a corresponding income tax benefit of $73 million, $78 million and $61 million, respectively.

In accordance with guidance on share-based payments, we classify stock-based compensation within Cost of goods sold, Selling, general and administrative expenses and Research and development expenses corresponding to the same line item as the cash compensation paid to respective employees, officers and non-employee directors.

We currently use shares in treasury stock to satisfy share award exercises.

The cash tax benefits realized from stock awards exercised for 2013, 2012 and 2011 were $127 million, $217 million and $235 million, respectively. We use the direct only method and tax law ordering approach to calculate the tax effects of stock-based compensation. In certain jurisdictions, tax deductions for exercises of stock-based awards did not generate a cash benefit. A tax benefit of approximately $39 million will be recorded in additional paid-in capital when these deductions reduce our future income taxes payable.

| |

| 3. | Derivative financial instruments and risk management |

Our earnings and cash flow are subject to fluctuations due to changes in foreign currency exchange rates, interest rates and commodity prices. Our Risk Management Policy (policy) allows for the use of derivative financial instruments to prudently manage foreign currency exchange rate, interest rate and commodity price exposures. Our policy specifies that derivatives are not to be used for speculative purposes. Derivatives that we use are primarily foreign currency forward, option and cross currency contracts, interest rate swaps and commodity forward and option contracts. Our derivative activities are subject to the management, direction and control of our senior financial officers. Risk management practices, including the use of financial derivative instruments, are presented to the Audit Committee of the Board of Directors at least annually.

All derivatives are recognized in Statement 3 at their fair value. On the date the derivative contract is entered into, we designate the derivative as (1) a hedge of the fair value of a recognized asset or liability (fair value hedge), (2) a hedge of a forecasted transaction or the variability of cash flow to be paid (cash flow hedge), or (3) an undesignated instrument. Changes in the fair value of a derivative that is qualified, designated and highly effective as a fair value hedge, along with the gain or loss on the hedged recognized asset or liability that is attributable to the hedged risk, are recorded in current earnings. Changes in the fair value of a derivative that is qualified, designated and highly effective as a cash flow hedge are recorded in Accumulated other comprehensive income (loss) (AOCI), to the extent effective, in Statement 3 until they are reclassified to earnings in the same period or periods during which the hedged transaction affects earnings. Changes in the fair value of undesignated derivative instruments and the ineffective portion of designated derivative instruments are reported in current earnings. Cash flow from designated derivative financial instruments are classified within the same category as the item being hedged on Statement 5. Cash flow from undesignated derivative financial instruments are included in the investing category on Statement 5.

We formally document all relationships between hedging instruments and hedged items, as well as the risk-management objective and strategy for undertaking various hedge transactions. This process includes linking all derivatives that are designated as fair value hedges to specific assets and liabilities in Statement 3 and linking cash flow hedges to specific forecasted transactions or variability of cash flow.

We also formally assess, both at the hedge’s inception and on an ongoing basis, whether the designated derivatives that are used in hedging transactions are highly effective in offsetting changes in fair values or cash flow of hedged items. When a derivative is determined not to be highly effective as a hedge or the underlying hedged transaction is no longer probable, we discontinue hedge accounting prospectively, in accordance with the derecognition criteria for hedge accounting.

| |

| A. | Foreign currency exchange rate risk |

Foreign currency exchange rate movements create a degree of risk by affecting the U.S. dollar value of sales made and costs incurred in foreign currencies. Movements in foreign currency rates also affect our competitive position as these changes may affect business practices and/or pricing strategies of non-U.S.-based competitors. Additionally, we have balance sheet positions denominated in foreign currencies, thereby creating exposure to movements in exchange rates.

Our Machinery and Power Systems operations purchase, manufacture and sell products in many locations around the world. As we have a diversified revenue and cost base, we manage our future foreign currency cash flow exposure on a net basis. We use foreign currency forward and option contracts to manage unmatched foreign currency cash inflow and outflow. Our objective is to minimize the risk of exchange rate movements that would reduce the U.S. dollar value of our foreign currency cash flow. Our policy allows for managing anticipated foreign currency cash flow for up to five years.

