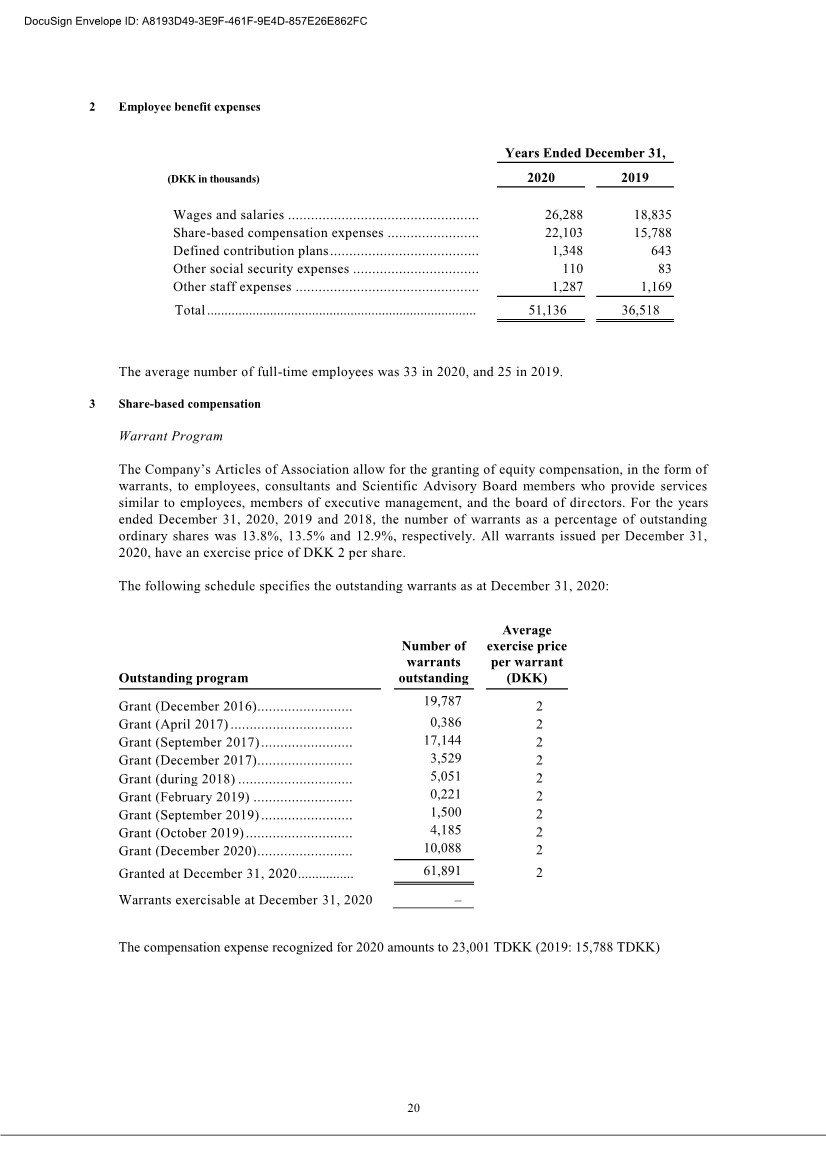

| 20 2 Employee benefit expenses Years Ended December 31, (DKK in thousands) 2020 2019 Wages and salaries .................................................. 26,288 18,835 Share-based compensation expenses ........................ 22,103 15,788 Defined contribution plans ....................................... 1,348 643 Other social security expenses ................................. 110 83 Other staff expenses ................................................ 1,287 1,169 Total ............................................................................. 51,136 36,518 , The average number of full-time employees was 33 in 2020, and 25 in 2019. 3 Share-based compensation Warrant Program The Company’s Articles of Association allow for the granting of equity compensation, in the form of warrants, to employees, consultants and Scientific Advisory Board members who provide services similar to employees, members of executive management, and the board of directors. For the years ended December 31, 2020, 2019 and 2018, the number of warrants as a percentage of outstanding ordinary shares was 13.8%, 13.5% and 12.9%, respectively. All warrants issued per December 31, 2020, have an exercise price of DKK 2 per share. The following schedule specifies the outstanding warrants as at December 31, 2020: Outstanding program Number of warrants outstanding Average exercise price per warrant (DKK) Grant (December 2016) ......................... 19,787 2 Grant (April 2017) ................................ 0,386 2 Grant (September 2017) ........................ 17,144 2 Grant (December 2017) ......................... 3,529 2 Grant (during 2018) .............................. 5,051 2 Grant (February 2019) .......................... 0,221 2 Grant (September 2019) ........................ 1,500 2 Grant (October 2019) ............................ 4,185 2 Grant (December 2020) ......................... 10,088 2 Granted at December 31, 2020 ................ 61,891 2 Warrants exercisable at December 31, 2020 – The compensation expense recognized for 2020 amounts to 23,001 TDKK (2019: 15,788 TDKK) DocuSign Envelope ID: A8193D49-3E9F-461F-9E4D-857E26E862FC |