We generally designate as cash flow hedges at inception of the contract any Australian dollar, Brazilian real, British pound, Canadian dollar, Chinese yuan, euro, Indian rupee, Japanese yen, Mexican peso, Singapore dollar, or Swiss franc forward or option contracts that meet the requirements for hedge accounting and the maturity extends beyond the current quarter-end. Designation is performed on a specific exposure basis to support hedge accounting. The remainder of Machinery and Power Systems foreign currency contracts are undesignated, including any hedges designed to protect our competitive exposure.

As of December 31, 2013, $9 million of deferred net gains, net of tax, included in equity (AOCI in Statement 3), are expected to be reclassified to current earnings (Other income (expense) in Statement 1) over the next twelve months when earnings are affected by the hedged transactions. The actual amount recorded in Other income (expense) will vary based on exchange rates at the time the hedged transactions impact earnings.

In managing foreign currency risk for our Financial Products operations, our objective is to minimize earnings volatility resulting from conversion and the remeasurement of net foreign currency balance sheet positions, and future transactions denominated in foreign currencies. Our policy allows the use of foreign currency forward, option and cross currency contracts to offset the risk of currency mismatch between our receivables and debt, and exchange rate risk associated with future transactions denominated in foreign currencies. Substantially all such foreign currency forward, option and cross currency contracts are undesignated.

Interest rate movements create a degree of risk by affecting the amount of our interest payments and the value of our fixed-rate debt. Our practice is to use interest rate derivatives to manage our exposure to interest rate changes and, in some cases, lower the cost of borrowed funds.

Our Machinery and Power Systems operations generally use fixed rate debt as a source of funding. Our objective is to minimize the cost of borrowed funds. Our policy allows us to enter into fixed-to-floating interest rate swaps and forward rate agreements to meet that objective with the intent to designate as fair value hedges at inception of the contract all fixed-to-floating interest rate swaps. Designation as a hedge of the fair value of our fixed rate debt is performed to support hedge accounting.

Financial Products operations has a match-funding policy that addresses interest rate risk by aligning the interest rate profile (fixed or floating rate) of Cat Financial’s debt portfolio with the interest rate profile of their receivables portfolio within predetermined ranges on an ongoing basis. In connection with that policy, we use interest rate derivative instruments to modify the debt structure to match assets within the receivables portfolio. This matched funding reduces the volatility of margins between interest-bearing assets and interest-bearing liabilities, regardless of which direction interest rates move.

Our policy allows us to use fixed-to-floating, floating-to-fixed, and floating-to-floating interest rate swaps to meet the match-funding objective. We designate fixed-to-floating interest rate swaps as fair value hedges to protect debt against changes in fair value due to changes in the benchmark interest rate. We designate most floating-to-fixed interest rate swaps as cash flow hedges to protect against the variability of cash flows due to changes in the benchmark interest rate.

As of December 31, 2013, $3 million of deferred net losses, net of tax, included in equity (AOCI in Statement 3), related to Financial Products floating-to-fixed interest rate swaps, are expected to be reclassified to current earnings (Interest expense of Financial Products in Statement 1) over the next twelve months. The actual amount recorded in Interest expense of Financial Products will vary based on interest rates at the time the hedged transactions impact earnings.

We have, at certain times, liquidated fixed-to-floating and floating-to-fixed interest rate swaps at both Machinery and Power Systems and Financial Products. The gains or losses associated with these swaps at the time of liquidation are amortized into earnings over the original term of the previously designated hedged item.

In anticipation of issuing debt for the planned acquisition of Bucyrus International, Inc., we entered into interest rate swaps to manage our exposure to interest rate changes. For the year ended December 31, 2011, we recognized a net loss of $149 million, included in Other income (expense) in Statement 1. The contracts were liquidated in conjunction with the debt issuance in May 2011. These contracts were not designated as hedging instruments, and therefore, did not receive hedge accounting treatment.

Commodity price movements create a degree of risk by affecting the price we must pay for certain raw material. Our policy is to use commodity forward and option contracts to manage the commodity risk and reduce the cost of purchased materials.